Embed Size (px)

DESCRIPTION

My First Public Presentation.

Citation preview

Standard & Poor’s Negative Outlook Impact on Indian Economy & Financial Markets

Group 2 MBF Mumbai Batch 13th May

20121

Sovereign Credit Rating – What is it ?

• Credit rating evaluates credit worthiness of debt issuer

• A Sovereign credit rating is rating of sovereign entity –a national government

• Poor rating indicate high risk of defaulting

• It is not base on mathematical formulas.• It is not base on mathematical formulas.

• Credit Rating Agencies use their experience and judgment

• Sovereign credit rating indicates risk level of investing environment of a country

• Sovereign rating takes political risk into account

Group 2 MBF Mumbai Batch 13th May

20122

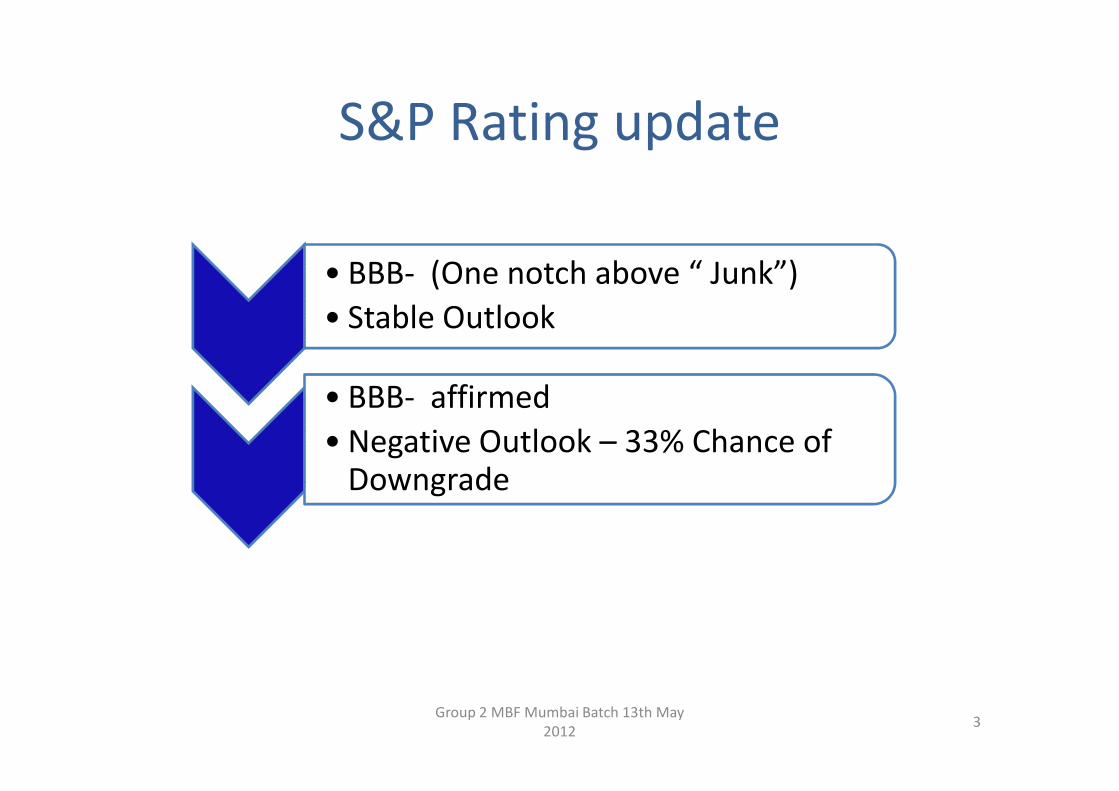

S&P Rating update

• BBB- (One notch above “ Junk”)

• Stable Outlook

• BBB- affirmed• BBB- affirmed

• Negative Outlook – 33% Chance of Downgrade

Group 2 MBF Mumbai Batch 13th May

20123

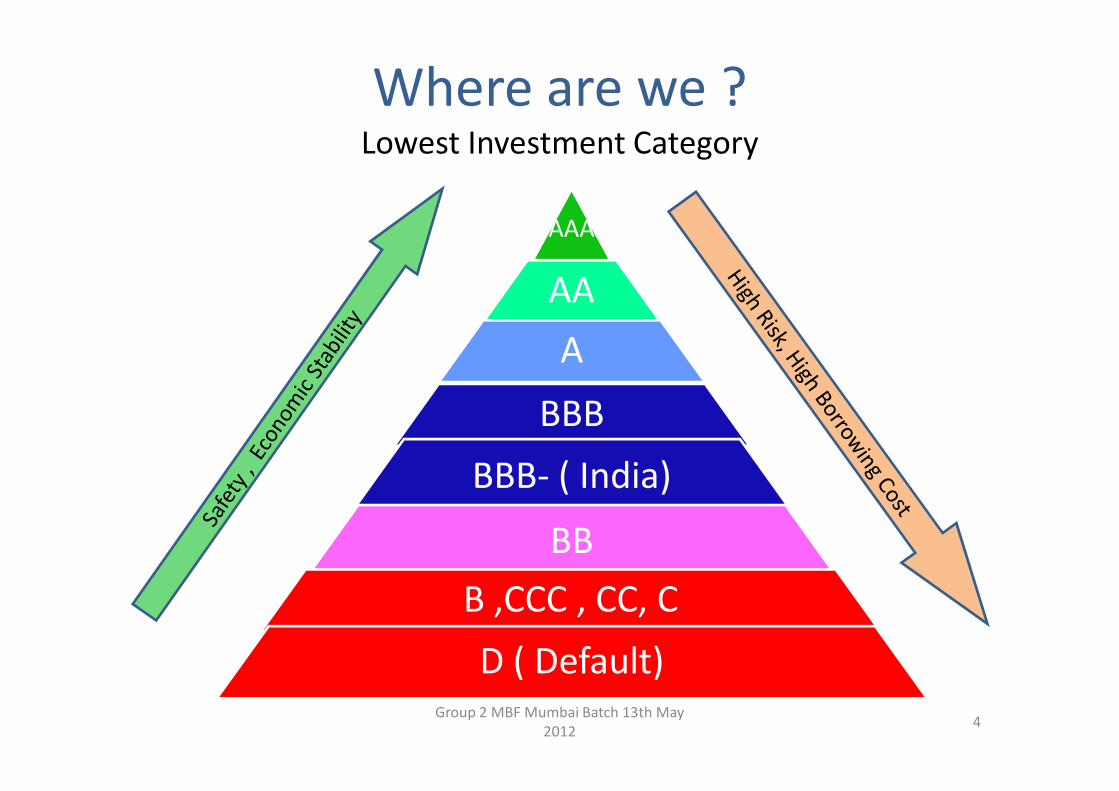

Where are we ? Lowest Investment Category

AAA

AA

A

BBBBBB

BBB- ( India)

BB

B ,CCC , CC, C

D ( Default)Group 2 MBF Mumbai Batch 13th May

20124

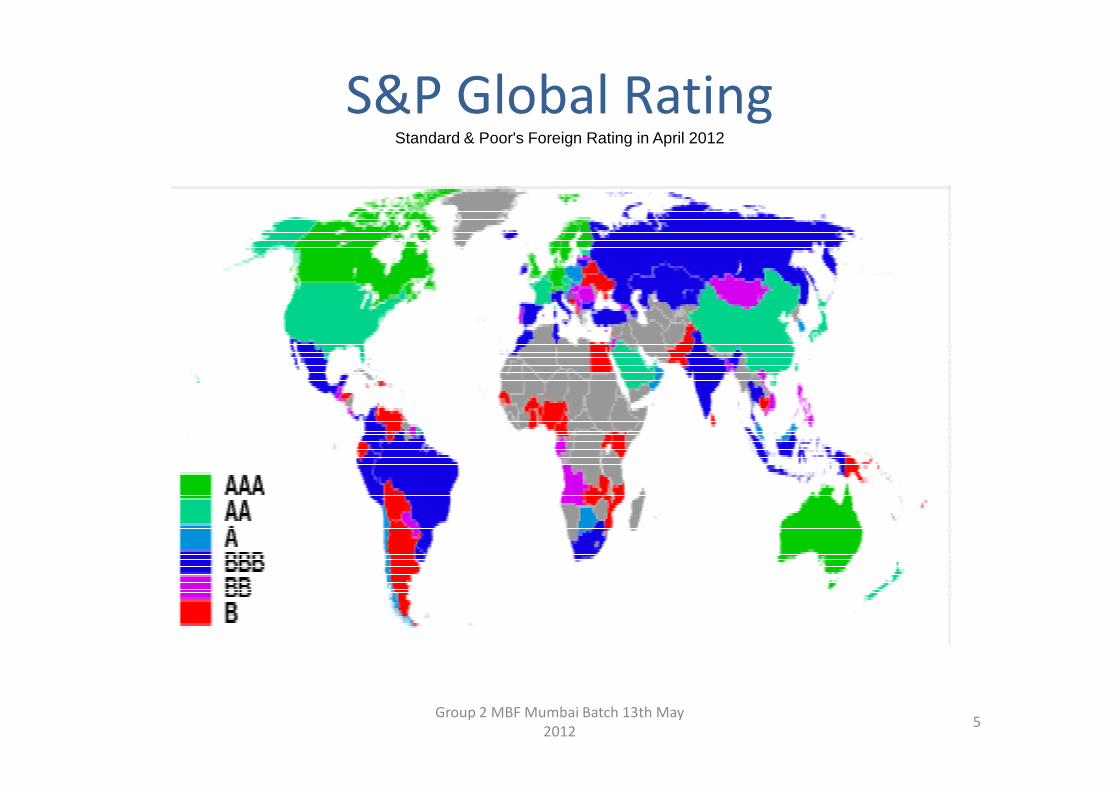

S&P Global RatingStandard & Poor's Foreign Rating in April 2012

Group 2 MBF Mumbai Batch 13th May

20125

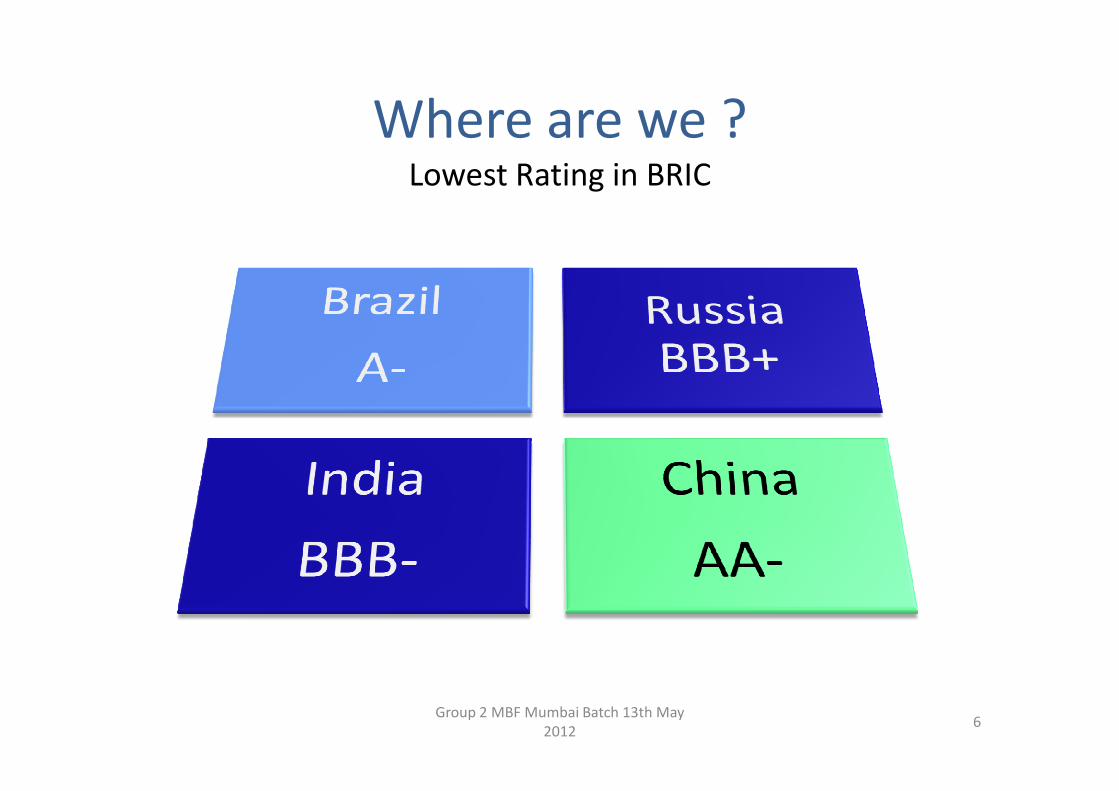

Where are we ? Lowest Rating in BRIC

Group 2 MBF Mumbai Batch 13th May

20126

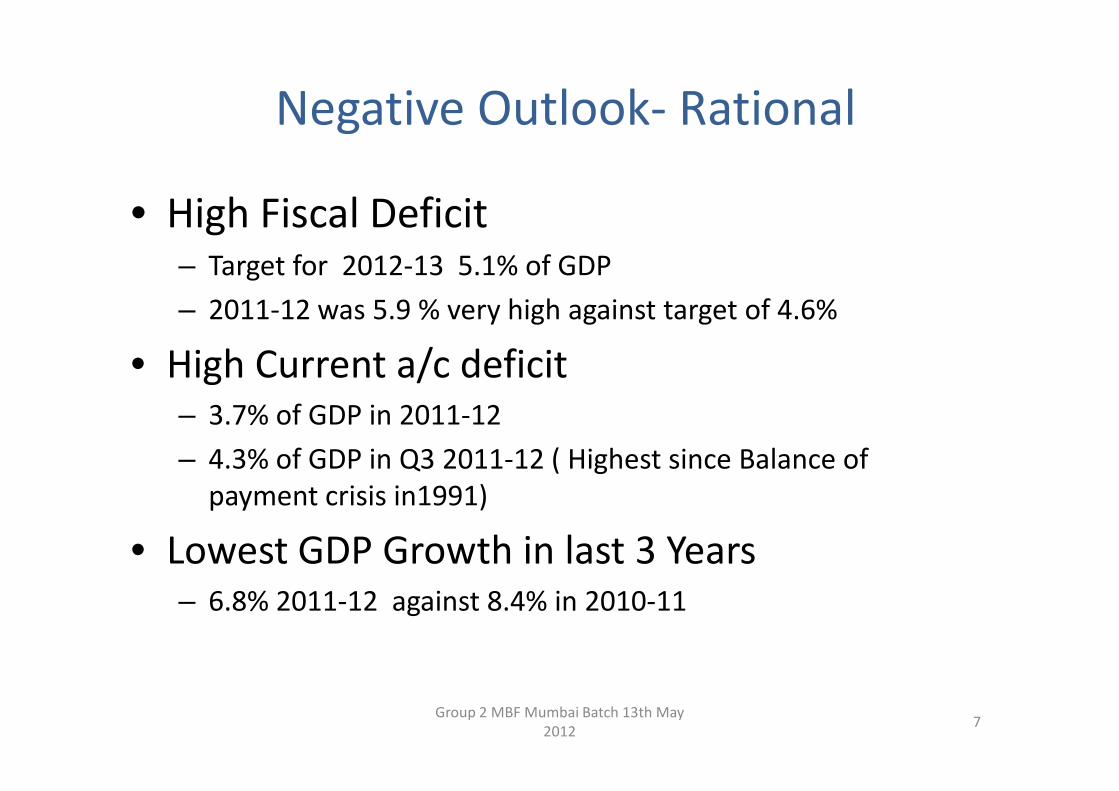

Negative Outlook- Rational

• High Fiscal Deficit – Target for 2012-13 5.1% of GDP

– 2011-12 was 5.9 % very high against target of 4.6%

• High Current a/c deficit 3.7% of GDP in 2011-12– 3.7% of GDP in 2011-12

– 4.3% of GDP in Q3 2011-12 ( Highest since Balance of

payment crisis in1991)

• Lowest GDP Growth in last 3 Years – 6.8% 2011-12 against 8.4% in 2010-11

Group 2 MBF Mumbai Batch 13th May

20127

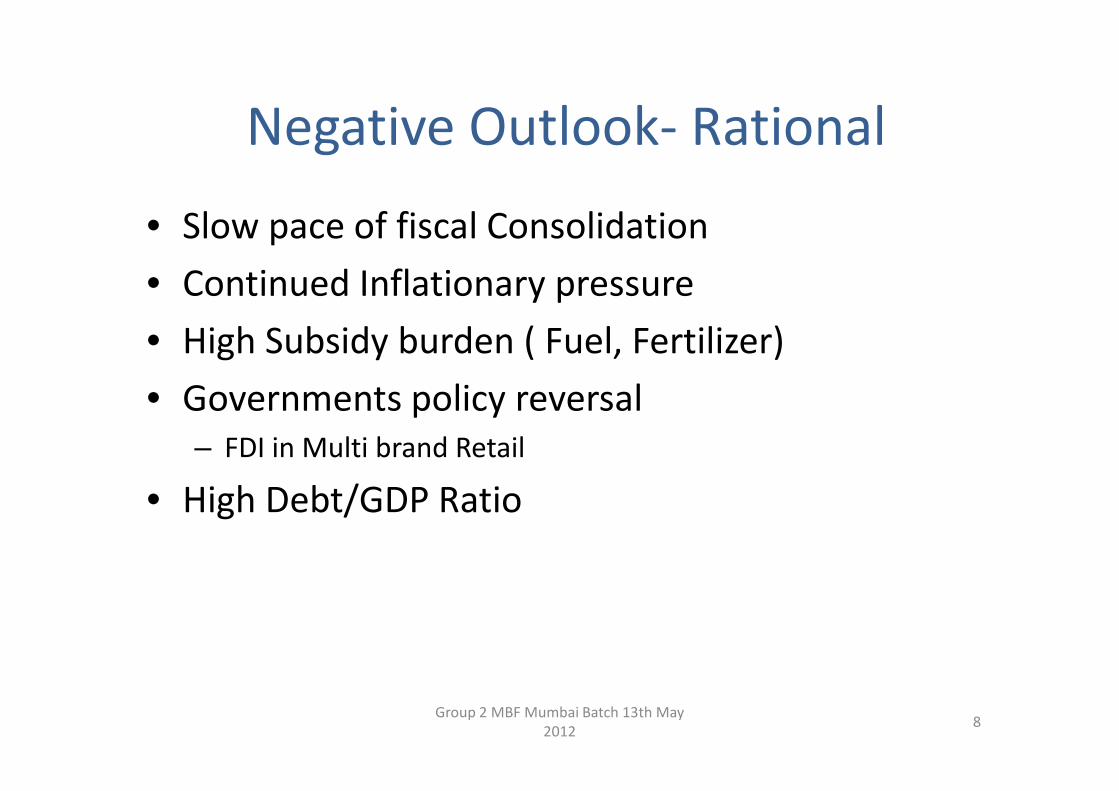

Negative Outlook- Rational

• Slow pace of fiscal Consolidation

• Continued Inflationary pressure

• High Subsidy burden ( Fuel, Fertilizer)

• Governments policy reversal• Governments policy reversal

– FDI in Multi brand Retail

• High Debt/GDP Ratio

Group 2 MBF Mumbai Batch 13th May

20128

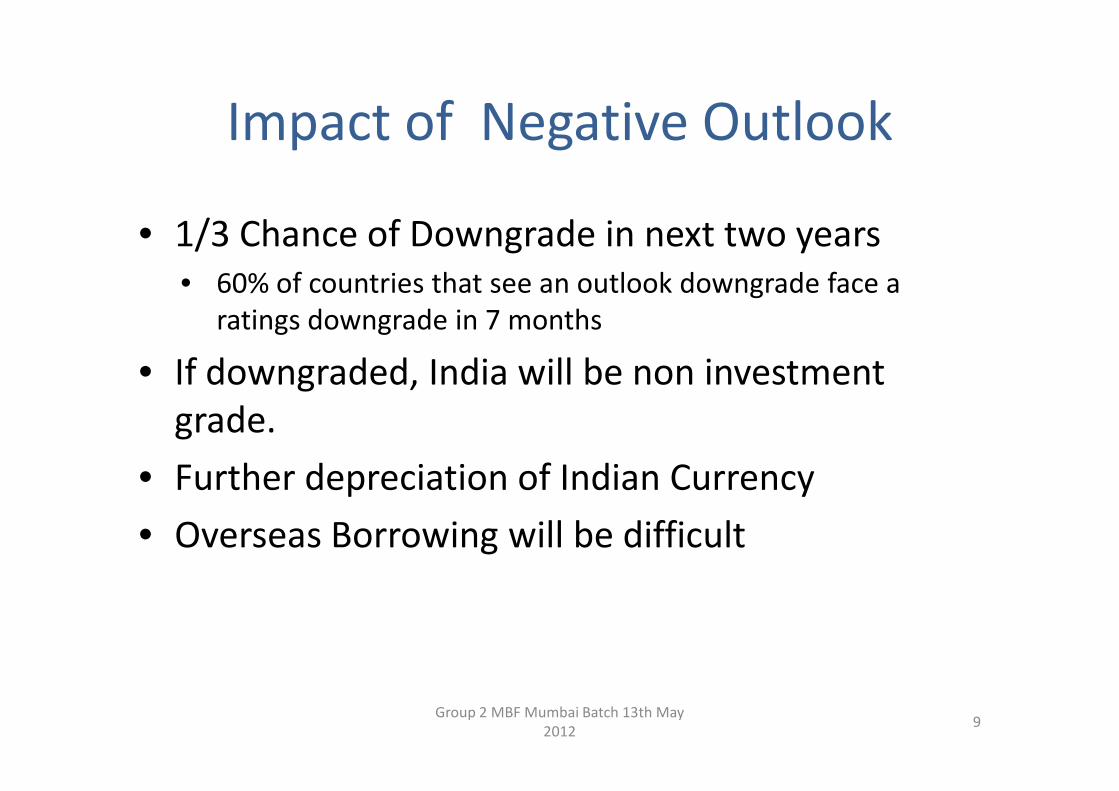

Impact of Negative Outlook

• 1/3 Chance of Downgrade in next two years

• 60% of countries that see an outlook downgrade face a

ratings downgrade in 7 months

• If downgraded, India will be non investment

grade.grade.

• Further depreciation of Indian Currency

• Overseas Borrowing will be difficult

Group 2 MBF Mumbai Batch 13th May

20129

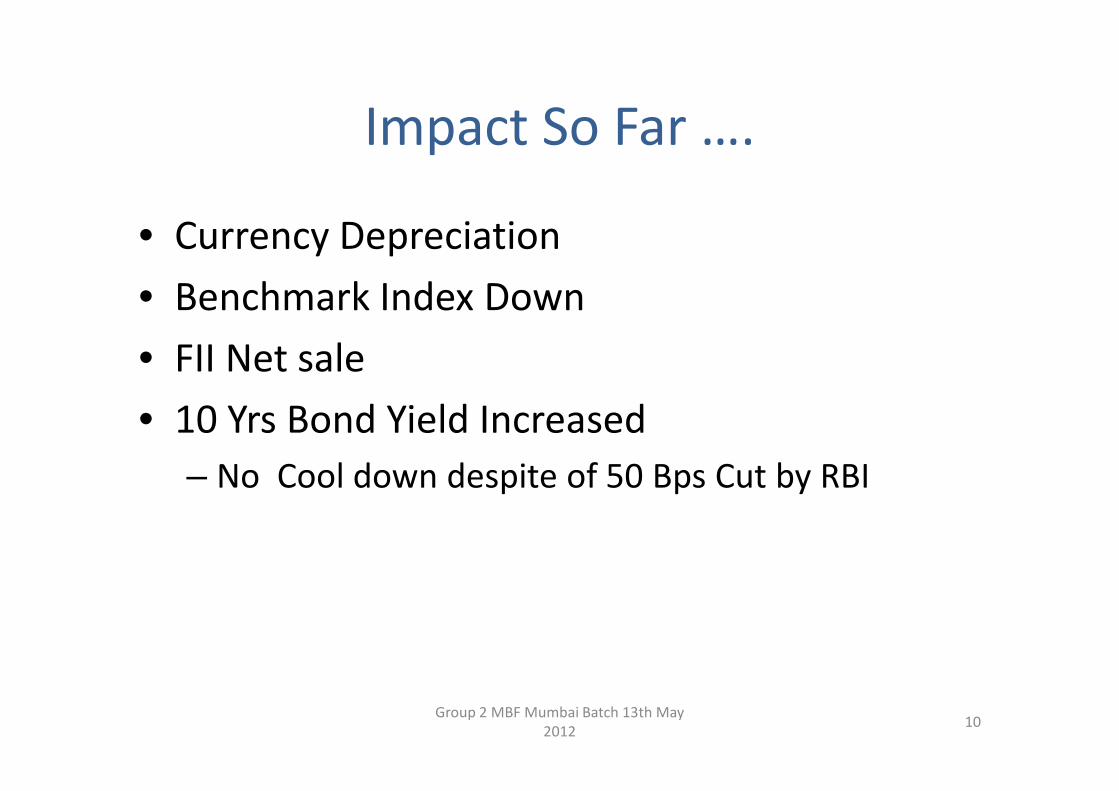

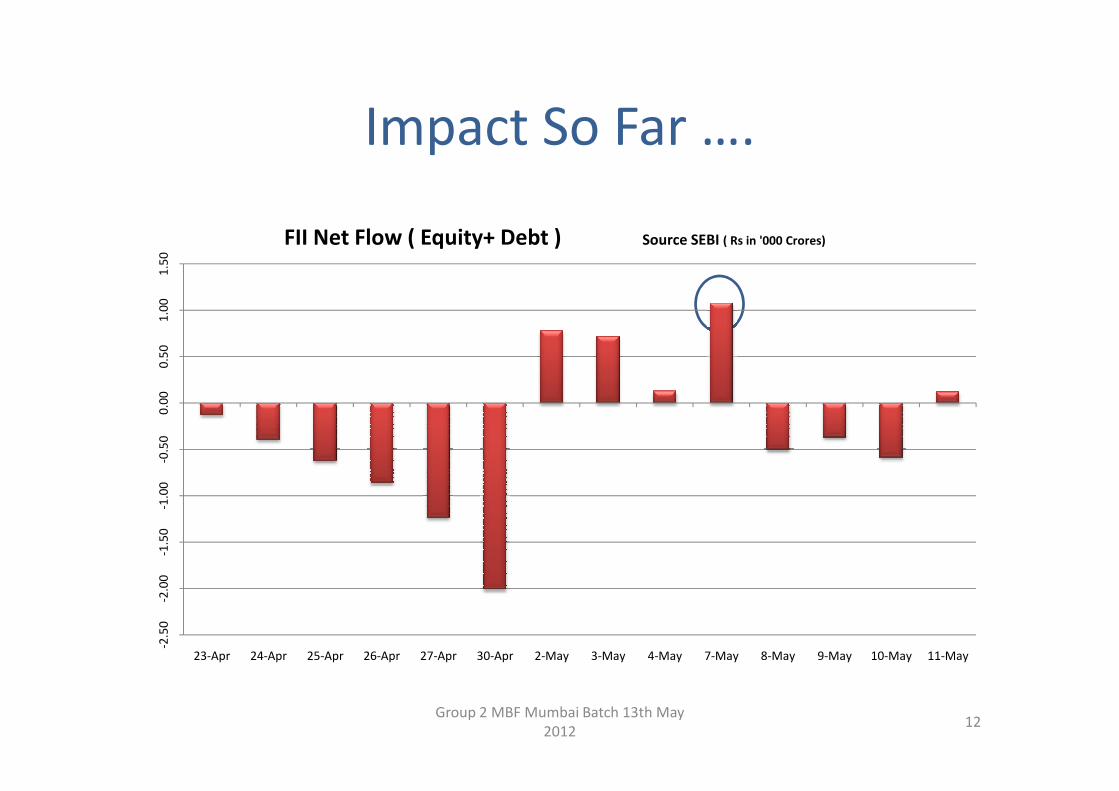

Impact So Far ….

• Currency Depreciation

• Benchmark Index Down

• FII Net sale

• 10 Yrs Bond Yield Increased • 10 Yrs Bond Yield Increased

– No Cool down despite of 50 Bps Cut by RBI

Group 2 MBF Mumbai Batch 13th May

201210

Impact So Far ….15th April 11th May

NIFTY – 5207 4928

INR/Dollar – 51.42 53.64RBI Reference Rate

0.99

1.00

1.01

1.02

1.03

Group 2 MBF Mumbai Batch 13th May

2012

0.94

0.95

0.96

0.97

0.98

INR/USD

Nifty

11

Impact So Far ….0

.00

0.5

01

.00

1.5

0

FII Net Flow ( Equity+ Debt ) Source SEBI ( Rs in '000 Crores)

Group 2 MBF Mumbai Batch 13th May

2012

-2.5

0-2

.00

-1.5

0-1

.00

-0.5

00

.00

23-Apr 24-Apr 25-Apr 26-Apr 27-Apr 30-Apr 2-May 3-May 4-May 7-May 8-May 9-May 10-May 11-May

12

Impact So Far ….10 Year Bond Yield Since 10th April 2012

Source : www.bloomberg.com

50 Bps Rate Cut by RBI

No Impact of 50

Bps Rate Cut by RBI50 Bps Rate Cut by RBI

Group 2 MBF Mumbai Batch 13th May

201213

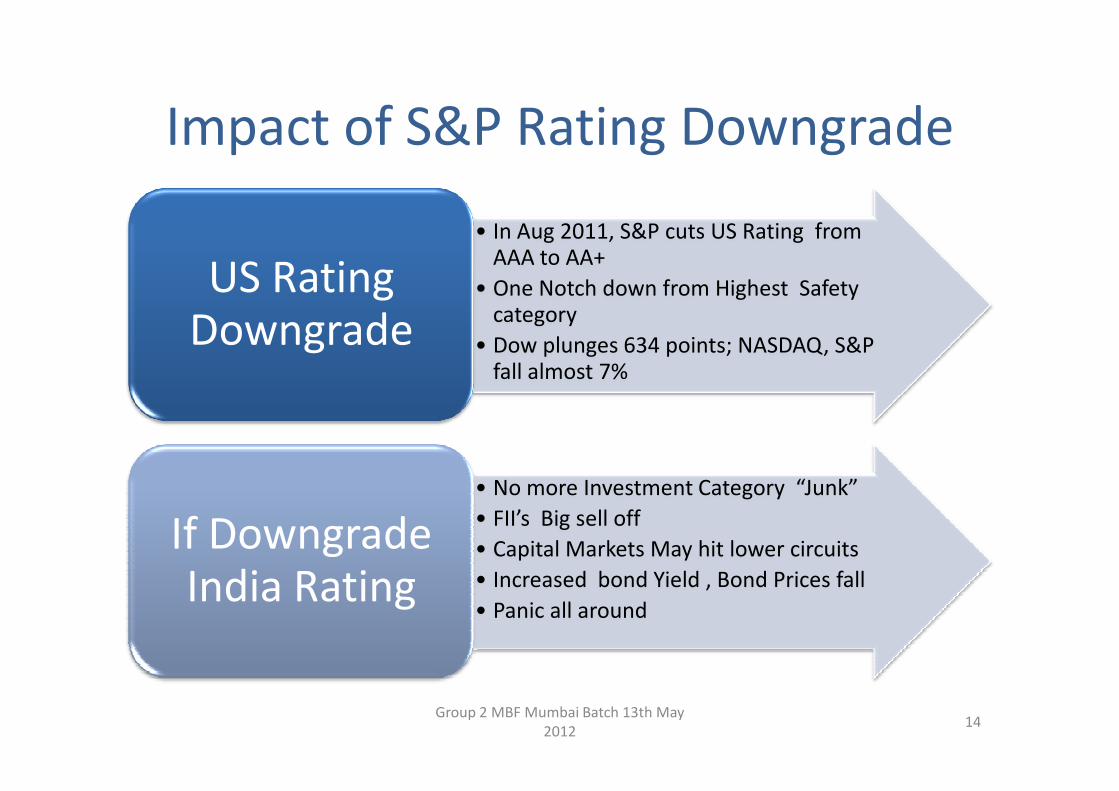

Impact of S&P Rating Downgrade

• In Aug 2011, S&P cuts US Rating from AAA to AA+

• One Notch down from Highest Safety category

• Dow plunges 634 points; NASDAQ, S&P fall almost 7%

US Rating Downgrade

Group 2 MBF Mumbai Batch 13th May

2012

• No more Investment Category “Junk”

• FII’s Big sell off

• Capital Markets May hit lower circuits

• Increased bond Yield , Bond Prices fall

• Panic all around

If Downgrade India Rating

14

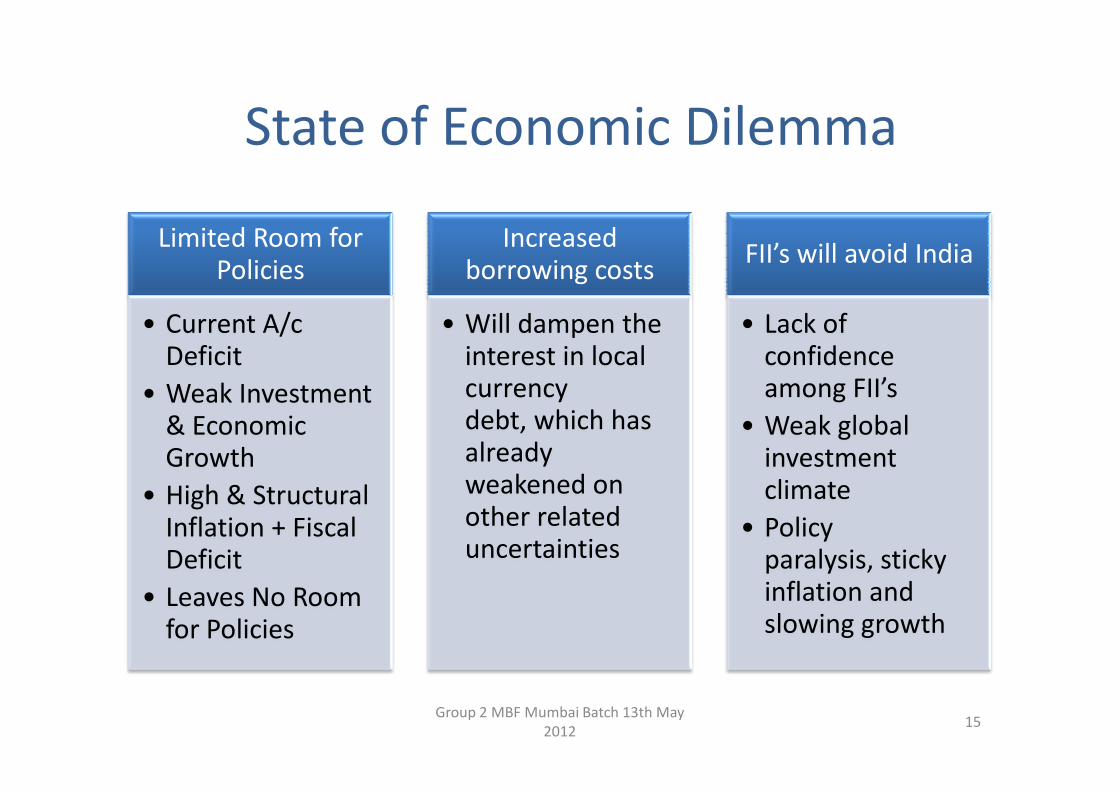

State of Economic Dilemma

Limited Room for Policies

• Current A/c Deficit

• Weak Investment

Increased borrowing costs

• Will dampen the interest in local currency

FII’s will avoid India

• Lack of confidence among FII’s

Group 2 MBF Mumbai Batch 13th May

2012

• Weak Investment & Economic Growth

• High & Structural Inflation + Fiscal Deficit

• Leaves No Room for Policies

currency debt, which has already weakened on other related uncertainties

among FII’s

• Weak global investment climate

• Policy paralysis, sticky inflation and slowing growth

15

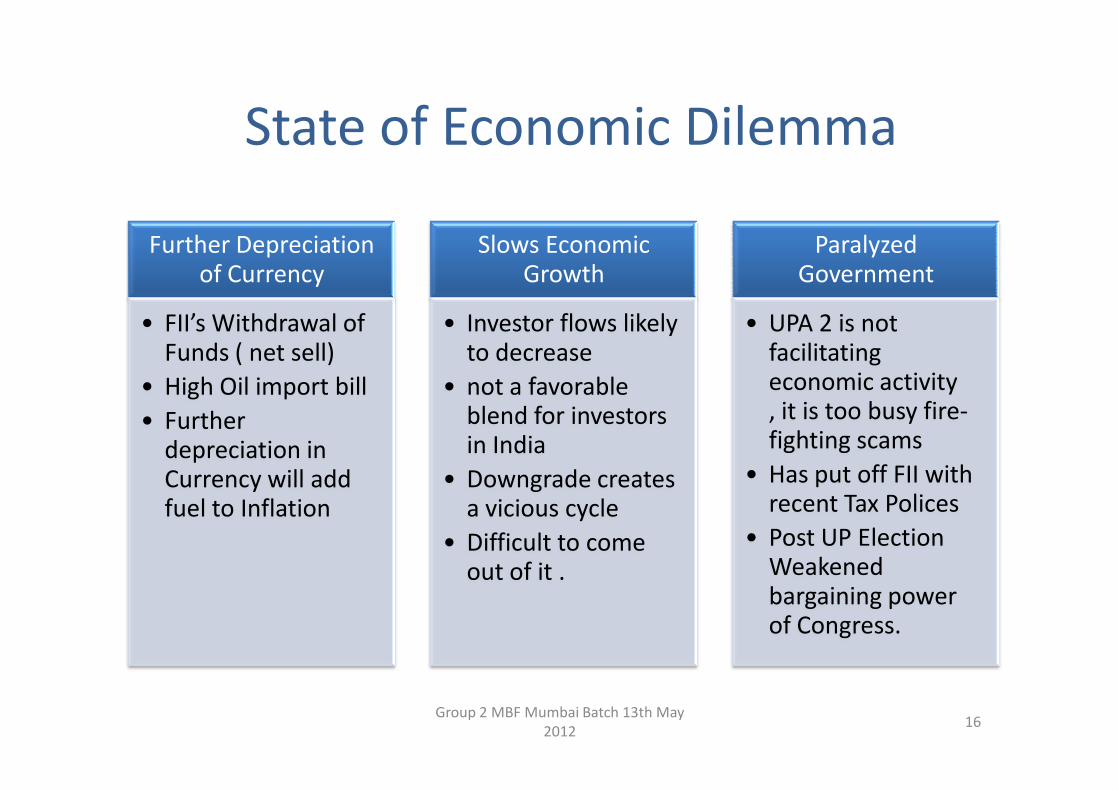

State of Economic Dilemma

Further Depreciation of Currency

• FII’s Withdrawal of Funds ( net sell)

• High Oil import bill

Slows Economic Growth

• Investor flows likely to decrease

• not a favorable

Paralyzed Government

• UPA 2 is not facilitating economic activity , it is too busy fire-

Group 2 MBF Mumbai Batch 13th May

2012

• High Oil import bill

• Further depreciation in Currency will add fuel to Inflation

• not a favorable blend for investors in India

• Downgrade creates a vicious cycle

• Difficult to come out of it .

economic activity , it is too busy fire-fighting scams

• Has put off FII with recent Tax Polices

• Post UP Election Weakened bargaining power of Congress.

16

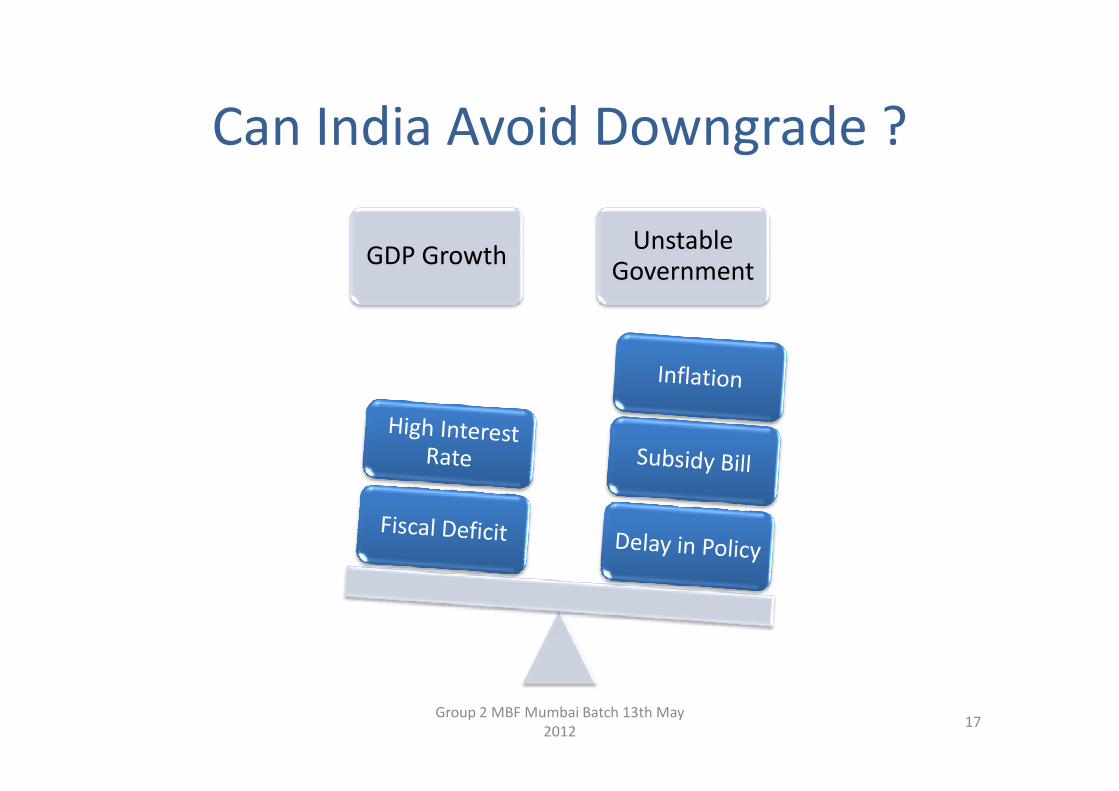

Can India Avoid Downgrade ?

GDP GrowthUnstable

Government

Group 2 MBF Mumbai Batch 13th May

201217

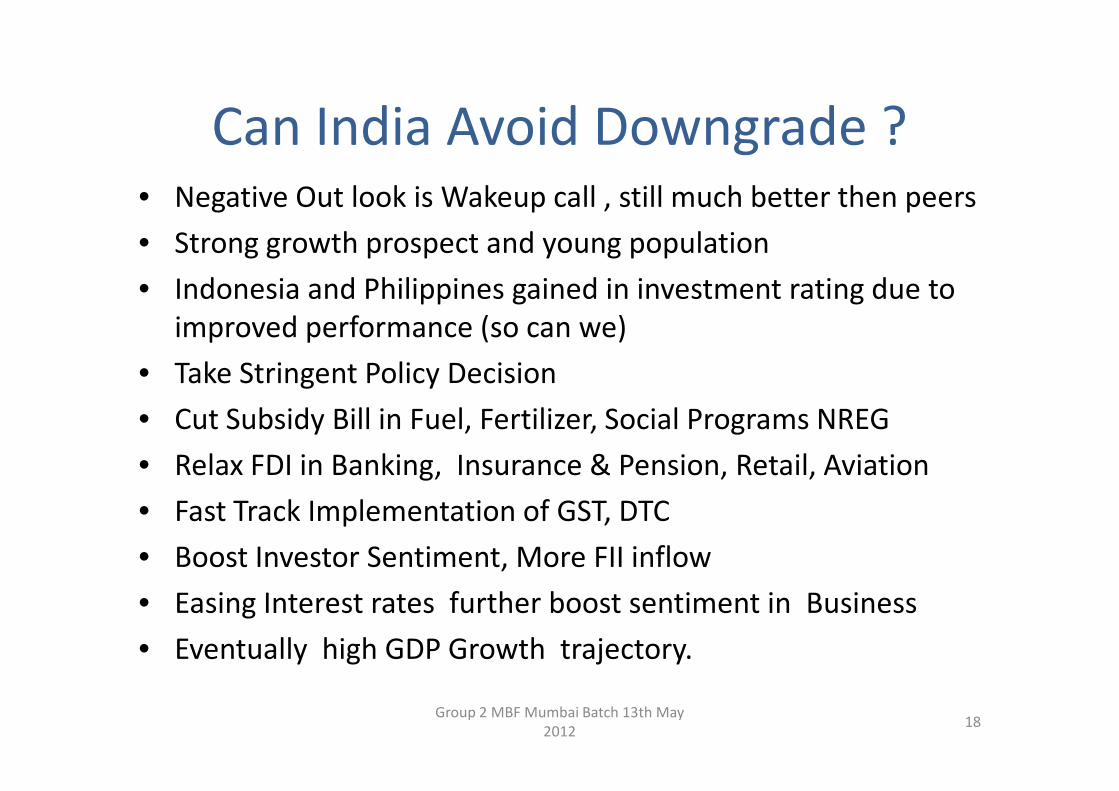

Can India Avoid Downgrade ?• Negative Out look is Wakeup call , still much better then peers

• Strong growth prospect and young population

• Indonesia and Philippines gained in investment rating due to

improved performance (so can we)

• Take Stringent Policy Decision

• Cut Subsidy Bill in Fuel, Fertilizer, Social Programs NREG

• Relax FDI in Banking, Insurance & Pension, Retail, Aviation

• Fast Track Implementation of GST, DTC

• Boost Investor Sentiment, More FII inflow

• Easing Interest rates further boost sentiment in Business

• Eventually high GDP Growth trajectory.

Group 2 MBF Mumbai Batch 13th May

201218

Risks

• Biggest Risk to Indian Economy is absence of Political

Consensus

• Implementation of key polices

• Opposition to reduce diesel subsidy, reversal of gold

duty, retro tax provision, GST rollback, FDI in retail rollbackduty, retro tax provision, GST rollback, FDI in retail rollback

• Un due Political Pressure from coalition parties.

Group 2 MBF Mumbai Batch 13th May

201219

S&P – Can we trust?

• Every Major crisis has been missed by the rating agencies and in aftermath of every crisis they have been very quick to downgrade – Montek singh Ahluwalia deputy chairman PMEAC

• Assigned high rating to Latin America in 1980’s especially at time when they were going bustespecially at time when they were going bust

• They had positive rating for Asian economics when they were going bust in 1997-98

• Euro crises – no downgrade

• They had not downgraded US in 2008 sub-prime crises

• They had not downgraded Lehman Brothers in 2008.

Group 2 MBF Mumbai Batch 13th May

201220

Various responses on Outlook revision

• No Need to Panic government is committed to economic reforms, it

should be taken as timely Warning – Pranab Mukhrejee Finance Minster

• Government should see this as a wake up call and address these issues –

CLSA Singapore

• Some concerns expressed by S&P will be resolved during the year. I would

expect S&P to reverse and perhaps upgrade rather than downgrade –expect S&P to reverse and perhaps upgrade rather than downgrade –

C Rangrajan PMEAC chairman

• A downgrade is likely if the economic growth prospects dim, external

position deteriorates, political climate worsen or fiscal reforms slow.-

Ogawa S&P

Group 2 MBF Mumbai Batch 13th May

201221

Thanks Thanks

Group 2 MBF Mumbai Batch 13th May

201222

Group 2 MBF Mumbai Batch 13th May

201223