Embed Size (px)

Citation preview

IMPACT OF TAXATION ON GROWTH OF SMALL AND MEDIUM ENTERPRISES. A

CASE STUDY OF BIDCO UGANDA (2013 -2016)

BY

APINYFOSCA

BBA/41211/133/DU

A RESEARCH REPORT SUBMITTED TO THE COLLEGE OF ECONOMICS

AND MANAGEMENT SCIENCE IN PARTIAL FULFILMENT OF THE

REQUTREMENTS FOR THE AW ARD OF BACHELORS

DEGREE IN BUSINESS ADMINISTRATION OF

KAMP ALA lNTERNATIONAL

UNIVERSITY

APRIL 2016

-------~- -

DECLARATION

I Apiny Fosca declare that this research report is my original work and to the best of my

knowledge, it has never been presented elsewhere in any university or institution of learning for

approval.

Signed ....... ~ ...... . .

APINYFOSCA

BBA/41211/133/DU

[STUDENT]

Date . .,_ r .r. C?.i.l ~! 6 .....

----~----

APPROVAL

I, the undersigned certify that I have read and hereby recommend for acceptance by Kampala

International University a research report titled, the Impact of taxation on growth of small and

medium enterprises. A case study ofBIDCO Uganda (2013 -2016).

Signed ~ --DR. STANLEY KINY ATTA

rsUPERVISOR]

Date . f. I./ 0 t. ./ ii:P.({,

ii

DEDICATION

I dedicate this piece of work to my parents Mr. and Mrs. Okot Omia Thomas and lovely classmates

in the College of Economics and Management Science and my supervisor Dr. Stanley Kinyatta.

Ei

ACKNOWLEDGEMENT

I extend a vote of thanks to a number of people who unreservedly contributed towards the

accomplishment of this research work. I also would like to acknowledge the assistance and role

played by the following personalities to the successful completion of this study. I cannot say

exactly how grateful I am to my supervisor, Dr. Stanley Kinyatta. His guidance in this study was

beyond measure. Thank you also for providing me with professional advice, encouragement and

your time that has spurred me to success.

I also extend sincere thanks to my friends; Maureen, Isabella, Lillian, Jerry, brothers; Arnold,

Samuel, Bonnie and Isaac, and not forgetting my aunt; Gorret and family for their inspirations in

my studies.

May the Almighty God Bless you abundantly

T ADLE OF CONTENTS

DECLARATION ............................................................................................................................. i

APPROVAL ................................................................................................................................... ii

DEDICATION ........ ............... ............................................. ......... .................................................. iii

ACKNOWLEDGEMENT ................................... ............................................................. .......... ... iv

ABSTRACT .. .. ......... .................... . . ............. ....... ........................... . ... ... ........ viii LIST OFT ABLES ............................ ............... ........................... ................... ................................ ix

LIST OF FJGURES ........................................................................................................................ X

CHAPTER ONE ........................................................................................................................... 1

INTRODUCTION ......................................................................................................................... 1

1.0 Introduction ....... ........................................... .................... .... .... ................................................. 1

1.1 Background of the study ........................................................................................................... 1

1.2 Statement of the problem .................... ...................................................................................... 3

1.3 Purpose of the study .................................................................................................................. 3

1.4 Objectives of the study .............................................................................................................. 3

1.5 Research questious ..................................................................................................... ............... 4

1.6 Scope of the study ..................................................................................................................... 4

1.6.1 Subject scope ................ ................................................................... ...................................... 4

1.6.2 Geographical scope ........ ..... .................. ......................... ............................................. ...... ..... 4

1.6.3 Time scope .............. ............................................................................................................... 4

1.7 Significance of the study ................................................................................................... ........ 4

1.8 Conceptual frame ,vork ... ....................................... ...................... ............................................. 6

CHAPTER 'fWO ...................................................................... , ................................................... 8

LITERATURE REVIE\V ............................................................................................................ 8

2.0 Introduction ..... .. .......................... ......................................................................... ........... .......... 8

2.1 Effect of progressive tax on growth of SMEs ........................................................................... 8

2.2 The effect of corporation tax on growth of SNIEs ... ................... .......................................... . 10

2.3 The effect ofregressive tax on growth of SMEs ............. ............................. .................... ...... 12

V

CHAPTER THREE .................................................................................................................... 15

METHODOLOGY ..................................................................................................................... 15

3.0 Introduction ............................................................................................................................. 15

3 .1 Research Design ...................................................................................................................... 15

3 .2 Research Population .............. .................................................................................................. 15

3.2.1 Sample Size ...... ............. ....................................................................................................... 15

3.2.2 Sampling techniques and Procedure .................................................................................... 16

3.3 Sources of data ........................................................................................................................ 17

3.3.1 Primary data .................................................. ....................................................................... 17

3.3.2 Secondary data ..................................................................................................................... 17

3.4 Data collection Methods ..................................................... ..... ..................................... .......... 17

3.4.1 Questionnaire method ............................................................... .................................. ......... 17

3.4.2 Interview method ................................................................................................................. 18

3.5 Validity and reliability of research instrument ................................................................ ....... 18

3.5.1 Validity ................................................................................................................................ 18

3.5.2 Reliability ............................................................................................................................. 18

3.6 Data Processing and Analysis .............................................................................. ............. ..... . 19

3. 7 Ethical Considerations .......................................... .................................................................. 19

3.8 Limitations of the Study ........ .. ........ ............................................. ........................................... 19

CHAPTER FOUR ....................................................................................................................... 20

PRESENTATION, INTERPRETATION AND ANALYSIS OF FINDINGS ...................... 20

4.0 Introduction ........................................ ...... ........................................... ...... .................. ............ 20

4.1 Demographic Characteristics .................. ............. .. ................................................................. 20

4.1.1 Gender of respondents ...... : .................................................................................................. 20

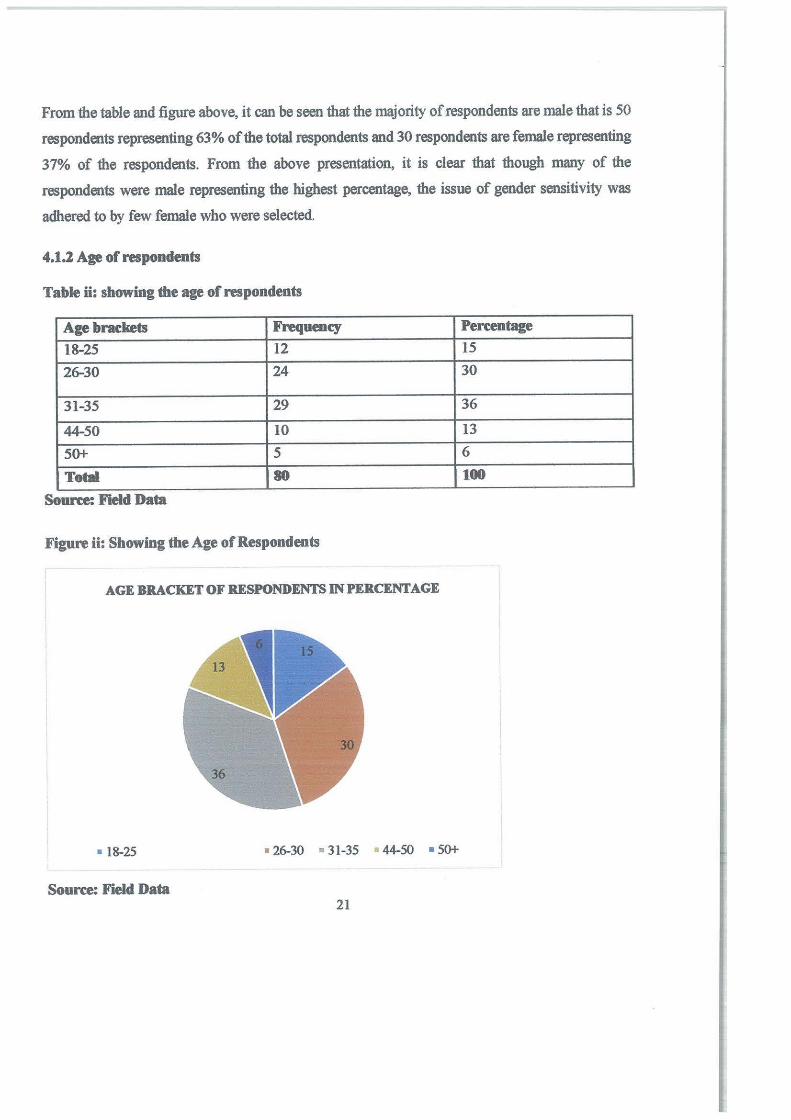

4.1.2 .t\ge of respondents .............................................................................................................. 21

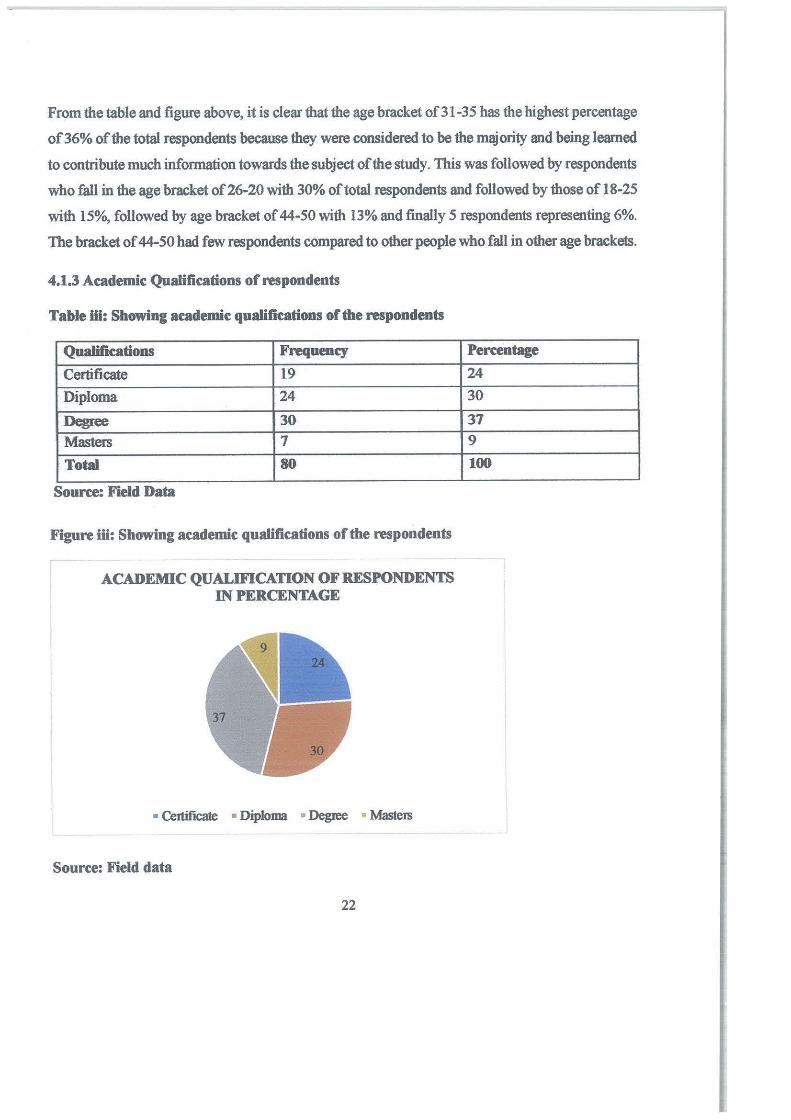

4.1.3 Academic Qualifications ofrespundents ............................................................................ 22

4.1.4 Marital status of respondents ................ ...................... ........................................ ................. 23

4.2 The effect of progressive tax on growth of SMEs in Kampala central division ..................... 24

vi

4.3 Effect of corporation tax on growth of SME~ in Kampala cer.tral division, Kampala district.

..................................................................................................................................... .. ................ 27

4.4 The effect of regressive tax on growth of SMEs in Kampala central division, Kampala

district. .............................................. ............................................................................................ 30

CHARPTER FIVE ...................................................................................................................... 33

SUMMARYs CONCLUSIONS, RECOMMENDATIONS AND AREAS OF FURTHER

RESEARCH ...................... , ......................................................................................................... 33

5.0 Introduction ............................... ............ .. ...... ... ............... .............................. ............... .. ......... 33

5.1 Summary of the findings ......................................................................................................... 33

5.2 Conclusions ................ .......... ................... ..................................................................... ........... 34

5.3 Recommendations ................................................................................................................... 35

5.4 Areas for further research ............................................. ........................................ .................. 35

REFERENCES ............................................................................................................................. 36

APPENDICES ............ ................................. ......................... .......... .............................................. 38

APPENDIX I: RESEARCH INSTRUfvffiNT: QUESTlO1'l'NAIRES .......................................... 38

APPENDIX H: INTERVIEW GUIDE ...................... ..................... ... .......... ............. ...... .. .... ........ 41

Appendix ii: Res~arch Budget ........................ ..... ........................... ........... ....................... ........... 42

APPEl\rorx iii: Research Time Fra!'ne ... .... ..... . ..... ........... . ... .. .......... . .... . ............... 44

Vl!

ABSTRACT

The topic entitled impact of taxation on growth of small and medium enterprises a case study of BIDCO Uganda (2013 -2016) was done under the following objectives; to examine the effect of progressive tax on growth of SMEs in Kampala central division, to examine the effect of corporation tax on growth of SMEs in Kampala central division and to examine the effect of regressive tax on growth of SMEs in Kampala central division. The researcher used a descriptive correlational survey research design where by both quantitative and qualitative approaches in data collection were used. The researcher used Slovene's Formula to come up with appropriate sample size to be used in the study and sample size of 80 respondents was selected to participate in the study. The researcher used the questionnaire which helped her in collecting data. The researcher' s findings were that taxation affe:;t and impact much on the growth of SMEs in Kampala central division, Kampala district according to the data collected whf.:reby 66% agreed almost in all perspectives. The researcher's conclusion was that progressive tax impact much on the growth of SMEs in Kampala central division, Kamp .. la district accordiug tc 66% respondents who agreed that they ensure valuable evaluation of business, reduce the operational capacity of business had 66% of the respondents, 53% of the respondents agreed that they are responsible for improved

steady operations of SMEs and tax holidays have heired you to invest in other side businesses had 57%, Will direct the growth course of the business had 52% and 41 % agreed that they Provide

avenues for improved organizational sustainability, corporation tax has effects on growth of SMEs in Kampala central division, Kampala district according to the respondents who strongly agreed and agreed that there are effects of corporation tax on growth of Sfv1Es in Kampala central division,

Kampala district, majority responder1ts were that there SMEs Enables the legal operation of busit}esses had 70%, Reduces the sales capacity of small &nd medium enterprise had 69%, reduces

the· profitability of the organizations had ' 65%, It caa be used as a marketing tool for the

organizational resources had 64% and Encourages the businesses operation on legal terms had 56% and regressive tax has effects the on grcwth of SMEs in Karr.p:1la c~ntral division, Kampala district according to 66% respondents who agreed Vvith Reduces the business resources, Can

contribute to collapse of businesses ha<l 62%, reduces the business operational capacities had 52% of the respondents, 52% of the respondents agreed Increase the operational means of organization had 45%. The researcher's recommendations were tax collection should be defined with respect to which government should collect certain truces from small and medium enterprises. This will avoid the government collecting taxes from the same particular organization, government should

also put a policy in place to avoid iliegal taxes, such as community levy, boys or youth levy and as well as association or uni0n levy .and taxes should be collected in relati'on to the sizes and profit

of Small scale businesses consid':!ring all other factors that can constrain the progress of such Small scale busi!iesses as there is a r1~!at:onship between smail scale businesses siz'es and their ability to pay taxes.

viii

LIST OFT ABLES

Table i: Showing Gender respondents ..... ........... ...................................... ..... ............................... 20

Table ii: Showing the age of respondents ..................................................................................... 21

Table iii: Showing academic qualificc1.tions of the respondents .................................................... 22

Table iv: Showing marital status of the respondents ............................................................ ........ 23

Table v: Showing the response on effect of progressive tax on growth of SMEs in Kampala

central division, Kampala district. ................................................................................................ 24

Table vi: Showing response to the effect of corporation tax on gro\\1h of SMEs in Kampala

central division, Katnpala district ................................................................................................. 27

Ta!Jle vii: Showing responses to the effect of regressive tax on growth of SMEs in Kampala

central division, Kampala district. ................................................................................................ 30

ix

LIST OF FIGURES

Figure i: Showing Gender respondents ......................................................................................... 20

Figure ii: Showing the Age of Respondents ... ...... ............................ .................... ......... .... ........... 21

Figure iii: Showing academic qualifications of the respondents .................................................. 22

Figure iv: Showing marital status of the respondents ................................................................... 23

Figure v: Showing the response to the effect of progressive tax on growth of SMEs in Kampala

central division, Kampala district showing those who Strongly agree and Agree in percentage. 26

Figure vi: Showing the response to the effect of corporation tax on growth of SMEs in Kampala

central division, Kampala district showing those who Strongly agree and Agree in percentage. 29

Figure vii: Showing responses to the effect of regressive tax on growth of SMEs in Kampala

central division, Kampala district. (Those who strongly agreed and agreed) ............................ ... 32

CHAPTER ONE

INTRODUCTION

1.0 Introduction

The study was meant to investigate tax systems and growth of small and medium enterprises in

Kampala Central Division. This chapter consists of the background to the study, statement of the

problem, purpose of the study, objectives of the study, research questions, scope of the study,

significance of the study and the conceptual frame work.

1.1 Background of the study

Worldwide, different governments use different kinds of taxes and vary the tax rates. This is done

to distribute the tax burden among individuals or classes of the population involved in taxable

activities, such as business, or to redistribute resources between individuals or classes in the

population. Historically, the nobili.ty were supported by taxes on the poor; modern social security

systems are intended to support the poor, the disabled, or the retired by taxes on those who are still

working. In addition, taxes are applied to fund foreign aid and military ventures, to influence the

macroeconomic performance of the economy (the government's strategy for doing this is called

its fiscal policy; see also tax exempti0n), or to modify patterns of consumption or employment

within an economy, by making some classes of trcr.saction more or less attractive Income tax

proficiencies as a center of attention is rising hastily in both the private and public sectors and it is

imperative to appreciate the commenc!abk performan~e of many organizations of varying sizes as

a result (Kock, Gill and Ellstrom 2008; Risher 2000). Conversely, there are perceptible confines;

studies have often been predisposed towards large enterprises and public organization (Hill, 2004);

little (if any) proficiency literature in the area of taxation. But from a limited number of studies on

proficiencies in small to medium-sized enterprises (SMEs), the concentration has mainly been on

entrepreneurial, managerial and technological proficiencies.

Tax systems increase incentives· for· public · participation in the political process and creates

pressure for more accountability, better g,rver:iam:e, ·.;nd improved efficiency of government

spending. Tax systems also create incentives for governments to upgrade their institutions for tax

collection and administration and to provide more public services (Moore, 2007).

The tax systems affect the growth of small and medium enterprises in different ways for different

entrepreneurs and corporations. This calls for a thorough analysis of any proposed changes in the

tax system. The Uganda's tax system has witnessed a number of challenges since 1980. In the

l 980's, export taxes played a significant role in revenue collections when its share of total revenue

ranged between 15 percent and 68 percent. As the role of expo1t taxes started diminishing in the

late 80's, which was followed by a fall in tax-to-GDP ratio, Uganda sought tax reforms that could

improve revenue collections in a sustained manner. The reibrms started with the formation of a

semi-autonomous revenue agency (Uganda Revenue Authority, URA) to collect tax revenues on

behalf of the central Government. Later in the mid 1990's VAT was introduced to replace sales

tax and Commercial Transaction Levy (CTL), and the new Income Tax Act (!TA) (1997) replaced

the Income tax decree (1974). These tax reforms partly attributed to the increase in the tax-to-GDP

to 13.6 percent by end of2003/04, from its low level of7.8 percent in the pre-reform period and

thus affecting the growth of smail and medium enterprises.

According to Chen Loo & Keng Ho, (2005), an appropriate compliance can only be realized when

taxpayers liability is correctly computed, after taking into account all factors that have a bearing

on the tax liability. The taxpayer has to be competent to comprehend the income tax law and the

administrative procedures, given the complexities, uncertainties and ambiguities of the tax law,

rules and administrative procedures. Therefore, taxpayers who are tax illiterate or inadequately

informed may either be under-pitying or over-paying taxes. As well, the revenue authority has to

provide adequate resources to meet the needs of enhancing taxpayer functional literacy elements

in terms of skills and knowledge required to deal with tax matters and provide understanding about

tax systems.

In Uganda the tax systems and reforms of 1997 were implemented as a means of increasing the

government's revenue in a sustainable manner. It was expected that the revenue raised would be

used to support the government's poverty reduction interventions as identified in its Poverty

Eradication Action Plan (PEAP). But morethaa 40 percent of public spending in pove1ty reduction

activities is supported by donors. Tax revenue as a share of Gross Domestic Product (GDP)

increased from 10.8 percent in 1997/98 to only 13.6 percent in 2003/04. Uganda like many other

developing countries tax revenue as a share of the GDP remains small, constraining the

government's overall expenditure capacity and strict imposed rules in small and medium

e;nterprises.

All businesses in Kampala Central Division adhere to different forms of taxes and different

taxation systems are employed. At leas! 50 small scale :ind medium enterprises pay taxes to the

government. The small scale businesses are locally mirned and managed by private individuals

who sometimes employ their family members and s0me medium enterprises are owned by a group

of individuals and cooperatives. It's clear that both small scale and medium enterprises bear a wide

tax burden which has led to poor performance. Therefore, it was against this background that the

researcher undertook the study to investigate more about tax systems and growth of small and

medium enterprises in Kampala Central Division.

1.2 Statement of the problem

Despite of the tax systems in plac~-such as progrcssiv_e tax, corp_orate tax and regressive taxes

introduced to improve on Sl\1E's, th~ performance_ of SMES has not improved and one wonders

why they are still performing poorly. Therefore, the study is to establish the r_elationship between

tax system and grovvth of Small Scale and Medium Enterprises in Kampala central division,

Uganda.

1.3 Purpose of the study

The purpose of the study was to investigate tax system and growth of small and medium

enterprises i::i Kampala Central Divis:on, U~anda.

1.4 Objeetives of the study

i. To examine the effect of progressive t::ix on growth of SMEs in Kampala central division.

ii. To examine the effect of corporation tax on growth of SMEs in Kampala central division.

iii. To examine the effect ofregressi.ve tax on growth of SMEs in Kampala central division.

" J

1.5 Research questions

i. How does progressive tax affect growth of SMEs in Kampala central division?

ii. How does corporation tax affect growth of SMEs in Kampala central division?

iii. How does regressive tax affect growth of SMEs in Kampala central division?

1.6 Scope of the study

1.6.1 Subject scope

The study covered small scale and medium enterprises in Kampala Central Division. Specifically,

the study investigated the tax systems and growth of small scale and medium enterprises. The

researcher divided the topic inform of objectives which were to; examine the effect of progressive

tax on growth of SMEs in Kampala central division, examine the effect of corporation tax on

growth of SMEs in Kampala central division and to examine the effect ofregressive tax on growth

of SMEs in Kampala central division.

1.6.2 Geographical scope

The study was carried out in BIDCO, Kampala ce_ntral division, Kampala district. The area was

purposely selected because the researcher stays within the vicinity and therefore this eased data

collection.

1.6.3 Time scope

The study was carried out for the period between 2013 to 2016. This was considered because it

was appropriate eno,1gh for th~ researcher to get the required information about the topic of the

study. This period was also selected to enable the researcher come up with coherent information

from the respondents as it enabled the respo_ndents to give responses that were typical of their

opinion from the observations made over this period.

1.7 Significance of the study

The findings of tht: study are signif:c&nt on the following ways; 4

To scholars and researchers, the findings of the study are expected to contribute to the existing

literature about taxation and small and medium enterprises.

To the tax authority and government, the study will guide them in adjusting tax policies and tax

systems to suit requirements of small scale and medium enterprises.

To future academicians especially of Kampala International University, the study will help in

gaining insight about tax systems and growth of sr.1all scale and medium enterprises.

The accomplishment of the study wil! enable the researcher to acquire hands on skills about

processing of research work and data anc.lysis. This proficiency will enable the researcher to handle

such related work with a lot of precision and proficiency.

5

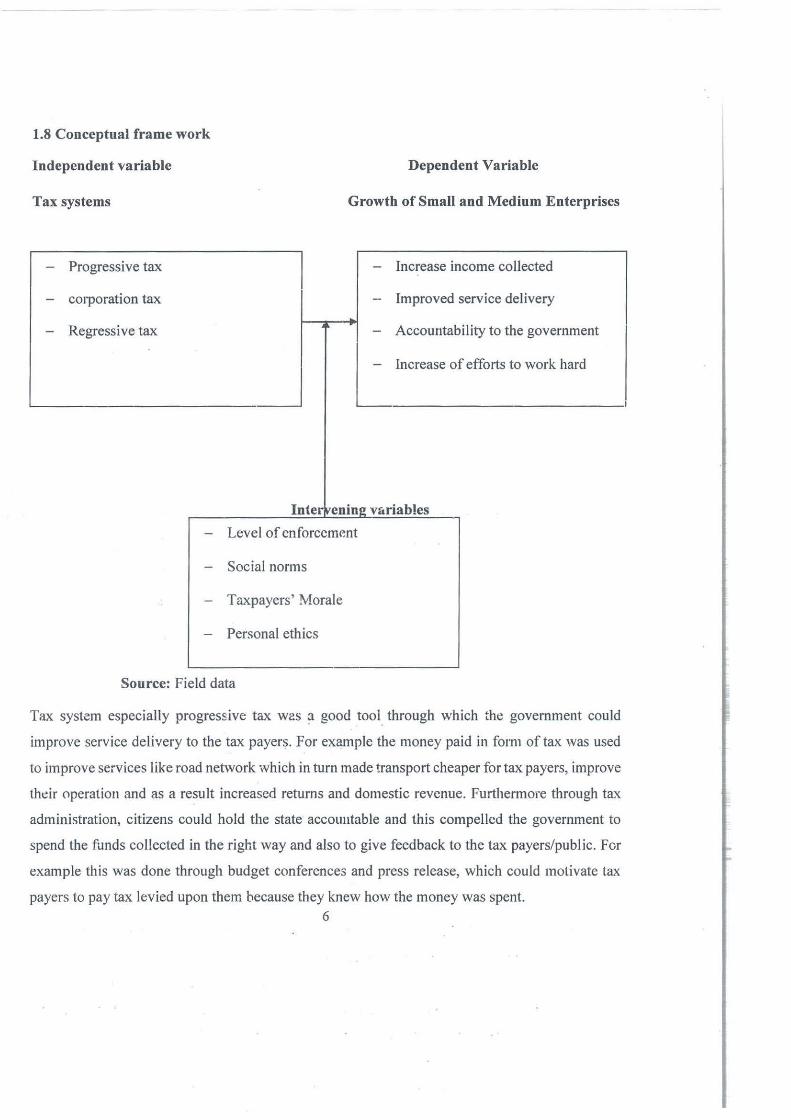

1.8 Conceptual frame work

Independent variable

Tax systems

- Progressive tax

- corporation tax

- Regressive tax

-

-

-

-

Dependent Variable

Growth of Small and Medium Enterprises

- Increase income collected

- Improved service delivery . ·~ .

Accountability to the government -

- Increase of efforts to work hard

Inter venine: v&riables

Level of enforcement

Social norms

Taxpayers' Morale

Personal ethics

Source: Field data

Tax system especially progres~ive tax was ;i good tool through which the government could

improve service delivery to the tax payer~. For example the money paid in form of tax was used

to improve services like road network ·,vhich in turn made transport cheaper for tax payers, improve

thdr operation and as a result increased returns and domestic revenue. Furthermore through tax

administration, citizens could hold the state accountable and this compelled the government to

spend the fonds collected in the right way and also to give feedback to the tax payers/public. For

example this was done through budget conferences and press release, which could motivate tax

payers to pay tax levied upon them because they knew how the money was spent. 6

I

Good and efficient tax administration of tax systems can increase the level of domestic revenue

collected. This was possible especially when the funds collected were correctly registered and

allocated to the right purpose.

'7 I

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction.

In this literature review, several materials for example textbooks, magazines, pamphlets

newspapers and the internet were consulted. This chapter provided literature on objectives of the

study.

2.1 Effect of progressive tax on growth of SMEs

A progressive tax is a tax where the tax rate increases as the taxable base amount increases. The

tem1 "progressive" refers to the way the tax rate progresses from low to high, with the result that

a taxpayer's average tax rate is less than the person's marginal tax rate. The term can be applied

to individual taxes or to a tax system as a whole; a year, multi-year, or lifetime. Progressive taxes

are imposed in an attempt to reduce the tax incidence of people with a lower ability-to-pay, as such

taxes shift the incidence increasingly to those with a higher ability-to-pay. The opposite of a

progressive tax is a regressive tax, where the relative tax rate or burden decreases as an individual's

ability to pay increases.

Progressive taxation is a form taxation where the taxpayer's tax base and liability are ascertained

basing on estimation ofactual activity. It is levied to combat avoidance; evasion buttressed by high

costs of verification and detection; and compliance difficulty, because of the nature of the activity

or perhaps at the lower income reaches, ignorance of procedures (Rajaraman, 1995). In Uganda,

progressive taxation is meant to be used when charging income taxes on the incomes of small and

medium enterprises. In Uganda, progressive taxation is meant to be used when charging income

taxes on the incomes of small and medium enterprises. The small and medium enterprises are most

of the time considered to make up the informal sector and normally do not keep records.

It is apparent that preferences for p·rogressivity in response· to conciete questions differ

significantly from abstract questions. Blum and Kalven (1953); Keene (1983) have suggested that

the complexities of progressive taxation may not be well understood by the general public. If the

8

consequences of progressive taxation are not well under- stood, then the results of surveys that

rely solely on abstract questions to determine public support for progressive or flat tax rates may

be misleading. In order to better describe the preferences for fair tax rates among the public,

researchers should consider using multiple methods, including more concrete frames, and

questions that allow a determination of the respondents understanding of tax terminology.

Progressive taxes are primarily aimed at financing public expenditures. Progressive taxes are also

used to promote other objectives, such as equity, and to address social and economic concerns.

They need to be set up to minimize taxpayers" compliance costs and government. The

administrative cost, while also discouraging tax avoidance and eyasion. But taxes also affect the

decisions of households to save, supply labour and invest in human capital, the decisions of firms

to produce, create jobs, invest and innovate, as well as the choice of savings channels and assets

by investors. What matters for these decisions is not only the level of taxes but also the way in

which different tax instruments are designed and combined to generate revenues (what this paper

will henceforth refer to as tax structures). The effects of tax levels and tax structures on agents"

economic behaviour arc likely to be reflected in overall living standards. Recognizing this, over

the past decades many OECD countries have undertaken structural reforms in their tax systems.

Most of the personal income tax reforms have tried to create a fiscal environment that encourages

saving, investment, entrepreneurship and provides increased work incentives. Likewise, most

corporate tax reforms have been ririven by the desire to promote cor,1petition and avoid tax-induced

distortions. Almost all of these tax reforms can be characterized as involving rate cuts and base

broadening in order to improve efficiency, while at the same time maintain tax revenues.

According to Mwenney (2003) Progressive tax syslem will need to consider the design of tax

systems in other countries, since countries are increasingly using their tax systems to improve their

ability tu compete in global m:!rkets. Globalization may also increase the opportunities for tax

avoidance and evasion especially as concerns mobile capital fr1come tax bases. Therefore, the

mobi I ity of the tax base plays some part in the design of tax reforms at the national level, and ,·

increased international tax policy cooperation among countries may allow for efficiency gains in

some areas.

9

Progressive tax system refers to a method of collecting taxes from tax payers using the gross annual

flirnovcr 1997). The income tax liability of the tax payers is determined without using financial

reports. The progressive method applies to resident, non-professionals with a gross annual turnover

ci not exceeding fifty million shilling (Akileng, 2006). This tax system does not apply to resident's

tax payers who are in the business of providing medical, dental, architectural, engineering,

accounting, legal or other professional services, public entertainer's public utility services and

construction services (1TA 1997 and Waliya 2005).

Braithwaite, V. (2009) argues that Self-Employment Tax is a social security and Medicare tax

imposed en freelancl.)rs and other self-employed workers. I It is identical to the social security tax

withheld from the pay of most workers, but because they are required to contribute both the

employer and the employee portions of the social security tax, the self-employed pay at :'l rate of

15.3% of net earnings double the amount paid by traditional employees The high social security

tax rate is a significant expense for many independent workers. Is it reasonable to require the self

employed to pay double social security taxes because they can be considered both the employer

and the employee, despite the fact th<!t they·aro a single worker? As the number of self- employed

workers grows, it may become time to consider strategies aimed at equalizing the social security

tax burden across all workers.

According to most political philosophies, taxes are justified as· they fund activities that are

necessary and beneficial to society. Addilionally, p:-ogressive taxation can be used to reduce

economic inequality in a society. According to this view, taxation in modern nation-states benefits

the majority of the population and social development. A common presentation of this view,

paraphrasing various· statements by Oliver Wendell Holmes, Jr. is Taxes are the price of civilization.

2.2 The effect of co:-.poration tax ou grow~t of SNlEs.

There have been severe.I writers who have talked about the cor:-elation cf corporation tax and

growth of small and medium erlterpiises. For example (Bird, 1992); (IMF, Jakarata 2000) noted

that improvement :n corporation tax woul<l lead to .ir.~re~sed revenue pt!rformance. In China,

corporation tax has led to increased contribution to the total revenue collection. More sources of

revenue were identified: corporation tax was able to contribute 61.6% to total revenue in 1995

10

~ ,: • J

from 7.8% in 1952. (IMF, China, October 2000). The same is the case for Malaysia and Singapore

(IMF. S. I I Asia studies 200 I).

Corporate taxes, influence productivity in several ways. Evidence in this study suggests that

towering statutory corporate tax rates can lead to particularly large productivity gains in firms that

are dynamic and profitable, i.e. those that can make the largest contribution to GDP growth. It also

appears that corporate taxes adversely influence productivity in all firms except in young and small

firms since these firms are often not very prcfitable. One possible implication is that tax

exemptions or reduced statutory corp0rate tax rates for small firm5 might be much less effective

in rais;ng productivity than a generalized reducti:.in in the overall stelutory corporate tax rnte. This

reduction could be financed by scaling down ex0mptions granted on firm size as they may only

waste resources without any substantial positive growth effects.

A widely-used policy avenue to improve productivity is to stimulate private-sector innovative

activity by giving tax incentives to R&D expenditure. This study finds that the effect of these tax

incentives on productivity appears to be relatively modest, although it is larger for industries that

are structurally mere R&D intensive. Nonetheless,' tax incentives have been found to have a

stronger effect on R&D expenditure than direct fimdlng. Lower corporate and labour taxes may

aiso epcourage inbcur.d fo~cign direct investment, wnici, has bee,1 f'"1und tc increase productivity

of resident firms. In addition, multinational eateq.,ris~s are attrnc:eJ by.tax systems that are stable

and p1:edictable, and which are administered in an efficier:t and transparent manner.

Corpt>rate tax is where a government authority determines the tax i·evcnue of organization:!! units

by identifying eligible taxpayers, assessing through setting the tax rate, collecting and sensitizing

the potential tax payers Bailey (I 999). As a reliable source of revenue, corporate tax as observed

by Musgrnve and Musgrave (1989) is the major representative of wealth taxation and third most

important tax in !he United Strrtcs and continues to dominate local taxation (US Statistics of

income, 20.05) The fimct:cins .. of the· Domestic Direct T~xes (DDT) m<i to ensur0 gnalily, timely

corporatimi t~xes a·J1Tl.inistr2.tio.a. The t:Xe:, i'nVoivcJ ~;e co;·pora~i·cn tax; individual inCome tax,

Pay as you c~rn (PA '{E) rGntal tax a1~d withhold[r.g tax. Co~poration !ax is ta:; ·1evid on the income

1 I

' ..

I I f,

I II I.

II r

I

I

ofcompanies following enactment of the Income Tax Act 1997 as amended to sustain the country's

growth.

Compulsory taxation of individuals, such as income tax, is often justified on grounds including

territorial sovereignty, and the social contract. Defenders of business taxation argue that it is an

efficient method of taxing income that ultimately flows to individuals, or that separate taxation of

business is justified on the grounds that commercial activity necessarily involves use of publicly

established and maintained economic infrastructure, and that businesses are in effect charged for

this use. Georgis! economists argue that all of the economic rent collected from natural resources

(land, mineral extraction, fishing quotas, etc.) is unearned income, and belongs to the community

rather than any individual.

2.3 The effect of regressive tax on growth of SMEs

According to Tindimwebwa (1999), basically regressive taxation is a method of determining

income and tax liability of small business taxpayers with the view of widening the tax base and

increasing the tax revenue yield. Rajaraman (1995) explains that the type of indicator selected

determines the form of presumption chosen and categories the indicators into; measures of entity

specific flows at either the output or input ends of the activity, stock measures of income

generating capacity or an income average across enterprises. In Uganda, the indicator ofestimation

used is the gcoss anr:ual turnover without dependence on financial accounting reports (Income fax

Act. l 997). The residents and nonµrofossional businesses with a gross turnover not exceeding fifty

million shillings are at liberty to use this system. Irrespective of the tax reforn1s to include small

and medium enterprises in Uganda's tax system, the non-compliance rate among the SMEs has

remained high (Sserwanga, 2003).

Sunley et al. (1996), recognizes the complex and complicated nature of taxation of small business

that existed under the deposit system before 1995, in making a recommendation for Uganda to re

adopt a form of regressive income taxation for sm~ll b~isiness enterprises based upon standard

assessments did not shO\v whether it was ari efficient kill'.l ofta'x for small business tax payers as

to qualify fer a good tax system.

12 I

I

As pointed out by Bird and Wallace (2004) the critical issue is whether these regressive methods

of taxation are really effective first in bringing firms into the formal economy and then, after few

years, forcing them to move into the normal tax system, while minimizing the number of firms

that move from the normal tax regime into the simplified one. The main problem is that these

objectives arc to some extent inconsistent. To be attractive for informal firms the methods need

not to be simple and based on readily available information to reduce compliance costs (Araujo,

Bonjean and Chambas, 2004), they should also provide for an effective taxation that will be lower

than that based on the normal tax rules. However, this would discourage them from moving into

the normal tax regime and attract firms that are in the formal sector to move to the regressive

regime, resulting in loss of revenue to the Tax Authority. One solution to this conundrum might

be a periodical revision of the threshold for eligibility for the simplified regime.

Many low-income countries have a tax-to-GDP ratio of less than 15% which could he due to low

tax potential, such as a limited taxable economic activity, or Low tax effort due to policy choice,

non-compliance, or administrative constraints. Some low-income countries have relatively high

tax-to- GOP ratios due to resource tax revenues (e.g. Angola) or relatively efficient tax

administration (e.g. Kenya, Brazil) whereas some middle-income countries have lower tax-to

GOP ratios (e.g. Malaysia) which reflect a more tax-friendly policy choice. Whiie overall tax

revenues have remained broadly const~nt, the global trend shows trade taxes have been declining

as a proportion of total revenues (IMF, 2011 ), with the share of revenue shifting away from border

trade taxes towards domestically levied sales taxes on goods and services. Low-income countries

tend to have a higher dependence on wade taxes, and a smaller proportion of from income and

consumption taxes, when compared to high income countries.

Regressive systems based on indicators have become increasingly popular in transition countries,

these systems aim at being more precise than turnover - based systems in estimating the profit

potential of the individual entrepreneur (Hughes, 1999). Howe.ver, this brings up a clear conflict

of the objective. The objecti,1e to tax the true potential profit of the small business conflicts with

tli~ objective to design a simple and transpa:·ent system policy makers in transition countries face

considerable difficulties designing indicator based systems that est?.blish a:'i acceptable balance

these objectives. Systems tend to be cxfremely complicated and unclear or tr.ey do not sufficiently

13

differentiate between business activities (Drake, 2000). The latter is in case Georgia, where

regressive system only distinguishes between five groups of activities. The gap left will be filled

by the current study using the case study of Uganda.

14

CHAPTER THREE

METHODOLOGY

3.0 Introduction

This chapter deals with research design, research population, sample size, instrumentation,

validity, reliability, data gathering procedures, data analysis, ethical considerations and limitations

of the study.

3.1 Research Design

This research study employed a descriptive correlational survey research design. The study was

descriptive since it describes the indicators of taxation and their effect on SMEs performance in

Kampala. The correlational design related the two variables of the study; taxation and their effect

on SMEs performance in Kampala includiI}g the di~ensions of regressive, progressive and

corporation taxes.

3.2 Research Population

According to Diamantopoulos et al., (2000), population is the totality of an entities in which the

researcher has an interest, means it is the collection of individuals, objects or events in which the

researchc.- wants to make inferences. The target popul?.tion of the ~tudy was selected frcm tile

business communit-; in BIDCO especially those with Small and medium enterprises. This study

intended to tackle a group of 100 business owners of the market. The total population therefore

was amount to 100; these was selected for data collection.

3.2.1 Sample Size

From the estimated population of 100, a sample size was determined using Slovene's Formula to

come up with appropriate sample size t0 b~ ust:d in the stl,ldy . .

Solven's Formula states tha~, given a population, the minimum Sa~ple size is given by:

15

Where; n = the sample size

n = total population of targeted respondents 100

a= the level of significance, that is 0.05

n= N

l+Na2

n = 100

1+100(0.05)2

n = 100

I+ JOO *0.0025

n = 100

1.25

N = 80

Therefore, the sample size was be 80

3.2.2 Sampling techniques and Procedure

It's the process of extracting a pc,rtion of the population from which generalization to the

population can be made, lsman, A. et ai. (2003) Because of resource constraints, a small sample

was chosen and handled using stratified sampling procedure to select the sample population and

the respective people for data collection. Then the researcher selected simple random sample

independently from each Sub-population. Purposive sampling was used in the selection of

management of the market, these is because these arc perceived to have more suitable information

so purposive sampling enabled the attaining data from those officials with key knowledge on

taxation policy in the market.

16

3.3 Sources of data

In this study two types of data were used by the researcher, in that secondary and primary data

were used.

3.3.1 Primary data

Primary data is that data collected afresh and for the first time, has not been processed (Mugenda,

2006). Primary data was gathered basically through structured questionnaires and

interviews involving the selection of respondents to provide information.

3.3.2 Secondary data

Secondary data is information which has been already collected by someone else for other

purposes and can be used to compile data or raw dat:i. Secondary data was obtained through notes,

correspondences and minutes of meetings from, jo:.imals published in majorly on the taxation

policies and their subsequent effect on SMEs performance.

3.4 Data collection Methods

3.4.1 Questionnaire method

This is a technique in which the researcher gave a list of short questions to the respondents

requesting them to fill and collect them later. Closed ended questions designed to suit the

objectives were used to effectively attain data for the study. The approved questionnaires were

hand delivered to the respmidents ofBIDCO by the researcher and or any other research assistant

to be appointed by the researcher. The researcher designed a questionnaire on taxation and

performance of SMEs in KampaJa on 4 point scale rating. Therefore, a 4 point likcrt scale self

administered questionnaire comprising of statements and responses ranging from 1 =Strongly

Disagree to 4=Strongly Agree was formulated. Questionnaires were designed to capture all the

aspects of the objectives of the study.

17 ·

3.4.2 Interview method

The interview is one of the data collection methods. Rather than asking respondents to fill out

questionnaires, interviewers ask questions orally and simultaneously record the respondents'

answers. This data collection method generally decreases the number of the respondents that do

not know the answers compared with self-administered surveys. Interviewers also provide a guard

against confusing items. If a respondent has misunderstood a question, the interviewer can clarify,

thereby obtaining relevant responses.

3.5 Validity and reliability of researeh instrument

3.5.1 Validity

To ensure that the instrument used was valid, face validity was done by the supervisors and other

research consultants. Content validit}' index was also ascertained by the researcher and her

supervisor. These authorities declared the instrument valid and suitable for use in the study.

3.5.2 Reliability

The instrumeut was piloted on a few r~spondents that were not included in the study sample and

modified to improve their validity and reliability coefficients to at least 0.70. Items with validity

and reliability coefficients of at least 0.70 were accepted as valid and reliable in research Amin,

(2005). Reliability estimates the consistency of the _measurement. The reliability test involves a

"test and retest" exercise. This means -the instruments were subjected to a representative sample.

According to Amin (2005) validity of instrument is determined by the formula:

CVI = RQ TQ

Legends: CVI =Content Validity Index RQ = Relevant Questions

TQ = Total number of Questions

18

3.6 Data Processing and Analysis

During and after data collection, the researcher used different methods to process the data that was

collected so as to come up with a report that is easy to interpret and understand. Quantitative data

and information collected using questionnaires and responses from numerous respondents were

coded. (Open-ended questions was also coded appropriately), and entered and analyzed using

tables. The data again was presented inform of descriptive analysis, tables and graphs. The findings

was then been determined arising from the analysis and interpretation of information.

3.7 Ethical Considerations

The respondents were protected by keeping the information given confidential and where there is

a need to reveal, consent was first obtained.

The questionnaires were not including the names of the respondents for issue of privacy and

secrecy.

After the collection of data, questionnaires -were destroyed so that collected information doesn't

leak.

3.8 Limitations of the Study

It was not easy to locate the respondents the fact that these respondents were widely spread and

conducted their activities from different departments, this hindered data collection. The researcher

however designed a structured questionnaire that enabled respondents fill in their free time.

f'i!:ancial constraints, it was difficult for the researcher to raise enough funds for the research study.

The researcher used the fonds saved sparingly so that it could fund the entire budget.

The time frame was too limited to allow the researcher gather meaningful data and also make

realistic conclusions. The researcher ensured that the set time for the research was adhered to and

timely data collection accomplished the research.

19

CHAPTER FOUR

PRESENTATION, INTERPRETATION AND ANALYSIS OF FINDINGS

4.0 Introduction

This chapter comprises of the findings that were gathered by the researcher from BIDCO Uganda

in relation to the topic; Impact of taxation on growth of small and medium enterprises. The data is

presented and interpreted in view of the objectives mentioned in chapter one of this research. The

interpretation also seeks to answer the research questions that were raised in chapter one.

Presentation and interpretation of data in this chapter has been done with the aid of quantitative

and qualitative methods for example the use of tables, graphs, percentages and personal analysis

and interpretation presented in essay form. Questionnaires were provided to 80 respondents who

filled them to the best of their knowledge.

4.1 Demographic Characteristics 4.1.1 Gender of respondents Table i: Showing Gender respondents

Respondents Frequency Percentage

Male 50 63

Female 30 37

Total 80 100

Source: Field data

Figure i: Showing Gender respondents

GENDER OF RESPONDENTS IN PERCENTAGE

• Male • Female

Source: Field data

20

- ,- - --

From the table and figure above, it can be seen that the majority of respondents are mal

respondents representing 63% of the total respondents and 30 respondents are female rep

37% of the respondents. From the above presentation, it is clear that though man

respondents were male representing the highest percentage, the issue of gender sens

ethatis 50

resenting

y of the

itivity was

adhered to by few female who were selected.

4.1.2 Age of respondents

Table ii: showing the age of respondents

Age brackets Frequency Percentage

18-25 12 15

26-30 24 30

31-35 29 36

44-50 10 13

so+ 5 6

Teal 80 100

Source: Field Data

Figure ii: Showing the Age of Respondents

AGEBRACKETOFRESPONDENTSINPERCENTAGE

• 18-25 • 26-30 • 31-35 44-50 • so+

Source: Field Da1a 21

· .cc_~ ~ --·--~-

I:

I•

i,

11 1:

!i p , I :

I:

1; 1: 1;:

1,

I •

'"

- ---

bracket of 31-35 has the highest percentage From the table and figure above, it is clear that the age

of 36% of the total respondents because they were cons

to contribute much information towards the subject of

who fall in the age bracket of 26-20 with 30% of total

with 15%, followed by age bracket of 44-50 with 13'¾

The bracket of 44-50 had few respondents compared t

idered to be the majority and being learned

the study. This was followed by respondents

respondents and followed by those of 18-25

o and finally 5 respondents representing 6%.

o other people who fall in other age brackets.

4.1.3 Academic Qualifications of respondents

pondents Table iii: Showing academic qualifications of ffle res

Qualifications Frequency

Certificate 19

Diploma 24

Degree 30 Masters 7

Total 80

Source: Field Data

Figure iii: Showing academic qualifications of the respondents

PONDENTS ACADEMIC QUALMCATION OF RES IN PERCENTAGE

• Certificate • Diploma • Degree • Maste IS

Source: Field data

22

Percentage

24

30

37

9

100

1::

1:,

:;:

!: 1,

I •

1:

ii Ii

1,

;,

u

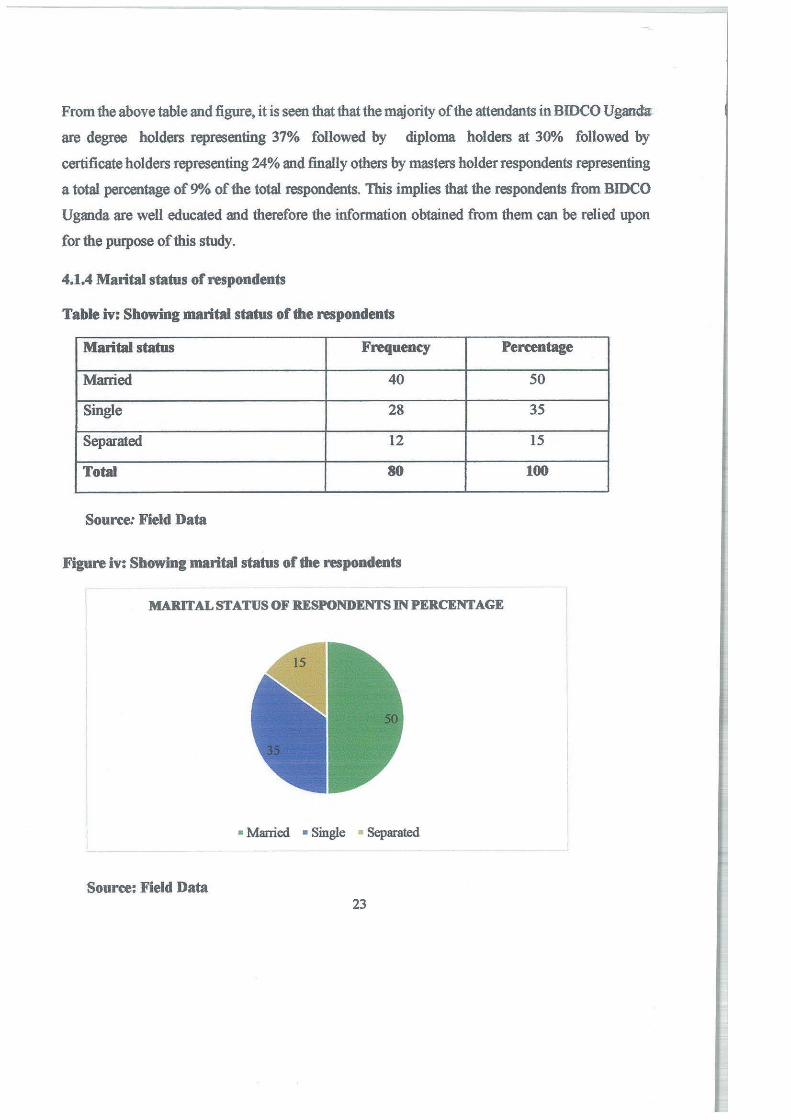

From the above table and figure, it is seen that that the majority of the attendants in BIDCO Uganda:

are degree holders representing 37% followed by diploma holders at 300/o followed by

certificate holders representing 24% and finally others by masters holder respondents representing

a total percentage of 9% of the total respondents. This implies that the respondents from BIDCO

Uganda are well educated and therefore the information obtained from them can be relied upon

for the purpose of this study.

4.1.4 Marital status of respondents

Table iv: Showing marital status of the respondents

Marital status Frequency Percentage

Married 40 50

Single 28 35

Separated 12 15

Total 80 100

Source: Field Data

Figure iv: Showing marital status of the respondents

MAlllTALSTATUSOFRESPONDENTSINPERCENTAGE

• Married • Single • Separated

Source: Field Data 23

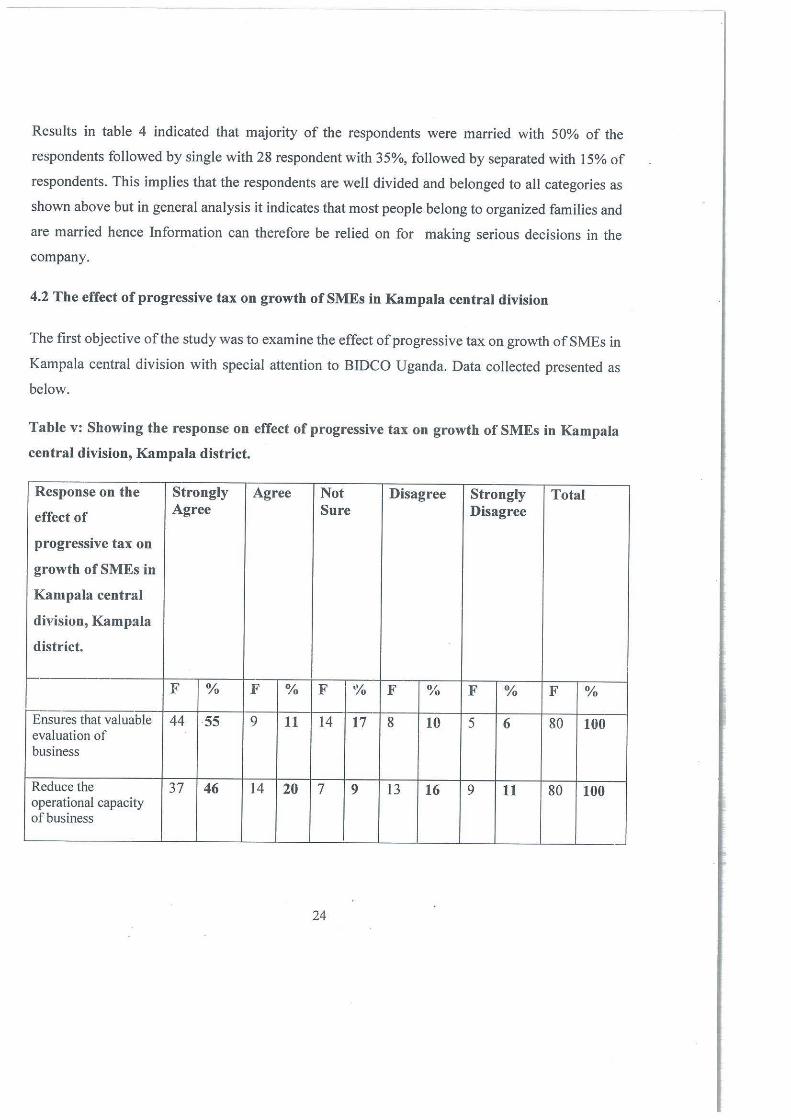

Results in table 4 indicated that majority of the respondents were married with 50% of the

respondents followed by single with 28 respondent with 35%, followed by separated with 15% of

respondents. This implies that the respondents are well divided and belonged to all categories as

shown above but in general analysis it indicates that most people belong to organized families and

are married hence Information can therefore be relied on for making serious decisions in the

company.

4.2 The effect of progressive tax on growth of SMEs in Kampala central division

The first objective of the study was to examine the effect of progressive tax on growth of SMEs in

Kampala central division with special attention to BIDCO Uganda. Data collected presented as

below.

Table v: Showing the response on effect of progressive tax on growth of SMEs in Kampala

central division, Kampala district.

Response on the Strongly Agree Not Disagree Strongly Total

effect of Agree Sure Disagree

progressive tax on

growth of SMEs in

Kampala central

division, Kampala

district.

F % F % F % F % F % F %

Ensures that valuable 44 .55 9 11 14 17 8 10 5 6 80 100 evaluation of business

Reduce the 37 46 14 20 7 operational capacity

9 13 16 9 11 80 100

of business

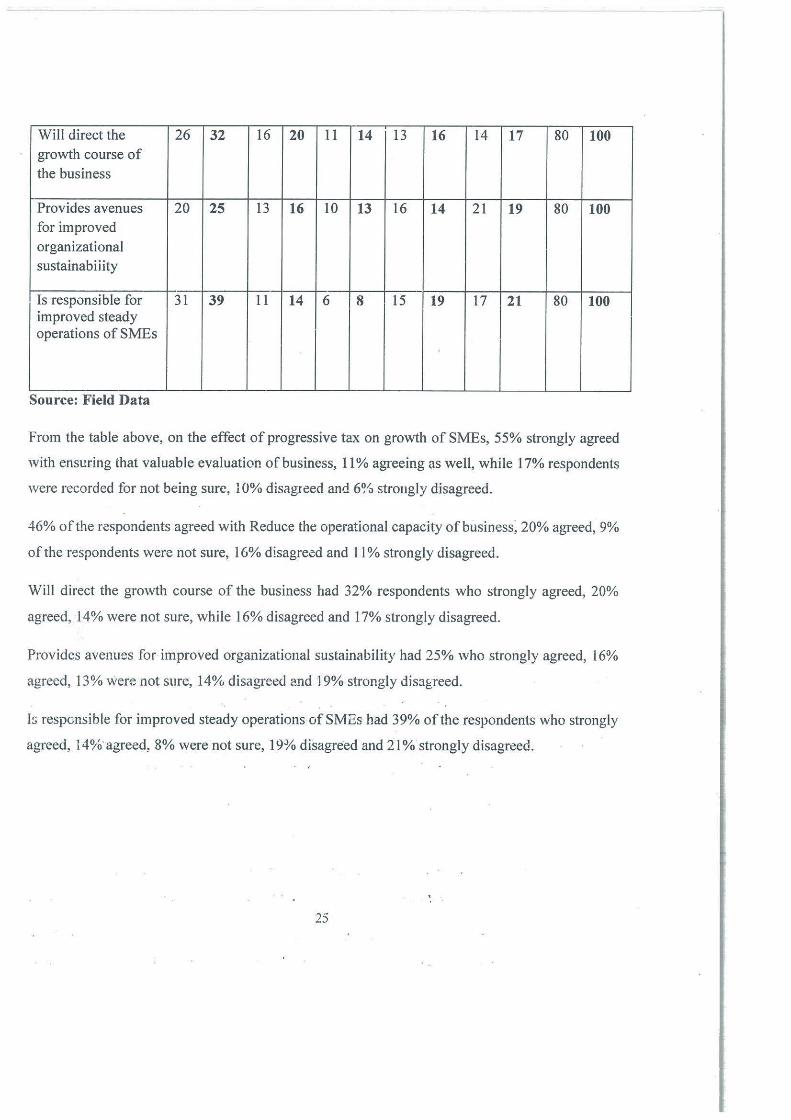

24

Will direct the 26 32 16 20 11 14 13 16 14 17 80 100 growth course of the business

Provides avenues 20 25 13 16 10 13 16 14 21 19 80 100 for improved

organizational sustainabiiity

Is responsible for 31 39 11 14 6 8 15 19 17 21 80 100 improved steady operations of SMEs

Source: Field Data

From the table above, on the effect of progressive tax on growth of SMEs, 55% strongly agreed

with ensuring that valuable evaluation of business, 11 % agreeing as well, while 17% respondents

were recorded for not being sure, 10% disagreed and 6% stro11gly disagreed.

46% of the respondents agreed with Reduce the operational capacity of business; 20% agreed, 9%

of the respondents were not sure, 16% disagreed and 11 % strongly disagreed.

Will direct the growth course of the business had 32% respondents who strongly agreed, 20%

agreed, 14% were not sure, while 16% disagreed and 17% strongly disagreed.

Provides avenues for improved organizational sustainability had 25% who strongly agreed, 16%

agreed, 13% were not sure, 14% disagreed and J 9% strongly dis:igreed.

I:; responsible for improved steady operations of SMEs had 39% of the respondents who strongly

agreed, 14%·agreed, 8% were not sure, 19¾ disagreed and 21% strongly disagreed.

25

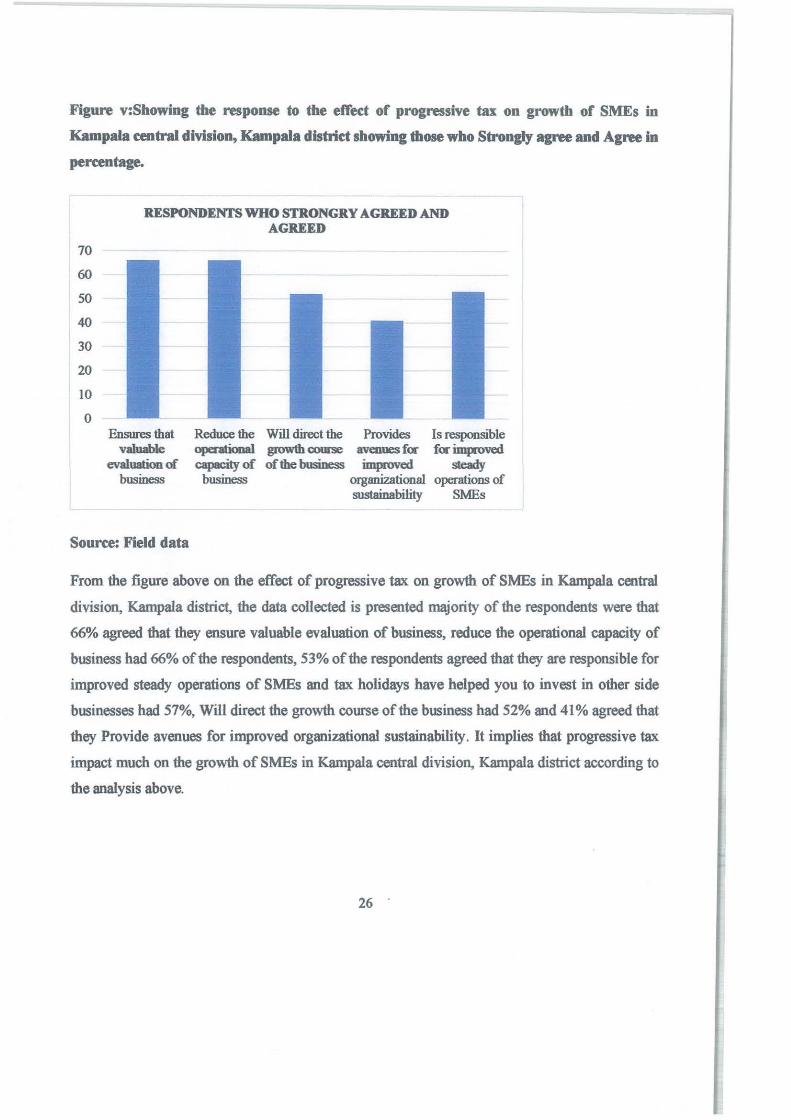

Figure v:Showing the response to the effect of progressive tax on growth of SMEs in

Kampala central division, Kampala district showing those who Strongly agree and Aaree in

percentage.

70

60

50

40

30

20

10

0

RESPONDENfS WHO STRONGRY AGRE:ED AND AGRE:ED

Ensures that valuable

evaluation of business

Reduce the opeaatiooal cai-:it:Yof

business

Will direct the Provides Is responsible growth course avenues f<r f<r improved of the business improved steady

organizational operations of sustainability SMEs

Source: Field data

From the figure above on the effect of progressive tax on growth of SMEs in Kampala central

division, Kampala district, the data collected is presented majority of the respondents were that

66% agreed that they ensure valuable evaluation of business, reduce the operational capacity of

business had 66% of the respondents, 53% of the respondents agreed that they are responsible for

improved steady operations of SMEs and tax holidays have helped you to invest in other side

businesses had 57%, Will direct the growth course of the business had 52% and 41% agreed that

they Provide avenues for improved organizational sustainability. It implies that progressive tax

impact much on the growth of SMEs in Kampala central division, Kampala district according to

the analysis above.

26 .

4.3 Effect of corporation tax on growth of SMEs in Kampala central division, Kampala

district.

The second objective of the study was to examine the effect of corporation tax on growth of SMEs

in Kampala central division, Kampala district. The responses to this objective were gathered on a

likert scale measure of I; 5 measuring responses.

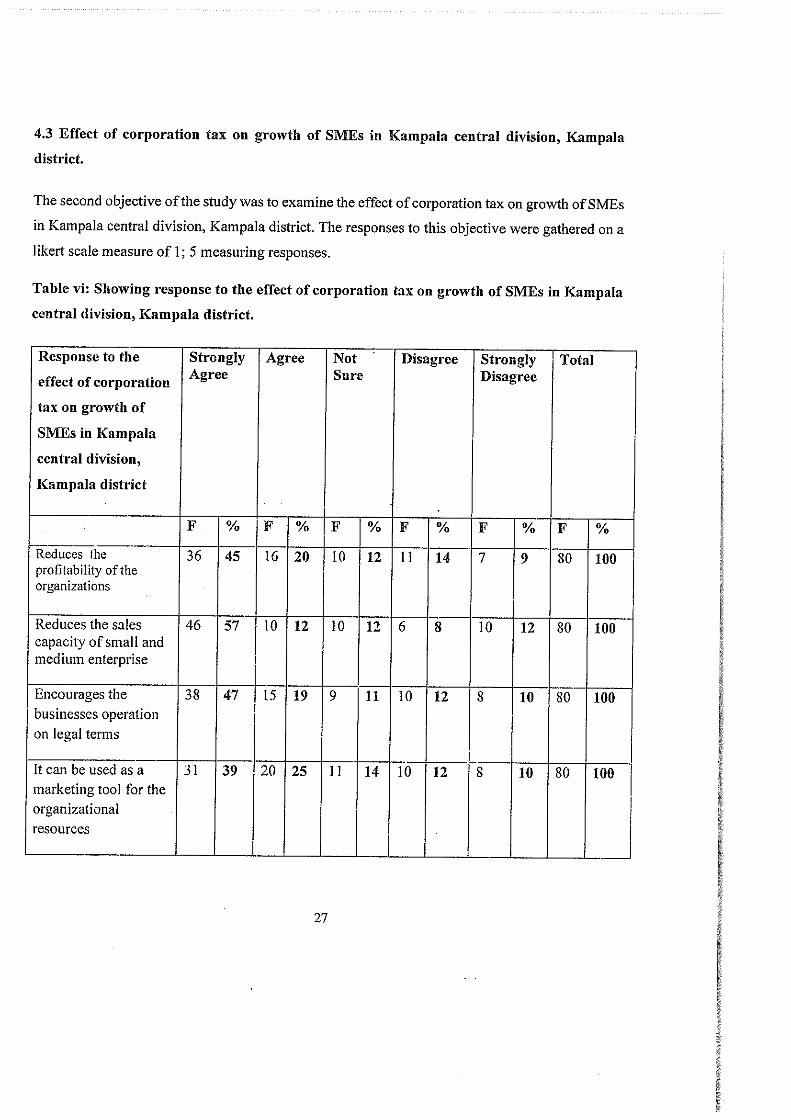

Table vi: Showing response to the effect of corporation tax on growth of SMEs in Kampala

central division, Kampala district.

Response to the Strongly Agree Not Disagree Strongly Total

effect of corporation Agree Sure Disagree

tax on growth of

SMEs in Kampala

central division,

Kampala district

F % F % F % F % F % F %

Reduces the 36 45 16 20 10 12 11 14 7 9 80 100 profitability of the organizations

Reduces the sales 46 57 10 12 10 12 6 8 10 12 80 100 capacity of small and medium enterprise

Encourages the 38 47 15 19 9 11 10 12 8 10 80 100 businesses operation

on legal terms

I

It can be used as a JI 39 20 25 11 14 10 12 8 10 80 100 marketing tool for the organizational

resources

27

Enables the legal 35 44 21 26 6 8 9 11 7 9 80 100 operation of businesses

Source: Field data

The data collected above shows that in line with the response to effect ofcorporation tax on growth

of SMEs in Kampala central division, Kampala district, corporation tax reduces the profitability

of the organizations had 45% of the respondents who strongly agreed, 20% agreed, 12% disagreed,

14% respondents were not sure and 9% strongly disagreed.

Reduces the sales capacity of small and medium enterprise had 57% of the respondents who

strongly agreed, 12% agreed, 12% disagreed, 8% of the respondents strongly disagreed and 12%

were not sure.

Encourages the businesses operation on legal terms had 47% of the respondents who strongly

agreed, 19% agreed, 11 % disagreed, 12% of the respondents were not sure and 10% strongly

disagreed.

3 9% of the respondents strongly agreed with it can be used as a marketing tool for the

organizational resources, 25% agreed, 14% disagreed and 12% of the respondents strongly

disagreed and 10% of the respondents were not sure.

Enables the legal operation of businesses had 44% of the respondents who strongly agreed, 26%

agreed, 8% were not sure, 11 % disagreed and 9% of the respondents strongly disagreed.

28

Figure vi: Showing the response to the effect of corporation tax on growth of SMEs in

Kampala central division, Kampala district showing those who StronalY aaree and Agree in

percentage

80

70

60

50

40

30

20

10

0

RESPONDENTS WHO STRONGLY AGREED AND AGREED

Reduces the Reduces the sales Encourages the profitability of capacity of small businesses

the organizations and medium operation on enterprise legal tenns

It can be used as Enables the legal a marketing tool operation of

for the businesses organizational

resouroes

Source: Field data

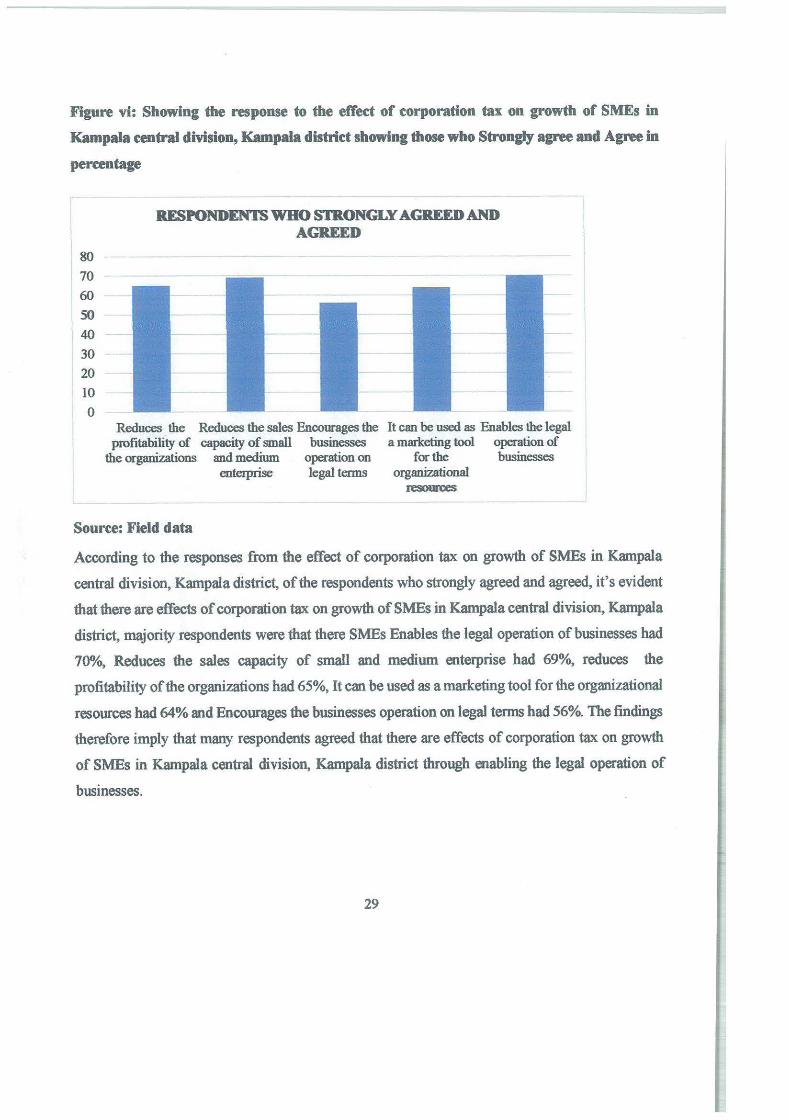

According to the responses from the effect of corporation tax on growth of SMEs in Kampala

central division, Kampala district, of the respondents who strongly agreed and agreed, it's evident

that there are effects of corporation tax on growth of SMEs in Kampala central division, Kampala

district, majority respondents were that there SMEs Enables the legal operation of businesses had

70%, Reduces the sales capacity of small and medium enterprise had 69%, reduces the

profitability of the organizations had 65%, It can be used as a marketing tool for the organizational

resources had 64% and Encourages the businesses operation on legal terms had 56%. The findings

therefore imply that many respondents agreed that there are effects of corporation tax on growth

of SMEs in Kampala central division, Kampala district through enabling the legal operation of

businesses.

29

4.4 The effect of regressive tax on growth of SMEs in Kampala central division, Kampala

district.

The third objective of the study was to examine the effect of regressive tax on growth of SMEs in

Kampala central division, Kampala district. The responses to this objective were gathered on a

likert scale measure of I; 5 measuring responses.

Table vii: Showing responses to the effect of regressive tax on growth of SMEs in Kampala

central division, Kampala district.

The effect of Strongly Agree Not Disagree Strongly Total

regressive tax on Agree Sure Disagree

growth of SMEs in

Kampala central

division, Kampala

district.

F % F % F % F % F % F %

Reduces the 43 54 10 12 11 14 9 11 7 9 80 100 business resources

Can contribute to 37 46 13 16 8 10 14 17 8 10 80 100 collapse of businesses

Reduces business 26 32 16 20 11 14 13 16 14 18 80 100 values affiliated to

pricing and

marketing

Reduces the 22 28 14 17 13 16 14 17 17 21 80 100 business

operational

capacities

30

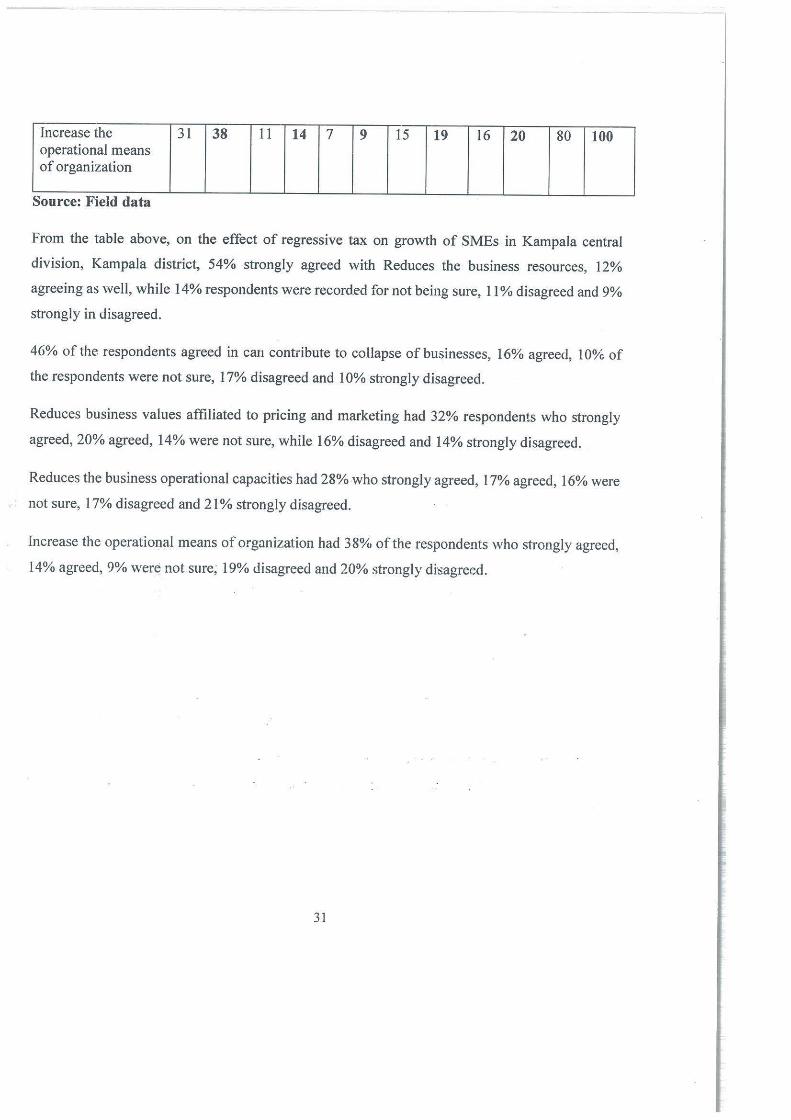

Increase the 31 38 11 14 7 9 15 19 16 20 80 100 operational means of organization

Source: Field data

From the table above, on the effect of regressive tax on growth of SMEs in Kampala central

division, Kampala district, 54% strongly agreed with Reduces the business resources, 12%

agreeing as we.II, while 14 % respondents were recorded for not being sure, 11 % disagreed and 9%

strongly in Jisagreed.

4G% of the respondents agreed in can contribute to collapse of businesses, 16% agreed, 10% of

the respondents were not sure, 17% disagreed and 10% strongly disagreed.

Reduces business values affiliated to pricing and marketing had 32% respondents who strongly

agreed, 20% agreed, 14% were not sure, while 16% disagreed and 14% strongly disagreed.

Reduces the business operational capacities had 28%-who strongly agreed, 17% agreed, 16% were

not sure, 17% disagreed and 21 % strongly disagreed.

Increase the operational means of organization had 38% of the respondents who strongly agreed,

14% agreed, 9% were not sure; 19% disagreed and 20% strongly dh,agreed.

31

Figure vii: Showing responses to the effect of regressive tax on growth of SMEs in Kampala

central division, Kampala district. (Those who strongly agreed and aareed)

70

60

50

40

30

20

10

0

RESPONDENTS WHO STRONGLY AGREED AND AGREED

Reduces the business resources

Can contribute Reduces to collapse of business values

businesses affiliated to pricing and marlceting

Reduces the business

operational capacities

Increase the operational means of

organization

Source: Field data

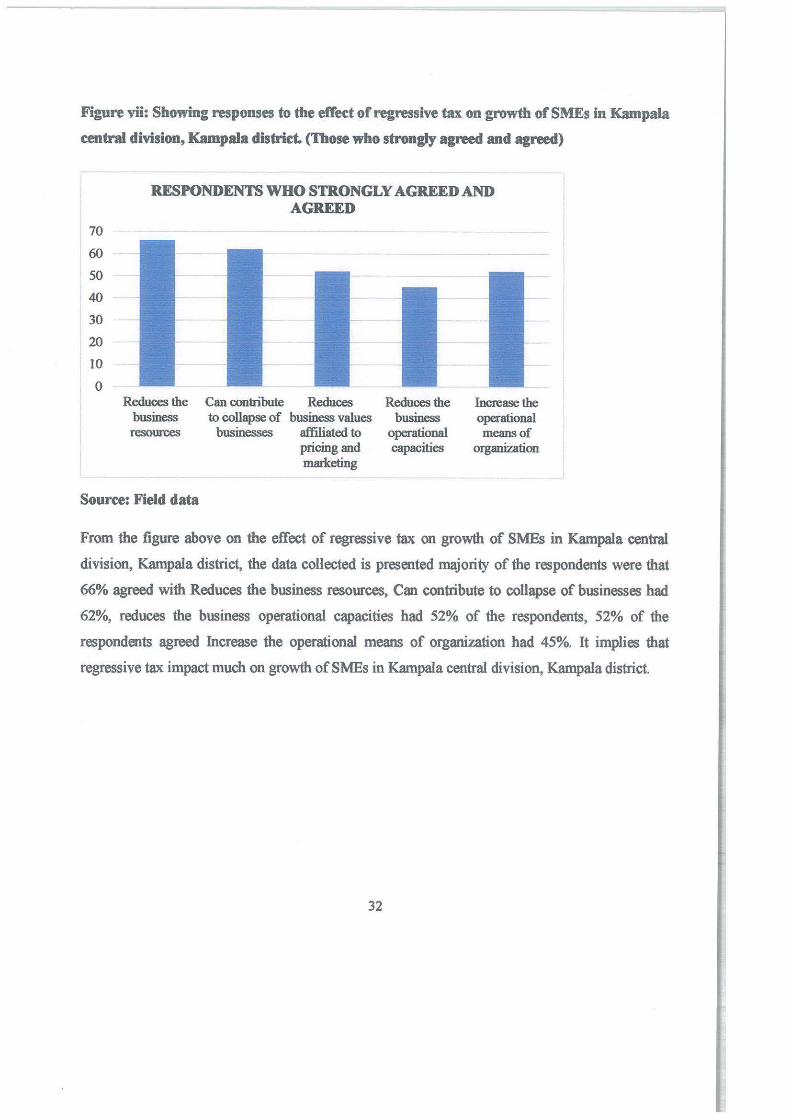

From the figure above on the effect of regressive tax on growth of SMEs in Kampala central

division, Kampala district, the data collected is presented majority of the respondents were that

66% agreed with Reduces the business resources, Can contribute to collapse of businesses had

62%, reduces the business operational capacities had 52% of the respondents, 52% of the

respondents agreed Increase the operational means of organi7.ation had 45%. It implies that

regressive tax impact much on growth of SMEs in Kampala central division, Kampala district.

32

CHARPTER FIVE

SUMMARY, CONCLUSIONS, RECOMMENDATIONS AND AREAS OF FURTHER

RESEARCH

5.0 Introduction

This chapter is concerned with summary, conclusion, recommendations and suggestions about the

findings that were gathered from the case study and the areas of further research. The study was

carried out with the view to investigate tax system and growth of small and medium enterprises

(SMEs) in Kampala Central Division, Uganda. This chapter is concerned with summary,

conclusion, recommendations and suggestions about the findings that were gathered from the case

study and the areas of further research.

5.1 Summary of the findings

On the effect of progressive tax on growth ofSMEs in Kampala central division, Kampala district,

the data collected is presented majority of the respondents were that 66% agreed that they ensure

valuable evaluation of business, reduce the operational capacity of business had 66% of the

respondents, 53 % . of the respondents agreed that they arc responsible for improved steady

operations of SMEs ::aid tax holidays have helped you to invest in other side businesses had 57%,

Will direct the growth course of the business had 52% and 41 % agreed that they Provide avenues

for improved organizational sustainability.

On the effect of corporation tax on growth of SMEs in Kampala central division, Kampala district,

of the respondents who strongly agreed and agreed, it's evident that there are effects of corporation

tax on growth of SMEs in Kampala central division, Kampala district, majority respondents were

that there SMEs Enables the legal operation of businesses had 70%, Reduces the sales capacity of

small and medium enterprise had 69%, reduces the profitability of the organizations had 65%, It

can be used as a marketing tool for the organizational resources had 64% and Encourages the

businesses operation on legal terms had 56%.

33

On the effect of regressive tax on growth of SMEs in Kampala central division, Kampala district,

the data collected is presented majority of the respondents were that 66% agreed with Reduces the

business resources, Can contribute to collapse of businesses had 62%, reduces the business

operational capacities had 52% of the respondents, 52% of the respondents agreed Increase the

operational means of organization had 45%.

5.2 Conclusions

The purpose of the study was to investigate tax system and growth of small and medium enterprises

(SMEs) in Kampala Central Division, Uganda and it was carried out on the three research

objectives which included to: examine the effect of progressive tax on growth ofSMEs in Kampala

central division, examine the effect of corporation tax on growth of SMEs in Kampala central

division and to examine the effect of regressive tax on growth of SMEs in Kampala central

division, Kampala district.

The findings reveal that that progressive tax impact much on the growth of SMEs in Kampala

central division, Kampala district according to 66% respondents who agreed that they ensure

valuable evaluation of business, reduce the operational capacity of business had 66% of the

respondents, 53% of the respondents agreed that they are responsible for improved steady

operations of SMEs and tax holidays have helped you to invest in other side businesses had 57%,

Will direct the growth course of the bt:siness had 52% and 41% agreed that they Provide avenues

for improved organizational sustainability. It can be concluded that progressive tax has effects on

the growth ofSMEs in Kampala central division, Kampala district, Uganda.

The findings reveal that corporation tax has effects on growth of SMEs in Kampala central

division, Kampala district according to the respondents who strongly agreed and agreed that there

are effects of corporation tax on growth of SMEs in Kampala central division, Kampala district,

majority respondents were that there SMEs Enables the legal operation of businesses had 70%,

Reduces the sales capacity of ,mall 1.nd medium enterprise had 69%, reduces the profitability of

the organizations had 65%, rt can be used as a marketing tool for the organizational resources had

64% and Encourages the businesses operation on legal terms had 56%. It can be concluded that

34

there are effects of corporation tax on growth of SMEs in Kampala central division, Kampala

district through enabling the legal operation of businesses.

The findings reveal that regressive tax has effects the on growth of SMEs in Kampala central

division, Kampala district according to 66% respondents who agreed with Reduces the business

resources, Can contribute to collapse of businesses had 62%, reduces the business operational

capacities had 52% of the respondents, 52% of the respondents agreed Increase the operational

means of organization had 45%. It can be concluded that regressive tax impact much on growth of

Small business enterprises in Kampala central division, Kampala district.

5.3 Recommendations

Tax collection should be defined with respect to which government should collect certain taxes

from small and medium enterprises. This will avoid the government collecting taxes from the same

particular organization.

Government should also put a policy in place to avoid illegal taxes, such as community levy, boys

or youth levy and as well as association or union levy.

Taxes should be collected in relation to the sizes and profit of Small scale businesses considering

all other factors that can constrain the progress of such Small scale businesses as there is a

relatiorn:,hip between small scale businesses sizes and their ability to pay taxes.

5.4 Areas for further research

The results presented in this report may not be conclusive and should be treated as being

preliminary. Further analysis of the survey data on tax system on the performance of small and

medium enterprises needs to be done to validate these findings and provide greater confidence in

explaining the interaction of the variables. Therefore based on these there is need for further study

to be conducted on the following.

• The impact of multiple taxatio:1 on small and medium scale businesses

" An assessment on the impact of taxation on small and medium enterprises in a developing

economy

• Taxation of small and medium sized enterprises 35

REFERENCES

Adam, C. S. and O'Connell, S.A. (1999): "Aid, Taxation and Development in Sub-Saharan

Addison, T. and S. M. Murshed (2002), "Credibility and reputation in Peace Making", Journal

Africa", Economics and Politics, Volume 11(3), 225-54

Ali A.G. Au (2001), "Can Africa cut its poverty level by half by 2015?" United Nations

Allingham, M. 0., & Sandmo, A. (1972), Income tax evasion: a theoretical analysis. Journal of

Public Economics.

Aim, J., Cherry, T., Jones, M., & McKee, M. (2010). Taxpayer information assistance services

and tax compliance behavior.

Alm. J., Jackson. B., & McKee, M. (1992). Institutional uncertainty and taxpayer compliance.

American Economic Review, 82(4), 1018-1026.

Alm, J.. Sanchez, I., & Dejuan, A. (1995). Economic and noneconomic factors in tax compliance.

Kylc/os, 48(1), 3-18.

Braithwaite. V. (2009). Defiance in taxation and govirnance: resisting and dismissing authority

in a democracy. Cheltenham, Glos: Edward Elgar Publishing Ltd.

Carroll. J. (1992). Flow taxpayers think about their taxes: Frames and values. In J. Slemrod (Ed),

Why people pay taxes. Michigan: University of Michigan.

Holmes, R. Y. (2011). Forcing cooperation: A strategy for improving tax compliance. University

of Cincinnati Law Review, 79(4), 1415-1459.

IMF (1999). "Burundi: Statistical Annex", IMF Staff Country Report No. 99/8 (February).

International Monetary Fund, Washington, D. C.

Lawsky, S. B. (2009). Probably? Understanding tax law's unce11ainty. University of Pennsylvania

Law Review, 157(4), 1017-1074.

36

Minarik, Joseph J. (2008). "Taxation'. in David R. Henderson (ed). Concise Encyclopedia of

Economics (2nd ed). Library of Economics and Liberty.

Moser, D. V., Evans, J. H., & Kim, C. K. (1995). The effects of horizontal and exchange inequity

on tax reporting decisions. Accounting Review, 70(4), 619-634.

Rothengatter. M. R. (2008). 'Taxing taxis' - limits and possibilities for regulating tax compliance

behaviours of taxi-drivers an Australian case study. Doctor of Philosophy, University of

Queensland, Brisbane.

Wahl, I., Kastlunger, B., & Kirchier, E. (2010). Trust in Authorities and Power to Enforce Tax

Compliance: An Empirical Analysis of the "Slippery Slope Framework'. Law & Policy, 32( 4), 3

83-406

Wenzel. M. (2005). The multiplicity of taxpayer identities and their implications for tax ethics

Centre for Tax System Integrity, Australian National University. Canberra

37

APPENDICES

APPENDIX I: RESEARCH INSTRUMENT: QUESTIONNAIRES