Embed Size (px)

Citation preview

Editorial Committee

Kamara, Abdul B. (Chair)Anyanwu, John C.Osei, BarfourRajhi, TaoufikVencatachellum, Desire J. M.

Managing Editors

Mafusire, AlbertMoummi, Ahmed

Copyright © 2009Africain Development BankAngle des trois rues: Avenue du Ghana,Rue Pierre de Coubertin, Rue Hédi NouiraBP 323 - 1002 TUNIS belvédère (Tunisia)Tél: +216 71 333 511 / 71 103 450Fax: +216 71 351 933E-mail: [email protected]

Rights and Permissions

All rights reserved.

The text and data in this publication may bereproduced as long as the source is cited.Reproductions for commercial purposes areforbidden.

The Working Paper Series (WPS) are produc-ced by the Development ResearchDepartment of the African Development Bank.The WPS disseminates the findings of work inprogress, preliminary research results, anddevelopment experience and lessons, toencourage the exchange of ideas and innova-tive thinking among researchers, developmentpractitioners, policymakers, and donors. Thefindings, interpretations, and conclusionsexpressed in the Bank’s WPS are entirelythose of the author(s) and do not necessarilyrepresent the view of the African DevelopmentBank, its Board of Directors, or the countriesthey represent.

Working Papers are available online athttp:/www.afdb.org/

ISBN - 978 - 9973 - 071 - 17 - 0

Correct citation : Kasekende Louis, Ndikumana Léonce, Rajhi Taoufik (2009), Impact of the Global Financial andEconomic Crisis on Africa, Working Papers Series N° 96, African Development Bank, Tunis, Tunisia. 36 pp.

AFRICAN DEVELOPMENT BANK GROUP

Impact of the Global Financialand Economic Crisis on Africa

Working Paper No. 96March 2009

ECONOFFICE OF THE CHIEF ECONOMIST

4

EXECUTIVE SUMMARY

The current financial and economic crisishas affected the drivers of Africa’s recentgrowth performance. Demand for andprices of African commodities are falling,capital flows are declining, and promisedincreased aid has not materialized.China’s growth has slowed. The onlygood news is the easing of inflationarypressures. In Asia and Latin-America,growth forecasts have already been dras-tically revised downwards. Although theimmediate impact of the crisis werecontained, the medium-term effects arelikely to be greater.

Africa’s low level of financial integrationmeant that African economies were relati-vely isolated from the direct impact of thefinancial crisis. Thus, Africa found itselfshielded from the impact of the 2007 sub-prime and the summer 2008 bankingcrises, thereby avoiding the negativeeffects of a financial crisis that affectedthe very foundations of international finan-cial markets.

African financial systems are dominatedby the banking sector, and financial mar-kets are still underdeveloped and evennon-existent in many countries. Foreign

borrowing by banks is regulated in thecontext of exchange control and banksface little risk associated with off-balancesheet operations. This largely explains thelimited impact on the banking sector inAfrica.

Most African financial markets were affec-ted by contagion effects, resulting in largelosses in value and capital outflows. ForAfrica’s relatively liquid financial markets(e.g. Egypt and Nigeria) the contagiouseffect were amplified by pre-crisis stockover-valuation and limited diversificationof stocks.

The financial crisis amplified the increasein the margin applied to loans in the inter-national financial markets, especially foremerging and African countries. FromOctober 2008, sovereign debt spreadshave increased. For that similar reason,several African countries (Tunisia, Kenya,Uganda and Tanzania) decided to postpo-ne resorting to international financial mar-kets to mobilize the resources necessaryfor financing their growth, turning insteadto local markets.

With the deepening crisis in developedcountries and in China, the downwardtrend of primary commodity prices has

Kasekende Louis, Ndikumana Léonce, Rajhi Taoufik*

increased and threatens to undermine thegains recorded in recent years. Thisdecrease will have several consequencesincluding declining reserves, non-profitabi-lity of some oil fields and mineral depo-sits, reduction in government fundingcapacity and cancellation or postpone-ment of a number of investments in extra-ctive industries that are highly dependenton foreign direct investment.

Africa will not be spared from the pessi-mistic world trade outlook for 2009. Thisoutlook is reflecting the bad growth out-look of industrialized and emerging coun-tries, resulting in weak global demand.Export growth rate is expected to drop by7% and import growth rate will decline by4.7%, resulting in a deterioration of com-mercial balance.

In the short run, the financial and econo-mic crisis is expected to have an impor-tant negative impact on Foreign DirectInvestment (FDI), contributing to a conti-nuing fall in FDI in 2009.

Preliminary estimates of private flows toAfrica are relatively better than for otherregions for several reasons. Among theseare Africa’s low share of total capitalflows, the limited number of countriesleveraging funds on international marketsand the limited correlation betweenAfrican and industrialized countries’ finan-

cial markets. However, no bonds issue inforeign currency has been registered in2008 for African countries. This situationraises concern in particular as severalcountries rely on foreign private capital tocover their current account deficits.

Recent data on migrant remittances showsigns of stagnation or slight decline world-wide. However, in the absence of data, itis too early to draw a definitive conclusionfor Africa

Overall, Africa will move from a budgetarysurplus accounting for 2.3% of GDP in2008 to a budgetary deficit of 5.5% in2009. Oil exporters will register a deficit of7.7% of GDP 2008, down from a surplusof more than 5% in 2008. The deficit willdeepen for oil importers as well (from -1.6% to -2.8%).

From an overall current account surplusposition of 3.5% of GDP in 2008, thecontinent will face a deficit of 3.8% ofGDP in 2009. The large surplus of 9.8%of GDP for the group of oil exporters willturn into a deficit of 4% of GDP. This is adirect result of the expected decline in oilrevenue.

For the continent as a whole, inflation washigher in 2008 (10.9%) than in 2007(7.4%). The 10.4% inflation was 3 percen-tage points above projections made prior

to the financial crisis. In contrast, lowerinflation is expected in 2009 (8.7%).However, falling oil prices notwithstan-ding, inflationary pressures will persist inseveral countries, mainly due to the highcost of foodstuff and supply bottlenecks.

Africa is expected to grow at a low rate of2.9% in 2009, down from 5.75 in 2008and 6 % in 2007. Preliminary projectionsshow expected a loss of 4.2% of growthrate for oil-exporters in 2009 and 1.2%decline in growth for oil-importing coun-

tries. For the first time since the 2000s,oil-importing countries will register highergrowth rates (3.4%) than oil-exportingcountries (2.4%).

The sectors most affected by the crisiswill be mining, tourism, textile, and manu-facturing. Enterprise failures, cancella-tions and postponements of projects arebecoming widespread in African countries.Substantial job losses are registered, withnegative effects on household’s standardsof living.

Author’s Affiliation :* Louis Kasekende, Léonce Ndikumana, Taoufik Rajhi - African Development Bank.

8

1. INTRODUCTION

2. Impact on the banking system

3. The Impacts of the financial crisis on markets

3.1 The collapse of financial markets

3.2 The rise of sovereign debt spreads

3.3 Volatility of exchange markets

3.4 The fall of commodities prices

4. The long and medium term transmission channels

4.1 Trade flows

4.2 Capital flows

5. The economic outlook after the financial crisis

5.1 The fall in reserves and government budget

5.2 Inflation

5.3 Growth Prospects

5.4 Sectoral impact

6. CONCLUSION

1

1

4

5

5

5

7

10

10

10

12

12

13

14

14

16

TABLE OF CONTENTS

10

1. INTRODUCTIONPrior to July 2008 and despite the sub-prime crisis, Africa recorded excellent eco-nomic growth. The drivers of strong econo-mic growth included macroeconomicreforms, a world economic situation thatwas characterized by high demand forcommodities, rising capital inflows andChina’s strong growth. Analysts were opti-mistic about the capacity of the continentand the world economy to generate thenecessary resources for development andpoverty reduction.

Despite early signs of a pending downturnsince 2007, few could have anticipated acrisis of the magnitude observed since thesecond half of 2008. Today, the world eco-nomy is officially in stagnation, industriali-zed countries are in recession and Africafaces serious uncertainties over its growthand development prospects. The currentfinancial and economic crisis has affectedAfrica’s growth drivers. Demand for andprices of commodities are falling, capitalinflows are declining and promises ofincreased aid have not materialized yet.China’s growth has slowed. The only goodnews is the easing in inflationary pressures.Although the immediate impact of the crisiswere contained, the medium-term effectsare likely to be greater.

This paper presents a preliminary assess-ment of the impact of the financial crisis onAfrican economies thus far. The paper firstexplains the impact on the banking sectorand why Africa has not been directly affec-

ted by the banking crisis (Section 2). Itgoes on to discuss the direct impact of thecrisis on financial markets, foreign exchan-ge markets and commodity markets(Section 3). Section 4 shows that the nega-tive effects will mainly be felt through tradeand capital flows, including foreign directinvestment and migrant remittances.Section 5 discusses the prospects forpublic finance, inflation and growth. A sec-toral analysis is also carried out, highligh-ting the impact on tourism and mining.Section 6 concludes by a discussion onsome policies that could mitigate the impactof the crisis.

2. Impact on the bankingsystem

Africa’s low level of financial integrationmeant that African economies were relati-vely isolated from the direct impact of thefinancial crisis. Thus, Africa found itselfshielded from the impact of the 2007 sub-prime and the summer 2008 bankingcrises, thereby avoiding the effects of afinancial crisis that affected the very foun-dations of international financial markets.Compared to emerging countries, Africa’sexternal financing (bond issue, stocks andprivate borrowing) is low, representing only4% in 2007 of overall issue for emergingeconomies. In 2007, bond issues stood atonly USD 6 billion, compared to USD 33billion for Asia and USD 19 billion for LatinAmerica. Furthermore, in terms of accessto private resources, Africa received onlyUSD 3 billion in 2007, compared to USD 42billion for Asia.

1

Africa’s stock market capitalization is stillvery low, representing only 2.09% of worldcapitalization. Furthermore, African bankingassets represent only 0.87% of global ban-king assets, compared to 58.15% for the

15 countries of the Euro zone and 15.09%for the United States. Africa’s financial glo-balization ratio is comparable to LatinAmerica’s, at 181.3% and 176.4%, respec-tively, far behind that of Asia at 369.8%

2

Figure 1 : Financial Globalization Indicators

Source: IMF, Global Financial Stability Report, October 2008

Emerging Market external financing : TotalBonds, Equities and Loans (in % of total)

Emerging Market external financing :Equity Issurance (in % of Total)

2002

2003

2004

2005

2006

2007

2002

2003

2004

2005

2006

2007

Asia

Asia

Emerging Market external financing : BondIssurance (in billions of US Dollars)

Africa external financing : Loan syndication(in billions of US Dollars)

2002

2003

2004

2005

2006

2007 Asia

2002

2003

2004

2005

2006

2007 Asia

The low financial integration indicatorspartly explain why Africa escaped both thesub-prime and banking crises. No Africancountry announced a bank rescue plan atthe scale observed in many developedcountries. Few banks and investmentfirms in Africa have held derivatives bac-ked by sub-prime mortgages (or “toxicassets”). No difficulties have been repor-ted on African sovereign wealth funds andthe eventual impact on their returns.Generally, African banks have not enga-ged in complex derivative products andare not heavily dependent on externalfinancing.

The contagion effects may be amplifiedby foreign bank presence, which is highin some countries. The share of foreignbank assets reaches 100% in somecountries such as Mozambique,

Swaziland and Madagascar. The head-quarters of these foreign banks are loca-ted mainly in France, Portugal and theUnited Kingdom, where banking institu-tions suffered tremendous losses instock capitalization and profit during thefinancial crisis.

The financial meltdown suffered by theparent banks following market capitaliza-tion losses was not passed down to theirAfrican subsidiaries. In fact, some subsi-diaries of foreign banks saw a conside-rable increase in their market capitaliza-tion. For example, Swaziland Nedbank,Bank of Africa Benin and Standard Bankof Ghana saw their market capitalizationincrease between July 2007 and January2009. Therefore, the contagion effect offinancial meltdown is weak compared tothe effect on parent banks.

3

Table 1: Share of Banking assets held by foreign banks (%)

Source: Global Development Finance, World Bank 2008 and JPMorgan

Countries Share of Banking assets held byforeign banks (%)

Largest Foreign Banks Homecountry

Angola

Botswana

Mozambique

Swaziland

Uganda

Zambia

Ghana

Cote d’Ivoire

Madagascar

Cameroun

PortugalUKPortugalSASASAUKUKUKUKFranceFranceBeninFrance

53

77

100

100

80

77

65

66

100

63

Banco BPIBarclays BankBanco Commercial PortuguesStandard BankNetBankStandard BankBarclays BankStandard Chartered BankStandard Chartered BankBarclays BankSociété GéneraleCalyonBank of AfricaBFBP

African financial systems are dominatedby the banking sector, and the role playedby financial markets is weak, or in somecases non-existent. Borrowing from forei-gn banks is regulated in the context ofexchange control regulations. Off-balancesheet exposure is not widespread inAfrica, which is in contrast to industriali-zed countries that have complex financialsecurization instruments such as the onesthat triggered the sub-prime crisis.

The accumulation of reserves followingthe commodities boom has supportedthe expansion of sovereign wealth fundsin Nigeria and Botswana and the crea-tion of new ones in Libya, Algeria, Sao-Tome and Principe and Sudan. Whilethese funds represent only 2% of thesovereign funds’ global assets, the accu-mulated volume amounted to more thanUSD 124 billion, before the 2008 finan-cial crisis.

4

Table 2 : Sovereign wealth funds by country (billions of US dollars) mid-2008

Source: Sovereign Wealth Fund Institute, 2008FN: — not applicable

Country Nonpension % Africa

LibyaAlgeriaNigeriaBotswanaGabonSudanSão Tomé and PrincipeAfricaWorldAfrica, % of World

40 %38 %14 %6 %

100 %

50471770.400.100.02124.422975.004.1

The sterilization of such reserves andtheir conversion into foreign assets hel-ped countries avoid strong exchange rateappreciation. So far, there is little informa-tion on the negative effect of the financialcrisis on African sovereign wealth funds.Nevertheless, sovereign funds profitabilityis expected to drop, in line with otherfinancial wealth instruments on the globalmarket. It is certain that the fall in oilprices will contribute to a dramatic reduc-

tion in the investment capacity and thesize of such funds.

3. Impact of the financial crisison markets

There are three distinguishable immediateeffects of the crisis, namely the contagioneffects on financial markets, foreignexchange markets and commodity mar-kets. These are discussed in the followingsections.

3.1 Effects on financial markets

Although African banking systems were notdirectly exposed to the sub-prime crisis,there were strong indications of increasedasset price and risk premium volatility onAfrican financial markets as early as thesummer of 2008. The contagion and inter-dependence significantly affected theregion’s financial markets. For someAfrican markets (e.g. Egypt and Nigeria),the impact was much higher than for mar-kets in developed countries (Table 1).

Africa’s relatively liquid financial marketsnot only suffered from the contagiouseffect but also faced amplification thereof,possibly attributable to the over-valuationof stocks and the outflow of portfolioinvestments. African investors, in general,and Egyptian and Nigerian investors inparticular, recorded within six months anaverage loss of more than half the wealthinvested at the end of July 2008. This ishigher than the losses recorded onAmerican, French and Japanese markets.

3.2 The rise of sovereign debtspreads

The costs of external debt for emergingcountries on international financial mar-kets started to increase in July 2007. Thespreads remained moderate until thebeginning of the financial crisis. Tunisiafelt the brunt of the crisis in its attempt toissue bonds on the international financialmarkets in July and August 2007. The firstattempt to raise funds on the Japanese

financial market was hampered by restric-tive financial requirements. Indeed, facedwith debt spreads estimated at between45 and 50 basis points, Tunisia had toincrease its offer by 25 basis points toattract entice investors.

The financial crisis amplified the increasein the margin applied to loans in the inter-national financial markets, especially foremerging and African countries. FromOctober 2008, sovereign debt spreadsrose by an average of 250 basis points foremerging countries. The spread of theJPMorgan emerging countries equity indexreached its highest level since 2002,increasing by 800 basis points in October2008. Spreads increased by 100 basispoints for Egypt and rapidly increased toabove 200 basis points for Tunisia duringthe toughest periods of bank failures in theUnited States. The increase in the risk pre-mium forced Kenya, Uganda and Tanzaniato postpone tapping of international finan-cial markets to mobilize long-termresources, turning instead to local markets.

3.3 Volatility of foreign exchangemarkets

In most countries, the impact of the finan-cial crisis manifested itself through curren-cy fluctuations, especially against the USdollar or the Euro. The depreciation ofsome currencies is attributable to theimpact of the financial crisis on commodi-ty prices and the decline in foreignexchange reserves. Thus, the 65.8% dropin copper prices, from the highest recor-

5

ded price of July 2008 at USD 8985/metricton to USD 2 902/metric ton at end

December 2008, led to a considerable fallin Zambia’ foreign reserves.

6

*Benchmark as at 31/07/2008 except for Zimbabwe at 31/08/2008Sources: AfDB Statistics Department and Oanda, Online Database January 2009

Rateof depreciation

Value at end ofWeek

(13/02/2009)

Benchmark07/31/2008

Currency nameRegion/Country

AlgeriaAngolaBeninBotswanaBurundiCape VerdeComoresCongo. Dem. Rep. ofDjiboutiEgyptEthiopiaGambia, TheGhanaGuineaKenyaLesothoLiberiaLibyaMadagascarMalawiMauritaniaMauritiusMoroccoMozambiqueNamibiaNigeriaRwandaSão Tomé & PrincipeSeychellesSierra LeoneSomaliaSouth AfricaSudanSwazilandTanzaniaTunisdiaUgandaZambiaZimbabwe

EuiropeJapan

Algerian DinarNew KwanzaCFA FrancPulaBurundi FrancEscudoComoros FrancCongolese FrancDjibouti FrancEgyptian PoundBirrGambian DalasiNew CediGuinea FrancKenyan ShillingLotiLiberian DollarLibyan DinarAriaryKwanchaOuguiyaMauritius RupeeDirhamNew MeticalNamibian DollarNairaRwandan FrancDobraSeychelles RupeeLeoneSomali ShillingRandSudanese PoundLilangeniTanzanian ShillingTunisian DinarUganda ShillingZambian KwachaZimbabwe Dollar

EuroYen

63.075.2429.26.5

1,191.571.8316.9437.0178.75.410.021.51.2

4,653.668.77.564.01.2

1,612.9144.0234.527.67.424.17.6

118.9556.5

14,773.48.0

2,997.71,450.9

7.42.17.4

1,187.61.2

1,671.03,588.9

353,950.0OTHERS

0.6108.1

73.775.2520.18.1

1,233.587.1381.9712.8179.65.611.226.61.4

4,868.683.010.165.01.3

2,018.6143.8263.534.28.625.610.2149.1578.4

14,661.916.9

3,093.91,448.510.02.39.9

1,341.61.4

1,978.55,398.6

37,456,777.0

0.890.2

-14.50.0

-17.5-19.8-3.4-17.6-17.0-38.7-0.5-4.3-10.8-19.3-15.1-4.4-17.2-25.6-1.5-8.5-20.10.2

-11.0-19.3-14.5-5.9-25.6-20.3-3.80.8

-52.4-3.10.2

-26.1-6.8-25.1-11.5-16.3-15.5-33.5-99.1

-17.519.7

Table 3: African exchange rates against the US dollar

The Zambian Kwacha exchange rate tothe US dollar depreciated sharply in 2008by as much as 50%, although the exchan-ge rate slightly improved at the end of theyear.

3.4 The fall of commodity prices

Commodity exports have been one of themain drivers of growth in many Africancountries. Strong growth in industrializedand emerging countries such as India and

China has been an important factor of theincrease in the prices and demand forcommodities. Unfortunately, the financialcrisis has had a negative impact on worldgrowth prospects and seriously dampe-ned expectations on commodity futuresmarkets (Table 4), thus inducing fallingprices and demand for most commodities.For instance, the price of crude oil drop-ped by 65 percent, from USD 125.73 perbarrel at the start of the financial crisis toUSD 43.48 in January 2009.

7

Source: World Bank, Global Economic Prospects 2009: Commodity markets

20102008 200920062000-2005% Change

EnergyOilNatural GazCoalNon energyAgricultureFoodsGrainsRaw materialsMetals and mineralsCooper

13.513.610.412.78.3664.8512.315.2

17.320.433.93.129.112.71018.422.756.982.7

2007

10.810.6133.9172025.626.19125.9

45.142.357.297.822.428.435.250.91350.6

-25-26.4-10.8-23.1-23.2-20.9-23.4-27.714.925.5-32.2

0.91.8-4.2-10-4.3-1.3-0.32.62.75.5-4.2

Table 4 : Forecast of commodity prices

The crisis has taken a heavy toll on coun-tries that are highly dependent on naturalresources, especially those relying oncopper, oil, timber and diamonds. The fallin copper prices resulted in a significantdrop of export receipts for Zambia and aconsiderable reduction in its foreignexchange reserves. Since the second halfof 2008, the volume of reserves genera-ted by the mining sector dropped by 30%,

from USD 649 million during the first halfof 2008 to USD 454.5 million during thesecond semester of that year.

In Burkina Faso, export growth droppedfrom 6.9% in 2007 to 3.5% in 2008, follo-wing the fall in cotton production and thedecline in lint cotton export. The balance oftrade sharply deteriorated under the combi-ned impact of falling agricultural production

and declining lint cotton export (fromCFAF 160 million in 2007 to CFAF 12 mil-lion in 2008). The current account deficitis estimated at 12.9% of GDP in 2008, a3.8 point decline compared to 2007.

The adverse impact of the crisis on exportcommodity prices and resource inflowsthreatens to reverse the gains from therecent economic performance of Africaneconomies. Key consequences includedeclining reserves, non-profitability ofsome oil fields that have high extractioncosts, reduction in government fundingcapacity and cancellation or postpone-

ment of a number of investments in extra-ctive industries that are highly dependenton foreign direct investment.

The effects of the crisis will hit both oilexporters as well as producers of non-energy commodities, namely minerals andagricultural products (Table 5). Agriculturaland food products are following a similardownward trend estimated at around20%. The decline in food prices shouldmitigate the impact of the economic crisison African countries, especially on thebalance of payments and governmentbudget.

8

Source: AfDB, February 2009

Table 5: Commodity prices

% Change IndexValue at end of

Week(13/02/2009)

Benchmark07/31/2008

UnitCommodity

Crude Oil (Brent)*

Gold

Silver

Platinum

Cotton, N° 2 Future

Cocoa beans

Coffee, Arabica

Coffee, Robusta

US$ per barrel

US$ per Troy Ounce

US$ per Troy ounce

US$ per Troy ounce

USd/lb.

US$ per tonne

US cents per pound

US cents per pound

125.73

918.00

17.48

1,758.00

49.71

2,908.50

131.10

115.09

44.09

935.50

13.37

1,055.00

45.22

2,682.12

99.00

81.75

-64.93

1.91

-23.51

-39.99

-9.03

-7.78

-24.49

-28.97

However, the decrease of primary com-modity prices will have a positive impacton the external accounts of oil importingcountries, in particular countries that have

sustained a large deficit on the tradeaccount due to the large oil import bill.These include Burundi, Seychelles, Togoand Malawi.

These countries have large current accountdeficits ranging between -37.6% for Burundiand -18.6% for Malawi (Table 7). The effectwill depend on the combined impact of thedecrease of energy prices and non-oil pri-mary commodity prices. The deficit on the

current account will need to be financed bya surplus on the capital account, notablyaid and private capital inflows. These coun-tries would face significant difficulties if FDIand ODA were to decrease due to theeffects of the global slowdown.

9

Table 6: Countries vulnerable to commodities prices decreaseCountries dependenton non-oil primarycommodities

Share of nonfuelprimary commodities

in exports (%)

Countriesdependent on oil

exports

Share of oil inexports (%)

Gambia

Uganda

Ethiopia

Niger

Malawi

Rwanda

Burundi

97

91

84

83

82

80

79

Libya

Algeria

Nigeria

Congo. Rep.

Angola

Equatorial Guinea

Sudan

Gabon

98.7

95.7

95.6

92.1

92

83.8

74.5

71.1

Source: World Economic Situation and Prospects, United Nations, 2009

Source: World Economic Situation and Prospects, United Nations, 2009

Table 7: African countries with large oil imbalances, 2007 (% of GDP)

Net ODAdisbursements

Commoditiesbalance

FDIinflows

OilBalance

CurrentaccountCountry

Burundi

Seychelles

Togo

Malawi

-37.6

-32.7

-21.9

-18.6

-11.6

-36.5

-8.5

-4.3

Non-oilcommoditiesbalance

0.4

0.7

4.6

11.6

-12.0

-35.8

-4.0

7.3

0.0

18.8

3.5

-

46.0

1.8

3.6

21.3

4. The long and medium termtransmission channels

4.1 Trade flows

The global recession will adverselyimpact the flow of goods and services.World and African trade were part of themain drivers of growth between 2000and 2007. However, signs of a slow-down have been registered since 2008and will likely continue in 2009. The glo-bal economy has recorded a decreasein volume and value of tradable goodsand services. Indeed, world trade involume increased by 6.3% in 2007, by4.4% in 2008, and by only 2.1% in 2009.Due to the economic downturn in theindustrialized countries and lower prima-ry commodity prices, global trade isexpected to contract by 4.4% in value in2009.

Africa will not be spared from the pessi-mistic world trade outlook for 2009.Exports and imports growth rates areforecast at 3.6% and 10.5% in 2009, res-pectively compared to 10.6% and 15.2%in 2008. As a result, the impact of thecrisis on foreign exchange reserves isexpected to be large. Having benefitedfrom the recent primary commodityboom, Africa will experience a loss of

45.4% of its exports value in 2009.Losses in export growth rates are notcompensated for by decreasing importgrowth rates in value terms, implying thatthe trade balance may deteriorate.

4.2 Capital flows

4.2.1 Impact on foreign directinvestment

The latest global foreign direct invest-ment estimates show a sharp decline of21% in 2008 that is likely to worsen in2009. Total foreign direct investment in2008 is estimated at USD 1.4 trillion.FDI inflow to Africa are currently steadyat a relatively low level at USD 61.9 bil-lion (2008), an increase of 16.8% from2007. However, there are large discre-pancies across countries: whereasEgypt and Morocco respectively repor-ted a decline of -5.6% and -7%, FDI inSouth Africa more than doubled in 2008(Table 8).

In the short term, the financial and eco-nomic crisis is expected to cause FDI tofall further in 2009. Africa will not be spa-red, especially if commodity prices conti-nue to fall. This will further increaseAfrica’s financial marginalization andundermine growth in foreign capitaldependent sectors such as naturalresources.

10

4.2.2 Short term private capital flows

According to last estimates, short term netprivate capital flows to emerging countriesaccounted for USD 253 billions in 2007and declined to USD 141 billions in 2008.Net portfolio inflows to Africa have alsodeteriorated in 2008 relative to 2007. Thisdecrease shows the scarcity of financialresources, a result of the deterioratingmarket conditions and the contraction ofthe economy in some emerging countries.

Preliminary estimates for capital inflows inAfrica are not as bad as for other regionsfor a number of reasons. Among theseare Africa’s low share of total capitalflows, the limited number of countriesleveraging funds on international marketsand the limited correlation betweenAfrican and industrialized countries finan-

cial markets. However, no bonds issue inforeign currency has been registered in2008 for African countries, whereas it hadreached 6.5 billion dollars in 2007 compa-red to 1.5 billion dollars in 2005. Thissituation raises concerns, as many coun-tries such as South Africa rely on inflowsof private capital to cover their currentaccount deficits.

4.2.3 Impact on remittances

Remittances, which have become a majorsource of external financing for Africancountries, have been adversely affectedby the slowdown in developed countries.In some countries, remittances exceedofficial development aid as a source ofexternal financing. The total volume ofremittances to Africa stood at USD 38 bil-

11

Table 8: FDI inflows

2007 2008 Growth rate (%)

WorldDeveloped economiesDeveloping economiesAfricaEgyptMoroccoSouth AfricaLatin AmericaAsia and OcceaniaSouth East AsiaSouth-East Europe and the CIS

1833.31247.6499.753

11.62.65.7

126.3320.5247.885.9

1449.1840.1517.761.910.92.412

142.3313.5256.191.3

-21-32.73.616.8-5.6-7

111.212.7-2.23.36.2

Source: World Economic Situation and Prospects, United Nations, 2009

FDI inflows (billion of dollar)

lion in 2007. Remittances between Africancountries have fallen following job cutsand the decline of activity in the miningsector. The decline in the volume of remit-tances has a direct negative impact onthe well-being of households since suchtransfers – unlike other types of transfers– are directly used to cover primary needssuch as food, education and healthcare.

While updated data on emigrant transfersremain incomplete, they tend to showsigns of a negative impact of the crisis.Monthly data for December 2008 andJanuary 2009 indicate some stagnation ora slight decline worldwide. Surprisingly,remittances in some countries such asKenya have increased. Nonetheless, inthe absence of data, it is too early to drawa definitive conclusion on the impact ofthe crisis on remittances in Africa.

5. The economic outlook afterthe financial crisis

5.1 The fall in reserves andgovernment budget

Rising commodity prices have enabledAfrican countries to accumulate foreignexchange. Thus, Africa accumulated USD369 billion in 2007, USD 110 billion byAlgeria, compared to USD 79 billion byLibya and USD 51 billion by Nigeria.These receipts enabled oil-exporting

countries to acquire considerable fiscalspace to undertake major public invest-ment programs and repay foreign debt.Now, some countries that had preparedbudgets based on prices averaging USD70 will be forced to scale down theirinvestment plans if the downward pricepressures persist. Forecasts show a bud-get deficit of -7.7% of GDP for oil expor-ting countries in 2009 against a surplus of5.1% of GDP in 2008 and 4% of GDP in2007.

Overall, Africa will move from a globalbudget surplus accounting 2.3% of theGDP in 2008 to a deficit of 5.5% in 2009.The deficit will deepen for oil importers aswell (from -1.6% to -2.8%).

Under the effect of the crisis, currentaccount deficits have worsened since2008 in twenty-six countries. From anoverall current account surplus position of3.5% of GDP in 2008, the continent willface deficit of -3.8% of GDP in 2009. Thelarge surplus of 9.8% of GDP for thegroup of oil exporters will turn into a defi-cit of -3.9% of GDP. This is a direct resultof the expected decline in oil revenue.North-Africa is the only region with a cur-rent account surplus of approximately 3%of GDP, led by Morocco (10.7%) andAlgeria (5.6%).

In 2009, some countries will face a twindeficit (current account and budget defi-

12

cits). This is because exports will fall fas-ter than imports (causing current accountdeficit) while governments try to keep upwith expenditure levels in the context ofdeclining revenue. Thus several countriesface the threat of structural macroecono-mic imbalances in the medium term if thecrisis persists.

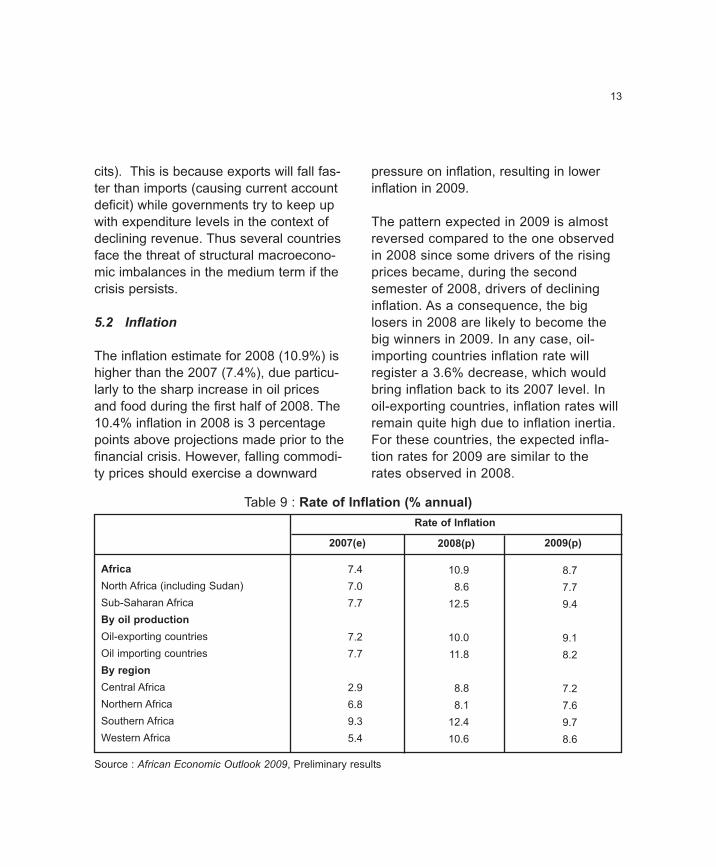

5.2 Inflation

The inflation estimate for 2008 (10.9%) ishigher than the 2007 (7.4%), due particu-larly to the sharp increase in oil pricesand food during the first half of 2008. The10.4% inflation in 2008 is 3 percentagepoints above projections made prior to thefinancial crisis. However, falling commodi-ty prices should exercise a downward

pressure on inflation, resulting in lowerinflation in 2009.

The pattern expected in 2009 is almostreversed compared to the one observedin 2008 since some drivers of the risingprices became, during the secondsemester of 2008, drivers of declininginflation. As a consequence, the biglosers in 2008 are likely to become thebig winners in 2009. In any case, oil-importing countries inflation rate willregister a 3.6% decrease, which wouldbring inflation back to its 2007 level. Inoil-exporting countries, inflation rates willremain quite high due to inflation inertia.For these countries, the expected infla-tion rates for 2009 are similar to therates observed in 2008.

13

Table 9 : Rate of Inflation (% annual)

2007(e) 2008(p) 2009(p)

AfricaNorth Africa (including Sudan)Sub-Saharan AfricaBy oil productionOil-exporting countriesOil importing countriesBy regionCentral AfricaNorthern AfricaSouthern AfricaWestern Africa

7.47.07.7

7.27.7

2.96.89.35.4

10.98.612.5

10.011.8

8.88.112.410.6

8.77.79.4

9.18.2

7.27.69.78.6

Source : African Economic Outlook 2009, Preliminary results

Rate of Inflation

5.3 Growth Prospects

Global growth prospects have been revie-wed downwards for most regions. Slowinggrowth worldwide and in all industrializedcountries was the rule in 2008. For 2009growth is expected to be at 0.9% for theworld and -0.1% for industrialized coun-tries. Only China will continue to post asustained growth rate of 7%, which wasrevised downward from 12% at the begin-ning of 2008.

Although Africa escaped direct effect ofthe financial crisis, it cannot be shieldedfrom global recession, even if the degreeof the continent’s trade integrationremains low. Africa’s projected growthrate in 2009 (2.9%) is about half that of2008 level (5.7%) (Table 4). Preliminaryprojections show expected losses of 4.4%of growth rate for oil-exporters in 2009and 1.2% decline in growth for oil-impor-ting countries. For the first time since the2000s, oil-importing countries shouldregister higher growth rates than oil-exporting countries. Middle-income coun-tries will be affected by decreasing foreigndemand for manufactured products, textileand tourism and should suffer growthlosses comparable to oil-importing andlow-income countries. Growth decelera-tion may compromise Africa’s effortstowards reaching the MillenniumDevelopment Goals and poverty reduc-tion.

5.4 Sectoral impact

Although it is too early to accurately pre-dict the impact of the global financial andeconomic crisis, preliminary evidencedemonstrates that some key sectors inAfrican economies have already felt itsadverse effects.

5.4.1 Tourism

Tourism has suffered a big hit from thecrisis as a result in declining incomes indeveloped and emerging countries, wheremost tourist flows originate. Yet tourismreceipts represent an important share ofgovernment revenues in many countries.Both arrivals and receipt have declinedsubstantially in many countries. Kenyaannounced a 25 % to 30% decline in tou-rist arrivals. Kenya Airways posted a62.7% drop in profit for the half-year atthe end of September 2008. The declinein tourism would have a negative impacton the services sector, which was beco-ming a key growth engine prior to the cri-sis. This calls for further efforts towardsdiversification not only of the servicessector but also of the entire economy.Egypt also announced a 40% cancellationof hotel reservations. The Seychellesannounced a 10% fall in tourism revenue.

5.4.2 Mining Sector

Several projects in the extractive indus-tries were cancelled or postponed in

14

DRC, Zambia, South Africa, CAR andCameroon. In Zambia, the USD 1.5 billionKafu Gorge Dam Project was kept inabeyance following the reticence of seve-ral investors caused by falling copperprices. Such mining companies as FirstQuantam Minerals, Albidon and MakamboCopper Mine have given up all new explo-rations. At the same time, KonkolaCopper Mines – the largest copper minein Zambia – has ordered a 40% reductionin all supplier contracts.

In the Democratic Republic of Congo,extraction operations at the open-castmine Tilwezembe and the treatment of oreat Kolwezi plant have nearly been broughtto a halt because of the slump in prices ofcobalt. As many as 70 mining companiesoperating in Kantaga closed. Since theend of 2008, Forrest International laid off650 employees and indicated that theexploitation of cobalt is not profitable atthe price of USD9/pound. According to theMinistry of mining in DRC, these closureswould have caused a loss of up to200000 jobs.

The fall of the price of manganese by60% in 2008 had serious repercussions inGabon, second world manganese produ-cer. The Comilog company, which hasoperations in the South-east of the coun-try (Moanda), decided to reduce by halfits production in the first quarter of 2009.

If the price of oil and manganese is notrestored, Gabon will be suffer negativeeffects on its budget and current accountbalances.

The fall in the price of the iron since thecrisis has also affected Senegal andMauritania. For Senegal this fall delayedthe operational startup of the exploitationin Flémé whose production is envisagedfor 2011and the agreement was signedFebruary 2007 with Arcelor Metal, aFrench company. The Mauritanian pro-duction of iron which accounts for 50% ofexports was heavily affected by the fall inthe price of the iron.

The price of the uranium declined fromUSD140 to USD53 per pound betweenJuly 2008 and January 2009 will haveharmful consequences on the export ear-nings of Niger. Uranium accounts for 50%of these export earnings. Niger counts onthe increase in production although it maynot compensate for the drop in prices.The French company Areva signed acontract to exploit the second largestreserves in Africa.

The fall of the price of bauxite whichdominates the mining sector of Guinea,the second largest exporter in the world,will affect export earnings. The miningsector accounts for 30% of the publicrevenue and 70% of the export earnings.

15

A project to construct an aluminum facto-ry, gathering three international groups, islikely to be deferred.

5.4.3 Textile

Several textile factories were closed inMadagascar and Lesotho. The latterrecorded a decline in external textiledemand from South Africa and the UnitedStates, its major trading partners. InMadagascar, recent data shows an 8% to15% decline in economic activity invarious sectors. Employment pressureshave emerged, attributable to the vulnera-bility of labor-intensive sectors (tourismand textile) to the crisis. A local textilecompany in the West of the country clo-sed, causing the loss of 4000 jobs.

5.4.4 Other sectors

The manufacturing sector has been affec-ted by both falling global demand andrising cost of imports of intermediategoods caused partly by currency depre-ciation. As a result, factories run at lowcapacity and employment is seriouslythreatened. For instance in Uganda, theUganda Manufacturers Association (UMA)reported that fifteen factories closed in2008 due to the high cost of doing busi-ness. South Africa announced a signifi-cant drop in the sale of new cars, reflec-ting the crisis facing vehicle manufactu-

rers worldwide. The decline in activity inthe manufacturing sector has causedlarge job losses with damaging effects onliving standards.

6. CONCLUSION

The global financial crisis will have asignificant impact on Africa, althoughAfrica’s growth outlook is still better com-pared to industrialized countries. A 3.2%growth rate compared to a decline of 0.1% for advanced economies may appearas a good performance. However, compa-red to 2007, it represents a loss of 3 per-centage points. In addition, this level is farfrom the growth required to reach theMillennium Development Goals. The cur-rent economic crisis affects all the driversof African growth: prices and demand forprimary commodities, capital flows, espe-cially foreign direct investment. Manycountries face the risk of twin deficits (cur-rent account and budget deficits). If thecrisis was to last, it could even threatenthe gains achieved in the last decade inthe fight against poverty.

The major challenge is to mobilizeresources to finance growth, develop-ment, investment in infrastructure andpoverty reduction programs. This willrequire that aid commitments by donorsare met, and that African countries impro-ve their performance in resource mobiliza-

16

tion at the national and regional level.However, long-term strategies must beoriented toward building more resilienceto the crisis and sustaining growth.

The following areas will require immediateattention from African governments, theBank and the continent’s developmentpartners.

• Supporting domestic growth drivers:Economic policy at the macroeconomicand sectoral level needs to targetsupport for domestic growth driversand be tailored to each country’scircumstances. Measures should beinvestigated to support tourism, miningand other export oriented activities.

• Increasing investment ininfrastructure: It is critically importantthat African countries keep an adequa-te level of infrastructure investment tosupport private sector activity in gene-ral and enhance competitiveness anddiversification in particular.

• Preparedness and targeted responsesby the Bank: the Bank should play a

critical role in assisting African coun-tries to devise strategies for preventingand mitigating the impact of financialcrises. In particular, it is important toevaluate the resource requirementsfor assisting countries affected by thecrisis.

• Ensuring adequate flows of develop-ment aid: Despite the economicdownturn in developed and emergingcountries, it is important that donorshonor their aid commitments. Anyreduction in aid will amplify the nega-tive impact of the crisis on Africaneconomies, which in turn will delayglobal economic recovery by depres-sing demand.

The Bank will share it analysis of theimpact of the financial crisis on differentsectors in African economies. The analysiswill also serve as input for the OperationsDepartments in the preparation of CountryAssistance Strategies as well as Projectand Programme Interventions. The Bankenvisages intensified interventions inRMCs by targeting growth drivers and themost affected sectors.

17

28

19

African Development Bank (2009)Financial Crisis Monitoring group WeeklyReport, February 2009

African Development Bank (2009)Financial Crisis Monitoring Group WeeklyReport January 2009

African Economic Outlook 2008/09,Preliminary results

Global Development Finance, World Bank2008 and JPMorgan

International Monetary Fund (2008)Global Financial Stability Report, October2008

Sovereign Wealth Fund Institute, 2008

UNCTAD (2008) World Investment Report2008

United Nations (2009) Department ofEconomic and Social Affairs, February2009

World Bank (2009) Global EconomicProspects 2009: Commodity markets

References

20

Annex 1: Impact on selected financial markets

Region/CountryBenchmark07/31/2008

Value at endof Week

(13/02/2009)

Losses duesto financialcrisis (%)CodeName

INDEX

Cote d’Ivoire

Egypt

Kenya

Mauritius

Morocco

Nigeria

South Africa

Tunisia

USA

France

Japan

BRVMCompositeIndexCASE 30IndexKenyaStock IndexMauritiusAllSharesCasa AllShare IndexNSE AllShare IndexAll ShareIndexTunis seTnse IndexSTK

Dow JonesIndustrialCAC 40IndexNikkei 225Index

BRVM CI

CASE 30

KSE

SEMDEX

MASI

NSE

JALSH

TUNINDEX

DJ Index

CAC 40

N 225

242.54

9251.19

4868.27

1735.77

14134.70

52916.66

27552.65

3036.87

11378.02

4392.36

13376.81

169.34

3600.79

2855.87

1005.69

10352.81

23814.46

20650.38

3049.6

7,850.41

2,997.86

7,779.40

-30.18

-61.08

-41.34

-42.06

-26.76

-55.00

-25.05

0.42

-31.00

-31.75

-41.84

AFRICA

OTHERS

Source: AfDB, Statistics Department, January 2009

21

Annex 2: World and African trade prospects

Rate of Growth Rate of GrowthLoss ofGrowth

Loss ofGrowth

2006 2007 2008 2009 2008-2007

2009-2008 2006 2007 2008 2009 2008-

20072009-2008

World

Africa

North Africa

Sub-SaharanAfrica (excludingNigeria and SouthAfrica)

8.8

0.2

16.5

4.7

6.3

10.1

10.4

8.1

4.4

10.6

14.3

6.1

2.1

3.6

6.6

4.9

-1.9

0.5

3.9

-2

-2.3

-7

-7.7

-1.2

14.9

18.6

33.1

20.7

15.6

20.1

19.4

21.2

18.9

38.3

52.7

42.1

-4.4

-7.1

-5.4

-22.5

3.3

18.2

33.3

20.9

-23.3

-45.4

-58.1

-64.6

World

Africa

North Africa

Sub-Saharan

Africa (excluding

Nigeria and South

Africa)

8.8

11.6

16

4.7

6.3

17.6

24.9

8.1

4.4

15.2

24.3

6.1

2.1

10.5

17.9

4.9

-1.9

-2.4

-0.6

-2

-2.3

-4.7

-6.4

-1.2

14.9

19.5

20.8

12

15.6

25.5

33.7

18.7

18.9

29.1

50.8

18.2

-4.4

6.6

15.2

2.8

3.3

3.6

17.1

-0.5

-23.3

-22.5

-35.6

-15.4

Source: World Economic Situation and Prospects, United Nations, 2009

Volume of Exports

Volume of Imports

Value of Exports

Value of Imports

22

Annex 3: Overall fiscal balance and current account balance (% GDP), 2007-2009

Source: African Economic Outlook 2009 (preliminary estimates), AfDB, 2009

Africa

North Africa (including Sudan)

Sub-Saharan Africa

By oil production

Oil-exporting countries

Oil importing countries

By region

Central Africa

Northern Africa

Southern Africa

Western Africa

1.89

2.90

1.25

3.87

-0.41

5.46

3.51

2.47

-0.54

1.82

2.38

1.48

4.32

-1.75

10.73

2.98

2.32

-0.08

-5.06

-5.79

-4.61

-7.30

-2.12

3.26

-6.15

-3.46

-9.00

2.66

10.65

-2.37

9.11

-4.79

-1.47

13.05

-3.34

0.11

2.72

10.14

-1.68

8.78

-5.88

3.88

12.15

-3.01

0.72

-4.05

1.75

-7.70

-4.00

-4.13

-9.39

3.02

-7.65

-8.57

Fiscal balance Current account

2007 2008(e) 2009(p) 2007(e) 2008e) 2009(p)

23

Annex 4 : Growth and inflation in Africa, 2007-2009

Source: African Economic Outlook 2009 (preliminary estimates), AfDB, 2009

Africa

North Africa (including Sudan)

Sub-Saharan Africa

By oil production

Oil-exporting countries

Oil importing countries

By region

Central Africa

Eastern Africa

Northern Africa

Southern Africa

Western Africa

7.4

7.0

7.7

7.2

7.7

2.9

10.1

6.8

9.3

5.4

10.9

8.6

12.5

10.0

11.8

8.8

17.8

8.1

12.4

10.6

8.7

7.7

9.4

9.1

8.2

7.2

10.2

7.6

9.7

8.6

6.1

5.7

6.4

6.8

5.4

4.0

8.8

5.3

7.0

5.4

5.7

6.0

5.5

6.6

4.6

5.0

7.3

5.8

5.3

5.4

2.9

3.5

2.4

2.4

3.4

2.8

5.5

3.3

0.4

4.2

Inflation Real GDP growth

2007 2008(f) 2009(p) 2007 2008(e) 2009(p)

2 5

R e c e n t P u b l i c a t i o n s i n t h e S e r i e s

N °

9 5

9 4

9 3

9 2

9 1

9 0

8 9

8 8

8 7

8 6

Y e a r

2 0 0 8

2 0 0 8

2 0 0 7

2 0 0 7

2 0 0 7

2 0 0 7

2 0 0 7

2 0 0 7

2 0 0 7

2 0 0 7

A u t h o r ( s )

M a r g a r e t C h i t i g a , T o n i a K a n d i e r o a n d P h i n d i l e N g w e n y a

V a l é r i e B é r e n g e r a n d A u d r e y V e r d i e r - C h o u c h a n e

R e s e a r c h D i v i s i o n ; A f D B

J o h n C . A n y a n w u a n d A n d r e w E . O . E r h i j a k p o r

J o h n C . A n y a n w u a n d A n d r e w E . O . E r h i j a k p o r

T o n i a K a n d i e r o

M a a r t e n v a n A a l s t , M o l l y H e l l m u t h a n d D a n i e l e P o n z i

A b d u l B . K a m a r a , L o b n a B o u s r i h , M a g i d u N y e n d e

B . D h e h i b i , L . L a c h a a l , B . K a r r a y a n d A . A . C h e b i l

N i c h o l a s A d a m t e y , V i t u s A z e e m a n d S a m u e l F a m b o n

T i t l e

A g r i c u l t u r a l T r a d e P o l i c y R e f o r m i n S o u t h A f r i c a

D e s I n é g a l i t é s d e g e n r e à l ’ i n d i c e d e q u a l i t é d e v i e d e s f e m m e s

T h e I m p a c t o f H i g h O i l P r i c e s o n A f r i c a n E c o n o m i e s

E d u c a t i o n E x p e n d i t u r e s a n d S c h o o l E n r o l m e n t i n A f r i c a : I l l u s t r a t i o n s f r o m N i g e r i a a n d O t h e r S A N E C o u n t r i e s

H e a l t h E x p e n d i t u r e s a n d H e a l t h O u t c o m e s i n A f r i c a

C u r r e n t A c c o u n t S i t u a t i o n i n S o u t h A f r i c a : I s s u e s t o C o n s i d e r

C o m e R a i n o r S h i n e - I n t e g r a t i n g C l i m a t e R i s k M a n a g e m e n t i n t o A f r i c a n D e v e l o p m e n t B a n k O p e r a t i o n s

G r o w i n g a K n o w l e d g e - B a s e d E c o n o m y : E v i d e n c e f r o m P u b l i c E x p e n d i t u r e o n E d u c a t i o n i n A f r i c a

D e c o m p o s i t i o n o f O u t p u t G r o w t h i n t h e T u n i s i a n O l i v e - G r o w i n g S e c t o r : A F r o n t i e r P r o d u c t i o n F u n c t i o n A p p r o a c h

A R e v i e w o f E x - a n t e P o v e r t y I m p a c t A s s e s s m e n t s o f M a c r o e c o n o m i c P o l i c i e s i n C a m e r o u n a n d G h a n a