Embed Size (px)

Citation preview

Impacts of COVID-19 on Firms in the Philippines

Results from the Philippines COVID-19 Firms Survey conducted in July 2020

Key Findings

• These findings are based on the survey of 74,031 firms carried out between July 7 to 14, 2020, to assess the COVID-19 impact on firms’ activities.

• COVID-19 community quarantine measures had a significant temporary and permanent impact on firms’ operations. In July 2020, 40 percent of firms reported the temporary suspension of their operations -- 20 percent by government mandate and 20 percent voluntarily. About 15 percent of firms reported to have closed permanently.

• Despite the easing of the community quarantine in June 2020, firms reported a deep reduction in sales revenue. Reported sales revenue has gone down by 64 percent on average between April and July 2020, with 89 percent of firms reporting a continued reduction in sales.

• The negative impact on employment is also extensive as 1 out of 2 firms reported having reduced payments to employees. Close to half (48 percent) of firms reported that they reduced the number of their employees, while the rest maintained the level of employment with only 1 percent reporting new employment.

2

Key Findings

• Almost two thirds of firms turned to digital solutions for sales, marketing, and payment methods to adapt to the new normal. A sizable share of firms also invested in digital solutions (23 percent) or repackaged their product mix (40 percent).

• Firms expressed a high degree of uncertainty and general pessimism about their operations, sales and employees for the next three months. Such lack of confidence will likely limit additional investment and employment, restraining firms’ growth. These suggest that business activities are expected to stay subdued for an extended period.

• Firms say the most useful form of government support are those that would improve their liquidity, such as cash transfers, subsidized interest rates, deferral of loan, rent, or utility payments, and tax exemptions or reductions. About 1 out of 5 firms received support from the national or local government, mainly in the form of cash transfers directly paid to employees.

3

Philippines COVID-19 Firm Survey

• Objective: To better understand the impacts of COVID-19 on the private sector

• Sponsors: The World Bank in collaboration with the Department of Finance (DOF) and the National Economic Development Authority (NEDA) and support from the Australian Government

• Survey round• July 7 - 14, 2020, following the April 2020 survey by the

government• First of five rounds

• Data collection method: Self-administered online survey

• Sample and representativeness: • 74,031 responses• Sample was reweighed to follow the distribution of firms by

region and firm size based on employment as reported by the Philippine Statistics Authority’s 2018 Listing of Establishments

• Analysis of impacts on firms conducted by asset size (micro, small, medium, and large), location (17 regions), and sector (agriculture, manufacturing, and services)

4

How COVID-19 is affecting firms

5

COVID-19 shocks operate through many channels, but the magnitude and who is more affected is hard to predict.

The PH COVID-19 Firm Survey measured the impact of shocks on firms’ sales and employment, their operations, expectations, as well as their adjustment mechanisms and access to government support.

Responses by firms and government

Government SupportGovernments can provide fiscal support to firms facing negative shocks

Employment measuresFirms can adjust by tightening their labor force and wage bill

Digital TechnologyFirms can adjust by adopting new digital technology and business models

Lockdown effectsPublic health measures require

non-essential businesses to close

Demand shocksEconomic downturn drives down demand domestically and abroad

Financial shocksOpportunities for finance

becoming further constrained

UncertaintyUncertainty is driving down investment and innovation

Temporary shock, targeting non-essential businesses, mostly in retail, hotels/restaurants

(tourism) and personal services.

Broad-based shock. Will especially hit firms producing durables, apparel/textiles and those reliant on export (manufacturing & services –

e.g. tourism).

Supply shocksDecline in labor and intermediate

inputs, global value chains disrupted

E.g., firms that rely on imports are affected.

Deterioration in availability of credit while demand increases will affect access to finance

Country Context

The Government of the Philippines imposed strict community quarantine measures to minimize the spread of COVID-19

6

Impact on firmsLockdown and economic downturn can drive down demand domestically and abroad, disrupt input supply, and drive down liquidity.

7

Community quarantine had a significant effect on the operational status of firms

• 40 percent of firms were closed temporarily, either by government mandate (20 percent) or voluntarily (20 percent)

• 15 percent of firms stated that they were permanently closed

8

2% 5%

21%

40%

77% 40%

15%

April July

Operating status of firms (% of firms)

PermanentlyclosedClosed

Partially Open

Open

4 out of 5 firms in the arts, entertainment, and recreation and tourism and accommodation sectors were closed

929%

31%

34%

27%

33%

34%

37%

38%

39%

40%

43%

41%

51%

56%

60%

61%

40%

12%

11%

10%

19%

13%

13%

13%

14%

13%

15%

14%

20%

18%

16%

20%

21%

16%

UtilitiesHealth

Auto repairFinancial activities

AgricultureWholesale and retail trade

ConstructionProfessional services

ManufacturingICT: BPO and others

Real estate and leasingFood services

EducationTransportation

TourismArts & entertainment

All sectors

Operational status of firms by sector (% of firms)

Temporarily Closed Permanently Closed

Demand shock continues despite the easing of the community quarantine: firms have reported a deep reduction in sales revenue

0 10 20 30 40 50 60 70 80 90 100

Utilities

Construction

Education

Transportation and storage

Financial activities

Total

Professional services and other servce activities

Real estate, rental and leasing services

Tourism and accomodation services

All sector

Change in sales in July 2020 compared with April 2020 (% of firms)

Don't know Increased Remained the same Decreased

10

Three quarters of firms experienced a decrease in demand, with 1 in 3 firms reporting a decline by more than 50 percent.

11

4%

3%

5%

6%

9%

5%

5%

4%

6%

5%

8%

5%

4%

4%

4%

4%

7%

4%

11%

7%

11%

9%

15%

10%

11%

13%

15%

13%

13%

13%

27%

30%

29%

28%

24%

28%

37%

38%

29%

35%

24%

34%

Other services

Accomodations & food

Wholesale & retail

Manufacturing

Agriculture

All sectors

Impact on Demand for Products and Services

Increased by more than 50% Increased by 25% to 50% Increased by less than 25% Remained the sameDecreased by less than 25% Decreased by 25% to 50% Decreased by more than 50%

12

0% 20% 40% 60% 80%

Quality and price remain the same, butcustomers show less interest

Customers are less aware of the products orservices

Price of products or services has increased

Customers cannot purchase products or servicesusing mobile phone or online platform

Quality of products or services has decreased

Customers cannot travel to the establishment topurchase products or services

Reasons for the decreased demand for products and services (% of firms)

70 percent of firms reported having their operations affected by a decrease in the availability of inputs and raw materials

13

2%

2%

2%

4%

5%

2%

2%

2%

2%

4%

5%

2%

2%

2%

3%

4%

4%

3%

2%

2%

3%

4%

4%

3%

30%

23%

18%

19%

23%

22%

23%

29%

30%

27%

22%

27%

25%

20%

23%

21%

21%

23%

Other services

Accomodations & food

Wholesale & retail

Manufacturing

Agriculture

All sectors

Impact on availability of inputs, raw materials, or finished goods to resell

Increased by more than 50% Increased by 25% to 50% Increased by less than 25% Remained the sameDecreased by less than 25% Decreased by 25% to 50% Decreased by more than 50%

14

Reasons for the decreased availability of inputs and raw materials (% of firms)

0% 10% 20% 30% 40% 50% 60%

International suppliers have ceased or reducedoperations

Slow customs clearance has reduced availability ofinputs, raw materials, or finished goods to resell

Don't know

Local distributors are experiencing delays due tocheckpoints

Domestic suppliers have ceased or reduced operations

Local distributors have ceased or reduced operations(e.g. limited availability of trucks/drivers)

40 percent of firms reported that prices of inputs and raw materials increased

15

5%

4%

4%

5%

5%

5%

10%

16%

15%

13%

13%

14%

15%

23%

23%

24%

20%

21%

39%

30%

30%

29%

27%

32%

6%

7%

8%

7%

11%

8%

10%

10%

10%

11%

11%

10%

15%

10%

9%

10%

13%

11%

Other services

Accomodations & food

Wholesale & retail

Manufacturing

Agriculture

All sectors

Impact on price of inputs, raw materials, or finished goods to resell

Increased by more than 50% Increased by 25% to 50% Increased by less than 25% Remained the sameDecreased by less than 25% Decreased by 25% to 50% Decreased by more than 50%

Firms faced a deterioration of their cash flow …

16

1%

2%

2%

3%

2%

2%

2%

2%

3%

4%

3%

3%

2%

3%

2%

2%

3%

3%

7%

7%

8%

8%

11%

8%

11%

11%

15%

14%

18%

13%

29%

31%

34%

28%

26%

31%

47%

45%

37%

41%

36%

42%

Other services

Accomodations& food

Wholesale &retail

Manufacturing

Agriculture

All sectors

Impact on availability of cash flow

Increased by more than 50% Increased by 25% to 50% Increased by less than 25% Remained the sameDecreased by less than 25% Decreased by 25% to 50% Decreased by more than 50%

… and decreased access (among those needing) to financial services for funding

17

4%

5%

4%

7%

5%

5%

4%

3%

4%

3%

3%

4%

3%

3%

3%

3%

4%

3%

19%

16%

19%

17%

19%

18%

10%

12%

12%

13%

14%

12%

22%

23%

25%

23%

17%

23%

39%

38%

32%

34%

37%

36%

Other services

Accomodations & food

Wholesale & retail

Manufacturing

Agriculture

All sectors

Impact on access to financial services for funding

Increased by more than 50% Increased by 25% to 50% Increased by less than 25% Remained the sameDecreased by less than 25% Decreased by 25% to 50% Decreased by more than 50%

Loans from friends and family were most accessible, while loans from government institution and banks were least accessible

180% 10% 20% 30% 40%

Earlier payments from customers

Delayed payments from suppliers andproviders

Delayed payment terms of taxes anddebt

Loans from friends and family

Loans from banks

Loans from informal lenders

Loans from non-bank financialinstitutions

Loans from digital financing platforms

Loans from government institution

Liquidation of assets

Financial services or funding that firms applied and received (% of firms)

0% 10% 20% 30% 40%

Earlier payments from customers

Delayed payments from suppliers andproviders

Delayed payment terms of taxes anddebt

Loans from friends and family

Loans from banks

Loans from informal lenders

Loans from non-bank financialinstitutions

Loans from digital financing platforms

Loans from government institution

Liquidation of assets

Financial services or funding that firms applied but did not receive (% of firms)

Responses by firmsFirms have taken cost saving measures by reducing hours of operations, wages, and their employees, as well as adjusting business models to use digital solutions.

19

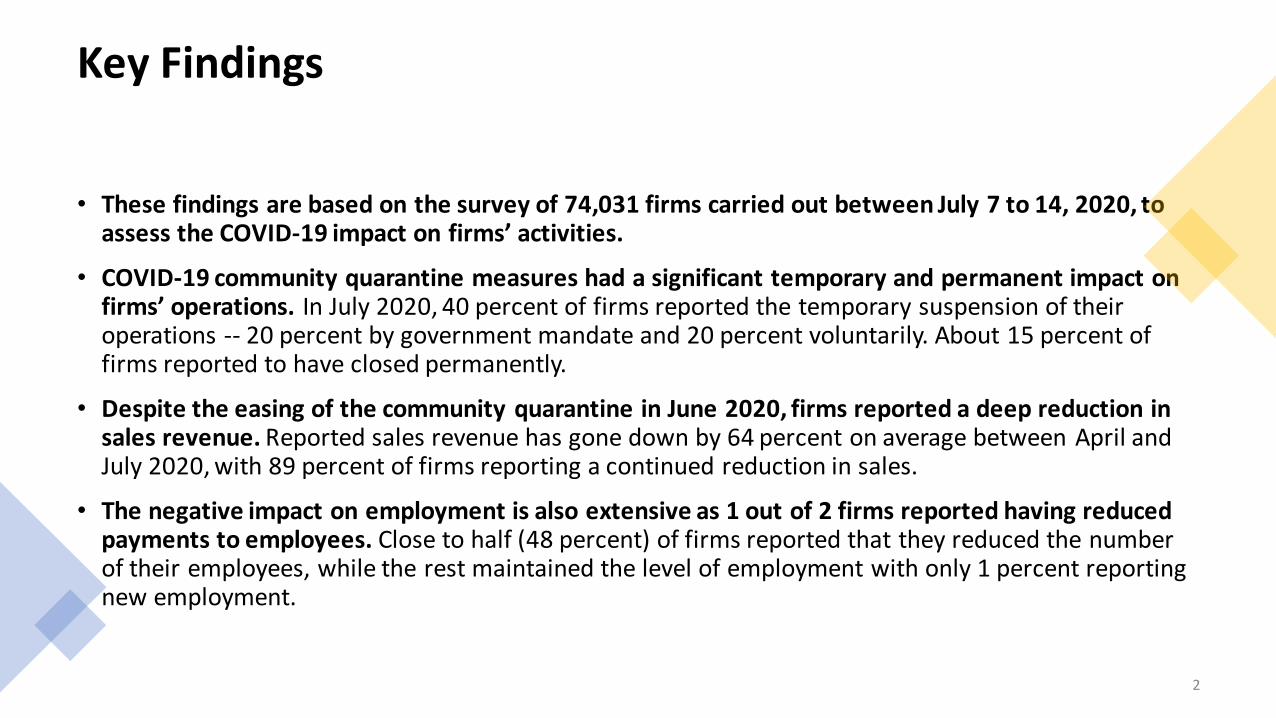

52 percent of firms reduced payment to employees, and 48 percent of firms laid off workers

20

1%

37%

48%52%

Increased Remained the same Decreased Reduced payment toemployees

Impact on employment and compensation in July 2020 compared to April 2020 (% of firms)

… with firms from education, food services and construction cutting down manpower the most

21

51%38%

42%52%

43%43%44%

37%38%

37%36%

37%33%

29%27%

26%37%

37%39%

40%40%

43%44%44%

48%50%

52%54%54%

56%62%62%

65%48%

Financial activitiesWholesale and retail trade

Real estate, rental and leasing servicesHealth

Transportation and storageAutomotive repairs

Agriculture, fishing, miningArts, entertainment, and recreation

UtilitiesICT: BPO and others

Tourism and accomodationProfessional services

ManufacturingConstruction

Food servicesEducationAll sectors

Impact on employment by sector (% of firms)

Don't know Increased Remained the same Decreased

Many firms (58% of SMEs and large firms, 63% of micro firms) turned to digital solutions to adapt to the new normal

22

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Automotive repairAgriculture

Food servicesWholesale and retail trade

TransportationOther services

UtilitiesManufacturing

ConstructionReal estate

HealthRental and leasing

Arts & entertainmentFinancial activities

TourismEducation

Professional servicesICT

Use of digital solutions in the new normal (% of firms)

Just started using Increased use Not using

Uptake in digital solutions so far have focused on front-end functions such as sales, marketing, and payment methods.

23

0% 10% 20% 30% 40% 50% 60%

Fabrication of goods

Production planning

Supply chain management

Business Administration

Payment methods

Service delivery

Sales

Marketing

Business functions where digital solutions are being used (% of firms)

70% of firms noted that less than 2% of their employees worked from home

• The most cited obstacle is that the nature of work was not suited to home-based work

• Only 5 percent of firms noted that 90 percent or more of their employees worked from home

24

0% 10% 20% 30% 40% 50% 60%

Infrastructure of employee’s homes inadequate for homebased work

Employees’ competing caregiving / family responsibilities

Unreliable or expensive internet connection in employees’ homes

Lack of equipment needed foremployees to work from home

Nature of work not suited to home-based work

Major obstacles faced by the firm in maximizing the number of employees to work from home (% of firms)

UncertaintyUncertainty is an important additional channel affecting firms during the pandemic, and as the economy re-opens, this could result in a lower desire for risk-taking and additional investments.

25

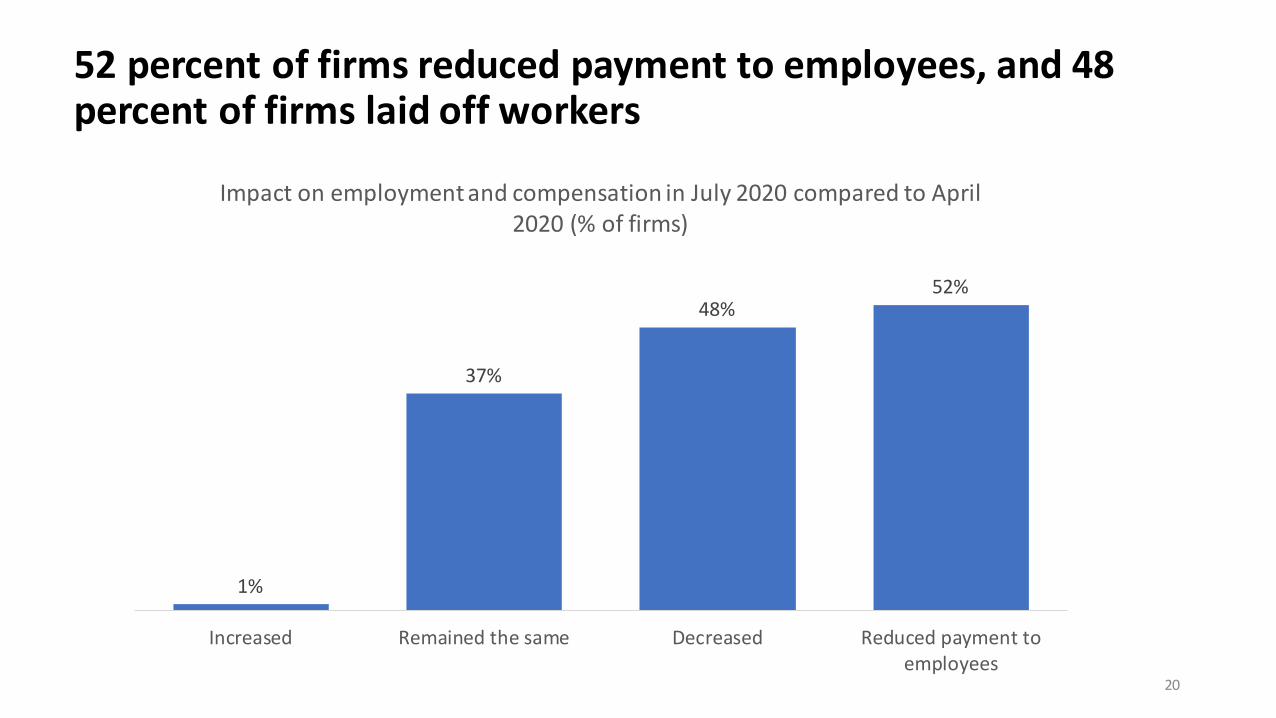

45 percent of the currently closed firms did not know when their businesses could resume

26

8% 9%15% 14%

9%

45%

5%11%

20%

13% 12%

39%

Less than 2 weeks Between 2 and 4weeks

Between 1 and 3months

Between 3 and 6months

More than 6months

Don't know

Expected opening and closure (% of firms)When closed firms expect to open When operating firms expect to close

About one third of firms did not know how they sales and employment will change in the next 3 months

27

23%18%

32%28%

10%

33%

24%

33%

Is expected to increase Is expected to remain thesame

Is expected to decrease Don't know

Expected changes in sales and employment, July vs. September 2020 (% of firms)

Sales Employment

Policy supportGovernments can provide support to firms facing negative shocks

28

About 1 out of 5 firms reported receiving some support from the national or local government. • Cash transfers provided to employees through the Pantawid Pamilyang Pilipino Program (4Ps) and Social

Amelioration Program were the most cited government support received by these firms.

290% 10% 20% 30% 40% 50%

Others

Training: business skills

Wage subsidies

Regulatory relief

Credit mediation and refinancing

Deferral or loan payments

Deferral or reduction of rent, mortgage, orutilities

New loans with subsidized interest rates

Cash transfer

Government support received by firms (% of firms)

0% 5% 10% 15% 20% 25% 30%

Region 16: BARMM (formerly ARMM)Region 15: CAR

Region 13: CaragaRegion 12: SOCCSKSARGEN

Region 11: DavaoRegion 10: Northern Mindanao

Region 9: Zamboanga PeninsulaRegion 8: Eastern VisayasRegion 7: Central Visayas

Region 6: Western VisayasRegion 5: Bicol

Region 4B: MIMAROPARegion 4A: Calabarzon

Region 3: Central LuzonRegion 2: Cagayan Valley

Region 1: IlocosNational Capital Region

All locations

Firms that received government support (% of firms)

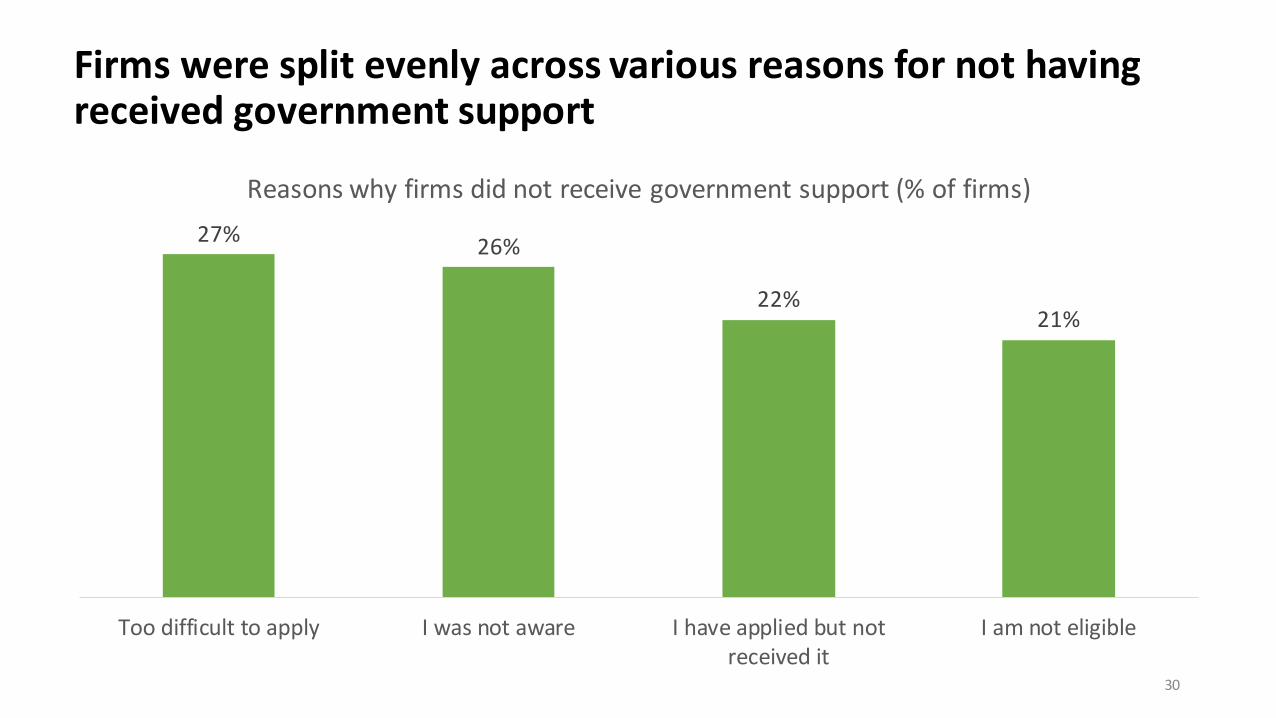

Firms were split evenly across various reasons for not having received government support

30

27% 26%

22%21%

Too difficult to apply I was not aware I have applied but notreceived it

I am not eligible

Reasons why firms did not receive government support (% of firms)

Liquidity improving measures are the most desired government support

31

6%

4%

8%

9%

9%

10%

14%

15%

19%

22%

22%

36%

46%

Others

Tax deferral

Training: digital skills

Improved public transportation services

Training: business skills

Wage subsidies

Regulatory relief

Credit mediation and refinancing

Deferral or loan payments

Deferral or reduction of rent, mortgage, or utilities

Tax exemptions or reductions

New loans with subsidized interest rates

Cash transfer

Government support desired by firms (% of firms)

Effort should be concentrated on re-establishing demand, supply, and financial channels and helping firms adjust to the normal by improving firm capabilities.

• The Government of the Philippines is currently considering additional measures to further support the Philippine firms through tax reductions and expanding access to new loans.

• Future government support should also note that the new normal is characterized by high uncertainty, which can make access to finance programs less effective as firms are less willing to borrow, and banks are hesitant to lend.

• Clear communications and consistent messaging about community quarantine measures on business operations in a timely manner will be crucial to reduce firms’ uncertainties about the future.

32

Annexes

33

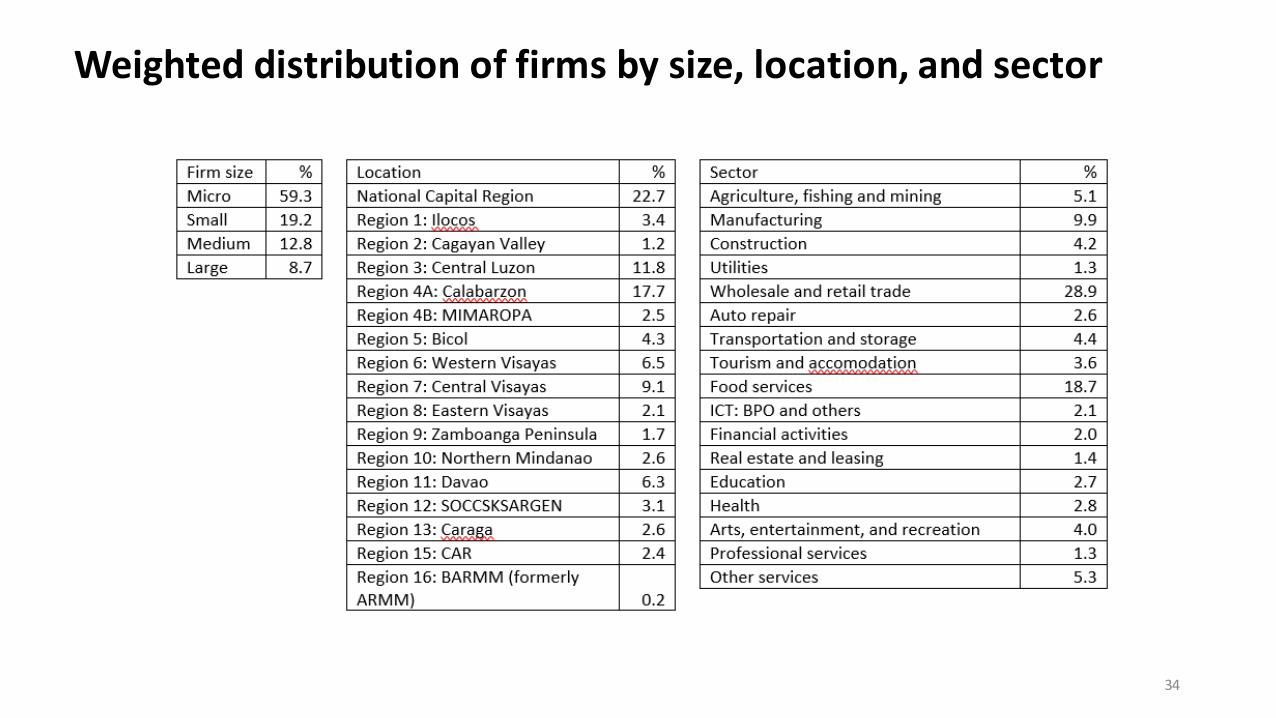

Weighted distribution of firms by size, location, and sector

34

Government support measures that were available to firms as of July 2020• Cash transfers: Pantawid Pamilyang Pilipino Program (4Ps) and Social Amelioration Program (SAP)

• Deferral or reduction of rent, mortgage, or utilities: DTI’s rent deferment grace period

• Deferral of credit payments, suspension of interest payments, or rollover of debt: grace period for loans

• Access to loans with subsidized interest rates: DTI/SB Corp’s P3-ERF / Covid-19 Assistance to Restart Enterprises (CARES) program, Landbank’s I-RESCUE Lending, DA-ACPC’s Plant Plant Plant under SURE Aid program, PhilGuarantee’s loan guarantee

• Credit mediation and refinancing: Landbank’s I-RESCUE Lending

• Wage subsidies: DOF’s Small Business Wage Subsidy (SBWS)

• Support programs related to business advisory, education, and training for entrepreneurship and SMEs: DTI’s Livelihood Seeding Program – Negosyo Sa Barangay

• Regulatory relief: suspended, reduced, or waived fees and payments for licensing, registration, permits and inspection, DOLE’s labor regulation adjustments

35

Acknowledgement

The note was prepared by the World Bank team led by Sharon Piza (Economist, EEAPV), comprising of Jin Lee (Private Sector Specialist, ETIFE), Rong Qian (Senior Economist, EEAM2), and Yoonyoung Cho (Senior Economist, HEASP). The survey is a component of the Real Time Monitoring of COVID-19 Impacts in the Philippines Project supported by the Australian Government. Survey implementation and data processing was supported by the Department of Finance (DOF), National Economic Development Authority (NEDA), National Telecommunications Commission (NTC), along with Gio Santos and Rina Gonzalez (Consultants, EEAPV). The survey design, implementation, and results analysis received the guidance of Cecile Niang (Practice Manager, EEAF2) and Rinku Murgai (Practice Manager, EEAPV), with inputs from Asya Akhlaque (Lead Economist, EEAF2), Leonardo Iacovone (Lead Economist, ETIFE), Shawn Tan (Senior Economist, EEAF1), Trang Tran (Senior Economist, ETIFE), Jaime Frias (Senior Economist, EEAF2), Clarissa C. David (Senior External Affairs Officer, ECREA) and David Llorito (External Affairs Officer, ECREA).

For more information, please contact Sharon Piza ([email protected]) and Jin Lee ([email protected]).

36