Embed Size (px)

DESCRIPTION

A research paper on the affect of GST in Malaysia

Citation preview

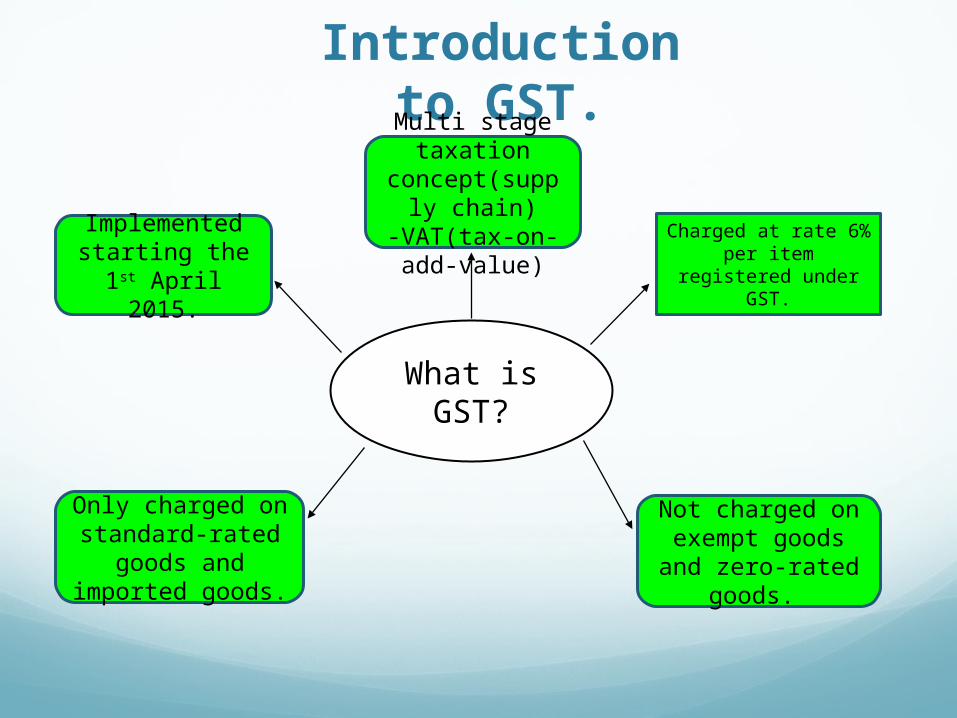

Introduction to GST.

Charged at rate 6% per item registered

under GST.

What is GST?

Multi stage taxation

concept(supply chain)

-VAT(tax-on-add-value)

Implemented starting the 1st

April 2015.

Only charged on standard-rated goods and imported goods.

Not charged on exempt goods and zero-rated goods.

How GST works in the supply chain…..

The difference between GST and SST.

Single versus multiple stage of taxation.

Goods and Services subjected to tax.

Tax payment and accounting period.

Imported services and intangibles.

Why is GST better than SST?More comprehensive - GST does not inherent weaknesses

under the present tax system.Exp :cascading tax, double tax

More effective - increase tax compliance thus easier to administer.

More transparent - All records and documents related to the business are only kept by the GST auditor in the business premise.

Why does the government wants to implement GST

now

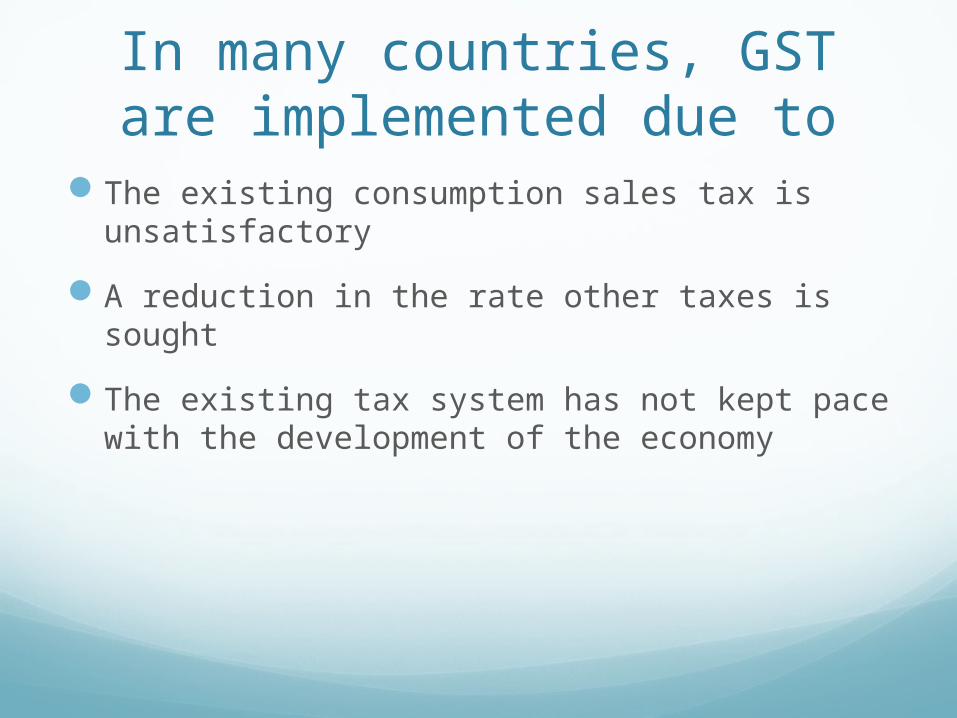

In many countries, GST are implemented due to

The existing consumption sales tax is unsatisfactory

A reduction in the rate other taxes is sought

The existing tax system has not kept pace with the development of the economy

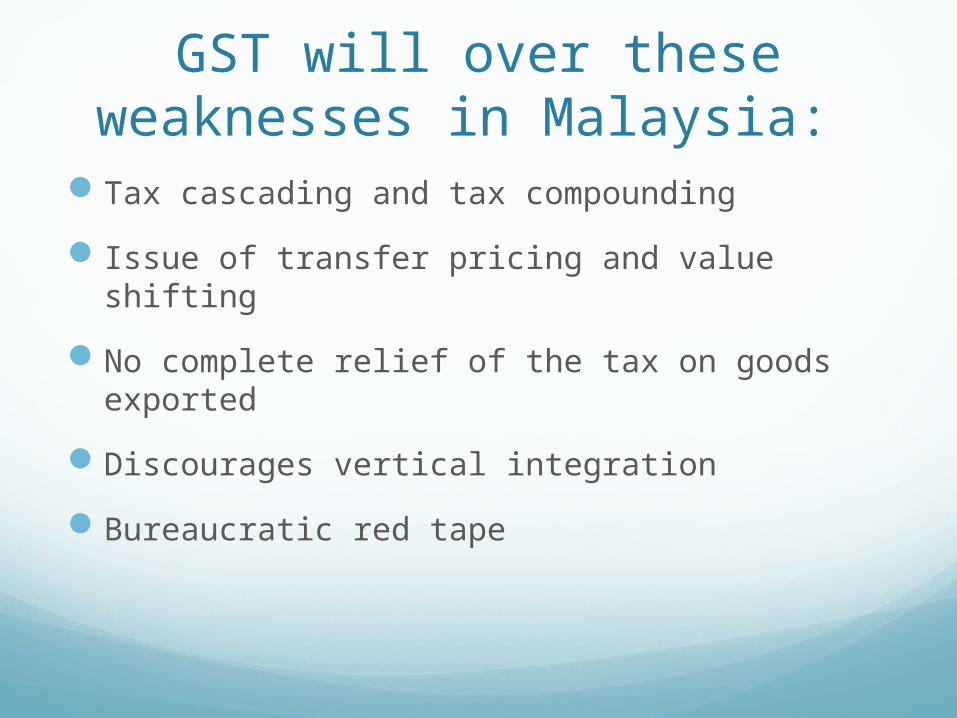

GST will over these weaknesses in Malaysia:

Tax cascading and tax compounding

Issue of transfer pricing and value shifting

No complete relief of the tax on goods exported

Discourages vertical integration

Bureaucratic red tape

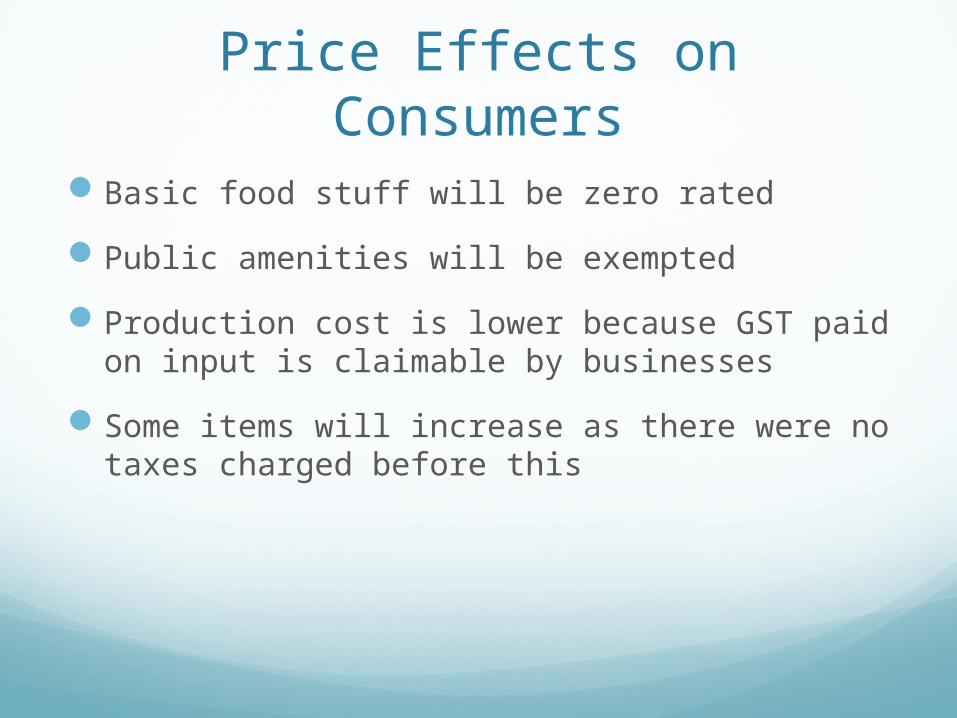

How does GST affect Malaysian Consumers

Price Effects on ConsumersBasic food stuff will be zero rated

Public amenities will be exempted

Production cost is lower because GST paid on input is claimable by businesses

Some items will increase as there were no taxes charged before this

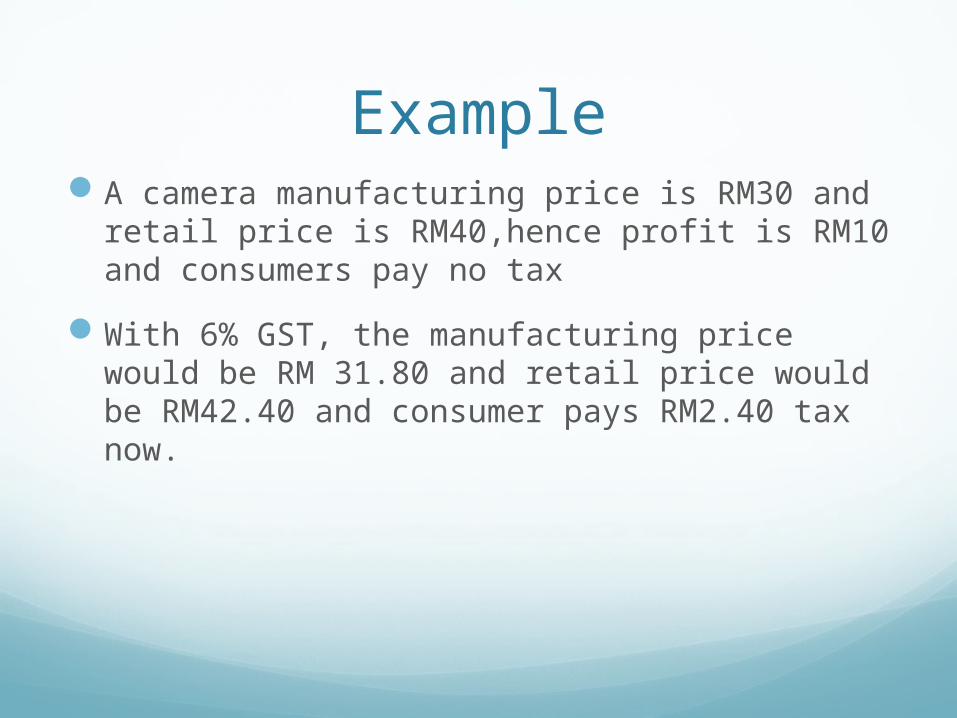

ExampleA camera manufacturing price is RM30 and

retail price is RM40,hence profit is RM10 and consumers pay no tax

With 6% GST, the manufacturing price would be RM 31.80 and retail price would be RM42.40 and consumer pays RM2.40 tax now.

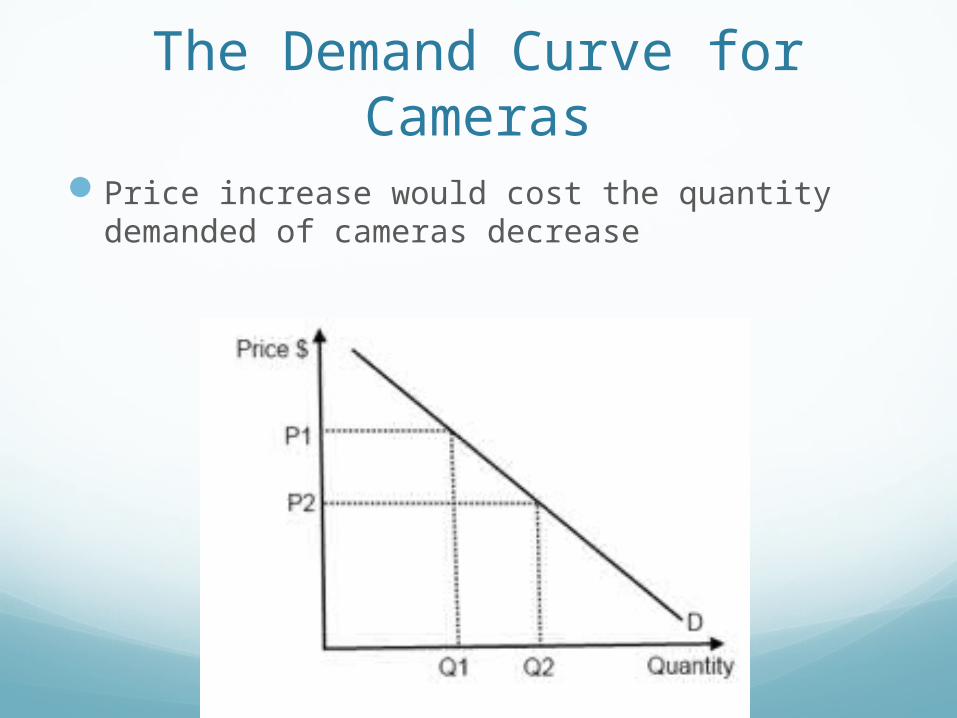

The Demand Curve for Cameras

Price increase would cost the quantity demanded of cameras decrease

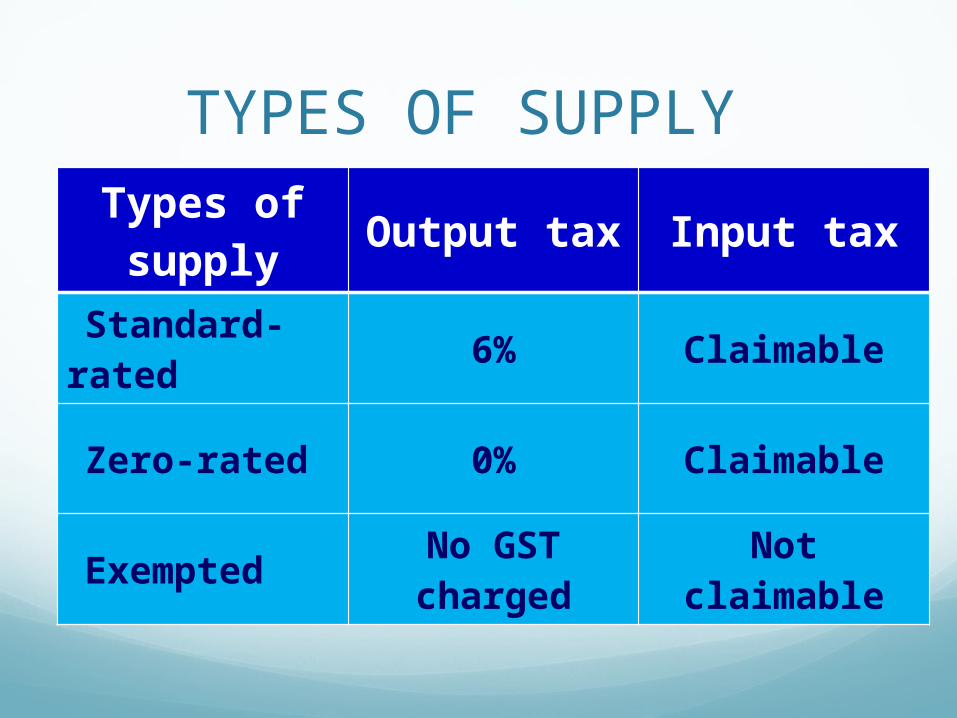

TYPES OF SUPPLY

Types of supply Output tax Input tax

Standard-rated 6% Claimable

Zero-rated 0% Claimable

Exempted No GST charged Not claimable

STANDARD RATED

Manufacturer claims back GST on input

Consumer pays

6%GST only

Wholesaler claims back

GST on input

Retailer claims back

GST on input

Manufacturer

Wholesaler

Retailer Consumer

GST AT 6%

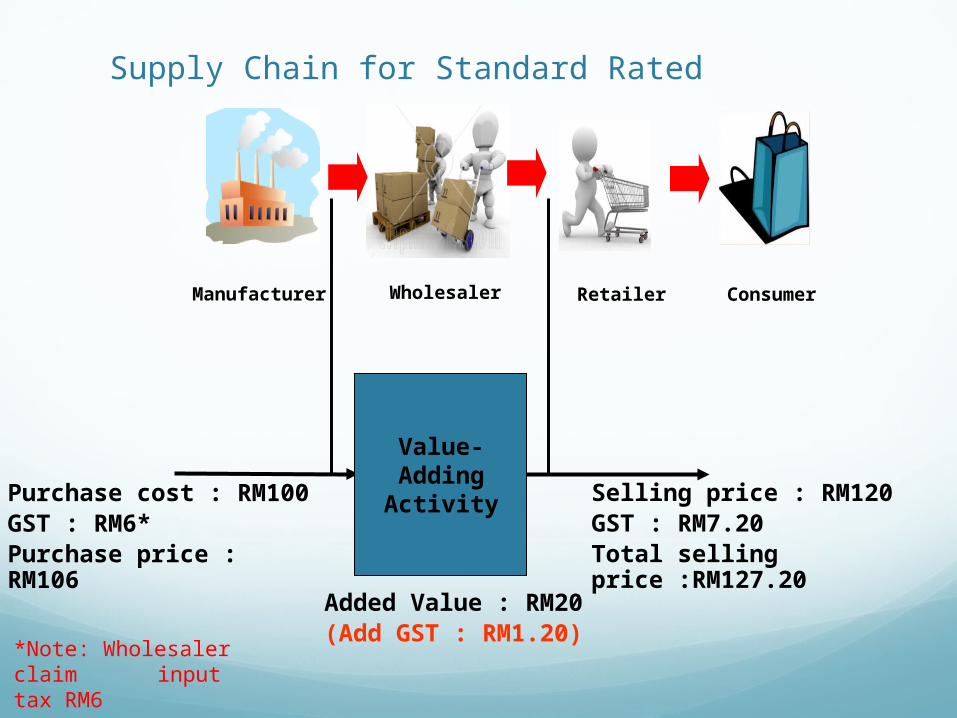

Supply Chain for Standard Rated

Selling price : RM120GST : RM7.20Total selling price :RM127.20

Purchase cost : RM100GST : RM6*Purchase price : RM106

Manufacturer Wholesaler

Retailer Consumer

*Note: Wholesaler claim input tax RM6

Value-Adding Activity

Added Value : RM20(Add GST : RM1.20)

EXAMPLES

Standard Rate

6%

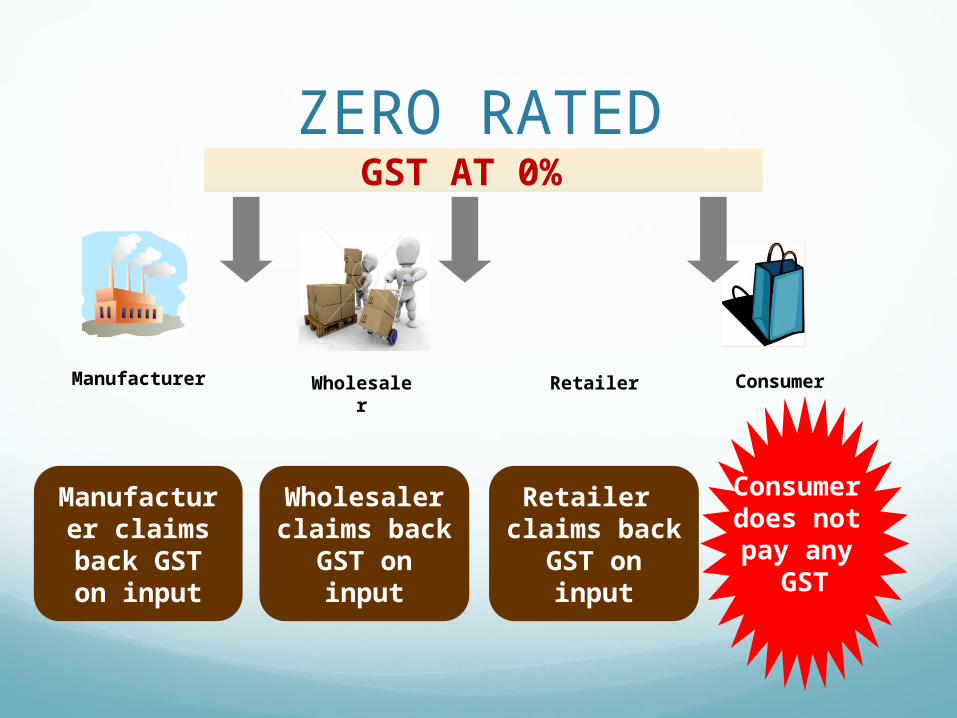

ZERO RATED

Manufacturer claims back GST on input

Consumer does not pay any

GST

Wholesaler claims back

GST on input

Retailer claims back

GST on input

Manufacturer

Wholesaler

Retailer Consumer

GST AT 0%

Selling price : RM120GST : RM0Total selling price :RM120

Purchase cost : RM100GST* : RM0Purchase price : RM100

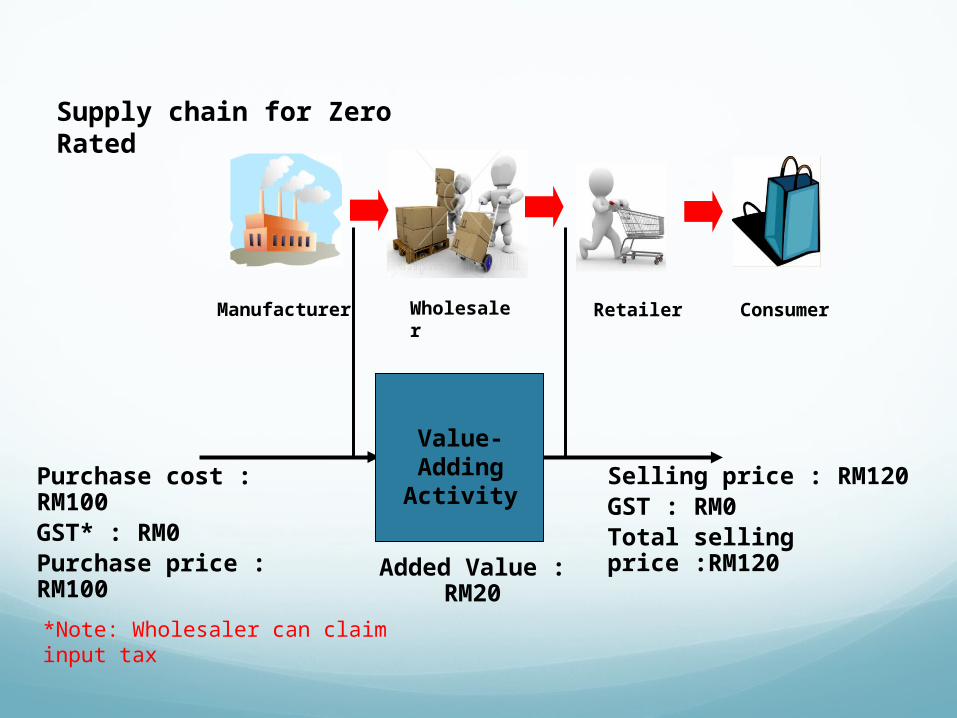

Supply chain for Zero Rated

Manufacturer Wholesaler

Retailer Consumer

*Note: Wholesaler can claim input tax

Value-Adding Activity

Added Value : RM20

Examples of Zero Rated

0%

First 300 units of electricity per month for

domestic use only

Exported goods and services

Infant milk

Water for domestic use only

EXEMPT SUPPLY

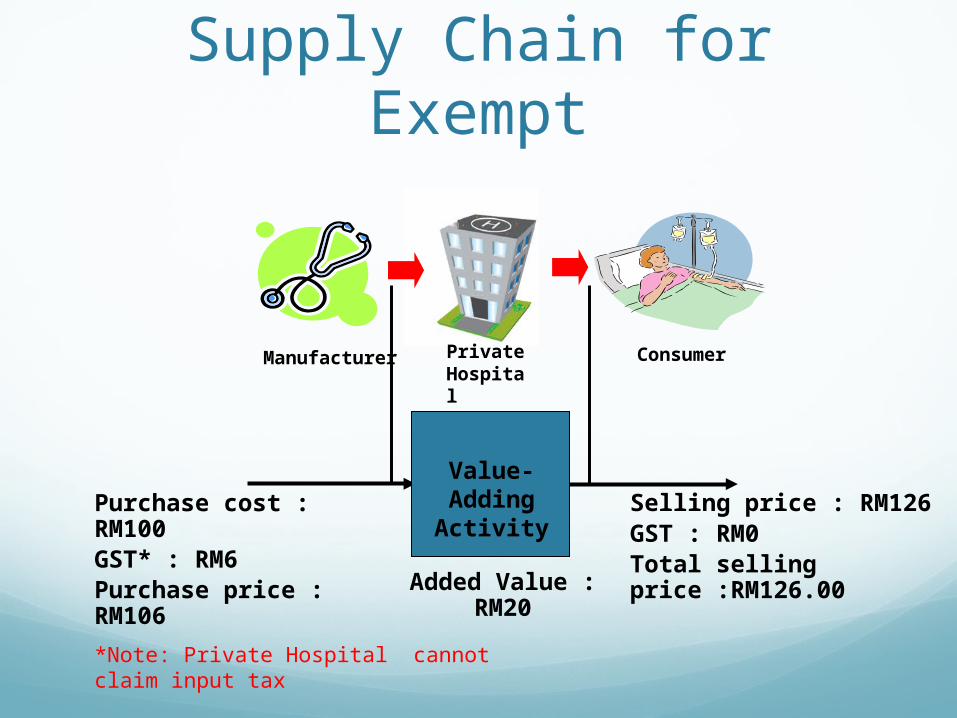

Supplier Private hospital Consumer

Supplier claims tax

paid on input

Private hospital cannot

claim tax paid on input

No GST imposed on the supply to consumer

GST AT 6 % NO GST

Supply Chain for Exempt

Selling price : RM126GST : RM0Total selling price :RM126.00

Purchase cost : RM100GST* : RM6Purchase price : RM106

Manufacturer

Private Hospital

Consumer

*Note: Private Hospital cannot claim input tax

Value-Adding Activity

Added Value : RM20

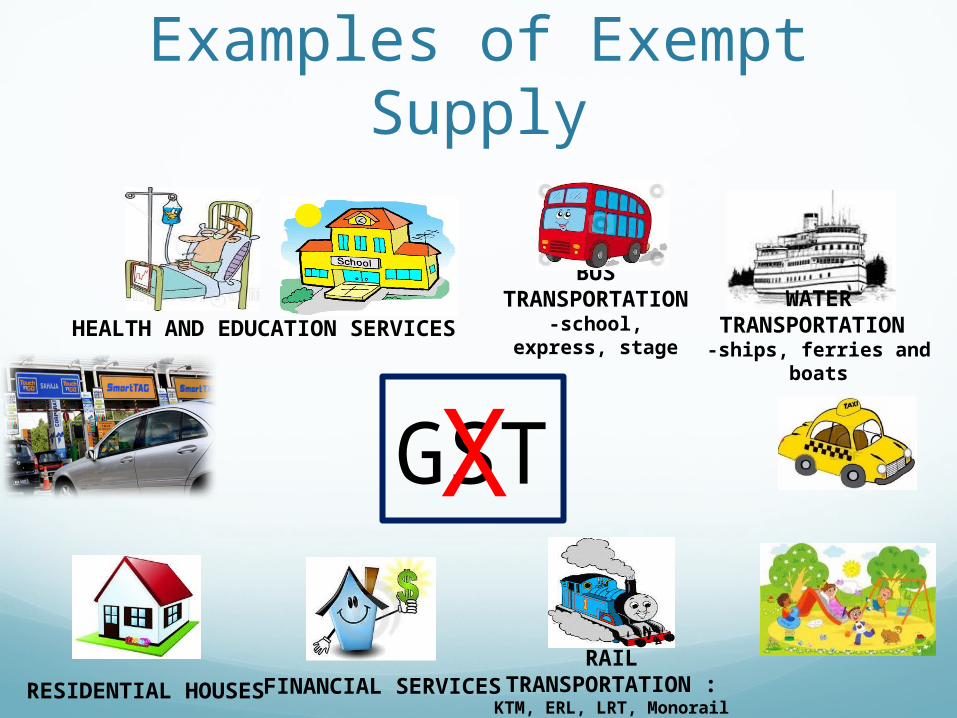

Examples of Exempt Supply

RAIL TRANSPORTATION :KTM, ERL, LRT, Monorail

BUS TRANSPORTATION

-school, express, stage

RESIDENTIAL HOUSES FINANCIAL SERVICES

HEALTH AND EDUCATION SERVICES

GSTXWATER TRANSPORTATION

-ships, ferries and boats

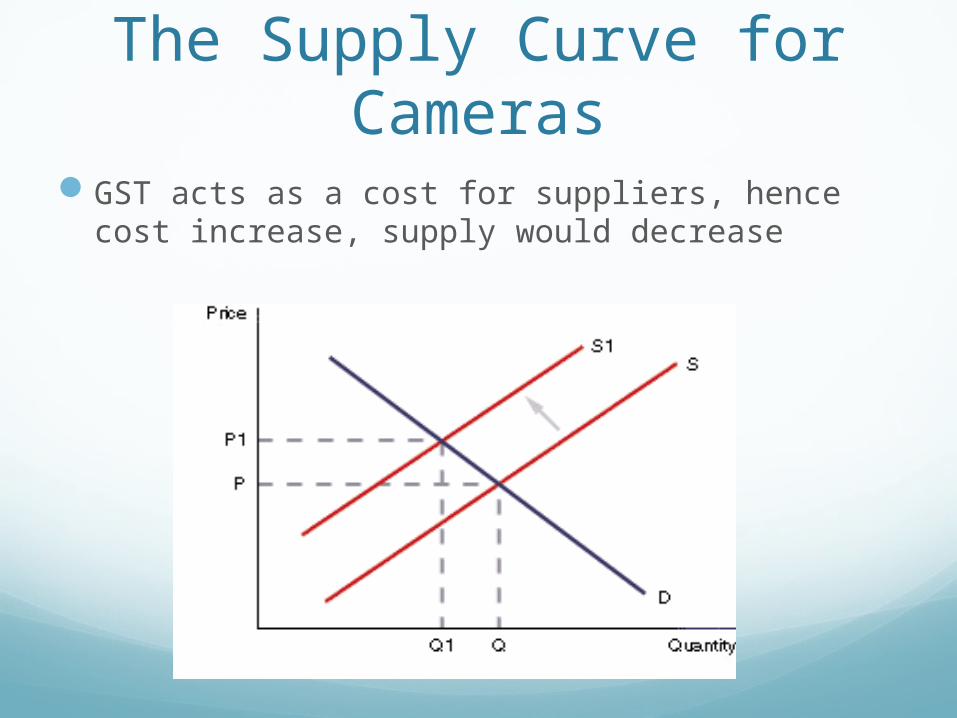

What is the effect on Supply Curve

The Supply Curve for Cameras

GST acts as a cost for suppliers, hence cost increase, supply would decrease

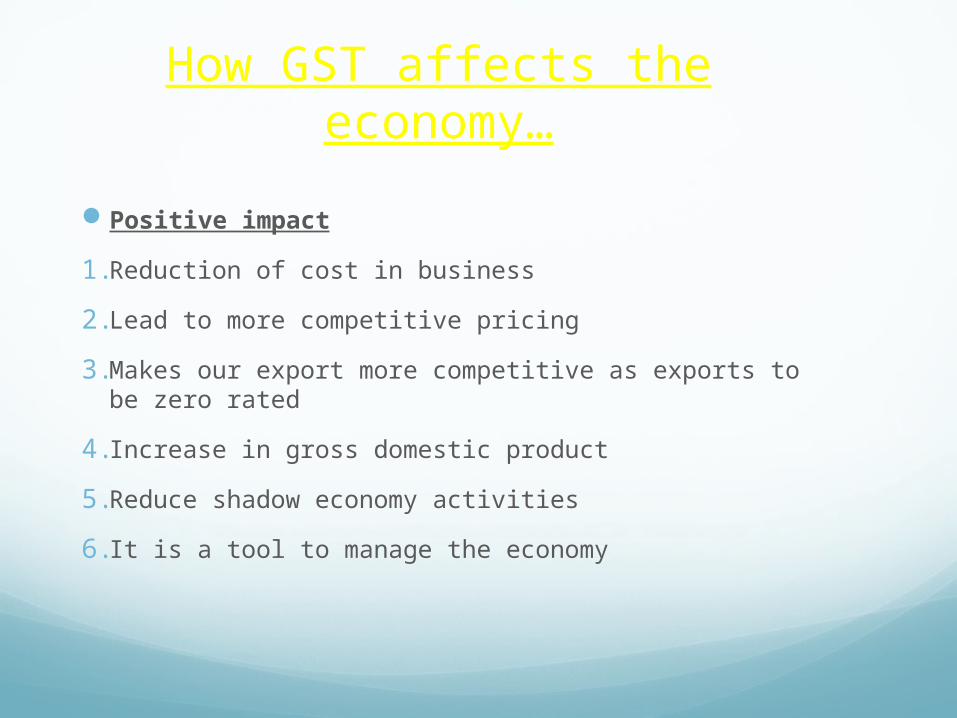

How GST affects the economy…

Positive impact

1. Reduction of cost in business

2. Lead to more competitive pricing

3. Makes our export more competitive as exports to be zero rated

4. Increase in gross domestic product

5. Reduce shadow economy activities

6. It is a tool to manage the economy

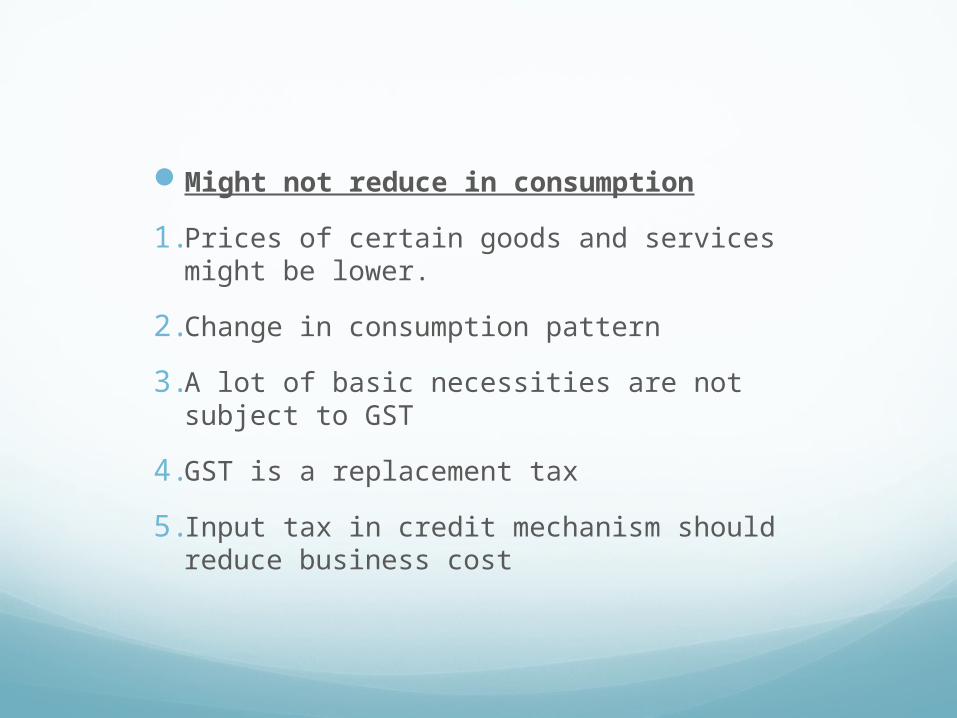

Might not reduce in consumption

1. Prices of certain goods and services might be lower.

2. Change in consumption pattern

3. A lot of basic necessities are not subject to GST

4. GST is a replacement tax

5. Input tax in credit mechanism should reduce business cost

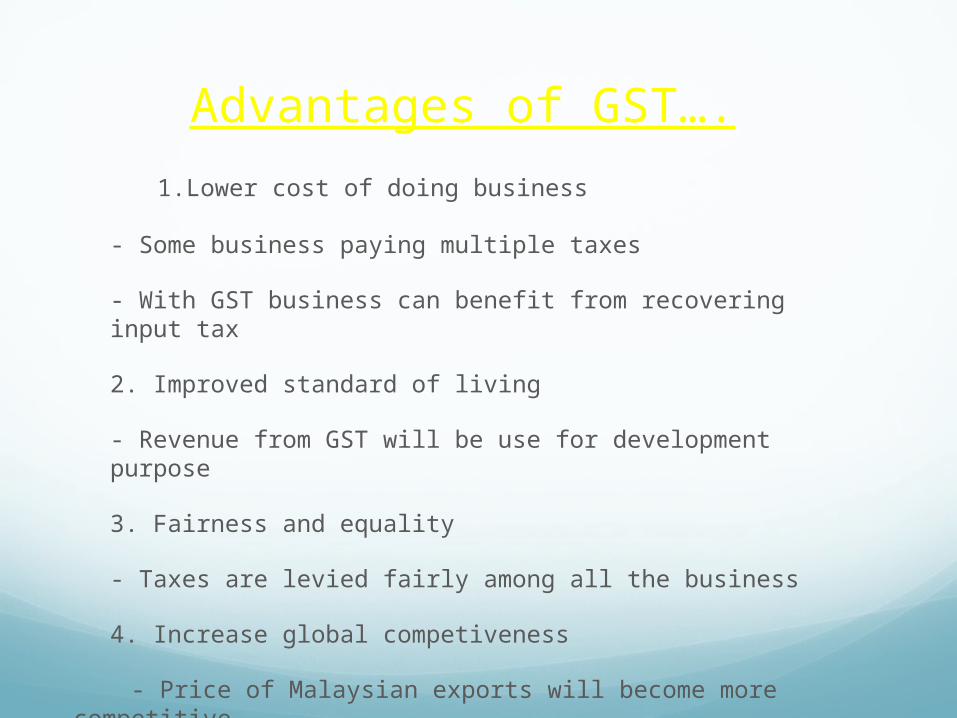

Advantages of GST….

1.Lower cost of doing business

- Some business paying multiple taxes

- With GST business can benefit from recovering input tax

2. Improved standard of living

- Revenue from GST will be use for development purpose

3. Fairness and equality

- Taxes are levied fairly among all the business

4. Increase global competiveness

- Price of Malaysian exports will become more competitive

on the global stage.

5. Fair pricing

- GST eliminate double taxation under SST.

Disadvantages of GST….

1. low and middle income group will be affected badly

- When prices of some good go up and money will be the major issue for the specific group

2. There isn't any assurance that the price of good and

services will increase

- Government are helpless in controlling price of essential

items.

Conclusion ….

As a conclusion, the overriding rationale to introduce the GST is to modernise our tax system and to overcome the inefficiency of the indirect tax system in the country.

From the studies done by the Ministry of finance and Customs, it is evident that zero-rating and exempting has made the Malaysian model a progressive one rather than a regressive one.

GST based on spending. If the spending is higher, then tax charged will be more. Some items may be slightly more expensive and cheaper.

Furthermore, government income will increase. This will enable further development and budget control to the country, other than relying just on petroleum or income tax revenues.

Even though, government introduce GST they are always there to help low-income people by designed a compensation packages to offset any additional tax burden.