Embed Size (px)

Citation preview

Implementing ERM, Solvency II and Capital

The Actuarial Society of Hong Kong

Eberhard Mueller, Chief Risk Officer

6th May, 2013

2

Overview

• Risk and governance – the pillar II requirements

– Organisational requirements

– Basic documents / Strategic framework

– Communication and enforcement

• Capital requirements

– Internal Model vs. Standard Formula

– Global Reinsurer vs. Life Insurer

– Impact of reinsurance

3

Solvency II - More than "just" new capital requirements

Solvency II -The three pillars

Capital and Resources

Solvency / minimum capital requirement (SCR/MCR)

Available financial resources

Standard and internal model

Internal controls and risk management

Internal risk assessment

Supervisory activities

Reporting and Transparency

Supervisory reporting

Public disclosure

Market discipline

Risk and Control

4

Risk Management requirements

(MaRisk)

Solvency IISupervisory Framework

(effective 2016/7?)

Insurance Supervision Act (VAG)Qualitative Requirements based on Pillar II

(Risk Reporting and sound management)

(effective since 1.1.2008 / transition period

until 31.12.2008)

Minimum requirements on risk management (MaRisk)Overarching set of qualitative

requirements based on VAG

(effective from 3/2009)

Enterprise Risk ManagementRisk Management Framework

Strategic principles

5

German MaRisk (VA): Separation of tasks required

• German "advanced" Pillar II introduction: MaRisk1)

– Minimum requirements for the risk management of insurance undertakings

– Valid from 2009

• Principle based requirements

– Strategic Framework

– Organisational Framework

– Internal Steering and Control System: ISCS2)

• Organisational Framework: Clear separation required between:

– Units responsible for "creating and reporting profits and losses"

• Underwriting

• Accounting

– Independent risk controlling function

• Quantitative Risk Management

• Qualitative Risk Management

– Process independent internal auditing

6

General structure

Overall responsibility of the board

Process independent control

(on behalf of board)

"controls"

Steering / P&L responsibility

(incl. controls within processes)

"monitors"

Risk monitoring

(independent risk control function within processes)

Auditing

CROBusiness-

segment

Risk

Committee

steering

Unit

Board

Supported by

Controlling

et.al.

supported by

(Risk Mgmt.)

et.al..RISK

7

Centralized Group Risk Management

� CEO (Chair)� CFO� COO Life� COO Non-Life � CRO� Chief Controller � Chief Auditor (guest)

Risk hierarchy

1. Reserving risk

2. Exposure risk

3. Mispricing risk

4. Asset risk

5. Operational risks

Group Risk Management headed by Chief Risk Officer

Executive Board

Group Auditing

Internalcontrol system

Quantitativerisk management

(DFA-Model)

Qualitativerisk management

(Risk Cockpit)

Group Risk Committee RC

8

The "Blue" and the "Yellow"

... Segregation of Tasks (MaRisk) compatible with "Lines of Defence"

Internal Audit

Board

Risktaker

Independent Risk-Con-

trolling Function (IRCF)

First line of defence Second line of defence

Third line of defence

9

Functions according to Solvency II Framework Guideline

... Actuarial Function in both "lines of defence"

Board

Actuarial

Function

Internal Audit

Risktaker

Independent Risk-Con-

trolling Function (URCF)

e.g.

Reserving

e.g.

Pricing

10

Level 2 Implementing Measures (Draft): 4 Functions!!!

... Risk Management, Actuarial, Compliance and Audit Function

11

BUT: Segregation of 4 functions!

... Risk Management, Actuarial, Compliance and Audit Function

12

Segregation according to Implementing Measures

More colours occur ...

Board

Compliance FunctionActuarial Function

Internal Audit

Risktaker Independent Risk-Con-

trolling Function (IRCF)

13

Compliance Evolution … it´s getting sharky

Actuarial

Function

Risk

Management

Function

Audit

Function

Compliance

Function ?U/W

14

Risk Management requirements

(MaRisk)

Solvency IISupervisory Framework

(effective 2016/7?)

Insurance Supervision Act (VAG)Qualitative Requirements based on Pillar II

(Risk Reporting and sound management)

(effective since 1.1.2008 / transition period

until 31.12.2008)

Minimum requirements on risk management (MaRisk)Overarching set of qualitative

requirements based on VAG

(effective from 3/2009)

Enterprise Risk ManagementRisk Management Framework

Strategic principles

15

Strategic principles

16

• Corporate Strategy

– Strategic objectives (already addressing risk management)

• Risk Strategy

– Overriding Objective

– Ten Principles

• Risk Management Framework Guideline

– Overarching rules for group wide risk management

– Principle oriented framework with room for local fitting

• System of Limits and Thresholds

– Warning and escalating ladder

– Risk categories according to Risk Register

Strategic principles

17

All starts with the Corporate Strategy

... Basis for Value Creation

• Our mission: "Growing Hannover Re profitably"

• We seek to strengthen and further

expand our position as a leading,

globally operating reinsurance group,

delivering profitability that is above the

average of the sector.

• We are passionate about reinsurance

and chart our own course. We are quick,

flexible and independent; striving for

excellence in our actions. We aspire to

be the best option for our business

partners when it comes to choosing a

reinsurance provider.

18

1. Our business model

2. We have ambitious profit and growth targets

3. We manage risks actively

4. We are a preferred business partner

5. We aim for successful employees

6. We maintain an adequate level of capitalisation

7. We strive for a stable investment income

8. We ensure a lean organisation

9. We are committed to sustained compliance

10. We strive for performance excellence

A corporate strategy with 10 strategic principles

19

Active Risk Management is 3rd strategic commandment

• In order to accomplish our business objectives, we enter into a broad range of

risks which – while offering opportunities for profit – can also have adverse

implications for the company.

• Risk management – in both quantitative and qualitative terms – is therefore of

vital importance. The foundation of our risk management strategy is our

Economic Capital Model. Based on this model we manage our risk exposure to

achieve a positive IFRS net income with a probability of XX%. We also ensure

that the probability of a complete loss of our economic as well as IFRS

shareholders' equity does not exceed 0.0Y% p.a..

• On this basis, our shareholders' equity is allocated to the individual areas of our

business activity with the aim of maximizing the risk-adjusted profits.

• The details of our risk management approach are set out in the Risk Strategy

which is approved and regularly reviewed by the Executive Board. In this regard

special importance is given to the initiative of the Chief Risk Officer.

20

The risk strategy reflects the segregation of tasks

21

• Our overriding objective

• The overriding objective of our risk management is to adhere to the strategically

defined risk positions of the Hannover Re Group: The expected return on equity

after tax shall be at least ZZZ basis points above the risk-free interest rate.

• Occurrence of a net loss under IFRS (return on equity less than or equal to 0) with

a recurrence period of maximum once in AA years.

• Complete loss of IFRS shareholders' equity with a probability of less than 0.0Y %

p.a.

• In this context a capitalisation that ensures the 3 following conditions is absolutely

indispensable:

– The target rating (Example: "AA-" from Standard & Poor's, "A+" from A.M. Best)

– Regulatory Solvency Ratio: Solvency Ratio >100%

– Probability of economic ruin < 0.0Y% p.a.

Our overriding objective

22

Our risk conception

• Overriding Objective

– Adhere to risk positions

• Risk Conception

– Holistic

23

Risk management framework guideline

24

Risk management framework guideline

25

• Explain rationale for ERM

– External requirements (supervisors, rating agencies)

– Internal motivation (contribution to value creation)

– Necessary organisational platform (segregation of tasks)

• Explain basic documents and their strategic embedding

– Point of departure: corporate strategy

– Risk strategy

– Risk management framework guideline (incl. tasks and responsibilities)

– System of limits and thresholds (Overview)

– Specific guidelines (e. g. BCM, IS, DQM)

• Compare group situation with local situation

– Supervisory environment

– Business risk environment

• Agree on to do´s

– Local vs. central ERM responsibility (local CRO? Local Risk Committee?)

– Reporting lines, reporting formats (incl. ad hoc reporting)

Risk communication throughout the entire organisation

26

Challenge for HR: covering presence in all 5 continents

Content

27

Hannover Re´s Risk Management Roll-Out

• HR Roll out of risk management system in local offices (Life and Non-Life) from

June 2010 through August 2011:

– 10 subsidiaries: Ireland (2), UK (2), Bermuda (2), South Africa (2), USA (1), Australia (1)

– 7 branches: Australia, Canada, China, France, Korea, Malaysia, Sweden

• Roll out at smaller entities in May-June 2012:

– Hong Kong, Bogota, HR Bahrain (+ branch),

• Implementation of organisational features at subsidiary level:

– Position of a Chief Risk Officer or of a risk monitoring responsible

– Reporting dotted line to Group CRO

– Implementation of a risk committee

– CRO or head of central RM unit is usually guest or member of local risk committees

28

Solvency II - More than "just" new capital requirements

... but of course they are there, too ...

Solvency II -The three pillars

Capital and Resources

Solvency / minimum capital requirement (SCR/MCR)

Available financial resources

Standard and internal model

Internal controls and risk management

Internal risk assessment

Supervisory activities

Reporting and Transparency

Supervisory reporting

Public disclosure

Market discipline

Risk and Control

29

From standard to individual company implementation

Capital requirements and treatment of reinsurance

• Standard model with simplifications

• Standard model

• Standard model and undertaking specific parameters

• Standard model and partial internal model

• Full internal model

• Standard risk profile• Inadequate recognition of reinsurance

• Individual risk profile • Appropriate recognition of reinsurance

Incre

asin

g c

om

ple

xity a

nd ris

k-s

ensitiv

ity

30

Hannover Re will apply for internal model approval

Convergence of internal and external requirements?

Standard Model

•Value-at-Risk at 99.5% confidence level

•Scenario based approach

•Predefined risk categories - not tailored to the company's individual risk profile

•Calibration of risk factors based on "average company"

•"Average company" correlation structure

•Adequate for small companies without complex or highly unique risks

•Limited resource requirements

•Limited suitability for risk management and business decision purposes (just external reporting)

Internal Model

•Full distribution of capital requirements

•Stochastic modelling

•Quantitative modelling of all material risk categories for Hannover Re

•Calibration of risk factors by company-specific data

•Company-specific dependency structure reflecting (worldwide) diversification effects adequately (e.g. catastrophe risk)

•Adequate for a Global Reinsurer and large multi-national insurers

•Gives important additional information for capital management and business decision purposes (internal and external reporting)

•Adequate integration into decision processes and risk management of the HR Group

31

• Hannover Re has engaged in 2008 with the German regulator to prepare Solvency

II pre-application for internal model approval

• Since then we have explained our approach to capital modelling in over 100

meetings to the regulator

– Coverage of all major areas of the model

– Coverage of all aspects of Pillar II

– Coverage of almost all EEA entities and one non-EEA entities � early engagement with

local regulators

• All areas where gaps had been identified in the review process have been

addressed in the past years. Currently, we are in the process of fine-tuning our

systems and processes, e.g. in the areas

– Own risk and solvency assessment (ORSA)

– Model validation

– Profit and loss attribution

– Legal entity reporting (in contrast to group reporting)

Internal model approval on track

32

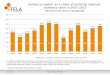

Hannover Re Group very well capitalised

Internal model results

Available capital and required risk capital* in EUR million 2012 2011

Underwriting risks in non-life reinsurance 3.340,0 3.048,3

Underwriting risks in life and health reinsurance 1.973,5 2.029,1

Market risks 2.943,2 1.992,2

Credit risks 671,8 569,4

Operational risks 404,0 408,6

Diversification effect (3.364,6) (2.562,9)

Total required capital 5.967,9 5.484,7

Available economic capital 10.379,7 8.758,7

Capitalisation ratio 173,9% 159,7%

33

Risk profiles

Market risk dominates

life insurers‘ risk profile

34

Risk profiles

Different levels of diversification

35

The (double) impact of risk mitigation

Substantial decrease

due to reinsurance Moderate increase

due to reinsurance

Moderate decrease

due to dominance of market risk

Substantial increase of own funds due to

lower risk margin***