Embed Size (px)

DESCRIPTION

Implications of the new “Fair Value” Standard. Guide to Valuation & Depreciation for the Public Sector. Standards. Decision Trees available from www.apv.net www.fairvaluepro.com.au. Issued late 2011 Applies for 1 Jan 2013 onwards Fair Value consistency across all standards - PowerPoint PPT Presentation

Citation preview

www.apv.net

David Edgerton FCPADirector

Quality + Expertise +Flexibility + Innovation =Confidence & Real Value

Implications of the new “Fair Value” Standard

www.apv.net

David Edgerton FCPADirector

Quality + Expertise +Flexibility + Innovation =Confidence & Real Value

Guide to Valuation & Depreciation for the

Public Sector

www.apv.net

Standards

Decision Trees available from

www.apv.netwww.fairvaluepro.com.au

www.apv.net

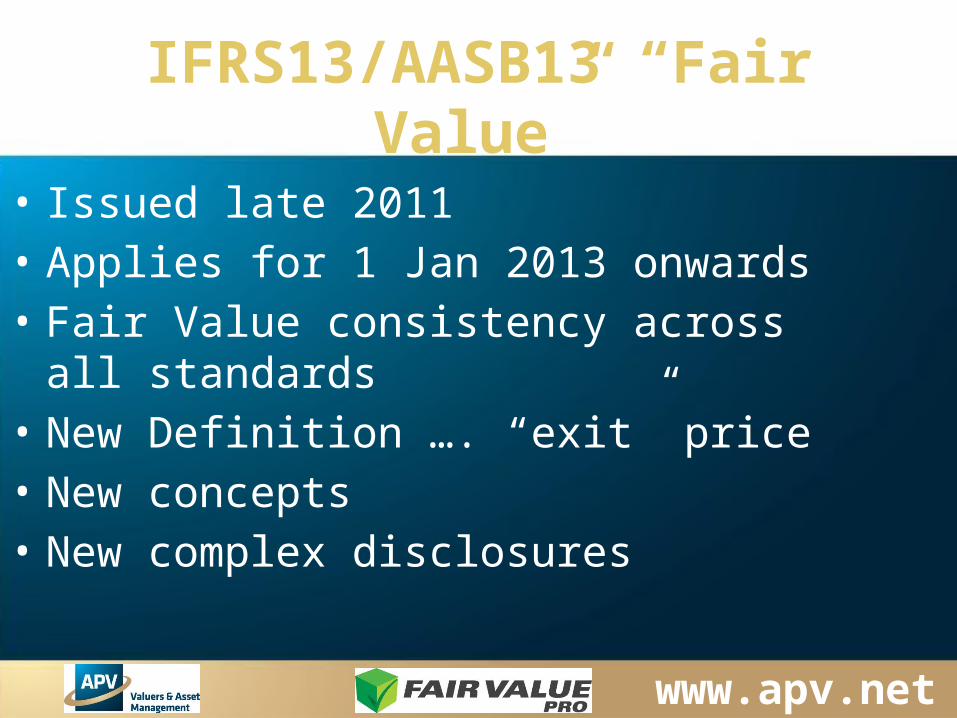

IFRS13/AASB13 “Fair Value”

• Issued late 2011• Applies for 1 Jan 2013 onwards• Fair Value consistency across all standards• New Definition …. “exit” price• New concepts• New complex disclosures

www.apv.net

Fair Value Definition

Will be: “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

Was: “the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction.”

www.apv.net

Residual Value Definition

Will be: “the amount an entity could receive for the asset currently (at the financial reporting date) if the asset were already as old and worn as it will be when the entity expects to dispose of it.”

Was: “is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.”

www.apv.net

New Concepts

• Hierarchy of Valuation Input– Level 1 (Quoted Price)– Level 2 (Observable Market Evidence)– Level 3 (Non-observable market evidence)

• Recurring v Non-Recurring Valuations

www.apv.net

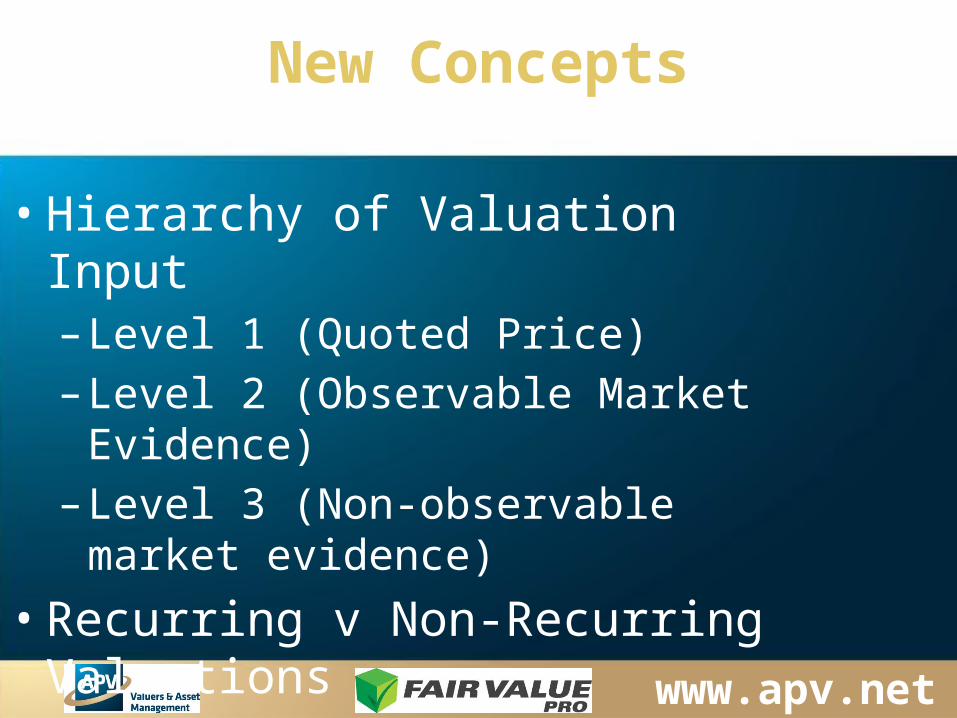

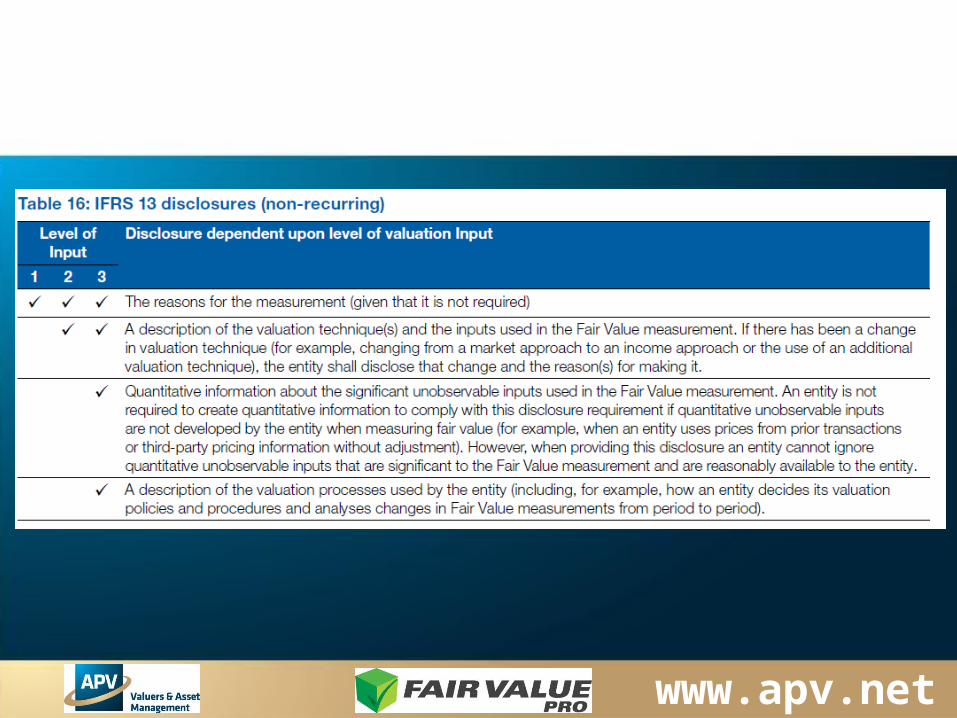

New Disclosure

• Dependent upon whether– Recurring or Non-Recurring valuation– Level of Valuation Input

www.apv.net

David Edgerton FCPADirector

Quality + Expertise +Flexibility + Innovation =Confidence & Real Value

www.apv.net

www.apv.net

www.apv.net

Draft CPA Guide, Tools & Help

APV website (www.apv.net)

Fair Value Pro websites (www.fairvaluepro.com.au)