Embed Size (px)

Citation preview

“IMPORTANCE OF DUE DILIGENCE

AND

FINANCIAL DUE DILIGENCE”

12th Nov 2011

- CA. SUJAL SHAH

Contents

� Meaning of Due Diligence Review (DDR)

� Scope of DDR

� Situations calling for DDR

� Types of DDRTypes of DDR

� Financial DDR

� Practical Situations

� Findings and their Impact

� Limitations

� Risks Involved and Steps to Mitigate

� Reporting

Meaning of DDR� Dictionary Meaning of ‘Due’ is ‘Sufficient’ & ‘Diligence’ is ‘Persistent effort or work’.

� It is an investigation into the affairs of an entity prior to its acquisition, flotation, restructuring or other similar its acquisition, flotation, restructuring or other similar transaction

� Due Diligence Review is a process whereby an individual or an organization seeks sufficient information about a business entity to reach an informed judgment as to its value for a specific purpose.

Due Diligence – What is it?� The process by which information is gathered

about:

√ A target Company

√ Its Business; and√ Its Business; and

√ The Environment in which the target company operates

� Objective:

√ To ensure that prospective investors make an informed investment decision

Due Diligence – What is it? (Cont)

� It is a business oriented analysis not an accountinganalysis

� A fact gathering exercise with focused analysis ofinformationinformation

� Understanding the industry of the target

� Reasonable level of enquiry into the affairs havingmaterial impact on the prospects of the business

� Evaluation of business model and key business practices

Scope of DDR� Scope is determined by the client.

� The degree of diligence required in any given review cannot be precisely defined.precisely defined.

� Purpose for review defines what is ‘due’ or ‘sufficient’ diligence.

� Extent of the review required is a judgment call.

� Engagement letter with the client is important.

Who conducts a DDR?� Chartered Accountants

� Investment Bankers

� Attorneys

� Lead & Co-Investors� Lead & Co-Investors

� Corporate Development Staff

Situations Calling for DDR� Firm considering a potentialacquisition

� Investment banker consideringunderwriting a public security

� Banker considering the grant of aloan

� Venture Capitalist considering anInvestment

� Seller of a business commissioning aDDR

� Lead Investment Banker in case ofIPO as per SEBI Norms

� Business Due Diligence

� Financial Due Diligence

� Legal Due Diligence

Types of DDR

� Legal Due Diligence

� Tax Due Diligence

� System Due Diligence

� Environmental Due Diligence

� Human Resource Due Diligence

9

“Financial due diligence has the highest significance –the finaldecision, for an investor, would be in the form of financial termsand information. It is therefore imperative that the results of allkinds of due diligence should be translated in monetary terms.”

Introduction to Financial DDR

10

• Identification of hidden risks & deal breakers

• Ensuring that all liabilities, current and contingent, are considered

• Establishing price adjustments / negotiation extent of dependency oncustomers and vendors

• Off balance sheet financing

• Identification of specific indemnities & warranties required fromtarget

� Buy Side• Due Diligence commissioned by the acquirer

• Focused on areas of interest for potential acquirer

• Reporting – generally issue based

Types of Financial DDR

• Reporting – generally issue based

• Dataroom < > exclusive

� Sell Side (Vendor DD)• Independent due diligence commissioned by the vendor

• Key tool for maximising saleability of the business in a reduced timetable

• To identify potential issues and take corrective measures upfront

11

� Limited• Focus on certain key areas based on the level of comfort desired by

the Client

� Full Scale

Types of Financial DDR

� Full Scale• Focus on all major aspects of financial statements

• Extent of detail is more as compared to limited due diligence

It is important to know what’s driving value for your clients

12

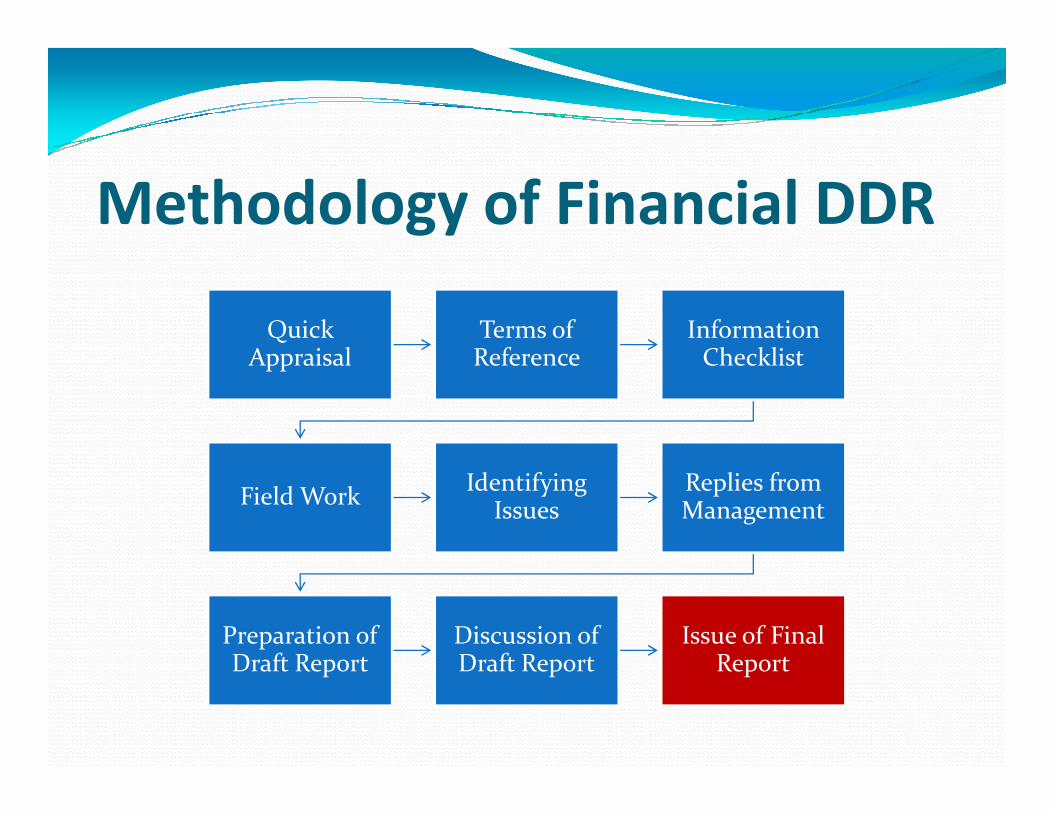

Methodology of Financial DDR

Quick Appraisal

Terms of Reference

Information Checklist

Field WorkIdentifying

IssuesReplies from Management

Preparation of Draft Report

Discussion of Draft Report

Issue of Final Report

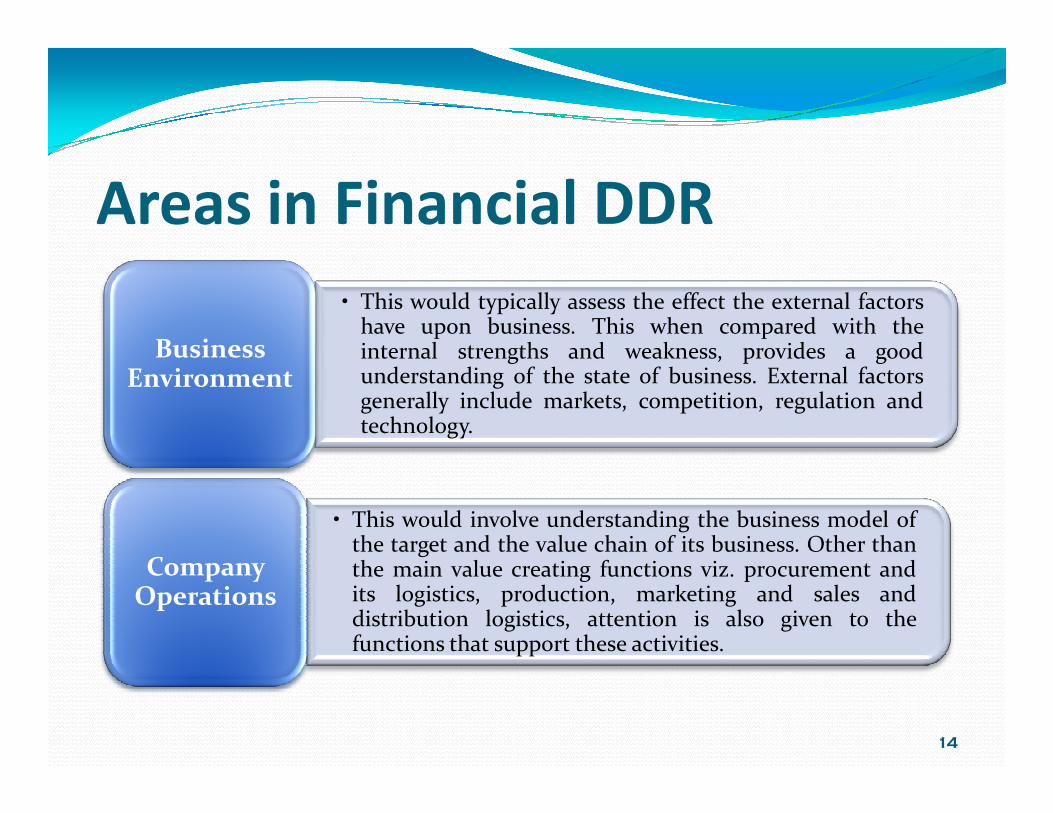

Areas in Financial DDR

• This would typically assess the effect the external factorshave upon business. This when compared with theinternal strengths and weakness, provides a goodunderstanding of the state of business. External factorsgenerally include markets, competition, regulation and

Business Environment

14

generally include markets, competition, regulation andtechnology.

• This would involve understanding the business model ofthe target and the value chain of its business. Other thanthe main value creating functions viz. procurement andits logistics, production, marketing and sales anddistribution logistics, attention is also given to thefunctions that support these activities.

Company Operations

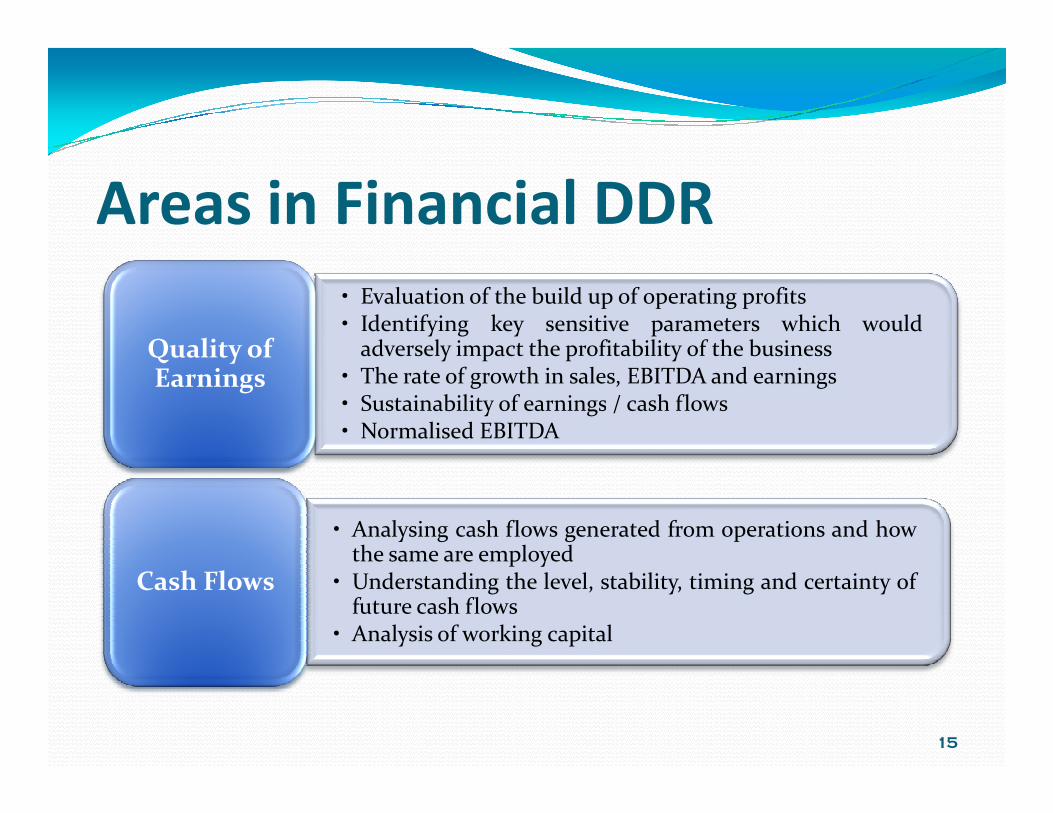

Areas in Financial DDR

• Evaluation of the build up of operating profits• Identifying key sensitive parameters which would

adversely impact the profitability of the business• The rate of growth in sales, EBITDA and earnings• Sustainability of earnings / cash flows

Quality of Earnings

15

• Sustainability of earnings / cash flows• Normalised EBITDA

• Analysing cash flows generated from operations and howthe same are employed

• Understanding the level, stability, timing and certainty offuture cash flows

• Analysis of working capital

Cash Flows

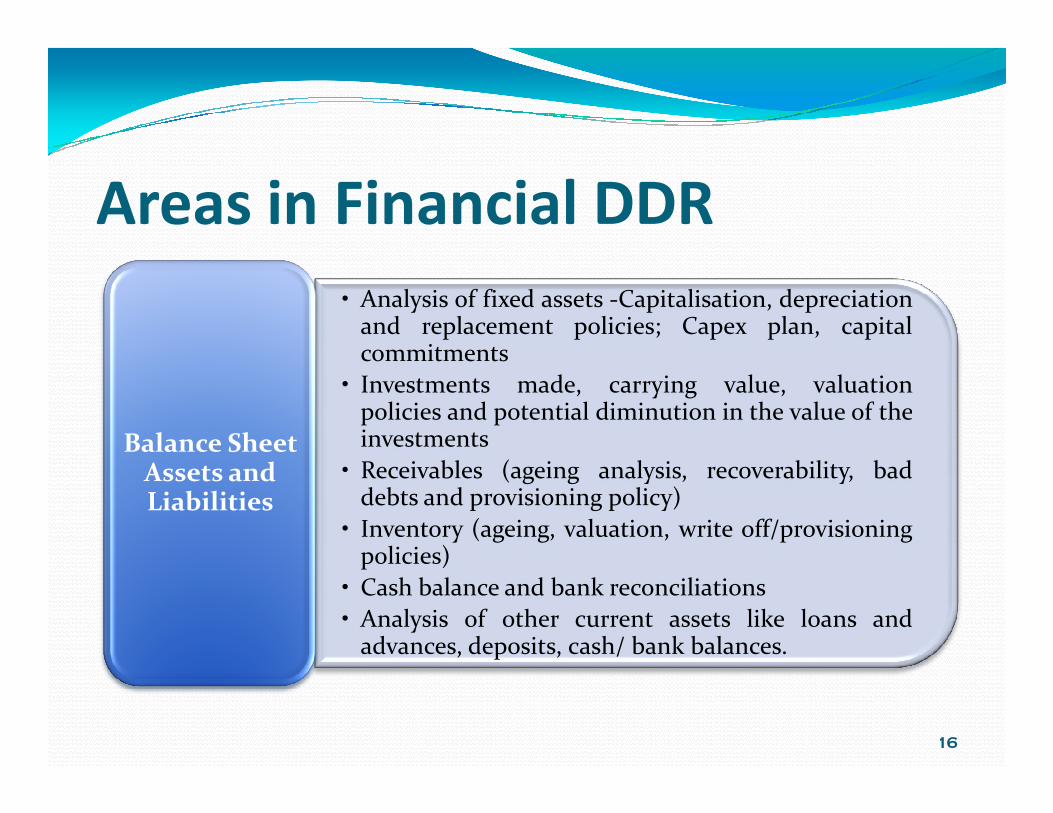

Areas in Financial DDR

• Analysis of fixed assets -Capitalisation, depreciationand replacement policies; Capex plan, capitalcommitments

• Investments made, carrying value, valuationpolicies and potential diminution in the value of the

16

policies and potential diminution in the value of theinvestments

• Receivables (ageing analysis, recoverability, baddebts and provisioning policy)

• Inventory (ageing, valuation, write off/provisioningpolicies)

• Cash balance and bank reconciliations• Analysis of other current assets like loans and

advances, deposits, cash/ bank balances.

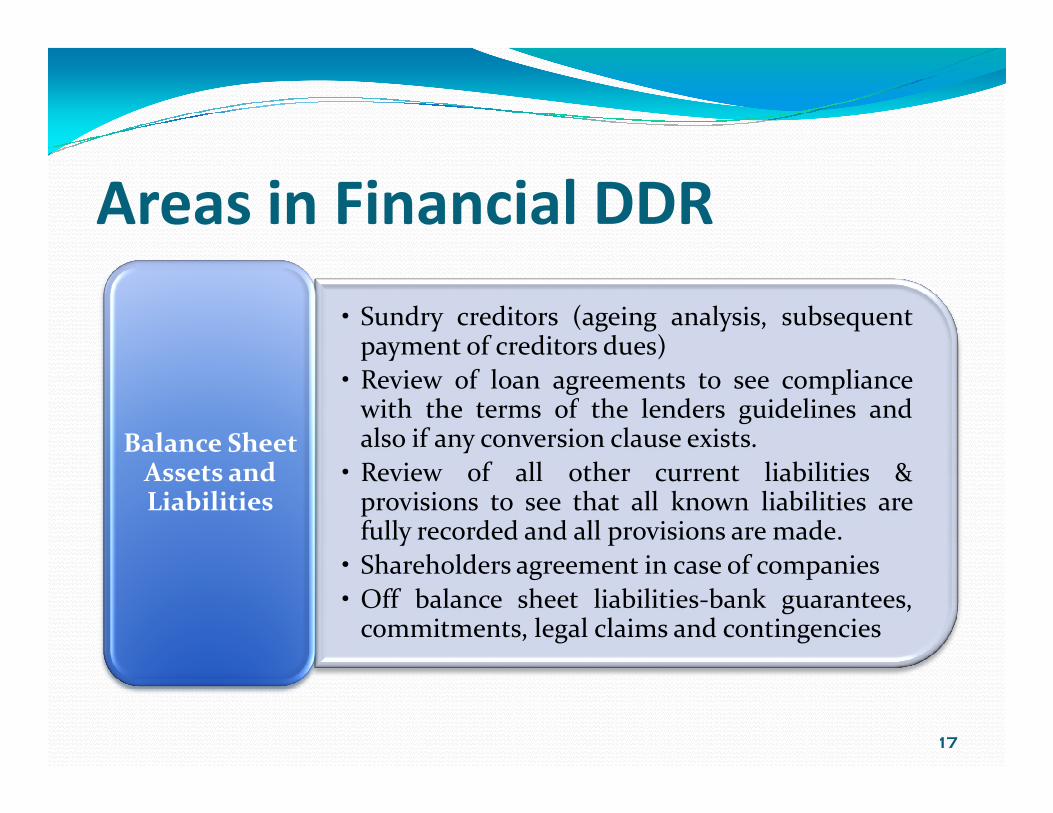

Balance Sheet Assets and Liabilities

Areas in Financial DDR

• Sundry creditors (ageing analysis, subsequentpayment of creditors dues)

• Review of loan agreements to see compliancewith the terms of the lenders guidelines and

17

with the terms of the lenders guidelines andalso if any conversion clause exists.

• Review of all other current liabilities &provisions to see that all known liabilities arefully recorded and all provisions are made.

• Shareholders agreement in case of companies• Off balance sheet liabilities-bank guarantees,

commitments, legal claims and contingencies

Balance Sheet Assets and Liabilities

Areas in Financial DDR

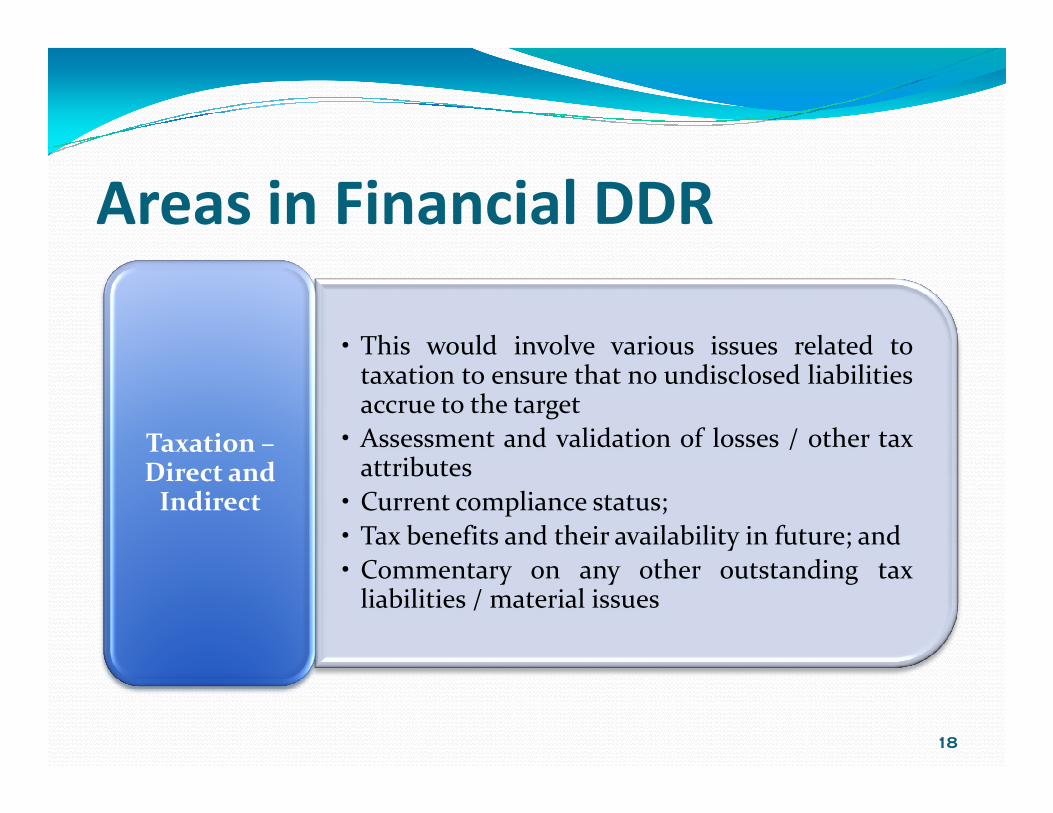

• This would involve various issues related totaxation to ensure that no undisclosed liabilitiesaccrue to the target

18

accrue to the target• Assessment and validation of losses / other tax

attributes• Current compliance status;• Tax benefits and their availability in future; and• Commentary on any other outstanding tax

liabilities / material issues

Taxation –Direct and

Indirect

Areas in Financial DDR

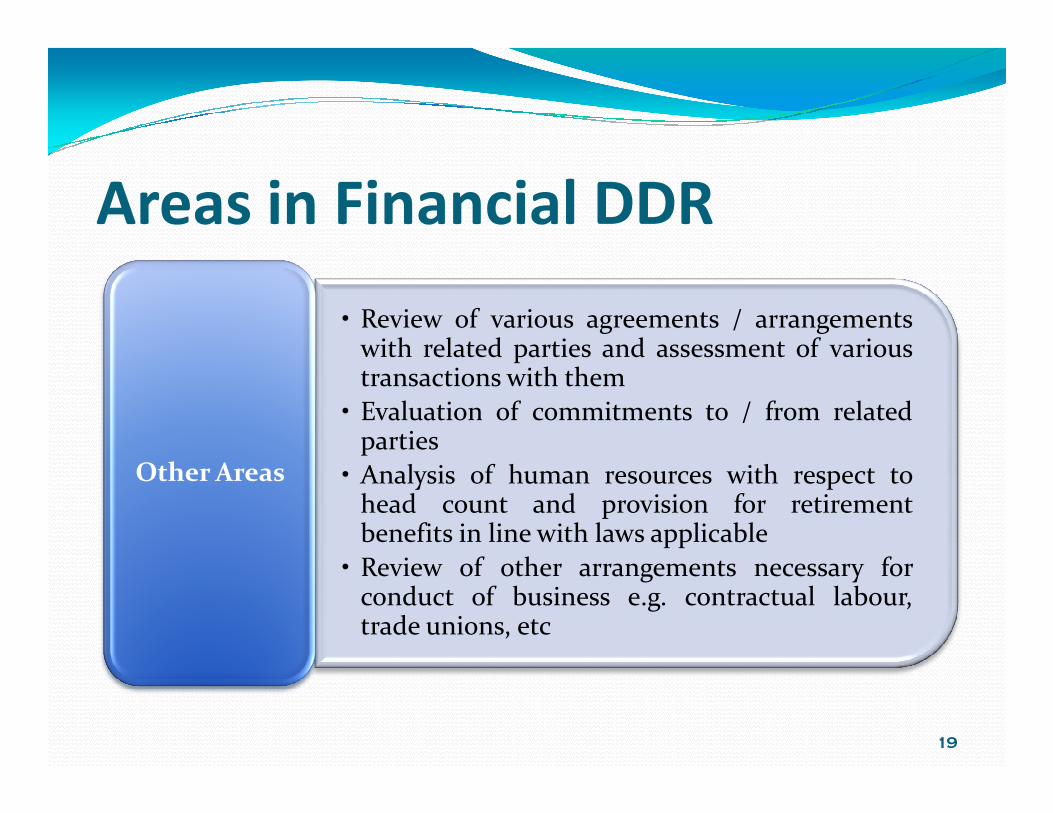

• Review of various agreements / arrangementswith related parties and assessment of varioustransactions with them

• Evaluation of commitments to / from related

19

• Evaluation of commitments to / from relatedparties

• Analysis of human resources with respect tohead count and provision for retirementbenefits in line with laws applicable

• Review of other arrangements necessary forconduct of business e.g. contractual labour,trade unions, etc

Other Areas

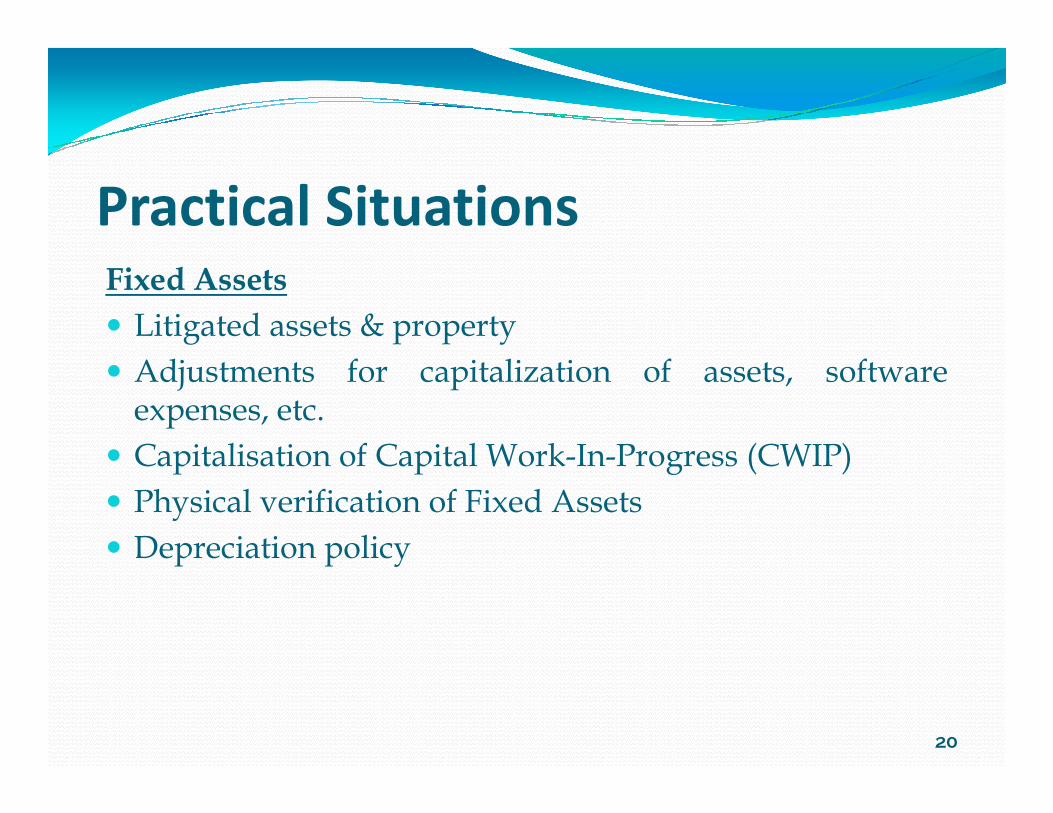

Fixed Assets

� Litigated assets & property

� Adjustments for capitalization of assets, softwareexpenses, etc.

Practical Situations

expenses, etc.

� Capitalisation of Capital Work-In-Progress (CWIP)

� Physical verification of Fixed Assets

� Depreciation policy

20

Investments

� Investments carried at cost though realizable value ismuch lower

� Investments carrying a very low rate of income / return

Practical Situations

� Investments carrying a very low rate of income / return

� Clear title to all Investments

21

Working Capital

� Uncollected/ uncollectible receivables

� Obsolete, slow & non-moving inventories or inventoriesvalued above Net Realizable Value

Practical Situations

valued above Net Realizable Value

� Adjustment for Inventories with old names/logos in thecase of hotel industry

� Inventories in case of discontinued products

� Group company balances under reconciliation, etc.

22

Deferred Revenue Expenditure

� Deferred revenue expenditure included under advancesor not normally deferrable

Practical Situations

Taxes

� Non Deduction of TDS

� Timely filing of returns

23

Other Claims

� Environmental problems/claims, third party claims

� Huge labour claims under negotiation when the labourwage agreement has already expired

Practical Situations

wage agreement has already expired

� Non-funded gratuity/superannuation/leave salaryliabilities

� Non-compliance with enactments such as the Income TaxAct, FEMA/FERA, Customs Act, etc. that could result inlitigation & levy of penalties

� Product warranties, defects & other liability claims, productreturns & discounts, liquidated damages for late deliveries

24

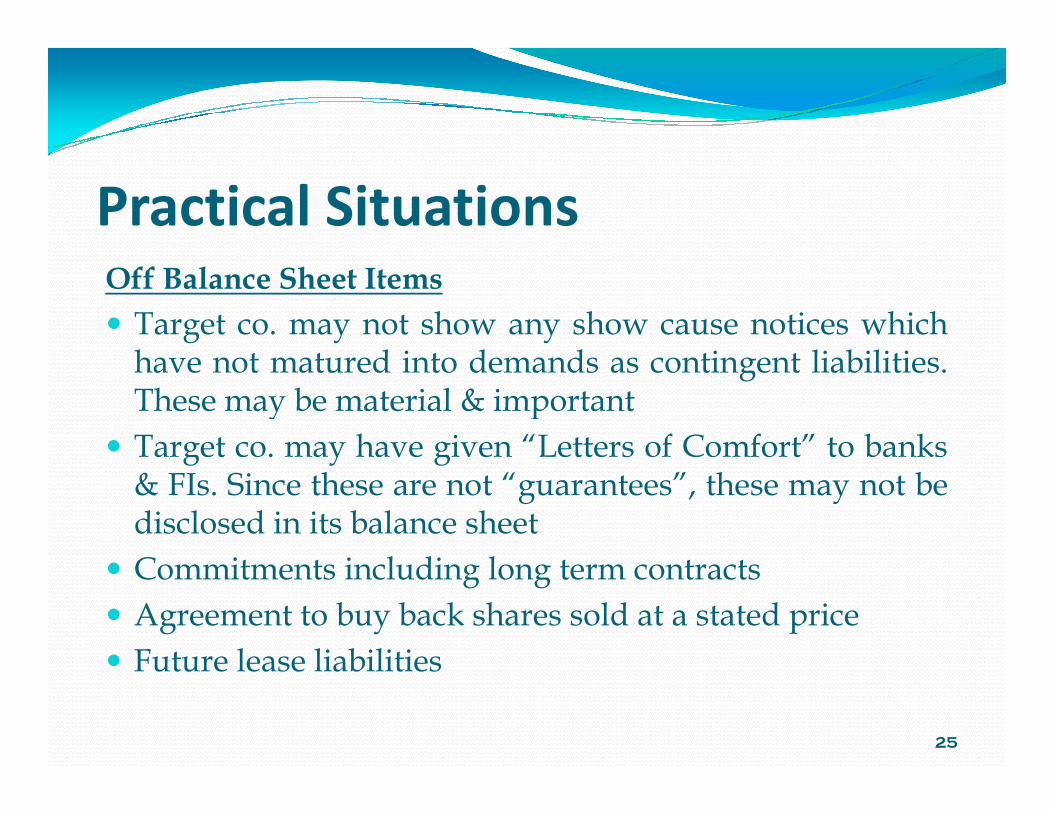

Off Balance Sheet Items

� Target co. may not show any show cause notices whichhave not matured into demands as contingent liabilities.These may be material & important

Practical Situations

These may be material & important

� Target co. may have given “Letters of Comfort” to banks& FIs. Since these are not “guarantees”, these may not bedisclosed in its balance sheet

� Commitments including long term contracts

� Agreement to buy back shares sold at a stated price

� Future lease liabilities

25

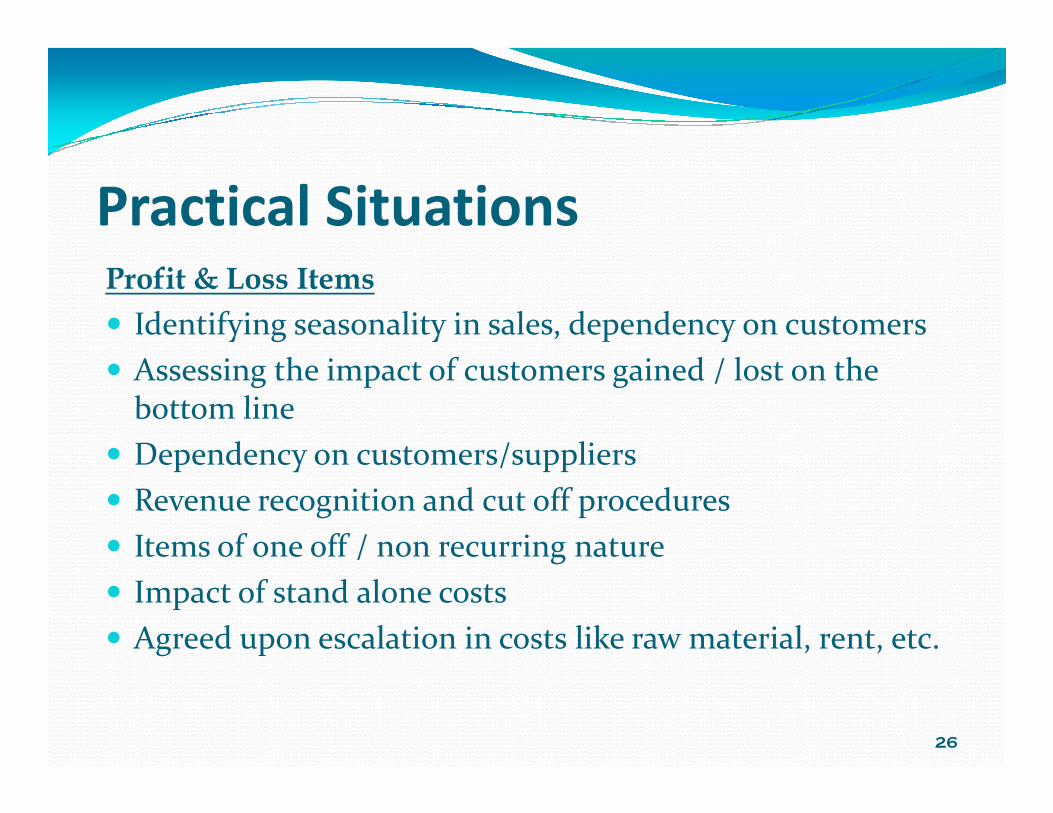

Profit & Loss Items

� Identifying seasonality in sales, dependency on customers

� Assessing the impact of customers gained / lost on the bottom line

Practical Situations

bottom line

� Dependency on customers/suppliers

� Revenue recognition and cut off procedures

� Items of one off / non recurring nature

� Impact of stand alone costs

� Agreed upon escalation in costs like raw material, rent, etc.

26

Profit & Loss Items

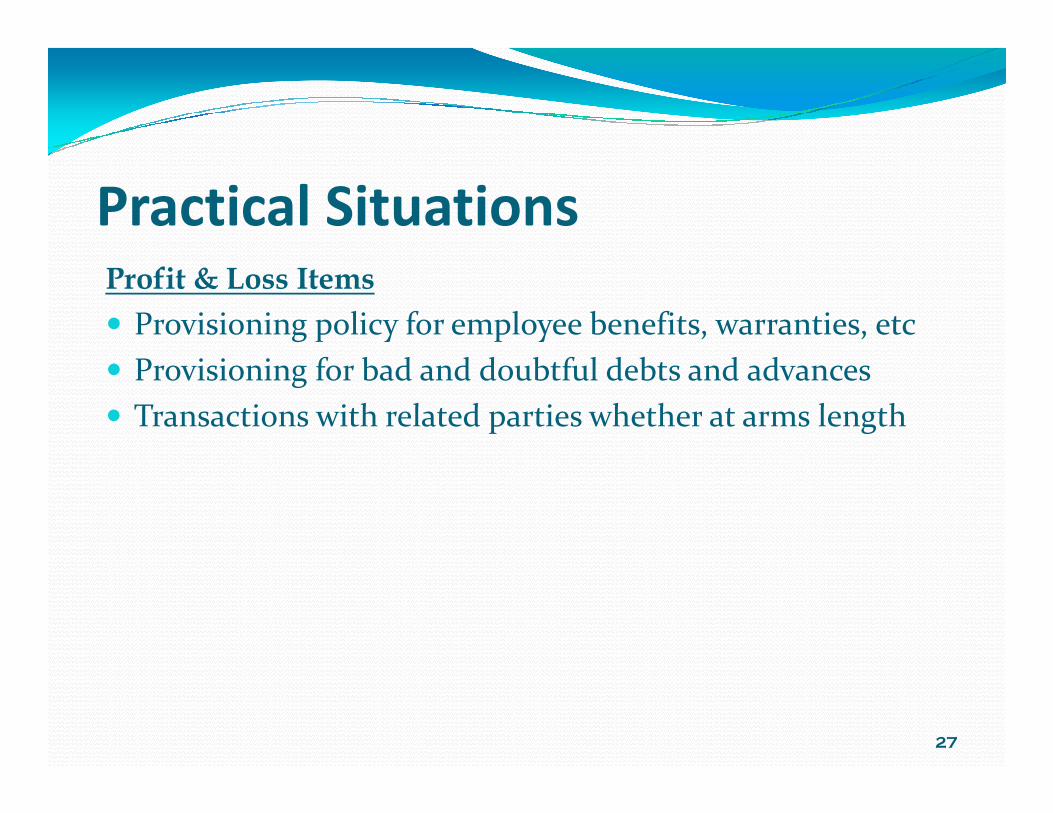

� Provisioning policy for employee benefits, warranties, etc

� Provisioning for bad and doubtful debts and advances

� Transactions with related parties whether at arms length

Practical Situations

� Transactions with related parties whether at arms length

27

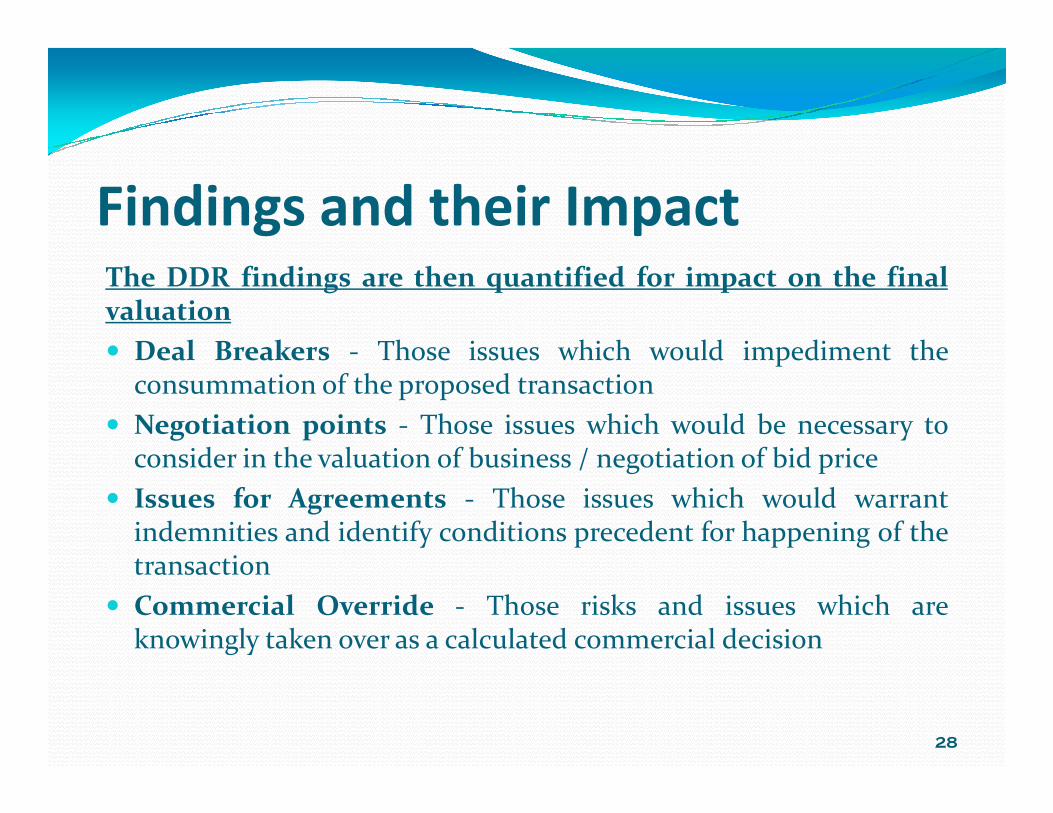

The DDR findings are then quantified for impact on the finalvaluation

� Deal Breakers - Those issues which would impediment theconsummation of the proposed transaction

Findings and their Impact

� Negotiation points - Those issues which would be necessary toconsider in the valuation of business / negotiation of bid price

� Issues for Agreements - Those issues which would warrantindemnities and identify conditions precedent for happening of thetransaction

� Commercial Override - Those risks and issues which areknowingly taken over as a calculated commercial decision

28

For Service Providers

� Limited scope of review fixed by the client

� “Too much to see in too little time”

Limitations

For Acquirers/Investors

� Inability to determine the scope

� Inability to ensure proper co-ordination between service providers

29

For Service Providers

� Failing to meet the needs of the party commissioning a due

Risks Involved

commissioning a due diligence

� Financial indemnification of the consequential loss

30

For Acquirer/Investor

� The investor may pay higher than the fair price for acquisition

� The investment performance may

Risks Involved

� The investment performance may not be upto the expectation or may perform badly

� A bad strategic investment may result in losing a considerable market share or reputation

31

By Service Provider

� Clearly understand the objectives & the complexities of the assignment based on which the

Steps to Mitigate Risks

assignment based on which the scope should be finalized

� The DDR report should disclose all the limitations of the assignment

� A proper engagement review should be carried out before accepting the assignment and deciding the scope

32

By Service Provider

� Schedule meetings with other reviewers

� Collect from the client reports of

Steps to Mitigate Risks

� Collect from the client reports of all other due diligences

� The due diligence team should consist of at least one person who is familiar with the industry, the target is involved in

33

By Acquirer/Investor

� Should ensure that the scope is comprehensive

� Proper coordination amongst all

Steps to Mitigate Risks

� Proper coordination amongst all service providers should be encouraged

� An integrated service provider may be hired

� To ensure that the target provides all necessary information

34

Due Diligence plays an important role in identifying, quantifying and reducing the risks of an

acquisition.

To Conclude ……..

Although Due Diligence focuses on negative information, the aim is not to raise obstacles to

transactions, but rather to facilitate transactions by identifying problems and risks by devising solutions to problems or devices to reduce or manage the risks

involved in corporate acquisitions.

35