Embed Size (px)

Citation preview

WHO TO CONTACT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code. You will have to write down

only the final verification code on the attestation form, which will be emailed to registered attendees.

• To earn full credit, you must remain connected for the entire program.

In-Kind Contributions: Accounting for Nonprofits Determining Optimal Classification and Valuation of Gifts and Services, Appropriate Timing of Recording

WEDNESDAY, MARCH 9, 2016, 1:00-2:50 pm Eastern

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

March 9, 2016

In-Kind Contributions

Robert C. Brackett, President

Crandall & Brackett

Bruce Levi, CPA, Partner

Lane Gorman Trubitt

Renee Ordeneaux, CPA, Partner

Armanino

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

5 © ArmaninoLLP | armaninoLLP.com © ArmaninoLLP | armaninoLLP.com

Noncash Contributions

Renee Ordeneaux

March 9, 2016

6 © ArmaninoLLP | armaninoLLP.com

• Gifts in Kind o Tangible personal property used in operations

o Items contributed for sale at fundraising events

o Contributed fundraising material, including advertising and media time

o Use of long-lived assets

o Contributed collection items

o Contributed securities

o Bargain purchase

• Contributed Services o Create or enhance non-financial asset

o Require specialized skills

o Provided by an affiliate

What We Will Cover

7 © ArmaninoLLP | armaninoLLP.com

• Why recognize non-cash contributions? o Provides better information about an organization’s support and costs

o Allows for more comparability between similar organizations that have different sources of support

o Required in certain circumstances by generally accepted accounting principles

• When would revenue recognition not be appropriate? o Goods are not in a condition that allows for their use

o An organization receives goods for benefit of another organization (agency transaction)

o The value is so difficult to determine that it cannot be recognized

Revenue Recognition (tangible personal property)

8 © ArmaninoLLP | armaninoLLP.com

• Recognize at fair value

• Record as contribution and related

expense (unless agency transaction) o Debit Appropriate Expense Account

• Credit Appropriate Contribution Account

• Contributions may be restricted

• Expense should be recorded in its natural

account (inventory/cost of sales, supplies)

rather than “in-kind expense”

General Treatment of Non-Cash Contributions

9 © ArmaninoLLP | armaninoLLP.com

Example: Donated Auction Items

• Initially record a contribution at fair value when the item is received

• Recognize an adjustment to the original contribution upon sale

– A charity receives a wine collection valued at $2,000 on the date of donation. The collection ultimately sells for $2,500.

– Initial entry DR Inventory $2,000

CR Contribution Income $2,000

– Entry upon sale DR Cash $2,500

DR Contribution Income $500

CR Inventory $2,000

In practice, this may be recorded as one transaction after the event

10 © ArmaninoLLP | armaninoLLP.com

Contribution of Use of An Asset - Media

• As noted in FASB ASC 958-605-55-23 ,

the use of property, utilities, or

advertising time are considered to be

forms of contributed assets rather than

contributed services. Therefore, the

criteria for recognition of contributed

services in FASB ASC 958-605-25-16 ,

as discussed in paragraph 5.112, are not

applicable.

• FinREC believes that in the case of

fund-raising material, informational

material, advertising, and media time or

space, the NFP has received an asset

(future economic benefit) and can

control others’ access to the benefit, and

therefore has received a contribution, if

the NFP has an active involvement in

determining and managing the message

and the use of the materials. The future

economic benefit received may be either

(a) cash inflows, such as contributions

arising from fund-raising activities or

revenues arising from exchange

transactions, or (b) service potential in

conducting program or management and

general activities.

11 © ArmaninoLLP | armaninoLLP.com

Use of Long-Lived Assets

• Donor retains legal title to asset

• NFP is allowed to use asset without

charge

• Determination of recognition is

unaffected by whether the organization

can afford to purchase

• If multiple years involved, must consider

the fair value for the entire term of the

arrangement

• FV of “lease” cannot exceed FV of

property

• Multiyear arrangement would generally

be recorded as temporarily restricted

and released over term of agreement

12 © ArmaninoLLP | armaninoLLP.com

Contribution of Long-Lived Assets

• NFP gains legal title to asset

• Two choices in accounting:

o Recognize all as unrestricted in first year,

depreciation expense incurred over useful

life

• Advantage – easier, since NFP does not have to

track and record releases from restriction

• Disadvantage – built-in “loss” each year from the

depreciation expense

o Treat as if there is a time restriction, and

release from restriction annually, matching

unrestricted revenue to depreciation

expense.

13 © ArmaninoLLP | armaninoLLP.com

Definition of collection:

“(a) They are held for public exhibition, education, or research in furtherance of public

service rather than financial gain,

(b) They are protected, kept unencumbered, cared for, and preserved, and

(c) They are subject to an organizational policy that requires the proceeds of items that

are sold to be used to acquire other items for collections.”

Contributions of Collection Items

Three alternatives:

1. Capitalize all collection assets

2. Capitalize all obtained after a certain date

3. Don’t capitalize at all

Selective capitalization is not permitted, but if a specimen is

obtained only for scientific study, it may not have a market

value.

Capitalized items must be depreciated and considered for

impairment.

14 © ArmaninoLLP | armaninoLLP.com

• Three relevant dates:

o Pledge date – if pledged, but not yet received, record at value on pledge date

o Received date – adjust value upon receipt

o Sale date – recognize gain/loss on sale

Example:

• 12/01/14 – Shares of stock valued at $10,000 are pledged

• 12/31/14 – Shares are received and worth $9,500

• 01/05/15 – NFP’s broker sells the shares $9,700, after $50 trade fee

Common Noncash Contribution: Donated Stock

15 © ArmaninoLLP | armaninoLLP.com

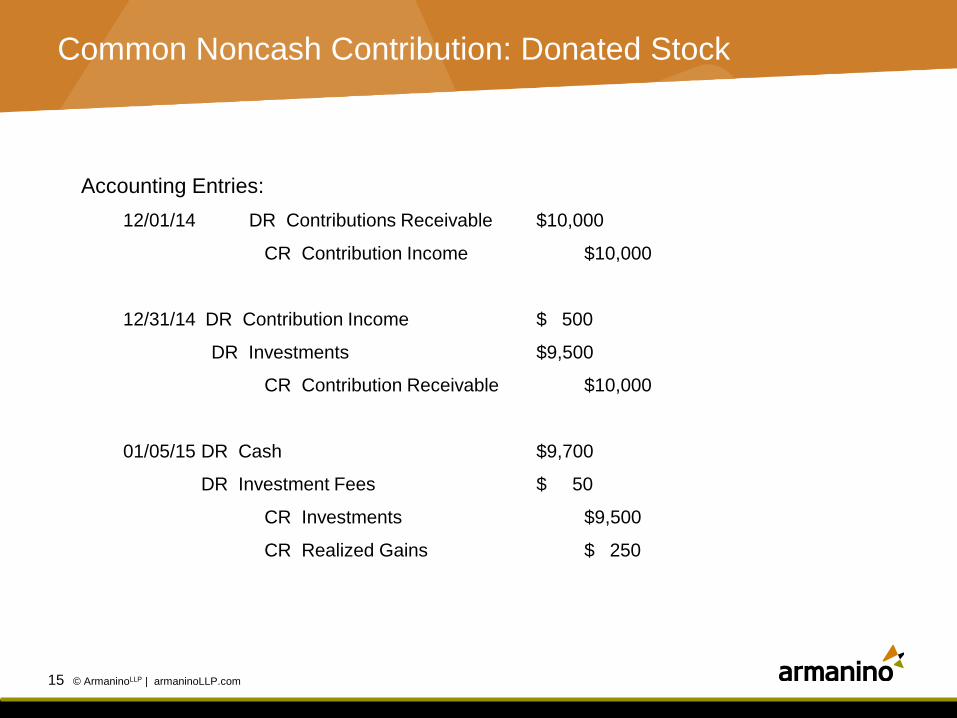

Accounting Entries:

12/01/14 DR Contributions Receivable $10,000

CR Contribution Income $10,000

12/31/14 DR Contribution Income $ 500

DR Investments $9,500

CR Contribution Receivable $10,000

01/05/15 DR Cash $9,700

DR Investment Fees $ 50

CR Investments $9,500

CR Realized Gains $ 250

Common Noncash Contribution: Donated Stock

16 © ArmaninoLLP | armaninoLLP.com

ASC 230-45-21A Cash receipts resulting from the sale of

donated financial assets (for example, donated debt or equity

instruments) by NFPs that upon receipt were directed without any NFP-

imposed limitations for sale and were converted nearly immediately into

cash shall be classified as operating cash flows. If, however, the donor

restricted the use of the contributed resource to a long-term purpose of

the nature of those described in paragraph 230-10-45-14(c), then those

cash receipts meeting all the conditions in this paragraph shall be

classified as a financing activity.

Classification of Proceeds from Sale in Stmt of Cash Flows

17 © ArmaninoLLP | armaninoLLP.com

A contribution may occur

as part of an exchange

transaction. For example,

nonprofit land trust

purchases compensates

a resort to set aside part

of its land from

development. The

appraised value of the

land is $3 million but the

resort agrees to accept

only $500,000. The

difference between the

appraised value and the

purchase price is a

contribution.

Bargain Purchase

18 © ArmaninoLLP | armaninoLLP.com

Recognized when:

• The services create or enhance non-financial assets

• Or, requires a specialized skill, which the contributor has,

and would typically need to be purchased

Contributed Services

19 © ArmaninoLLP | armaninoLLP.com

Example: Volunteers help to renovate a homeless shelter. The shelter was

appraised at $100,000 before the renovation and $150,000 after the

renovation.

DR Building improvements $50,000

CR Contributed services $50,000

The estimated value of the donor time could be used instead of change in

appraised value.

Creating or Enhancing Nonfinancial Asset

20 © ArmaninoLLP | armaninoLLP.com

• “Services requiring specialized skills are provided by

accountants, architects, carpenters, doctors, electricians,

lawyers, nurses, plumbers, teachers, and other

professionals and craftspeople.”

• “Whether such contributions should be reported is

unaffected by whether the NFP could afford to purchase

the services at their fair value.”

Specialized Services

21 © ArmaninoLLP | armaninoLLP.com

• Board members frequently have specialized professional skills, and

are expected to draw on those skills as part of their normal board

duties.

• Occasionally, board members may use their expertise on a project

that would normally be considered outside the scope of normal board

duties.

• Example: An attorney serving on a board and providing general

advice would generally not be recognized as contributed services.

However, if the attorney represented the organization in a lawsuit, that

would generally constitute contributed services.

Contributed Board Member Services

22 © ArmaninoLLP | armaninoLLP.com

ASC 958-720-25-9 A not-for-profit entity (NFP) shall recognize all services received

from personnel of an affiliate that directly benefit the recipient NFP (that is, are similar to

personnel directly engaged by the recipient NFP). For example, that would include

services performed by personnel of an affiliate for and under the direction of the recipient

NFP and shared services. Shared services generally refers to services provided by a

centralized function of one or more individuals within the affiliate group that the recipient

NFP would otherwise typically need to purchase or have donated, if not provided by

those personnel.

Example: A corporation has established a related foundation that provides grants to

organizations in communities in which the corporation has projects. The corporation

provides all bookkeeping and administrative functions. The foundation should record the

value of all services provided.

Services Received from Affiliates

23 © ArmaninoLLP | armaninoLLP.com © ArmaninoLLP | armaninoLLP.com

310-745-5700 [email protected]

Renee Ordeneaux, Partner Renee has more than 25 years of experience in public

accounting and industry―including serving as the CFO of

a nonprofit organization―and brings an entrepreneurial

approach to her work. She provides audit and consulting

services to a broad range of clients, including nonprofit

organizations, privately held businesses and public

companies. In the nonprofit sector, her expertise extends to

income tax matters pertaining to unrelated business

income and non-recurring business transactions.

She serves on the finance committee of the Theodore

Payne Foundation and the board of Upward Bound House.

She is a former board president and treasurer of the Los

Angeles Junior Chamber of Commerce.

Renee has a B.A. in English literature from the University

of Texas, Austin, and an M.B.A. from the Anderson School

of Management at the University of California, Los Angeles

(UCLA). She is a member of the American Institute of

Certified Public Accountants and the California Society of

Certified Public Accountants, and has taught nonprofit

accounting at UCLA Extension.

24 © ArmaninoLLP | armaninoLLP.com

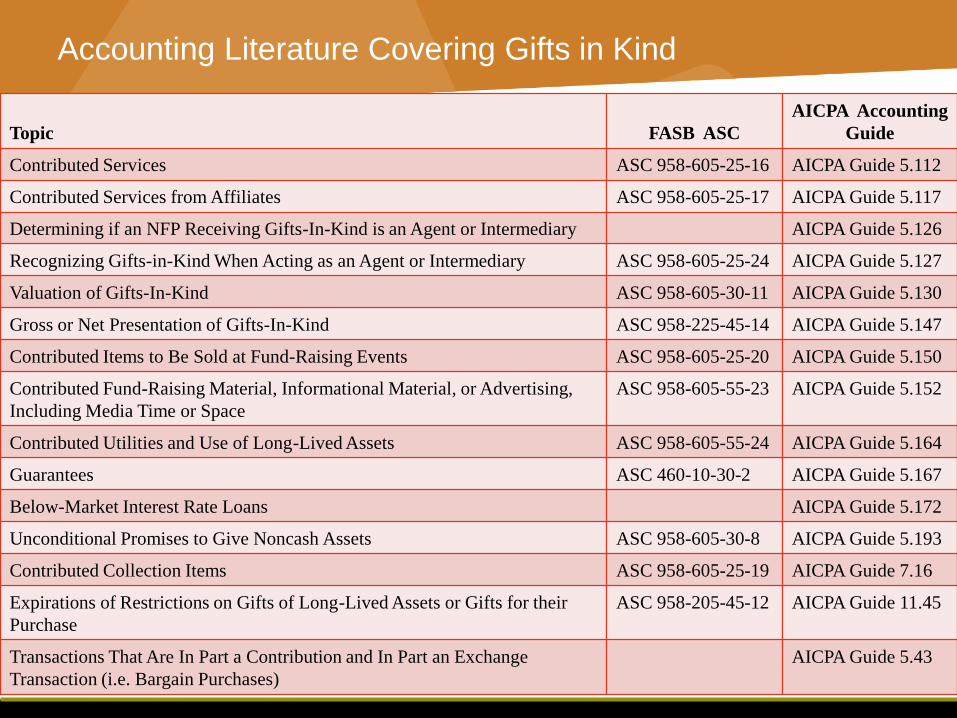

Accounting Literature Covering Gifts in Kind

Topic FASB ASC

AICPA Accounting

Guide

Contributed Services ASC 958-605-25-16 AICPA Guide 5.112

Contributed Services from Affiliates ASC 958-605-25-17 AICPA Guide 5.117

Determining if an NFP Receiving Gifts-In-Kind is an Agent or Intermediary AICPA Guide 5.126

Recognizing Gifts-in-Kind When Acting as an Agent or Intermediary ASC 958-605-25-24 AICPA Guide 5.127

Valuation of Gifts-In-Kind ASC 958-605-30-11 AICPA Guide 5.130

Gross or Net Presentation of Gifts-In-Kind ASC 958-225-45-14 AICPA Guide 5.147

Contributed Items to Be Sold at Fund-Raising Events ASC 958-605-25-20 AICPA Guide 5.150

Contributed Fund-Raising Material, Informational Material, or Advertising,

Including Media Time or Space

ASC 958-605-55-23 AICPA Guide 5.152

Contributed Utilities and Use of Long-Lived Assets ASC 958-605-55-24 AICPA Guide 5.164

Guarantees ASC 460-10-30-2 AICPA Guide 5.167

Below-Market Interest Rate Loans AICPA Guide 5.172

Unconditional Promises to Give Noncash Assets ASC 958-605-30-8 AICPA Guide 5.193

Contributed Collection Items ASC 958-605-25-19 AICPA Guide 7.16

Expirations of Restrictions on Gifts of Long-Lived Assets or Gifts for their

Purchase

ASC 958-205-45-12 AICPA Guide 11.45

Transactions That Are In Part a Contribution and In Part an Exchange

Transaction (i.e. Bargain Purchases)

AICPA Guide 5.43

Noncash Contributions:

Tax Considerations Bruce Levi, CPA, Partner

Lane Gorman Trubitt, PLLC

Topics

• Reporting on Form 990

• Donor reporting and acknowledgment

• Charity auctions

• Vehicle donation programs

• Unrelated business income potential

• Limitations on deductions of in-kind contributions

• Conservation easements

26

Tax Recognition on Form 990

• Property other than cash

• No recognition of services or use of facilities, even when recognized for GAAP

• Must be reflected at fair market value

• If total noncash contributions exceed $25,000 in FMV, must prepare Schedule M

• Part IV, “Checklist of Required Schedules”, lines 7, 8, 29 and 30

27

Definition: Noncash Contributions

• Contributions of property, tangible or intangible, other than money. Noncash contributions include, but are not limited to, stocks, bonds, and other securities; real estate; works of art; stamps, coins, and other collectibles; clothing and household goods; vehicles, boats, and airplanes; inventories of food, medical equipment or supplies, books, or seeds; intellectual property, including patents, trademarks, copyrights, and trade secrets; donated items that are sold immediately after donation, such as publicly traded stock or used cars; and items donated for sale at a charity auction. Noncash contributions do not include volunteer services performed for the reporting organization or donated use of materials, facilities, or equipment

28

Definition: Fair Market Value

• The price at which property, or the right to use

property, would change hands between a willing

buyer and a willing seller, neither being under any

compulsion to buy, sell, or transfer property or the

right to use property, and both having reasonable

knowledge of the facts.

29

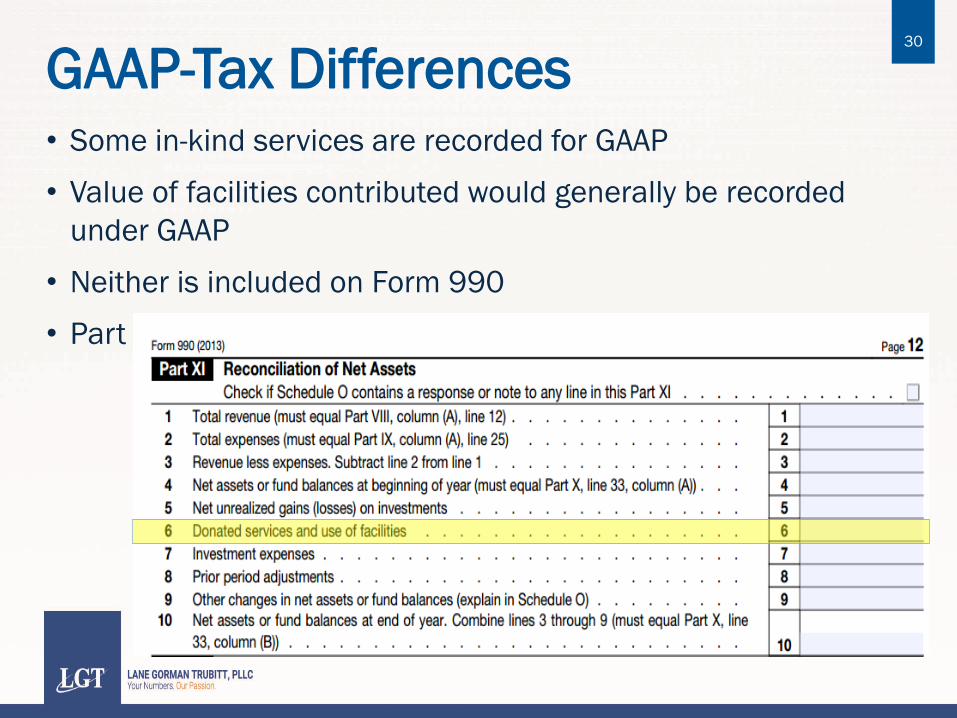

GAAP-Tax Differences • Some in-kind services are recorded for GAAP

• Value of facilities contributed would generally be recorded

under GAAP

• Neither is included on Form 990

• Part XII has a reconciliation to GAAP figures

30

31

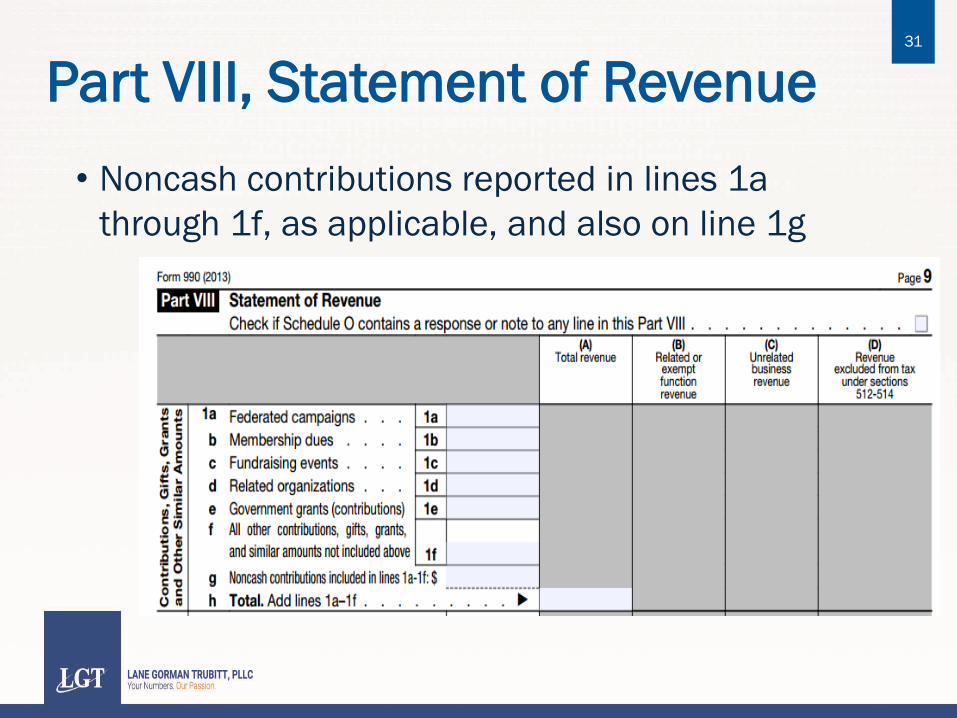

Part VIII, Statement of Revenue

• Noncash contributions reported in lines 1a

through 1f, as applicable, and also on line 1g

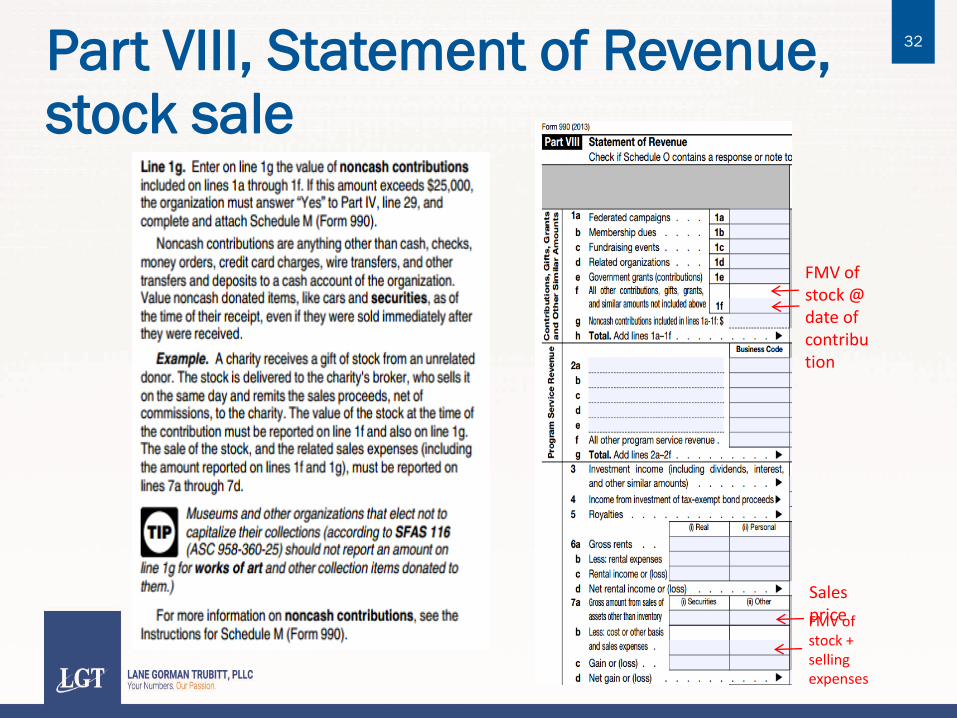

32 Part VIII, Statement of Revenue, stock sale

FMV of stock @ date of contribution

FMV of stock + selling expenses

Sales price

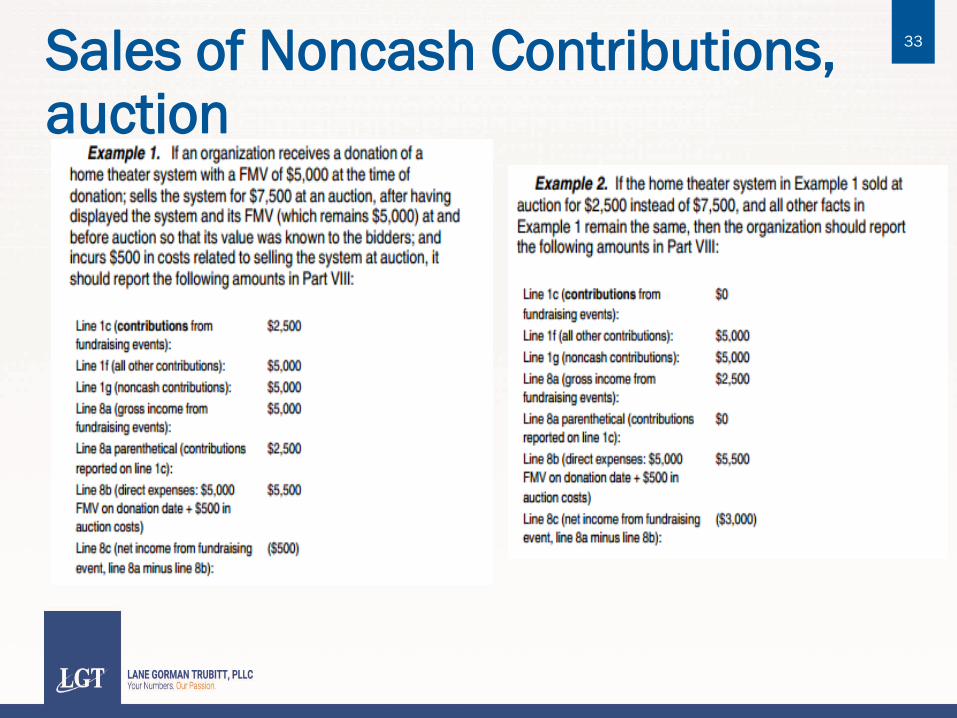

33 Sales of Noncash Contributions, auction

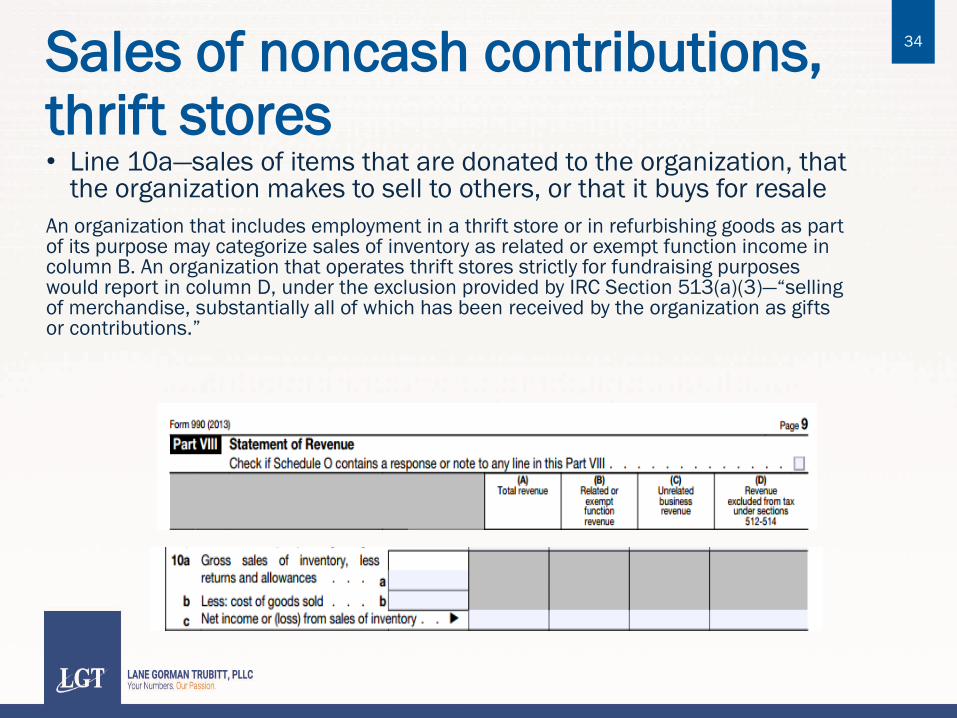

Sales of noncash contributions, thrift stores • Line 10a—sales of items that are donated to the organization, that

the organization makes to sell to others, or that it buys for resale

An organization that includes employment in a thrift store or in refurbishing goods as part of its purpose may categorize sales of inventory as related or exempt function income in column B. An organization that operates thrift stores strictly for fundraising purposes would report in column D, under the exclusion provided by IRC Section 513(a)(3)—“selling of merchandise, substantially all of which has been received by the organization as gifts or contributions.”

34

Reporting Contributed Goods Distributed to Others

• An organization that receives contributed goods may end up distributing them to needy individuals or other charitable organizations

• The recipient organization will first need to consider whether it is the actual beneficiary of the contributed goods, or whether it is an agent for the ultimate recipient.

• If recognizable as income, will end up being reported on page 10 as a grant when it goes out as grant expense

35

Schedule B: Schedule of Contributors

• Must indicate whether noncash for each contribution exceeding $5,000 or 2%, as appropriate

• Part III requires additional information on noncash property given, primarily the description

• The IRS receives donor names, addresses and the FMV, but does not obtain the tax ID and does not cross-reference

36

Schedule M: Noncash Contributions

• Not required for 990-EZ

• Required when total noncash contributions are $25,000 or more

• Lots of detail needed • 24 categories of contributions

• Number of items contributed

• Method of determining value

• Other compliance disclosures, including donor reporting

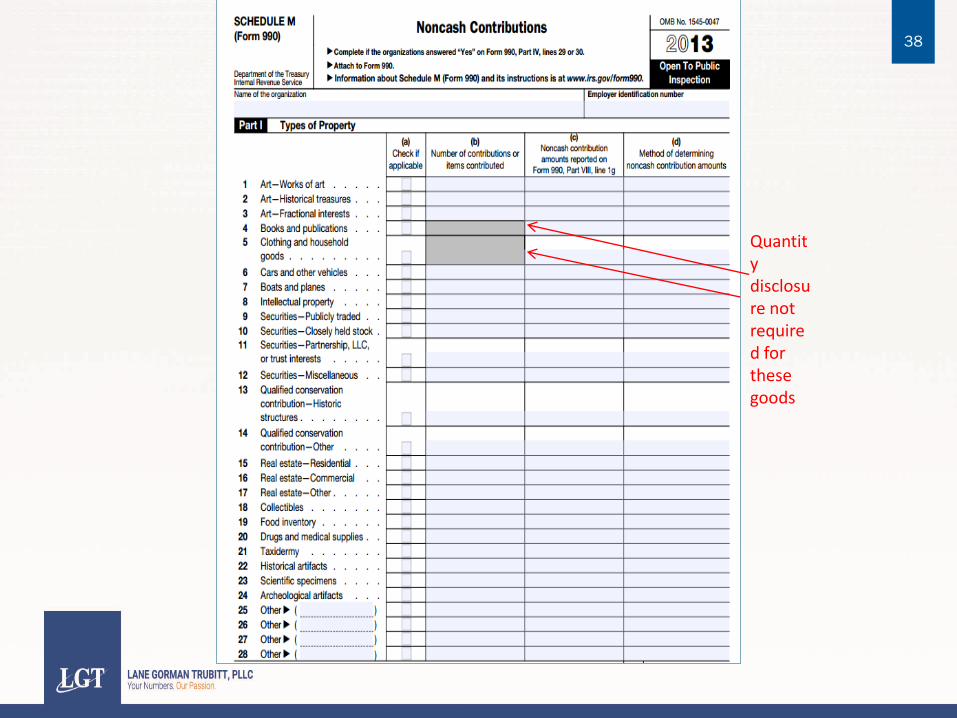

37

Quantity disclosure not required for these goods

38

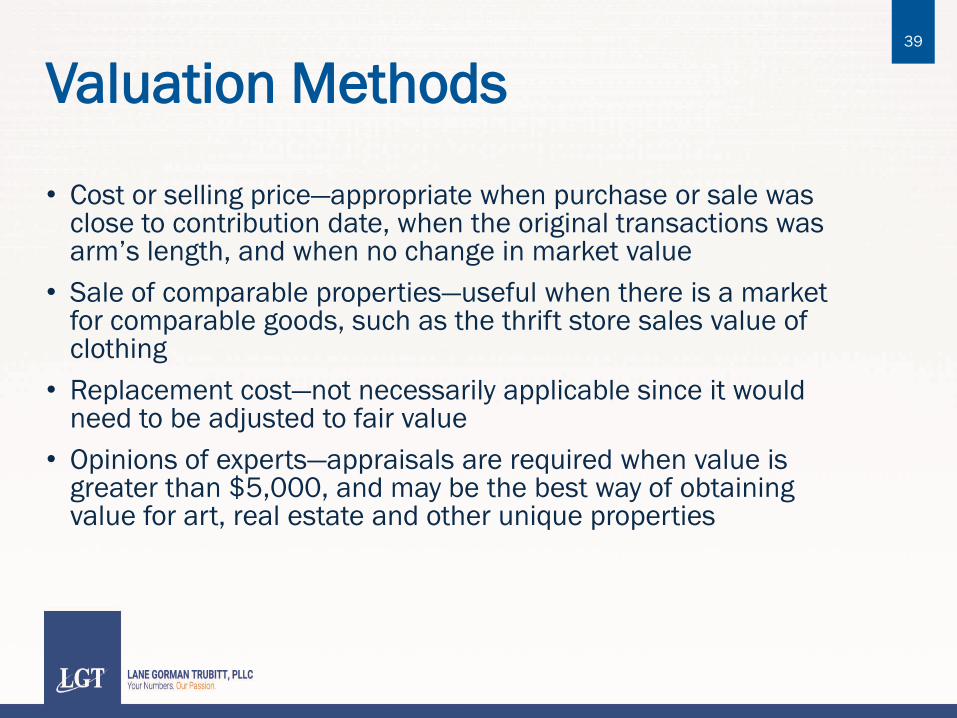

Valuation Methods

• Cost or selling price—appropriate when purchase or sale was close to contribution date, when the original transactions was arm’s length, and when no change in market value

• Sale of comparable properties—useful when there is a market for comparable goods, such as the thrift store sales value of clothing

• Replacement cost—not necessarily applicable since it would need to be adjusted to fair value

• Opinions of experts—appraisals are required when value is greater than $5,000, and may be the best way of obtaining value for art, real estate and other unique properties

39

Schedule M Donor-Related

• Number of Forms 8283

• Receipt of property with a three-year holding

period

• Gift-acceptance policy

• Third-party solicitation, processing or selling

40

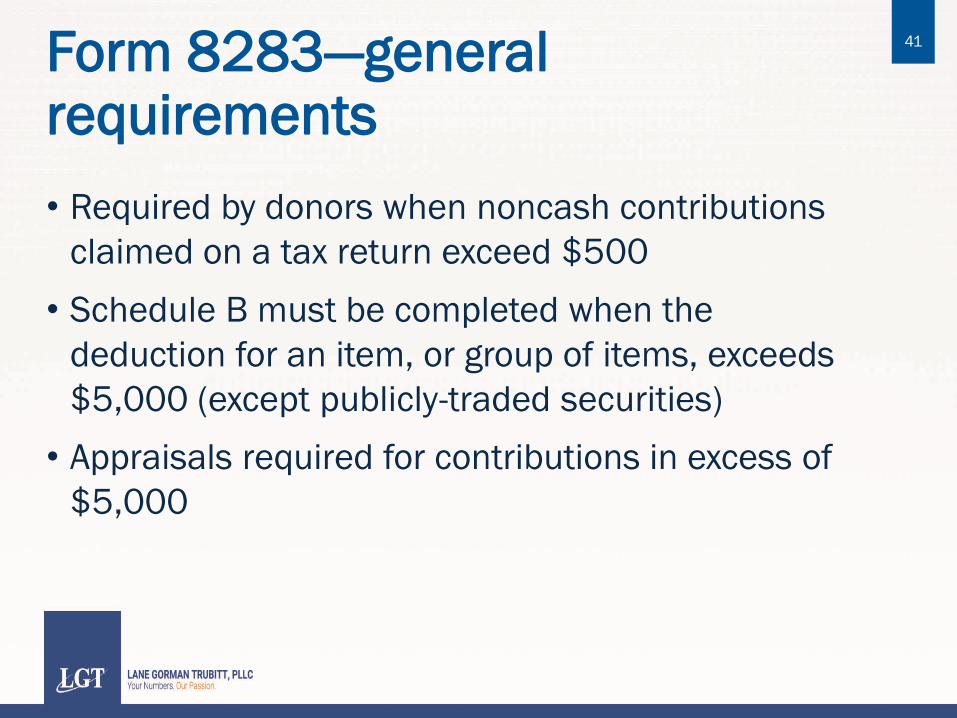

Form 8283—general requirements

• Required by donors when noncash contributions

claimed on a tax return exceed $500

• Schedule B must be completed when the

deduction for an item, or group of items, exceeds

$5,000 (except publicly-traded securities)

• Appraisals required for contributions in excess of

$5,000

41

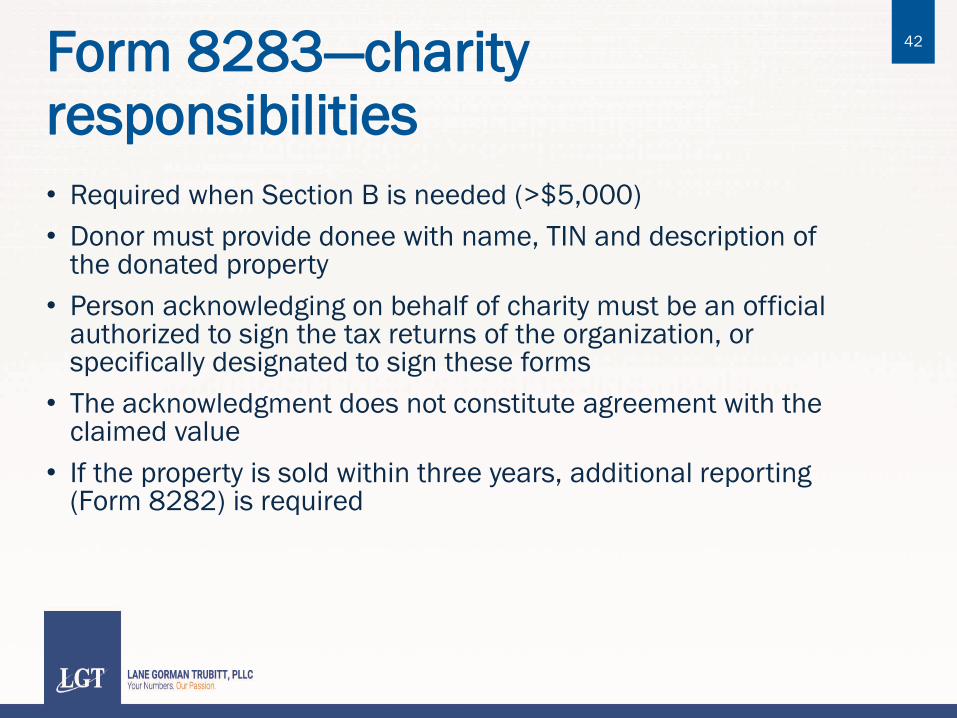

Form 8283—charity responsibilities

• Required when Section B is needed (>$5,000)

• Donor must provide donee with name, TIN and description of the donated property

• Person acknowledging on behalf of charity must be an official authorized to sign the tax returns of the organization, or specifically designated to sign these forms

• The acknowledgment does not constitute agreement with the claimed value

• If the property is sold within three years, additional reporting (Form 8282) is required

42

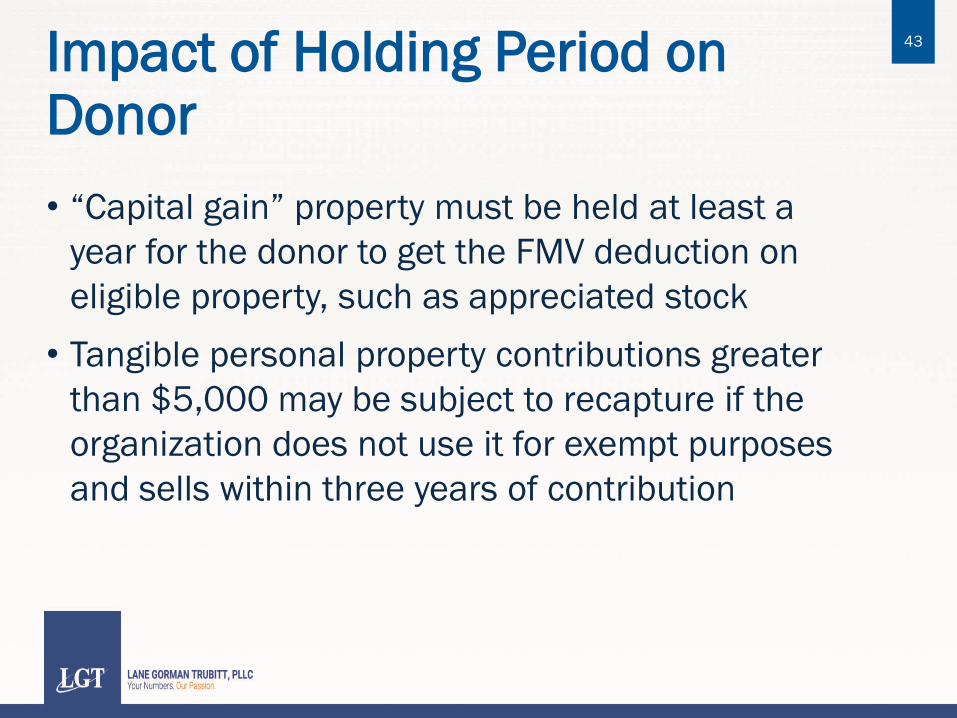

Impact of Holding Period on Donor

• “Capital gain” property must be held at least a

year for the donor to get the FMV deduction on

eligible property, such as appreciated stock

• Tangible personal property contributions greater

than $5,000 may be subject to recapture if the

organization does not use it for exempt purposes

and sells within three years of contribution

43

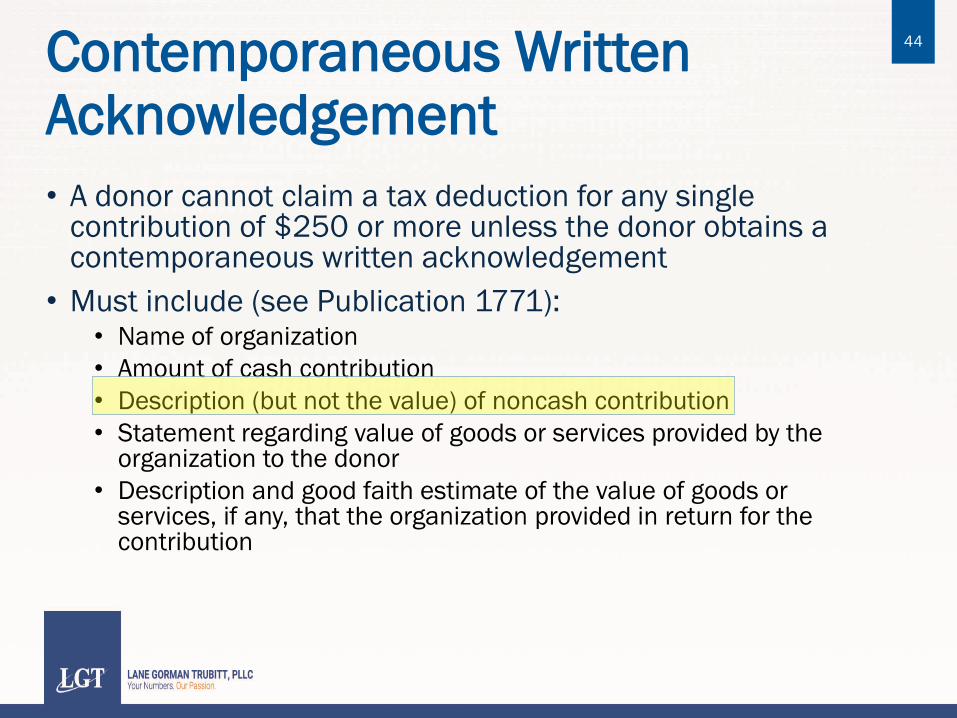

Contemporaneous Written Acknowledgement

• A donor cannot claim a tax deduction for any single contribution of $250 or more unless the donor obtains a contemporaneous written acknowledgement

• Must include (see Publication 1771): • Name of organization

• Amount of cash contribution

• Description (but not the value) of noncash contribution

• Statement regarding value of goods or services provided by the organization to the donor

• Description and good faith estimate of the value of goods or services, if any, that the organization provided in return for the contribution

44

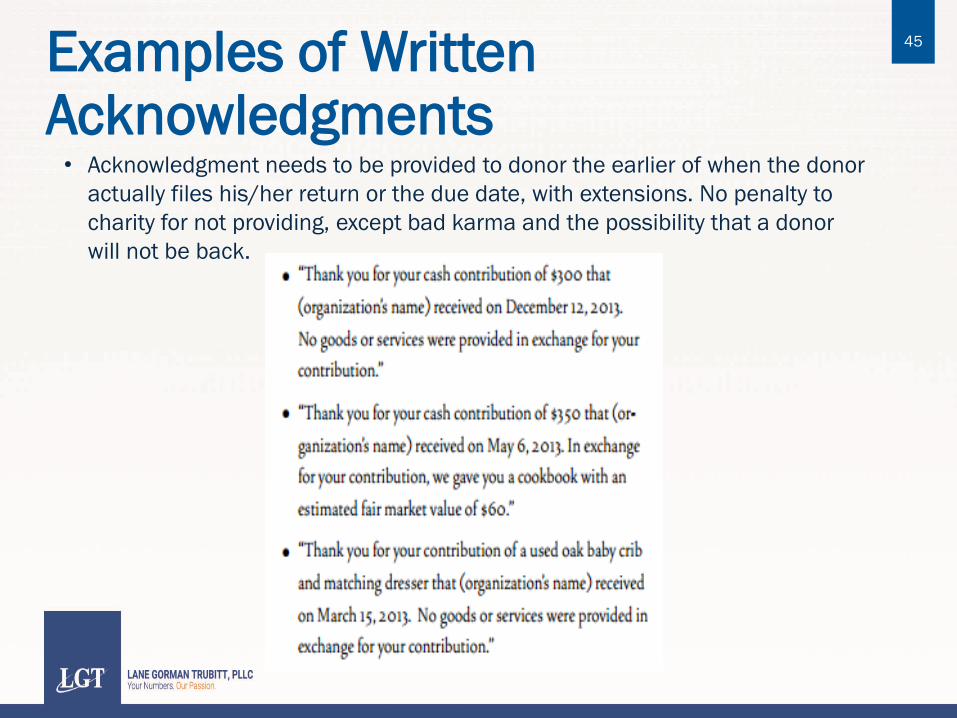

Examples of Written Acknowledgments

45

• Acknowledgment needs to be provided to donor the earlier of when the donor

actually files his/her return or the due date, with extensions. No penalty to

charity for not providing, except bad karma and the possibility that a donor

will not be back.

Contributions Subject to Special Rules • Clothing or household items—must be in good used condition

• A car, boat, or airplane—limited to lower of gross proceeds from the organization’s sale of the property or FMV on date of contribution

• Taxidermy property—limited to lower of basis or FMV; basis does not include any hunting costs

• Property subject to a debt—must reduce FMV by any interest paid after contribution (if debt retained) or the debt if “contributed”

• A partial interest in property—see previous slide

• A fractional interest in tangible personal property—see previous slide

• A qualified conservation contribution—complex rules

• A future interest in tangible personal property—not deductible until it actually transfers

• Inventory from your business—lower of FMV or basis

• A patent or other intellectual property—lower of FMV or basis

46

Tax Planning Opportunities for Donors

• Appreciated stock—donor received FMV deduction

if held for longer than one year

• Bargain sale—a reduction in sale price below FMV

to a charity results in a contribution for the

amount of the difference between the sales price

and FMV

47

Unrelated Business Income Tax

• Closely-held stock—trade or business activity

could generate ordinary income (partnership or S

corporation)

• Rental real estate—if transferred with debt, then

rental real estate income may become subject to

UBIT

48

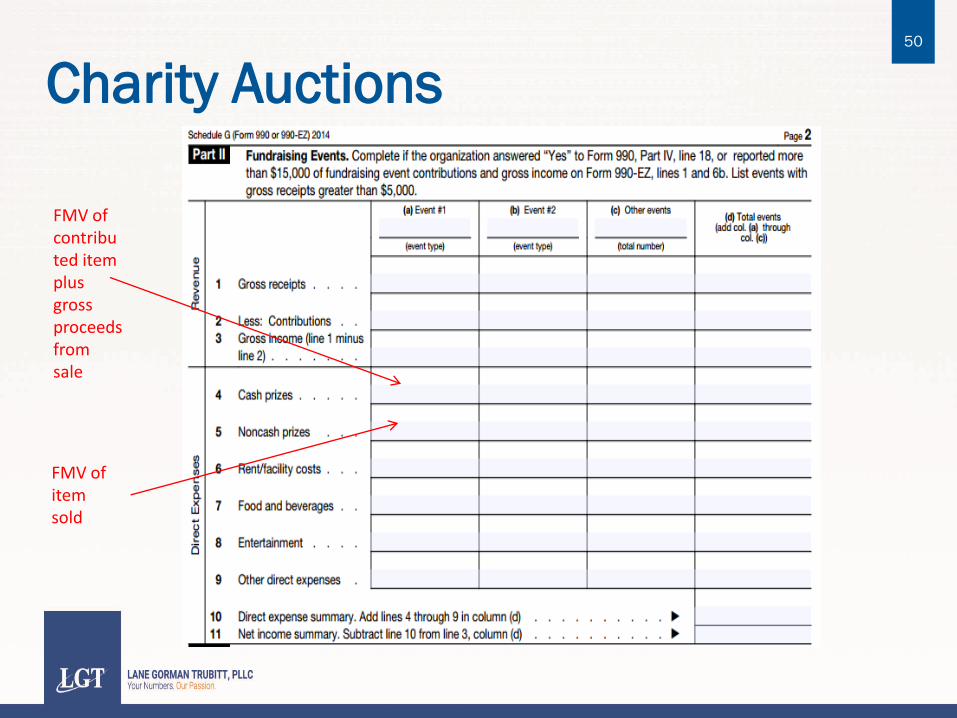

Charity Auctions

• Goods donated for sale in an auction should be included on Schedule M

• Donated services of use of asset (i.e., stay at a vacation home) do not get recorded on Schedule M

• Proceeds of the auction sale and the fair value of the items are reflected on Schedule G

• UBTI if “regularly carried on”

49

Charity Auctions

FMV of contributed item plus gross proceeds from sale

FMV of item sold

50

Vehicle Donation Programs: Three Scenarios

• Charity operates the program—generally fine,

though subject to some rules

• Charity hires agent to operate the program—must

establish valid agency relationship

• For-profit entity receives and sells vehicles using

charity’s name—will eliminate ability to take

contribution deduction

51

Responsibilities of Charity Operating Program

• Comply with state law regarding program

• Provide required donor acknowledgment

• File Form 1098-C and provide a copy to the donor

• File Form 8282, if required

52

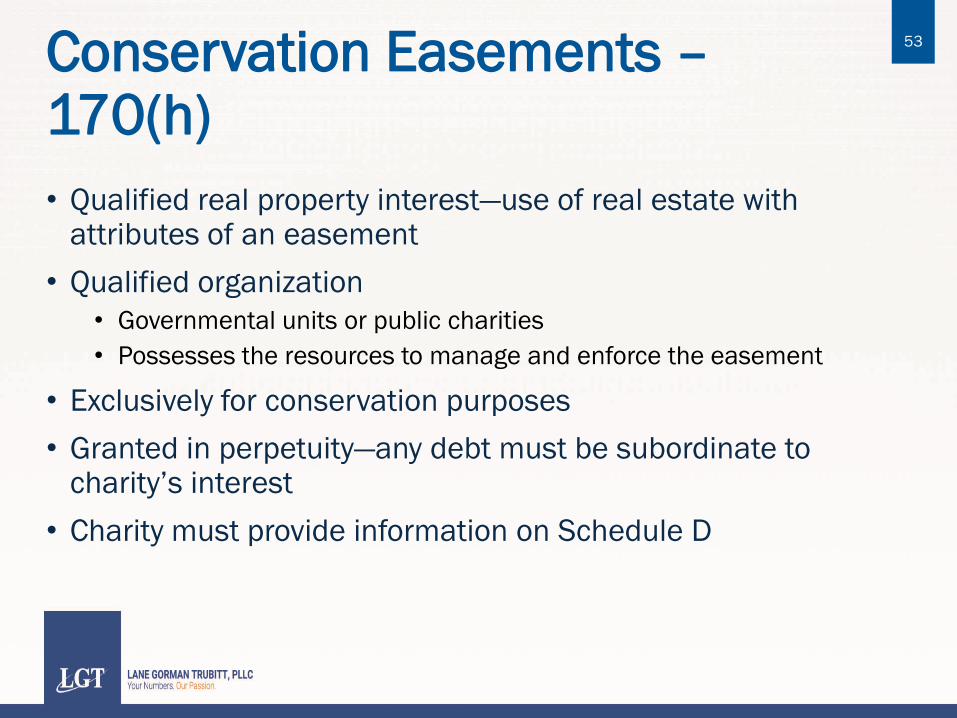

Conservation Easements – 170(h)

• Qualified real property interest—use of real estate with attributes of an easement

• Qualified organization

• Governmental units or public charities

• Possesses the resources to manage and enforce the easement

• Exclusively for conservation purposes

• Granted in perpetuity—any debt must be subordinate to charity’s interest

• Charity must provide information on Schedule D

53

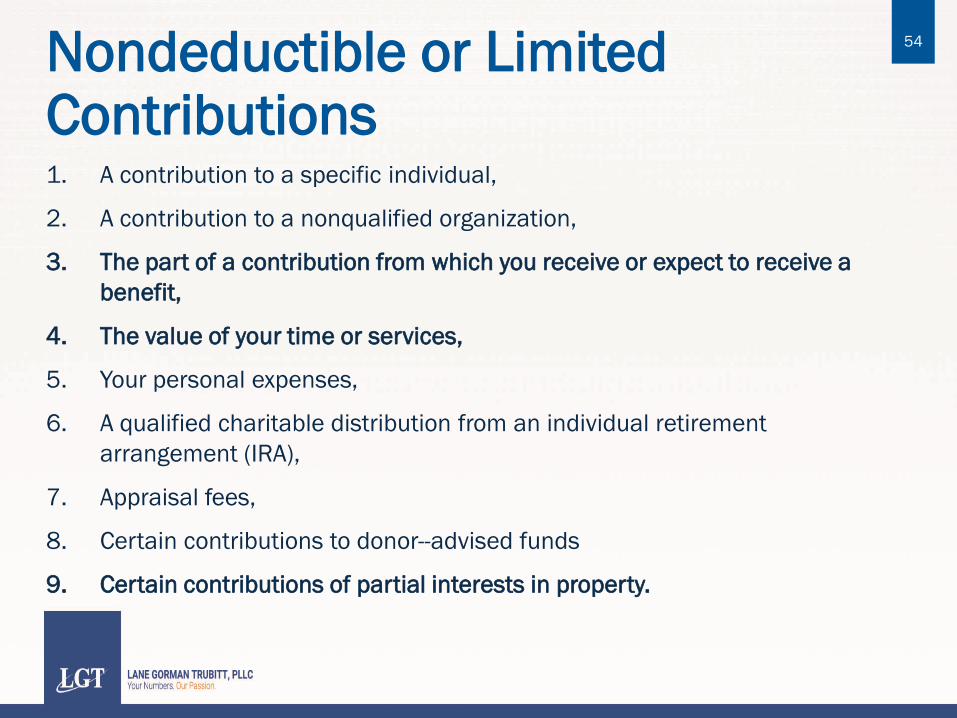

Nondeductible or Limited Contributions 1. A contribution to a specific individual,

2. A contribution to a nonqualified organization,

3. The part of a contribution from which you receive or expect to receive a

benefit,

4. The value of your time or services,

5. Your personal expenses,

6. A qualified charitable distribution from an individual retirement

arrangement (IRA),

7. Appraisal fees,

8. Certain contributions to donor-advised funds

9. Certain contributions of partial interests in property.

54

55

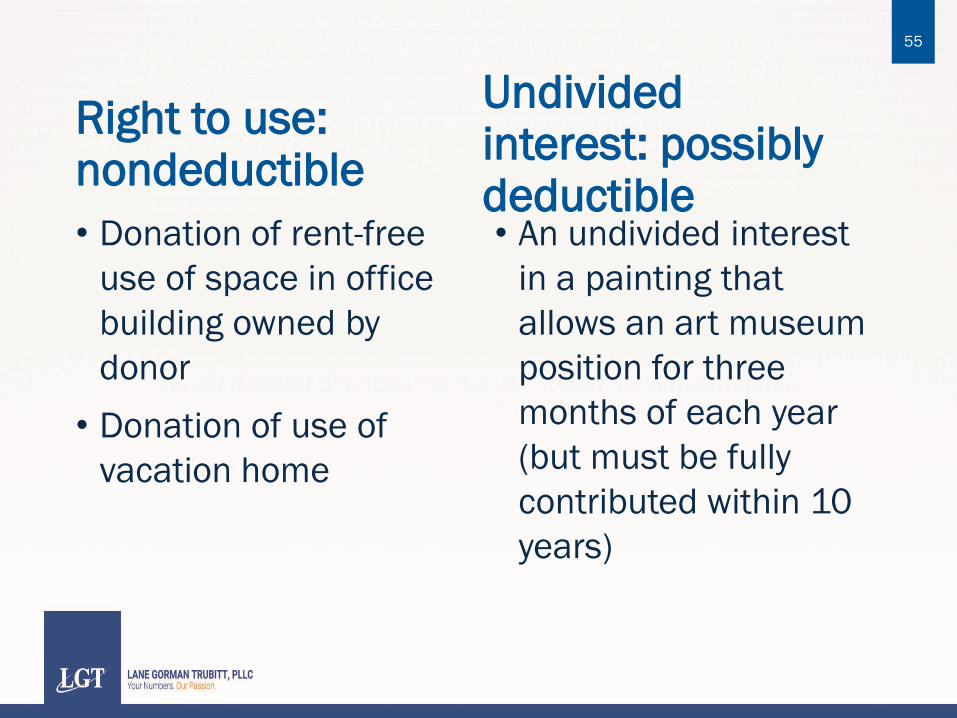

Right to use: nondeductible

• Donation of rent-free

use of space in office

building owned by

donor

• Donation of use of

vacation home

• An undivided interest

in a painting that

allows an art museum

position for three

months of each year

(but must be fully

contributed within 10

years)

Undivided interest: possibly deductible

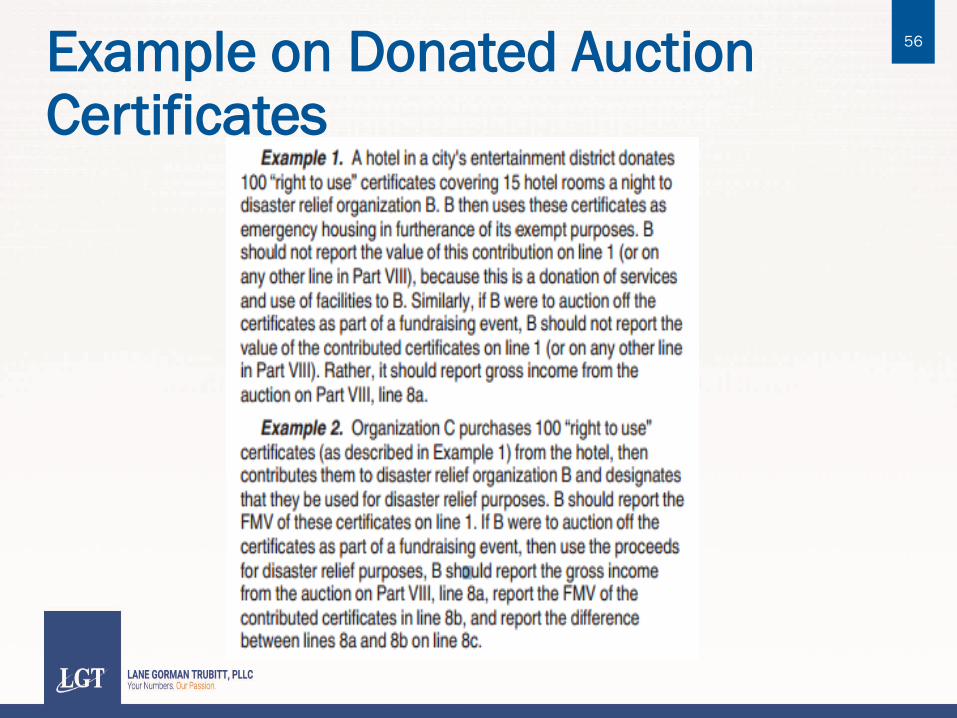

Example on Donated Auction Certificates

56

Contact Information

• Bruce Levi, CPA

• Partner, Not-for-Profit Group, Lane Gorman

Trubitt, PLLC

• 214-461-1411

57

IRS Resources

• Form 990 and instructions

• Schedule M and instructions

• Form 8283 and instructions

• Form 8282 and instructions

• Publication 561, Determining the Value of Donated Property

• Publication 526, Charitable Contributions

• Publication 1771, Charitable Contributions-Substantiation and Disclosure Requirements

• Publication 4302, A Charity’s Guide to Vehicle Donations

• Publication 598, Tax on Unrelated Business Income of Exempt Organizations

• Form 1098-C and instructions

58

Valuation Issues Gifts in Kind

Robert C. Brackett, CGMA, CPA, CVA, ICVS, MM

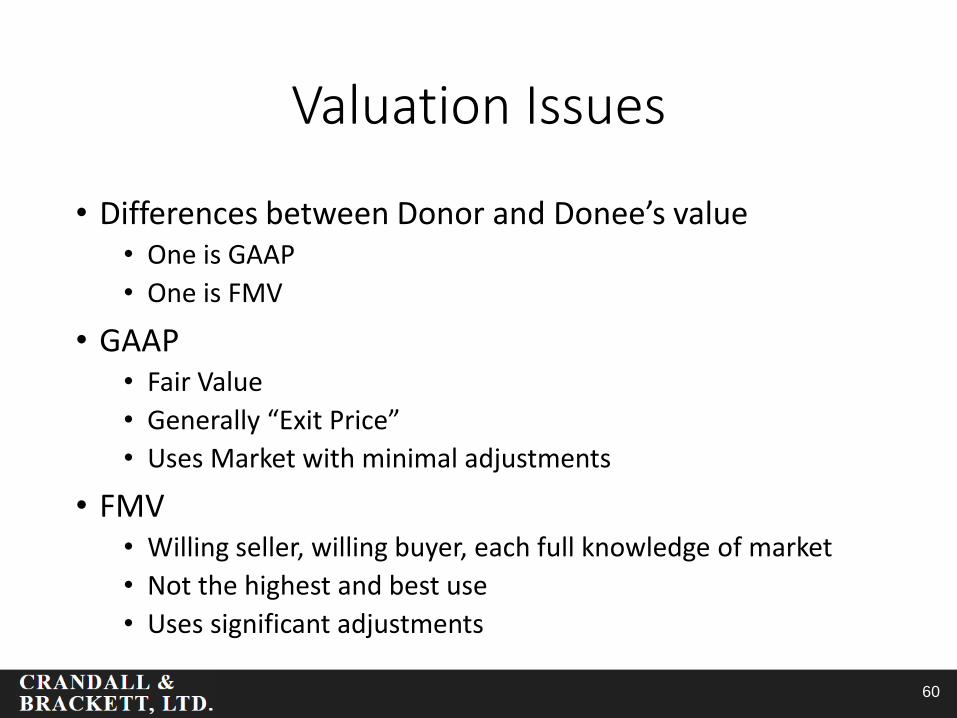

Valuation Issues

• Differences between Donor and Donee’s value • One is GAAP

• One is FMV

• GAAP • Fair Value

• Generally “Exit Price”

• Uses Market with minimal adjustments

• FMV • Willing seller, willing buyer, each full knowledge of market

• Not the highest and best use

• Uses significant adjustments

60

GAAP

• Exit price • Willing buyer, willing seller . . . . but the seller has no say in the value

• Little “Best Practices” in this area • We looked to AERDO

• Publish http://www.dochas.ie/Shared/Files/4/Gift_in_kind_Standards.pdf

• Focuses on Donee value • Primarily on Pharma, but written to be open

• AICPA http://www.berrydunn.com/uploads/55/doc/financial-reporting-whitepaper-measurement-of-fair-value.pdf

• ASC 820 codification of 157 http://www.fasb.org/cs/BlobServer?blobcol=urldata&blobtable=MungoBlobs&blobkey=id&blobwhere=1175822486936&blobheader=application/pdf

61

GAAP

• 2 major valuation related points/focus • Disclosure & documentation

• Valuing

62

GAAP

• Disclosures AERDO & GAAP (820-10-55-1): • Description of item or property, including sources and uses

(500 bales of used adult clothing, versus used adult clothing) • Valuation premise (GAAP & IRS differ dramatically) • Dates, of appraisal and of transfer • Consideration received (e.g. mktg, PR) • Identify both donor and donee (include relationship,

including NONE) • Description of valuation method used (detailed) • Financial data used in valuation (beginning, sources for

adjustments, etc) • Must be conclusion of value (AICPA) and Appraisal Report

(USPAP)

63

GAAP

• Disclosures (continued) • The principal market

• Market participants

• Judgments applied

64

GAAP

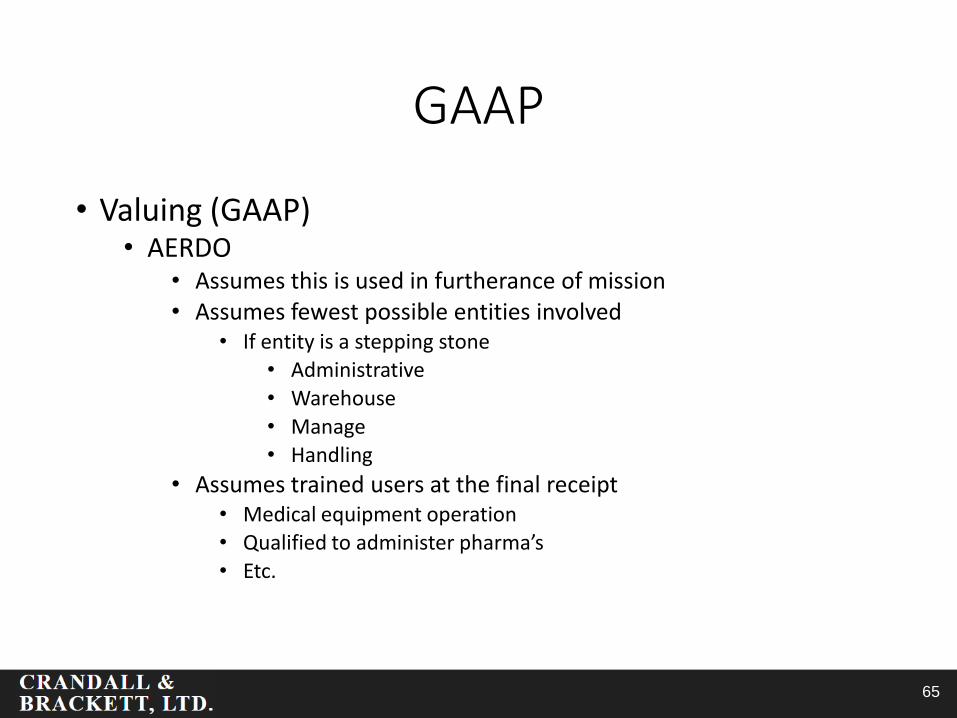

• Valuing (GAAP) • AERDO

• Assumes this is used in furtherance of mission • Assumes fewest possible entities involved

• If entity is a stepping stone • Administrative

• Warehouse

• Manage • Handling

• Assumes trained users at the final receipt • Medical equipment operation • Qualified to administer pharma’s

• Etc.

65

GAAP

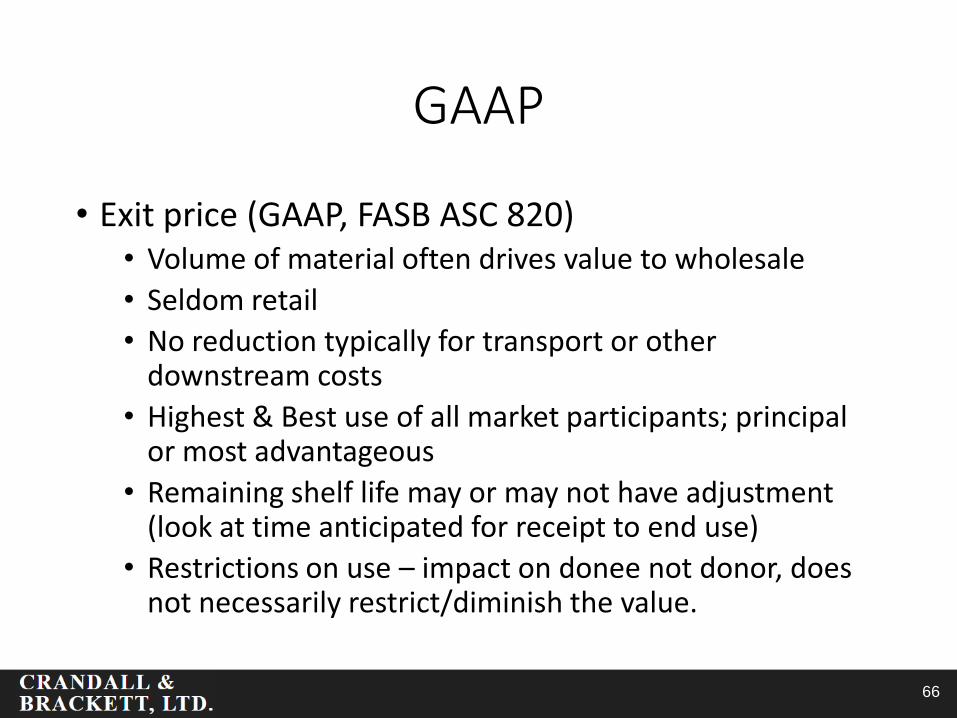

• Exit price (GAAP, FASB ASC 820) • Volume of material often drives value to wholesale

• Seldom retail

• No reduction typically for transport or other downstream costs

• Highest & Best use of all market participants; principal or most advantageous

• Remaining shelf life may or may not have adjustment (look at time anticipated for receipt to end use)

• Restrictions on use – impact on donee not donor, does not necessarily restrict/diminish the value.

66

GAAP

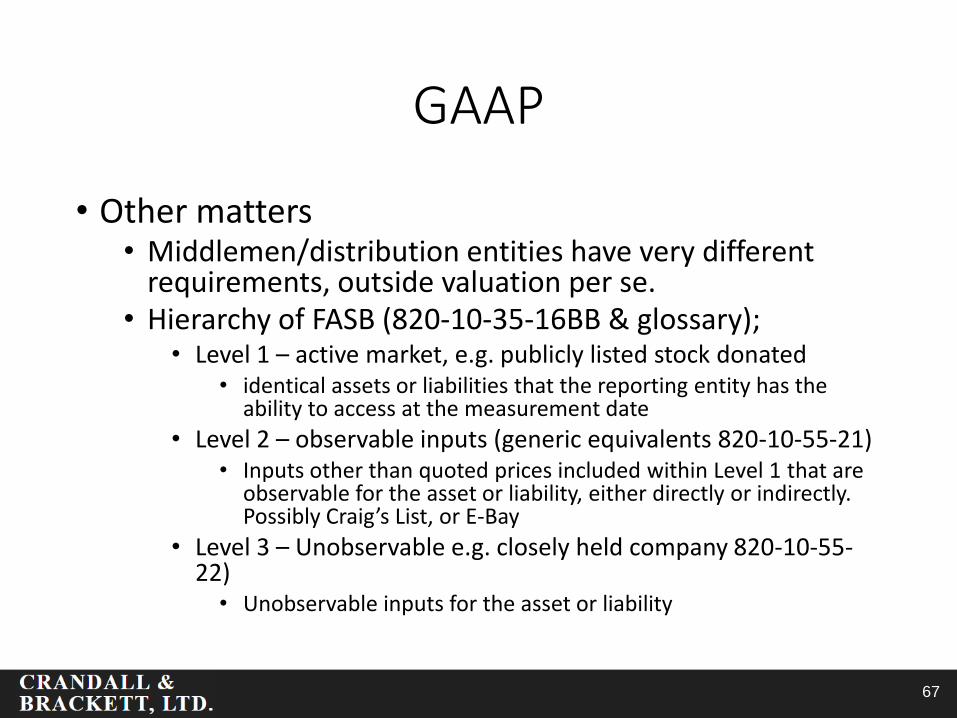

• Other matters • Middlemen/distribution entities have very different

requirements, outside valuation per se. • Hierarchy of FASB (820-10-35-16BB & glossary);

• Level 1 – active market, e.g. publicly listed stock donated • identical assets or liabilities that the reporting entity has the

ability to access at the measurement date

• Level 2 – observable inputs (generic equivalents 820-10-55-21) • Inputs other than quoted prices included within Level 1 that are

observable for the asset or liability, either directly or indirectly. Possibly Craig’s List, or E-Bay

• Level 3 – Unobservable e.g. closely held company 820-10-55-22)

• Unobservable inputs for the asset or liability

67

IRS

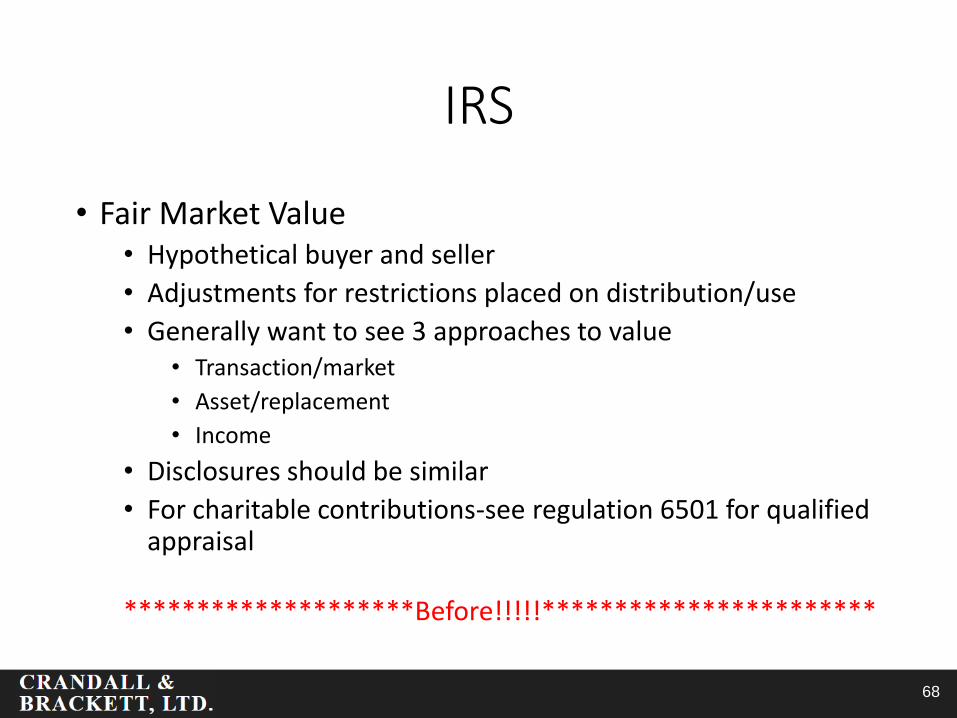

• Fair Market Value • Hypothetical buyer and seller

• Adjustments for restrictions placed on distribution/use

• Generally want to see 3 approaches to value • Transaction/market

• Asset/replacement

• Income

• Disclosures should be similar

• For charitable contributions-see regulation 6501 for qualified appraisal

********************Before!!!!!***********************

68

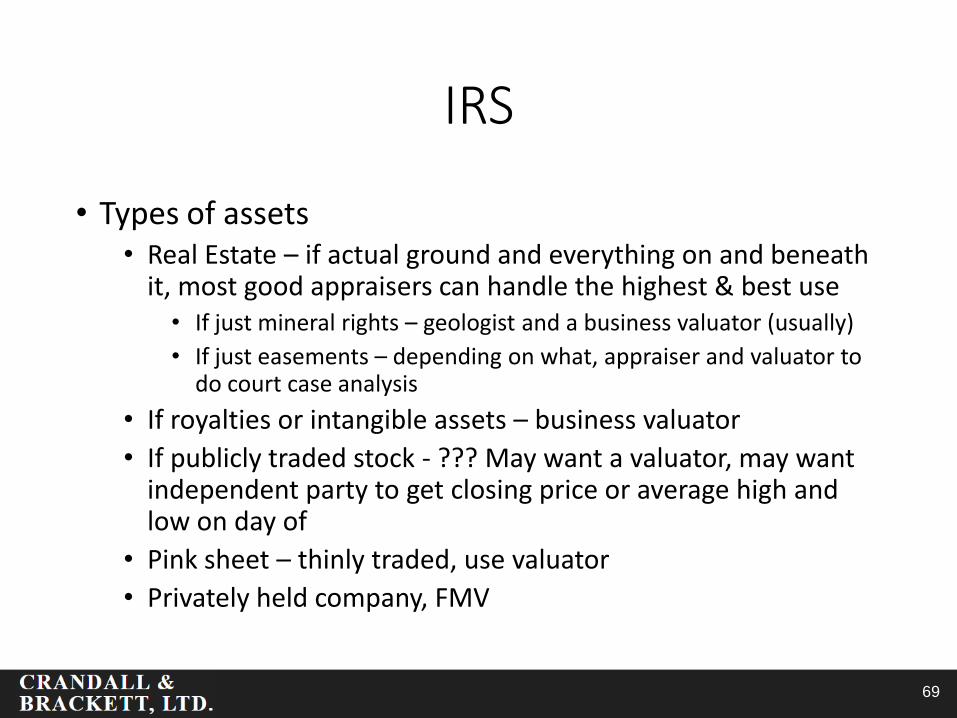

IRS

• Types of assets • Real Estate – if actual ground and everything on and beneath

it, most good appraisers can handle the highest & best use • If just mineral rights – geologist and a business valuator (usually)

• If just easements – depending on what, appraiser and valuator to do court case analysis

• If royalties or intangible assets – business valuator

• If publicly traded stock - ??? May want a valuator, may want independent party to get closing price or average high and low on day of

• Pink sheet – thinly traded, use valuator

• Privately held company, FMV

69

Summary

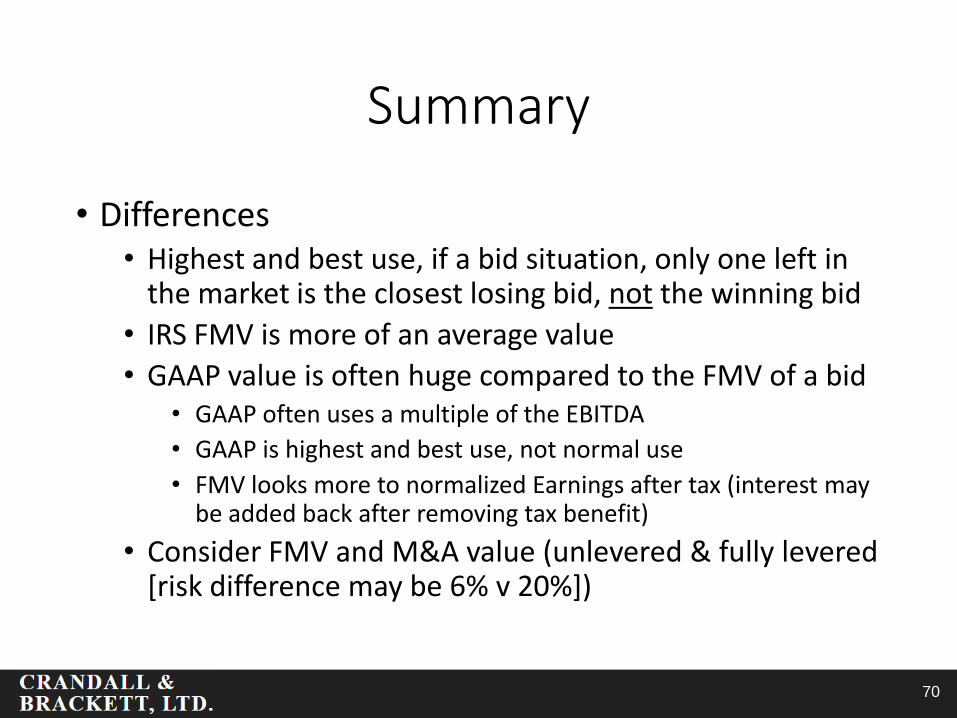

• Differences • Highest and best use, if a bid situation, only one left in

the market is the closest losing bid, not the winning bid

• IRS FMV is more of an average value

• GAAP value is often huge compared to the FMV of a bid • GAAP often uses a multiple of the EBITDA

• GAAP is highest and best use, not normal use

• FMV looks more to normalized Earnings after tax (interest may be added back after removing tax benefit)

• Consider FMV and M&A value (unlevered & fully levered [risk difference may be 6% v 20%])

70

Robert C. Brackett, CPA, ICVS, CVA, MM, CGMA

• Mr. Brackett has served as president of Crandall & Brackett, Ltd. since 1991. As a respected member of the profession, Mr. Brackett is active in professional organizations that provide training and standards setting for business valuators and fraud deterrence professionals. He is a founding member and Secretary General of the International Association of Consultants, Valuators, and Analysts (IACVA); the world’s largest association of business valuators and fraud deterrence professionals (more than 6,000 members in over 50 countries). Mr. Brackett also serves on the Standards Committee for the National Association of Certified Valuators and Analysts. He served on NACVA’s Executive Advisory Board until 1996 when he was elected to chair the newly established Membership Board, now past chairman. At the Illinois CPA Society, he served on various Business Valuation-related committees.

• Mr. Brackett has authored and taught courses in business valuation theory and practice through the Illinois CPA Foundation, the American Institute of CPAs, IACVA, and NACVA. Mr. Brackett’s professional credentials include: a Certificate of Educational Achievement in Business Valuations from the Illinois CPA Society, and the American Institute of Certified Public Accountants; as well as the International Certified Valuation Specialist designation awarded by IACVA. He maintains his CPA license, and has been awarded the Chartered Global Management Accountant (CGMA) designation by the AICPA.

• Mr. Brackett conducts seminars on valuations and ownership issues for many professional associations and business groups, and writes articles for monthly trade publications.

71