Embed Size (px)

Citation preview

1

IN THE COURT OF COMMON PLEASOF THE FIRST JUDICIAL DISTRICT OF PENNSYLVANIA

CIVIL TRIAL DIVISION

: William R. Liss : June 2001 : No. 2063 v. :

: Commerce Program Sheldon J. Liss, Liss Brothers, : Control No. 062237 Inc., Liss Global, Inc., Jeffrey : Waldman :

OPINION

Introduction

Petitioner William Liss (“William”) has filed a motion for the imposition of a receivership or

a constructive trust on a corporation, Liss Global, that was incorporated by his brother Sheldon Liss

(“Sheldon”) on February 21, 2001. Sheldon is the sole shareholder of Liss Global. William’s request

for the imposition of a receivership on Liss Global is linked to the contentious liquidation of another

corporation, Liss Brothers, Inc., in which William and his brother Sheldon were both 50 percent

shareholders.

Liss Brothers was incorporated in September 1976. Initially, the brothers consulted with

each other concerning the management of the company. Eventually, however, they engaged in

prolonged negotiations concerning the buy-out of William’s interests in Liss Brothers. Around 1997

William began to play an increasingly limited role in the work of the corporation, while continuing

to enjoy a substantial salary and benefits.

After many prosperous years, Liss Brothers became encumbered by bank debts and other

overhead. Although Sheldon attempted to secure additional financing, he was unable to do so. Liss

Brothers was liquidated after a meeting of the shareholders on February 13, 2001 and after receiving

notice by letter dated February 21, 2001 from Summit Bank that it was in default of its loan. Once

it became clear that liquidation was imminent, the defendant through his counsel urged selection of

1 Viener v. Jacobs, 2000 WL 33539470, 51 Pa. D. & C. 4th 260, *280 (Berks Cty. 2000),quoting Orchard v. Covelli, 590 F. Supp. 1548, 1550 (W.D. Pa. 1984), aff’d, 791 F.2d 916 (3d Cir.1986).

2 Testimony at the hearing will be identified as to the witness as “William” for William Lissor “Sheldon” for Sheldon Liss. Other witnesses will be identified by their surnames.

2

a third-party to oversee the process. Both brothers eventually agreed on a liquidator, who supervised,

inter alia, the sale of the corporate assets of Liss Brothers.

William now claims that a constructive trust or receivership must be appointed as to Liss

Global to protect his interests and those of the unsecured creditors of Liss Brothers. Numerous days

of hearings were held on this motion. Testimony revealed the painful breakdown of a business and

family relationship, suggesting how with closely-held corporations the “survival of the business

association is perilously tied to the continuing vitality of intimate personal relationships.”1 Both

brothers testified to a profound sadness at the liquidation of a company that they had devoted 27

years to building for themselves and their families. Yet their inability to agree on a buy-out contract

and their company’s severe economic problems led to the demise of Liss Brothers. For the reasons

set forth below, plaintiff’s request for imposition of a receivership or constructive trust on Liss

Global is denied.

Findings of Fact

The Parties

1. Plaintiff William R. Liss (“William”)2 is a fifty percent shareholder as well as Vice President,

Secretary and Treasurer of defendant Liss Brothers, Inc. 1/30/2002 N.T. at 13 (William);

Amended Complaint¶ 1; Answer, ¶1; Plaintiff’s Motion and Response thereto, ¶ 4.

2. Defendant Sheldon J. Liss (“Sheldon”) is William’s brother and the other fifty percent

shareholder of defendant Liss Brothers, Inc. Sheldon is the President of Liss Brothers.

1/30/2002 N.T. at 13 (William); Amended Complaint ¶2; Answer ¶2; Plaintiff’s Motion and

Response thereto, ¶ 6.

3

3. Sheldon and William were also fifty percent owners of a partnership, Sheldon J. Liss and

William R. Liss (the “Partnership”), which engages in real estate transactions. 1/30/2002 N.T.

at 44 (William). Until November 1, 2000, the partnership owned property located at 14501

Townsend Road where Liss Brothers conducted its business. The Partnership no longer

conducts business. 1/30/2002 N.T. at 44, 47 (William); Amended Complaint ¶5; Answer,

¶5; Defendants’ New Matter and Plaintiff’s Response thereto ¶ 5; Plaintiff’s Motion and

Response thereto, ¶ 8.

4. Defendant Liss Global, Inc. (“Liss Global”) is a corporation that was incorporated on

February 21, 2001. Sheldon Liss is the founder and sole shareholder of Liss Global. He is

also a director and officer of Liss Global. 1/31/2002 N.T. at 316 & 366 (Sheldon); Amended

Complaint, ¶ 6; Answer ¶6; Plaintiff’s Motion and Response thereto, ¶ 6.

5. Defendant Jeffrey Waldman (“Waldman”) is employed by defendant Liss Global as Chief

Financial Officer. He had also been Chief Financial Officer of Liss Brothers.1/30/2002 N.T.

at 42-43; Amended Complaint, ¶ 8; Answer ¶¶ 8 & 15.

The Creation and History of Liss Brothers, Inc

6. Liss Brothers, Inc. was incorporated on September 23, 1976. Amended Complaint ¶ 12;

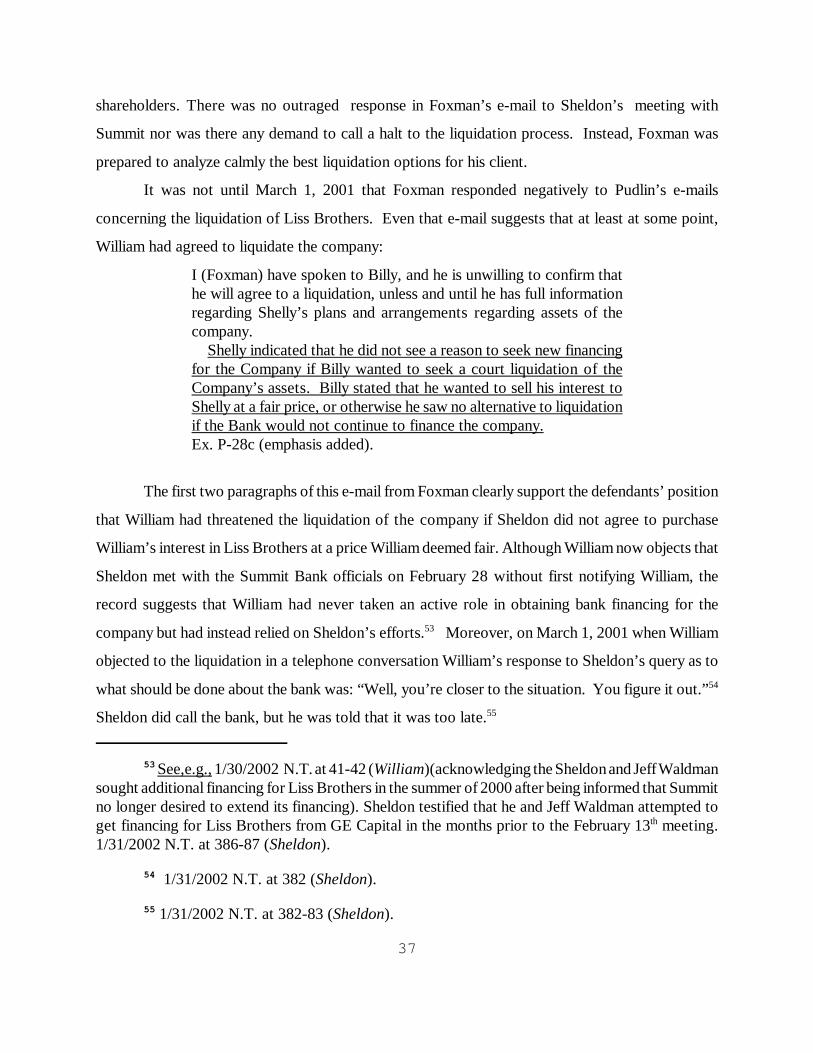

Answer, ¶ 12. Its operations consisted of purchasing, importing, and selling general

merchandise such as giftware, housewares, seasonal merchandise, hardware and novelties. Id.

See 1/30/2002 N.T. at 12-13 (William).

7. In the 1980s, Liss Brothers acquired a catalog candle business under the fictitious name

Robert Alan Candle Company through which it bought and sold candles. 1/30/2002 N.T. at

13 (William); Amended Complaint ¶ 13; Answer ¶ 13; Defendants’ New Matter and

Plaintiff’s Response thereto ¶¶ 1-3.

4

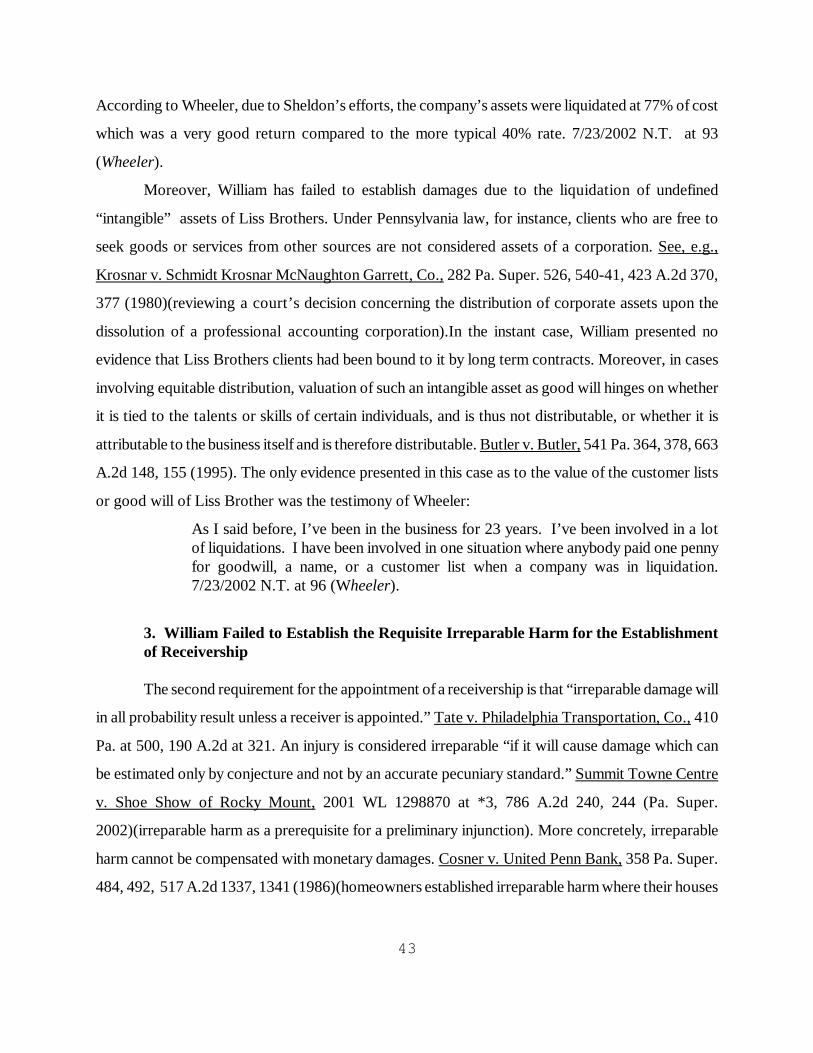

8. The By-Laws of Liss Brothers provide:

a. Art. III. Par. 7: “Special meetings of the shareholders may be called at any

time by the President, or the Board of Directors, or shareholders entitled to

cast at least one fifth of the votes which all shareholders are entitled to cast

at the particular meeting.”

b. Art. III. Par. 9 :“Written notice of a special meeting of shareholders stating

the time and place and object thereof, shall be given to each shareholder

entitled to vote thereat at least three days before such meeting . . ..”

c. Art. IV. Par. 6: “Special meetings of the Board may be called by the President

on 3 days’ notice to each director, either personally or by mail or by telegram;

special meetings shall be called by the President or Secretary in like manner

and on like notice on the written request of a majority of the directors in

office.”

d. Art. V. Par. 2: “The salaries of all officers and agents of the corporation shall

be fixed by the Board of Directors.”

e. Art. V. Par. 5: “The Secretary shall attend all sessions of the Board and all

meetings of the shareholders and act as clerk thereof, and record all the votes

of the corporation and minutes of its transactions in the book to be kept for

that purpose.”

See Ex. P-23.

9. At its peak, Liss Brothers employed over 100 people and occupied 400,000 feet of warehouse

space with over $40,000,000 in revenue. 1/30/2002 N.T. at 16 (William); Defendants’ New

Matter and Plaintiff’s Response thereto, ¶ 8.

10. William and Sheldon agree that initially after the incorporation of Liss Brothers, the brothers

regularly consulted with each other on the management of Liss Brothers concerning such

matters as salary increases and employment policies. Amended Complaint,¶ 18; Answer, ¶ 18.

11. Sheldon maintains that as President, he was charged with the management of Liss Brothers

5

but he regularly consulted with William until William refused to participate in the company’s

management and then began interfering with its operations. William contends that Sheldon

had a long-term scheme to take over control of Liss Brothers. Amended Complaint, ¶ 18;

Answer ¶ 18.

12. The parties agree that for many years William managed some of the internal affairs of Liss

Brothers, especially real estate matters and the warehouse. Sheldon maintains that beginning

around 1997 when Liss Brothers downsized its operations relating to close-out merchandise,

“William began to voluntarily withdraw as an active employee.” Amended Complaint, ¶ 19;

Answer, ¶19. He nonetheless maintained the authority and powers as a director and

shareholder. William, in contrast, maintains that his role in the company declined as “Sheldon

began to implement his scheme to take over control” of Liss Brothers. Amended Complaint,

¶19; Answer ¶ 19; 1/30/2002 N.T. at 14-18 (William).

13. In a March 9, 2000 Memorandum, Sheldon expressed dissatisfaction with William’s “level

of effort and productivity” as a 50% owner of Liss Brothers, Inc. This memorandum outlined

certain responsibilities and requested that William work on a full-time basis “which means no

less than 8:00 a.m. to 5:00 p.m. Monday through Friday.” See Ex. D-1; 1/30/2002 N.T. at

150 (William).

14. During the period addressed by Sheldon’s March 9th Memorandum, William concedes that

he typically arrived at work around 8:30 or 9:00 a.m. and then left “11:30, 12:00, 12:30, 1:00,

it would vary.”After leaving, he went “sometimes” to the country club but “not usually” to

make sales calls. 1/30/2002 N.T. at 154 (William). See also 1/30/2002 N.T. at 17

(William)(after the company downsized around 1997, William’s hours were from 8:30 to

12:00 or 1).

15. Through December 31, 2000, Sheldon received a salary of $330,000 and William received

$260,000. 1/30/2002 N.T. at 145 (William); 1/31/2002 N.T. at 230 (Sheldon). Liss Brothers

6

had a liberal expense reimbursement policy, which compensated some personal expenses of

both William and Sheldon. 1/31/2002 N.T. at 242-43 & 396-97 (Sheldon). William testified

that his total compensation package was approximately $400,000 when health benefits, car

payments and restaurant expenses were included. William stated that prior to January 2001

his restaurant expenses were paid whether or not they related to business. 1/30/2002 N.T. at

145-46 (William).

16. Sheldon had his salary increased by Liss Brothers effective January 1, 2001 by approximately

$40,000 with no increase for William.. 1/31/2002 N.T. at 230-234 (Sheldon).

17. No evidence was presented that Liss Brothers had long-term or exclusive agreements with

any of its suppliers, vendors or customers, including Rite Aid. See Ex. P-28f (e-mail from

Pudlin).

The Summit Bank Loan, The Sale of the 14501 Townsend Road Property and Investmentof the Sale Proceeds Into Liss Brothers in November 2000

18. Liss Brothers maintained various financing packages with lenders because of the general

nature of its business with its inventory requirements and marketing costs. Defendants’ New

Matter and Plaintiff’s Response thereto, ¶ 9; 2/21/2002 N.T.at 200-03 (Sheldon); 1/31/2002

N.T. at 372 (Sheldon) (describing lending relations with PNC and Summit Bank).

19. Liss Brothers entered into a loan and security agreement (“Bank Agreement”) with Summit

Bank (“Summit”) on March 3, 1999. 1/31/2002 N.T. at 372; 2/21/2002 N.T. at 201-02

(Sheldon); Ex. D-6.

20. Summit issued the following three separate loans to Liss Brothers pursuant to the Bank

Agreement:

(1) a working capital line of credit totaling six million five hundred thousand

dollars ($6,500,000);

7

(2) a letter of credit facility note totaling three million dollars ($3,000,000); and

(3) a term loan totaling four hundred seventy thousand one hundred dollars

($470,100).

The notes were secured by Liss Brothers, William and his wife, Sheldon and his wife as well

as by the partnership with, inter alia, personal guarantees and mortgages against real property.

Amended Complaint, ¶9; Answer, ¶ 9; Plaintiff’s Motion and Response thereto, ¶ 9; Ex. P-1,

Defendants’Admission 54.

21. Pursuant to the Bank Agreement, Summit held a mortgage on property located at 14501

Townsend Road, (“Townsend Road Property”) Philadelphia. Amended Complaint, ¶ 23(b);

Answer, ¶ 23(b). In the original loan documents, Summit required that the proceeds from a

sale of the real estate be invested into Liss Brothers up to $3,000,000 or returned to the bank.

Answer to Amended Complaint ¶ 27; 2/21/2002 N.T. at 193-97 (Sheldon); 1/30/2002 N.T.

128, 48 (William); Ex. D-6, ¶ 5.6.

22. Liss Brothers experienced severe financial problems during its fourth quarter of 2000.

Although in the first three quarters it made a profit of $400,000, it lost $700,000 in the fourth

quarter. 1/31/2002 N.T. at 395 (Sheldon).

23. William, likewise, acknowledged that around November 2000 Liss Brothers was in “very

deep debt.” 1/30/2002 N.T. at 130 (William). Sheldon believed it was crucial to sell the

Townsend Road property because vendors had to be paid and there were accounts past due.

2/21/2002 N. T. at 200 (Sheldon). William conceded that “Liss Brothers needed my portion

of the money in order to maintain the company, go forward, and pay down the vendors.”

1/30/2002 N.T. at 130-31 (William).

24. At the time when a purchaser for the Townsend Street Property had been found, William

objected to putting his share of the proceeds back into the company and insisted on a Sales

Proceeds Disposition Agreement. 2/21/2002 N.T. at 198 (Sheldon); 1/30/2002 N.T. at 47

8

(William).

25. William believed that Summit Bank would have permitted him to deposit his share of the net

proceeds from the sale of the Townsend Road property into a separate account at Summit

Bank under its control and as security for the outstanding notes. 1/30/2002 N.T. at 48-50,

128-29 (William).

26. William also conceded that under the Bank Agreement, Summit was entitled to require that

proceeds from the sale of the Townsend Road property should be invested back into Liss

Brothers to build up its assets. 1/30/2002 N.T. at 128, 48-50 (William).

27. To protect his interests and make sure that Sheldon “would not steal the money” that was

going back into the company, William entered into the Sales Proceeds Disposition Agreement

“so that when we did sell the property, instead me of putting the money in an account with

Summit Bank, I gave it to the company and in exchange he told me that certain things would

or would not happen based on my cooperation at that time.” 1/30/2002 N.T. at 47-48

(William); see also id. at 128-30. Simultaneously with the sale of the Townsend Road

property, William and Sheldon entered into a “Sales Proceeds Disposition Agreement” on

November 1, 2000. 1/30/2002 N.T. at 47 (William); 2/21/2002 N.T. at 198-99 (Sheldon);

Ex. P-4.

28. In November 2000, the Partnership sold the Townsend Road property. The proceeds from

that sale in the amount of two million eight hundred and sixty six thousand four hundred and

fifty six ($2,866,456) were invested by William and Sheldon into Liss Brothers as a capital

contribution. Plaintiff’s Motion and Response thereto, ¶21; 1/30/2002 N.T. at 63-64

(William); Ex. P-5.

29. William conceded that by “ me putting this money into the company and my brother putting

his money into the company, the company was able to pay the vendors that we owed a lot of

3 See 1/31/2002 N.T. at 218-19, 228, 240-41, 256 (Sheldon).

4 See 1/31/2002 N.T. at 227 & 243 (Sheldon).

5 1/31/2002 N.T. at 243-44 (Sheldon).

6 See e.g., 1/31/2002 N.T. at 218-19, 221-22, 257, 227, 262-64 (Sheldon).

9

money to and the company was able to continue on.” 1/30/2002 at 63 (William). William’s

attorney, Stephen Foxman (“Foxman”), acknowledged that William and Sheldon made equal

capital contributions to the company pursuant to their Bank Agreement. 5/9/2002 N.T. at

107, 109-112 (Foxman)( referencing Ex. D-6).

30. Liss Brothers continued to operate out of the Townsend Road Property after its sale pursuant

to a lease with the new owner. Under this lease, Liss Brothers occupied substantially less

space than it had prior to the sale of the property. The lease did not permit Liss Brothers to

occupy the space that had formerly been occupied as William’s office. Defendants’ New

Matter and Plaintiff’s Response, ¶¶ 32-34. After November 1, 2000, William still had an office

to use “because the person that bought the property who was upstairs was not moving into

that office until January or February. So I was able to use that; but my brother did not make

space for me in the new company.” 1/30/2002 N.T. at 65-66 (William).

31. During the period between May and December 2000, there was $188,027 charged to

Sheldon’s corporate account. See Exs. P-6 through P-13. Sheldon admitted to charging

personal expenses to the corporate credit account,3 clarified that some were charged by other

employees of Liss Brothers,4 some were business expenses or reimbursed expenses,5 but he

was often unclear as to the exact nature of a charge.6 Among the charges admitted to by

Sheldon were a family vacation trip to Florida, personal restaurant meals and a weekend trip

to New Orleans to visit his son in college. 1/31/2002 N.T. at 218-19; 221-22; 240-41

(Sheldon). During that same period, charges totaling $25,751 were listed for William. Exs.

P-6 through P-13.

10

32. In 1998, William borrowed money from Liss Brothers to pay for gambling debts. He also

conceded that his corporate credit card had been canceled because he had charged personal

airplane tickets to the company. Sheldon criticized these actions in an e-mail as improper and

detrimental to the company’s interests. 1/30/2002 N.T. at 167-69 (William); D-25 (e-mail

from Sheldon dated December 16, 1998).

33. Sheldon increased his own salary by 12% effective January 1, 2001. He stated that he did not

give William a raise then because “he didn’t work at the company.” 1/31/2002 N.T. at 234,

230 (Sheldon).

34. Sheldon acknowledged that there was a culture within the company that began when the

company was doing well in the late 1980's that permitted certain liberties as to charges. He

decided to put a stop to these practices effective January 2001. 1/31/2002 N.T. at 233-34,

242-43, 246 (Sheldon).

35. Sheldon therefore proposed a change in the company’s expense reimbursement policy under

which a clear business purpose had to be presented for an expenditure as a prerequisite for

reimbursement. 1/31/2002 N.T. at 396-97 (Sheldon).

36. After January 1, 2002, William’s salary remained the same but he no longer received the same

compensation for expenses. His corporate and gas credit cards were canceled. 1/30/2002

N.T. at 67 (William). No evidence was presented by plaintiff concerning Sheldon’s expense

charges after December 2000. See Exs. P-6 through P-19 (corporate account invoices from

May through December 2000).

Efforts to Buy Out the Interests of William Liss in Liss Brothers, Inc.

37. Since 1998, Sheldon and William actively discussed a buy-out of William’s interest in Liss

Brothers. 1/30/2002 N.T. at 17-19 (William).

11

38. According to Sheldon, beginning around May 1997 William did not participate actively in the

company’s operations but instead spent most of his time trying to sell or lease the Townsend

Road property, trading stocks on his computer, or doing transactions for Liss Realty, a

company William started in 1998 that was owned 100% by William and was distinct from Liss

Brothers. 1/31/2002 N.T. at 410- 412 (Sheldon).

39. On May 31, 2000 William and Sheldon signed a Letter of Intent (“Letter of Intent”), which

was hand written by Sheldon. The parties dispute whether this was a binding contract.

Amended Complaint, ¶ 29-31; Answer ¶ 29-31 & 34(a); Plaintiff’s Motion and Response

thereto, ¶ 10. See Ex. P-3.

40. The Letter of Intent was “between Sheldon Liss and William Liss regarding Sheldon

purchasing William’s 50% share of Liss Brothers.” Ex. P-3. The price set forth was

$3,200,000 with $1,000,000 at settlement and $2,200,000 paid equally over 11 years

beginning January 1, 2001. Ex. P-3. The Letter concluded:

*This agreement is subject to the preparation of an agreed final agreement of sale. Ex.P-3.

41. This court concluded that the Letter of Intent did not constitute a binding contract for

Sheldon to pay William $3,200,000 for his interests in Liss Brothers because the letter

explicitly stated that “this agreement is subject to the preparation of an agreed final agreement

of sale.” Liss v. Liss, 2002 WL 576510 at * 13 (Phila. Com. Pleas 2002).

See Ex. P-3.

42. Sheldon testified that around November 2000, he told William that Liss Brothers was not

doing well financially, and as a consequence, they had to think in different terms about the

buyout deal. 1/31/2002 N.T. at 214, 311 (Sheldon).

The February 13, 2001 Meeting

12

43. Sheldon and his attorney, David Pudlin, called for a meeting on February 13, 2001 at the

office of William’s attorney, Stephen Foxman. 1/30/2002 N.T. at 82 (William); 1/31/2002

N.T. at 346 (Sheldon).

44. According to Pudlin, the purpose of the meeting was to inform William about the financial

status of the company and especially about relations with the bank. 2/21/2002 N.T. at 139

(Pudlin).

45. Stephen Foxman, as counsel for William, assumed that the meeting was another attempt to

resolve the impasse between the brothers. 5/9/2002 N.T. at 6 (Foxman).

46. No formal notice of this meeting was sent out by the secretary, William. But, according to

Sheldon, William had never sent out any formal notice for a meeting in 27 years nor had he

prepared minutes in their entire years of doing business. 1/31/2002 N.T. at 348 (Sheldon).

Pudlin testified that in the two year period he had been doing legal work for Liss Brothers,

William had never signed corporate minutes. 2/21/2002 N.T. at 140-42 (Pudlin).

47. Minutes of the meeting were prepared by David Pudlin, but they were never sent to William.

2/21/2002 N.T. at 26-27 (Pudlin). According to Pudlin, the minutes were never shown to

Summit Bank but were merely placed in the file. 2/21/2002 N.T. at 103 (Pudlin). See Ex. P-

24.

48. According to Foxman and Pudlin, Sheldon opened the February 13th meeting by discussing

the poor financial status of Liss Brothers. He noted that the bank loan was coming due on

February 28 and that would be the end of the company. 2/21/2002 N.T. at 113-14 (Pudlin);

5/9/2002 N.T. at 11, 13-14 (Foxman).

49. At the meeting, Sheldon noted that Summit Bank desired to terminate its lending relationship

with Liss Brothers as of December 31, 2000, but it agreed to maintain its credit for an

13

additional two months until February 28, 2001 at the request of Sheldon and David Waldman.

2/21/2002 N.T. at 113 (Pudlin).

50. William was aware that Summit Bank wanted Liss Brothers to find a new lender. 1/30/2002

N.T. at 104 (William). He realized that February 28, 2001 or March 1, 2001 was a deadline

for Summit’s continued relationship with Liss Brothers. 1/30/2002 at 123-24 (William).

51. At the meeting, Sheldon proposed two scenarios to William that, in his opinion, would allow

Liss Brothers to continue its operations:

(1) Sheldon offered to buy out William’s interest in Liss Brothers for

$3,000,000 to be paid out over a ten year period; or

(2) The parties could maintain the status quo, with William continuing to

receive his salary and Sheldon keeping his raise.

Defendants’ New Matter and Plaintiff’s Answer thereto, ¶ 50; 1/30/2002 N.T. at 106-

09, 112, 82-87 (William); 1/31/2002 N.T. at 394-98 (Sheldon); 5/9/2002 N.T. at 11-

13 (Foxman) (according to Foxman, the proposal was presented by Pudlin).

52. William stated that when confronted with Sheldon’s proposal at the meeting, “[h]e mentioned

the fact that we could liquidate. I mentioned the fact that we could liquidate. On my point

of view, it was just a threat.” 1/30/2002 N.T. at 87 (William). See also 1/30/2002 N.T. at

112; 116-17; 200 (William).

53. Sheldon stated that when confronted with the two proposals, William rejected both and said

he would rather liquidate the company. 1/31/2002 N.T. at 361 (Sheldon). David Pudlin

likewise testified that “Billy not only rejected those proposals, but he said that he would rather

liquidate the company than accept those proposals.” 2/21/2002 N.T. at 110 (Pudlin).

54. Foxman testified that William would accept the proposal to maintain the status quo but

without a raise for Sheldon. According to Foxman, neither William nor he agreed to liquidate

14

the company. 5/9/2002 N.T. at 16 (Foxman). Foxman did concede that William stated he

wanted to sell his interests at a fair price or otherwise there was no alternative to liquidation.

5/9/2002 N.T. at 120 (Foxman).

55. Pudlin testified that at the meeting, he and Foxman discussed the need for a liquidation plan

to present to the bank so that Liss Brothers could control the liquidation rather than the bank.

He said that they also discussed the need for an outside liquidator. 2/21/2002 N.T. at 116

(Pudlin).

56. William conceded that he was told at this meeting by Sheldon’s attorney, David Pudlin, that

if the company liquidated either brother would be free to deal with former customers and

vendors of Liss Brothers. 1/30/2002 N.T. at 114-116 (William). See also 1/31/2002 N.T. at

363-64 (Sheldon).

57. After the February 13th meeting, Sheldon began to put together a liquidation plan for Liss

Brothers that had to be completed prior to the meeting with Summit Bank on February 27.

1/31/2002 N.T. at 317-18, 324-25 (Sheldon). See Ex. P-21.

58. Foxman stated that he had several telephone conversations and e-mail exchanges with Pudlin

after the February 13th meeting during which Pudlin would bring up liquidation and discuss

the choice of a liquidator. Foxman stated that he did not think that liquidation would occur

at that point but he did not know what actions the bank might take regarding its loan.

5/9/2002 N.T. at 19-20 (Foxman).

59. On February 19, 2001, Pudlin sent an e-mail to Foxman which began by stating “As you and

I discussed, now that Billy and Shelly have agreed to liquidate and dissolve the company, it

is important that the process be moved along quickly because our lending facility with Summit

Bank is expiring on 2/28/01.”Ex. P-28(a)(e-mail). Foxman concedes that he received the e-

mail. 5/9/2002 N.T. at 73-74 (Foxman). Although Foxman admitted that he understood the

15

e-mail as referring to a liquidation, he did not respond to it or indicate that William opposed

liquidation. Id. at 74-76 (Foxman).

60. By letter dated February 21, 2001 from Summit to Liss Brothers, the bank gave “notice to

you that an Event of Default currently exists under the Loan Agreement as a result of

Borrower’s failure to comply with certain of the financial covenants set forth therein.” The

letter indicated that copies were sent to both Sheldon and William. Ex. D-70.

61. Pudlin sent another e-mail to Foxman on February 27, 2001 about the letter of default from

Summit Bank and Sheldon’s meeting with Summit Bank officials on that day. Pudlin informed

Foxman that:

At that meeting, Shelly gave an update to Summit, which necessarily included theagreement of Billy and Shelly to liquidate the company. In anticipation of Summit’scalling of the loan, Shelly had prepared a plan of orderly liquidation, and he presentedit to Summit today.Ex. P-28b.

Pudlin also noted that Shelly presented the idea of having a third party liquidator and

referenced a company “whose brochure I had delivered to you 2/21/01.” Ex. P-28b. Foxman

conceded that he received that brochure/resume. 5/9/2002 N.T. at 78 (Foxman); Ex. D-16.

62. On February 28, 2001, Foxman admits he sent the following e-mail to Pudlin:

I will try to find out Billy’s position on that -- I had sent him the brochure thatyou mailed to me and he called to discuss it but we have not had a chance to considerpotential other liquidators who may have experience in this particular line of business(i.e. the Liss Bros. business).

I am wondering whether it makes the most sense to liquidate under the gunfrom Summit, or to attempt to line up a new lender in the interim, so that theliquidation process can be conducted in a way that will bring the highest return toBilly and Shelly.

Assuming liquidation, now or in the future, what is Shelly going to do?Obviously, certain “assets” of the Company will benefit him if he is intending to gointo the same business, and it would be a matter of some concern to Billy tounderstand Shelly’s plans, and how he would compensate the Company for takingover continuing contracts, equipment, space, etc. I think we need some ground rulesin this area to make Billy comfortable with proceeding with the liquidation on an

16

agreed basis, without appointment of an outside liquidator. Ex. P-28e; 5/9/2002 N.T.at 90-92 (Foxman)(emphasis added).

63. Foxman stated that as late as this February 28 e-mail, which was 15 days after the February

13th meeting, he had never told Pudlin, Sheldon or Summit Bank that William was opposed

to liquidation despite the e-mails from Pudlin. 5/9/2002 N.T. at 92 (Foxman).

64. On February 28, 2001, Pudlin sent Foxman another e-mail requesting a final decision on a

liquidator. Pudlin responded to Foxman’s reference to “new purchases” by stating that there

would be none since the company was liquidating. He informed Foxman that Liss Brothers

had no continuing contracts with customers other than Rite Aid which had the right to

terminate on 30 days notice for any reason. Ex. P-28f.

65. William stated that he was not notified about Sheldon’s visit to Summit Bank of February

26, 2002 (sic) to inform it about the plan to liquidate Liss Brothers. 1/30/2002 N.T. at 89-90.

66. On March 1, 2001, Foxman sent Pudlin an e-mail in which he stated that William did not want

to go through with the liquidation of Liss Brothers “unless and until he has full information

regarding Shelly’s plans and arrangements regarding assets of the company.”Ex. P-28c.

Foxman conceded that this was the first time he had written Pudlin that William opposed

liquidation. 5/9/2002 N.T. at 104-05 (Foxman)

67. One day later, Foxman sent an e-mail to Pudlin which stated that “I am at a loss to understand

how a meeting at which Shelly and Billy exchanged proposals with each other has been turned

into a purported agreement to liquidate the Company.” Ex.P-28(d); 2/21/2002 N.T. at 82

(Pudlin). From the date of this March 2, 2002 e-mail, Pudlin realized that liquidation was a

contentious matter. 2/21/2002 N.T. at 83 (Pudlin).

68. According to Sheldon, he did not learn that William opposed liquidation until after the

meeting with Summit Bank and around March 1. At that point, William did not suggest any

17

options to liquidation but expected Sheldon to come up with solutions. 2/21/2002 N.T.at 207-

09, 218-20 (Sheldon).

69. Sheldon expressed surprise to William that he had not been contacted earlier, especially since

their attorneys had been discussing liquidation. Sheldon, nonetheless, told William that he

would contact the bank, but when he did Sheldon was told that it was too late and “as far as

we’re concerned you guys are out of here in 90 days and that’s it.” 1/31/2002 N.T. at 381-83

(Sheldon).

70. Foxman also contacted the bank at this point and was told there was no way to go back.

5/9/2002 N.T. at 44 (Foxman).

71. Counsel for William and Sheldon discussed potential liquidators and the parties agreed on the

selection of Robert Wheeler as liquidator. Defendants’ New Matter and Plaintiff’s Answer,

¶ 63.

72. Robert Wheeler met with William and Sheldon in early March 2001, at which point William

agreed to Wheeler serving as the liquidator. 7/23/2002 N.T. at 89 (Wheeler).

73. Wheeler stated that Sheldon assisted in the liquidation process by meeting with customers and

assisting in collection matters. Sheldon was available “full-time” and “Shelly’s efforts almost

doubled what would be expected in a liquidation.” William, in contrast, offered no assistance.

7/23/2002 N.T. at 92-94 (Wheeler). William’s “concern was with a continuation of his salary

and a payment of a loan that was a personal, the proceeds of which he had put into the

company.” Id. at 90.

74. According to Wheeler, due to Sheldon’s efforts, the company’s assets were liquidated at 73%

of cost which is a very good return since a 43% rate is more typical. 7/23/2002 N.T. at 93

(Wheeler).

18

75. Sheldon purchased assets from Liss Brothers such as computers and furniture. The price,

however, was set by an outside auctioneer and then the price was adjusted up. William was

kept informed of this process. 7/23/2002 N.T. at 94-95 (Wheeler).

76. Wheeler in his 23 years of experience with liquidations was unaware of “one situation where

anybody paid one penny for goodwill, a name or a customer list when a company was in

liquidation.” 7/23/2002 N.T. at 96 (Wheeler).

77. As a result of the liquidation, the bank was paid but the 1.5 million in unsecured debt was not.

7/23/2002 N.T. at 122-23 (Wheeler).

78. According to Sheldon, in May 2001 William refused to cooperate with Summit Bank

regarding liquidation documentation. Consequently, a hearing was held and the bank assumed

control of the liquidation. 2/21/2002 N.T. at 191 (Sheldon).

Creation of Liss Global

79. On February 21, 2001, Sheldon incorporated Liss Global. Defendants’ New Matter and

Plaintiff’s Answer, ¶ 69; 1/31/2002 N.T. at 319 (Sheldon). Sheldon testified that he began

planning for the creation of this new company after the February 13 meeting. 1/31/2002 N.T.

at 319 (Sheldon).

80. William is not an employee, director or shareholder of Liss Global. Defendants’ New Matter

and Plaintiff’s Answer thereto, ¶ 72.

81. Sheldon maintains that while Liss Global’s operations are similar to those of Liss Brothers

there are significant differences: Liss Global does not warehouse significant amounts of

product and consequently occupies less space; its credit package is significantly lower than

that of Liss Brothers. William, in contrast, denies that these two companies are significantly

19

different. Defendants’ New Matter and Plaintiff’s Response thereto, ¶73.

82. Approximately one-third of the business income for Liss Brothers in 2000 came from dealings

with Rite Aid. 1/31/2002 N.T. at 332-33 (Sheldon). No evidence was presented to contradict

defendants’ assertion that Liss Brothers had no continuing contracts with customers and that

the Rite Aid contract gave it the right to terminate at any time for any reason on 30 days

notice. Ex. P-28(f).

83. Deposition testimony of Rite Aid employees presented by plaintiff indicated that they had had

no relationship whatsoever with William; instead, their contacts were with Sheldon or other

Liss Brother employees. See Ex. P-2A (Depo. of Steven Moss at 6 stating “absolutely no

working relationship with Billy at all”); Ex. P-2B (Depo. of Steve Koch at 6 stating that he

did not know Billy); Ex. P-2C (Deposition of Bryan Shirtliff at 6 & 18 stating that he did not

know William but Sheldon offered particular expertise).

84. Liss Global has between 21 to 23 employees and, according to Sheldon, it is on good terms

with the banks. 2/21/2002 N.T. at 216 (Sheldon). Plaintiff presented no evidence to the

contrary.

Procedural History

85. William Liss filed a complaint against Sheldon in June 2001, and thereafter filed an Amended

Complaint asserting the following claims: Breach of Fiduciary Duty(I); Breach of Written or

Oral Contract to Purchase William Liss’ Interest in Defendant Liss Brothers (II); Breach of

Duty to Negotiate in Good Faith Pursuant to the Letter of Intent (III); Promissory Estoppel

(IV); Conversion (V); Fraud (VI); Intentional Misrepresentation (VII); Appointment of a

Custodian/Receiver(VIII); Appointment of a Constructive Trust (IX); Claim against Jeffrey

Waldman as Co-conspirator (X)..

20

86. Defendants filed preliminary objections to this Amended Complaint, which were granted in

part and overruled in part. This court dismissed Counts II and III of the Amended Complaint

with a detailed analysis because William failed to plead an enforceable agreement based on

the attached May 31, 2000 Letter of Intent. Liss v. Liss, 2002 WL 576510 at *11-14 (Phila.

Com. Pleas 2002). See Ex. P-3. It concluded that the bare allegations in Count VIII for the

appointment of a receiver survived the demurrer. Id. at *14.

87. Plaintiff also filed a Motion for the Appointment of a Receiver and Imposition of a

Constructive Trust as to defendant Liss Global, Inc. A series of hearings were held on this

Motion beginning January 30, 2002 through July 23, 2002. Thereafter, the parties submitted

supplemental briefs and proposed findings of fact and law.

Legal Analysis

I. William Liss Has Not Satisfied the Criteria for Imposition of a Receivership on LissGlobal

A. Requirements for Imposition of a Receivership

The appointment of a receiver is a harsh remedy that is typically imposed only as a last resort.

Mayhue v. Mayhue, 336 Pa. Super. 188, *193, 485 A.2d 494, *497 (1984). As the Pennsylvania

Supreme Court has observed, “[t]here is nothing . . . which affects a corporation with such serious

consequences” since “the appointment is a distress signal, and is immediately followed by lowering

of financial credit and a general readjustment.” McDougal v. Huntingdon & Broad Top Mountain

Railroad & Coal Co., 294 Pa. 108, 117, 143 A. 574, *577-78 (1928). Especially for a solvent

corporation, the appointment of a receiver can cause stigma to the ongoing business. Hankin v.

Hankin, 507 Pa. 603, 612-13, 493 A.2d 675, 679 (1985). Under Pennsylvania law, a receivership

is imposed on a solvent corporation as a drastic remedy that should be granted when the following

criteria are met:

(a) only when the right to a receivership is clear, and(b) irreparable damage will in all probability result unless a receiver is

7 Plaintiff’s Motion, Wherefore Clause.

8 See Plaintiff’s 9/30/2002 Proposed Findings of Law, ¶ 1(invoking 15 Pa.C.S.A. §1767).

21

appointed, and (c) a receivership will not substantially injure or interfere with the rights of creditorsand stockholders, and (d) greater damage will result if a receiver is not appointed than if one isappointed.Tate v. Philadelphia Transportation Co., 410 Pa. 490, *500, 190 A.2d 316,*321 (1963).

The Pennsylvania Supreme Court has also cautioned that “a receiver will not be appointed

unless it appears that the appointment is necessary to save the property from injury or threatened loss

or dissipation.” Credit Alliance Corp. v. Philadelphia Minit-Man Car Wash Corp., 450 Pa. 367, 372,

301 A.2d 816, 818-19 (1973). A receivership is not imposed merely because one party has a claim

against another. DeAngelis v. Commonwealth Title Ins. Co., 467 Pa. 410, *414, 358 A.2d 53, *55

(1976)(court erred in appointing a receiver on petition on non-lien holding judgment creditors). In

addition, courts require that “a receiver will be appointed only in aid of some recognized, presently

existing right, and no appointment will be made in a case where receivership is the sole remedy”

sought. Tate, 410 Pa.. at * 500, 190 A.2d at *321. See also Northampton National Bank v. Piscanio,

475 Pa. 57, 62, 379 A.2d 870, 872 (1977).

1. On the Record Presented, Petitioner Failed to Establish His Interest in Liss Global

As a threshold matter, therefore, William must establish a “presently existing right” in Liss

Global to justify the imposition of a receivership upon it. William has conceded that he is not a

shareholder of Liss Global. See Amended Complaint, ¶ 6 and Motion, ¶ 6 (stating that Sheldon is

the sole shareholder of Liss Global). He contributed no capital to Liss Global nor does he assert any

judgment against it. Nonetheless, William argues that a receiver should be imposed on Liss Global

under Pa. Rule of Civil Procedure 15337 and 15 Pa.C.S.A ¶ 1767.8

Pennsylvania Rule of Civil Procedure 1533 provides for the appointment of a receiver when

“required by the exigencies of the case.” Pa.R.C.P. 1533. Section 1767, in contrast, is more narrowly

9 See Liss v. Liss, 2002 WL 576510 at n. 4 (Phila. Com. Pleas 2002)(noting that § 1767 doesnot apply as to Liss Global “because William does not legally have shares in Liss Global which iswholly-owned by Sheldon”). This court noted, however, that Pa.R.C.P. 1533 was more properlyinvoked because William’s claim is general and equitable in nature. Id.

22

defined to be invoked by “shareholders” since it provides:

§ 1767. Appointment of custodian of corporation on deadlock or other cause

(a) General rule - Except as provided in subsection (b) upon application of anyshareholder, the court may appoint one or more persons to be custodians of and forany business corporation when it is made to appear that:(2) in the case of a closely held corporation, the directors or those in control of thecorporation have acted illegally, oppressively or fraudulently toward one or moreholders or owners of 5% or more to the outstanding shares of any class of thecorporation in their capacities as shareholders, directors, officers or employees. . .

15 Pa.C.S.A § 1767 (emphasis added).

On its face, section 1767 can be invoked only by a shareholder of a corporation who seeks

the appointment of a receiver on his or her corporation.9 It would therefore be inapplicable to Liss

Global, since only Sheldon –and not William – is a shareholder of that corporation. Moreover, the

acts by Sheldon that William focuses on as the basis for the imposition of a receivership on Liss

Global relate primarily to Sheldon’s actions as a shareholder of Liss Brothers. William, for instance,

states that a receiver should be appointed on Liss Global because Sheldon breached his fiduciary

duties towards William as a 50% shareholder of Liss Brothers due to the following actions when

Sheldon:

a. exercised total control over defendant Liss Brothers and freezing William out of theday to day operations of defendant Liss Brothers by eliminating William’s office andcomputer access;

b. terminated William’s corporate benefits (and ultimately his salary when defendantSheldon liquidated defendant Liss Brothers);

c. granted himself an annual salary increase of $40,000 from $330,000 per year to$370,000 per year;

d. charged $188,027.00 to defendant Sheldon’s corporate credit card from May 2000until December 2000 which included extravagant charges for personal expenses;

10 See Plaintiff’s 9/30/2002 Proposed Findings of Fact and Conclusions of Law, II, ¶ 1. See,also Plaintiff’s 10/7/2002 Memorandum at 14.

11 Leech, 762 A.2d at 718. The receivership in Leech was imposed pursuant to 15 Pa.C.S.A§ 1767 on Leech Tool & Die, Inc. which was a closely owned corporation with two 50%shareholders who were brothers pursuant to a petition by one of the shareholders. Leech Tool & Die,Inc. had entered into an agreement with Leech Industries, Inc. which was incorporated for thepurpose of ultimately becoming the operating company for the Leech Tool & Die, Inc. Thereceivership over Leech Tool & Die, Inc.was sought after one of its 50% shareholders left the employof Leech Industries, Inc. which resulted in the other shareholder of Leech Tool & Die, Inc. deprivinghim of certain corporate benefits, information and responsibilities. The key fact, however, is that thereceivership was sought by a shareholder of the company at issue.

23

e. prepared a liquidation plan for defendant Liss Brothers;

f. presented the liquidation plan of defendant Liss Brothers to Summit Bank; and

g. caused the transfer of the entire business of defendant Liss Brothers to defendant LissGlobal for non consideration.

Plaintiff’s 9/30/2002 Proposed Findings of Fact and Conclusions of Law, II, ¶1.

Significantly, all of these allegedly oppressive acts by Sheldon relate to Liss Brothers except

for the averrals in paragraph (g) that Sheldon caused the transfer of the entire business of Liss

Brothers to Liss Global for no consideration. William cites a number of cases to support his claim

that a receiver must be appointed under section 1767 or Rule 1533 to oversee Sheldon’s operation

of Liss Global: Mayhue v. Mayhue, 336 Pa. Super. 188, 485 A.2d 494 (1984); Leech v. Leech, 2000

Pa. Super. 334, 762 A.2d 718 (2000); Arc Manufacturing Co., Inc. v. Konrad, 321 Pa. Super. 72,

467 A.2d 1133 (1983); and Viener v. Jacobs, 61 Pa.D. & C. 4th 260 (Berks Cty. 2000).10

These cases are inapposite, however, because in each the plaintiff had a direct interest in the

corporation or legal entity over which a receivership was requested. In Leech v. Leech, for instance,

a receivership was imposed on a closely-held corporation at the request of one of its 50%

shareholders under 20 Pa.C.S.A. § 1767 due to the oppressive acts of the other 50% shareholder.11

Hence, Leech might be invoked for the imposition of a receivership on Liss Brothers, but it does not

apply in the instant case where a nonshareholder is seeking a receivership on Liss Global.

Likewise, in the case of Arc Manufacturing Co., Inc. v. Konrad, a receivership was imposed

12 Similarly, the fourth case cited by William, Viener v. Jacobs, 51 Pa. D.& C. 4th 260 (BerksCty. 2000) involved a minority shareholder’s request, inter alia, for a receivership on the twocorporations in which he was a shareholder. The plaintiff abandoned this request after thecorporations entered into bankruptcy. Id., at *284 & *286.

24

on a corporation at the request of one of its three shareholders during the pendency of litigation over

his removal as president of the corporation. The Superior Court approved the appointment of this

receiver as an attempt to “preserve a business which somehow prospered despite the conflicts among

its owner/operators.” Arc Manufacturing, 321 Pa. Super. at *82, 467 A.2d at *1138. In the present

case, in contrast, William does not seek a receivership to preserve the corporation that he owned with

Sheldon. Rather, he seeks to impose it on a corporation with only Sheldon as its shareholder.12

The other appellate case cited by William, Mayhue v. Mayhue, is inapposite since it deals with

the appointment of a receiver to prevent the fraudulent misappropriation of marital property under

the Divorce Code, 23 P.S. § 403 & 401. Mayhue, 336 Pa. Super. at 191, 485 A.2d at 495. In

concluding that a receivership was properly imposed on defendant husband’s company after he

allegedly diverted funds from a company that he had operated with his former wife, the Mayhue court

observed:

Here, however, the receiver has not been appointed to protect the rights of anordinary creditor but, rather, has been appointed to protect the interests of a spousein marital property. We cannot conceive of a clearer factual situation justifyinginjunctive relief and the appointment of a trustee in receivership. The appellant hasappropriated marital property and has been held in contempt several times for refusingto comply with court orders. His conduct has demonstrated that his clear purpose wasto dispose of or hide such property in which his wife might have a marital interest.Mrs. Mayhue’s need for injunctive relief was clear, immediate and necessary in orderto prevent greater injury.Mayhue, 336 Pa. Super. at 194, 485 A.2d at *497(emphasis added).

Mayhue is thus distinguishable not only because it involves a receivership imposed under the

divorce code to protect marital property but because one of the parties had been found by a court to

have misappropriated property. Although William has broadly alleged that Sheldon engaged in a

scheme to trick and defraud William by transferring William’s interests in Liss Brothers to Liss

13 See, e.g., Amended Complaint, ¶ 32; Plaintiff’s 1/28/2001 Motion at 5; Plaintiff’s10/7/2002 Memorandum at 13 (“Sheldon robbed the company of its business”).

14 In a prior opinion focusing on preliminary objections to Count VIII of the AmendedComplaint seeking the appointment of a receiver for Liss Global, this court concluded that theallegations of oppression were sufficient to survive a demurrer. Liss v. Liss, 2002 WL 576510, at(Phila.Ct. Common Pleas 2002). The present motion seeking the appointment of a receiver has beensupplemented with a factual record consisting of hearing testimony and relevant documents. Thepresent factual record upon analysis does not support the imposition of a receivership on Liss Global.

15 See, e.g., Plaintiff’s 6/28/2001 Memorandum at 5-6; Amended Complaint, ¶ 32.

16 In analyzing the imposition of a receiver under Pa.R.C.P. 1533, the Court in Northamptonv. Piscanio, 475 Pa. 57, *62, 379 A.2d 870, 872 (1977) emphasized that receivers are “appointedonly in aid of some recognized, presently existing legal right... .”

25

Global,13 for the reasons set forth below the record presented by William does not support a claim

that a receivership must be appointed over Liss Global to prevent the misappropriation of his interests

without consideration.14

2. On the Present Record, Petitioner Failed to Establish That His Right to aReceivership Is Clear Based on Sheldon’s Alleged Wrongdoing in the Liquidation ofLiss Brothers

A central theme of William’s request for the imposition of a receivership on Liss Global is

that Sheldon engaged in an intricate scheme to bring about the improper liquidation of Liss Brothers,

Inc. and deprive William of his interests in that company by creating Liss Global.15 William, in

essence, argues that Sheldon “stole” Liss Brothers and that, as a consequence, William has an

interest in Liss Global. Alternatively, William suggests that a receiver be imposed under Pa.R.C.P.

1533.

The present record, however, does not support William’s theory. Even assuming that William

could establish the requisite interest in Liss Global to invoke section 1767 or Rule 1533,16 the record

and arguments presented fail to establish that Sheldon “acted illegally, oppressively or fraudulently”

toward William. See, e.g., 15 Pa.C.S.A. § 1767(a)(2). Oppression, for instance, has been defined

as “unjust or cruel exercise of authority or power.” Leech v. Leech, 762 A.2d at* 720.

17 Plaintiff’s 9/30/2002 Memorandum at 3. See also Amended Complaint, ¶ 32.

18 See Ex. P-3.

26

In analyzing whether William is entitled to a receiver for Liss Global, each element of

Sheldon’s “scheme” as set forth by William will be analyzed. Although much of the record presented

by William deals with actions involving Liss Brothers, it is important to keep constantly in mind that

William seeks a receivership as to Liss Global. Significantly, at the insistence of Sheldon, a third-party

liquidator was chosen by both shareholders to oversee the dissolution of Liss Brothers, thereby

undermining the argument that Sheldon “stole” the business. For this reason, plaintiff’s invocation

of Hankin v. Hankin, 507 Pa. 603, 493 A.2d 675 (1985) is particularly inapposite. In Hankin, the

court concluded that a partnership’s liquidation was unduly delayed because the trial court had agreed

to the appointment of two of the partners as liquidators. Thereafter, they delayed the sale of assets

due to their own interests in them. In the instant case, in contrast, it was defendant Sheldon who

urged the selection of a third-party liquidator for Liss Brothers, thereby avoiding the conflict of

interest issues in Hankin.

a. The Allegations Concerning Sheldon’s Breach the Alleged Buy-OutAgreement Set Forth in the May 31, 2000 Letter of Intent Have Been PreviouslyDismissed

William argues that one of the key events in Sheldon’s scheme “to steal the business from

William” involves a May 31, 2000 Letter of Intent between Sheldon and William. See Ex. P-3.

According to William, the first such event occurred in May 2000, when “Defendant Sheldon agreed

to pay William $3,200,000 for his fifty percent interest in defendant Liss Brothers, Inc subject to

entering into a formal agreement and defendant Sheldon handwrote and signed a Letter of Intent.”17

The legal implications of this Letter of Intent were previously addressed at length by this court

in response to defendant’s preliminary objection. Because the Letter of Intent contained language

that “this agreement is subject to the preparation of an agreed final agreement of sale,”18 this court

concluded that it did not constitute a binding agreement to purchase William’s interest in Liss

19 Liss v. Liss, 2002 WL 576510 at *14. As a result of this ruling Count II of the AmendedComplaint was dismissed.

20 Plaintiff’s 9/30/2002 Memorandum at 3.

21 Plaintiff’s 9/30/2002 Memorandum at 4.

27

Brothers.19 The rationale and precedent cited in support of this conclusion as set forth in detail in

Liss v. Liss, 2002 WL 576510 at *11-14 are explicitly incorporated into this opinion. Curiously,

plaintiff has neither acknowledged that ruling nor attempted to show either why it was in error or is

distinguishable.

Nonetheless, for the reasons set forth in this court’s previous opinion, Sheldon’s alleged

failure to pay William $3,200,000 for his interests in Liss Brothers pursuant to this letter does not

constitute evidence of wrongdoing by Sheldon that would support imposition of a constructive trust

on Liss Global.

b. William’s Deposit of Proceeds from the Sale of the Townsend Road Property Backinto Liss Brothers and the Sales Proceeds Disposition Agreement

The next event in Sheldon’s alleged scheme to defraud William was that he induced William

to deposit his proceeds from the sale of the business real estate, the Townsend Road property, which

amounted to $1,433,228, into defendant Liss Brothers by signing a Sales Proceeds Disposition

Agreement.20 According to William with the Sales Proceeds Disposition Agreement, Sheldon thereby

promised William that he would

(a) complete the buyout of William’s fifty (50%) percent interest in defendantLiss Brothers for $3,200,00.00; (b) continue William’s salary and benefits according to the terms of the SalesProceeds Disposition Agreement;(c) continue to make payments on William’s personal loan to PNC bank,which had a balance of $370,000.00; and (d) repay to William the $1,433,228.00 sales proceeds he deposited intodefendant Liss Brothers.21

William has conceded, however, that Summit Bank held a mortgage on the Townsend Road

Property and in its original loan documents, Summit required that the proceeds from a sale of the real

22 1/30/2002 N.T. at 48, 128 (William). See also Finding of Fact, ¶ 21; 2/21/2002 N.T. at193-97 (Sheldon); Ex. D-6, ¶ 5.6.

23 1/31/2002 N.T. at 395 (Sheldon). During the first three quarters, the company had madea profit of $400,000. Id.

24 Plaintiff’s Motion and Response thereto, ¶ 21; 1/30/2002 N.T. at 63-64 (William).

25 Ex. P-4, ¶¶ 4 & 5; 1/30/2002 N.T. at 145-47 & 175-76 (William).

26 See Plaintiff’s 9/30/2002 Proposed Findings of Fact, ¶ 41(b) stating that the Sales ProceedsDisposition Agreement “b. promised to repay to William, William’s share of the net proceeds fromthe sale of the Townsend Road property which was deposited with defendant Liss Brothers in theamount of One Million Four Hundred Thirty Three Thousand Two Hundred Twenty Eight dollars($1,433,228.00) Dollars.” Rather than the Sales Proceeds Disposition Agreement, however, William

28

estate be invested into Liss Brothers up to $3,000,000 or returned to the bank.22 Sheldon testified

that the fourth quarter of 2000 had been very difficult for Liss Brothers since it lost $700,000.23

William likewise acknowledged that around November 2000, Liss Brothers was in “very deep debt.”

1/30/2002 N.T. at 130 (William). Moreover, not only William, but also Sheldon, invested his

proceeds from the real estate sale back into Liss Brothers as a capital contribution.24

William concedes that this infusion of capital allowed the company to pay its debts:

Well, by me putting this money into the company and my brother putting hismoney into the company, the company was able to pay the vendors that weowed a lot of money to and the company was able to continue on. 1/30/2002N.T. at 63 (William).

Nonetheless, despite the legal requirement and practical necessities for investing the real

estate sale proceeds back into Liss Brothers, William required Sheldon to enter into the Sales

Proceeds Disposition Agreement as precondition for his cooperation. 1/30/2002 N.T. at 48

(William); 2/21/2002 N.T. at 198-99 (Sheldon). This agreement provided, inter alia, that William

would continue to receive his salary as well as reimbursements for his expenses.25 William also

maintains that under the Sales Proceeds Disposition Agreement, Sheldon promised to repay him for

the net proceeds of the real estate sale (i.e. the $1,433,228.00) as well as for his share 50% ownership

interest in Liss Brothers at $3,2000,000; William does not, however, cite a specific provision of that

agreement but instead relies on his own testimony.26

cites his own testimony or “TR, WL, January 30, 2002, pages 62-63.” Id. Similarly, in paragraph41(c) of his Proposed Findings of Fact, William asserts that with the Sales Proceeds DispositionAgreement, Sheldon “promised to finalize the purchase of William’s fifty percent(50%) ownershipinterest in Liss Brothers for Three Million Two Hundred Thousand ($3,200,000) Dollars.” Onceagain, however, William cites not to the Agreement, but to his own testimony: “TR, WL, January 30,2002, pages 54, 56, 60, 70 and 80.” Id.

27 Plaintiff’s 9/30/2002 Memorandum at 4.

28 Plaintiff’s 9/30/2002 Memorandum at 2.

29 See Exs. P-6 through P-13.

29

In any event, the implication of the Sales Proceeds Agreement for this court is the opposite

of that intended by William. Rather than signifying a wrongdoing by Sheldon, it suggests that William

was milking Liss Brothers for all that he could get. Rather than helping his brother solve their

company’s financial problems by satisfying the legal requirements established by Summit Bank,

William adopted an obstructionist stance. He forced Sheldon to enter into an agreement as a

precondition for depositing his share of the Townsend Property sales proceeds back into the

company. Moreover, he maintains that Sheldon promised to repay this legal obligation back to him.

Whether or not such a legal obligation exists remains to be determined. For the purposes of the

motion to impose a receivership on Liss Global, however, the issues and evidence pertaining to the

Sales Proceeds Agreement provides no basis for imposing such a drastic measure on Liss Global.

c. William Failed to Provide Evidence that the Elimination of Certain CorporateBenefits Constituted Oppressive Action by Sheldon

After the closing on the Townsend Road property, William asserts that he was effectively

frozen out of Liss Brothers when Sheldon eliminated William’s office, revoked his access to the

computer system and virtually eliminated the payment of William’s corporate benefits.27 William also

asserts that Sheldon between May 2000 and December 20, 2000 had charged extravagant personal

expenses to the corporate credit card for such things as expensive restaurants, family vacations,

theater and train tickets totaling $188,027.00.28 William’s corporate charges for that period totaled

$25,751.29

30 See 1/31/2002 N.T. at 218-19, 228, 240, 256, 261 (Sheldon).

31 1/31/2002 N.T. at 227 & 243 (Sheldon).

32 1/31/2002 N.T. at 243-44 (Sheldon).

33 See 1/31/2002 N.T. at 218-19, 221-22, 256-57, 262-64 (Sheldon).

34 1/31/2002 N.T. at 233-34 (Sheldon).

35 See Exs. P-6 through P-13 (corporate credit card invoices) and Exs. P-14 through P-19(discrete invoices). Likewise, Sheldon was cross examined as to these charges for that period. See1/31/2002 N.T. at 215-229, 236-299 (Sheldon).

30

In fact, Sheldon was questioned extensively concerning personal charges to the corporate

account. He admitted to many of them, 30clarified that some were charged by other employees of Liss

Brothers31 some were business expenses or some were reimbursed,32 and was often unclear as to the

exact nature of a particular charge.33 He explained that there had been a culture at Liss Brothers that

had permitted such charges but that he finally decided to put a stop to this both for himself and for

his brother as economic conditions became difficult for the company.34 In response to these problems,

Sheldon instituted a new reimbursement policy effective January 1, 2001 “that would affect all the

employees of the corporation, including myself and Billy and everybody else.” 1/21/2002 N.T. at 397

(Sheldon). Under this new policy, “essentially there had to be a business purpose that was being

reimbursed for.” Id.

Consequently, William’s assertion that the imposition of a policy restricting personal charges

to the company account after January 1, 2002 was part of a scheme that should be a grounds for

imposing a receivership on Liss Global is unconvincing. He presents no evidence that the expense

reimbursement policy was applied differently to William and Sheldon after the new policy was

instituted in January 2001 to deal with the company’s financial problems. Corporate credit card

records were offered by plaintiff, for example, only for the periods from May 2000 to a closing date

of December 20, 2000.35

There was also testimony that Sheldon was not the only shareholder to benefit from the

generous expense reimbursement policy of Liss Brothers prior to January 2001. William testified that

while his salary was approximately $260,000 a year, his total compensation package was nearly

36 1/30/2002 N.T. at 145-47 & 175-76 (William).

37 1/30/2002 N.T. at 165-69 (William).

31

$400,000 when health benefits, car payments and restaurant expenses were included. Moreover,

William noted that his restaurant expenses were reimbursed whether or not they related to business.36

William also conceded that in 1998 he had borrowed money from Liss Brothers to pay gambling

debts and that he had charged personal airline tickets to the company.37 Defendants presented an e-

mail dated December 16, 1998 in which Sheldon wrote to “Billy” that “it has come to my attention

that you have made an unauthorized cash withdrawal in the amount of $9,000 dollars. You told our

cfo that you desperately needed money to pay gambling debts to people who were not forgiving.”

After warning William not to put the company at risk, Sheldon objected that William had made credit

card charges unrelated to business for a trip to St. Maarten. Ex. D-25. Both brothers, it thus appears,

took advantage of the company’s liberal reimbursement policy. Apparently, it was only Sheldon who

saw the need to curtail it in January 1, 2001 as Liss Brothers fought for its economic survival. The

restrictions on William’s expense reimbursements at that point do not constitute shareholder

oppression or grounds for imposing a receivership on Liss Global.

Moreover, plaintiff’s claims that Sheldon deprived him of an office and computer access were

not developed with evidence except unclear testimony by William. The defendants attribute the loss

of William’s office to the sale of the Townsend Road property in November 2000. Under the new

lease, Liss Brothers no longer had access to the area that had been William’s office. The plaintiff did

not disagree with this point. See Defendants’ New Matter and Response thereto, ¶ 32-34. In his

testimony, William stated that after November 1, 2000 he “still had an office to use, because the

person that bought the property who was upstairs was not moving into that office until January or

February. So I was able to use that; but my brother did not make space for me in the new company.”

1/30/2002 N.T. at 65-66 (William). Sheldon’s failure to provide William office space in Liss Global

would not constitute an oppressive act in the context of Liss Brothers. Alternatively, it would not be

a grounds for imposing a constructive trust on Liss Global since William was not a shareholder of that

corporation.

As for William’s complaint that he was denied computer access, he concedes that computer

38 Defendants’ 9/30/2002 Proposed Findings of Fact, ¶¶ 41-43.

39 Plaintiff’s 9/30/2002 Proposed Findings of Fact, ¶ 58.

40 Plaintiff’s 10/7/2002 Memorandum at 3-4 and n.2 & 3.

41 1/30/2002 N.T. at 82 (William); 1/31/2002 N.T. at 346 (Sheldon).

42 2/21/2002 N.T. at 139 (Pudlin).

43 5/9/2002 N.T. at 6 (Foxman).

32

access was restored to him after intervention by his attorney and did not elaborate on this issue with

additional evidence. Defendants’ New Matter and Response thereto, ¶ 16.

d. On the Evidence Presented, After the Shareholders Were Unable to Reach anAgreement for Buying Out William’s Interests at the February 13th Meeting, TheyAgreed to Liquidate the Company and Liss Brothers Was Liquidated Upon Default ofthe Summit Bank Loan and the Lack of Additional Financing

William finally asserts that a February 13, 2001 meeting was the ultimate “set up” for

“Sheldon’s ultimate theft of the business.” Plaintiff’s 9/30/2002 Memorandum at 5. This meeting was

attended by both Sheldon and William as well as by their respective attorneys, David Pudlin and

Stephen Foxman. Although defendants maintain that William preferred to liquidate Liss Brothers

rather than cooperate with Sheldon’s efforts to find financing for the company,38 William contends

that he did not agree to liquidate Liss Brothers.39 Moreover, he claims that the meeting of February

13, 2001 was invalid under Pennsylvania Business Law, 15 Pa.C.S.A. §§ 1703(B) & 1704 and the

By-laws of Liss Brothers due to Sheldon’s failure to provide written notice that it was a special

meeting called to liquidate the company.40 A review of the record as well as relevant statutory

provisions and precedent, however, offers no support for William’s contentions.

It is undisputed that Sheldon and his attorney, David Pudlin, called for the February 13th

meeting which was held at Foxman’s office.41 According to Pudlin, its purpose was to inform

William about the financial status of the company and especially about relations with the bank.42

Stephen Foxman assumed it was another attempt to resolve the impasse between the brothers.43 There

was thus no evidence presented that the meeting was called for the special purpose of liquidating Liss

44 2/21/2002 N.T. at 138 (Pudlin).

45 1/31/2002 N.T. at 348 (Sheldon). Pudlin likewise testified that in the two year period hehad been doing legal work for Liss Brothers, William had never signed corporate minutes. 2/21/2002N.T. at 140-42 (Pudlin).

46 2/21/2002 N.T. at 113-14 (Pudlin); 5/9/2002 N.T. at 11, 13-14 (Foxman).

47 1/30/2002 N.T. at 104, 123-24 (William).

48 1/30/2002 N.T. at 106-09, 112, 82-87 (William); 1/31/2002 N.T. 394-98 (Sheldon)5/9/2002 N.T. at 11-13 (Foxman) (according to Foxman, the proposal was presented by Pudlin). Seealso Defendants’ New Matter and Plaintiff’s Answer thereto, ¶ 50.

33

Brothers. No formal notice was sent out for the meeting,44 but according to Sheldon, William, though

secretary of Liss Brothers, had never sent any formal notice for a corporate meeting in 27 years nor

had he prepared minutes throughout their entire business relationship.45

Sheldon thus opened the meeting by discussing the poor financial status of Liss Brothers. He

noted that the Summit bank loan was coming due on February 28 and that would be the end of the

company.46 William testified that he was aware that Summit Bank wanted Liss Brothers to find a new

lender and that February 28, 2001 or March 1, 2001 was a deadline for Summit’s continued

relationship with Liss Brothers.47 William and Sheldon agree that at this meeting Sheldon presented

the following two options to William:

(1) Sheldon offered to buy out William’s interest in Liss Brothers for $3,000,000 tobe paid out over a ten year period; or

(2) The parties could maintain the status quo, with William continuing to receive hissalary.48

According to William both of these options were unacceptable. The option to buy out his

interests in Liss Brothers by paying him $3,000,000 over the course of ten years was unacceptable

because it was unsecured and it was $2,000,000 less than the amount William believed Sheldon had

promised him only 3 months earlier. In November 2000, William asserts, Sheldon had offered to pay

him the following: (1) $3,200,000 for his one-half interest in Liss Brothers with a payment of

$1,000,000 at closing and the balance in equal payments over the course of ten years, with a security

interest granted by Liss Brothers; (2) $1,433,228.00 as repayment for William’s investment of his

49 Plaintiff’s 9/30/2002 Memorandum at 5-6.

50 1/30/2002 N.T. at 87 (William). See also 1/30/2002 N.T. at 112 (Q:”I didn’t ask youthat. Did you mention the word “liquidate?” A: yes”)(William); 1/30/2002 N.T. at 116-117 (“Iremember mentioning liquidation. It was part of a threat to try to get –“)(William); 1/30/2002 N.T.at 200(Q: I’m asking you now about February 13th. You did it on that occasion, didn’t you? A: Wediscussed liquidation on that day.”)(William)(emphasis added)..

51 2/21/2002 N.T. at 110 (Pudlin). Foxman testified that William would have accepted theproposal to maintain the status quo so long as Sheldon did not get to keep his raise. In contrast tothe other participants at the meeting, Foxman stated that neither he nor William agreed to liquidatethe company. 5/9/2002 N.T. at 13, 16 (Foxman). Foxman did concede, however, that William statedhe wanted to sell his interests at a fair market price or otherwise there was no alternative toliquidation. 5/9/2002 N.T. at 120 (Foxman).

34

proceeds from the sale of the Townsend Road property; and (3) $370,000 as the balance of William’s

PNC loan that the company had been paying. The option to maintain the status quo by continuing to

pay William his $260,000 salary was unacceptable because Sheldon would keep the “unauthorized”

raise of $40,000 that he had given himself in January 2001.49

William’s precise response to this offer–and whether he agreed to the liquidation of Liss

Brothers– is obviously a key issue. Three of those attending the meeting–William, Sheldon, and

Pudlin–agree that William brought up liquidation of the company at that meeting. William testified

that when confronted with Sheldon’s proposal at the meeting, “[h]e mentioned the fact that we could

liquidate. I mentioned the fact that we could liquidate. On my point of view, it was just a threat.”50

Sheldon likewise testified that when confronted with the two proposals, William rejected them both

and said he would rather liquidate the company. 1/31/2002 N.T. at 361 (Sheldon). Pudlin confirmed

this recollection, observing that “Billy not only rejected those proposals, but he said he would rather

liquidate the company than accept those proposals.”51

The February 13th meeting was followed by a series of crucial e-mails between the brothers’

attorneys as well as by critical correspondence from Summit Bank that undercuts William’s claim that

Liss Brothers was “stolen” from him. On February 19, 2001, Pudlin by e-mail wrote Foxman:

As you and I discussed, now that Billy and Shelly have agreed to liquidate anddissolve the company, it is important that the process be moved along quickly becauseour lending facility with Summit Bank is expiring on 2/28/01. Obviously, the morequickly we can show Summit that we have a game plan for an orderly liquidation, the

52 5/9/2002 N.T. at 73-76 (Foxman).

35

more likely it is that Summit will not move into a panic mode and remove all controlfrom us and the more likely there will be something left over for Billy and Shelly afterthe creditors are satisfied. Ex. P-28a (emphasis added).

Pudlin then suggested potential candidates as liquidators. This e-mail is significant for at least

two reasons: it states in blunt, unequivocal terms Pudlin’s impression that the brothers had agreed

to liquidate their company; moreover, it suggests that the attorneys had been carrying on discussions

about the liquidation of Liss Brothers. Foxman subsequently testified that he understood that this e-

mail referred to a liquidation. Foxman conceded that he did not respond to it to object that William

opposed liquidation. In fact, not until March 1 did Foxman specifically object to this conclusion that

the brothers had agreed to liquidate their company.52

Another crucial document is a letter dated February 21, 2001 from Summit Bank to Liss

Brothers, Inc. which stated:

This letter is to serve as notice to you that an Event of Default currently exists underthe Loan Agreement as a result of the Borrower’s failure to comply with certain ofthe financial covenants set forth therein. This letter shall further serve as notice toyou that on March 1, 2001 (the “Termination Date”), the outstanding principalbalance of the Working Capital Line, the Letter Credit Facility, the Term Loan, allaccrued and unpaid thereon and all other sums due in connection therewith and allother Bank Indebtedness are due and payable in full upon further notice or demand. Effective as of the Termination Date, in addition to all bank indebtedness beingdue and payable in full, no further advances shall be made under the Working CapitalLine or the Letter of Credit Facility. Therefore, Borrower shall be required to directlyreimburse Bank for any draws made on or after the Termination Date under anyletters of credit issued under the Loan Agreement. No advances will be made by theBank under any of the Loans to fund such reimbursement obligations of Borrower.Ex. D-70.

Pudlin subsequently sent an e-mail to Foxman dated February 27, 2001 noting that this notice

of default had been expected since “the extension of credit was expiring on 2/28/01” Ex. P-28b.

Pudlin then informed Foxman that in response to this notice and the credit deadline, Sheldon met with

lending officers of Summit that day:

At the meeting, Shelly gave an update to Summit, which necessarily included the

36

agreement of Billy and Shelly to liquidate the company. In anticipation of Summit’scalling of the loan, Shelly had prepared a plan of orderly liquidation, and he presentedit to Summit today. The Summit people responded that the liquidation plan makessense, and they would run it by their workout people and get back tomorrow. Shellyalso presented the idea of having a third party come in to oversee the liquidation, andhe mentioned Bob Starr at Penn Hudson (the company whose brochure I handdelivered to you on 2/21/2001).Ex. P-28b (emphasis added).

This e-mail is noteworthy in several regards: first, it clearly informs Foxman of the meeting

Sheldon had with Summit officials to discuss the liquidation of Liss Brothers; it also informed him

that Sheldon had prepared a liquidation plan. Most significantly, it expressed Sheldon’s desire to

have a third party oversee the liquidation of the brothers’ company. Such an intent for third-party

oversight of the liquidation process is clearly incompatible with William’s assertion that Sheldon was

attempting to steal Liss Brothers and its assets.

Foxman replied to this e-mail with a calm, matter-of-fact e-mail dated February 28, 2001 that

began by stating: