Embed Size (px)

DESCRIPTION

Economics 210a Weblog Archives DeLong Hot on Google DeLong Hot on Google Blogsearch October 01, 2010 The Semi-Daily Journal of Economist J. Bradford DeLong: Fair, Balanced, Reality- Based, and Even-Handed Department of Economics, U.C. Berkeley #3880, Berkeley, CA 94720-3880; 925 708 0467; [email protected]. 10/21/10 10:49 AMInWhichMeganMcArdleandArnoldKlingAreVeryWrongOnceAgain-GraspingRealitywithBothHands Dashboard Blog Stats Edit Post

Citation preview

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 1 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

Grasping Reality with Both HandsThe Semi-Daily Journal of Economist J. Bradford DeLong: Fair, Balanced, Reality-Based, and Even-HandedDepartment of Economics, U.C. Berkeley #3880, Berkeley, CA 94720-3880; 925 7080467; [email protected].

Economics 210aWeblog ArchivesDeLong Hot on GoogleDeLong Hot on Google BlogsearchOctober 01, 2010

In Which Megan McArdle and Arnold Kling Are Very Wrong

Once Again

Megan McArdle:

Megan McArdle: It's commonamong programmers to say"Garbage In, Garbage Out": your result is only as good asyour data. The same could besaid of economic models,except the problem is not somuch the data, as theincompleteness of the models. Arnold Kling recounts aninteresting encounter:

At the unpleasant session yesterday, I did learn something interesting fromDoyne Farmer of the Santa Fe Institute, while he was ranting against the stateof the art in macroeconomic models. He said that in 2006, the Fed simulateda 20 percent decline in home prices in its model, and the effect was minor.

That sounds highly plausible, of course. But it just adds to my frustrationabout the infamous Blinder-Zandi black-box simulations purporting to showthat the economy would have been much worse without TARP. Such anexercise assumes that we have precise quantitative knowledge of the feedbackbetween real and financial variables. But the exercise that Farmer referred toillustrates just how weak an assumption that is...

It would have been an act of honesty on Kling's part to reveal that back in 2006--when

Dashboard Blog Stats Edit Post

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 2 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

Fed staffers thought that there was definitely a housing bubble and that they should tryto forecast the causes of its collapse--he was writing things like:

Housing Bubble Revisited: There are two ways to look at house prices. 1. Relativeto historical norms, prices are very hig.h 2. Relative to rents, prices arereasonable. Both statements are true. The first implies a bubble, and the seconddoes not.

Historical norms are for prices to be low relative to rents. That might reflect a riskpremium or a liquidity premium for owning a house. In my view, there are goodreasons for a liquidity premium to have shrunk over time. The mortgage markethas become more efficient, so that the cost of having money tied up in a house hasfallen. This story suggests to me that the rise in prices from historical norms couldbe rational....

I would rate the probability of a bubble at about 20 percent...

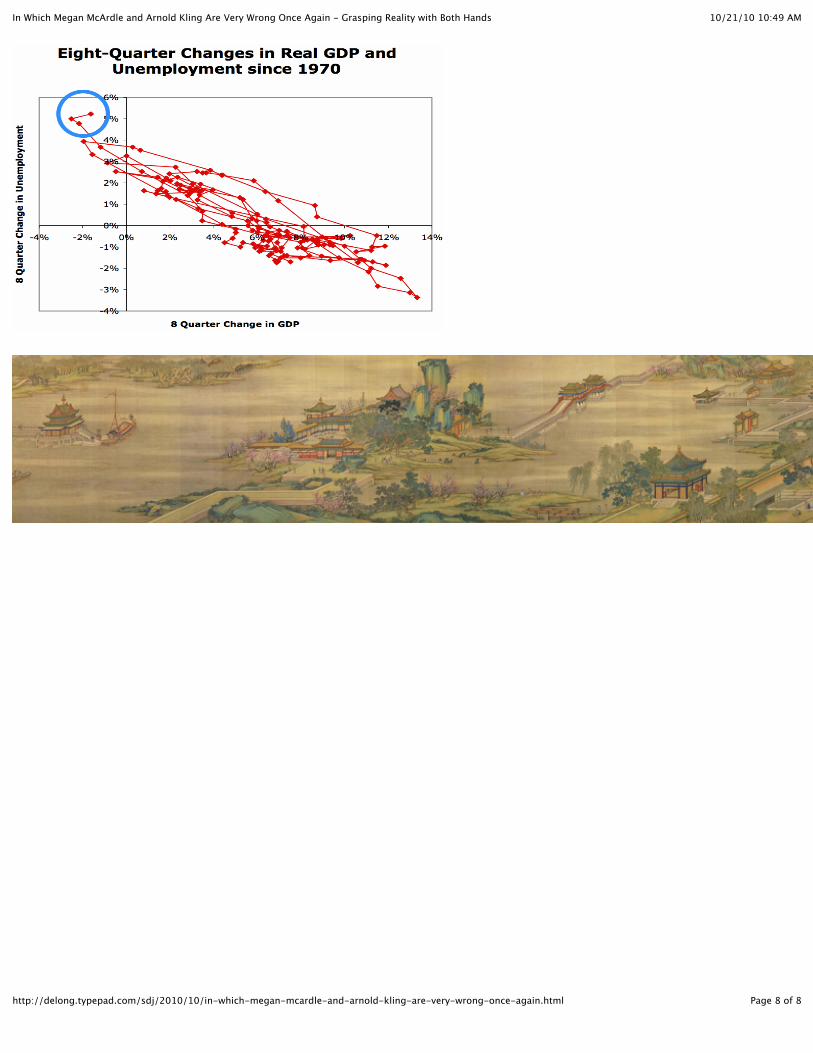

And it would have been an act of honesty on Kling's and McArdle's part to reveal thatthe Federal Reserve staff was right: the collapse of the housing bubble had little effecton the economy. What caused the crash and our current near-depression wassomething very different from the collapse of the housing bubble--as you can see if youcast your mind back to August 2008 when it was clear how large the collapse of thehousing bubble was and yet the consensus forecast was of the smallest post-WWIIrecession.

What caused our current crisis was the fact that banks that claimed to be running anoriginate-and-distribute MBS business were running an originate-and-retain businessinstead, and were extraordinarily exposed to housing price declines in a way that very,very few people understood in 2006.

This isn't rocket science, people. All you have to do is honestly report what you werethinking in mid-2006 and in the aftermath of the crash of the housing bubble in mid-2008. It wasn't that long ago.

Brad DeLong on October 01, 2010 at 01:58 PM in Economics, Economics: Finance,Economics: Macro | Permalink

Reblog (0) |

Favorite

| Digg This | Save todel.icio.us | Tweet This!

TrackBack

TrackBack URL for this entry:http://www.typepad.com/services/trackback/6a00e551f0800388340133f4c7894d970bListed below are links to weblogs that reference In Which Megan McArdle and Arnold Kling AreVery Wrong Once Again:

Comments

howard said...

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 3 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

i honestly don't understand what arnold kling is doing in economics. now, i don't knowthe guy or his work, so conceivably my impression of him is skewed by the fact that mygeneral familiarity with him results from quotes the prof post.

but every single quote of his i read suggests that he has no interest in economics at all:it appears that his theme is que sera, sera.

which just makes me wonder: what is the point? is his choice of profession entirely anopportunity to serve as a drama critic to the aesthetic beauty that is (his version of) themarket system?

Reply October 01, 2010 at 02:08 PMazlib said...Where were the risk managers in this debacle? Oh wait! I suppose they were in on thebonuses and had no incentive to blow the whistle.

Reply October 01, 2010 at 02:43 PMSora said in reply to azlib...Asking risk managers to reflect on the market is like asking seagulls to ensuresustainability of the fish they eat. They don't really care; so long as they can eat, it'sgood enough.

Reply October 01, 2010 at 02:52 PMBernard Yomtov said..."Where were the risk managers in this debacle? "

I don't know, but my guess is that at least some of them were dismissed as "nervousNellies" and told to quit worrying so much. Remember, the phrase is "irrationalexuberance." The first word means something.

Reply October 01, 2010 at 03:06 PMpartha neogy said...Kudos to Brad DeLong. The real antidote to the likes of McArdle and Kling arerepeated posts like this that cut through incompetence, obfuscation and dishonesty.

Reply October 01, 2010 at 04:13 PMDean Baker said...Oh no, do I have to agree with Megan McArdle and Arnold Kling against theincomparable Brad DeLong? I'm afraid that the answer is a partial "yes."

As much as I and every once else enjoyed the theatrics of the financial meltdown twoyears ago, that is not the story of this downturn. The reality is that we would be inpretty much the same shape today if the financial crisis had not occurred. Thedownturn is a story of a collapse in construction due to huge overbuilding in bothresidential and non-residential real estate. It is also a story of consumption and savingrates returning to more normal levels (the current 6.0 percent rate is still well belowthe average for the 50s, 60s, 70s and 80s ) now that the housing bubble wealth haslargely disappeared. In other words, the downturn is the housing bubble.

One would be very hard-pressed to explain how this situation would be different if thefinancial crisis had not taken place but the bubble had still burst. Politicians like to tellstories about how small businesses can't get loans (get out the violins and the applepie), but this is just cheap demogoguery. Small businesses always become greatercredit risks in a downturn. If there were really all these small businesses that werebeing stifled in their expansion plans because of a lack of access to credit then weshould be seeing the Wal-Marts and the Starbucks, who can get credit at record lowrates, expanding like crazy to grab market share. There is zero evidence of this. In fact,

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 4 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

they have cutback their expansion plans.

So, we have two competing explanations for the downturn. One, the collapsed housingbubble, fits the data like a glove. The second, the financial crisis, has no evidence tosupport it whatsoever. So, naturally economists embrace the second explanation. Ofcourse, these were people who could not see an $8 trillion housing bubble

Reply October 01, 2010 at 05:46 PMFull Employment Hawk said in reply to Dean Baker...House prices declined and housing construction decreased long before the nearmeltdown of the financial system, but the economy was only in a mild recession untilthe near meltdown of the financial system. It was only after that, that the bottom fellout of the economy. This is very hard to explain if the near meltdown of the financialsystem was not a major cause. Obviously the decline in household wealth resultingfrom the large drop in housing prices would significantly increase the saving rate.

This does not appear to be a case of either or. Both the drop in housing prices and thenear meltdown of the financial system appear to have played major roles and researchis needed to determine how much each contributed. But it is hard to believe that ifthere had not been a near meltdown of the financial system the recession would havebeen anywhere as bad.

Reply October 01, 2010 at 06:18 PMFull Employment Hawk said in reply to Full Employment Hawk...Of course since the collapse of the housing bubble caused the near meltdown of thefinancial system, the collapse of the housing bubble is the ULTIMATE cause of therecession. The only question is how much of the effect was through the direct channelof the decrease in household wealth increasing saving, and how much was through theindirect channel of causing a near meltdown of the financial system.

Reply October 01, 2010 at 06:27 PMdd said...Yikes! In Kling's words "This story suggests to me that the rise in prices from historicalnorms could be rational...." "Could be" is quite far from outright denial of a bubble.Even supposing that Kling didn't see the bubble, it's mere ad hominem to say that he'snot in a position to cast doubt on the practice of economic forecasting because, in fact,he was wrong about the bubble.

I won't get into whether the banks' originate-and-retain policy was due to rising andinflated housing prices. In fact, your claim is a red herring. It may even be that Klingdraws a different conclusion while assuming your claim when he says "Such anexercise assumes that we have precise quantitative knowledge of the feedback betweenreal and financial variables."

Reply October 01, 2010 at 06:39 PMBob Athay said in reply to Full Employment Hawk...The sense I get is that the collapse of the housing bubble was the trigger, but not thereal cause of the Panic of 2008. Rather, it seems to me that the fundamental structureof the financial markets was unstable because too many systemically important firmssuch as AIG had taken on far more risk than they realized and anything that caused awidespread loss of confidence would have had the same effect.

On the subject of models and the simulations that implement them: there are threebasic ways of getting bad results: incorrect input data; using the model on a problemfor which it isn't valid; setting up the problem incorrectly or, of course, any

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 5 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

combination of the above.

Back when I was a TA for my advisor's undergraduate simulation class, I had a lot ofleeway in making up the exams and grading their term projects. None of them evermake this sort of stupid mistake. Obviously, Megan McArdle and Arnold Kling wouldbenefit from a little re-education.

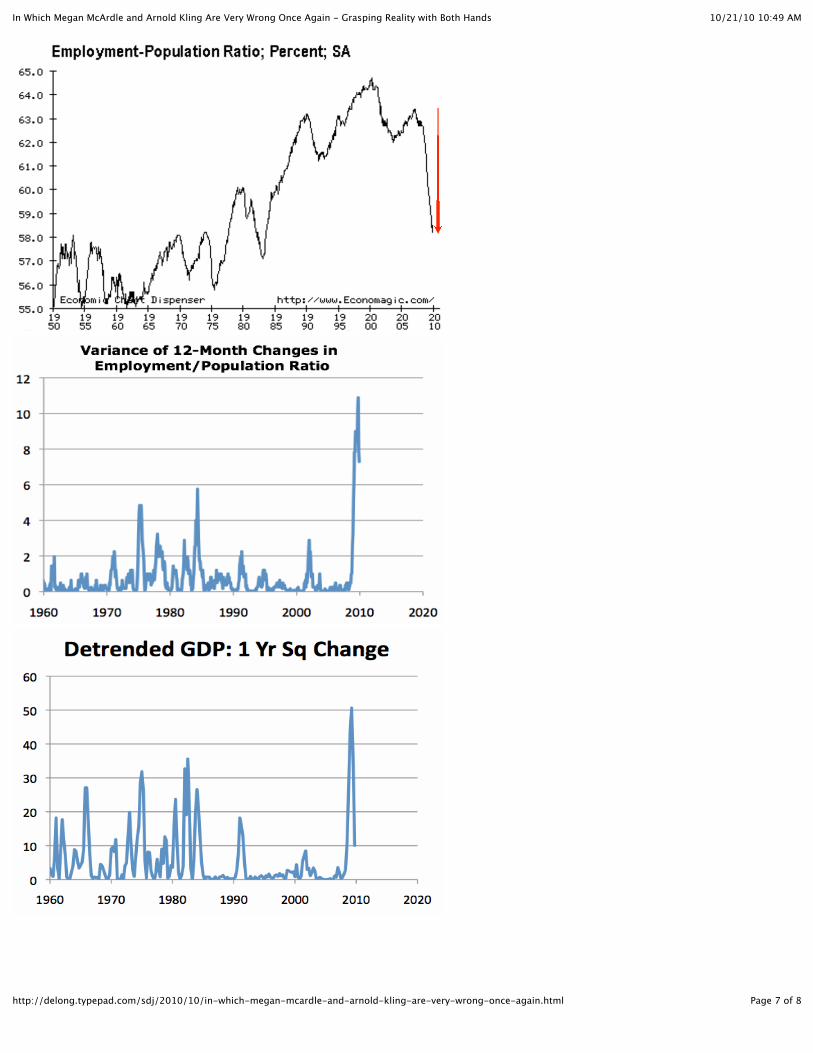

Reply October 01, 2010 at 09:27 PMOmega Centauri said...When I see something likethe Fed simulated a 20 percent decline in home prices in its model, and the effect wasminor.I want to ask, "did they just assume 20% across the board". We know the bubble wasvery uneven, and that should have led to the inference that the unwinding could bevery uneven as well. We've had a lot of markets where the peak to trough decline wason the order of fifty percent, and some with only minor reversals. I suspect that amodel with say 40% of markets being hit with 50% declines and the other sixty percentflat would show a quite different overall effect on both the economy and the financialsystem, then a uniform 20% drop. Were the right questions even asked?

Reply October 01, 2010 at 10:13 PMogmb said...Shorter McArdle, shorter Kling, shorter Cochrane: Externalities do not exist,information asymmetries do not exist, principal-agent problems do not exist, contractsare always complete, rationality is unbounded, and all economic ills result from theshiftlessness of the poor.

It's like reading a textbook from the 1960's.

Reply October 02, 2010 at 06:21 AMComment below or sign in with TypePad Facebook Twitter and more...

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 6 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

Me: Economists:

PaulKrugmanMark ThomaCowen andTabarrokChinn andHamiltonBrad Setser

Juicebox

Mafia:

Ezra KleinMatthewYglesiasSpencerAckermanDanaGoldsteinDanFroomkin

Moral

Philosophers:

Hilzoy andFriendsCrookedTimber ofHumanityMarkKleiman andFriendsEricRauchwayand FriendsJohn Holboand Friends

Post Preview

First, Kill all the PensionsThe Atlantic (blog) - Oct 19, 2010She may or may not have been the first major economics blogger, depending onwhether we are allowed to throw outlying variables such as Brad Delong out of ...Related Articles » « Previous Next »

economics DeLong

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 7 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html

10/21/10 10:49 AMIn Which Megan McArdle and Arnold Kling Are Very Wrong Once Again - Grasping Reality with Both Hands

Page 8 of 8http://delong.typepad.com/sdj/2010/10/in-which-megan-mcardle-and-arnold-kling-are-very-wrong-once-again.html