Embed Size (px)

DESCRIPTION

Â

Citation preview

Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

1 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

Editors In ChiefBenjamin EliasJesse Schanzer

Avi Siegal

EditorsYona Benjamin

Jeremy HorowitzIlan Wolff

Layout EditorRose Frankel

Raphael Kepecs

Art EditorsLiat Katz

Emanuel Kuflik

Faculty AdvisorMs. Gloria Schneider

Writers

Features

Business Manager

Yona BenjaminDaniel Best

Judah BlumenthalRuthie Charendoff

Ben EliasAlon Futter

Jeremy HorowitzDaniel Jubas

Nate KatzShabbos Kestenbaum

Ronit MorrisShoshana Rosenzweig

Shalhevet SchwartzAvi Siegal

John TurekIlan Wolff

SAR High School503 West 259th StreetRiverdale, NY 10471

Rabbi Tully Harczstark, PrincipalPhone: 718-548-2727

Fax: 718-548-4400

Liat KatzNoam Lindenbaum

Adina NobleJulian Snyder

IncentivesSAR High School’s Economics

and Business Journal Spring 2015

Tany Neuhaus

2SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

Letter from the EditorsWhen we first began working on this year’s edition of the journal many students came up to us expressing their frustration - they told us they really wanted to be a part of the journal but simply knew nothing about econom-ics. During our initial editorial meetings, this was something we singled out as a problem we would like the

journal to address. Too often economics is subject to the misconception that it is a discipline limited to money or business or finance. So as we began to compile our ambitious goals for the journal, we resolved to focus on

communicating the impact of economics in contexts beyond just money. While money is of course integral to many economic structures, economics permeates virtually every aspect of life; education, terrorism, psy-

chology, you name it. No matter where you live or what you do, you encounter situations every day to which economics can be applied -- and that is what we wanted our journal to reflect.

The study of economics is divided into macroeconomics and microeconomics. A macroeconomist is drawn to the big picture, while a microeconomist is fascinated by detail and nuance. Both types of practitioners are certainly partisan to their respective areas of study; they rarely cross the treacherous chasm between the two fields. It is for this reason that an economist could not possibly understand the role our academic advisor Ms. Schneider has played in this journal. From overseeing the management of editors to ensuring that not a single

misplaced comma slips through the cracks, Ms. Schneider toed the line that joins macro and micro with her trademark grace and excellence.

We would also like to thank all the contributors involved in every aspect of this undertaking. Writers, editors and designers, we thank you for putting up with our antics, late night emails and formidable deadlines. You

have all worked with passion and rigor.

Enjoy!

Benjamin Elias, Jesse Schanzer, and Avi Siegal

All headlines were printed Hoefler Text and all copy was printed in Times New Roman on 2/sided 60# text paper uncoated paper.

The 4/C, 1 sided 100#/gloss cover

was photographed by Liat Katz and designed by Emanuel Kuflik and Rose Frankel. The magazine was created using Adobe In Design on a Macbook laptop.

Beehive Press was responsible for

printing the two hundred copies of this thirty-six page book.

Incentives is distributed free, to the SAR High School Community.

Colophon

3 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

Table of ContentsHealthy Economy? The Economics Behind Ebola 4

Moshe Kahlon: 2012 Cellular Revolution, Oligopolies in Israel 6

The Paradox of Value 8

Crossword Puzzle 9

Access Versus Ownership: Transitioning to a Sharing Economy 10

Which High School to Attend? 12

Will the Fed Really Hike in 2015? 14

Exploding Economies: a Look at the Economics of Terrorism 16

The Eurozone: Past, Present and Future 19

To Migrate or Not to Migrate? 21

Trading Genders: Men, Women and Investing 24

Dear John Maynard 26

Anger Management: a Look at Behavioral Economics 27

Why Junk Bonds May Not Be Such Garbage After All 28

Wealth Inequality in the 21st Century 29

Universal Healthcare, Universal Tradeoff 31

Who Was F.A. Hayek? 32

Crossword Answers 34

Bibliography 35

4SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

When most people hear the word “Ebola,” they think of disease, death,

and hazmat suits, not economics. How-ever, economics has been one of the larg-est issues in the recent outbreak of Ebola. The disease has not only affected the economies of the countries plagued with Ebola, but has struck the global economy as well.

Obviously, Ebola has had its great-est effect on the economies of the three West African countries hit hardest in the crisis, those being Guinea, Sierra Le-one, and Liberia. While these countries account for roughly 2% of the GDP of Sub-Saharan Africa, the International Monetary Fund (IMF) has cut its growth forecast for all of Sub-Saharan Africa from 5.5% to 5%, seemingly in response to the Ebola crisis. Before the Ebola epi-demic hit, the World Bank predicted that Sierra Leone’s economy alone would grow almost 9% in 2015. On the other hand, the new estimate, predicts that it will shrink by 2%.

The question remains, why is this disease having such a massive impact on the economy? The answer lies in the ef-fort to halt the spread of the disease. Not only do these countries have to deal with the costs of the disease itself, in finding doctors and quarantining patients, but they also struggle to prevent the disease from spreading further. In order to stop the spread, trade must suffer. Exports

simply cannot move as freely through ports or borders, and as exports have fallen, so has overall economic perfor-mance.

Even before the epidemic, these countries were already in debt and cur-rently owe creditors $3.6 billion. The tourism industry was, not surprisingly, hit very hard post-outbreak and contin-ues to decline drastically as many com-panies impose travel restrictions, not to mention many others who are scared off from Ebola-stricken countries. For in-stance, in Gambia, a nation dependent on its tourism, hotel bookings are down by 65%. Lagos, one of the largest cities in Africa, has seen a decline of demand of roughly 30% due to the decreased eco-nomic activity as people remain in their homes and tourism falls. In response to these economic troubles, these countries have attempted to spur the economy through increased spending. Alas, what comes of this is only inflation and greater debt. Ebola has not only affected these few countries in Africa, but also has had an impact on a larger scale. If you have gone to the supermarket recently, you may have noticed that the price of cocoa has spiked. The 23% increase in price is due to the fear that Ebola may spread to the Ivory Coast, the world’s largest cocoa producing country, which happens to lie near Ebola-infected countries. Further-more, we may see an increase in prices of oil and precious materials, products we

import from Ghana, if Ebola continues to spread. Guinea, is home to ⅔ of the world’s bauxite resources, a crucial part of aluminum, as well as massive iron-ore deposits. If the Ebola crisis doesn’t end in the near future, we can expect spikes in these prices as well. In reaction to the epidemic, many airlines have stopped flying to affected countries, and share prices for companies that are heavily ex-posed to the disease have plunged. For-eign companies have pulled out workers, put billion dollar expansions on hold, and some companies, such as London Min-ing PLC, have even filed for bankruptcy. In addition to individual consumer costs, foreign-aid groups and governments are expected to spend roughly $32.6 billion by the end of 2015 on the containment of Ebola and the care of Ebola patients.

But why does Ebola have such far reaching effects? Fear of Ebola has been high in the U.S., despite having killed only one person, while thousands of Americans die of the flu each year. An overreaction to disease outbreaks is not unprecedented. The outbreak of Severe Acute Respiratory Syndrome (SARS), which is estimated to have cost over $50 billion in damage to the global econo-my, killed fewer than 800 people and infected roughly 8,000. This damage to the economy is not caused by the disease itself, rather it is largely caused by panic and confusion in reaction to the disease. Studies show that lethal diseases without

Healthy Economy?by Ruthie CharendoffThe Economics Behind Ebola

5 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

a cure often cause overreactions even if the transmission rate is low. In the case of Ebola, the government finds itself stuck doing its best to limit the spread of the disease without causing excessive disruption and panic. Still, people tend to be uninformed and make false assump-tions, causing the fear to spread farther. For instance, many people associate Ebola with all of West Africa when it re-ally only covers a tiny part of the west-ern portion of the country. Also, people generally act in self-interest. It is human nature to put yourself before others, as

the infected nurses did when they flew back to the U.S., putting everyone on board the flight in danger. These types of reactions tend to cost the global econo-my far more than the disease itself other-wise would. These reactions are, in many ways, the cause for the drop in tourism and the stifled trade in and around Ebola-stricken countries.

Ultimately, Ebola has caused wide-spread economic harm as well as taking the lives of 7,533 people. If the disease had struck a more stable part of the world, one with an economic and health

care infrastructure that would have al-lowed it to weather the storm, the story may have been over by now. Due to the less than ideal state of the West African countries’ economies before the epidem-ic, their debt, reliance on foreign aid, and the panicked reactions of society as a result of the epidemic, the countries rid-den with Ebola have spiraled farther and farther from economic stability. While the disease may be responsible for taking fewer than 8,000 lives it has landed in a part of the world that has allowed it to claim millions of economic victims.

Ruthie ChaRendoff In addition to her infamous role on the economics journal, Ruthie has also achieved her school-wide fame as the founder of “Cookies For a Cause,” a group which bakes and sells cookies in school to raise money for the Children’s Hospital at Montefiore as well as other causes. Ruthie is also a member of the debate team, a squad she has been a part of since her freshman year. As a senior in SAR, Ruthie is sad to leave high school but knows she left behind a strong legacy as a baker, a debater and an economist. After spending a gap year in Israel, Ruthie hopes to earn degrees in sociology and politics

at Northwestern University.

by Eliana Rohrig

6SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

Moshe Kahlon, the 2012 Cellular Revolution, and Oligopolies in Israelby Shalhevet Schwartz

With the advent of Knesset elections in early 2015, some new faces have ar-

rived on the Israeli political stage. One of those faces is that of Moshe Kahlon, who started a new center-right party called Kulanu in November 2014. While many Israelis hadn’t heard of Kahlon until re-cently, he came into the limelight with one claim to fame: he’s the man respon-sible for Israel’s “Cellular Revolution,” for breaking the country’s three-compa-ny oligopoly on cell phone service and causing the prices of cell phone plans to plummet.

Until 2012, the three compa-nies, Cellcom, Partner and Pele-phone, were the only cell phone plan providers in the country. Israel’s Min-istry of Communications wouldn’t al-low other companies to enter the mar-ket. This policy created an oligopoly in the cell phone industry. An oligopoly is when a small number of sellers control the market for a specific product.

Oligopolies can work in differ-ent ways depending on the relationship between the sellers - there can be very little competition or there can be a lot of it. When companies work together, they can engage in any number of activities in order to increase their profits, such as price-fixing or market sharing.

Market sharing is when several

companies agree to split up the market, i.e., to divide the consumers among the companies to avoid competing for the same ones. This saves resources that would otherwise be spent on advertising or other methods of trying to attract buy-ers.

Price-fixing, which took place, in some form, in Israel in the years before the “Cellular Revolution,” occurs when a small group of companies that dominate the market all set prices higher than they need to and agree not to lower prices. When such an agreement is for-mal, it’s called a cartel and is illegal in

most countries under antitrust laws.As far as we know, Cellcom, Part-

ner and Pelephone never engaged in any illegal activity, but for years they of-fered nearly identical plans and prices, controlled approximately one third of the market, and did not seem particu-larly intent on changing the status quo. However, on May 14th, 2012, all of that changed. The government permitted two

new companies, Golan Telecom and HOT Communications, to enter the

market, offering plans at a fraction of the rates of the three other com-panies. Golan and HOT offered, for example, unlimited data and international calls for only NIS 99 per month. The three dominant companies had required a separate

(and very high) fee for internation-al calls, and their monthly prices

had hovered around NIS 125-135.As a result, business flooded to the

two new companies. Cellcom, Partner and Pelephone were forced to respond. Partner came out with a new lower-cost brand in order to compete with the new-comers to the market, and all three com-panies were forced to seriously cut their spending in order to make up for their lower profits.

Kahlon’s push for reforms in the Ministry of Communications broke the cell phone oligopoly. But the cell phone

“An oligopoly is

when a small number of sellers

control the market for a specific

product.”

7 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

industry isn’t the only area in Israel con-trolled by either one company or a few companies. Supermarkets, for example, are dominated by the Strauss Group Ltd. and Nestle-Osem. The Strauss Group is the umbrella company for Israel’s Milki, Pesek Zman chocolate, Cheetos, Doritos, Must candy and gum, Sabra hummus, and much more, while Nestle-Osem owns Bisli, Bamba, and much more.

But while we all wish that hummus was cheaper, the supermarket oligopoly is relatively unimportant when compared

with the oligopoly of Israel’s banks. Five Israeli banks currently dominate the mar-ket, free from the competition of smaller banks or larger international banks. The incumbent companies make it difficult for small or medium-sized businesses to obtain loans. Part of Kahlon’s vision is to do to the banks what he did to the cell phone market: break the companies’ hold on the industry. He wants to legislate re-forms that would encourage the growth of smaller banks, providing them with state money if they agree to lend to small

businesses.Without competition, prices won’t

go down, which makes it harder for con-sumers to pay for goods and services. That problem is behind many of Israel’s financial troubles, and people are trying to fix it in any way they can. We’ll have to wait and see what happens in the next Knesset - but at least now, with Golan’s unlimited international calls, you’ll be able to find out relatively easily.

Shalhevet SChwaRtz The economic journal’s resident renaissance woman, Shalhevet has enjoyed time on SAR’s Mock Trial team, acapella group, Model UN team and school newspaper. During her time outside of school, Shalhevet enjoys her new found hobby of harvesting ginger in her backyard. Shalhevet thought it best to harvest her own ginger after a ginger incident caused a small riff among the economics journal editorial staff. After spending the upcoming year in Israel, Shalhevet

hopes to pursue a degree in philosophy and public policy at Yale University.

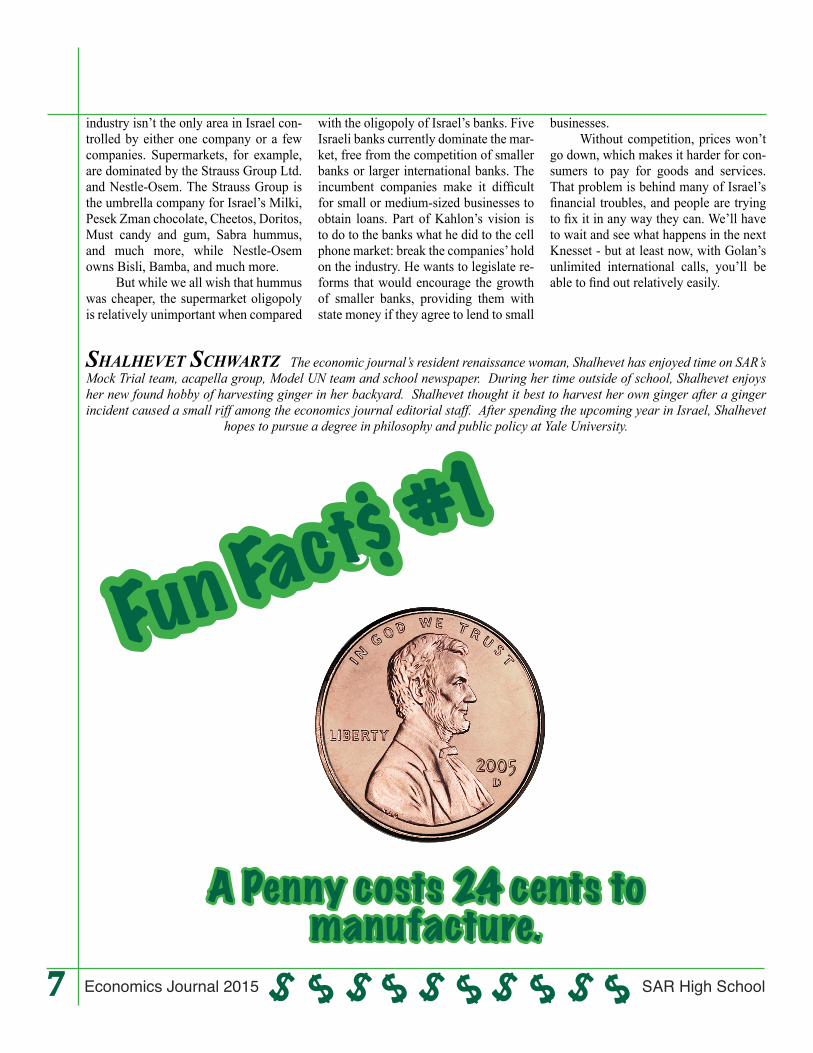

A Penny costs 2.4 cents to manufacture.

Fun Fact$ #1

8SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

We generally like to think of our actions as making sense. As being part of

a framework of reason that is inherently true. If I buy something, I would like to think that what I am buying is inherently valuable. The only problem is that value is a construct, and thus all of economics is based on people just making it up as we go along as opposed to acting “ratio-nally.”

Let us begin with an intuition pump, a thought experiment. There are ten people and ten pencils. Each person needs a pencil. The seller of the pen-cils will set a price that the buyers are willing to pay. This is called the “equi-librium price.” Now let us assume that there were actually four pencils. We have ten people who still need one pencil each. Now, the seller sees that he can get more money for his pencils, as they are rare. The imbalance between supply and demand only allows the four highest bidders to get the pencils, consequently at a higher equilibrium price. All very straight forward. We can postulate from this experiment that since value is de-termined by how much the purchaser is willing to pay for limited resources, it is dependent as well on the purchaser’s own limited resources. But how do we make these decisions? How do we de-termine what to use our limited resourc-es on? Now is the time that reason and inherent truth would be nice, then we

could clearly understand how to spend our hard earned money. So how do these decisions happen?

One would assume that as creatures obsessed with survival, things that help us live, like food and water, would have the greatest value. That’s a fact. Things that help us survive are important. Here’s another fact. I can buy a loaf of bread for less than ten dollars, maybe even less than five, but a good wedding ring for no less than hundreds of dollars. How is that so? How is it that things which provide us with relatively minimal utility have such high prices while things that are essential for our survival can be so cheap? Behold, the Paradox of Value.

To solve this issue, we look to what has had value throughout history.Throughout history, many things have been used as currency: Salt, furs, live-

stock, spices and above all gold. to name a few. . Gold, more than anything else, has stood for value (Dare we say “The Gold Standard” of value). Now what can this tell us about value? How is it that a yellowish metal that we melt out of rocks has taken on this ubiquitous symbol of value? It is at once very simple, and yet very odd.

As it turns out, value is merely a construct, a subjective marker that we assign to things that are contingent upon our culture and where we live. Gold and diamonds are more valuable than wa-ter and bread because we say they are. That’s the true paradox. So next time you buy something, understand that you can act as an individual, you have the power to decide what matters, you have the power to choose. Dont be a blind consumer, rather be a creator of value.

Paradox ofValueby Yona Benjamin

Yona Benjamin Yona Benjamin, is a senior at SAR High School. During breaks from writing for Incentives, Yona can often be seen scurrying across the auditorium stage as a member of SAR’s tech team. While Yona claims to have first joined the Economics journal for his love of tweed jackets, Yona has developed a fascination for economic indicators such as GDP and interest rates and is our resident PPC expert. After a gap year in Israel, Yona hopes to pursue a degree in religion at Emory

University.

by Liat Katz

9 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

Economics Crosswordby Julian Snyder

2. The ownership of shares in a company.4. The current Federal Reserve Chair is ___.5. When a company is unable to pay its creditors it must declare _______.7. ‘Father’ of modern macroeconomics.8. The market value of all final goods and services pro-duced within a country’s borders.9. An estimate of income and expenditure for a set period of time.11. When a company sells equity to the public for the first time.14. A sustained increase in the general price level of goods and services over a period of time.15. Type of economy where economic decisions are made by a central body.

Across1. Central banks manage _______ policy.3. A place where coins are made.6. A type of economic system that allows for prices to be determined by supply and demand.9. The ____ market is bigger than the stock market and is comprised of loans over a period of time, most often with a set interest rate.10. Economist who wrote The Wealth of Nations.12. A type of market structure where one company con-trols the supply in an industry. 13. U.S. Federal Reserve committee that decides whether to increase or decrease interest rates.

Down

Created on TheTeachersCorner.net Crossword Maker

10SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

At any given moment, there is a tremendous quantity of underutilized assets in

the economy. Physical goods, skills, and time frequently lay idle. With the rise of the Internet, pioneering companies, in-cluding Uber and Airbnb, have noticed and exploited this latent productivity. They facilitate the use of these resources by acting as middlemen between con-sumers and people who wish to provide services. Since consumers now have the on-demand ability to access the resourc-es of strangers, this entire enterprise has been termed the “sharing economy.”

The nature of the sharing economy has generated huge numbers of partici-pants; for instance, Airbnb, the wildly successful online marketplace for prop-erty rentals, has over one million list-ings worldwide. The sharing economy is built on a motivational framework cre-ated by the Internet. On the web, people collaborate on activities ranging from open-source projects to file-sharing; en-gage in online social commerce; share information, goods, and services; and collectively pursue the advancement of various ideologies and ideas. The com-bination of these norms leads to a culture of comfort with the buying and selling of assets in the sharing economy. Trust – a precious commodity – exists between

the consumer and producer by way of re-views and ratings, social media, and an abiding sense of community. While the risks assumed by both sides in the trans-action seem alarmingly large, in context, people’s willingness to participate in the sharing economy makes abundant sense.

Proponents of the sharing economy trumpet the widespread benefits that have accompanied its rise. Companies built on the sharing model are streamlin-ing the economy and extracting maximal productivity from the assets within. The so-called micro-entrepreneurs, dubbed thusly since they essentially run their own businesses with the assistance of the aforementioned companies, enjoy enor-mous flexibility and the ability to make money from their possessions. Their cus-tomers also profit from sharing economy transactions. Buyers enjoy lower prices and greater convenience. They can col-lect the advantages of consuming with-out assuming the costs of ownership. Yet the disruption caused by the sharing economy is not exclusively favorable.

The sharing economy threatens entrenched and free-agent sellers alike. To illustrate, Uber has intruded on the taxi business; Airbnb, the hotel business. These structurally significant industries enjoy extensive protection via govern-ment regulation. Services that imperil

these protected industry behemoths must contend with the law; indeed, Uber and Airbnb are deemed illegal in many places. Perhaps, as the interlopers insist, such regulation is outdated and hurts consumers, but the legal hurdles remain. Participants in established companies are hurting as well. For example, New York City taxi medallions, which are licenses to operate NYC taxi cabs that have been historically prudent investments, may drop in value.

The sharing economy also relies on wealth inequality to amass its le-gions of workers. Micro-entrepreneurs they may be, but workers who take part in the sharing economy generally do so because their own economic situations are unsound. Since they operate as in-dependent contractors, sharing economy workers do not receive the benefits, such as health insurance, usually accorded to employees. The only certain winners in the sharing economy are the middlemen and the consumer.

Regardless of its potential ad-vantages and drawbacks, the sharing economy is expanding at breakneck pace. Skyrocketing valuations are defy-ing comprehension; Uber’s current $40 billion valuation (as of the first quarter of 2015) places it in the arena of corpo-rations like FedEx and Ford. Frenzied

Access Versus Ownership

by Avi Siegal

Transitioning to a Sharing Economy

11 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

predictions about the impact of sharing economy companies suggest that this is no fad and our economy is facing a pe-riod of massive and rewarding change. Case in point: Uber could conceivably

replace the need for car ownership, re-moving the need for parking lots and ushering in an age of automated, rapid transportation. Numerous barriers lie in the way of such a future. Still, the sweep-

ing adoption of collaborative consump-tion indicates that the sharing economy isn’t going anywhere.

avi Siegel A member of the Model UN team, Witness Theater and the Hebrew Journal, Avi has managed to keep his three years in SAR quite busy. Always maximizing his free time, Avi can often be seen riding the BX7 bus home captivated amidst the writings of Kant and Rousseau. Reading the likes of Adam Smith and Thomas Robert Malthus, it is these bus rides that have

introduced Avi to the origins of Economics.

5685 Riverdale AvenueRiverdale, NY 10471718-543-TACO (8226)

www.carlosandgabbysbronx.com

If you have $10 in your pocket and no debts, you are wealthier than 25% of

Americans.

Fun Fact$ #2

12SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

GDP. Military strength. Obe-sity. No matter what the statistic, it is by no means

surprising to find America atop the list.

However, America hasn’t been doing nearly as well in education. As of 2012, the U.S. ranked 36th in math, 28th in sci-ence and 17th in reading, near the world

average. Considering the deep rooted causes, there is no quick fix to this edu-cation problem. While the best teachers flock to the best pay and end up teach-

Which High School to Attend?

by Ben Elias and Ilan Wolff

Why School Choice May Solve the Educational Crisis

by Daniela Krausz

13 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

ing only the top few percent, money is poured into public schools where a mix of problems such as tenure and contract disputes leave those who cannot afford private schools overlooked. Perhaps the future of educational improvement is not in hiring and firing teachers, or in new smart boards and online classrooms. Rather, it may be in the hands of indi-viduals; maybe it is in school choice.

Private schools are signifi-cantly more efficient than public schools. A study

which tracked New York City students who were randomly given a small voucher to attend a cheap private school, found that these students were 24 per-cent more likely to enroll in college, and the average percentage of students with SAT scores above 1100 (math and read-ing) more than doubled, as compared to students who attended public schools. Furthermore, these incredible accom-plishments were achieved without a sig-nificant monetary contribution from the city. In fact, the vouchers were slightly less than half the cost of the average pub-lic school education.

Yet, the private schools yield sig-nificantly better results with less funding

because they have an incentive to do so. In the private school system, parents are able to choose between multiple schools, forcing private schools to compete with one another in order to receive more applicants. On the other hand, public schools face no such competition. Not only are they wholly funded by the gov-ernment, but also they take in students on a geographical basis so school choice is essentially a non-factor.

Furthermore, in public schools, school evaluations are based on inac-curate criteria, such as observations of teachers and standardized test scores. In fact, even though many New York City students are struggling, the govern-ment rank 95% of teachers as “highly effective.” Even when bad schools are identified and closed, many of the weak teachers are rehired because they re-ceived lifetime tenure after a mere three years of positive performance. Although these inefficiencies are well documented, there is little incentive to make positive changes because the school system is not subject to consumer demand. A public school system which emphasizes school choice would thus be significantly more efficient than the current system, one

which seems to emphasize mediocrity if anything at all.

The public school system is also an invasion of basic liberties because it makes a private school education pro-hibitively expensive for the majority of Americans, and many do not agree with the values the public school system trans-mits. Although it endeavors to provide a “value free” education, being value free is a value in and of itself, and the public schools end up promoting an unsophisti-cated moral and epistemological relativ-ism. Furthermore, secular schools are often poorly suited to teach religious stu-dents, but through their taxes, religious families are forced to pay for an educa-tion which does not meet their needs. The disconnect between certain people’s core values and public school educa-tion points to a larger problem: since the schools do not need to respond to con-sumer demand, they are thus unlikely to provide for individual people in the best way possible. If school choice was pro-moted, one can only begin to imagine the plethora of new school options which would better fit the needs of individual children, now coming from all classes within the American population.

Benjamin eliaS Ben Elias is a senior with a passion for Model UN and Chickies. Ben is known for setting the stan-dard for excellence in thank you notes and holds the record for the most emails from Ms. Schneider. Ben will be attending Yeshivat

Orayta before heading to the University of Chicago.

ilan wolff A senior at SAR, Ilan has enjoyed his high school career as a member of the debate team and the slam poetry club. When not debating and slamming, Ilan can be found playing minor league tagpro or meticulously scanning his email for an invite to major league tagpro. Ilan also devotes an immense amount of time to fantasy sports, and while he is not known for his success, one can always count on thorough midseason reports. After a gap year in Israel at Maale Gilboa, Ilan plans to

follow the path of some of his favorite academics such as Nate Silver and attend the University of Chicago.

14SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

The topic on most economists and market watchers minds this spring is when will lift

off occur. A strong second half of 2014 and very good employment data has led many to believe the time for the Fed to exit is this year. The Fed has been very careful with its rhetoric regarding the prospect of raising interest rates; it has

removed words and changed guidance. The beginning of Q1 had many econo-mists believing the Fed’s June meeting is when the Fed would lift off, but after a poor March non-farm payroll number, consensus macro has tempered their ex-citement about raising rates during the June meeting. The recent jobs number will not be only thing on the minds of

policy members as they wrestle with the dilemma of timing; many concerns exist and some might push off a rate hike until 2016.

There are many factors and indica-tors the Fed will look at that will make it most challenging to raise interest rates at this time. Q1 of 2015 looks to be a disap-pointing one in terms of growth.

Will the Fed Really Hike in 2015?by Jonathan Turek

The Fed has continuously said that it will remain “data dependent” when it comes to assessing the time to lift off. Other economic factors will also worry

the Fed, most notably the strength of the US dollar. The DXY dollar index remains at multi year highs, and in Forex markets the dollar has been king relative to other

major currencies. There are benefits to a strong dollar, such as lower input costs in manufacturing and increased purchasing power for US citizens abroad. A strong

15 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

dollar also can incur losses for multi-nationals as weak currency translation weakens earnings; exporters struggle to stay competitive as cheaper substitutes come to market. For America’s biggest multinational corporations these issues will hamper earnings power in quarters to come. Another concern for the Fed is inflation. As many countries in Europe and developed Asia struggle with defla-tion, the U.S. still has inflation numbers above 1%; unfortunately the Fed targets a 2% number. PCE, which is the Fed’s preferred method of tracking inflation, has not reached 2% in 34 months. These readings show concern for an economy that has been in expansion for six years and has had unorthodox monetary policy to assist it. One of the main drivers of this disinflation has been stagnant wage growth. Wages have limped to the up-side in the past few years and 0.3% in the March Bureau of Labor Statistics report. I have a theory that Quantitative Easing has led to perverse incentives in capital allocation that has incentivized compa-

nies to be more worried about short-term stock prices than capital expenditure and longer-term growth. Whether that is true or not is irrelevant because the facts sug-gest that people are still not comfortable with their economic condition and have not felt “safe” enough to really spend, and this is evident with current disinfla-tion. All of these factors make it very dif-ficult for the Fed to raise rates.

What makes this decision all the more interesting is some of the economic backdrops that exist. Many advocates of a rate hike are more concern-oriented rather than raging U.S. economic out-put bulls. We have uncertain economic growth. I understand that is a debated statement but that adds to my point be-cause the last time the Fed hiked rates in 2004, GDP growth was at 7.2% nomi-nally. You have corporate debt currently at around $7 trillion while in 2007 it was around $3.5 trillion; Stanley Drucken-miller of Duquesne Capital Management has been sounding off on this recently. Another concern that exists is the tool

box for the next recession, because if the Fed Funds rate remains close to the zero bound the monetary policies needed to restore economic confidence will be lim-ited. These concerns could lead to a rate hike as they present large questions that the Fed has been unable to answer.

All of this will be in the minds of the Fed governors and Chairwoman Yel-len’s head in the coming months. While many see the need for a lift off of rates, I believe that this dovish Fed will be more diligent and patient (even though they removed this word from their recent pol-icy statement) when it comes to making this all important decision, more so than many others have predicted. I am person-ally in the 2016 camp, but I would not be surprised if the September meeting pres-ents an opportunity for a slight lift off, but I find a June hike unlikely.

Editor’s Note: This article was written in April 2015 and is based on economic and market conditions at that time.

While not all of a person’s income is taxable in Norway, some people there pay more than 100% of their taxable

income.

Fun Fact$ #3

jonathan tuRek Jonathan Turek is Incentives first alumni writer who is currently spending a gap year in Israel at Yeshivat Orayta. Throughout his high school career, Jonathan was defined by his passion for economics and capital markets. Whether it be a deep conversation of macroeconomics or a debate over the intricate details of finance, Jon was always there to add his two cents. After completing his learning in Israel, Jonathan hopes to pursue a degree in finance at Yeshiva University.

16SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

Less than a year af-ter the 9/11 attacks on the World Trade

Center, President George Bush stated, “We fight against pover-ty because hope is an answer to terror.” Laura Bush, the former First Lady, shared her husband’s opinion on the connection be-tween socio-economic class and terrorism (Socio-econom-ic class is a measure of social class based off a number of fac-tors including income and edu-cation). The First Lady claimed that, “Educated children are much more likely to embrace the values that defeat terror.” However, the notion that ter-rorism stems from poverty and lack of education extends be-yond the White House. For ex-ample, James Wolfensohn, the former World Bank President, believes, “The war on terrorism will not be won until we have come to grips with the problem of poverty, and thus the sources of discontent.” Whether it be in the White House or the World Bank, the prevailing assump-tion regarding the origins of terrorism was that it stemmed from poverty and poor educa-tion. Over the past few years, economists have become skep-tical of this assumption, ques-tioning the seemingly causative connection between poverty and terrorism. Their findings have reshaped the way we look at and attempt to combat the

Exploding EconomiesA Look at the Economics of Terrorism by Benjamin Elias

by Eliana Rohrig

17 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

evolving and growing problem that is terrorism.

On July 17th 2008, a petite Paki-stani woman was arrested in Afghanistan. This woman, Aafia Siddiqui, was car-rying notes and instructions for making bombs along with containers of sodium cyanide when she was arrested. Siddiqui was not merely a courier of weapons, but was even among the FBI’s list of seven most wanted terrorists. Some may as-sume along the lines of President Bush and Mr. Wolfensohn and link Siddiqui’s motives to poverty or a lack of education. When looking into Siddiqui’s background, one might expect to see some form of military history or ties with radical Islamist groups; however, what one will actually find is that Siddiqui lived in America during the 1990’s and the early 2000’s. Dur-ing her time in the U.S., Siddiqui at-tended MIT, where she triple majored in biology, anthropol-ogy, and archaeology. She then graduated in 1995 with a Bachelors of Science in biology. While at MIT, Siddiqui did not limit her talents to the classroom. In her junior year, Siddiqui obtained a City Days fel-lowship grant of $1,200 through MIT’s program to help clean up Cambridge el-ementary school playgrounds.

While Siddiqui’s background may seem unusual, it is by no means an outlier among modern terrorists. For instance, in 2007’s unsuccessful car-bombing plot in London, seven of the eight men arrested were doctors. In his study on the eco-nomic roots of terrorism, Alan Krueger, a Princeton economist and former Chair of the President’s Council of Economic Ad-visors, found that a country’s economic performance is not a statistically signifi-

cant predictor of their terrorist popula-tion. In another one of Krueger’s studies he revealed that, “As a group, terrorists are better educated and from wealthier families than the typical person in the same age group in the societies from which they originate.” While not ev-ery terrorist has tripled majored at MIT and obtained a PhD, Krueger holds that, “there is not much question that poverty has little to do with terror-

i s m . ” And so it seems that both President Bush and World Bank President, James Wolfensohn, were wrong, for there is little to no connection between socioeco-nomic status and an individual becoming a terrorist. But how could we all be so wrong? Why are all these educated and economically stable individuals resorting to such violence?

When pondering the impact a col-lege education will have on success in the job market, few consider the value

of a college degree in the field of terror-ism. In 2007, a study on “Attack Assign-ments in Terror Organizations and the Productivity of Suicide Bombers” was conducted by Harvard economist Efraim Benmelech and Claude Berrebi of the Rand Corporation. The two attempted to assess terror organizations use of their members just as they would assess pro-ductivity in any industrial study. In their study, Benmelech and Berrebi collected data on suicide bombers in Israel between the years 2000 and 2005. They discov-

ered that just like in any other industry, in the field of terrorism experience

and education improve success rates. According to their data,

older (late 20’s to early 30’s) and more educated suicide

bombers are less likely to get caught than younger, less educated suicide bombers. Thus, the ter-rorists with more edu-cation and experience are utilized in the more high profile cases due to their decreased like-lihood of getting caught

and increased likelihood of killing more people.

To put numbers to these findings, Benmelech and

Berrebi found that for each additional year of age, a ter-

rorist’s chances of getting caught decreased by 12%. Additionally,

Benmelech and Berrebi discovered that a terrorist with education beyond high school is half as likely to be apprehended as a terrorist whose education stops after high school. After conducting their stud-ies, Benmelech and Berrebi found it no surprise that while the average age of the terrorists in the 9/11 attacks was 26, the leader of the operation was a 33 year old leader with a graduate degree. Not only are educated and experienced terrorists more valuable to terror organizations be-cause they are smart and therefore proba-bly more successful, but having a college and or graduate degree goes a far way in

“The prevailing

assumption regarding the origins of terrorism was that it

stemmed from poverty and poor education. Over the past few years, economists have become skeptical

of this assumption, questioning the seemingly causative

connection between poverty and terrorism.”

18SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

circumventing counterterrorist selection bias. When going through a screening process someone with a college degree is a lot less suspicious of being a terrorist than someone who has seen little to no formal education, simply because the as-sumption is that college graduates don’t become terrorists. This is also the reason terrorist organizations like to recruit flu-ent English speakers; they seem a lot less suspicious. The extreme of this screen-ing phenomenon occurred in 2006 during a failed liquid explosives plot. One of the arrested suspects from the plot was a woman with a baby, many speculated she planned to hide the liquid explosives in her baby’s bottle. While this particular woman may have been a terrorist, secu-rity forces are less suspicious of women with babies and this particular case did not increase security checks on women with babies. For this exact reason some-one like Siddiqui is not only valuable be-cause her college degree adds brains to a terrorist organization but because her college degree and time spent in the U.S. serves as disguise for a terrorist. As it turns out, it is for the very reason that we so wrongly assume that terrorists won’t be graduates of Western universities (or

universities at all) that terrorist organiza-tions recruit college graduates.

While recruiting benefits may ex-plain the high rates of education and eco-nomic stability among terrorists the ques-tion of why people turn to terrorism if not for poverty still prevails. Among the academic circles there is no universally agreed upon cause of terrorism, however many economists such as Krueger have presented hypothesis. Krueger favors the idea that people turn to terrorism as a result of frustration over lack of civil liberties and political rights. Economist Eli Berman points to religious institu-tions as the perfect structure to support terrorism. One of the biggest problems terror organizations face is mobilization and weeding out low-commitment mem-bers. Religious organizations solve this problem by providing public goods and creating barriers to entry. By providing public goods like prayer houses, people are mobilized while the significant bar-riers of entry such as subscribing to the religion’s way of life turn away all those who are not fully committed.

Economists have made it clear over the past decade that terrorist organiza-tions are not as foreign as many thought

they were. Just as it would affect the auto industry, economics pervades terrorism. Once the U.S. installed metal detectors, the rate of hijackings decreased but other forms of terrorism increased - something any econ student would know as the substitution effect. When governments attempt counter-terrorist efforts, they in-vestigate what locations would have the highest expected value for terrorists to attack and respond based on those val-ues. However, often when one country implements significant counter-terrorist efforts they create a negative externality for other countries by diverting attacks to countries which have not focused on counter terrorism as intensely. While the economic thinking behind terrorist groups may be a bit of a scare to those who think of Western education and re-sources as our greatest advantage against terrorism, it is the examination of these groups through economic perspectives that has allowed us to better understand the groups that threaten us most. As we enter a time when our enemies are rec-ognized as college graduates maybe it is also a time that our battles are no longer won with guns on the battlefield but with pens in the classroom.

New Zealand’s currency is called the kiwi, named after the national icon -

the kiwi bird.

Fun Fact$ #4

19 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

Coming after decades of gradual economic unifica-tion in Europe, the euro sig-

nified the official economic unification of members of the eurozone. In order to keep the euro stable, a set of criteria for any country that wished to adopt the euro was established, including an annual rise in inflation no greater than 1.5% while maintaining an annual deficit no bigger than 3% of the GDP and maintaining a debt-to-GDP ratio below 60%. These re-strictions were created in order to force governments to manage their debt bur-den by cutting spending and raising tax-es. In practice however, the restrictions proved to be burdens on many emerging European economies. As Jason Manolo-poulos stated in his book, Greece’s ‘Odi-ous’ Debt, “There was shockingly weak due diligence in assessing the suitability for entry into the euro, and equally weak application of the few rules that were supposed to police its operation.”

By the time the euro was fully implemented in 2002, all the members of the eurozone, in addition to discon-tinuing their own currencies, also dis-continued their monetary policies, thus giving control to the European Central Bank. However, each country was able to maintain its own fiscal policy, a key factor in the current crisis. Before the eurozone, countries like Greece could only borrow a certain amount of money at a high interest rate. Once joining the

eurozone, member countries were able to borrow significantly more money at significantly lower rates like other, more financially stable, countries. The think-ing went, that if countries like Greece could not pay back their debts, other, more stable countries would help pay it back since their economies were tied to the performance of the euro as well. However, as Jason Manolopoulos stated earlier, rules were not well enforced and countries that previously had been lim-ited in the amount of money they could borrow took advantage of the amount of money they could now borrow to the point of accumulating unpayable debts. When credit is available and economies are doing well, all of this spending is not as much of an issue because countries can simply keep on borrowing. Whether a system like this could be sustainable in bad economic times is another question.

In 2008, following the crash of the U.S. housing market, a global credit crisis ensued, essentially bringing much of the global lending to a halt. As a re-sult, countries such as Greece were not able to borrow the same sums of money as before to pay off their budget defi-cits or repay old loans. Ordinarily, this problem would have been relatively con-tained. However, since the euro’s full implementation, the economies of all the countries in the eurozone have become extremely intertwined. As a result, even if a country could not pay back its own

debts, another one would have to or risk significant damage to the euro. So, when many countries could no longer pay back their debts, they all turned to the stron-gest economy in Europe, Germany, to help them.

To understand why Germany had the strongest economy and was asked to help save the euro, we must go back into Germany’s past. Following the horrors of World War II, the German economy was in shambles. Many Germans were left homeless, food was rationed and in-dustrial output was only a third of what it was in 1938. A full economic recov-ery may have taken quite some time if not for a series of shrewd economic de-cisions. Just a few years after the war, the German mark was replaced with a significantly fewer amount of deutsche marks, the new German currency. The currency reform was massive; the overall money supply in Germany was reduced by 93%. This move vastly reduced the amount of wealth Germans held. Addi-tionally, taxes were cut and pre-existing price controls were gradually removed. These economic reforms ended up being so successful that the German economy turned around nearly overnight. Over the next 60 years or so, Germany built itself into the strongest economy in Eu-rope, and one of the strongest in the world. Because of its past, Germany has been both economically sensitive and re-sponsible to ensure the longevity of the

The Eurozoneby Alon FutterPast, Present and Future

20SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

German economy. When other countries in the euro-

zone were having trouble paying back their debts, it was no surprise then, that Germany was called on to bail them out. Germany agreed to bail out several other European countries on the condition that their governments would implement aus-terity measures, meaning a combination of reduced spending, increased taxes and increased debt repayment. While this may appear to be a sound idea on the part of Germany, austerity measures come with their own challenges. By cut-ting spending, a government would be guaranteeing further, even worse eco-nomic hardships, making life harder on its citizens and economic recovery more uncertain, thus making austerity politi-

cally challenging. Additionally, if a gov-ernment spends less money, people will have less money, which in the end will mean lower employment, income and fewer taxes for the government to col-lect.

In the short run, austerity put the brakes on the debt crisis, to an extent. The lack of government spending and improvement in fiscal responsibility did help troubled eurozone countries manage their debt. However, in the longer run, a lack of government spending took its toll and Europe entered into another re-cession in 2011. Furthermore, expected growth for 2015 is a mere 1.2% and the eurozone’s total rate of unemployment is an astonishing 11.5%, compared to the USA’s 5.6%. Needless to say, the euro-

zone has still not fully recovered and the euro is still not particularly strong leav-ing many criticizing austerity and its ad-vocates, namely Germany. Recently, to help stimulate the European economies, the European Central Bank announced a plan to embark on a major bond buy-ing initiative, also known as quantitative easing, in which they will buy a wealth of bonds. By 2016, the ECB is planning to purchase 1.1 trillion euros worth of government and corporate bonds. This is in the hope that the resulting lower in-terest rates will spur economic growth, but more significantly, is a sign that the eurozone has finally sobered up on the reality and results of austerity measures and intends to fix this mistake.

alon futteR After switching to SAR in his sophomore year, Alon quickly found outlets to pursue his interests in poli-tics and journalism as a member of the Model UN team and the Buzz, SAR’s official newspaper. Alon’s passion for economics surfaced in his Junior year after reading Charles Wheelan’s Naked Economics. Recently, Alon has characterized his economic stance as “post modernist” and looks forward to an economic future in which “computers will replace politicians.” Alon hopes

to find some fellow “post modernist” comrades as he pursues a degree in finance at New York University.

33% of the S&P 500 CEOs’ undergraduate degrees are in

engineering and only 11% are in business administration.

Fun Fact$ #5

21 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

The controversy of illegal im-migration has always been a pressing issue in contem-

porary American politics. However, it’s time we finally face the facts- Unless you are of Native-American or African-American descent, forced onto boats some 200 years ago, you come from a long line of immigrants. Immigration has and always will be a source of pro-ductivity, promoting labor, trade, and diversity. Unfortunately though, illegal immigrants in our country are viewed as lethal, framed as thieves of American jobs and the source of turning the United States into a post-apocalyptic multicul-tural society. Yet, the economic benefits of illegal immigration are undeniable and the idea of deportation of any kind, is delusional.

The most basic way to look at the positive effects of illegal immigration is through population growth. 80% of total U.S. population growth is due to immi-grants who subsequently boost aggregate demand as both consumers and aggre-gate supply as producers. In fact, popu-lation increase through immigration is the fastest way to grow GDP and would foster economic growth. The national debt is 17.7 trillion dollars, amounting to $56,000 per U.S. household. Increases in population would split that burden among more people. Furthermore, the economic activity produced by the 12 million illegal immigrants in our coun-

try is now visible. According to the Con-gressional Budget Office, “Over the past two decades, most efforts to estimate the fiscal impact of immigration in the Unit-ed States have concluded that, in aggre-gate and over the long term, tax revenues of all types generated by immigrants—both legal and unauthorized—exceed the cost of the services they use.” As very few undocumented workers are able to receive federal benefits, workers contrib-ute about $15 billion a year to Social Se-curity through payroll taxes, while only receiving $1 billion. Last year, the IRS reported that around 50% of unauthor-ized immigrants filed individual income tax returns, whether it be local, state, or federal. The Institute on Taxation and Economic Policy found that if undocu-mented immigrants were to be legalized, tax rates would increase to 7%, amount-ing to billions in government revenue. In total, illegal immigrants have pumped around $250 billion into our economy. Immigrants, like natural citizens, spend billions each year in commercial goods or services as basic consumer capitalists, spurring economic activity and creating jobs in the process.

One of the most misused argument on the anti-immigrant side is that illegal immigrants take American jobs and ret-roactively steal hard earned money from legal workers. While this theory seems legitimate, it has no standing. No- seri-ously. There is no evidence, study, or

research to support this claim. Essen-tially, a new report found that 80% of un-documented workers have low-paying, daily laboring jobs. When asked if they would accept these low paying jobs, oc-cupied by immigrants, most Americans responded that they would not. Actually, when the low paying jobs are available, no Americans take them; The Depart-ment of Labour and Labour Statistics found the vast majority of American citi-zens do not work, or want to work in day laboring jobs. When Arizona tried im-plementing preventative measures to re-strict employment for illegal immigrants known as SB 1070, 2,761 jobs were lost, resulting in a $253 million loss in eco-nomic output according to the Center for American Progress. Clearly, if we were for some reason listen to the fear-mongerers on the anti-immigrant side and deport our workers, it would have severe economic consequences. The USDA reports 3/5 of the hired workers employed in the crop agriculture sector are unauthorized. From the perspective of National Milk Producers Federation, retail milk prices would increase by 61% if its immigrant labor force were to be eliminated. Overall, illegal immigrants represent 5.5% of the entire labor force, and no country looking to progress and prosper, deports 5.5% of their labor force. That’s bad economics, and as a great Democrat once said, “it’s the econ-omy, stupid.”

To Migrate or Not to Migrate?

AFFIRMATIVE by Shabbos Kestenbaum

Are Illegal Immigrants Beneficial to the Economy?

22SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

Illegal immigration negatively af-fects the American economy. First and foremost, illegal immigrants take jobs away from Americans. With over 9 mil-lion Americans jobless and looking for work, unemployed Americans simply do not need any more competition in the job market. Not only is the compe-tition from illegals unwanted, it is also unfair. Employers, whose primary focus is cheap labor, prefer illegal immigrants to documented workers, because illegal immigrants will work for far below mini-mum wage pay. The Pew Hispanic Cen-ter estimates that approximately 8 mil-lion illegal immigrants work in America, thus occupying 8 million jobs that might otherwise go to unemployed Americans. If Americans worked these 8 million jobs rather than illegal immigrants, the unem-ployment rate would drop from under 6.0% to about 0.65%. While people of-ten argue that illegal immigrants occupy jobs unwanted by American workers, the facts show otherwise: The Bureau of La-bor Statistics estimates that the vast ma-jority of illegal immigrants work in food preparation, cleaning and maintenance, construction, or production jobs -- fields

that are already filled overwhelmingly by Americans. It is clear that Americans are willing to work these lower-wage jobs, but cannot find employment simply be-cause the job field is too crowded. With-out illegal immigrants contributing to the busy workforce, many more low-wage jobs would go to Americans.

In addition to taking jobs away from Americans, illegal immigrants re-ceive many costly benefits from the gov-ernment. First, undocumented children attend public schools just like American children. The 1982 U.S. Supreme Court ruling in Plyler vs. Doe ruled that public schools cannot: reject students based on documentation, question student’s legal-ity, or require Social Security numbers in the enrollment process. The Federa-tion for American Immigration Reform estimates that educating undocumented children in the 2014-2015 school year will cost about $761 million. Further-more, $11-$22 billion is spent on welfare for illegal immigrants annually, over $7 billion is spent on Social Security and Medicare, and about $8.1 billion is spent on Medicaid. With almost two-thirds of illegal immigrants paying no taxes, and

the remaining third regaining much of their money in tax refunds and tax cred-its, illegal immigrants contribute little through taxes on a net basis in return for valuable benefits. In 2012, the Federa-tion for American Immigration Reform estimated that illegal immigrants cost American taxpayers about $113 billion annually. With a national debt of more than $17 trillion, taxpayers do not need to assume the financial burdens of il-legal immigrants. By taking jobs from Americans, and receiving expensive benefits from the US government, ille-gal immigrants impose a steep economic cost on the United States. In the wake of President Obama’s unilateral immigra-tion action, Americans must make clear to their representatives that initiatives to help immigrants must primarily assist those who adhere to immigration laws. Amnesty programs should be limited and should quickly move illegal immi-grants to lawful and economically self-sufficient status. The financial burden of illegal immigration is simply too much for the United States to bear.

NEGATIVE by Nate Katz

Rebuttal by Nate Katz:Shabbi, unfortunately, you are

misguided. In this case, you allow your feelings to cloud your economic judge-ment. While I too am saddened by the thought of illegal immigrants being de-ported back to difficult situations in their homelands, I am only trying to point out how economically disastrous it would be to keep them all here. I too am in favor of an ethnically diverse country, I just want all immigrants to go through the legal im-migration process to join the American family. And sure, if we had more people

to split the debt burden with, then each individual family would have to pay less, right? Wrong. There may be more people to split the national debt among, but the national debt would be even higher with all the money that will be spent on these illegal immigrants- immigrants who will benefit even more off of Social Security, Medicaid, welfare, etc. The bottom line here is that our country can’t afford the economic burden. You are quite simply wrong in stating that Americans refuse to work low-wage jobs, considering that low-wage jobs are filled overwhelming-

ly by Americans. And I will close with this: yes, milk prices may increase with the elimination of the immigration labor force. But the reason for this is that im-migrants work for illegally low rates! How can we, as caring Americans, allow these undocumented workers to be taken advantage of by their employers? Rather, they should just do it the old-fashioned way: complying with immigration laws. Do it the right way, don’t allow yourself to be taken advantage of, come to our country legally, and enjoy your own slice of the American dream.

Rebuttal by Shabbos KestenbaumNate, you’re a nice guy and I like

being in history class with you, but no-where do you offer a single idea or prac-tical concrete solution. Your vision of America is a fanatical society. Reality: There are 12 million illegal immigrants.

If we absorb them into our society and grant them full citizenship, we force all to pay taxes, all to live within the law, and all to be productive members of so-ciety as most already are. The United States has the largest economy in the world, and with GDP expected to in-

crease by 4% this year alone, combined with 12 million new workers, economic sustainability and productivity will final-ly be a reality. We are a country of immi-grants and it’s time we stop undermining our values in order to conform to selfish thinking.

23 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

ShaBBoS keStenBaum Shabbos Kestenbaum is sophomore at SAR and the youngest writer for the Economics journal. Shabbos was first introduced to economics by way of politics; issues such as welfare and immigrant workers whetted Shabbos’ appetite for supply and demand. Shabbos’ interests though reach far beyond politics, Shabbos is a member of SAR’s

debate team, slam poetry club and drama society.

nate katz Nate Katz is a sophomore at SAR and has spent his two years at SAR as a member of the Model UN team and the Tennis team. Nate has been introduced to economics by his father who exposed him to classics such as, A Random Walk Down Wall Street. Nate who takes a keen interest in politics, hopes to one day conduct research in the field of behavioral economics.

During Obama’s first term, the federal government

accumulated more debt than it did under the prior 42 U.S presidents combined.

Fun Fact$ #6

24SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

If you walk into an SAR eco-nomics class, you will likely see a classroom overrun with

boys - this is no coincidence. Studies show the high levels of testosterone in men motivate their interest in stocks, trading and gambling. However, despite this unique drive, it is women that have been found to be more successful inves-tors. In fact, the very reason women are better investors than men is in part due to the very hormones in men that attract them to investing.

A recent study by Barclays Capital and Ledbury Research connects the dots. They found that women were more like-ly to make money in the market, largely because they didn’t take as many risks compared to men. The female tendency towards conservative investing could be due to a variety of reasons. This includes greater self-control and perhaps less con-fidence in decision making, two habits which may explain the female tendency towards conservative investing and are shown to become more prevalent under lower testosterone levels. This notion is further supported in a six-year study by two professors, Brad Barber and Ter-rance Odean. Data from over 35,000

households was used and the study con-cluded that men trade on average 45% more than women. Trading frequency reduced the net return for men by 2.65% and that of women by 1.72%. Thus, not only do men trade with higher frequency, but also they trade with less efficiency compared to women.

Sometimes trading is profitable and if done right, can make one a fortune. However, studies have shown that men generally have not seemed to maximize trading’s potential as a result of taking risks investing behind limited home-work. Nelli Oster, Director and Invest-ment Strategist at BlackRock Capital, explained, “Several studies, including a national survey by LPL Financial, show that women tend to research investments in depth before making portfolio deci-sions, and the process, as a result, tends to take more time.” He further stated, “Women also tend to be more patient as investors and consult their advisors be-fore adjusting their portfolio positioning, whereas men are more prone to market timing impulses. To gather information, women often prefer group discussions to men’s more independent learning ap-proach.” Others have argued that women

more often believe that money represents security and independence and therefore view it as a long-term, non-monetary goal. They are also not as reluctant to seeking advice on their decisions, as op-posed to the majority of men who pre-fer to make independent financial deci-sions. According to a Prudential study, 44% of women say they usually rely on some input from a professional advisor. Greater planning and collaboration when it comes to making financial decisions seems to be a factor in women’s greater success in the capital markets. Clearly, as women’s investing habits and greater returns show, doing your homework is the key to success, whether inside the classroom or out on Wall Street.

It is a common misperception that men are the ones that dominate the fi-nancial markets, that their nature is more favorable to business and finance. How-ever, as many new studies suggest, it is women who are generally more success-ful in the stock market. Don’t be fooled by the underrepresentation of women in SAR’s economic classes. While the boys may own the classroom today, don’t be surprised if it is the girls that own the market tomorrow.

TradingGenders

by Shoshana Rosenzweig

ShoShana RoSenzweig Shoshana is a senior at SAR high school. Shoshana has enjoyed her four years in high school as a member of the JCC on the Palisades swim team. After discovering her swim coach is actually a retired economics professor, Shoshana began researching economics and quickly fell in love with macroeconomics. Shoshana hopes to pursue a

degree in biology at the University of Michigan where she hopes to also swim for the Women’s varsity swim team.

Men, Womenand Investing

by Liat Katz

25 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

T (718)884.2222 F (718)884.3175

www.riverdalekoshermarket.com

5677 Riverdale AveBronx NY 10471

T (718)708.7004

www.thepizzablock.com

26SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

I don’t really believe in global warming but I was going to buy a hybrid car anyway to save on

gas mileage. Now that gas is so cheap, I no longer have the same incentive to buy a hybrid. What do you think I should do?

At the root of your question is sim-ply whether or not the price of gas will remain low. Like everything straight-forward in economics, this is primarily dependant on supply and demand. Cur-rently, there is more gas being produced than is needed. In other words, supply is higher than demand. Due to recent developments such as the American oil boom, supply has increased. Meanwhile, the world’s largest oil cartel, OPEC, has made the decision to not decrease pro-duction and raise prices. Leading this movement is Saudi Arabia whom, in a similar scenario in the 1980’s in which prices were falling, decreased produc-tion in order to counter the falling prices and ended up losing market share. Re-cently, King Salman of Saudi Arabia, learning from his country’s mistakes 30 years ago, promised that oil will remain below 100 dollars a barrel. However, other countries will possibly have to cut back production. The price of oil is sim-ply too low for many countries to make

a profit. On the other hand, Saudi Arabia can produce at a relatively cheap rate and has piled up cash reserves of $750B to help in case prices slip even too much for them. Many will try and hold out, hoping to survive long enough to see the price rise, but at current rates, the oil industry is a money loser for most oil-producing countries and some will have to fold. This will inevitably decrease pro-duction and cause prices to rise.

However, it is the demand side that is more concerning for you. While the decrease in demand itself is not the key concern, the nature of the decrease in de-mand is. Perhaps it’s because the world is now transitioning to solar energy. Un-fortunately, it’s not.. At some point, if the excessive stimulus campaigns abroad do not work, America will probably feel additional economic drag. Even worse, if oil remains this low, the American oil industry will slow down given that it will be too expensive to expand. Al-ready, we see that expansion has slowed. Drilling projects have been put on hold as the benefits of investment have been outweighed by the dismal prospects of returns. Also, as a reflection of the pains felt by the oil industry, workers at extrac-tion sites are increasingly being laid off by oil companies. Gasoline and oil ex-

traction jobs, although still higher than a year ago, have decreased by nearly three thousand jobs in the first three months of 2015, according to the Bureau of La-bor Statistics. Even while year over year employment is up, the unemployment rate in the industry has increased by 2.7 percentage points, as in 24,000 jobs. As a main sector of post-recession growth, the oil and gas sector’s decline will likely have ripple effects on the overall health of the economy.

In conclusion, prices will likely not remain as low as they are now, but if tough economic times do come, they won’t get too high either. Still, your main concern is the economy. I would forego the hybrid, as long as you are not concerned with environmental issues, and in doing so, you can save that money you would be spending up front to get through potentially difficult times in the future. If you end up making the wrong decision it will be because the economy stayed strong - which isn’t that bad all in all. Of course, I would recommend con-sulting someone who has at least taken an economics course, this not including myself, before you make your final deci-sion.

Dear JohnMaynardby Daniel Jubas

daniel juBaS Daniel Jubas is a senior in SAR. While having never taken a high school economics class, Daniel’s interest in economics was probed by reading some of his friend’s economics homework assignments. Sometimes Daniel also does other’s homeworks in a more formal setting as he has been heavily involved in tutoring in high school. Daniel is also a member of the Jazz band, Student Council and the Model Congress team. After spending a gap year in Israel, Daniel hopes to pursue a

degree in engineering at Princeton University.

27 Economics Journal 2015 SAR High School$ $ $ $ $ $$ $ $ $

Every year, the day after Thanksgiving is marked by floods of people rushing to

do their holiday shopping or buy their new TV. Black Friday, with its promises of huge sales and limited offers, is care-fully crafted to make people spend more money than they otherwise would have. People see that something is “on sale” and suddenly feel they need to have it, even if it had previously never occurred to them to buy it.

The field of behavioral economics explores why people spend money the way they do. In his book Predictably Ir-rational: The Hidden Forces That Shape Our Decisions, MIT professor Dan Ari-ely describes how, “Our irrational behav-iors are neither random nor senseless—they are systematic...We all make the same types of mistakes over and over.” In the case of Black Friday, people turn out year after year to buy that new TV on sale, but once they throw in the mounting

equipment and the extra video game that they just couldn’t resist, they will have spent more money than they saved on the sale.

This type of pattern emerges with coupons. Take the rare SAR student who never goes to Dunkin’ in the morning. If such a student found a Dunkin’ Donuts coupon offering a free donut anytime they buy a large drink, they would be incentivized to make a trip to Dunkin’ Donuts they wouldn’t have taken oth-erwise. In short, a student that usually buys nothing at Dunkin’ has now bought a large drink and a donut, all because he found a coupon.

While regular store sales can have a similar effect on customers, coupons, a form of price discrimination, are unique-ly effective in generating sales. Essential-ly, price discrimination charges different people different prices for the same prod-uct. While one person might be willing to buy something for $3.00, someone

else might only be willing to pay $2.50. Economic blogger Stuart Buck writes in his blog “The Buck Stops Here” that cou-pons allow stores to do this more easily: “The only customers who use coupons are those who find it worth their time to rummage through the Sunday paper and cut out coupons and keep track of them,” he writes. “But if the sellers put the items on sale, it wouldn’t be price discrimina-tion, because all customers would get the same sale price.”

In both of these scenarios, the cus-tomer spends more money with the sup-posed discount than they would have without it. Coupons and other sales, such as those on Black Friday, tend to lead people to buy things that they don’t need or necessarily want, simply because it’s cheaper or free. So next time you see a Dunkin’ Donuts coupon, make sure you really want that free donut.

Anger Management

by Ronit MorrisA Look at Behavioral Economics

Ronit moRRiS Ronit Morris is a senior at SAR high school. Ronit enjoys reading classical literature, long distance running and dancing. In SAR, Ronit can often be found hosting social events with small assortments of food, such as the fan favorite peanut butter and celery. After spending a gap year in Israel, Ronit hopes to pursue a degree in English at Barnard

College.

Apple earns $300,000 per minute.Fun Fact$ #7

28SAR High School Economics Journal 2015 $ $ $ $ $ $ $ $ $ $

After their steepest price decline in more than a year, junk bonds are

finally bouncing back now that in-vestors are caring more about high-er yielding assets. What are junk bonds you may ask? Buying a bond is the process of lending money to someone in exchange for a future re-payment with interest. Junk bonds or high yield bonds are a higher risk investment but they come with ex-pectations of much higher returns. A bond is seen as higher grade when the borrower has better credit, and is strongly expected to pay back the loan on time. Low grade or non-investment grade bonds, aka junk bonds, are issued by companies with low credit ratings who might not necessarily be able to pay it back; to compensate for that risk, there is a higher yield if eventually paid back. Junk bonds have proven re-silient even after other investment grade bonds have been yielding lower amounts to investors. There were even a record 21 “covenant-lite junk-bond” deals in September 2014. These are bonds with even less protection for the people in-