Embed Size (px)

Citation preview

Wealth Strategies Group

Sarah D. McDaniel, CFA

Will Benner

Utkarsh Dalmia

Willis Davis, CFA

Chloe Duanshi

Patrick Gremban

Eliana Greenberg

Income and Estate Tax Planning Toolkit

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

2

Source and Footnotes Guideline

Agenda

Gifting Early

Irrevocable Life Insurance Trust (ILIT)

Marital Credit Shelter Trust (CST)

Grantor Retained Annuity Trust (GRAT)

Sale/Loan to Irrevocable Grantor Trust (IDGT)

Qualified Personal Residence Trust (QPRT)

Charitable Lead Trust (CLT)

Charitable Remainder Trust (CRT)

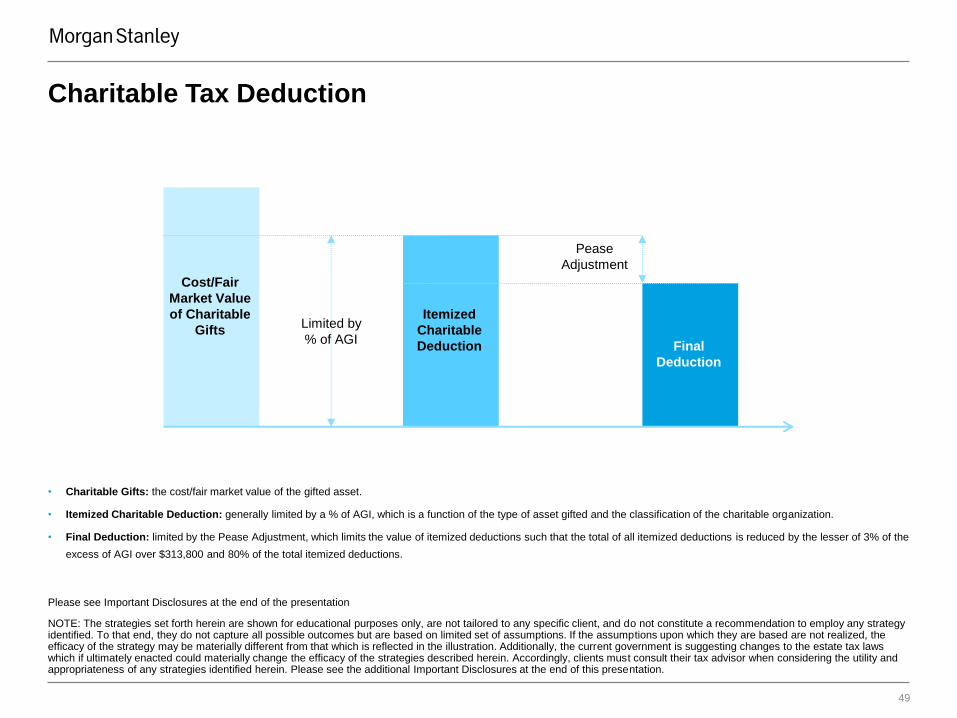

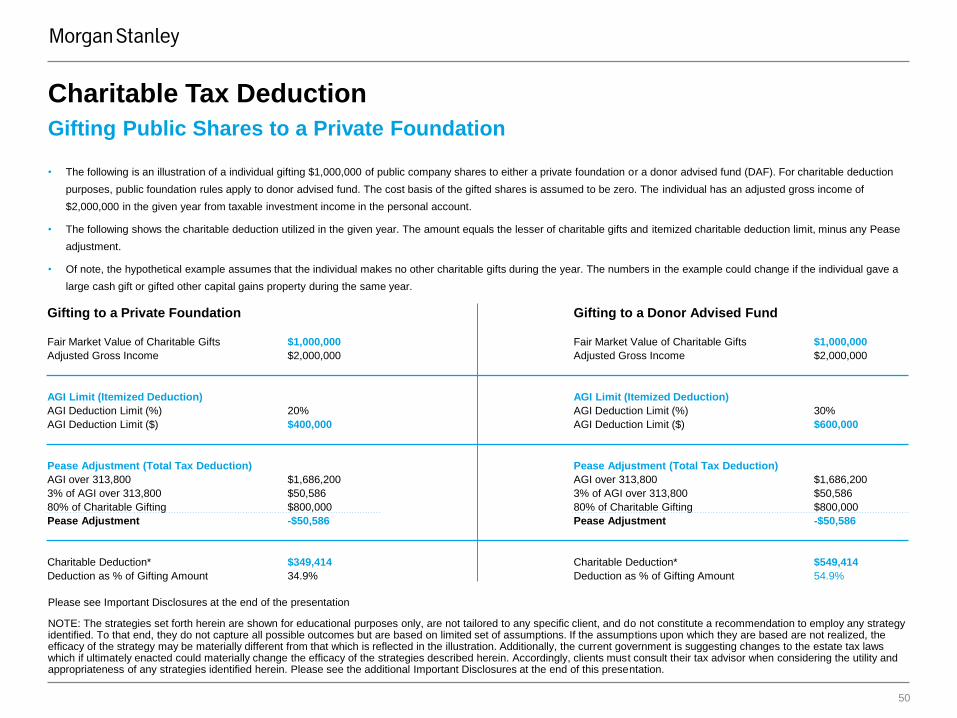

Charitable Tax Deduction

Appendix & Disclosure

Overview

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

4

Source and Footnotes Guideline

Executive Summary

• The Wealth Strategies Group is a differentiating resource within Private Wealth Management and serves as “virtual”

team members for Private Wealth Advisors in the creation of customized strategies for ultra-high net worth families.

The goal of the group is to provide Private Wealth Advisors and clients with holistic solutions that integrate structural,

behavioral and investment decisions.

• The Wealth Strategies Group works closely with clients to thoroughly explore factors relevant to existing or future

estate structures and strategies, and educates clients on general tax and estate planning strategies given specific

objectives, philosophies, concerns, income needs as well as other considerations.

• The goal of Income and Estate Tax Planning Toolkit is to help clients develop a general understanding of the tax and

estate planning techniques. The presentation dedicates one chapter to each technique. Each chapter comprises three

complementary sections: summary of considerations, graphic illustration, and custom example.

• This presentation was designed to illustrate the financial impact of a particular planning decision. The slides herein do

not constitute a recommendation.

Caution: many estate techniques share the common risk of the loss of control of the assets once the gift of the assets

is complete.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Important: The projections regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not

guarantees of future results.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

5

Source and Footnotes Guideline

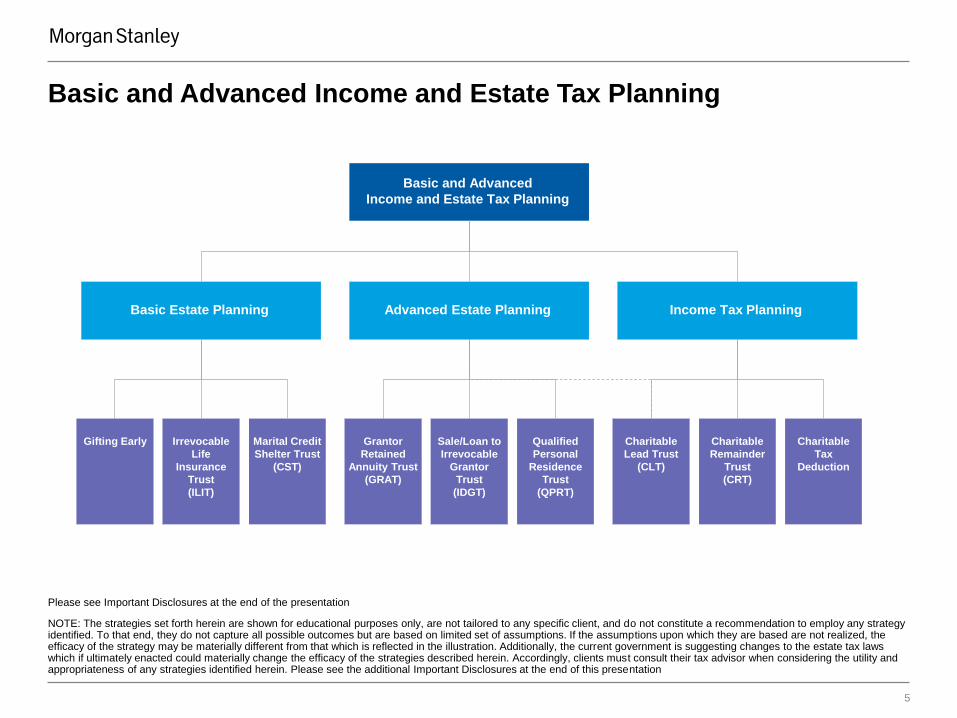

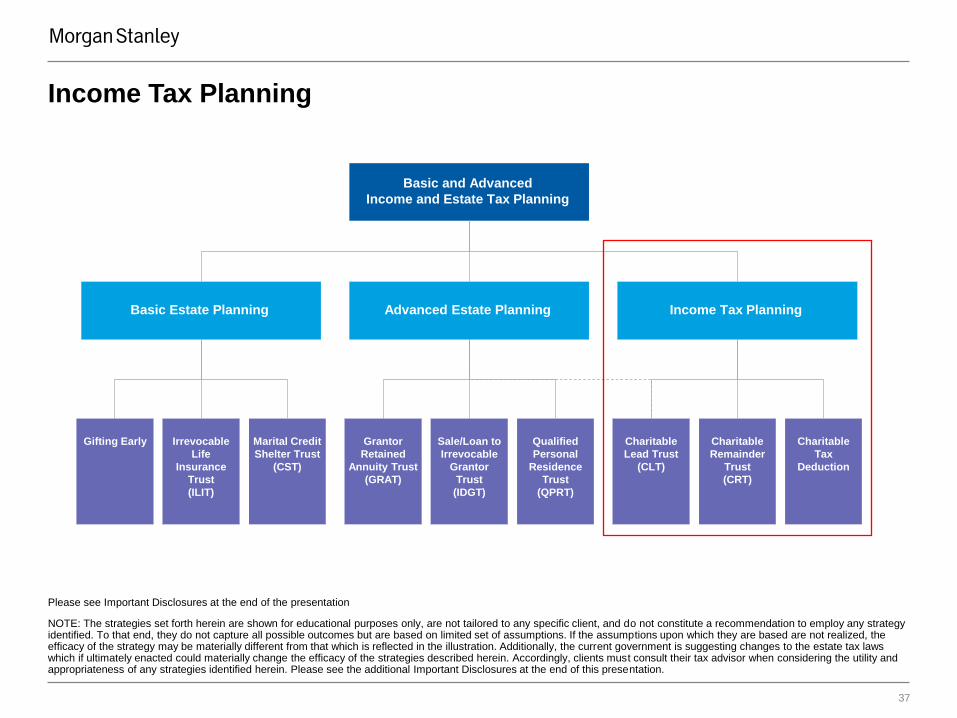

Basic and Advanced Income and Estate Tax Planning

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Basic and Advanced

Income and Estate Tax Planning

Basic Estate Planning Income Tax Planning Advanced Estate Planning

Gifting Early

Irrevocable

Life

Insurance

Trust

(ILIT)

Marital Credit

Shelter Trust

(CST)

Qualified

Personal

Residence

Trust

(QPRT)

Grantor

Retained

Annuity Trust

(GRAT)

Sale/Loan to

Irrevocable

Grantor

Trust

(IDGT)

Charitable

Tax

Deduction

Charitable

Remainder

Trust

(CRT)

Charitable

Lead Trust

(CLT)

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

6

Source and Footnotes Guideline

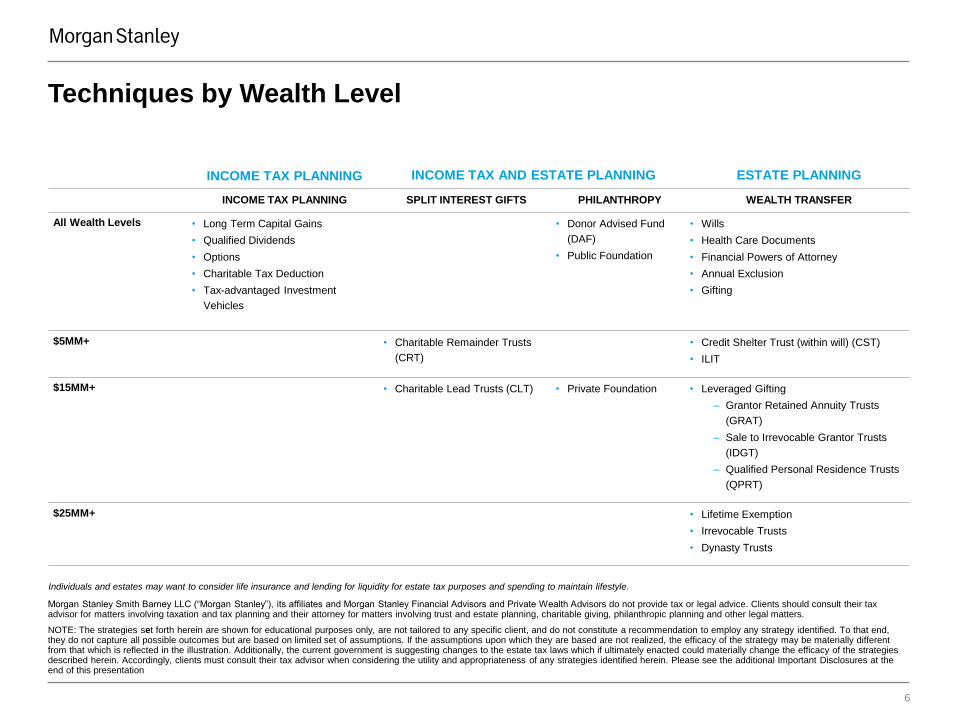

Techniques by Wealth Level

INCOME TAX PLANNING INCOME TAX AND ESTATE PLANNING ESTATE PLANNING

INCOME TAX PLANNING SPLIT INTEREST GIFTS PHILANTHROPY WEALTH TRANSFER

All Wealth Levels • Long Term Capital Gains

• Qualified Dividends

• Options

• Charitable Tax Deduction

• Tax-advantaged Investment

Vehicles

• Donor Advised Fund

(DAF)

• Public Foundation

• Wills

• Health Care Documents

• Financial Powers of Attorney

• Annual Exclusion

• Gifting

$5MM+ • Charitable Remainder Trusts

(CRT)

• Credit Shelter Trust (within will) (CST)

• ILIT

$15MM+ • Charitable Lead Trusts (CLT) • Private Foundation • Leveraged Gifting

– Grantor Retained Annuity Trusts

(GRAT)

– Sale to Irrevocable Grantor Trusts

(IDGT)

– Qualified Personal Residence Trusts

(QPRT)

$25MM+ • Lifetime Exemption

• Irrevocable Trusts

• Dynasty Trusts

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Individuals and estates may want to consider life insurance and lending for liquidity for estate tax purposes and spending to maintain lifestyle.

Morgan Stanley Smith Barney LLC (“Morgan Stanley”), its affiliates and Morgan Stanley Financial Advisors and Private Wealth Advisors do not provide tax or legal advice. Clients should consult their tax advisor for matters involving taxation and tax planning and their attorney for matters involving trust and estate planning, charitable giving, philanthropic planning and other legal matters.

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

7

Source and Footnotes Guideline

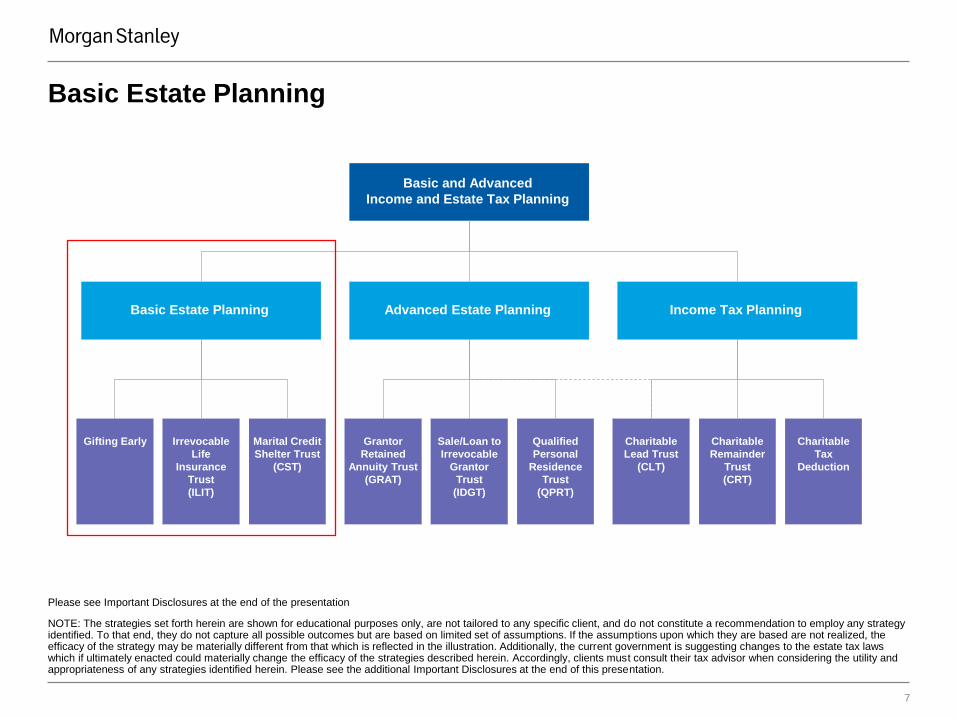

Basic Estate Planning

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation.

Basic and Advanced

Income and Estate Tax Planning

Basic Estate Planning Income Tax Planning Advanced Estate Planning

Gifting Early

Irrevocable

Life

Insurance

Trust

(ILIT)

Marital Credit

Shelter Trust

(CST)

Qualified

Personal

Residence

Trust

(QPRT)

Grantor

Retained

Annuity Trust

(GRAT)

Sale/Loan to

Irrevocable

Grantor

Trust

(IDGT)

Charitable

Tax

Deduction

Charitable

Remainder

Trust

(CRT)

Charitable

Lead Trust

(CLT)

Please see Important Disclosures at the end of the presentation

Gifting Early

SECTION 1

Basic Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

9

Source and Footnotes Guideline

Gifting Early

Gift Tax

• Generally, all transfers prior to death (except those to charity or a U.S. citizen spouse) are subject to gift tax. Excluded from gift tax are the $14,000 “annual exclusion” gifts per

recipient. Of note, there may be as many recipients as desired. Direct payments of certain medical and educational expenses on anyone’s behalf are also excluded from gift tax.

• Under the American Taxpayer Relief Act of 2012 (“the Act”), the inflation-adjusted $5MM gift tax credit was made permanent, and this amount is adjusted for inflation. When

taxable gifts total the available exemption ($5.49MM in 2017) the credit is fully used and the gift tax is assessed on any additional gifts. The maximum rate of the federal gift tax

for any gifts in excess of the exemption amount is 40%. A limited number of states also impose a gift tax in addition to the federal gift tax. To the extent an individual wants to

transfer asset free of tax beyond available credits or exclusions, more advanced gifting strategies need to be employed.

Estate Tax

• The amount that can be passed at death free of estate tax increased in 2017 to $5,490,000. The maximum federal estate tax rate on any estate in excess of $5.49 million is 40%.

Certain states also impose an estate tax in addition to the federal estate tax. The cost basis of asset included in a decedent’s gross estate will generally be adjusted to fair market

value on the date of the decedent’s death, which is referred to as a “step up” on basis when the asset has appreciated in value. Asset can also receive a “step down” in basis

depending on the value.

Gifting Early

• Individuals anticipating an estate in excess of the federal estate tax exemption amount often consider making gifts because a lifetime gift removes the asset and any of its future

appreciation from the total estate. This potentially reduces the total estate and gift tax.

• Individuals may enhance the potential benefit of gifting early by creating an irrevocable grantor trust. If a trust is structured as a grantor trust, the grantor of the trust is treated as

the owner of the trust asset for income tax purposes. By paying taxes incurred in the trust, the grantor effectively makes an indirect gift to the trust, which is not subject to gift tax.

• If the asset gifted represent a non-managing membership of a Family Limited Partnership (FLP) or Limited Liability Company (LLC), an appraisal of the asset may reflect a

potential liquidity discount and/or a potential lack of control discount. Gifting with valuation discounts may further enhance the wealth transfer.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

10

Source and Footnotes Guideline

Gifting Early

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

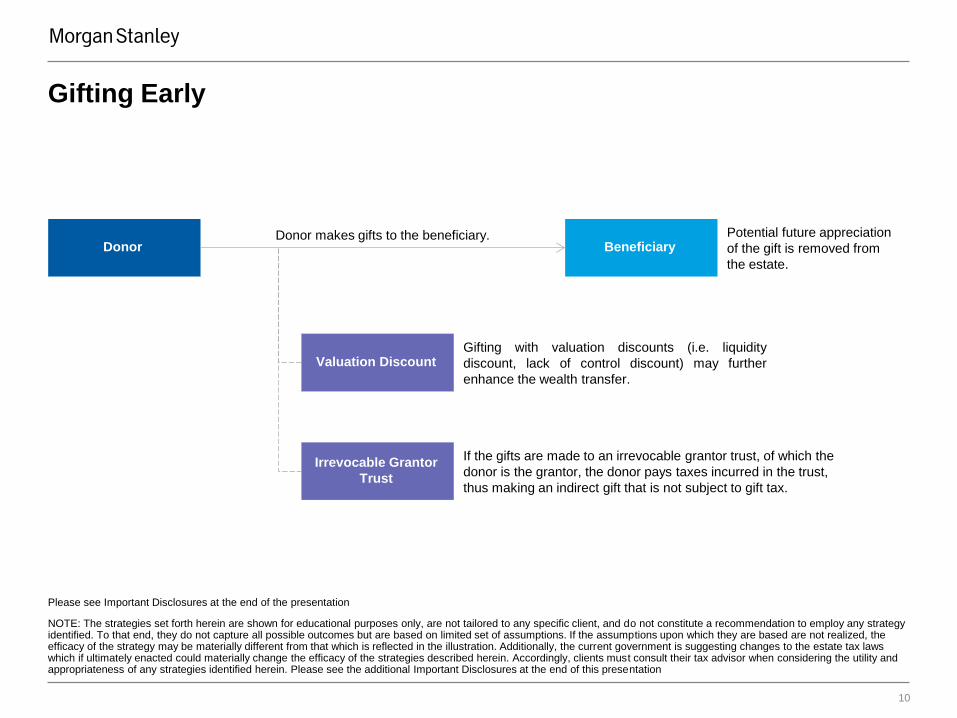

Donor Beneficiary Donor makes gifts to the beneficiary.

If the gifts are made to an irrevocable grantor trust, of which the

donor is the grantor, the donor pays taxes incurred in the trust,

thus making an indirect gift that is not subject to gift tax.

Potential future appreciation

of the gift is removed from

the estate.

Valuation Discount Gifting with valuation discounts (i.e. liquidity

discount, lack of control discount) may further

enhance the wealth transfer.

Irrevocable Grantor

Trust

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

11

Source and Footnotes Guideline

Gifting Early

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

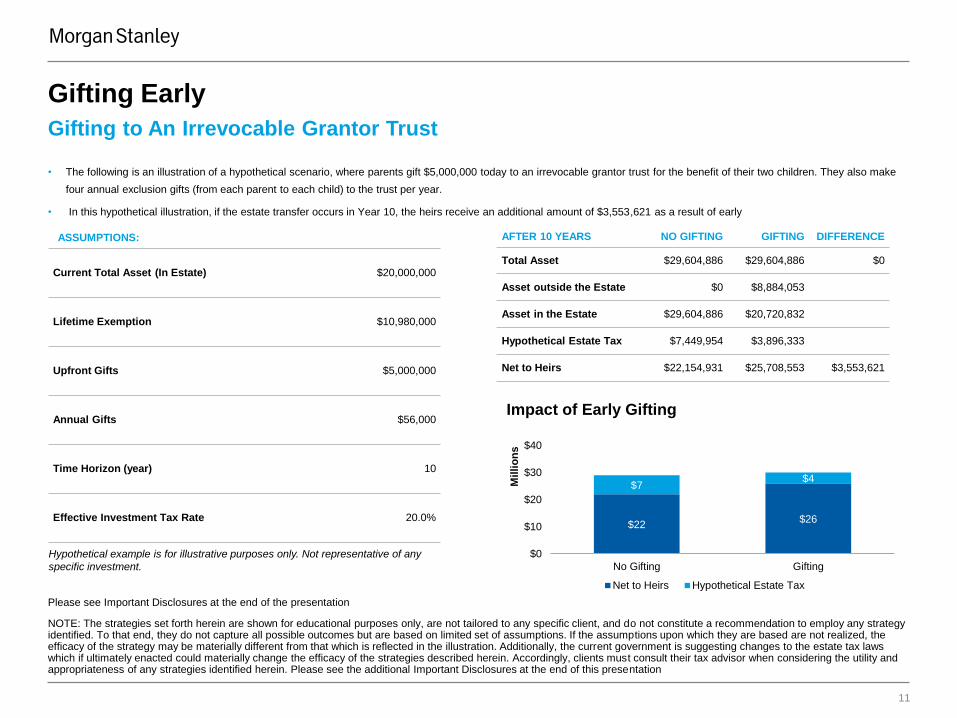

Gifting to An Irrevocable Grantor Trust

• The following is an illustration of a hypothetical scenario, where parents gift $5,000,000 today to an irrevocable grantor trust for the benefit of their two children. They also make

four annual exclusion gifts (from each parent to each child) to the trust per year.

• In this hypothetical illustration, if the estate transfer occurs in Year 10, the heirs receive an additional amount of $3,553,621 as a result of early

Impact of Early Gifting

$22 $26

$7 $4

$0

$10

$20

$30

$40

No Gifting Gifting

Mil

lio

ns

Net to Heirs Hypothetical Estate Tax

ASSUMPTIONS:

Current Total Asset (In Estate) $20,000,000

Lifetime Exemption $10,980,000

Upfront Gifts $5,000,000

Annual Gifts $56,000

Time Horizon (year) 10

Effective Investment Tax Rate 20.0%

Hypothetical example is for illustrative purposes only. Not representative of any

specific investment.

AFTER 10 YEARS NO GIFTING GIFTING DIFFERENCE

Total Asset $29,604,886 $29,604,886 $0

Asset outside the Estate $0 $8,884,053

Asset in the Estate $29,604,886 $20,720,832

Hypothetical Estate Tax $7,449,954 $3,896,333

Net to Heirs $22,154,931 $25,708,553 $3,553,621

Please see Important Disclosures at the end of the presentation

Irrevocable Life Insurance Trust (ILIT)

SECTION 2

Basic Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

13

Source and Footnotes Guideline

Irrevocable Life Insurance Trust (ILIT)

Life insurance can be used to help protect one’s family by replacing lost future earnings or to help provide liquidity to pay estate taxes

or other expenses. However, the proceeds of a life insurance policy owned or controlled by the insured will generally be included in his

or her gross estate for estate tax purposes. A life insurance policy can be excluded from an insured’s gross estate if an irrevocable trust

(rather than the insured himself or herself) purchases the insurance.

• Creating an Irrevocable Life Insurance Trust (ILIT): An ILIT is set up during the insured’s lifetime in order to purchase a life insurance policy.

Upon the death of the insured, the proceeds are paid to the ILIT generally free of estate tax. If an insured transfers an existing insurance policy

to the ILIT, the proceeds will still be subject to estate tax in his or her estate unless he or she survives the transfer by three years (the “three-

year contemplation of death rule”).

• Paying Premiums: In order to fund the policy, the insured typically makes gifts to the trust so that the trustee may pay the premiums on the life

insurance. Gifts made to a trust will qualify for the annual gift tax exclusion if the beneficiaries are given certain rights of withdrawal over the gifts

contributed to the trust (“Crummey powers”). If the ILIT contains Crummey powers and a notification is sent to each beneficiary, the gifts will be

allocated to the annual exclusion gifts. If the gifts exceed the annual exclusions, then they will count toward the grantor’s lifetime exemption

(currently $5,490,000). When the gifts exceed both the annual exclusion and lifetime exemption available, a gift tax would be payable on the

excess amount.

• Payment of Death Benefit: The proceeds of a life insurance policy paid to an ILIT upon the death of the insured are generally received income

tax free and estate tax free. Once received by the trustee, the proceeds are administered according to the terms of the trust agreement. When

drafted properly, the asset held in an ILIT is exempt from claim of the beneficiary's creditors.

• Selecting a trustee: The insured cannot be the trustee of an ILIT. However, when the trust is drafted to provide distributions of income and/or

principal to the beneficiary according to a standard known as HEMS (health, education, maintenance, and support), the insured’s spouse and/or

children can be a trustee. Alternatively, a corporate fiduciary can be selected as the trustee due to the ongoing administration and

responsibilities once the proceeds are paid.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

14

Source and Footnotes Guideline

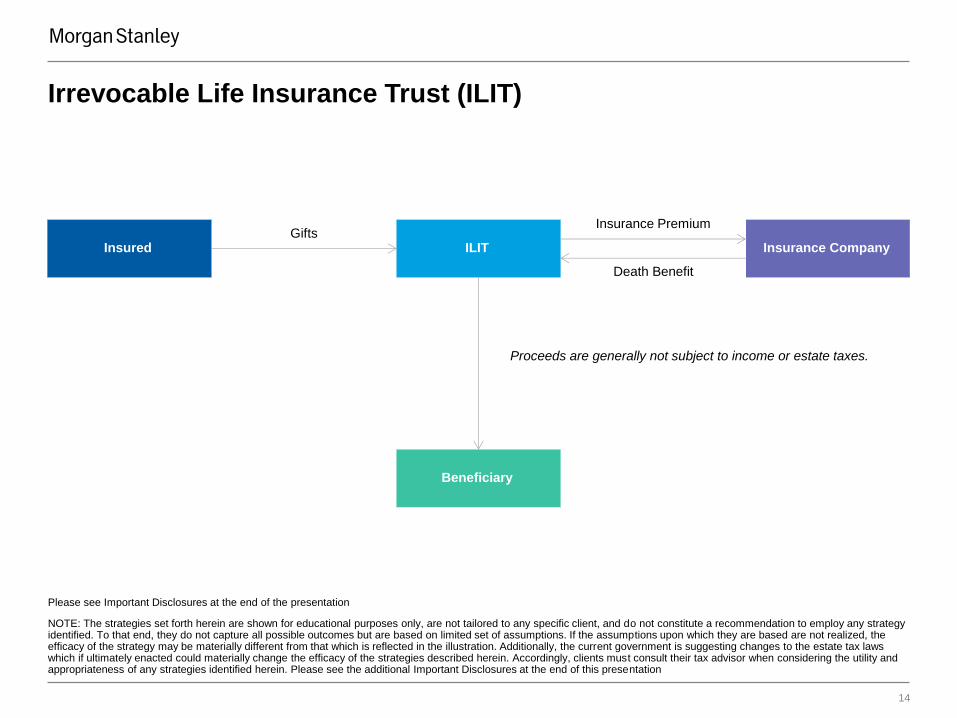

Irrevocable Life Insurance Trust (ILIT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Insured ILIT

Beneficiary

Insurance Premium Gifts

Insurance Company

Death Benefit

Proceeds are generally not subject to income or estate taxes.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

15

Source and Footnotes Guideline

Irrevocable Life Insurance Trust (ILIT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

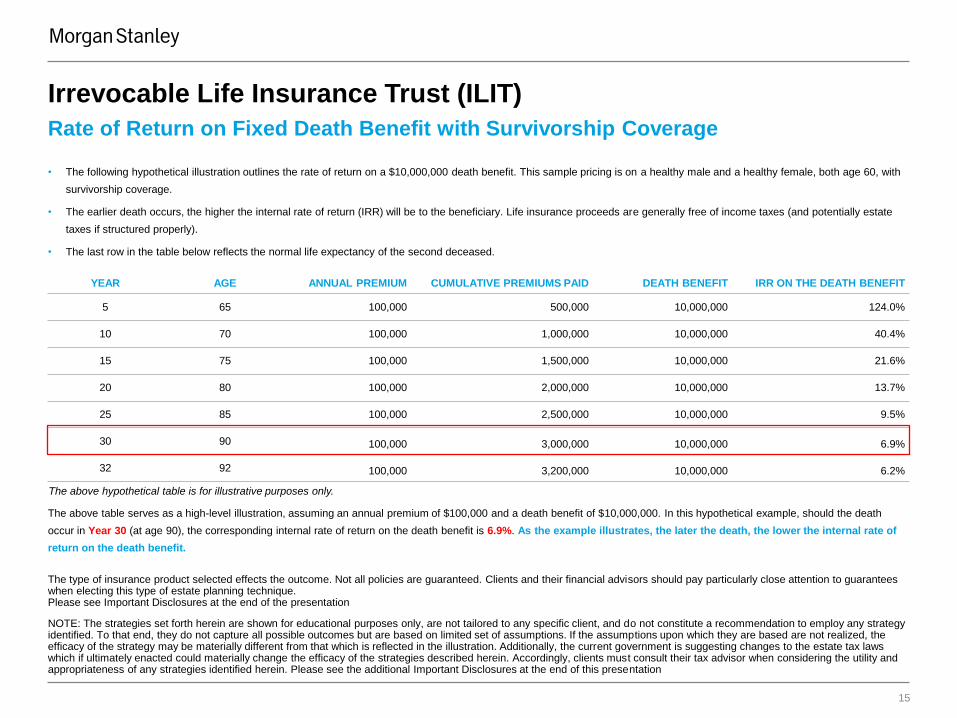

Rate of Return on Fixed Death Benefit with Survivorship Coverage

• The following hypothetical illustration outlines the rate of return on a $10,000,000 death benefit. This sample pricing is on a healthy male and a healthy female, both age 60, with

survivorship coverage.

• The earlier death occurs, the higher the internal rate of return (IRR) will be to the beneficiary. Life insurance proceeds are generally free of income taxes (and potentially estate

taxes if structured properly).

• The last row in the table below reflects the normal life expectancy of the second deceased.

The above hypothetical table is for illustrative purposes only.

YEAR AGE ANNUAL PREMIUM CUMULATIVE PREMIUMS PAID DEATH BENEFIT IRR ON THE DEATH BENEFIT

5 65 100,000 500,000 10,000,000 124.0%

10 70 100,000 1,000,000 10,000,000 40.4%

15 75 100,000 1,500,000 10,000,000 21.6%

20 80 100,000 2,000,000 10,000,000 13.7%

25 85 100,000 2,500,000 10,000,000 9.5%

30 90 100,000 3,000,000 10,000,000 6.9%

32 92 100,000 3,200,000 10,000,000 6.2%

The above table serves as a high-level illustration, assuming an annual premium of $100,000 and a death benefit of $10,000,000. In this hypothetical example, should the death

occur in Year 30 (at age 90), the corresponding internal rate of return on the death benefit is 6.9%. As the example illustrates, the later the death, the lower the internal rate of

return on the death benefit.

The type of insurance product selected effects the outcome. Not all policies are guaranteed. Clients and their financial advisors should pay particularly close attention to guarantees when electing this type of estate planning technique. Please see Important Disclosures at the end of the presentation

Marital Credit Shelter Trust (CST)

SECTION 3

Basic Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

17

Source and Footnotes Guideline

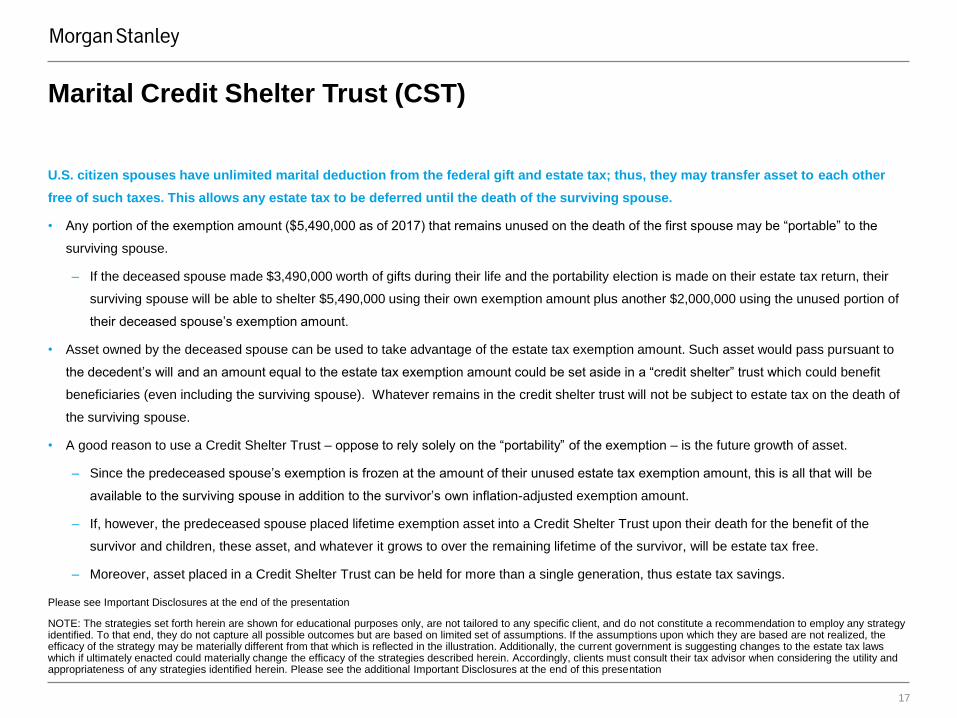

Marital Credit Shelter Trust (CST)

U.S. citizen spouses have unlimited marital deduction from the federal gift and estate tax; thus, they may transfer asset to each other

free of such taxes. This allows any estate tax to be deferred until the death of the surviving spouse.

• Any portion of the exemption amount ($5,490,000 as of 2017) that remains unused on the death of the first spouse may be “portable” to the

surviving spouse.

– If the deceased spouse made $3,490,000 worth of gifts during their life and the portability election is made on their estate tax return, their

surviving spouse will be able to shelter $5,490,000 using their own exemption amount plus another $2,000,000 using the unused portion of

their deceased spouse’s exemption amount.

• Asset owned by the deceased spouse can be used to take advantage of the estate tax exemption amount. Such asset would pass pursuant to

the decedent’s will and an amount equal to the estate tax exemption amount could be set aside in a “credit shelter” trust which could benefit

beneficiaries (even including the surviving spouse). Whatever remains in the credit shelter trust will not be subject to estate tax on the death of

the surviving spouse.

• A good reason to use a Credit Shelter Trust – oppose to rely solely on the “portability” of the exemption – is the future growth of asset.

‒ Since the predeceased spouse’s exemption is frozen at the amount of their unused estate tax exemption amount, this is all that will be

available to the surviving spouse in addition to the survivor’s own inflation-adjusted exemption amount.

‒ If, however, the predeceased spouse placed lifetime exemption asset into a Credit Shelter Trust upon their death for the benefit of the

survivor and children, these asset, and whatever it grows to over the remaining lifetime of the survivor, will be estate tax free.

‒ Moreover, asset placed in a Credit Shelter Trust can be held for more than a single generation, thus estate tax savings.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

18

Source and Footnotes Guideline

Marital Credit Shelter Trust (CST)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

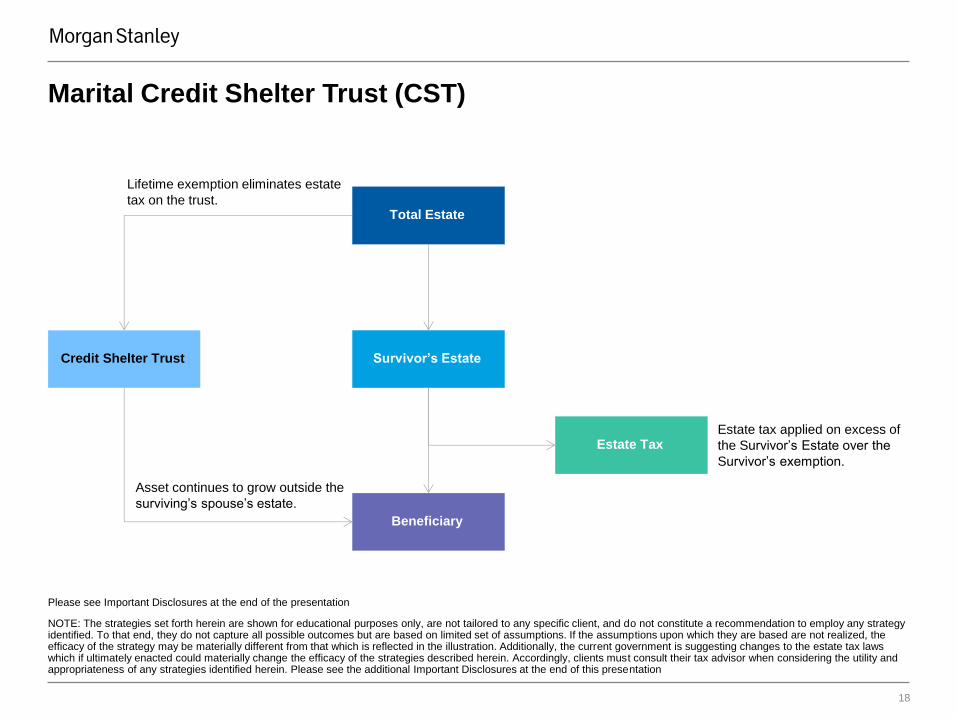

Total Estate

Credit Shelter Trust

Beneficiary

Asset continues to grow outside the

surviving’s spouse’s estate.

Estate Tax Estate tax applied on excess of

the Survivor’s Estate over the

Survivor’s exemption.

Survivor’s Estate

Lifetime exemption eliminates estate

tax on the trust.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

19

Source and Footnotes Guideline

Marital Credit Shelter Trust (CST)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

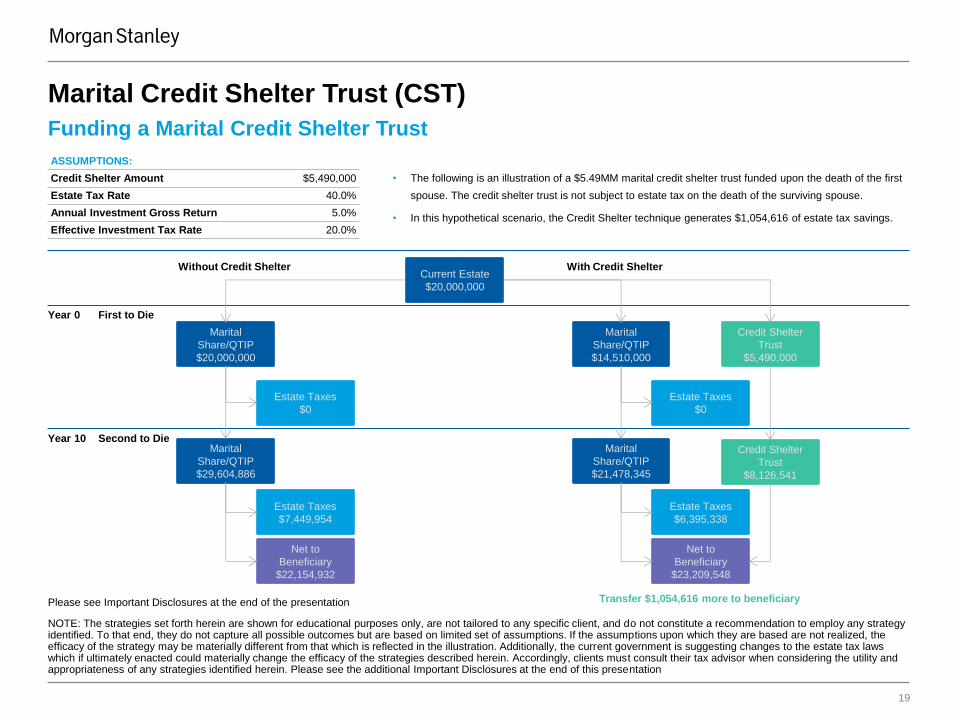

Funding a Marital Credit Shelter Trust

• The following is an illustration of a $5.49MM marital credit shelter trust funded upon the death of the first

spouse. The credit shelter trust is not subject to estate tax on the death of the surviving spouse.

• In this hypothetical scenario, the Credit Shelter technique generates $1,054,616 of estate tax savings.

ASSUMPTIONS:

Credit Shelter Amount $5,490,000

Estate Tax Rate 40.0%

Annual Investment Gross Return 5.0%

Effective Investment Tax Rate 20.0%

Marital

Share/QTIP

$20,000,000

Marital

Share/QTIP

$29,604,886

Estate Taxes

$0

Estate Taxes

$7,449,954

Net to

Beneficiary

$22,154,932

Marital

Share/QTIP

$14,510,000

Marital

Share/QTIP

$21,478,345

Estate Taxes

$0

Estate Taxes

$6,395,338

Net to

Beneficiary

$23,209,548

Credit Shelter

Trust

$5,490,000

Credit Shelter

Trust

$8,126,541

Transfer $1,054,616 more to beneficiary

With Credit Shelter Without Credit Shelter

Year 0 First to Die

Year 10 Second to Die

Please see Important Disclosures at the end of the presentation

Current Estate

$20,000,000

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

20

Source and Footnotes Guideline

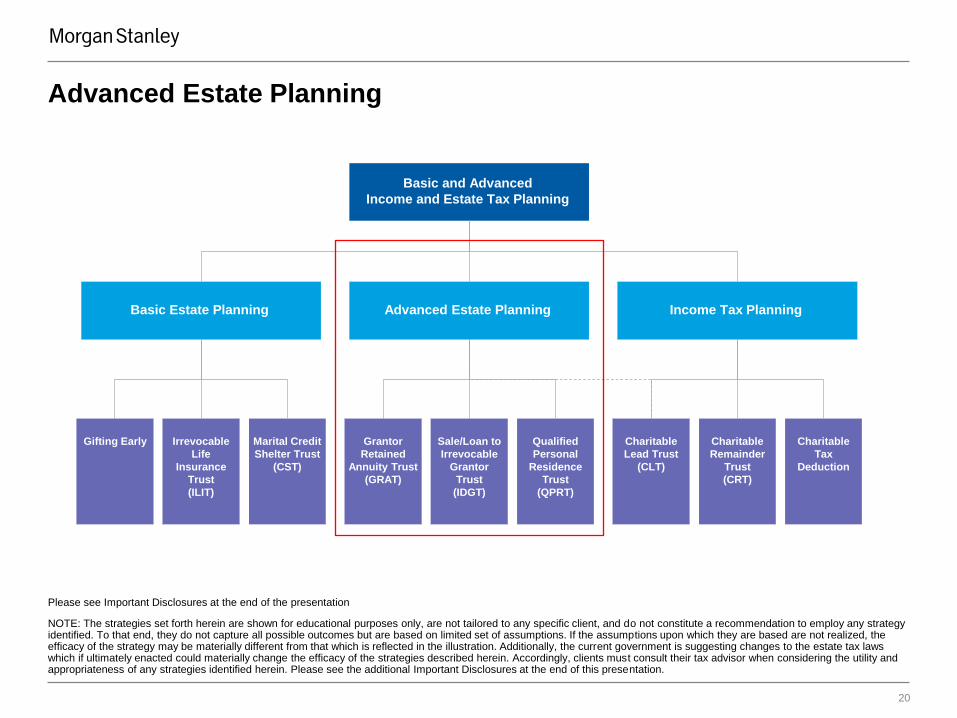

Advanced Estate Planning

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation.

Basic and Advanced

Income and Estate Tax Planning

Basic Estate Planning Income Tax Planning Advanced Estate Planning

Gifting Early

Irrevocable

Life

Insurance

Trust

(ILIT)

Marital Credit

Shelter Trust

(CST)

Qualified

Personal

Residence

Trust

(QPRT)

Grantor

Retained

Annuity Trust

(GRAT)

Sale/Loan to

Irrevocable

Grantor

Trust

(IDGT)

Charitable

Tax

Deduction

Charitable

Remainder

Trust

(CRT)

Charitable

Lead Trust

(CLT)

Please see Important Disclosures at the end of the presentation

Grantor Retained Annuity Trust (GRAT)

SECTION 4

Advanced Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

22

Source and Footnotes Guideline

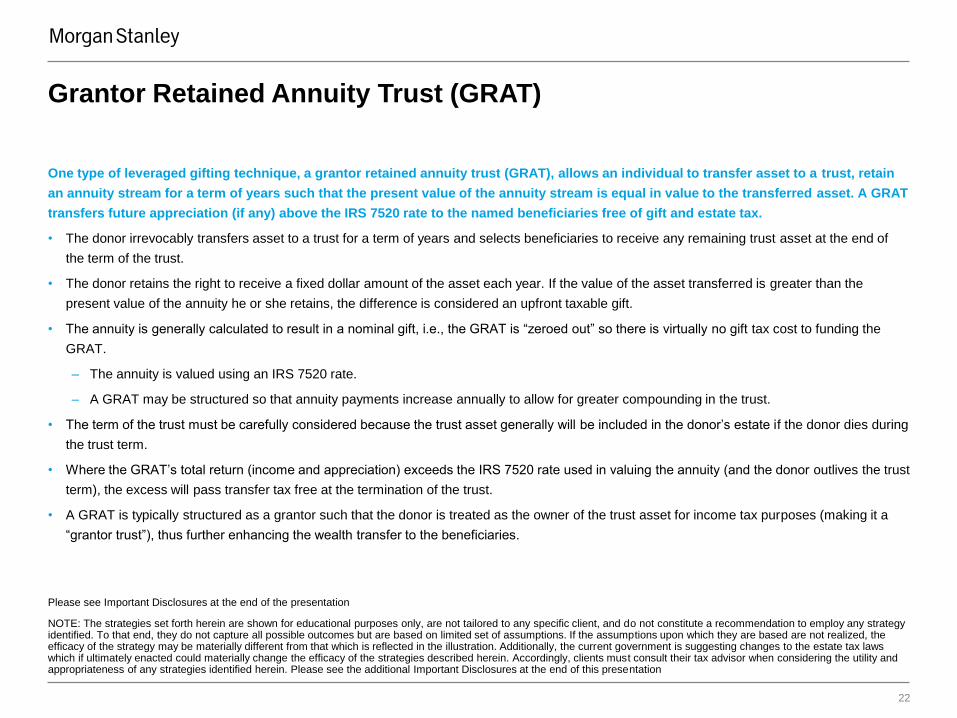

Grantor Retained Annuity Trust (GRAT)

One type of leveraged gifting technique, a grantor retained annuity trust (GRAT), allows an individual to transfer asset to a trust, retain

an annuity stream for a term of years such that the present value of the annuity stream is equal in value to the transferred asset. A GRAT

transfers future appreciation (if any) above the IRS 7520 rate to the named beneficiaries free of gift and estate tax.

• The donor irrevocably transfers asset to a trust for a term of years and selects beneficiaries to receive any remaining trust asset at the end of

the term of the trust.

• The donor retains the right to receive a fixed dollar amount of the asset each year. If the value of the asset transferred is greater than the

present value of the annuity he or she retains, the difference is considered an upfront taxable gift.

• The annuity is generally calculated to result in a nominal gift, i.e., the GRAT is “zeroed out” so there is virtually no gift tax cost to funding the

GRAT.

– The annuity is valued using an IRS 7520 rate.

– A GRAT may be structured so that annuity payments increase annually to allow for greater compounding in the trust.

• The term of the trust must be carefully considered because the trust asset generally will be included in the donor’s estate if the donor dies during

the trust term.

• Where the GRAT’s total return (income and appreciation) exceeds the IRS 7520 rate used in valuing the annuity (and the donor outlives the trust

term), the excess will pass transfer tax free at the termination of the trust.

• A GRAT is typically structured as a grantor such that the donor is treated as the owner of the trust asset for income tax purposes (making it a

“grantor trust”), thus further enhancing the wealth transfer to the beneficiaries.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

23

Source and Footnotes Guideline

Grantor Retained Annuity Trust (GRAT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

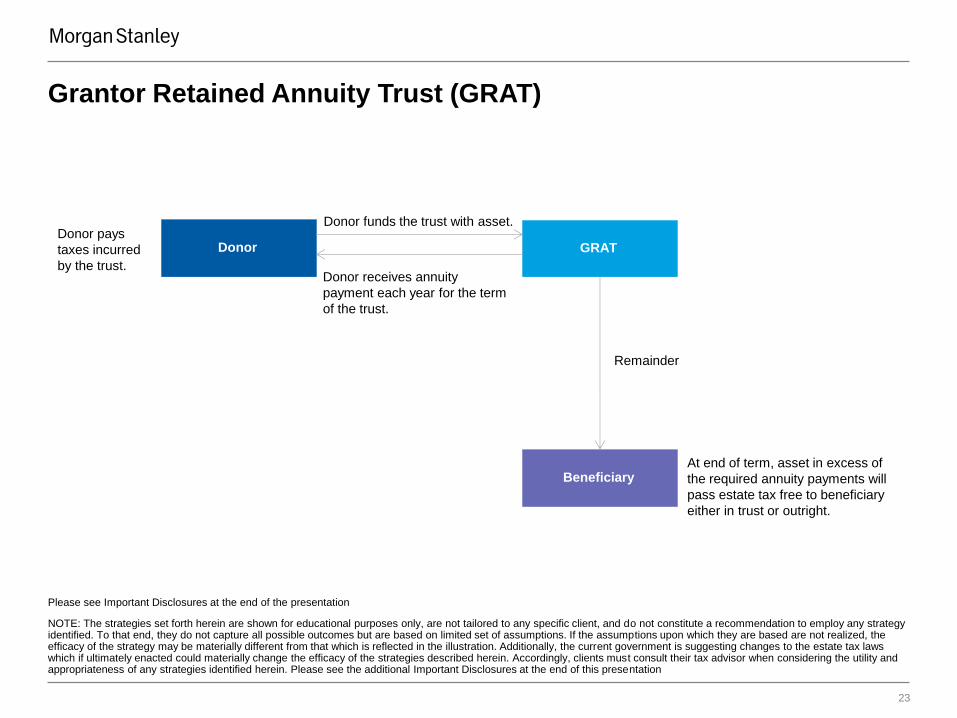

Donor GRAT

Beneficiary

Donor receives annuity

payment each year for the term

of the trust.

At end of term, asset in excess of

the required annuity payments will

pass estate tax free to beneficiary

either in trust or outright.

Donor funds the trust with asset.

Remainder

Donor pays

taxes incurred

by the trust.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

24

Source and Footnotes Guideline

Grantor Retained Annuity Trust (GRAT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

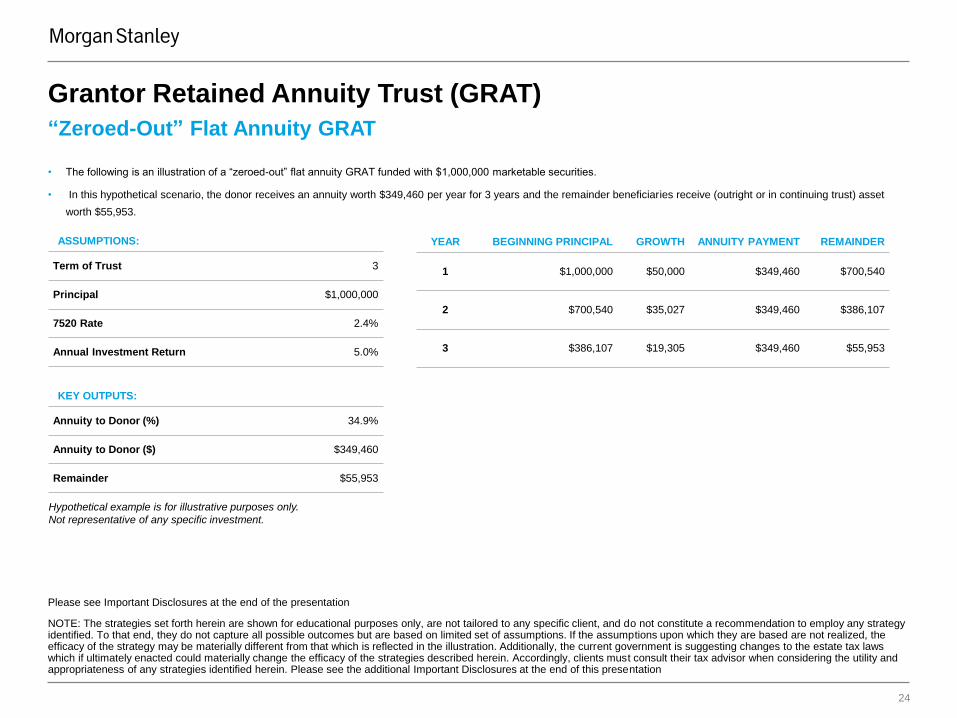

“Zeroed-Out” Flat Annuity GRAT

• The following is an illustration of a “zeroed-out” flat annuity GRAT funded with $1,000,000 marketable securities.

• In this hypothetical scenario, the donor receives an annuity worth $349,460 per year for 3 years and the remainder beneficiaries receive (outright or in continuing trust) asset

worth $55,953.

ASSUMPTIONS:

Term of Trust 3

Principal $1,000,000

7520 Rate 2.4%

Annual Investment Return 5.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

YEAR BEGINNING PRINCIPAL GROWTH ANNUITY PAYMENT REMAINDER

1 $1,000,000 $50,000 $349,460 $700,540

2 $700,540 $35,027 $349,460 $386,107

3 $386,107 $19,305 $349,460 $55,953

KEY OUTPUTS:

Annuity to Donor (%) 34.9%

Annuity to Donor ($) $349,460

Remainder $55,953

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

25

Source and Footnotes Guideline

Grantor Retained Annuity Trust (GRAT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

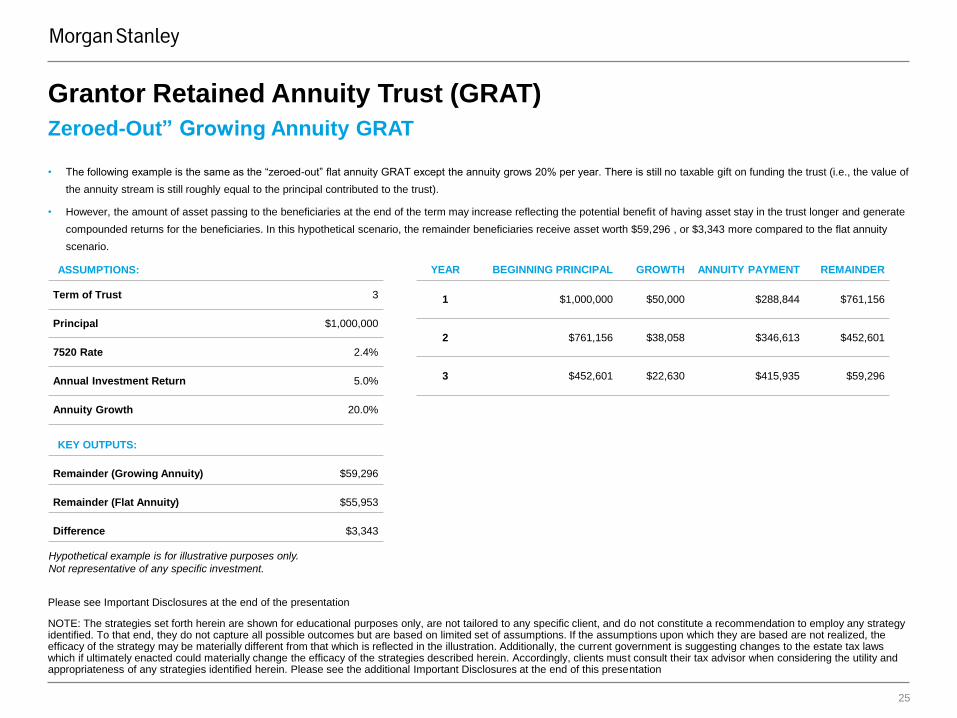

Zeroed-Out” Growing Annuity GRAT

• The following example is the same as the “zeroed-out” flat annuity GRAT except the annuity grows 20% per year. There is still no taxable gift on funding the trust (i.e., the value of

the annuity stream is still roughly equal to the principal contributed to the trust).

• However, the amount of asset passing to the beneficiaries at the end of the term may increase reflecting the potential benefit of having asset stay in the trust longer and generate

compounded returns for the beneficiaries. In this hypothetical scenario, the remainder beneficiaries receive asset worth $59,296 , or $3,343 more compared to the flat annuity

scenario.

ASSUMPTIONS:

Term of Trust 3

Principal $1,000,000

7520 Rate 2.4%

Annual Investment Return 5.0%

Annuity Growth 20.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

KEY OUTPUTS:

Remainder (Growing Annuity) $59,296

Remainder (Flat Annuity) $55,953

Difference $3,343

YEAR BEGINNING PRINCIPAL GROWTH ANNUITY PAYMENT REMAINDER

1 $1,000,000 $50,000 $288,844 $761,156

2 $761,156 $38,058 $346,613 $452,601

3 $452,601 $22,630 $415,935 $59,296

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

26

Source and Footnotes Guideline

Grantor Retained Annuity Trust (GRAT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

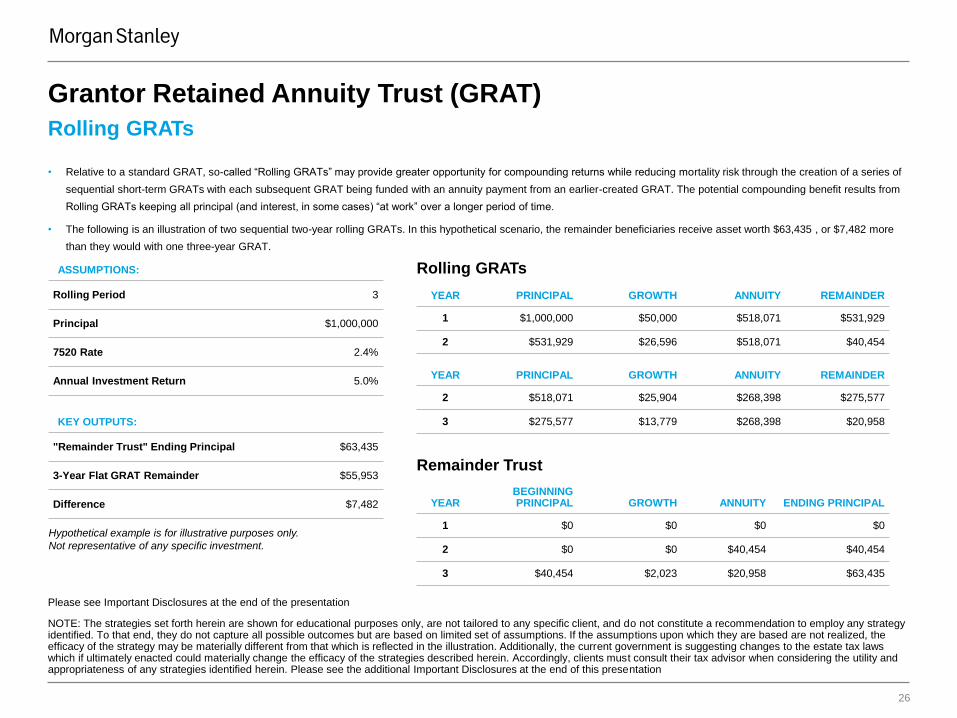

Rolling GRATs

• Relative to a standard GRAT, so-called “Rolling GRATs” may provide greater opportunity for compounding returns while reducing mortality risk through the creation of a series of

sequential short-term GRATs with each subsequent GRAT being funded with an annuity payment from an earlier-created GRAT. The potential compounding benefit results from

Rolling GRATs keeping all principal (and interest, in some cases) “at work” over a longer period of time.

• The following is an illustration of two sequential two-year rolling GRATs. In this hypothetical scenario, the remainder beneficiaries receive asset worth $63,435 , or $7,482 more

than they would with one three-year GRAT.

ASSUMPTIONS:

Rolling Period 3

Principal $1,000,000

7520 Rate 2.4%

Annual Investment Return 5.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

KEY OUTPUTS:

"Remainder Trust" Ending Principal $63,435

3-Year Flat GRAT Remainder $55,953

Difference $7,482

YEAR PRINCIPAL GROWTH ANNUITY REMAINDER

1 $1,000,000 $50,000 $518,071 $531,929

2 $531,929 $26,596 $518,071 $40,454

Rolling GRATs

YEAR PRINCIPAL GROWTH ANNUITY REMAINDER

2 $518,071 $25,904 $268,398 $275,577

3 $275,577 $13,779 $268,398 $20,958

YEAR BEGINNING PRINCIPAL GROWTH ANNUITY ENDING PRINCIPAL

1 $0 $0 $0 $0

2 $0 $0 $40,454 $40,454

3 $40,454 $2,023 $20,958 $63,435

Remainder Trust

Please see Important Disclosures at the end of the presentation

Sale/Loan to Irrevocable Grantor Trust

SECTION 5

Advanced Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

28

Source and Footnotes Guideline

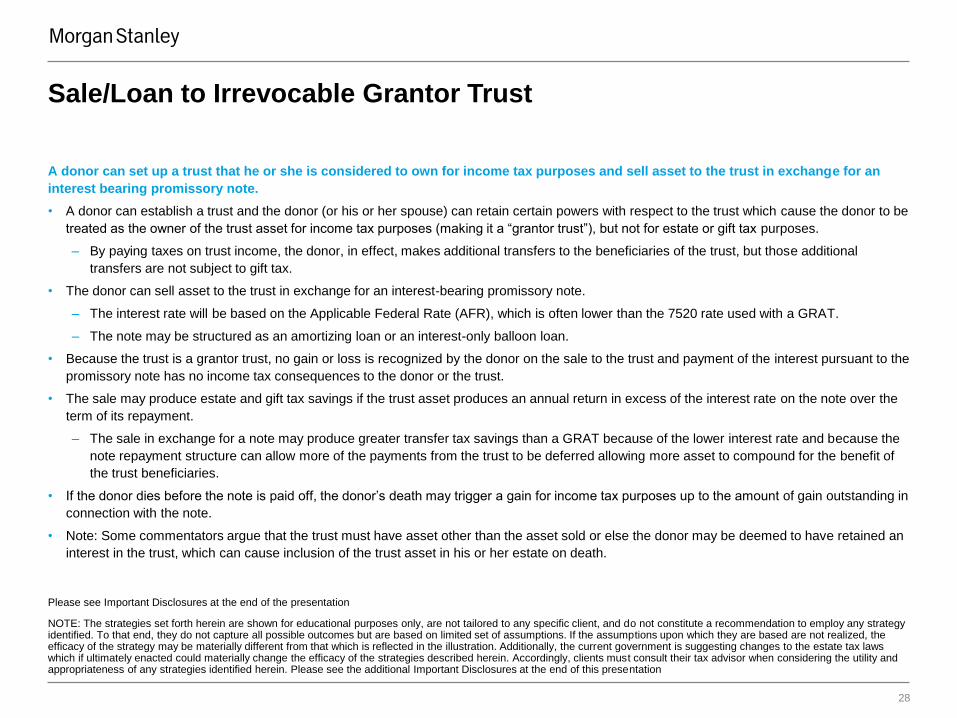

Sale/Loan to Irrevocable Grantor Trust

A donor can set up a trust that he or she is considered to own for income tax purposes and sell asset to the trust in exchange for an

interest bearing promissory note.

• A donor can establish a trust and the donor (or his or her spouse) can retain certain powers with respect to the trust which cause the donor to be

treated as the owner of the trust asset for income tax purposes (making it a “grantor trust”), but not for estate or gift tax purposes.

– By paying taxes on trust income, the donor, in effect, makes additional transfers to the beneficiaries of the trust, but those additional

transfers are not subject to gift tax.

• The donor can sell asset to the trust in exchange for an interest-bearing promissory note.

‒ The interest rate will be based on the Applicable Federal Rate (AFR), which is often lower than the 7520 rate used with a GRAT.

‒ The note may be structured as an amortizing loan or an interest-only balloon loan.

• Because the trust is a grantor trust, no gain or loss is recognized by the donor on the sale to the trust and payment of the interest pursuant to the

promissory note has no income tax consequences to the donor or the trust.

• The sale may produce estate and gift tax savings if the trust asset produces an annual return in excess of the interest rate on the note over the

term of its repayment.

‒ The sale in exchange for a note may produce greater transfer tax savings than a GRAT because of the lower interest rate and because the

note repayment structure can allow more of the payments from the trust to be deferred allowing more asset to compound for the benefit of

the trust beneficiaries.

• If the donor dies before the note is paid off, the donor’s death may trigger a gain for income tax purposes up to the amount of gain outstanding in

connection with the note.

• Note: Some commentators argue that the trust must have asset other than the asset sold or else the donor may be deemed to have retained an

interest in the trust, which can cause inclusion of the trust asset in his or her estate on death.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

29

Source and Footnotes Guideline

Sale/Loan to Irrevocable Grantor Trust

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

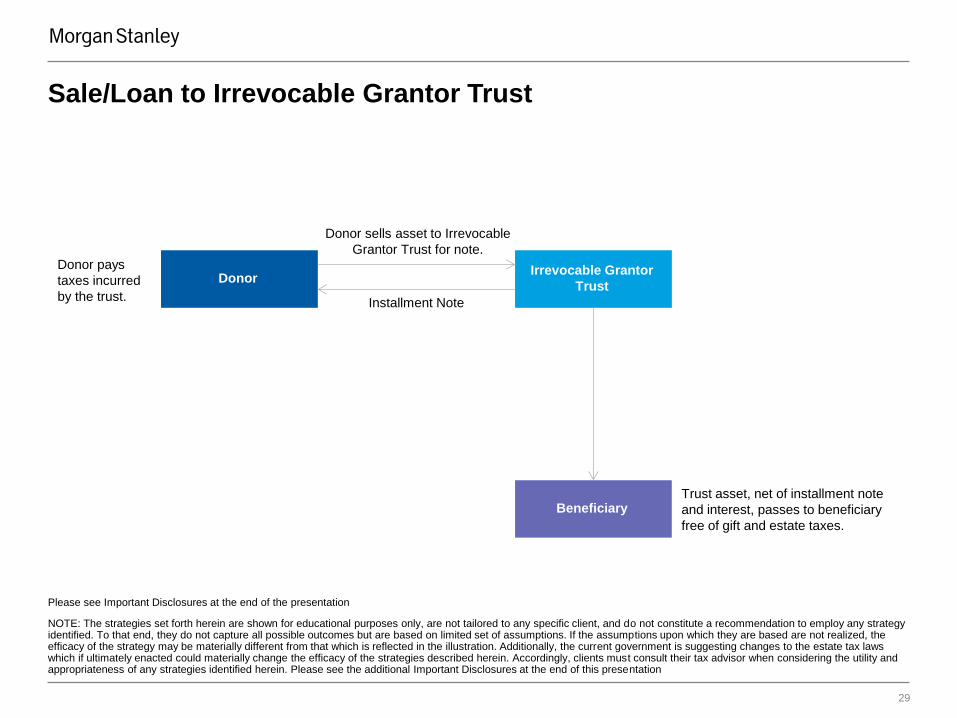

Donor Irrevocable Grantor

Trust

Beneficiary

Donor pays

taxes incurred

by the trust.

Trust asset, net of installment note

and interest, passes to beneficiary

free of gift and estate taxes.

Donor sells asset to Irrevocable

Grantor Trust for note.

Installment Note

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

30

Source and Footnotes Guideline

Sale/Loan to Irrevocable Grantor Trust

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

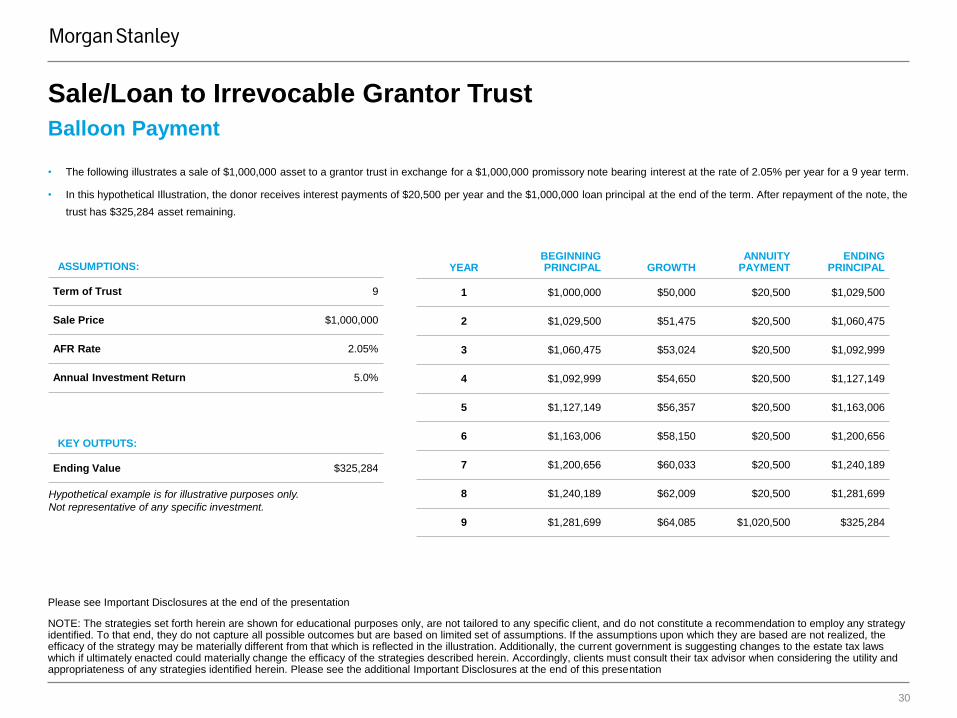

Balloon Payment

• The following illustrates a sale of $1,000,000 asset to a grantor trust in exchange for a $1,000,000 promissory note bearing interest at the rate of 2.05% per year for a 9 year term.

• In this hypothetical Illustration, the donor receives interest payments of $20,500 per year and the $1,000,000 loan principal at the end of the term. After repayment of the note, the

trust has $325,284 asset remaining.

ASSUMPTIONS:

Term of Trust 9

Sale Price $1,000,000

AFR Rate 2.05%

Annual Investment Return 5.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

KEY OUTPUTS:

Ending Value $325,284

YEAR BEGINNING PRINCIPAL GROWTH

ANNUITY PAYMENT

ENDING PRINCIPAL

1 $1,000,000 $50,000 $20,500 $1,029,500

2 $1,029,500 $51,475 $20,500 $1,060,475

3 $1,060,475 $53,024 $20,500 $1,092,999

4 $1,092,999 $54,650 $20,500 $1,127,149

5 $1,127,149 $56,357 $20,500 $1,163,006

6 $1,163,006 $58,150 $20,500 $1,200,656

7 $1,200,656 $60,033 $20,500 $1,240,189

8 $1,240,189 $62,009 $20,500 $1,281,699

9 $1,281,699 $64,085 $1,020,500 $325,284

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

31

Source and Footnotes Guideline

Sale/Loan to Irrevocable Grantor Trust

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

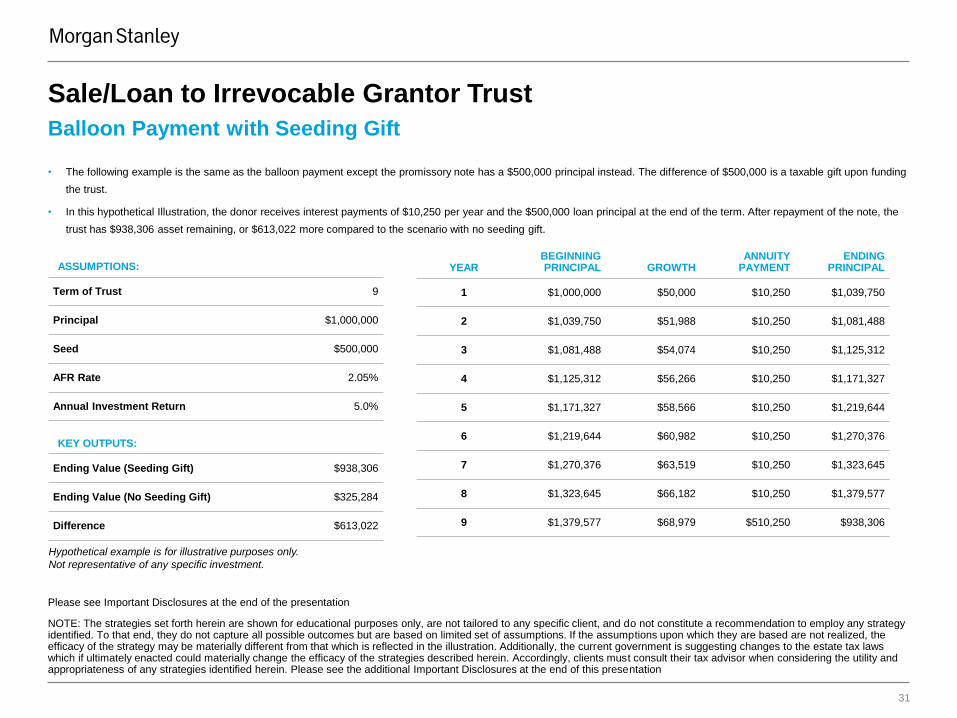

Balloon Payment with Seeding Gift

• The following example is the same as the balloon payment except the promissory note has a $500,000 principal instead. The difference of $500,000 is a taxable gift upon funding

the trust.

• In this hypothetical Illustration, the donor receives interest payments of $10,250 per year and the $500,000 loan principal at the end of the term. After repayment of the note, the

trust has $938,306 asset remaining, or $613,022 more compared to the scenario with no seeding gift.

ASSUMPTIONS:

Term of Trust 9

Principal $1,000,000

Seed $500,000

AFR Rate 2.05%

Annual Investment Return 5.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

KEY OUTPUTS:

Ending Value (Seeding Gift) $938,306

Ending Value (No Seeding Gift) $325,284

Difference $613,022

YEAR BEGINNING PRINCIPAL GROWTH

ANNUITY PAYMENT

ENDING PRINCIPAL

1 $1,000,000 $50,000 $10,250 $1,039,750

2 $1,039,750 $51,988 $10,250 $1,081,488

3 $1,081,488 $54,074 $10,250 $1,125,312

4 $1,125,312 $56,266 $10,250 $1,171,327

5 $1,171,327 $58,566 $10,250 $1,219,644

6 $1,219,644 $60,982 $10,250 $1,270,376

7 $1,270,376 $63,519 $10,250 $1,323,645

8 $1,323,645 $66,182 $10,250 $1,379,577

9 $1,379,577 $68,979 $510,250 $938,306

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

32

Source and Footnotes Guideline

Sale/Loan to Irrevocable Grantor Trust

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

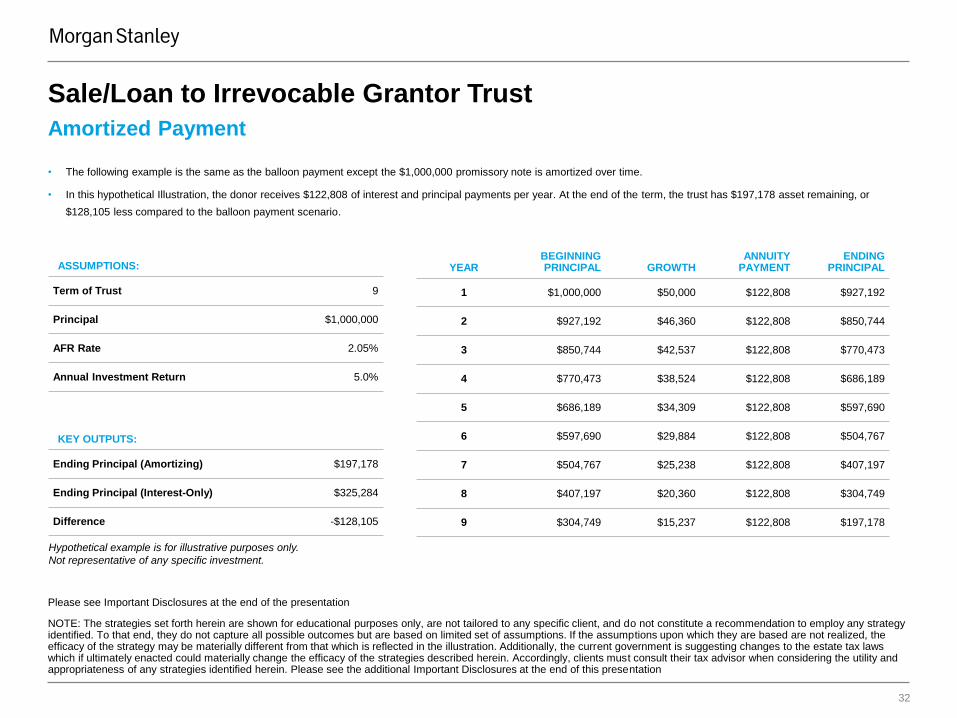

Amortized Payment

• The following example is the same as the balloon payment except the $1,000,000 promissory note is amortized over time.

• In this hypothetical Illustration, the donor receives $122,808 of interest and principal payments per year. At the end of the term, the trust has $197,178 asset remaining, or

$128,105 less compared to the balloon payment scenario.

ASSUMPTIONS:

Term of Trust 9

Principal $1,000,000

AFR Rate 2.05%

Annual Investment Return 5.0%

Hypothetical example is for illustrative purposes only.

Not representative of any specific investment.

KEY OUTPUTS:

Ending Principal (Amortizing) $197,178

Ending Principal (Interest-Only) $325,284

Difference -$128,105

YEAR BEGINNING PRINCIPAL GROWTH

ANNUITY PAYMENT

ENDING PRINCIPAL

1 $1,000,000 $50,000 $122,808 $927,192

2 $927,192 $46,360 $122,808 $850,744

3 $850,744 $42,537 $122,808 $770,473

4 $770,473 $38,524 $122,808 $686,189

5 $686,189 $34,309 $122,808 $597,690

6 $597,690 $29,884 $122,808 $504,767

7 $504,767 $25,238 $122,808 $407,197

8 $407,197 $20,360 $122,808 $304,749

9 $304,749 $15,237 $122,808 $197,178

Please see Important Disclosures at the end of the presentation

Qualified Personal Residence Trust (QPRT)

SECTION 6

Advanced Estate Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

34

Source and Footnotes Guideline

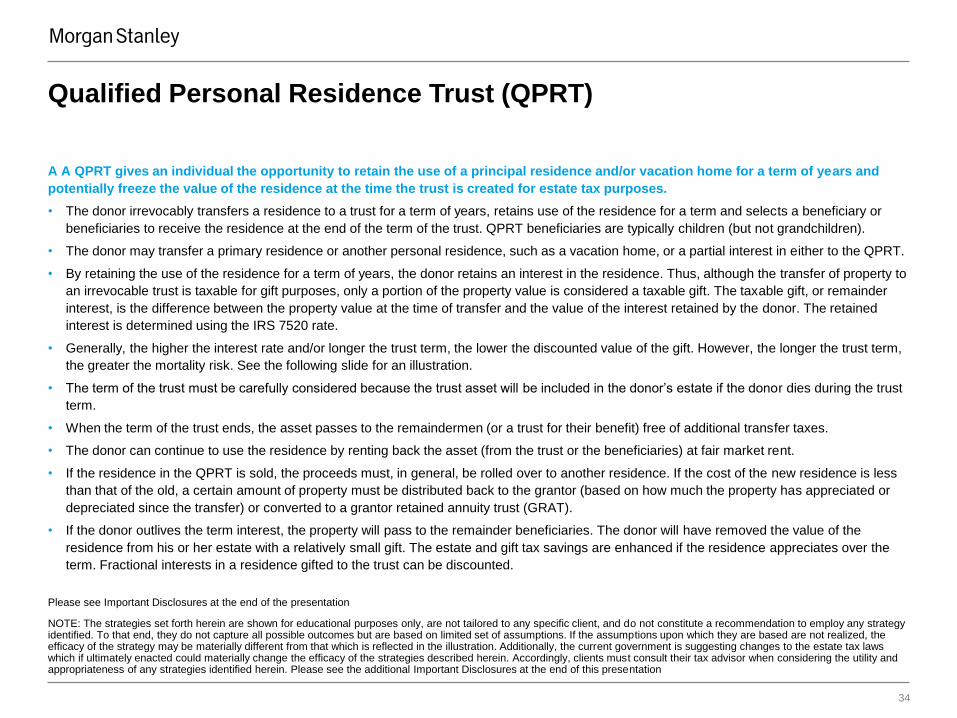

Qualified Personal Residence Trust (QPRT)

A A QPRT gives an individual the opportunity to retain the use of a principal residence and/or vacation home for a term of years and

potentially freeze the value of the residence at the time the trust is created for estate tax purposes.

• The donor irrevocably transfers a residence to a trust for a term of years, retains use of the residence for a term and selects a beneficiary or

beneficiaries to receive the residence at the end of the term of the trust. QPRT beneficiaries are typically children (but not grandchildren).

• The donor may transfer a primary residence or another personal residence, such as a vacation home, or a partial interest in either to the QPRT.

• By retaining the use of the residence for a term of years, the donor retains an interest in the residence. Thus, although the transfer of property to

an irrevocable trust is taxable for gift purposes, only a portion of the property value is considered a taxable gift. The taxable gift, or remainder

interest, is the difference between the property value at the time of transfer and the value of the interest retained by the donor. The retained

interest is determined using the IRS 7520 rate.

• Generally, the higher the interest rate and/or longer the trust term, the lower the discounted value of the gift. However, the longer the trust term,

the greater the mortality risk. See the following slide for an illustration.

• The term of the trust must be carefully considered because the trust asset will be included in the donor’s estate if the donor dies during the trust

term.

• When the term of the trust ends, the asset passes to the remaindermen (or a trust for their benefit) free of additional transfer taxes.

• The donor can continue to use the residence by renting back the asset (from the trust or the beneficiaries) at fair market rent.

• If the residence in the QPRT is sold, the proceeds must, in general, be rolled over to another residence. If the cost of the new residence is less

than that of the old, a certain amount of property must be distributed back to the grantor (based on how much the property has appreciated or

depreciated since the transfer) or converted to a grantor retained annuity trust (GRAT).

• If the donor outlives the term interest, the property will pass to the remainder beneficiaries. The donor will have removed the value of the

residence from his or her estate with a relatively small gift. The estate and gift tax savings are enhanced if the residence appreciates over the

term. Fractional interests in a residence gifted to the trust can be discounted.

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

35

Source and Footnotes Guideline

Qualified Personal Residence Trust (QPRT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

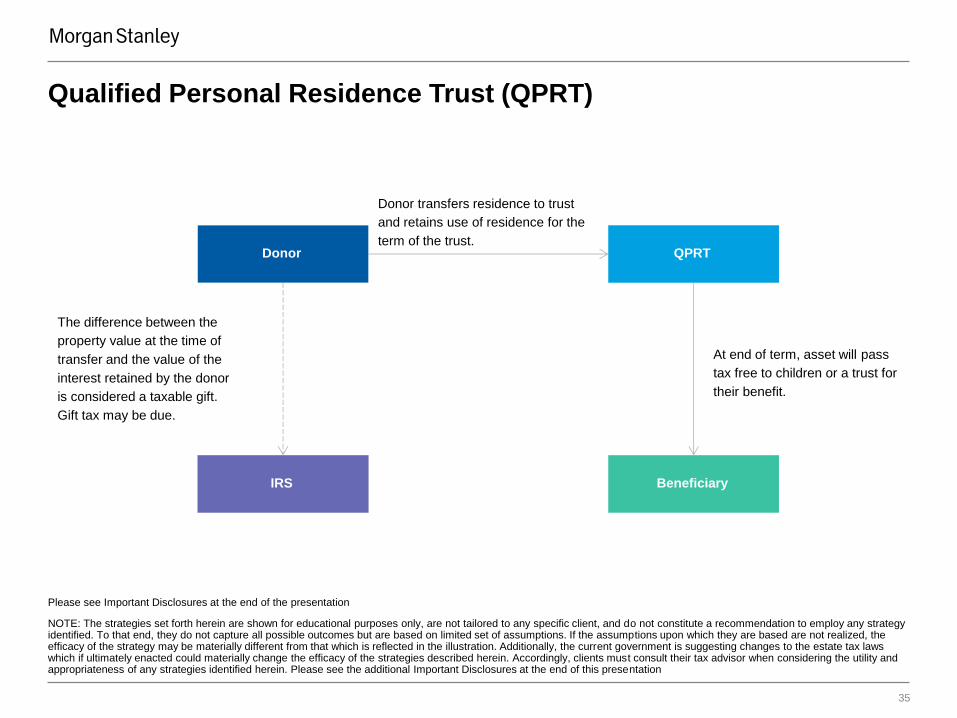

Donor QPRT

IRS Beneficiary

Donor transfers residence to trust

and retains use of residence for the

term of the trust.

The difference between the

property value at the time of

transfer and the value of the

interest retained by the donor

is considered a taxable gift.

Gift tax may be due.

At end of term, asset will pass

tax free to children or a trust for

their benefit.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

36

Source and Footnotes Guideline

Qualified Personal Residence Trust (QPRT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

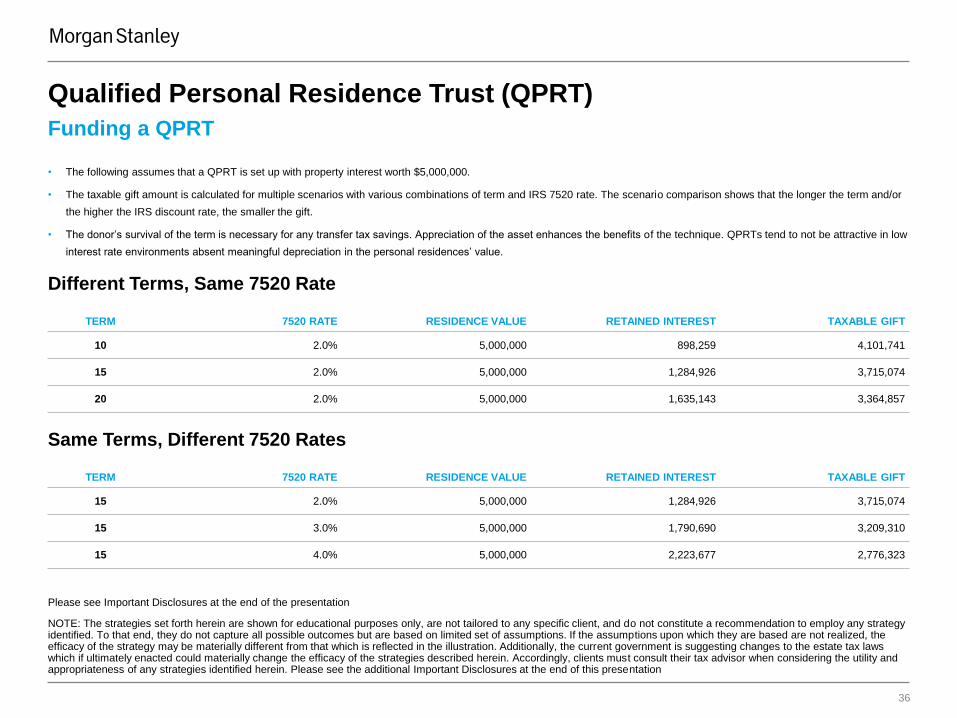

Funding a QPRT

• The following assumes that a QPRT is set up with property interest worth $5,000,000.

• The taxable gift amount is calculated for multiple scenarios with various combinations of term and IRS 7520 rate. The scenario comparison shows that the longer the term and/or

the higher the IRS discount rate, the smaller the gift.

• The donor’s survival of the term is necessary for any transfer tax savings. Appreciation of the asset enhances the benefits of the technique. QPRTs tend to not be attractive in low

interest rate environments absent meaningful depreciation in the personal residences’ value.

TERM 7520 RATE RESIDENCE VALUE RETAINED INTEREST TAXABLE GIFT

10 2.0% 5,000,000 898,259 4,101,741

15 2.0% 5,000,000 1,284,926 3,715,074

20 2.0% 5,000,000 1,635,143 3,364,857

Different Terms, Same 7520 Rate

TERM 7520 RATE RESIDENCE VALUE RETAINED INTEREST TAXABLE GIFT

15 2.0% 5,000,000 1,284,926 3,715,074

15 3.0% 5,000,000 1,790,690 3,209,310

15 4.0% 5,000,000 2,223,677 2,776,323

Same Terms, Different 7520 Rates

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

37

Source and Footnotes Guideline

Income Tax Planning

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation.

Basic and Advanced

Income and Estate Tax Planning

Basic Estate Planning Income Tax Planning Advanced Estate Planning

Gifting Early

Irrevocable

Life

Insurance

Trust

(ILIT)

Marital Credit

Shelter Trust

(CST)

Qualified

Personal

Residence

Trust

(QPRT)

Grantor

Retained

Annuity Trust

(GRAT)

Sale/Loan to

Irrevocable

Grantor

Trust

(IDGT)

Charitable

Tax

Deduction

Charitable

Remainder

Trust

(CRT)

Charitable

Lead Trust

(CLT)

Please see Important Disclosures at the end of the presentation

Charitable Lead Trust (CLT)

SECTION 7

Income and Estate Tax Planning

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

39

Source and Footnotes Guideline

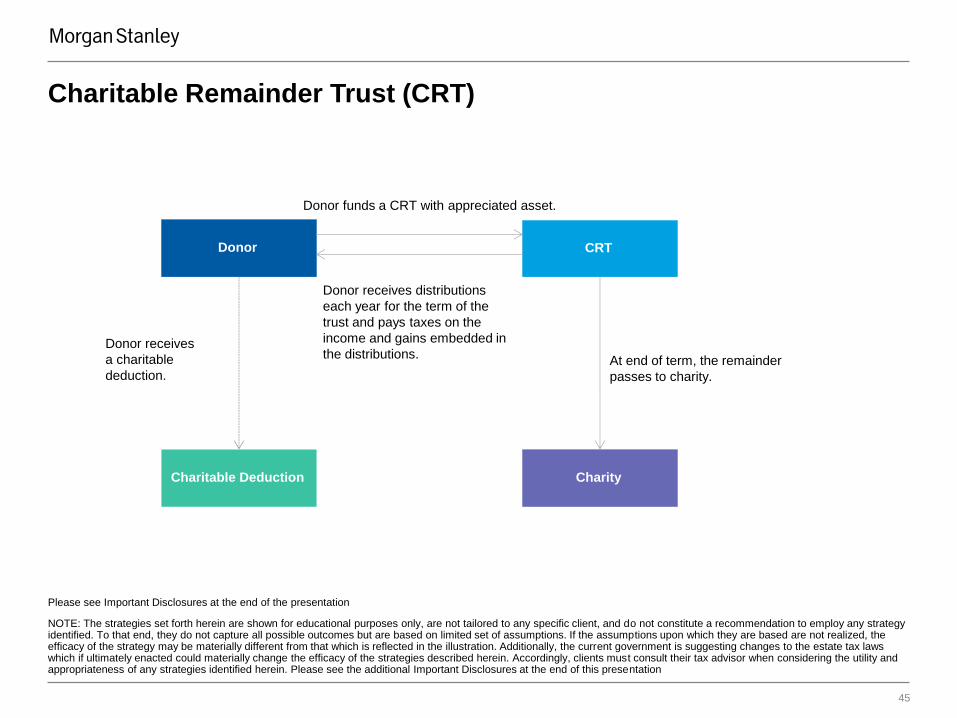

Charitable Lead Trust (CLT) (1), (2)

A A CLT allows a donor to transfer asset to a trust that makes annual payments to charity and remove future appreciation (if any) above

an IRS 7520 rate from the donor’s estate.

• A CLAT provides one or more charities with an annuity for a period of years. When the period ends, the remaining trust asset is paid to one or

more designated non-charitable beneficiaries.

‒ The value of the charity’s annuity interest is calculated using an IRS 7520 rate. The difference between the initial value of the asset

contributed to the trust and the present value of the charity’s annuity interest is a taxable gift to the remainder beneficiaries.

‒ The annuity can be structured to result in no taxable gift, i.e., the CLT is “zeroed out” so there is no tax cost to funding the CLT.

• A CLT may also be structured as a CLUT (unitrust), where the charity receives a set percentage of the fair market value of the trust’s asset, as

predetermined annually. These structures are not commonly used because any appreciation is shared with the charity, thus reducing the

remainder.

• If the total return (income and appreciation) exceeds the IRS 7520 rate used in valuing the periodic payments, the excess passes to the

remainder beneficiaries (typically, children and/or grandchildren) at the termination of the trust free of gift and estate taxes.

• The donor may or may not be treated as the owner and thus subject to tax on all of the trust’s income during the charitable term:

‒ Grantor Trust: where the donor is treated as the owner of the trust, he or she is entitled to a charitable income tax deduction equal to the

actuarial value of the charity’s interest in the trust. The benefit of that income tax deduction may be recaptured over the trust’s term because

the donor is taxed on all of the trust’s income.

‒ Non-Grantor Trust: where the donor is not treated as the owner of the trust, he or she does not receive a charitable income tax deduction

on the creation of the trust. The trust is a separate taxable entity which receives a charitable income deduction for the payments made to

charity each year.

• If structured carefully, the donor’s own private foundation can receive the periodic payments to charity.

• Certain prohibitions associated with private foundations may also apply to a CLT (regardless of the identity of the charitable beneficiary).

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

1. A CLT may also be structured as a unitrust (a CLUT), where the charity receives a set percentage of the fair market value of the trust’s asset, as predetermined annually. These structures are not commonly used because any appreciation is shared with the charity, thus reducing the remainder

2. Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

40

Source and Footnotes Guideline

Charitable Lead Trust (CLT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation.

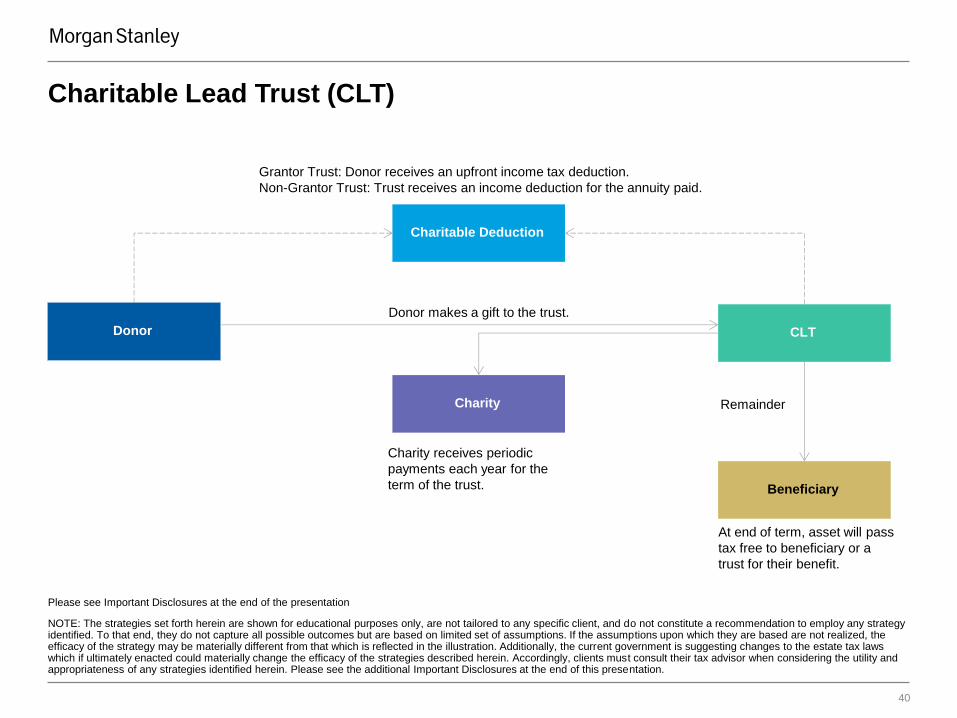

Donor CLT

Charitable Deduction

Beneficiary

Grantor Trust: Donor receives an upfront income tax deduction.

Non-Grantor Trust: Trust receives an income deduction for the annuity paid.

Donor makes a gift to the trust.

At end of term, asset will pass

tax free to beneficiary or a

trust for their benefit.

Remainder Charity

Charity receives periodic

payments each year for the

term of the trust.

Please see Important Disclosures at the end of the presentation

No content left

of this line

No content left

of this line

No content right

of this line

No content right

of this line

Place content below this line

Place content

below this line

41

Source and Footnotes Guideline

Charitable Lead Trust (CLT)

NOTE: The strategies set forth herein are shown for educational purposes only, are not tailored to any specific client, and do not constitute a recommendation to employ any strategy identified. To that end, they do not capture all possible outcomes but are based on limited set of assumptions. If the assumptions upon which they are based are not realized, the efficacy of the strategy may be materially different from that which is reflected in the illustration. Additionally, the current government is suggesting changes to the estate tax laws which if ultimately enacted could materially change the efficacy of the strategies described herein. Accordingly, clients must consult their tax advisor when considering the utility and appropriateness of any strategies identified herein. Please see the additional Important Disclosures at the end of this presentation

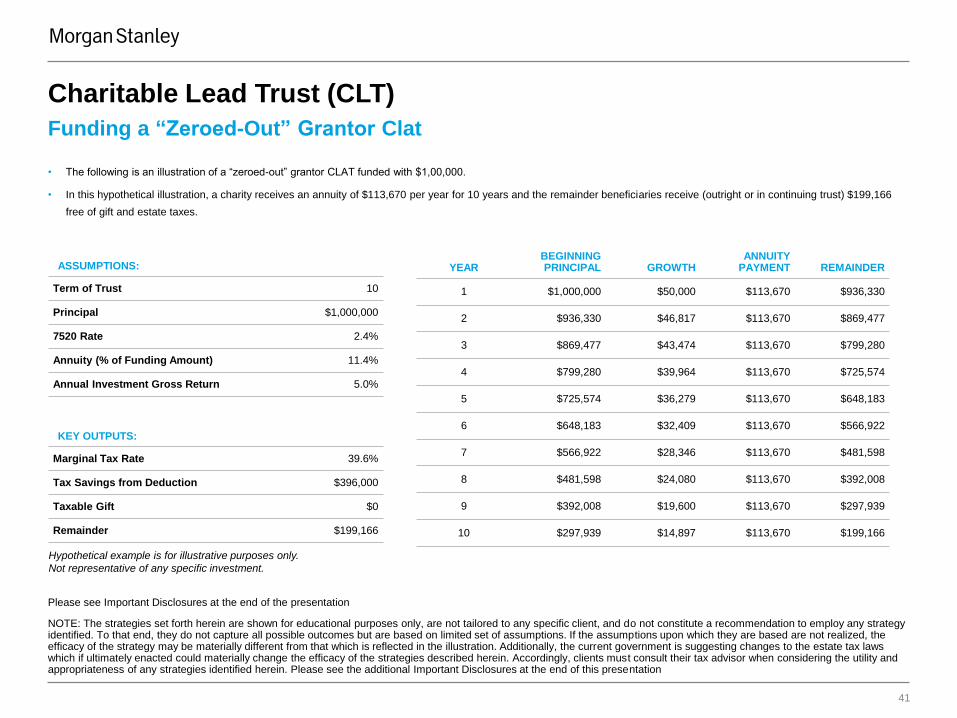

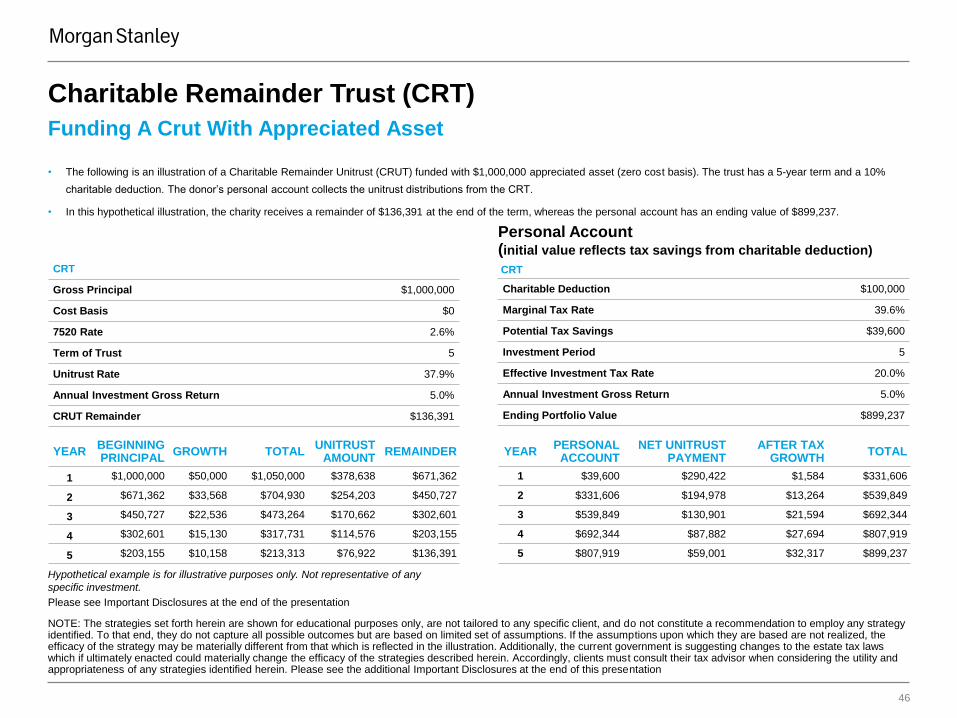

Funding a “Zeroed-Out” Grantor Clat

• The following is an illustration of a “zeroed-out” grantor CLAT funded with $1,00,000.

• In this hypothetical illustration, a charity receives an annuity of $113,670 per year for 10 years and the remainder beneficiaries receive (outright or in continuing trust) $199,166

free of gift and estate taxes.

ASSUMPTIONS:

Term of Trust 10

Principal $1,000,000

7520 Rate 2.4%

Annuity (% of Funding Amount) 11.4%

Annual Investment Gross Return 5.0%