Embed Size (px)

Citation preview

(Explanation)

Income Statement

Your AccountingCoach PRO membership includes lifetime access to all of our materials.Take a quick tour by visiting www.accountingcoach.com/quicktour.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 2

Introduction to Income Statement

The income statement is one of the major financial statements used by accountants and business owners. (The other major financial statements are the balance sheet, statement of cash flows, and the statement of stockholders’ equity.) The income statement is sometimes referred to as the profit and loss statement (P&L), statement of operations, or statement of income. We will use income statement and profit and loss statement throughout this explanation.

The income statement is important because it shows the profitability of a company during the time interval specified in its heading. The period of time that the statement covers is chosen by the business and will vary. For example, the heading may state:

“For the Three Months Ended December 31, 2012” (The period of October 1 through December 31, 2012.)

“The Four Weeks Ended December 27, 2012” (The period of November 29 through December 27, 2012.)

“The Fiscal Year Ended June 30, 2013” (The period of July 1, 2012 through June 30, 2013.)

Keep in mind that the income statement shows revenues, expenses, gains, and losses; it does not show cash receipts (money you receive) nor cash disbursements (money you pay out).

People pay attention to the profitability of a company for many reasons. For example, if a company was not able to operate profitably—the bottom line of the income statement indicates a net loss—a banker/lender/creditor may be hesitant to extend additional credit to the company. On the other hand, a company that has operated profitably—the bottom line of the income statement indicates a net income—demonstrated its ability to use borrowed and invested funds in a successful manner. A company’s ability to operate profitably is important to current lenders and investors, potential lenders and investors, company management, competitors, government agencies, labor unions, and others.

The format of the income statement or the profit and loss statement will vary according to the complexity of the business activities. However, most companies will have the following elements in their income statements:

A. Revenues and Gains 1. Revenues from primary activities 2. Revenues or income from secondary activities 3. Gains (e.g., gain on the sale of long-term assets, gain on lawsuits)

B. Expenses and Losses 1. Expenses involved in primary activities 2. Expenses from secondary activities 3. Losses (e.g., loss on the sale of long-term assets, loss on lawsuits)

If the net amount of revenues and gains minus expenses and losses is positive, the bottom line of the profit and loss statement is labeled as net income. If the net amount (or bottom line) is negative, there is a net loss.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 3

A. Revenues and Gains

1. Revenues from primary activities are often referred to as operating revenues. The primary activities of a retailer are purchasing merchandise and selling the merchandise. The primary activities of a manufacturer are producing the products and selling them. For retailers, manufacturers, wholesalers, and distributors the revenues resulting from their primary activities are referred to as sales revenues or sales. The primary activities of a company that provides services involve acquiring expertise and selling that expertise to clients. For companies providing services, the revenues from their primary services are referred to as service revenues or fees earned. (Some people use the word income interchangeably with revenues.)

It’s critical that you don’t confuse revenues with receipts. Under the accrual basis of accounting, service revenues and sales revenues are shown at the top of the income statement in the period they are earned or delivered, not in the period when the cash is collected. Put simply, revenues occur when money is earned, receipts occur when cash is received.

For example, if a retailer gives customers 30 days to pay, revenues occur (and are reported) when the merchandise is sold to the buyer, not when the cash is received 30 days later. If merchandise is sold in December, the sale is reported on the December income statement. When the retailer receives the check in January for the December sale, the retailer has a January receipt—not January revenues.

Similarly, if a consulting company asks clients to pay within 30 days of receiving their service, revenues occur (and are reported) when the service is performed (earned), not 30 days later when the consulting company receives the cash from the client.

If an attorney requires a client to prepay $1,000 before beginning to research the client’s case, the attorney has a receipt, but does not have revenues until some of the research is done.

If a company sells an item to a buyer who immediately pays for it with cash, the company has both a receipt and revenues for that day—it has a cash receipt because it received cash; it has sales revenues because it sold merchandise.

By knowing the difference between receipts and revenues, we make certain that revenues from a transaction are reported only once—when the primary activities have been completed (and not necessarily when the cash is collected).

Let’s reinforce the distinction between revenues and receipts with a few more examples. (Keep in mind that all of the examples below assume the accrual basis of accounting.)

• A company borrows $10,000 from its bank by signing a promissory note due in 90 days. The company will have a receipt of $10,000 at the time of the loan, but it does not have revenues because it did not earn the money from performing a service or from a sale of merchandise.

• If a company provided a $1,000 service on January 31 and gave the customer until March 10 to pay for the service, the company’s January income statement will show revenues of $1,000. When the money is actually received in March, the March income statement will not show revenues for this transaction. (In March the company will report a receipt of cash and a reduction/collection of an accounts receivable.)

• A company performs a $400 service on December 31 and receives the $400 on the very same day (December 31). This company will report $400 in revenues on December 31—not because the company had a cash receipt on December 31, but because the service was performed (earned) on that day.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 4

• On December 10, a new client asks your consulting company to provide a $2,500 service in January. You are uncertain as to whether or not this client is credit worthy, so to be on the safe side you ask for an immediate partial payment of $1,000 before you agree to schedule the work for January. Although your consulting company has a receipt of $1,000 in December, it does not have revenues in December. (In December your company will record a liability of $1,000.) Your consulting company will report the $1,000 of revenues when it performs $1,000 of services in January.

2. Revenues from secondary activities are often referred to as nonoperating revenues. These are the amounts a business earns outside of purchasing and selling goods and services. For example, when a retail business earns interest on some of its idle cash, or earns rent from some vacant space, these revenues result from an activity outside of buying and selling merchandise. As a result the revenues are reported on the income statement separate from its primary activity of sales or service revenues.

As is true with operating revenues, nonoperating revenues are reported on the profit and loss statement during the period when they are earned, not when the cash is collected.

3. Gains such as the gain on the sale of long-term assets, or lawsuits result from a transaction that is outside of the primary activities of most businesses. A gain is reported on the income statement as the net of two amounts: the proceeds received from the sale of a long-term asset minus the amount listed for that item on the company’s books (book value). A gain occurs when the proceeds are more than the book value.

Consider this example: Assume that a clothing retailer decides to dispose of the company’s car and sells it for $6,000. The $6,000 received for the car (the proceeds from the disposal of the car) will not be included with sales revenues since the account Sales is used only for the sale of merchandise. Since this retailer is not in the business of buying and selling cars, the sale of the car is outside of the retailer’s primary activities. Over the years, the cost of the car was being depreciated on the company’s accounting records and as a result, the money received for the car ($6,000) was greater than the net amount shown for the car on the accounting records ($3,500). This means that the company must report a gain equal to the amount of the difference—in this case, the gain is reported as $2,500. This gain should not be reported as sales revenues, nor should it be shown as part of the merchandiser’s primary activities. Instead, the gain will appear in a section on the income statement labeled as “nonoperating gains” or “other income”. The gain is reported in the period when the disposal occurred.

Here’s a Tip

Don't confuse revenues with receipts — Revenues (operating and nonoperating) occur when a sale is made or when they are earned. Revenues are frequently earned and reported on the income statement prior to receiving the cash.

Receipts occur when cash is received/collected.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 5

B. Expenses and Losses

1. Expenses involved in primary activities are expenses that are incurred in order to earn normal operating revenues. Under the accrual basis of accounting sales commissions expense should appear on the income statement in the same period that the related sales are reported, regardless of when the commission is actually paid. In the same way, the cost of goods sold is matched with the related sales on the income statement, regardless of when the supplier of the merchandise is paid.

Costs used up (or expiring) in the accounting period shown in the heading of the income statement are also considered to be expenses of that period. For example, the utilities used in a retail store in December should appear on the December income statement, even if the utility’s meters are not read until January 1 and the bill is paid on February 1.

The above examples reflect the matching principle and show that under the accrual basis of accounting, expenses on the income statement are likely to be reported at different times than the cash expenditures/disbursements.

It is common for expenses to occur before the company pays for them (e.g., wages earned by employees, employee bonuses and vacations, utilities, and sales commissions). However, some expenses occur after the company has paid for them. For example, let’s say a company buys a building on December 31, 2012 for $300,000 (excluding the cost of land). The building is assumed to have a useful life of 30 years. The company paid cash for the building on December 31, 2012 but it will record depreciation expense of $10,000 in each of the years 2013 through 2042.

Cash payments do not always mean that an expense has occurred. For example, a company might pay $20,000 to the bank to reduce its bank loan. This payment will reduce the company’s cash and its liability to the bank, but it is not an expense.

Some expenses are matched against sales on the income statement because there is a cause and effect linkage—the sale of the merchandise caused the cost of goods sold and the sales commission expense. Other expenses are not directly linked to sales and as a result they are matched to the accounting period when they are consumed or used—examples include utilities expense, office salaries expense, and depreciation expense. Some expenses such as advertising expense and research and development expense can neither be linked with sales nor a specific accounting period and as a result, they are reported as expenses as soon as they occur.

The income statements or profit and loss statements of merchandisers and manufacturers will use a separate line for the cost of goods sold. The other expenses involved in their primary activities will either be grouped together as operating expenses or subdivided into the categories “selling” and “administrative.”

2. Expenses from secondary activities are referred to as nonoperating expenses. For example, interest expense is a nonoperating expense because it involves the finance function of the business, rather than the primary activities of buying/producing and selling.

Here’s a Tip

Under the accrual basis of accounting, the cost of goods sold and expenses are matched to sales and/or the accounting period when they are used, not the period in which they are paid.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 6

3. Losses such as the loss from the sale of long-term assets, or the loss on lawsuits result from a transaction that is outside of a business’s primary activities. A loss is reported as the net of two amounts: the amount listed for the item on the company’s books (book value) minus the proceeds received from the sale. A loss occurs when the proceeds are less than the book value.

Let’s assume that a clothing retailer decides to dispose of the company’s car. The proceeds from the disposal are $2,800. This is less than the $3,500 amount shown in the company’s accounting records. Since this retailer is not in the business of buying and selling cars (the sale of the car is outside of the operating activities of buying and selling clothing), the money received for the car will not be included in sales revenues, and the loss experienced on the sale of the car ($700) will not be included in operating expenses. Instead, the $700 loss will appear in a section on the income statement labeled “nonoperating gains or losses” or “other income or losses”. The loss is reported in the time period when the disposal occurs.

Additional Considerations

Then vs. Now. The income statement covers a past period of time, and the past may or may not be indicative of the future. For example, a company supplying a high-demand fad item for the recent holiday season may have had a great year financially, but if it does not produce a similarly successful item for the next holiday season, it may experience a poor year financially.

Expenses Do Not Equal Economic Reality. Because of the cost principle and inflation, the expenses shown on the income statement reflect old costs. For example, assume that a company is operating a forty-year-old manufacturing plant that had a cost of $400,000. The depreciation expense for this plant may be zero on the current income statement because the plant was depreciated over 30 years. The cost of a new plant might be $4,000,000 today and the depreciation expense on the new plant might be $130,000 per year. The cost principle, however, prohibits showing the depreciation based on the cost of a new plant.

Using Estimates. An accountant is not allowed the luxury of waiting until things are known with certainty. In order to recognize revenues when they are earned, recognize expenses when they are incurred, or match expenses with revenues, accountants must often use estimates.

Here’s a Tip

The income statement or profit and loss statement shows revenues, expenses, gains, and losses.

The income statement does not show cash receipts and cash dis-bursements.

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 7

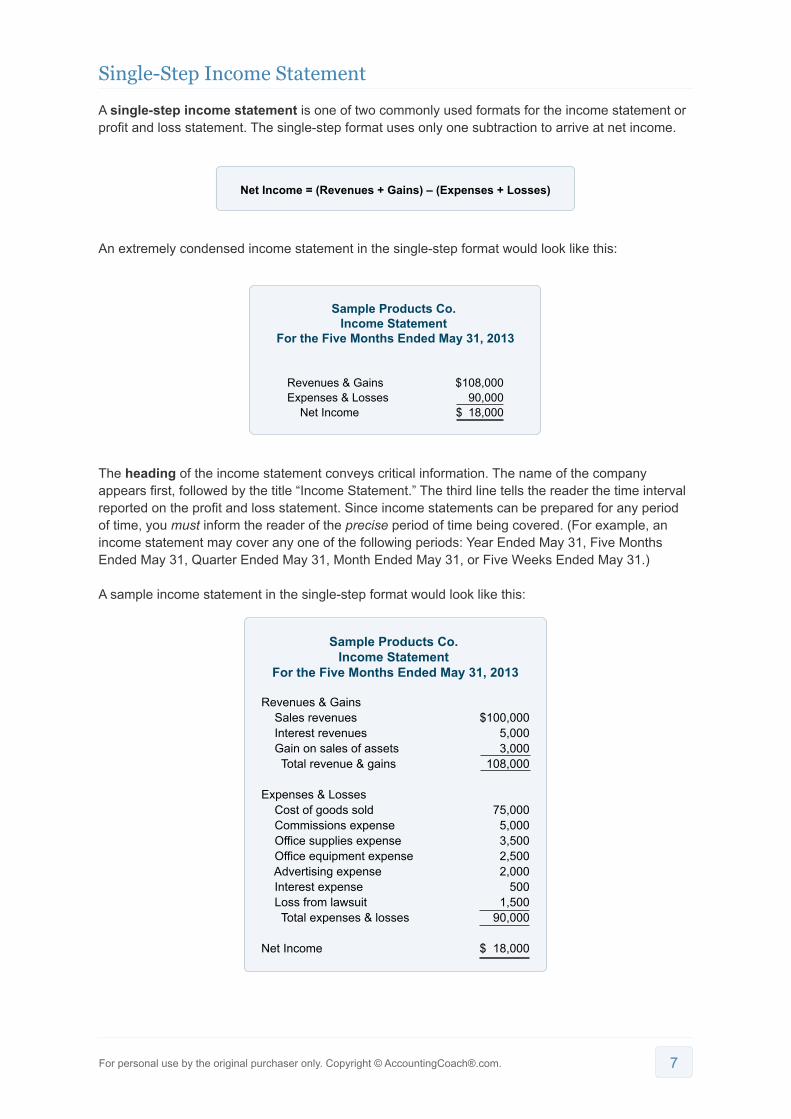

Single-Step Income Statement

A single-step income statement is one of two commonly used formats for the income statement or profit and loss statement. The single-step format uses only one subtraction to arrive at net income.

An extremely condensed income statement in the single-step format would look like this:

The heading of the income statement conveys critical information. The name of the company appears first, followed by the title “Income Statement.” The third line tells the reader the time interval reported on the profit and loss statement. Since income statements can be prepared for any period of time, you must inform the reader of the precise period of time being covered. (For example, an income statement may cover any one of the following periods: Year Ended May 31, Five Months Ended May 31, Quarter Ended May 31, Month Ended May 31, or Five Weeks Ended May 31.)

A sample income statement in the single-step format would look like this:

Net Income = (Revenues + Gains) – (Expenses + Losses)

Sample Products Co. Income Statement

For the Five Months Ended May 31, 2013

Revenues & GainsExpenses & Losses Net Income

$108,00090,000

$ 18,000

Sample Products Co. Income Statement

For the Five Months Ended May 31, 2013

Revenues & Gains Sales revenues Interest revenues Gain on sales of assets Total revenue & gains

Expenses & Losses Cost of goods sold Commissions expense Office supplies expense Office equipment expense Advertising expense Interest expense Loss from lawsuit Total expenses & losses

Net Income

$100,0005,0003,000

108,000

75,0005,0003,5002,5002,000

5001,500

90,000

$ 18,000

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 8

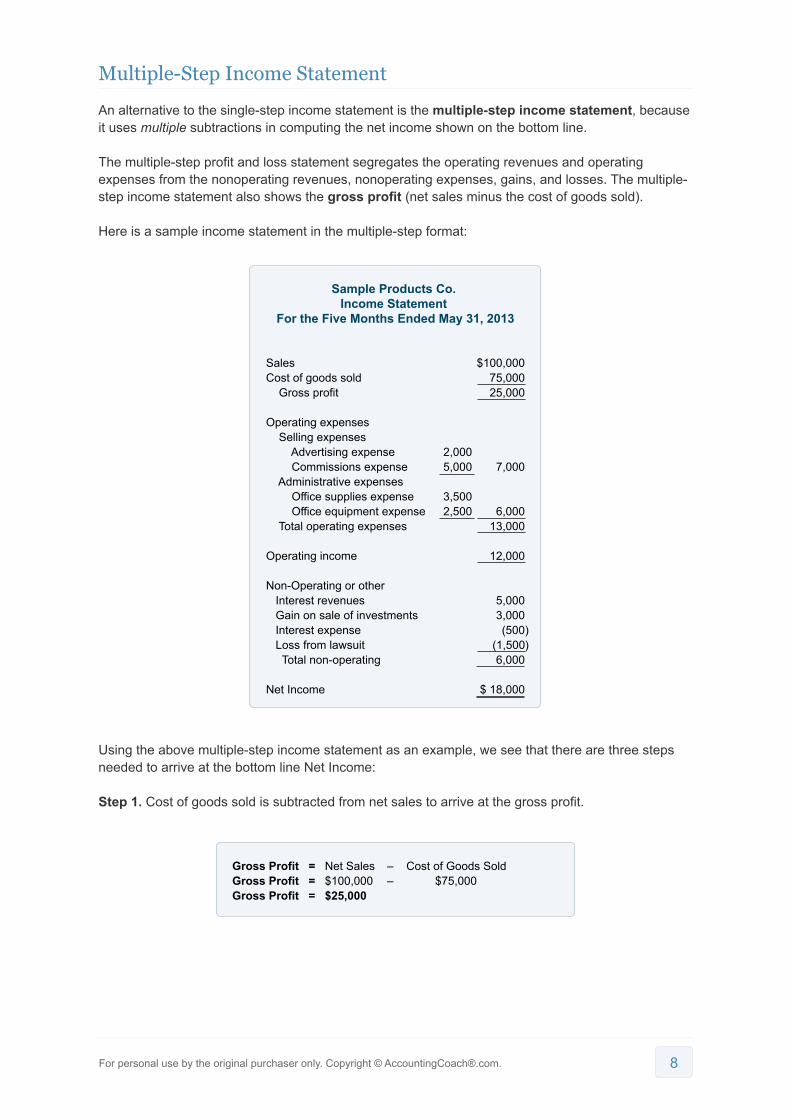

Multiple-Step Income Statement

An alternative to the single-step income statement is the multiple-step income statement, because it uses multiple subtractions in computing the net income shown on the bottom line.

The multiple-step profit and loss statement segregates the operating revenues and operating expenses from the nonoperating revenues, nonoperating expenses, gains, and losses. The multiple-step income statement also shows the gross profit (net sales minus the cost of goods sold).

Here is a sample income statement in the multiple-step format:

Using the above multiple-step income statement as an example, we see that there are three steps needed to arrive at the bottom line Net Income:

Step 1. Cost of goods sold is subtracted from net sales to arrive at the gross profit.

Sample Products Co. Income Statement

For the Five Months Ended May 31, 2013

SalesCost of goods sold Gross profit

Operating expenses Selling expenses Advertising expense Commissions expense Administrative expenses Office supplies expense Office equipment expense Total operating expenses

Operating income

Non-Operating or other Interest revenues Gain on sale of investments Interest expense Loss from lawsuit Total non-operating

Net Income

$100,00075,00025,000

7,000

6,00013,000

12,000

5,0003,000(500)

(1,500)6,000

$ 18,000

2,0005,000

3,5002,500

Gross Profit = Net Sales – Cost of Goods Sold Gross Profit = $100,000 – $75,000Gross Profit = $25,000

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 9

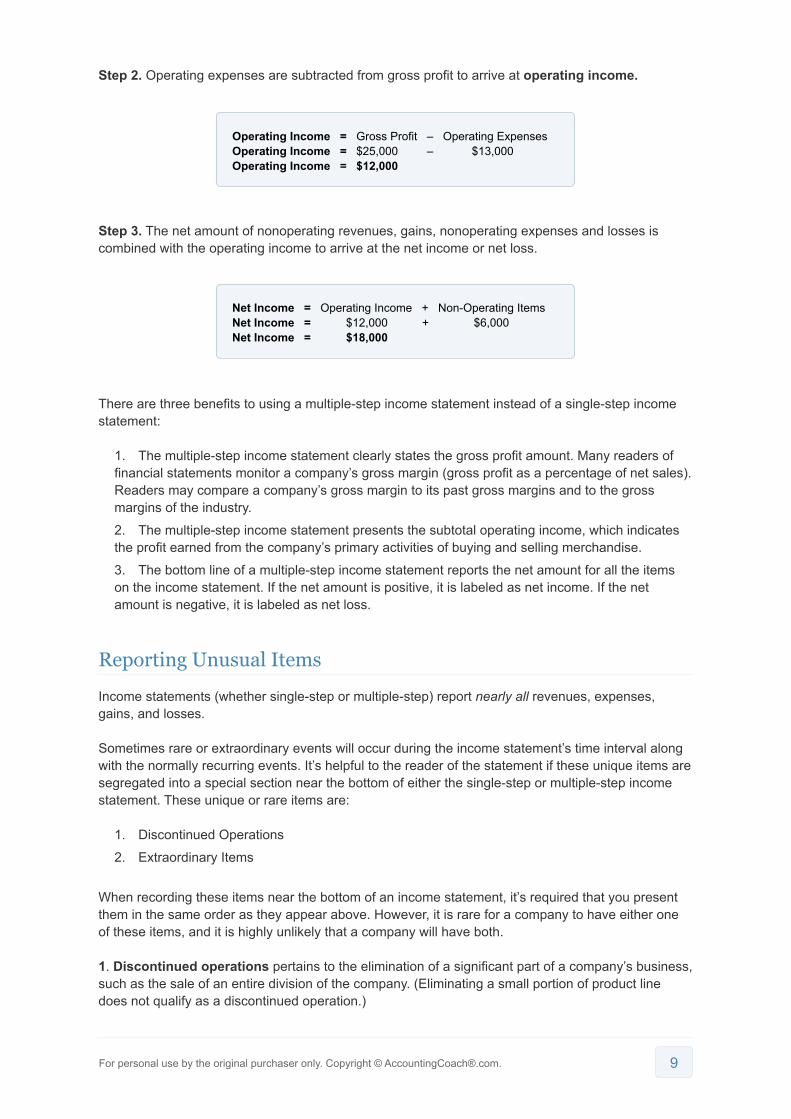

Step 2. Operating expenses are subtracted from gross profit to arrive at operating income.

Step 3. The net amount of nonoperating revenues, gains, nonoperating expenses and losses is combined with the operating income to arrive at the net income or net loss.

There are three benefits to using a multiple-step income statement instead of a single-step income statement:

1. The multiple-step income statement clearly states the gross profit amount. Many readers of financial statements monitor a company’s gross margin (gross profit as a percentage of net sales). Readers may compare a company’s gross margin to its past gross margins and to the gross margins of the industry.

2. The multiple-step income statement presents the subtotal operating income, which indicates the profit earned from the company’s primary activities of buying and selling merchandise.

3. The bottom line of a multiple-step income statement reports the net amount for all the items on the income statement. If the net amount is positive, it is labeled as net income. If the net amount is negative, it is labeled as net loss.

Reporting Unusual Items

Income statements (whether single-step or multiple-step) report nearly all revenues, expenses, gains, and losses.

Sometimes rare or extraordinary events will occur during the income statement’s time interval along with the normally recurring events. It’s helpful to the reader of the statement if these unique items are segregated into a special section near the bottom of either the single-step or multiple-step income statement. These unique or rare items are:

1. Discontinued Operations

2. Extraordinary Items

When recording these items near the bottom of an income statement, it’s required that you present them in the same order as they appear above. However, it is rare for a company to have either one of these items, and it is highly unlikely that a company will have both.

1. Discontinued operations pertains to the elimination of a significant part of a company’s business, such as the sale of an entire division of the company. (Eliminating a small portion of product line does not qualify as a discontinued operation.)

Operating Income = Gross Profit – Operating Expenses Operating Income = $25,000 – $13,000 Operating Income = $12,000

Net Income = Operating Income + Non-Operating Items Net Income = $12,000 + $6,000 Net Income = $18,000

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 10

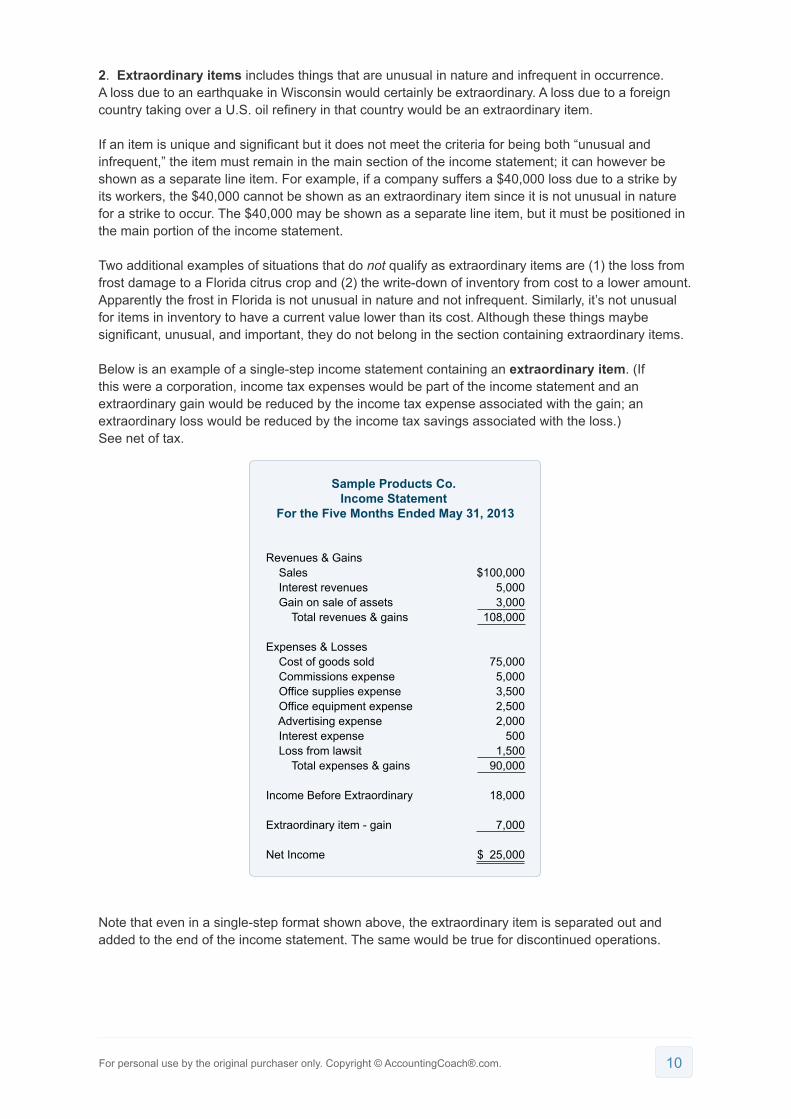

2. Extraordinary items includes things that are unusual in nature and infrequent in occurrence. A loss due to an earthquake in Wisconsin would certainly be extraordinary. A loss due to a foreign country taking over a U.S. oil refinery in that country would be an extraordinary item.

If an item is unique and significant but it does not meet the criteria for being both “unusual and infrequent,” the item must remain in the main section of the income statement; it can however be shown as a separate line item. For example, if a company suffers a $40,000 loss due to a strike by its workers, the $40,000 cannot be shown as an extraordinary item since it is not unusual in nature for a strike to occur. The $40,000 may be shown as a separate line item, but it must be positioned in the main portion of the income statement.

Two additional examples of situations that do not qualify as extraordinary items are (1) the loss from frost damage to a Florida citrus crop and (2) the write-down of inventory from cost to a lower amount. Apparently the frost in Florida is not unusual in nature and not infrequent. Similarly, it’s not unusual for items in inventory to have a current value lower than its cost. Although these things maybe significant, unusual, and important, they do not belong in the section containing extraordinary items.

Below is an example of a single-step income statement containing an extraordinary item. (If this were a corporation, income tax expenses would be part of the income statement and an extraordinary gain would be reduced by the income tax expense associated with the gain; an extraordinary loss would be reduced by the income tax savings associated with the loss.) See net of tax.

Note that even in a single-step format shown above, the extraordinary item is separated out and added to the end of the income statement. The same would be true for discontinued operations.

Sample Products Co. Income Statement

For the Five Months Ended May 31, 2013

Revenues & Gains Sales Interest revenues Gain on sale of assets Total revenues & gains

Expenses & Losses Cost of goods sold Commissions expense Office supplies expense Office equipment expense Advertising expense Interest expense Loss from lawsit Total expenses & gains

Income Before Extraordinary

Extraordinary item - gain

Net Income

$100,0005,0003,000

108,000

75,0005,0003,5002,5002,000

5001,500

90,000

18,000

7,000

$ 25,000

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 11

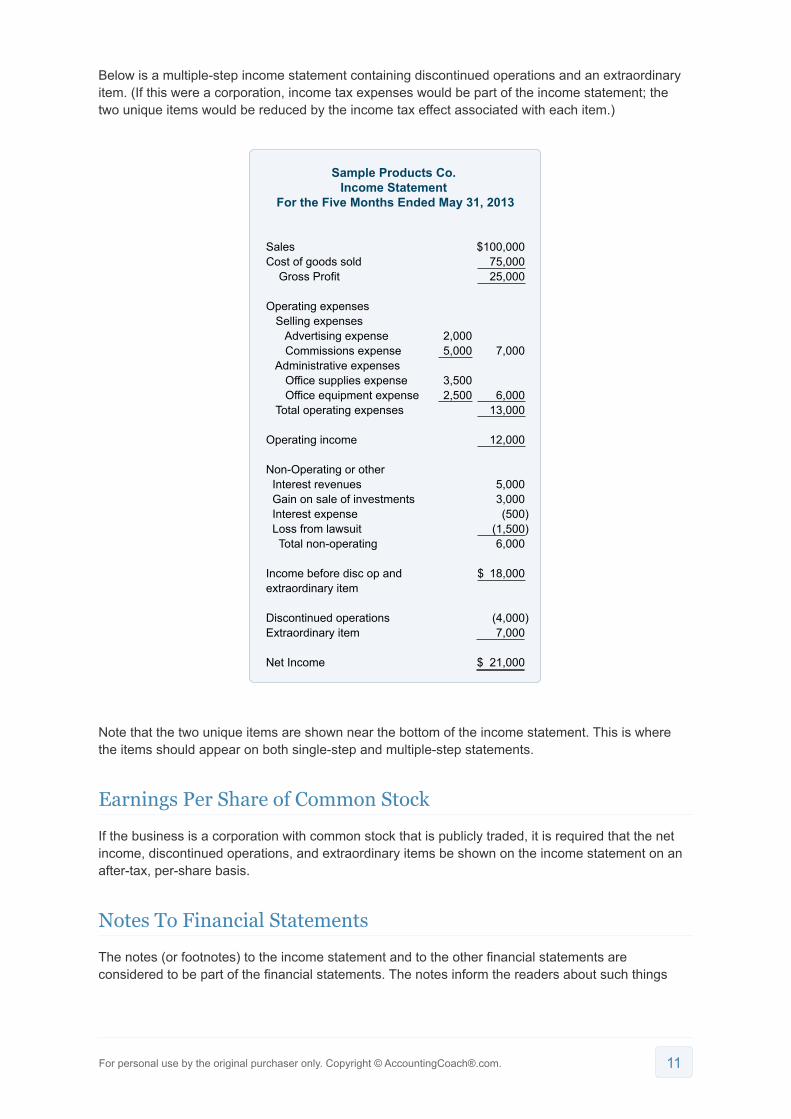

Below is a multiple-step income statement containing discontinued operations and an extraordinary item. (If this were a corporation, income tax expenses would be part of the income statement; the two unique items would be reduced by the income tax effect associated with each item.)

Note that the two unique items are shown near the bottom of the income statement. This is where the items should appear on both single-step and multiple-step statements.

Earnings Per Share of Common Stock

If the business is a corporation with common stock that is publicly traded, it is required that the net income, discontinued operations, and extraordinary items be shown on the income statement on an after-tax, per-share basis.

Notes To Financial Statements

The notes (or footnotes) to the income statement and to the other financial statements are considered to be part of the financial statements. The notes inform the readers about such things

Sample Products Co. Income Statement

For the Five Months Ended May 31, 2013

SalesCost of goods sold Gross Profit

Operating expenses Selling expenses Advertising expense Commissions expense Administrative expenses Office supplies expense Office equipment expense Total operating expenses

Operating income

Non-Operating or other Interest revenues Gain on sale of investments Interest expense Loss from lawsuit Total non-operating

Income before disc op andextraordinary item

Discontinued operationsExtraordinary item

Net Income

$100,00075,00025,000

7,000

6,00013,000

12,000

5,0003,000(500)

(1,500)6,000

$ 18,000

(4,000)7,000

$ 21,000

2,0005,000

3,5002,500

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 12

as significant accounting policies, commitments made by the company, and potential liabilities and potential losses. The notes contain information that is critical to properly understanding and analyzing a company’s financial statements.

It is common for the notes to the financial statements of large companies to be 10-20 pages in length. Go to the website for a company whose stock is publicly traded and locate its annual report. Look at the notes near the end of the annual report.

Other Income Statement Formats

The single-step and multiple-step income statement formats are the required formats when the statement is distributed to people and places outside of the company. The company’s management, however, might prefer other formats when the profit and loss statement remains inside the company.

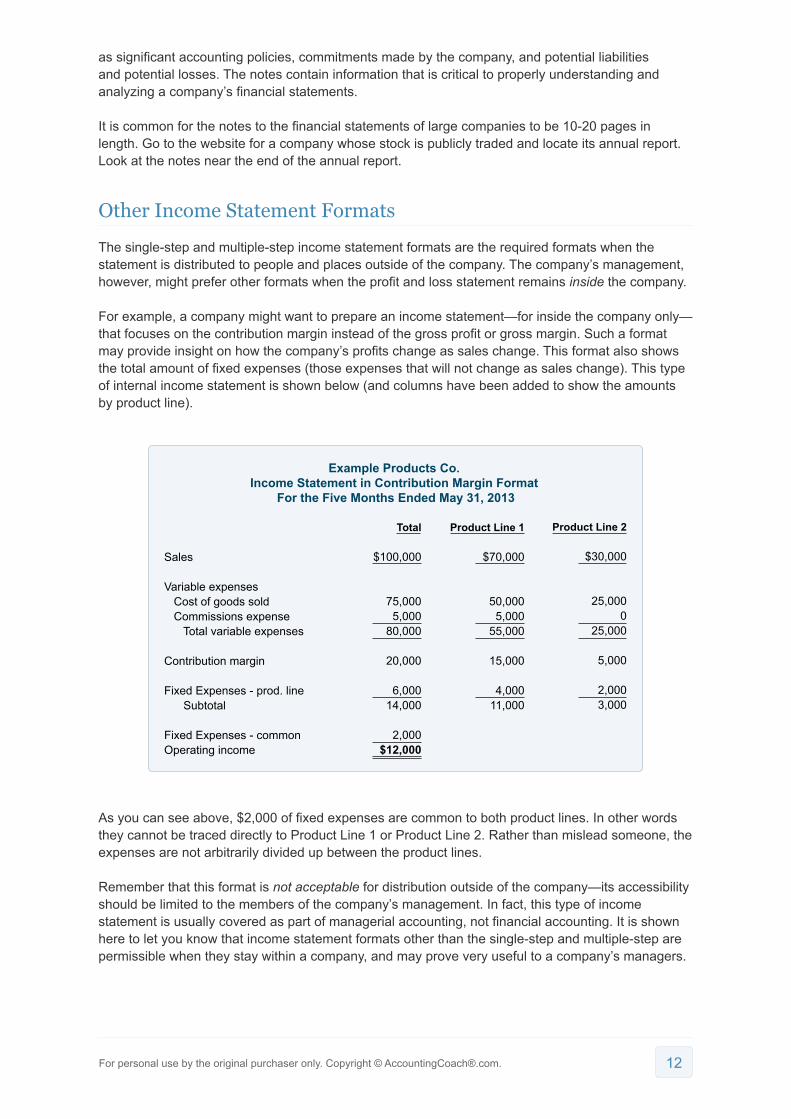

For example, a company might want to prepare an income statement—for inside the company only—that focuses on the contribution margin instead of the gross profit or gross margin. Such a format may provide insight on how the company’s profits change as sales change. This format also shows the total amount of fixed expenses (those expenses that will not change as sales change). This type of internal income statement is shown below (and columns have been added to show the amounts by product line).

As you can see above, $2,000 of fixed expenses are common to both product lines. In other words they cannot be traced directly to Product Line 1 or Product Line 2. Rather than mislead someone, the expenses are not arbitrarily divided up between the product lines.

Remember that this format is not acceptable for distribution outside of the company—its accessibility should be limited to the members of the company’s management. In fact, this type of income statement is usually covered as part of managerial accounting, not financial accounting. It is shown here to let you know that income statement formats other than the single-step and multiple-step are permissible when they stay within a company, and may prove very useful to a company’s managers.

Example Products Co. Income Statement in Contribution Margin Format

For the Five Months Ended May 31, 2013

Sales

Variable expenses Cost of goods sold Commissions expense Total variable expenses

Contribution margin

Fixed Expenses - prod. line Subtotal

Fixed Expenses - commonOperating income

Product Line 2

$30,000

25,0000

25,000

5,000

2,0003,000

Product Line 1

$70,000

50,0005,000

55,000

15,000

4,00011,000

Total

$100,000

75,0005,000

80,000

20,000

6,00014,000

2,000$12,000

For personal use by the original purchaser only. Copyright © AccountingCoach®.com. 13

Conclusion

Because the material covered here is considered an introduction to this topic, many complexities have been omitted. You should always consult with an accounting professional for assistance with your own specific circumstances.