Embed Size (px)

Citation preview

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 1/76

On The Job Training Report

OnOn

INCOME TAXINCOME TAX

ANDAND

WEALTH TAX PRACTICESWEALTH TAX PRACTICES

With special emphasis onWith special emphasis on

Income from Salaries (In Case of Income from Salaries (In Case of Individual )Individual )

Submitted in partial fulfillment of the requirement Submitted in partial fulfillment of the requirement

For the award of Degree of For the award of Degree of

Bachelor of Commerce (Vocational Tax Procedure &Bachelor of Commerce (Vocational Tax Procedure & Practices)Practices)

Session 2010-2011Session 2010-2011

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 2/76

Under supervision of Submitted by:-

Mrs. Luxmi Phutela NEETUSHARMAHead of Commerce Department CollegeRoll no.

Uni.Roll no:………

Uni. Roll No. (InWords)

C.M.K. National Post Graduate Girls College, SirsaC.M.K. National Post Graduate Girls College, Sirsa

( Affilated to Kurukshetra University, Kurukshetra )( Affilated to Kurukshetra University, Kurukshetra )

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 3/76

ACKNOWLEDGEMENTACKNOWLEDGEMENT

Before going ahead , I would like to express my deepBefore going ahead , I would like to express my deep sense of gratitude towards all those people who helped mesense of gratitude towards all those people who helped me in this endevour .in this endevour .

I deem it my privilege to say thanks toI deem it my privilege to say thanks to Dr.(Mrs.)VijayaDr.(Mrs.)Vijaya TomarTomar , principal , C.M.K.collage , Sirsa who provide me an, principal , C.M.K.collage , Sirsa who provide me an opportunity to under go this training .opportunity to under go this training .

I am also thankful toI am also thankful to Mrs. Luxmi Phutela Head of Mrs. Luxmi Phutela Head of commerce departmentcommerce department for her supervision andfor her supervision and guidance.guidance.

I am highly greatful toI am highly greatful to Mr. Pardeep UterjaMr. Pardeep Uterja C.A. forC.A. for granting me permission to undertake my job training undergranting me permission to undertake my job training under his able guidance .his able guidance .

I am also very thankful to Mrs. Rama Gupta for herI am also very thankful to Mrs. Rama Gupta for her cooperation.cooperation.

I am extremely grateful to my parents who always pray toI am extremely grateful to my parents who always pray to God for my success.God for my success.

(NEET(NEETU SHARMA)U SHARMA)

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 4/76

PREFACEPREFACE..

The succeeding pages contain a report on practical trainingunder gone by me in the Supervision of Mr. Pardeep Uterja ,

C.A. during the training my main aim was to gain as much as

knowledge & possible information in the stipulated time period

and to develop a thorough understanding to get familiar with

actual working conditions prevailing in the market. The report

also includes the details of the project work under taken by me

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 5/76

CONTENTSCONTENTS

Sr.No Name Of The Topic

1 .1 . Introduction About TaxIntroduction About Tax

2. Introduction About Income Tax2. Introduction About Income Tax

3. Five Head of Income Tax 3. Five Head of Income Tax

4. Advanced Payment of Tax4. Advanced Payment of Tax

5. Income tax & Authorities & their5. Income tax & Authorities & theirpowerspowers

6. Agriculture Income6. Agriculture Income

7. Introduction of Wealth Tax7. Introduction of Wealth Tax

8. Conclusion8. Conclusion

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 6/76

9. Bibliography & Suggestions9. Bibliography & Suggestions

INTRODUCTION OF INCOME TAX

INTRODUCTION

Income tax is a very important and direct tax . it is a mostIncome tax is a very important and direct tax . it is a most

significant source of revenue of the Government. The Govt.significant source of revenue of the Government. The Govt.

needs money to maintain law and order in the country safeguardneeds money to maintain law and order in the country safeguard

the security of the country from foreign powers and promote thethe security of the country from foreign powers and promote the

welfare of the people. Income tax, being a direct tax, is anwelfare of the people. Income tax, being a direct tax, is an

important tool to achieve balanced social-economic growth byimportant tool to achieve balanced social-economic growth by

providing concessions and incentives in income tax for variousproviding concessions and incentives in income tax for various

developments purpose.developments purpose.

Who is liable to pay income tax every person whose taxableWho is liable to pay income tax every person whose taxable

income for the previous financial year exceeds the minimumincome for the previous financial year exceeds the minimum

taxable limit is liable to pay the central govt. income tax duringtaxable limit is liable to pay the central govt. income tax during

the current financial year on the income of the previous financialthe current financial year on the income of the previous financial

year at the rate in force during the current financial year.year at the rate in force during the current financial year.

BRIEF HISTORY:-

•• In India, this tax was introduced for the first time in 1860,In India, this tax was introduced for the first time in 1860,

by Fir James Nulson.by Fir James Nulson.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 7/76

•• In 1886, a separate Income Tax act was passed.In 1886, a separate Income Tax act was passed.

•• In 1918 a new Income Tax act was passed and again it wasIn 1918 a new Income Tax act was passed and again it was

replaced by another new act which was passed in 1922.replaced by another new act which was passed in 1922.

•• It come into force with effect from 1It come into force with effect from 1stst April 1961.April 1961.

BASIS OF CHARGE OF INCOME TAX:-

•• Income tax is an annual tax on income.Income tax is an annual tax on income.

•• Income of previous year is taxable in the next followingIncome of previous year is taxable in the next following

assessment year.assessment year.

•• Tax rates are fixed by the annual finance Act. Tax rates are fixed by the annual finance Act.

•• Tax is charged on the total income of every person Tax is charged on the total income of every person

computed in accordance with precisions of this act.computed in accordance with precisions of this act.

•• Income tax is to be deducted at the source.Income tax is to be deducted at the source.

•• The total income is computed on the basis of the The total income is computed on the basis of the

residential status of the assessee and is classified into theresidential status of the assessee and is classified into the

following five heads :-following five heads :-

1.1. Income from SalaryIncome from Salary

2.2. Income from House PropertyIncome from House Property

3.3. Profit & Gain business or Professions.Profit & Gain business or Professions.

4.4. Capital GainsCapital Gains

5.5. Income from other Sources.Income from other Sources.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 8/76

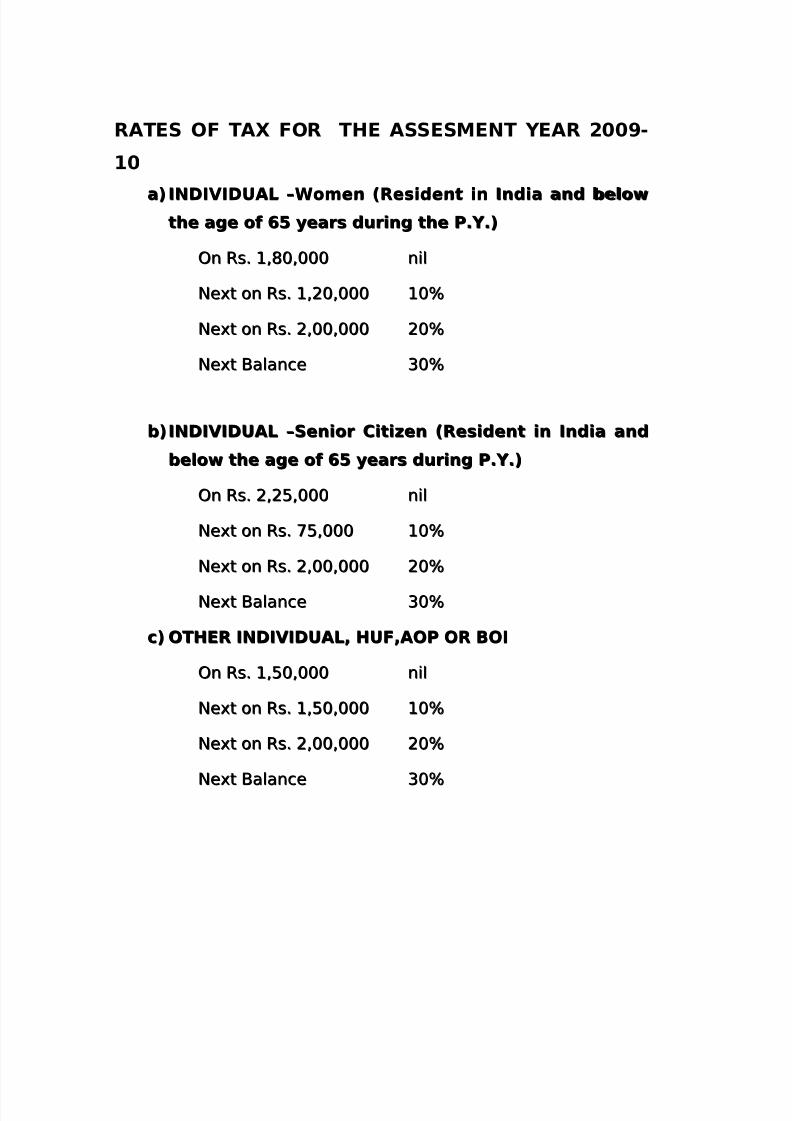

RATES OF TAX FOR THE ASSESMENT YEAR 2009-

10

a)a) INDIVIDUAL –Women (Resident in India and belowINDIVIDUAL –Women (Resident in India and below

the age of 65 years during the P.Y.)the age of 65 years during the P.Y.)

On Rs. 1,80,000On Rs. 1,80,000 nilnil

Next on Rs. 1,20,000Next on Rs. 1,20,000 10%10%

Next on Rs. 2,00,000Next on Rs. 2,00,000 20%20%

Next BalanceNext Balance 30%30%

b)b) INDIVIDUAL –Senior Citizen (Resident in India andINDIVIDUAL –Senior Citizen (Resident in India and

below the age of 65 years during P.Y.)below the age of 65 years during P.Y.)

On Rs. 2,25,000On Rs. 2,25,000 nilnil

Next on Rs. 75,000Next on Rs. 75,000 10%10%

Next on Rs. 2,00,000Next on Rs. 2,00,000 20%20%

Next BalanceNext Balance 30%30%

c)c) OTHER INDIVIDUAL, HUF,AOP OR BOIOTHER INDIVIDUAL, HUF,AOP OR BOI

On Rs. 1,50,000On Rs. 1,50,000 nilnil

Next on Rs. 1,50,000Next on Rs. 1,50,000 10%10%

Next on Rs. 2,00,000Next on Rs. 2,00,000 20%20%

Next BalanceNext Balance 30%30%

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 9/76

SURCHARGE –SURCHARGE –if total income exceeds Rs. 10 lakh @ 10%if total income exceeds Rs. 10 lakh @ 10%

education less on the amount of Income Tax and surchargeeducation less on the amount of Income Tax and surcharge

@2%.@2%.

Secondary and higher education less on the amount of Secondary and higher education less on the amount of

income tax and surcharge @ 1%.income tax and surcharge @ 1%.

Competition of Income and Tax Payable :-Competition of Income and Tax Payable :-

a)a) Total of all Head’s Income Total of all Head’s Income

b)b) On the total Income tax as per Slab is calculated.On the total Income tax as per Slab is calculated.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 10/76

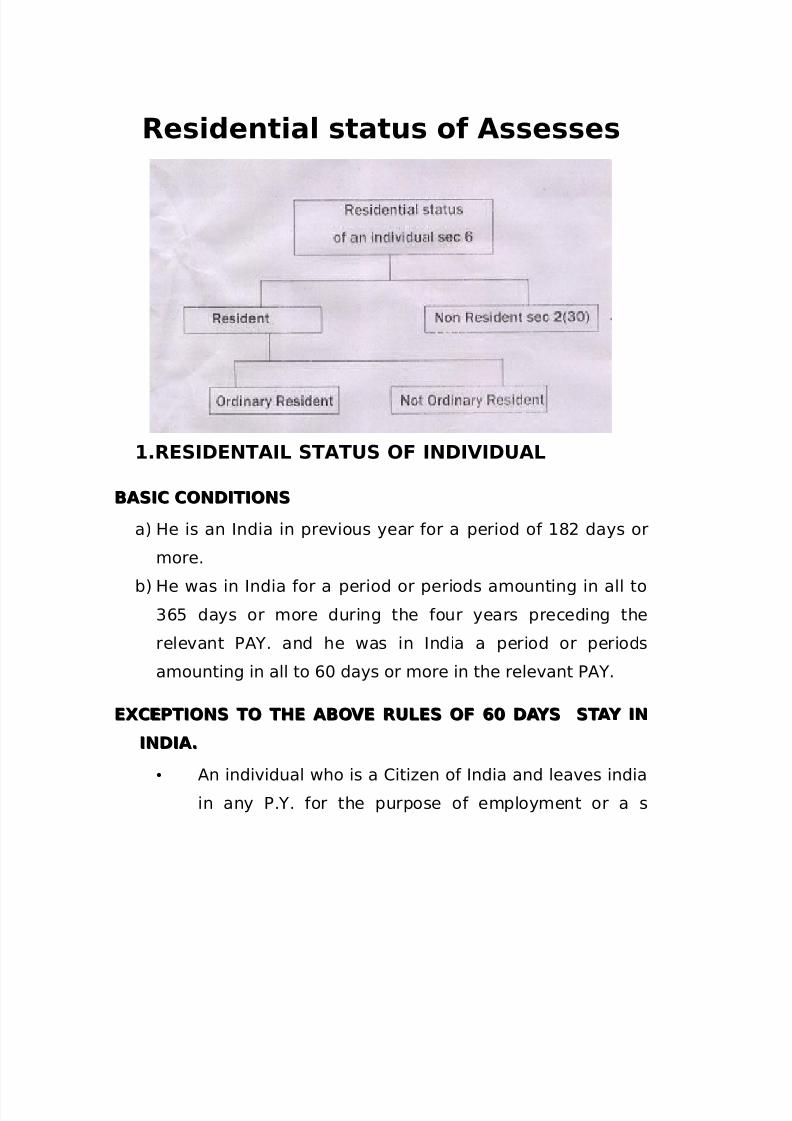

Residential status of Assesses

1.RESIDENTAIL STATUS OF INDIVIDUAL

BASIC CONDITIONSBASIC CONDITIONS

a) He is an India in previous year for a period of 182 days ormore.

b) He was in India for a period or periods amounting in all to

365 days or more during the four years preceding the

relevant PAY. and he was in India a period or periods

amounting in all to 60 days or more in the relevant PAY.

EXCEPTIONS TO THE ABOVE RULES OF 60 DAYS STAY INEXCEPTIONS TO THE ABOVE RULES OF 60 DAYS STAY IN

INDIA.INDIA.

• An individual who is a Citizen of India and leaves india

in any P.Y. for the purpose of employment or a s

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 11/76

member of the crew of an Indian ship then first

condition is applicable.

• If a person of Indian origin, who is living outside India,

visit in India during the P.Y. then first basic condition is

taken into consideration.

ADDITIONAL CONDITION :- (SEC.6(6) (A))ADDITIONAL CONDITION :- (SEC.6(6) (A))

(i) He has been resident in India at least 2 out of the 10 P.y.

proceeding the relevant P.Y.

(ii) At least 730 days in all during the 7 P.Y. preceding the

relevant previous year.

ORDINARILY RESIDENT:- (SEC.6(I)) :-ORDINARILY RESIDENT:- (SEC.6(I)) :- If a person satisfies atIf a person satisfies at

least one basic condition or both additional condition.least one basic condition or both additional condition.

NOT ORDINARILY RESIDENT:- (SEC.6(6)(a)) :-NOT ORDINARILY RESIDENT:- (SEC.6(6)(a)) :- If a personIf a person

does not satisfies any of condition.does not satisfies any of condition.

NON RESIDENT :-NON RESIDENT :- If a person does not satisfies any of If a person does not satisfies any of

condition.condition.

RESIDENTIAL STATUS OF HUF,FIRM OR AOP :- (SEC.6(2)RESIDENTIAL STATUS OF HUF,FIRM OR AOP :- (SEC.6(2)

RESIDENT :-RESIDENT :- Management & control of their affairs are wholly orManagement & control of their affairs are wholly or

partly situated in India.partly situated in India.

ii) Non Ordinarily Resident- Firm and A.O.P. cannot 'not

ordinarily resident.' Only H.U.F is 'not ordinarily resident' in

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 12/76

India, if, its Karta or manages (as an individual) is not ordinarily

resident in India.

III) Non Resident - H.U.F., firm or A.O.P. are not resident only

when the control & management of their affairs is situated

wholly outside India.

Company {Sec. 6(3)}

I Resident - (a) it is an India co.; or (b) control &

management of its affairs it situated wholly in India.

II Not Ordinarily Resident - A co. is never not ordinarilyResident.

III Non-Resident:- If a co does not satisfy both the aforesaid

condition of resident it is said to be a 'non-resident' company.

1. In earlier year but later

on remitted to India

during the P.Y.

No. No. No.

Every other person :- {Sec. 6(4)}

Every other person local authority, artificial juridical person,

e.g. idols) is said to be resident in India in any P.Y. in every case,

except where during that year the control & management of its

affairs it situated wholly outside India.If a person is resident in India in a P.Y. relevant to an A.Y. is

respect of any source of income, he shall be deemed to be

resident in the P.Y. relevant to the A.Y. in respect of each of his

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 13/76

other sources of income. Thus different residential status for

different sources of income for the same A.Y. is not possible.

{Sec. 6(5)}

Importance of determining Residential Status :- Since the

determination of total income depends upon the residential

status of an assesses, there is great importance of determining

the residential status for every previous year separately.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 14/76

First Head of Income

Salary

Sec. 15 to 17

Salaries (Sec.-15)

Any remuneration paid by an employer to his employee in

consideration of his services is called salary.

Some important point regarding salaries:-

1. Salaries of any kind.

2. Foreign salary and pension;

3. Relationship of employer and employee,

4. Receipts from person other than employees;

5. Pension;

6. Tax-free salary;

7. Salary of a member of parliament;

8. Salary of a partner;

9. Family pension:

10. Salary grade or scale of Pay;

11. Dearness Pay;

12. Surrender of Salary.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 15/76

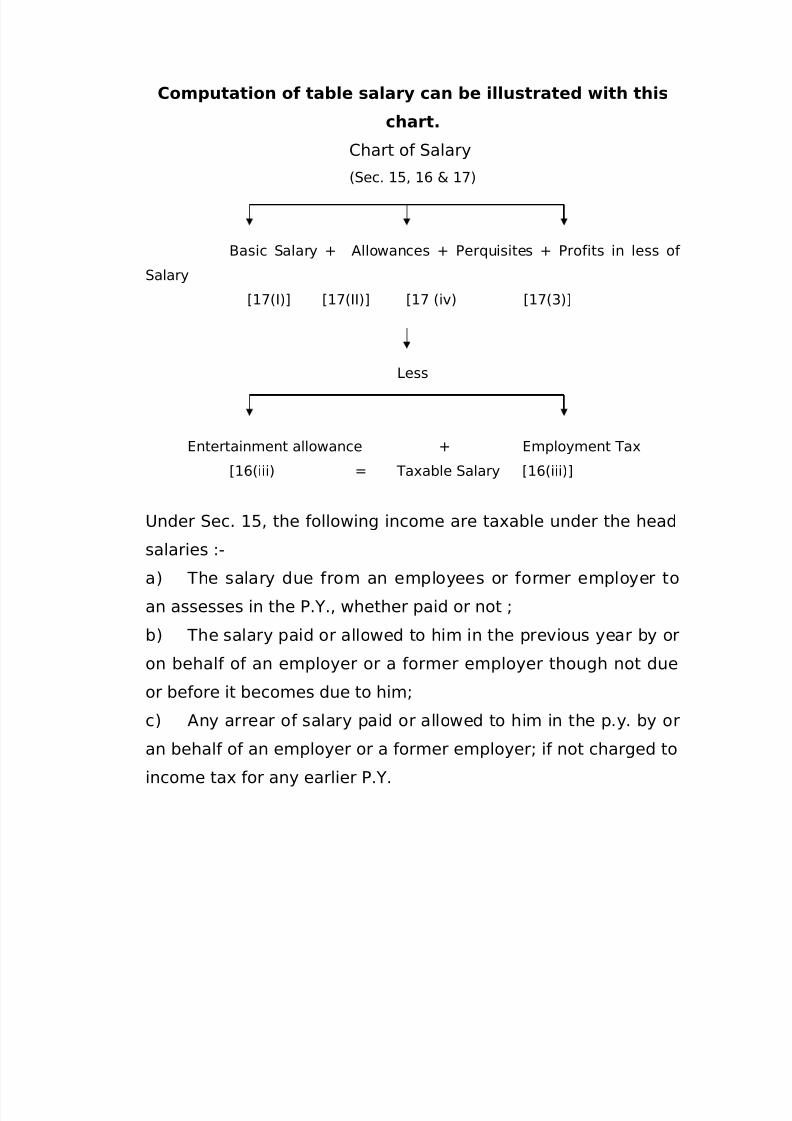

Computation of table salary can be illustrated with this

chart.

Chart of Salary

(Sec. 15, 16 & 17)

Basic Salary + Allowances + Perquisites + Profits in less of

Salary

[17(I)] [17(II)] [17 (iv) [17(3)]

Less

Entertainment allowance + Employment Tax

[16(iii) = Taxable Salary [16(iii)]

Under Sec. 15, the following income are taxable under the head

salaries :-

a) The salary due from an employees or former employer to

an assesses in the P.Y., whether paid or not ;

b) The salary paid or allowed to him in the previous year by or

on behalf of an employer or a former employer though not due

or before it becomes due to him;

c) Any arrear of salary paid or allowed to him in the p.y. by or

an behalf of an employer or a former employer; if not charged to

income tax for any earlier P.Y.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 16/76

[Sec. 9 (i) (ii)]

Explanation -

1. Any salary, bonus , commission or remuneration due to or

received by a partner of a firm from the firm shall not be

regarded as salary for the purpose of Se. 15.

2. If any salary paid in advance is include of in the total

income of any person for any previous year, it shall not be

includes again in the total income of the person when the salary

becomes due.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 17/76

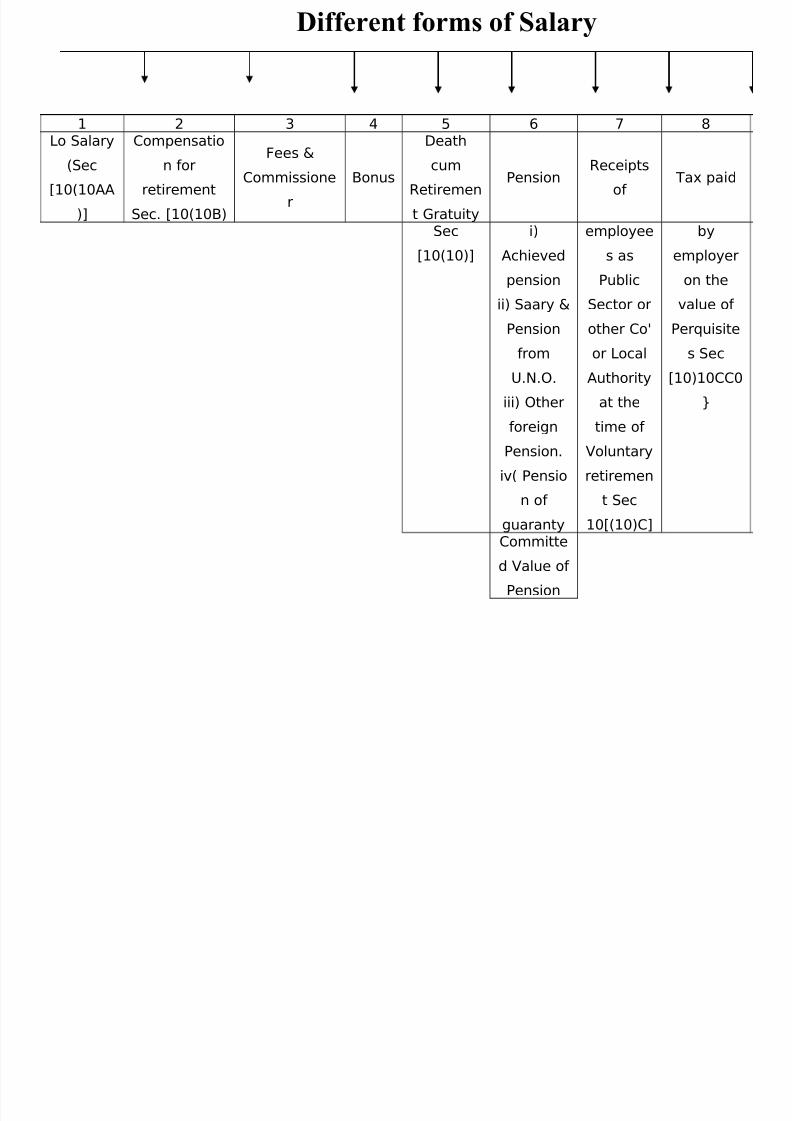

1 2 3 4 5 6 7 8Salary

(Sec

0(10AA

)]

Compensatio

n for

retirement

Sec. [10(10B)

Fees &

Commissione

r

Bonus

Death

cum

Retiremen

t Gratuity

Pension

Receipts

of Tax p

Sec

[10(10)]

i)

Achieved

pension

ii) Saary &

Pension

fromU.N.O.

iii) Other

foreign

Pension.

iv( Pensio

n of

guaranty

employee

s as

Public

Sector or

other Co'

or LocalAuthority

at the

time of

Voluntary

retiremen

t Sec

10[(10)C]

by

empl

on t

valu

Perqu

s S[10)10

}

Committe

d Value of

Pension

Different forms of Salary

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 18/76

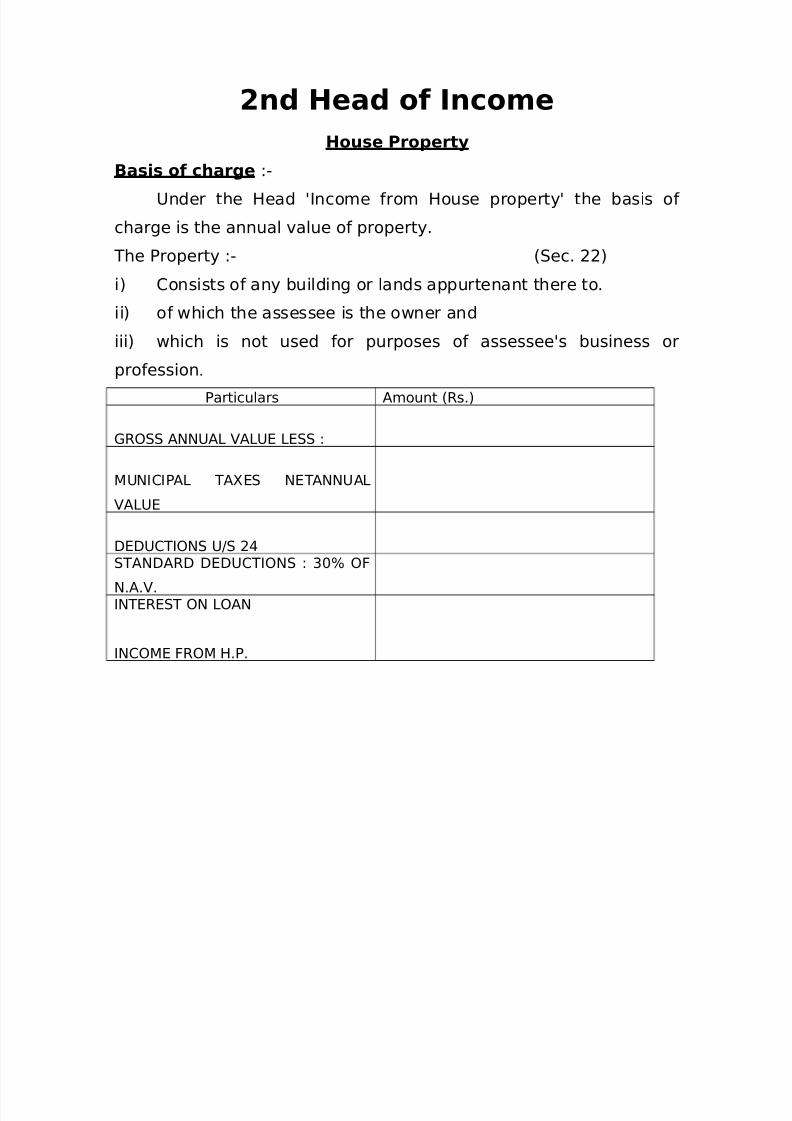

2nd Head of Income

House Property

Basis of charge :-Under the Head 'Income from House property' the basis of

charge is the annual value of property.

The Property :- (Sec. 22)

i) Consists of any building or lands appurtenant there to.

ii) of which the assessee is the owner and

iii) which is not used for purposes of assessee's business or

profession.

Particulars Amount (Rs.)

GROSS ANNUAL VALUE LESS :

MUNICIPAL TAXES NETANNUAL

VALUE

DEDUCTIONS U/S 24STANDARD DEDUCTIONS : 30% OF

N.A.V.INTEREST ON LOAN

INCOME FROM H.P.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 19/76

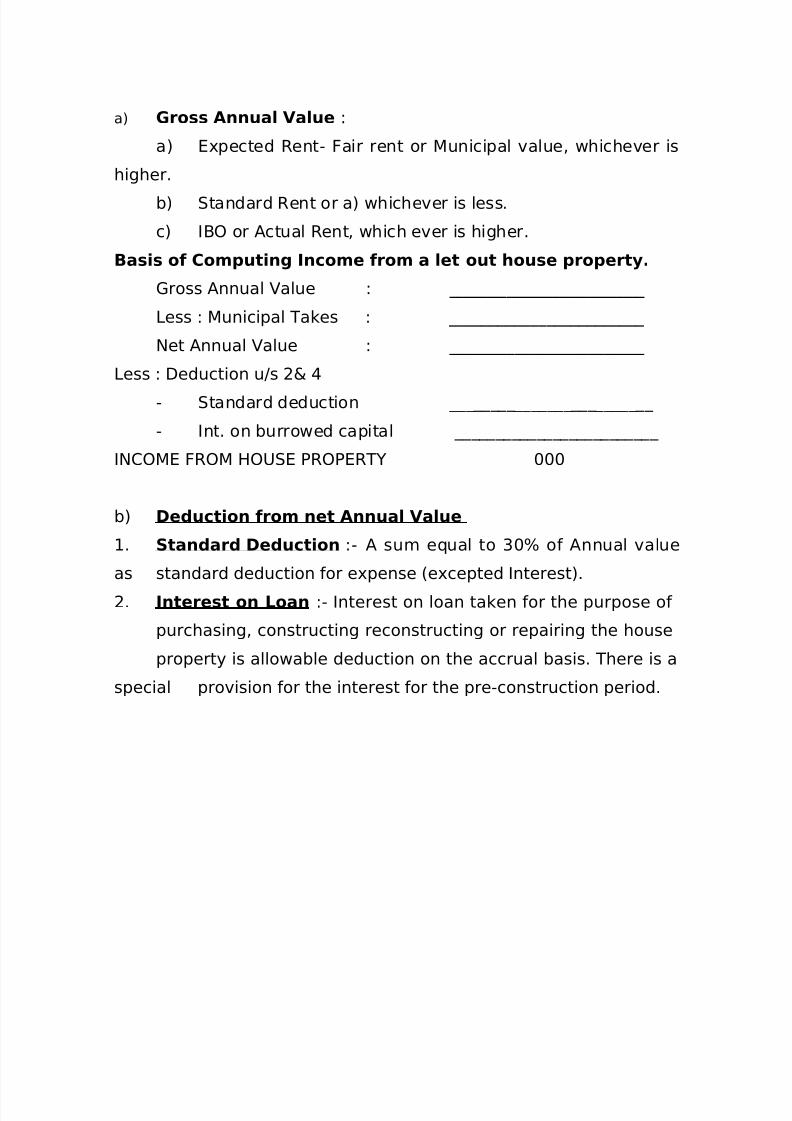

a) Gross Annual Value :

a) Expected Rent- Fair rent or Municipal value, whichever is

higher.b) Standard Rent or a) whichever is less.

c) IBO or Actual Rent, which ever is higher.

Basis of Computing Income from a let out house property.

Gross Annual Value : ________________________

Less : Municipal Takes : ________________________

Net Annual Value : ________________________

Less : Deduction u/s 2& 4

- Standard deduction _________________________

- Int. on burrowed capital _________________________

INCOME FROM HOUSE PROPERTY 000

b) Deduction from net Annual Value

1. Standard Deduction :- A sum equal to 30% of Annual value

as standard deduction for expense (excepted Interest).

2. Interest on Loan :- Interest on loan taken for the purpose of

purchasing, constructing reconstructing or repairing the house

property is allowable deduction on the accrual basis. There is a

special provision for the interest for the pre-construction period.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 20/76

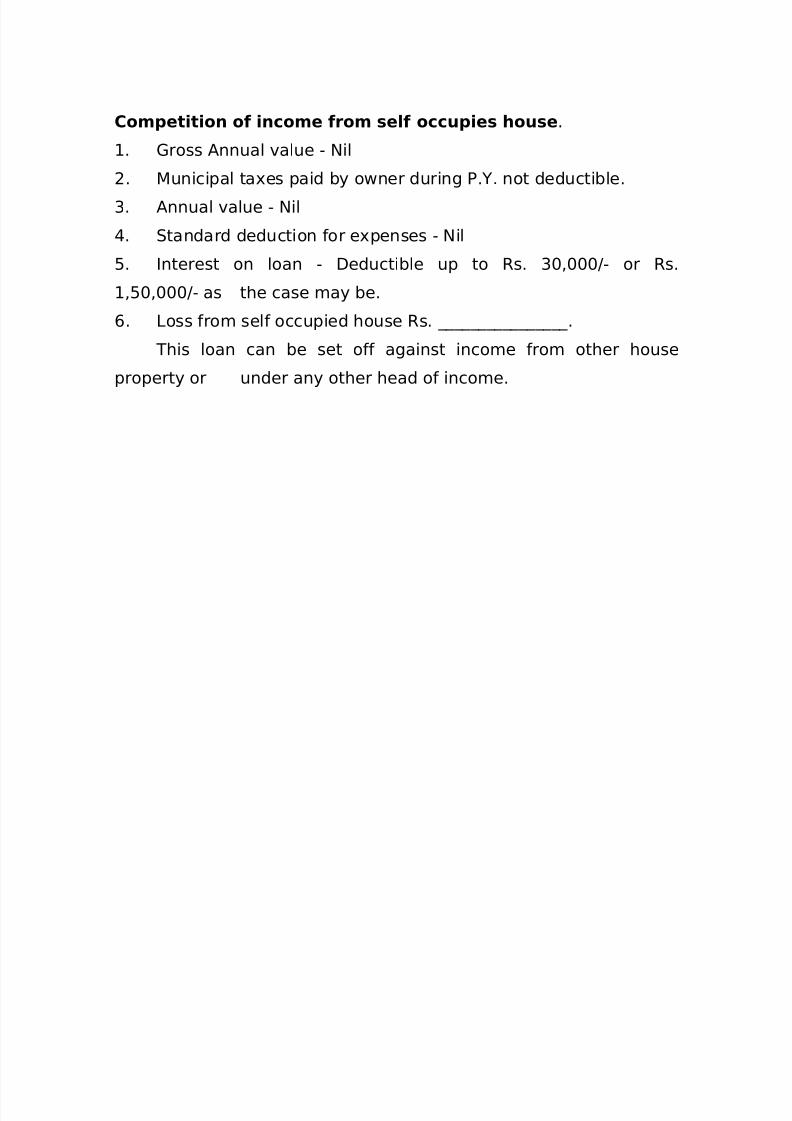

Competition of income from self occupies house.

1. Gross Annual value - Nil

2. Municipal taxes paid by owner during P.Y. not deductible.

3. Annual value - Nil

4. Standard deduction for expenses - Nil

5. Interest on loan - Deductible up to Rs. 30,000/- or Rs.

1,50,000/- as the case may be.

6. Loss from self occupied house Rs. ________________.

This loan can be set off against income from other houseproperty or under any other head of income.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 21/76

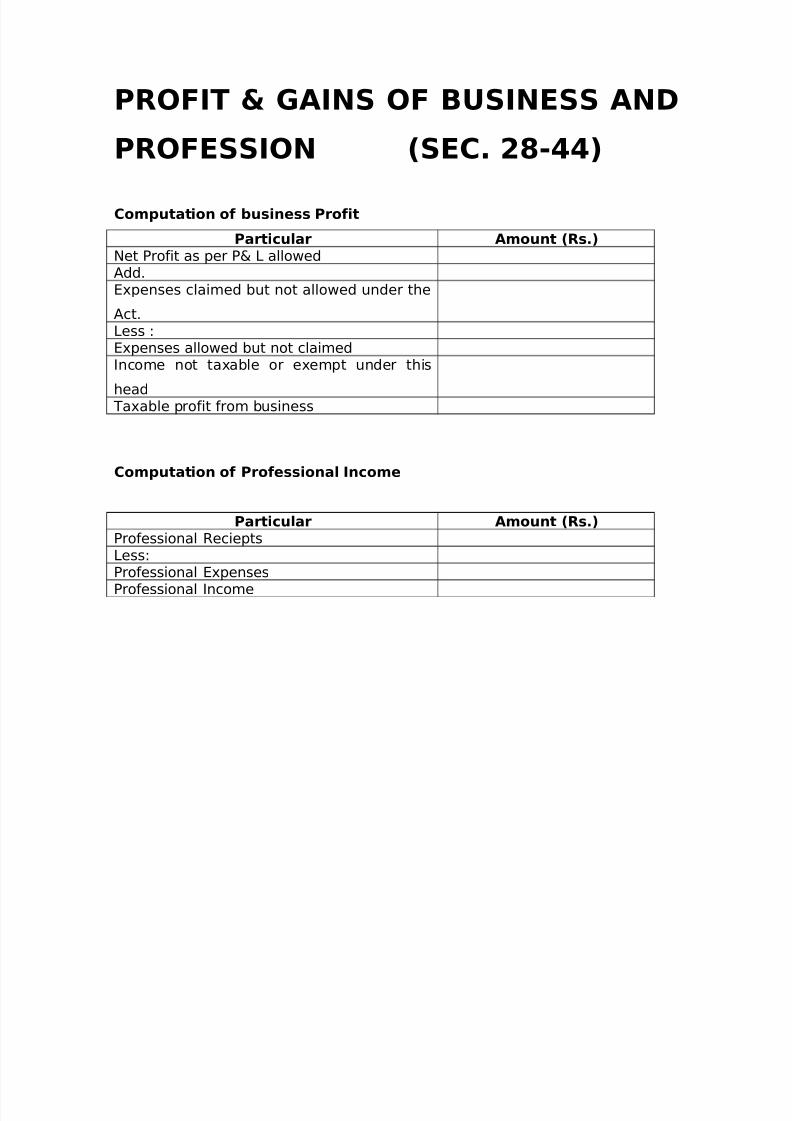

PROFIT & GAINS OF BUSINESS AND

PROFESSION (SEC. 28-44)

Computation of business Profit

Particular Amount (Rs.)Net Profit as per P& L allowedAdd.Expenses claimed but not allowed under the

Act.Less :

Expenses allowed but not claimedIncome not taxable or exempt under this

head Taxable profit from business

Computation of Professional Income

Particular Amount (Rs.)

Professional RecieptsLess:Professional ExpensesProfessional Income

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 22/76

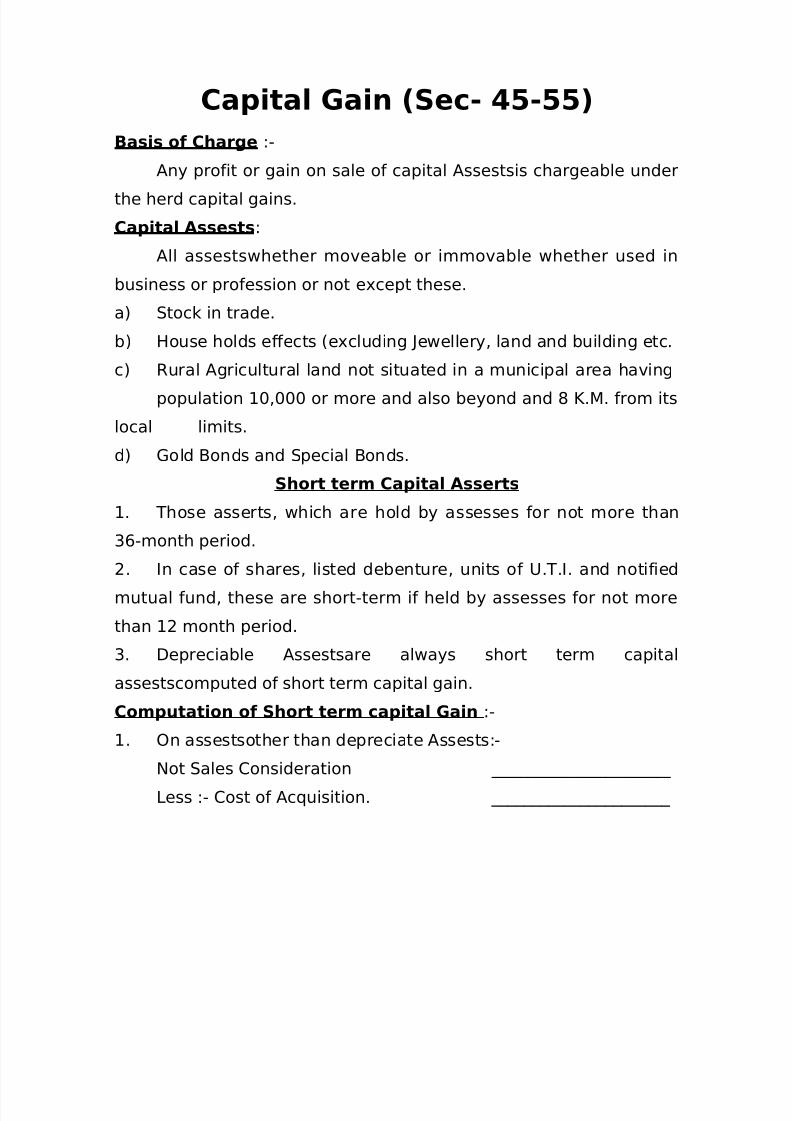

Capital Gain (Sec- 45-55)

Basis of Charge :-

Any profit or gain on sale of capital Assestsis chargeable underthe herd capital gains.

Capital Assests:

All assestswhether moveable or immovable whether used in

business or profession or not except these.

a) Stock in trade.

b) House holds effects (excluding Jewellery, land and building etc.

c) Rural Agricultural land not situated in a municipal area having

population 10,000 or more and also beyond and 8 K.M. from its

local limits.

d) Gold Bonds and Special Bonds.

Short term Capital Asserts

1. Those asserts, which are hold by assesses for not more than

36-month period.

2. In case of shares, listed debenture, units of U.T.I. and notified

mutual fund, these are short-term if held by assesses for not more

than 12 month period.

3. Depreciable Assestsare always short term capital

assestscomputed of short term capital gain.

Computation of Short term capital Gain :-

1. On assestsother than depreciate Assests:-

Not Sales Consideration ______________________

Less :- Cost of Acquisition. ______________________

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 23/76

Cost of improvement

______________________

Short term capital Gain ______________________

2. On Depreciable Assests:-

a) If some part of the block is sold and net sales consideration

exceeds the written down value than surplus is short-term capital

gain.

b) If whole block is sold and net sales consideration is less than

the written down value than the difference of sales consideration

and written down value will be called short-term capital loss.Computation of Long-Term Capital Gain :-

Net Sales consideration ___________________________

Less :- Induced cost of Acquisition ___________________________

Indexed cot of improvement ___________________________

Long Term Capital Gain ___________________________

Indexed Cost :- Original cost x index No. of year of sales.

Index No. of the year of Purchase.

Cost of Acquisition :-

Cost of acquisition of an assert is the value for which it is

acquired by the assesses. It means that whatever cost is incurred for

getting an assestsplus all expenses incurred to acquire it is cost of

acquisition.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 24/76

Computation of long-term Capital Gain :-

(INDEXATION)

For the purpose of computing gain arising from the transfer of long

term capital assert then.

a) "Indexed cost of acquisition" shall be taken instead of "Cost of

Acquisition."

b) "Index cost of improvement" shall be taken instead of "cost of

improvement".

NOTE 1: "Indexed cost of Acquisition" Means - cost of Acquisition x

cost inflation index for the year in which assert is transferred - cost

inflation index for the first year in which assert was held by the

assesses r for the year beginning on 01-04-1981, whichever is lates.

NOTE 2: "Indexed cost of improvement" means - cost of

improvement x cost inflation index for the year in which assert is

transferred - cost inflation index for the first year in which the

improvement to the assert took place.

NOTE 3: Indexation is not allowed in case of BOND & DEBENTURESexcept capital indexed Bonds.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 25/76

Income from others sources (u/s(56-

59)

General Income - [Sec 56)1)]- General income includes those

general incomes which do not fall under the first four i.e. salaries,

House property, business and capital gains) head.

Specific Income : [Sec. 56(2)]- It includes, divided, casual incomes,

income from plant and machinery belonging to assessee on hire andis not chargeable under PGBP interest on securities etc.

- Dividends

- income from winning from lotteries, cross word puzzles, races

and other games of any sort.

- Any sum received by the assessee from his employee as

contribution to any provident fund.

- Income from machinery, plant or furniture belonging to the

assessee and let out on hire, if the income is not charged to income

tax under the head profit or gains from business or professions etc.

Beside the above, there are some other incomes, which are

also chargeable under this head, which are as follows:-

- Any fees or commission received by an employee from a

person other than his employer.

- Any annuity received under a will

- Income of royalty.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 26/76

- Director's fees.

- Remuneration received by a teacher or a lawyer.

- Rent of land.

- Agriculture income not situated in India.

- Income from leasehold property.

- Family pension.

- Causal income.

- Salary of member of parliament.

- Director's commission for giving guarantees to bank.

- Insurance commission.- Interest received on securities from co-operative society.

- Income from markets and fisheries.

- Remuneration received for writing articles in journals.

- Receipts by the cricketers selected to play for India.

Some other important points relating to income from other

sources

1- Winnings from lotteries, crossword puzzles, card games,

gambling or betting, races including horse races.

2- Fund of Employees.

3- Hire of machinery, Plant etc.

4- Hire of Machinery, Plant and building not separately.

5- Interest on Kisan Vikas Patra.

6- Interest on National Savings certificate VIII

7- Interest on Securities.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 27/76

Clubbing of Income (Sec 60 to 65)

There is a growing tendency on the part of the tax-payer either not

to disclose certain assestsor investment in the records maintained

by than or to disclose it at a figure lower than its cost. An assessee

therefore, attempts to shift his income to others so included is called

demand income.

Income of other person is included in assessee total income in the

following cases:

- Income of spouse. [ 64 (i) (II) ]

- Income of daughter in law .[64 (i) (vi)

- Transfer of assests to other person or AOP for the benefit of his

son's wife.(64(i) (vii) ]

- Income from the assests transferred to a persons or AOP for

the benefit of his son's wife (64(i) (viii)]

- Income from business [64 (i) (ii)]

- Income of a minor child [64(1A)

- Cross transfer [64]

- Benami transactions.

- Revocable transfer to assests [61]

- Transfer of income without transfer of assests.

Deemed Incomes -- Cash credit (68)

- Unrecorded & unexplained income (69)

- Unrecorded & unexplained money (69B)

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 28/76

- Amount of investment not fully disclosed in books of accounts

(69B)

- Unexplained expenditure (69 C)

- Hundi borrowals and repayments (69D)

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 29/76

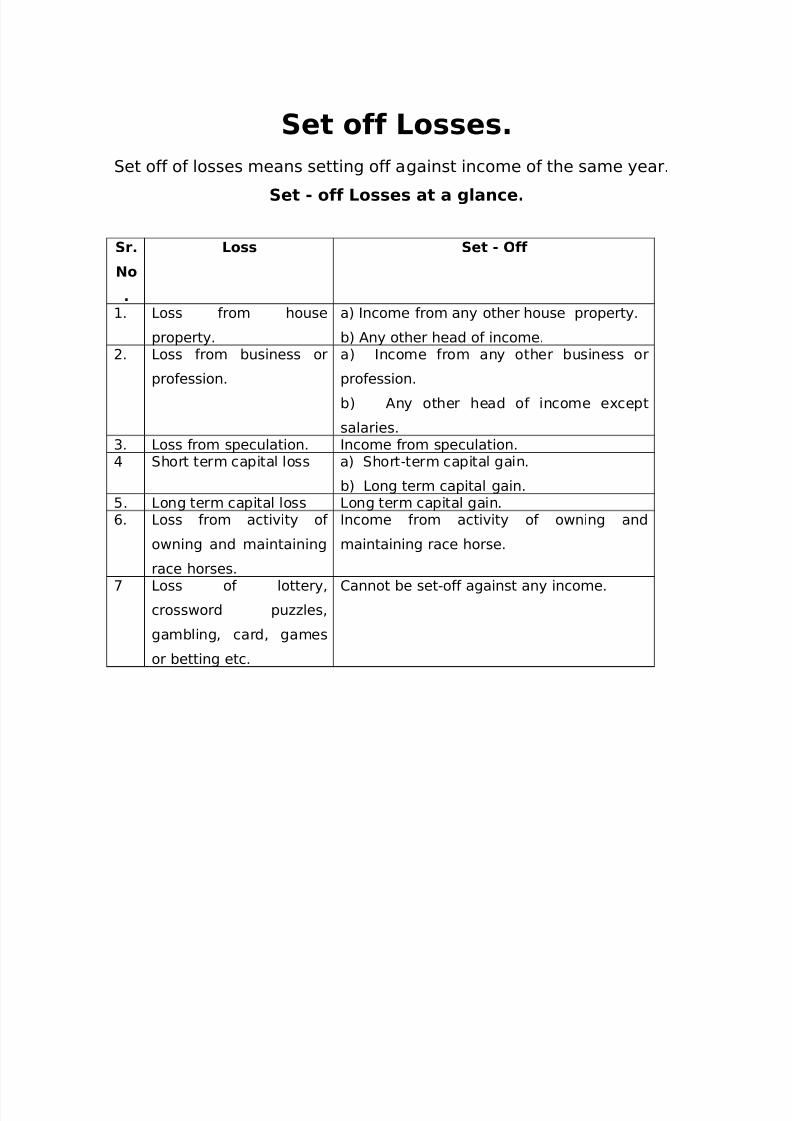

Set off Losses.

Set off of losses means setting off against income of the same year.

Set - off Losses at a glance.

Sr.

No

.

Loss Set - Off

1. Loss from house

property.

a) Income from any other house property.

b) Any other head of income.

2. Loss from business orprofession.

a) Income from any other business orprofession.

b) Any other head of income except

salaries.3. Loss from speculation. Income from speculation.4 Short term capital loss a) Short-term capital gain.

b) Long term capital gain.5. Long term capital loss Long term capital gain.6. Loss from activity of

owning and maintaining

race horses.

Income from activity of owning and

maintaining race horse.

7 Loss of lottery,

crossword puzzles,

gambling, card, games

or betting etc.

Cannot be set-off against any income.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 30/76

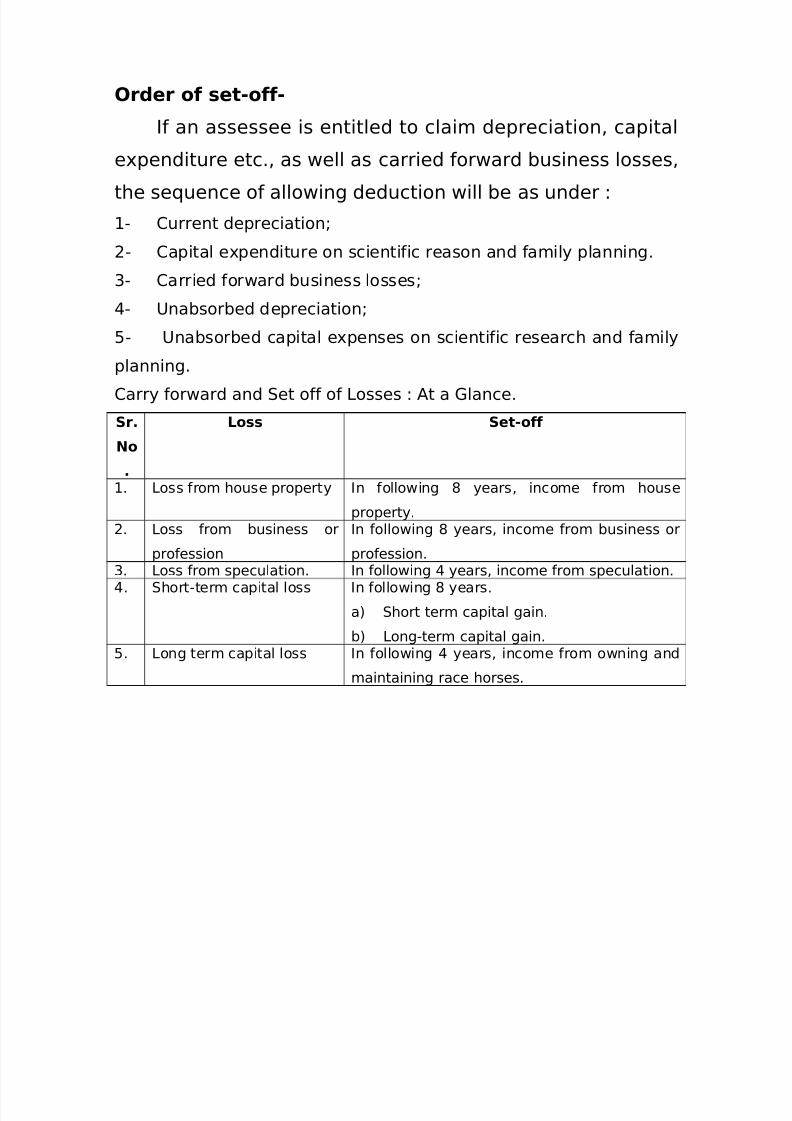

Order of set-off-

If an assessee is entitled to claim depreciation, capital

expenditure etc., as well as carried forward business losses,

the sequence of allowing deduction will be as under :

1- Current depreciation;

2- Capital expenditure on scientific reason and family planning.

3- Carried forward business losses;

4- Unabsorbed depreciation;

5- Unabsorbed capital expenses on scientific research and family

planning.

Carry forward and Set off of Losses : At a Glance.

Sr.

No

.

Loss Set-off

1. Loss from house property In following 8 years, income from house

property.

2. Loss from business orprofession

In following 8 years, income from business orprofession.

3. Loss from speculation. In following 4 years, income from speculation.4. Short-term capital loss In following 8 years.

a) Short term capital gain.

b) Long-term capital gain.5. Long term capital loss In following 4 years, income from owning and

maintaining race horses.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 31/76

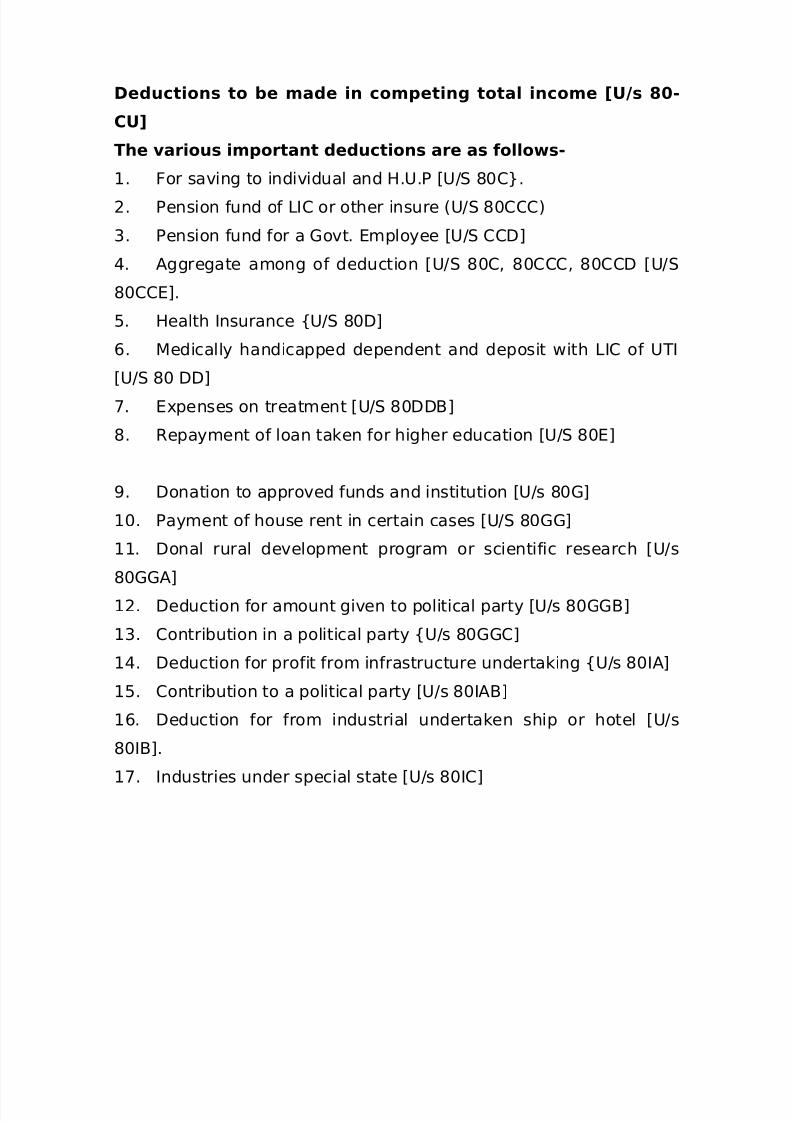

Deductions to be made in competing total income [U/s 80-

CU]

The various important deductions are as follows-

1. For saving to individual and H.U.P [U/S 80C}.

2. Pension fund of LIC or other insure (U/S 80CCC)

3. Pension fund for a Govt. Employee [U/S CCD]

4. Aggregate among of deduction [U/S 80C, 80CCC, 80CCD [U/S

80CCE].

5. Health Insurance {U/S 80D]

6. Medically handicapped dependent and deposit with LIC of UTI[U/S 80 DD]

7. Expenses on treatment [U/S 80DDB]

8. Repayment of loan taken for higher education [U/S 80E]

9. Donation to approved funds and institution [U/s 80G]

10. Payment of house rent in certain cases [U/S 80GG]

11. Donal rural development program or scientific research [U/s

80GGA]

12. Deduction for amount given to political party [U/s 80GGB]

13. Contribution in a political party {U/s 80GGC]

14. Deduction for profit from infrastructure undertaking {U/s 80IA]

15. Contribution to a political party [U/s 80IAB]

16. Deduction for from industrial undertaken ship or hotel [U/s

80IB].

17. Industries under special state [U/s 80IC]

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 32/76

18. Profit and gains of bio waster [U/s 80JJA]

19. Any industrial undertaking which creates new jobs [u/s 80JJAA]

20. Income off shore banking unit [U/s 80LA]

21. Income on co-operative societies [U/s80P]

22. Royalty of books [U/s 80QQB]

23. Income from patent [U/s 80RRB]

24. Medical handicapped or monthly reiterated assesses [U/s 80U]

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 33/76

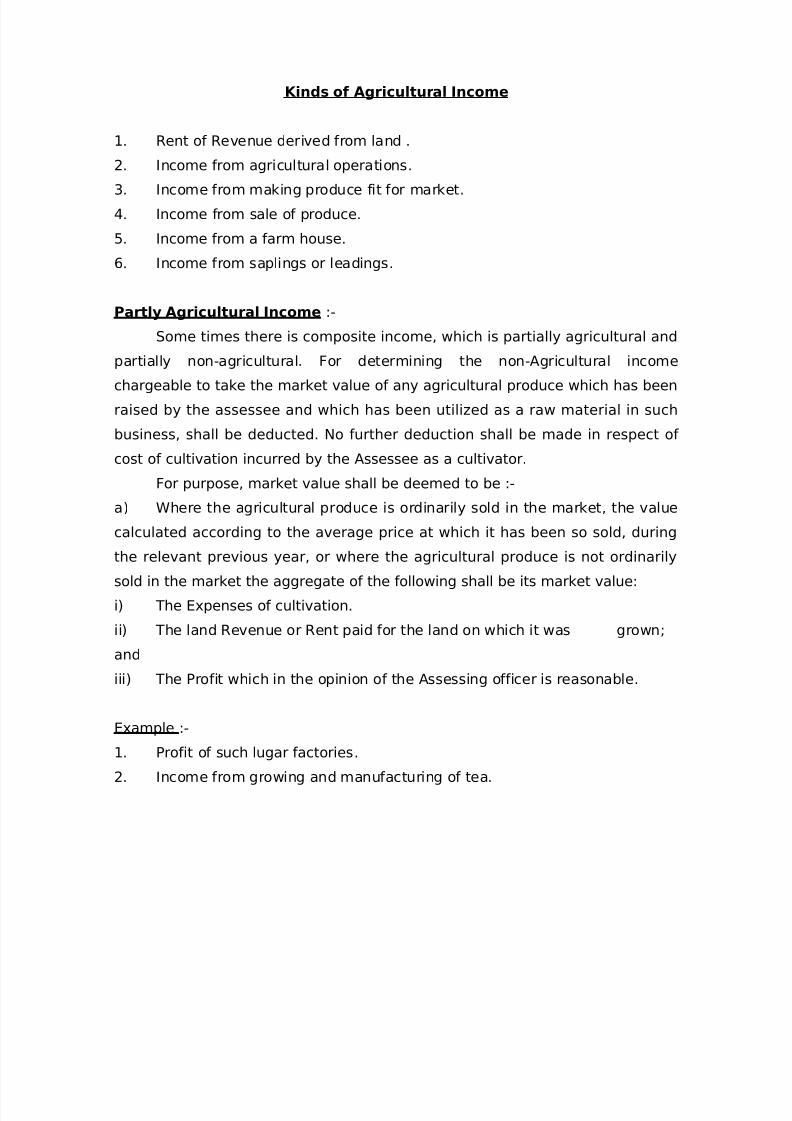

Kinds of Agricultural Income

1. Rent of Revenue derived from land .

2. Income from agricultural operations.

3. Income from making produce fit for market.

4. Income from sale of produce.

5. Income from a farm house.

6. Income from saplings or leadings.

Partly Agricultural Income :-

Some times there is composite income, which is partially agricultural and

partially non-agricultural. For determining the non-Agricultural income

chargeable to take the market value of any agricultural produce which has been

raised by the assessee and which has been utilized as a raw material in such

business, shall be deducted. No further deduction shall be made in respect of

cost of cultivation incurred by the Assessee as a cultivator.

For purpose, market value shall be deemed to be :-

a) Where the agricultural produce is ordinarily sold in the market, the value

calculated according to the average price at which it has been so sold, duringthe relevant previous year, or where the agricultural produce is not ordinarily

sold in the market the aggregate of the following shall be its market value:

i) The Expenses of cultivation.

ii) The land Revenue or Rent paid for the land on which it was grown;

and

iii) The Profit which in the opinion of the Assessing officer is reasonable.

Example :-

1. Profit of such lugar factories.

2. Income from growing and manufacturing of tea.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 34/76

3. Income from growing and manufacturing of centrifuged later or

cenex.

4. Income from growing and manufacturing of coffee.

Non-Agricultural Income from Land :-

The following incomes, are not derived from land used for agricultural

purposes, hence they are non-agricultural incomes :-

i) Income from market;

ii) Income from stone quarries;

iii) Income from mining royalties.

iv) Income from land used for storing agricultural produce;

v) Income from supply of water for irrigation purpose (e.g. Income from

supply of water for irrigation from a tube-well or well, as it does not involve

any agricultural operation.

vi) Income from self-grown grass, trees or bamboos;

vii) Income from fisheries;

viii) Income from the sale of earth for brick making ;

ix) Remuneration received as manager of an agricultural form;

x) Dividend from a company engaged in agriculture;xi) Income of the buyer of a ripe crop;

xii) Income from dairy farm, poultry farming, etc; and

xiii) Income from interest on Arrears of rent of agricultural land.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 35/76

INCOME TAX

AUTHORITIES AND

THEIR POWERS

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 36/76

APPOINMENT AND CONTROL

The government of India has organized a member of authorities to

execute the Income Tax Act and to administer the Income Tax Department

efficiently.

The Central Board of Direct takes is the apex body in the direct tax set up.

It performs various statutory functions under the various act and is responsible

for formulation and implementation of policies relating to direct tax

administration. The Board consists of a chairman and six members.

The CBDT has attached offices under the Directors General of Income Tax,

VIZ.,

1. D.G. (Administration), New Delhi;

2. D.G. (Vigilance), New Delhi;

3. D.G. (Systems), New Delhi;

4. D.G. (International Taxation), New Delhi;

5. D.G. (Research), New Delhi;

6. D.G. (Training), Nagpur;

7. D.G. (Exemption), Kolkata;

Proceedings before Income Tax Authorities to be Judicial Proceedings :-

(Sec. 136)

Any proceeding under this Act before an income tax authority shall be

deemed to be a judicial proceeding within the meaning of Sections 193 and 228

and for the purpose of section 196 o the Indian Penal Code, 1860 and every

income tax authority shall be deemed to be a civil court for the purpose of

section 195, but not for the purpose of chapter XXVI of the code of criminal

procedure, 1973.

The Powers of Income tax authorities can also be discussed as under :-

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 37/76

1. The commissioner (Appeals) shall have the same powers as are

vested in a court under the code of civil Procedure, 1908, when trying a suit

under this Act.

(Sec. 131)

2. The Commissioner (Appeals) shall have all power to call for

information U/S 133.

(Sec. 133)

3. The Commissioner (Appeals) may inspect or take copies of any register of

members, debenture holder or mortgagees of any company.

(Sec. 134)

4. The Commissioner(Appeals) which disposing of an appeal, shall have the

following powers:-

(a) in an appeal against an order of assessment be may confirm, reduce,

enhance annual the assessment;

(b) in an appeal against an order imposing a penalty, he may confirm or

cancel such order or vary it so as either to enhance or to reduce the penalty;

(c) in any other case, he may pass such order in the appeal as be thinks

fit.Provided that he shall not enhance an assessment or a penalty or reduce

the amount of refund unless the appellant has had a reasonable opportunity of

showing causes against such enhancement or reduction.

Further, the commissioner (Appelas) may consider and decide any matter

arising out of the proceedings, even if such matter was not raised before the

commissioner (Appeals) by the appellant.

Inspectors of Income Tax :-

The income tax inspectors are appointed by the commissioner of income

tax and are required to perform such functional as may be assigned to them

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 38/76

from time to time either by the commissioner or by the authority under whom

they are working.

Assessing Officers :- {Sec. 2(7A)}

An assessing officer means the Assistant Commissioner or Deputy

Director or Deputy Commissioner or Assistant Director or the Income tax officer

who is vested with the relevant jurisdiction by virtue of directions or orders

issued by the Central Board of Direct Takes and it also includes the Joint

Commissioner or Joint Director who is Directed to exercise or perform all or any

of the powers and functions conferred on or assigned to an Assessing officer.

Jurisdiction of Assessing Officers :-

An Assessing Officer performs his functions in respect of such area and

classes of assesses as are vested with him. Where he has been vested with

jurisdiction over any area, within the limit of such area, he shall have

jurisdiction.

i) In the case of business assessees:

Over all such assessees whose business are situated in that area if the

business of an assessee is situated at different places, the principals place of

his business will be considered and the Assessing officer under whose

jurisdiction that place is situated, shall assess the income of such assessee.ii) in the case of any other person residing in that area.

Appeal against jurisdiction:-

An assessee cannot make any appeal against the jurisdiction of an

Assessing Officer in the following cases:-

a) (i) He has made a return u/s 139(1) voluntarily,

(ii) After the expiry of one month from the date on which he was

served with a notice u/s 142 (1) or u/s /143 (2); or

(iii) After the completion of Assessment, whichever is earlier.

b) Where he ails to file the return after the expiry of the time allowed u/s

148 or show cause u/s 144 why assessment should not be completed on the

basis of best judgment assessment whichever is earlier.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 39/76

An assessing officer shall have all the powers conferred by or under this

Act in respect of all incomes accruing or arising received within the area

assigned to him.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 40/76

ADVANCE

PAYMENT OF TAX

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 41/76

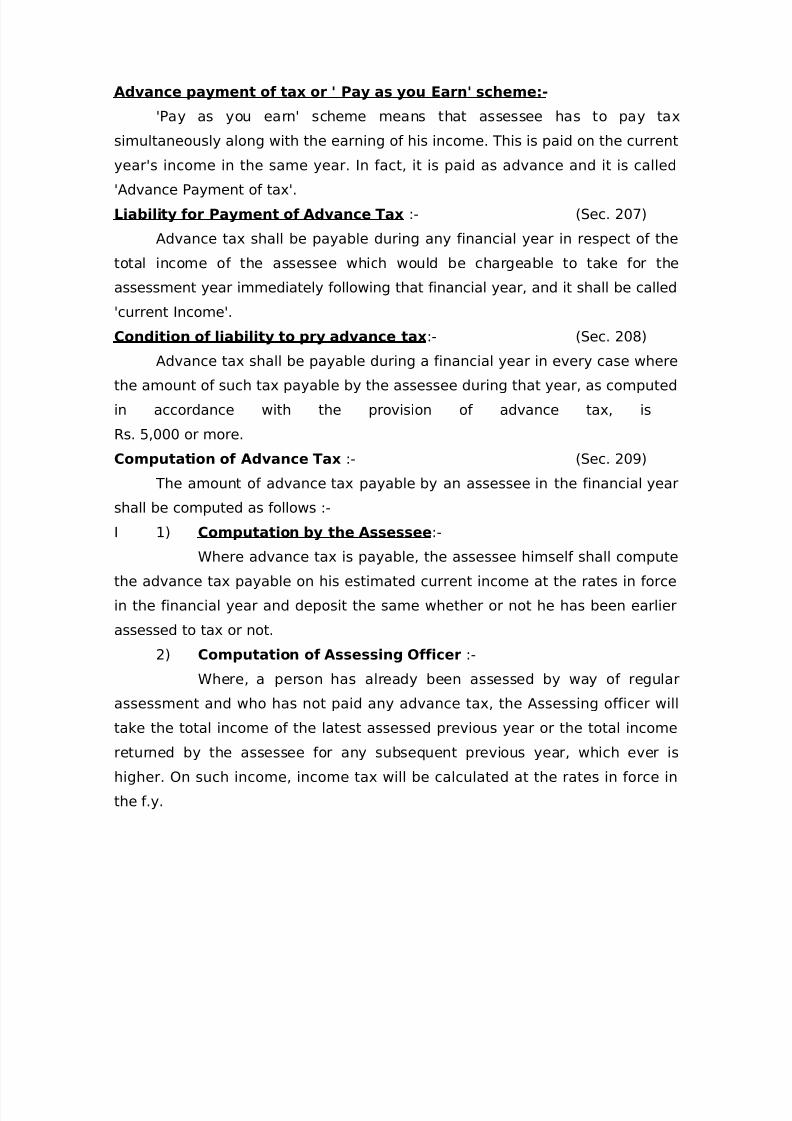

Advance payment of tax or ' Pay as you Earn' scheme:-

'Pay as you earn' scheme means that assessee has to pay tax

simultaneously along with the earning of his income. This is paid on the current

year's income in the same year. In fact, it is paid as advance and it is called

'Advance Payment of tax'.

Liability for Payment of Advance Tax :- (Sec. 207)

Advance tax shall be payable during any financial year in respect of the

total income of the assessee which would be chargeable to take for the

assessment year immediately following that financial year, and it shall be called

'current Income'.

Condition of liability to pry advance tax:- (Sec. 208)

Advance tax shall be payable during a financial year in every case where

the amount of such tax payable by the assessee during that year, as computed

in accordance with the provision of advance tax, is

Rs. 5,000 or more.

Computation of Advance Tax :- (Sec. 209)

The amount of advance tax payable by an assessee in the financial year

shall be computed as follows :-

I 1) Computation by the Assessee:-Where advance tax is payable, the assessee himself shall compute

the advance tax payable on his estimated current income at the rates in force

in the financial year and deposit the same whether or not he has been earlier

assessed to tax or not.

2) Computation of Assessing Officer :-

Where, a person has already been assessed by way of regular

assessment and who has not paid any advance tax, the Assessing officer will

take the total income of the latest assessed previous year or the total income

returned by the assessee for any subsequent previous year, which ever is

higher. On such income, income tax will be calculated at the rates in force in

the f.y.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 42/76

3) The income tax calculated under para (a) or (2) above, as the case

may be shall in each case, be reduced by the amount of take deductible or

collective at source during the financial year from any income which has been

taken into account in computing the current income or total income. The

balance will be the amount of advance tax payable.

II) Net agricultural income to be taken in to account.

Where, in case of any class of assessees, net agricultural income has to

be taken into account for computing advance tax, such income will be added to

the aforesaid income.

Assessee deemed to be in default :- (Sec. 218)

if any assessee (i) does not pay on the due date specified in section 211)

any installment of advance tax that he is required to pay by an order of the

Assessing officer and does not, on or before the due date,.

ii) Send to the assessing officer an intimation that as per his estimate of the

current income the advance tax payable would be less than the amount

specified in his order or does not pay on the basis of his estimate of his current

income the advance tax payable by him, he shall be deemed to be an assessee

in default in respect of such installment or installments.

Credit for advance tax:- (Sec. 219)Any sum paid by the assessee as advance tax shall be treated as a

payment of tax and credit therefore shall be given to the assessee in the

regular assessment.

Installments of advance tax and due dates :- (Sec. 211)

Advance tax on the current income shall be payable by all assessee who

are liable to pay the same as per for following table during the financial year

2009-10.

A) Companies :-

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 43/76

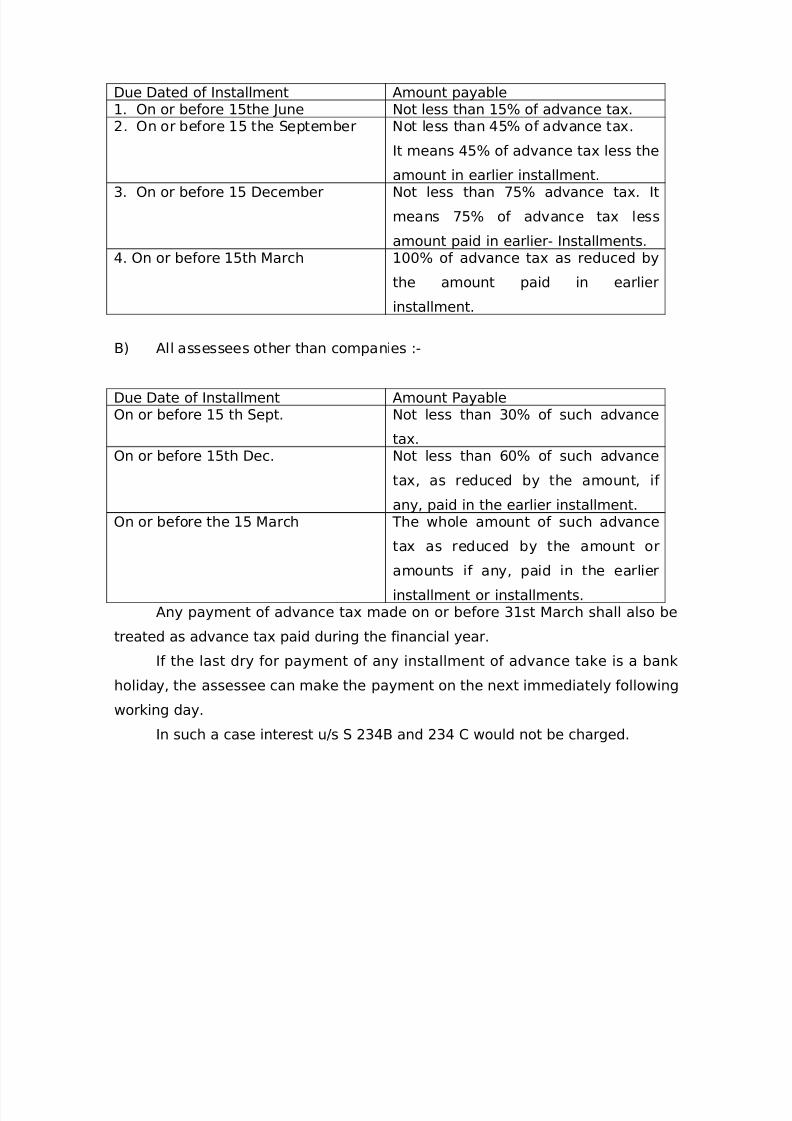

Due Dated of Installment Amount payable1. On or before 15the June Not less than 15% of advance tax.2. On or before 15 the September Not less than 45% of advance tax.

It means 45% of advance tax less the

amount in earlier installment.3. On or before 15 December Not less than 75% advance tax. It

means 75% of advance tax less

amount paid in earlier- Installments.4. On or before 15th March 100% of advance tax as reduced by

the amount paid in earlier

installment.

B) All assessees other than companies :-

Due Date of Installment Amount PayableOn or before 15 th Sept. Not less than 30% of such advance

tax.On or before 15th Dec. Not less than 60% of such advance

tax, as reduced by the amount, if

any, paid in the earlier installment.On or before the 15 March The whole amount of such advance

tax as reduced by the amount or

amounts if any, paid in the earlier

installment or installments.Any payment of advance tax made on or before 31st March shall also be

treated as advance tax paid during the financial year.

If the last dry for payment of any installment of advance take is a bank

holiday, the assessee can make the payment on the next immediately following

working day.In such a case interest u/s S 234B and 234 C would not be charged.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 44/76

OTHER

TAX

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 45/76

ASSESSMEN

T

OF

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 46/76

INDIVIDUAL

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 47/76

ASSESSMENT OF INDIVIDUALS

Under the Income Tax Act, 1961 the assessee are of the

following types :Sec [2(31] or Sec (4).

1. Individual.

2. Hindu undivided family.

3. Firm,

4. Association of persons or Body of Individuals.

5. Company.

6. Local authority and

7. Artificial judicial person.

A study of the provision of the Income Tax Act regarding the

assessment of the aforesaid assessees has done in this.

Individuals -

An individual means a woman, man, minor child or any human

being. An individual has to pay income tax on his total income at a

graded scale of tax rates ruling during the concerned assessment

year. In addition to his own income under different heads, an

individual may also get a share of income from his membership in

the following institutions and some income of others are also to be

included in his total income.

1- As a member of Hindu Undivided Family-

Share of income received by an individual as a member of a

Hindu undivided family out of the income of the family is rather

taxable nor it is included in his total income, but if a member of the

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 48/76

family makes some personal earning of his own, they are taxable in

the hands of that member as an individual.

But, under section 64(2), where an individual converts his

separate in divided property into property of the H.U.F. of which he

is a member, then the income derived from such converted property

is to be included in the individual's total income and not in the

family's total income.

2- As a member of an Association of Persons or Body of

Individuals -

The income received by its members from the association of persons or body of Individuals shall be dealt with as under :

a) Where the A.O.P. or B.O.I is taxed at the minimum marginal

rate or any higher rate, the share of member shall not be included in

his total income at all.

b) Where no income tax is chargeable on the total income of the

A.O.P. or B.O.I, the share of member in that shall be chargeable to

tax as part of his total income.

c) Where tax has been paid by the A.O.P. or B.O.I at normal rate,

income tax shall not be payable in respect of such share although it

shall from part of total income of the member. It means on such

share income tax rebate shall be allowed at average rate of tax.

3. As a member (Shareholder) of a company -

As a member of a company an individual received divided from

the company on the distribution of its profits, whether out of taxable

income or tax-free income. It is immaterial whether it is received in

cash or in kind.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 49/76

Any payment by a closely held company by way of advance or

loan to a share holder having at least 10% of the voting power or a

partner to any concern in which such shareholder is a member or a

partner and in which he has a substantial interest.

Income of others to be included in the total income of an

individual :-

a) Where a person transfers his income from an assest to anthers

person without transferring the assest itself, such income shall be

included in the total income of the transferor.

b) Whether there is a revocable transfer of assests the incomefrom such assests shall be included in the total income the

transferor. There are, however certain exceptions to this rule.

c) Under to certain circumstances the income of the spouse of an

individual is included in his total income.

d) The income of a minor child is included in the total income of

his or her parent either mother or father, as the case may be.

c) Income from assests transferred to other persons is included in

the total income of the transferor if such a transfer results directly or

indirectly, in a benefit to the spouse of the transferor.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 50/76

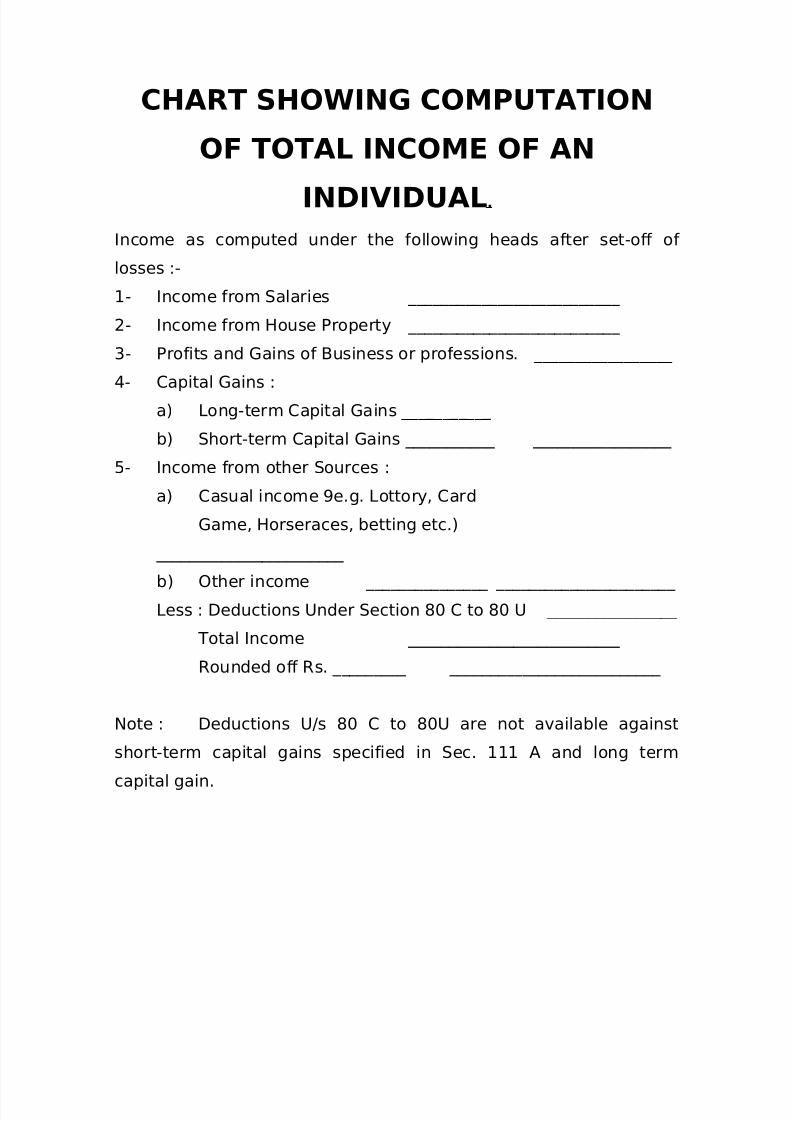

CHART SHOWING COMPUTATION

OF TOTAL INCOME OF AN

INDIVIDUAL.

Income as computed under the following heads after set-off of

losses :-

1- Income from Salaries __________________________

2- Income from House Property __________________________

3- Profits and Gains of Business or professions. _________________ 4- Capital Gains :

a) Long-term Capital Gains ___________

b) Short-term Capital Gains ___________ _________________

5- Income from other Sources :

a) Casual income 9e.g. Lottory, Card

Game, Horseraces, betting etc.) _______________________

b) Other income _______________ ______________________

Less : Deductions Under Section 80 C to 80 U ________________

Total Income __________________________

Rounded off Rs. _________ __________________________

Note : Deductions U/s 80 C to 80U are not available against

short-term capital gains specified in Sec. 111 A and long term

capital gain.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 51/76

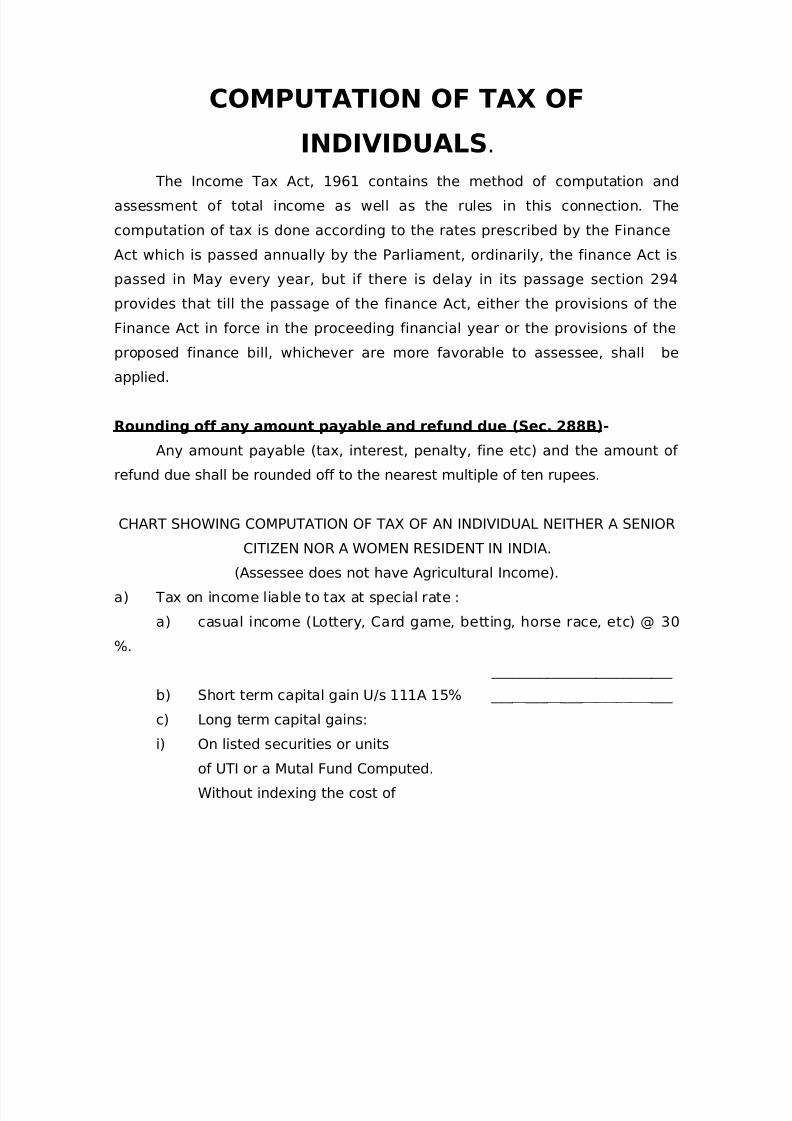

COMPUTATION OF TAX OF

INDIVIDUALS.

The Income Tax Act, 1961 contains the method of computation and

assessment of total income as well as the rules in this connection. The

computation of tax is done according to the rates prescribed by the Finance

Act which is passed annually by the Parliament, ordinarily, the finance Act is

passed in May every year, but if there is delay in its passage section 294

provides that till the passage of the finance Act, either the provisions of the

Finance Act in force in the proceeding financial year or the provisions of the

proposed finance bill, whichever are more favorable to assessee, shall beapplied.

Rounding off any amount payable and refund due (Sec. 288B)-

Any amount payable (tax, interest, penalty, fine etc) and the amount of

refund due shall be rounded off to the nearest multiple of ten rupees.

CHART SHOWING COMPUTATION OF TAX OF AN INDIVIDUAL NEITHER A SENIOR

CITIZEN NOR A WOMEN RESIDENT IN INDIA.

(Assessee does not have Agricultural Income).

a) Tax on income liable to tax at special rate :

a) casual income (Lottery, Card game, betting, horse race, etc) @ 30

%.

__________________________

b) Short term capital gain U/s 111A 15% __________________________

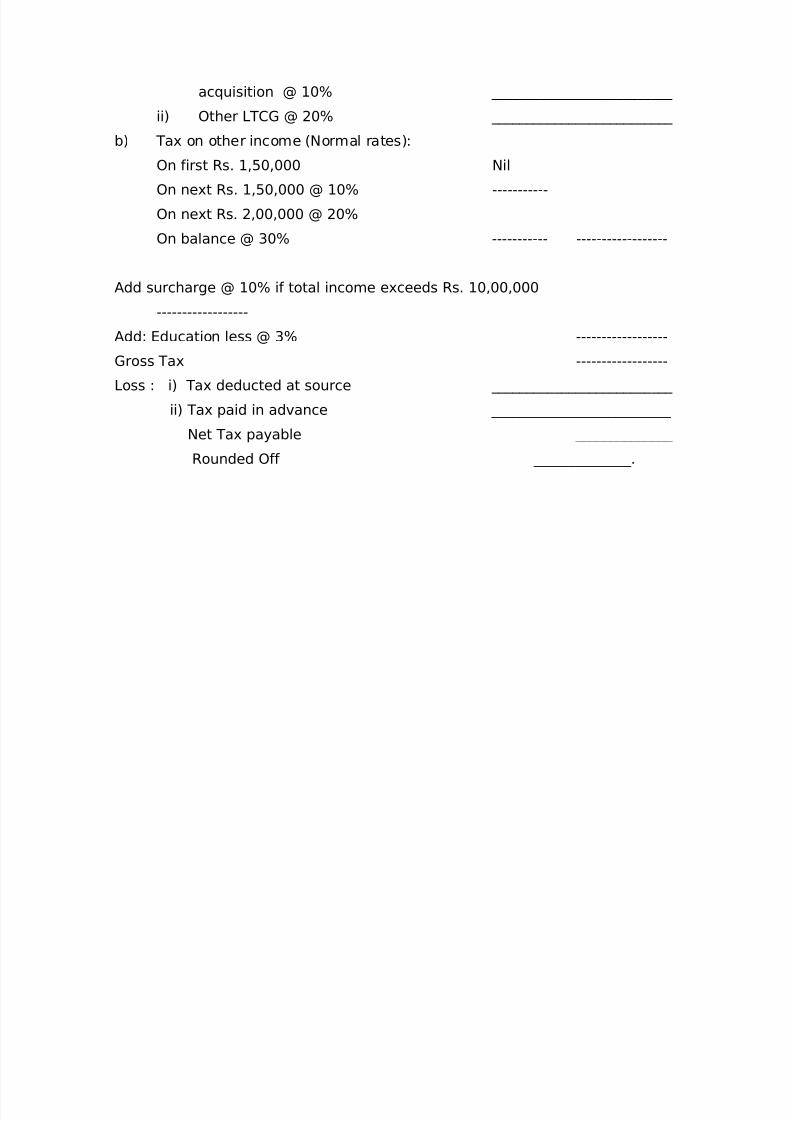

c) Long term capital gains:

i) On listed securities or units

of UTI or a Mutal Fund Computed.

Without indexing the cost of

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 52/76

acquisition @ 10% __________________________

ii) Other LTCG @ 20% __________________________

b) Tax on other income (Normal rates):

On first Rs. 1,50,000 Nil

On next Rs. 1,50,000 @ 10% -----------

On next Rs. 2,00,000 @ 20%

On balance @ 30% ----------- ------------------

Add surcharge @ 10% if total income exceeds Rs. 10,00,000

------------------

Add: Education less @ 3% ------------------

Gross Tax ------------------

Loss : i) Tax deducted at source __________________________

ii) Tax paid in advance __________________________

Net Tax payable ______________

Rounded Off ______________.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 53/76

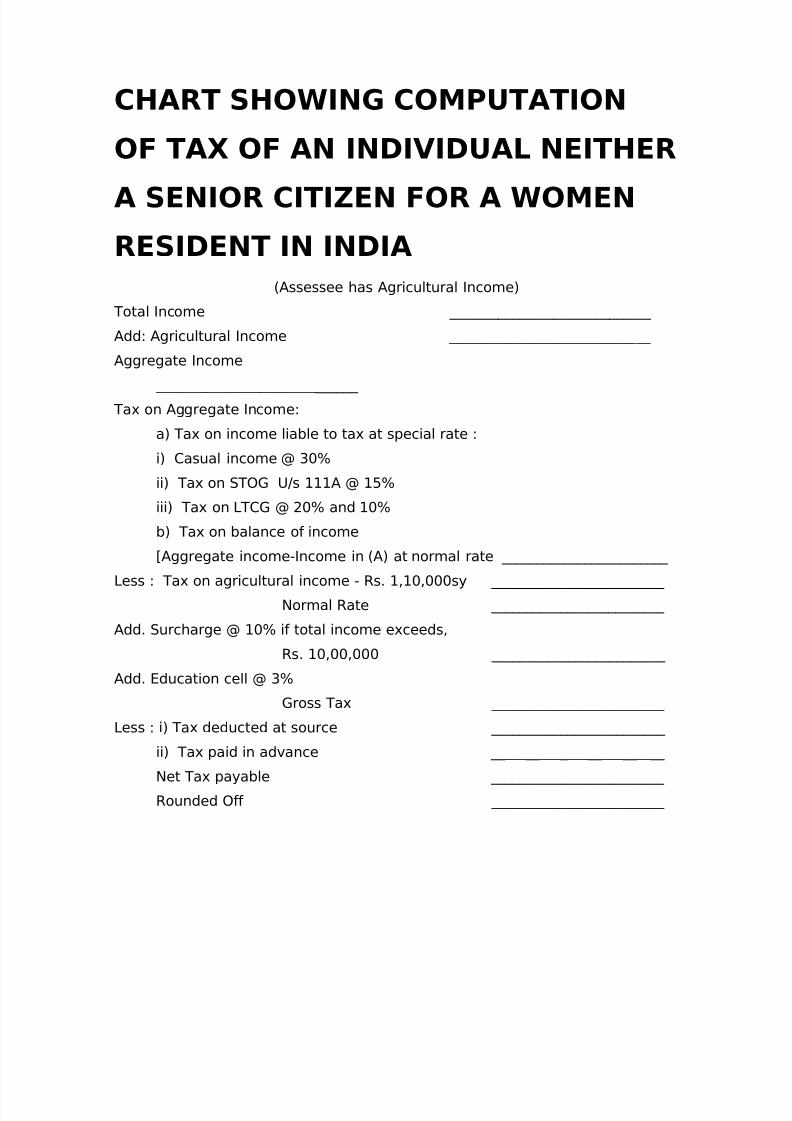

CHART SHOWING COMPUTATION

OF TAX OF AN INDIVIDUAL NEITHER

A SENIOR CITIZEN FOR A WOMEN

RESIDENT IN INDIA

(Assessee has Agricultural Income)

Total Income _____________________________

Add: Agricultural Income _____________________________

Aggregate Income

_____________________________

Tax on Aggregate Income:

a) Tax on income liable to tax at special rate :

i) Casual income @ 30%

ii) Tax on STOG U/s 111A @ 15%

iii) Tax on LTCG @ 20% and 10%

b) Tax on balance of income[Aggregate income-Income in (A) at normal rate ________________________

Less : Tax on agricultural income - Rs. 1,10,000sy _________________________

Normal Rate _________________________

Add. Surcharge @ 10% if total income exceeds,

Rs. 10,00,000 _________________________

Add. Education cell @ 3%

Gross Tax _________________________

Less : i) Tax deducted at source _________________________

ii) Tax paid in advance _________________________

Net Tax payable _________________________

Rounded Off _________________________

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 54/76

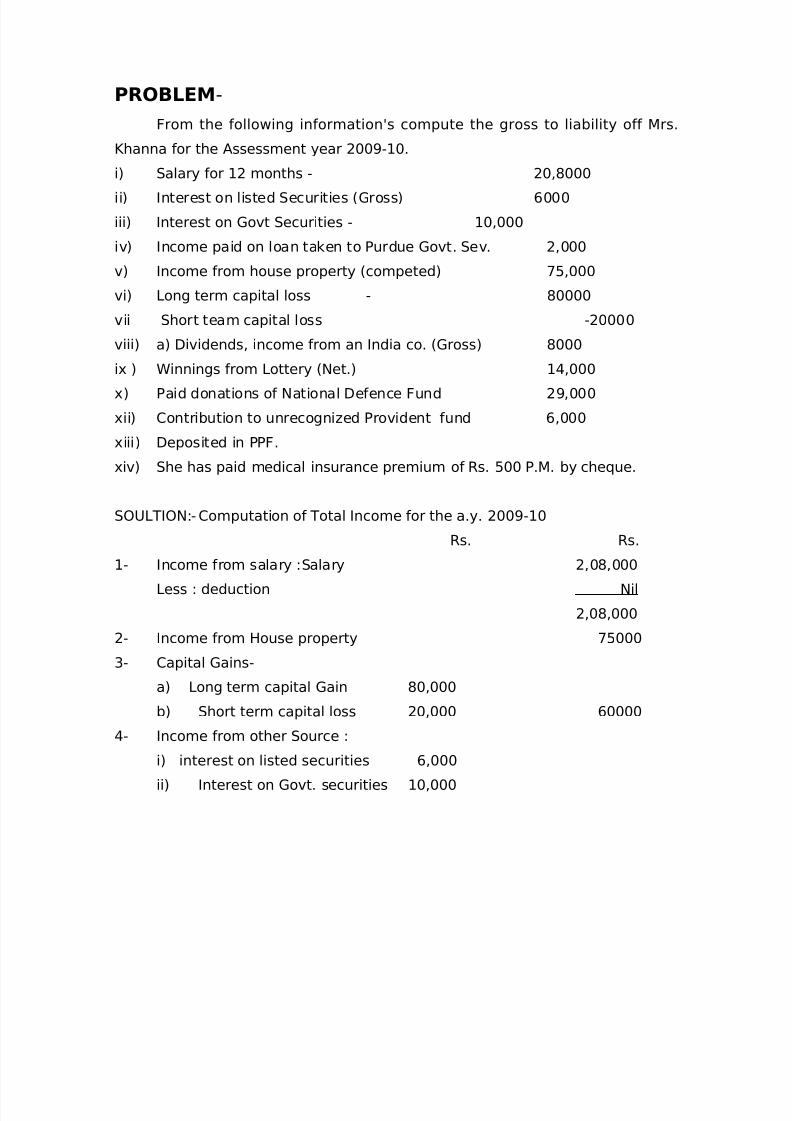

PROBLEM-

From the following information's compute the gross to liability off Mrs.

Khanna for the Assessment year 2009-10.

i) Salary for 12 months - 20,8000ii) Interest on listed Securities (Gross) 6000

iii) Interest on Govt Securities - 10,000

iv) Income paid on loan taken to Purdue Govt. Sev. 2,000

v) Income from house property (competed) 75,000

vi) Long term capital loss - 80000

vii Short team capital loss -20000

viii) a) Dividends, income from an India co. (Gross) 8000

ix ) Winnings from Lottery (Net.) 14,000

x) Paid donations of National Defence Fund 29,000

xii) Contribution to unrecognized Provident fund 6,000

xiii) Deposited in PPF.

xiv) She has paid medical insurance premium of Rs. 500 P.M. by cheque.

SOULTION:- Computation of Total Income for the a.y. 2009-10

Rs. Rs.

1- Income from salary :Salary 2,08,000

Less : deduction Nil

2,08,000

2- Income from House property 75000

3- Capital Gains-

a) Long term capital Gain 80,000

b) Short term capital loss 20,000 60000

4- Income from other Source :

i) interest on listed securities 6,000

ii) Interest on Govt. securities 10,000

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 55/76

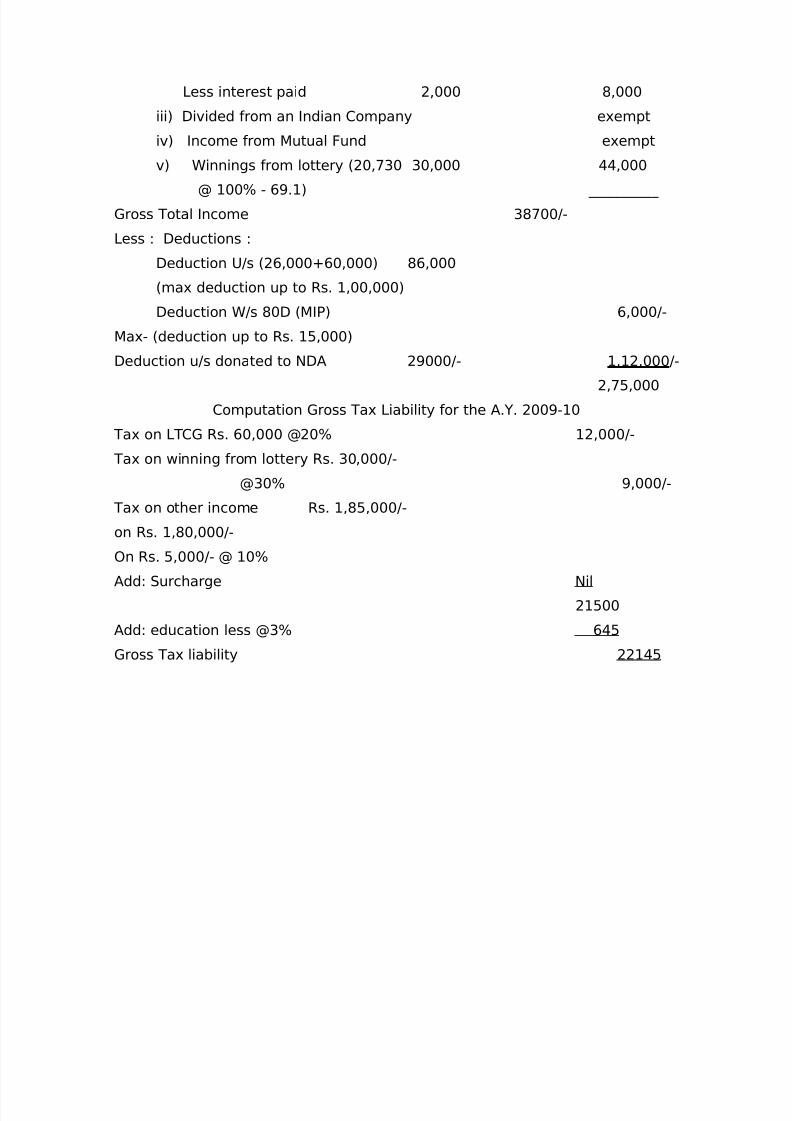

Less interest paid 2,000 8,000

iii) Divided from an Indian Company exempt

iv) Income from Mutual Fund exempt

v) Winnings from lottery (20,730 30,000 44,000

@ 100% - 69.1) __________

Gross Total Income 38700/-

Less : Deductions :

Deduction U/s (26,000+60,000) 86,000

(max deduction up to Rs. 1,00,000)

Deduction W/s 80D (MIP) 6,000/-

Max- (deduction up to Rs. 15,000)

Deduction u/s donated to NDA 29000/- 1,12,000/-

2,75,000

Computation Gross Tax Liability for the A.Y. 2009-10

Tax on LTCG Rs. 60,000 @20% 12,000/-

Tax on winning from lottery Rs. 30,000/-

@30% 9,000/-

Tax on other income Rs. 1,85,000/-

on Rs. 1,80,000/-On Rs. 5,000/- @ 10%

Add: Surcharge Nil

21500

Add: education less @3% 645

Gross Tax liability 22145

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 56/76

INTRODUCTION

OF

WEALTH TAX

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 57/76

The wealth tax Act extends to whole of India, and it come into

force on Ist April, 1957.

(Sec. 1)

A constitution bench of the supreme court has hold that the

wealth tax Act 1975 fell under entry 86 of the union list of the

constitution of India and therefore Parliament was competent to

exact the statute with reference to the state of Jammu & Kashmir.

Charge of Wealth Tax :- (Sec.

3)

Subject to the other provision of wealth Tax Act, 1957, thewealth tax is charged for every assessment year commencing from

Ist April, 1993 in respect of the net wealth on the corresponding

valuation date of every Individual Hindu Individuated Hindu

Undivided Family (governed by take share low) and company @ 1%

of the amount by which the net wealth exceeds 15 lakh rupees.

Meaning of Importance Items :-

Individual

The term individual has not been defined in the Act but in

general sense Individual means a natural person or human being

and includes :-

i) Hindu Deity or mutawali of wakf as a juristic individual.

ii) Group of individual being trustees holding property for the

benefit of an individual beneficiary.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 58/76

iii) Body of individuals, being joint heirs, joint donees and joint

purchasers.

iv) Holder of an importable estate.

v) A joint family (other than a H.U.F.) such as muslim undivided

family.

A trade union registered under the trade union Act is not

assessable as an individual.

Hindu undivided Family :-

A family governed by Hindu law is a H.U.F. a Jain undivided

family is treated as H.U.F. However if a Hindu converts toChristianity through he follows Hindu Law of Secession, cannot be

assessed as H.U.F.

For wealth take purpose it is essential that a family must be a

Hindu undivided family governed by mitakshare law. It is not

essential that the family must Raw coparceners. If a coparcener,

having a wife and minor daughters and no son receives his share inthe joint family property on partition, such property in his hands

shall be assessed as property of H.U.F.

Company :-

A company means :-

i) any Indian company, or

ii) any body corporate incorporated by or under the law of a

country outside India, or

iii) Any institution, association or body which is or was assessable

or was assessed as a company for any assessment year under the

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 59/76

Income tax Act, 1922 or which is or was assessable or was

assessed under the Income Tax Act, 1961 as a company for

any assessment year upto 1970-71, or

iv) Any institution, association or body, whether incorporated or

not and whether Indian or non-Indian, which is declared by general

or non-Indian, which is declared by general or special or special

order of the Board to be a company provided that it will be

deemed to be a company only for the assessment year specified in

the order.

Person not liable to pay wealth tax :-(Sec. 45)

a) Any co-operative Society.

b) Any Political Party.

c) A mutual fund the income of which is exempt u/s 10(23D) of

the Income tax Act.

d) Any Social Club.e) Any company registered u/s 25 fo the companies Act, 1956.

Valuation Date {Sec. 2

(Q)}

Wealth tax is lived on the net wealth of a person as on a

particular date. This date is known as valuation date. According to

section 2(Q) the valuation date is the last day of the previous year

relevant to the assessment year. Hence, valuation date is march 31,

immediately proceeding the assessment year.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 60/76

Net Wealth:- {Sec.

2 (M)}

'Net Wealth' means the amount by which the aggregate value

of all assets (excluding exempted assets), belonging to the assessee

on the valuation date, including assets required to be including in

his net wealth, is in excess of the aggregate value of all debts

owned by him on the valuation date which have been incused in

relation to the taxable assets.

Assessee {Sec. 2

(C)}

'Assessee' means a person by whom wealth tax or any other

sum of money is payable under this Act, and includes:-

i) every person in respect of whom any proceeding under this Act

has been taken for the determination of wealth tax payable by hi or

by any other person or the amount of refund due to him or such

other person;

ii) Every person who is deemed to be an assessee under this Act;

iii) Every person who is deemed to be an assessee in default

under this Act.

Deemed Assessee :-

1. Legal representative of a deceased person (Sec. 19A);

2. Executor or executors of the estate of a deceased person (Sec.

19A)

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 61/76

3. Guardian or trustee of any person being a minor, lunatic or

idiot who holds any assets on behalf of and for the benefit of such

beneficiary {Sec. 21 (3)}' and

4. a person deemed to be the agent of any person residing

outside India.

Assessment year :- {Sec. 2

(d)}

It means a period of 112 months commencing on Ist day of

April every year.

Assets :- {Sec. 2

(ea)}

The assets include the following :-

1) Any building or land appurtenant thereto:

i) Commercial building;

ii) Residential building;

iii) Any guest house;

iv) A form house situated within 25 Kilo-metre from the local

limit of a local authority.

2) Motor cars (excluding those used by the assessee in the

business of running them on hire or as stock-in-trade).

Jeeps owned by the assessee should be treated motors cars.3) Jewellary, buillion, furniture, utensils or any other article made

wholly or partly of gold, silver, platinum or any other precious

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 62/76

metal or any alloy containing one or more of such precious

metal (excluding those hold as stock-in-trade by the Assessee)

4) Yachts, boats and aircrafts (excluding those used by assessee

for commercial purposes).

5) Urban Land :-

'Urban land' means land situated :-

i) in any area which is comprised within the jurisdiction of a local

authority and which has a population of not less than 10,000

according to the last preceding census of which the relevant figureshave been published before the valuation date;

ii) any area within such distance, not being more than 8 Kilo-

metre from the local limit of a local authority as the central

government may, having regard to the extent and scope for

urbanization of that area and other relevant considerations, specify

in this behalf by notification in the official Gazette.6) Cash in hand:-

i) in case of an individual and H.U.F. cash in hand in excess

of Rs. 50,000 shall be included in assets;

ii) in case of any other person cash in hand not recorded in

the books of account shall be included in assets.

Scheme of wealth Tax at Glance :-

Wealth tax is levied on not wealth u/s 2 (m) as it exits on

valuation date. The computation of not wealth may be summarized

at a glance in the following manner:-

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 63/76

ADD:-

1) The value of Assets wherever, located, which are chargeable

belonging the assessess.

2) The value of assets required to be included in the not wealth of

assessee under deeming under provisions.

LESS:-

Debts owned by the assessee on valuation date which have

been incurred in relation to said asset.

COMPUTATION

OF

NET WEALTH

AND

WEALTH TAX

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 64/76

While computing the net wealth the value of the following assets in

aggregated:-

1. Assets owned by the assessee.

2. Assets required to be included in his net wealth u/s A.

However the value of the following assets is not included in the

wealth:

1. Assets excluded from the term 'Assets' u/s 2(ea)

2. Assets exempt u/s 5;

3. Assets not liable to tax u/s 6;

4. Assets last, destroyed or stolen or before the valuation date.From the aggregate value of assets the aggregate value of the

debts is deducted. Debts owed by the assessee on the valuation

date which have been incurred in relation to assets belonging to the

assessee including the deemed Assets u/s 4.

Debts and liabilities not deductible :-

i) if the assessee is not a citizen of India and/or non-resident ornon ordinarily resident in India the debts situated outside India.

A debt is located at the place where it is payable. If the place of

payment is not specified than the location of debt is determined by

the place of residence of the creditor.

2. Debts which have been incurred in relation to any property

which is not included in 'assets'.

Rate of Tax

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 65/76

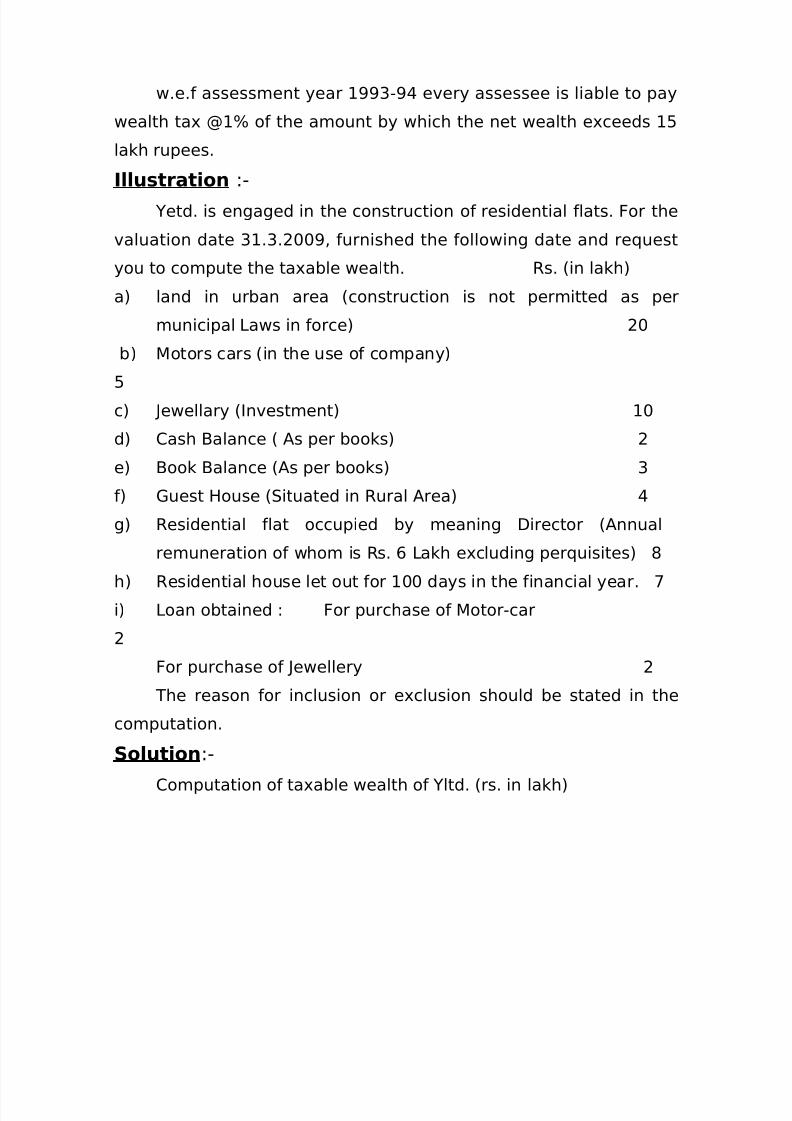

w.e.f assessment year 1993-94 every assessee is liable to pay

wealth tax @1% of the amount by which the net wealth exceeds 15

lakh rupees.

Illustration :-

Yetd. is engaged in the construction of residential flats. For the

valuation date 31.3.2009, furnished the following date and request

you to compute the taxable wealth. Rs. (in lakh)

a) land in urban area (construction is not permitted as per

municipal Laws in force) 20

b) Motors cars (in the use of company)5

c) Jewellary (Investment) 10

d) Cash Balance ( As per books) 2

e) Book Balance (As per books) 3

f) Guest House (Situated in Rural Area) 4

g) Residential flat occupied by meaning Director (Annualremuneration of whom is Rs. 6 Lakh excluding perquisites) 8

h) Residential house let out for 100 days in the financial year. 7

i) Loan obtained : For purchase of Motor-car

2

For purchase of Jewellery 2

The reason for inclusion or exclusion should be stated in the

computation.

Solution:-

Computation of taxable wealth of Yltd. (rs. in lakh)

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 66/76

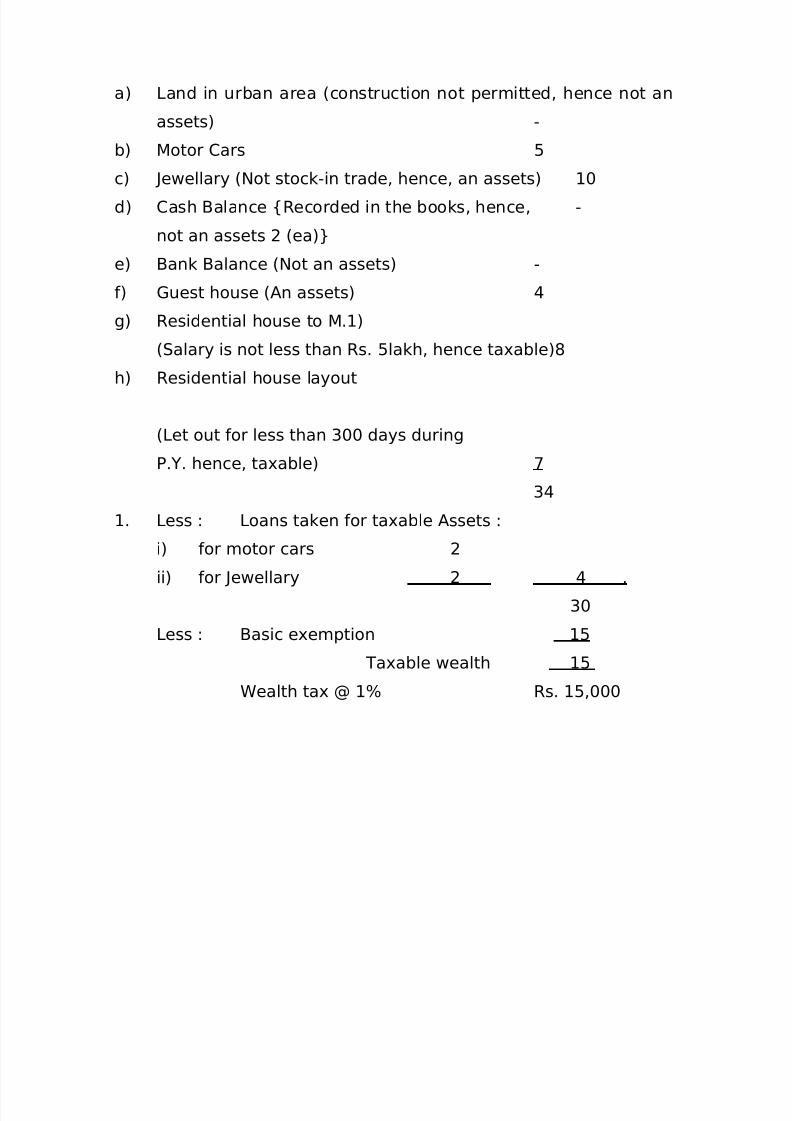

a) Land in urban area (construction not permitted, hence not an

assets) -

b) Motor Cars 5

c) Jewellary (Not stock-in trade, hence, an assets) 10

d) Cash Balance {Recorded in the books, hence, -

not an assets 2 (ea)}

e) Bank Balance (Not an assets) -

f) Guest house (An assets) 4

g) Residential house to M.1)

(Salary is not less than Rs. 5lakh, hence taxable)8h) Residential house layout

(Let out for less than 300 days during

P.Y. hence, taxable) 7

34

1. Less : Loans taken for taxable Assets :

i) for motor cars 2

ii) for Jewellary 2 4 .

30

Less : Basic exemption 15

Taxable wealth 15

Wealth tax @ 1% Rs. 15,000

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 67/76

ASSESSMENT

OF

INSURANCE BUSINESS

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 68/76

Section 44 of the Income Tax Act provides that the profits and gains

of any business of insurance including any such business carried on

by a mutual insurance company or by a co-operative Society shall

be computed in accordance with the rules prescribed in the First

schedule to the Income Tax Act, 1961. Here it is important to note

that for an insurance business, the entire income is business

income, though for a non-insurance concern income may fall under

various Head viz; 'Income From House Property' 'Capital Gains' or

'Income from other Sources'. Thus for an insurance concern all such

incomes are business income.Mutual Insurance Company:-

Mutual Insurance company means an insurer, being a company

incorporated under the Indian Company law which has no share

capital and of which by its constitution, only all policy holders are

members.

Co-operative Society:-Co-operative life Insurance Society means an insurer being a

society registered under the co-operative societies Act, 1912 or

under an Act of a State Legislature governing the registration of co-

operative Societies which carries on business of life insurance and

which has no share capital on which dividend or bonus is payable

and of which, by its constitution only original members on whose

application the society is registered and policy holders are

members.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 69/76

Under Section 80 P (2) (C) the income of such a society is

exempt up to Rs. 50,000

Probably, this clause has lost its utility on account of

nationalization of insurance business.

Life Insurance Business:-

The Profits and gains of life insurance business shall be

computed separately from the profits and gains from any other

business.

The Profits and gains of life insurance business shall be taken

to be the annual average of the surplus arrived at by adjusting thesurplus or deficit disclosed by the actuarial valuation made in

accordance with the insurance Act, 1938, in respect of the last inter-

valuation period ending before the commencement of the

assessment year, so as to exclude from it any surplus or defect

included therein which was made in any earlier inter-valuation

period.It means the annual average of the surplus is only a national

figure of income which is taken as the base for assessment and the

actual income of the relevant year which may be more or less than

the annual average of the last inter-valuation period.

Rate of tax for assessment year 2009-10.

On the profits and gains of the life insurance business income

tax shall be charged @ 12½ %, surcharge @ 10% if total income

exceeds one crore rupees. on the amount of income tax and

surcharge education less shall be payable @ 3%

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 70/76

(Sec. 115 B)

Other Insurance Business:-

The profit of non-life insurance business, e.g. fire insurance

business marine insurance business, general insurance business etc,

shall be the profits disclosed by the annual account required to be

prepared under the Insurance Act, 1938. However, the following

adjustments are made to such profits:

1. If such profits are arrived at after deducting any expenditureof allowance including any amount debited to P. & L. as

either by way of provisions for any tax, dividend, reserve or

any other provision as may be prescribed by the Board,

which is not admissible under sections 30 to 43 B of the

Income Tax Act, such expenditure or allowance shall be

added back to the profits.2. The reserve for in expired risks shall be allowed as a

deduction to the following extent

(Rule 6E)

3. Where the insurance business relations to fire insurance or

engineering insurance and which provides insurance for

terrorism risks - 100% of the net premium income of such

business of the provisions year;

a) where the insurance business relates to fire

insurance or miscellaneous insurance other than

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 71/76

covered under (a) -50% of the net premium income

of such business of the previous year.

b) Where the insurance business relates to marine

insurance - 100% of the net premium income of such

business of the previous year.

'Net Premium Income' means the amount of

premium received as reduced by the amount of re-

insurance premiums paid during the relevant

previous year.

Amount set apart by G.I.C. of India for redemption of preference shared Under General Insurance Business

(Nationalization) Rules, 1973. The amount cannot be

added back in computing profits and gains for

income tax purposes.

Other Provisions :-

Profits and gains of non-resident person:-

The and gains of the branches in India of a person not resident

in India and carrying on any business of insurance, may in the

absence of more reliable date be deemed to be that proportion of

the worth income of such person which corresponds to the

proportion which his premium income derived from India bears to

his total premium income.

The world income in relation to life insurance business of a

person not resident in India shall be computed in the manner laid

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 72/76

down in the First schedule for the computation of the profit and

gains of life insurance carried on in India.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 73/76

Rate of Tax for non-life insurance Business:-

The assessee will pay tax on such income at ordinary rate

applicable to him.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 74/76

BIBLIOGRAPHY

- INCOME TAX LAW AND PRACTICE

By. Dr. H.C. Malhotra.

- TAXMANN'S STUDENTS UGIDE TO INCOME TAX AND SALES TAX

By Dr. V.K. Singhania.

- DIRECT & INDIRECT TAXES.

By Dr. Girish Ahuja.

- INCOME TAX LOW

By V.P. Gaur & D.B. Narang.

- INCOME TAX & GUIDELINES & MANI READY RECKONER.

By Nabli Publication.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 75/76

CONCLUSION

From the above, I have conclude that the income tax is tough,

but it is not so hard that the other say, It is too easy, if we deeply

read or understanding or each concept. The knowledge of tax is very

important in the practical life of every person.

The income tax is a direct tax and wealth tax, Sales Tax etc, is

direct tax. The tax is levied on every person's income. Indian tax

system is a multiple taxation system as Indian country is a mix of

direct or direct taxes. In brief the tax is source of government

revenue.

7/27/2019 Income Tax & Wealth Tax MODIFY

http://slidepdf.com/reader/full/income-tax-wealth-tax-modify 76/76

SUGGESTION

- Tax is levied on every person, whose income is assessable in

the Income Tax Act, 1961.

- The tax offices should be honestly and efficiently in their work.

- Suitable amendment is a land revenues sales tax.

- High rate of tax is levied on luxury goods.

- The penalty or fine is not much higher that the person are

trying to evade that type of money.

- Those found quilts of evading tax be levied penalized.

- The rules and regulation of tax is simply so that people can

understand easily.