Embed Size (px)

Citation preview

Increasing Your

Bank’s

Profitability

David Mendoza – Senior Business Consultant

Sales and Service Solutions

FIS

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Market Challenges • Bank revenues are under pressure

– Reg E overdraft amendment / Durbin amendment

– Decrease in loan demand

– Commercial credit renewals 2011-2013

– Consumer confidence / unemployment

– Additional regulation - Future Focus of Consumer Protection Agency?

– TCF moving to flat OD fee policy – Will end per item OD fee by year end

2

Durbin?

TowerGroup estimates that regulatory changes will reduce bank fees by an estimated $25B annually

$36B

$12B

$22B

$4B $3B Exception Fees (Mainly NSF/OD) Interchange Fees

Net Interest Margin

Transaction Fees

Maintenance Fees

Checking Account Income Components Annual Income in $Billions

Source: Federal Reserve Bank (Transaction Deposits, Commercial Banks) Source: Profit vs. Growth: Banks Unveil New Checking Account Pricing Strategies, July 2011

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Build a Foundation for Profitable Growth Back to the Basics

Understand the profitability of your customers.

Develop segmentation schemes that divide customers into useful and actionable

segments based on profitability, demographic, and lifecycle attributes.

Leverage technology, people, and process to execute tactics based on customer

segments.

3

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 4

Relationship Profitability A Bottom-Up Approach

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 5

Why Customer Profitability Still Matters? 80/20 Rule Too Optimistic

($700)

$0

$700

$1,400 Rolling 12 Average Profit

10 9 8 7 6 5 4 3 2 1 Decile

370 of 4,000 (9.2%) customers drive 85% of total profits 54% of customers have sub-par returns of LESS than $25 per month

Source: FIS

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

• Assign relationship managers to top 100 customers and have proactive calling effort to ensure their on-going satisfaction with bank.

• Empower employees to make pricing and fee decisions.

• Identify unprofitable customers with a:

– Waived fee status and evaluate if the status is correct

– Negative Net Interest Margin and determine why. Use information in re-pricing efforts

– Single product and cross-sell profitable product or change product features

• Incent relationship managers to increase the profitability of their portfolios.

… to achieve Profitable Customer Growth

Actionable Strategies

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Why Product Profitability is Important…

7

Our industry is evolving and customers have more choices than ever!

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 8

Top Banking Trends #1 retail banking re-pricing

“By the end of 2011, customers will have to earn the right to waive fees with behaviors and balances.”

Top 10 Trends in Retail Banking, 2011

February, 2011

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 9

What is Best Approach to Change Consumer Behavior?

What is the most effective approach to attract and retain profitable customers?

OR

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 10

Do Carrots Really Work? Lift in adoption of services

Source: Case study from financial institutions based in West

46%

58%

12%

61%

1%

90% 94%

83%

90%

99%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Check Card Penetration

Online Banking Enrollment

Electronic Statements

Direct Deposit Valid E-Mail Address

Behavior Not Required

Behavior Required

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 11

Do Carrots Really Work? Lift in monthly transaction activity

Source: Case study from financial institutions based in West

1 1

13

4 3

25

0

5

10

15

20

25

Bill Pay Transactions ACH Transactions Debit Card Transactions

Behavior Not Required

Behavior Required

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 12

Popular automatically offers higher rates on existing CDs if customers open additional deposit accounts with qualifying balances. • Average CD balances

60% higher • 50% penetration of

accounts with Checking, Money Market, and Savings

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Build a Foundation for Profitable Growth Back to the Basics

Understand the profitability of your customers.

Develop segmentation schemes that divide customers into useful and actionable

segments based on profitability, demographic, and lifecycle attributes.

Leverage technology, people, and process to execute tactics based on customer

segments.

13

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

• Segmentation provides a framework to group customers together that:

– Behave in a similar way

– Have similar needs, profit clusters, attitudes, and preferences

• Segmentation helps answer questions like: – Who are my best customers?

– What are they like?

– How do they use bank products?

• Why segment?

– Offer more relevant products

– Better understand customer value propositions

– Project customer reaction to change

2. Develop Customer Segments

14

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Overlay External Demographic Data Gain a richer understanding of customer segments

– Financial behavior

– Investment behavior

– Household Income

– Age of Householder

– Family Composition

– Household size

– Presence of children

– Home ownership

– Own/Rent

– Single-family home

– Multi-family dwelling

15

The solution leverages external data, like Nielsen-Claritas P$YCLE lifestage segmentation, to better understand product buying and usage propensities of individual households and customer segments:

Courtesy of the Nielsen Company

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Analysis Output = Product Reconfiguration

• Most banks are re-thinking their products

• Some are already re-positioning and re-pricing

• Old customer value propositions are being tweaked

• New propositions are being developed

• Some trends are emerging...

16

More qualifiers for "free" checking

Customized "build it" accounts

More emphasis on "relationship"

New propositions on savings "discipline"

Renewed focus on electronic channels

Less aggressive debit card rewards

New OD protection or credit offerings

Totally electronic accounts

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Build a Foundation for Profitable Growth Back to the Basics

Understand the profitability of your customers.

Develop segmentation schemes that divide customers into useful and actionable

segments based on profitability, demographic, and lifecycle attributes.

Leverage technology, people, and process to execute tactics based on customer

segments.

17

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Connections Profitability

With CONNECTIONS’ Profitability Analysis, you can determine the net profit of each product, account, household, branch location, and employee portfolio in your institution. CONNECTIONS calculates profitability in an income statement format.

18

Considerations Captures

Each account’s interest income or expense Individual account fees

Cost of funds (loans) Volumes

Earnings credit (deposits) Transactions

Direct and indirect fees

Non-interest expense

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Connections – High Value / Low TCO

Browser Based Solution

Requirements: Computer; Internet; User ID/Password

Integrated with core

Account information automatically updated daily

Interface with non-core systems that house customer information

Wealth Management

Trust/Investments

Mortgage

Insurance

Householding

Updated daily based on address and tax ID

Demographic Data

Appended to each household to build customer profile

Data includes: average age, income, marital status, children, own/rent, etc.

19

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 20

Relationship Management

Sales Management

Marketing Automation

Profitability

Connections

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 21

Profitability

Marketing Relationship /

Product Pricing

An End-to-End Business Strategy

Demo

22

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Profitability Displayed at Customer Level

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Profit Ranking by Deciles Summary

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Profit Ranking by Detail

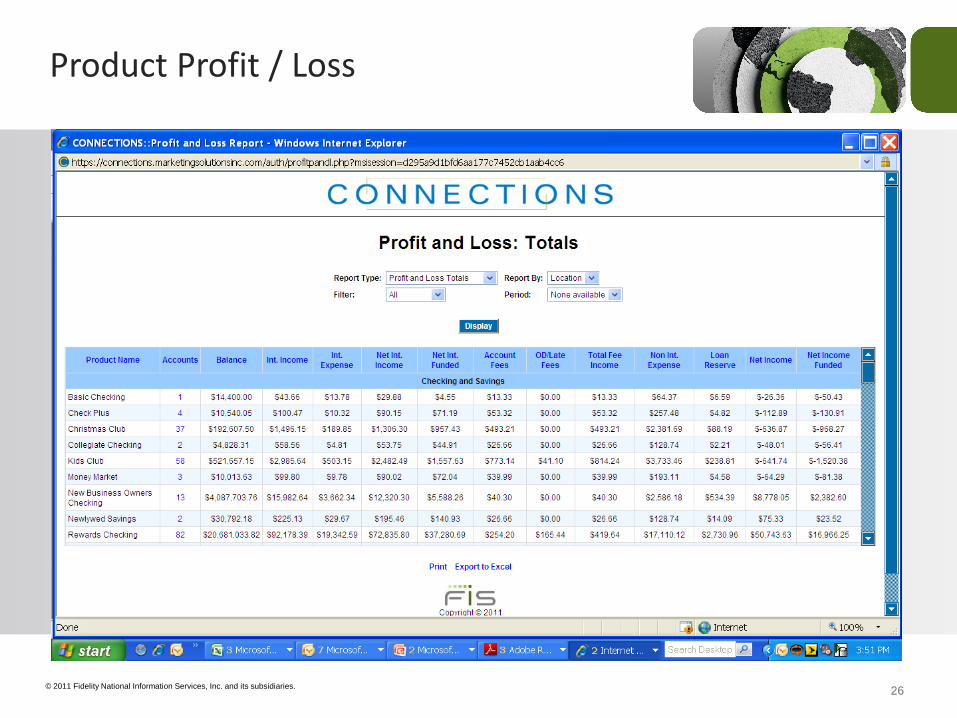

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 26

Product Profit / Loss

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

What-If Modeling

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 28

What-if Modeling – Adding Products

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 29

What-if Modeling – Apply Discount

© 2011 Fidelity National Information Services, Inc. and its subsidiaries.

Surveys

© 2011 Fidelity National Information Services, Inc. and its subsidiaries. 31

Let's Summarize…

• Regulatory and market changes are driving innovation in retail strategy and product offerings.

• Consumer attitudes and expectations are changing and shifting toward value-based offerings.

• To win, banks must better understand the profitability of customers so as to better define actionable business strategies.

• FIS can help!

David Mendoza Senior Business Consultant Sales and Service Solutions FIS 951-789-0425 [email protected] LinkedIn / Keywords: David Mendoza