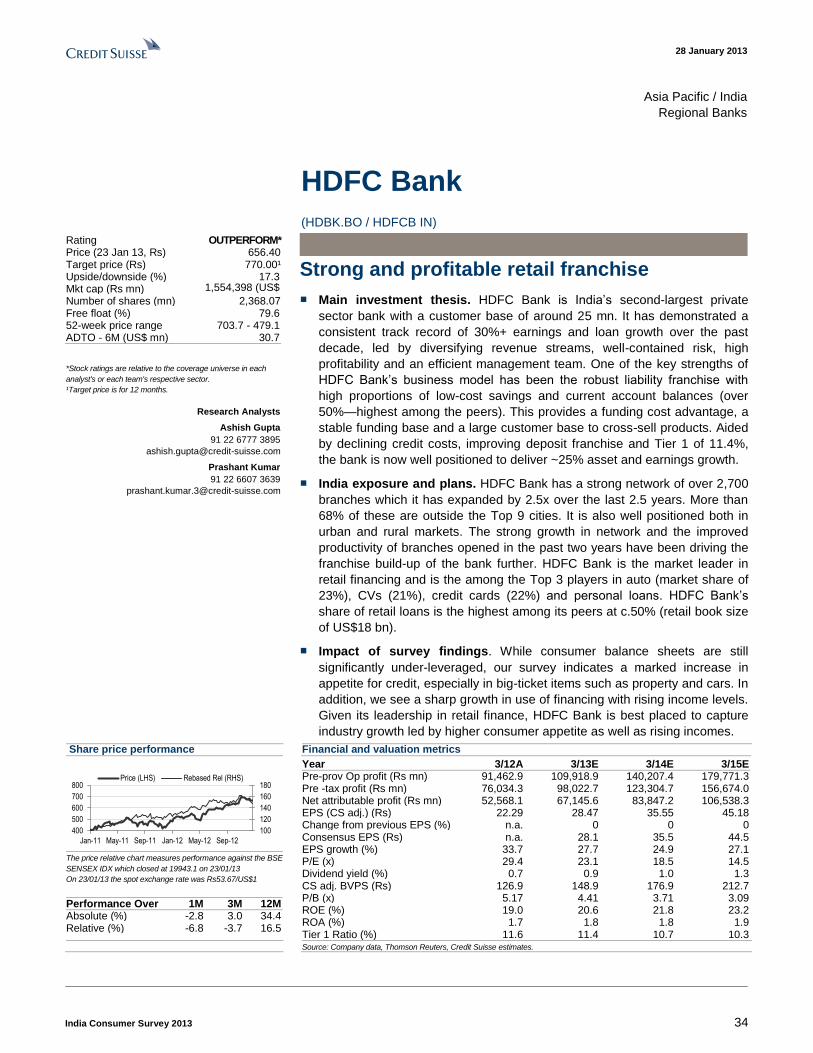

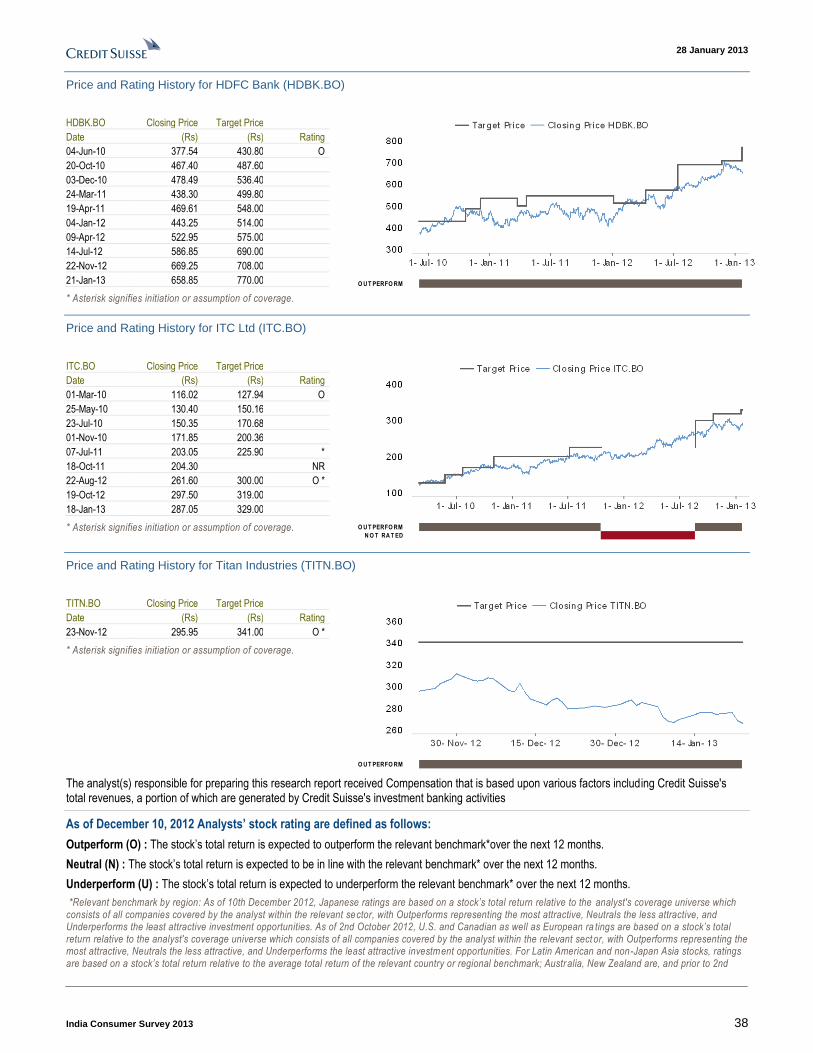

Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

28 January 2013

Asia Pacific/India

Equity Research

Consumer Discretionary / Consumer Staples

India Consumer Survey 2013 THEME

A sum of different parts

Figure 1: Urban mean household income dropped 3%, but rose 6% in rural India

16

17

18

19

20

21

22

Total Urban Rural

Mean monthly household income 2011 ('000 Rs) 2012

Source: Credit Suisse India Consumer Survey 2013

■ Consumer optimism still falling. The decline in Indian consumer optimism

observed in 2011 intensified on the back of continued adverse macro

conditions. Compared to 2011, more people expect lower salary increases

and expect personal finances to worsen, making it a bad time for large-ticket

purchases. Only 5% of consumers we surveyed expect inflation to fall.

Confidence in the government is also waning.

■ Signs of down-trading in discretionary items. Not surprisingly there was

a temporary reversal in 2012 of the up-trading trend observed in 2011. The

preference for purchasing unbranded products again rose. Fewer people

bought smartphones and more now want to buy an entry-level car. This

trend is reflected in the commentary of many companies who operate in

discretionary consumption categories and are indicating a growth slowdown.

■ Rural doing better than urban. Spending patterns show a significant

divergence across rural and urban India. While the mean household income

of urban India declined 3%, it increased 6% in rural India. Car penetration

has stagnated in urban India, but doubled in the past two years in rural.

Monthly ARPU in urban India fell ~15%, but showed a small increase in rural.

■ Low penetration bodes well for long-term growth. Another silver lining for

the long-term growth potential of India is low penetration across categories.

Of the eight countries surveyed, ownership of cars, smartphones and

electronic items is the lowest in India. They are among the lowest

consumers of items, such as beer, spirits, meat and cigarettes. While

spending on education has come off this year, at ~10% of household income

it is still pretty high compared to other countries. This, combined with the

greater participation of rural India and lower income categories, bodes well

for India’s consumption story. Our top picks in the Indian consumption

universe are: ITC, Bajaj Auto, Titan, HDFC Bank and Emami.

Research Analysts

Arnab Mitra

91 22 6777 3806

Akshay Saxena

91 22 6777 3825

28 January 2013

India Consumer Survey 2013 2

Introduction We are delighted to publish the third edition of the Credit Suisse Global Emerging

Consumer Survey and its accompanying Databook. At a time when investor confidence in

the outlook for global growth is improving, it is opportune to review the dynamics and

drivers of what is a key component of the prospects for global growth —the role played by

the consumer in the emerging world. The analysis carried in this report, provides insights

not available from public sources of economic information.

To undertake this project, the Credit Suisse Research Institute has again engaged the

leading global market research firm Nielsen to conduct face to face interviews with over

14,000 consumers across eight emerging economies posing more than 125 questions to

help reflect a granular picture of their spending habits, future intentions and importantly the

factors that influence them.

The 2013 survey has again been refreshed to address new issues—social and

economic—and alongside Brazil, China, India, Indonesia, Russia, Saudi Arabia and

Turkey, we have added South Africa. The detailed analysis of the differing demographic,

income and rural/urban characteristics underlines that these emerging consumers cannot

be viewed in a generic fashion.

Analysts from across the breadth of Credit Suisse’s global research team have drawn out

the key trends and investment conclusions for stocks both in the emerging and developed

world. These are detailed in the pages that follow.

28 January 2013

India Consumer Survey 2013 3

Research analysts Research Analyst Telephone Email

Arnab Mitra 91 22 6777 3806 [email protected]

Akshay Saxena 91 22 6777 3825 [email protected]

Credit Suisse India research team, lead Research Analysts for this report in bold

Ashish Gupta 91 22 6777 3895 [email protected]

Abhishek Bansal 91 22 6777 3968 [email protected]

Akshay Saxena 91 22 6777 3825 [email protected]

Amish Shah 9122 6777 3743 [email protected]

Anantha Narayan 91 22 67773730 [email protected]

Anubhav Aggarwal 9122 6777 3808 [email protected]

Arnab Mitra 91 22 6777 3806 [email protected]

Badrinath Srinivasan 91 22 6777 3715 [email protected]

Chunky Shah 91 22 6777 3872 [email protected]

Ishan Mahanjan 91 22 6777 3839 [email protected]

Jatin Chawla 91 22 6777 3719 [email protected]

Kush Shah 91 22 6777 3862 [email protected]

Neelkanth Mishra 9122 6777 3716 [email protected]

Prashant Kumar 9122 6777 3942 [email protected]

Ravi Shankar 91 22 6777 3869 [email protected]

Sagar Rastogi 91 22 6777 3851 [email protected]

Sanjay Mookim 65 6212 3017 [email protected]

Sunil Tirumalai 91 22 6777 3714 [email protected]

Vikash Patwari 91 22 6777 3747 [email protected]

28 January 2013

India Consumer Survey 2013 4

Focus table and charts Figure 2: Key themes

Themes

1 Consumer

optimism still

falling

Consumers are clearly seeing a lowering of optimism. Few expect inflation to fall and more people are

now postponing their major purchase decisions. Confidence in the government is waning and compared

to the year before people are less confident about salary rises and the state of their personal finances.

Figure 3, p 10-11

2 Down-trading in

discretionary

items

A reversal of the up-trading trend seen before in discretionary items, as people now buy more

unbranded products and there is a fall in mean purchase value across categories, such as apparel,

shoes, etc.

Figure 4, p 12

3 Rural doing better

than urban

A divergence in income and spending patterns between rural and urban India. Be it growth in income or

proliferation of branded goods, car penetration or spending on mobiles—rural has done better than urban

Figure 5, p 13-14

4 Low penetration

bodes well for

long-term growth

India is still among the lowest penetrated of all countries across categories implying high growth

potential. Spending on education is still pretty high with the highest percentage of people wishing to

send children to private schools in India. India continues to build on a solid base to capitalise on the

demographic dividend that bodes well for Indian consumption story

Figure 6, p 15-16

Source: Credit Suisse India Consumer Survey 2013

Figure 3: More people postponing their major purchase

decisions

Figure 4: After a decline last year, the preference for

unbranded goods in discretionary has again risen

0%

10%

20%

30%

40%

50%

% respondents who feelnot a good time to make

major purchase

% expecting personalfinances to get worse

% feeling govt. iseffective in solving

problems

2010 2011 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents buying unbranded in 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Figure 5: While mean household income of urban India

declined 3%, it increased 6% for rural India

Figure 6: India’s penetration across categories much

lower than global average implying high growth potential

16

17

18

19

20

21

22

Total Urban Rural

Mean monthly household income 2011 ('000 Rs) 2012

0 10 20 30 40 50 60

Cars

Cigarettes

LCD TV

Acess to internet

Beer

Spirits

Other countries average India

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 5

Executive summary Equity exposure to the projected growth in consumption in the emerging world has been a

key investment theme in Credit Suisse research for five years now—a megatrend. Our

Global Equity Strategy team again highlighted this in their note, 2013 Outlook: themes,

sectors and styles, structurally the consumption share of GDP still remains low—only

35% in China—and consumers are not hindered by the need to deleverage in the way we

see in the West. Cyclically, the negative impediments of food prices, weak currencies and

global growth are receding while they believe concerns over valuation are overplayed.

However, while common threads of this macro theme do appear throughout the emerging

world, our survey suggests that the consumption theme is by no means uniform in

direction or scope. Hence, investment implications for stocks, sectors and markets can

vary considerably. The survey provides a differentiated input to such decision making.

Key themes

Consumer confidence improving

The survey suggests that, after stalling in 2012, confidence is strengthening—a feature our

macro views would endorse and expect. 37% believe their personal finances will improve

over the next six months while 9% expect some deterioration. This marks a net expected

improvement of 3% points on a like-for-like basis. However, our survey casts a spotlight on

the striking contrasts across the emerging world.

Optimism is strongest and improving in Brazil, China and Indonesia. At the other end of

the scale, the greatest degree of pessimism in financial prospects was recorded in South

Africa, Russia and Turkey (albeit improving). Troubling are the effective “fault lines” that

still seem to exist between rich and poor in some countries. For example, our survey

revealed that nearly as many South Africans (22%) predicted a worse financial position as

those who expected some improvement (28%). We remember—if in a far more extreme

manner—how severe disparity in experience for Egypt stood out in our 2010 survey.

Income trends are the key driver—who has it?

The outlook for and the distribution of income has replaced the influence of food prices as

the determinant of optimism. The countries with the highest income growth expectations

display the greatest optimism—Brazil, Indonesia and Saudi Arabia. Wage expectations

remain relatively depressed in Turkey, Russia and South Africa. However, equally notable

is the fact that the highest income earners are the most optimistic in every country. In

certain countries, that is particularly stark—South Africa and India for example. In contrast,

Brazil reflects far greater equality of expectations.

As much as regional contrasts in the income outlook, age profile within the countries is a

notable differentiator. In a number of countries, the high income consumers are clustered

in the younger age brackets of the working population. China is a stand out example.

Moreover, the incomes are not only higher but are typically growing more rapidly. This

picture is in marked contrast to the West. The drivers at work in the emerging world are

relative educational attainment, urban/rural migration and the necessity of technology

based skill-sets.

28 January 2013

India Consumer Survey 2013 6

Discretionary spending back on track

Understanding what younger, wealthier and typically better educated consumers will

spend their money upon is a key investment theme as this is where growth is likely to be

strongest. This would structurally point to areas of discretionary spending. Our survey

illustrates that this theory is borne out in practice. The survey asks consumers what

categories of spending they have been spending most upon and effectively what they

expect to prioritise looking forward. Having stalled last year, discretionary spending looks

back on track and should maintain its momentum.

In terms of specifics, meat and protein gets a higher profile on the menu. A thirst for

technology, smartphones and tablets, is supported by ever greater expansion in internet

penetration. This was a theme last year and is if anything an even stronger one. Bigger

ticket items such as cars and property also display strong prospects though notably

without the typical appetite for borrowing we have historically seen in the West.

Interestingly, the outlook for services such as healthcare and education seems more

muted. However, it seems the state is increasingly stepping in to supply the former while

private educational spend has simply been exceptionally strong in recent years and seeing

a moderation from a high base. It remains a structural story in our view, with India still

displaying it best of all.

Key discretionary spending plays from our analysts are detailed below. We would

also highlight our custom Delta One Emerging Consumer Discretionary basket,

based on direct and indirect plays ‘CSGLEMDS Index’.

Brand recognition… momentum and critical mass

The track record being built by the survey is allowing us to delve deeper into our analysis

of brands. We can analyse with the help of our Databook brands displaying momentum,

where local brands hold sway over global rivals and the income sensitivity of brands.

Important themes have emerged: (i) the significance of the unbranded segment of

spending; (ii) the resilience of domestic brands in the essential areas of spending space

and their attractiveness to acquisitive global companies; and (iii) the aspirational quality (or

lack thereof) of specific brands in the discretionary space, which plays to the international

names.

With improving income trends being the key driver of the emerging consumer structurally,

and also a key differentiator of the immediate outlook in the survey as suggested above,

we specifically analyse brands with this theme in mind. With high income earners being

where income growth expectations and optimism are the highest, we want to identify

which brands exhibit momentum or dominance in this category. Equally, at the low income

end where a transition from unbranded to branded products is likely, we wish to be

positioned to exploit that. We would be concerned about brands that are losing momentum

and also those whose attractions peter out markedly higher up the income scale given this

is the direction of travel in emerging consumer markets.

The table and scorecard identifies from our brands database, those listed companies

owning brands in emerging markets that either dominate their space or have momentum

with low or high income earners.

We display below those where we have Outperform or Neutral ratings. These form the

constituents of our Custom Delta One Emerging Brands Basket ‘CSEMBRND Index’.

28 January 2013

India Consumer Survey 2013 7

Country highlights

Key highlights include:

Brazil: The beat goes on

The Brazilian consumer remains the most optimistic in our survey, with confidence raised

year-on-year despite an economic slowdown. A definitive characteristic of this confidence

is its breadth; both low and high income consumers are confident, unlike the findings for

many other developing economies. Although an implicit savings ratio seems to have

increased, it remains substantially lower than the other larger economies. Momentum

remains in discretionary products such as technology, fashion and spirits. Education is

also a priority.

China: An educated consumer

Optimism amongst the Chinese consumer remains relatively robust against a weaker

economic background. Much of this increased strength can be attributed to the low income

brackets rather than the high. Attitudes surrounding savings remain unhindered, although

the routes adopted to achieve this are changing; the increased role of the stock market

and life products for savings. The key feature of spending is a heavy focus on technology

and education, with the strongest spend in smartphones out of any country surveyed.

India: A sum of different parts

Although the optimism of the Indian consumer remains robust, there is an increasing

divergence between the confidence levels of rich and poor consumers: poor consumers

demonstrate a sharp decline in confidence. Spending momentum in education continues

to stride ahead, supported by numerous government initiatives. Discretionary spend

categories are the stronger areas within India though appear relatively more mute vs.

other countries, with India in fact being the only country surveyed showing a fall in the

smartphones bought for example. Aggressive promotion of property investment has led to

positive expectations for the direction of property prices.

Indonesia: BRIC becomes BIIC?

The Indonesian consumer continues to grow increasingly confident, corresponding with

the trend growth seen in the Indonesian economy. The increases in minimum wages have

contributed to the relatively steeper growth in confidence amongst the lower earners.

Rising incomes and lowered food prices have resulted in increased spending on

discretionary goods, with fashion and holidays being items of choice. As the vast majority

of Indonesia remains offline, technology growth remains concentrated in basic mobile

phones rather than internet enabled devices such as smartphones.

Russia: The poor BRIC relation

Low optimism, poor income growth and a large disparity between the expectations of rich

and poor consumers characterised Russia in 2012. Inflation rates are forecast to be one of

the highest out of our survey. With a large proportion of income being devoted to food,

Russian consumers have been constrained in spending elsewhere, though this should

ease. At present, only discretionary spend categories in reach of the rich remain robust,

with others on the whole weak. Technology is the strongest feature.

Saudi Arabia: Contrasting fortunes

Although the Saudi Arabian consumer remains one of the most optimistic in our survey,

optimism has dropped relatively year-on-year post 2011’s boost from the major

government initiatives for employment and pay. It remains highly progressive in relation to

incomes. There is high growth in highly penetrated markets, in particular, computers,

smartphones, fashion apparel and perfumes. There remains considerable structural

opportunity for the financial industry to tap into the deep pool of savings which are

currently predominantly held in bank accounts.

28 January 2013

India Consumer Survey 2013 8

South Africa: Challenges and opportunities

South Africa is a new edition to the Credit Suisse Emerging Consumer Survey for 2013.

Consumer optimism levels in South Africa fall toward the lower end of the survey

spectrum. The polarity of experience within the population is concerning. Nearly as many

South African consumers predicted a worse financial position as those who expected

some improvement. Despite broad pay rises for many, it does not appear to have

completely assuaged negative perceptions of the financial outlook of low income earners

which has impacted the pattern of spending and its relative position vs other countries in

the survey. A major distinguishing feature of South Africa is the institutionalised savings

and a more developed banking system.

Turkey: Potential emerging

While optimism is relatively weak compared to other countries in the survey, Turkey has

seen an improvement in overall confidence, with greatest improvement amongst the

higher earners. They are comparable with Saudi Arabia. Spending patterns more generally

are beginning to look like those of a middle-income country, with smartphones, computers,

internet access, cars and holidays seeing some of the strongest gains. Growth in alcohol

spend has not been deterred by recent tax hikes. Bank penetration remains poor,

indicating a structural opportunity.

28 January 2013

India Consumer Survey 2013 9

CS India Consumer Survey 2013 Our comprehensive consumer survey for India interviewed 2,602 respondents across 10

cities and rural areas, and asked more than 100 questions. This report discusses the key

themes and implications for the Indian market.

Consumer optimism still falling The decline in Indian consumer optimism observed last year has further intensified on the

back of continued adverse macro conditions: high inflation and slower growth. Consumers

are clearly more worried. Compared to last year, more people expect lower salary

increases and personal finances to worsen, making it a bad time for large-ticket purchases

this time around. Only 5% of consumers we surveyed expect inflation to fall, clearly

indicating that the Reserve Bank of India’s (RBI) worries over high inflation expectations

becoming entrenched are not unfounded. Confidence in the government is also waning,

with only ~35% respondents believing that it is effective in solving problems against ~50%

the year before. The savings culture remains conservative with most savings channelled

towards banks and gold, etc. With increasing economic uncertainty, Indian consumers’

savings rate, already among the highest in the world, further rose in 2012.

Signs of down-trading in discretionary items Given the economic slowdown, not surprisingly there was a temporary reversal in 2012 of

the up-trading trend observed in 2011. The preference for purchasing unbranded products

again rose this year. Even though more people continued to buy items, such as apparel,

shoes, watches and perfumes, there was a fall in mean purchase values with consumers

preferring to reduce discretionary spending in order to save more. Fewer people bought

smartphones (though mobile penetration went up) and more now want to buy an entry-

level car. More consumers are also postponing major purchase decisions. This trend is

reflected in the commentary of many companies who operate in discretionary consumption

categories and are indicating a slowdown in growth rates.

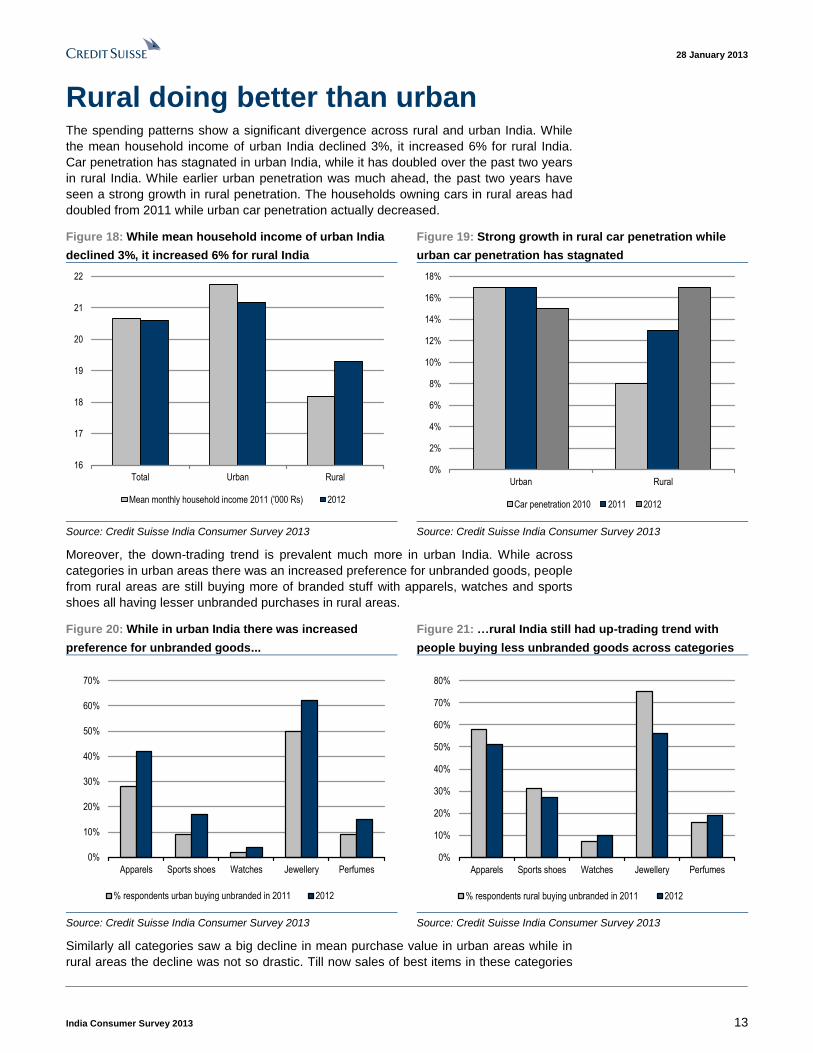

Rural doing better than urban

Spending patterns show a significant divergence across rural and urban India. While the

mean household income of urban India declined 3%, it increased 6% for rural India. Car

penetration has stagnated in urban India, but doubled in the past two years in rural India.

Monthly average revenue per unit (ARPU) on mobile phones for urban India fell ~15%,

while for rural Indians it showed a small increase. Moreover, this down-trading trend is

prevalent much more in urban India. People from rural areas are still buying more branded

products. With India’s rural: urban population ratio still highly skewed at 70:30, strong rural

performance would continue to support growth for Indian consumer companies.

Low penetration bodes well for long-term growth Another silver lining for the long-term growth potential of India is the low penetration

across categories. Of the eight countries surveyed, ownership of cars, smartphones and

electronic items is the lowest in India. They are among the lowest consumers of items,

such as beer, spirits, meat and cigarettes, and have the lowest access to the Internet.

While spending on education has come off this year, at ~10% of household income it is

still pretty high compared to other countries. India has the highest percentage of people

wanting to send children to private schools. Moreover, while falling this year, over a longer

period the nutrient content in dietary patterns is also rising, with more people consuming

meat and dairy products. As a result, India is building a solid base to capitalise on the

demographic dividend that the country is expected to enjoy in the coming decades.

This, combined with the greater participation of rural India and lower income categories

(those at the bottom of pyramid), bodes well for India’s consumption story. We advise

investors to buy brands and market leaders in their respective segments. Our top picks in

the Indian consumption universe are: ITC, Bajaj Auto, Titan, HDFC Bank and Emami.

28 January 2013

India Consumer Survey 2013 10

Consumer optimism still falling In 2011, we observed a fall in the optimism of Indian consumers across most categories.

This year (2012) with continued adverse macro conditions (high inflation and greater

economic uncertainty), consumers have become much more worried. Confidence in the

government is also dropping with just ~35% respondents believing the government is

effective in solving problems against ~50% the year before.

More than 60% of respondents we surveyed expect inflation to increase further and just

~5% expect it to come down in the next 12 months. This is a worrying trend indicating the

high inflation expectations that have been entrenched in people’s minds. Inflation seems to

have hit the lower-income group the hardest with a much higher percentage of rural and

low-income population being concerned about inflation.

Figure 7: Just ~3% of people expect inflation to get lower Figure 8: Confidence in government is coming down

% respondents expecting

inflation to be Higher62%

Expecting inflation to

remain same Same33%

Expecting inflation to be

Lower5%

0

10

20

30

40

50

60

Total Urban Rural

How effective govt. in solving problems 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Just ~30% respondents saw salary hikes in 2012 and the quantum of wage hikes also

came down slightly. On the other hand, income of ~20% respondents came down in 2012.

Consequently fewer people feel this this is a good time to make a major purchase (the

number fell from 73% in 2010 to 66% in 2011 and 59% in 2012).

Figure 9: Only ~30% saw salary increases in 2012 while

~22% of respondents had their salaries fall

Figure 10: More people are postponing purchase

decisions

% whose income

remained same in last one year

44%

Increase34%

Decrease22%

0%

20%

40%

60%

80%

Good Time to make major purchase Not a good time to buy

2010 2011 2011

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 11

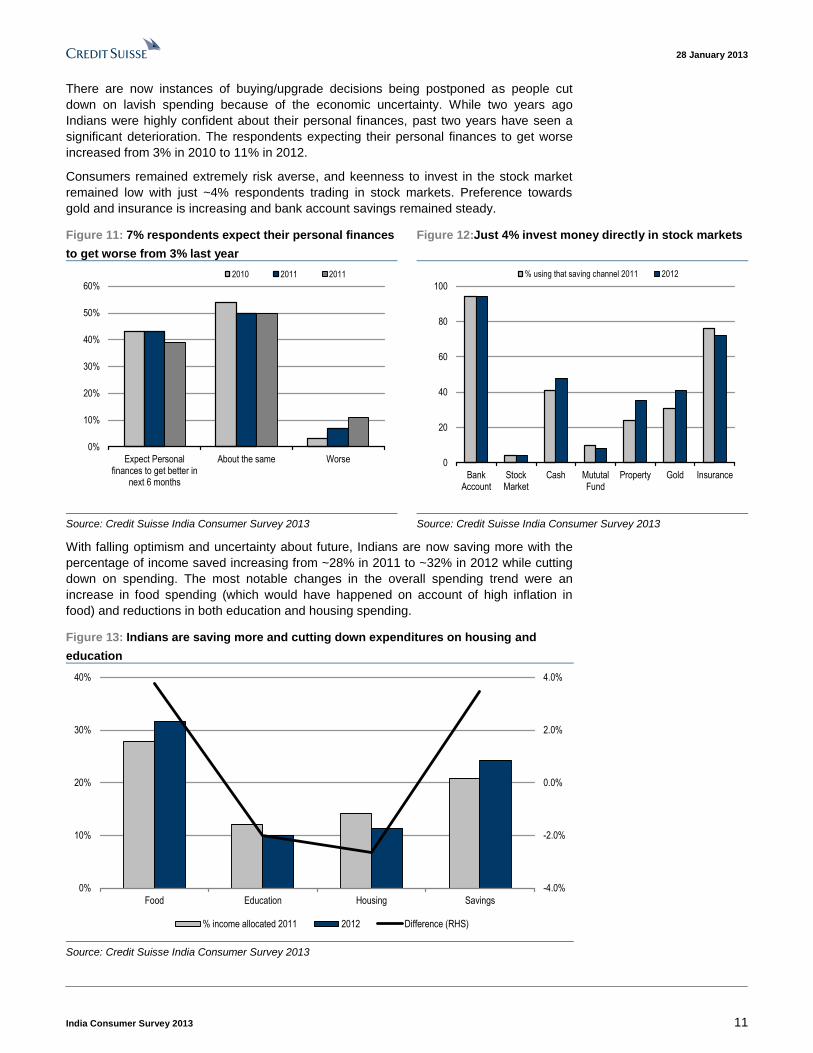

There are now instances of buying/upgrade decisions being postponed as people cut

down on lavish spending because of the economic uncertainty. While two years ago

Indians were highly confident about their personal finances, past two years have seen a

significant deterioration. The respondents expecting their personal finances to get worse

increased from 3% in 2010 to 11% in 2012.

Consumers remained extremely risk averse, and keenness to invest in the stock market

remained low with just ~4% respondents trading in stock markets. Preference towards

gold and insurance is increasing and bank account savings remained steady.

Figure 11: 7% respondents expect their personal finances

to get worse from 3% last year

Figure 12:Just 4% invest money directly in stock markets

0%

10%

20%

30%

40%

50%

60%

Expect Personalfinances to get better in

next 6 months

About the same Worse

2010 2011 2011

0

20

40

60

80

100

BankAccount

StockMarket

Cash MututalFund

Property Gold Insurance

% using that saving channel 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

With falling optimism and uncertainty about future, Indians are now saving more with the

percentage of income saved increasing from ~28% in 2011 to ~32% in 2012 while cutting

down on spending. The most notable changes in the overall spending trend were an

increase in food spending (which would have happened on account of high inflation in

food) and reductions in both education and housing spending.

Figure 13: Indians are saving more and cutting down expenditures on housing and

education

-4.0%

-2.0%

0.0%

2.0%

4.0%

0%

10%

20%

30%

40%

Food Education Housing Savings

% income allocated 2011 2012 Difference (RHS)

Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 12

Signs of down-trading in discretionary items Given the economic slowdown, not surprisingly there was a temporary reversal in 2012 of

up-trading trend observed in the prior years. Even though more people continued to buy

items like apparels, shoes, watches and perfumes, there was a fall in mean purchase

values with consumers preferring to cut down on discretionary spending to save more.

While 2011 survey showed Indian consumer becoming brand conscious, there was a trend

reversal in 2012. Demand for unbranded items after decreasing drastically for each of the

items in 2011 increased again in 2012. While over a two-year period, the preference for

branded products has increased, 2012 saw some slowdown.

Figure 14: Other than jewellery, mean value of purchases

came down for all other categories

Figure 15: After a decline in 2011, preference for

unbranded goods again went up

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Apparels Sports shoes Watches Jewellery Perfumes

Increase in mean spending over last year 2011 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents buying unbranded in 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Fewer people bought smartphones (even though mobile phone penetration went up)

compared with that in 2011. Similarly, while over a longer period there has been a clear

trend towards ‘up-gradation’ in cars (costing more than Rs400,000), more respondents in

our survey wanted to buy an entry level car. All these point to people cutting down on

lavish spending in the wake of economic uncertainty.

Figure 16: No. of people owning smartphones came down Figure 17: More people now want to buy cheaper cars

0%

5%

10%

15%

20%

25%

30%

35%

2010 2011 2012

People not owning mobiles Owning smartphones

0%

10%

20%

30%

40%

50%

2010 2011 2012

% respondents wishing to spend less than Rs400k on car purchase

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 13

Rural doing better than urban The spending patterns show a significant divergence across rural and urban India. While

the mean household income of urban India declined 3%, it increased 6% for rural India.

Car penetration has stagnated in urban India, while it has doubled over the past two years

in rural India. While earlier urban penetration was much ahead, the past two years have

seen a strong growth in rural penetration. The households owning cars in rural areas had

doubled from 2011 while urban car penetration actually decreased.

Figure 18: While mean household income of urban India

declined 3%, it increased 6% for rural India

Figure 19: Strong growth in rural car penetration while

urban car penetration has stagnated

16

17

18

19

20

21

22

Total Urban Rural

Mean monthly household income 2011 ('000 Rs) 2012

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Urban Rural

Car penetration 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Moreover, the down-trading trend is prevalent much more in urban India. While across

categories in urban areas there was an increased preference for unbranded goods, people

from rural areas are still buying more of branded stuff with apparels, watches and sports

shoes all having lesser unbranded purchases in rural areas.

Figure 20: While in urban India there was increased

preference for unbranded goods...

Figure 21: …rural India still had up-trading trend with

people buying less unbranded goods across categories

0%

10%

20%

30%

40%

50%

60%

70%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents urban buying unbranded in 2011 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents rural buying unbranded in 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Similarly all categories saw a big decline in mean purchase value in urban areas while in

rural areas the decline was not so drastic. Till now sales of best items in these categories

28 January 2013

India Consumer Survey 2013 14

were restricted to urban India. However, now with most big retail brands opening up shops

in Tier 2 and 3 cities, the difference in purchasing preferences is coming down as even the

people in rural India are willing to try out the more fashionable and expensive goods.

Figure 22: Mean purchase values came down much more

in urban areas than rural; greater down-trading in urban

Figure 23: Mobile ARPU for urban consumer declined

15%; for rural consumer showed a small increase

-40%

-20%

0%

20%

40%

Apparels Sports shoes Watches Jewellery Perfumes

Increase in mean spending for Urban over last year Rural

200

250

300

350

400

450

Total Urban Rural

Mean monthly mobile bill 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Computer penetration per household increased from ~0.2 to ~0.3 in rural areas while it

was stable in urban. All the above point to that while 2012 saw a big decline in consumer

sentiment in urban India, rural India remained relatively buoyant and growing fast. With the

rural-to-urban population ratio in India still highly skewed at 70:30, strong rural

performance would continue to support growth for Indian consumer companies.

Figure 24: Mean computers per household saw a

significant jump in rural while was flat in urban

Figure 25: Rural:urban population ratio at 70:30, so rural

doing better bodes well for the Indian consumption story

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Rural Urban

Mean computers per household 2011 2012

Rural68%

Urban32%

Source: Credit Suisse India Consumer Survey 2013 Source: Census India 2011

28 January 2013

India Consumer Survey 2013 15

Low penetration bodes well for long-term growth Another silver lining for the long-term growth potential is low penetration in India across

categories. Out of all the eight countries surveyed, ownership of cars, smartphones and

electronic items is the lowest in India. They are among the lowest consumers of items like

beer, spirits, meat, cigarettes and LCD TVs, and have the lowest access to Internet.

Figure 26: Fewest Indians own cars... Figure 27: …and fewest people have Internet access

0

20

40

60

80

100

Brazil China India Indonesia Russia Saudi Turkey SouthAfrica

% respondents owning cars

0

20

40

60

80

100

Brazil China India Indonesia Russia Saudi Turkey SouthAfrica

% respondents with access to internet

Source Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Figure 28: Cigarette penetration is the lowest... Figure 29: …and so is alcohol penetration

0

10

20

30

40

50

60

Brazil China India Indonesia Russia Saudi Turkey SouthAfrica

% of cigarette smokers

0 10 20 30 40 50 60 70 80

Brazil

China

India

Russia

Turkey

SA

% of Spirits consumers % of beer drinkers

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

While the spending on education came off in 2012, at ~10% of household income it is still

pretty high and compares favourably to other countries. India has the highest percentage

of people who want to send their children to private schools. Moreover, while there was a

drop in 2012, over a longer period the nutrient content in the dietary patterns is also going

up with more and more consuming meat and dairy products, meaning that India is building

a solid base to capitalise on the demographic dividend that the country is expected to

enjoy in the coming decades.

28 January 2013

India Consumer Survey 2013 16

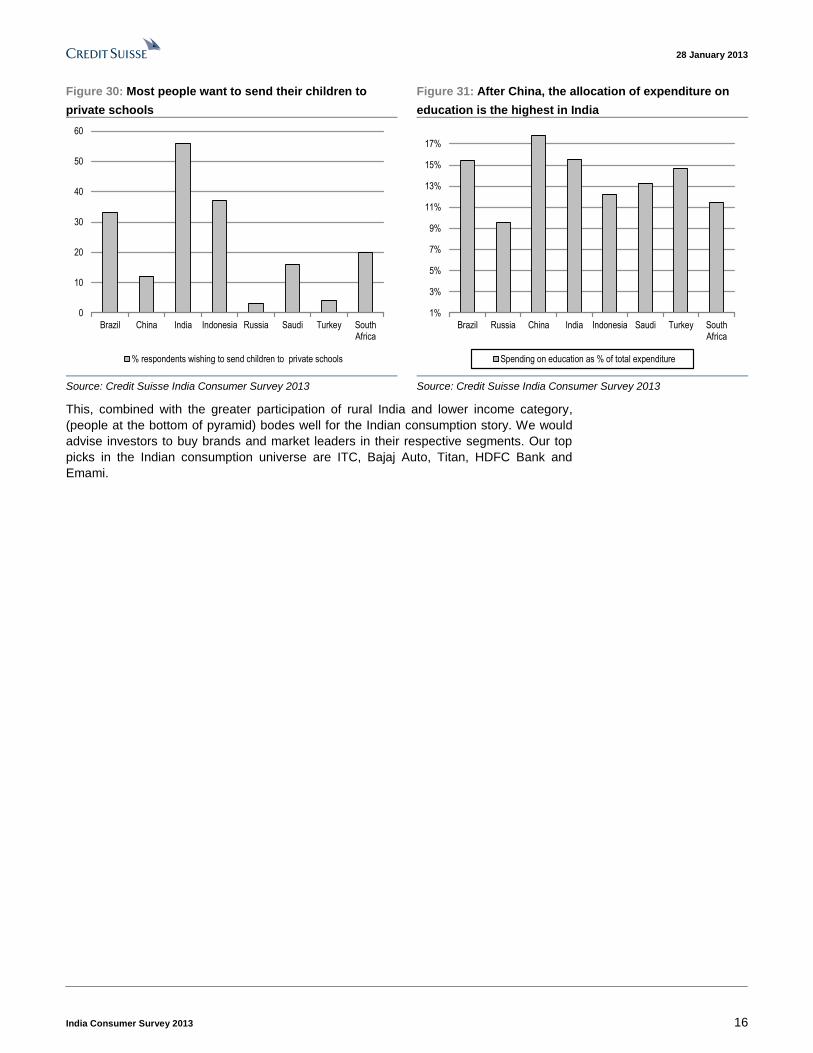

Figure 30: Most people want to send their children to

private schools

Figure 31: After China, the allocation of expenditure on

education is the highest in India

0

10

20

30

40

50

60

Brazil China India Indonesia Russia Saudi Turkey SouthAfrica

% respondents wishing to send children to private schools

1%

3%

5%

7%

9%

11%

13%

15%

17%

Brazil Russia China India Indonesia Saudi Turkey SouthAfrica

Spending on education as % of total expenditure

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

This, combined with the greater participation of rural India and lower income category,

(people at the bottom of pyramid) bodes well for the Indian consumption story. We would

advise investors to buy brands and market leaders in their respective segments. Our top

picks in the Indian consumption universe are ITC, Bajaj Auto, Titan, HDFC Bank and

Emami.

28 January 2013

India Consumer Survey 2013 17

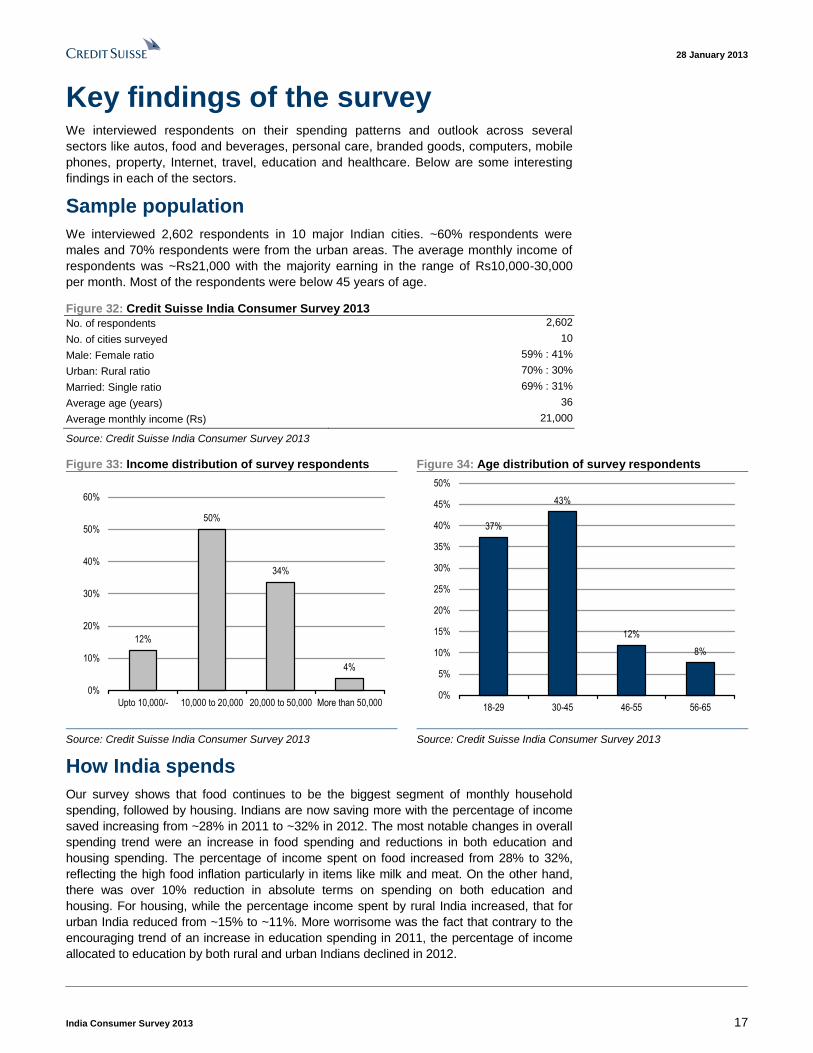

Key findings of the survey We interviewed respondents on their spending patterns and outlook across several

sectors like autos, food and beverages, personal care, branded goods, computers, mobile

phones, property, Internet, travel, education and healthcare. Below are some interesting

findings in each of the sectors.

Sample population

We interviewed 2,602 respondents in 10 major Indian cities. ~60% respondents were

males and 70% respondents were from the urban areas. The average monthly income of

respondents was ~Rs21,000 with the majority earning in the range of Rs10,000-30,000

per month. Most of the respondents were below 45 years of age.

Figure 32: Credit Suisse India Consumer Survey 2013

No. of respondents 2,602

No. of cities surveyed 10

Male: Female ratio 59% : 41%

Urban: Rural ratio 70% : 30%

Married: Single ratio 69% : 31%

Average age (years) 36

Average monthly income (Rs) 21,000

Source: Credit Suisse India Consumer Survey 2013

Figure 33: Income distribution of survey respondents Figure 34: Age distribution of survey respondents

12%

50%

34%

4%

0%

10%

20%

30%

40%

50%

60%

Upto 10,000/- 10,000 to 20,000 20,000 to 50,000 More than 50,000

37%

43%

12%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

18-29 30-45 46-55 56-65

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

How India spends

Our survey shows that food continues to be the biggest segment of monthly household

spending, followed by housing. Indians are now saving more with the percentage of income

saved increasing from ~28% in 2011 to ~32% in 2012. The most notable changes in overall

spending trend were an increase in food spending and reductions in both education and

housing spending. The percentage of income spent on food increased from 28% to 32%,

reflecting the high food inflation particularly in items like milk and meat. On the other hand,

there was over 10% reduction in absolute terms on spending on both education and

housing. For housing, while the percentage income spent by rural India increased, that for

urban India reduced from ~15% to ~11%. More worrisome was the fact that contrary to the

encouraging trend of an increase in education spending in 2011, the percentage of income

allocated to education by both rural and urban Indians declined in 2012.

28 January 2013

India Consumer Survey 2013 18

Figure 35: Food constitutes the biggest segment of the

monthly household spending

Figure 36: Indians are now saving more; spending on

food also increased

Housing11%

Auto6%

Education10%

Food32%Home &

Personal Care6%

Healthcare6%

Savings24%

Entertainment5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2010 2011 2012

% income spent on Food % of income saved

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Figure 37: Spending on housing fell in urban India… Figure 38: …while spending on education fell overall

0%

4%

8%

12%

16%

20%

Rural Urban

% spent on housing in 2010 2011 2012

0%

4%

8%

12%

16%

Rural Urban

% spent on education in 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

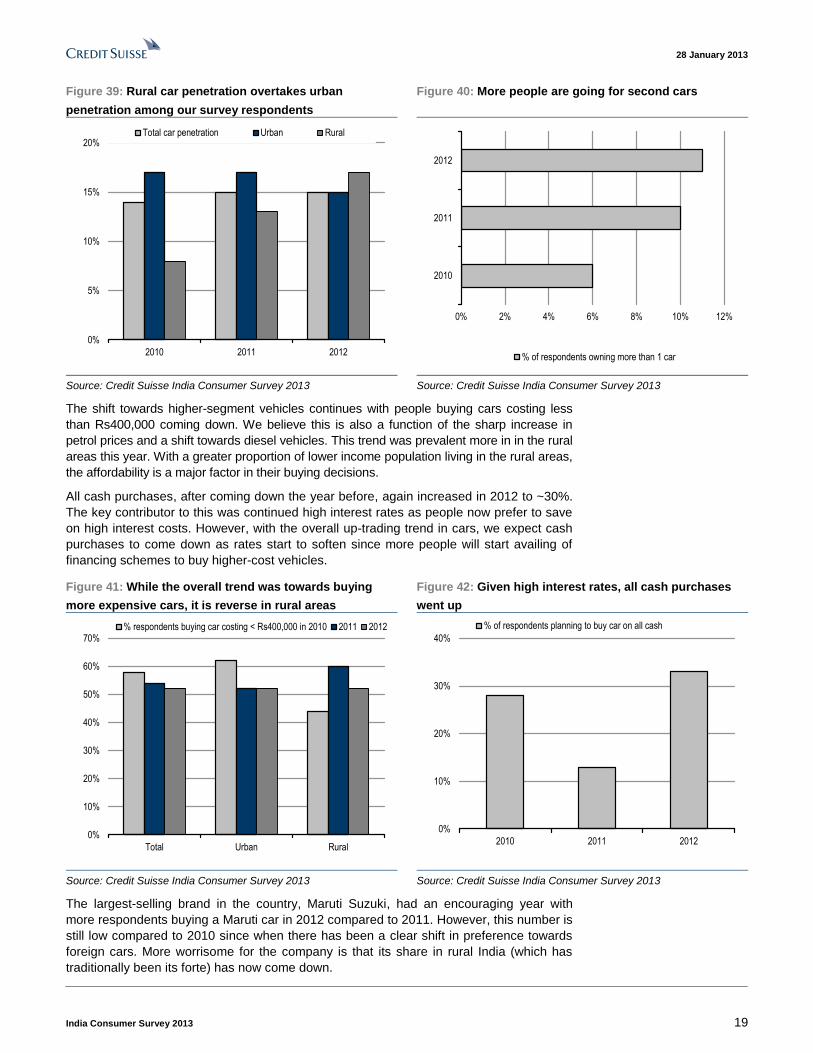

Autos

India has among the world’s most under-penetrated car market with less than 15% of the

people in our survey owning cars (actual household penetration stands much lower at just

~7%). Among the respondents in our survey, rural penetration has now crossed urban

penetration. While earlier urban penetration was double that of rural, the past two years

have seen strong growth in rural penetration. Households owning cars in rural areas had

doubled from 2011. On the other hand, urban penetration went down, which seems to

indicate that with rising fuel costs people in cities are using more public transport. A similar

pattern is observed in two-wheelers. Among the respondents in our survey, ~70% of

households own a two-wheeler much higher than the Indian average of ~30% with more

people in rural areas owning a two-wheeler than in urban areas. In reality, the gap

between rural and urban penetration is much less in two-wheelers than in four-wheelers.

People owning multiple cars went up from 6% to 11% indicating more members in

households need individual cars for their daily travel.

28 January 2013

India Consumer Survey 2013 19

Figure 39: Rural car penetration overtakes urban

penetration among our survey respondents

Figure 40: More people are going for second cars

0%

5%

10%

15%

20%

2010 2011 2012

Total car penetration Urban Rural

0% 2% 4% 6% 8% 10% 12%

2010

2011

2012

% of respondents owning more than 1 car

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

The shift towards higher-segment vehicles continues with people buying cars costing less

than Rs400,000 coming down. We believe this is also a function of the sharp increase in

petrol prices and a shift towards diesel vehicles. This trend was prevalent more in in the rural

areas this year. With a greater proportion of lower income population living in the rural areas,

the affordability is a major factor in their buying decisions.

All cash purchases, after coming down the year before, again increased in 2012 to ~30%.

The key contributor to this was continued high interest rates as people now prefer to save

on high interest costs. However, with the overall up-trading trend in cars, we expect cash

purchases to come down as rates start to soften since more people will start availing of

financing schemes to buy higher-cost vehicles.

Figure 41: While the overall trend was towards buying

more expensive cars, it is reverse in rural areas

Figure 42: Given high interest rates, all cash purchases

went up

0%

10%

20%

30%

40%

50%

60%

70%

Total Urban Rural

% respondents buying car costing < Rs400,000 in 2010 2011 2012

0%

10%

20%

30%

40%

2010 2011 2012

% of respondents planning to buy car on all cash

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

The largest-selling brand in the country, Maruti Suzuki, had an encouraging year with

more respondents buying a Maruti car in 2012 compared to 2011. However, this number is

still low compared to 2010 since when there has been a clear shift in preference towards

foreign cars. More worrisome for the company is that its share in rural India (which has

traditionally been its forte) has now come down.

28 January 2013

India Consumer Survey 2013 20

Figure 43: Preference for Maruti cars increased over 2011

but is still down since 2010

Figure 44: No. of people wish to buy Maruti in future

increased slightly

0%

10%

20%

30%

40%

50%

60%

Total Urban Rural

% of respondents buying Maruti Suzuki in 2010 2011 2012

0%

10%

20%

30%

40%

50%

2010 2011 2012

% of respondents likely to buy Maruti Suzuki in future

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Food and beverages

Eating and drinking habits in India have traditionally been influenced by cultural factors

rather than affordability. Overall, alcohol and meat consumption in India is very low. In our

survey, ~30% of people were vegetarians (with a significant percentage of meat-eaters

restricting meat consumption to less than 10% of the total intake). Similarly less than 10%

respondents consumed alcohol.

Compared to 2011 when there was an increase in meat-eaters, 2012 saw a decline, which

was larger in rural areas (the proportion of meat-eaters in rural areas decreased from 77%

to 54%). This was probably driven by lower affordability of meat as there has been quite a

big increase in meat prices over the course of 2011. Demand for spirits broadly remained

stable as there was no change in the number of alcohol consumers. Over the long term,

we believe the trend in 2012 will reverse and there will be a steady increase in both meat-

eaters and alcohol consumers as the present generation gives lesser importance to older

traditions and wants to try out new things.

Figure 45: Demand for meat is down driven by rural Figure 46: No. of alcohol consumers remained stable

40%

50%

60%

70%

80%

Total Urban Rural

% of meat-eaters in 2010 2011 2012

0% 2% 4% 6% 8%

2010

2011

2012

Alcohol Consumers

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 21

The usage of dairy products remains encouraging. More than 90% respondents consume

dairy products and this number remained stable versus 2011. However, like meat,

respondents are worried about high inflation in milk and few of them want to spend more

on milk in future compared to 2011. All the items—meat, eggs and milk—saw large price

increases in 2012. With price moderation, the intake of meat and milk should remain

robust as people get conscious about the nutrient content in their diet.

Figure 47: People will spend less on dairy products... Figure 48:…and meat due to high inflation

40%

50%

60%

70%

80%

2010 2011 2012

Expecting to spend more on dairy products in future

0% 5% 10% 15% 20% 25% 30%

2010

2011

2012

Expecting to consume more meat in future

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Just ~10% of respondents smoke cigarettes in India with penetration being slightly higher

in rural (12% in rural versus 10% in urban). India’s cigarette potential stands quite low

compared to that of other emerging countries indicating high growth potential.

Figure 49: India’s cigarette penetration stands at 10%... Figure 50: …much less compared to other countries

6% 8% 10% 12% 14%

Total

Urban

Rural

% of cigarette smokers

0%

10%

20%

30%

40%

50%

60%

Brazil China Indonesia India Russia

% of cigarette smokers

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 22

Personal care

Use of personal care products is also on an upswing in all categories and across most

segments. Among our survey respondents, the usage of skincare products is quite high

with more than 90% of them using such products. This number has risen significantly over

the past two years. Moreover, many respondents are willing to spend considerably more

on personal care products in the future, indicating that people are getting much more

conscious of their looks and hygiene. Not surprisingly, higher-income people are using

more of these products, though this trend is visible across most segments.

Figure 51: Usage of personal care products going up significantly

50%

60%

70%

80%

90%

% respondents who spent on skin care products in last 3months

% expecting to spend more on these products in future

2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013

Luxury goods

Nearly all categories of luxury goods (fashion apparel, shoes, watches, jewellery and

perfumes) saw an increase in demand with a greater percentage of respondents reporting

having bought these goods recently as compared to those in 2011. Of the total money

spent on these luxury goods, jewellery still remains by far the biggest across income

categories. Indians have typically been large consumers of gold (predominantly in the

jewellery form) for both consumption and investment purposes.

Figure 52: Jewellery still remains by far the largest category

9% 8% 10% 8% 8% 9% 10% 11% 10%

8% 8%9%

7% 8% 8% 8% 7% 7%

9% 7%10%

8% 10% 10% 9% 11%8%

70% 72%64%

71% 70% 69% 69% 68% 72%

4% 5% 6% 5% 4% 4% 4% 4% 4%

0%

20%

40%

60%

80%

100%

Overall Up to 7500/- Rs. 7501to10000/-

Rs. 10001 to15000/-

Rs. 15001 to20000/-

Rs. 20001 to30000/-

Rs. 30001 to40000/-

Rs. 40001 to50000/-

More thanRs.50000/-

Proportion spent on Apparels Sports shoes Watches Jewellery Perfumes

Source Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 23

However, the mean value of purchase went down in each category other than jewellery.

This is exactly opposite of 2011 which saw people buying more expensive items.

The increase in purchase price of jewellery was solely due to a huge rise in gold prices.

Given that prices would have increased across other categories, it means that while more

people are buying these goods, they are also buying the cheaper ones. There is down-

trading happening with consumers buying lower-end products as they cut down on

discretionary spending to save more in this adverse macroeconomic environment.

Figure 53: More people are buying luxury goods... Figure 54: …but the value of purchases went down

0%

10%

20%

30%

40%

50%

60%

70%

80%

FashionApparel

Sports shoes Watches Jewellery Perfumes

% respondents spending on these products in 2010 2011 2012

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Apparels Sports shoes Watches Jewellery Perfumes

Increase in mean spending over last year 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

The down-trading trend was more prevalent in urban areas than in rural. All categories

saw a big decline in the mean purchase value in urban areas while it was not so drastic in

rural. Till now sales of best items in these categories were restricted to urban India.

However, now with the most big retail brands opening up shops in Tier 2 and 3 cities, the

difference in purchasing preferences is coming down with even the rural consumers willing

to try out more fashionable and expensive goods.

We note that consumers especially those in the lower-income category continue to be

price conscious about the higher-ticket items like jewellery, watches and perfumes. While

their mean spending on lower-ticket basic items like apparel and shoes is increasing, it

actually went down for more expensive accessories like watches and jewellery.

Figure 55: While rural people are spending less... Figure 56: …down-trading trend prevalent more in urban

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Apparels Sports shoes Watches Jewellery Perfumes

Increase in mean spending for Rural over last year 2011 2012

-40%

-30%

-20%

-10%

0%

10%

20%

Apparels Sports shoes Watches Jewellery Perfumes

Increase in mean spending for Urban over last year 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 24

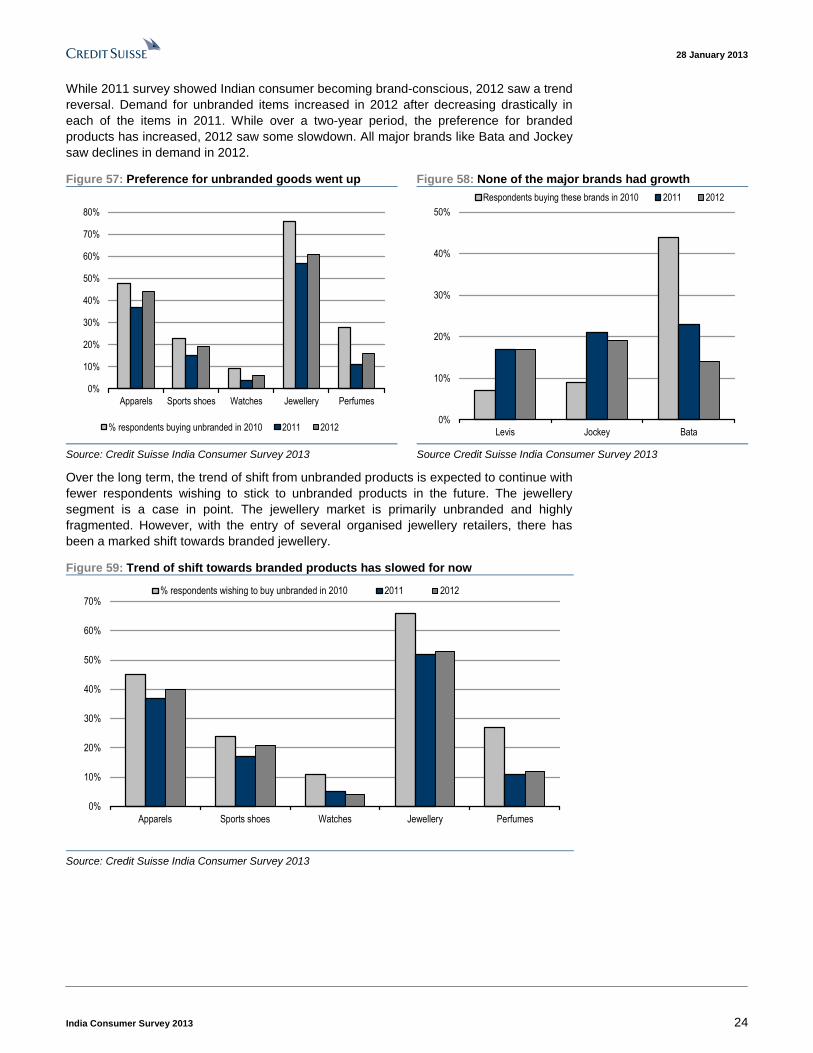

While 2011 survey showed Indian consumer becoming brand-conscious, 2012 saw a trend

reversal. Demand for unbranded items increased in 2012 after decreasing drastically in

each of the items in 2011. While over a two-year period, the preference for branded

products has increased, 2012 saw some slowdown. All major brands like Bata and Jockey

saw declines in demand in 2012.

Figure 57: Preference for unbranded goods went up Figure 58: None of the major brands had growth

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents buying unbranded in 2010 2011 2012

0%

10%

20%

30%

40%

50%

Levis Jockey Bata

Respondents buying these brands in 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source Credit Suisse India Consumer Survey 2013

Over the long term, the trend of shift from unbranded products is expected to continue with

fewer respondents wishing to stick to unbranded products in the future. The jewellery

segment is a case in point. The jewellery market is primarily unbranded and highly

fragmented. However, with the entry of several organised jewellery retailers, there has

been a marked shift towards branded jewellery.

Figure 59: Trend of shift towards branded products has slowed for now

0%

10%

20%

30%

40%

50%

60%

70%

Apparels Sports shoes Watches Jewellery Perfumes

% respondents wishing to buy unbranded in 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 25

Electronic goods

Penetration of most electronic goods remains low in the country and replacement/

upgradation of these happens after a much longer time compared to that in other countries.

Hence very few respondents have purchased these items over the past 12 months.

Moreover, the purchases were skewed towards lower-priced items like desktop PCs.

Figure 60: Buying electronic goods still remains low

0

2

4

6

8

10

Computer Camera DVD player Smart Phone LCD TV Notebook

% respondents who bought these products last year Likely to buy in near future

Source: Credit Suisse India Consumer Survey 2013

In the cable TV, penetration of DTH (direct to home) remains low. Moreover, people

expecting to shift to DTH/cable are less now than in 2011. There is no incentive to shift to

DTH and high prices deter customers from making the shift.

Figure 61: DTH penetration is still low Figure 62: Fewer people are willing to shift to DTH

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

DTH (direct-to-home) Cable Television

% people with access to cable/ DTH 2011 2012

0%

10%

20%

30%

40%

50%

60%

70%

% people expecting shift to DTH Cable Television

2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 26

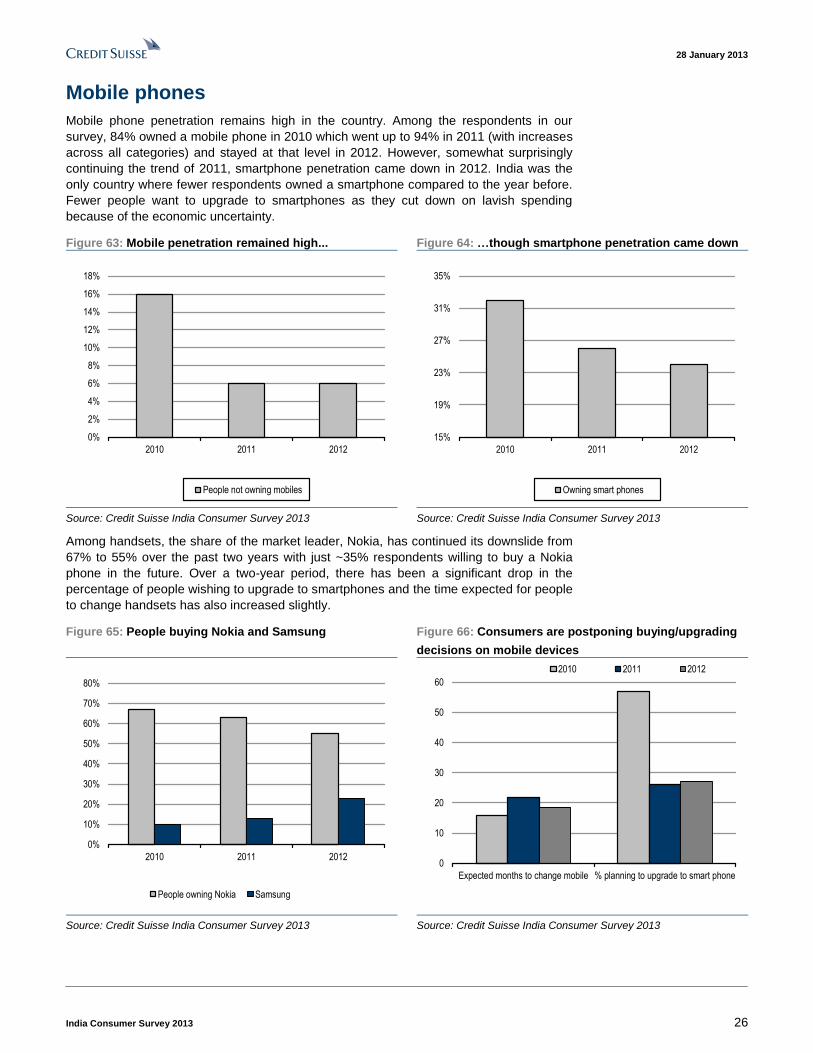

Mobile phones

Mobile phone penetration remains high in the country. Among the respondents in our

survey, 84% owned a mobile phone in 2010 which went up to 94% in 2011 (with increases

across all categories) and stayed at that level in 2012. However, somewhat surprisingly

continuing the trend of 2011, smartphone penetration came down in 2012. India was the

only country where fewer respondents owned a smartphone compared to the year before.

Fewer people want to upgrade to smartphones as they cut down on lavish spending

because of the economic uncertainty.

Figure 63: Mobile penetration remained high... Figure 64: …though smartphone penetration came down

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2010 2011 2012

People not owning mobiles

15%

19%

23%

27%

31%

35%

2010 2011 2012

Owning smart phones

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Among handsets, the share of the market leader, Nokia, has continued its downslide from

67% to 55% over the past two years with just ~35% respondents willing to buy a Nokia

phone in the future. Over a two-year period, there has been a significant drop in the

percentage of people wishing to upgrade to smartphones and the time expected for people

to change handsets has also increased slightly.

Figure 65: People buying Nokia and Samsung Figure 66: Consumers are postponing buying/upgrading

decisions on mobile devices

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012

People owning Nokia Samsung

0

10

20

30

40

50

60

Expected months to change mobile % planning to upgrade to smart phone

2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 27

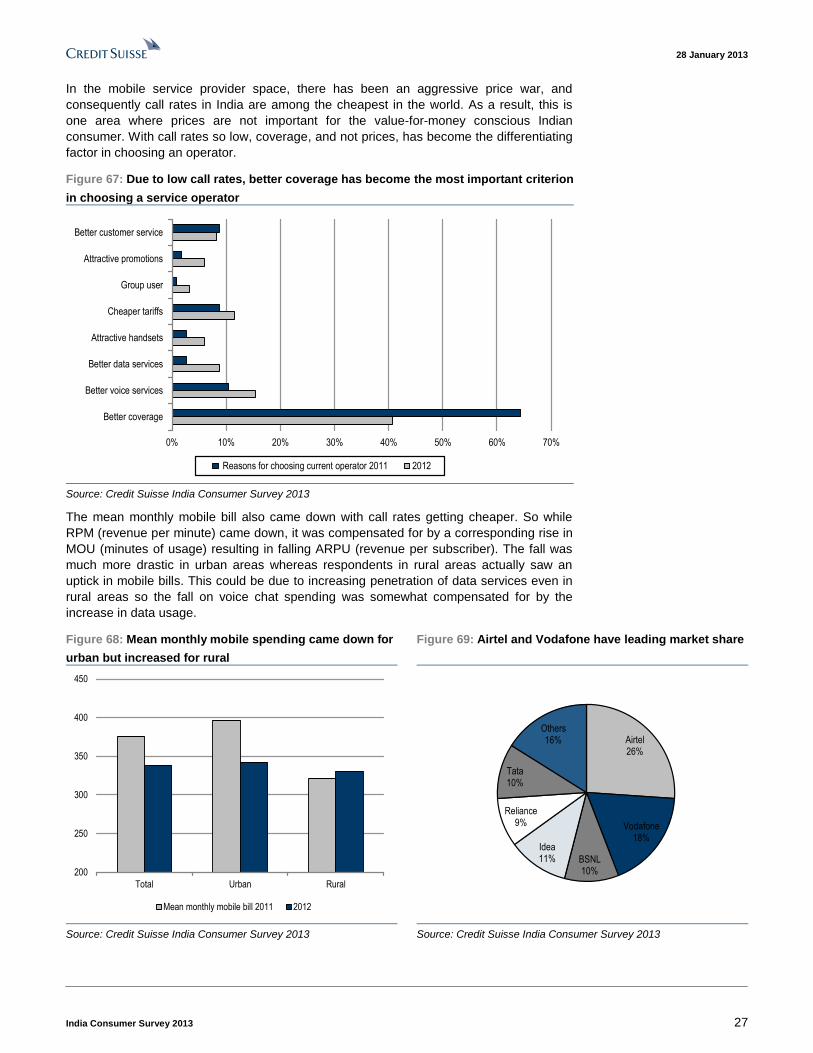

In the mobile service provider space, there has been an aggressive price war, and

consequently call rates in India are among the cheapest in the world. As a result, this is

one area where prices are not important for the value-for-money conscious Indian

consumer. With call rates so low, coverage, and not prices, has become the differentiating

factor in choosing an operator.

Figure 67: Due to low call rates, better coverage has become the most important criterion

in choosing a service operator

0% 10% 20% 30% 40% 50% 60% 70%

Better coverage

Better voice services

Better data services

Attractive handsets

Cheaper tariffs

Group user

Attractive promotions

Better customer service

Reasons for choosing current operator 2011 2012

Source: Credit Suisse India Consumer Survey 2013

The mean monthly mobile bill also came down with call rates getting cheaper. So while

RPM (revenue per minute) came down, it was compensated for by a corresponding rise in

MOU (minutes of usage) resulting in falling ARPU (revenue per subscriber). The fall was

much more drastic in urban areas whereas respondents in rural areas actually saw an

uptick in mobile bills. This could be due to increasing penetration of data services even in

rural areas so the fall on voice chat spending was somewhat compensated for by the

increase in data usage.

Figure 68: Mean monthly mobile spending came down for

urban but increased for rural

Figure 69: Airtel and Vodafone have leading market share

200

250

300

350

400

450

Total Urban Rural

Mean monthly mobile bill 2011 2012

Airtel26%

Vodafone18%

BSNL10%

Idea11%

Reliance9%

Tata10%

Others16%

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 28

Education

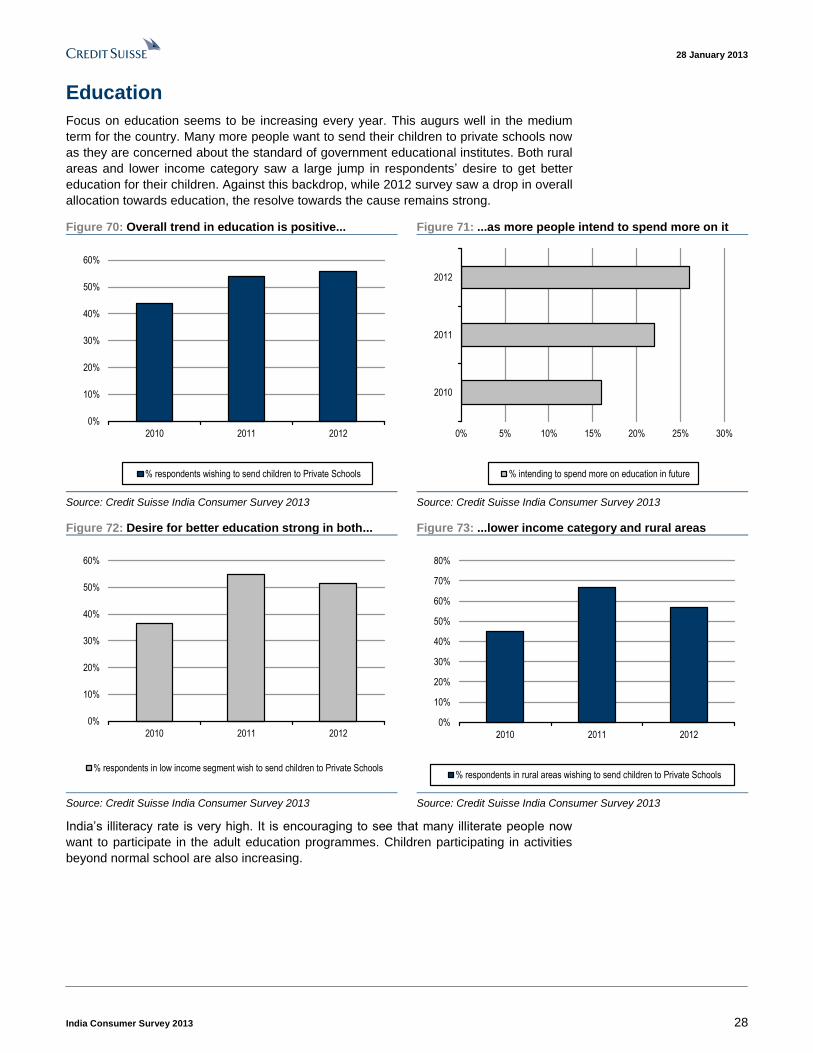

Focus on education seems to be increasing every year. This augurs well in the medium

term for the country. Many more people want to send their children to private schools now

as they are concerned about the standard of government educational institutes. Both rural

areas and lower income category saw a large jump in respondents’ desire to get better

education for their children. Against this backdrop, while 2012 survey saw a drop in overall

allocation towards education, the resolve towards the cause remains strong.

Figure 70: Overall trend in education is positive... Figure 71: ...as more people intend to spend more on it

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012

% respondents wishing to send children to Private Schools

0% 5% 10% 15% 20% 25% 30%

2010

2011

2012

% intending to spend more on education in future

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Figure 72: Desire for better education strong in both... Figure 73: ...lower income category and rural areas

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012

% respondents in low income segment wish to send children to Private Schools

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012

% respondents in rural areas wishing to send children to Private Schools

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

India’s illiteracy rate is very high. It is encouraging to see that many illiterate people now

want to participate in the adult education programmes. Children participating in activities

beyond normal school are also increasing.

28 January 2013

India Consumer Survey 2013 29

Figure 74: High no. of people still want adult education Figure 75: Participation in extra activities is increasing

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012

% of respondents in rural taking adult continuation education

0% 10% 20% 30% 40%

2010

2011

2012

Children participating in activities outside normal courses

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Travel

Holiday is predominantly limited to domestic destinations in India. There was even greater

preference for domestic tourist destinations this time around. Previous year’s trend of a

higher proportion of respondents in rural areas going on holidays reversed this time

around. Rural people going on holiday went down while that in urban increased.

Air travel is still an under-penetrated category in India and respondents using air travel

remained low (as air fares went up), but those using road travel (car/bus) went up. This is

another sign that people are cutting down on lavish spending.

Figure 76: Penetration of air travel remained low Figure 77: Preference for domestic tourism went up

0%

10%

20%

30%

40%

50%

60%

Car Bus Train Aeroplane

% respondents using particular mode in 2010 2011 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Home Domestic touristdestination

International

Holiday destination 2010 2011 2012

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Internet

Just 24% of respondents surveyed had access to Internet (actual Internet penetration is

even lower at ~10%). While the overall number is similar to that in 2011, Internet users

increased significantly in higher-income categories. However, India is still far behind other

emerging countries. E-commerce is also on an upward trajectory in India, with

respondents using Internet for online shopping going up in almost all the categories like

books, electronics and clothes.

28 January 2013

India Consumer Survey 2013 30

Figure 78: Only ~24% have access to Internet, though this

is increasing especially in higher-income categories

Figure 79: Internet penetration still low in country

17% 19%24%

83% 81%76%

0%

20%

40%

60%

80%

100%

2010 2011 2012

% repondents with access to internet No access to internet

76

70

24

9

71

86

51

0

20

40

60

80

100

Brazil China India Indonesia Russia Saudi Turkey

Internet Penetration

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Healthcare

The state of healthcare is quite poor in the country primarily due to under-investment by

government especially in the rural areas. Less than 40% of respondents have access to

free healthcare from state which, though an improvement over the past two years, is still

very low. Patients largely pay out from their own pockets. About ~34% of respondents

were regular purchasers of medicines implying that they had chronic problems (regular

medicines required like in diabetes). The share of medicines for acute diseases stands

much higher at 66% (actual chronic: acute ratio is 25:75)

Figure 80: Despite a steady increase, less than 34% of

patients have access to healthcare from state

Figure 81: Respondents who are regular purchasers of

medicines (chronic problems) constitute 34%

0%

10%

20%

30%

40%

50%

Total Urban Rural

Access to free health-care from state 2010 2011 2012

Regular purchaser

of medicine (Chronic

problems)34%

Not regular purchaser

66%

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 31

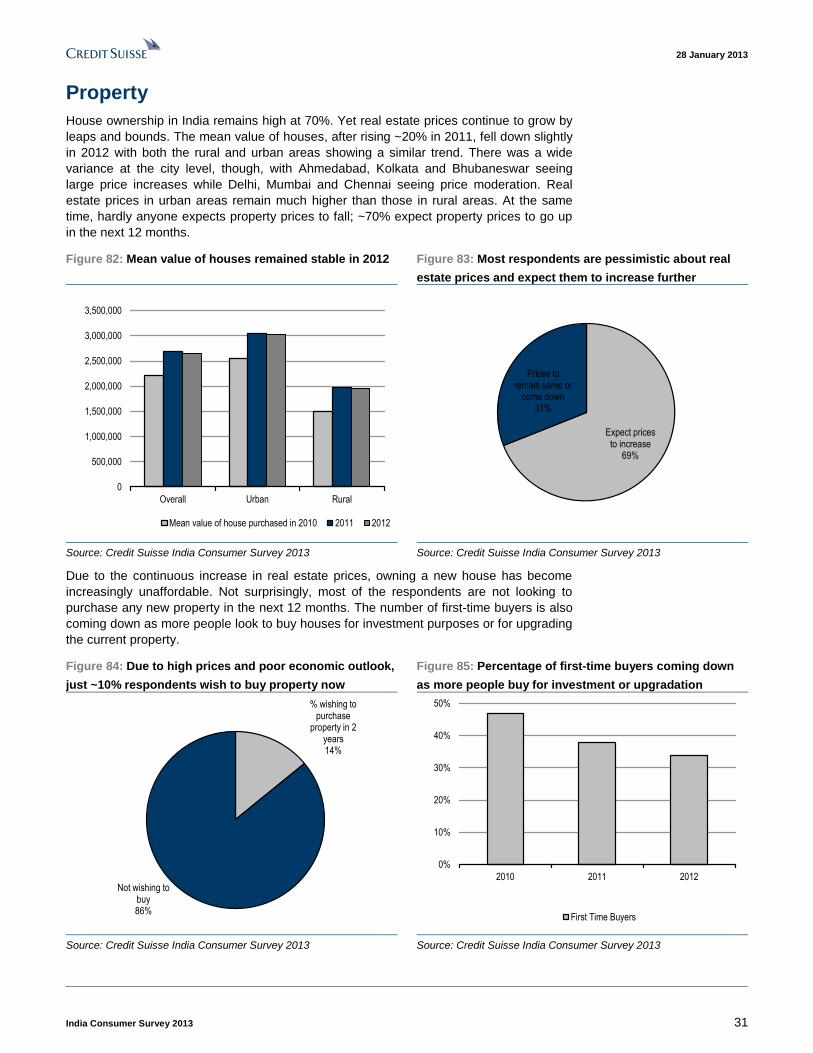

Property

House ownership in India remains high at 70%. Yet real estate prices continue to grow by

leaps and bounds. The mean value of houses, after rising ~20% in 2011, fell down slightly

in 2012 with both the rural and urban areas showing a similar trend. There was a wide

variance at the city level, though, with Ahmedabad, Kolkata and Bhubaneswar seeing

large price increases while Delhi, Mumbai and Chennai seeing price moderation. Real

estate prices in urban areas remain much higher than those in rural areas. At the same

time, hardly anyone expects property prices to fall; ~70% expect property prices to go up

in the next 12 months.

Figure 82: Mean value of houses remained stable in 2012 Figure 83: Most respondents are pessimistic about real

estate prices and expect them to increase further

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Overall Urban Rural

Mean value of house purchased in 2010 2011 2012

Expect prices to increase

69%

Prices to remain same or

come down31%

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

Due to the continuous increase in real estate prices, owning a new house has become

increasingly unaffordable. Not surprisingly, most of the respondents are not looking to

purchase any new property in the next 12 months. The number of first-time buyers is also

coming down as more people look to buy houses for investment purposes or for upgrading

the current property.

Figure 84: Due to high prices and poor economic outlook,

just ~10% respondents wish to buy property now

Figure 85: Percentage of first-time buyers coming down

as more people buy for investment or upgradation

% wishing to purchase

property in 2 years14%

Not wishing to buy86%

0%

10%

20%

30%

40%

50%

2010 2011 2012

First Time Buyers

Source: Credit Suisse India Consumer Survey 2013 Source: Credit Suisse India Consumer Survey 2013

28 January 2013

India Consumer Survey 2013 32

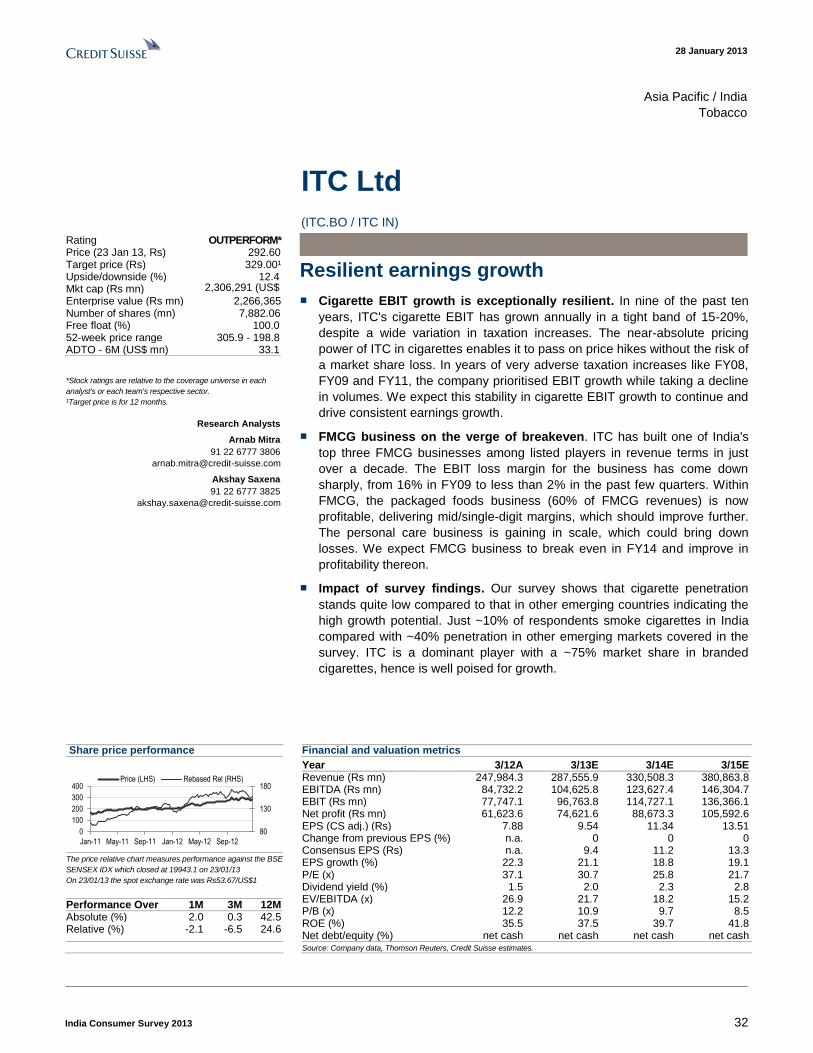

Asia Pacific / India

Tobacco

ITC Ltd

(ITC.BO / ITC IN)

Resilient earnings growth

■ Cigarette EBIT growth is exceptionally resilient. In nine of the past ten

years, ITC's cigarette EBIT has grown annually in a tight band of 15-20%,

despite a wide variation in taxation increases. The near-absolute pricing

power of ITC in cigarettes enables it to pass on price hikes without the risk of

a market share loss. In years of very adverse taxation increases like FY08,

FY09 and FY11, the company prioritised EBIT growth while taking a decline

in volumes. We expect this stability in cigarette EBIT growth to continue and

drive consistent earnings growth.

■ FMCG business on the verge of breakeven. ITC has built one of India's

top three FMCG businesses among listed players in revenue terms in just

over a decade. The EBIT loss margin for the business has come down

sharply, from 16% in FY09 to less than 2% in the past few quarters. Within

FMCG, the packaged foods business (60% of FMCG revenues) is now

profitable, delivering mid/single-digit margins, which should improve further.

The personal care business is gaining in scale, which could bring down

losses. We expect FMCG business to break even in FY14 and improve in

profitability thereon.

■ Impact of survey findings. Our survey shows that cigarette penetration

stands quite low compared to that in other emerging countries indicating the

high growth potential. Just ~10% of respondents smoke cigarettes in India

compared with ~40% penetration in other emerging markets covered in the

survey. ITC is a dominant player with a ~75% market share in branded

cigarettes, hence is well poised for growth.

Share price performance

80

130

180

0

100

200

300

400

Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the BSE

SENSEX IDX which closed at 19943.1 on 23/01/13

On 23/01/13 the spot exchange rate was Rs53.67/US$1

Performance Over 1M 3M 12M Absolute (%) 2.0 0.3 42.5 Relative (%) -2.1 -6.5 24.6

Financial and valuation metrics

Year 3/12A 3/13E 3/14E 3/15E Revenue (Rs mn) 247,984.3 287,555.9 330,508.3 380,863.8 EBITDA (Rs mn) 84,732.2 104,625.8 123,627.4 146,304.7 EBIT (Rs mn) 77,747.1 96,763.8 114,727.1 136,366.1 Net profit (Rs mn) 61,623.6 74,621.6 88,673.3 105,592.6 EPS (CS adj.) (Rs) 7.88 9.54 11.34 13.51 Change from previous EPS (%) n.a. 0 0 0 Consensus EPS (Rs) n.a. 9.4 11.2 13.3 EPS growth (%) 22.3 21.1 18.8 19.1 P/E (x) 37.1 30.7 25.8 21.7 Dividend yield (%) 1.5 2.0 2.3 2.8 EV/EBITDA (x) 26.9 21.7 18.2 15.2 P/B (x) 12.2 10.9 9.7 8.5 ROE (%) 35.5 37.5 39.7 41.8 Net debt/equity (%) net cash net cash net cash net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (23 Jan 13, Rs) 292.60 Target price (Rs) 329.00¹ Upside/downside (%) 12.4 Mkt cap (Rs mn) 2,306,291 (US$

42,972) Enterprise value (Rs mn) 2,266,365 Number of shares (mn) 7,882.06 Free float (%) 100.0 52-week price range 305.9 - 198.8 ADTO - 6M (US$ mn) 33.1

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Arnab Mitra

91 22 6777 3806

Akshay Saxena

91 22 6777 3825

28 January 2013

India Consumer Survey 2013 33

Asia Pacific / India

Automobile Manufacturers

Bajaj Auto Limited

(BAJA.BO / BJAUT IN)

Distinctly global

■ Main investment thesis. We expect the Indian two-wheeler industry to grow

at about 12% p.a. over the next few years. Increasing penetration in rural

India, driven by rising incomes and improving infrastructure, and higher

ownership among women in urban areas are the key growth drivers. Bajaj is

the second largest player in Indian two-wheeler market with a ~25% market

share in motorcycles. Bajaj has high free cash flow generation given its

higher margins and lower capex requirements.

■ Robust export growth complements domestic story. While exports have

been lacklustre in FY13 on account of issues with end-markets, Bajaj has

started gaining share from the Chinese, evident from the steep decline in

Chinese exports. We reckon on a lower base most of these end-markets will

witness healthy growth and that combined with even faster market share

gains for Bajaj (with currency benefits kicking in from FY14) will drive healthy

20% growth in export volumes. The export tie-up with Kawasaki will also

start bearing results from 2H FY14, in our view.

■ Margins set to expand on improved currency realisations. We expect

Bajaj’s margins to improve ~100 bp YoY in FY14 largely on account of better

export realisation which will move up from Rs50/US$ to Rs55/US$.

Potentially margins can expand much more (10% greater realisations on

exports which are 35% of sales) but we are building in lesser improvement

given that we expect the company to pass on a part of the benefit to its

customers. Also a part of the improvement in export margins will be negated

by the decline in DEPB rates which have gone down from 5.5% to 2%.

■ Impact of survey findings. Our survey results point to still good growth

potential for two-wheelers especially in smaller cities. Given the brand

positioning of Bajaj and its wide sales and service network, it is extremely

well positioned to cater to this growth. We also observe that an increased

appetite for credit, which if combined with higher availability of financing,