Embed Size (px)

Citation preview

DEALS SNAPSHOT

April - June 2017

INDIA MARKET UPDATE

DEALS SNAPSHOT

Dear Clients and Associates:

Welcome to the KNAV India Market Update for the quarter ended June 2017.

This update includes an analysis of private equity/venture capital investments and the key M&A deals in the quarter ended June 30, 2017.

Key highlights

• The quarter had around 277 private equity/venture capital investments rounding up to a value of USD ~5 bn. Some notable deals include:o Paytm’s fund raise of USD 1.4 bn from SoftBank showcases the potential of digital payments in India; &o Private placement of USD 360 mn in Tata Technologies by KKR and CPPIB.

• The quarter had around 78 M&A transactions rounding up to USD ~1.5 bn. The prominent deals are:o Sale of 12.18% stake in ICICI Lombard General Insurance by Fairfax to Warburg Pincus; &o HCL Tech’s acquisition of US BPO firm Urban Fulfillment for USD 30 mn.

• A detailed analysis and a selected listing of a few notable deals are presented in this update.

• Some notable and disruptive strategic moves by companies have also been included in this quarter’s edition.

Do share your comments and/or feedback on [email protected]

Thank you.

Vaibhav ManekPartner - Advisory services

2

Suparna DuaPartner - Investment banking

DEALS SNAPSHOT

Private equity/Venture capital investments

April-June 2017

3

DEALS SNAPSHOT

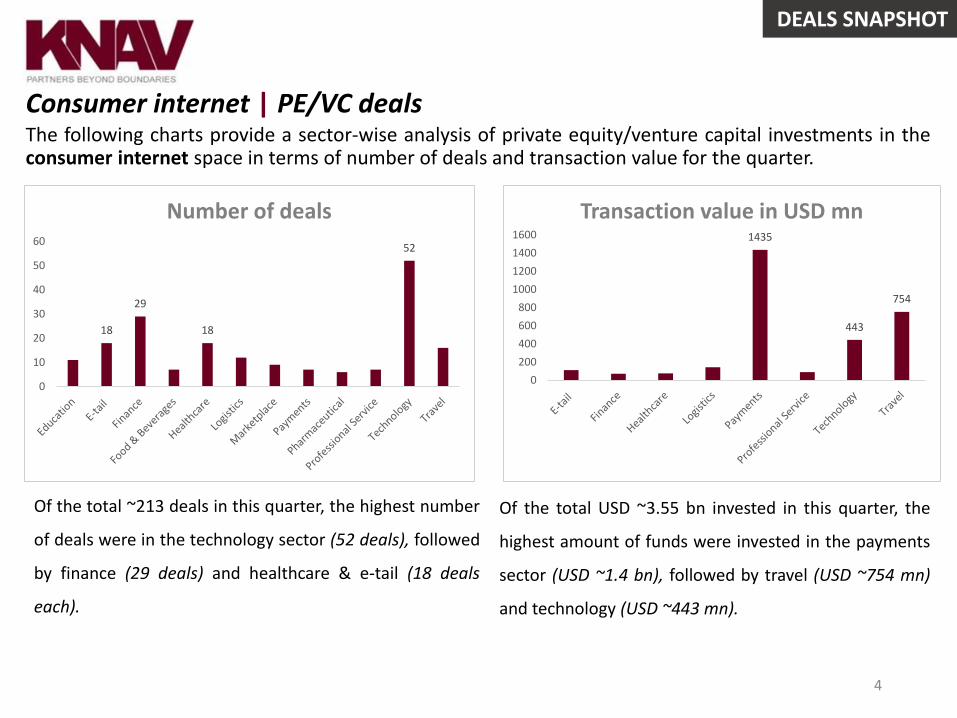

Of the total ~213 deals in this quarter, the highest number

of deals were in the technology sector (52 deals), followed

by finance (29 deals) and healthcare & e-tail (18 deals

each).

Of the total USD ~3.55 bn invested in this quarter, the

highest amount of funds were invested in the payments

sector (USD ~1.4 bn), followed by travel (USD ~754 mn)

and technology (USD ~443 mn).

4

Consumer internet | PE/VC dealsThe following charts provide a sector-wise analysis of private equity/venture capital investments in theconsumer internet space in terms of number of deals and transaction value for the quarter.

18

29

18

52

0

10

20

30

40

50

60

Number of deals1435

443

754

0

200

400

600

800

1000

1200

1400

1600

Transaction value in USD mn

DEALS SNAPSHOT

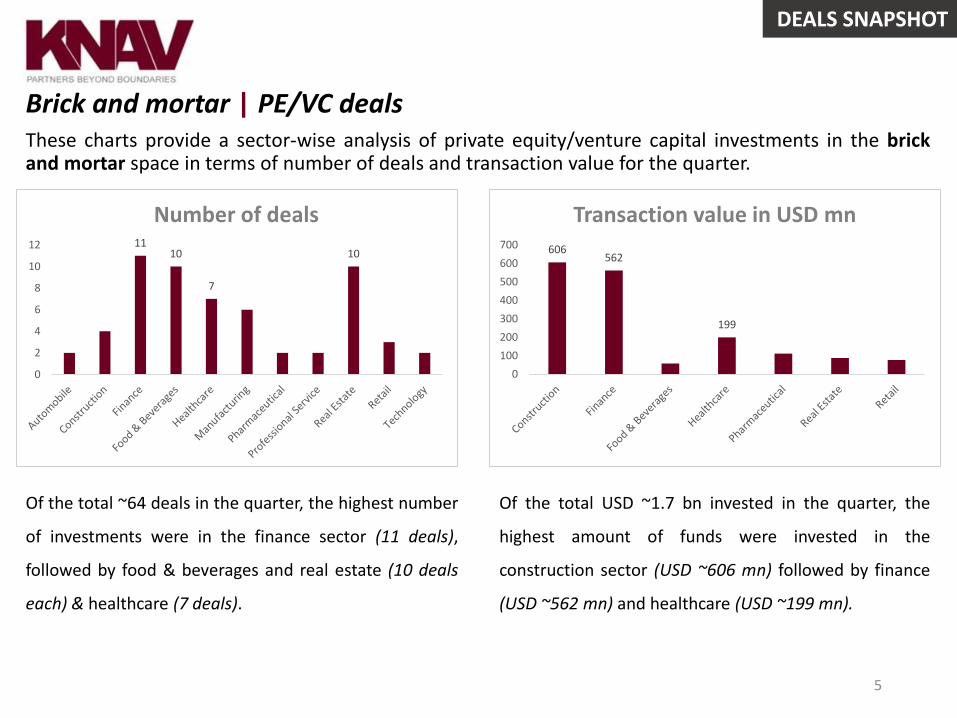

Brick and mortar | PE/VC deals These charts provide a sector-wise analysis of private equity/venture capital investments in the brickand mortar space in terms of number of deals and transaction value for the quarter.

5

Of the total ~64 deals in the quarter, the highest number

of investments were in the finance sector (11 deals),

followed by food & beverages and real estate (10 deals

each) & healthcare (7 deals).

Of the total USD ~1.7 bn invested in the quarter, the

highest amount of funds were invested in the

construction sector (USD ~606 mn) followed by finance

(USD ~562 mn) and healthcare (USD ~199 mn).

1110

7

10

0

2

4

6

8

10

12

Number of deals

606562

199

0

100

200

300

400

500

600

700

Transaction value in USD mn

DEALS SNAPSHOT

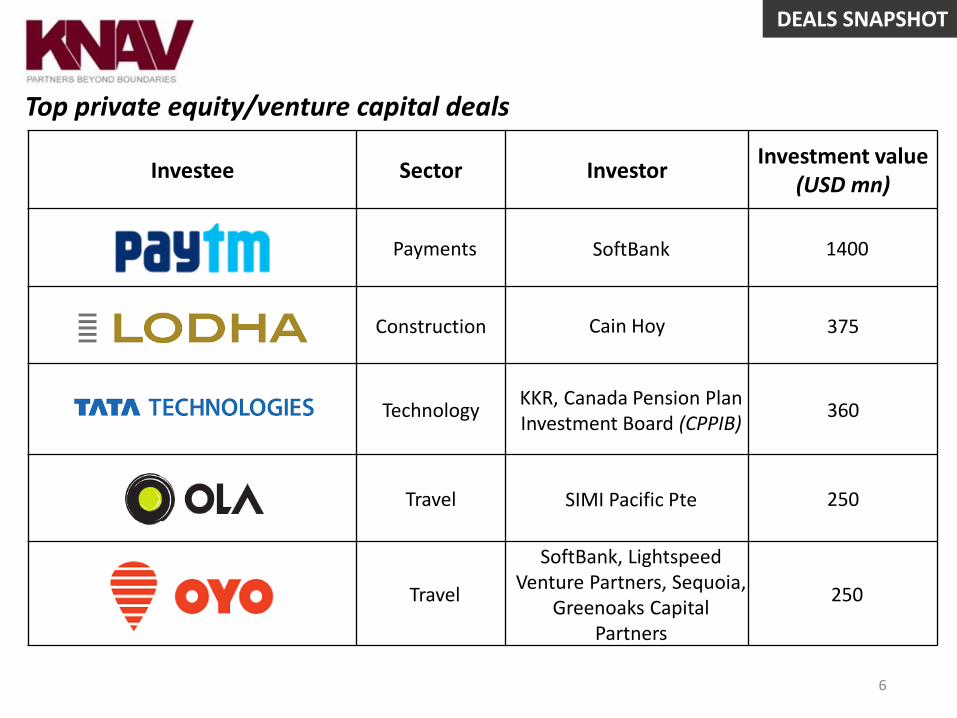

Investee Sector InvestorInvestment value

(USD mn)

Payments SoftBank 1400

Construction Cain Hoy 375

TechnologyKKR, Canada Pension Plan Investment Board (CPPIB)

360

Travel SIMI Pacific Pte 250

Travel

SoftBank, Lightspeed Venture Partners, Sequoia,

Greenoaks Capital Partners

250

6

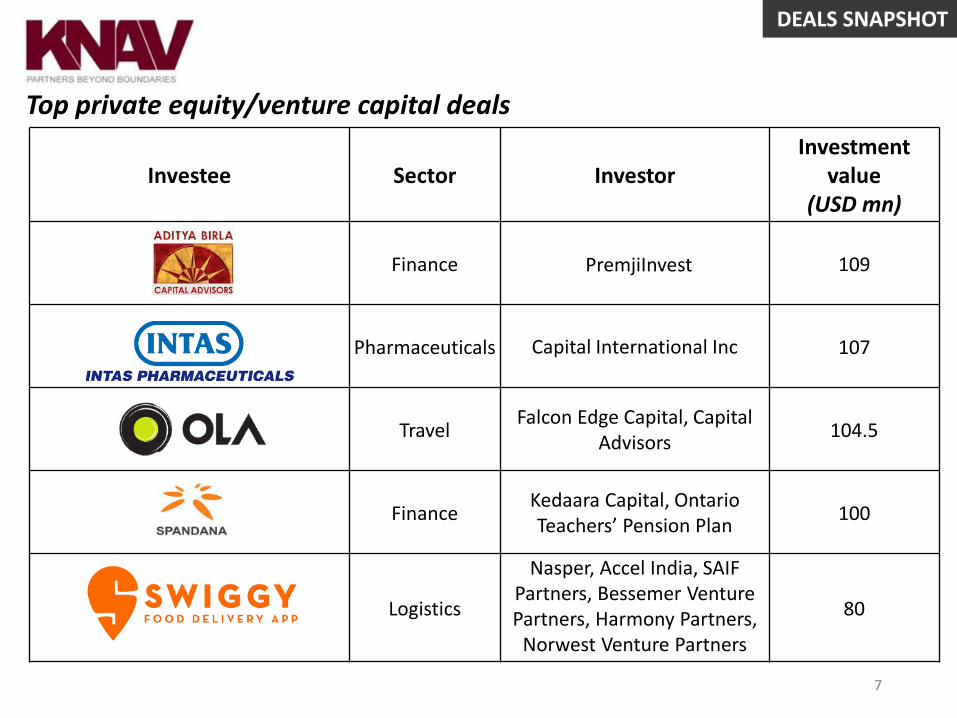

Top private equity/venture capital deals

DEALS SNAPSHOT

Investee Sector InvestorInvestment

value (USD mn)

Finance PremjiInvest 109

Pharmaceuticals Capital International Inc 107

TravelFalcon Edge Capital, Capital

Advisors104.5

FinanceKedaara Capital, Ontario Teachers’ Pension Plan

100

Logistics

Nasper, Accel India, SAIF Partners, Bessemer Venture Partners, Harmony Partners,

Norwest Venture Partners

80

Top private equity/venture capital deals

7

DEALS SNAPSHOT

Mergers & acquisitions

April-June 2017

8

DEALS SNAPSHOT

9

• Technology retains #1 position with 14 dealsSome of the highlights in the technology sector deals were: MapMyIndia’s acquisition of VIDTEQ, HCL Tech’s acquisition of Urban Fulfillment Services and Cognizant’s acquisition of TMG Health.

• Professional Services is placed at #2 position with 7 dealsSome of the prime deals in the professional services sector were: Anuj Puri’s acquisition of the Residential brokerage arm of JLL India, Tenon Group’s acquisition of Elite Cleaning and the merger of TMT Law Practice and DPSA Legal.

• Pharmaceuticals, Media & Entertainment and Finance are placed at #3 position with 6 deals eachSome of the deals in these sectors were: Pfizer’s acquisition of Neksium brand previously belonging to AstraZeneca AB, Casino Pride’s acquisition of a 30% stake in Baadshah and FlexiLoans Technologies’ acquisition of CreditPeriod.

Top M&A sectors

Professional services

Pharma, Media and Finance

Technology

DEALS SNAPSHOT

Sector-wise analysis | M&A deals

10

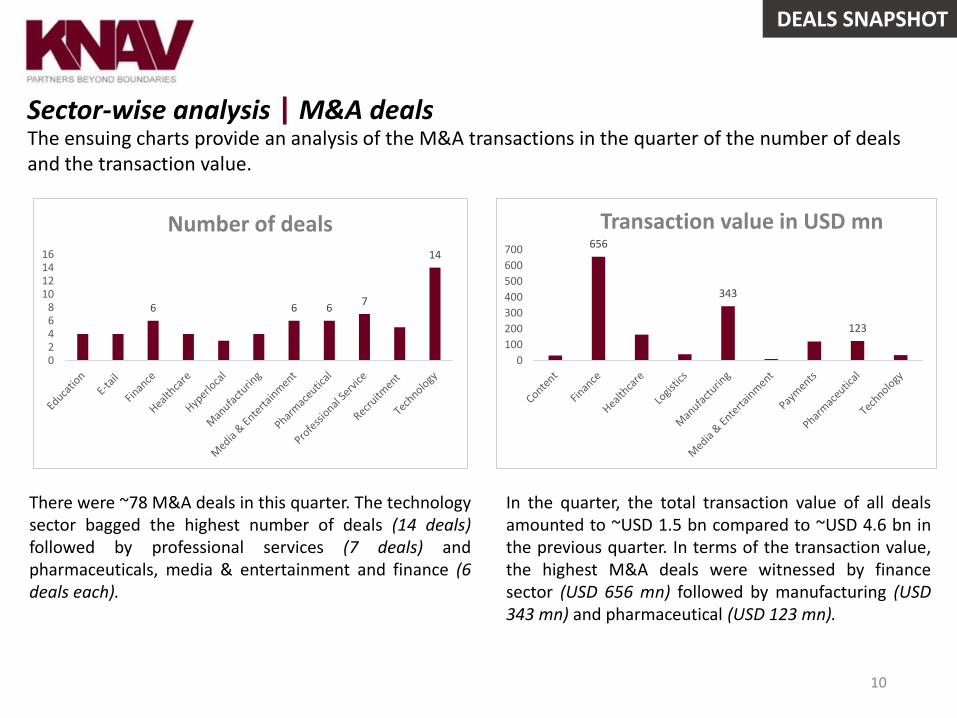

The ensuing charts provide an analysis of the M&A transactions in the quarter of the number of deals and the transaction value.

There were ~78 M&A deals in this quarter. The technologysector bagged the highest number of deals (14 deals)followed by professional services (7 deals) andpharmaceuticals, media & entertainment and finance (6deals each).

In the quarter, the total transaction value of all dealsamounted to ~USD 1.5 bn compared to ~USD 4.6 bn inthe previous quarter. In terms of the transaction value,the highest M&A deals were witnessed by financesector (USD 656 mn) followed by manufacturing (USD343 mn) and pharmaceutical (USD 123 mn).

6 6 67

14

02468

10121416

Number of deals656

343

123

0

100

200

300

400

500

600

700

Transaction value in USD mn

DEALS SNAPSHOT

Technology space as a leading sector attracting investments

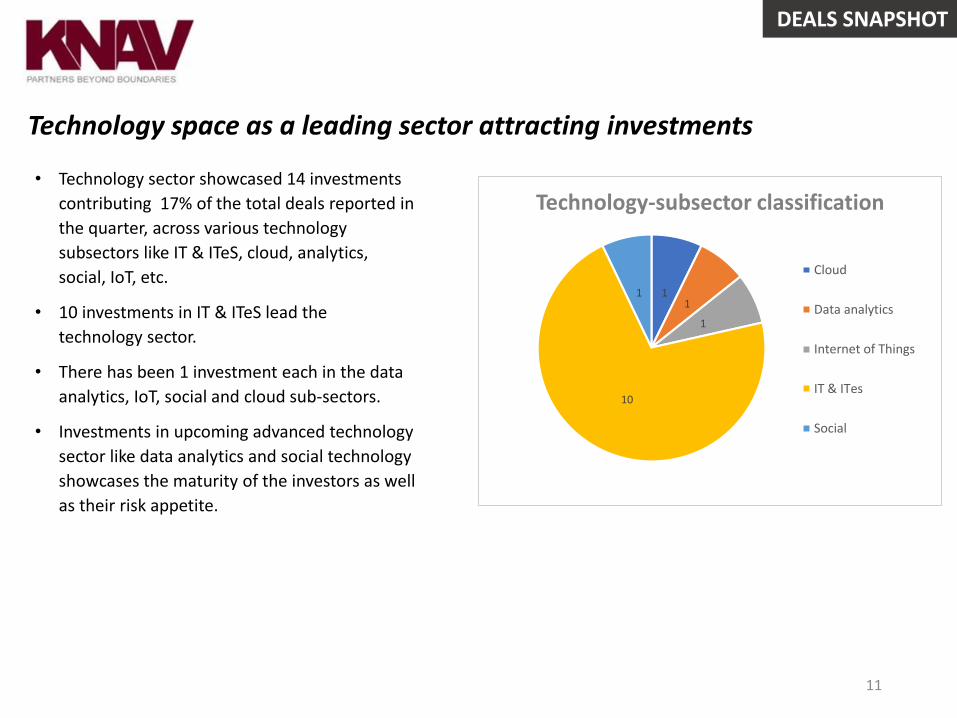

• Technology sector showcased 14 investments

contributing 17% of the total deals reported in

the quarter, across various technology

subsectors like IT & ITeS, cloud, analytics,

social, IoT, etc.

• 10 investments in IT & ITeS lead the

technology sector.

• There has been 1 investment each in the data

analytics, IoT, social and cloud sub-sectors.

• Investments in upcoming advanced technology

sector like data analytics and social technology

showcases the maturity of the investors as well

as their risk appetite.

11

11

1

10

1

Technology-subsector classification

Cloud

Data analytics

Internet of Things

IT & ITes

Social

DEALS SNAPSHOT

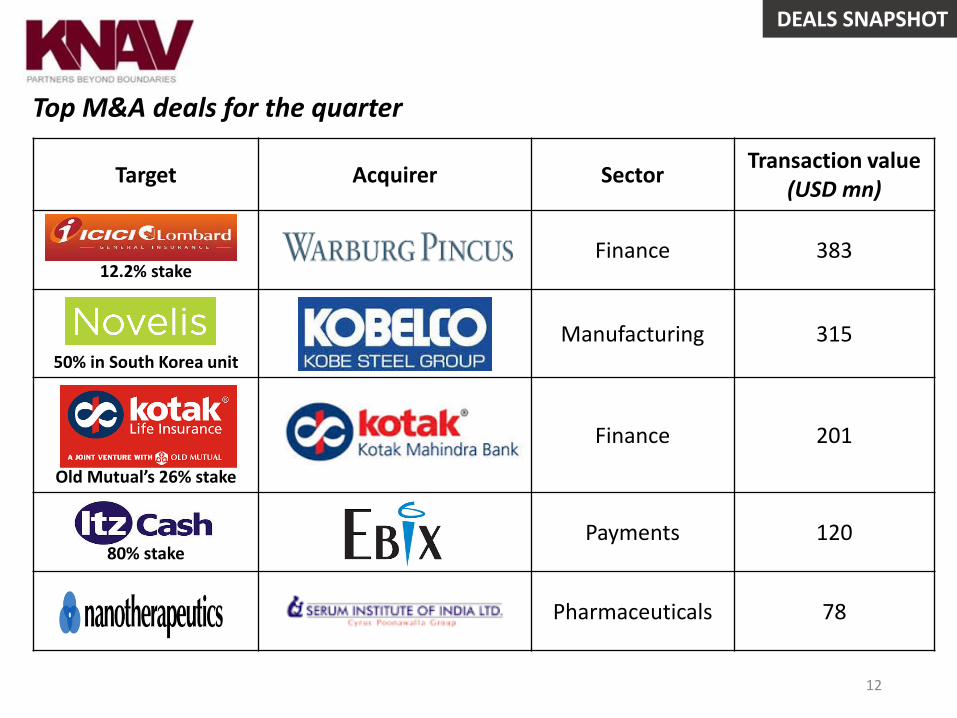

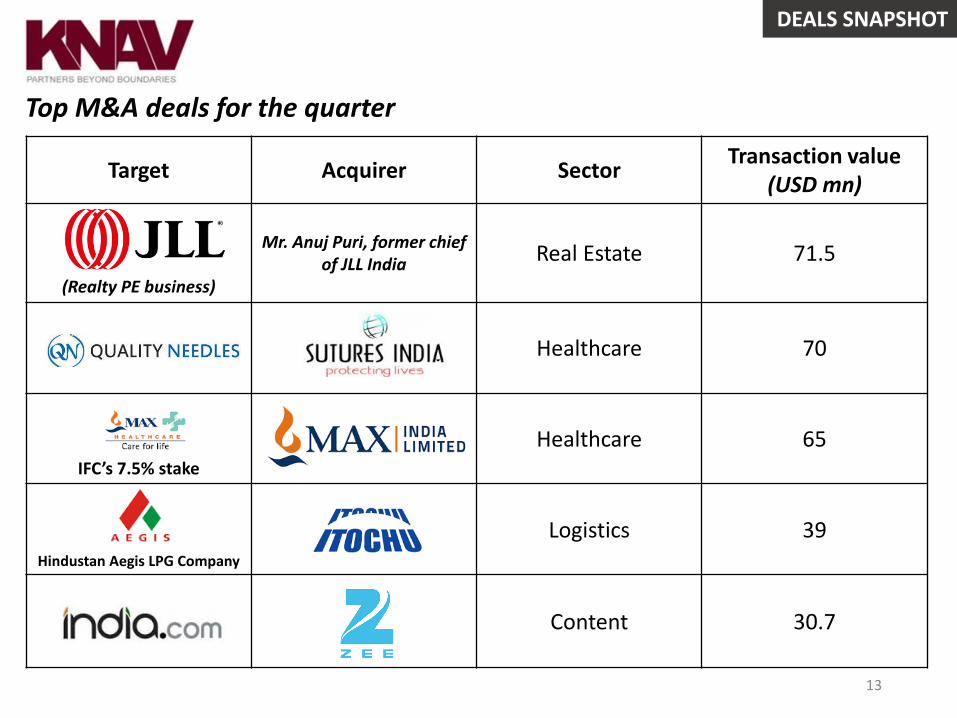

Top M&A deals for the quarter

Target Acquirer SectorTransaction value

(USD mn)

12.2% stakeFinance 383

50% in South Korea unit

Manufacturing 315

Old Mutual’s 26% stake

Finance 201

80% stakePayments 120

Pharmaceuticals 78

12

DEALS SNAPSHOT

Target Acquirer SectorTransaction value

(USD mn)

(Realty PE business)

Mr. Anuj Puri, former chief of JLL India

Real Estate 71.5

Healthcare 70

IFC’s 7.5% stake

Healthcare 65

Hindustan Aegis LPG Company

Logistics 39

Content 30.7

13

Top M&A deals for the quarter

DEALS SNAPSHOT

Analysis of a few transactions

April-June 2017

14

DEALS SNAPSHOT

• Fairfax Financial Holdings sold 12.18% of its stake in ICICI Lombard General Insurance to Warburg Pincus, Clermont Group and IIFL Special Opportunities Fund for USD 383 million.

• ICICI Lombard General Insurance was formed as a joint venture between ICICI Bank and Fairfax Financial Holdings, owned by Mr. Prem Watsa.

• While Warburg Pincus acquired 9% of the entity from Fairfax, Clermont Group and IIFL Special Opportunities Fund took 1.59% each.

• This deal values ICICI Lombard General Insurance at USD 3.1 billion.

• The deal comes at a time when ICICI Lombard plans to file documents for an IPO (first private sector insurance company to go public).

• This stake sale forms a part of the plan of Fairfax to sell 25% in the present JV and launch a new insurance joint venture. 15

Fairfax sale of 12.2% stake in ICICI Lombard to Warburg Pincus, others

Deal analysis

9%

DEALS SNAPSHOT

Zee Group buys India.com along with a minority stake in Tagos Design Innovations

• Zee Group has acquired the remaining 49% stake in India Webportal Pvt. Ltd. (which operates India.com) for USD 30.7 million and a 12.5% stake in Tagos Design Innovations Pvt. Ltd. for USD 2.5 million.

• India Webportal, formed as a JV between Zee and US digital media publisher Penske Media Corporation, operates content brands and distribution businesses across television, print, and the internet.

• Tagos Innovations, founded in 2014 by GBS Bindra, Sushant Panda and Tripat Preet Singh, has a unique product-Charmboard, an in-video discovery platform that makes videos respond to a user’s touch and allows the user to discover more from the video.

• Zee Entertainment will acquire the 49% stake from existing investors MMC Investments Holding Company II Ltd (44%), and Ashok Kurien (5%).

• These deals are primarily been made for the purpose of consolidation of businesses and to leverage the use of technology to boost its existing portfolio.

Deal analysis

16

Acq

uires 1

2.5

%

Acq

uires

DEALS SNAPSHOT

17

• Lockheed Martin, one of the world’s largest companies in the aerospace and defence sector, has tied up with Tata Group to produce the latest version of F-16 fighter jets in India.

• This deal pitches against the Saab-Adani deal for manufacturing Gripen-E fighter.

• Tata Lockheed Martin Aerostructures Limited has been formed with an aim to ‘produce, operate and export the F-16 Block 70 aircraft’ under the ‘Make in India’ initiative.

• Tata Group (under Tata Advanced Systems) will use the technology and manufacturing facilities of Lockheed Martin for the production.

• On a political aspect, this indicates that despite US President Donald Trump’s promises to keep skilled jobs in the US, his administration is willing to transfer F-16 production line from Texas to India.

• This deal creates numerous new job opportunities in India and the US and brings the world’s most combat-proven multi-role fighter aircraft manufacturing to India.

Lockheed Martin partners with TATA Group to manufacture F-16 jets in India

Deal analysis

DEALS SNAPSHOT

Disruptive strategic moves

April-June 2017

18

DEALS SNAPSHOT

• Amazon’s foray into the grocery segment is indicative of disruptive changes in this competitive high-volume business.

• Amazon’s recent acquisition of US-based supermarket chain Whole Foods Market for USD 13.7 billion is an acknowledgement of the importance of Brick and Mortar (B&M) stores in the Grocery segment.

• With this acquisition, it is likely to establish a combination of online and in-store goods, where customers can come into their local Whole Foods outlets and pick up their entire Amazon order.

• It is anticipated that this acquisition will improve supply chain capability, physical retail, big data analytics and minimum wastage of perishable commodities due to spoilage, as in the case of Amazon Fresh.

• The launch of Amazon Now (product delivery within 2 hours)and Amazon Pantry (next day delivery) for supply of grocery and other household essentials are indicative of the increasing interest of Amazon.

• Thus, while we are seeing several physical stores going online, we are also witnessing online marketplace opening B&M stores and going offline, indicating the interdependence of both the segments.

19

Amazon’s entry into the groceries sector

Disruptive strategic moves

DEALS SNAPSHOT

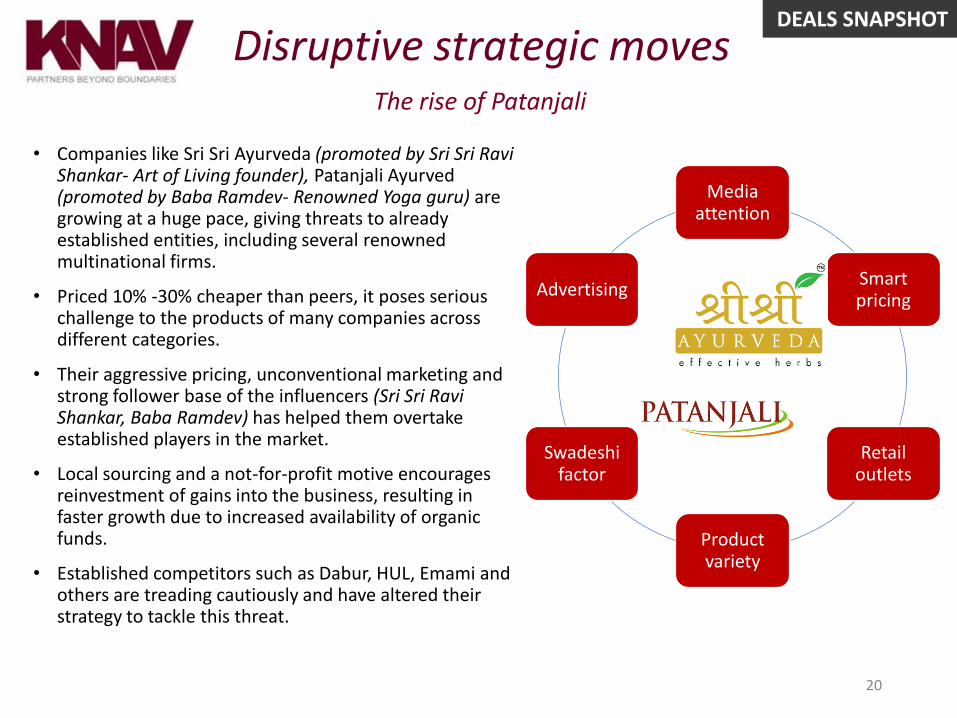

• Companies like Sri Sri Ayurveda (promoted by Sri Sri Ravi Shankar- Art of Living founder), Patanjali Ayurved(promoted by Baba Ramdev- Renowned Yoga guru) are growing at a huge pace, giving threats to already established entities, including several renowned multinational firms.

• Priced 10% -30% cheaper than peers, it poses serious challenge to the products of many companies across different categories.

• Their aggressive pricing, unconventional marketing and strong follower base of the influencers (Sri Sri Ravi Shankar, Baba Ramdev) has helped them overtake established players in the market.

• Local sourcing and a not-for-profit motive encourages reinvestment of gains into the business, resulting in faster growth due to increased availability of organic funds.

• Established competitors such as Dabur, HUL, Emami and others are treading cautiously and have altered their strategy to tackle this threat.

20

The rise of Patanjali

Disruptive strategic moves

Media attention

Smart pricing

Retail outlets

Product variety

Swadeshi factor

Advertising

DEALS SNAPSHOT

About KNAV

KNAV refers to one or more of the member firms of KNAV International Limited (‘KNAV International’), which itself is a not-for-profit, non-practicing, non-trading corporation incorporated in Georgia, USA.

KNAV International is a charter umbrella organization that does not provide services to clients. Services of audit, tax, valuation, risk and business advisory are delivered by KNAV's independent member firms in their respective global jurisdictions. All member firms of KNAV in India and North America are member firms of the US$ 2.01 billion, US headquartered Allinial Global.

Website - www.knavcpa.com

Reach us

If you want to know more about KNAV or its services please contact Mr. Vaibhav Manek at [email protected]. We will be glad to hear from you.

Suggestions/Feedback

For suggestions/feedback on this newsletter, please contact Ms. Suparna Dua at the KNAV Mumbai office on: [email protected]

Editorial credits

Deals Snapshot Editorial Hardik Adenwala and Akshay Mahalaxmikar –– KNAV Mumbai

The source of our data is our market research, publicly available reports and press items, and independent databases. While KNAV has made reasonable endeavors to ensure that the information provided in this newsletter is accurate and up to date as at the time of issue, KNAV shall not be liable for any errors, inaccuracies or delays in the information, nor for any actions taken in reliance thereon, nor does it endorse any views or opinions. KNAV disclaims all warranty, express or implied, as to the accuracy or completeness of any of the content provided, or as to the fitness of the content for any purpose to the extent permitted by law. The content herein is not appropriate for the purposes of making a decision to carry out a transaction or trade and does not provide any form of advice (investment, tax, legal) amounting to investment advice, nor make any recommendations or solicitations regarding particular financial instruments, investments or products, including the buying or selling of securities. KNAV has not undertaken any liability or obligation relating to the purchase or sale of securities for or by any person in connection with this document.

This newsletter is intended only for the individuals addressed. The information contained in this newsletter is privileged, confidential, and may be protected from disclosure; please be aware that any other use, printing, copying, disclosure or dissemination of this communication may be subject to legal restriction or sanction. Copyright and any other intellectual property rights in its contents are the sole property of KNAV.

CANADA | FRANCE | INDIA | NETHERLANDS | SINGAPORE | SWITZERLAND | USA | UK

21

DEALS SNAPSHOT

22

ContactAmsterdam

Drs. Henk Burke

Tel: +312 066 44 054

Atlanta

Atul Deshmukh

Tel: +1 678 584 1200

Bangalore

Shrenik Kataria

Tel: +91 80 4113 1896

Geneva

Claude Rey

Tel: +41 24 466 77 27

Hyderabad

Dayaniwas Sharma

Tel: +91 40 2324 0700

London

Amanjit Singh

Tel: +44 20 3617 6200

Lyon

Martine Chabert

Tel: +33 478 182 694

Mumbai

Khozema Anajwalla

Tel: +91 22 6164 4800

New Delhi

Monish Chatrath

Tel: +91 11 4106 9400

Singapore

Wayne Soo

Tel: +65 6846 8376

Toronto

Harshad Parekh

Tel: +1 416 229 1411