Embed Size (px)

Citation preview

INDIRECT TAX AND REAL ESTATE

Real Estate Summit

Bombay Chartered Accountants’ Society

and

Indian Merchants’ Chamber

By Vikram Nankani1

2nd February, 2013

AGENDA

1. VAT and Real Estate

K. Raheja Development Corporation Vs. State of Karnataka [141STC 298 (SC)],

Assotech Realty Pvt. Ltd. vs. State of UP [2007 (7) STR 129 All.]

Maharashtra Chamber of Housing Industry and Ors v. State of Maharashtra and Ors [2012-VIL-35-BOM]

Valuation of VAT

2. Service Tax and Real Estate

Commercial or Industrial Service.

Construction of a Complex.

Valuation of Service Tax.

Works Contract Services.

Valuation of tax for Works Contract services.

Judicial Decisions.

Renting of immovable property.

2

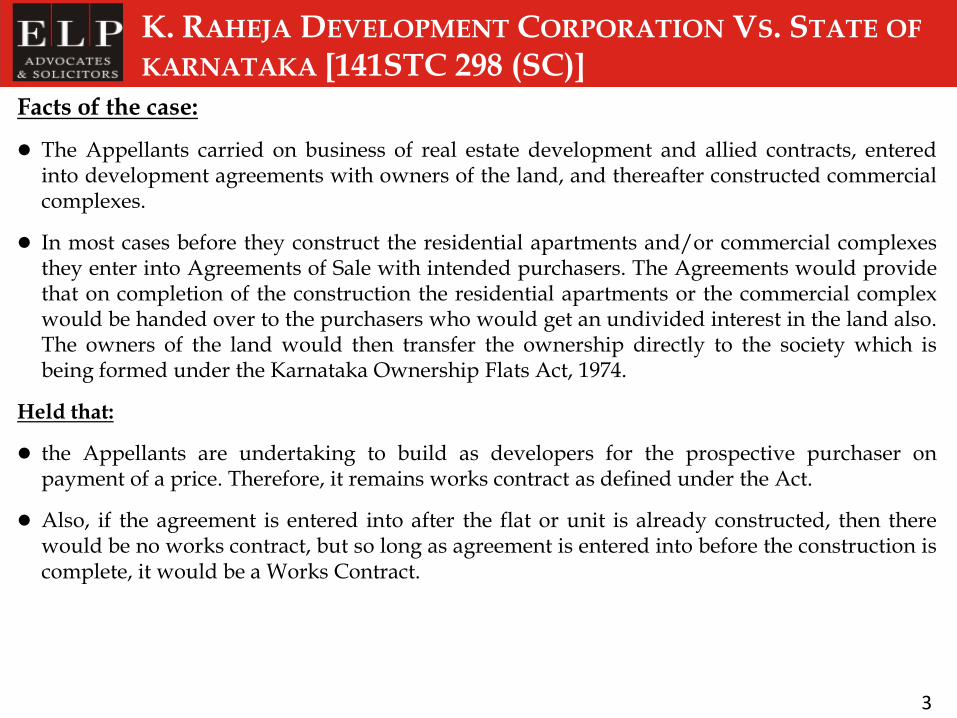

K. RAHEJA DEVELOPMENT CORPORATION VS. STATE OF

KARNATAKA [141STC 298 (SC)]

3

Facts of the case:

The Appellants carried on business of real estate development and allied contracts, enteredinto development agreements with owners of the land, and thereafter constructed commercialcomplexes.

In most cases before they construct the residential apartments and/or commercial complexesthey enter into Agreements of Sale with intended purchasers. The Agreements would providethat on completion of the construction the residential apartments or the commercial complexwould be handed over to the purchasers who would get an undivided interest in the land also.The owners of the land would then transfer the ownership directly to the society which isbeing formed under the Karnataka Ownership Flats Act, 1974.

Held that:

the Appellants are undertaking to build as developers for the prospective purchaser onpayment of a price. Therefore, it remains works contract as defined under the Act.

Also, if the agreement is entered into after the flat or unit is already constructed, then therewould be no works contract, but so long as agreement is entered into before the construction iscomplete, it would be a Works Contract.

DEVELOPMENTS

4

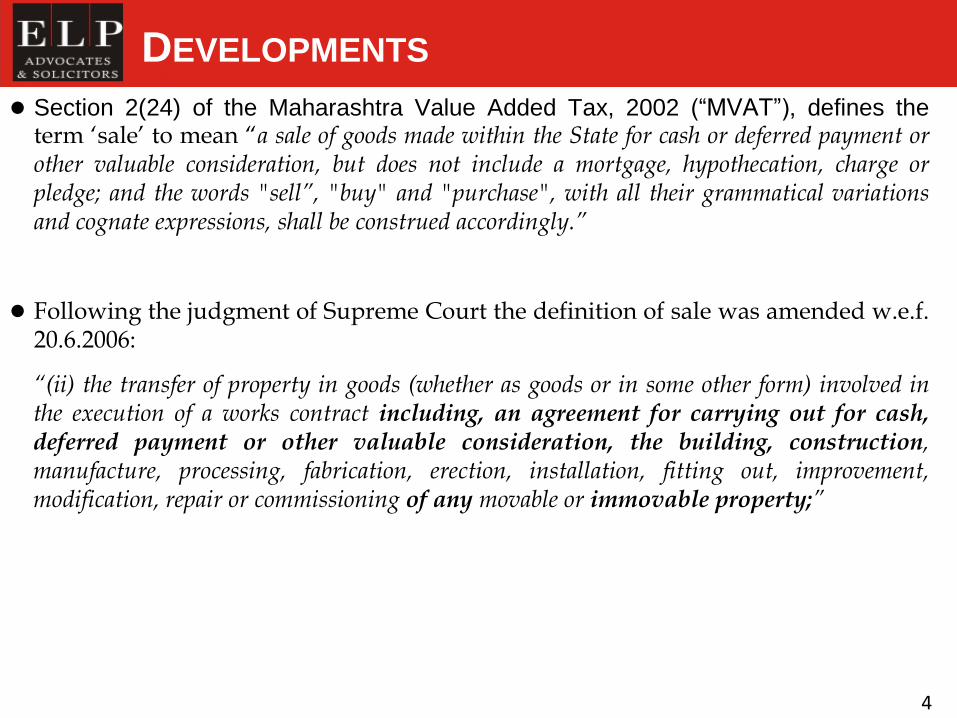

Section 2(24) of the Maharashtra Value Added Tax, 2002 (“MVAT”), defines theterm „sale‟ to mean “a sale of goods made within the State for cash or deferred payment orother valuable consideration, but does not include a mortgage, hypothecation, charge orpledge; and the words "sell”, "buy" and "purchase", with all their grammatical variationsand cognate expressions, shall be construed accordingly.”

Following the judgment of Supreme Court the definition of sale was amended w.e.f.20.6.2006:

“(ii) the transfer of property in goods (whether as goods or in some other form) involved inthe execution of a works contract including, an agreement for carrying out for cash,deferred payment or other valuable consideration, the building, construction,manufacture, processing, fabrication, erection, installation, fitting out, improvement,modification, repair or commissioning of any movable or immovable property;”

DEVELOPMENTS

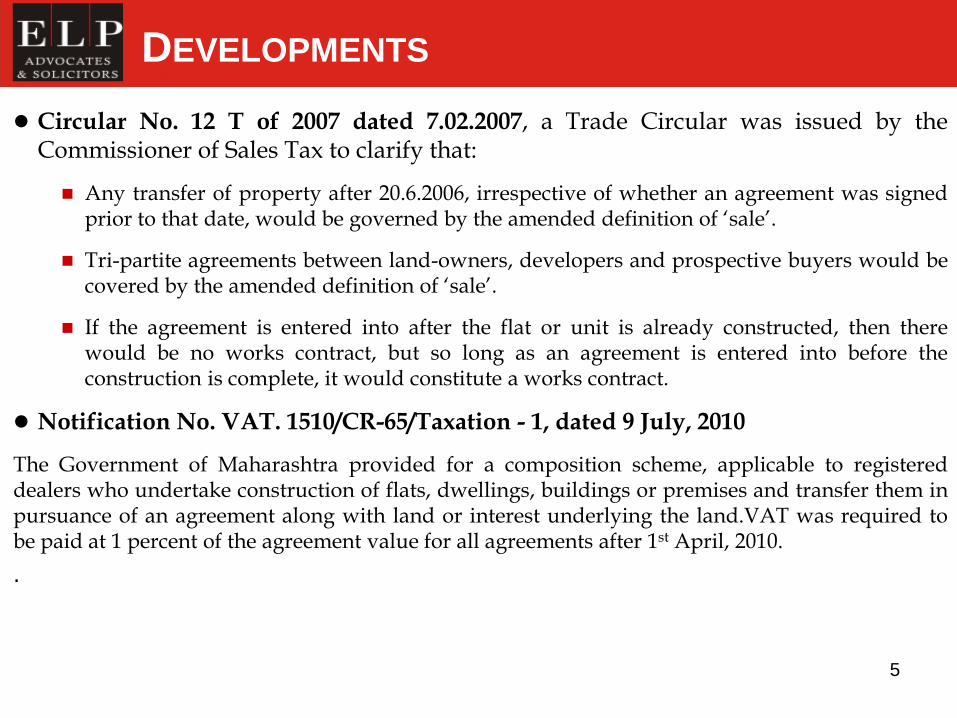

Circular No. 12 T of 2007 dated 7.02.2007, a Trade Circular was issued by theCommissioner of Sales Tax to clarify that:

Any transfer of property after 20.6.2006, irrespective of whether an agreement was signedprior to that date, would be governed by the amended definition of „sale‟.

Tri-partite agreements between land-owners, developers and prospective buyers would becovered by the amended definition of „sale‟.

If the agreement is entered into after the flat or unit is already constructed, then therewould be no works contract, but so long as an agreement is entered into before theconstruction is complete, it would constitute a works contract.

Notification No. VAT. 1510/CR-65/Taxation - 1, dated 9 July, 2010

The Government of Maharashtra provided for a composition scheme, applicable to registereddealers who undertake construction of flats, dwellings, buildings or premises and transfer them inpursuance of an agreement along with land or interest underlying the land.VAT was required tobe paid at 1 percent of the agreement value for all agreements after 1st April, 2010.

.

5

MAHARASHTRA CHAMBER OF HOUSING INDUSTRY AND ORS V. STATE

OF MAHARASHTRA AND ORS [2012-VIL-35-BOM]

6

The constitutional validity of the amended definition of „sale‟, the Trade Circulardated 7.02.2007 and the 1% Composition Scheme introduced w.e.f. 9.07.2010, waschallenged in a spate of writ petitions.

On behalf of the petitioners, it was contended as under:

The amendment was beyond the scope of the States power to tax under Sl. No.54 of List II of the Seventh Schedule to the Constitution.

In order to attract the application of Article 366(29A)(b), a contract would haveto inter alia involve a transfer of property in „goods‟ and immovable propertydoes not constitute „goods‟.

Consequent to the 46th Amendment to the Constitution, only a transfer ofproperty in goods involved in the execution of a works contract is taxable and acontract for the sale of immovable property is not a works contract.

A works contract involves only two elements viz. (i) the transfer of property ingoods; and (ii) supply of labour and services. If a third element, the sale ofimmovable property, is involved in the contract it does not constitute a workscontract and hence to such a contract, the legal fiction which is created byArticle 366(29A) would not apply.

CONTD…

7

Agreements contemplated to be brought within the purview of the amended definition ofsale, per the Circular dated 07.02.2007, are simplicitor agreements for the sale ofimmovable property.

Contracts governed by the Maharashtra Ownership Flats (Regulations of the Promotionof Construction, Sale, Management and Transfer) Act, 1963 („MOFA‟) cannot be regardedas a works contract, being agreements for the purchase of immovable property.

The MVAT ignores the concept of plurality of deemed sales. Where the developer is theowner of the land, the promoter is both the owner and developer. Alternately, adeveloper may enter into a development agreement with the owner of the land. When apromoter appoints a sub contractor and gets a building constructed, that contract is aworks contract under Article 366(29A) and a transfer of the property in the goodsinvolved in the execution of the works contract takes place to the developer. That wouldbe the first deemed sale. When the developer enters into an agreement with a purchaserunder the MOFA, a sale of goods is not involved since that would amount to a seconddeemed sale of the same goods which cannot be brought to tax. Once a promoter hasappointed a sub contractor the property passes to him as a promoter owner or to theowner, as the case may be, where there is only a developer. Property has already passedon accretion and the same transaction of deemed sale cannot be taxed twice.

An executory contract does not fit into the conception of a sale of goods within themeaning of Entry 54 of the State List to the Seventh Schedule. The amended definition ofsale was beyond the scope of the States power to tax under Sl. No. 54 of List II of theSeventh Schedule to the Constitution.

CONTD….

8

On behalf of the Revenue, it was contended as under:

An unduly restrictive or contrived meaning should not be given to the provisions ofArticle 366(29A) otherwise the object underlying the Constitutional amendment would bedefeated.

The purpose underlying the enactment of the deeming fiction in Article 366(29A) was tooverride the limited definition of the expression „sale‟ in the Sale of Goods Act, 1930 andto isolate the sale of goods element involved, inter alia, in a contract which is a workscontract. The amended definition of „sale‟ falls within the compass of Article 366(29A).

A works contract is a contract to execute works and encompasses a wide range ofcontracts; it is not restricted to building contracts having only two elements viz. the saleof material and goods and the supply of labour and services.

The well settled connotation of the expression „works contract‟ is that a building contractmay also involve in certain situations a sale of land. A works contract does not cease to besuch merely because any other obligation exists.

In an agreement which is governed by the MOFA, a conveyance of the interest in the flator at any rate an interest therein is created at the stage of the execution of an agreement.The doctrine of accretion is always subject to a contract to the contrary. The provisions ofthe MOFA contain a statutory stipulation to the contrary where the accretion to theproperty enures to the benefit of the flat purchaser; and

The Trade Circular and the deduction schemes are only clarificatory in nature.

CONTD……

9

Held:

Works contracts have numerous variations and it is not possible to accept the contentioneither as a matter of first principle or as a matter of interpretation that a contract for workin the course of which title is transferred to the flat purchaser would cease to be a workscontract.

The effect of the amendment to Section 2(24) is to clarify the legislative intent that atransfer of property in goods involved in the execution of works contract including anagreement for building and construction of immovable property would fall within thedescription of a sale of goods within the meaning of the provision.

The constitutional validity of the provisions of the MVAT Act, 2002, as amended, is notcontingent upon any other statutory regulation of apartments under cognate legislation inthe State of Maharashtra.

Having regard to this statutory scheme, it is not possible to accept the submissionthat a contract involving an agreement to sell a flat within the purview of the MOFAis an agreement for sale of immovable property simplicitor.

The Constitutional validity of the amended definition of „sale‟, the Trade Circular dated7.02.2007 etc. upheld.

DEVELOPMENTS:

Trade circular No. 14T of 2012 dated 06.08.2012, issued by the Commissioner of SalesTax, Maharashtra

States that developers are liable to pay tax under the MVAT Act, w.e.f. 20.06. 2006

Provides for certain facilitation for obtaining registration, grant administrative relief forunregistered period, and filing of returns for the period from 20.06.2006.

A Special Leave petition was filed by developer‟s representative organization MCHI-CREDAI challenging the Order of the Bombay High Court. The Supreme Court onAugust 28, 2012 passed an interim Order , and extending the deadline for payingVAT by two months for dealers in Maharashtra. The developers were allowed to payVAT by October 31st and register themselves by October 15, 2012. It also directed that,if tax is paid no penalty and interest will be imposed on assesses who have paid thetax by 31st October, 2012.The Taxes so collected by the Sales Tax Development will beparked in a separate account and will be refunded to developers in the event the SLPsucceeds.

10

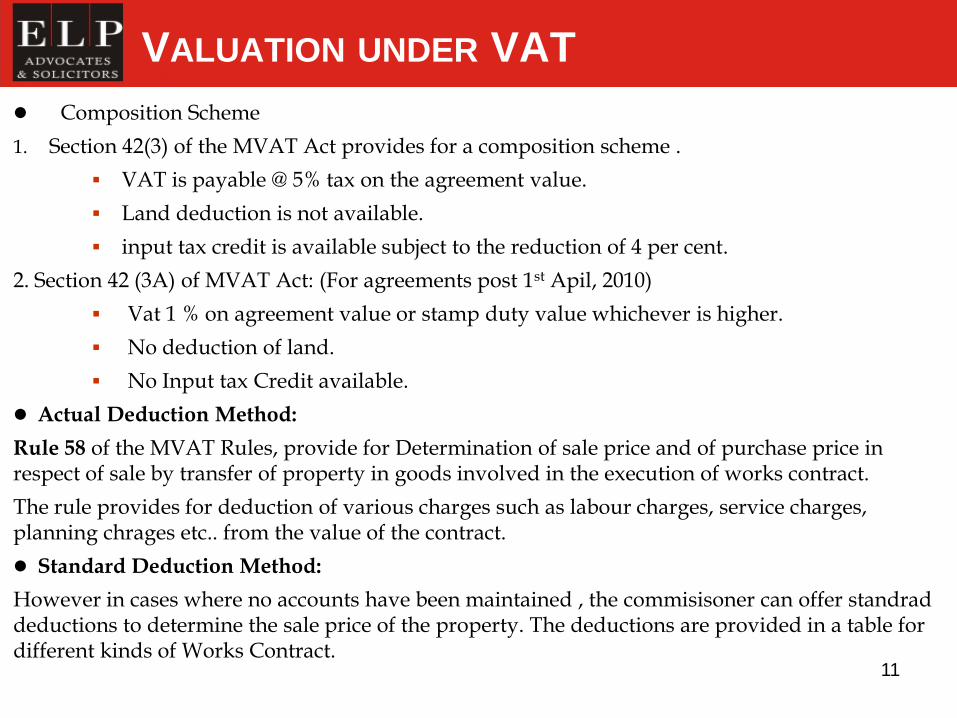

VALUATION UNDER VAT

Composition Scheme

1. Section 42(3) of the MVAT Act provides for a composition scheme .

VAT is payable @ 5% tax on the agreement value.

Land deduction is not available.

input tax credit is available subject to the reduction of 4 per cent.

2. Section 42 (3A) of MVAT Act: (For agreements post 1st Apil, 2010)

Vat 1 % on agreement value or stamp duty value whichever is higher.

No deduction of land.

No Input tax Credit available.

Actual Deduction Method:

Rule 58 of the MVAT Rules, provide for Determination of sale price and of purchase price in respect of sale by transfer of property in goods involved in the execution of works contract.

The rule provides for deduction of various charges such as labour charges, service charges, planning chrages etc.. from the value of the contract.

Standard Deduction Method:

However in cases where no accounts have been maintained , the commisisoner can offer standrad deductions to determine the sale price of the property. The deductions are provided in a table for different kinds of Works Contract.

11

SERVICE TAX AND REAL ESTATE

12

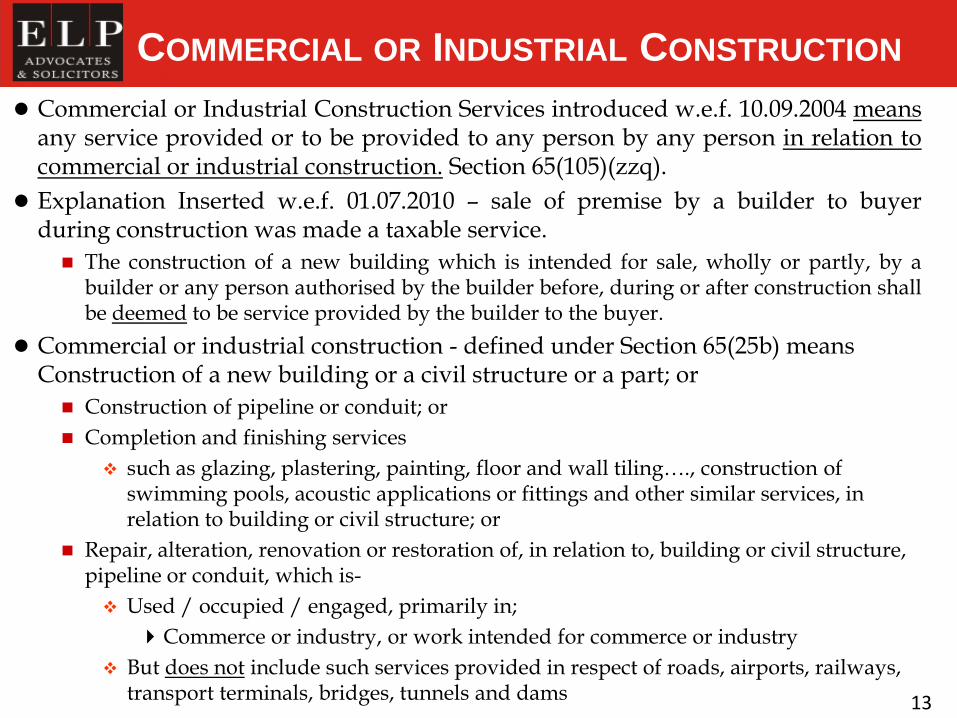

COMMERCIAL OR INDUSTRIAL CONSTRUCTION

Commercial or Industrial Construction Services introduced w.e.f. 10.09.2004 meansany service provided or to be provided to any person by any person in relation tocommercial or industrial construction. Section 65(105)(zzq).

Explanation Inserted w.e.f. 01.07.2010 – sale of premise by a builder to buyerduring construction was made a taxable service.

The construction of a new building which is intended for sale, wholly or partly, by abuilder or any person authorised by the builder before, during or after construction shallbe deemed to be service provided by the builder to the buyer.

Commercial or industrial construction - defined under Section 65(25b) means Construction of a new building or a civil structure or a part; or

Construction of pipeline or conduit; or

Completion and finishing services

such as glazing, plastering, painting, floor and wall tiling…., construction of swimming pools, acoustic applications or fittings and other similar services, in relation to building or civil structure; or

Repair, alteration, renovation or restoration of, in relation to, building or civil structure, pipeline or conduit, which is-

Used / occupied / engaged, primarily in;

Commerce or industry, or work intended for commerce or industry

But does not include such services provided in respect of roads, airports, railways, transport terminals, bridges, tunnels and dams 13

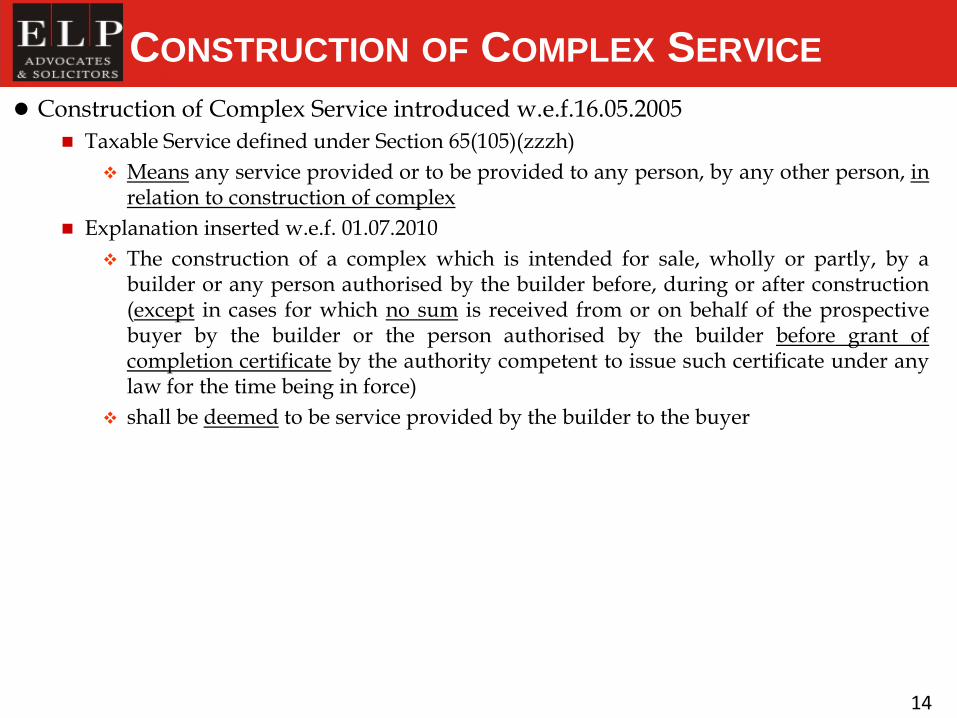

Construction of Complex Service introduced w.e.f.16.05.2005

Taxable Service defined under Section 65(105)(zzzh)

Means any service provided or to be provided to any person, by any other person, inrelation to construction of complex

Explanation inserted w.e.f. 01.07.2010

The construction of a complex which is intended for sale, wholly or partly, by abuilder or any person authorised by the builder before, during or after construction(except in cases for which no sum is received from or on behalf of the prospectivebuyer by the builder or the person authorised by the builder before grant ofcompletion certificate by the authority competent to issue such certificate under anylaw for the time being in force)

shall be deemed to be service provided by the builder to the buyer

14

CONSTRUCTION OF COMPLEX SERVICE

MAGUS CONSTRUCTION PVT. LTD. VS. UNION OF INDIA [2008 (11) S.T.R. 225 (GAU.)]

when a builder, promoter or developer undertakes construction for its own self, in suchcases, there would not be a question of providing „taxable service‟ by one person toanother. The only transaction between the petitioner and the prospective buyer is that onsale and purchase of flat. Any advance paid by the prospective buyer representsconsideration received towards sale of flat to such prospective buyer and is not forobtaining service from the petitioner.

Held – Not liable to Service tax

16

VALUATION- PRE 2012

17

Particulars Option 1COMPOSITION SCHEME

Option 2

Rate of tax 4.12% of (Gross Amount charged Less VAT/Sales

tax)

10.3% of [(Gross amount Less VAT / Sales tax) Less value of goods]

Availability of Credit to Service provider

Available for Capital Goods & Input Services

Available for Capital Goods & Input services

The definition of works contract has been amended to inlcude movable property as well.

“works contract” means a contract wherein transfer of property in goods involved in theexecution of such contract is leviable to tax as sale of goods and such contract is for thepurpose of carrying out construction, erection, commissioning, installation, completion, fittingout, repair, maintenance, renovation, alteration of any movable or immovable property or forcarrying out any other similar activity or a part thereof in relation to such property;

Vide Notification 30/2012-S.T. dated 20.06.2012 (applicable w.e.f. 01.07.2012), inrespect of Works Contract service:

Both the service provider and service recipient are required to discharge 50% of the Servicetax liability. Applicable only where the service provider is individual or HUF orpartnership firm or LLP or AOP and the service recipient is a body corporate.

In other cases, service provider is required to apply and recover tax

18

VALUATION OF SERVICE TAX UNDER WORKS CONTRACT

Value of service portion in works contracts will be determined in terms of the 2A of the ServiceTax (Determination of Value) Rules, 2006 (“Valuation Rules”).

As per Rule 2A (i) of the Valuation rules, the value of service portion in the contract shall beequivalent to the gross amount charged for works contract less the value of the property in thegoods transferred.

19

VALUATION CONTD...

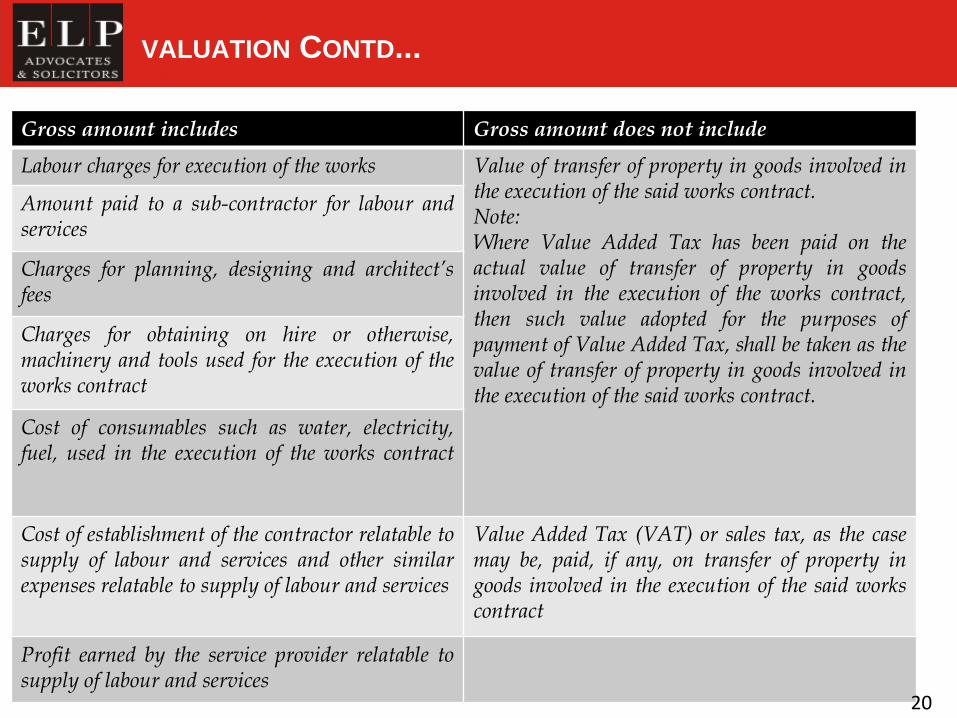

Gross amount includes Gross amount does not include

Labour charges for execution of the works Value of transfer of property in goods involved inthe execution of the said works contract.Note:Where Value Added Tax has been paid on theactual value of transfer of property in goodsinvolved in the execution of the works contract,then such value adopted for the purposes ofpayment of Value Added Tax, shall be taken as thevalue of transfer of property in goods involved inthe execution of the said works contract.

Amount paid to a sub-contractor for labour andservices

Charges for planning, designing and architect’sfees

Charges for obtaining on hire or otherwise,machinery and tools used for the execution of theworks contract

Cost of consumables such as water, electricity,fuel, used in the execution of the works contract

Cost of establishment of the contractor relatable tosupply of labour and services and other similarexpenses relatable to supply of labour and services

Value Added Tax (VAT) or sales tax, as the casemay be, paid, if any, on transfer of property ingoods involved in the execution of the said workscontract

Profit earned by the service provider relatable tosupply of labour and services

20

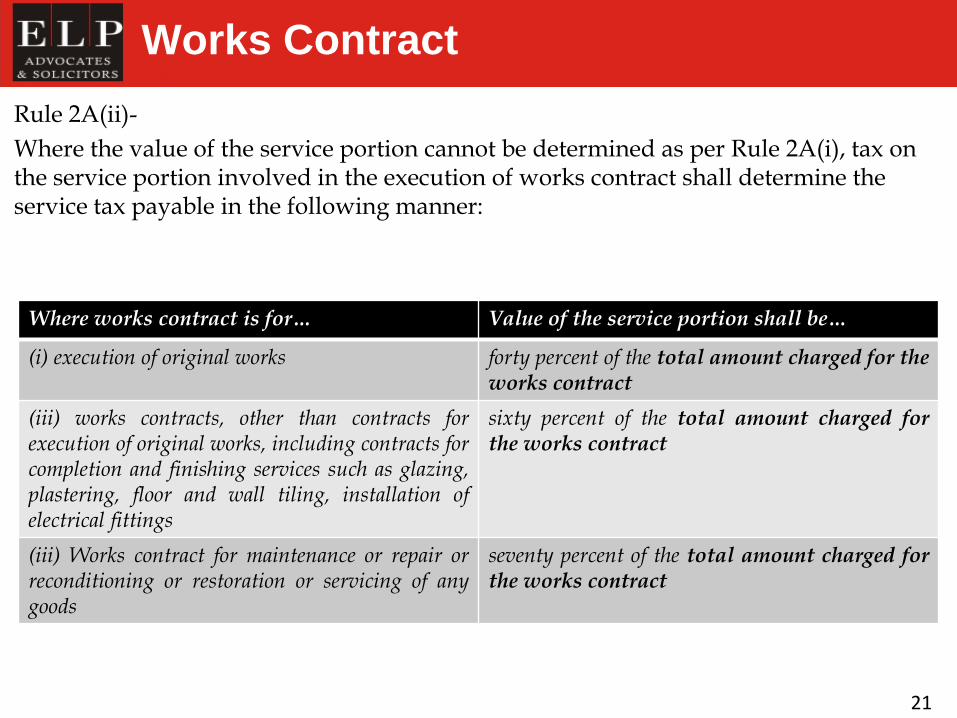

Works Contract

Rule 2A(ii)-

Where the value of the service portion cannot be determined as per Rule 2A(i), tax on the service portion involved in the execution of works contract shall determine the service tax payable in the following manner:

Where works contract is for… Value of the service portion shall be…

(i) execution of original works forty percent of the total amount charged for theworks contract

(iii) works contracts, other than contracts forexecution of original works, including contracts forcompletion and finishing services such as glazing,plastering, floor and wall tiling, installation ofelectrical fittings

sixty percent of the total amount charged forthe works contract

(iii) Works contract for maintenance or repair orreconditioning or restoration or servicing of anygoods

seventy percent of the total amount charged forthe works contract

21

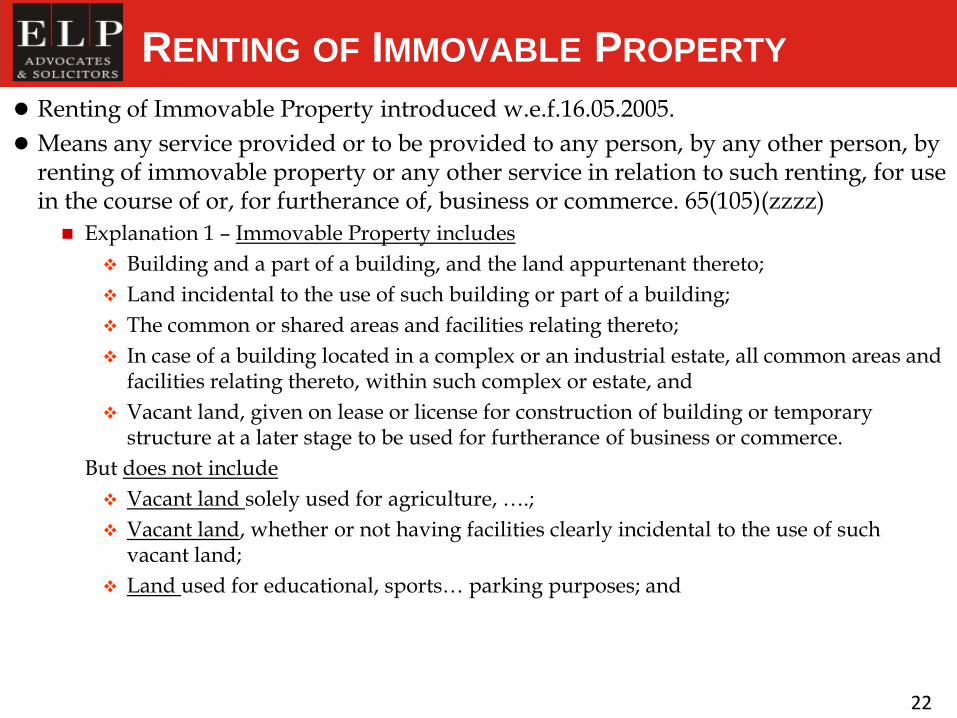

RENTING OF IMMOVABLE PROPERTY

Renting of Immovable Property introduced w.e.f.16.05.2005.

Means any service provided or to be provided to any person, by any other person, by renting of immovable property or any other service in relation to such renting, for use in the course of or, for furtherance of, business or commerce. 65(105)(zzzz)

Explanation 1 – Immovable Property includes

Building and a part of a building, and the land appurtenant thereto;

Land incidental to the use of such building or part of a building;

The common or shared areas and facilities relating thereto;

In case of a building located in a complex or an industrial estate, all common areas and facilities relating thereto, within such complex or estate, and

Vacant land, given on lease or license for construction of building or temporary structure at a later stage to be used for furtherance of business or commerce.

But does not include

Vacant land solely used for agriculture, ….;

Vacant land, whether or not having facilities clearly incidental to the use of such vacant land;

Land used for educational, sports… parking purposes; and

22

RENTING OF IMMOVABLE PROPERTY

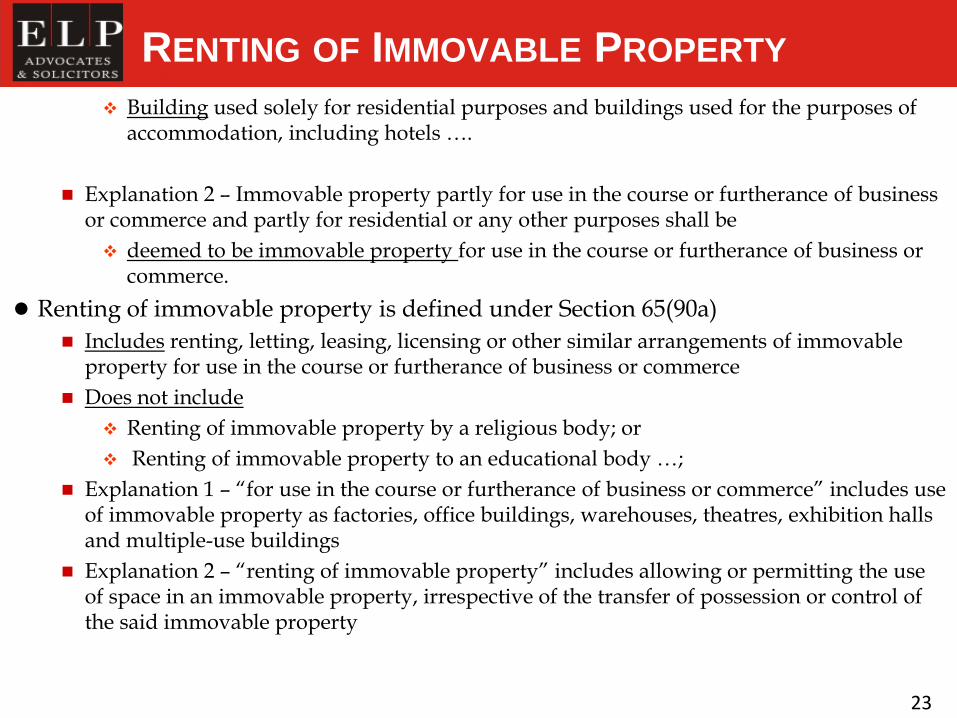

Building used solely for residential purposes and buildings used for the purposes of accommodation, including hotels ….

Explanation 2 – Immovable property partly for use in the course or furtherance of business or commerce and partly for residential or any other purposes shall be

deemed to be immovable property for use in the course or furtherance of business or commerce.

Renting of immovable property is defined under Section 65(90a)

Includes renting, letting, leasing, licensing or other similar arrangements of immovable property for use in the course or furtherance of business or commerce

Does not include

Renting of immovable property by a religious body; or

Renting of immovable property to an educational body …;

Explanation 1 – “for use in the course or furtherance of business or commerce” includes use of immovable property as factories, office buildings, warehouses, theatres, exhibition halls and multiple-use buildings

Explanation 2 – “renting of immovable property” includes allowing or permitting the use of space in an immovable property, irrespective of the transfer of possession or control of the said immovable property

23

RENTING OF IMMOVABLE PROPERTY

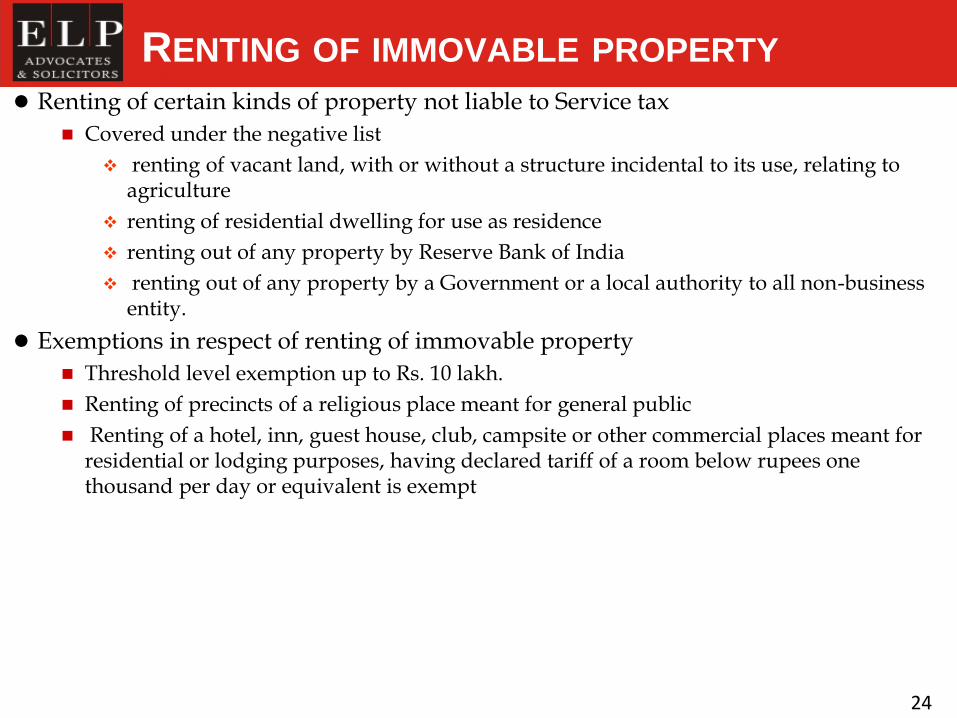

Renting of certain kinds of property not liable to Service tax

Covered under the negative list

renting of vacant land, with or without a structure incidental to its use, relating to agriculture

renting of residential dwelling for use as residence

renting out of any property by Reserve Bank of India

renting out of any property by a Government or a local authority to all non-business entity.

Exemptions in respect of renting of immovable property

Threshold level exemption up to Rs. 10 lakh.

Renting of precincts of a religious place meant for general public

Renting of a hotel, inn, guest house, club, campsite or other commercial places meant for residential or lodging purposes, having declared tariff of a room below rupees one thousand per day or equivalent is exempt

24

Mumbai1502, A Wing, Dalamal Towers, Nariman Point, Mumbai 400 021

Phone: + 91 22 6636 7000, Fax: + 91 22 6636 7172, Email: [email protected]

Delhi405-406, 4th Floor, World Trade Centre, Barakhamba Lane, New Delhi 110 001

Phone: + 91 11 4152 8400, Fax: + 91 11 4152 8404, Email: [email protected]

Ahmedabad801, Abhijeet III, Mithakali Six Roads, Ellisbridge, Ahmedabad-380 006

Phone: +91 79 6605 4480 / 8, Fax: +91 79 6605 4482, Email: [email protected]

Pune Suyog Fusion, 7th Floor, No.1, 97 Dhole Patil Road, Nr. Ruby Hall Clinic, Pune 411 001

Tel:+91 20 4146 7400 / 02 Fax:+91 20 4146 7499Email: [email protected]