Embed Size (px)

Citation preview

Volume 7 Issue 3

Named the Nation’s Best Newsletter by the National Association of Real Estate Editors

Individual Investors Feeling Squeezed Out By Bulk BuyersBy Octavio Nuiry, Staff Writer

Greg Fallacara is feeling squeezed.The Fort Myers, Fla., investor said he's

being forced out of the Florida foreclosure

market by all-cash buyers. He's paying moreand buying fewer properties because his offersare being outbid by all-cash Wall Street buyers.

He's finding it hard to compete with the floodof all-cash offers, with no contingencies,swooping into and snapping up properties he

was bidding on.“I've seen significant competition from

hedge funds here in Florida,” said Fallacara, a

part-time foreclosure flipper who typicallyquick-turns five or six properties a year. “Now

I'm only flipping two or four properties a year.They're driving up prices. I can't compete with

the deep-pocket investors.”The rental housing business, long domi-

nated by local mom-and pop investors like

Fallacara, has morphed into one of the trendi-est investments on Wall Street. Dozens of largeregional real estate investment firms and

national private equity companies such asBlackstone Group, Colony Capital andAmerican Residential Properties, are rushing

into the foreclosure landscape, purchasingthousands of properties for all-cash.

In January, Florida had nearly 30,000

Continued next page >

C O N T E N T S7 News Briefs

8 Legal Updates

9 My Ta k e : Gary Beasley, CEO

Waypoint Homes

1 1 S p o t l i g h t: Housing Climate

Change in Arizona

1 6 Ye a r-End 2012

Fo re c l o s u re and

S h o rt Sales Re p o rt

17 Ye a r-End 2012

Fo re c l o s u re Sales by St a t e

2 0 1 3M a r

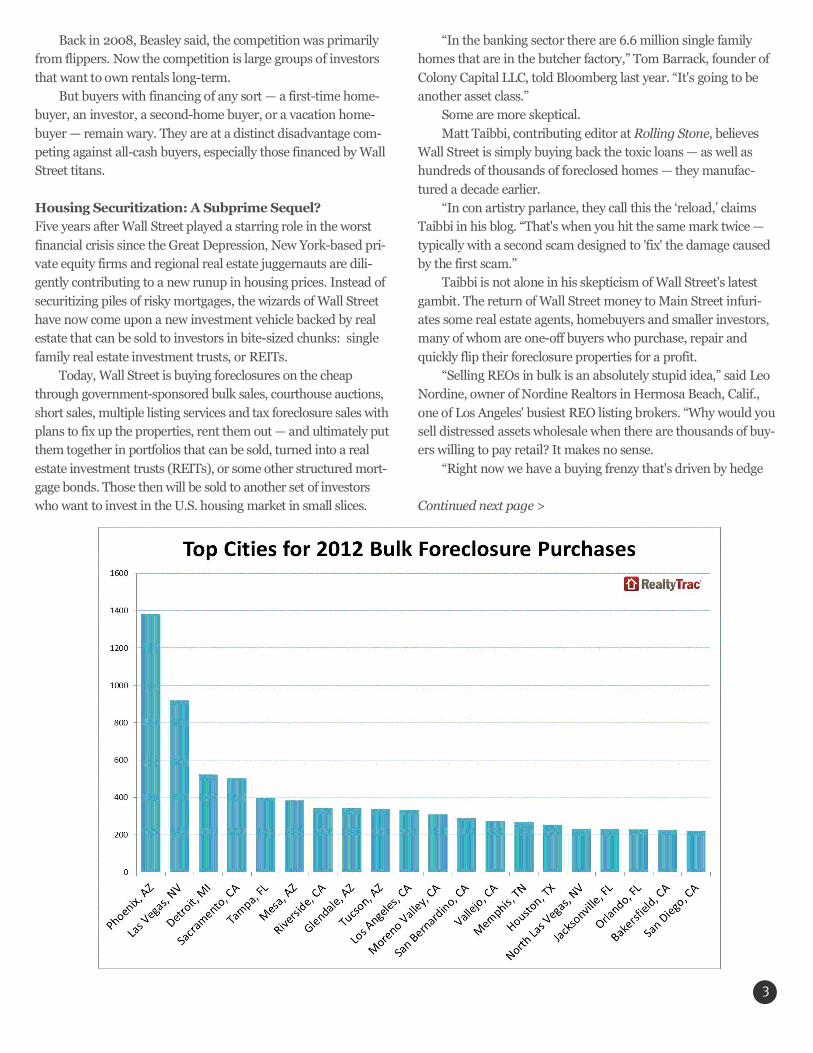

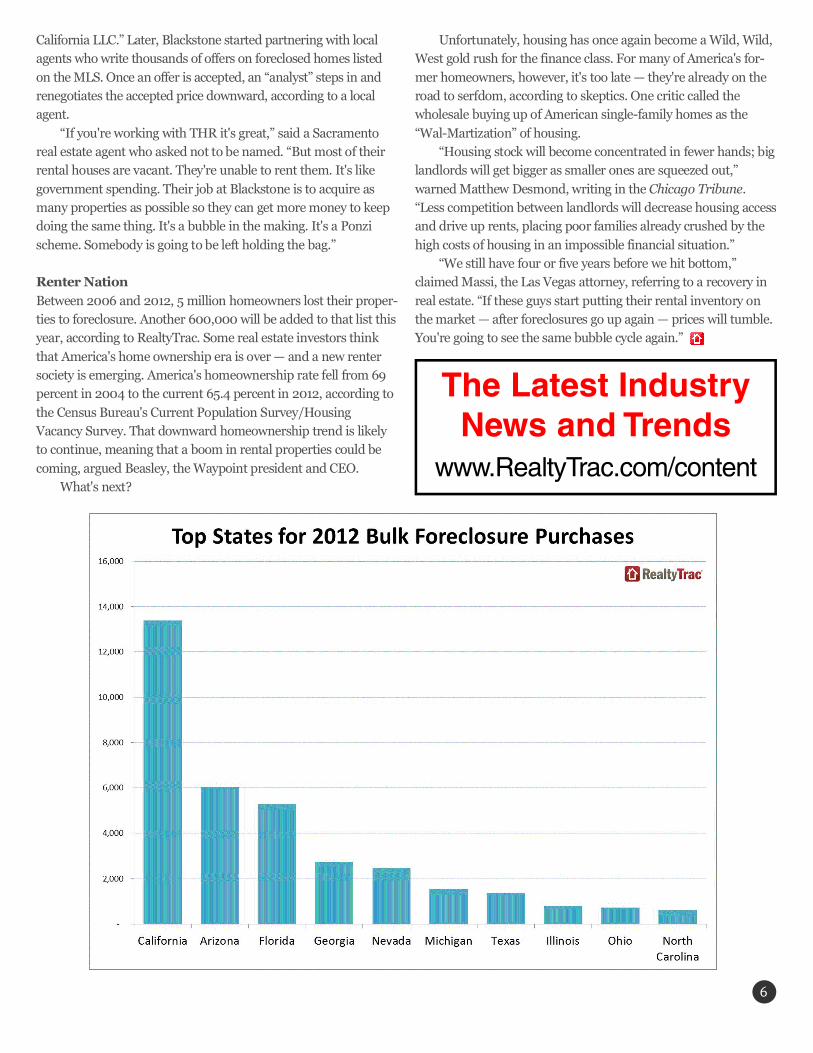

Bulk purchases are defined as sales involving buyers who purchased 10 or more foreclosure properties nationwide in 2012.

*

*

properties with a foreclosure filing — the most of any state — a n ddozens of investment firms have descended on the state to scoop

them up. Companies backed by Blackstone bought 199 Floridaproperties in some stage of foreclosure last year, according toRealtyTrac data. Various LLC companies that appear to be creat-

ed by American Homes 4 Rent purchased 340 Florida homes insome stage of foreclosure during the year. Another big foreclo-sure buyer was West Florida Wholesale Properties LLC, which

purchased 162 homes in some stage of foreclosure during theyear, the vast majority (153) in Hillsborough County — t h elargest county in the Tampa Bay metropolitan area.

Wall Street Cash Buyers GrowingMany smaller investors in hard-hit markets like Arizona,

California, Florida and Nevada can't compete with a flood of all-cash offers from well-heeled Wall Street war chests. Last year,through October, bulk buyers snapped up 39,423 foreclosure

properties nationwide repre-senting 5 percent of all foreclo-sure-related sales, according to

RealtyTrac. In Florida, the 5,289 fore-

closure purchases in 2012 by

buyers who purchased at least10 foreclosure propertiesnationwide during the year also

represented about 5 percent ofall foreclosure sales. However,that number could grow in

2013 as bulk buyers scramble tofind markets with more foreclo-sure inventory available.

In some markets the percentage of foreclosure sales going toinstitutional investors is higher. In Riverside and San Bernardinocounties in Southern California, for example, foreclosure sales to

bulk buyers represented about 8.5 percent of all foreclosuresales. In Maricopa County, Ariz., more than 10 percent of allforeclosure sales went to institutional investors.

Private equity firms have raised an estimated $8 billion to$10 billion to buy more than 100,000 single-family foreclosedhomes they plan to convert into rentals, according to news

reports. Marc Joseph, broker/owner of Marc Joseph Realty Fort

Myers, Fla., said that southwest Florida, like much of the

Sunshine State, is ground zero for the hedge fund buying craze.“We have a couple of big hedge funds that are here in Fort

Myers buying big time right now,” said Joseph, one of the lead-

ing REO listing agents in the region. “They are definitely drivingup prices. The little mom-and-pop investors are getting squeezedout. They're still buying, but they're buying less and paying more.

The big hedge funds are creating an artificial market.”Joseph said that Wall Street cash was pouring into every

corner of the distressed housing market: tax deed sales, REOsales, short sales and Multiple Listing Service (MLS) purchases.He said one LLC in particular — Sun Cny Properties LLC — w a s

particularly active in southwest Florida. “They're running upeverything,” claimed Joseph, referring to Sun Cny PropertiesLLC, and other Wall Street hedge funds.

“I've lost deals to Sun Cny Properties LLC,” said Fallacara,the Fort Myers flipper.

RealtyTrac data for 2012 shows Sun Cny Properties LLC

purchased 20 properties in some stage of foreclosure in LeeCounty, which comprises the Cape Coral-Fort Myers metro area.It was the fifth biggest bulk foreclosure buyer in terms of total

number of purchases during the year. In all, bulk buyers pur-chased 370 foreclosure properties in Lee County in 2012, repre-senting more than 5 percent of all foreclosure purchases in the

county for the year.According to RealtyTrac, Sun

Cny Properties made 60 per-

cent of its foreclosure purchasesin 2012 on properties that werescheduled for foreclosure auc-

tion, likely at the foreclosureauction itself. But the companyalso made some purchases of

bank-owned properties andsome properties that had start-ed the foreclosure process but

not yet been scheduled for thepublic foreclosure auction, likely

short sales.

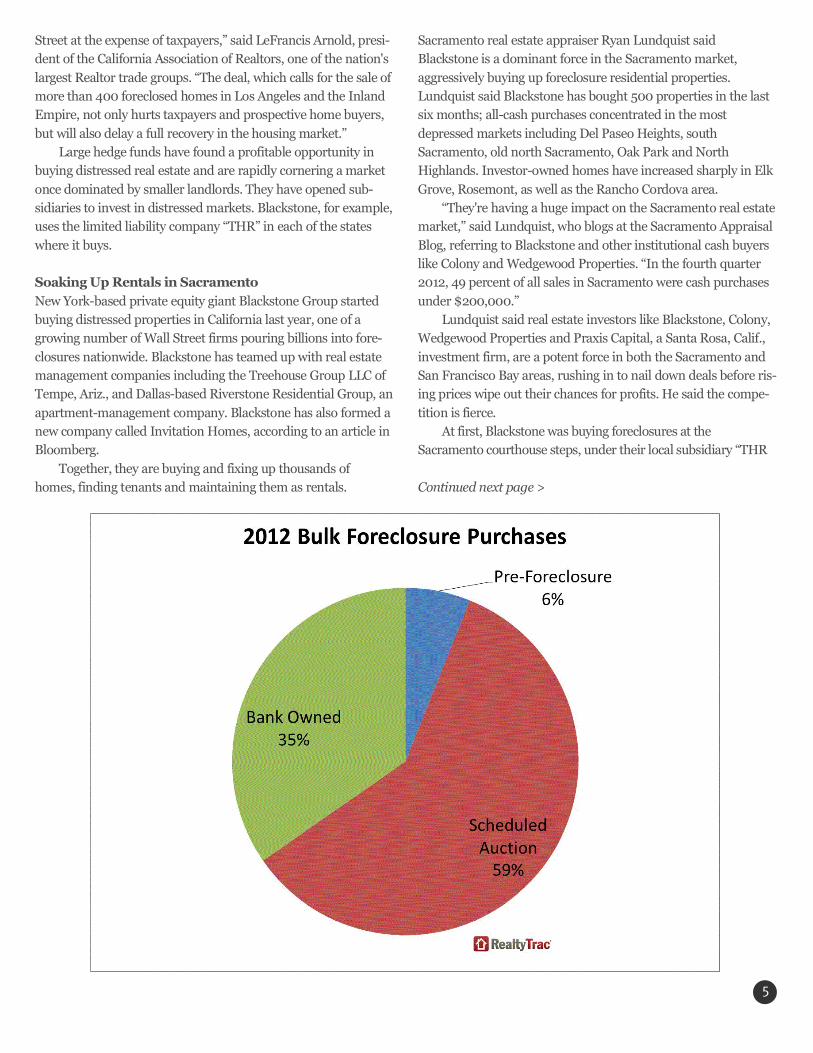

In Florida overall, 40 percent of bulk foreclosure purchaseswere of properties scheduled for foreclosure auction, while 38percent were of bank-owned properties and about 22 percent

were properties in the earliest stage of foreclosure. But the financial industry is hardly a monolith. And not all

Wall Street buyers have the same acquisition strategies. Some

buy in bulk. Others, like Oakland, Calif.-based Waypoint RealEstate Group LLC, prefer to purchase foreclosures one at a time.

“We have a different strategy than most companies in the

market,” said Gary Beasley, president and CEO of Waypoint,whose company buys foreclosed properties in Arizona,California, Georgia, Florida and Illinois. “We prefer the one-at-a-

time approach. We started out buying at the courthouse stepsexclusively in 2008. Now, we're buying almost exclusivelythrough the MLS. Today, we own about 3,400 homes. We'd like

to get to 10,000 by the end of the year.”

Continued next page >

2

3r “The little mom-and-pop investors are

getting squeezed out. They’re stillbuying, but they’re buying less and

paying more. The big hedge funds arecreating an artificial market.”

Marc Joseph

REO listing brokerin Fort Myers, Fla.

Back in 2008, Beasley said, the competition was primarily from flippers. Now the competition is large groups of investors

that want to own rentals long-term.But buyers with financing of any sort — a first-time home-

buyer, an investor, a second-home buyer, or a vacation home-

buyer — remain wary. They are at a distinct disadvantage com-peting against all-cash buyers, especially those financed by WallStreet titans.

Housing Securitization: A Subprime Sequel?Five years after Wall Street played a starring role in the worst

financial crisis since the Great Depression, New York-based pri-vate equity firms and regional real estate juggernauts are dili-gently contributing to a new runup in housing prices. Instead of

securitizing piles of risky mortgages, the wizards of Wall Streethave now come upon a new investment vehicle backed by realestate that can be sold to investors in bite-sized chunks: single

family real estate investment trusts, or REITs.Today, Wall Street is buying foreclosures on the cheap

through government-sponsored bulk sales, courthouse auctions,

short sales, multiple listing services and tax foreclosure sales withplans to fix up the properties, rent them out — and ultimately putthem together in portfolios that can be sold, turned into a real

estate investment trusts (REITs), or some other structured mort-gage bonds. Those then will be sold to another set of investorswho want to invest in the U.S. housing market in small slices.

“In the banking sector there are 6.6 million single familyhomes that are in the butcher factory,” Tom Barrack, founder of

Colony Capital LLC, told Bloomberg last year. “It's going to beanother asset class.”

Some are more skeptical.

Matt Taibbi, contributing editor at Rolling Stone, believesWall Street is simply buying back the toxic loans — as well ashundreds of thousands of foreclosed homes — they manufac-

tured a decade earlier. “In con artistry parlance, they call this the ‘reload,’ claims

Taibbi in his blog. “That's when you hit the same mark twice —

typically with a second scam designed to 'fix' the damage causedby the first scam.”

Taibbi is not alone in his skepticism of Wall Street's latest

gambit. The return of Wall Street money to Main Street infuri-ates some real estate agents, homebuyers and smaller investors,many of whom are one-off buyers who purchase, repair and

quickly flip their foreclosure properties for a profit.“Selling REOs in bulk is an absolutely stupid idea,” said Leo

Nordine, owner of Nordine Realtors in Hermosa Beach, Calif.,

one of Los Angeles' busiest REO listing brokers. “Why would yousell distressed assets wholesale when there are thousands of buy-ers willing to pay retail? It makes no sense.

“Right now we have a buying frenzy that's driven by hedge

Continued next page >

3

funds and Wall Street money. They completely control the mar-ket. They buy in bulk, but they don't disclose the price. It's a total

gift to Wall Street. That's Wall Street 101. Meanwhile, my inven-tory is the lowest it's been in 25 years. When guys that big areinvolved in the market, they play me like a piano.”

Brokers like Nordine, smaller investors, homebuyers andsome housing analysts view the new REO-to-rent buyers aspredatory carpetbaggers who are peddling foreclosed zombie

properties for big profits. Critics say the Wall Street-WashingtonAxis is once again up to its old tricks.

Another Las Vegas Housing Bubble?Las Vegas attorney Robert A. Massi, who does legal analysis onFox News' “Shattered Dreams” segment, said the Wall Street

cash is artificially inflating prices in the Las Vegas real estatemarket. He fears that institution-al cash is setting the foundation

for the next real estate bubble.“The problem is this: How

do you stop it?” said Massi, a

longtime legal expert inHenderson, Nev. “If you're in, it’sgreat. If you're out, it's terrible.

You can't embarrass these WallStreet guys. They don't care.”

Realtor Frank Napoli, with

Prudential Americana in LasVegas, disagreed.

He said institutional buyers

were helping stabilize the Valley,buying up excess supply, drivingup home prices and helping to

strengthen the local housingm a r k e t .

“If you're a listing agent, they're making offers you can't

refuse,” said Napoli, referring to the hedge fund cash buyers.“They come in with all-cash offers, with no contingencies. Iteliminates the headaches for me.”

The hedge fund housing gold rush started in 2011, when thefederal government began sending smoke signals to Wall Streetinvestors. Uncle Sam wanted to unload their growing inventory

of REO properties, and they needed the private sector’s help.Lured by President Barack Obama's plan to sell 250,000 govern-ment-owned REOs, the feds solicited ideas on how to turn the

government's foreclosure war chest into rental properties thatcould be managed by the private sector, i.e., Wall Street. InAugust 2011, the Federal Housing Finance Agency, teaming up

with the Department of Urban Housing and the TreasuryDepartment, released a request for ideas on how to dump theapproximately one quarter million foreclosed homes owned by

Fannie Mae, Freddie Mac and the Federal HousingAdministration.

Five months later, the Federal Reserve, advocating moregovernment and taxpayer intervention in the housing market,produced a 26-page housing white paper, endorsing the REO-to-

rent scheme. Fed Chairman Ben Bernanke, in an unprecedentedmove, encouraged Wall Street venture capitalists to become part-ners with the federal government in the largest land grab since

the Great Depression. Many observers saw this as gift to WallStreet. Others called it a backdoor bailout.

The federal government unveiled its bulk-buying REO pilot

program in August 2012, consisting of 2,500 properties, dividedin eight sub-pools located in Atlanta, Chicago, Las Vegas, LosAngeles-Riverside, Calif., Phoenix, and south, central and west-

ern Florida. Not only was the government willing to sell the fore-closed properties at steep dis-counts, they subsidized the bulk-

buyers with favorable financing.On Sept. 6, 2012, Pacifica

Companies, a little-known San

Diego real estate investmentfirm, was the first company toemerge as the winner in FHFA's

bulk pilot program, purchasingan interest in 699 Fannie Maerepos throughout Florida for

$12.3 million, which gives them10 percent of equity cash flow,shifting to 50 percent after hit-

ting a threshold of $49.2 mill-lion, according FHFA.

A day later, Fannie

announced that the CogsvilleGroup, an obscure New York

private equity firm led by former professional soccer player

Donald Cogsville, bought an interest in 94 Fannie foreclosures inChicago for $2.1 million, for which they get 10 percent of equitycash flow shifting to 50 percent after hitting a threshold of $8.39

million. A third company, Colony Capital, using the amusingly trans-

parent name of CSFR FM 2012 -1 U.S. WEST, LLC, paid $34.1

million for an interest in 970 properties in Phoenix, Las Vegasand Southern California valued at $176 million, according toFHFA. Similar to the previous deals, Colony Capital received 10

percent equity cash flow that shifts to 50 percent after hitting a threshold of $136.47 million.

“Fannie Mae and FHFA's decision to move forward with the

REO bulk sale in California amounts to another gift to Wall

Continued next page >

4

“Why would you sell distressed assetswholesale when there are thousands

of buyers willing to pay retail? Itmakes no sense. Right now we have abuying frenzy that’s driven by hedgefunds and Wall Street money. They

completely control the market.”

Leo NordineREO listing brokerin Hermosa Beach,Calif.

5

Street at the expense of taxpayers,” said LeFrancis Arnold, presi-dent of the California Association of Realtors, one of the nation's

largest Realtor trade groups. “The deal, which calls for the sale ofmore than 400 foreclosed homes in Los Angeles and the InlandEmpire, not only hurts taxpayers and prospective home buyers,

but will also delay a full recovery in the housing market.”Large hedge funds have found a profitable opportunity in

buying distressed real estate and are rapidly cornering a market

once dominated by smaller landlords. They have opened sub-sidiaries to invest in distressed markets. Blackstone, for example,uses the limited liability company “THR” in each of the states

where it buys.

Soaking Up Rentals in Sacramento

New York-based private equity giant Blackstone Group startedbuying distressed properties in California last year, one of agrowing number of Wall Street firms pouring billions into fore-

closures nationwide. Blackstone has teamed up with real estatemanagement companies including the Treehouse Group LLC ofTempe, Ariz., and Dallas-based Riverstone Residential Group, an

apartment-management company. Blackstone has also formed anew company called Invitation Homes, according to an article inBloomberg.

Together, they are buying and fixing up thousands of homes, finding tenants and maintaining them as rentals.

Sacramento real estate appraiser Ryan Lundquist saidBlackstone is a dominant force in the Sacramento market,

aggressively buying up foreclosure residential properties.Lundquist said Blackstone has bought 500 properties in the lastsix months; all-cash purchases concentrated in the most

depressed markets including Del Paseo Heights, southSacramento, old north Sacramento, Oak Park and NorthHighlands. Investor-owned homes have increased sharply in Elk

Grove, Rosemont, as well as the Rancho Cordova area.“They're having a huge impact on the Sacramento real estate

market,” said Lundquist, who blogs at the Sacramento Appraisal

Blog, referring to Blackstone and other institutional cash buyerslike Colony and Wedgewood Properties. “In the fourth quarter2012, 49 percent of all sales in Sacramento were cash purchases

under $200,000.”Lundquist said real estate investors like Blackstone, Colony,

Wedgewood Properties and Praxis Capital, a Santa Rosa, Calif.,

investment firm, are a potent force in both the Sacramento and San Francisco Bay areas, rushing in to nail down deals before ris-ing prices wipe out their chances for profits. He said the compe-

tition is fierce. At first, Blackstone was buying foreclosures at the

Sacramento courthouse steps, under their local subsidiary “THR

Continued next page >

California LLC.” Later, Blackstone started partnering with localagents who write thousands of offers on foreclosed homes listed

on the MLS. Once an offer is accepted, an “analyst” steps in andrenegotiates the accepted price downward, according to a locala g e n t .

“If you're working with THR it's great,” said a Sacramentoreal estate agent who asked not to be named. “But most of theirrental houses are vacant. They're unable to rent them. It's like

government spending. Their job at Blackstone is to acquire asmany properties as possible so they can get more money to keepdoing the same thing. It's a bubble in the making. It's a Ponzi

scheme. Somebody is going to be left holding the bag.”

Renter Nation

Between 2006 and 2012, 5 million homeowners lost their proper-ties to foreclosure. Another 600,000 will be added to that list thisyear, according to RealtyTrac. Some real estate investors think

that America's home ownership era is over — and a new rentersociety is emerging. America's homeownership rate fell from 69percent in 2004 to the current 65.4 percent in 2012, according to

the Census Bureau's Current Population Survey/HousingVacancy Survey. That downward homeownership trend is likelyto continue, meaning that a boom in rental properties could be

coming, argued Beasley, the Waypoint president and CEO. What's next?

Unfortunately, housing has once again become a Wild, Wild,West gold rush for the finance class. For many of America's for-

mer homeowners, however, it's too late — they're already on theroad to serfdom, according to skeptics. One critic called thewholesale buying up of American single-family homes as the

“Wal-Martization” of housing.“Housing stock will become concentrated in fewer hands; big

landlords will get bigger as smaller ones are squeezed out,”

warned Matthew Desmond, writing in the Chicago Tribune.“Less competition between landlords will decrease housing accessand drive up rents, placing poor families already crushed by the

high costs of housing in an impossible financial situation.”“We still have four or five years before we hit bottom,”

claimed Massi, the Las Vegas attorney, referring to a recovery in

real estate. “If these guys start putting their rental inventory onthe market — after foreclosures go up again — prices will tumble.You're going to see the same bubble cycle again.”

6

The Latest IndustryNews and Trends

w w w. R e a l t y Tra c . c o m / c o n t e n t

7

Victims to Collect Up to$125,000 for Fo re c l o s u re sStarting in March, borrowers who were fore-closed on by “robo-signing” banks will beginreceiving cash payments ranging from hundreds

of dollars to as much as $125,000.The payments are part of an $8.5 billion

deal struck in January with 13 banks that

abruptly ended foreclosure reviews of some 4.2million mortgages after widespread mistakes were found in docu-ments used to foreclose millions of American homes following the

housing bust.“The modified consent orders will provide $3.6 billion in pay-

ments to 4.2 million eligible borrowers and $5.7 billion in addition-

al foreclosure prevention assistance” said Thomas Curry,Comptroller of the Currency, in a recent speech referring to loanmodifications and loan forgiveness. “That's the largest cash payout

of any foreclosure-related settlement to date. Under this approachborrowers will be contacted and we expect checks will start to goout by the end of March.”

Critics say the settlement hasn't worked as planned.Banks “have dragged their feet in modifying first mortgages,

much less agreeing to forgive part of the principal on homes that

are underwater,” said New York City lawyer Elizabeth M. Lynch ina New York Times opinion piece. “The problem involves secondmortgages, which millions of homeowners took out during the

housing bubble. The second mortgages have given the banks aloophole: each dollar a bank forgives goes toward fulfilling its obli-gation under last year's settlement. But many lenders have made it

a point to almost exclusively modify secondary loans while all butignoring the troubled, larger primary mortgages.”

The lenders are Aurora Bank, Bank of America, Citibank,

Goldman Sachs, HSBC, JPMorgan Chase, MetLife Bank, MorganStanley, PNC, Sovereign Bank, SunTrust, U.S. Bank and WellsF a r g o .

Sources: Office of Comptroller of the Currency

The New York Times

Re p o rt: Eliminate Fannie and Freddie A bipartisan group of former senators and U.S. housing secretariescalled for the elimination of government-sponsored enterprises(GSEs) Fannie Mae and Freddie Mac as part of a broader effort to

have private lenders take on more of the risk of supplying credit to

the U.S. housing market.The report, “Housing America's Future: New Direction for

National Policy,” prepared by the Bipartisan Policy Center, a

Washington think tank, aims to reform the housing finance industrywith greater influence from the private sector and a limited govern-ment role.

Under the plan, banks and other private lenders would take thelead not only in originating mortgages, but in issuing mortgage-backed securities as well.

Chief among the recommendations was eliminating Fannie andFreddie and replacing them with a completely government-ownedentity called the “Public Guarantor,” which would not buy or sell

mortgages, but would guarantee investors’ payment of principal andinterest on securities.

While it was necessary for the government to step in when the

market collapsed five years ago, the government's role in financinghousing has ballooned beyond what is sustainable, the commissionargued. Fannie, Freddie and the Federal Housing Administration

now support 90 percent of single-family mortgages.“Reducing the government footprint and encouraging greater

participation by risk-bearing private capital will protect taxpayers

while providing for a greater diversity of funding sources,” said thereport, a product of a 21-member commission that met over 16months.

The group's housing commission is headed by former U.S. Sens.Christopher “Kit” Bond, a Republican and former governor ofMissouri; former Housing and Urban Development Secretaries

Henry Cisneros, a Democrat who served in the Clinton administra-tion; and Mel Martinez, a Republican who served in the George W.Bush administration; and George Mitchell, formerly the Democratic

Senate Majority Leader.

S o u r c e :Bipartisan Policy Center

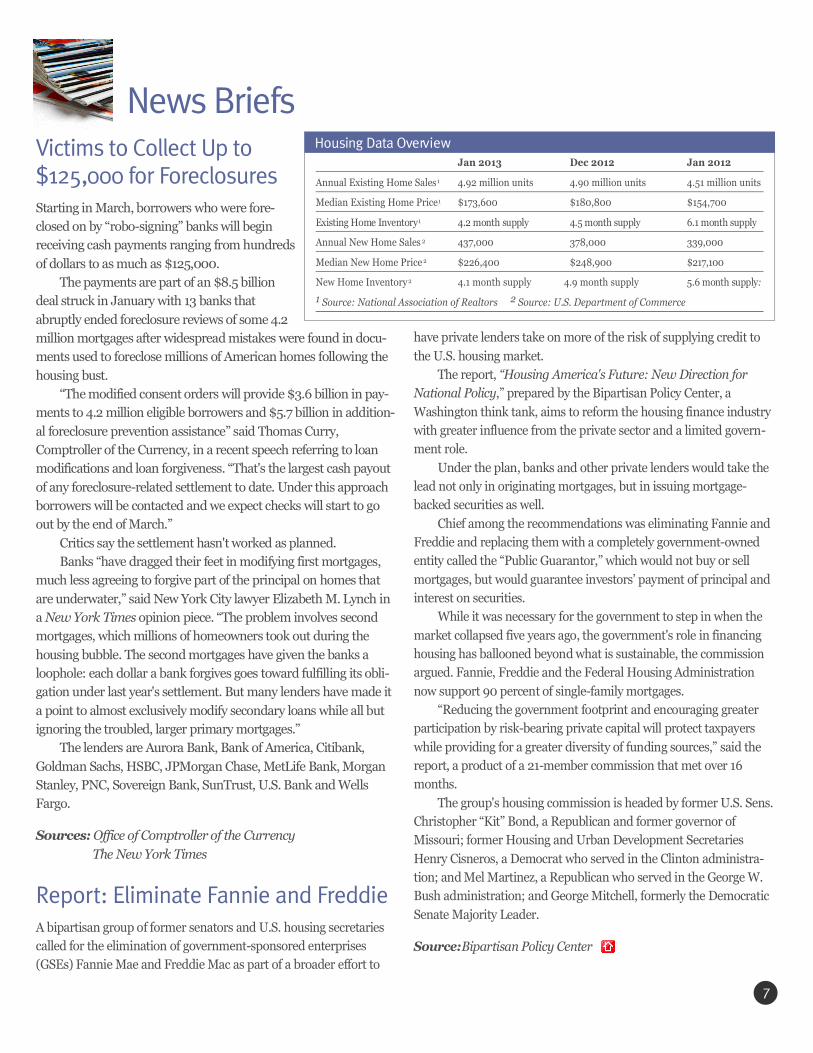

News BriefsJan 2013 Dec 2012 Jan 2012

Annual Existing Home Sales1 4.92 million units 4.90 million units 4.51 million units

Median Existing Home Price1 $173,600 $180,800 $154,700

Existing Home Inventory1 4.2 month supply 4.5 month supply 6.1 month supply

Annual New Home Sales 2 437,000 378,000 339,000

Median New Home Price 2 $226,400 $248,900 $ 2 1 7 , 1 0 0

New Home Inventory2 4.1 month supply 4.9 month supply 5.6 month supply:

1 Source: National Association of Realtors 2 Source: U.S. Department of Commerce

Housing Data Ove rv i e w

WA Supreme Court Holds Tr u s t e eViolated Consumer LawThe Washington Supreme Court held in late February that a well-known foreclosure trustee violated the state consumer protectionlaw when it falsely notarized legal documents.

In overturning an appeal’s court ruling, the high court alsoheld that the trustee — Quality Loan Service — further violatedconsumer protection law by not considering requests to delay the

auction of a Whidbey Island home, reported The Seattle Times.In his opinion for the court, Justice Tom Chambers wrote

that Quality “has demonstrated little understanding or regard for

Washington law. Foreclosure trustees are not simply agents forthe lender. The power to sell another person’s property — o f t e nthe family home itself — is a tremendous power to vest in any-

one’s hands.” The case dates back to 2008 when Washington Mutual and

its trustee, Quality Loan Service, were sued by Puget Sound

Guardians for allowing the sale at auction of homeowner DorothyHalstien’s home for one dollar more than was owed on the mort-gage. Halstein lost $150,000 in equity and the new owner quickly

flipped the property for $235,000, the T i m e s story explained.Repeated requests by Puget Sound Guardians to delay the

sale were rejected by Quality, which the court found to have false-

ly notarized the date on the notice of trustee sale — a practice ithad trained its notaries to do regularly between 2004 and 2007.

Source: The Seattle Times

IL High Court Approves New Ru l e sThe Illinois Supreme Court has adopted new rules that willchange the way the mortgage foreclosure process is handled bylenders. The new rules take effect June 1.

The rules require lenders to file an affidavit with the courtshowing they have exhausted all efforts to work out a loan modi-fication with the homeowner before being allowed to proceed

with the foreclosure. The rules are aimed at helping out borrowers who are either

already in foreclosure or well on their way towards being fore-

closed on.With almost two years going into their drafting, the rules

have some overlap with the new mortgage servicing rules recent-

ly released by the Consumer Financial Protection Bureau, whichare due to go into effect January 2014.

Source: Chicago Tribune

B i p a rtisan Lawmakers Propose Bill toReform Fannie and Fre d d i eSenators from both sides of the political aisle got together to agreeon a bill that would restrict how monies generated by fee increasesfrom Fannie Mae and Freddie Mac are spent.

In particular, the bill, titled the “Jumpstart GSE Reform Act” isintended to keep lawmakers from using those increased fees to payfor spending increases and tax cuts.

Sponsored by Sen. Bob Corker, R-Tenn., Sen. Mark Warner, D-Va., Sen. David Vitter, R-La. and Sen. Elizabeth Warren, D-Mass.,the bill shows that “Republicans and Democrats do agree on the

urgency required to reform the mortgage finance system,” Vittersaid in a statement, according to a report in The Wall StreetJ o u r n a l.

The bill would also keep the Obama Administration from sell-ing off preferred shares in the GSEs without the approval ofC o n g r e s s .

Source: The Wall Street Journal

Transfer of Mortgage SettlementMoney to State General Fund OKThe Arizona Court of Appeals ruled March 12 that Arizona AttorneyGeneral Tom Horne did not misappropriate funds allocated from thestate’s $1.6 billion share of the national mortgage settlement when he

transferred $50 million to the state general fund to help balance theb u d g e t .

Attorney Tim Hogan argued that the mortgage settlement

required funds be spent only on services benefitting homeownerssuch as financial counselors, legal assistance, and services for home-owners facing foreclosure.

Writing for the court, Justice Jon Thompson rejected the arg-ment. Instead, Thompson held that Horne had the discretion to givethe funds to the state Legislature.

In Thompson’s view the funds became the property of the state,and thus Horne was powerless to restrict how those funds are dis-tributed on his own.

According to a published report from Howard Fischer CapitolMedia Services, most of the settlement funds are meant for helpingto reduce homeowner mortgages and to compensate those who have

already lost their homes to foreclosure.

Source: Howard Fischer Capitol Media Services

Legal Updates

8

9

Plug any real estate-related term into a search engine and you'relikely to find a binary debate: owning versus renting, fixed rateversus adjustable, and, most recently, investors versus individual

buyers. While I can see the attraction of a simple story, to mymind this is an old-fashioned way of looking at a very new realestate market — one that's been utterly and completely

transformed by the events of the past decade. To continue to make progress on solving the foreclosure

crisis, we need to focus on a multifaceted market, where a variety

of alternatives can co-exist and work together to solve this (still)very large problem. Companies that own portfolios of singlefamily homes have emerged to meet the growing need for

high-quality rental housing and operate on the scale that themagnitude of the challenge demands.

Let's start with the growing demand for rental housing. The

nation's home ownership rate is currently 65.4 percent, accordingto NerdWallet, the lowest it has been in 16 years and more thanfour percentage points lower than its 2005 peak. Based on one

analyst's views that each one percentage point drop in thehomeownership rate creates a need for an additional 750,000rental units, approximately 3 million more rental units are

needed today compared to before the crash.Add in the effects of tight credit, which means more people

don't have the higher down payments and credit scores banks

now require, the residual skepticism about the wisdom ofhomeownership generated by the bust, and the siren song ofwhat venture capitalist Mary Meeker calls an “asset light” lifestyle

and you're looking at an even larger demand: the share ofhouseholds who rent is estimated to be 36 percent by 2015, anincrease of a full five percentage points from 2005.

According to the U.S. Census, there were almost 115 millionU.S. households in 2010, implying about 41 million householdswill rent in 2015. While it's hard to calculate precisely how many

of those will want to rent single-family homes, at an average of

Continued next page >

MyTa k e :

New Problems Require New SolutionsGary Beasley, President and CEO, Waypoint Homes, Inc.

2.6 persons per household, it's likely that many will.Next, let's take a look at supply. Almost 11 million homeown-

ers have negative equity in their homes, and almost five and ahalf million single family mortgage loans are in some stage ofdelinquency. Again citing the analyst's study, if just half of those

distressed loans were resolved via foreclosure or short sale, thatwould equate to 2.7 million homes that will need to be repur-posed and absorbed into the market.

Finally, let's take a look at scale and impact. While an addi-tional 2.7 million homes may not sound like much compared tothe 41 million households that may be renting in 2015, to bridge

even that small portion of the gap between supply and demand isa huge challenge — and a hugely expensive one. At an average of$25,000 per home, as just one

example, it would require morethan $67 billion to renovatethese homes — and that's not

counting the $270 billion itwould cost to purchase them,even at a very conservative

$100,000 each. The alternative isn't pretty.

The Department of Housing

and Urban Development(HUD) estimates that everyforeclosure costs local govern-

ments $19,277 and the eightadjacent neighbors $14,459.Looking just at the 2.7 million

number cited above, we're talk-ing about a cost to local govern-ments of $52 billion — and to

these properties' 21.6 millionneighbors, a cost of more than$39 billion in lost wealth.

Of course, these numbersare not set in stone. There'sconsiderable debate about how

many homes are or will beunderwater, and about howmany of those will progress

through the foreclosure/shortsale pipeline (not to mentionhow quickly the economy will improve, and how quickly the rate

of household formation will respond). But no matter how youlook at it, these are staggering numbers, and they may actuallyunderestimate some of the impacts when you factor in social as

well as economic costs. Given the scale of the problem, these are,quite simply, not numbers that mom-and-pop investors and non-profits can swallow.

Which brings me back to my introductory point. Residentialreal estate in the United States can't be characterized by simple

alternatives — too much has changed too quickly — and no singlesolution will solve the problem we're facing, which is new in bothits scale and potential impact.

Residential housing is the largest real estate asset class in theU.S., with more than 130 million units worth approximately $17trillion. The advent of companies with large portfolios in the sin-

gle-family home sector generates jobs, prevents blight, and offersquality homes for the growing number of Americans who want orneed to rent.

This market is large enough for everyone. Non-profits bringeducational expertise and grant funds that can help their clients

make that leap from renting to

owning. Banks have the capitaland know-how to underwriteloans for those ready and able

to purchase. Mom and popowner-investors can have a pos-itive impact on their local

neighborhoods. Investors bring capital and the

ability to scale — to buy and

renovate 50 or 100 or 500homes a month, and get themout on the market so that fami-

lies can live in them. As Japanese real estate mogul

Akira Mori noted, “In my expe-

rience, in the real-estate busi-ness, past success stories aregenerally not applicable to new

situations. We must continuallyreinvent ourselves, respondingto changing times with innova-

tive new business models.”

Gary Beasley became aninvestor and advisory boardmember at Waypoint Homes

in early 2009, eventually join -ing full-time as a managing

director in December 2011 and becoming President and CEO in

January 2013. Prior to joining Waypoint, Gary served as bothan operating executive and principal investor across a widerange of industries including hospitality (Joie de Vivre), real

estate (Zip Realty), consumer Internet, and clean tech. Garyholds a B.A. in Economics from Northwestern University and anM.B.A. from Stanford Graduate School of Business.

10

“The advent of companies

with large portfolios in the

single-family home sector

generates jobs, prevents

blight, and offers quality

homes for the growing number

of Americans who want or

need to rent...Given the scale

of the problem, these are,

quite simply, not numbers

that mom-and-pop investors

and non-profits can swallow.”

11

S p o t l i g h t

Housing Climate ChangeRoils Arizona Market

By Joel Cone, Staff Writer

After three years with the third highest state foreclosure total inthe nation, the Grand Canyon State cooled off substantially in

2012, coming in with the eighth highest state foreclosure total forthe year.

But the cool down in foreclosure activity is not deterring real

estate investors from pursuing potential investment propertiesvery much at this point. Instead, it's prompting them to re-thinktheir investment strategy now that multiple offers are common-

place at the low-end price range, and because other types ofinvestors — primarily the large institutional type — have enteredthe game.

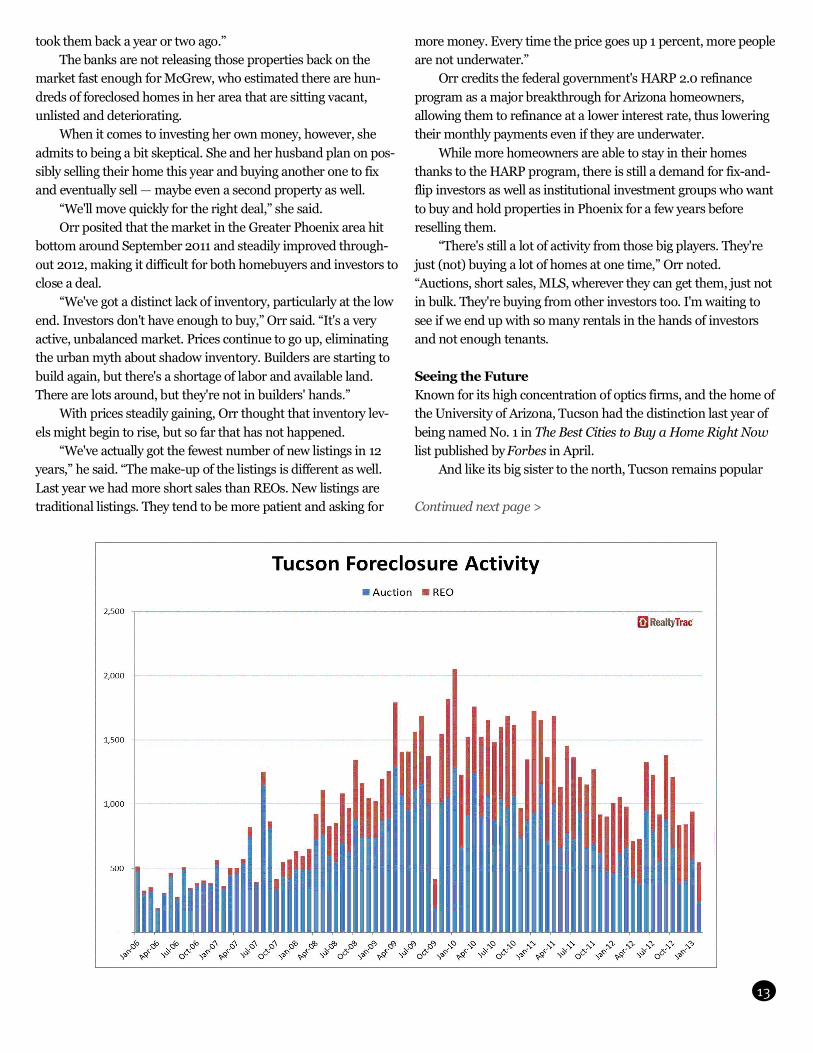

Any discussion regarding the foreclosure market in Arizonareally boils down the state's two largest cities — Phoenix andTucson. Both have seen fast and furious changes in the make-up

and size of their available real estate inventory as bank-ownedproperties (REOs) have taken a back seat, and short sales remaina popular choice, albeit harder to acquire.

Instead, a resurgence of traditional sales and new home sales

is expected to take hold in the not-too-distant future.

A Buying Frenzy in PhoenixIn Phoenix, which B u s i n e s s w e e k ranked 44th amongst A m e r i c a ' s50 Best Cities in September 2012 — a wildfire of foreclosure

activity for the past several years has attracted real estateinvestors from other states (particularly California), and othercountries (especially Canada, where their dollar buys a lot more

in the United States).Now the desert winds have taken a dramatic shift for the bet-

ter, according to the latest statistics for the Greater Phoenix hous-

ing market, as reported by Michael J. Orr, director of the Centerfor Real Estate Theory and Practice at Arizona State University.

As of December 2012, the median sales price in the metro

area increased 34 percent from December 2011, and the averagesales price per square foot rose 27 percent for the same period.

Continued next page >

Phoenix City Hall Tucson City Hall

Overall supply of inventory was down 6 percent betweenJanuary 2012 and January 2013, and the supply of distressed

homes dropped 42 percent over the same period. New homesales were up 30 percent while the volume of resales climbed 65percent year-over-year.

Phoenix foreclosure starts in February 2013 were down 68percent from a year ago, while bank repossessions (REO)dropped 48 percent during the same period, according to

RealtyTrac. Meanwhile, the average foreclosure price is skyrock-eting as supply shrivels up. The average price of a home in somestage of foreclosure or bank-owned during the fourth quarter of

2012 was $158,786 in the Phoenix metro area, up 26 percentfrom a year ago although still 21 percent below the average priceof a non-distressed property, according to RealtyTrac.

Orr's report shows that investors purchased 32 percent of allresidential properties in 2012, but that is down from the peak of40 percent reported in July 2012.

Most important to investors are the homes sold at a discountfrom full market value. Orr's report shows some dramaticdeclines overall:

Investor flips down 20 percent Short sales and pre-foreclosures down 36 percent

Bank-owned (REO) properties down 55 percent Fannie Mae and Freddie Mac owned properties down

70 percent

HUD sales down 44 percent Third party purchased at trustee sales down 51 percent

According to Orr, most of the foreclosure activity in the twocounties that make up the metro area — Maricopa and Pinalcounties — was not REO properties last year. Both counties

reported a 50 percent reduction in the number of REO proper-ties. Bank-owned properties accounted for just 15 percent of all

residential home sales in Maricopa County and 8 percent of allhome sales in Pinal County, according to RealtyTrac.

The downward trend in bank-owned homes has not escaped

the attention of Scottsdale-based investor Michelle McGrew whorefers to herself and her husband as “slow-motion flippers,”meaning that they buy and hold longer than the typical 90 days

before selling off the property. In the upscale market where theylive, it was not that long ago that it seemed like every other housein the neighborhood was bank-owned, McGrew said. Now, two

years later, there are no bank-owned REOs to be found.“What I'm paying attention to, as somebody who sniffs

around real estate a lot, is that right now the market here is turn-

ing into a seller's market,” she said. “There's hardly anything forsale. It's better than it's been in the last four years. Builders areabout to go great guns. Last several months there's been a bur-

geoning glut of customers willing to wait for a new home.”Homes priced at $300,000 and below are getting 15 offers

within hours after the listing comes out, according to McGrew.

Her friends who flip real estate are telling her that those proper-ties are being sucked up by investors with all-cash transactions.

But even with prices going up an estimated 23 percent last

year, McGrew said that any property under $750,000 that ispriced right is not going to be on the market very long. Even mil-lion dollar properties are seeing multiple offers.

McGrew and her husband bought the home they live in backin January 2011 at a trustee's sale they found listed on RealtyTrac.“It was the easiest thing we ever did. The kicker was, on this

house we never saw the inside. There was a video online, but itdid not show the secondary bedrooms.”

Starting with a minimum bid of $983,000, the McGrews

bought their house at auction for slightly over $1 million. At thesame time the house next door was up for sale and had 13 offerson it before selling for $1.15 million, about $250,000 over asking

price. “They had 13 offers from the Friday morning it hit the MLS

to the following Monday morning,” McGrew noted.

Although she believes that many investors paid too much forthe houses they've purchased over the past few years, McGrewstill sees plenty of opportunity for investors if the banks get their

act together and put inventory on the market.“All those banks that went into receivership and ended up

with the FDIC taking them over, I'm still running into those prop-

erties,” she said. “The banks themselves that have taken proper-ties back are sitting on them. This one I got is 6,100 square feet.These houses are between 5,000 and 7,000 square feet, and the

bank is sitting on them and they're not for sale. I know the bank

Continued next page >

12

“Investors don’t have enough to buy.It’s a very active, unbalanced market.Prices continue to go up, eliminatingthe urban myth of shadow inventory.Builders are starting to build again,

but there’s a shortage of laborand available land.”

Michael J. Orr

Director of the Centerfor Real Estate Theoryand Practice at ArizonaState University

took them back a year or two ago.”The banks are not releasing those properties back on the

market fast enough for McGrew, who estimated there are hun-

dreds of foreclosed homes in her area that are sitting vacant,unlisted and deteriorating.

When it comes to investing her own money, however, she

admits to being a bit skeptical. She and her husband plan on pos-sibly selling their home this year and buying another one to fixand eventually sell — maybe even a second property as well.

“We'll move quickly for the right deal,” she said.Orr posited that the market in the Greater Phoenix area hit

bottom around September 2011 and steadily improved through-

out 2012, making it difficult for both homebuyers and investors toclose a deal.

“We've got a distinct lack of inventory, particularly at the low

end. Investors don't have enough to buy,” Orr said. “It's a veryactive, unbalanced market. Prices continue to go up, eliminatingthe urban myth about shadow inventory. Builders are starting to

build again, but there's a shortage of labor and available land.There are lots around, but they're not in builders' hands.”

With prices steadily gaining, Orr thought that inventory lev-

els might begin to rise, but so far that has not happened. “We've actually got the fewest number of new listings in 12

years,” he said. “The make-up of the listings is different as well.

Last year we had more short sales than REOs. New listings aretraditional listings. They tend to be more patient and asking for

more money. Every time the price goes up 1 percent, more peopleare not underwater.”

Orr credits the federal government's HARP 2.0 refinance

program as a major breakthrough for Arizona homeowners,allowing them to refinance at a lower interest rate, thus loweringtheir monthly payments even if they are underwater.

While more homeowners are able to stay in their homesthanks to the HARP program, there is still a demand for fix-and-flip investors as well as institutional investment groups who want

to buy and hold properties in Phoenix for a few years beforereselling them.

“There's still a lot of activity from those big players. They're

just (not) buying a lot of homes at one time,” Orr noted.“Auctions, short sales, MLS, wherever they can get them, just notin bulk. They're buying from other investors too. I'm waiting to

see if we end up with so many rentals in the hands of investorsand not enough tenants.

Seeing the FutureKnown for its high concentration of optics firms, and the home ofthe University of Arizona, Tucson had the distinction last year of

being named No. 1 in The Best Cities to Buy a Home Right Nowlist published by F o r b e s in April.

And like its big sister to the north, Tucson remains popular

Continued next page >

13

with real estate investors even with the economic winds of changesweeping through.

“We have a very cyclical market here,” said Bob Zachmeier,

broker/owner of Win3 Realty in Tucson. “We don't have daylightsavings here so it's dark at 5 to 5:30 in the winter. In the summerwe can show homes until 8:30 to 9 o'clock.

“We always sell twice as many homes in June as in January,”he added. “If we look back over the past 21 years we sell about 15percent of our inventory in wintertime and 26 to 27 percent in the

summer. In the summertime we usually have slightly less than afour-month supply. In the winter it's normally about a seven-month supply. We're running almost summertime numbers in

J a n u a r y . ”Zachmeier characterizes it as a market that's moving the

right direction, and January numbers from the Tucson

Association of Realtors bear that out. For the most recentmonth reported TAR noted a 16 percent year-over-year increasein median sales price from

January 2012 and a 15 percentincrease in average list pricecompared to a year ago. Sales

volume increased 12 percent forthe same period, while unit saleswere down 3 percent.

Unlike some areas of thecountry where inventory is notbeing added quickly enough, TAR

reported a 58 percent increase innew listings year-over-year, and a40 percent monthly increase

from December.Two items of special impor-

tance for investors to know are: 1)

the average days on the marketwent up two days to 57 days in January, but were down 29 per-cent from the 80 days reported in January 2012; and 2) cash

sales accounted for 37 percent of sales in January, up from 33percent reported the previous month.

“Activity at the entry level — between $100,000 and

$150,000 — is very competitive. There's multiple offers in a lot ofcases,” said Realtor Shawn Polston with Keller Williams SouthernArizona. “There's not that same frenzy at higher price ranges

above $200,000. It's more of an equal market until you get above$400,000. At that level it's still a buyer's market.”

At the low end, Polston sees investors buying homes built

in 2005 and 2006. The problem is that institutional investorshave swooped into the area and are gobbling up a lot of thoseproperties.

“Institutional investors are bringing more competition to the

table. There's a lot of moms and pops pumping some cash outtoo. They're not buying 100 properties at a time but they are buy-ing two to three. The financing in the non-owner occupied space,

we're seeing that financing remains very tight and making it veryhard for them to compete,” he said.

Zachmeier noted that out-of-state investors and Canadians

are still coming in droves to Tucson to buy property. Plus otherbig players such as American Homes 4 Rent, which has pur-chased 265 properties in the Tucson metro area during the past

12 months, he explained. “They seem to be looking for houses they can rent out for 10

percent of the purchase price, which is doable. They intend to

hold them they say for five to seven years and then they can sellthem at a pretty significant increase,” Zachmeier noted.

While the Tucson metro area may not have the volume of

distressed properties it once had, Polston said he has seen moreshort sales in the market but fewer bank-owned properties.

“There still seems to be quite a

few HUD foreclosures and FannieMae properties out there,” he said.

RealtyTrac's data for 2012

confirms that the number of bank-owned (REO) sales was down near-ly 18 percent in Pima County last

year. On the other hand, the num-ber of pre-foreclosure sales (includ-ing short sales and properties sold

at the foreclosure auction)increased 33 percent for the regionfor 2012. Pre-foreclosure sales

accounted for 14 percent of all resi-dential sales last year, while REOsales fell from 32 percent of all sales

in 2011 to 23 percent of total salesin 2012.

With fewer foreclosures available, demand for the low-end

product continues to grow while inventory in that price range istight thanks to high sales volume last year. By Zachmeier'saccount, as much as 70 percent of all inventory on the low end

sold last summer, an unprecedented purging of inventory. “With twice the number of buyers and quite a bit lower

inventory than we had a year ago, we're going to have a feeding

frenzy at the lower price point,” he added.However, higher price ranges have more available properties

and a better selection to choose from, according to Polston.

“What's happening is pricing's gone up a bit. We're seeingsome trade-up buyers coming back into the market at the

Continued next page >

14

“With twice the number of buyersand quite a bit lower inventorythan we had a year ago, we’regoing to have a feeding frenzy

at the lower price point.”

Bob ZachmeierBroker/owner ofWin3 Realty inTucson, Ariz.

15

$300,000 to $400,000 level.There's still a lot of options at that

price range,” said Polston, whoseteam sold 110 houses in 2012.

Even with the upward price

trend, Polston said he continues tosee interest in second homes fromCalifornia and Canadian investors.

“I think it's a pretty good timeto buy so long as you're looking atthe big picture for the long-term,”

Polston noted.When it comes to picking a

property worth buying in Tucson,

Zachmeier breaks the marketplaceinto four levels: the top 25 percentof all homes sold, he said, are

excellent houses that are move-inready. The next 25 percent arethose that need some cosmetic

work (carpet and paint). The thirdquarter of homes sold are thosethat have major issues, while the bottom 25 percent are those

where you need to “bring a bulldozer.”As a Realtor who regularly works with investors, Zachmeier

made a couple of keen observa-tions about the current state of the

market. First, that this is the firsttime ever he's seen the number ofall-cash sales come in higher than

those financed with conventionalloans. Second, more investors areflying in for a quick turnaround,

buying three or four homes andthen leaving.

“The biggest opportunity is

finding home sellers who are inthe penalty box,” he said. “Theyhave a short sale or foreclosure on

their records and the banks aretelling them it's going to be two tofive years before they can buy

another house. I'm findinginvestors to offer them a first posi-tion mortgage, bring in a 20 per-

cent down payment and have theseller take back a second. I'm get-

ting them a 7 to 8 percent mortgage. I can get them in a house for

far less than what they're paying in rent.”

“The banks themselves thathave taken properties back

are sitting on them. This oneI got is 6,100 square feet.

These houses are between5,000 and 7,000 square feet,

and the bank is sitting onthem and they’re not for sale.

I know the bank took themback a year or two ago.”

Michelle McGrewA self-described “slow motion flipper” in Scottsdale, Ariz.

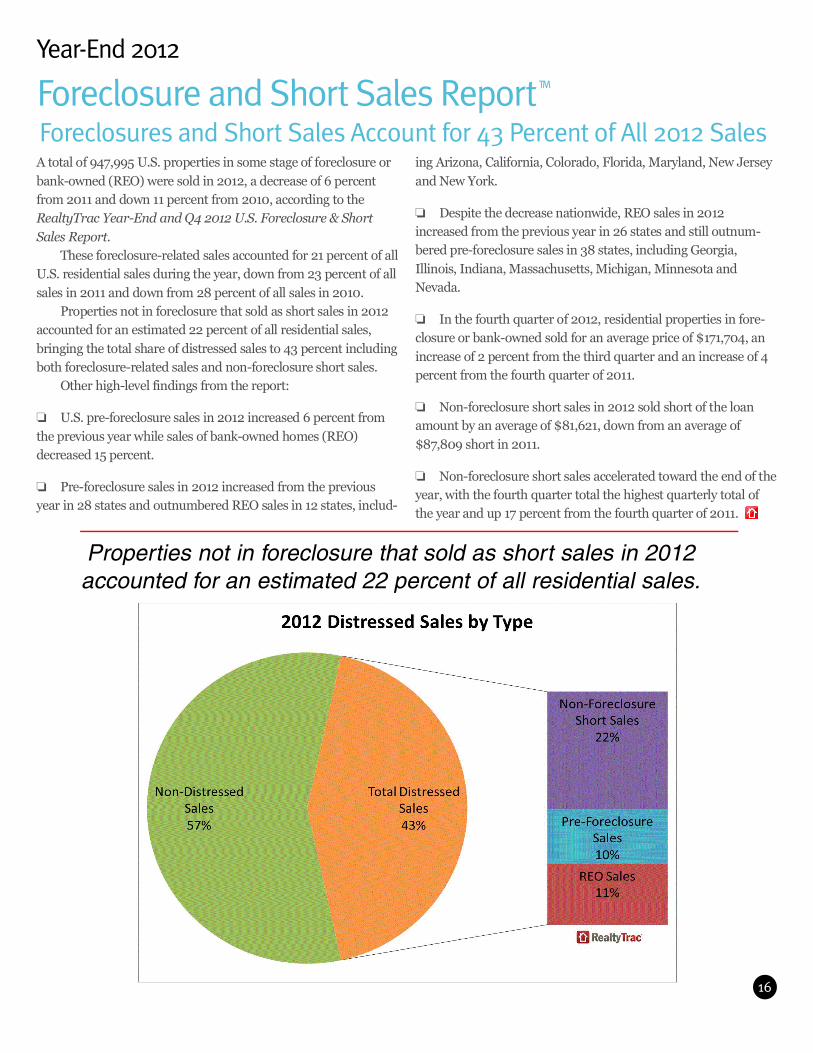

A total of 947,995 U.S. properties in some stage of foreclosure or

bank-owned (REO) were sold in 2012, a decrease of 6 percentfrom 2011 and down 11 percent from 2010, according to theRealtyTrac Year-End and Q4 2012 U.S. Foreclosure & Short

Sales Report. These foreclosure-related sales accounted for 21 percent of all

U.S. residential sales during the year, down from 23 percent of all

sales in 2011 and down from 28 percent of all sales in 2010. Properties not in foreclosure that sold as short sales in 2012

accounted for an estimated 22 percent of all residential sales,

bringing the total share of distressed sales to 43 percent includingboth foreclosure-related sales and non-foreclosure short sales.

Other high-level findings from the report:

❏ U.S. pre-foreclosure sales in 2012 increased 6 percent from

the previous year while sales of bank-owned homes (REO)decreased 15 percent.

❏ Pre-foreclosure sales in 2012 increased from the previousyear in 28 states and outnumbered REO sales in 12 states, includ-

ing Arizona, California, Colorado, Florida, Maryland, New Jersey

and New York.

❏ Despite the decrease nationwide, REO sales in 2012increased from the previous year in 26 states and still outnum-bered pre-foreclosure sales in 38 states, including Georgia,

Illinois, Indiana, Massachusetts, Michigan, Minnesota andN e v a d a .

❏ In the fourth quarter of 2012, residential properties in fore-closure or bank-owned sold for an average price of $171,704, an

increase of 2 percent from the third quarter and an increase of 4percent from the fourth quarter of 2011.

❏ Non-foreclosure short sales in 2012 sold short of the loanamount by an average of $81,621, down from an average of

$87,809 short in 2011.

❏ Non-foreclosure short sales accelerated toward the end of theyear, with the fourth quarter total the highest quarterly total ofthe year and up 17 percent from the fourth quarter of 2011.

16

Ye a r-End 2012

Fo re c l o s u re and Short Sales Re p o rtTM

Fo re c l o s u res and Short Sales Account for 43 Pe rcent of All 2012 Sales

Properties not in foreclosure that sold as short sales in 2012accounted for an estimated 22 percent of all residential sales.

To p2012 Metro Areas With Non-Foreclosure Short Sales

Miami, FL

Washington, DC

Chicago, IL

Tampa, FL

D e t roit, MI

Phoenix, AZ

Las Vegas, NV

Orlando, FL

Los Angeles, CA

Philadelphia, PA

New York, NY

R i verside, CA

Seattle, WA

Atlanta, GA

D e n ve r, CO

San Francisco, CA

B a l t i m o re, MD

Jacksonville, FL

Columbus, OH

S a c ramento, CA

3 0 %

3 %

1 7 %

2 6 %

- 1 %

- 1 9 %

1 0 4

- 6 %

- 7 %

1 1 %

5 %

- 5 %

3 8 %

- 7 %

2 6 %

- 3 %

2 1 %

0 %

3 9 %

1 7 %

M e t ro Are aPe rc e n t a g e

Change from 2011

Ye a r-End 2012

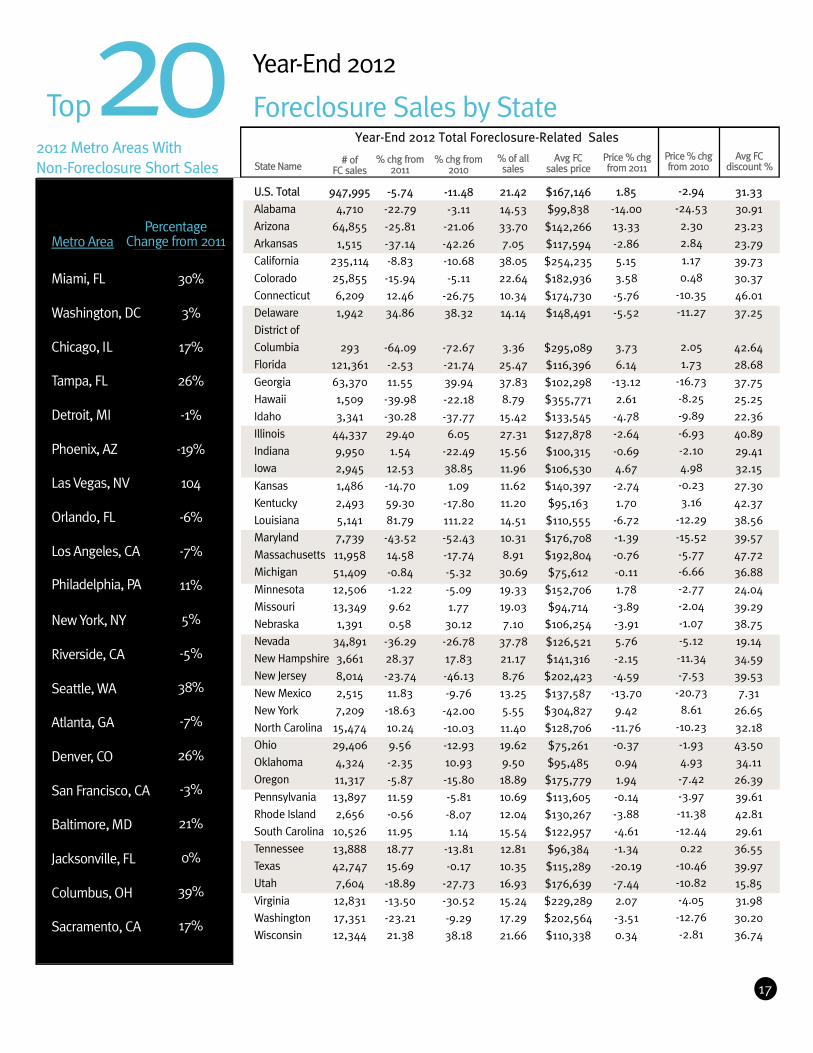

Fo re c l o s u re Sales by St a t e2 0# of

F C s a l e s% of all

s a l e sPrice % chgfrom 2011

947,9954,710

64,8551,515

235,11425,8556,2091,942

293121,36163,3701,5093,341

44,3379,9502,9451,4862,4935,1417,73911,95851,40912,50613,3491,391

34,8913,6618,0142,5157,20915,47429,4064,32411,31713,8972,65610,52613,88842,7477,60412,83117,35112,344

% chg from2 0 1 1

-5.74-22.79-25.81-37.14-8.83-15.9412.4634.86

-64.09-2.5311.55

-39.98-30.2829.401.54

12.53-14.7059.3081.79-43.5214.58-0.84-1.229.620.58

-36.2928.37-23.7411.83-18.6310.249.56-2.35-5.8711.59-0.5611.9518.7715.69-18.89-13.50-23.2121.38

% chg from2 0 1 0

-11.48-3.11

-21.06-42.26-10.68-5.11

-26.7538.32

-72.67-21.7439.94-22.18-37.776.05

-22.4938.851.09

-17.80111.22-52.43-17.74-5.32-5.091.77

30.12-26.7817.83-46.13-9.76

-42.00-10.03-12.9310.93-15.80-5.81-8.071.14

-13.81-0.17

-27.73-30.52-9.2938.18

State Name

U.S. TotalA l a b a m aA r i zo n aA r k a n s a sC a l i f o r n i aC o l o ra d oC o n n e c t i c u tD e l a w a reDistrict ofC o l u m b i aF l o r i d aG e o rg i aH a w a i iI d a h oI l l i n o i sI n d i a n aI ow aKa n s a sKe n t u c k yLo u i s i a n aM a r y l a n dM a s s a c h u s e t t sM i c h i g a nM i n n e s o t aM i s s o u r iN e b ra s k aN e va d aNew HampshireNew JerseyNew MexicoNew Yo r kN o rth Caro l i n aO h i oO k l a h o m aO re g o nPe n n s y l va n i aRhode IslandSouth Caro l i n aTe n n e s s e eTe x a sU t a hVi rg i n i aWa s h i n g t o nWi s c o n s i n

21.4214.5333.707.05

38.0522.6410.3414.14

3.3625.4737.838.7915.4227.3115.5611.9611.6211.2014.5110.318.91

30.6919.3319.037.10

37.7821.178.7613.255.5511.4019.629.5018.8910.6912.0415.5412.8110.3516.9315.2417.2921.66

1.85-14.0013.33-2.865.153.58-5.76-5.52

3.736.14

-13.122.61-4.78-2.64-0.694.67-2.741.70-6.72-1.39-0.76-0.111.78-3.89-3.915.76-2.15-4.59-13.709.42

-11.76-0.370.941.94-0.14-3.88-4.61-1.34

-20.19-7.442.07-3.510.34

Price % chgfrom 2010

-2.94-24.532.302.841.170.48

-10.35-11.27

2.051.73

-16.73-8.25-9.89-6.93-2.104.98-0.233.16

-12.29-15.52-5.77-6.66-2.77-2.04-1.07-5.12-11.34-7.53

-20.738.61

-10.23-1.934.93-7.42-3.97-11.38-12.440.22

-10.46-10.82-4.05-12.76-2.81

Avg FCdiscount %

31.3330.9123.2323.7939.7330.3746.0137.25

42.6428.6837.7525.2522.3640.8929.4132.1527.3042.3738.5639.5747.7236.8824.0439.2938.7519.1434.5939.537.31

26.6532.1843.5034.1126.3939.6142.8129.6136.5539.9715.8531.9830.2036.74

Avg FCsales price

$167,146$99,838$142,266$117,594$254,235$182,936$174,730$148,491

$295,089$116,396$102,298$355,771$133,545$127,878$100,315$106,530$140,397$95,163$110,555$176,708$192,804$75,612

$152,706$94,714

$106,254$126,521$141,316$202,423$137,587$304,827$128,706$75,261$95,485$175,779$113,605$130,267$122,957$96,384$115,289$176,639$229,289$202,564$110,338

Year-End 2012 Total Foreclosure-Related Sales

17

Managing EditorDaren Blomquist

WritersJoel ConeOctavio Nuiry

LayoutJoel Cone

Contact UsSubscriptions800.306.9886

Advertising949.502.8300 x250

Letters to the [email protected]

Foreclosure News Report1 Venture Plaza, Suite 300

Irvine, CA 92618

© 2013 Renwood RealtyTrac LLC

Fo r e c l o s u r e R e p o rt