Embed Size (px)

Citation preview

PT Pertamina (Persero)

Jln. Medan Merdeka Timur No.1A Jakarta 10110

Telp (62-21) 381 5111 Fax (62-21) 384 6865

http://www.pertamina.com

“Strategies to boost gas production and utilization”

Syamsu Alam

Upstream Director

PT. Pertamina (Persero)

Jakarta, 27-29 January 2015

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of Pertamina is strictly prohibited

DRAFT Indogas 2015 The 7th International Indonesia Gas

Conference & Exhibition

BANGKITKAN ENERGI NEGERI

Page 2

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 3

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 4

Full production

Banyu Urip di thn

2015. Produksi

PEPC pada RJPP

2012-2016 lebih

tinggi

dibandingkan

RJPP 2011-2015

karena

percepatan

produksi gas JTB,

Cendana, dan

Kedung Keris.

To be a world class national energy company

Mission

Clean, Competitive, Confident, Customer Focus, Commercial, Capable

Pertamina’s Corporate Vision, Mission and Values

Challenges to synchronize national energy security and energy commercialization

To carry out integrated core business in oil, gas, & renewables based on strong commercial principles

Vision

Values

Page 5

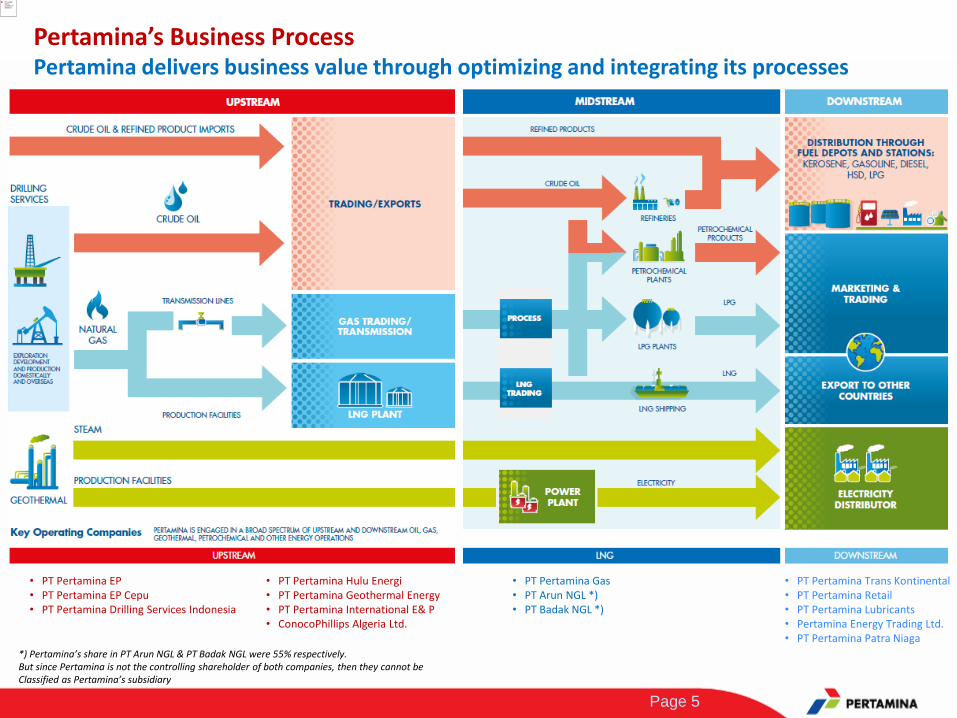

Pertamina’s Business Process Pertamina delivers business value through optimizing and integrating its processes

• PT Pertamina EP • PT Pertamina EP Cepu • PT Pertamina Drilling Services Indonesia

• PT Pertamina Hulu Energi • PT Pertamina Geothermal Energy • PT Pertamina International E& P • ConocoPhillips Algeria Ltd.

• PT Pertamina Gas • PT Arun NGL *) • PT Badak NGL *)

• PT Pertamina Trans Kontinental • PT Pertamina Retail • PT Pertamina Lubricants • Pertamina Energy Trading Ltd. • PT Pertamina Patra Niaga

*) Pertamina’s share in PT Arun NGL & PT Badak NGL were 55% respectively. But since Pertamina is not the controlling shareholder of both companies, then they cannot be Classified as Pertamina’s subsidiary

Page 6

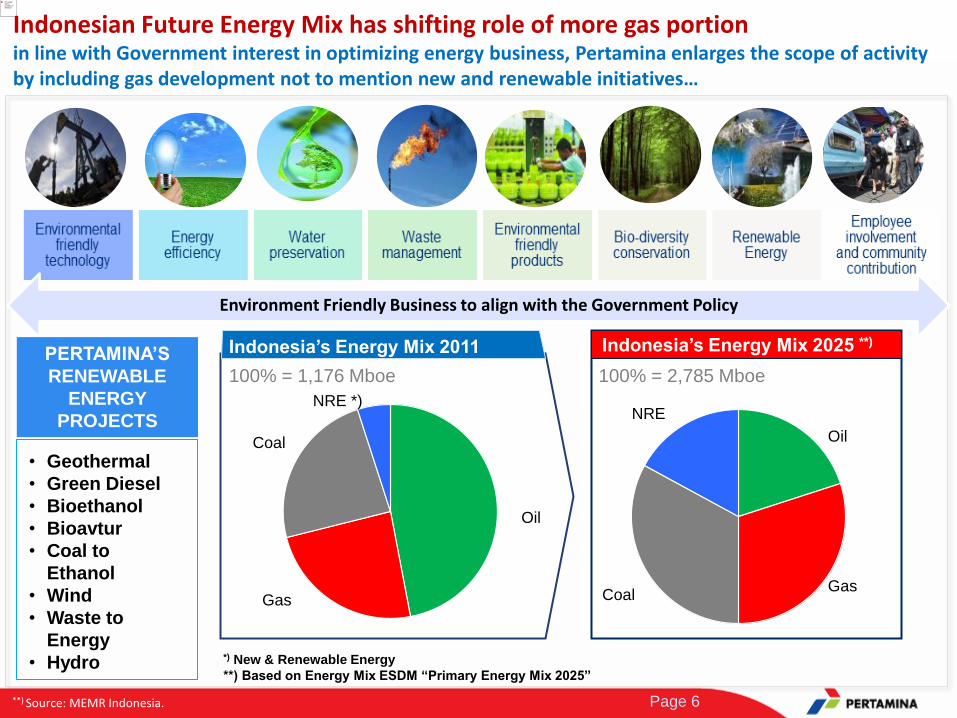

Indonesian Future Energy Mix has shifting role of more gas portion in line with Government interest in optimizing energy business, Pertamina enlarges the scope of activity by including gas development not to mention new and renewable initiatives…

Indonesia’s Energy Mix 2025 **)

100% = 1,176 Mboe 100% = 2,785 Mboe

Indonesia’s Energy Mix 2011

*) New & Renewable Energy

**) Based on Energy Mix ESDM “Primary Energy Mix 2025”

**) Source: MEMR Indonesia.

Environment Friendly Business to align with the Government Policy

• Geothermal

• Green Diesel

• Bioethanol

• Bioavtur

• Coal to

Ethanol

• Wind

• Waste to

Energy

• Hydro

PERTAMINA’S

RENEWABLE

ENERGY

PROJECTS

Oil

Gas

Coal

NRE *)

Oil

Gas Coal

NRE

Page 7

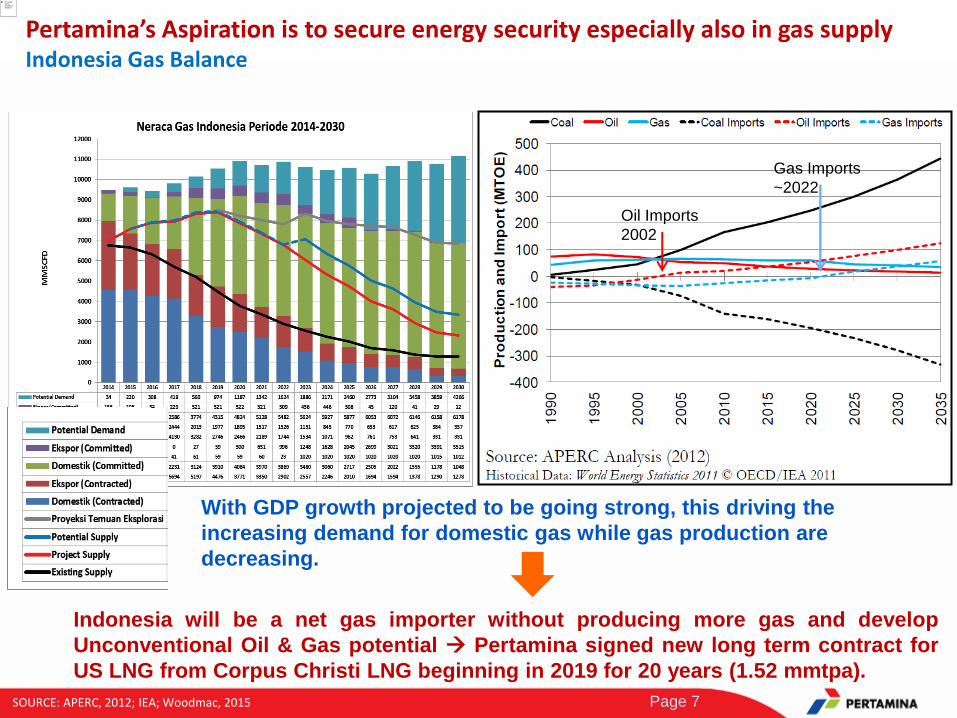

Oil Imports

2002

Gas Imports

~2022

With GDP growth projected to be going strong, this driving the

increasing demand for domestic gas while gas production are

decreasing.

Pertamina’s Aspiration is to secure energy security especially also in gas supply Indonesia Gas Balance

Indonesia will be a net gas importer without producing more gas and develop

Unconventional Oil & Gas potential Pertamina signed new long term contract for

US LNG from Corpus Christi LNG beginning in 2019 for 20 years (1.52 mmtpa).

SOURCE: APERC, 2012; IEA; Woodmac, 2015

Page 8

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 9

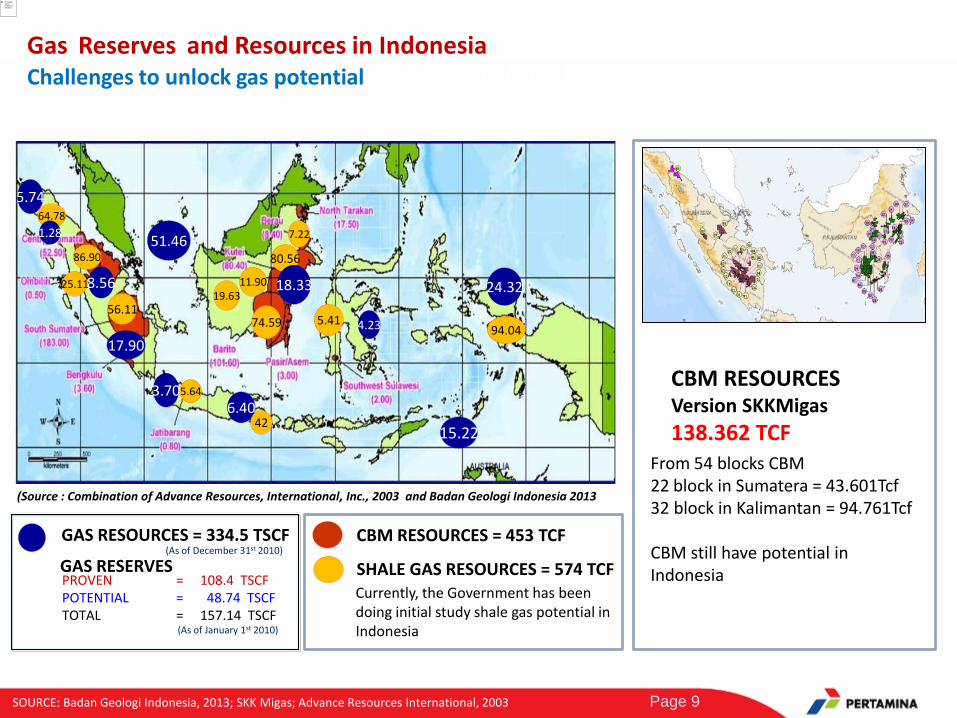

GAS RESOURCES = 334.5 TSCF

PROVEN = 108.4 TSCF POTENTIAL = 48.74 TSCF TOTAL = 157.14 TSCF

GAS RESERVES

NATURAL GAS RESOURCES - RESERVES & CBM RESOURCES, SHALE GAS POTENTIAL

(As of January 1st 2010)

(As of December 31st 2010)

25.11

7.22

11.90 19.63

4.23

8.56

3.70

51.46

24.32

5.74

15.22

17.90

6.40

(Source : Combination of Advance Resources, International, Inc., 2003 and Badan Geologi Indonesia 2013

80.56

74.59

42

86.90

56.11

5.64

64.78

1.28

18.33

94.04 5.41

From 54 blocks CBM 22 block in Sumatera = 43.601Tcf 32 block in Kalimantan = 94.761Tcf CBM still have potential in Indonesia

CBM RESOURCES Version SKKMigas

138.362 TCF

CBM RESOURCES = 453 TCF

SHALE GAS RESOURCES = 574 TCF Currently, the Government has been doing initial study shale gas potential in Indonesia

Gas Reserves and Resources in Indonesia Challenges to unlock gas potential

25.11 11.90 19.63

7.22

SOURCE: Badan Geologi Indonesia, 2013; SKK Migas; Advance Resources International, 2003

Page 10

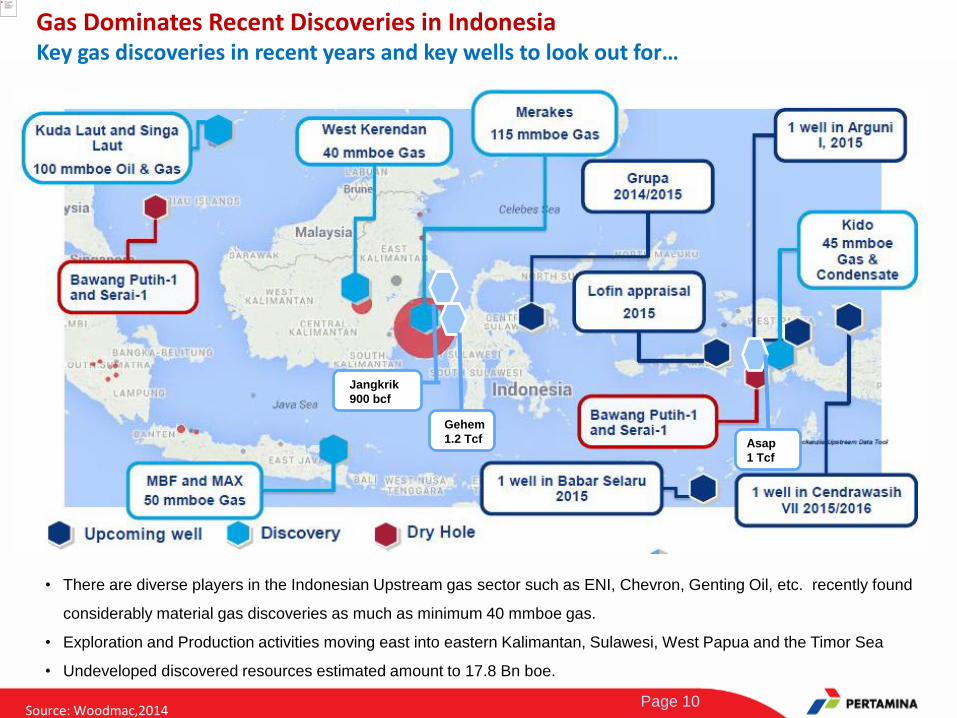

Gas Dominates Recent Discoveries in Indonesia Key gas discoveries in recent years and key wells to look out for…

Source: Woodmac,2014

Jangkrik

900 bcf

Gehem

1.2 Tcf Asap

1 Tcf

• There are diverse players in the Indonesian Upstream gas sector such as ENI, Chevron, Genting Oil, etc. recently found

considerably material gas discoveries as much as minimum 40 mmboe gas.

• Exploration and Production activities moving east into eastern Kalimantan, Sulawesi, West Papua and the Timor Sea

• Undeveloped discovered resources estimated amount to 17.8 Bn boe.

Page 11

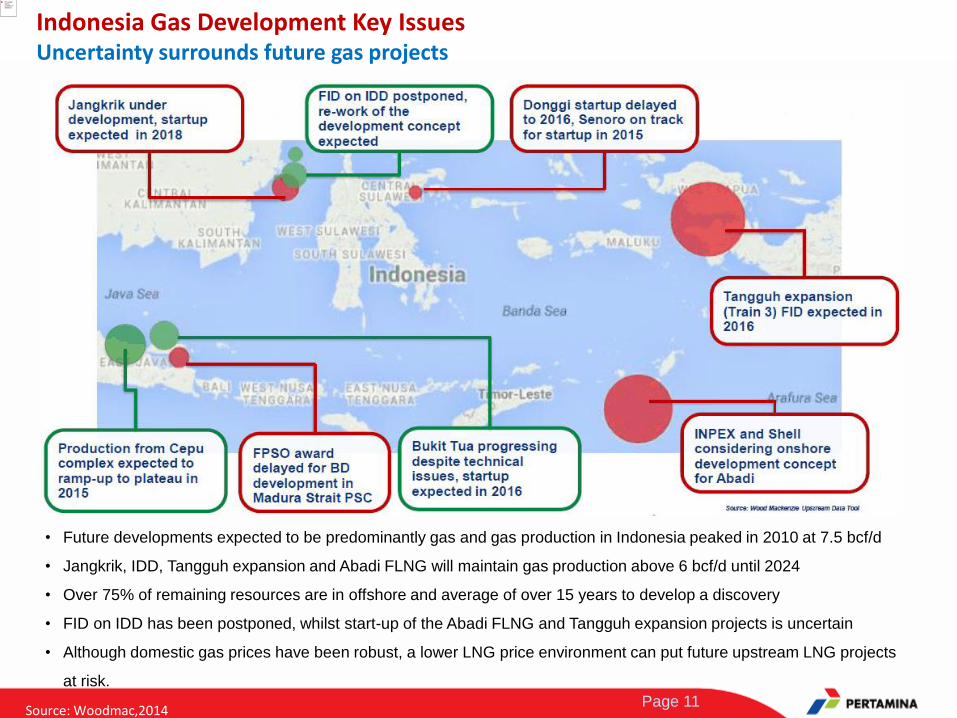

Indonesia Gas Development Key Issues Uncertainty surrounds future gas projects

Source: Woodmac,2014

• Future developments expected to be predominantly gas and gas production in Indonesia peaked in 2010 at 7.5 bcf/d

• Jangkrik, IDD, Tangguh expansion and Abadi FLNG will maintain gas production above 6 bcf/d until 2024

• Over 75% of remaining resources are in offshore and average of over 15 years to develop a discovery

• FID on IDD has been postponed, whilst start-up of the Abadi FLNG and Tangguh expansion projects is uncertain

• Although domestic gas prices have been robust, a lower LNG price environment can put future upstream LNG projects

at risk.

Page 12

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 13

68.06

67.06

67.45

67.72

68.8

65 65.5 66 66.5 67 67.5 68 68.5 69

2009

2010

2011

2012

2013

LNG Sales

(Million MMBTU)

502.05

532.85

558.6

563.15

557.67

480 490 500 510 520 530 540 550 560 570

2009

2010

2011

2012

2013

Gas Production

(BSCF)

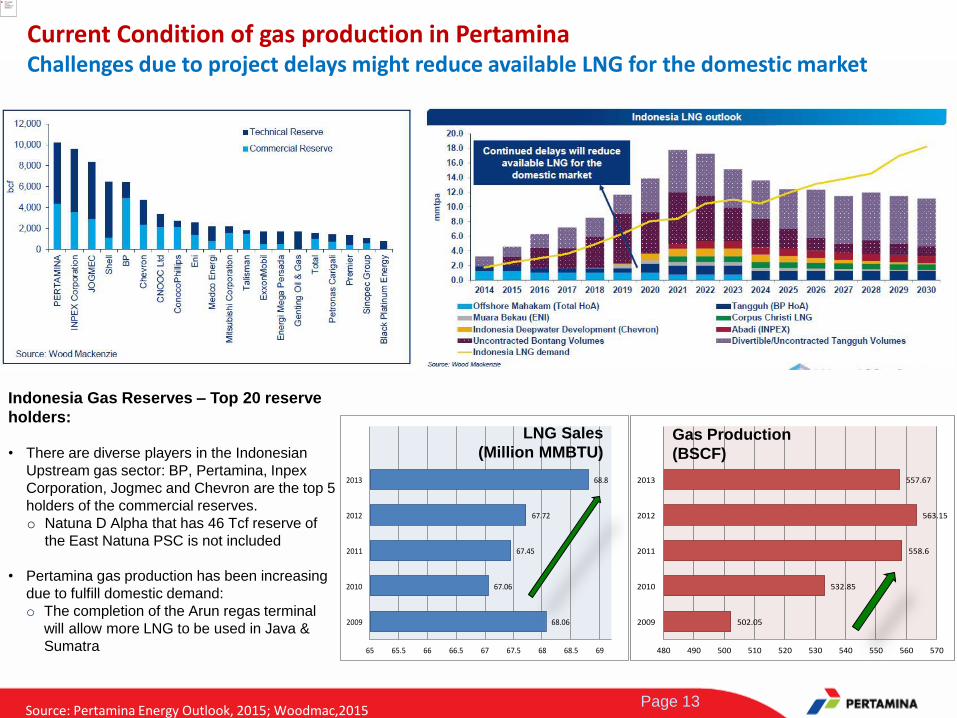

Source: Pertamina Energy Outlook, 2015; Woodmac,2015

Current Condition of gas production in Pertamina Challenges due to project delays might reduce available LNG for the domestic market

Indonesia Gas Reserves – Top 20 reserve

holders:

• There are diverse players in the Indonesian

Upstream gas sector: BP, Pertamina, Inpex

Corporation, Jogmec and Chevron are the top 5

holders of the commercial reserves.

o Natuna D Alpha that has 46 Tcf reserve of

the East Natuna PSC is not included

• Pertamina gas production has been increasing

due to fulfill domestic demand:

o The completion of the Arun regas terminal

will allow more LNG to be used in Java &

Sumatra

Page 14

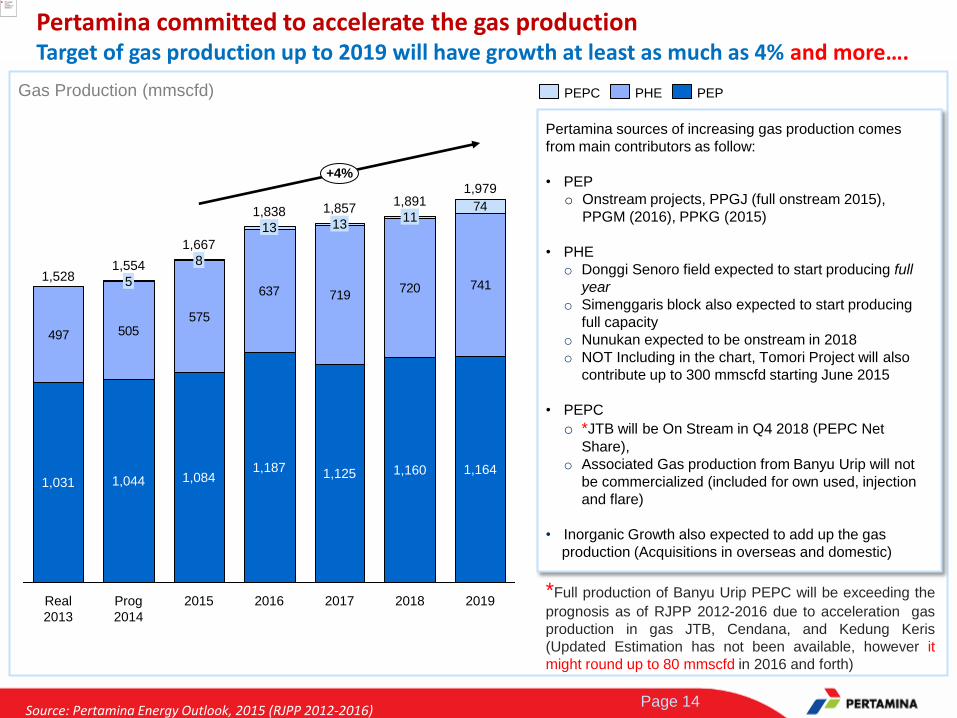

Gas Production (mmscfd)

497 505575

637 719720 741

74

+4%

2019

1,979

1,164

2018

1,891

1,160

11

2017

1,857

1,125

13

2016

1,838

1,187

13

2015

1,667

1,084

8

Prog

2014

1,554

1,044

5

Real

2013

1,528

1,031

PEP PHE PEPC

Pertamina sources of increasing gas production comes

from main contributors as follow:

• PEP

o Onstream projects, PPGJ (full onstream 2015),

PPGM (2016), PPKG (2015)

• PHE

o Donggi Senoro field expected to start producing full

year

o Simenggaris block also expected to start producing

full capacity

o Nunukan expected to be onstream in 2018

o NOT Including in the chart, Tomori Project will also

contribute up to 300 mmscfd starting June 2015

• PEPC

o *JTB will be On Stream in Q4 2018 (PEPC Net

Share),

o Associated Gas production from Banyu Urip will not

be commercialized (included for own used, injection

and flare)

• Inorganic Growth also expected to add up the gas

production (Acquisitions in overseas and domestic)

Source: Pertamina Energy Outlook, 2015 (RJPP 2012-2016)

Pertamina committed to accelerate the gas production Target of gas production up to 2019 will have growth at least as much as 4% and more….

Full production Banyu Urip di thn 2015.

Produksi PEPC pada RJPP 2012-2016

lebih tinggi dibandingkan RJPP 2011-2015

karena percepatan produksi gas JTB,

Cendana, dan Kedung Keris. *Full production of Banyu Urip PEPC will be exceeding the

prognosis as of RJPP 2012-2016 due to acceleration gas

production in gas JTB, Cendana, and Kedung Keris

(Updated Estimation has not been available, however it

might round up to 80 mmscfd in 2016 and forth)

Page 15

Pertamina is increasing awareness of gas potential in turbulence condition of global oil & gas industry Acceleration and Improvement in technology and capabilities to unlock gas potential

Exploration and Production • Increasing gas production from existing fields

• Accelerating upstream projects with gas production in order to monetize the gas

production soonest as crude price being deeply falling

• Expanding business activities and operations, including using inorganic methods

(acquisitions)

• Developing the potential of Unconventional Oil & Gas (Shale Gas, Tight Sand

Gas and CBM) in Pertamina areas

• Forming strategic alliances to support the expansion and building specific skills.

Non Exploration and Production • Increasing the domestic gas trading business while taking the opportunity to

expand the gas

• Transport and process business through synergy with other Pertamina

subsidiaries

• Being pro-active in formulating pricing policy, in accordance with national policies

• Building capacity and specific skills in drilling services to support oil and gas

expansion plans, especially in unconventional oil & gas potential.

Page 16

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 17

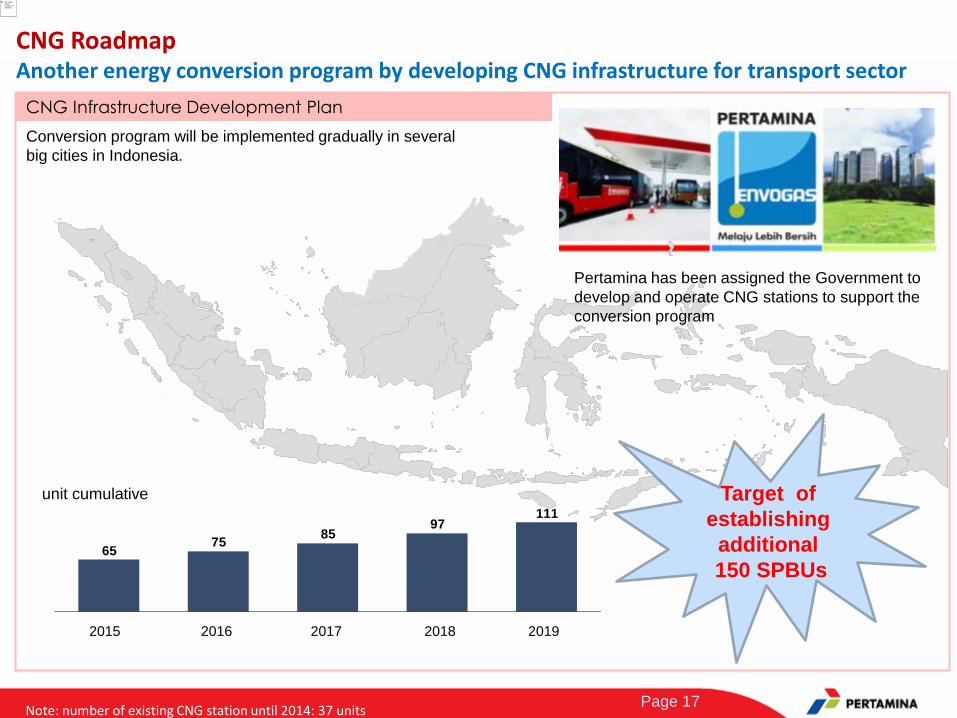

CNG Roadmap Another energy conversion program by developing CNG infrastructure for transport sector

CNG Infrastructure Development Plan

Pertamina has been assigned the Government to

develop and operate CNG stations to support the

conversion program

Conversion program will be implemented gradually in several

big cities in Indonesia.

Note: number of existing CNG station until 2014: 37 units

11197

8575

65

2019 2018 2017 2016 2015

unit cumulative Target of

establishing

additional

150 SPBUs

Page 18

Agenda

2

3 Pertamina’s Strategies to Boost Gas Production

4

Indonesia Gas Potential

Pertamina Strategic Gas Utilization

5

1 Pertamina’s Strategic View on Gas Development

Conclusion

Page 19

hank You T

Page 20

T These materials have been prepared by PT Pertamina (Persero) together with its subsidiaries, (the “Company”) and have not been independently verified. No representation or warranty, express or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the information presented, contained or referred to in these materials. Neither the Company nor any of its affiliates, advisers or representatives accepts any liability whatsoever for any loss howsoever arising from any information presented, contained or referred to in these materials. The information presented, contained and referred to in these materials is subject to change without notice and its accuracy is not guaranteed.

These materials contain statements that constitute forward-looking statements. These statements include descriptions regarding the intent, belief or current expectations of the Company or its officers with respect to, among other things, the operations, business, strategy, consolidated results of operations and financial condition of the Company. These statements can be recognized by the use of words such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and involve risks, uncertainties, and assumptions and actual results may differ from those in the forward-looking statements as a result of various factors. Forward-looking statements contained herein that reference past trends or activities should not be taken as a representation that such trends or activities will necessarily continue in the future. The Company has no obligation and does not undertake to update or revise forward-looking statements to reflect future events or circumstances.

These materials are highly confidential, are being given solely for your information and for your use and may not be copied, reproduced or redistributed to any other person in any manner. Unauthorized copying, reproduction or redistribution of these materials into the U.S. or to any U.S. persons as defined in Regulations under the U.S. Securities Act of 1933, as amended or other third parties (including journalists) could result in a substantial delay to, or otherwise prejudice, the success of the offering. You agree to keep the contents of this presentation and these materials confidential and such presentation and materials form a part of confidential information.

Disclaimer