Embed Size (px)

Citation preview

ed-CK / sa- MA, PY

Tiptoeing through a recovery

Commodity price and lagged impact of policy

loosening to sustain recovery traction in 2017

We see downside risk to staples’ earnings as raw

material price increases

Retailers’ PE discount to staples at historical low;

time for bargain hunting?

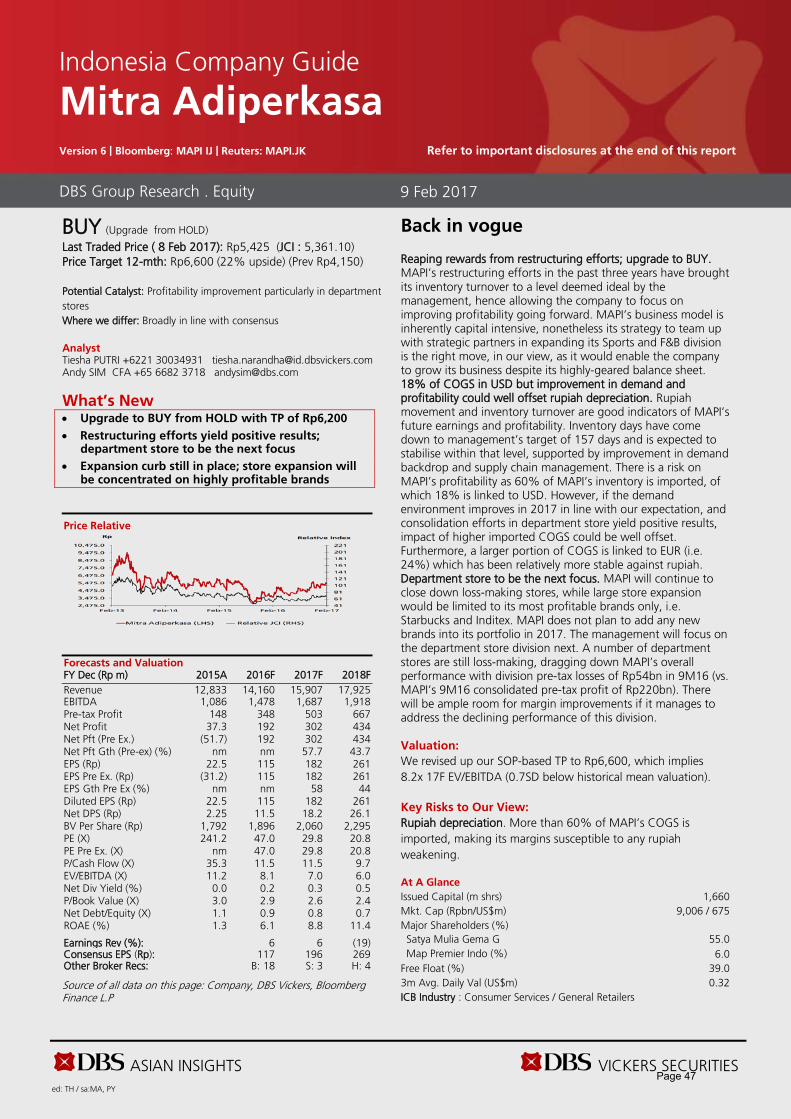

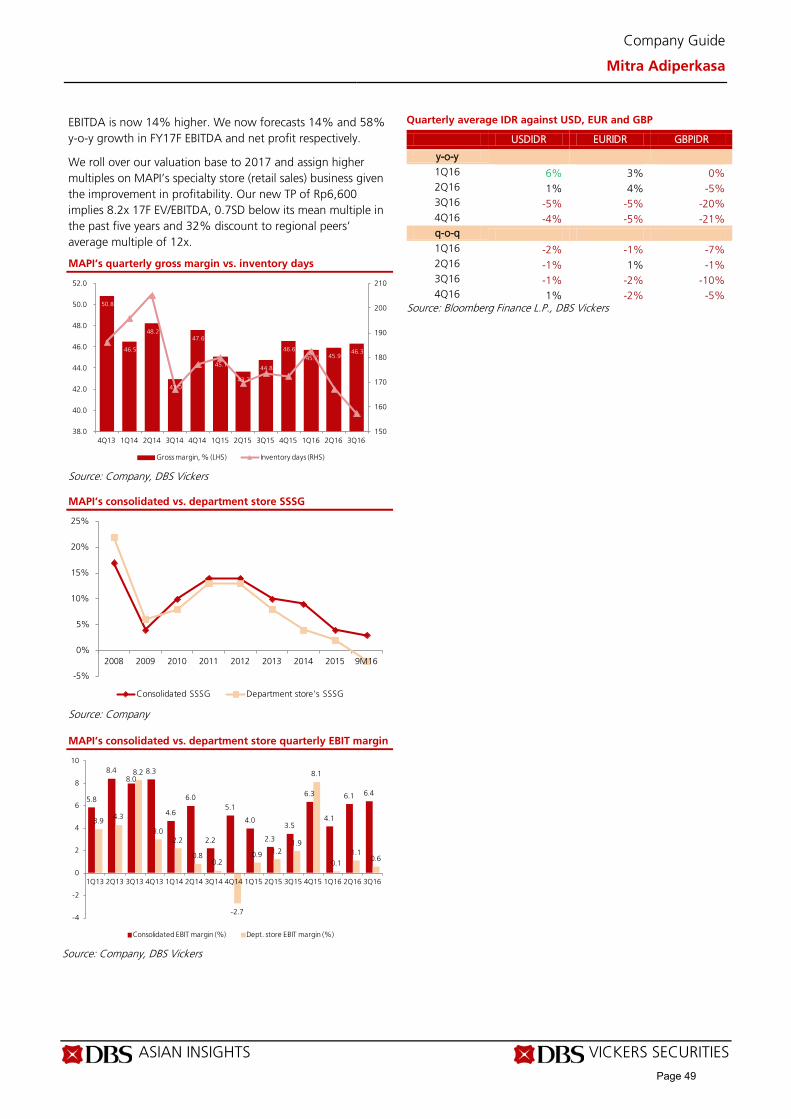

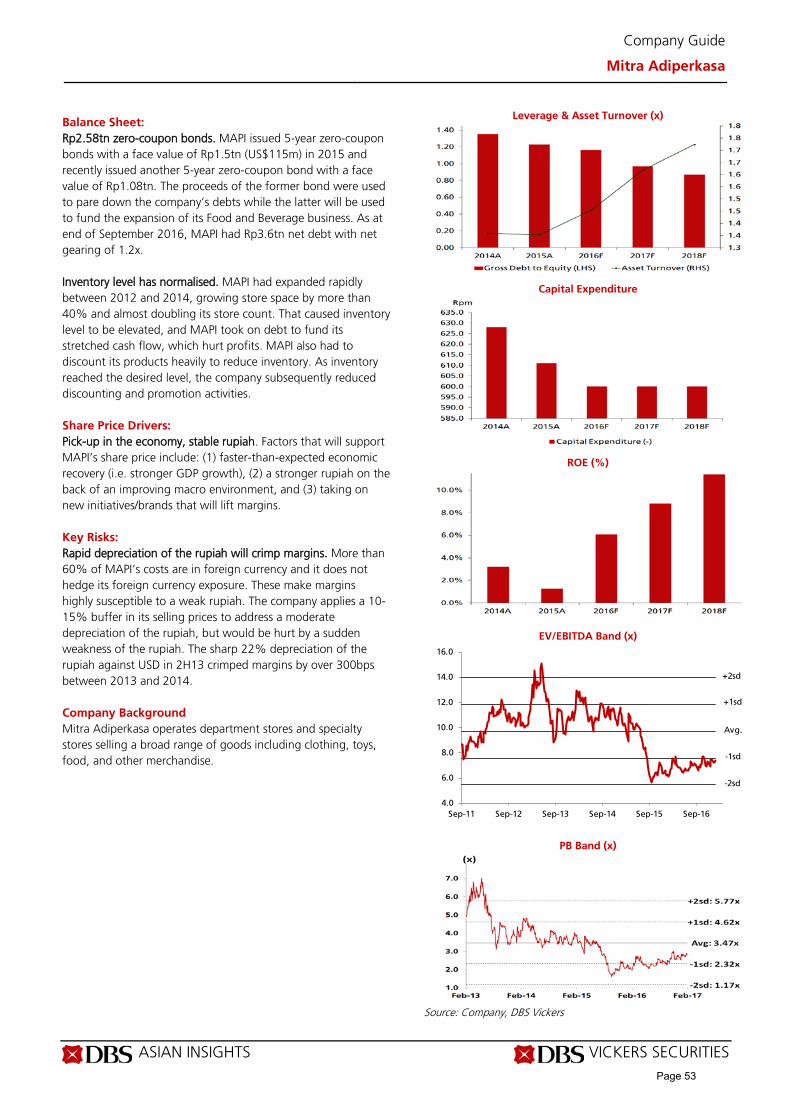

Maintain INDF as top pick; upgrade MAPI to BUY

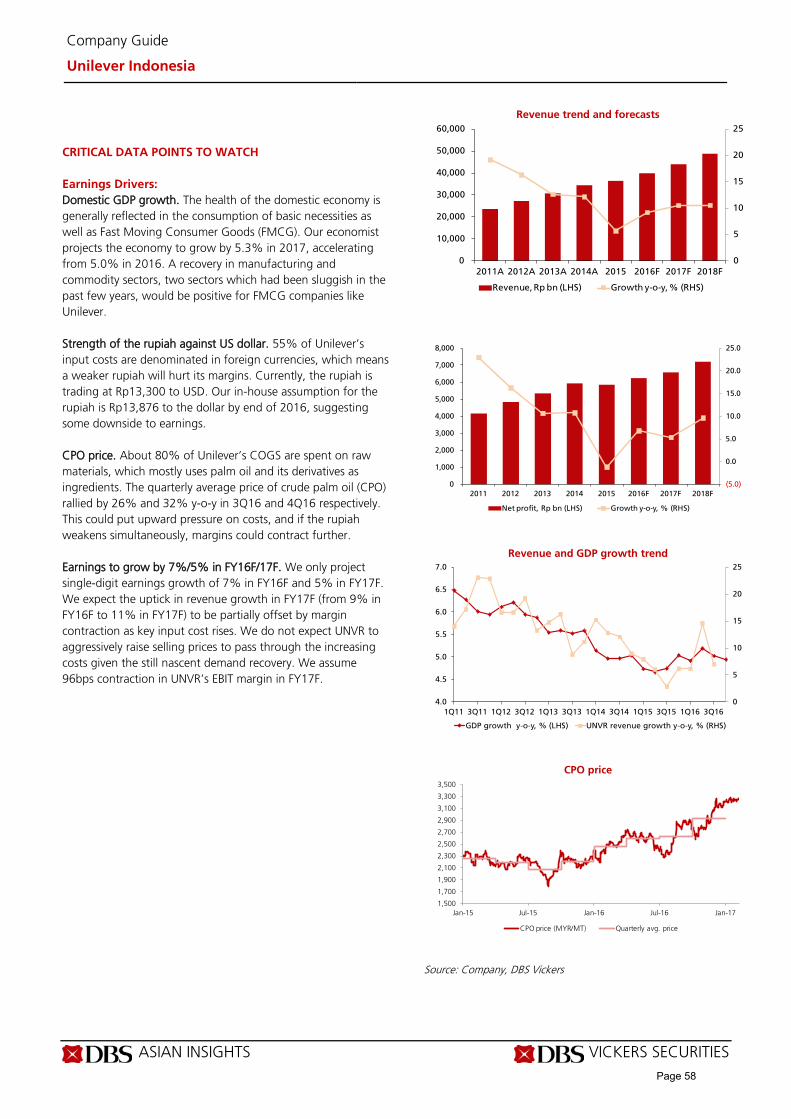

On the path of gradual recovery. Demand recovery has remained nascent to date but with commodity prices having turned the corner, the purchasing power of consumers, particularly those residing outside Java, should improve. In addition, we think the impact from the policy loosening measures in 2016 is likely to be seen this year. Two key themes that we highlight in this report are: 1) rising soft commodity prices and the impact on consumer staples companies, and 2) retailers’ valuation which appears to have priced in the current economic cycle and risk of structural shift from one retail channel to another. Rising soft commodity prices pose downside risk to

consumer staples’ earnings. Consumer staples’ margin will likely shrink as raw material prices have started to rise. We expect the sector’s earnings growth to decelerate this year, hence, we advise investors to avoid companies that trade at a lofty valuation such as UNVR. We prefer cheaper names with dominant market share in key products, which should translate to a better flexibility in passing on higher raw material costs to consumers. For this reason, we maintain INDF as our top pick. Retailers trade near historical low multiples; focus on

company-specific factors. Retailers’ current valuation appears to have priced in the weak economy, trading at a significant PE discount to staples companies. However, as discretionary spending has yet to show signs of bottoming, we advise investors to put more focus on company-specific drivers. We upgrade MAPI to BUY as we believe the company will continue to reap rewards from its restructuring efforts that started three years ago. This upper-middle retailer also benefits from a weaker euro as 24% of its COGS are linked to the euro. We maintain our FULLY VALUED call on MPPA as we believe the market’s earnings expectation for the company is too high. It now trades at a high multiple of 39x PE FY17F vs. regional supermarkets which trade at 22x PE FY17F on average, making it prone to a de-rating if the company fails to deliver.

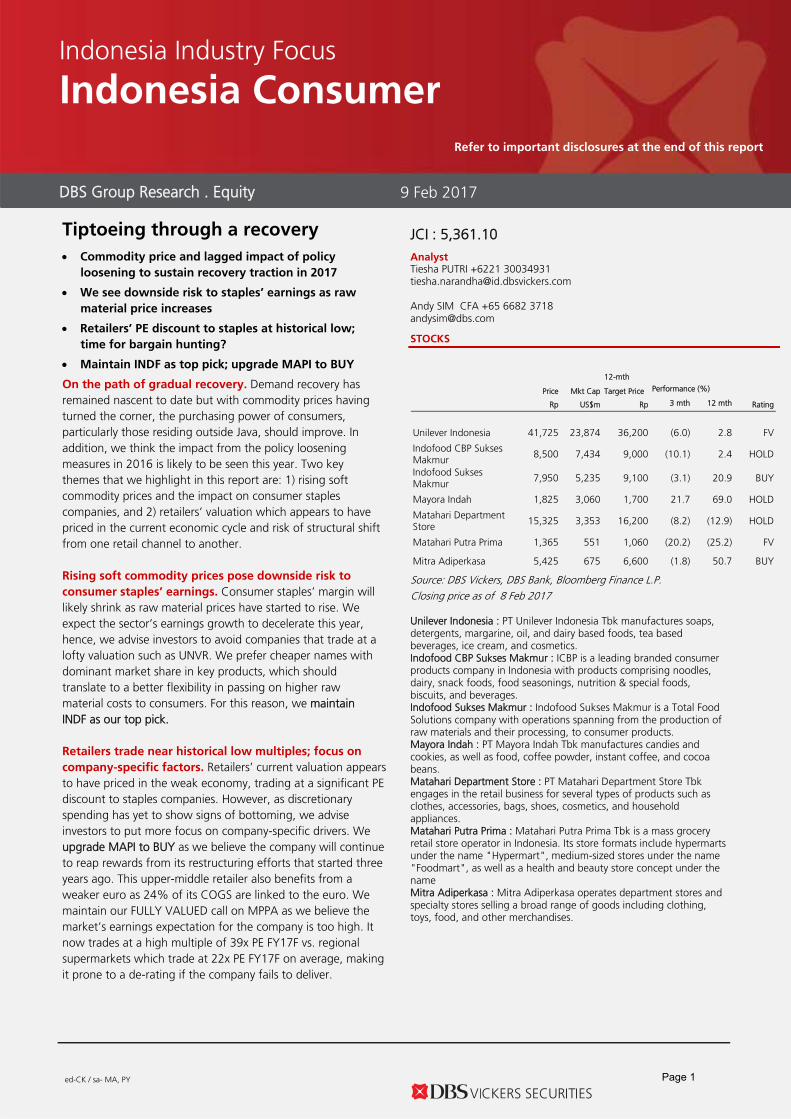

JCI : 5,361.10

Analyst Tiesha PUTRI +6221 30034931 [email protected] Andy SIM CFA +65 6682 3718

STOCKS

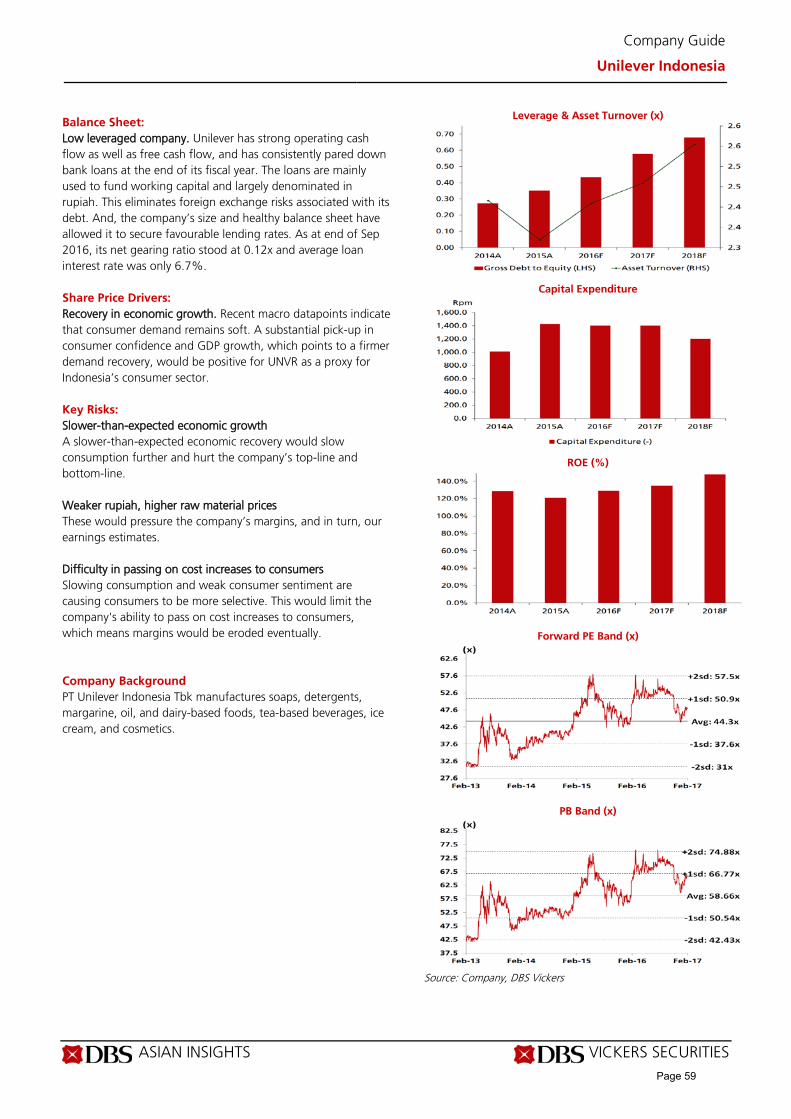

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P. Closing price as of 8 Feb 2017 Unilever Indonesia : PT Unilever Indonesia Tbk manufactures soaps, detergents, margarine, oil, and dairy based foods, tea based beverages, ice cream, and cosmetics. Indofood CBP Sukses Makmur : ICBP is a leading branded consumer products company in Indonesia with products comprising noodles, dairy, snack foods, food seasonings, nutrition & special foods, biscuits, and beverages. Indofood Sukses Makmur : Indofood Sukses Makmur is a Total Food Solutions company with operations spanning from the production of raw materials and their processing, to consumer products. Mayora Indah : PT Mayora Indah Tbk manufactures candies and cookies, as well as food, coffee powder, instant coffee, and cocoa beans. Matahari Department Store : PT Matahari Department Store Tbk engages in the retail business for several types of products such as clothes, accessories, bags, shoes, cosmetics, and household appliances. Matahari Putra Prima : Matahari Putra Prima Tbk is a mass grocery retail store operator in Indonesia. Its store formats include hypermarts under the name "Hypermart", medium-sized stores under the name "Foodmart", as well as a health and beauty store concept under the name Mitra Adiperkasa : Mitra Adiperkasa operates department stores and specialty stores selling a broad range of goods including clothing, toys, food, and other merchandises.

DBS Group Research . Equity 9 Feb 2017

Indonesia Industry Focus

Indonesia Consumer

Refer to important disclosures at the end of this report

12-mth

Price Mkt Cap Target Price Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

Unilever Indonesia 41,725 23,874 36,200 (6.0) 2.8 FV

Indofood CBP Sukses Makmur

8,500 7,434 9,000 (10.1) 2.4 HOLD

Indofood Sukses Makmur

7,950 5,235 9,100 (3.1) 20.9 BUY

Mayora Indah 1,825 3,060 1,700 21.7 69.0 HOLD

Matahari Department Store 15,325 3,353 16,200 (8.2) (12.9) HOLD

Matahari Putra Prima 1,365 551 1,060 (20.2) (25.2) FV

Mitra Adiperkasa 5,425 675 6,600 (1.8) 50.7 BUY

Page 1

Industry Focus

Indonesia Consumer

Page 2

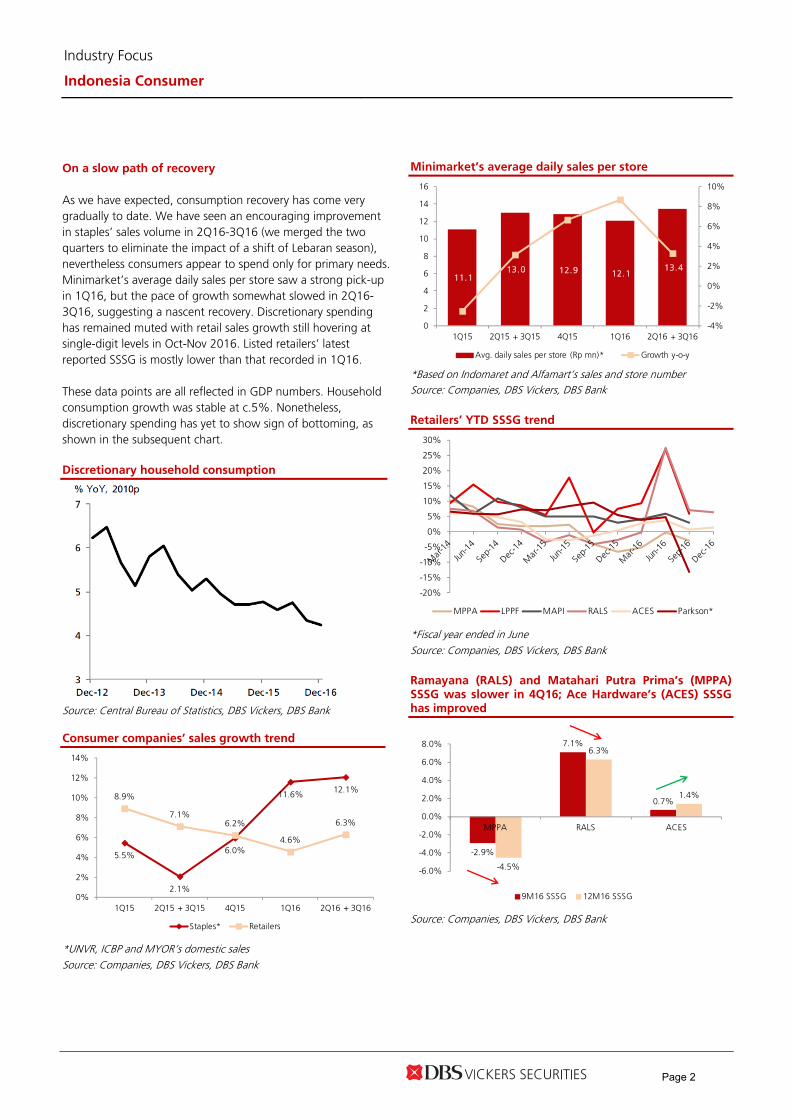

On a slow path of recovery As we have expected, consumption recovery has come very gradually to date. We have seen an encouraging improvement in staples’ sales volume in 2Q16-3Q16 (we merged the two quarters to eliminate the impact of a shift of Lebaran season), nevertheless consumers appear to spend only for primary needs. Minimarket’s average daily sales per store saw a strong pick-up in 1Q16, but the pace of growth somewhat slowed in 2Q16-3Q16, suggesting a nascent recovery. Discretionary spending has remained muted with retail sales growth still hovering at single-digit levels in Oct-Nov 2016. Listed retailers’ latest reported SSSG is mostly lower than that recorded in 1Q16. These data points are all reflected in GDP numbers. Household consumption growth was stable at c.5%. Nonetheless, discretionary spending has yet to show sign of bottoming, as shown in the subsequent chart. Discretionary household consumption

Source: Central Bureau of Statistics, DBS Vickers, DBS Bank Consumer companies’ sales growth trend

*UNVR, ICBP and MYOR’s domestic sales Source: Companies, DBS Vickers, DBS Bank

Minimarket’s average daily sales per store

*Based on Indomaret and Alfamart’s sales and store number Source: Companies, DBS Vickers, DBS Bank Retailers’ YTD SSSG trend

*Fiscal year ended in June Source: Companies, DBS Vickers, DBS Bank Ramayana (RALS) and Matahari Putra Prima’s (MPPA) SSSG was slower in 4Q16; Ace Hardware’s (ACES) SSSG has improved

Source: Companies, DBS Vickers, DBS Bank

5.5%

2.1%

6.0%

11.6% 12.1%8.9%

7.1%6.2%

4.6%

6.3%

0%

2%

4%

6%

8%

10%

12%

14%

1Q15 2Q15 + 3Q15 4Q15 1Q16 2Q16 + 3Q16

Staples* Retailers

11.1 13.0 12.9 12.1

13.4

-4%

-2%

0%

2%

4%

6%

8%

10%

0

2

4

6

8

10

12

14

16

1Q15 2Q15 + 3Q15 4Q15 1Q16 2Q16 + 3Q16

Avg. daily sales per store (Rp mn)* Growth y-o-y

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

MPPA LPPF MAPI RALS ACES Parkson*

-2.9%

7.1%

0.7%

-4.5%

6.3%

1.4%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

MPPA RALS ACES

9M16 SSSG 12M16 SSSG

Page 2

Industry Focus

Indonesia Consumer

Page 3

Consumer tracker: data points reaffirm our view that

recovery momentum will sustain in 2017

Key commodity prices have reversed their downward trend. The low commodity prices in the past years have eroded consumer’s purchasing power, particularly those residing outside Java. We note that 33% and 7% of workforce are employed in the agriculture and construction sectors respectively. Rising soft commodity prices, particularly rubber, CPO, coffee and cocoa, along with an increase in infrastructure spending would help to raise household income, spur consumption and sustain the demand recovery momentum in 2017. Our recent check with plantation companies suggests that the key players are planning to hire more workers in 2017. Regional elections should also serve as a short-term boost to consumption. Three months campaign period will precede the voting day, which is scheduled to take place in mid-Feb 2017. Employment by sector

Source: Central Bureau of Statistics Indonesia’s key export commodities

Source: Bloomberg Finance L.P., DBS Vickers, DBS Bank Consumers turning more upbeat with confidence index above historical mean. Consumers have turned more upbeat with the consumer confidence index (CCI) consistently staying above its

5-year average through 4Q16. In Dec 2016, the CCI slid slightly to 115.4 from 115.9 in Nov 2016. Interestingly, the decline was mostly seen among low-income consumers with monthly expenditure of Rp1m-3m, while the confidence index of consumers with an income range of Rp3m-5m continued to improve. Bank Indonesia’s consumer confidence index

Source: Bank Indonesia But this has yet to be reflected in retail sales. The stronger consumer confidence has yet to translate to strong growth in the retail sales index (RSI). RSI growth moderated from the low-teens level (since Nov 2015) to 8%-10% in Oct-Dec 2016, in line with nominal GDP growth. Retail sales index

Source: Bank Indonesia Vehicle sales – positive read-through from motorcycle sales data. Motorcycle sales in 11M16 were still 8% lower y-o-y, while car sales held up relatively well with 4% growth y-o-y. However, we are encouraged to see a pick-up in monthly motorcycle sales in November which showed a positive growth of 7% y-o-y for the first time since Mar 2016, indicating that consumers have started to spend on bigger-ticket items.

Agriculture33%

Mining1%

Industrial13%

Construction7%

Trade23%

Others23%

-

20

40

60

80

100

120

140

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

2011 = 100

CPO Coffee Cocoa Rubber

-5.0

0.0

5.0

10.0

15.0

20.0

90

95

100

105

110

115

120

125

CCI 5-year avg. CCI AdministeredCPI y-o-y

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

RSI index (2010=100) Growth y-o-y (RHS)

Page 3

Industry Focus

Indonesia Consumer

Page 4

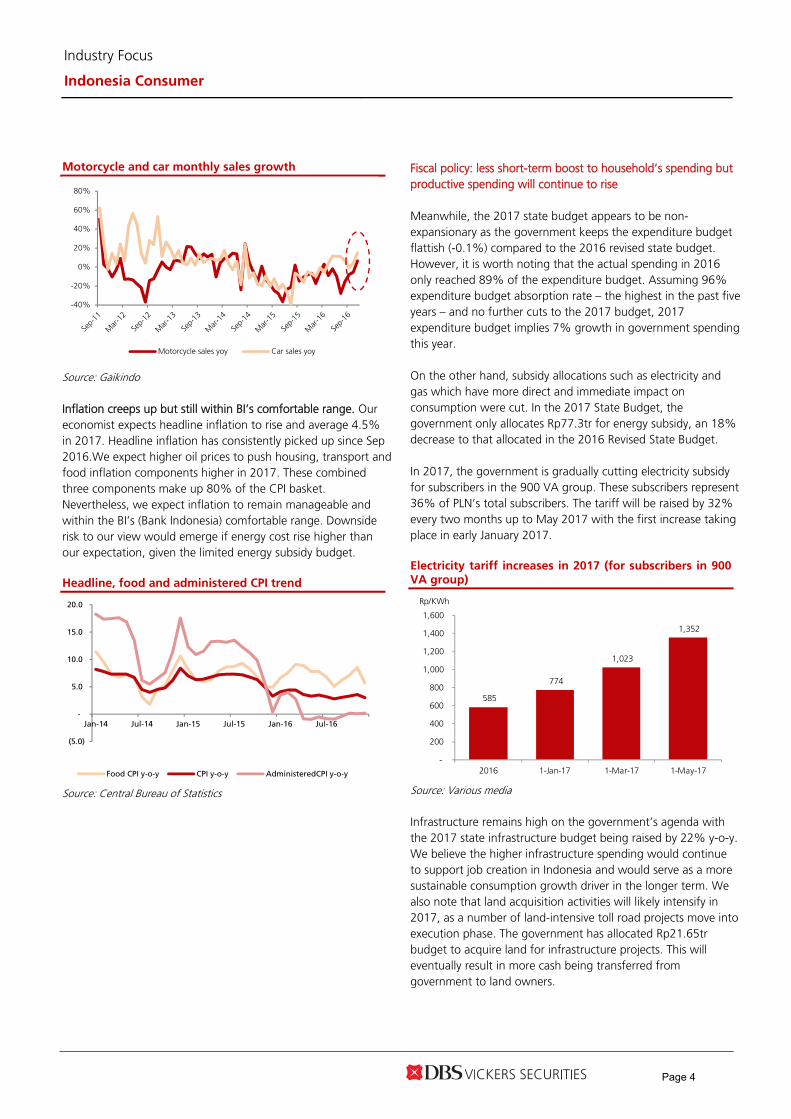

Motorcycle and car monthly sales growth

Source: Gaikindo Inflation creeps up but still within BI’s comfortable range. Our economist expects headline inflation to rise and average 4.5% in 2017. Headline inflation has consistently picked up since Sep 2016.We expect higher oil prices to push housing, transport and food inflation components higher in 2017. These combined three components make up 80% of the CPI basket. Nevertheless, we expect inflation to remain manageable and within the BI’s (Bank Indonesia) comfortable range. Downside risk to our view would emerge if energy cost rise higher than our expectation, given the limited energy subsidy budget. Headline, food and administered CPI trend

Source: Central Bureau of Statistics

Fiscal policy: less short-term boost to household’s spending but productive spending will continue to rise Meanwhile, the 2017 state budget appears to be non-expansionary as the government keeps the expenditure budget flattish (-0.1%) compared to the 2016 revised state budget. However, it is worth noting that the actual spending in 2016 only reached 89% of the expenditure budget. Assuming 96% expenditure budget absorption rate – the highest in the past five years – and no further cuts to the 2017 budget, 2017 expenditure budget implies 7% growth in government spending this year. On the other hand, subsidy allocations such as electricity and gas which have more direct and immediate impact on consumption were cut. In the 2017 State Budget, the government only allocates Rp77.3tr for energy subsidy, an 18% decrease to that allocated in the 2016 Revised State Budget. In 2017, the government is gradually cutting electricity subsidy for subscribers in the 900 VA group. These subscribers represent 36% of PLN’s total subscribers. The tariff will be raised by 32% every two months up to May 2017 with the first increase taking place in early January 2017. Electricity tariff increases in 2017 (for subscribers in 900 VA group)

Source: Various media Infrastructure remains high on the government’s agenda with the 2017 state infrastructure budget being raised by 22% y-o-y. We believe the higher infrastructure spending would continue to support job creation in Indonesia and would serve as a more sustainable consumption growth driver in the longer term. We also note that land acquisition activities will likely intensify in 2017, as a number of land-intensive toll road projects move into execution phase. The government has allocated Rp21.65tr budget to acquire land for infrastructure projects. This will eventually result in more cash being transferred from government to land owners.

-40%

-20%

0%

20%

40%

60%

80%

Motorcycle sales yoy Car sales yoy

(5.0)

-

5.0

10.0

15.0

20.0

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Food CPI y-o-y CPI y-o-y AdministeredCPI y-o-y

585

774

1,023

1,352

-

200

400

600

800

1,000

1,200

1,400

1,600

2016 1-Jan-17 1-Mar-17 1-May-17

Rp/KWh

Page 4

Industry Focus

Indonesia Consumer

Page 5

Moderate increase in minimum wage More regions comply with the minimum wage formula stipulated by Government Regulation No. 78/2015 in 2017. The implication is a slower minimum wage increase in 2017 compared to that in the past years, as the regulation pegs the minimum wage growth to inflation and GDP growth rate. On average, the minimum wage in 34 provinces could rise by only 9% in 2017 vs. a 12% increase each in 2015 and 2016. Labour-intensive companies, including retailers, are set to benefit from this moderate wage inflation as labour costs typically account for 10-15% of revenue. We nonetheless acknowledge that this could also mean a more muted boost to consumers’ purchasing power in 2017. Minimum wage trend

Source: Central Bureau of Statistics, DBS Vickers, DBS Bank Consumer staples – watch out for cost inflation

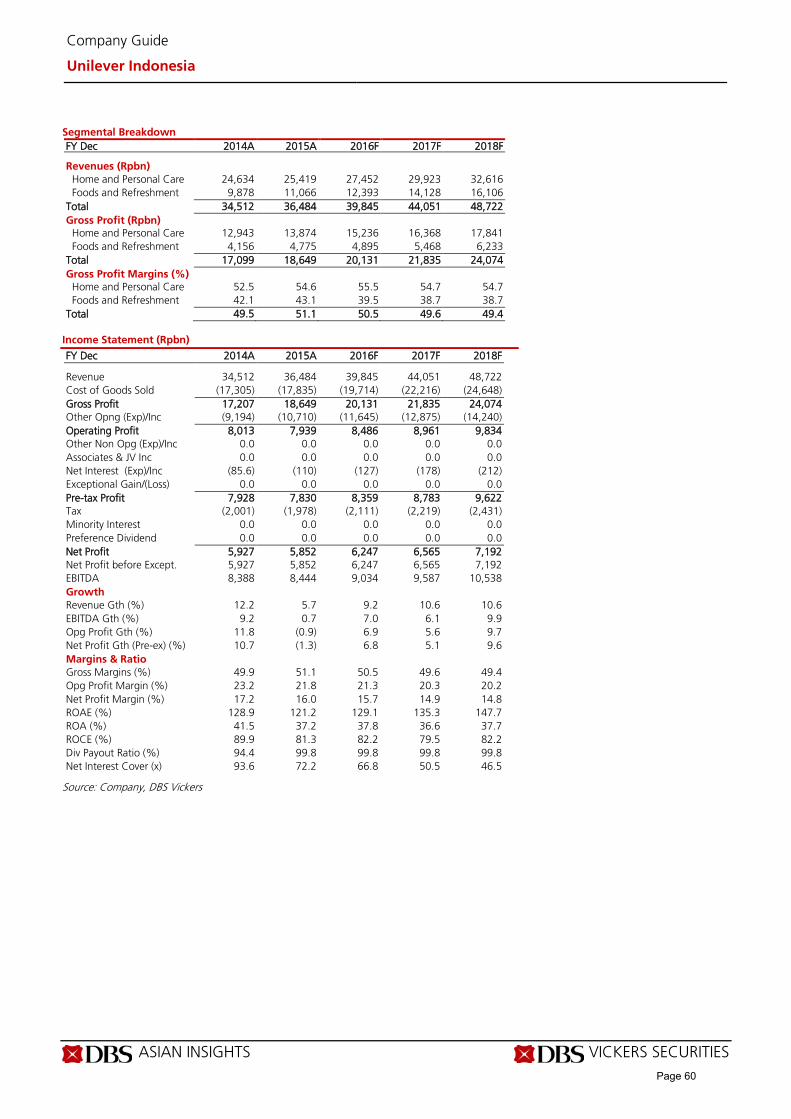

In 2015, communal price increases occurred in most of FMCG’s categories, as producers passed on input cost inflation to consumers. This to some extent has impacted consumers’ purse string negatively in the past one year. Not long after a series of selling price hikes, soft commodity prices have receded. Given the sticky nature of consumer goods’ pricing, consumer companies have enjoyed earnings growth boost in 2016 on a combination of higher selling prices and input costs tailwinds. Key commodity prices have reversed their downward trend in mid-2016. Factoring in inventory lag, we expect higher raw material costs to start impacting consumer staples companies in 4Q16-1Q17. Among staples companies that we cover, only MYOR reported a sequential contraction in gross margin in 3Q16. For FY17, we assume an EBIT margin decline of 20-100bps for UNVR, MYOR and ICBP. Given the still-soft demand environment, we do not expect consumer companies to

aggressively raise selling prices and will take a gradual approach instead. We project a slower earnings growth of 6% y-o-y in FY17F vs. 11% y-o-y in FY16F, with revenue growth holding steady at 10% y-o-y in FY17F. Key soft commodity prices trend (quarterly avg. price)

USDIDR Wheat CPO Skim Milk

Powder Coffee Cocoa Sugar

y-o-y

1Q16 6% -11% 9% -31% -22% 1% 2%

2Q16 1% -7% 19% -17% -5% 0% 37%

3Q16 -5% -21% 26% 21% 18% -8% 79%

4Q16 -4% -18% 32% 18% 25% -23% 42%

q-o-q

1Q16 -2% -5% 11% -11% -1% -10% -2%

2Q16 -1% 1% 5% -2% 6% 4% 18%

3Q16 -1% -14% 1% 17% 14% -2% 19%

4Q16 1% -1% 12% 15% 4% -16% 3%

Source: Bloomberg Finance L.P., Global Dairy Trade, DBS Vickers, DBS Bank

Consumer staples’ gross margin trend

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P.

1.30 1.51

1.69 1.91

2.08 19%

16%

12% 12%

9%

0%

5%

10%

15%

20%

25%

-

0.50

1.00

1.50

2.00

2.50

2013 2014 2015 2016 2017

Avg. minimum wage, Rp mn (LHS) Growth y-o-y (RHS)

0%

10%

20%

30%

40%

50%

60%

10%

15%

20%

25%

30%

35%

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

ICBP INDF MYOR UNVR (RHS) Aggregate ex-INDF

Page 5

Industry Focus

Indonesia Consumer

Page 6

Consumer staples sector’s forward PE band

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P. Consumer staples companies’ PE valuation range in the past five years

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P.

Retailers – is it time for bargain-hunting?

We believe the retail sector warrants a re-look as some names trade below their historical mean valuation. Broad-based sector re-rating is possible if we see signs of firmer demand recovery. Retailers’ PE discount over staples has widened in the past two years, reflecting where we are in the economic cycle. On top of the cyclicality factor, the risk of structural shifts from one retail channel to another – from brick and mortar to e-commerce retailing and from supermarkets or hypermarkets to minimarkets – has also contributed to the sector de-rating. Among our coverage, LPPF now trades at 2.5SD below its historical mean PE. We believe this is partly due to concerns over potential higher capex in the future as the company works its way to be a leading omni-channel retailer in Indonesia. Meanwhile, MPPA saw its sales slowing down on the back of a slow demand environment, which prompted its customers to cut down spending on discretionary items such as electronics and clothes. Tightening competition among retail channels has also impacted MPPA’s sales negatively. Competition risk has yet to abate as the two largest minimarket chains, Indomaret and Alfamart (AMRT), are still

expanding aggressively. Both companies on average opened eight new minimarkets per day in the past three years. In 2017, Indomaret and Alfamart have announced its plan to open 1,600 and 1,400 new stores respectively. The combined store opening target of 3,000 is a tad higher than last year’s target of 2,990 stores. Excluding MPPA, we think the downside risks to retailers’ earnings and share price are lower compared to those of staples. It is worth highlighting that over the past one year, retailers have coped well with the economic slowdown. Inventory trend has remained healthy with no sign of a build-up despite the slowing sales growth (refer to the subsequent chart). Should the pace of demand recovery remain slow in 2017, the healthy inventory level would keep the risk of margin compression low, in our view. Retailers’ revenue and inventory growth trend*

*LPPF and MAPI. We excluded MPPA as the company changed its inventory measurement method in 3Q16. Source: Companies, DBS Vickers, DBS Bank Retailers’ gross margin trend (trailing 12-month)

Source: Companies, DBS Vickers, DBS Bank

20

25

30

35

40

45

50

+2sd

+1sd

‐1sd

‐2sd

Avg.

5

15

25

35

45

55

65

75

85

95

ICBP INDF UNVR MYOR Staples

-

1,000

2,000

3,000

4,000

5,000

6,000

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

4Q11 2Q12 4Q12 2Q13 4Q13 2Q14 4Q14 2Q15 4Q15 2Q16

Inventory, Rp bn (RHS) T12M revenue growth y-o-y (LHS)

Inventory growth y-o-y (LHS)

15%

15%

16%

16%

17%

17%

18%

18%

35%

40%

45%

50%

55%

60%

65%

70%

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

LPPF (LHS) MAPI (LHS) Aggregate (LHS) MPPA (RHS)

Page 6

Industry Focus

Indonesia Consumer

Page 7

Retailers’ PE valuation range in the past five years

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P.

Retailers’ PE relative to consumer staples companies

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P.

What consensus is expecting?

For staples (ICBP, UNVR, MYOR), consensus is expecting 13% and 12% y-o-y net profit growth in FY16 and FY17, respectively, vs. 12% y-o-y growth in FY15A. Expectation appears to be high for staples. With no growth slowdown expected in 2017, the numbers suggest that consensus has assumed either one of these scenarios or the combination of the two to play out in FY17: a) costs are going to be stable or some cost efficiency measures would be rolled out to offset the impact of commodity prices or imported inflation; or, b) consumer staples companies would be able to successfully pass through cost inflation through price increases. The inability to fully pass on cost inflation through price hikes presents downside risk to our and consensus’ earnings forecasts. Meanwhile, retailers are expected to see a strong pick-up in earnings growth in 2016 and 2017. Consensus currently expects 21% y-o-y net profit growth in FY16 and 25% y-o-y in FY17 – an upturn after a 2% decline in net profit in FY15A.

Staples – DBS’ net profit forecast relative to consensus

Source: Bloomberg Finance L.P., DBS Vickers, DBS Bank Retailers – DBS’ net profit forecast relative to consensus

Source: Bloomberg Finance L.P., DBS Vickers, DBS Bank

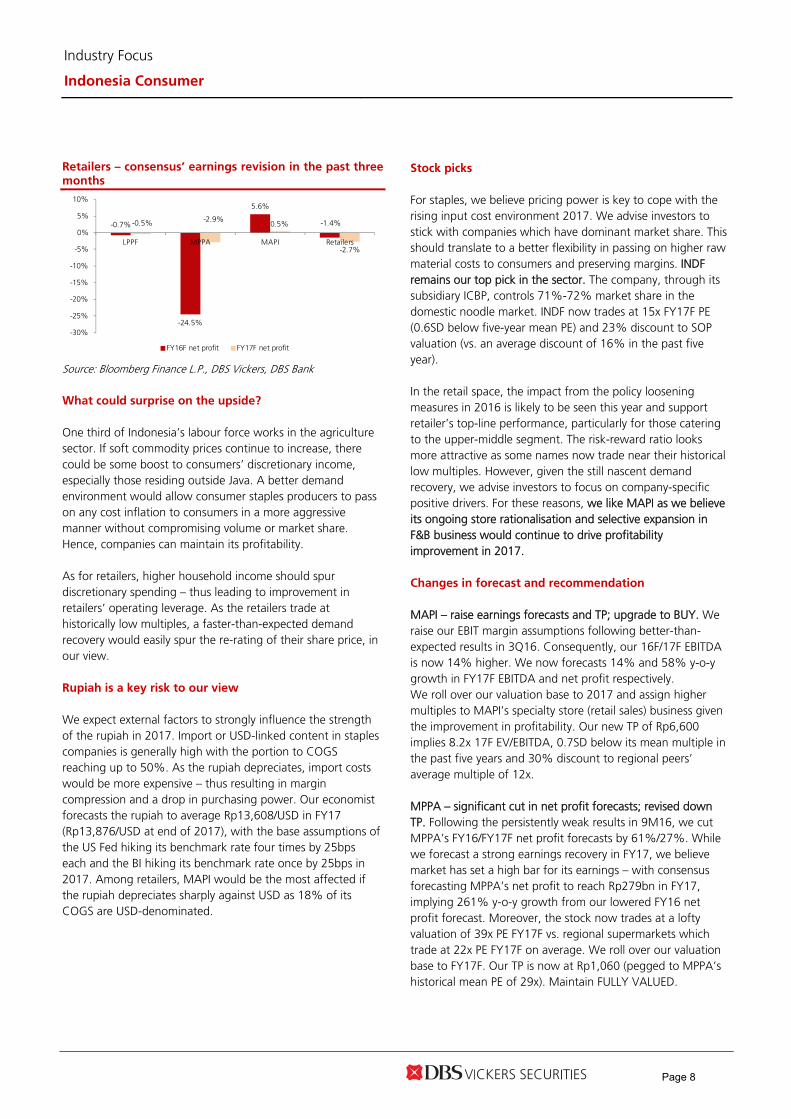

Staples – consensus’ earnings revision in the past three months

Source: Bloomberg Finance L.P., DBS Vickers, DBS Bank

5

55

105

155

205

255

305

MAPI LPPF MPPA Retailers

5

15

25

35

45

55

65

+2sd

+1sd

‐1sd

‐2sd

Avg.

0.98

1.01

0.97

1.01

0.98

1.03

0.96

0.92 0.92

0.95

INDF ICBP UNVR MYOR Staples

Net profit FY16F Net profit FY17F

0.98 1.00

0.86

0.98 0.98 0.96 0.94

0.74

0.94 0.96

LPPF MAPI MPPA Retailers Retailers ex-MPPA

Net profit FY16F Net profit FY17F

-0.2% 0.0%

-0.5%

-0.3% -0.1%

-0.7% -0.8%

-2.0%

2.5%

-0.3%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

UNVR ICBP INDF MYOR Staples*

FY16F net profit FY17F net profit

Page 7

Industry Focus

Indonesia Consumer

Page 8

Retailers – consensus’ earnings revision in the past three months

Source: Bloomberg Finance L.P., DBS Vickers, DBS Bank

What could surprise on the upside?

One third of Indonesia’s labour force works in the agriculture sector. If soft commodity prices continue to increase, there could be some boost to consumers’ discretionary income, especially those residing outside Java. A better demand environment would allow consumer staples producers to pass on any cost inflation to consumers in a more aggressive manner without compromising volume or market share. Hence, companies can maintain its profitability. As for retailers, higher household income should spur discretionary spending – thus leading to improvement in retailers’ operating leverage. As the retailers trade at historically low multiples, a faster-than-expected demand recovery would easily spur the re-rating of their share price, in our view. Rupiah is a key risk to our view

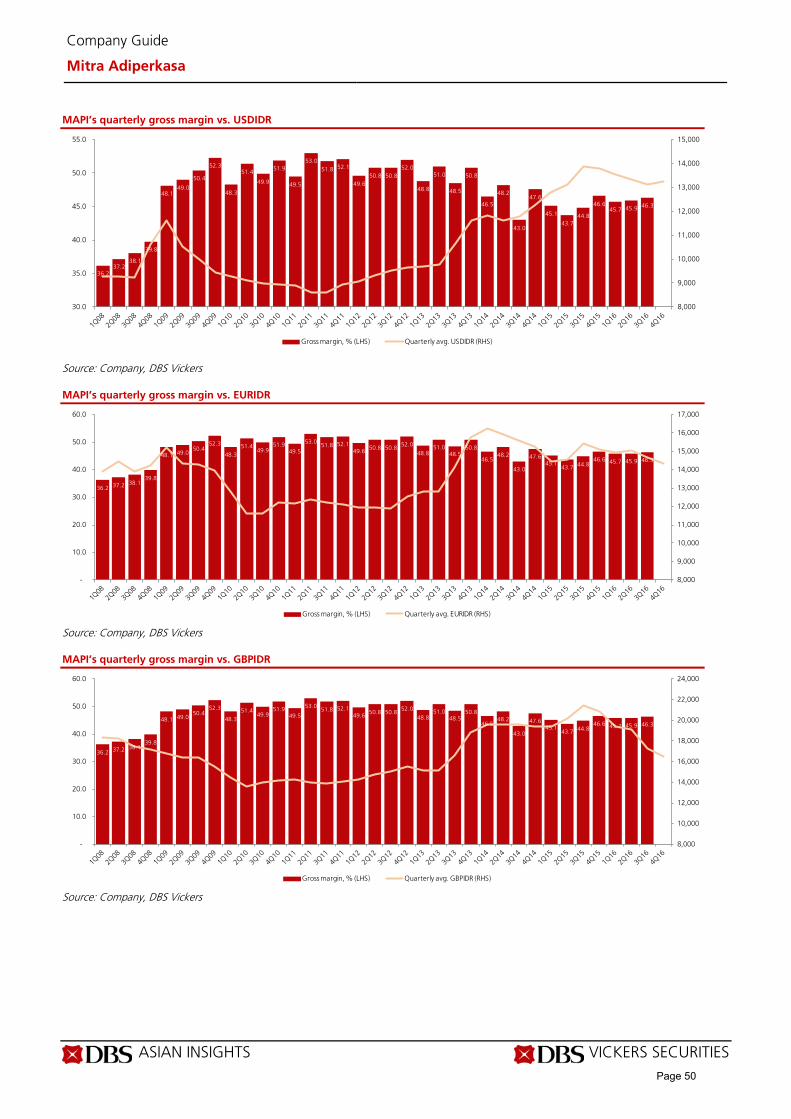

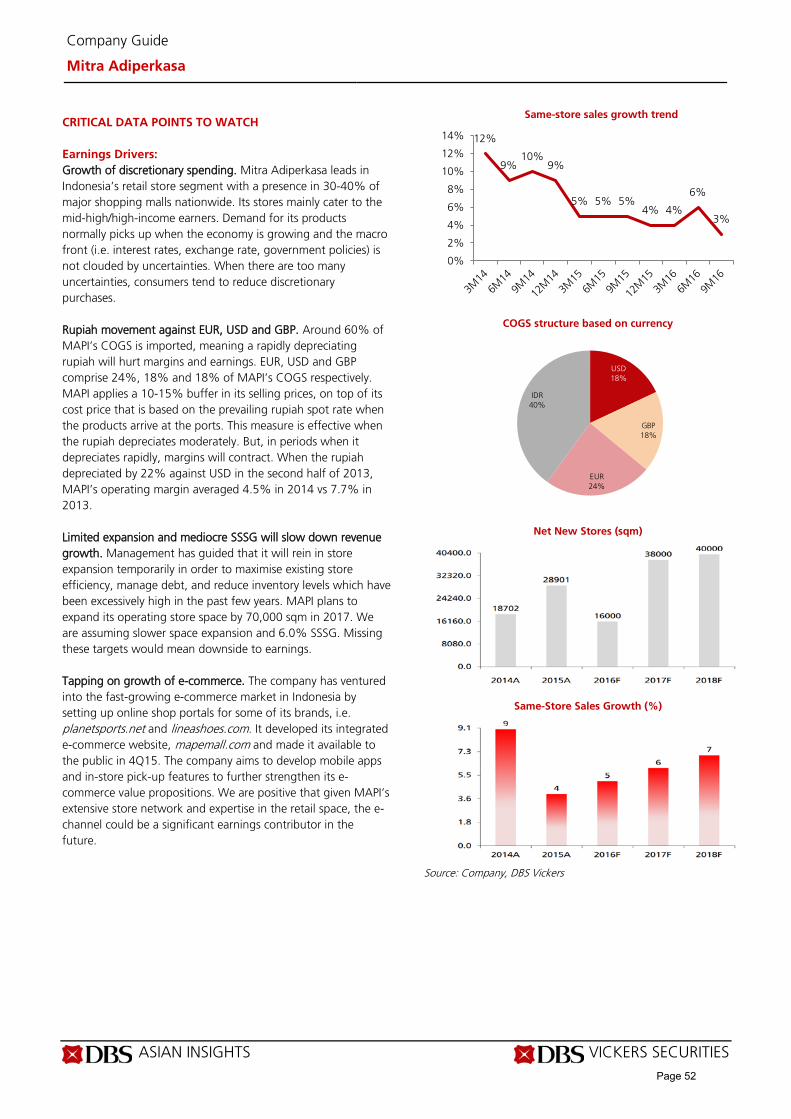

We expect external factors to strongly influence the strength of the rupiah in 2017. Import or USD-linked content in staples companies is generally high with the portion to COGS reaching up to 50%. As the rupiah depreciates, import costs would be more expensive – thus resulting in margin compression and a drop in purchasing power. Our economist forecasts the rupiah to average Rp13,608/USD in FY17 (Rp13,876/USD at end of 2017), with the base assumptions of the US Fed hiking its benchmark rate four times by 25bps each and the BI hiking its benchmark rate once by 25bps in 2017. Among retailers, MAPI would be the most affected if the rupiah depreciates sharply against USD as 18% of its COGS are USD-denominated.

Stock picks

For staples, we believe pricing power is key to cope with the rising input cost environment 2017. We advise investors to stick with companies which have dominant market share. This should translate to a better flexibility in passing on higher raw material costs to consumers and preserving margins. INDF remains our top pick in the sector. The company, through its subsidiary ICBP, controls 71%-72% market share in the domestic noodle market. INDF now trades at 15x FY17F PE (0.6SD below five-year mean PE) and 23% discount to SOP valuation (vs. an average discount of 16% in the past five year). In the retail space, the impact from the policy loosening measures in 2016 is likely to be seen this year and support retailer’s top-line performance, particularly for those catering to the upper-middle segment. The risk-reward ratio looks more attractive as some names now trade near their historical low multiples. However, given the still nascent demand recovery, we advise investors to focus on company-specific positive drivers. For these reasons, we like MAPI as we believe its ongoing store rationalisation and selective expansion in F&B business would continue to drive profitability improvement in 2017. Changes in forecast and recommendation

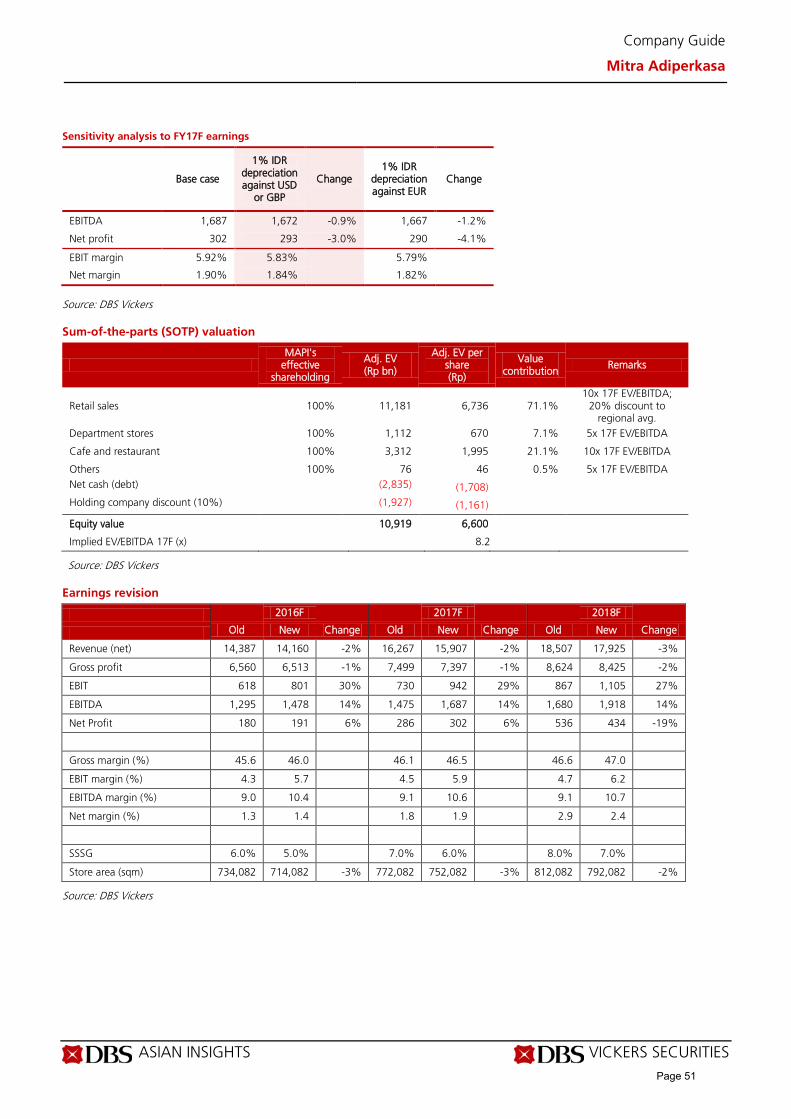

MAPI – raise earnings forecasts and TP; upgrade to BUY. We raise our EBIT margin assumptions following better-than-expected results in 3Q16. Consequently, our 16F/17F EBITDA is now 14% higher. We now forecasts 14% and 58% y-o-y growth in FY17F EBITDA and net profit respectively. We roll over our valuation base to 2017 and assign higher multiples to MAPI’s specialty store (retail sales) business given the improvement in profitability. Our new TP of Rp6,600 implies 8.2x 17F EV/EBITDA, 0.7SD below its mean multiple in the past five years and 30% discount to regional peers’ average multiple of 12x. MPPA – significant cut in net profit forecasts; revised down TP. Following the persistently weak results in 9M16, we cut MPPA’s FY16/FY17F net profit forecasts by 61%/27%. While we forecast a strong earnings recovery in FY17, we believe market has set a high bar for its earnings – with consensus forecasting MPPA’s net profit to reach Rp279bn in FY17, implying 261% y-o-y growth from our lowered FY16 net profit forecast. Moreover, the stock now trades at a lofty valuation of 39x PE FY17F vs. regional supermarkets which trade at 22x PE FY17F on average. We roll over our valuation base to FY17F. Our TP is now at Rp1,060 (pegged to MPPA’s historical mean PE of 29x). Maintain FULLY VALUED.

-0.7%

-24.5%

5.6%

-1.4%-0.5% -2.9%0.5%

-2.7%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

LPPF MPPA MAPI Retailers

FY16F net profit FY17F net profit

Page 8

Industry Focus

Indonesia Consumer

Page 9

UNVR – revised up earnings on better-than-expected operational efficiency. We revise up UNVR’s FY16/FY17 net profit forecasts by 7% for better cost control. Our FY17F net profit is now 8% below consensus as we assume lower margin in FY17F on the back of higher raw material costs, particularly palm oil. Our FULLY VALUED call is unchanged as we believe UNVR’s lofty valuation of 49x PE FY17F is not justified by its earnings growth prospect. Summary of earnings forecast changes

Source: DBS Vickers, DBS Bank

Summary of recommendation changes

Source: DBS Vickers, DBS Bank

Old New Change Old New ChangeUNVR 5,836 6,247 7% 6,138 6,564 7%MYOR 1,264 1,305 3% 1,431 1,454 2%ICBP 3,660 3,660 0% 3,953 3,868 -2%INDF 3,927 3,927 0% 4,529 4,545 0%LPPF 2,130 2,095 -2% 2,429 2,357 -3%MAPI 180 191 6% 286 302 6%MPPA 197 77 -61% 267 196 -27%A ggregate 17,194 17,502 2% 19,033 19,287 1%

F Y16F net prof it F Y17F net prof it

Old New ChangeUNVR 30,700 36,200 18% Maintain Fully ValuedMYOR 1,568 1,700 8% Maintain HoldICBP 9,800 9,000 -8% Maintain HoldINDF 9,900 9,100 -8% Maintain BuyLPPF 20,300 16,200 -20% Maintain HoldMAPI 4,150 6,600 59% Upgrade to Buy from HoldMPPA 1,160 1,060 -9% Maintain Fully Valued

Target PriceRecommendat ion

Page 9

Industry Focus

Indonesia Consumer

Page 10

Indonesian consumer sector: valuation summary

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P

Company ICBP INDF MYOR UNVR MAPI LPPF MPPA

Market cap (US$m) 7,438 5,238 3,062 23,888 676 3,355 551Share price (Rp)* 8,500 7,950 1,825 41,725 5,425 15,325 1,365Recommendation HOLD BUY HOLD FULLY VALUED BUY HOLD FULLY VALUEDTarget price 9,000 9,100 1,700 36,200 6,600 16,200 1,060Upside (downside) 6% 14% -7% -13% 22% 6% -22%PE (x)FY15A 33.0 23.5 33.4 54.4 241.2 25.1 40.1FY16F 27.1 17.8 31.3 51.0 47.0 21.3 95.1FY17F 25.6 15.4 28.1 48.5 29.8 19.0 37.4FY18F 23.0 14.3 24.3 44.3 20.8 17.0 29.3PB (x)FY15A 6.4 2.6 8.0 65.9 3.0 40.4 2.9FY16F 5.7 2.4 6.8 65.8 2.9 22.9 2.9FY17F 5.2 2.2 5.8 65.6 2.6 15.7 2.7FY18F 4.6 2.1 5.0 65.4 2.4 11.7 2.6EV/EBITDA (x)FY15A 20.3 9.5 18.5 37.8 11.2 17.1 13.1FY16F 17.2 9.1 16.9 35.4 8.1 14.9 14.6FY17F 15.9 8.4 15.3 33.5 7.0 13.1 10.7FY18F 14.3 7.5 13.5 30.5 6.0 11.4 9.0Revenue growthFY15A 5.7% 0.7% 4.6% 5.7% 8.5% 13.6% 2.5%FY16F 9.8% 5.1% 12.3% 9.2% 10.3% 10.5% -0.4%FY17F 8.8% 7.5% 13.9% 10.6% 12.3% 10.9% 9.4%FY18F 9.2% 8.9% 12.9% 10.6% 12.7% 11.5% 9.0%Net profit growthFY15A 13.5% -24.7% 202.3% -1.3% -52.8% 25.5% -67.0%FY16F 22.0% 32.3% 6.9% 6.8% 412.8% 17.6% -57.8%FY17F 5.7% 15.7% 11.4% 5.1% 57.7% 12.5% 154.2%FY18F 11.4% 7.7% 15.6% 9.6% 43.7% 11.6% 27.5%Gros s marginFY15A 30.3% 26.9% 28.3% 51.1% 45.1% 35.2% 16.2%FY16F 29.5% 26.8% 26.0% 50.5% 46.0% 35.5% 15.7%FY17F 28.6% 26.8% 25.2% 49.6% 46.5% 35.9% 15.9%FY18F 28.8% 26.8% 25.2% 49.4% 47.0% 36.1% 15.9%EBIT marginFY15A 12.6% 11.5% 12.6% 21.8% 4.1% 14.4% 1.8%FY16F 13.5% 11.8% 12.0% 21.3% 5.7% 14.8% 1.3%FY17F 13.4% 12.0% 11.5% 20.3% 5.9% 15.2% 2.1%FY18F 13.6% 12.5% 11.5% 20.2% 6.2% 15.4% 2.4%Net gearingFY15A Net cash 24% 29% 18% 51% Net cash 9%FY16F Net cash 18% 24% 27% 49% Net cash 16%FY17F Net cash 17% 18% 35% 45% Net cash 18%FY18F Net cash 16% 11% 40% 40% Net cash 13%ROAEFY15A 19.4% 10.9% 24.0% 121.2% 1.3% 161.0% 7.3%FY16F 21.2% 13.4% 21.8% 129.1% 6.1% 107.2% 3.0%FY17F 20.1% 14.4% 20.7% 135.3% 8.8% 82.9% 7.3%FY18F 20.2% 14.4% 20.5% 147.7% 11.4% 68.8% 8.8%

Page 10

Industry Focus

Indonesia Consumer

Page 11

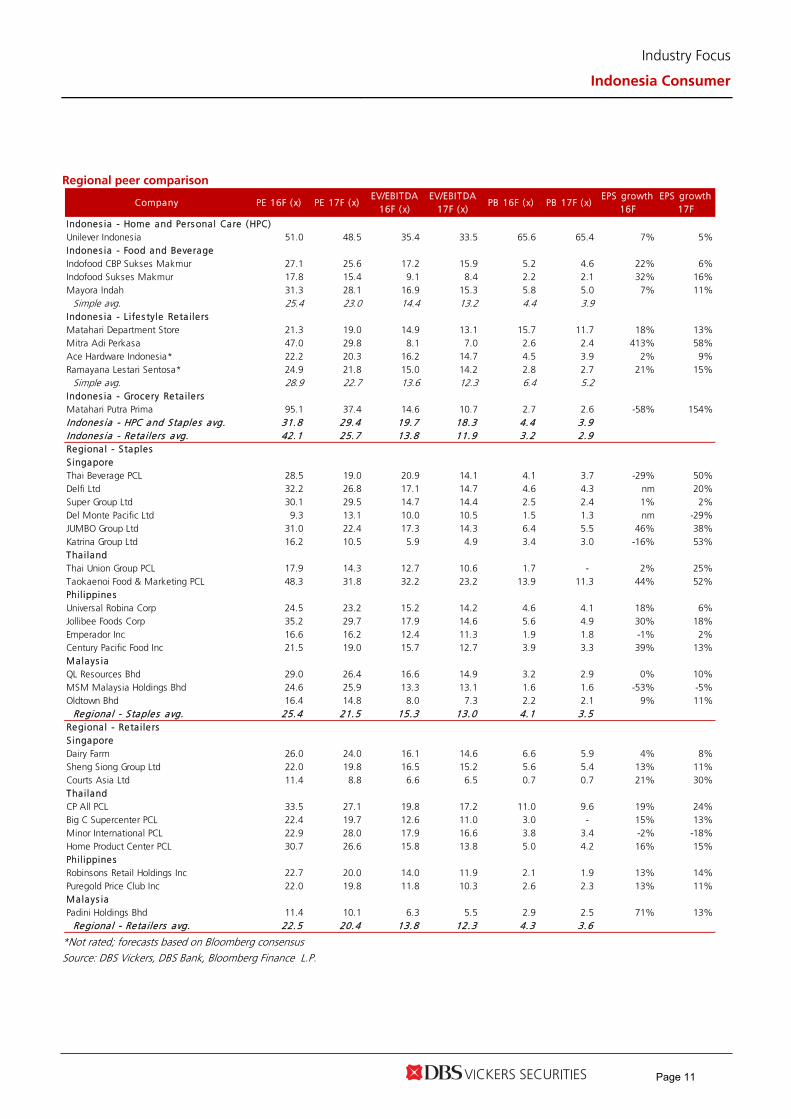

Regional peer comparison

*Not rated; forecasts based on Bloomberg consensus Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P.

Company PE 16F (x) PE 17F (x)EV/EBITDA

16F (x)EV/EBITDA

17F (x)PB 16F (x) PB 17F (x)

EPS growth 16F

EPS growth 17F

Indones ia - Home and Pers ona l Care (HPC)Unilever Indonesia 51.0 48.5 35.4 33.5 65.6 65.4 7% 5%Indones ia - Food and BeverageIndofood CBP Sukses Makmur 27.1 25.6 17.2 15.9 5.2 4.6 22% 6%Indofood Sukses Makmur 17.8 15.4 9.1 8.4 2.2 2.1 32% 16%Mayora Indah 31.3 28.1 16.9 15.3 5.8 5.0 7% 11%

Simple avg. 25.4 23.0 14.4 13.2 4.4 3.9 Indones ia - L ifes tyle Reta i le rsMatahari Department Store 21.3 19.0 14.9 13.1 15.7 11.7 18% 13%Mitra Adi Perkasa 47.0 29.8 8.1 7.0 2.6 2.4 413% 58%Ace Hardware Indonesia* 22.2 20.3 16.2 14.7 4.5 3.9 2% 9%Ramayana Lestari Sentosa* 24.9 21.8 15.0 14.2 2.8 2.7 21% 15%

Simple avg. 28.9 22.7 13.6 12.3 6.4 5.2 Indones ia - Grocery Reta i le rsMatahari Putra Prima 95.1 37.4 14.6 10.7 2.7 2.6 -58% 154%Indones ia - HPC and S taples avg. 31.8 29.4 19.7 18.3 4.4 3.9 Indones ia - Reta i le rs avg. 42.1 25.7 13.8 11.9 3.2 2.9 Regiona l - S taplesS ingaporeThai Beverage PCL 28.5 19.0 20.9 14.1 4.1 3.7 -29% 50%Delfi Ltd 32.2 26.8 17.1 14.7 4.6 4.3 nm 20%Super Group Ltd 30.1 29.5 14.7 14.4 2.5 2.4 1% 2%Del Monte Pacific Ltd 9.3 13.1 10.0 10.5 1.5 1.3 nm -29%JUMBO Group Ltd 31.0 22.4 17.3 14.3 6.4 5.5 46% 38%Katrina Group Ltd 16.2 10.5 5.9 4.9 3.4 3.0 -16% 53%Tha ilandThai Union Group PCL 17.9 14.3 12.7 10.6 1.7 - 2% 25%Taokaenoi Food & Marketing PCL 48.3 31.8 32.2 23.2 13.9 11.3 44% 52%Phil ippinesUniversal Robina Corp 24.5 23.2 15.2 14.2 4.6 4.1 18% 6%Jollibee Foods Corp 35.2 29.7 17.9 14.6 5.6 4.9 30% 18%Emperador Inc 16.6 16.2 12.4 11.3 1.9 1.8 -1% 2%Century Pacific Food Inc 21.5 19.0 15.7 12.7 3.9 3.3 39% 13%Malays iaQL Resources Bhd 29.0 26.4 16.6 14.9 3.2 2.9 0% 10%MSM Malaysia Holdings Bhd 24.6 25.9 13.3 13.1 1.6 1.6 -53% -5%Oldtown Bhd 16.4 14.8 8.0 7.3 2.2 2.1 9% 11%

Regiona l - S taples avg. 25.4 21.5 15.3 13.0 4.1 3.5 Regiona l - Reta i le rsS ingaporeDairy Farm 26.0 24.0 16.1 14.6 6.6 5.9 4% 8%Sheng Siong Group Ltd 22.0 19.8 16.5 15.2 5.6 5.4 13% 11%Courts Asia Ltd 11.4 8.8 6.6 6.5 0.7 0.7 21% 30%Tha ilandCP All PCL 33.5 27.1 19.8 17.2 11.0 9.6 19% 24%Big C Supercenter PCL 22.4 19.7 12.6 11.0 3.0 - 15% 13%Minor International PCL 22.9 28.0 17.9 16.6 3.8 3.4 -2% -18%Home Product Center PCL 30.7 26.6 15.8 13.8 5.0 4.2 16% 15%Phil ippinesRobinsons Retail Holdings Inc 22.7 20.0 14.0 11.9 2.1 1.9 13% 14%Puregold Price Club Inc 22.0 19.8 11.8 10.3 2.6 2.3 13% 11%Malays iaPadini Holdings Bhd 11.4 10.1 6.3 5.5 2.9 2.5 71% 13%

Regiona l - Reta ile rs avg. 22.5 20.4 13.8 12.3 4.3 3.6

Page 11

Industry Focus

Indonesia Consumer

Page 12

COMPANY GUIDES COMPANY GUIDES COMPANY GUIDES

COMPANY GUIDES

COMPANY GUIDES

Page 12

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:MA, PY

HOLD Last Traded Price ( 8 Feb 2017): Rp8,500 (JCI : 5,361.10) Price Target 12-mth: Rp9,000 (6% upside) (Prev Rp9,800) Potential Catalyst: Further drop in raw material prices, particularly wheat, and rupiah appreciation Where we differ: Broadly in line with consensus Analyst Tiesha PUTRI +6221 30034931 [email protected] Andy SIM CFA +65 6682 3718 [email protected]

What’s New • Margin to moderate as key raw material prices

namely CPO, sugar and milk powder have rallied

• ICBP raised noodle prices by 4-5% in early January 2017

• Maintain HOLD; TP cut to Rp9,000

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2015A 2016F 2017F 2018F Revenue 31,741 34,848 37,900 41,380 EBITDA 4,691 5,473 5,864 6,451 Pre-tax Profit 4,010 4,972 5,255 5,853 Net Profit 3,001 3,660 3,868 4,308 Net Pft (Pre Ex.) 3,001 3,660 3,868 4,308 Net Pft Gth (Pre-ex) (%) 13.5 22.0 5.7 11.4 EPS (Rp) 257 314 332 369 EPS Pre Ex. (Rp) 257 314 332 369 EPS Gth Pre Ex (%) 13 22 6 11 Diluted EPS (Rp) 257 314 332 369 Net DPS (Rp) 129 157 166 185 BV Per Share (Rp) 1,325 1,482 1,648 1,833 PE (X) 33.0 27.1 25.6 23.0 PE Pre Ex. (X) 33.0 27.1 25.6 23.0 P/Cash Flow (X) 28.4 21.7 22.3 20.3 EV/EBITDA (X) 20.3 17.2 15.9 14.3 Net Div Yield (%) 1.5 1.8 2.0 2.2 P/Book Value (X) 6.4 5.7 5.2 4.6 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 19.4 21.2 20.1 20.2 Earnings Rev (%): 0 (2) (1) Consensus EPS (Rp): 594 N/A N/A Other Broker Recs: B: 16 S: 1 H: 12

Source of all data on this page: Company, DBS Vickers, Bloomberg Finance L.P

A less exciting year Input cost tailwind dissipates. ICBP’s share price has underperformed the JCI by 15% since early Sep 2016, possibly owing to concerns over rising raw material prices. As mentioned in our previous report, we believe ICBP’s margin had peaked in 3Q16 and would moderate going forward as the prices of its key raw materials, namely CPO, sugar, milk powder and recently chilli, have risen considerably. Pre-emptive price increase for noodles in Jan 2017. The company raised its noodle ASP by Rp100/pack in early January 2017, translating to 4-5% hike. We believe this price hike is a pre-emptive move taken to preserve its profitability in 2017. ICBP remains the price leader in the domestic noodle market with a market share of 71-72% in the past five years. The noodle segment contributed to 65% and 75% of ICBP’s consolidated revenue and EBIT respectively. An improving demand environment and the strong pricing power of ICBP’s noodle products are two things that it can leverage on to prevent a sharp margin contraction. 2017 outlook: expecting deceleration in earnings growth. Looking ahead to 2017, we expect earnings to only grow by 6% y-o-y as input cost rises. This is a deceleration from 22% y-o-y growth that we projected for FY16. For this reason, we lower our PE multiple to 27x PE FY17F or +1SD of ICBP’s five-year mean PE (from +29x or +2SD above mean PE previously). Our revised TP of Rp9,000 only provides limited upside from the last closing price. Upside risks to our call would be faster-than-expected turnaround of its loss-making beverage business and market share gain, particularly for its less mature segments such as dairy. Valuation: Our TP of Rp9,000 is based on 27x FY17F PE or +1SD of ICBP’s five-year historical mean PE. Key Risks to Our View: Rapid rupiah depreciation and commodity price hikes could hurt ICBP’s margins as they directly impact input costs. At A Glance Issued Capital (m shrs) 11,662 Mkt. Cap (Rpbn/US$m) 99,126 / 7,434 Major Shareholders (%) PT Indofood Sukses Makmur (%) 80.5

Free Float (%) 19.5 3m Avg. Daily Val (US$m) 2.7 ICB Industry : Consumer Goods / Food Producers

DBS Group Research . Equity

9 Feb 2017

Indonesia Company Guide

Indofood CBP Sukses Makmur Version 6 | Bloomberg: ICBP IJ | Reuters: ICBP.JK Refer to important disclosures at the end of this report

Page 13

ASIAN INSIGHTS VICKERS SECURITIES Page 2

Company Guide

Indofood CBP Sukses Makmur

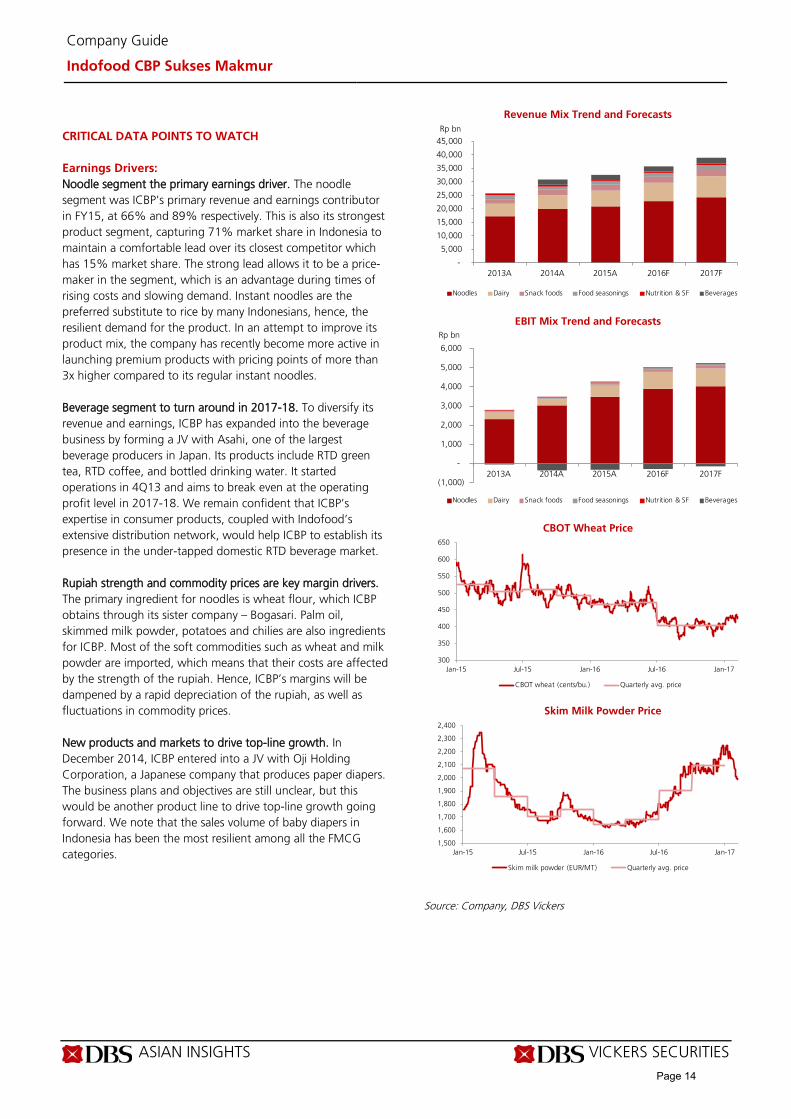

CRITICAL DATA POINTS TO WATCH Earnings Drivers: Noodle segment the primary earnings driver. The noodle segment was ICBP’s primary revenue and earnings contributor in FY15, at 66% and 89% respectively. This is also its strongest product segment, capturing 71% market share in Indonesia to maintain a comfortable lead over its closest competitor which has 15% market share. The strong lead allows it to be a price-maker in the segment, which is an advantage during times of rising costs and slowing demand. Instant noodles are the preferred substitute to rice by many Indonesians, hence, the resilient demand for the product. In an attempt to improve its product mix, the company has recently become more active in launching premium products with pricing points of more than 3x higher compared to its regular instant noodles. Beverage segment to turn around in 2017-18. To diversify its revenue and earnings, ICBP has expanded into the beverage business by forming a JV with Asahi, one of the largest beverage producers in Japan. Its products include RTD green tea, RTD coffee, and bottled drinking water. It started operations in 4Q13 and aims to break even at the operating profit level in 2017-18. We remain confident that ICBP’s expertise in consumer products, coupled with Indofood’s extensive distribution network, would help ICBP to establish its presence in the under-tapped domestic RTD beverage market. Rupiah strength and commodity prices are key margin drivers. The primary ingredient for noodles is wheat flour, which ICBP obtains through its sister company – Bogasari. Palm oil, skimmed milk powder, potatoes and chilies are also ingredients for ICBP. Most of the soft commodities such as wheat and milk powder are imported, which means that their costs are affected by the strength of the rupiah. Hence, ICBP’s margins will be dampened by a rapid depreciation of the rupiah, as well as fluctuations in commodity prices. New products and markets to drive top-line growth. In December 2014, ICBP entered into a JV with Oji Holding Corporation, a Japanese company that produces paper diapers. The business plans and objectives are still unclear, but this would be another product line to drive top-line growth going forward. We note that the sales volume of baby diapers in Indonesia has been the most resilient among all the FMCG categories.

Revenue Mix Trend and Forecasts

EBIT Mix Trend and Forecasts

CBOT Wheat Price

Skim Milk Powder Price

Source: Company, DBS Vickers

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2013A 2014A 2015A 2016F 2017F

Rp bn

Noodles Dairy Snack foods Food seasonings Nutrition & SF Beverages

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

2013A 2014A 2015A 2016F 2017F

Rp bn

Noodles Dairy Snack foods Food seasonings Nutrition & SF Beverages

300

350

400

450

500

550

600

650

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

CBOT wheat (cents/bu.) Quarterly avg. price

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

Skim milk powder (EUR/MT) Quarterly avg. price

Page 14

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Company Guide

Indofood CBP Sukses Makmur

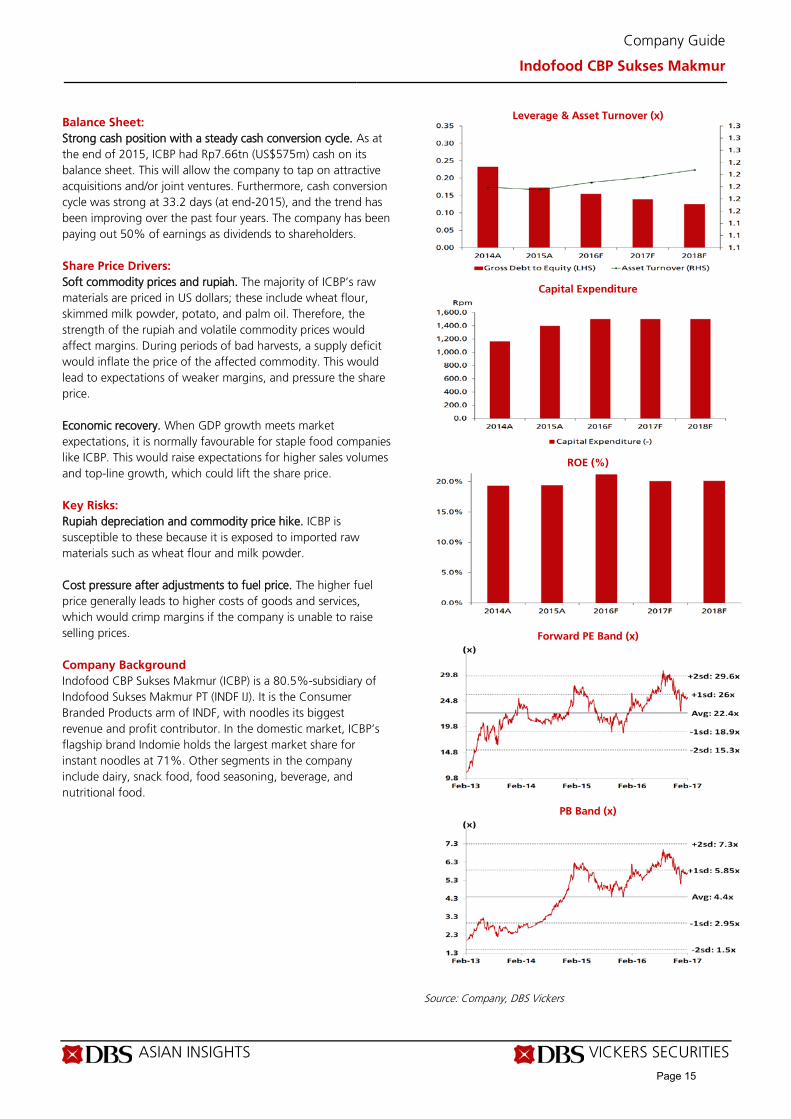

Balance Sheet: Strong cash position with a steady cash conversion cycle. As at the end of 2015, ICBP had Rp7.66tn (US$575m) cash on its balance sheet. This will allow the company to tap on attractive acquisitions and/or joint ventures. Furthermore, cash conversion cycle was strong at 33.2 days (at end-2015), and the trend has been improving over the past four years. The company has been paying out 50% of earnings as dividends to shareholders. Share Price Drivers: Soft commodity prices and rupiah. The majority of ICBP’s raw materials are priced in US dollars; these include wheat flour, skimmed milk powder, potato, and palm oil. Therefore, the strength of the rupiah and volatile commodity prices would affect margins. During periods of bad harvests, a supply deficit would inflate the price of the affected commodity. This would lead to expectations of weaker margins, and pressure the share price. Economic recovery. When GDP growth meets market expectations, it is normally favourable for staple food companies like ICBP. This would raise expectations for higher sales volumes and top-line growth, which could lift the share price. Key Risks: Rupiah depreciation and commodity price hike. ICBP is susceptible to these because it is exposed to imported raw materials such as wheat flour and milk powder. Cost pressure after adjustments to fuel price. The higher fuel price generally leads to higher costs of goods and services, which would crimp margins if the company is unable to raise selling prices. Company Background Indofood CBP Sukses Makmur (ICBP) is a 80.5%-subsidiary of Indofood Sukses Makmur PT (INDF IJ). It is the Consumer Branded Products arm of INDF, with noodles its biggest revenue and profit contributor. In the domestic market, ICBP’s flagship brand Indomie holds the largest market share for instant noodles at 71%. Other segments in the company include dairy, snack food, food seasoning, beverage, and nutritional food.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Vickers

Page 15

ASIAN INSIGHTS VICKERS SECURITIES Page 4

Company Guide

Indofood CBP Sukses Makmur

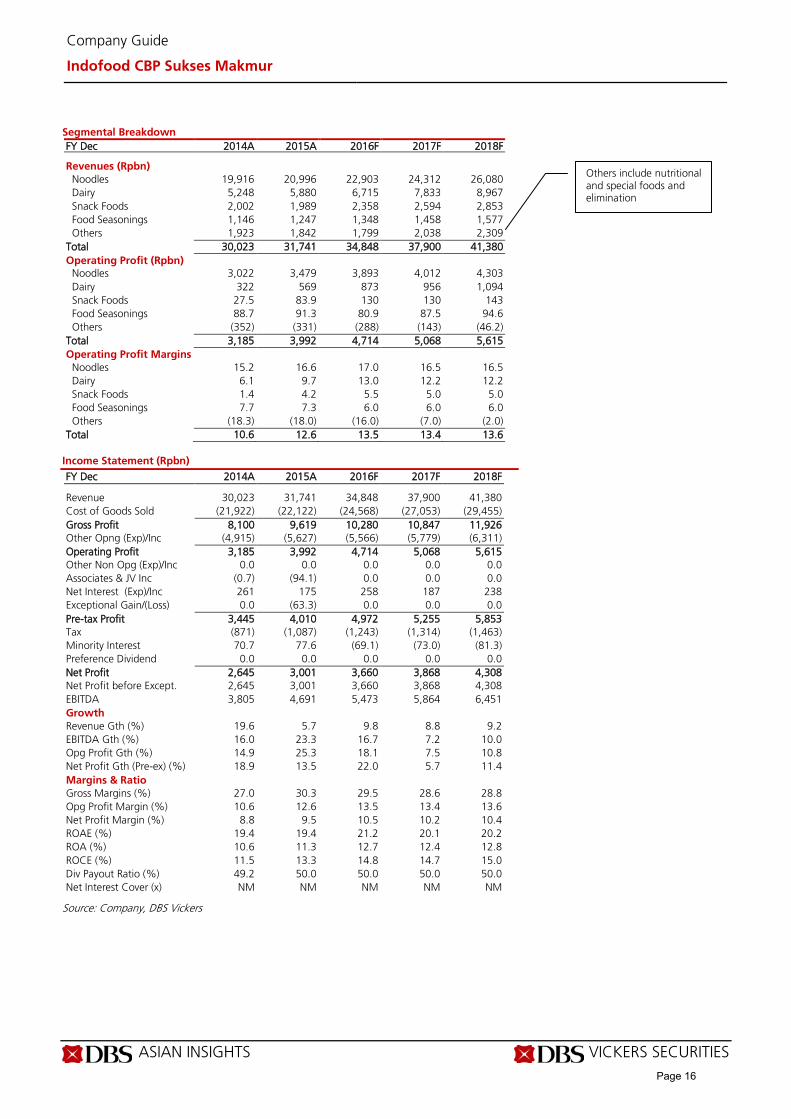

Segmental Breakdown FY Dec 2014A 2015A 2016F 2017F 2018F Revenues (Rpbn) Noodles 19,916 20,996 22,903 24,312 26,080 Dairy 5,248 5,880 6,715 7,833 8,967 Snack Foods 2,002 1,989 2,358 2,594 2,853 Food Seasonings 1,146 1,247 1,348 1,458 1,577 Others 1,923 1,842 1,799 2,038 2,309 Total 30,023 31,741 34,848 37,900 41,380 Operating Profit (Rpbn) Noodles 3,022 3,479 3,893 4,012 4,303 Dairy 322 569 873 956 1,094 Snack Foods 27.5 83.9 130 130 143 Food Seasonings 88.7 91.3 80.9 87.5 94.6 Others (352) (331) (288) (143) (46.2) Total 3,185 3,992 4,714 5,068 5,615 Operating Profit Margins

Noodles 15.2 16.6 17.0 16.5 16.5 Dairy 6.1 9.7 13.0 12.2 12.2 Snack Foods 1.4 4.2 5.5 5.0 5.0 Food Seasonings 7.7 7.3 6.0 6.0 6.0 Others (18.3) (18.0) (16.0) (7.0) (2.0) Total 10.6 12.6 13.5 13.4 13.6

Income Statement (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Revenue 30,023 31,741 34,848 37,900 41,380 Cost of Goods Sold (21,922) (22,122) (24,568) (27,053) (29,455) Gross Profit 8,100 9,619 10,280 10,847 11,926 Other Opng (Exp)/Inc (4,915) (5,627) (5,566) (5,779) (6,311) Operating Profit 3,185 3,992 4,714 5,068 5,615 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc (0.7) (94.1) 0.0 0.0 0.0 Net Interest (Exp)/Inc 261 175 258 187 238 Exceptional Gain/(Loss) 0.0 (63.3) 0.0 0.0 0.0 Pre-tax Profit 3,445 4,010 4,972 5,255 5,853 Tax (871) (1,087) (1,243) (1,314) (1,463) Minority Interest 70.7 77.6 (69.1) (73.0) (81.3) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 2,645 3,001 3,660 3,868 4,308 Net Profit before Except. 2,645 3,001 3,660 3,868 4,308 EBITDA 3,805 4,691 5,473 5,864 6,451 Growth Revenue Gth (%) 19.6 5.7 9.8 8.8 9.2 EBITDA Gth (%) 16.0 23.3 16.7 7.2 10.0 Opg Profit Gth (%) 14.9 25.3 18.1 7.5 10.8 Net Profit Gth (Pre-ex) (%) 18.9 13.5 22.0 5.7 11.4 Margins & Ratio Gross Margins (%) 27.0 30.3 29.5 28.6 28.8 Opg Profit Margin (%) 10.6 12.6 13.5 13.4 13.6 Net Profit Margin (%) 8.8 9.5 10.5 10.2 10.4 ROAE (%) 19.4 19.4 21.2 20.1 20.2 ROA (%) 10.6 11.3 12.7 12.4 12.8 ROCE (%) 11.5 13.3 14.8 14.7 15.0 Div Payout Ratio (%) 49.2 50.0 50.0 50.0 50.0 Net Interest Cover (x) NM NM NM NM NM

Source: Company, DBS Vickers

Others include nutritional and special foods and elimination

Page 16

ASIAN INSIGHTS VICKERS SECURITIES Page 5

Company Guide

Indofood CBP Sukses Makmur

Quarterly / Interim Income Statement (Rpbn)

FY Dec 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 Revenue 7,545 7,645 8,922 9,253 8,296 Cost of Goods Sold (5,229) (5,418) (6,113) (6,302) (5,596) Gross Profit 2,315 2,227 2,809 2,951 2,700 Other Oper. (Exp)/Inc (1,311) (1,432) (1,477) (1,545) (1,469) Operating Profit 1,004 796 1,332 1,406 1,232 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc (41.8) (9.1) (20.7) (43.9) (20.6) Net Interest (Exp)/Inc (71.2) 153 35.4 15.6 45.6 Exceptional Gain/(Loss) 0.0 (63.3) 0.0 0.0 0.0 Pre-tax Profit 891 876 1,346 1,378 1,257 Tax (237) (280) (348) (328) (354) Minority Interest 50.9 (39.7) (53.9) (15.2) (50.3) Net Profit 706 557 945 1,035 853 Net profit bef Except. 706 620 945 1,035 853 EBITDA 1,180 980 1,514 1,588 1,419 Growth Revenue Gth (%) (12.1) 1.3 16.7 3.7 (10.3) EBITDA Gth (%) (12.9) (17.0) 54.5 4.9 (10.6) Opg Profit Gth (%) (15.1) (20.8) 67.4 5.6 (12.4) Net Profit Gth (Pre-ex) (%) (25.1) (12.1) 52.4 9.5 (17.6) Margins Gross Margins (%) 30.7 29.1 31.5 31.9 32.5 Opg Profit Margins (%) 13.3 10.4 14.9 15.2 14.8 Net Profit Margins (%) 9.4 7.3 10.6 11.2 10.3

Balance Sheet (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Net Fixed Assets 5,810 6,556 7,298 8,001 8,665 Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0 Other LT Assets 5,598 6,044 6,044 6,044 6,044 Cash & ST Invts 7,285 7,643 8,880 9,894 11,124 Inventory 2,813 2,547 2,976 3,277 3,568 Debtors 3,103 3,513 3,412 3,703 4,046 Other Current Assets 421 258 258 258 258 Total Assets 25,030 26,561 28,868 31,177 33,705 ST Debt

1,805 1,395 1,395 1,395 1,395 Creditor 2,756 2,581 2,989 3,291 3,583 Other Current Liab 1,648 2,027 2,027 2,027 2,027 LT Debt 1,590 1,432 1,432 1,432 1,432 Other LT Liabilities 2,647 2,740 2,740 2,740 2,740 Shareholder’s Equity 13,656 15,455 17,285 19,219 21,373 Minority Interests 929 932 1,001 1,074 1,156 Total Cap. & Liab. 25,030 26,561 28,868 31,177 33,705 Non-Cash Wkg. Capital 1,933 1,711 1,631 1,921 2,262 Net Cash/(Debt) 3,891 4,817 6,054 7,068 8,298 Debtors Turn (avg days) 37.7 40.4 35.7 35.7 35.7 Creditors Turn (avg days) 47.2 44.0 45.8 45.8 45.7 Inventory Turn (avg days) 48.2 43.4 45.6 45.6 45.5 Asset Turnover (x) 1.2 1.2 1.2 1.2 1.2 Current Ratio (x) 2.2 2.3 2.4 2.6 2.7 Quick Ratio (x) 1.7 1.9 1.9 2.0 2.2 Net Debt/Equity (X) CASH CASH CASH CASH CASH Net Debt/Equity ex MI (X) CASH CASH CASH CASH CASH Capex to Debt (%) 34.3 49.4 53.1 53.1 53.1 Z-Score (X) 8.3 8.6 8.5 8.4 8.3

Source: Company, DBS Vickers

Page 17

ASIAN INSIGHTS VICKERS SECURITIES Page 6

Company Guide

Indofood CBP Sukses Makmur

Cash Flow Statement (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Pre-Tax Profit 3,445 4,010 4,972 5,255 5,853 Dep. & Amort. 619 699 758 796 836 Tax Paid (871) (1,087) (1,243) (1,314) (1,463) Assoc. & JV Inc/(loss) 0.70 94.1 0.0 0.0 0.0 Chg in Wkg.Cap. 298 117 80.3 (290) (342) Other Operating CF 369 (348) 0.0 0.0 0.0 Net Operating CF 3,861 3,486 4,568 4,447 4,884 Capital Exp.(net) (1,164) (1,396) (1,500) (1,500) (1,500) Other Invts.(net) 0.0 0.0 0.0 0.0 0.0 Invts in Assoc. & JV (218) (619) 0.0 0.0 0.0 Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 Other Investing CF (368) (32.6) 0.0 0.0 0.0 Net Investing CF (1,750) (2,047) (1,500) (1,500) (1,500) Div Paid (1,108) (1,295) (1,830) (1,934) (2,154) Chg in Gross Debt 686 (29.9) 0.0 0.0 0.0 Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF 135 59.5 0.0 0.0 0.0 Net Financing CF (287) (1,265) (1,830) (1,934) (2,154) Currency Adjustments 22.6 144 0.0 0.0 0.0 Chg in Cash 1,847 318 1,238 1,013 1,230 Opg CFPS (Rp) 306 289 385 406 448 Free CFPS (Rp) 231 179 263 253 290

Source: Company, DBS Vickers

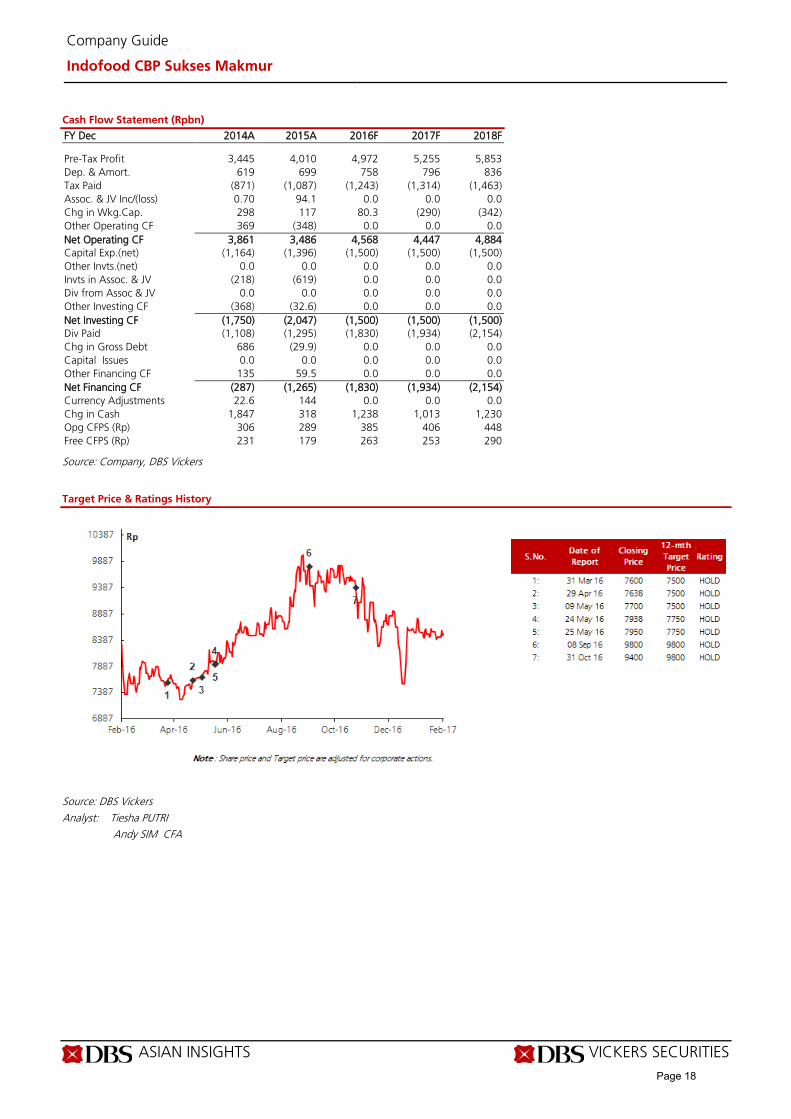

Target Price & Ratings History

Source: DBS Vickers

Analyst: Tiesha PUTRI Andy SIM CFA

Page 18

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:MA, PY

BUY Last Traded Price ( 8 Feb 2017): Rp7,950 (JCI : 5,361.10) Price Target 12-mth: Rp9,100 (14% upside) (Prev Rp9,900) Potential Catalyst: Stronger pick-up in domestic consumption and recovery in CPO price Where we differ: Broadly in line with consensus Analyst Tiesha PUTRI +6221 30034931 [email protected] Andy SIM CFA +65 6682 3718 [email protected]

What’s New • Attractive valuation; trades at 22% to its SOP

valuation • Agribusiness to support earnings growth in FY17 • Potential valuation upgrade post Minzhong

divestment

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2015A 2016F 2017F 2018F Revenue 64,062 67,329 72,389 78,861 EBITDA 10,391 10,607 11,602 13,098 Pre-tax Profit 4,962 6,874 7,646 8,840 Net Profit 2,968 3,927 4,545 4,894 Net Pft (Pre Ex.) 2,968 3,927 4,545 4,894 Net Pft Gth (Pre-ex) (%) (24.7) 32.3 15.7 7.7 EPS (Rp) 338 447 518 557 EPS Pre Ex. (Rp) 338 447 518 557 EPS Gth Pre Ex (%) (25) 32 16 8 Diluted EPS (Rp) 338 447 518 557 Net DPS (Rp) 169 224 259 279 BV Per Share (Rp) 3,106 3,329 3,588 3,867 PE (X) 23.5 17.8 15.4 14.3 PE Pre Ex. (X) 23.5 17.8 15.4 14.3 P/Cash Flow (X) 16.6 9.9 8.4 7.8 EV/EBITDA (X) 9.5 9.1 8.4 7.5 Net Div Yield (%) 2.1 2.8 3.3 3.5 P/Book Value (X) 2.6 2.4 2.2 2.1 Net Debt/Equity (X) 0.3 0.2 0.2 0.2 ROAE (%) 10.9 13.4 14.4 14.4 Earnings Rev (%): 0 0 (3) Consensus EPS (Rp): 458 502 574 Other Broker Recs: B: 26 S: 0 H: 0

Source of all data on this page: Company, DBS Vickers, Bloomberg Finance L.P

Attractively valued Maintain BUY on attractive valuation. INDF remains our top pick in the regional consumer sector. Our BUY call is premised on INDF’s attractive valuation. Based on our calculation, the company now trades at a 22% discount to its SOP valuation vs. an average discount of 16% in the past five years. INDF offers a cheaper entry to invest in ICBP, trading at 15x FY17F PE (0.7SD below 5-year mean) vs. ICBP’s 26x FY17F PE (0.7SD above 5-year mean). Minzhong divestment – a done deal. INDF’s shares have been trading at a deep discount to its SOP valuation in the past three years, which may be mainly attributable to the company’s venture into the cultivation business through the acquisition of China Minzhong Food Corporation (CMFC) in 2013. In 2016, INDF has divested a 52.94% stake in CMFC to Marvellous Glory Holdings Ltd., an SPV controlled by Anthoni Salim. The company had received the entire cash payment of SGD416m and settled part of its debt at the end of 2016. Post transaction, INDF maintains a minority ownership (29.9% stakes) in CMFC. We believe this positive development will help to narrow INDF’s current discount to SOP valuation. 2017 outlook: getting a green boost from agribusiness. We expect the recent commodity price rally to support the demand recovery momentum in 2017, which would eventually translate to stronger sales for consumer companies, including INDF. While we expect higher raw material prices would weigh down the margin of INDF’s consumer business, a more stable palm oil prices along with the recovery in FFB yield would support earnings recovery in INDF’s agribusiness segment. We expect INDF to register 32%/16% net profit growth in FY16F/17F. Valuation: We raised our SOP-based TP to Rp9,900 (implying 19x FY17F PE) to factor in higher DCF-based TP of INDF’s agribusiness. ICBP and agribusiness contributes 84% and 9% to our valuation, respectively, before a holding discount of 15%. Key Risks to Our View: Volatile commodity prices. Fluctuations in commodity prices could swing costs, and consequently, margins. At A Glance Issued Capital (m shrs) 8,780 Mkt. Cap (Rpbn/US$m) 69,804 / 5,235 Major Shareholders (%) CAB Holding (%) 51.5

Free Float (%) 48.5 3m Avg. Daily Val (US$m) 5.2 ICB Industry : Consumer Goods / Food Producers

DBS Group Research . Equity

9 Feb 2017

Indonesia Company Guide

Indofood Sukses Makmur Version 8 | Bloomberg: INDF IJ | Reuters: INDF.JK Refer to important disclosures at the end of this report

Page 19

ASIAN INSIGHTS VICKERS SECURITIES Page 2

Company Guide

Indofood Sukses Makmur

Sum-of-parts (SOP) valuation

Source: DBS Vickers, DBS Bank

INDF’s SOP valuation discount trend in the past five years

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P

INDF’s SOP valuation vs. CPO price

Source: DBS Vickers, DBS Bank, Bloomberg Finance L.P

Ent it yINDF 's ef fect iv e shareholding

EVadj, to INDF 's

ownership(Rp bn)

A dj. EV per share

(Rp)Remark s

ICBP 80.5% 78,787 8,973 DBS target price; pegged to 26x FY17F EPS or +1SD above historical mean (lowered from 29x

FY17F EPS or +2SD above historical mean initially )

Bogasari 100.0% 12,814 1,459 6x FY17F EV/EBITDA

Indofood Agri Resources 62.8% 9,801 1,116 DBS target price; DCF-based

Distribution 100.0% 2,280 260 6x FY17F EV/EBITDA

China Minzhong 29.9% 499 57 Offer price for majority stake

Net debt/ cash (9,684) (1,103)

Holding company di ( )

(14,175) (1,614)

Target price 80,324 9,100 Implied PE 17F 17.6

-22%

-16%

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Premium (discount) to RNAV Avg. Premium (discount) to RNAV

INDF divested 52.94% stakes

in CMFC

INDF acquired 29.33% stakes

in CMFC

INDF owned 82.88% stakes

in CMFC

1,500

2,000

2,500

3,000

3,500

4,000

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Premium (discount) to RNAV CPO price (RHS)

Page 20

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Company Guide

Indofood Sukses Makmur

CRITICAL DATA POINTS TO WATCH Earnings Drivers: Consumer Branded Products (CBP) segment is the primary earnings driver. In 2015, Indofood’s CBP segment contributed more than 50% of INDF’s EBIT. Agribusiness and Bogasari contributed 20% and 18% respectively. Growth in the CBP segment is predominantly driven by the noodle business which generated c.90% of ICBP’s earnings in FY15. Also, noodles are considered a cheap substitute to rice for many Indonesians, which is why noodle sales are relatively resilient even in a slow economy. Wheat price and rupiah strength. Bogasari produces wheat flour, of which 30% is used by ICBP, 65% is sold to SMEs, and the rest to retail consumers. Bogasari imports its entire wheat requirements, which means it is susceptible to fluctuations in global wheat prices and the strength of the rupiah. It adjusts average selling price according to its costs, which eventually affects ICBP’s margins. The sharp depreciation of the rupiah in 2013-14 had reduced EBIT margins at the CBP segment by about 300bps to 10.2% in 2014 from 13.1% in 2012. CPO price and output. The Agribusiness segment, under 62.8%-owned subsidiary Indofood Agri Resources (IFAR SP), is involved in both upstream and downstream operations. Our plantation analyst expects a flattish CPO price in FY17F, but sales volume recovery should help to boost Agribusiness’ performance next year with EBIT projected to grow 19% y-o-y in FY17F after staying flat y-o-y in FY16F. The Agribusiness segment contributed 20% and 15% of Indofood’s FY15 and 9M16 EBIT respectively. Recovery in the domestic economy. We are expecting a gradual recovery in consumption going into 2017. This, coupled with favourable soft commodity prices and stabilising rupiah, should support INDF’s earnings growth, particularly for its CBP and Bogasari segments. As for the latter, around 65% of Bogasari’s wheat flour is sold to SMEs. Improving domestic consumer demand would eventually lead to more business expansion by SMEs and higher demand for wheat flour. Competition in FMCG industry. Indonesia’s rising consumerism has attracted a number of new local and foreign players to the Fast Moving Consumer Goods (FMCG) industry. Rising competition would dent INDF’s pricing power and top-line growth for its consumer goods products. In the event of rising input costs, weak competitive position would result in INDF not being able to pass through the rising costs, hence a drag on earnings.

Revenue Trend and Forecasts

Net Profit Trend and Forecasts

Margin Trend and Forecasts

CBOT Wheat Price

CPO Price

Source: Company, DBS Vickers

-

2%

4%

6%

8%

10%

12%

14%

16%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2013A 2014A 2015A 2016F 2017F

Revenue (Rp bn) Growth y-o-y (RHS)

(30%)

(20%)

(10%)

-

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2013A 2014A 2015A 2016F 2017F

Net profit (Rp bn) Growth y-o-y (RHS)

-

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2013A 2014A 2015A 2016F 2017F

EBIT margin Net margin

300

350

400

450

500

550

600

650

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

Wheat (cents/bu.) Quarterly avg. price

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

3,100

3,300

3,500

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

CPO price (MYR/MT) Quarterly avg. price

Page 21

ASIAN INSIGHTS VICKERS SECURITIES Page 4

Company Guide

Indofood Sukses Makmur

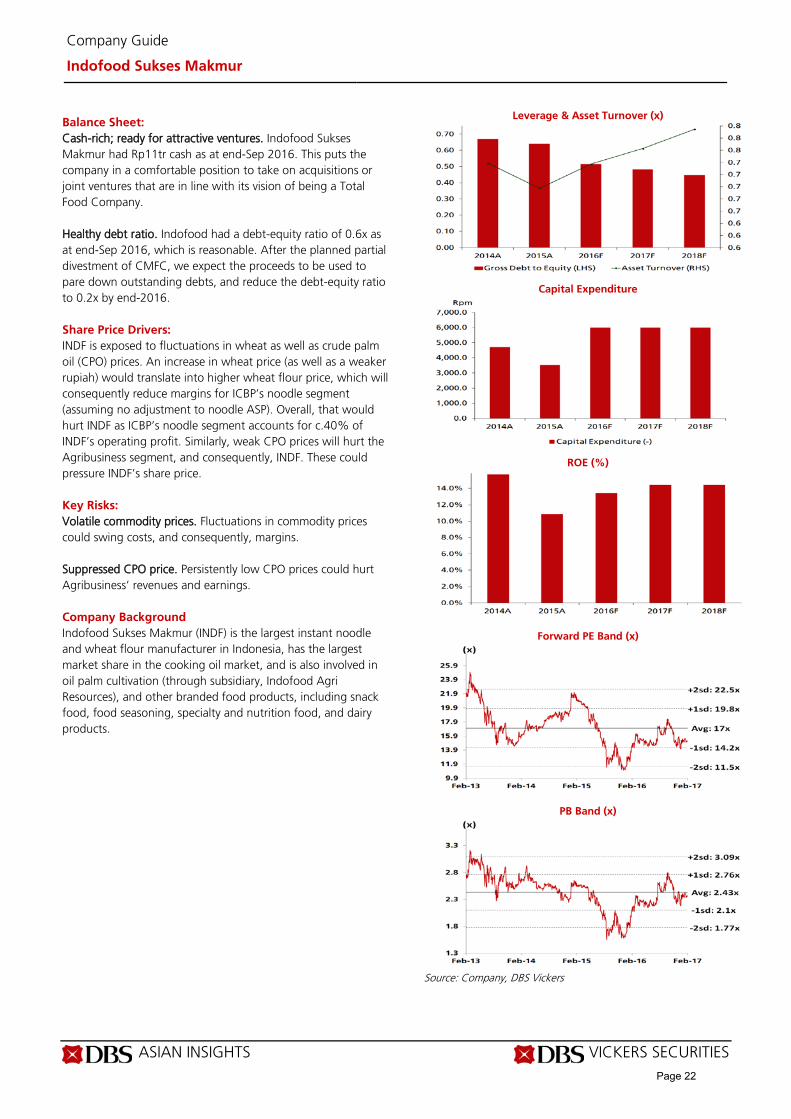

Balance Sheet: Cash-rich; ready for attractive ventures. Indofood Sukses Makmur had Rp11tr cash as at end-Sep 2016. This puts the company in a comfortable position to take on acquisitions or joint ventures that are in line with its vision of being a Total Food Company. Healthy debt ratio. Indofood had a debt-equity ratio of 0.6x as at end-Sep 2016, which is reasonable. After the planned partial divestment of CMFC, we expect the proceeds to be used to pare down outstanding debts, and reduce the debt-equity ratio to 0.2x by end-2016. Share Price Drivers: INDF is exposed to fluctuations in wheat as well as crude palm oil (CPO) prices. An increase in wheat price (as well as a weaker rupiah) would translate into higher wheat flour price, which will consequently reduce margins for ICBP’s noodle segment (assuming no adjustment to noodle ASP). Overall, that would hurt INDF as ICBP’s noodle segment accounts for c.40% of INDF’s operating profit. Similarly, weak CPO prices will hurt the Agribusiness segment, and consequently, INDF. These could pressure INDF’s share price. Key Risks: Volatile commodity prices. Fluctuations in commodity prices could swing costs, and consequently, margins. Suppressed CPO price. Persistently low CPO prices could hurt Agribusiness’ revenues and earnings. Company Background Indofood Sukses Makmur (INDF) is the largest instant noodle and wheat flour manufacturer in Indonesia, has the largest market share in the cooking oil market, and is also involved in oil palm cultivation (through subsidiary, Indofood Agri Resources), and other branded food products, including snack food, food seasoning, specialty and nutrition food, and dairy products.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Vickers

Page 22

ASIAN INSIGHTS VICKERS SECURITIES Page 5

Company Guide

Indofood Sukses Makmur

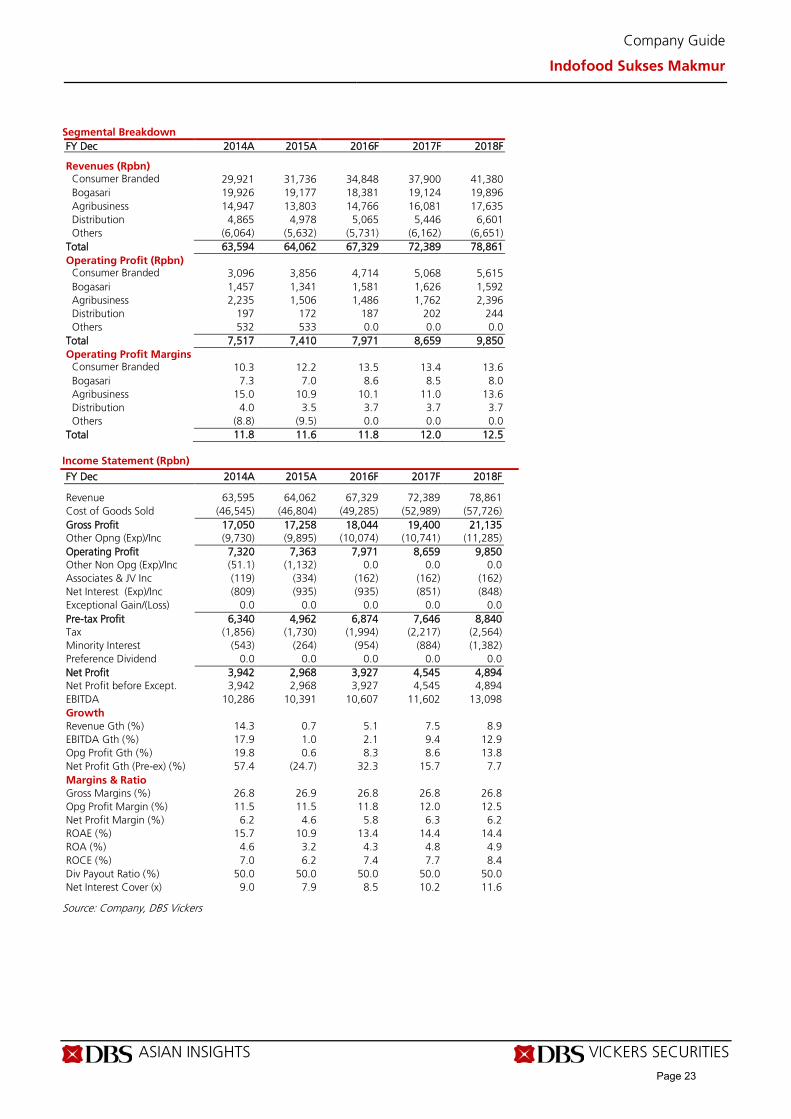

Segmental Breakdown FY Dec 2014A 2015A 2016F 2017F 2018F Revenues (Rpbn) Consumer Branded

29,921 31,736 34,848 37,900 41,380

Bogasari 19,926 19,177 18,381 19,124 19,896 Agribusiness 14,947 13,803 14,766 16,081 17,635 Distribution 4,865 4,978 5,065 5,446 6,601 Others (6,064) (5,632) (5,731) (6,162) (6,651) Total 63,594 64,062 67,329 72,389 78,861 Operating Profit (Rpbn) Consumer Branded

3,096 3,856 4,714 5,068 5,615

Bogasari 1,457 1,341 1,581 1,626 1,592 Agribusiness 2,235 1,506 1,486 1,762 2,396 Distribution 197 172 187 202 244 Others 532 533 0.0 0.0 0.0 Total 7,517 7,410 7,971 8,659 9,850 Operating Profit Margins

Consumer Branded

10.3 12.2 13.5 13.4 13.6 Bogasari 7.3 7.0 8.6 8.5 8.0 Agribusiness 15.0 10.9 10.1 11.0 13.6 Distribution 4.0 3.5 3.7 3.7 3.7 Others (8.8) (9.5) 0.0 0.0 0.0 Total 11.8 11.6 11.8 12.0 12.5

Income Statement (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Revenue 63,595 64,062 67,329 72,389 78,861 Cost of Goods Sold (46,545) (46,804) (49,285) (52,989) (57,726) Gross Profit 17,050 17,258 18,044 19,400 21,135 Other Opng (Exp)/Inc (9,730) (9,895) (10,074) (10,741) (11,285) Operating Profit 7,320 7,363 7,971 8,659 9,850 Other Non Opg (Exp)/Inc (51.1) (1,132) 0.0 0.0 0.0 Associates & JV Inc (119) (334) (162) (162) (162) Net Interest (Exp)/Inc (809) (935) (935) (851) (848) Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 6,340 4,962 6,874 7,646 8,840 Tax (1,856) (1,730) (1,994) (2,217) (2,564) Minority Interest (543) (264) (954) (884) (1,382) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 3,942 2,968 3,927 4,545 4,894 Net Profit before Except. 3,942 2,968 3,927 4,545 4,894 EBITDA 10,286 10,391 10,607 11,602 13,098 Growth Revenue Gth (%) 14.3 0.7 5.1 7.5 8.9 EBITDA Gth (%) 17.9 1.0 2.1 9.4 12.9 Opg Profit Gth (%) 19.8 0.6 8.3 8.6 13.8 Net Profit Gth (Pre-ex) (%) 57.4 (24.7) 32.3 15.7 7.7 Margins & Ratio Gross Margins (%) 26.8 26.9 26.8 26.8 26.8 Opg Profit Margin (%) 11.5 11.5 11.8 12.0 12.5 Net Profit Margin (%) 6.2 4.6 5.8 6.3 6.2 ROAE (%) 15.7 10.9 13.4 14.4 14.4 ROA (%) 4.6 3.2 4.3 4.8 4.9 ROCE (%) 7.0 6.2 7.4 7.7 8.4 Div Payout Ratio (%) 50.0 50.0 50.0 50.0 50.0 Net Interest Cover (x) 9.0 7.9 8.5 10.2 11.6

Source: Company, DBS Vickers

Page 23

ASIAN INSIGHTS VICKERS SECURITIES Page 6

Company Guide

Indofood Sukses Makmur

Quarterly / Interim Income Statement (Rpbn)

FY Dec 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 Revenue 14,929 16,498 16,516 17,568 15,782 Cost of Goods Sold (11,015) (12,107) (11,902) (12,383) (11,020) Gross Profit 3,915 4,391 4,614 5,186 4,762 Other Oper. (Exp)/Inc (2,341) (2,453) (2,735) (3,051) (2,844) Operating Profit 1,574 1,938 1,879 2,135 1,918 Other Non Opg (Exp)/Inc (1,125) 710 0.0 0.0 0.0 Associates & JV Inc (109) (50.6) (78.4) (116) 7.40 Net Interest (Exp)/Inc (286) (258) (69.8) (161) (56.8) Exceptional Gain/(Loss) 29.9 55.7 101 82.6 86.2 Pre-tax Profit 83.6 2,395 1,832 1,941 1,955 Tax (97.0) (793) (468) (547) (613) Minority Interest (34.0) (318) (278) (249) (333) Net Profit (47.3) 1,284 1,086 1,146 1,009 Net profit bef Except. (77.2) 1,229 985 1,063 923 EBITDA 2,227 2,539 2,487 3,391 3,917 Growth Revenue Gth (%) (15.2) 10.5 0.1 6.4 (10.2) EBITDA Gth (%) (16.6) 14.0 (2.0) 36.3 15.5 Opg Profit Gth (%) (25.1) 23.1 (3.1) 13.6 (10.2) Net Profit Gth (Pre-ex) (%) nm nm (19.9) 7.9 (13.2) Margins Gross Margins (%) 26.2 26.6 27.9 29.5 30.2 Opg Profit Margins (%) 10.5 11.7 11.4 12.2 12.2 Net Profit Margins (%) (0.3) 7.8 6.6 6.5 6.4

Balance Sheet (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Net Fixed Assets 30,575 34,184 33,644 36,701 39,452 Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0 Other LT Assets 14,488 14,831 14,669 14,507 14,345 Cash & ST Invts 14,823 14,167 13,272 13,351 13,843 Inventory 8,446 7,627 8,463 9,099 9,912 Debtors 4,358 5,117 5,350 5,318 5,794 Other Current Assets 13,386 15,906 15,906 15,906 15,906 Total Assets 86,077 91,832 91,303 94,882 99,253 ST Debt

10,096 10,712 10,712 10,712 10,712 Creditor 5,093 5,174 5,632 6,055 6,597 Other Current Liab 7,470 9,222 9,222 9,222 9,222 LT Debt 16,838 16,894 12,990 12,990 12,990 Other LT Liabilities 6,306 6,708 6,708 6,708 6,708 Shareholder’s Equity 25,104 27,269 29,233 31,506 33,953 Minority Interests 15,170 15,852 16,806 17,689 19,072 Total Cap. & Liab. 86,077 91,832 91,303 94,882 99,253 Non-Cash Wkg. Capital 13,628 14,254 14,865 15,046 15,794 Net Cash/(Debt) (12,110) (13,439) (10,430) (10,351) (9,859) Debtors Turn (avg days) 25.0 29.2 29.0 26.8 26.8 Creditors Turn (avg days) 42.7 43.1 44.1 44.2 44.2 Inventory Turn (avg days) 70.7 63.6 66.2 66.4 66.4 Asset Turnover (x) 0.7 0.7 0.7 0.8 0.8 Current Ratio (x) 1.8 1.7 1.7 1.7 1.7 Quick Ratio (x) 0.8 0.8 0.7 0.7 0.7 Net Debt/Equity (X) 0.3 0.3 0.2 0.2 0.2 Net Debt/Equity ex MI (X) 0.5 0.5 0.4 0.3 0.3 Capex to Debt (%) 17.5 12.8 25.3 25.3 25.3 Z-Score (X) 2.5 2.4 2.6 2.6 2.7

Source: Company, DBS Vickers

Page 24

ASIAN INSIGHTS VICKERS SECURITIES Page 7

Company Guide

Indofood Sukses Makmur

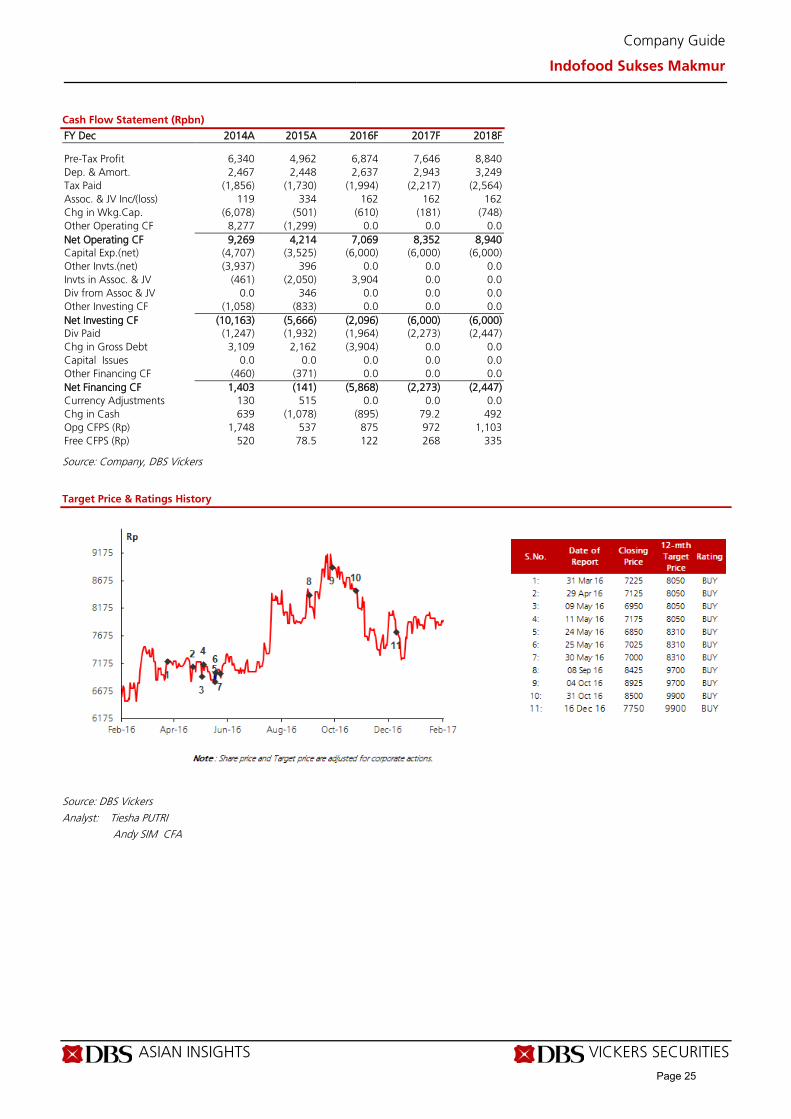

Cash Flow Statement (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Pre-Tax Profit 6,340 4,962 6,874 7,646 8,840 Dep. & Amort. 2,467 2,448 2,637 2,943 3,249 Tax Paid (1,856) (1,730) (1,994) (2,217) (2,564) Assoc. & JV Inc/(loss) 119 334 162 162 162 Chg in Wkg.Cap. (6,078) (501) (610) (181) (748) Other Operating CF 8,277 (1,299) 0.0 0.0 0.0 Net Operating CF 9,269 4,214 7,069 8,352 8,940 Capital Exp.(net) (4,707) (3,525) (6,000) (6,000) (6,000) Other Invts.(net) (3,937) 396 0.0 0.0 0.0 Invts in Assoc. & JV (461) (2,050) 3,904 0.0 0.0 Div from Assoc & JV 0.0 346 0.0 0.0 0.0 Other Investing CF (1,058) (833) 0.0 0.0 0.0 Net Investing CF (10,163) (5,666) (2,096) (6,000) (6,000) Div Paid (1,247) (1,932) (1,964) (2,273) (2,447) Chg in Gross Debt 3,109 2,162 (3,904) 0.0 0.0 Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF (460) (371) 0.0 0.0 0.0 Net Financing CF 1,403 (141) (5,868) (2,273) (2,447) Currency Adjustments 130 515 0.0 0.0 0.0 Chg in Cash 639 (1,078) (895) 79.2 492 Opg CFPS (Rp) 1,748 537 875 972 1,103 Free CFPS (Rp) 520 78.5 122 268 335

Source: Company, DBS Vickers

Target Price & Ratings History

Source: DBS Vickers

Analyst: Tiesha PUTRI Andy SIM CFA

Page 25

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:MA, PY

HOLD Last Traded Price ( 8 Feb 2017): Rp15,325 (JCI : 5,361.10) Price Target 12-mth: Rp16,200 (6% upside) (Prev Rp20,300) Potential Catalyst: Strong pick-up in same-store sales growth Where we differ: Generally in line with consensus Analyst Tiesha PUTRI +6221 30034931 [email protected] Andy SIM CFA +65 6682 3718 [email protected]

What’s New • Lowering SSSG and earnings forecasts; maintain

HOLD with a lower TP of Rp16,200 • Share price has de-rated sharply; our DDM

valuation analysis suggests that it is fairly valued • Lack of catalysts, with discretionary spending yet

to show signs of bottoming

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2015A 2016F 2017F 2018F Revenue 9,007 9,949 11,033 12,304 EBITDA 2,564 2,906 3,286 3,682 Pre-tax Profit 2,245 2,641 2,971 3,317 Net Profit 1,781 2,095 2,357 2,631 Net Pft (Pre Ex.) 1,781 2,095 2,357 2,631 Net Pft Gth (Pre-ex) (%) 25.5 17.6 12.5 11.6 EPS (Rp) 610 718 808 902 EPS Pre Ex. (Rp) 610 718 808 902 EPS Gth Pre Ex (%) 25 18 13 12 Diluted EPS (Rp) 610 718 808 902 Net DPS (Rp) 427 503 565 631 BV Per Share (Rp) 379 670 975 1,311 PE (X) 25.1 21.3 19.0 17.0 PE Pre Ex. (X) 25.1 21.3 19.0 17.0 P/Cash Flow (X) 20.6 18.7 16.2 14.4 EV/EBITDA (X) 17.1 14.9 13.1 11.4 Net Div Yield (%) 2.8 3.3 3.7 4.1 P/Book Value (X) 40.4 22.9 15.7 11.7 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 161.0 107.2 82.9 68.8 Earnings Rev (%): (2) (3) (6) Consensus EPS (Rp): 735 844 941 Other Broker Recs: B: 27 S: 2 H: 3

Source of all data on this page: Company, DBS Vickers, Bloomberg Finance L.P

No ray of hope yet Cut TP to Rp16,200; HOLD call unchanged. LPPF’s share price has de-rated sharply to near its record low PE since 2013 due to the concerns of slower SSSG and rising capex after the company announced its plan to increase stakes in MatahariMall.com. It now trades at 19x FY17F PE, -2.5SD below its historical mean PE of 25x. Nevertheless, we see limited catalysts for the share price, with household discretionary spending yet to show signs of bottoming. Recovering SSSG to double-digit level would be a challenging task. Excluding the impact of Lebaran seasonality shift in 1H16, cumulative SSSG has consistently hovered at single-digit levels over the past one year. Management reiterated that the decline in SSSG has nothing to do with competition, while the deterioration in 3Q16 was caused by the inventory assortment issue that management failed to address surrounding the Lebaran peak season. It is confident that this assortment issue has been addressed. However, we have yet to see a strong recovery in discretionary spending. We expect LPPF’s SSSG to only improve slightly to 7.1% in FY17F from 6.1% in FY16F. E-commerce foray – a long game. Following recent equity raising for MatahariMall.com led by Mitsui & Co, LPPF is going to inject Rp590bn cash into MatahariMall.com to avoid ownership dilution. E-commerce in Indonesia only represents c.2% of total retail sales but has grown at a spectacular pace. The intensifying competition has caused customer acquisition costs to remain elevated, hence funding is crucial to stay in the game. A question remains on what step LPPF is going to take if MatahariMall.com requires further equity injection in the future to remain in the game. While management has announced the plan to maintain its stakes in MatahariMall.com below 20%, the risk of LPPF having to inject more cash to avoid or limit ownership dilution still prevails should MatahariMall.com carry out further capital raising in the future. Valuation: We value LPPF at Rp16,200, based on 20x PE 17F (-2SD below its mean PE since 2013), on par with regional retailers. Key Risks to Our View: Slower-than-expected economic growth. LPPF’s target segment makes up c.60% of the country’s population. A further slowdown in the economy would impact this segment’s revenue growth, which would hurt its earnings. At A Glance Issued Capital (m shrs) 2,918 Mkt. Cap (Rpbn/US$m) 44,717 / 3,353 Major Shareholders (%) Multipolar 20.5 Asia Color 2.0

Free Float (%) 79.5 3m Avg. Daily Val (US$m) 7.7 ICB Industry : Consumer Services / General Retailers

DBS Group Research . Equity

9 Feb 2017

Indonesia Company Guide

Matahari Department Store Version 5 | Bloomberg: LPPF IJ | Reuters: LPPF.JK Refer to important disclosures at the end of this report

Page 26

ASIAN INSIGHTS VICKERS SECURITIES Page 2

Company Guide

Matahari Department Store

WHAT’S NEW

Fairly valued; lack of substantial positive catalysts ahead SSSG had consistently hovered at single-digit levels, reflecting the economic cycle. Following weaker-than-expected SSSG in 3Q16, management has lowered its SSSG guidance for FY16 to 5%-6.5% vs. its initial guidance of 7%-7.5%. Management claimed that the reason behind the weak 3Q16 sales was the misstep in inventory assortment surrounding the Lebaran peak season, particularly for women’s apparels, rather than competition from online or specialty retailers. On top of that, discretionary spending had remained muted in 3Q16, which we believe also contributed to the decline in SSSG.

The subsequent chart shows that LPPF’s SSSG has broadly moved in line with nominal household consumption growth. We expect the demand recovery momentum to continue in 2017 but only at a gradual pace. While demand for necessities had generally improved in 3Q16, discretionary household spending growth has yet to show signs of bottoming as it further eased to 4.3% y-o-y in 4Q16, still lagging behind non-discretionary household spending. We do not see a strong reason to expect a surge in nominal household consumption growth in the near future, which in the past year hovered between 7% and 8%. For this reason, restoring SSSG to double-digit levels would be a challenging task for LPPF, in our view. We now project LPPF’s same-store sales to grow by 6.1% in 2016F and 7.1% in 2017F (from 7.6%/8.4% for FY16F/FY17F initially). We therefore lower our net profit forecasts by 2%/3% for FY16F/FY17F. We expect LPPF net profit to grow by 18% in FY16F and 13% in FY17F.

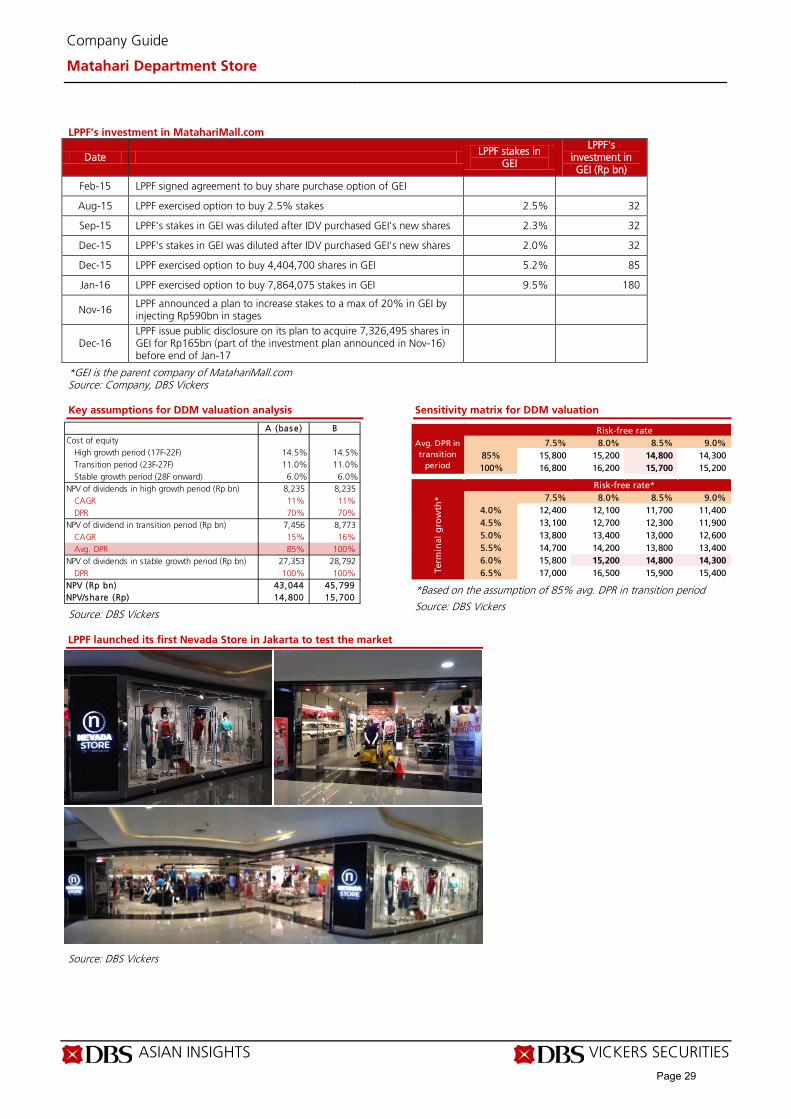

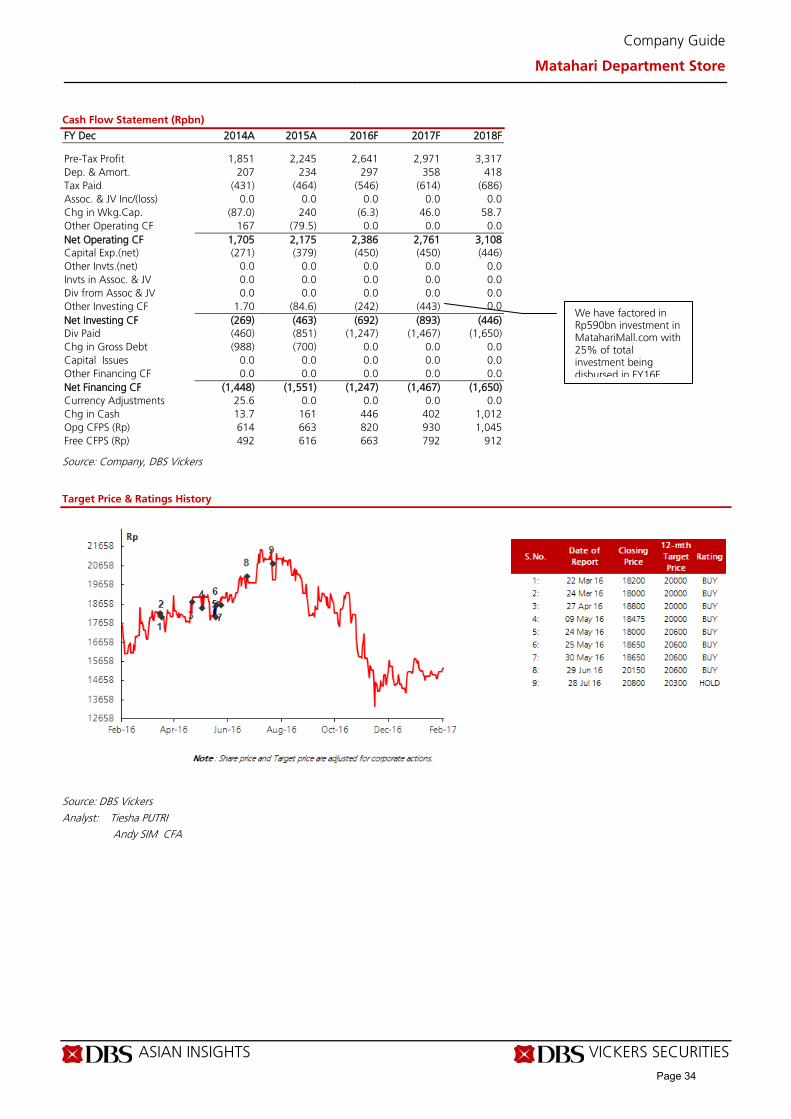

A change in strategy? LPPF has committed Rp590bn cash to be injected in stages into Lippo Group’s e-commerce arm MatahariMall.com from the end of 2016 to 3Q17. The additional investment is made to avoid LPPF’s ownership dilution in MatahariMall.com, which recently raised equity of USD100m – led by Japan’s Mitsui & Co. Prior to this, LPPF owned a minority stake of 9.47% in MatahariMall.com.

There appears to be a change in management’s strategy with regard to LPPF’s investment in MatahariMall.com as it previously guided for no further investment in MatahariMall.com. Looking ahead, the company aims to maintain its stake in MatahariMall.com below 20%.

In a statement release to the public, management stated that it had not planned to participate in any further funding initiatives by MatahariMall.com, but the question remains on how far LPPF would let its stake in MatahariMall.com being diluted should MatahariMall.com require further equity raising after 3Q17. Not letting its stakes being diluted would mean that LPPF has to top up its investment in

MatahariMall.com, possibly at a higher price. We note that in 7M16, MatahariMall.com booked a significant loss of Rp490bn.

PE multiple has de-rated sharply to 2.5SD below historical mean. LPPF now trades at 19x PE 17F, -2.5SD below its historical mean since April 2013. The sharp de-rating in the past month has brought down LPPF’s PE multiple to a level that is on par with regional peers despite having the highest ROE. We believe most of the negatives, including the increase of investment in MatahariMall.com, are already reflected in the share price.

The company generates more than enough operating cash flow to cover its capex annually and even if we are to assume an increase in inventory days by 10 days in 2017 and 2018 due to a persistently weak demand environment or management’s push toward direct purchase sales, our calculation shows that LPPF can still generate Rp2.4tr/Rp2.6tr operating cash flow in 2017F/2018F. If the company maintains a dividend payout ratio of 70% in the same period and double its capex budget to Rp1tr per year, it can still fund the expansion using internal cash.

Our DDM valuation analysis suggests limited downside to current share price. We ran a three-stage DDM valuation analysis to estimate the level of reduction in potential future dividends that the current share price has priced in. Currently, LPPF maintains a dividend payout ratio of 70% despite its ability to raise it to 100%. Our DDM model assumes LPPF will grow its dividend at 13% CAGR over the next 10 years on the back of: 1) 11% net profit and dividend CAGR in the first five years, 2) 7% net profit CAGR in the subsequent five years and a linear increase in dividend payout ratio (DPR) from 70% in year-5 to 100% in year-10, and 3) stable growth rate of 6% from year-11 onwards. We assume SSSG of 6%-7% in our model

Based on our calculation, LPPF’s current share price range of Rp14,800-Rp15,700 implies a scenario of 32%-37% of annual operating cash flow or roughly Rp1.2tr-Rp1.5tr being retained to fund capex or working capital needs over the next 10 years. As a comparison, LPPF only allocates Rp450bn capex budget for FY16 (excluding investment in MatahariMall.com). This affirms our view that the current valuation has largely priced in a slowing SSSG and more importantly the risk of significant rise in capex or investment as the company works to achieve its goal to become an omnichannel retailer. Our key assumptions and sensitivity analysis on the DDM valuation are presented on the subsequent page.

Page 27

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Company Guide

Matahari Department Store

We see limited positive catalysts, especially since the demand environment (particularly for discretionary spending) has yet to show signs of an encouraging pick-up. What can surprise on the upside would be if LPPF manages to improve its profitability, be it from further opex efficiency or improvement in sales mix (toward more direct purchase), and if there is further increase in its dividend payout ratio from the current level of 70%.

The company has continued to roll out initiatives to increase profitability, among which is to improve its sales mix. The company recently opens its first specialty store in Jakarta, called Nevada Store, to test the market. Nevada Store sells LPPF’s private label apparels and shoes i.e. Nevada, Connexion, Details, and Cole, which command higher margins compared to consigned merchandise. In 9M16, the higher-margin direct purchase (DP) accounted for 36.7% of LPPF’s gross sales (vs. 35.3% in 9M15). There is also room to improve its sales mix if LPPF can increase sales of women’s apparels, which command higher margins and currently only contribute 8%-9% of total sales.