Embed Size (px)

Citation preview

ed-CK / sa- MA, PY

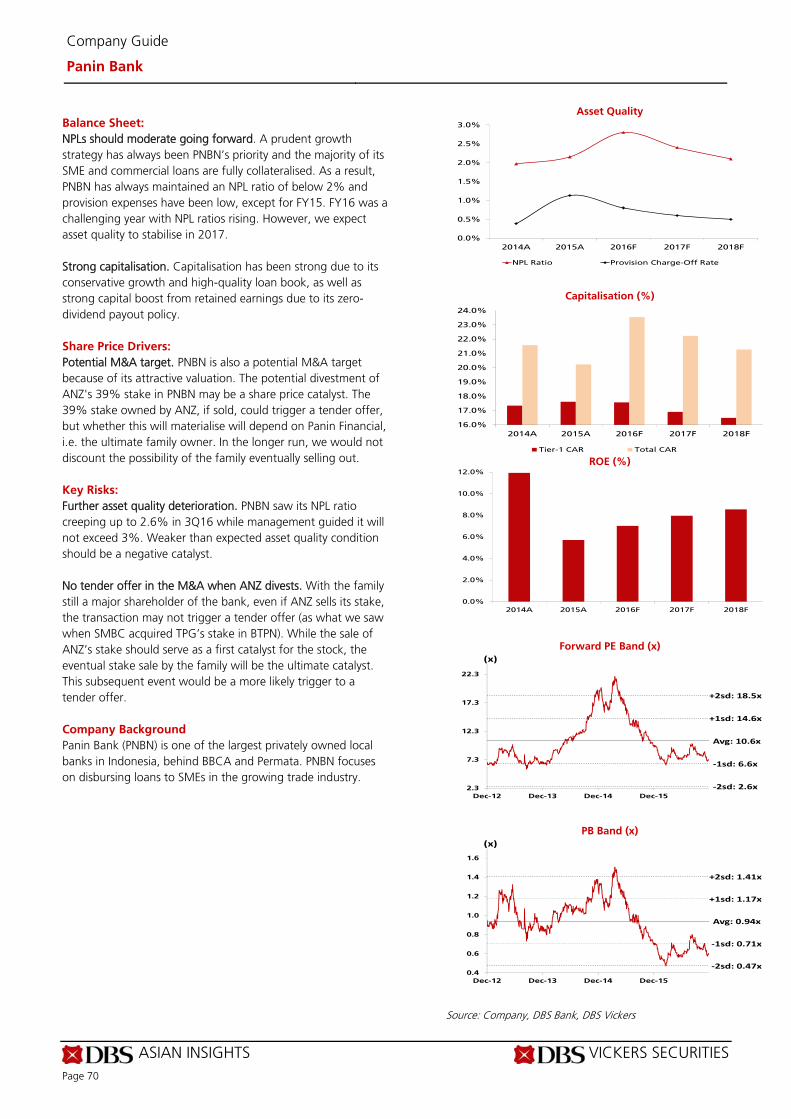

Eyeing a sustainable recovery

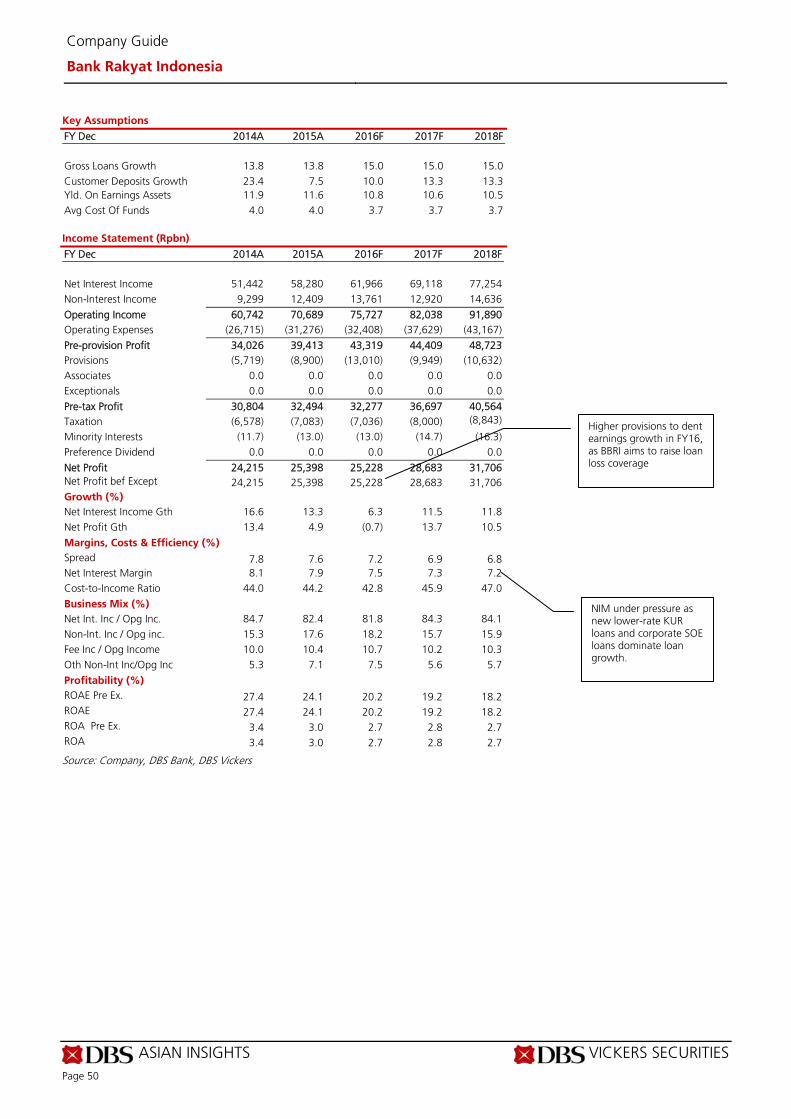

Earnings to recover but largely on lower provisions

NPL recovery and loan growth are critical factors

Clearer signals are needed for a sustainable re-rating

BBCA and BDMN remain our top picks

Hopeful but still cautious. Earnings growth is expected to recover in 2017, mainly from lower credit costs as provisions were largely accelerated in 2016. Higher provisions were set aside for existing NPL issues as well as potential ones; banks also took the opportunity where possible to build provision reserves, in anticipation of further deterioration. Loan loss reserve coverage ratios declined as NPLs mounted. However, we opine that NPL issues are not over yet and may drag till 2Q17 unless GDP growth picks up strongly. We however caution that regulatory pressures may resume to push lending rates lower, exerting stress on NIM. The possible removal of the deposit rate cap may spark another deposit war in the current tighter liquidity condition, posing risks to NIM trends. Waiting for signals: NPL recovery and loan growth are critical

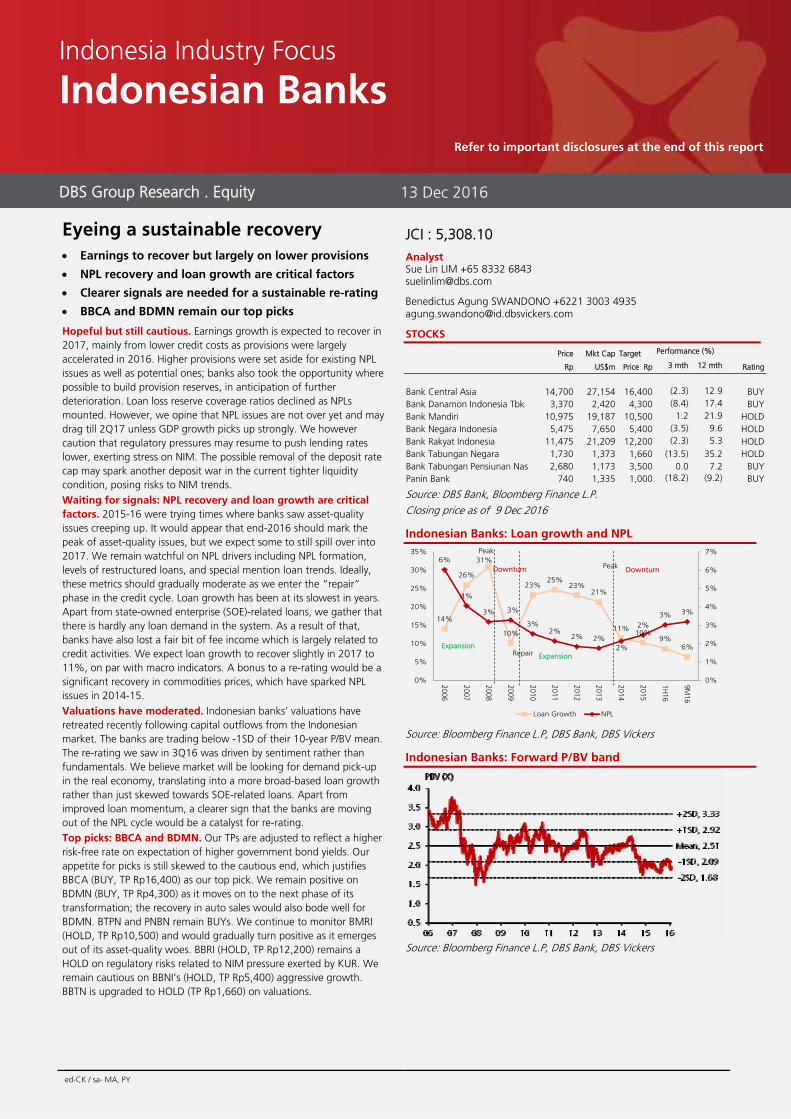

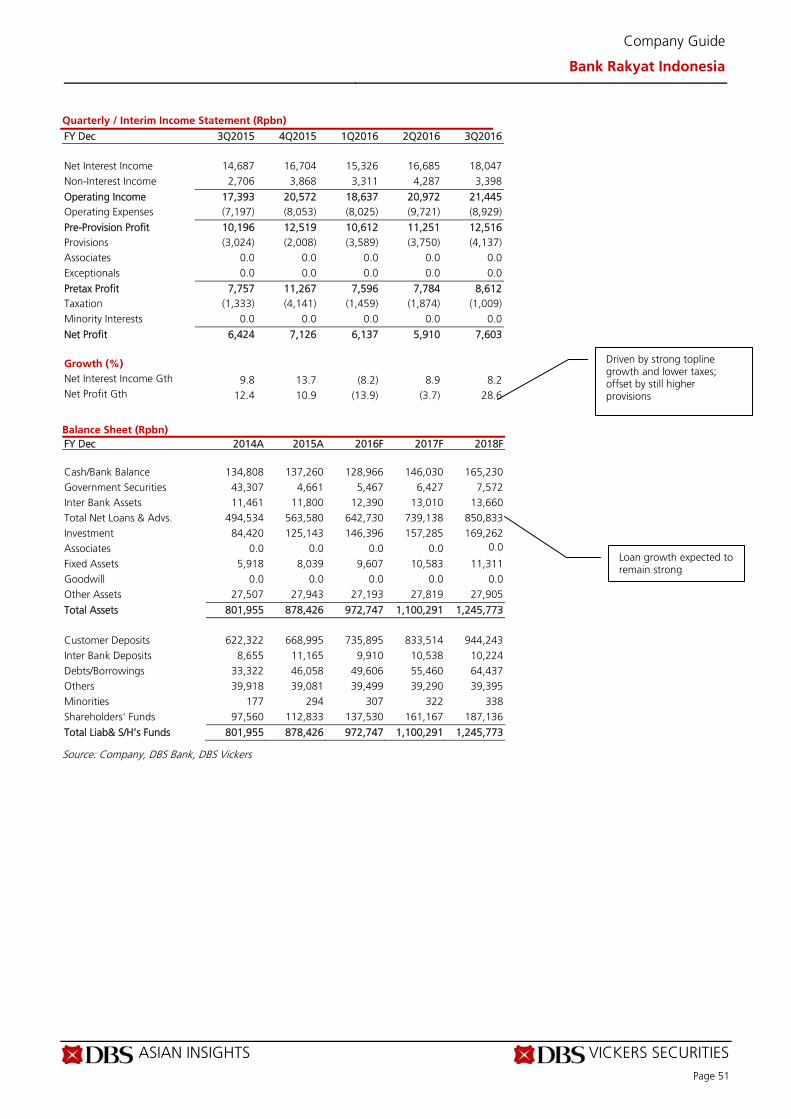

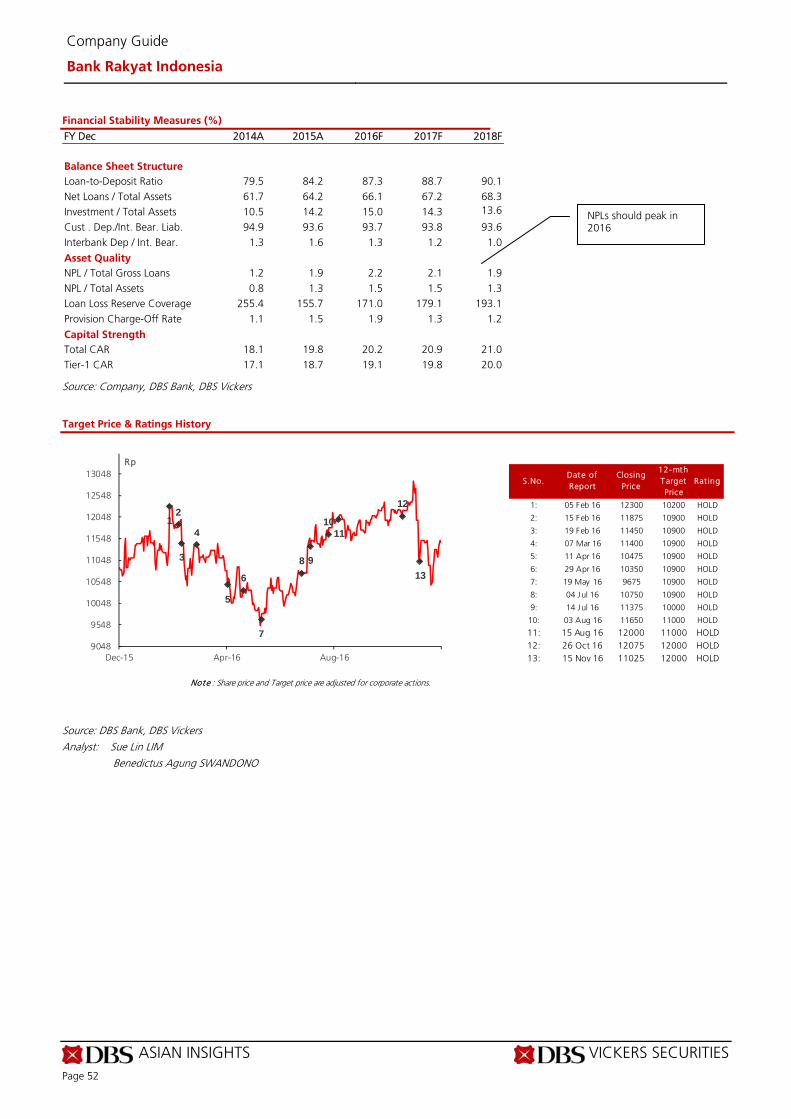

factors. 2015-16 were trying times where banks saw asset-quality issues creeping up. It would appear that end-2016 should mark the peak of asset-quality issues, but we expect some to still spill over into 2017. We remain watchful on NPL drivers including NPL formation, levels of restructured loans, and special mention loan trends. Ideally, these metrics should gradually moderate as we enter the “repair” phase in the credit cycle. Loan growth has been at its slowest in years. Apart from state-owned enterprise (SOE)-related loans, we gather that there is hardly any loan demand in the system. As a result of that, banks have also lost a fair bit of fee income which is largely related to credit activities. We expect loan growth to recover slightly in 2017 to 11%, on par with macro indicators. A bonus to a re-rating would be a significant recovery in commodities prices, which have sparked NPL issues in 2014-15. Valuations have moderated. Indonesian banks’ valuations have retreated recently following capital outflows from the Indonesian market. The banks are trading below -1SD of their 10-year P/BV mean. The re-rating we saw in 3Q16 was driven by sentiment rather than fundamentals. We believe market will be looking for demand pick-up in the real economy, translating into a more broad-based loan growth rather than just skewed towards SOE-related loans. Apart from improved loan momentum, a clearer sign that the banks are moving out of the NPL cycle would be a catalyst for re-rating. Top picks: BBCA and BDMN. Our TPs are adjusted to reflect a higher risk-free rate on expectation of higher government bond yields. Our appetite for picks is still skewed to the cautious end, which justifies BBCA (BUY, TP Rp16,400) as our top pick. We remain positive on BDMN (BUY, TP Rp4,300) as it moves on to the next phase of its transformation; the recovery in auto sales would also bode well for BDMN. BTPN and PNBN remain BUYs. We continue to monitor BMRI (HOLD, TP Rp10,500) and would gradually turn positive as it emerges out of its asset-quality woes. BBRI (HOLD, TP Rp12,200) remains a HOLD on regulatory risks related to NIM pressure exerted by KUR. We remain cautious on BBNI’s (HOLD, TP Rp5,400) aggressive growth. BBTN is upgraded to HOLD (TP Rp1,660) on valuations.

JCI : 5,308.10

Analyst Sue Lin LIM +65 8332 6843 [email protected]

Benedictus Agung SWANDONO +6221 3003 4935

STOCKS

Source: DBS Bank, Bloomberg Finance L.P. Closing price as of 9 Dec 2016

Indonesian Banks: Loan growth and NPL

Source: Bloomberg Finance L.P, DBS Bank, DBS Vickers

Indonesian Banks: Forward P/BV band

Source: Bloomberg Finance L.P, DBS Bank, DBS Vickers

14%

26%

31%

10%

23%25%

23%21%

11%10%

9%6%

6%

4%

3% 3%

3%2%

2% 2%2%

2%3% 3%

0%

1%

2%

3%

4%

5%

6%

7%

0%

5%

10%

15%

20%

25%

30%

35%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

1H16

9M16

Loan Growth NPL

RepairExpansion

Expansion

Downturn DownturnPeak

Peak

DBS Group Research . Equity 13 Dec 2016

Indonesia Industry Focus

Indonesian Banks

Refer to important disclosures at the end of this report

Price Mkt Cap Target Performance (%)

Rp US$m Price Rp 3 mth 12 mth Rating

Bank Central Asia 14,700 27,154 16,400 (2.3) 12.9 BUY Bank Danamon Indonesia Tbk 3,370 2,420 4,300 (8.4) 17.4 BUY Bank Mandiri 10,975 19,187 10,500 1.2 21.9 HOLD Bank Negara Indonesia 5,475 7,650 5,400 (3.5) 9.6 HOLD Bank Rakyat Indonesia 11,475 21,209 12,200 (2.3) 5.3 HOLD Bank Tabungan Negara 1,730 1,373 1,660 (13.5) 35.2 HOLD Bank Tabungan Pensiunan Nas 2,680 1,173 3,500 0.0 7.2 BUY Panin Bank 740 1,335 1,000 (18.2) (9.2) BUY

Industry Focus

Page 2

Table of Contents Key trends to watch for 2017 3

Turning a little more positive 4

Clearer signals are needed for a sustainable re-rating 8

Valuation and recommendation 11

Appendix – Key charts 13

Company Guides 16

Bank Central Asia 17

Bank Danamon 24

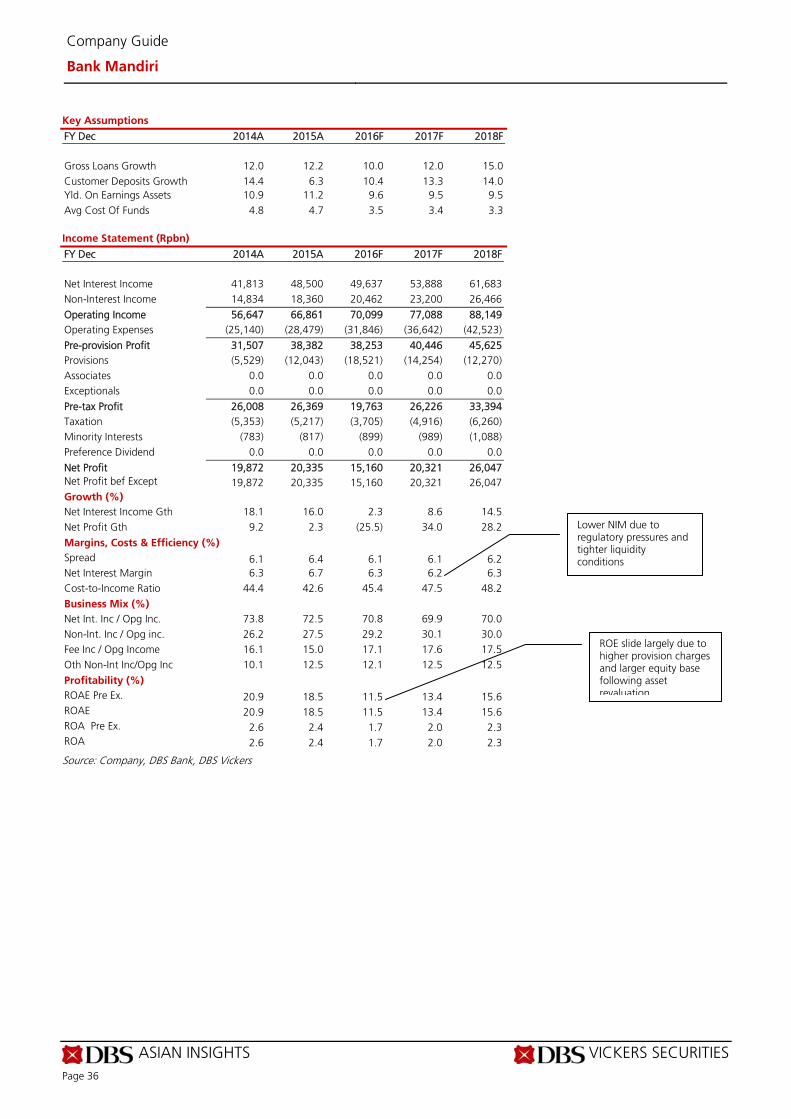

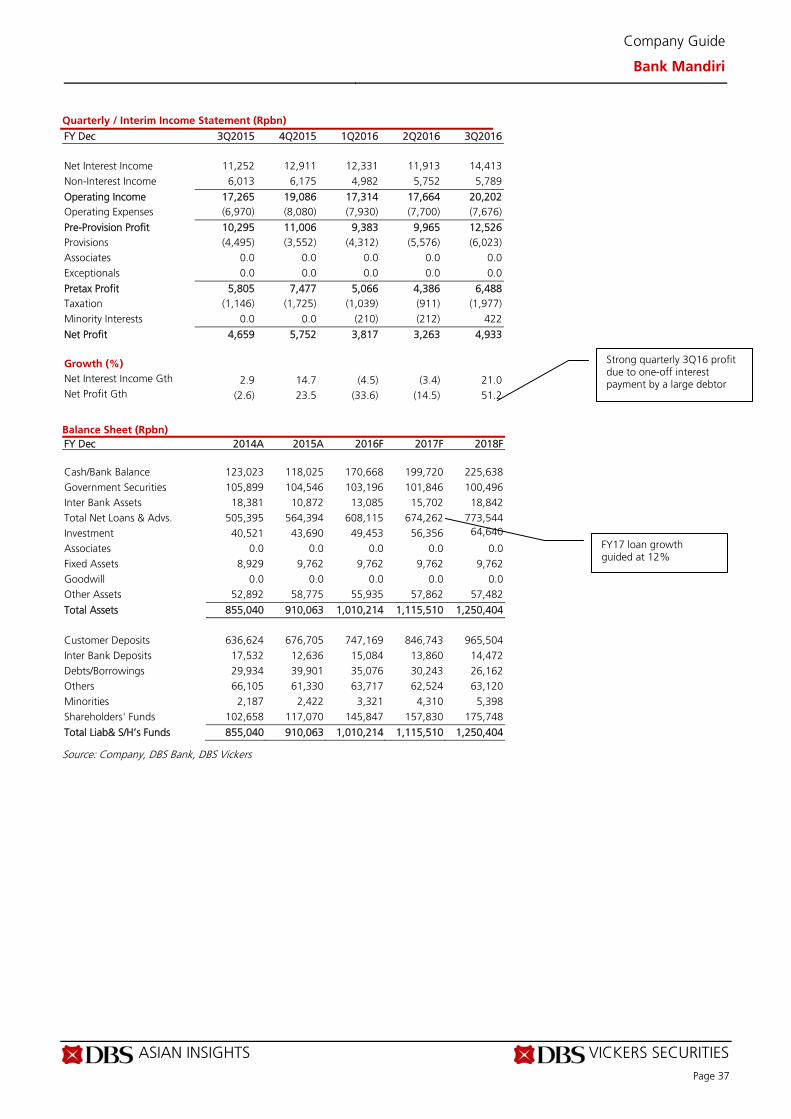

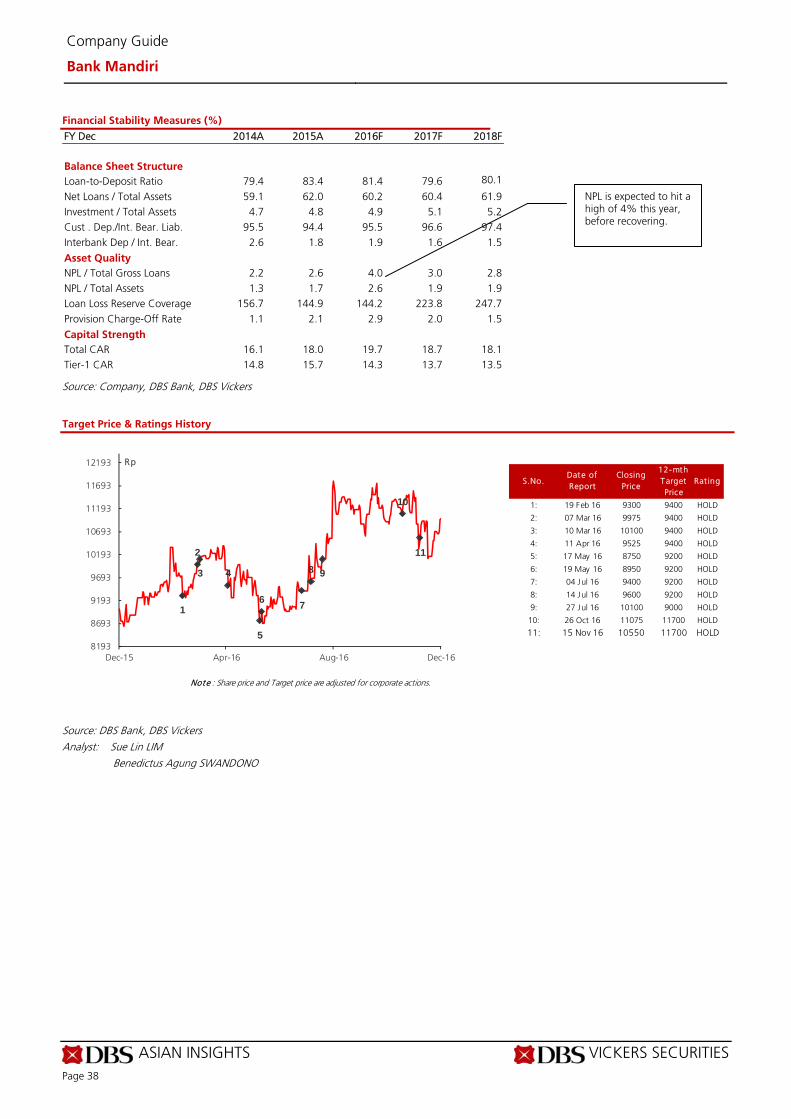

Bank Mandiri 32

Bank Negara Indonesia 39

Bank Rakyat Indonesia 46

Bank Tabungan Negara 53

Bank Tabungan Pensiunan Nasional 60

Panin Bank 67

Industry Focus

Page 3

Key trends to watch in 2017

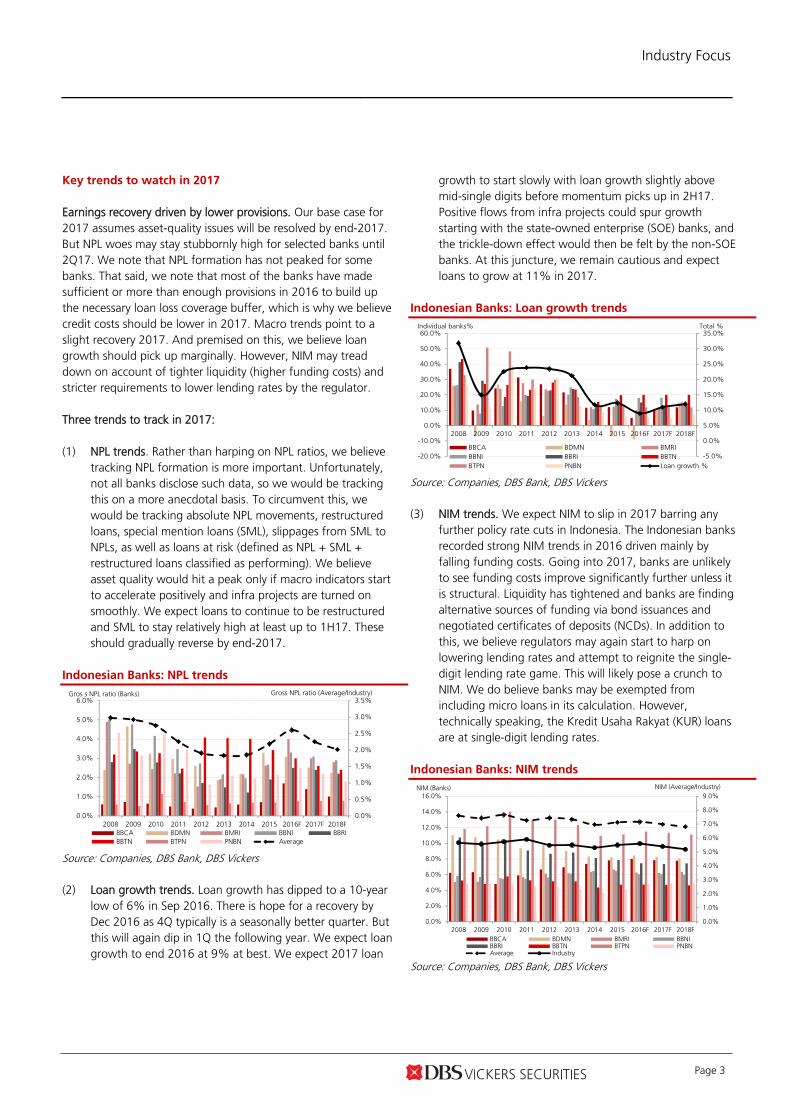

Earnings recovery driven by lower provisions. Our base case for 2017 assumes asset-quality issues will be resolved by end-2017. But NPL woes may stay stubbornly high for selected banks until 2Q17. We note that NPL formation has not peaked for some banks. That said, we note that most of the banks have made sufficient or more than enough provisions in 2016 to build up the necessary loan loss coverage buffer, which is why we believe credit costs should be lower in 2017. Macro trends point to a slight recovery 2017. And premised on this, we believe loan growth should pick up marginally. However, NIM may tread down on account of tighter liquidity (higher funding costs) and stricter requirements to lower lending rates by the regulator. Three trends to track in 2017: (1) NPL trends. Rather than harping on NPL ratios, we believe

tracking NPL formation is more important. Unfortunately, not all banks disclose such data, so we would be tracking this on a more anecdotal basis. To circumvent this, we would be tracking absolute NPL movements, restructured loans, special mention loans (SML), slippages from SML to NPLs, as well as loans at risk (defined as NPL + SML + restructured loans classified as performing). We believe asset quality would hit a peak only if macro indicators start to accelerate positively and infra projects are turned on smoothly. We expect loans to continue to be restructured and SML to stay relatively high at least up to 1H17. These should gradually reverse by end-2017.

Indonesian Banks: NPL trends

Source: Companies, DBS Bank, DBS Vickers (2) Loan growth trends. Loan growth has dipped to a 10-year

low of 6% in Sep 2016. There is hope for a recovery by Dec 2016 as 4Q typically is a seasonally better quarter. But this will again dip in 1Q the following year. We expect loan growth to end 2016 at 9% at best. We expect 2017 loan

growth to start slowly with loan growth slightly above mid-single digits before momentum picks up in 2H17. Positive flows from infra projects could spur growth starting with the state-owned enterprise (SOE) banks, and the trickle-down effect would then be felt by the non-SOE banks. At this juncture, we remain cautious and expect loans to grow at 11% in 2017.

Indonesian Banks: Loan growth trends

Source: Companies, DBS Bank, DBS Vickers

(3) NIM trends. We expect NIM to slip in 2017 barring any

further policy rate cuts in Indonesia. The Indonesian banks recorded strong NIM trends in 2016 driven mainly by falling funding costs. Going into 2017, banks are unlikely to see funding costs improve significantly further unless it is structural. Liquidity has tightened and banks are finding alternative sources of funding via bond issuances and negotiated certificates of deposits (NCDs). In addition to this, we believe regulators may again start to harp on lowering lending rates and attempt to reignite the single- digit lending rate game. This will likely pose a crunch to NIM. We do believe banks may be exempted from including micro loans in its calculation. However, technically speaking, the Kredit Usaha Rakyat (KUR) loans are at single-digit lending rates.

Indonesian Banks: NIM trends

Source: Companies, DBS Bank, DBS Vickers

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016F 2017F 2018FBBCA BDMN BMRI BBNI BBRIBBTN BTPN PNBN Average

Gros s NPL ratio (Banks) Gross NPL ratio (Average/Industry)

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRIBBNI BBRI BBTNBTPN PNBN Loan growth %

Individual banks% Total %

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016F 2017F 2018FBBCA BDMN BMRI BBNIBBRI BBTN BTPN PNBNAverage Industry

NIM (Banks) NIM (Average/Industry)

Industry Focus

Page 4

Turning a little more positive

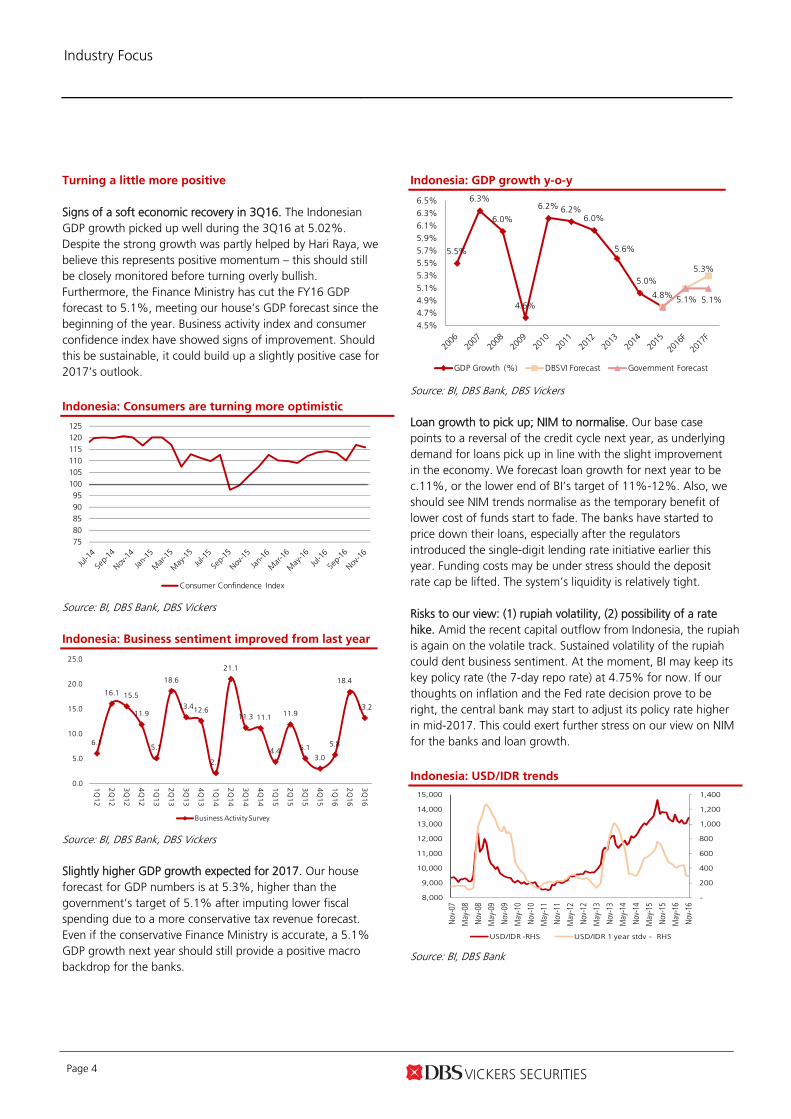

Signs of a soft economic recovery in 3Q16. The Indonesian GDP growth picked up well during the 3Q16 at 5.02%. Despite the strong growth was partly helped by Hari Raya, we believe this represents positive momentum – this should still be closely monitored before turning overly bullish. Furthermore, the Finance Ministry has cut the FY16 GDP forecast to 5.1%, meeting our house’s GDP forecast since the beginning of the year. Business activity index and consumer confidence index have showed signs of improvement. Should this be sustainable, it could build up a slightly positive case for 2017’s outlook.

Indonesia: Consumers are turning more optimistic

Source: BI, DBS Bank, DBS Vickers Indonesia: Business sentiment improved from last year

Source: BI, DBS Bank, DBS Vickers Slightly higher GDP growth expected for 2017. Our house forecast for GDP numbers is at 5.3%, higher than the government’s target of 5.1% after imputing lower fiscal spending due to a more conservative tax revenue forecast. Even if the conservative Finance Ministry is accurate, a 5.1% GDP growth next year should still provide a positive macro backdrop for the banks.

Indonesia: GDP growth y-o-y

Source: BI, DBS Bank, DBS Vickers Loan growth to pick up; NIM to normalise. Our base case points to a reversal of the credit cycle next year, as underlying demand for loans pick up in line with the slight improvement in the economy. We forecast loan growth for next year to be c.11%, or the lower end of BI’s target of 11%-12%. Also, we should see NIM trends normalise as the temporary benefit of lower cost of funds start to fade. The banks have started to price down their loans, especially after the regulators introduced the single-digit lending rate initiative earlier this year. Funding costs may be under stress should the deposit rate cap be lifted. The system’s liquidity is relatively tight. Risks to our view: (1) rupiah volatility, (2) possibility of a rate hike. Amid the recent capital outflow from Indonesia, the rupiah is again on the volatile track. Sustained volatility of the rupiah could dent business sentiment. At the moment, BI may keep its key policy rate (the 7-day repo rate) at 4.75% for now. If our thoughts on inflation and the Fed rate decision prove to be right, the central bank may start to adjust its policy rate higher in mid-2017. This could exert further stress on our view on NIM for the banks and loan growth.

Indonesia: USD/IDR trends

Source: BI, DBS Bank

7580859095

100105110115120125

Consumer Confindence Index

6.1

16.1 15.5

11.9

5.1

18.6

13.412.6

2.1

21.1

11.3 11.1

4.4

11.9

5.13.0

5.8

18.4

13.2

0.0

5.0

10.0

15.0

20.0

25.0

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

Business Activity Survey

5.5%

6.3%

6.0%

4.6%

6.2% 6.2%6.0%

5.6%

5.0%

4.8%

5.3%

5.1% 5.1%

4.5%

4.7%

4.9%

5.1%

5.3%

5.5%

5.7%

5.9%

6.1%

6.3%

6.5%

GDP Growth (%) DBSVI Forecast Government Forecast

-

200

400

600

800

1,000

1,200

1,400

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

Nov-

07

May

-08

Nov-

08

May

-09

Nov-

09

May

-10

Nov-

10

May

-11

Nov-

11

May

-12

Nov-

12

May

-13

Nov-

13

May

-14

Nov-

14

May

-15

Nov-

15

May

-16

Nov-

16

USD/IDR -RHS USD/IDR 1 year stdv - RHS

Industry Focus

Page 5

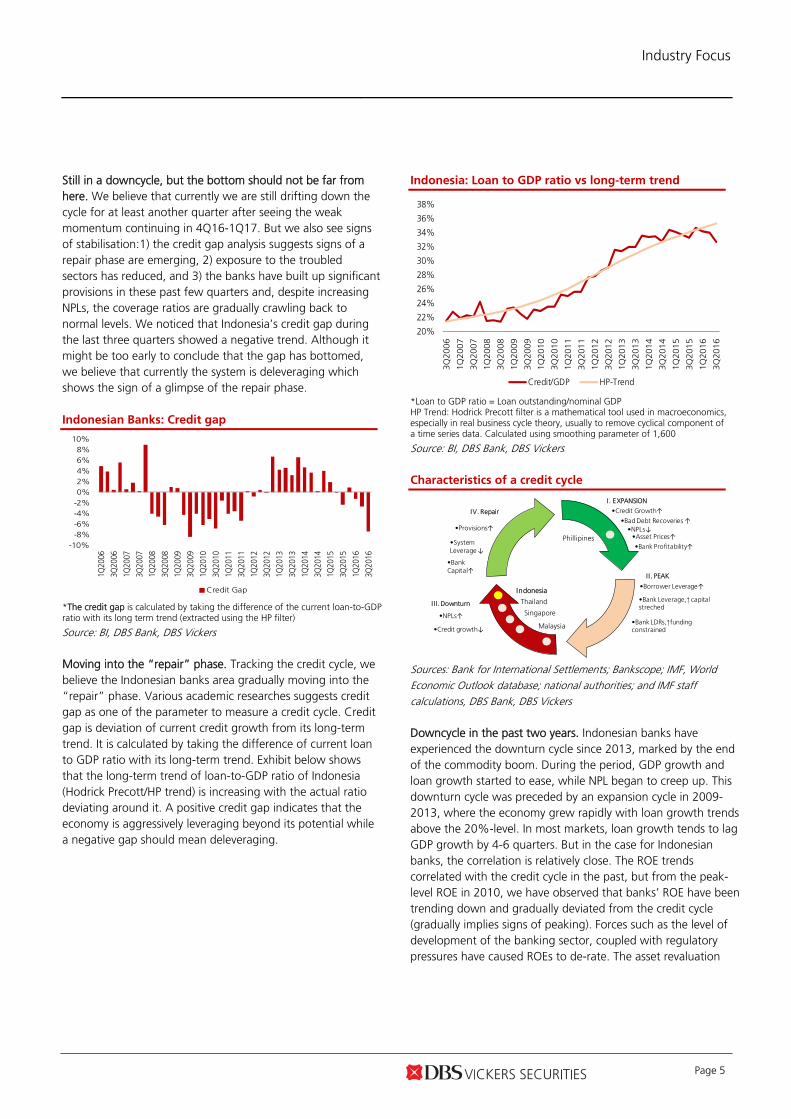

Still in a downcycle, but the bottom should not be far from here. We believe that currently we are still drifting down the cycle for at least another quarter after seeing the weak momentum continuing in 4Q16-1Q17. But we also see signs of stabilisation:1) the credit gap analysis suggests signs of a repair phase are emerging, 2) exposure to the troubled sectors has reduced, and 3) the banks have built up significant provisions in these past few quarters and, despite increasing NPLs, the coverage ratios are gradually crawling back to normal levels. We noticed that Indonesia’s credit gap during the last three quarters showed a negative trend. Although it might be too early to conclude that the gap has bottomed, we believe that currently the system is deleveraging which shows the sign of a glimpse of the repair phase. Indonesian Banks: Credit gap

*The credit gap is calculated by taking the difference of the current loan-to-GDP ratio with its long term trend (extracted using the HP filter)

Source: BI, DBS Bank, DBS Vickers Moving into the “repair” phase. Tracking the credit cycle, we believe the Indonesian banks area gradually moving into the “repair” phase. Various academic researches suggests credit gap as one of the parameter to measure a credit cycle. Credit gap is deviation of current credit growth from its long-term trend. It is calculated by taking the difference of current loan to GDP ratio with its long-term trend. Exhibit below shows that the long-term trend of loan-to-GDP ratio of Indonesia (Hodrick Precott/HP trend) is increasing with the actual ratio deviating around it. A positive credit gap indicates that the economy is aggressively leveraging beyond its potential while a negative gap should mean deleveraging.

Indonesia: Loan to GDP ratio vs long-term trend

*Loan to GDP ratio = Loan outstanding/nominal GDP HP Trend: Hodrick Precott filter is a mathematical tool used in macroeconomics, especially in real business cycle theory, usually to remove cyclical component of a time series data. Calculated using smoothing parameter of 1,600

Source: BI, DBS Bank, DBS Vickers Characteristics of a credit cycle

Sources: Bank for International Settlements; Bankscope; IMF, World Economic Outlook database; national authorities; and IMF staff calculations, DBS Bank, DBS Vickers Downcycle in the past two years. Indonesian banks have experienced the downturn cycle since 2013, marked by the end of the commodity boom. During the period, GDP growth and loan growth started to ease, while NPL began to creep up. This downturn cycle was preceded by an expansion cycle in 2009-2013, where the economy grew rapidly with loan growth trends above the 20%-level. In most markets, loan growth tends to lag GDP growth by 4-6 quarters. But in the case for Indonesian banks, the correlation is relatively close. The ROE trends correlated with the credit cycle in the past, but from the peak-level ROE in 2010, we have observed that banks’ ROE have been trending down and gradually deviated from the credit cycle (gradually implies signs of peaking). Forces such as the level of development of the banking sector, coupled with regulatory pressures have caused ROEs to de-rate. The asset revaluation

-10%-8%-6%-4%-2%0%2%4%6%8%

10%

1Q20

06

3Q20

06

1Q20

07

3Q20

07

1Q20

08

3Q20

08

1Q20

09

3Q20

09

1Q20

10

3Q20

10

1Q20

11

3Q20

11

1Q20

12

3Q20

12

1Q20

13

3Q20

13

1Q20

14

3Q20

14

1Q20

15

3Q20

15

1Q20

16

3Q20

16

Credit Gap

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

3Q20

06

1Q20

07

3Q20

07

1Q20

08

3Q20

08

1Q20

09

3Q20

09

1Q20

10

3Q20

10

1Q20

11

3Q20

11

1Q20

12

3Q20

12

1Q20

13

3Q20

13

1Q20

14

3Q20

14

1Q20

15

3Q20

15

1Q20

16

3Q20

16

Credit/GDP HP-Trend

Thailand

Indonesia

Singapore

Phillipines

I . EXPANSION

•↑↓

•Bank Profitability↑

•Provisions↑•Asset Prices↑

•NPLs↓•Bad Debt Recoveries ↑

•Credit Growth↑

•System Leverage ↓

•Bank Capital↑

•Credit growth↓

•NPLs↑•Bank LDRs,↑funding constrained

•Bank Leverage,↑ capital streched

•Borrower Leverage↑

I I . PEAK

I II. Downturn

IV. Repair

Malaysia

Industry Focus

Page 6

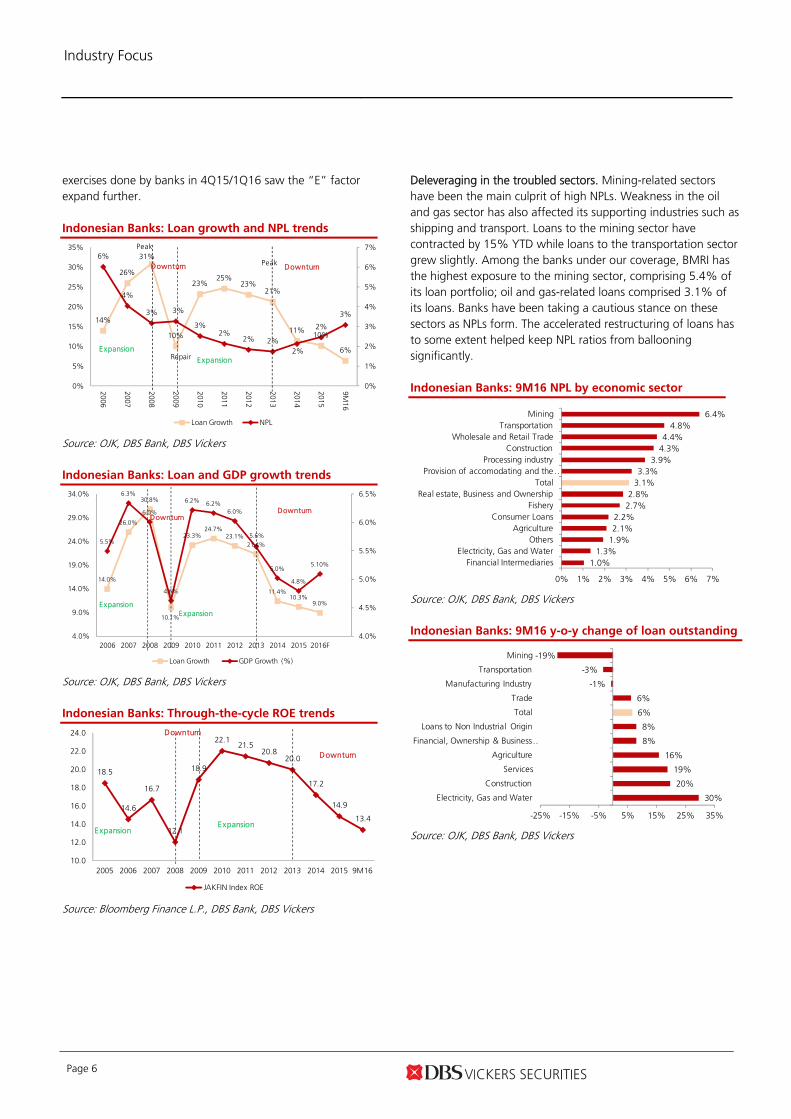

exercises done by banks in 4Q15/1Q16 saw the “E” factor expand further. Indonesian Banks: Loan growth and NPL trends

Source: OJK, DBS Bank, DBS Vickers Indonesian Banks: Loan and GDP growth trends

Source: OJK, DBS Bank, DBS Vickers Indonesian Banks: Through-the-cycle ROE trends

Source: Bloomberg Finance L.P., DBS Bank, DBS Vickers

Deleveraging in the troubled sectors. Mining-related sectors have been the main culprit of high NPLs. Weakness in the oil and gas sector has also affected its supporting industries such as shipping and transport. Loans to the mining sector have contracted by 15% YTD while loans to the transportation sector grew slightly. Among the banks under our coverage, BMRI has the highest exposure to the mining sector, comprising 5.4% of its loan portfolio; oil and gas-related loans comprised 3.1% of its loans. Banks have been taking a cautious stance on these sectors as NPLs form. The accelerated restructuring of loans has to some extent helped keep NPL ratios from ballooning significantly. Indonesian Banks: 9M16 NPL by economic sector

Source: OJK, DBS Bank, DBS Vickers Indonesian Banks: 9M16 y-o-y change of loan outstanding

Source: OJK, DBS Bank, DBS Vickers

14%

26%

31%

10%

23%25%

23%21%

11%10%

6%

6%

4%

3% 3%

3%2%

2% 2%2%

2%

3%

0%

1%

2%

3%

4%

5%

6%

7%

0%

5%

10%

15%

20%

25%

30%

35%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

9M16

Loan Growth NPL

RepairExpansion

Expansion

Downturn DownturnPeak

Peak

14.0%

26.0%

30.8%

10.1%

23.3%24.7%

23.1%21.4%

11.4%10.3%

9.0%

5.5%

6.3%

6.0%

4.6%

6.2% 6.2%6.0%

5.6%

5.0%

4.8%

5.10%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

4.0%

9.0%

14.0%

19.0%

24.0%

29.0%

34.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F

Loan Growth GDP Growth (%)

ExpansionExpansion

DownturnDownturn

18.5

14.6

16.7

12.1

18.9

22.121.5

20.820.0

17.2

14.9

13.4

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 9M16

JAKFIN Index ROE

Expansion

Downturn

Expansion

Downturn

1.0%1.3%

1.9%2.1%2.2%

2.7%2.8%

3.1%3.3%

3.9%4.3%4.4%

4.8%6.4%

0% 1% 2% 3% 4% 5% 6% 7%

Financial IntermediariesElectricity, Gas and Water

OthersAgriculture

Consumer LoansFishery

Real estate, Business and OwnershipTotal

Provision of accomodating and the …Processing industry

ConstructionWholesale and Retail Trade

TransportationMining

30%

20%

19%

16%

8%

8%

6%

6%

-1%

-3%

-19%

-25% -15% -5% 5% 15% 25% 35%

Electricity, Gas and Water

Construction

Services

Agriculture

Financial, Ownership & Business …

Loans to Non Industrial Origin

Total

Trade

Manufacturing Industry

Transportation

Mining

Industry Focus

Page 7

Indonesian Banks: Exposure to mining as at end-3Q16

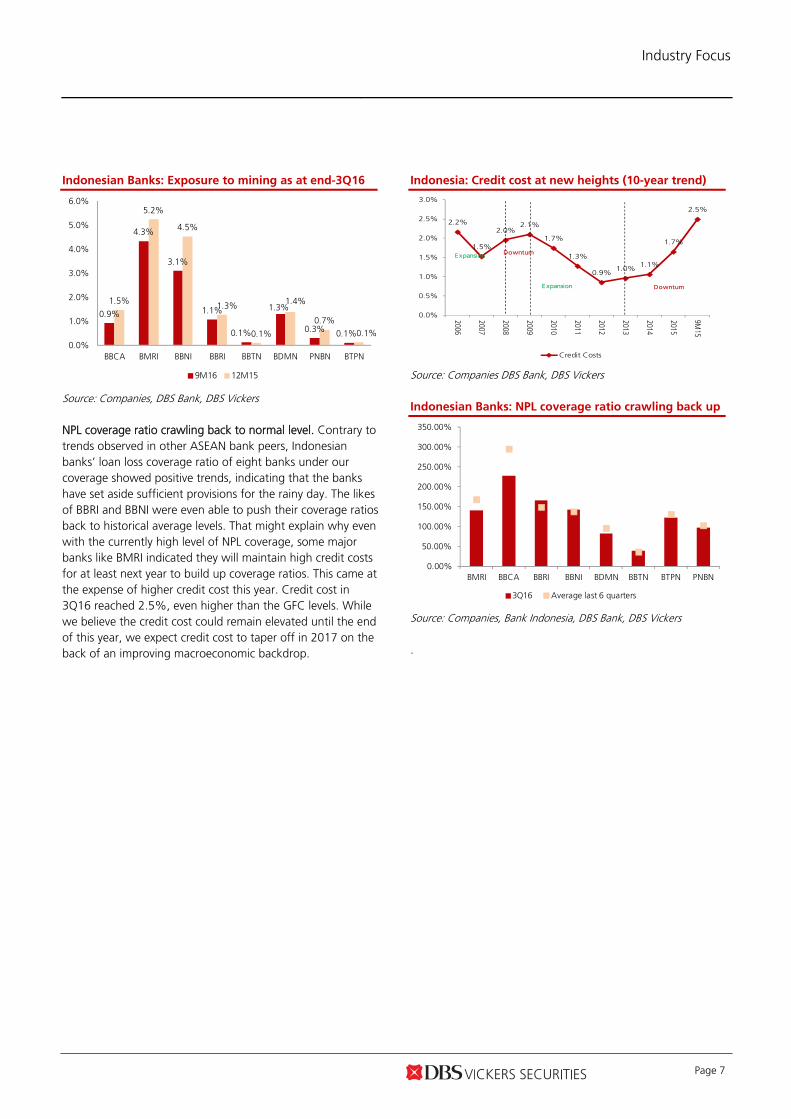

Source: Companies, DBS Bank, DBS Vickers NPL coverage ratio crawling back to normal level. Contrary to trends observed in other ASEAN bank peers, Indonesian banks’ loan loss coverage ratio of eight banks under our coverage showed positive trends, indicating that the banks have set aside sufficient provisions for the rainy day. The likes of BBRI and BBNI were even able to push their coverage ratios back to historical average levels. That might explain why even with the currently high level of NPL coverage, some major banks like BMRI indicated they will maintain high credit costs for at least next year to build up coverage ratios. This came at the expense of higher credit cost this year. Credit cost in 3Q16 reached 2.5%, even higher than the GFC levels. While we believe the credit cost could remain elevated until the end of this year, we expect credit cost to taper off in 2017 on the back of an improving macroeconomic backdrop.

Indonesia: Credit cost at new heights (10-year trend)

Source: Companies DBS Bank, DBS Vickers Indonesian Banks: NPL coverage ratio crawling back up

Source: Companies, Bank Indonesia, DBS Bank, DBS Vickers .

0.9%

4.3%

3.1%

1.1%

0.1%

1.3%

0.3% 0.1%

1.5%

5.2%

4.5%

1.3%

0.1%

1.4%

0.7%0.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

BBCA BMRI BBNI BBRI BBTN BDMN PNBN BTPN

9M16 12M15

2.2%

1.5%

2.0%2.1%

1.7%

1.3%

0.9%1.0%

1.1%

1.7%

2.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

9M15

Credit Costs

Expansion

E xpansion

Downturn

Downturn

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

350.00%

BMRI BBCA BBRI BBNI BDMN BBTN BTPN PNBN

3Q16 Average last 6 quarters

Industry Focus

Page 8

Clearer signals are needed for a sustainable re-rating

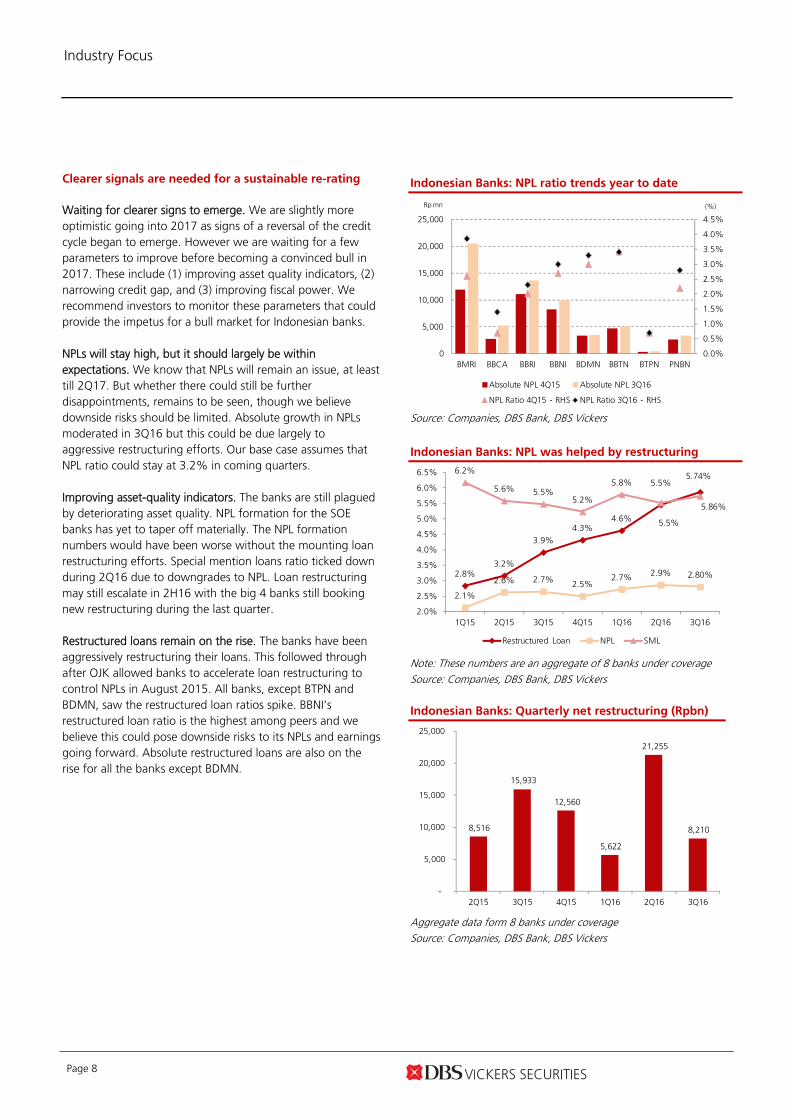

Waiting for clearer signs to emerge. We are slightly more optimistic going into 2017 as signs of a reversal of the credit cycle began to emerge. However we are waiting for a few parameters to improve before becoming a convinced bull in 2017. These include (1) improving asset quality indicators, (2) narrowing credit gap, and (3) improving fiscal power. We recommend investors to monitor these parameters that could provide the impetus for a bull market for Indonesian banks. NPLs will stay high, but it should largely be within expectations. We know that NPLs will remain an issue, at least till 2Q17. But whether there could still be further disappointments, remains to be seen, though we believe downside risks should be limited. Absolute growth in NPLs moderated in 3Q16 but this could be due largely to aggressive restructuring efforts. Our base case assumes that NPL ratio could stay at 3.2% in coming quarters. Improving asset-quality indicators. The banks are still plagued by deteriorating asset quality. NPL formation for the SOE banks has yet to taper off materially. The NPL formation numbers would have been worse without the mounting loan restructuring efforts. Special mention loans ratio ticked down during 2Q16 due to downgrades to NPL. Loan restructuring may still escalate in 2H16 with the big 4 banks still booking new restructuring during the last quarter. Restructured loans remain on the rise. The banks have been aggressively restructuring their loans. This followed through after OJK allowed banks to accelerate loan restructuring to control NPLs in August 2015. All banks, except BTPN and BDMN, saw the restructured loan ratios spike. BBNI’s restructured loan ratio is the highest among peers and we believe this could pose downside risks to its NPLs and earnings going forward. Absolute restructured loans are also on the rise for all the banks except BDMN.

Indonesian Banks: NPL ratio trends year to date

Source: Companies, DBS Bank, DBS Vickers

Indonesian Banks: NPL was helped by restructuring

Note: These numbers are an aggregate of 8 banks under coverage Source: Companies, DBS Bank, DBS Vickers Indonesian Banks: Quarterly net restructuring (Rpbn)

Aggregate data form 8 banks under coverage Source: Companies, DBS Bank, DBS Vickers

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0

5,000

10,000

15,000

20,000

25,000

BMRI BBCA BBRI BBNI BDMN BBTN BTPN PNBN

Absolute NPL 4Q15 Absolute NPL 3Q16

NPL Ratio 4Q15 - RHS NPL Ratio 3Q16 - RHS

Rp mn (%)

2.8%3.2%

3.9%4.3%

4.6% 5.5%

5.86%

2.1%

2.6% 2.7% 2.5%2.7% 2.9% 2.80%

6.2%

5.6% 5.5%5.2%

5.8% 5.5%5.74%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Restructured Loan NPL SML

8,516

15,933

12,560

5,622

21,255

8,210

-

5,000

10,000

15,000

20,000

25,000

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Industry Focus

Page 9

Indonesian Banks: Restructured loans

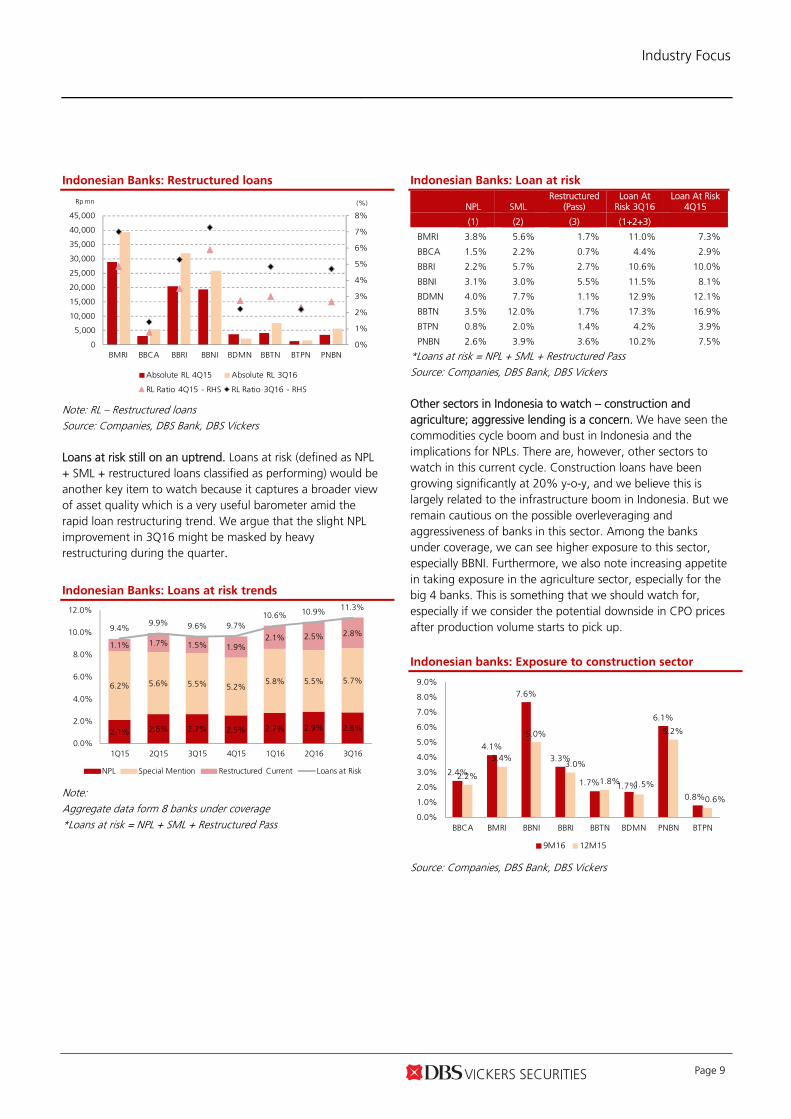

Note: RL – Restructured loans Source: Companies, DBS Bank, DBS Vickers Loans at risk still on an uptrend. Loans at risk (defined as NPL + SML + restructured loans classified as performing) would be another key item to watch because it captures a broader view of asset quality which is a very useful barometer amid the rapid loan restructuring trend. We argue that the slight NPL improvement in 3Q16 might be masked by heavy restructuring during the quarter.

Indonesian Banks: Loans at risk trends

Note: Aggregate data form 8 banks under coverage *Loans at risk = NPL + SML + Restructured Pass

Indonesian Banks: Loan at risk

NPL SML Restructured

(Pass) Loan At

Risk 3Q16 Loan At Risk

4Q15

(1) (2) (3) (1+2+3)

BMRI 3.8% 5.6% 1.7% 11.0% 7.3%

BBCA 1.5% 2.2% 0.7% 4.4% 2.9%

BBRI 2.2% 5.7% 2.7% 10.6% 10.0%

BBNI 3.1% 3.0% 5.5% 11.5% 8.1%

BDMN 4.0% 7.7% 1.1% 12.9% 12.1%

BBTN 3.5% 12.0% 1.7% 17.3% 16.9%

BTPN 0.8% 2.0% 1.4% 4.2% 3.9%

PNBN 2.6% 3.9% 3.6% 10.2% 7.5%

*Loans at risk = NPL + SML + Restructured Pass Source: Companies, DBS Bank, DBS Vickers Other sectors in Indonesia to watch – construction and agriculture; aggressive lending is a concern. We have seen the commodities cycle boom and bust in Indonesia and the implications for NPLs. There are, however, other sectors to watch in this current cycle. Construction loans have been growing significantly at 20% y-o-y, and we believe this is largely related to the infrastructure boom in Indonesia. But we remain cautious on the possible overleveraging and aggressiveness of banks in this sector. Among the banks under coverage, we can see higher exposure to this sector, especially BBNI. Furthermore, we also note increasing appetite in taking exposure in the agriculture sector, especially for the big 4 banks. This is something that we should watch for, especially if we consider the potential downside in CPO prices after production volume starts to pick up.

Indonesian banks: Exposure to construction sector

Source: Companies, DBS Bank, DBS Vickers

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

BMRI BBCA BBRI BBNI BDMN BBTN BTPN PNBN

Absolute RL 4Q15 Absolute RL 3Q16

RL Ratio 4Q15 - RHS RL Ratio 3Q16 - RHS

Rp mn (%)

2.1% 2.6% 2.7% 2.5% 2.7% 2.9% 2.8%

6.2% 5.6% 5.5% 5.2%5.8% 5.5% 5.7%

1.1% 1.7% 1.5% 1.9%2.1% 2.5% 2.8%

9.4%9.9% 9.6% 9.7%

10.6% 10.9% 11.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

NPL Special Mention Restructured Current Loans at Risk 2.4%

4.1%

7.6%

3.3%

1.7% 1.7%

6.1%

0.8%

2.2%

3.4%

5.0%

3.0%

1.8% 1.5%

5.2%

0.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

BBCA BMRI BBNI BBRI BBTN BDMN PNBN BTPN

9M16 12M15

Industry Focus

Page 10

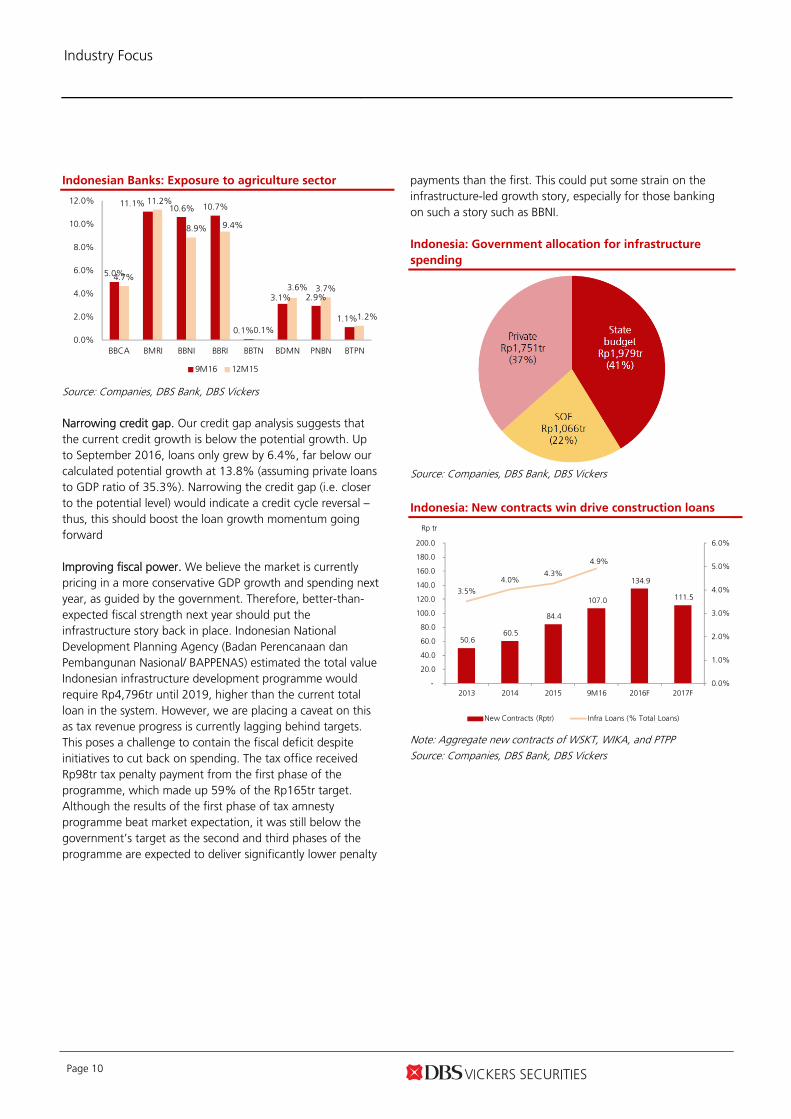

Indonesian Banks: Exposure to agriculture sector

Source: Companies, DBS Bank, DBS Vickers Narrowing credit gap. Our credit gap analysis suggests that the current credit growth is below the potential growth. Up to September 2016, loans only grew by 6.4%, far below our calculated potential growth at 13.8% (assuming private loans to GDP ratio of 35.3%). Narrowing the credit gap (i.e. closer to the potential level) would indicate a credit cycle reversal – thus, this should boost the loan growth momentum going forward Improving fiscal power. We believe the market is currently pricing in a more conservative GDP growth and spending next year, as guided by the government. Therefore, better-than- expected fiscal strength next year should put the infrastructure story back in place. Indonesian National Development Planning Agency (Badan Perencanaan dan Pembangunan Nasional/ BAPPENAS) estimated the total value Indonesian infrastructure development programme would require Rp4,796tr until 2019, higher than the current total loan in the system. However, we are placing a caveat on this as tax revenue progress is currently lagging behind targets. This poses a challenge to contain the fiscal deficit despite initiatives to cut back on spending. The tax office received Rp98tr tax penalty payment from the first phase of the programme, which made up 59% of the Rp165tr target. Although the results of the first phase of tax amnesty programme beat market expectation, it was still below the government’s target as the second and third phases of the programme are expected to deliver significantly lower penalty

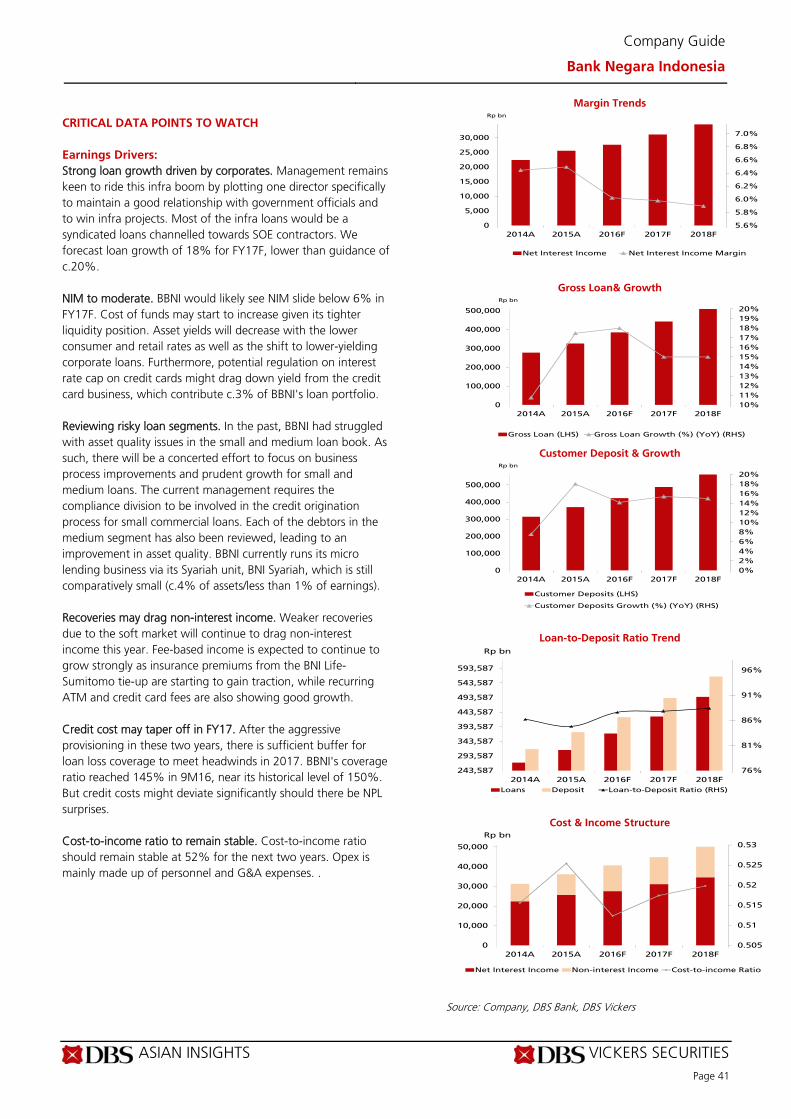

payments than the first. This could put some strain on the infrastructure-led growth story, especially for those banking on such a story such as BBNI. Indonesia: Government allocation for infrastructure

spending

Source: Companies, DBS Bank, DBS Vickers

Indonesia: New contracts win drive construction loans

Note: Aggregate new contracts of WSKT, WIKA, and PTPP Source: Companies, DBS Bank, DBS Vickers

5.0%

11.1%10.6% 10.7%

0.1%

3.1% 2.9%

1.1%

4.7%

11.2%

8.9% 9.4%

0.1%

3.6% 3.7%

1.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

BBCA BMRI BBNI BBRI BBTN BDMN PNBN BTPN

9M16 12M15

50.6 60.5

84.4

107.0

134.9

111.5 3.5%

4.0%4.3%

4.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2013 2014 2015 9M16 2016F 2017F

Rp tr

New Contracts (Rptr) Infra Loans (% Total Loans)

Industry Focus

Page 11

Valuation and recommendation

Through-the-cycle valuation trends. We note that during the downturn cycle, valuations are typically below average PBV, and vice versa. There are some anomalies (i.e. during 1Q15 where the investors were overly bullish after Jokowi was elected) but subsequent crashes had pushed valuations back below the average levels. This is a similar scenario with the current situation, where optimism over the tax amnesty programme is not supported by a credit cycle reversal. Indonesian banks were doing well in 3Q16 following the positive sentiment on the tax amnesty programme and the reshuffling of the cabinet (especially the appointment of the Finance Minister). However, recent capital outflows have affected valuations. Indonesian banks are now trading at -1.5 SD of their 10-year mean P/BV band. Indonesian Banks: Rolling forward PBV band

Source: Bloomberg Finance L.P., DBS Bank, DBS Vickers Market has probably overestimated the impact of the tax amnesty as a positive wildcard for the banks as the government expects the programme to be able to repatriate Rp1,000tr (significantly higher than Bank Indonesia’s (BI) target of Rp180tr). We understand that additional liquidity through funds repatriations should be positive for the banks while funds declarations, although would be positive for government fiscal spending, would have less or no impact on the banks. While we view the success of the tax amnesty being positive for the market and for the banks indirectly, we have held back on imputing this as the banks have yet to find a resounding way to monetise their newfound pool of liquidity. Too much liquidity without proper deployment could lead to negative carry for the banks.

Indonesia: JAKFIN performance

Source: Bloomberg Finance L.P., DBS Bank, DBS Vickers A little more optimistic but still with a pinch of cautiousness. Only BBNI sounds very positive. Approximately, another half of the banks sounded a little more optimistic on growth going into 2017, but remained cautious on asset quality issues at least for 1H17. All banks expect loan growth to pick up marginally in 2017. The state-owned enterprise (SOE) banks were more bullish on growth, except BMRI which expects asset quality issues to drag on till 2Q17. BBRI and BBTN expect loan growth to still be strong in 2017 (c.20%), driven by their respective niche products, i.e. micro (KUR mainly) and subsidised mortgages, respectively. The non-SOE banks (the likes of BBCA and PNBN) are still sounding cautious. BTPN is taking an alternative route to grow. BDMN will be embarking on the second phase of its transformation plan. Target prices adjusted to reflect higher risk free rate. The recent flight of capital outflows coupled with expected volatility has caused government bond yields to spike. We expect such rates to persist. Our risk free rate assumption has been raised to 8.5% (from 7.2% previously). Target prices for banks under our coverage have been adjusted accordingly. BBCA and BDMN remain our top picks. Our appetite for picks is still skewed to the cautious end, which justifies BBCA (BUY, TP Rp16,400) as our top pick. We remain positive on BDMN (BUY, TP Rp4,300) as it moves on to its next phase of its transformation. In addition, we believe the recovery in auto sales would also bode well for BDMN. Other stock ratings. BTPN and PNBN remain BUYs. We continue to monitor BMRI (HOLD, TP Rp10,500) and would gradually turn positive as it emerges out of its asset-quality woes. BBRI (HOLD, TP Rp12,200) remains a HOLD on regulatory risks related to NIM pressure exerted by KUR. We remain cautious on BBNI’s (HOLD, TP Rp5,400) aggressive growth. BBTN is upgraded to HOLD (TP Rp1,660) on valuations

Mean, 2.51

+1SD, 2.92

+2SD, 3.33

-1SD, 2.09

-2SD, 1.68

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

06 07 08 09 10 11 12 13 14 15 16

PBV (X)

600

650

700

750

800

850

JAKFIN Index

Tax amnesty bill passed in June EM market

correction after US election

Industry Focus

Page 12

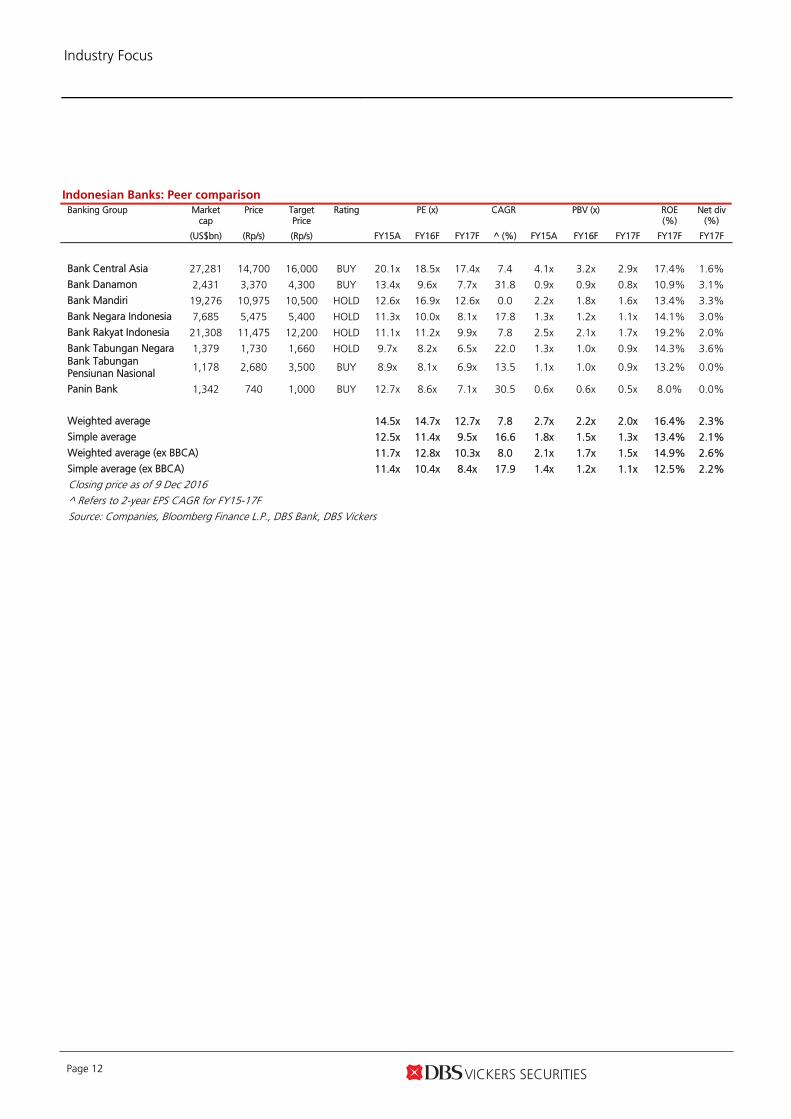

Indonesian Banks: Peer comparison Banking Group Market

cap Price Target

Price Rating PE (x)

CAGR PBV (x)

ROE (%)

Net div (%)

(US$bn) (Rp/s) (Rp/s) FY15A FY16F FY17F ^ (%) FY15A FY16F FY17F FY17F FY17F

Bank Central Asia 27,281 14,700 16,000 BUY 20.1x 18.5x 17.4x 7.4 4.1x 3.2x 2.9x 17.4% 1.6%

Bank Danamon 2,431 3,370 4,300 BUY 13.4x 9.6x 7.7x 31.8 0.9x 0.9x 0.8x 10.9% 3.1%

Bank Mandiri 19,276 10,975 10,500 HOLD 12.6x 16.9x 12.6x 0.0 2.2x 1.8x 1.6x 13.4% 3.3%

Bank Negara Indonesia 7,685 5,475 5,400 HOLD 11.3x 10.0x 8.1x 17.8 1.3x 1.2x 1.1x 14.1% 3.0%

Bank Rakyat Indonesia 21,308 11,475 12,200 HOLD 11.1x 11.2x 9.9x 7.8 2.5x 2.1x 1.7x 19.2% 2.0%

Bank Tabungan Negara 1,379 1,730 1,660 HOLD 9.7x 8.2x 6.5x 22.0 1.3x 1.0x 0.9x 14.3% 3.6% Bank Tabungan Pensiunan Nasional 1,178 2,680 3,500 BUY 8.9x 8.1x 6.9x 13.5 1.1x 1.0x 0.9x 13.2% 0.0%

Panin Bank 1,342 740 1,000 BUY 12.7x 8.6x 7.1x 30.5 0.6x 0.6x 0.5x 8.0% 0.0%

Weighted average 14.5x 14.7x 12.7x 7.8 2.7x 2.2x 2.0x 16.4% 2.3%

Simple average 12.5x 11.4x 9.5x 16.6 1.8x 1.5x 1.3x 13.4% 2.1%

Weighted average (ex BBCA) 11.7x 12.8x 10.3x 8.0 2.1x 1.7x 1.5x 14.9% 2.6%

Simple average (ex BBCA) 11.4x 10.4x 8.4x 17.9 1.4x 1.2x 1.1x 12.5% 2.2%

Closing price as of 9 Dec 2016 ^ Refers to 2-year EPS CAGR for FY15-17F Source: Companies, Bloomberg Finance L.P., DBS Bank, DBS Vickers

Industry Focus

Page 13

Appendix – Key charts

Industry Focus

Page 14

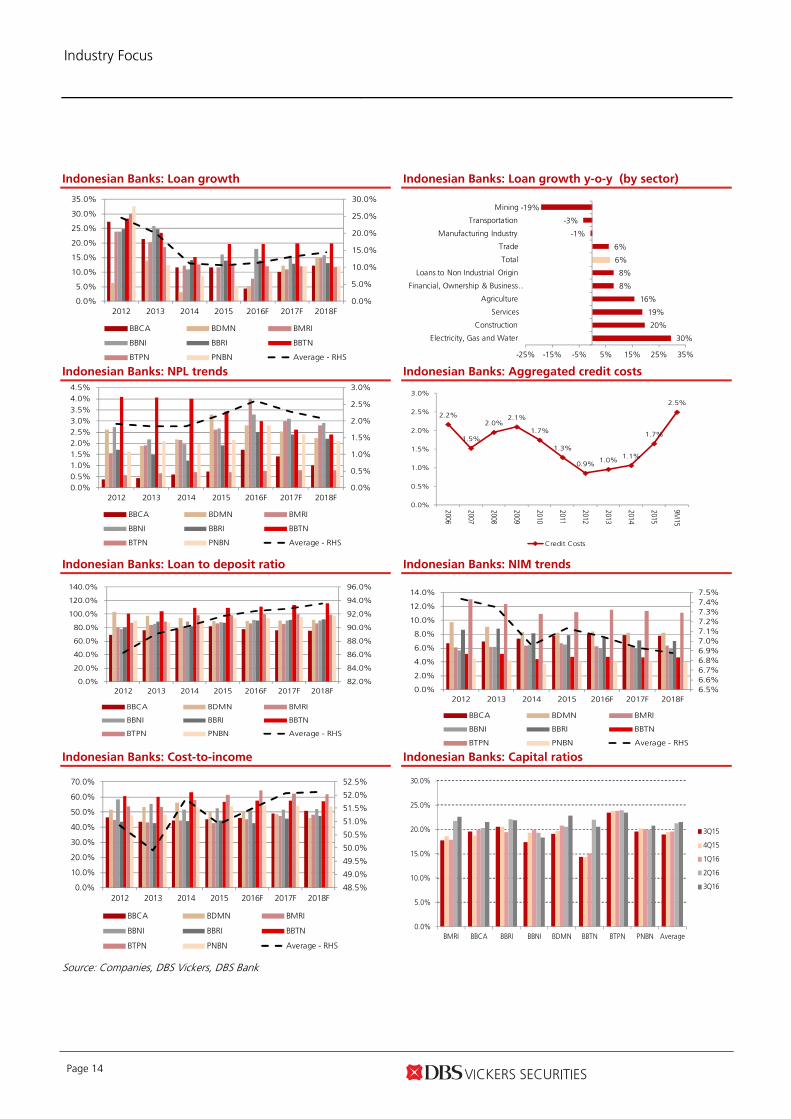

Indonesian Banks: Loan growth

Indonesian Banks: Loan growth y-o-y (by sector)

Indonesian Banks: NPL trends

Indonesian Banks: Aggregated credit costs

Indonesian Banks: Loan to deposit ratio

Indonesian Banks: NIM trends

Indonesian Banks: Cost-to-income

Indonesian Banks: Capital ratios

Source: Companies, DBS Vickers, DBS Bank

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRI

BBNI BBRI BBTN

BTPN PNBN Average - RHS

30%

20%

19%

16%

8%

8%

6%

6%

-1%

-3%

-19%

-25% -15% -5% 5% 15% 25% 35%

Electricity, Gas and Water

Construction

Services

Agriculture

Financial, Ownership & Business …

Loans to Non Industrial Origin

Total

Trade

Manufacturing Industry

Transportation

Mining

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%

2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRI

BBNI BBRI BBTN

BTPN PNBN Average - RHS

6.5%6.6%6.7%6.8%6.9%7.0%7.1%7.2%7.3%7.4%7.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRI

BBNI BBRI BBTN

BTPN PNBN Average - RHS

48.5%

49.0%

49.5%

50.0%

50.5%

51.0%

51.5%

52.0%

52.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRI

BBNI BBRI BBTN

BTPN PNBN Average - RHS

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

2012 2013 2014 2015 2016F 2017F 2018F

BBCA BDMN BMRI

BBNI BBRI BBTN

BTPN PNBN Average - RHS

2.2%

1.5%

2.0%2.1%

1.7%

1.3%

0.9%1.0%

1.1%

1.7%

2.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

9M15

Credit Costs

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

BMRI BBCA BBRI BBNI BDMN BBTN BTPN PNBN Average

3Q15

4Q15

1Q16

2Q16

3Q16

Industry Focus

Page 15

Indonesia: GDP growth

Indonesia: Policy rate trends

Indonesia: Currency

Indonesia: Inflation

Indonesia: Business sentiment

Indonesia: Consumer sentiment

Indonesia: Banking sector stock performance

Indonesia: Stock price performance until November

Source: Companies, DBS Vickers, DBS Bank, Bloomberg Finance L.P

5.5%

6.3%6.0%

4.6%

6.2% 6.2% 6.0%

5.6%

5.0%4.8%

5.1%5.3%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

GDP Growth

600

650

700

750

800

850

JAKFIN Index

Tax amnesty bill passed in June EM market

correction after US election

12%

7%

3%

21%

31%

12%

-5%

18%

13% 13%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

BBCA BBNI BBRI BMRI BBTN BDMN PNBN BTPN JAKFIN JCI

0

1

2

3

4

5

6

7

8

9

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Inflation (%)

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

BI Rate 7DRRR 12MSBI

-

200

400

600

800

1,000

1,200

1,400

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

Nov

-07

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Nov

-14

May

-15

Nov

-15

May

-16

Nov

-16

USD/IDR -RHS USD/IDR 1 year stdv - RHS

7580859095

100105110115120125

Consumer Confindence Index

6.1

16.1 15.5

11.9

5.1

18.6

13.412.6

2.1

21.1

11.3 11.1

4.4

11.9

5.13.0

5.8

18.4

13.2

0.0

5.0

10.0

15.0

20.0

25.0

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Business Activity Survey

Industry Focus

Page 16

Company Guides

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA, PY

BUY Last Traded Price ( 9 Dec 2016): Rp14,700 (JCI : 5,308.10) Price Target 12-mth: Rp16,400 (12% upside) (Prev Rp17,500) Potential Catalyst: Stronger-than-expected loan growth Where we differ: Earnings forecast is below consensus possibly on higher credit costs and lower loan growth Analyst Sue Lin LIM +65 8332 6843 [email protected] Benedictus Agung SWANDONO +6221 3003 4935 [email protected]

What’s New Prudence still remains a priority in 2017 Fee income and lower credit cost to drive earnings Solid asset quality and ample liquidity provide

room for growth next year Maintain BUY; TP lowered to Rp16,400 after

imputing higher risk-free rate following expected

higher government bond yields ahead

Price Relative

Forecasts and Valuation FY Dec (Rpbn) 2015A 2016F 2017F 2018F Pre-prov. Profit 26,162 28,335 28,851 30,953 Net Profit 18,036 19,617 20,813 23,032 Net Pft (Pre Ex.) 18,036 19,617 20,813 23,032 Net Pft Gth (Pre-ex) (%) 9.2 8.8 6.1 10.7 EPS (Rp) 731 795 844 934 EPS Pre Ex. (Rp) 731 795 844 934 EPS Gth Pre Ex (%) 9 9 6 11 Diluted EPS (Rp) 731 795 844 934 PE Pre Ex. (X) 20.1 18.5 17.4 15.7 Net DPS (Rp) 153 219 239 253 Div Yield (%) 1.0 1.5 1.6 1.7 ROAE Pre Ex. (%) 21.6 19.5 17.4 17.0 ROAE (%) 21.6 19.5 17.4 17.0 ROA (%) 3.1 3.1 2.9 2.9 BV Per Share (Rp) 3,623 4,549 5,154 5,835 P/Book Value (x) 4.1 3.2 2.9 2.5 Earnings Rev (%): 0 0 0 Consensus EPS (Rp): 807 904 1,010 Other Broker Recs: B: 19 S: 4 H: 11

Source of all data on this page: Company, DBS Bank, DBS Vickers, Bloomberg Finance L.P.

A better 2017, albeit cautious

Standing tall among peers despite staying cautious, maintain BUY. Bank Central Asia (BBCA) has the strongest CASA deposit franchise with CASA ratio consistently above 75% and the lowest cost of funds in the Indonesian banking universe. With this advantage, we believe BBCA will be able to navigate through the regulatory changes, especially the call for a single-digit lending rate. NPL blips are expected but BBCA’s asset quality still stands superior vs peers. We believe this is the key reason for BBCA to be valued at a premium vs its peers. Prudent growth ahead. BBCA is guiding for a moderate loan growth target (around nominal GDP growth) in view of a moderate improvement in Indonesia’s economic outlook. NIM will likely trend lower as the benefits from lower cost of funds start to taper off and as competitive pressures re-emerge. Fee income will continue to support earnings due to the steady performance of its subsidiaries (insurance, securities, and remittance). Asset quality and liquidity remain its plus points. BBCA still has the most conservative restructuring policies and one of the best asset quality metrics vs peers. We expect credit costs to be lower in 2017 with sufficient buffer already set aside in 2016. Its coverage ratio has recovered to above 200%. NPL ratio should improve, in tandem. Separately, BBCA is able to maintain ample liquidity with loan-to-deposit ratio at c.77%. Management indicated BBCA can push its loan-to-deposit ratio to c.85% level if the economy revs up and loan demand starts to pick up. Valuation:

We have a BUY on BBCA with a lower target price of Rp16,400 as we impute a higher risk-free rate of 8.5% (from 7.2%) following sustained high government bond yield. Our TP is based on the Gordon Growth Model (18% ROE, 10% growth and 13% cost of equity) implying 3.2x FY17 BV. Key Risks to Our View:

Inability to contain NPL issues. Should the economy not pick up as expected, NPLs and loan growth may continue to dwindle, posing downside risk to earnings. At A Glance Issued Capital (m shrs) 24,655 Mkt. Cap (Rpbn/US$m) 362,429 / 27,281 Major Shareholders (%) Farindo Investment Mauritius Lt 47.2

Free Float (%) 50.8 3m Avg. Daily Val (US$m) 21.6 ICB Industry : Financials / Banks

DBS Group Research . Equity 13 Dec 2016

Indonesia Company Guide

Bank Central Asia Version 7 | Bloomberg: BBCA IJ | Reuters: BBCA.JK Refer to important disclosures at the end of this report

87

107

127

147

167

187

207

7,695.0

8,695.0

9,695.0

10,695.0

11,695.0

12,695.0

13,695.0

14,695.0

15,695.0

16,695.0

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Relative IndexRp

Bank Central Asia (LHS) Relative JCI (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 18

Company Guide

Bank Central Asia

WHAT’S NEW

A better 2017, albeit cautious

Highlights A better 2017, albeit cautious. BBCA is guiding for a moderate loan growth target (around nominal GDP growth) due to a moderate improvement in economic outlook ahead. BBCA is expecting loan growth in 2017 to track nominal GDP levels (i.e. c. 8-9%). NPL is guided at 1.5-2% (9M16 at 1.5%); stresses are still seen in the tugboat and barge segments. BBCA still has the most conservative restructuring policies and one of the best asset quality metrics across the Indonesian banking sector. NIM will likely trend lower on a quarterly basis as the benefits from lower cost of funds start to taper off. Fee income will continue to support earnings due to the good performance of its subsidiaries (insurance, securities, Syariah banking, and remittance). 4Q16 could surprise. Although loans could grow by 8% y-o-y, strong repayment activities as BBCA’s customers deleverage could see loans outstanding just 5% ahead of 2015’s balance. Expect positive surprise in 4Q16 loan growth, taking note that 9M16 YTD loan growth has been virtually flat. NIM will likely stay stable from a quarter ago. We may see one more leg up of high provisions for the year as BBCA intends to build its loan loss coverage buffers. NPLs unlikely to taper off in a big way, but should stabilise. NPL ratio is guided at 1.5-2% excluding any write-offs for 2016. Although higher than historical levels, BBCA’s asset quality indicators are still more sound than most of its peers. Loans at risk (NPL+ special-mention loans [SML] + restructured loans that are not NPL) in 3Q16 are the lowest among banks under our coverage at 4.3% (1.5% NPL+ 2.2% SML+ 0.7% restructured loans which are not NPL). Management hinted that loans will still be restructured in the coming quarters. Note that BBCA does not de-classify restructured loans even if these loans are back to performing status. BBCA targets to make provisions to buffer its books, and has a target ratio of 2.9% for overall loan

loss reserves to gross loans. Management does not have a target in mind for loan loss coverage ratio. NIM may slip further from here. NIM rose the first two quarters of 2016 but started to slip a little in 3Q16. While overall NIM for 2016 should be higher than 2015, it is likely to fall further in 2017F as loans continue to be re-priced downwards and BBCA’s appetite to win largely high-quality clients. Unlike some banks which have struggled to comply with the single-digit lending rate initiative by regulators, BBCA should be able to navigate through the regulatory pressure better due to its relatively lower asset yields. The overall bank only asset yield was 8.58% in 3Q16, with only a few corporate loans priced at above the single-digit level. Liquidity is a plus point for BCA, but there is near-term tightness in the system. BBCA’s liquidity remains ample and is the best across the sector with LDR at c.75%. With this ammunition, BBCA will have ample room to grow its loan book once the economy starts to pick up. BBCA handled c.40% of tax penalty payments during the first phase of tax amnesty programme, and this caused a slight glitch in BBCA’s liquidity situation. The sector is faced with tighter liquidity conditions. Concerns on the possible lift of the deposit rate cap could intensify funding cost pressures among banks. Valuation and recommendation Maintain BUY, TP lowered to Rp16,400. We have a BUY call on BBCA but with a lower target price of Rp16,400 as we impute a higher risk-free rate of 8.5% (from 7.2%) following sustained correction in the government bond yields. Our TP is based on the Gordon Growth Model (18% ROE, 10% growth and 13% cost of equity) implying 3.2x FY17 BV. BBCA is trading at a large premium to peers because of its solid balance sheet and liquidity position. While asset quality is an issue BBCA needs to deal with, compared to peers, BBCA’s asset quality indicators are still better.

ASIAN INSIGHTS VICKERS SECURITIES Page 19

Company Guide

Bank Central Asia

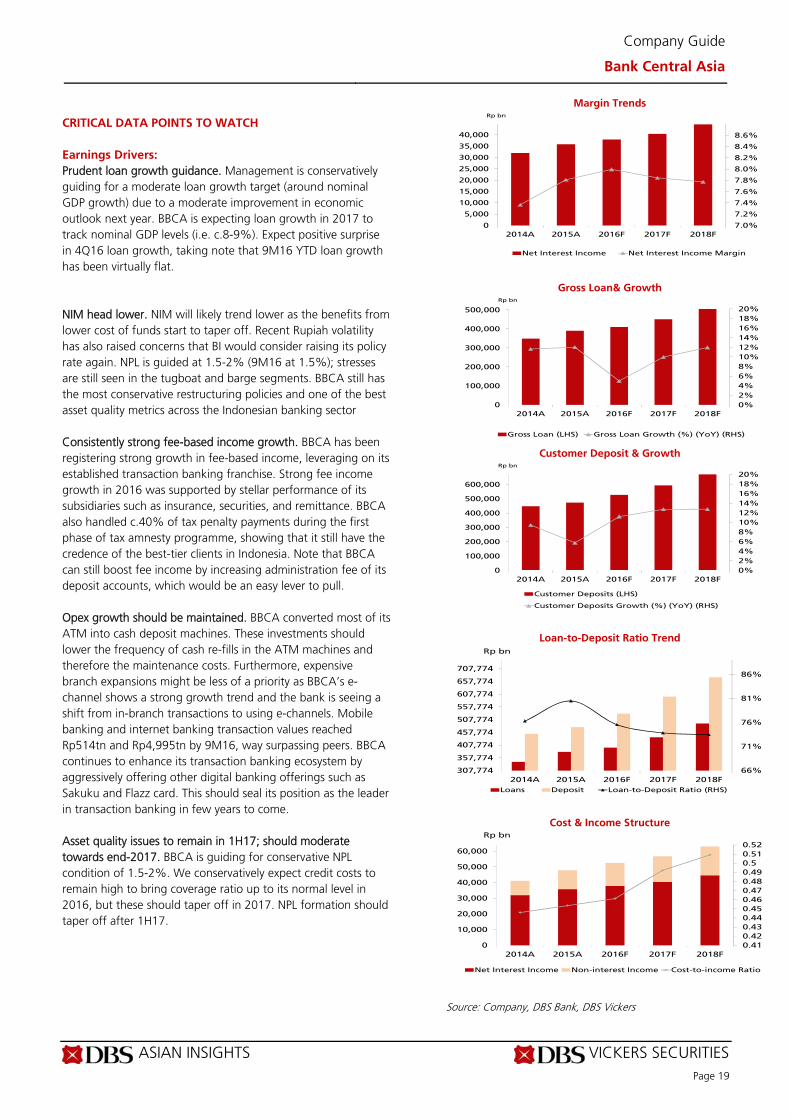

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Prudent loan growth guidance. Management is conservatively guiding for a moderate loan growth target (around nominal GDP growth) due to a moderate improvement in economic outlook next year. BBCA is expecting loan growth in 2017 to track nominal GDP levels (i.e. c.8-9%). Expect positive surprise in 4Q16 loan growth, taking note that 9M16 YTD loan growth has been virtually flat. NIM head lower. NIM will likely trend lower as the benefits from lower cost of funds start to taper off. Recent Rupiah volatility has also raised concerns that BI would consider raising its policy rate again. NPL is guided at 1.5-2% (9M16 at 1.5%); stresses are still seen in the tugboat and barge segments. BBCA still has the most conservative restructuring policies and one of the best asset quality metrics across the Indonesian banking sector Consistently strong fee-based income growth. BBCA has been registering strong growth in fee-based income, leveraging on its established transaction banking franchise. Strong fee income growth in 2016 was supported by stellar performance of its subsidiaries such as insurance, securities, and remittance. BBCA also handled c.40% of tax penalty payments during the first phase of tax amnesty programme, showing that it still have the credence of the best-tier clients in Indonesia. Note that BBCA can still boost fee income by increasing administration fee of its deposit accounts, which would be an easy lever to pull. Opex growth should be maintained. BBCA converted most of its ATM into cash deposit machines. These investments should lower the frequency of cash re-fills in the ATM machines and therefore the maintenance costs. Furthermore, expensive branch expansions might be less of a priority as BBCA’s e-channel shows a strong growth trend and the bank is seeing a shift from in-branch transactions to using e-channels. Mobile banking and internet banking transaction values reached Rp514tn and Rp4,995tn by 9M16, way surpassing peers. BBCA continues to enhance its transaction banking ecosystem by aggressively offering other digital banking offerings such as Sakuku and Flazz card. This should seal its position as the leader in transaction banking in few years to come. Asset quality issues to remain in 1H17; should moderate towards end-2017. BBCA is guiding for conservative NPL condition of 1.5-2%. We conservatively expect credit costs to remain high to bring coverage ratio up to its normal level in 2016, but these should taper off in 2017. NPL formation should taper off after 1H17.

Margin Trends

Gross Loan& Growth

Customer Deposit & Growth

Loan-to-Deposit Ratio Trend

Cost & Income Structure

Source: Company, DBS Bank, DBS Vickers

7.0%

7.2%

7.4%

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2014A 2015A 2016F 2017F 2018F

Rp bn

Net Interest Income Net Interest Income Margin

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

100,000

200,000

300,000

400,000

500,000

2014A 2015A 2016F 2017F 2018F

Rp bn

Gross Loan (LHS) Gross Loan Growth (%) (YoY) (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

100,000

200,000

300,000

400,000

500,000

600,000

2014A 2015A 2016F 2017F 2018F

Rp bn

Customer Deposits (LHS)

Customer Deposits Growth (%) (YoY) (RHS)

66%

71%

76%

81%

86%

307,774

357,774

407,774

457,774

507,774

557,774

607,774

657,774

707,774

2014A 2015A 2016F 2017F 2018F

Rp bn

Loans Deposit Loan-to-Deposit Ratio (RHS)

0.41

0.42

0.43

0.44

0.45

0.46

0.47

0.48

0.49

0.5

0.51

0.52

0

10,000

20,000

30,000

40,000

50,000

60,000

2014A 2015A 2016F 2017F 2018F

Rp bn

Net Interest Income Non-interest Income Cost-to-income Ratio

ASIAN INSIGHTS VICKERS SECURITIES Page 20

Company Guide

Bank Central Asia

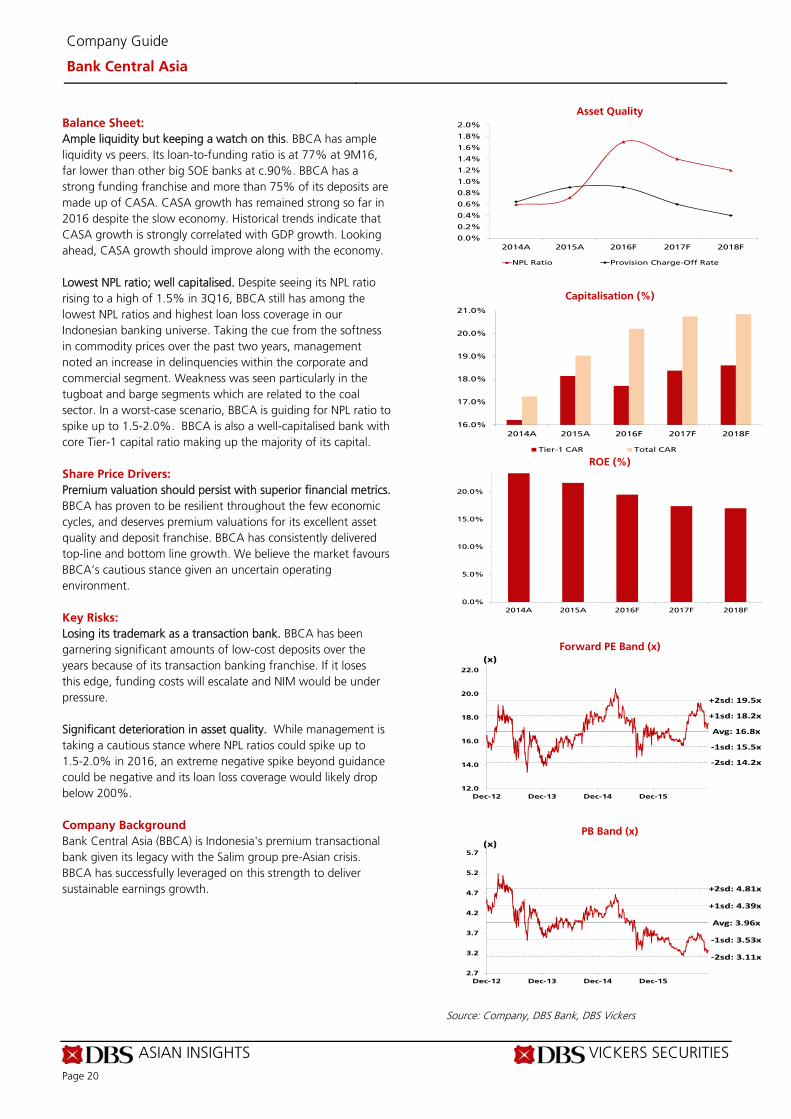

Balance Sheet:

Ample liquidity but keeping a watch on this. BBCA has ample liquidity vs peers. Its loan-to-funding ratio is at 77% at 9M16, far lower than other big SOE banks at c.90%. BBCA has a strong funding franchise and more than 75% of its deposits are made up of CASA. CASA growth has remained strong so far in 2016 despite the slow economy. Historical trends indicate that CASA growth is strongly correlated with GDP growth. Looking ahead, CASA growth should improve along with the economy. Lowest NPL ratio; well capitalised. Despite seeing its NPL ratio rising to a high of 1.5% in 3Q16, BBCA still has among the lowest NPL ratios and highest loan loss coverage in our Indonesian banking universe. Taking the cue from the softness in commodity prices over the past two years, management noted an increase in delinquencies within the corporate and commercial segment. Weakness was seen particularly in the tugboat and barge segments which are related to the coal sector. In a worst-case scenario, BBCA is guiding for NPL ratio to spike up to 1.5-2.0%. BBCA is also a well-capitalised bank with core Tier-1 capital ratio making up the majority of its capital. Share Price Drivers:

Premium valuation should persist with superior financial metrics. BBCA has proven to be resilient throughout the few economic cycles, and deserves premium valuations for its excellent asset quality and deposit franchise. BBCA has consistently delivered top-line and bottom line growth. We believe the market favours BBCA’s cautious stance given an uncertain operating environment. Key Risks:

Losing its trademark as a transaction bank. BBCA has been garnering significant amounts of low-cost deposits over the years because of its transaction banking franchise. If it loses this edge, funding costs will escalate and NIM would be under pressure. Significant deterioration in asset quality. While management is taking a cautious stance where NPL ratios could spike up to 1.5-2.0% in 2016, an extreme negative spike beyond guidance could be negative and its loan loss coverage would likely drop below 200%. Company Background

Bank Central Asia (BBCA) is Indonesia's premium transactional bank given its legacy with the Salim group pre-Asian crisis. BBCA has successfully leveraged on this strength to deliver sustainable earnings growth.

Asset Quality

Capitalisation (%)

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Bank, DBS Vickers

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2014A 2015A 2016F 2017F 2018F

NPL Ratio Provision Charge-Off Rate

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

2014A 2015A 2016F 2017F 2018F

Tier-1 CAR Total CAR

0.0%

5.0%

10.0%

15.0%

20.0%

2014A 2015A 2016F 2017F 2018F

Avg: 16.8x

+1sd: 18.2x

+2sd: 19.5x

‐1sd: 15.5x

‐2sd: 14.2x

12.0

14.0

16.0

18.0

20.0

22.0

Dec-12 Dec-13 Dec-14 Dec-15

(x)

Avg: 3.96x

+1sd: 4.39x

+2sd: 4.81x

‐1sd: 3.53x

‐2sd: 3.11x

2.7

3.2

3.7

4.2

4.7

5.2

5.7

Dec-12 Dec-13 Dec-14 Dec-15

(x)

ASIAN INSIGHTS VICKERS SECURITIES Page 21

Company Guide

Bank Central Asia

Key Assumptions

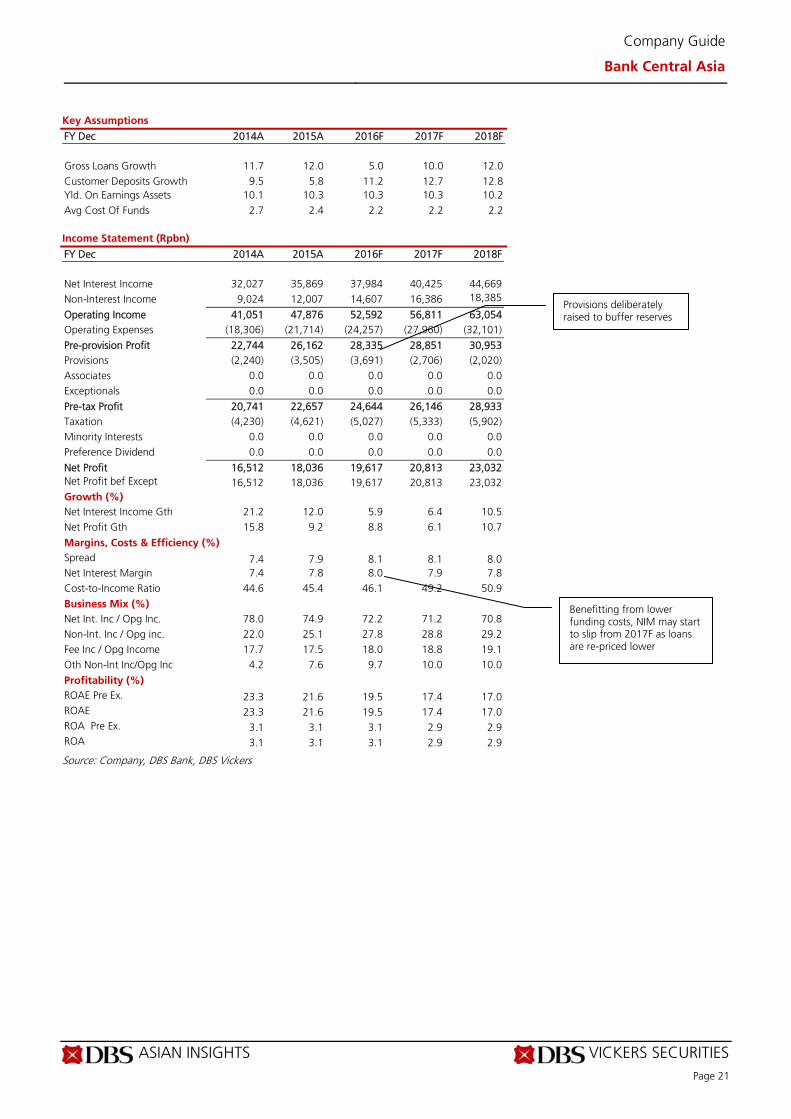

FY Dec 2014A 2015A 2016F 2017F 2018F

Gross Loans Growth 11.7 12.0 5.0 10.0 12.0 Customer Deposits Growth 9.5 5.8 11.2 12.7 12.8 Yld. On Earnings Assets 10.1 10.3 10.3 10.3 10.2 Avg Cost Of Funds 2.7 2.4 2.2 2.2 2.2 Income Statement (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Net Interest Income 32,027 35,869 37,984 40,425 44,669 Non-Interest Income 9,024 12,007 14,607 16,386 18,385

Operating Income 41,051 47,876 52,592 56,811 63,054 Operating Expenses (18,306) (21,714) (24,257) (27,960) (32,101)

Pre-provision Profit 22,744 26,162 28,335 28,851 30,953 Provisions (2,240) (3,505) (3,691) (2,706) (2,020) Associates 0.0 0.0 0.0 0.0 0.0 Exceptionals 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 20,741 22,657 24,644 26,146 28,933 Taxation (4,230) (4,621) (5,027) (5,333) (5,902) Minority Interests 0.0 0.0 0.0 0.0 0.0 Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net Profit 16,512 18,036 19,617 20,813 23,032 Net Profit bef Except 16,512 18,036 19,617 20,813 23,032 Growth (%) Net Interest Income Gth 21.2 12.0 5.9 6.4 10.5 Net Profit Gth 15.8 9.2 8.8 6.1 10.7

Margins, Costs & Efficiency (%) Spread 7.4 7.9 8.1 8.1 8.0 Net Interest Margin 7.4 7.8 8.0 7.9 7.8 Cost-to-Income Ratio 44.6 45.4 46.1 49.2 50.9

Business Mix (%) Net Int. Inc / Opg Inc. 78.0 74.9 72.2 71.2 70.8 Non-Int. Inc / Opg inc. 22.0 25.1 27.8 28.8 29.2 Fee Inc / Opg Income 17.7 17.5 18.0 18.8 19.1 Oth Non-Int Inc/Opg Inc 4.2 7.6 9.7 10.0 10.0

Profitability (%) ROAE Pre Ex. 23.3 21.6 19.5 17.4 17.0 ROAE 23.3 21.6 19.5 17.4 17.0 ROA Pre Ex. 3.1 3.1 3.1 2.9 2.9 ROA 3.1 3.1 3.1 2.9 2.9

Source: Company, DBS Bank, DBS Vickers

Provisions deliberately raised to buffer reserves

Benefitting from lower funding costs, NIM may start to slip from 2017F as loans are re-priced lower

ASIAN INSIGHTS VICKERS SECURITIES Page 22

Company Guide

Bank Central Asia

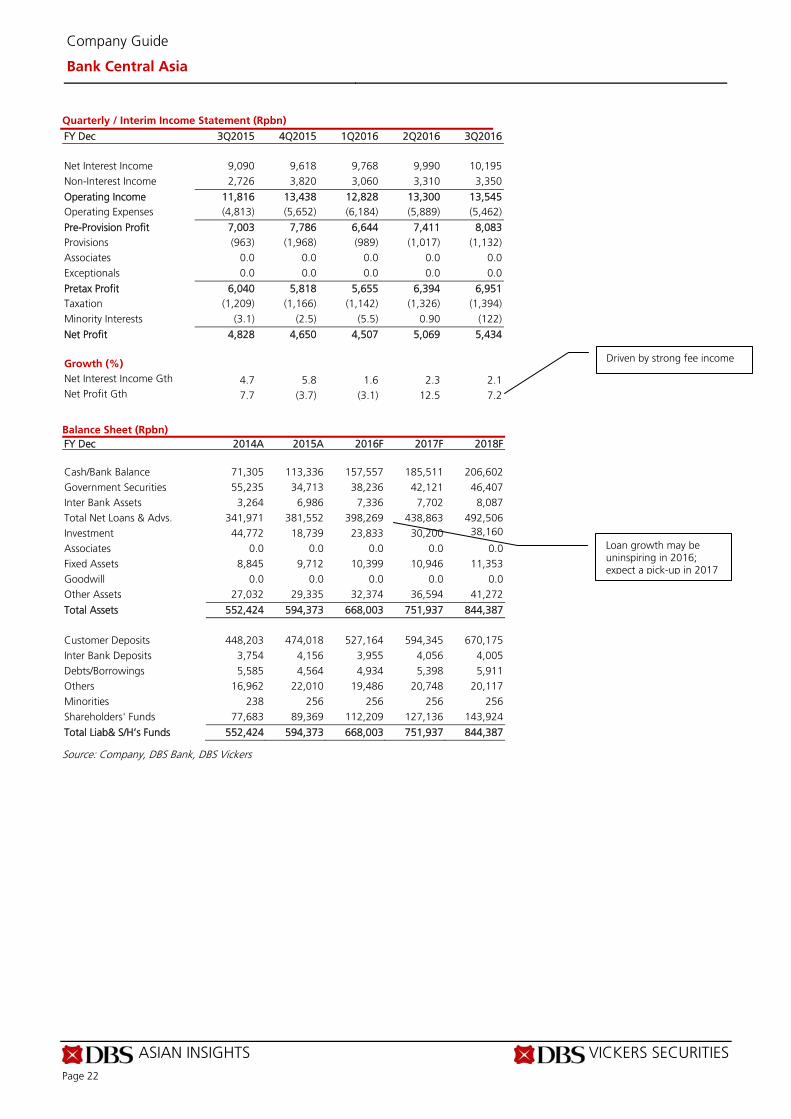

Quarterly / Interim Income Statement (Rpbn)

FY Dec 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 Net Interest Income 9,090 9,618 9,768 9,990 10,195 Non-Interest Income 2,726 3,820 3,060 3,310 3,350

Operating Income 11,816 13,438 12,828 13,300 13,545 Operating Expenses (4,813) (5,652) (6,184) (5,889) (5,462)

Pre-Provision Profit 7,003 7,786 6,644 7,411 8,083 Provisions (963) (1,968) (989) (1,017) (1,132) Associates 0.0 0.0 0.0 0.0 0.0 Exceptionals 0.0 0.0 0.0 0.0 0.0

Pretax Profit 6,040 5,818 5,655 6,394 6,951 Taxation (1,209) (1,166) (1,142) (1,326) (1,394) Minority Interests (3.1) (2.5) (5.5) 0.90 (122)

Net Profit 4,828 4,650 4,507 5,069 5,434

Growth (%) Net Interest Income Gth 4.7 5.8 1.6 2.3 2.1 Net Profit Gth 7.7 (3.7) (3.1) 12.5 7.2

Balance Sheet (Rpbn)

FY Dec 2014A 2015A 2016F 2017F 2018F Cash/Bank Balance 71,305 113,336 157,557 185,511 206,602 Government Securities 55,235 34,713 38,236 42,121 46,407 Inter Bank Assets 3,264 6,986 7,336 7,702 8,087 Total Net Loans & Advs. 341,971 381,552 398,269 438,863 492,506 Investment 44,772 18,739 23,833 30,200 38,160

Associates 0.0 0.0 0.0 0.0 0.0 Fixed Assets 8,845 9,712 10,399 10,946 11,353 Goodwill 0.0 0.0 0.0 0.0 0.0 Other Assets 27,032 29,335 32,374 36,594 41,272

Total Assets 552,424 594,373 668,003 751,937 844,387 Customer Deposits 448,203 474,018 527,164 594,345 670,175 Inter Bank Deposits 3,754 4,156 3,955 4,056 4,005 Debts/Borrowings 5,585 4,564 4,934 5,398 5,911 Others 16,962 22,010 19,486 20,748 20,117 Minorities 238 256 256 256 256 Shareholders' Funds 77,683 89,369 112,209 127,136 143,924

Total Liab& S/H’s Funds 552,424 594,373 668,003 751,937 844,387

Source: Company, DBS Bank, DBS Vickers

Driven by strong fee income

Loan growth may be uninspiring in 2016; expect a pick-up in 2017

ASIAN INSIGHTS VICKERS SECURITIES Page 23

Company Guide

Bank Central Asia

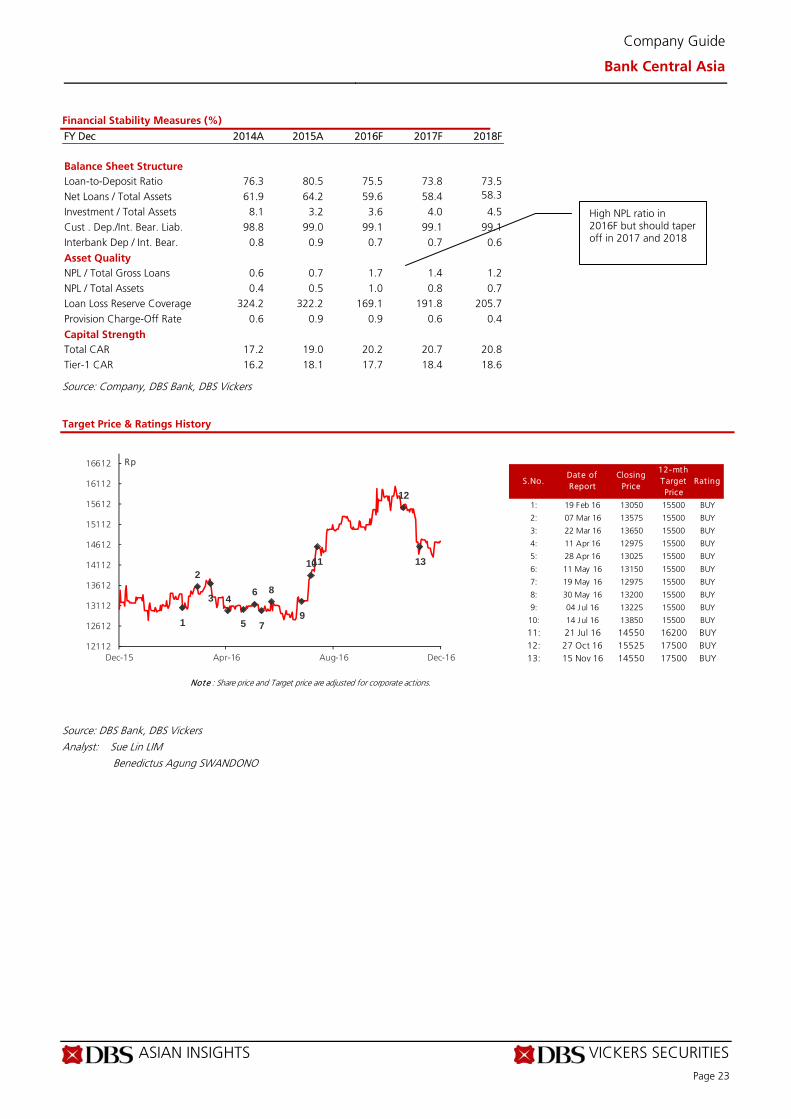

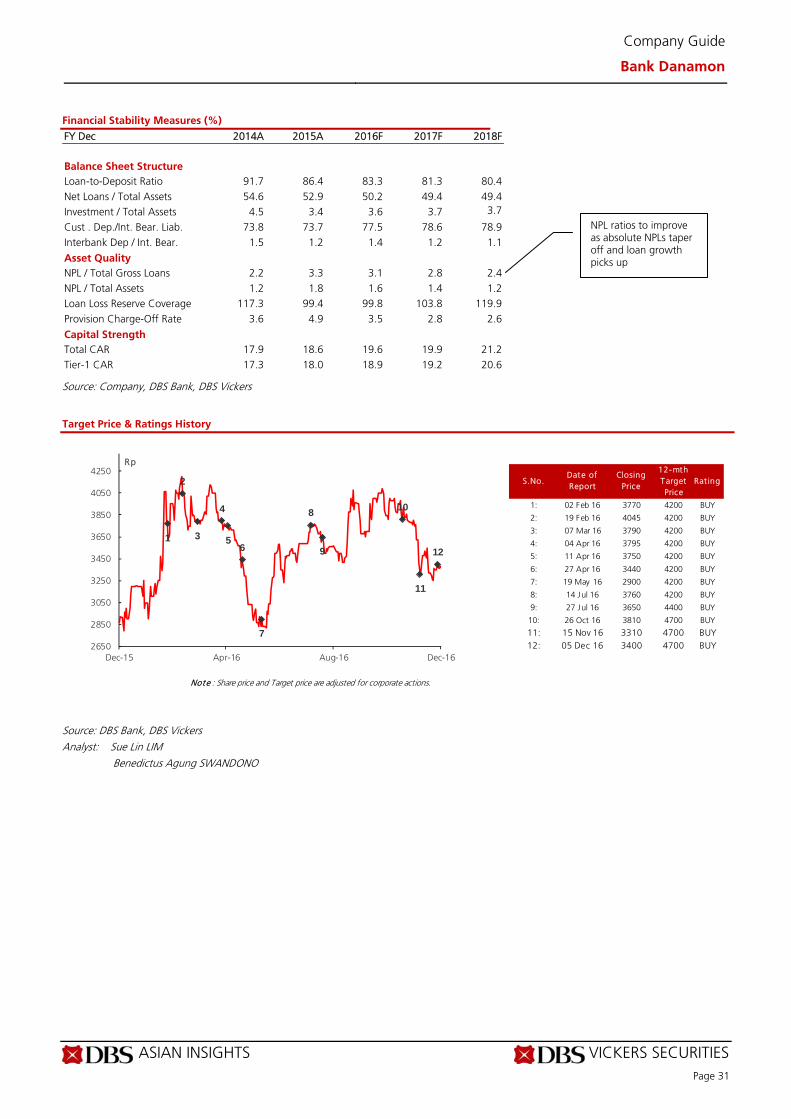

Financial Stability Measures (%)

FY Dec 2014A 2015A 2016F 2017F 2018F Balance Sheet Structure Loan-to-Deposit Ratio 76.3 80.5 75.5 73.8 73.5 Net Loans / Total Assets 61.9 64.2 59.6 58.4 58.3

Investment / Total Assets 8.1 3.2 3.6 4.0 4.5 Cust . Dep./Int. Bear. Liab. 98.8 99.0 99.1 99.1 99.1 Interbank Dep / Int. Bear. 0.8 0.9 0.7 0.7 0.6

Asset Quality NPL / Total Gross Loans 0.6 0.7 1.7 1.4 1.2 NPL / Total Assets 0.4 0.5 1.0 0.8 0.7 Loan Loss Reserve Coverage 324.2 322.2 169.1 191.8 205.7 Provision Charge-Off Rate 0.6 0.9 0.9 0.6 0.4

Capital Strength Total CAR 17.2 19.0 20.2 20.7 20.8 Tier-1 CAR 16.2 18.1 17.7 18.4 18.6

Source: Company, DBS Bank, DBS Vickers

Target Price & Ratings History

Source: DBS Bank, DBS Vickers Analyst: Sue Lin LIM

Benedictus Agung SWANDONO

S.No.Date of Report

Closing Price

12-mth Target Price

Rat ing

1: 19 Feb 16 13050 15500 BUY

2: 07 Mar 16 13575 15500 BUY

3: 22 Mar 16 13650 15500 BUY

4: 11 Apr 16 12975 15500 BUY

5: 28 Apr 16 13025 15500 BUY

6: 11 May 16 13150 15500 BUY

7: 19 May 16 12975 15500 BUY

8: 30 May 16 13200 15500 BUY

9: 04 Jul 16 13225 15500 BUY

10: 14 Jul 16 13850 15500 BUY

11: 21 Jul 16 14550 16200 BUY12: 27 Oct 16 15525 17500 BUY13: 15 Nov 16 14550 17500 BUY

Note : Share price and Target price are adjusted for corporate actions.

1

2

3 4

5

6

7

8

9

1011

12

13

12112

12612

13112

13612

14112

14612

15112

15612

16112

16612

Dec-15 Apr-16 Aug-16 Dec-16

Rp

High NPL ratio in 2016F but should taper off in 2017 and 2018

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA, PY

BUY

Last Traded Price ( 9 Dec 2016): Rp3,370 (JCI : 5,308.10) Price Target 12-mth: Rp4,300 (28% upside) (Prev Rp4,700) Potential Catalyst: Deliveries of transformation programme Where we differ: We are among the few bullish brokers on Danamon’s turnaround story, more visibility expected in FY17F Analyst Sue Lin LIM +65 8332 6843 [email protected] Benedictus Agung SWANDONO +6221 3003 4935 [email protected]

What’s New Remains our conviction pick for a turnaround story More deliveries in 2017 as retail and SME

businesses accelerate while micro business revamps

Double-digit ROEs over time as new business engines ramp up

Maintain BUY; TP lowered to Rp4,300 after imputing higher risk-free rate following expected higher government bond yields ahead

Price Relative

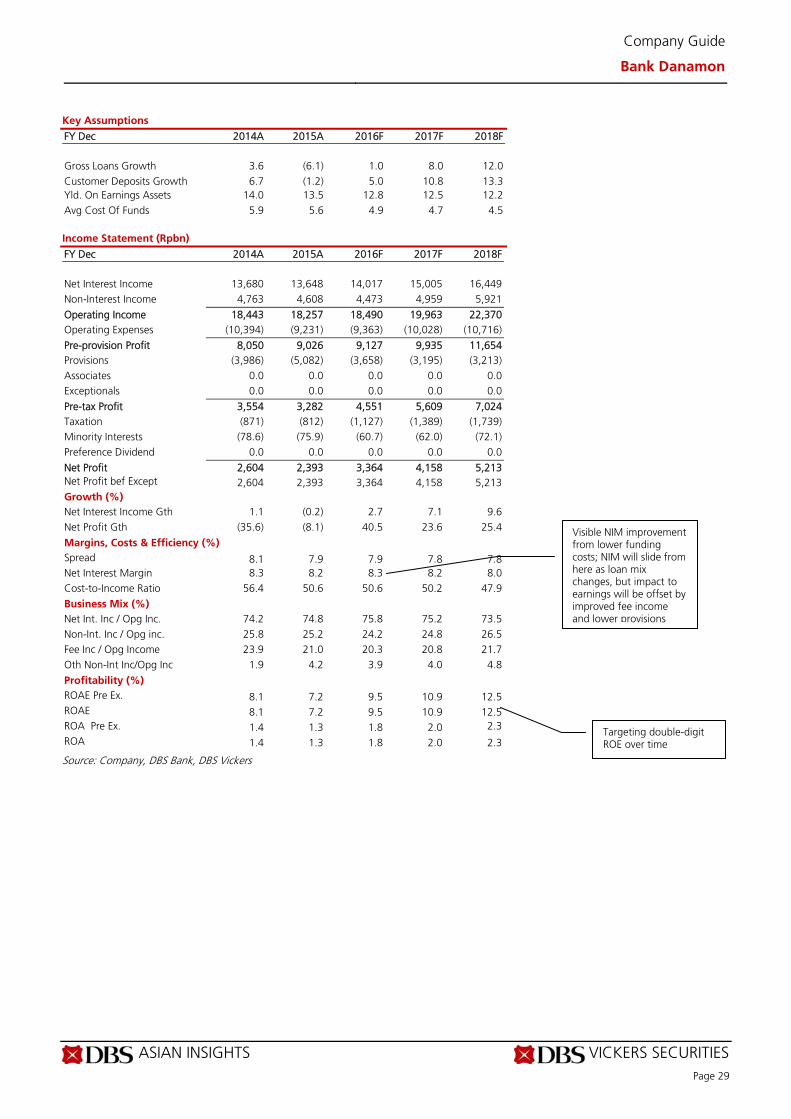

Forecasts and Valuation FY Dec (Rpbn) 2015A 2016F 2017F 2018F Pre-prov. Profit 9,026 9,127 9,935 11,654 Net Profit 2,393 3,364 4,158 5,213 Net Pft (Pre Ex.) 2,393 3,364 4,158 5,213 Net Pft Gth (Pre-ex) (%) (8.1) 40.5 23.6 25.4 EPS (Rp) 251 352 436 546 EPS Pre Ex. (Rp) 251 352 436 546 EPS Gth Pre Ex (%) (8) 41 24 25 Diluted EPS (Rp) 251 352 436 546 PE Pre Ex. (X) 13.4 9.6 7.7 6.2 Net DPS (Rp) 81.9 75.2 106 131 Div Yield (%) 2.4 2.2 3.1 3.9 ROAE Pre Ex. (%) 7.2 9.5 10.9 12.5 ROAE (%) 7.2 9.5 10.9 12.5 ROA (%) 1.3 1.8 2.0 2.3 BV Per Share (Rp) 3,556 3,849 4,179 4,595 P/Book Value (x) 0.9 0.9 0.8 0.7 Earnings Rev (%): 0 (1) 0 Consensus EPS (Rp): 331 376 433 Other Broker Recs: B: 5 S: 6 H: 10

Source of all data on this page: Company, DBS Bank, DBS Vickers, Bloomberg Finance L.P.

Transformation on track

Remains our conviction pick for a turnaround story; reiterate BUY. Bank Danamon (BDMN) remains a BUY and our conviction pick for a turnaround story. The successes of its transformation process are starting to bear fruit. Visible deliveries include lower funding costs and lower expenses. The bank is also now on a leaner scale. Expect more deliveries in FY17 with retail and SME businesses accelerating their pace, Adira turning around and the rationalisation of its micro business. Amid recent funds outflow from Indonesia, BDMN was not spared. BDMN is currently trading below book, significantly discounting deliveries of its transformation programme, in our view. Double-digit ROEs over time. Management’s target is to achieve double-digit ROEs over time. And that can only be possible once the current engines are revived and new revenue engines start to fire up. With the lower-cost base and a cleaner balance sheet, we expect ROEs to improve closer to the 10% mark by end-FY16F as loan growth starts to pick up and funding costs head lower. We have tweaked our FY17-18F forecasts for slower loan growth but higher fee income as its business mix shifts. We remain bullish on FY16-17F earnings; our forecasts remain above consensus. Capital management plans are on the cards. Key milestones to watch in 2017. In the coming year, we will be on the lookout for loan growth resumption and a revamp of its micro business. Loan growth is expected to be driven by auto, SME and Commercial banking while micro loans might still continue to slip as rationalisation of its micro business will be a feature in 1H17. Management is in the midst of reviewing its entire micro business model. There will be further clarity once a detailed strategy is outlined. Watch this space. Valuation: We have a BUY on BDMN with a lower target price of Rp4,300 as we impute higher risk-free rate of 8.5% (from 7.2%) following expected higher government bond yields. Our TP is based on the Gordon Growth Model (14% ROE, 10% growth and 13.9% cost of equity) implying 1.0x FY17 BV. Key Risks to Our View:

Ineffective transformation deliveries. Slower-than-expected changes to business processes could derail the turnaround story in 2016. Failure to improve the deposit franchise could pressure NIM, while loan-to-deposit ratio will remain high and could lead to liquidity risk. At A Glance Issued Capital (m shrs) 9,585 Mkt. Cap (Rpbn/US$m) 32,300 / 2,431 Major Shareholders (%) Asia Financial (Indonesia) Pte. Ltd (%) 68.9 Morgan Stanley Sec 5.0

Free Float (%) 26.1 3m Avg. Daily Val (US$m) 0.48 ICB Industry : Financials / Banks

DBS Group Research . Equity 13 Dec 2016

Indonesia Company Guide

Bank Danamon Version 7 | Bloomberg: BDMN IJ | Reuters: BDMN.JK Refer to important disclosures at the end of this report

41

61

81

101

121

141

161

181

201

221

2,425.5

2,925.5

3,425.5

3,925.5

4,425.5

4,925.5

5,425.5

5,925.5

6,425.5

6,925.5

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Relative IndexRp

Bank Danamon (LHS) Relative JCI (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 25

Company Guide

Bank Danamon

WHAT’S NEW

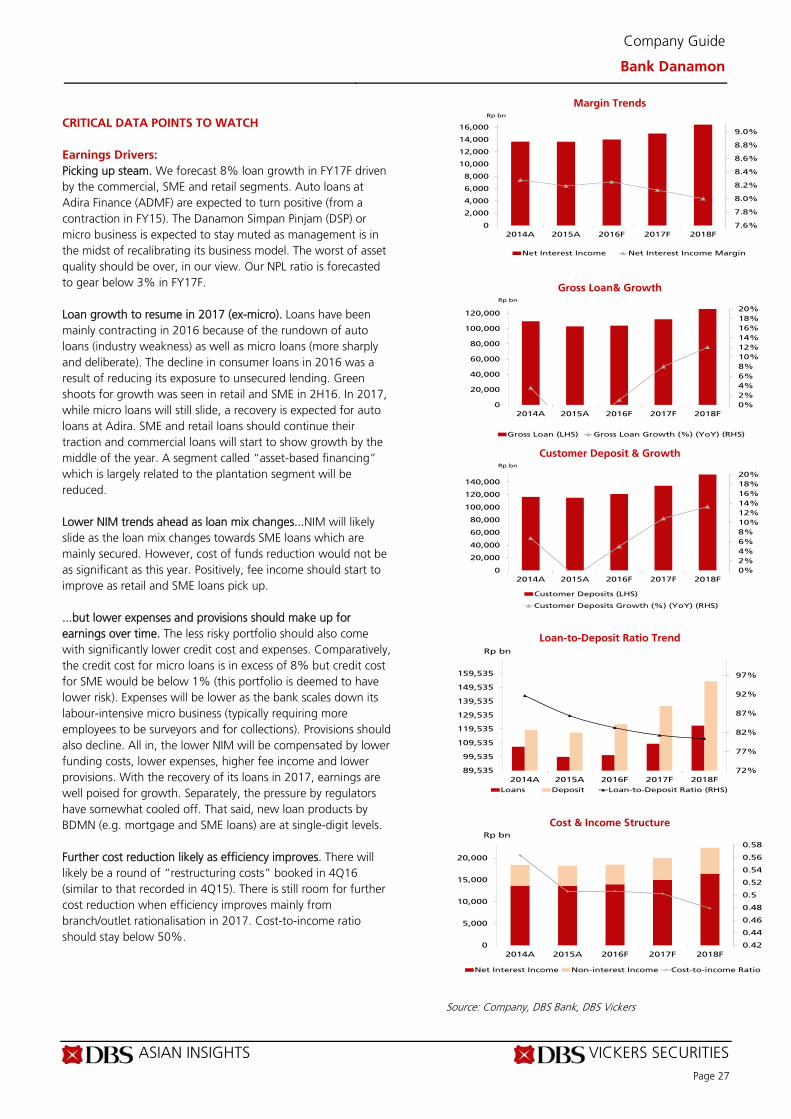

Transformation on track, more deliveries in 2017

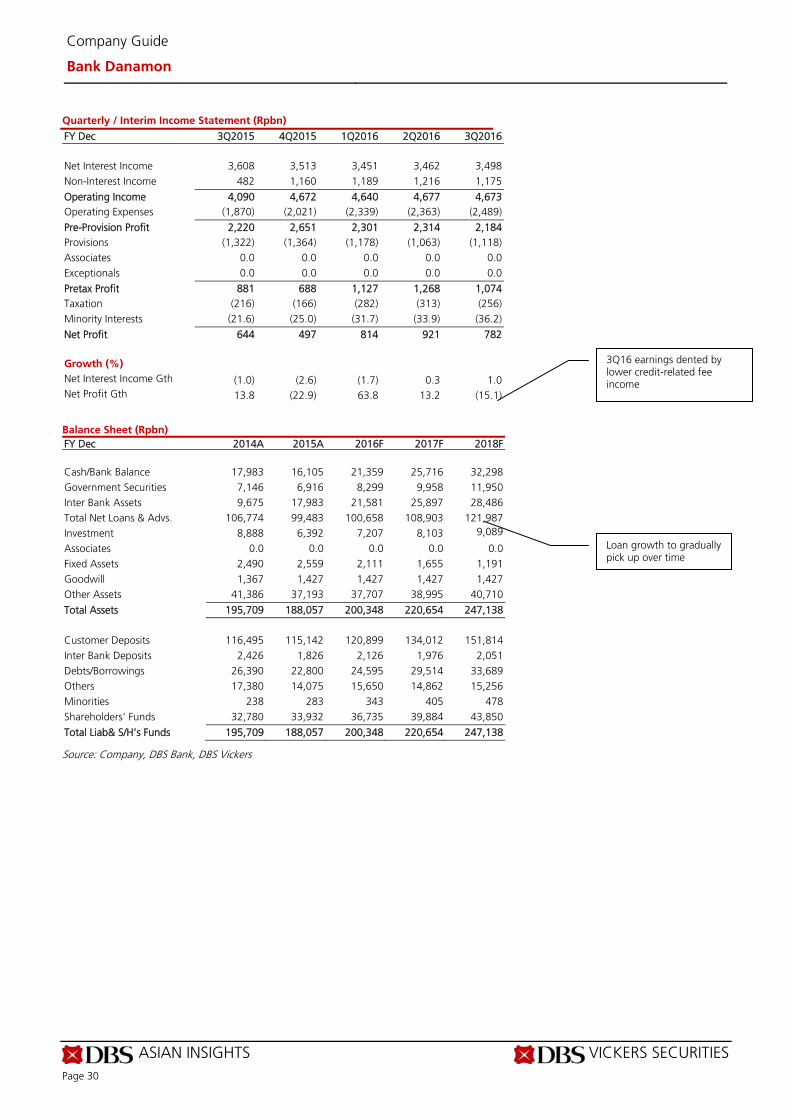

Highlights Moving away from concentrated business; more diversified revenue streams over time. The bank has been reliant on two main engines in the past – Adira (2W and 4W financing) and Danamon Simpan Pinjam (DSP; its micro business). Collectively, these used to contribute 67% of the bank’s books. But after challenges seen in the auto sector since 2014, and changes in the micro lending landscape with the introduction of Kredit Usaha Rakyat (KUR) loans, these two key engines have suffered declines. Positively, Adira is starting to turn around, after a round of restructuring completed; its funding costs have declined quite substantially. Over time, its business model will likely be less dependent on dealers; and alternative distribution channels have been established. Adira is poised to show growth next year as the 4W market recovers, with credit costs well under control. Adira remains an important part of BDMN’s business and is expected to remain so. Separately, its micro business has encountered disruption from KUR; virtually impossible to compete with KUR loan rates. As such, loans from the DSP have been running down. The micro business is still undergoing rationalisation. A clearer picture on its micro business will be made known early next year. New engines revving up: Retail, SME and commercial banking. To compensate for the slowdown in its two engines and to make revenue streams more diversified, the bank is heading towards three other new engines – retail, SME and commercial loans. Retail and SME loans are an important source for low-cost funding (CASA) and cross-sell opportunities to gain fee income traction over time. Both retail and SME loans have showed positive loan growth YTD. The commercial banking segment will be ready for growth by mid-next year. Within the retail space, mortgages have been introduced. While it is a low-NIM business, opportunities for cross-selling are ample. Mortgages are seen as a fee income feeder to the bank (for bancassurance (life insurance products for bancassurance tie-up with Manulife), general insurance (with Adira Insurance), and more importantly CASA (customers are encouraged to leave a balance amounting to 3-6 months of instalment payments in their CASA accounts). The retail business has been remodelled in 1H16 and the results were apparent in 2H16. As for SMEs, 9M16 YTD loan growth has been at 6% with the key success factor being its improved turnaround time from 2-3 weeks to five working days) Successes delivered in 2016. Two key metrics can measure the bank’s success from its transformation programme (approval by the Board in November 2015; implementation from early 2016) this year:

(i) Lower cost of funds (both at bank level and Adira) – the bank has successfully flushed out expensive time deposits and CASA. CASA-to-total deposits have dropped to below 40% but these involve non-promotional CASA rates. Even time deposits are no longer premium priced. At its peak, expensive time deposits formed close to 20% of total deposits. Funding cost at Adira has also declined. The ability to lower costs at the bank level also allows the bank to lend at a lower rate to Adira via joint-financing.

(ii) Lower operating costs – headcount has been on a decline

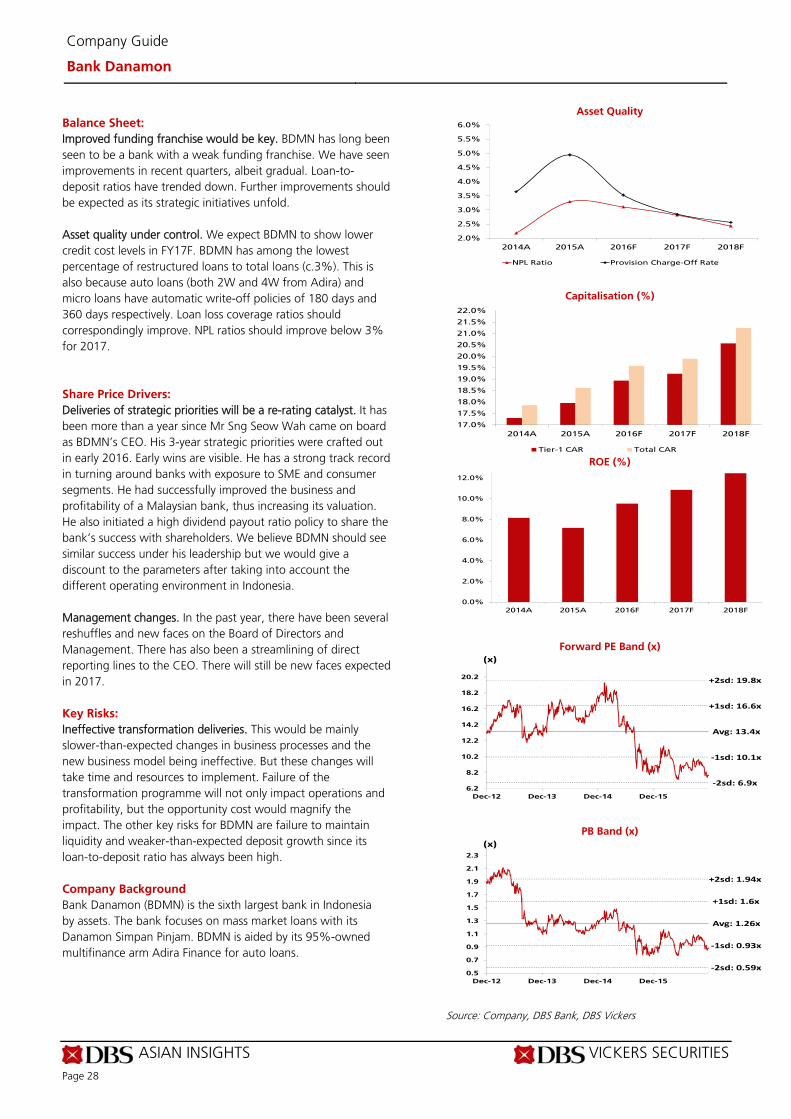

even before the current CEO joined. The bank’s expenses are on a downtrend y-o-y and the there is still room for more costs to be trimmed next year. Branches (and outlets) are also being rationalised where non-profitable ones will be closed down and/or relocated. The branch rationalisation programme forms part of its Sales and Distribution arm of its transformation programme.

Challenges faced. Changes will almost always be faced with challenges. The key challenge is human capital; to find the right fit for the right role. Several new faces have been introduced to the senior management team in the past two years. The bank’s previous Chief Risk Officer now heads and is responsible to manage/restructure/turn around its micro business – watch this space in the next 12-18 months. A new Chief Risk Officer has been appointed with experience in wholesale-commercial as well as retail granular business and micro business. A new IT head has been brought over as well, while a new Chief Credit Officer will soon join the bank. Lower NIM trends ahead as loan mix changes, but lower expenses and provisions should make up for earnings over time. NIM will likely slide as the loan mix changes towards SME loans which are mainly secured (carrying lower lending yields). But this portfolio will also come with significantly lower credit cost and expenses. Comparatively, the credit cost for micro loans is in excess of 8% but credit cost for SME would be below 1% (this portfolio is deemed to have lower risk). Expenses will be lower as the bank scales down its labour-intensive micro business (typically requiring more employees to be surveyors and for collections). Provisions should also decline. All in, the lower NIM will be compensated by lower funding costs, lower expenses, higher fee income and lower provisions. With the recovery of its loans in 2017, earnings are well poised for growth. Separately, the pressure by regulators have somewhat cooled off. That said, the growth of new loan products by BDMN (e.g. mortgage and SME loans) are at single-digit levels. Asset quality under control. More than 80% of Special-Mention Loans are below 30 days and these are deemed habitual. Special mention loans have been flat. Slippages from special-mention loans to NPL have been low. BDMN has among the lowest

ASIAN INSIGHTS VICKERS SECURITIES Page 26

Company Guide

Bank Danamon

percentage of restructured loans-to-total loans (c.3%). This is also because auto loans (both 2W and 4W from Adira) and micro loans have automatic write-off policies of 180 days and 360 days respectively. Most of BDMN’s asset quality issues have been settled. The credit cost figure and NPL ratio looks high because loans (the denominator for both the formulae for credit cost and NPL ratio) have been contracting. Further cost reduction likely as efficiency improves. There will likely be a round of “restructuring costs” booked in 4Q16 (similar to that recorded in 4Q15). There is still room for further cost reduction when efficiency improves mainly from branch/outlet rationalisation in 2017. Cost-to-income ratio should stay below 50%. Next key milestones. In the coming year, we will be on the lookout for loan growth resumption and a revamp of its micro business. (i) Loan growth to resume in 2017 (ex-micro). Loans have