Embed Size (px)

Citation preview

Industrial policy, Structural Change, and Pattern of Industrial

Productivity Growth in Taiwan

Tsu-tan Fu*

Department of Economics & Center for Efficiency and Productivity Research

Soochow University, Taiwan

Hsing-chun Lin

Department of Applied Economics, National Chiayi University, Taiwan

Yih-ming Lin

Department of Applied Economics, National Chiayi University, Taiwan

Wei-sing Kong

Taiwan Research Institute, Taiwan

(Taiwan KLEMS Research Team)

This paper is prepared for the third World KLEMS Conference,

Tokyo, Japan on May 19, 2014.

1

Industrial policy, Structural Change, and Pattern of

Industrial Productivity Growth in Taiwan

Tsu-Tan Fu, Hsing-Chun Lin, Yih-Ming Lin and Wen-Hsin Kong

(Taiwan KLEMS Research Team)

Abstract

The purpose of this study is to investigate the relationship between industrial policy,

structural change and productivity growth of Taiwan at industry level in 1981-2010.

To serve such purpose, we construct the Taiwan KLEMS Database, in which the

economy is divided into 31 industries. Following the methodology developed by

Jorgenson, Gollop and Fraumeni (1987) and Jorgenson, Ho and Stiroh (2005) and

the manual of Asia KLEMS, we decompose the output growth into contributions of

capital, labor and intermediate inputs (energy, materials and services) as well as total

factor productivity. In the last decades, Taiwan’s industrial policy focused on to

support the socalled “hi-tech” industries, such as ICT industry (13 Electrical and

Optical Equipment, Post and communications). The strategies include establishment

of science-based industrial parks, technological support from national research

institute and national plan, providing tax incentives and special support for

developing semiconductor industry, and so on. It is clear that there are significant

structural changes happened in past decades. The industry weights for primary and

secondary decrease over time, whilst the important of tertiary industry increases

during the period of 1981-2010. The industry weights of most other industries in the

Secondary Industry decreased except “Electrical and optical equipment” and “Basic

and fabricated metal”. On the contrary, most industries in Tertiary Industry increased

during 1981-2010. It is shown that the industrial policy is a significant factor to

influence the industrial structural change. It is also found that in several industrial,

such as food products and textile, rubber and plastics, the growth rates of labor input

(measured by total working hour, HEMP) are negative. We also find that the TFP

growth rate of “Electrical and Optical Equipment” industry is the highest in

secondary industries whilst the TFP growth rate of “Post and communications” is the

largest among the tertiary sector, which means the impact of the industrial policy

does not have impact on structural change, but also influences the TFP growth rate.

2

1. Introduction

The purpose of this paper is to investigate the relationship among industrial policy,

structure change and TFP growth pattern at industry level in 1981-2010. To reach this

purpose, we construct the Taiwan KLEMS Database, in which the economy is divided

into 31 industries based on the Asia KLEMS manual. Following the methodology

developed by Jorgenson, Gollop and Fraumeni (1987) and Jorgenson, Ho and Stiroh

(2005) and the manual of Asia KLEMS, we decompose the output growth into

contributions of capital, labor and intermediate inputs (energy, Materials and services)

as well as total factor productivity. We further conduct cross-period and cross-

industry comparisons on the structures of industry output growth and of the factor

contribution in Taiwan.

The empirical results show that the range of industry level growth rate varies

widely by industry and by time period. The results also show the structure of the

factor contribution share to be varied by industry. But, in general, the contribution

share from intermediate inputs dominates that from other inputs (capital and labor) for

most industries in Secondary Sectors. However, such input dominant contribution

effect differs by industry in Tertiary industries. The above mentioned results indicate

the importance of growth decomposition analysis at industry level.

We find that Capital is the main driver to value added (VA) output growth and

Intermediate input is the main driver to gross output (GO) growth. Among those

intermediates inputs, we find that the contribution share from Materials input (ConM)

outweighs those from other inputs (capital and labor) for most industries in Secondary

Sectors. We also find that the contribution share of Services input (ConS) plays

dominant role to the GO growth for most industries in Tertiary Sector. Furthermore,

our cross period comparison results indicate that the role of contribution shares of K

and II decreased over time, instead the contribution from TFP increased over time. At

last, Tertiary industries were having higher growth rate as well as higher TFP than

those secondary industries for the last 3 decades in Taiwan.

The structure of this paper is outlined as the following. We first give brief Taiwan

industrial development and related policies in section 2. In section 3, we will

introduce the methodology used with some descriptions on data and variables

employed. In section 4, the structure of Taiwanese industry based on industry weight

3

and growth rate are analyzed. Empirical cross-industry and cross-period comparisons

on the sources of output growth analyses will be conducted in Section 5. The paper

will be ended with the concluding remarks.

2. The Main Taiwan Industrial Development Strategies

Taiwan has experienced remarkable economic growth since the 1960s. In the 1960s,

the focus industries are the light industries, in which the government policy is

development of light industries for import substitution with its average high annual

GDP growth rate over 10.2%, which is called the “import substitution” stage. In the

1970’s, heavy and chemical industries grew rapidly due to the government’s export

promotion policy, which is called the “export expansion” stage. With the cheap

production costs and the availability of high quality labor force prior to the 1980s,

Taiwan’s policy of export expansion had been successfully pursued. The annual GDP

growth rates reached 9.27 on average during the period 1971 to 1980, as shown in

Figure 1.

Since 1980, Taiwan has been bumped into considerable challenges. In political

terms, Taiwan become a truly democratic society with the appearance of a powerful

opposition party, which make Taiwanese society become more diversified. In

economic arena, the appreciation of the New Taiwan dollars (NT$) which make the

exchange rate form 40NT$/US$ to 25 NT$/US$. The upward trend in the valuation of

the NT$ cause the inflation and asset bubbles. The stock market and real estate market

began to fluctuate. Furthermore, the low cost labor had gradually been exhausted. The

wages in Taiwan are gradually increasing. A number of labor intensive industries had

already lost their comparative advantage. In order to survive, manufacturers were

forced to move their production bases to Southeast Asia or to mainland China.

Economic liberalization and Internationalization

In the early 1980s, in order to solve the increasing trade disputes due to the

economic imbalance, the Taiwan government implements the policy of economic

liberalization, which including trade liberalization, the lifting of foreign exchange rate

control and the deregulation of financial sector. In 1991, the government approved 15

new private commercial banks establishment whist several new private banks were

established through the reorganization of trust companies and credit cooperatives.

4

There was a rapid increase in the number of commercial banks in Taiwan.

Furthermore, some new business of banks, such as commercial papers and short term

certificate, are permitted to engage.

On the other hand, since the labor cost and land cost gradually rise, a large amount

manufacturers which lost their competitiveness in the “traditional” manufacturing

industries moved oversea from the late 1980s. These manufacturers started to invest

in Mainland China and Southeast Asian countries, such as Vietnam, Indonesia,

Thailand, Philippines, Malaysia etc. The industries move their production oversea

includes paper and plastics, basic metals, textile products, garments, fur and leather

goods, wood and bamboo products, rubber products and other labor intensive

industries. The increase in oversea investment makes the structure change in Taiwan

economic development. The manufacturing sectors kept decreasing and the service

sectors kept increasing.

ITRI and the technical support of the NSTP

In order to maintain continued growth, the government’s industrial policy turned

toward a greater emphasis on the upgrading of the industrial technology, which makes

the capital and technology intensive industries replace the more labor intensive

industries. The Industrial Technology Research Institute (ITRI) is founded and

sponsored by Taiwanese government, which is a nonprofit R&D organization

engaging in applied research and technical services. ITRI’s main tasks are the

undertaking of industry-research technology and product R&D, along with the

diffusion of the results of their work among private manufacturers. In addition, ITRI

also provides technical supports and services for small and medium enterprises

(SMEs). With the support by the National Science and Technology Project (NSTP),

the ITRI gradually grew stronger and bigger.

The main objective of NSTP is to encourage industry to undertake R&D work. The

NSTPs promote the development of ICT industries, promote the upgrading of

traditional industries (modernization and automation), establish the basic

infrastructure for industrial development, improve efficient use of resources and solve

common problems shared by industries. ITRI and NSTPs carry out R&D work and

transfer the results to the private manufacturers, which made a significant, impressive

5

contribution to industrial upgrading. By disseminating both technology and talent,

ITRI has played a vital role in transforming Taiwan’s economy from a labor-intensive

industry to a high-tech industry. Numerous well-known, high-tech companies in

Taiwan, such as leaders in the semiconductor industry TSMC and UMC, can trace

their origins to ITRI.

The Establishment of the HSIP

Since the first oil crisis happened, the government realized that Taiwan’s industrial

development was based on a labor-intensive structure. Taiwan government understood

that it is necessary to pursue a policy of development hi-tech, high value-added

industries. In order to attract investment from foreign hi-tech manufacturers, the

government realized that government had to construct an appreciate, attractive

investment environment. Therefore, the Hsin-Chu Science-based Industrial Park

(HSIP) was founded for high-tech industries (ICT). The HSIP was established

similarly to those in Silicon Valley in California. No one can doubt the contribution of

the HSIP for Taiwan economic development. This Park had a major impact on

stimulating development of ICT industries. Firms located within the HSIP can enjoy

tax incentives and tariff exemptions and deductions, which is the main factor to attract

companies to invest within the Park. In addition, HSIP helped in the diffusion of

technology by encouraging manufacturers to recognize and reap the benefits of

congregating together. HSIP has become the main center of development of Taiwan

ICT industries. In 1997, there were 245 companies located in the Park, employing a

otal of 68410 workers. The total business revenue made by the Park is up to 13.9

billions US$, which account for 5% of total GDP.

The policy for subsidizing research and development (R&D) and sponsoring

cooperative research has helped to heighten the rapid technological progress in

high-tech industries, which grew quickly in the 1980s, and become the dominant

industry in the 1990s.

Tax incentives under the Statute of Upgrading Industries

In the mid-1980s, with the appreciation of the NT$, the labor and land cost begin to

rise gradually, which makes the labor-intensive industries loss their competitiveness.

It is necessary to accelerate the process of industrial upgrading, improve products

6

value-added, seek out competitiveness. At the end of 1980s, the “Statute of Upgrading

Industries” was passed and implemented on 1 January, 1991.The main content of the

statute is the provisions for tax incentives (tax credits, tax exemptions and tax

deferrals) to encourage manufacturers to undertake R&D work, implement

automations, and promote the development of ICT industries so as to strengthen

manufacturers competitive advantage.

Promotion of the Semiconductor industry

In 1976, 37 young engineers were dispatched to the US and to undergo training.

These young engineers not only bring technology, but also establish a Complementary

Metal Oxide on Silicon (CMOS) plant in ITRI laboratories. The government invested

in excess of NT$400 millions in the development of semiconductor industry and

signed various agreements with various foreign semiconductor manufacturers, such as

RCA for technology transfer and personal training at late 1970s. In addition, the

government also directed plans to bring together of private sector capital and transfer

technology to private companies. During the 1980s, the government directed the

establishment of United Microelectronic Corporation (UMC) and Taiwan

Semiconductor Manufacturing Company (TSMC). A number of small design

companies began to establish in HSIP. With the government’s investment in

semiconductor industry and the establishment of UMC and TSMC, not only was

production process technology being continuously improved, but various other

semiconductor related technologies were also innovated, including circuit design,

mask production, packaging and testing, and so on.

Taiwan’s economic growth slowed down in the late 1990s and become sluggish in

2000s as a result of a sequence of negative impacts such as the Asian financial crisis

in 1997, worldwide economic recession in 2000, the financial tsunami in 2008, and

the financial debt crisis in Europe in 2011. Up to date, the focus industries in Taiwan

include Information and Communications, Electronics and Optoelectronics, Material,

Chemical and Nanotechnology, Medical Device and Biomedical, Mechanical and

Systems, Green Energy and Environment.

7

Figure 1: An overview of Taiwan’s Industrial Development

3. Methodology

3.1 Growth and Productivity Accounts

We follow the growth accounting methodology provided by the Asia KLEMS

manual (2012) which was developed by Dale Jorgenson and associates as outlined in

Jorgenson, Gollop and Fraumeni (1987) and more recently in Jorgenson, Ho and

Stiroh (2005). It is assumed that industry gross output is a function of capital, labor,

intermediate inputs and technology. Following the notation of Asia KLEMS manual

(2012), the production functions are assumed to be separable in these inputs,

( ) ( , , , )j j ij j j j jY g Y f K L X T

where Y is output, K is an index of capital service flow, L is an index of labor service

flows and X is an index of intermediate inputs, which consists of the intermediate

inputs purchased from the other domestic industries and imported products.

Intermediate inputs (X) include energy (E), materials (M) and services (S) inputs in

this model. Under the assumptions of constant returns to scale and competitive

markets, the value of output is equal to the value of all inputs:

Y k L X

j j j j j j j jP Y P K P L P X

where Y

jP denotes the price of output, X

jP denotes the price of intermediate inputs,

K

jP denotes the price of capital services and L

jP denotes the price of labor services.

2000's Knowledge-Intensive Manufacturing and Service Industry

ICT Growth slow down 3.76%

1980-1990's High-Tech IndustryICT Rapid Growth 7.37%

1970's Heavy and Chemical IndustryExport Expansion 9.27%

1960's Light industryImport Substition Average GDP Growth rate 10.2%

8

The value share of each input is defined as follows:

;jt

Y

jt

jt

X

jtX

jtYP

XPv ;

jt

Y

jt

jt

L

jtL

jtYP

LPv

jt

Y

jt

jt

K

jtK

jtYP

KPv

The assumption of constant returns to scale implies 1 K

jt

L

jt

X

jt vvv .

The standard growth accounting decomposition of output growth into the

contribution of each input and TFP (denoted by YA ) can be expressed as:

Y

jtjt

L

jtjt

K

jtjt

X

jtjt ALvKvXvY lnlnlnlnln

where the contribution of each input is defined as the product of the input’s growth

rate and its two period average revenue share.

3.2 Taiwan KLEMS Database

We construct the Taiwan KLEMS Database following the Asia KLEMS manual, in

which the economy is divided into 31 industries. (the 32th sector, the

“EXTRA-TERRITORIAL ORGANIZATIONS AND BODIES” in Asia KLEMS manual,

is not available) The data resources are based on the data published by the Directorate

General of Budget, Accounting and Statistics, Taiwan (DGBAS) for the period

1981-2010. For the output data (Gross output and Value added), we utilize the

National Income Survey data (93 SNA) and convert 65 sectors into 31 sectors.

Since the capital data is still under constructing, we employ the capital stock as the

capital service in this paper. Capital stock data is also published by DGBAS. We

convert capital data (16 sectors available after 2001 and 11 sectors available before

2001) into the capital stock in format of 31 sectors. Labor data include labor

compensation and working hour data. We employed the raw survey data from

Manpower data, which is conducted in May since 1977. There are about 60,000

observations in this survey every year. Compiled manpower data with Employees’

Earnings Survey, we can obtain labor compensation and working hour data.

Intermediate Inputs (II) include energy(E), materials(M) and services(S). The data

from Intermediate Input of national income and divide all sectors into three sectors.

We use the Input-output table to get the inputs of E, M, S for each sector. Following

the methodology developed by Jorgenson, Gollop and Fraumeni (1987) and

9

Jorgenson, Ho and Stiroh (2005), we decompose the output growth into contributions

of capital, labor and intermediate inputs (energy, materials and services) as well as

total factor productivity.

4. Economic Performance of Taiwan: 1981-2010

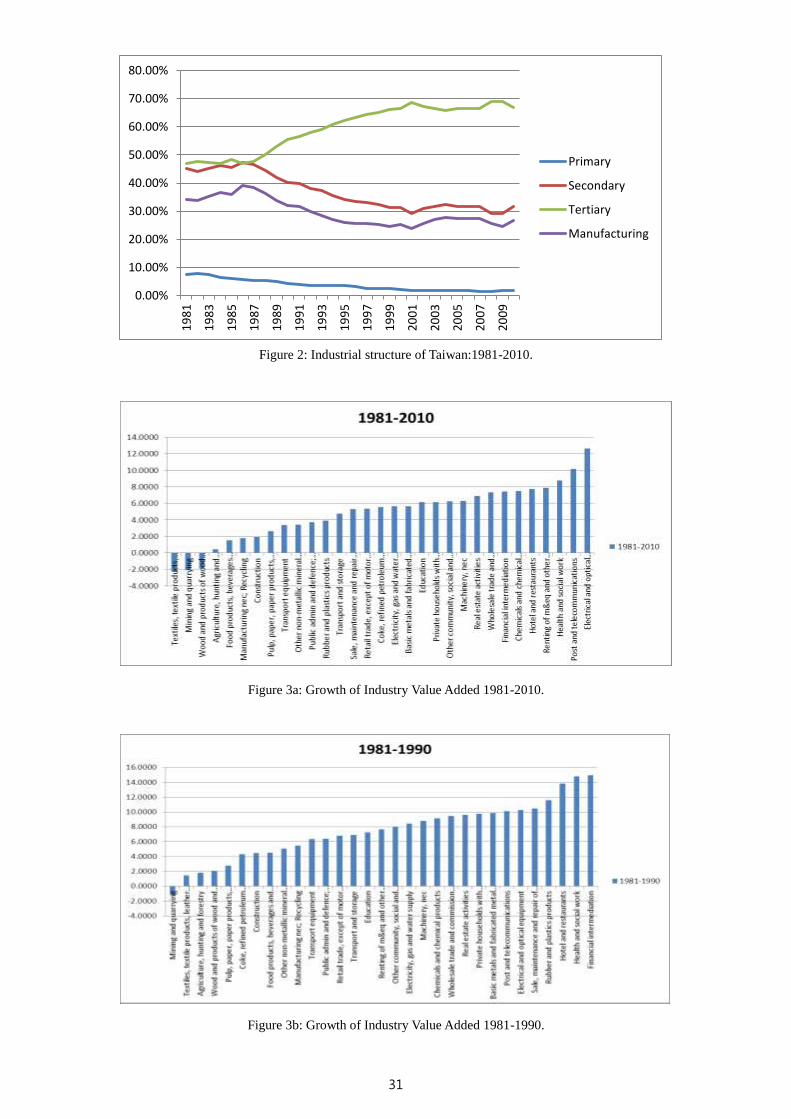

4.1 Industry structure in Taiwan

Value added weights at industry level:

The industry weights for primary and secondary decrease over time, the important

of tertiary industry increases during the period of 1981-2010, as shown in Table 1 and

Figure 2. Table 1 also indicates that the industry weights of primary, secondary and

tertiary industries are 1.73%, 30.99% and 67.27% in 2001-2010, respectively.

As for value added weights for 31 sectors, Table 2 shows the level and some

changes in industry weight in the last 3 decades. In 1981, we find that “ 3.Food

products, beverages and tobacco”, “4.Textiles, textile products, leather..”,

“13.Electrical and optical equipment”, “17.Construction” are important industries in

the Secondary Industry, whereas “27.Public admin and defense..”, “19.Wholesale

trade and commission trade”, “20.Retail trade..” and “25.Real estate activities” are

industries with high weight in the Tertiary Industry. However, Table 2 shows that that

except “13.Electrical and optical equipment” and “11.Basic and fabricated metal”, the

industry weights of most other industries in the Secondary Industry decreased over

time. On the contrary, Table 2 also shows industry weights of most of industries in the

Tertiary Industry to be increased over time. As a result, we can find that in 2010

industries such as “13.Electrical and Optical equipment”, “11.Basic and fabricated

metal products”, and “8.Chemicals and chemical products” in the Secondary Industry,

as well as “19.Wholesale trade and commission trade”, “25.Real estate activities”,

“27.Public admin and Defense.”, “20.Retail trade..” and 24.Financial intermediation”

in the Tertiary Industry, are sectors with relatively high weight.

4.2 Industrial Value Added and Output Growth by sub-period

Value Added Growth at Industry Level

10

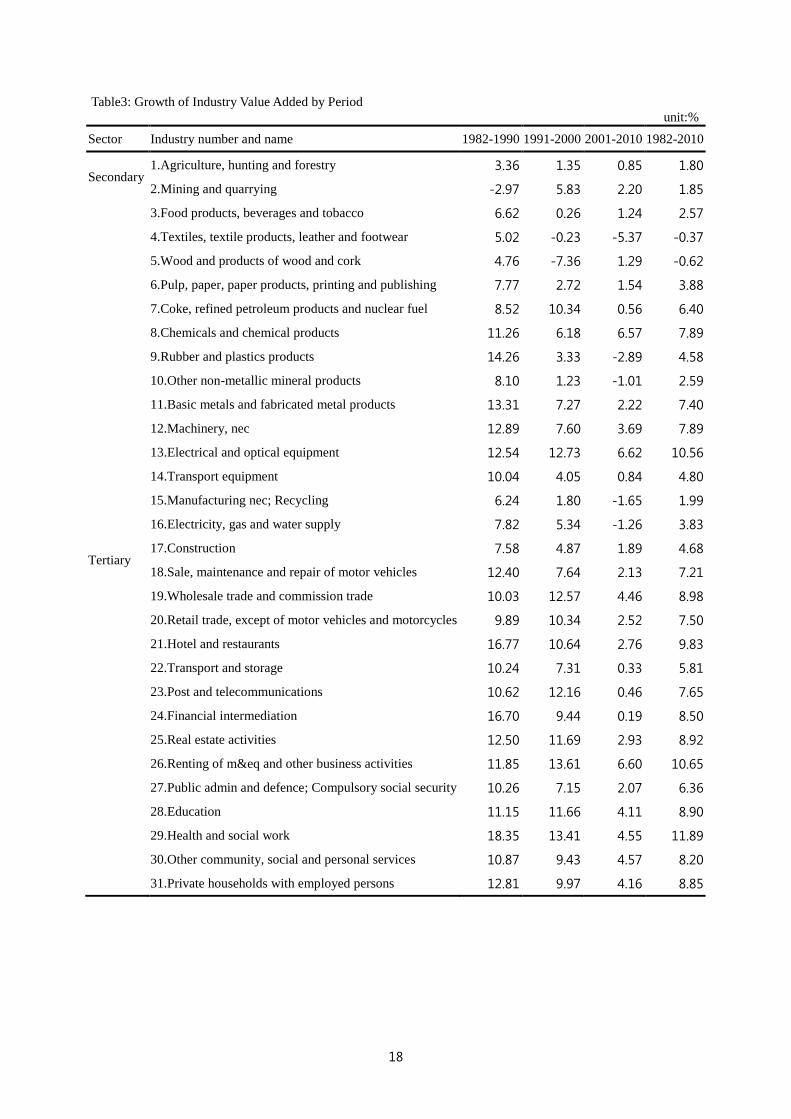

Table 3 presents the growth of industry value added for the last 3 decades. The

average growth rate in 1981-90 was 7.46%, but it decreased substantially in the later 2

decades. Among 31 sub-industries, we also find in Table 3 and Figure 3a that

“13.Electrical and optical equipment” and “8.Chemicals and chemical products” in

the Secondary Industry, as well as “23.Post and telecommunications”, “29.Health and

Social work”, “26.Renting of m&eq ..”, “19.Wholesale trade..”, and “Hotel and

restaurants” in Tertiary Industry, are sub-industries with annual growth rate higher

than 7%. Cross period comparisons on the annual growth rate at industry level can

also be seen in Figures 3b-3d. It is also noticed that growth rate for 31 industries

ranged from 15.76% (Industry#23) to -5.86% (industry#5) and varied by sub-period,

which implies the importance of analysis at industry level.

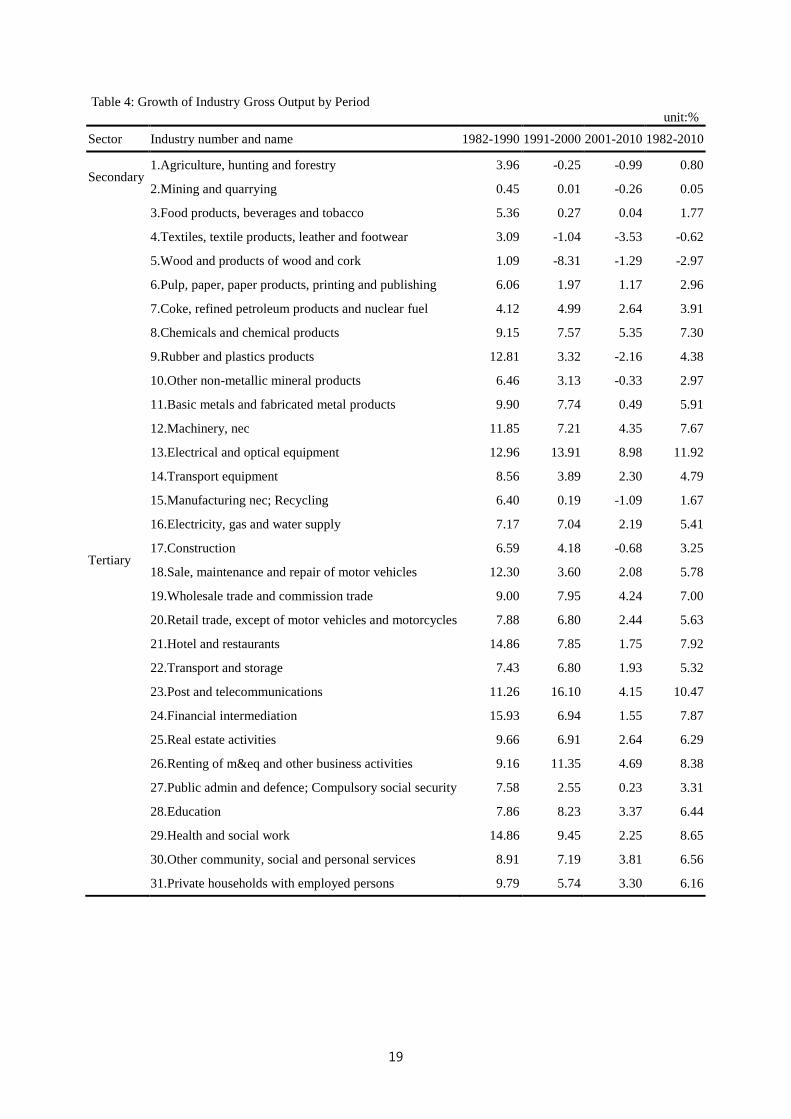

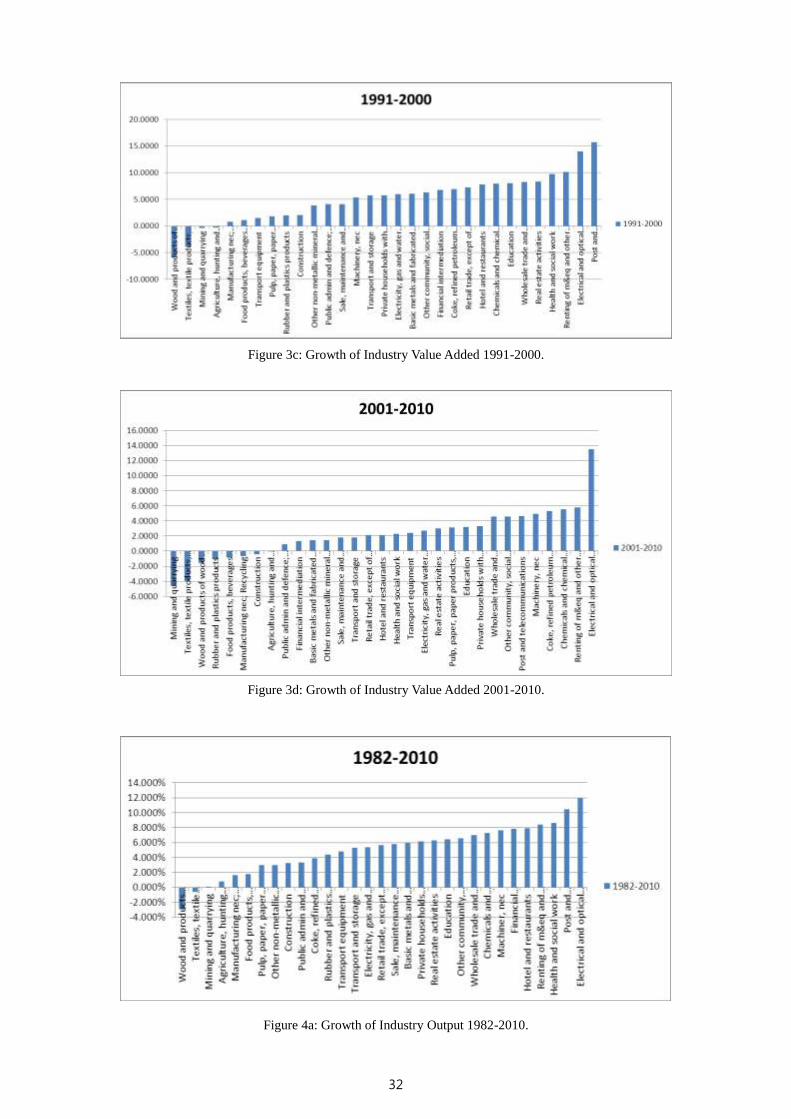

Output Growth at Industry Level

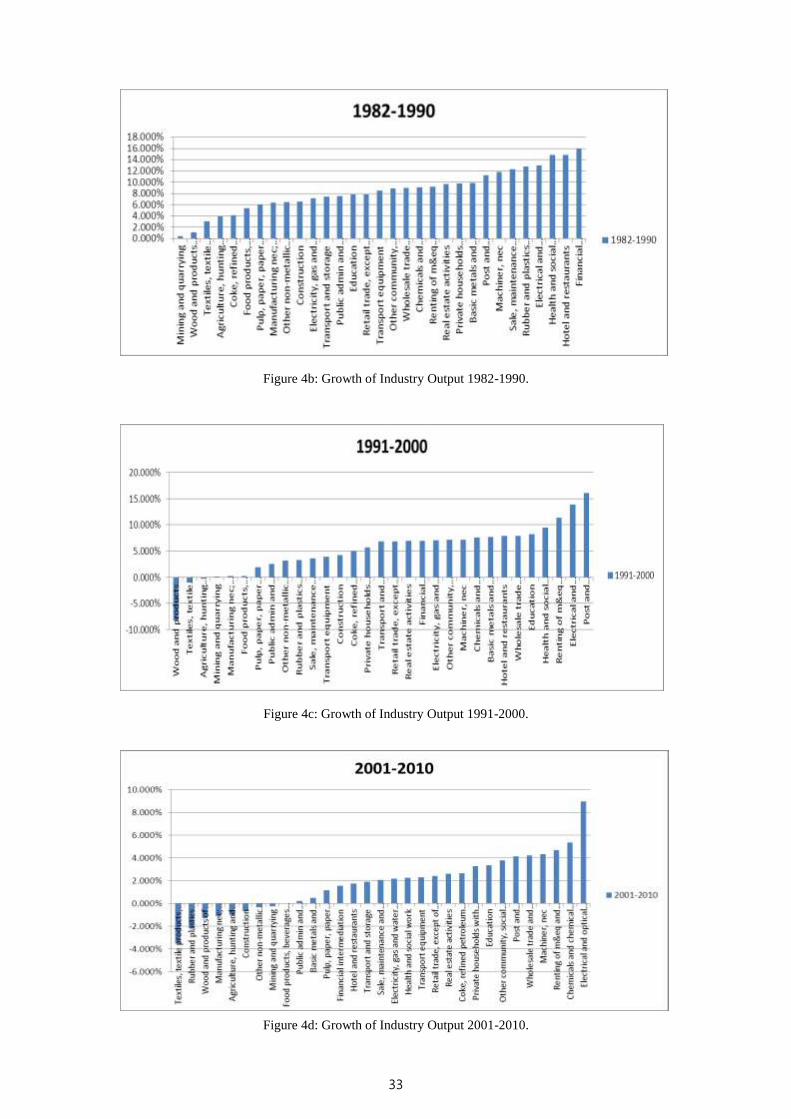

Output growth is defined to be the addition of value added and intermediate inputs.

Table 4 presents the growth of industry output for the 3 decades. Despite growth

rates in growth output are different from those in value added, however by comparing

Figures 3a and 4a, one can see that the growth rate ranks of 31 industries in gross

output (Figure 4a) and in value added (Figure 3a) are quite similar. Cross period

comparison of growth rate in industry output, Figures 3b-3d, also indicates vast

differences between industries and sub-periods.

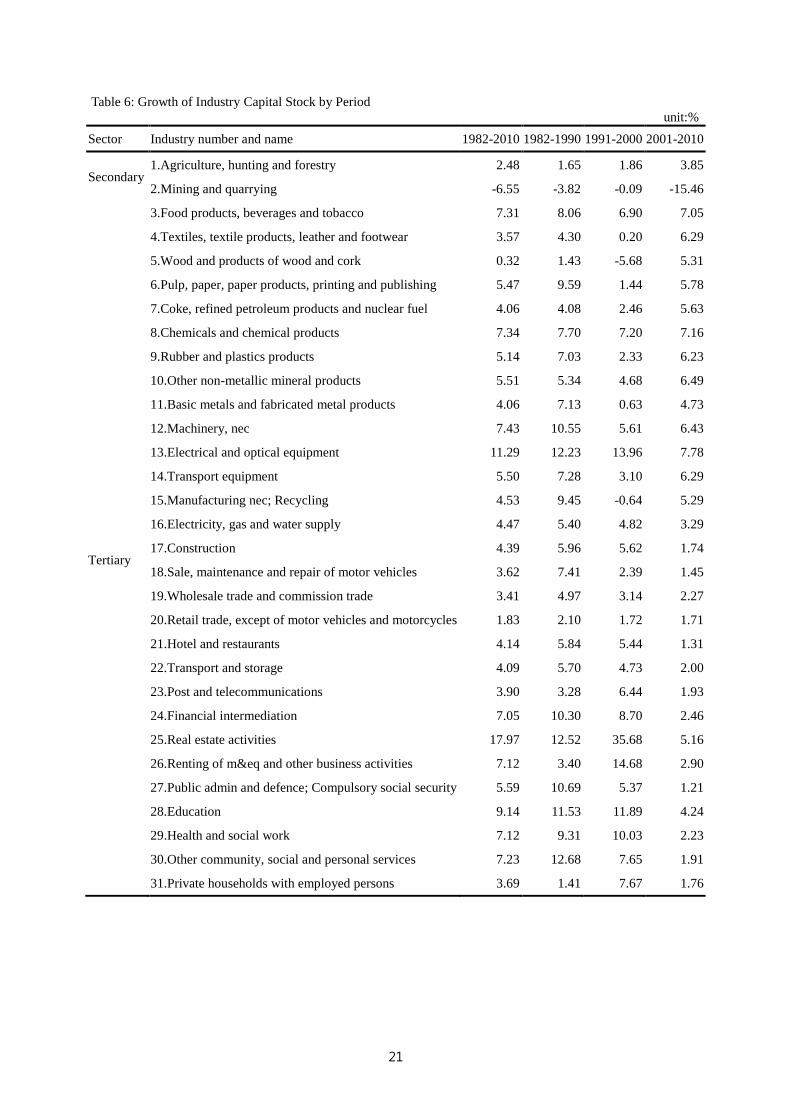

4.3 Input growth at industry level by period

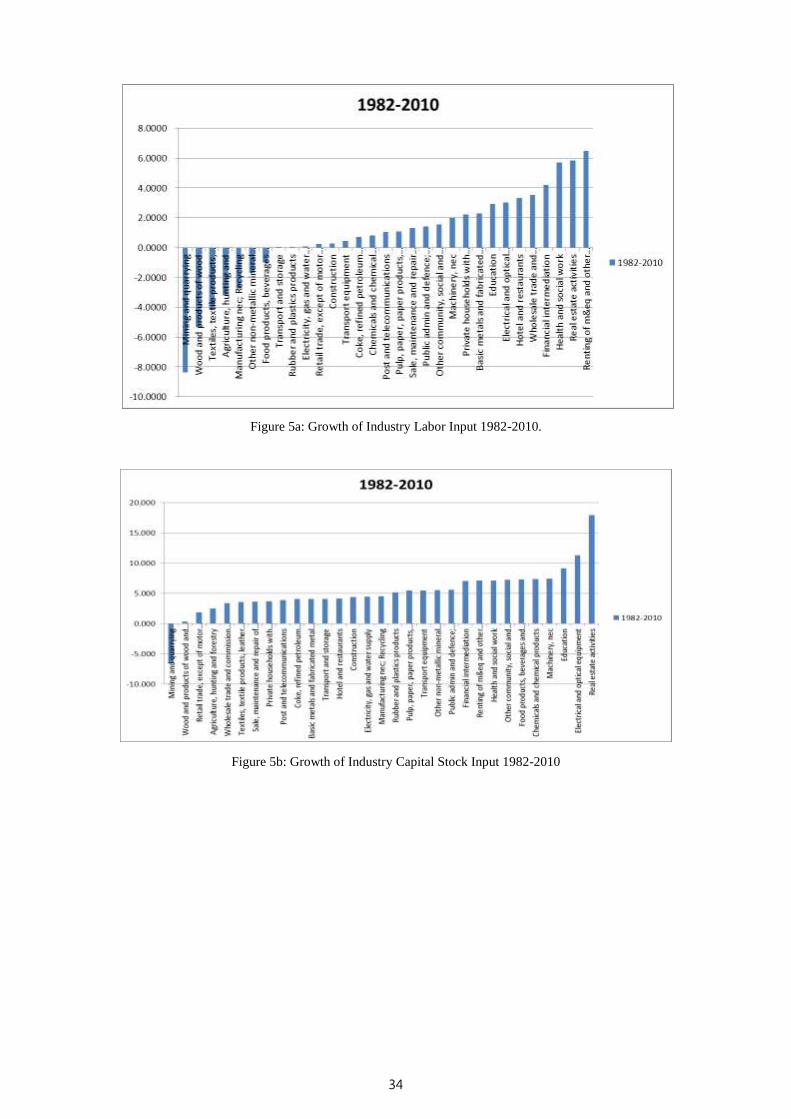

Regular inputs used for production include labor, capital and intermediate inputs

(energy, materials, and services). Table 5 shows the growth of labor input at industry

level by period whilst Table 6 shows the growth of capital stock at industry level by

period. Similar growth of other inputs can be generated from Taiwan KLEMS

database. In Figures 5a-5e, we show the growth of labor, capital, energy, materials

and service at industry level in 1981-2012. In general, we find all inputs have

positive growth for most industries in the sample period. But, we also find that growth

rates vary substantially by industry for all inputs.

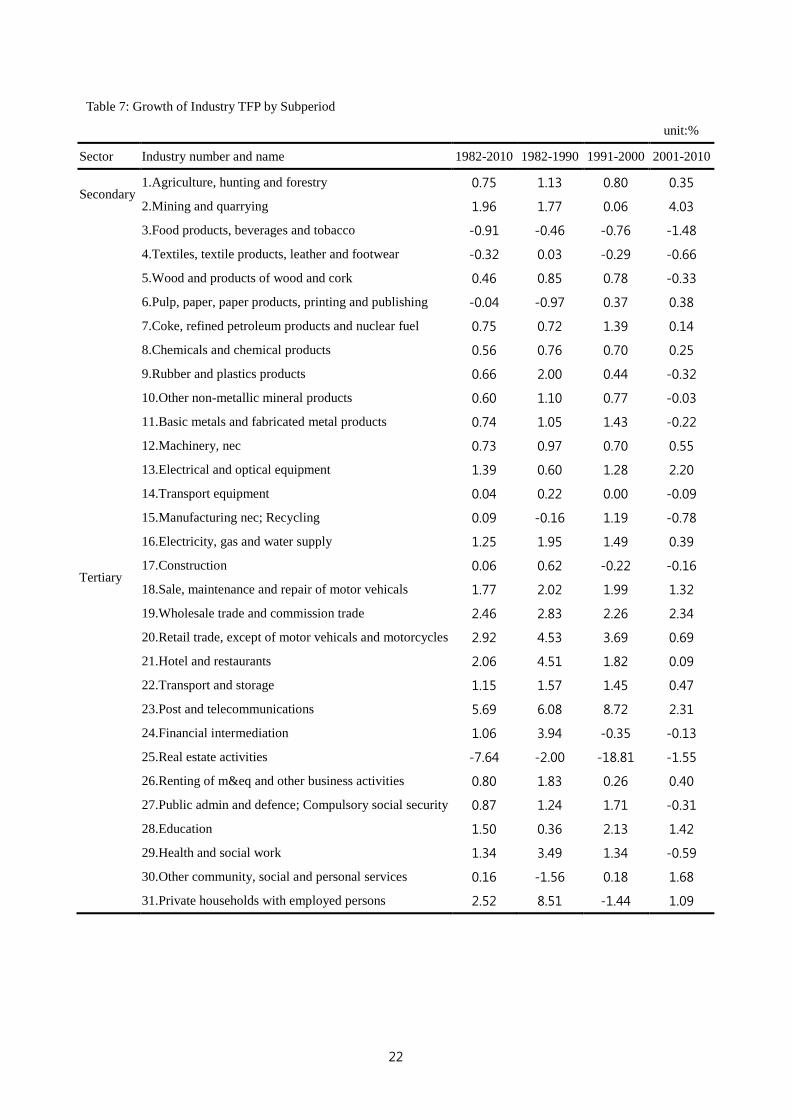

4.4 The TFP Growth at Industry level

Table 7 presents the TFP growth rate by industry in the last 3 decades. As in the

11

standard growth accounting practice, the TFP is defined as the residual contribution

which is unexplained by factor inputs. The resulted TFP growth for each industry can

be found in Table 7 and Figure 6a-6d. It is shown that the figures of TFP growth in

secondary industry are relative lower than the figures in tertiary industry. The TFP

growth rate of “Electrical and Optical Equipment” industry is the highest among

secondary industries whilst the TFP growth rate of “Post and communications” is the

largest among the tertiary sector, which means the impact of the industrial policy does

not have impact on structural change, but also influences the TFP growth rate.

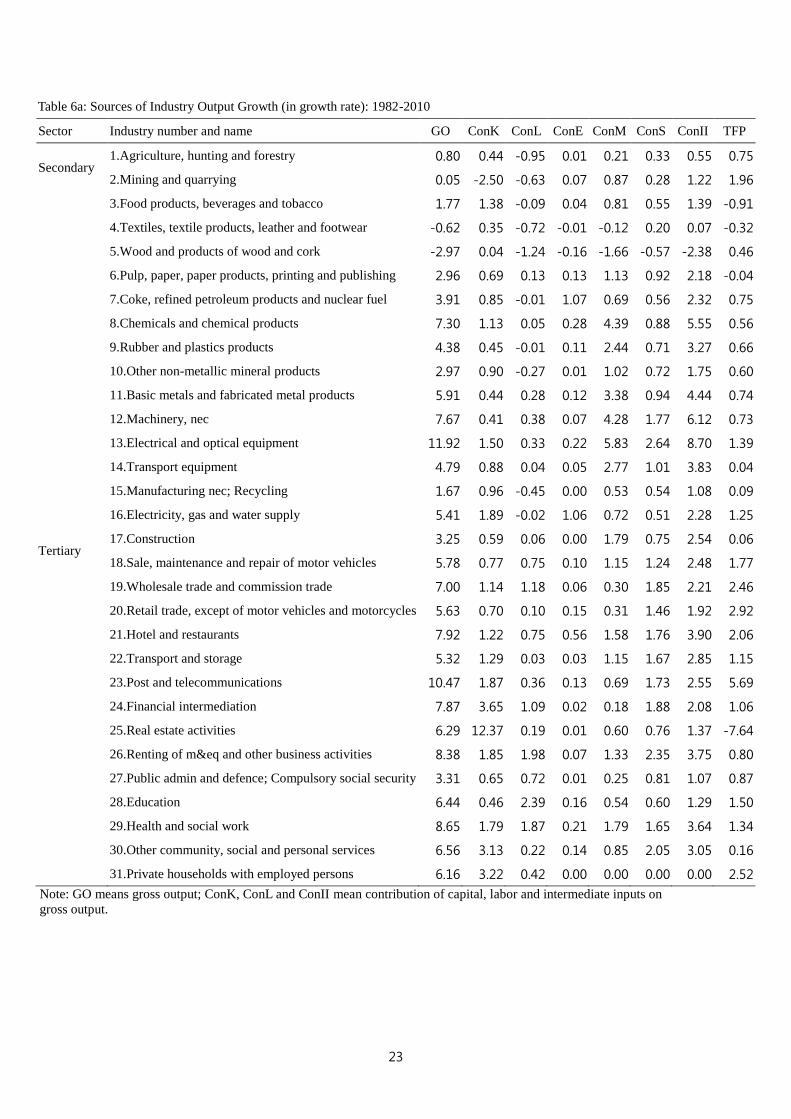

5. Sources of Gross Output Growth at Industry Level

5.1 Sources of Industry output for the whole sample period (1981-2010)

The standard growth accounting decomposes gross output (GO) growth into the

contribution of each input and TFP. That is, growth rate of GO can be decomposed

into contributions of K, L, II and TFP on GO growth. While Table 8a presents results

of such decomposition for 31 industries in 1982-2010, Table 8b presents such

contribution decomposition in percentage share for each input. Such output growth

decomposition for the whole economy can be further shown in Figure 5a and Figure

5b). Despite results of such decomposition vary by period, in general, we still can

easily see that the contribution from intermediate inputs (II) (sum of energy (E),

materials (M) and services (S)) dominates the growth, which is followed by

contribution from Capital (K), then Labor (L), and finally TFP.

The average contribution share of inputs for the whole economy, see Figures 5a and

5b, show that the contribution share of II seems to be larger in early decade

(1982-1990) than in later decades (1991-2000, 2001-2010). On the contrary,

contribution share from K (ConK) became increase over time. Such results seem

consistent with the change of industrial structure in Taiwan, of which the size of the

secondary (manufacturing) sector with relative high contribution share in II has been

reduced over time.

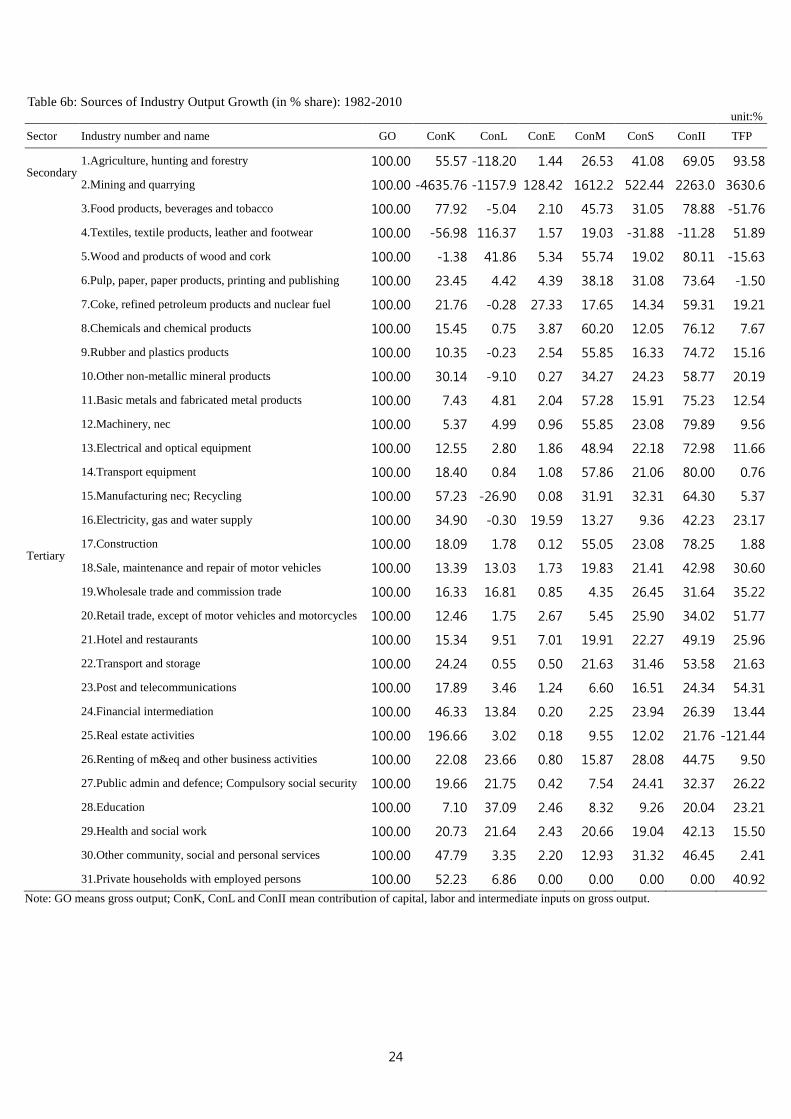

Despite that the share of factor contribution varies by industry, but, in general, the

results show that the contribution share from II dominates that from other inputs (K, L)

12

for most industries in Secondary Sectors. However, Table 6b shows that such input

dominant contribution effect may differ by industry in Tertiary sectors. For example,

among all factor contribution in “21.Hotel and restaurant” industry, II has the largest

contribution share (49%), TFP has the second largest share (18%), and K has the

lowest share (15%). In the industry “23.Post and telecommunications”, TFP share is

30%, L share is 28%, II share in only 24%, and K share is only 18%. In the case of

“28. Education” industry, L has dominant share of contribution (77%). Ranking of

contribution effect and percentage share for inputs for each industry during

1981-2010 can be seen in Figures 6a and 6b.

As for composition within intermediate inputs, Table 6b also shows that M

accounts for most contribution from II for those secondary industries. However, for

most tertiary industries, services input (S) accounts most of contribution from

intermediate inputs.

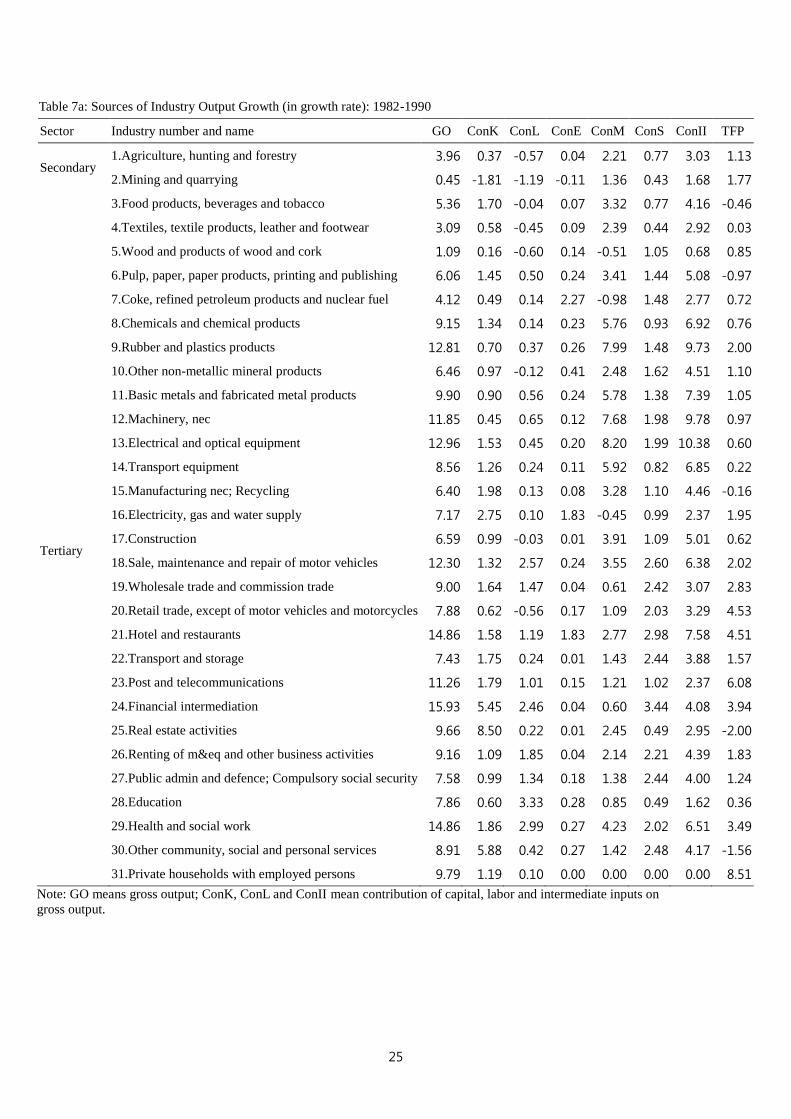

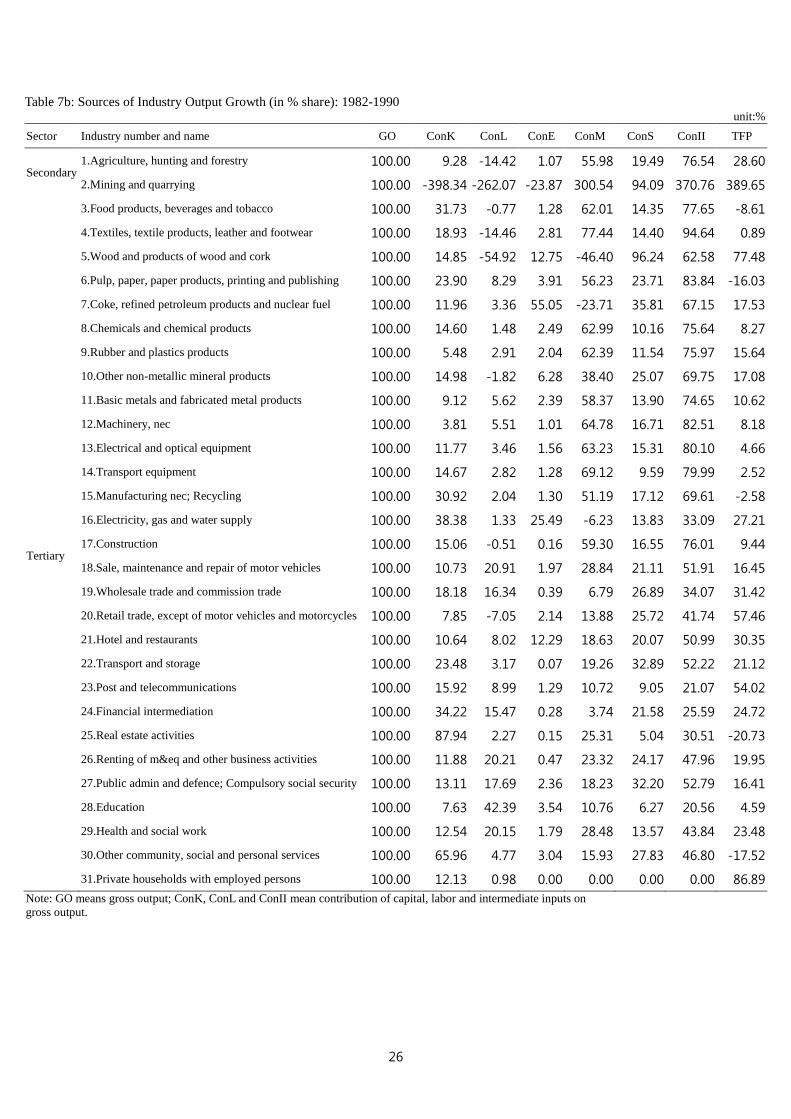

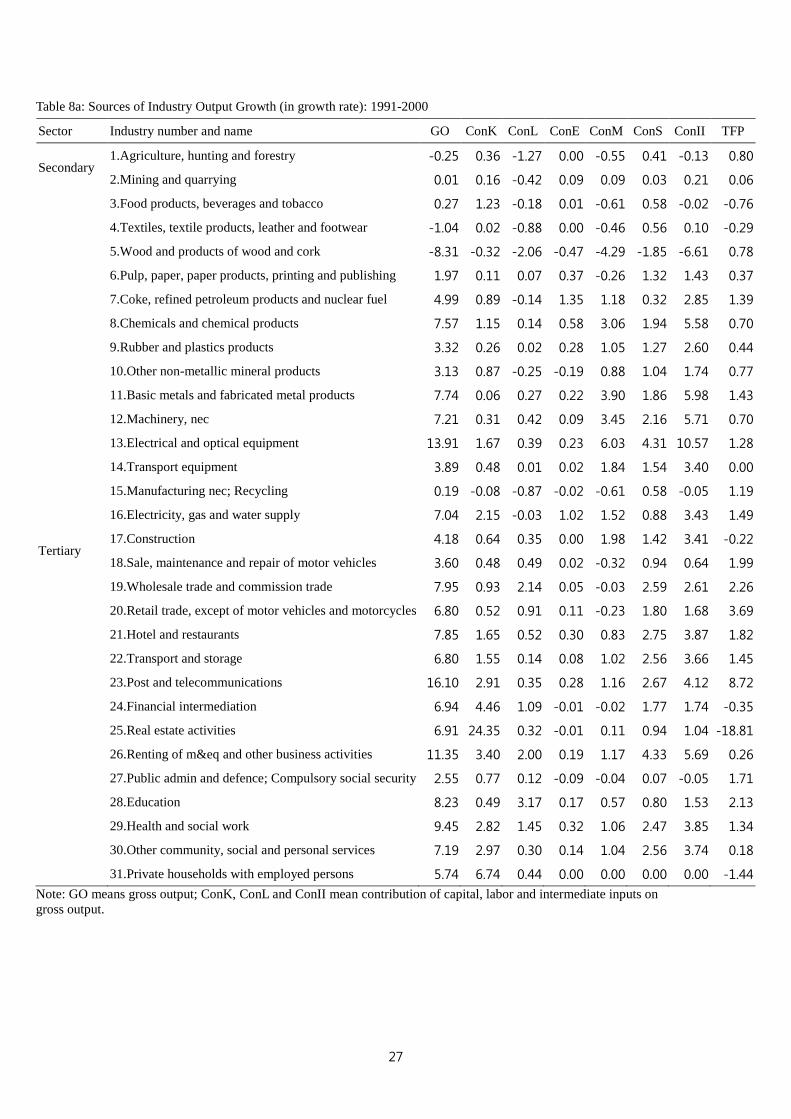

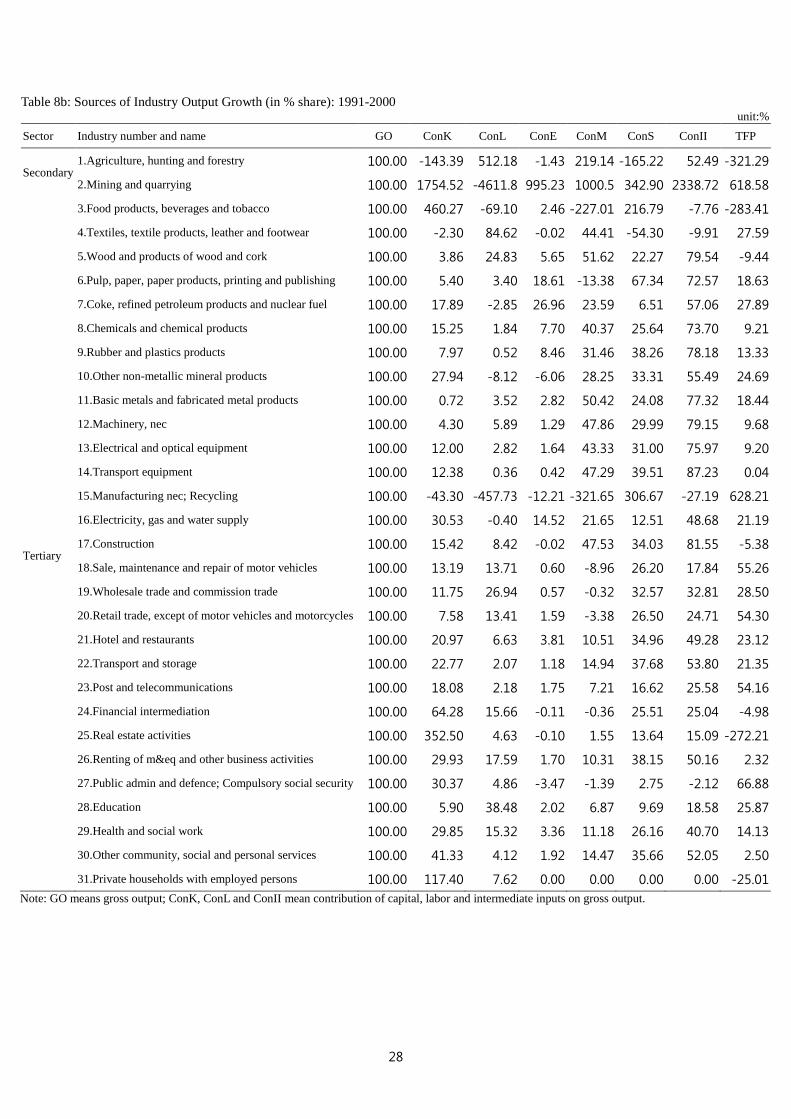

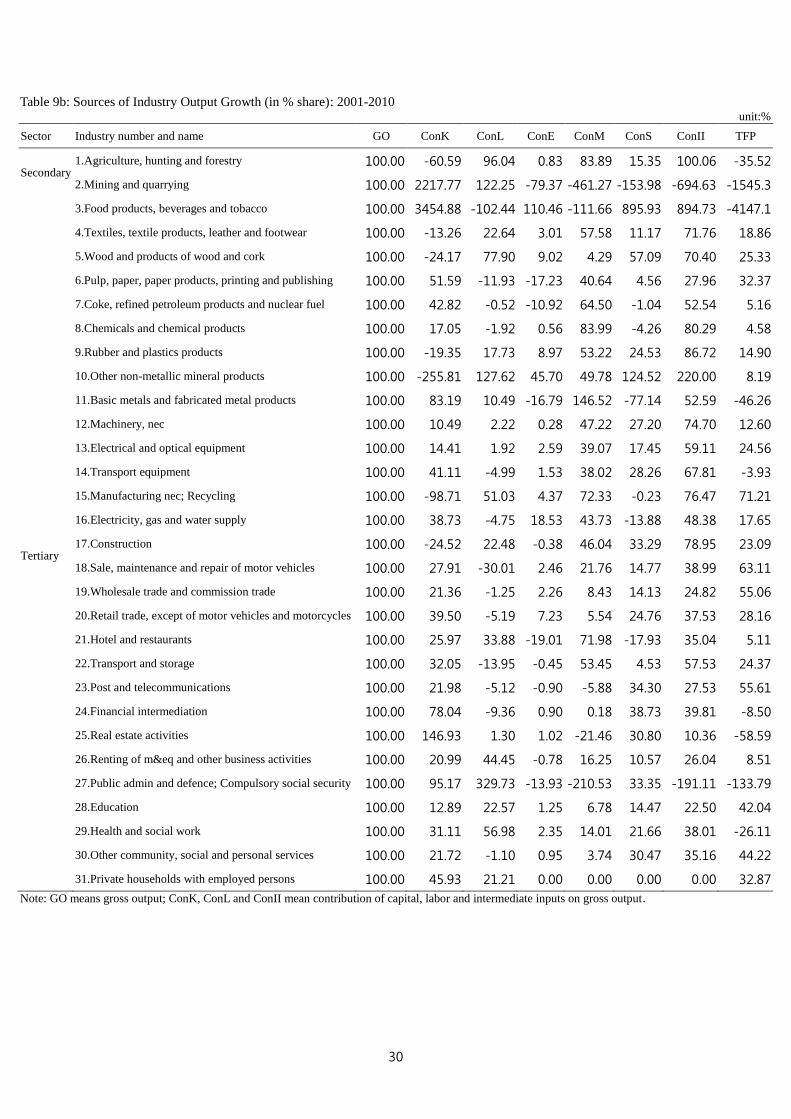

5.2 Sources of Industry output growth: Cross-period comparisons

Tables 7, 8 and 9 present sources of industry output growth analyses (in growth

rate (tables a) and in % share (tables b)) for periods of 1982-1990, 1991-2000, and

2001-2010, respectively. Since there are 31 industries with different decomposition

results, thus in this section we intend to choose 3 industries to show such vast

difference in industry level in Taiwan.

The “13.Electrical and optical equipment” is the industry with the largest

industry weight and growth rate in the Secondary sectors. It is also regarded as one of

ICT producing industry in Taiwan. Taking it as example, we find the shares of II have

been high in every period. But the size of such share reduced over time. The

contribution from M also dominates other intermediate inputs. The contributions from

K and L reduced were much smaller than that from II. TFP shows insignificant impact

on growth. The results can be seen in the following table:

Period ConK ConL ConE ConM ConS ConII TFP

1982-2010 12.55 2.80 1.86 48.94 22.18 72.98 11.66

1982-1990 11.77 3.46 1.56 63.23 15.31 80.10 4.66

1991-2000 12.00 2.82 1.64 43.33 31.00 75.97 9.20

13

2001-2010 14.41 1.92 2.59 39.07 17.45 59.11 24.56

*Sources of GO growth for the Electrical and Optical Equipment industry

The “19.Wholesale and commission trade” is the industry with the biggest

industry weight in the Tertiary sectors. We find the contribution shares of factor

inputs to be dominated by L in early decade, but by II and TFP in the later decades. It

should be noted that TFP increased over time, and became dominant driver in

2001-2010. The results discussed can be demonstrated in the following table:

Period ConK ConL ConE ConM ConS ConII TFP

1982-2010 16.33 16.81 0.85 4.35 26.45 31.64 35.22

1982-1990 18.18 16.34 0.39 6.79 26.89 34.07 31.42

1991-2000 11.75 26.94 0.57 -0.32 32.57 32.81 28.50

2001-2010 21.36 -1.25 2.26 8.43 14.13 24.82 55.06

*Sources of output growth in the “19.Wholesale and commission trade” industry

In addition, the “23.Post and communications” is the industry with the biggest

annual growth rate in the Tertiary sectors. This industry is also regarded as major ICT

using industry in Taiwan. We find that this industry had quite high contribution share

on L in 1982-1990, high share on II and TFP in 1991-2000, but very high share on K

in 2001-2010. We list such contribution shares of its factor inputs as the following:

Period ConK ConL ConE ConM ConS ConII TFP

1982-2010 17.89 3.46 1.24 6.60 16.51 24.34 54.31

1982-1990 23.48 3.17 0.07 19.26 32.89 52.22 21.12

1991-2000 18.08 2.18 1.75 7.21 16.62 25.58 54.16

2001-2010 21.98 -5.12 -0.90 -5.88 34.30 27.53 55.61

*Source of output growth in the “23.Post and communications” industry

Based upon the above discussions, we may conclude that the contribution share

of II to industry output in most Tertiary industries tends to be smaller than those

Secondary industries.

6. Concluding Remarks

14

In the last decades, Taiwan’s industrial policy focus on to help the so called “hi-tech”

industries, such as ICT industry (13 Electrical and Optical Equipment, Post and

communications). The strategies include establishment of science-based industrial

parks, technological support from national research institute and national plan,

providing tax incentives and special support for developing semiconductor industry,

and so on. It is clear that there are significant structural changes happened in the past

decades. The industry weights for primary and secondary decrease over time, whilst

the important of tertiary industry increases during the period of 1981-2010. The

industry weights of most other industries in the Secondary Industry decreased except

“Electrical and optical equipment” and “Basic and fabricated metal”. On the contrary,

most industries in Tertiary Industry increased during 1981-2010. It is shown that the

industrial policy is a significant factor to influence the industrial structural change.

The empirical results show that the output growth rate for 31 industries ranged

from 11.92% to -2.97% in 1981-2010 and varied by sub-period. The results also show

the structure of the factor contribution share to be varied by industry. But, in general,

the contribution share from intermediate inputs dominates that from other inputs

(capital and labor) for most industries in Secondary Sectors. In several industrial, such

as food products and textile, rubber and plastics, the growth rates of labor input

(measured by total working hour, HEMP) are negative. However, such input

dominant contribution effect differs by industry in Tertiary industries. This indicates

the importance of growth decomposition analysis at industry level.

We also find that the TFP growth rate of “Electrical and Optical Equipment”

industry is the highest in secondary industries whilst the TFP growth rate of “Post

and communications” is the largest among the tertiary sector, which means the

impact of the industrial policy does not have impact on structural change, but also

influences the TFP growth rate.

References

Jorgenson, D.W., F.M. Gollop and B.M. Fraumeni (1987), Productivity and US

Economic Growth, Cambridge MA: Harvard University Press.

15

Jorgenson, D.W., M. Ho and K. Stiroh. (2005) Information Technology and the

American Growth Resurgence, MIT, 2005.

Pyo, Hak, K.H. Rhee and H. Chun (2012), Asia KLEMS Growth and Productivity

Accounts, version1.0. Draft and Proposal, Part 1 Methodology. Asia KLEMS

consortium.

16

Table 1: The industry Value Added weights of Primary, secondary, Tertiary and Manufacturing by

sub-period unit:%

1981-1990 1991-2000 2001-2010 1981-2010

Primary 6.13 3.10 1.73 3.66

Secondary 44.75 34.70 30.99 36.82

Manufacturing 35.55 27.03 26.29 29.62

Tertiary 49.11 62.19 67.27 59.53

17

Table 2: Industry Value Added Weights by selected year

unit:%

Sector Industry number and name 1981 1990 2000 2010

Secondary 1.Agriculture, hunting and forestry 7.65 4.24 2.08 1.69

2.Mining and quarrying 2.16 0.68 0.52 0.48

3.Food products, beverages and tobacco 4.48 3.33 1.47 1.24

4.Textiles, textile products, leather and footwear 6.96 4.47 1.88 0.82

5.Wood and products of wood and cork 0.65 0.41 0.08 0.07

6.Pulp, paper, paper products, printing and publishing 1.57 1.29 0.73 0.63

7.Coke, refined petroleum products and nuclear fuel 1.30 1.14 1.38 1.09

8.Chemicals and chemical products 2.50 2.82 2.25 3.23

9.Rubber and plastics products 1.42 2.10 1.26 0.70

10.Other non-metallic mineral products 1.69 1.43 0.70 0.47

11.Basic metals and fabricated metal products 2.94 3.99 3.55 3.30

12.Machinery, nec 0.98 1.28 1.18 1.27

13.Electrical and optical equipment 4.31 5.46 8.37 12.08

14.Transport equipment 2.39 2.42 1.56 1.26

15.Manufacturing nec; Recycling 2.80 2.01 1.04 0.65

16.Electricity, gas and water supply 3.40 2.81 2.06 1.35

Tertiary

17.Construction 5.69 4.61 3.22 2.90

18.Sale, maintenance and repair of motor vehicles 1.16 1.44 1.33 1.23

19.Wholesale trade and commission trade 6.17 6.23 9.41 10.94

20.Retail trade, except of motor vehicles and motorcycles 5.78 5.76 6.97 6.67

21.Hotel and restaurants 0.90 1.67 2.09 2.05

22.Transport and storage 4.27 4.40 3.93 3.02

23.Post and telecommunications 1.62 1.72 2.50 1.95

24.Financial intermediation 4.22 7.77 8.58 6.51

25.Real estate activities 5.09 6.42 8.88 8.86

26.Renting of m&eq and other business activities 1.70 2.02 3.39 4.88

27.Public admin and defence; Compulsory social security 9.01 9.29 8.16 7.48

28.Education 2.74 3.06 4.22 4.74

29.Health and social work 0.75 1.60 2.63 3.09

30.Other community, social and personal services 3.22 3.51 3.87 4.55

31.Private households with employed persons 0.47 0.61 0.71 0.80

18

Table3: Growth of Industry Value Added by Period

unit:%

Sector Industry number and name 1982-1990 1991-2000 2001-2010 1982-2010

Secondary 1.Agriculture, hunting and forestry 3.36 1.35 0.85 1.80

2.Mining and quarrying -2.97 5.83 2.20 1.85

3.Food products, beverages and tobacco 6.62 0.26 1.24 2.57

4.Textiles, textile products, leather and footwear 5.02 -0.23 -5.37 -0.37

5.Wood and products of wood and cork 4.76 -7.36 1.29 -0.62

6.Pulp, paper, paper products, printing and publishing 7.77 2.72 1.54 3.88

7.Coke, refined petroleum products and nuclear fuel 8.52 10.34 0.56 6.40

8.Chemicals and chemical products 11.26 6.18 6.57 7.89

9.Rubber and plastics products 14.26 3.33 -2.89 4.58

10.Other non-metallic mineral products 8.10 1.23 -1.01 2.59

11.Basic metals and fabricated metal products 13.31 7.27 2.22 7.40

12.Machinery, nec 12.89 7.60 3.69 7.89

13.Electrical and optical equipment 12.54 12.73 6.62 10.56

14.Transport equipment 10.04 4.05 0.84 4.80

15.Manufacturing nec; Recycling 6.24 1.80 -1.65 1.99

16.Electricity, gas and water supply 7.82 5.34 -1.26 3.83

Tertiary 17.Construction 7.58 4.87 1.89 4.68

18.Sale, maintenance and repair of motor vehicles 12.40 7.64 2.13 7.21

19.Wholesale trade and commission trade 10.03 12.57 4.46 8.98

20.Retail trade, except of motor vehicles and motorcycles 9.89 10.34 2.52 7.50

21.Hotel and restaurants 16.77 10.64 2.76 9.83

22.Transport and storage 10.24 7.31 0.33 5.81

23.Post and telecommunications 10.62 12.16 0.46 7.65

24.Financial intermediation 16.70 9.44 0.19 8.50

25.Real estate activities 12.50 11.69 2.93 8.92

26.Renting of m&eq and other business activities 11.85 13.61 6.60 10.65

27.Public admin and defence; Compulsory social security 10.26 7.15 2.07 6.36

28.Education 11.15 11.66 4.11 8.90

29.Health and social work 18.35 13.41 4.55 11.89

30.Other community, social and personal services 10.87 9.43 4.57 8.20

31.Private households with employed persons 12.81 9.97 4.16 8.85

19

Table 4: Growth of Industry Gross Output by Period

unit:%

Sector Industry number and name 1982-1990 1991-2000 2001-2010 1982-2010

Secondary 1.Agriculture, hunting and forestry 3.96 -0.25 -0.99 0.80

2.Mining and quarrying 0.45 0.01 -0.26 0.05

3.Food products, beverages and tobacco 5.36 0.27 0.04 1.77

4.Textiles, textile products, leather and footwear 3.09 -1.04 -3.53 -0.62

5.Wood and products of wood and cork 1.09 -8.31 -1.29 -2.97

6.Pulp, paper, paper products, printing and publishing 6.06 1.97 1.17 2.96

7.Coke, refined petroleum products and nuclear fuel 4.12 4.99 2.64 3.91

8.Chemicals and chemical products 9.15 7.57 5.35 7.30

9.Rubber and plastics products 12.81 3.32 -2.16 4.38

10.Other non-metallic mineral products 6.46 3.13 -0.33 2.97

11.Basic metals and fabricated metal products 9.90 7.74 0.49 5.91

12.Machinery, nec 11.85 7.21 4.35 7.67

13.Electrical and optical equipment 12.96 13.91 8.98 11.92

14.Transport equipment 8.56 3.89 2.30 4.79

15.Manufacturing nec; Recycling 6.40 0.19 -1.09 1.67

16.Electricity, gas and water supply 7.17 7.04 2.19 5.41

Tertiary 17.Construction 6.59 4.18 -0.68 3.25

18.Sale, maintenance and repair of motor vehicles 12.30 3.60 2.08 5.78

19.Wholesale trade and commission trade 9.00 7.95 4.24 7.00

20.Retail trade, except of motor vehicles and motorcycles 7.88 6.80 2.44 5.63

21.Hotel and restaurants 14.86 7.85 1.75 7.92

22.Transport and storage 7.43 6.80 1.93 5.32

23.Post and telecommunications 11.26 16.10 4.15 10.47

24.Financial intermediation 15.93 6.94 1.55 7.87

25.Real estate activities 9.66 6.91 2.64 6.29

26.Renting of m&eq and other business activities 9.16 11.35 4.69 8.38

27.Public admin and defence; Compulsory social security 7.58 2.55 0.23 3.31

28.Education 7.86 8.23 3.37 6.44

29.Health and social work 14.86 9.45 2.25 8.65

30.Other community, social and personal services 8.91 7.19 3.81 6.56

31.Private households with employed persons 9.79 5.74 3.30 6.16

20

Table 5: Growth of Industry Labor Input (HEMP) by Period

unit:%

Sector Industry number and name 1982-2010 1982-1990 1991-2000 2001-2010

Secondary 1.Agriculture, hunting and forestry -3.21 -2.02 -4.18 -3.30

2.Mining and quarrying -8.38 -10.76 -6.22 -8.41

3.Food products, beverages and tobacco -0.99 -0.70 -2.05 -0.18

4.Textiles, textile products, leather and footwear -4.18 -2.37 -5.07 -4.92

5.Wood and products of wood and cork -5.34 -2.67 -9.34 -3.73

6.Pulp, paper, paper products, printing and publishing 1.07 3.60 0.30 -0.44

7.Coke, refined petroleum products and nuclear fuel 0.72 5.78 -3.52 0.40

8.Chemicals and chemical products 0.81 2.14 1.44 -1.03

9.Rubber and plastics products 0.02 2.19 0.08 -2.00

10.Other non-metallic mineral products -1.69 -0.65 -1.59 -2.73

11.Basic metals and fabricated metal products 2.28 4.58 1.74 0.75

12.Machinery, nec 2.01 3.17 1.89 1.08

13.Electrical and optical equipment 3.03 3.84 3.43 1.92

14.Transport equipment 0.45 1.91 0.11 -0.52

15.Manufacturing nec; Recycling -2.73 1.68 -5.24 -4.20

16.Electricity, gas and water supply 0.06 1.58 -0.31 -0.94

Tertiary 17.Construction 0.26 -0.25 1.54 -0.56

18.Sale, maintenance and repair of motor vehicles 1.32 5.05 0.96 -1.69

19.Wholesale trade and commission trade 3.54 5.02 5.96 -0.21

20.Retail trade, except of motor vehicles and motorcycles 0.25 -1.37 2.46 -0.49

21.Hotel and restaurants 3.32 4.73 2.25 3.14

22.Transport and storage 0.01 1.35 0.55 -1.73

23.Post and telecommunications 1.05 3.13 1.20 -0.98

24.Financial intermediation 4.20 9.47 4.25 -0.58

25.Real estate activities 5.83 9.08 7.03 1.71

26.Renting of m&eq and other business activities 6.48 5.51 5.70 8.15

27.Public admin and defence; Compulsory social security 1.43 2.76 0.23 1.43

28.Education 2.92 3.83 3.84 1.18

29.Health and social work 5.70 8.17 4.89 4.29

30.Other community, social and personal services 1.54 3.00 1.96 -0.19

31.Private households with employed persons 2.22 0.42 2.67 3.40

21

Table 6: Growth of Industry Capital Stock by Period

unit:%

Sector Industry number and name 1982-2010 1982-1990 1991-2000 2001-2010

Secondary 1.Agriculture, hunting and forestry 2.48 1.65 1.86 3.85

2.Mining and quarrying -6.55 -3.82 -0.09 -15.46

3.Food products, beverages and tobacco 7.31 8.06 6.90 7.05

4.Textiles, textile products, leather and footwear 3.57 4.30 0.20 6.29

5.Wood and products of wood and cork 0.32 1.43 -5.68 5.31

6.Pulp, paper, paper products, printing and publishing 5.47 9.59 1.44 5.78

7.Coke, refined petroleum products and nuclear fuel 4.06 4.08 2.46 5.63

8.Chemicals and chemical products 7.34 7.70 7.20 7.16

9.Rubber and plastics products 5.14 7.03 2.33 6.23

10.Other non-metallic mineral products 5.51 5.34 4.68 6.49

11.Basic metals and fabricated metal products 4.06 7.13 0.63 4.73

12.Machinery, nec 7.43 10.55 5.61 6.43

13.Electrical and optical equipment 11.29 12.23 13.96 7.78

14.Transport equipment 5.50 7.28 3.10 6.29

15.Manufacturing nec; Recycling 4.53 9.45 -0.64 5.29

16.Electricity, gas and water supply 4.47 5.40 4.82 3.29

Tertiary 17.Construction 4.39 5.96 5.62 1.74

18.Sale, maintenance and repair of motor vehicles 3.62 7.41 2.39 1.45

19.Wholesale trade and commission trade 3.41 4.97 3.14 2.27

20.Retail trade, except of motor vehicles and motorcycles 1.83 2.10 1.72 1.71

21.Hotel and restaurants 4.14 5.84 5.44 1.31

22.Transport and storage 4.09 5.70 4.73 2.00

23.Post and telecommunications 3.90 3.28 6.44 1.93

24.Financial intermediation 7.05 10.30 8.70 2.46

25.Real estate activities 17.97 12.52 35.68 5.16

26.Renting of m&eq and other business activities 7.12 3.40 14.68 2.90

27.Public admin and defence; Compulsory social security 5.59 10.69 5.37 1.21

28.Education 9.14 11.53 11.89 4.24

29.Health and social work 7.12 9.31 10.03 2.23

30.Other community, social and personal services 7.23 12.68 7.65 1.91

31.Private households with employed persons 3.69 1.41 7.67 1.76

22

Table 7: Growth of Industry TFP by Subperiod

unit:%

Sector Industry number and name 1982-2010 1982-1990 1991-2000 2001-2010

Secondary 1.Agriculture, hunting and forestry 0.75 1.13 0.80 0.35

2.Mining and quarrying 1.96 1.77 0.06 4.03

3.Food products, beverages and tobacco -0.91 -0.46 -0.76 -1.48

4.Textiles, textile products, leather and footwear -0.32 0.03 -0.29 -0.66

5.Wood and products of wood and cork 0.46 0.85 0.78 -0.33

6.Pulp, paper, paper products, printing and publishing -0.04 -0.97 0.37 0.38

7.Coke, refined petroleum products and nuclear fuel 0.75 0.72 1.39 0.14

8.Chemicals and chemical products 0.56 0.76 0.70 0.25

9.Rubber and plastics products 0.66 2.00 0.44 -0.32

10.Other non-metallic mineral products 0.60 1.10 0.77 -0.03

11.Basic metals and fabricated metal products 0.74 1.05 1.43 -0.22

12.Machinery, nec 0.73 0.97 0.70 0.55

13.Electrical and optical equipment 1.39 0.60 1.28 2.20

14.Transport equipment 0.04 0.22 0.00 -0.09

15.Manufacturing nec; Recycling 0.09 -0.16 1.19 -0.78

16.Electricity, gas and water supply 1.25 1.95 1.49 0.39

Tertiary 17.Construction 0.06 0.62 -0.22 -0.16

18.Sale, maintenance and repair of motor vehicals 1.77 2.02 1.99 1.32

19.Wholesale trade and commission trade 2.46 2.83 2.26 2.34

20.Retail trade, except of motor vehicals and motorcycles 2.92 4.53 3.69 0.69

21.Hotel and restaurants 2.06 4.51 1.82 0.09

22.Transport and storage 1.15 1.57 1.45 0.47

23.Post and telecommunications 5.69 6.08 8.72 2.31

24.Financial intermediation 1.06 3.94 -0.35 -0.13

25.Real estate activities -7.64 -2.00 -18.81 -1.55

26.Renting of m&eq and other business activities 0.80 1.83 0.26 0.40

27.Public admin and defence; Compulsory social security 0.87 1.24 1.71 -0.31

28.Education 1.50 0.36 2.13 1.42

29.Health and social work 1.34 3.49 1.34 -0.59

30.Other community, social and personal services 0.16 -1.56 0.18 1.68

31.Private households with employed persons 2.52 8.51 -1.44 1.09

23

Table 6a: Sources of Industry Output Growth (in growth rate): 1982-2010

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 0.80 0.44 -0.95 0.01 0.21 0.33 0.55 0.75

2.Mining and quarrying 0.05 -2.50 -0.63 0.07 0.87 0.28 1.22 1.96

3.Food products, beverages and tobacco 1.77 1.38 -0.09 0.04 0.81 0.55 1.39 -0.91

4.Textiles, textile products, leather and footwear -0.62 0.35 -0.72 -0.01 -0.12 0.20 0.07 -0.32

5.Wood and products of wood and cork -2.97 0.04 -1.24 -0.16 -1.66 -0.57 -2.38 0.46

6.Pulp, paper, paper products, printing and publishing 2.96 0.69 0.13 0.13 1.13 0.92 2.18 -0.04

7.Coke, refined petroleum products and nuclear fuel 3.91 0.85 -0.01 1.07 0.69 0.56 2.32 0.75

8.Chemicals and chemical products 7.30 1.13 0.05 0.28 4.39 0.88 5.55 0.56

9.Rubber and plastics products 4.38 0.45 -0.01 0.11 2.44 0.71 3.27 0.66

10.Other non-metallic mineral products 2.97 0.90 -0.27 0.01 1.02 0.72 1.75 0.60

11.Basic metals and fabricated metal products 5.91 0.44 0.28 0.12 3.38 0.94 4.44 0.74

12.Machinery, nec 7.67 0.41 0.38 0.07 4.28 1.77 6.12 0.73

13.Electrical and optical equipment 11.92 1.50 0.33 0.22 5.83 2.64 8.70 1.39

14.Transport equipment 4.79 0.88 0.04 0.05 2.77 1.01 3.83 0.04

15.Manufacturing nec; Recycling 1.67 0.96 -0.45 0.00 0.53 0.54 1.08 0.09

16.Electricity, gas and water supply 5.41 1.89 -0.02 1.06 0.72 0.51 2.28 1.25

Tertiary 17.Construction 3.25 0.59 0.06 0.00 1.79 0.75 2.54 0.06

18.Sale, maintenance and repair of motor vehicles 5.78 0.77 0.75 0.10 1.15 1.24 2.48 1.77

19.Wholesale trade and commission trade 7.00 1.14 1.18 0.06 0.30 1.85 2.21 2.46

20.Retail trade, except of motor vehicles and motorcycles 5.63 0.70 0.10 0.15 0.31 1.46 1.92 2.92

21.Hotel and restaurants 7.92 1.22 0.75 0.56 1.58 1.76 3.90 2.06

22.Transport and storage 5.32 1.29 0.03 0.03 1.15 1.67 2.85 1.15

23.Post and telecommunications 10.47 1.87 0.36 0.13 0.69 1.73 2.55 5.69

24.Financial intermediation 7.87 3.65 1.09 0.02 0.18 1.88 2.08 1.06

25.Real estate activities 6.29 12.37 0.19 0.01 0.60 0.76 1.37 -7.64

26.Renting of m&eq and other business activities 8.38 1.85 1.98 0.07 1.33 2.35 3.75 0.80

27.Public admin and defence; Compulsory social security 3.31 0.65 0.72 0.01 0.25 0.81 1.07 0.87

28.Education 6.44 0.46 2.39 0.16 0.54 0.60 1.29 1.50

29.Health and social work 8.65 1.79 1.87 0.21 1.79 1.65 3.64 1.34

30.Other community, social and personal services 6.56 3.13 0.22 0.14 0.85 2.05 3.05 0.16

31.Private households with employed persons 6.16 3.22 0.42 0.00 0.00 0.00 0.00 2.52 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on

gross output.

24

Table 6b: Sources of Industry Output Growth (in % share): 1982-2010 unit:%

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 100.00 55.57 -118.20 1.44 26.53 41.08 69.05 93.58

2.Mining and quarrying 100.00 -4635.76 -1157.9 128.42 1612.2 522.44 2263.0 3630.6

3.Food products, beverages and tobacco 100.00 77.92 -5.04 2.10 45.73 31.05 78.88 -51.76

4.Textiles, textile products, leather and footwear 100.00 -56.98 116.37 1.57 19.03 -31.88 -11.28 51.89

5.Wood and products of wood and cork 100.00 -1.38 41.86 5.34 55.74 19.02 80.11 -15.63

6.Pulp, paper, paper products, printing and publishing 100.00 23.45 4.42 4.39 38.18 31.08 73.64 -1.50

7.Coke, refined petroleum products and nuclear fuel 100.00 21.76 -0.28 27.33 17.65 14.34 59.31 19.21

8.Chemicals and chemical products 100.00 15.45 0.75 3.87 60.20 12.05 76.12 7.67

9.Rubber and plastics products 100.00 10.35 -0.23 2.54 55.85 16.33 74.72 15.16

10.Other non-metallic mineral products 100.00 30.14 -9.10 0.27 34.27 24.23 58.77 20.19

11.Basic metals and fabricated metal products 100.00 7.43 4.81 2.04 57.28 15.91 75.23 12.54

12.Machinery, nec 100.00 5.37 4.99 0.96 55.85 23.08 79.89 9.56

13.Electrical and optical equipment 100.00 12.55 2.80 1.86 48.94 22.18 72.98 11.66

14.Transport equipment 100.00 18.40 0.84 1.08 57.86 21.06 80.00 0.76

15.Manufacturing nec; Recycling 100.00 57.23 -26.90 0.08 31.91 32.31 64.30 5.37

16.Electricity, gas and water supply 100.00 34.90 -0.30 19.59 13.27 9.36 42.23 23.17

Tertiary 17.Construction 100.00 18.09 1.78 0.12 55.05 23.08 78.25 1.88

18.Sale, maintenance and repair of motor vehicles 100.00 13.39 13.03 1.73 19.83 21.41 42.98 30.60

19.Wholesale trade and commission trade 100.00 16.33 16.81 0.85 4.35 26.45 31.64 35.22

20.Retail trade, except of motor vehicles and motorcycles 100.00 12.46 1.75 2.67 5.45 25.90 34.02 51.77

21.Hotel and restaurants 100.00 15.34 9.51 7.01 19.91 22.27 49.19 25.96

22.Transport and storage 100.00 24.24 0.55 0.50 21.63 31.46 53.58 21.63

23.Post and telecommunications 100.00 17.89 3.46 1.24 6.60 16.51 24.34 54.31

24.Financial intermediation 100.00 46.33 13.84 0.20 2.25 23.94 26.39 13.44

25.Real estate activities 100.00 196.66 3.02 0.18 9.55 12.02 21.76 -121.44

26.Renting of m&eq and other business activities 100.00 22.08 23.66 0.80 15.87 28.08 44.75 9.50

27.Public admin and defence; Compulsory social security 100.00 19.66 21.75 0.42 7.54 24.41 32.37 26.22

28.Education 100.00 7.10 37.09 2.46 8.32 9.26 20.04 23.21

29.Health and social work 100.00 20.73 21.64 2.43 20.66 19.04 42.13 15.50

30.Other community, social and personal services 100.00 47.79 3.35 2.20 12.93 31.32 46.45 2.41

31.Private households with employed persons 100.00 52.23 6.86 0.00 0.00 0.00 0.00 40.92 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on gross output.

25

Table 7a: Sources of Industry Output Growth (in growth rate): 1982-1990

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 3.96 0.37 -0.57 0.04 2.21 0.77 3.03 1.13

2.Mining and quarrying 0.45 -1.81 -1.19 -0.11 1.36 0.43 1.68 1.77

3.Food products, beverages and tobacco 5.36 1.70 -0.04 0.07 3.32 0.77 4.16 -0.46

4.Textiles, textile products, leather and footwear 3.09 0.58 -0.45 0.09 2.39 0.44 2.92 0.03

5.Wood and products of wood and cork 1.09 0.16 -0.60 0.14 -0.51 1.05 0.68 0.85

6.Pulp, paper, paper products, printing and publishing 6.06 1.45 0.50 0.24 3.41 1.44 5.08 -0.97

7.Coke, refined petroleum products and nuclear fuel 4.12 0.49 0.14 2.27 -0.98 1.48 2.77 0.72

8.Chemicals and chemical products 9.15 1.34 0.14 0.23 5.76 0.93 6.92 0.76

9.Rubber and plastics products 12.81 0.70 0.37 0.26 7.99 1.48 9.73 2.00

10.Other non-metallic mineral products 6.46 0.97 -0.12 0.41 2.48 1.62 4.51 1.10

11.Basic metals and fabricated metal products 9.90 0.90 0.56 0.24 5.78 1.38 7.39 1.05

12.Machinery, nec 11.85 0.45 0.65 0.12 7.68 1.98 9.78 0.97

13.Electrical and optical equipment 12.96 1.53 0.45 0.20 8.20 1.99 10.38 0.60

14.Transport equipment 8.56 1.26 0.24 0.11 5.92 0.82 6.85 0.22

15.Manufacturing nec; Recycling 6.40 1.98 0.13 0.08 3.28 1.10 4.46 -0.16

16.Electricity, gas and water supply 7.17 2.75 0.10 1.83 -0.45 0.99 2.37 1.95

Tertiary 17.Construction 6.59 0.99 -0.03 0.01 3.91 1.09 5.01 0.62

18.Sale, maintenance and repair of motor vehicles 12.30 1.32 2.57 0.24 3.55 2.60 6.38 2.02

19.Wholesale trade and commission trade 9.00 1.64 1.47 0.04 0.61 2.42 3.07 2.83

20.Retail trade, except of motor vehicles and motorcycles 7.88 0.62 -0.56 0.17 1.09 2.03 3.29 4.53

21.Hotel and restaurants 14.86 1.58 1.19 1.83 2.77 2.98 7.58 4.51

22.Transport and storage 7.43 1.75 0.24 0.01 1.43 2.44 3.88 1.57

23.Post and telecommunications 11.26 1.79 1.01 0.15 1.21 1.02 2.37 6.08

24.Financial intermediation 15.93 5.45 2.46 0.04 0.60 3.44 4.08 3.94

25.Real estate activities 9.66 8.50 0.22 0.01 2.45 0.49 2.95 -2.00

26.Renting of m&eq and other business activities 9.16 1.09 1.85 0.04 2.14 2.21 4.39 1.83

27.Public admin and defence; Compulsory social security 7.58 0.99 1.34 0.18 1.38 2.44 4.00 1.24

28.Education 7.86 0.60 3.33 0.28 0.85 0.49 1.62 0.36

29.Health and social work 14.86 1.86 2.99 0.27 4.23 2.02 6.51 3.49

30.Other community, social and personal services 8.91 5.88 0.42 0.27 1.42 2.48 4.17 -1.56

31.Private households with employed persons 9.79 1.19 0.10 0.00 0.00 0.00 0.00 8.51 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on

gross output.

26

Table 7b: Sources of Industry Output Growth (in % share): 1982-1990 unit:%

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 100.00 9.28 -14.42 1.07 55.98 19.49 76.54 28.60

2.Mining and quarrying 100.00 -398.34 -262.07 -23.87 300.54 94.09 370.76 389.65

3.Food products, beverages and tobacco 100.00 31.73 -0.77 1.28 62.01 14.35 77.65 -8.61

4.Textiles, textile products, leather and footwear 100.00 18.93 -14.46 2.81 77.44 14.40 94.64 0.89

5.Wood and products of wood and cork 100.00 14.85 -54.92 12.75 -46.40 96.24 62.58 77.48

6.Pulp, paper, paper products, printing and publishing 100.00 23.90 8.29 3.91 56.23 23.71 83.84 -16.03

7.Coke, refined petroleum products and nuclear fuel 100.00 11.96 3.36 55.05 -23.71 35.81 67.15 17.53

8.Chemicals and chemical products 100.00 14.60 1.48 2.49 62.99 10.16 75.64 8.27

9.Rubber and plastics products 100.00 5.48 2.91 2.04 62.39 11.54 75.97 15.64

10.Other non-metallic mineral products 100.00 14.98 -1.82 6.28 38.40 25.07 69.75 17.08

11.Basic metals and fabricated metal products 100.00 9.12 5.62 2.39 58.37 13.90 74.65 10.62

12.Machinery, nec 100.00 3.81 5.51 1.01 64.78 16.71 82.51 8.18

13.Electrical and optical equipment 100.00 11.77 3.46 1.56 63.23 15.31 80.10 4.66

14.Transport equipment 100.00 14.67 2.82 1.28 69.12 9.59 79.99 2.52

15.Manufacturing nec; Recycling 100.00 30.92 2.04 1.30 51.19 17.12 69.61 -2.58

16.Electricity, gas and water supply 100.00 38.38 1.33 25.49 -6.23 13.83 33.09 27.21

Tertiary 17.Construction 100.00 15.06 -0.51 0.16 59.30 16.55 76.01 9.44

18.Sale, maintenance and repair of motor vehicles 100.00 10.73 20.91 1.97 28.84 21.11 51.91 16.45

19.Wholesale trade and commission trade 100.00 18.18 16.34 0.39 6.79 26.89 34.07 31.42

20.Retail trade, except of motor vehicles and motorcycles 100.00 7.85 -7.05 2.14 13.88 25.72 41.74 57.46

21.Hotel and restaurants 100.00 10.64 8.02 12.29 18.63 20.07 50.99 30.35

22.Transport and storage 100.00 23.48 3.17 0.07 19.26 32.89 52.22 21.12

23.Post and telecommunications 100.00 15.92 8.99 1.29 10.72 9.05 21.07 54.02

24.Financial intermediation 100.00 34.22 15.47 0.28 3.74 21.58 25.59 24.72

25.Real estate activities 100.00 87.94 2.27 0.15 25.31 5.04 30.51 -20.73

26.Renting of m&eq and other business activities 100.00 11.88 20.21 0.47 23.32 24.17 47.96 19.95

27.Public admin and defence; Compulsory social security 100.00 13.11 17.69 2.36 18.23 32.20 52.79 16.41

28.Education 100.00 7.63 42.39 3.54 10.76 6.27 20.56 4.59

29.Health and social work 100.00 12.54 20.15 1.79 28.48 13.57 43.84 23.48

30.Other community, social and personal services 100.00 65.96 4.77 3.04 15.93 27.83 46.80 -17.52

31.Private households with employed persons 100.00 12.13 0.98 0.00 0.00 0.00 0.00 86.89 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on

gross output.

27

Table 8a: Sources of Industry Output Growth (in growth rate): 1991-2000

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry -0.25 0.36 -1.27 0.00 -0.55 0.41 -0.13 0.80

2.Mining and quarrying 0.01 0.16 -0.42 0.09 0.09 0.03 0.21 0.06

3.Food products, beverages and tobacco 0.27 1.23 -0.18 0.01 -0.61 0.58 -0.02 -0.76

4.Textiles, textile products, leather and footwear -1.04 0.02 -0.88 0.00 -0.46 0.56 0.10 -0.29

5.Wood and products of wood and cork -8.31 -0.32 -2.06 -0.47 -4.29 -1.85 -6.61 0.78

6.Pulp, paper, paper products, printing and publishing 1.97 0.11 0.07 0.37 -0.26 1.32 1.43 0.37

7.Coke, refined petroleum products and nuclear fuel 4.99 0.89 -0.14 1.35 1.18 0.32 2.85 1.39

8.Chemicals and chemical products 7.57 1.15 0.14 0.58 3.06 1.94 5.58 0.70

9.Rubber and plastics products 3.32 0.26 0.02 0.28 1.05 1.27 2.60 0.44

10.Other non-metallic mineral products 3.13 0.87 -0.25 -0.19 0.88 1.04 1.74 0.77

11.Basic metals and fabricated metal products 7.74 0.06 0.27 0.22 3.90 1.86 5.98 1.43

12.Machinery, nec 7.21 0.31 0.42 0.09 3.45 2.16 5.71 0.70

13.Electrical and optical equipment 13.91 1.67 0.39 0.23 6.03 4.31 10.57 1.28

14.Transport equipment 3.89 0.48 0.01 0.02 1.84 1.54 3.40 0.00

15.Manufacturing nec; Recycling 0.19 -0.08 -0.87 -0.02 -0.61 0.58 -0.05 1.19

16.Electricity, gas and water supply 7.04 2.15 -0.03 1.02 1.52 0.88 3.43 1.49

Tertiary 17.Construction 4.18 0.64 0.35 0.00 1.98 1.42 3.41 -0.22

18.Sale, maintenance and repair of motor vehicles 3.60 0.48 0.49 0.02 -0.32 0.94 0.64 1.99

19.Wholesale trade and commission trade 7.95 0.93 2.14 0.05 -0.03 2.59 2.61 2.26

20.Retail trade, except of motor vehicles and motorcycles 6.80 0.52 0.91 0.11 -0.23 1.80 1.68 3.69

21.Hotel and restaurants 7.85 1.65 0.52 0.30 0.83 2.75 3.87 1.82

22.Transport and storage 6.80 1.55 0.14 0.08 1.02 2.56 3.66 1.45

23.Post and telecommunications 16.10 2.91 0.35 0.28 1.16 2.67 4.12 8.72

24.Financial intermediation 6.94 4.46 1.09 -0.01 -0.02 1.77 1.74 -0.35

25.Real estate activities 6.91 24.35 0.32 -0.01 0.11 0.94 1.04 -18.81

26.Renting of m&eq and other business activities 11.35 3.40 2.00 0.19 1.17 4.33 5.69 0.26

27.Public admin and defence; Compulsory social security 2.55 0.77 0.12 -0.09 -0.04 0.07 -0.05 1.71

28.Education 8.23 0.49 3.17 0.17 0.57 0.80 1.53 2.13

29.Health and social work 9.45 2.82 1.45 0.32 1.06 2.47 3.85 1.34

30.Other community, social and personal services 7.19 2.97 0.30 0.14 1.04 2.56 3.74 0.18

31.Private households with employed persons 5.74 6.74 0.44 0.00 0.00 0.00 0.00 -1.44 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on

gross output.

28

Table 8b: Sources of Industry Output Growth (in % share): 1991-2000 unit:%

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 100.00 -143.39 512.18 -1.43 219.14 -165.22 52.49 -321.29

2.Mining and quarrying 100.00 1754.52 -4611.8 995.23 1000.5 342.90 2338.72 618.58

3.Food products, beverages and tobacco 100.00 460.27 -69.10 2.46 -227.01 216.79 -7.76 -283.41

4.Textiles, textile products, leather and footwear 100.00 -2.30 84.62 -0.02 44.41 -54.30 -9.91 27.59

5.Wood and products of wood and cork 100.00 3.86 24.83 5.65 51.62 22.27 79.54 -9.44

6.Pulp, paper, paper products, printing and publishing 100.00 5.40 3.40 18.61 -13.38 67.34 72.57 18.63

7.Coke, refined petroleum products and nuclear fuel 100.00 17.89 -2.85 26.96 23.59 6.51 57.06 27.89

8.Chemicals and chemical products 100.00 15.25 1.84 7.70 40.37 25.64 73.70 9.21

9.Rubber and plastics products 100.00 7.97 0.52 8.46 31.46 38.26 78.18 13.33

10.Other non-metallic mineral products 100.00 27.94 -8.12 -6.06 28.25 33.31 55.49 24.69

11.Basic metals and fabricated metal products 100.00 0.72 3.52 2.82 50.42 24.08 77.32 18.44

12.Machinery, nec 100.00 4.30 5.89 1.29 47.86 29.99 79.15 9.68

13.Electrical and optical equipment 100.00 12.00 2.82 1.64 43.33 31.00 75.97 9.20

14.Transport equipment 100.00 12.38 0.36 0.42 47.29 39.51 87.23 0.04

15.Manufacturing nec; Recycling 100.00 -43.30 -457.73 -12.21 -321.65 306.67 -27.19 628.21

16.Electricity, gas and water supply 100.00 30.53 -0.40 14.52 21.65 12.51 48.68 21.19

Tertiary 17.Construction 100.00 15.42 8.42 -0.02 47.53 34.03 81.55 -5.38

18.Sale, maintenance and repair of motor vehicles 100.00 13.19 13.71 0.60 -8.96 26.20 17.84 55.26

19.Wholesale trade and commission trade 100.00 11.75 26.94 0.57 -0.32 32.57 32.81 28.50

20.Retail trade, except of motor vehicles and motorcycles 100.00 7.58 13.41 1.59 -3.38 26.50 24.71 54.30

21.Hotel and restaurants 100.00 20.97 6.63 3.81 10.51 34.96 49.28 23.12

22.Transport and storage 100.00 22.77 2.07 1.18 14.94 37.68 53.80 21.35

23.Post and telecommunications 100.00 18.08 2.18 1.75 7.21 16.62 25.58 54.16

24.Financial intermediation 100.00 64.28 15.66 -0.11 -0.36 25.51 25.04 -4.98

25.Real estate activities 100.00 352.50 4.63 -0.10 1.55 13.64 15.09 -272.21

26.Renting of m&eq and other business activities 100.00 29.93 17.59 1.70 10.31 38.15 50.16 2.32

27.Public admin and defence; Compulsory social security 100.00 30.37 4.86 -3.47 -1.39 2.75 -2.12 66.88

28.Education 100.00 5.90 38.48 2.02 6.87 9.69 18.58 25.87

29.Health and social work 100.00 29.85 15.32 3.36 11.18 26.16 40.70 14.13

30.Other community, social and personal services 100.00 41.33 4.12 1.92 14.47 35.66 52.05 2.50

31.Private households with employed persons 100.00 117.40 7.62 0.00 0.00 0.00 0.00 -25.01 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on gross output.

29

Table 9a: Sources of Industry Output Growth (in growth rate): 2001-2010

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry -0.99 0.60 -0.95 -0.01 -0.83 -0.15 -0.99 0.35

2.Mining and quarrying -0.26 -5.79 -0.32 0.21 1.20 0.40 1.81 4.03

3.Food products, beverages and tobacco 0.04 1.23 -0.04 0.04 -0.04 0.32 0.32 -1.48

4.Textiles, textile products, leather and footwear -3.53 0.47 -0.80 -0.11 -2.03 -0.39 -2.53 -0.66

5.Wood and products of wood and cork -1.29 0.31 -1.00 -0.12 -0.06 -0.73 -0.91 -0.33

6.Pulp, paper, paper products, printing and publishing 1.17 0.60 -0.14 -0.20 0.48 0.05 0.33 0.38

7.Coke, refined petroleum products and nuclear fuel 2.64 1.13 -0.01 -0.29 1.70 -0.03 1.39 0.14

8.Chemicals and chemical products 5.35 0.91 -0.10 0.03 4.49 -0.23 4.30 0.25

9.Rubber and plastics products -2.16 0.42 -0.38 -0.19 -1.15 -0.53 -1.87 -0.32

10.Other non-metallic mineral products -0.33 0.85 -0.42 -0.15 -0.17 -0.41 -0.73 -0.03

11.Basic metals and fabricated metal products 0.49 0.40 0.05 -0.08 0.71 -0.37 0.26 -0.22

12.Machinery, nec 4.35 0.46 0.10 0.01 2.06 1.18 3.25 0.55

13.Electrical and optical equipment 8.98 1.29 0.17 0.23 3.51 1.57 5.31 2.20

14.Transport equipment 2.30 0.95 -0.11 0.04 0.87 0.65 1.56 -0.09

15.Manufacturing nec; Recycling -1.09 1.08 -0.56 -0.05 -0.79 0.00 -0.84 -0.78

16.Electricity, gas and water supply 2.19 0.85 -0.10 0.41 0.96 -0.30 1.06 0.39

Tertiary 17.Construction -0.68 0.17 -0.15 0.00 -0.31 -0.23 -0.54 -0.16

18.Sale, maintenance and repair of motor vehicles 2.08 0.58 -0.63 0.05 0.45 0.31 0.81 1.32

19.Wholesale trade and commission trade 4.24 0.91 -0.05 0.10 0.36 0.60 1.05 2.34

20.Retail trade, except of motor vehicles and motorcycles 2.44 0.96 -0.13 0.18 0.14 0.60 0.92 0.69

21.Hotel and restaurants 1.75 0.45 0.59 -0.33 1.26 -0.31 0.61 0.09

22.Transport and storage 1.93 0.62 -0.27 -0.01 1.03 0.09 1.11 0.47

23.Post and telecommunications 4.15 0.91 -0.21 -0.04 -0.24 1.42 1.14 2.31

24.Financial intermediation 1.55 1.21 -0.15 0.01 0.00 0.60 0.62 -0.13

25.Real estate activities 2.64 3.87 0.03 0.03 -0.57 0.81 0.27 -1.55

26.Renting of m&eq and other business activities 4.69 0.98 2.08 -0.04 0.76 0.50 1.22 0.40

27.Public admin and defence; Compulsory social security 0.23 0.22 0.76 -0.03 -0.48 0.08 -0.44 -0.31

28.Education 3.37 0.43 0.76 0.04 0.23 0.49 0.76 1.42

29.Health and social work 2.25 0.70 1.28 0.05 0.32 0.49 0.86 -0.59

30.Other community, social and personal services 3.81 0.83 -0.04 0.04 0.14 1.16 1.34 1.68

31.Private households with employed persons 3.30 1.52 0.70 0.00 0.00 0.00 0.00 1.09 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on

gross output.

30

Table 9b: Sources of Industry Output Growth (in % share): 2001-2010 unit:%

Sector Industry number and name GO ConK ConL ConE ConM ConS ConII TFP

Secondary 1.Agriculture, hunting and forestry 100.00 -60.59 96.04 0.83 83.89 15.35 100.06 -35.52

2.Mining and quarrying 100.00 2217.77 122.25 -79.37 -461.27 -153.98 -694.63 -1545.3

3.Food products, beverages and tobacco 100.00 3454.88 -102.44 110.46 -111.66 895.93 894.73 -4147.1

4.Textiles, textile products, leather and footwear 100.00 -13.26 22.64 3.01 57.58 11.17 71.76 18.86

5.Wood and products of wood and cork 100.00 -24.17 77.90 9.02 4.29 57.09 70.40 25.33

6.Pulp, paper, paper products, printing and publishing 100.00 51.59 -11.93 -17.23 40.64 4.56 27.96 32.37

7.Coke, refined petroleum products and nuclear fuel 100.00 42.82 -0.52 -10.92 64.50 -1.04 52.54 5.16

8.Chemicals and chemical products 100.00 17.05 -1.92 0.56 83.99 -4.26 80.29 4.58

9.Rubber and plastics products 100.00 -19.35 17.73 8.97 53.22 24.53 86.72 14.90

10.Other non-metallic mineral products 100.00 -255.81 127.62 45.70 49.78 124.52 220.00 8.19

11.Basic metals and fabricated metal products 100.00 83.19 10.49 -16.79 146.52 -77.14 52.59 -46.26

12.Machinery, nec 100.00 10.49 2.22 0.28 47.22 27.20 74.70 12.60

13.Electrical and optical equipment 100.00 14.41 1.92 2.59 39.07 17.45 59.11 24.56

14.Transport equipment 100.00 41.11 -4.99 1.53 38.02 28.26 67.81 -3.93

15.Manufacturing nec; Recycling 100.00 -98.71 51.03 4.37 72.33 -0.23 76.47 71.21

16.Electricity, gas and water supply 100.00 38.73 -4.75 18.53 43.73 -13.88 48.38 17.65

Tertiary 17.Construction 100.00 -24.52 22.48 -0.38 46.04 33.29 78.95 23.09

18.Sale, maintenance and repair of motor vehicles 100.00 27.91 -30.01 2.46 21.76 14.77 38.99 63.11

19.Wholesale trade and commission trade 100.00 21.36 -1.25 2.26 8.43 14.13 24.82 55.06

20.Retail trade, except of motor vehicles and motorcycles 100.00 39.50 -5.19 7.23 5.54 24.76 37.53 28.16

21.Hotel and restaurants 100.00 25.97 33.88 -19.01 71.98 -17.93 35.04 5.11

22.Transport and storage 100.00 32.05 -13.95 -0.45 53.45 4.53 57.53 24.37

23.Post and telecommunications 100.00 21.98 -5.12 -0.90 -5.88 34.30 27.53 55.61

24.Financial intermediation 100.00 78.04 -9.36 0.90 0.18 38.73 39.81 -8.50

25.Real estate activities 100.00 146.93 1.30 1.02 -21.46 30.80 10.36 -58.59

26.Renting of m&eq and other business activities 100.00 20.99 44.45 -0.78 16.25 10.57 26.04 8.51

27.Public admin and defence; Compulsory social security 100.00 95.17 329.73 -13.93 -210.53 33.35 -191.11 -133.79

28.Education 100.00 12.89 22.57 1.25 6.78 14.47 22.50 42.04

29.Health and social work 100.00 31.11 56.98 2.35 14.01 21.66 38.01 -26.11

30.Other community, social and personal services 100.00 21.72 -1.10 0.95 3.74 30.47 35.16 44.22

31.Private households with employed persons 100.00 45.93 21.21 0.00 0.00 0.00 0.00 32.87 Note: GO means gross output; ConK, ConL and ConII mean contribution of capital, labor and intermediate inputs on gross output.

31

Figure 2: Industrial structure of Taiwan:1981-2010.

Figure 3a: Growth of Industry Value Added 1981-2010.

Figure 3b: Growth of Industry Value Added 1981-1990.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

Primary

Secondary

Tertiary

Manufacturing

32

Figure 3c: Growth of Industry Value Added 1991-2000.

Figure 3d: Growth of Industry Value Added 2001-2010.

Figure 4a: Growth of Industry Output 1982-2010.

33

Figure 4b: Growth of Industry Output 1982-1990.

Figure 4c: Growth of Industry Output 1991-2000.

Figure 4d: Growth of Industry Output 2001-2010.

34

Figure 5a: Growth of Industry Labor Input 1982-2010.

Figure 5b: Growth of Industry Capital Stock Input 1982-2010

35

Figure 5c: Growth of Industry Energy Input 1982-2010.

Figure 5d: Growth of Industry Material Input 1982-2010.

36

Figure 5e: Growth of Industry Service Input 1982-2010.

Figure 6a: Growth of Industry TFP 1982-1990.

37

Figure 6b: Growth of Industry TFP 1991-2000.

Figure 6c: Growth of Industry TFP 2001-2010.

38

Figure 6d: Growth of Industry TFP 1982-2010.

Figure 7 Sources of Industry Output Growth (in growth rate): 1982-2010

-0.1

-0.05

0

0.05

0.1

0.15

0.2

1982-2010

TFP

ConS

ConM

ConE

ConL

ConK