Embed Size (px)

Citation preview

Industrials SectorJason Kraynak and Wade Guzdanski

Agenda Overview Business Analysis Economic Analysis Financial Analysis Valuation Analysis Recommendation

Overview

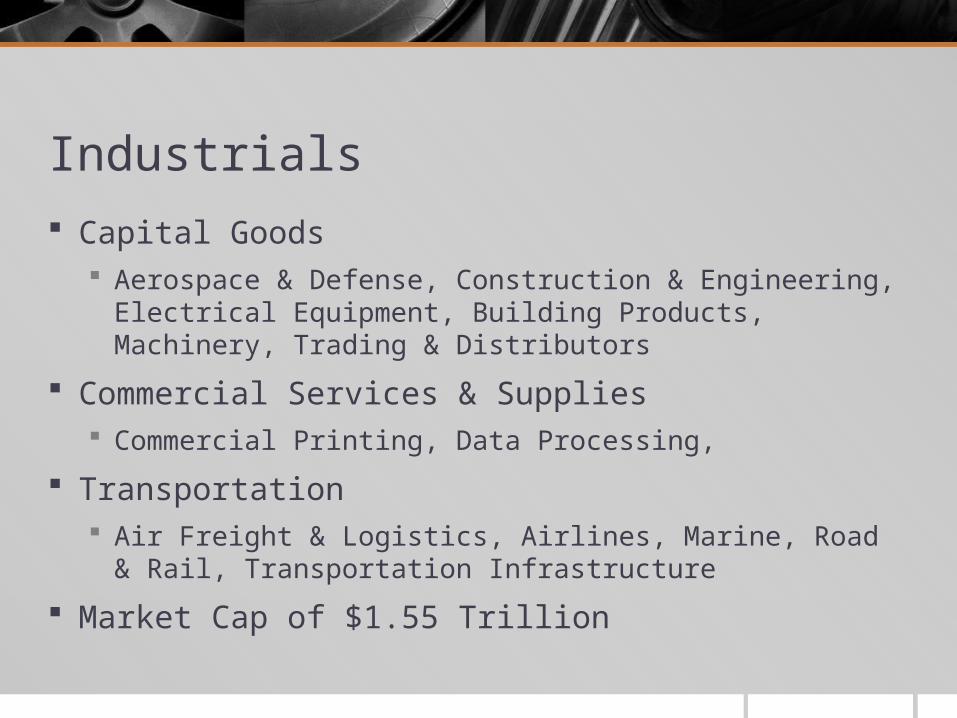

Industrials Capital Goods

Aerospace & Defense, Construction & Engineering, Electrical Equipment, Building Products, Machinery, Trading & Distributors

Commercial Services & Supplies Commercial Printing, Data Processing,

Transportation Air Freight & Logistics, Airlines, Marine, Road & Rail,

Transportation Infrastructure

Market Cap of $1.55 Trillion

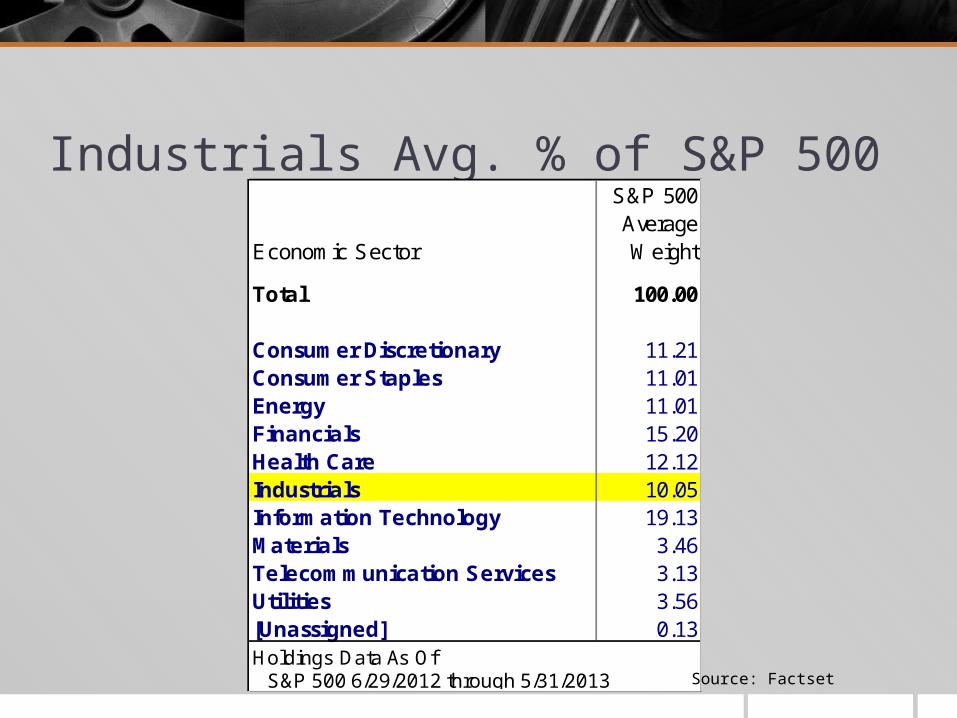

Industrials Avg. % of S&P 500S&P 500Average

Economic Sector Weight

Total 100.00

Consumer Discretionary 11.21Consumer Staples 11.01Energy 11.01Financials 15.20Health Care 12.12Industrials 10.05Information Technology 19.13Materials 3.46Telecommunication Services 3.13Utilities 3.56[Unassigned] 0.13Holdings Data As Of S&P 500 6/29/2012 through 5/31/2013 Source: Factset

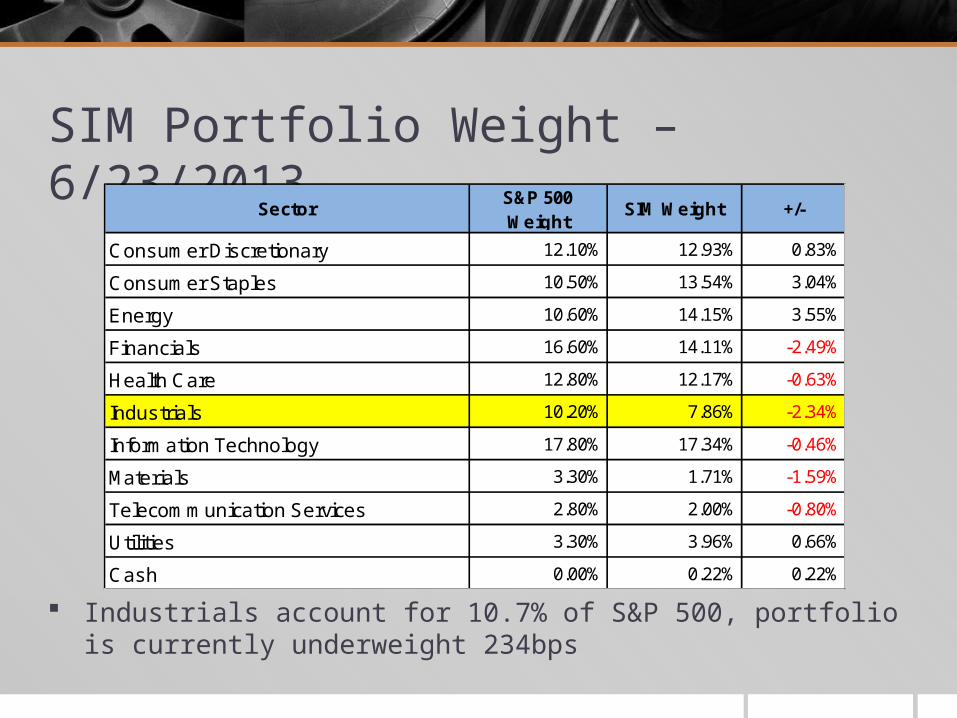

SIM Portfolio Weight – 6/23/2013

Industrials account for 10.7% of S&P 500, portfolio is currently underweight 234bps

SectorS&P 500 Weight

SIM Weight +/-

Consumer Discretionary 12.10% 12.93% 0.83%

Consumer Staples 10.50% 13.54% 3.04%

Energy 10.60% 14.15% 3.55%

Financials 16.60% 14.11% -2.49%

Health Care 12.80% 12.17% -0.63%

Industrials 10.20% 7.86% -2.34%

Information Technology 17.80% 17.34% -0.46%

Materials 3.30% 1.71% -1.59%

Telecommunication Services 2.80% 2.00% -0.80%

Utilities 3.30% 3.96% 0.66%

Cash 0.00% 0.22% 0.22%

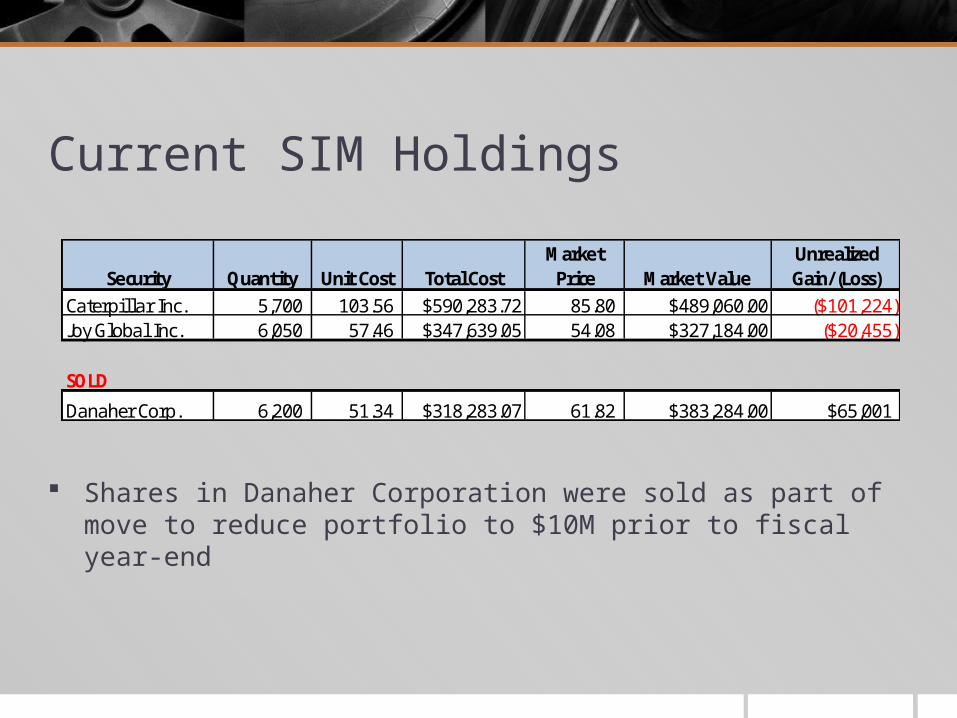

Current SIM Holdings

Shares in Danaher Corporation were sold as part of move to reduce portfolio to $10M prior to fiscal year-end

Security Quantity Unit Cost Total CostMarket

Price Market Value Unrealized Gain/(Loss)

Caterpil lar Inc. 5,700 103.56 $590,283.72 85.80 $489,060.00 ($101,224)Joy Global Inc. 6,050 57.46 $347,639.05 54.08 $327,184.00 ($20,455)

SOLD

Danaher Corp. 6,200 51.34 $318,283.07 61.82 $383,284.00 $65,001

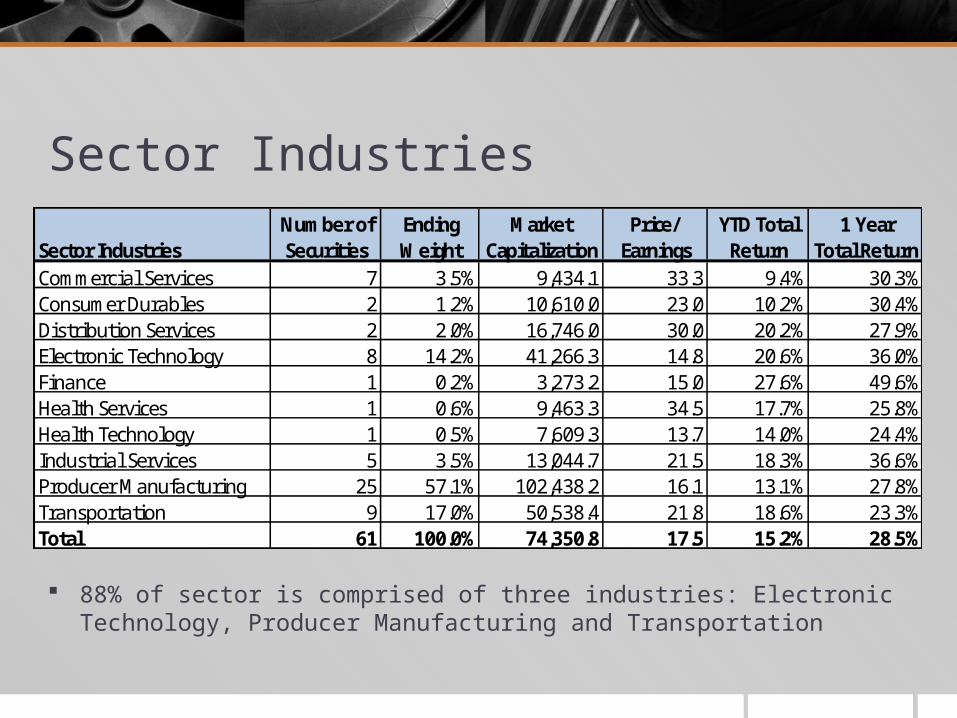

Sector Industries

88% of sector is comprised of three industries: Electronic Technology, Producer Manufacturing and Transportation

Number of Ending Market Price/ YTD Total 1 YearSector Industries Securities Weight Capitalization Earnings Return Total ReturnCommercial Services 7 3.5% 9,434.1 33.3 9.4% 30.3%Consumer Durables 2 1.2% 10,610.0 23.0 10.2% 30.4%Distribution Services 2 2.0% 16,746.0 30.0 20.2% 27.9%Electronic Technology 8 14.2% 41,266.3 14.8 20.6% 36.0%Finance 1 0.2% 3,273.2 15.0 27.6% 49.6%Health Services 1 0.6% 9,463.3 34.5 17.7% 25.8%Health Technology 1 0.5% 7,609.3 13.7 14.0% 24.4%Industrial Services 5 3.5% 13,044.7 21.5 18.3% 36.6%Producer Manufacturing 25 57.1% 102,438.2 16.1 13.1% 27.8%Transportation 9 17.0% 50,538.4 21.8 18.6% 23.3%Total 61 100.0% 74,350.8 17.5 15.2% 28.5%

Largest CompaniesMarket Ending

Rank Security Ticker Cap. ($) Weight1 General Electric Co. GE 241,131.6 16.4%2 United Technologies Corp. UTX 87,241.6 5.4%3 Union Pacific Corp. UNP 72,228.9 4.9%4 3M Co. MMM 76,107.8 4.7%5 Boeing Co. BA 75,089.0 4.6%6 Honeywell International Inc. HON 61,731.1 4.2%7 United Parcel Service Inc. UPS 81,089.6 4.2%8 Caterpillar Inc. CAT 56,412.2 3.8%9 Emerson Electric Co. EMR 41,412.0 2.8%

10 Danaher Corp. DHR 48,219.6 2.4%

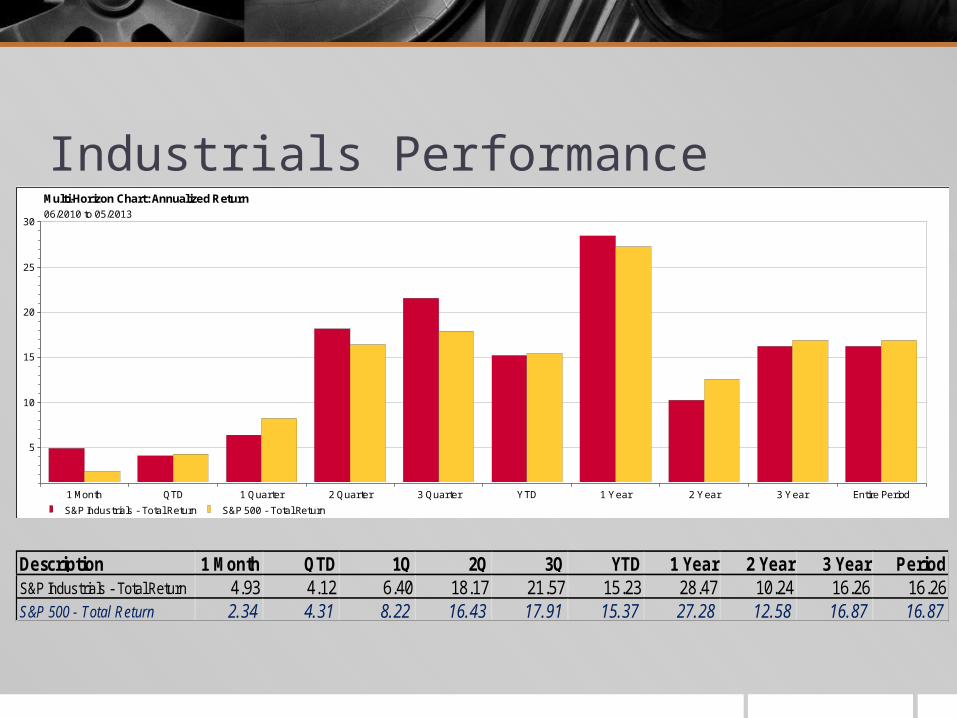

Industrials Performance

1 Month QTD 1 Quarter 2 Quarter 3 Quarter YTD 1 Year 2 Year 3 Year Entire Period

5

10

15

20

25

30

Multi-Horizon Chart: Annualized Return06/2010 to 05/2013

S&P Industrials - Total Return S&P 500 - Total Return

Description 1 Month QTD 1Q 2Q 3Q YTD 1 Year 2 Year 3 Year PeriodS&P Industrials - Total Return 4.93 4.12 6.40 18.17 21.57 15.23 28.47 10.24 16.26 16.26S&P 500 - Total Return 2.34 4.31 8.22 16.43 17.91 15.37 27.28 12.58 16.87 16.87

Business Analysis

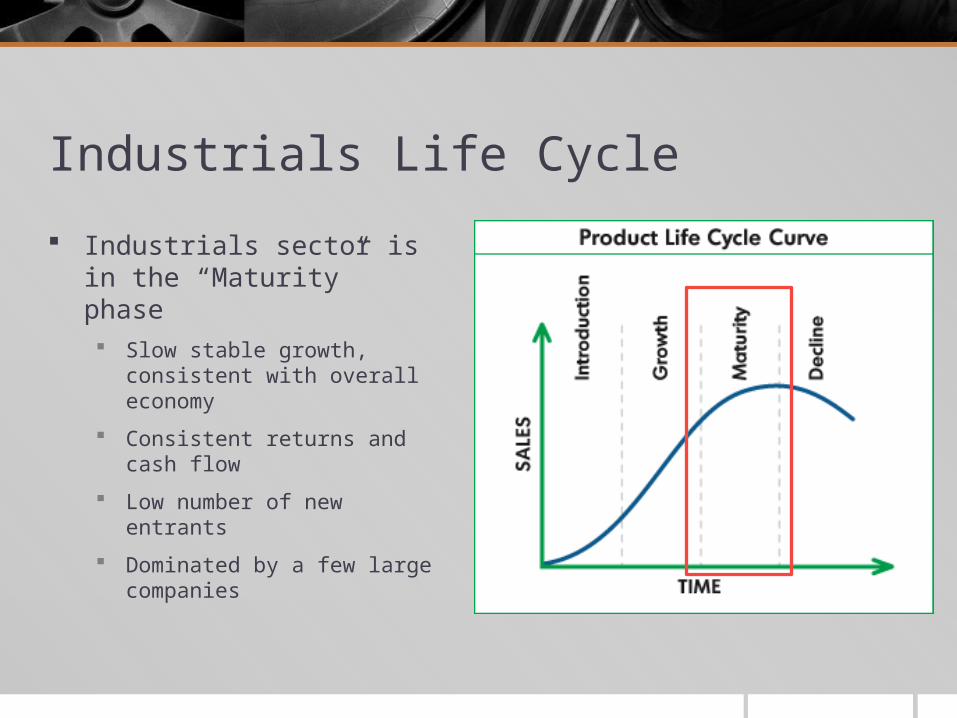

Industrials Life Cycle

Industrials sector is in the “Maturity” phase Slow stable growth, consistent with

overall economy

Consistent returns and cash flow

Low number of new entrants

Dominated by a few large companies

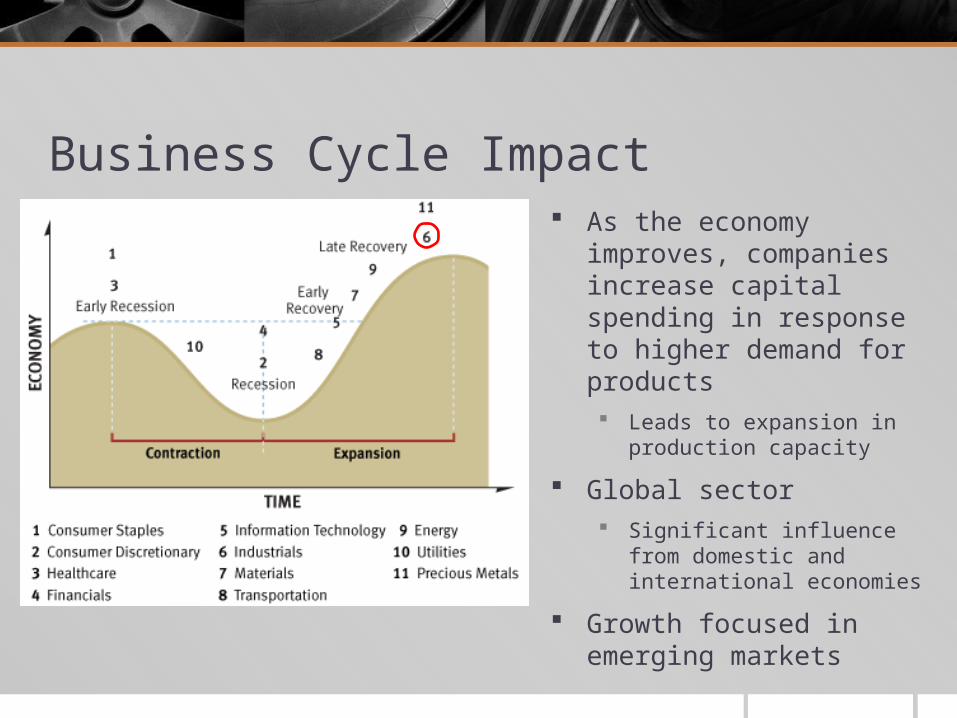

Business Cycle Impact As the economy improves,

companies increase capital spending in response to higher demand for products Leads to expansion in production

capacity

Global sector Significant influence from domestic

and international economies

Growth focused in emerging markets

Catalysts & Risks Catalysts

Europe coming out of their recession

Turnaround in China

Growth in emerging markets

Risks Lower government spending

Strengthening US Dollar

Uncertainty regarding monetary policy

Slow global growth forecast

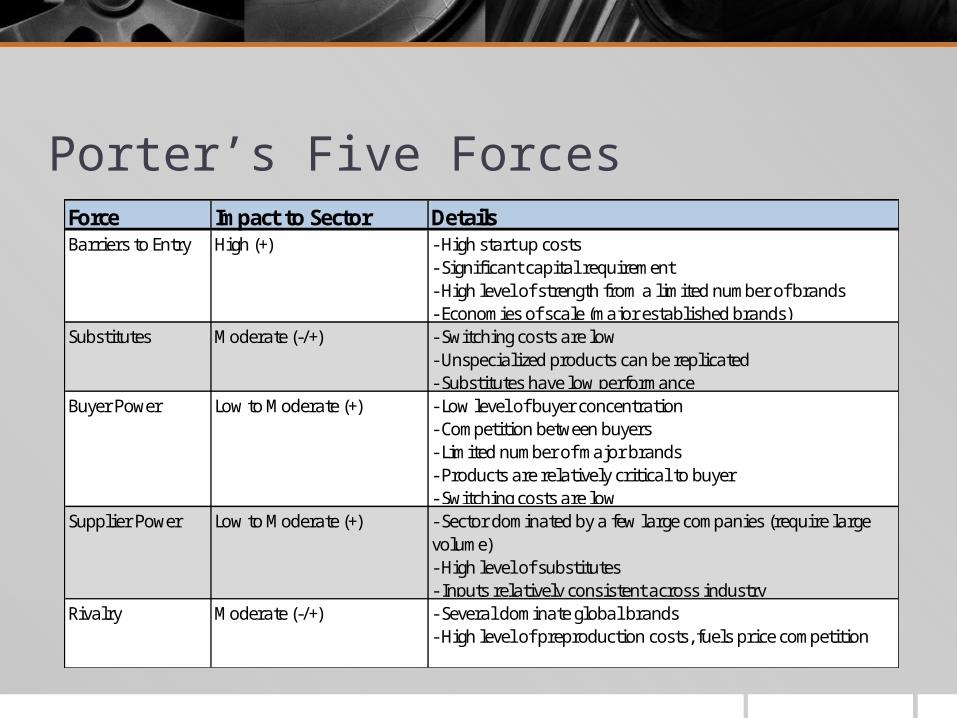

Porter’s Five ForcesForce Impact to Sector DetailsBarriers to Entry High (+) - High start up costs

- Significant capital requirement- High level of strength from a l imited number of brands- Economies of scale (major established brands)

Substitutes Moderate (-/+) - Switching costs are low- Unspecialized products can be replicated- Substitutes have low performance

Buyer Power Low to Moderate (+) - Low level of buyer concentration- Competition between buyers- Limited number of major brands- Products are relatively critical to buyer- Switching costs are low

Supplier Power Low to Moderate (+) - Sector dominated by a few large companies (require large volume)- High level of substitutes- Inputs relatively consistent across industry

Rivalry Moderate (-/+) - Several dominate global brands- High level of preproduction costs, fuels price competition

Economic Analysis

Industrials Drivers High Correlation to overall equity market

Production & Manufacturing

GDP

Unemployment

Crude Oil

Housing

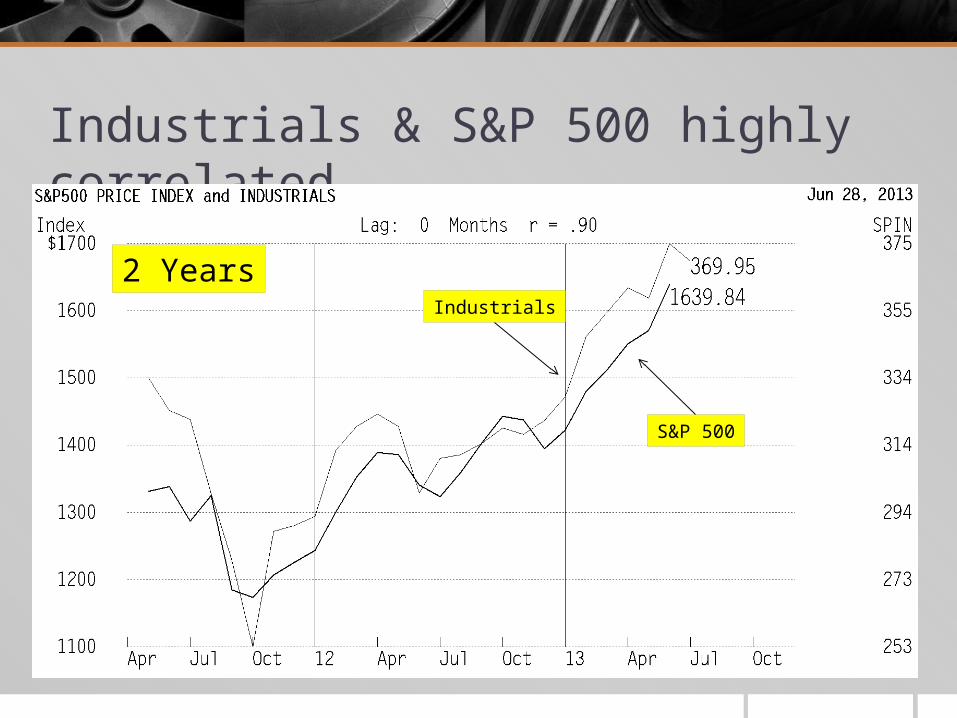

Industrials & S&P 500 highly correlated

10 YearsIndustrials

S&P 500

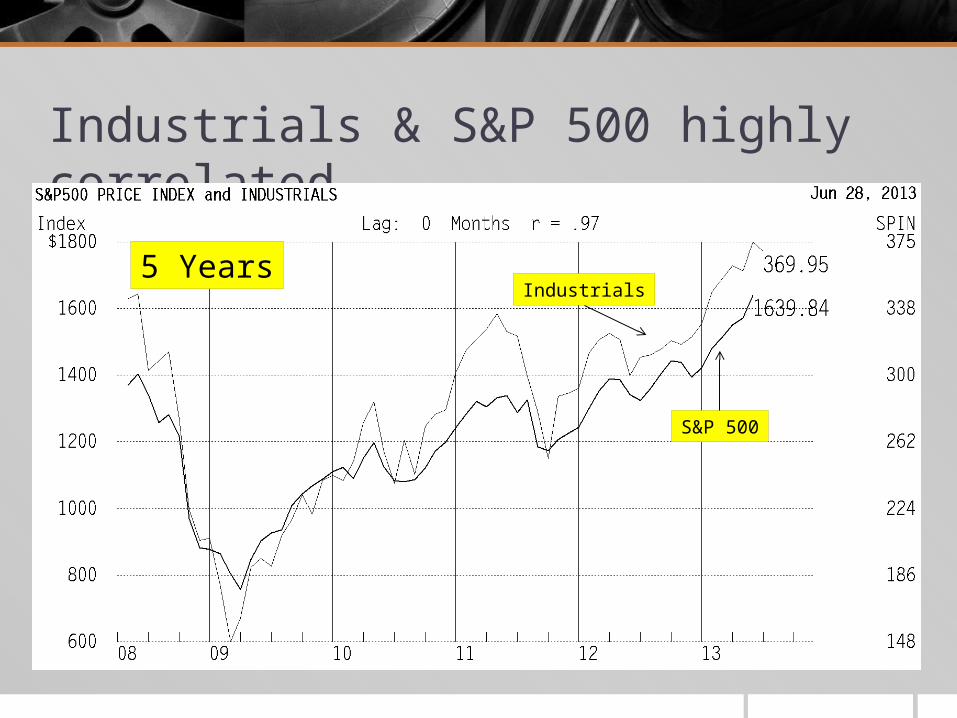

Industrials & S&P 500 highly correlated

5 YearsIndustrials

S&P 500

Industrials & S&P 500 highly correlated

2 YearsIndustrials

S&P 500

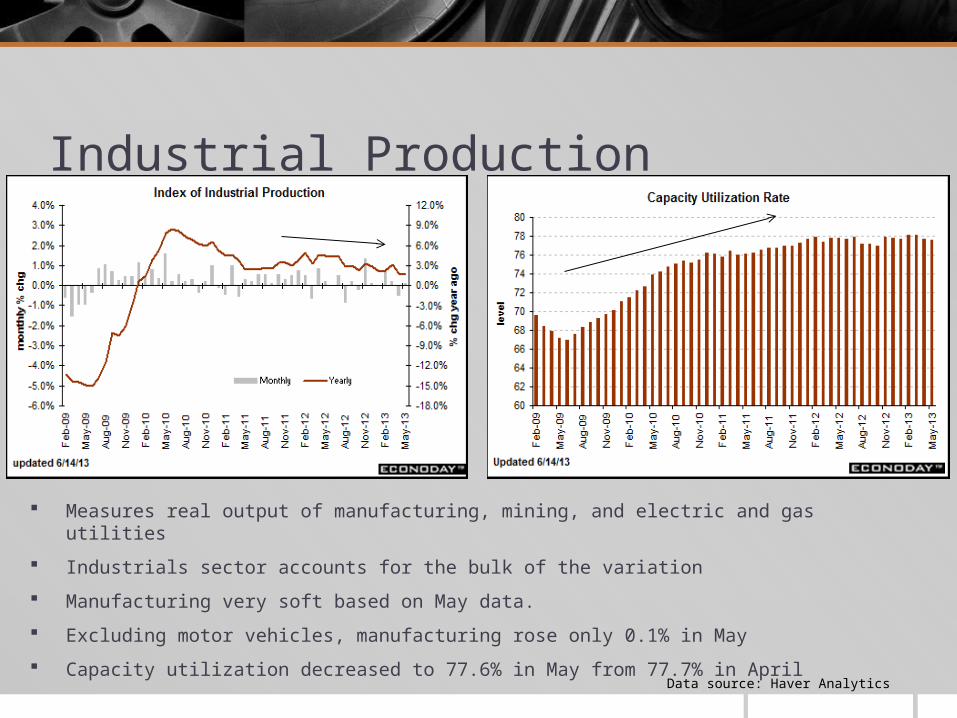

Industrial Production

Measures real output of manufacturing, mining, and electric and gas utilities

Industrials sector accounts for the bulk of the variation

Manufacturing very soft based on May data.

Excluding motor vehicles, manufacturing rose only 0.1% in May

Capacity utilization decreased to 77.6% in May from 77.7% in April

Data source: Haver Analytics

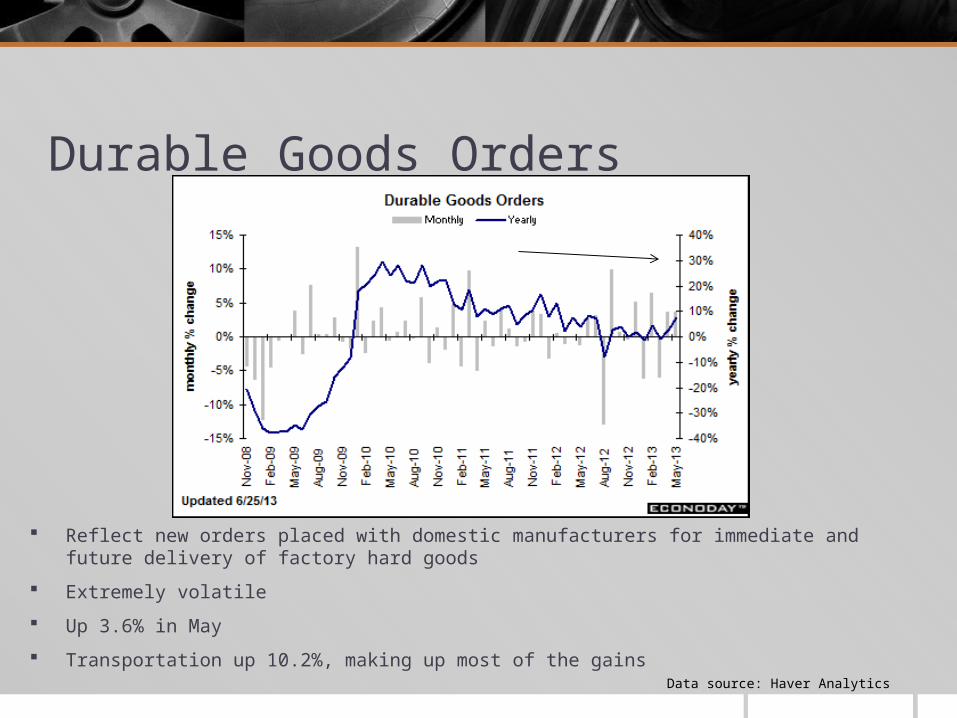

Durable Goods Orders

Data source: Haver Analytics

Reflect new orders placed with domestic manufacturers for immediate and future delivery of factory hard goods

Extremely volatile

Up 3.6% in May

Transportation up 10.2%, making up most of the gains

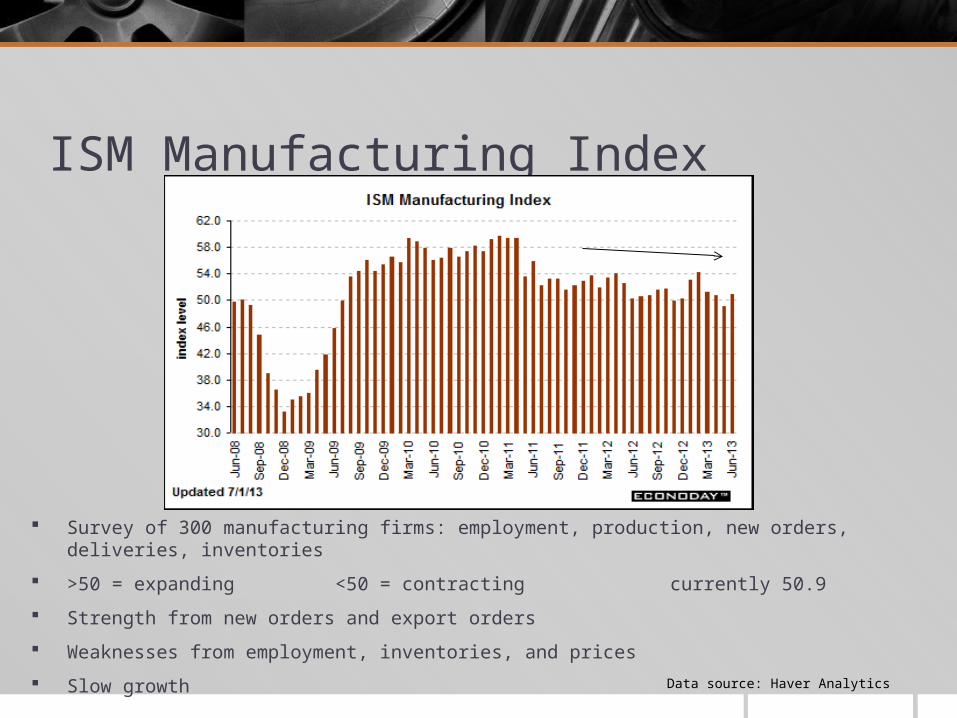

ISM Manufacturing Index

Data source: Haver Analytics

Survey of 300 manufacturing firms: employment, production, new orders, deliveries, inventories

>50 = expanding <50 = contracting currently 50.9

Strength from new orders and export orders

Weaknesses from employment, inventories, and prices

Slow growth

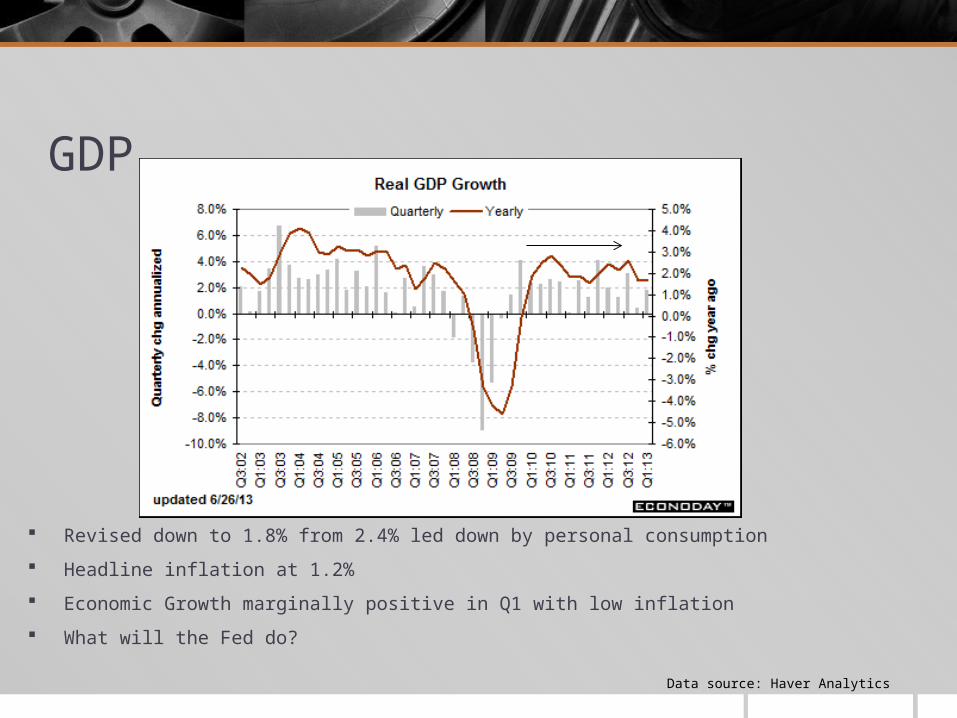

GDP

Data source: Haver Analytics

Revised down to 1.8% from 2.4% led down by personal consumption

Headline inflation at 1.2%

Economic Growth marginally positive in Q1 with low inflation

What will the Fed do?

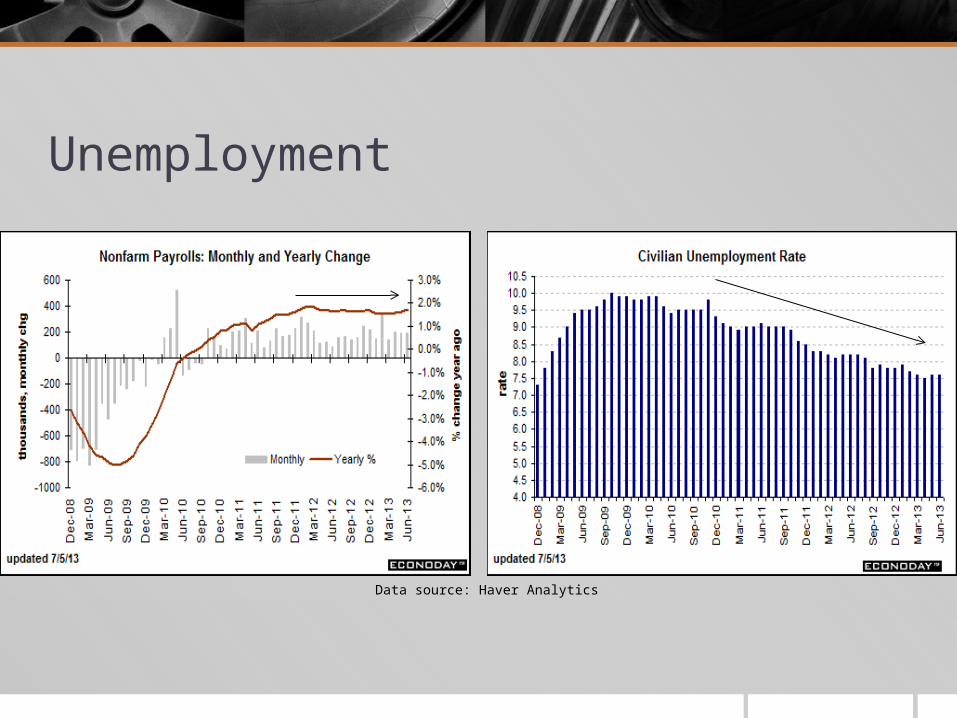

Unemployment

Data source: Haver Analytics

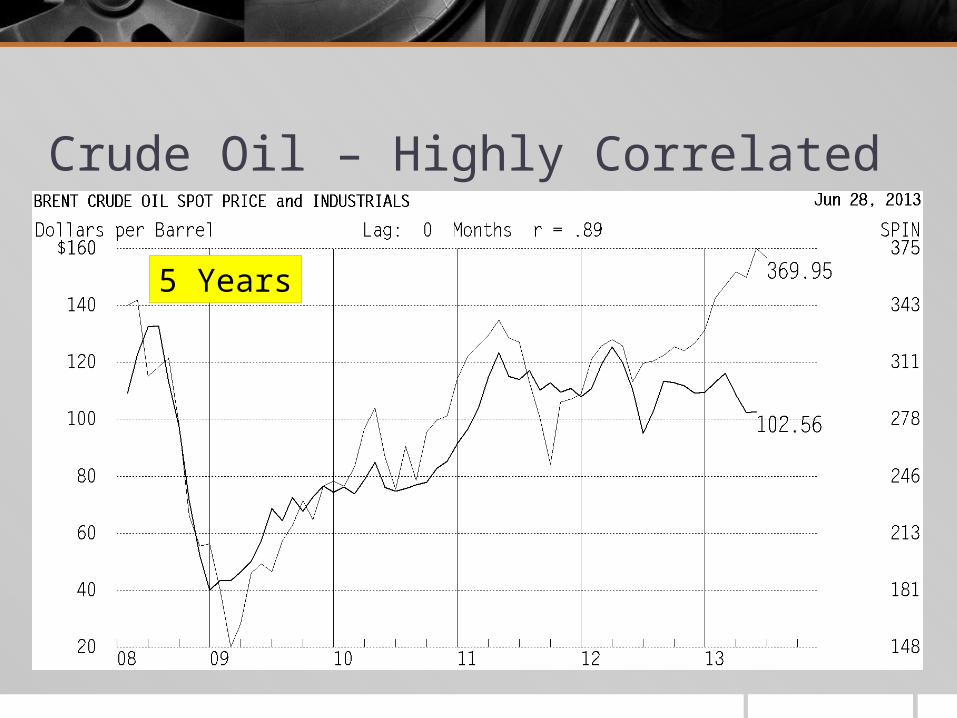

Crude Oil – Highly Correlated

5 Years

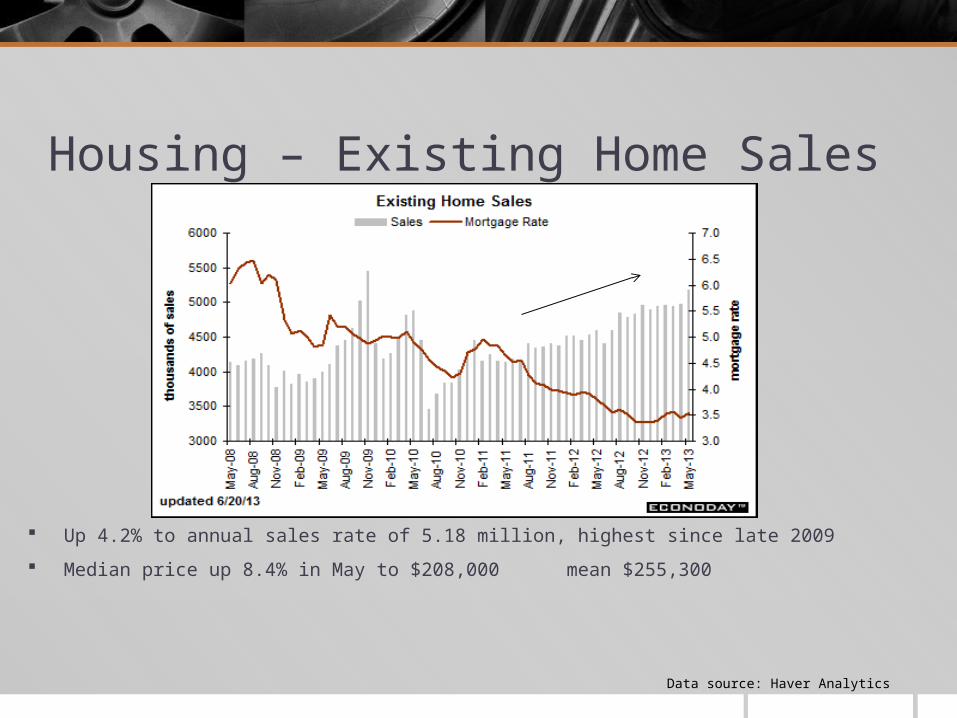

Housing – Existing Home Sales

Data source: Haver Analytics

Up 4.2% to annual sales rate of 5.18 million, highest since late 2009

Median price up 8.4% in May to $208,000 mean $255,300

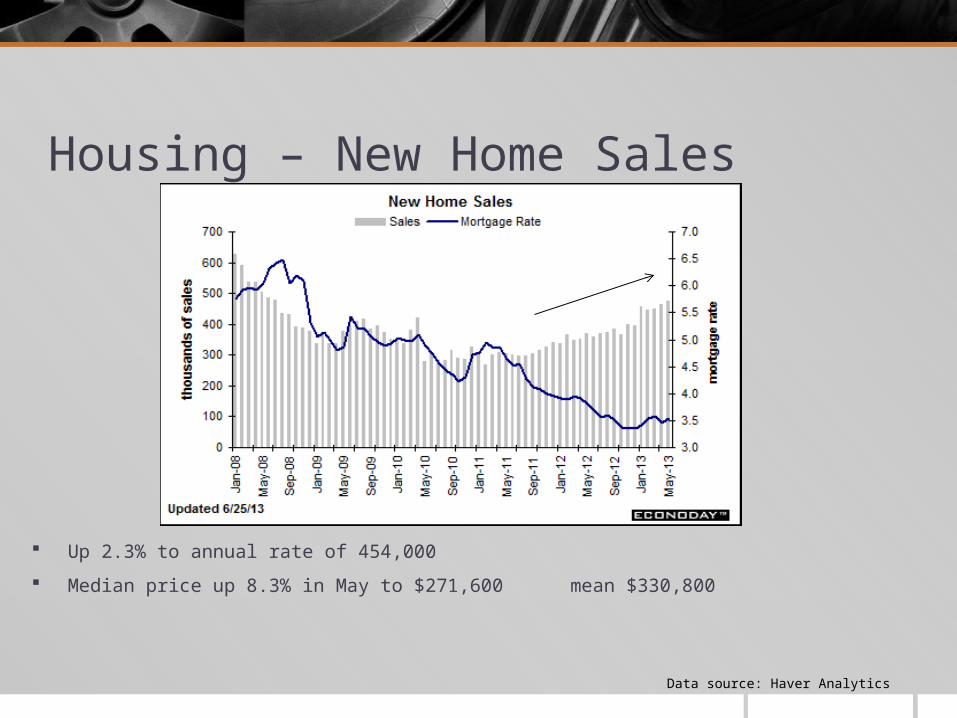

Housing – New Home Sales

Data source: Haver Analytics

Up 2.3% to annual rate of 454,000

Median price up 8.3% in May to $271,600 mean $330,800

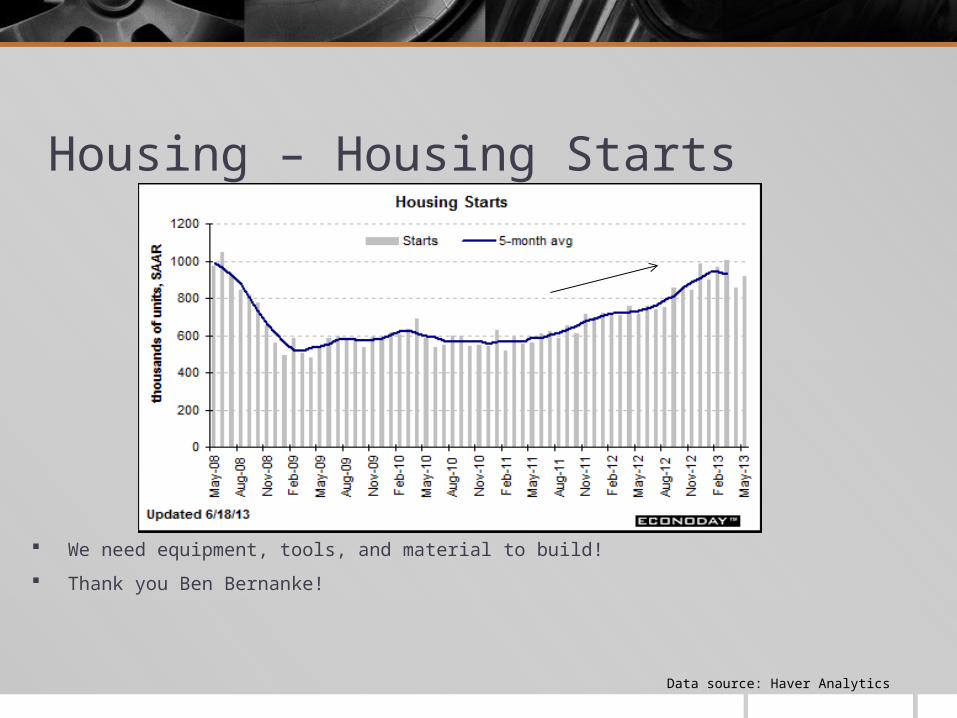

Housing – Housing Starts

Data source: Haver Analytics

We need equipment, tools, and material to build!

Thank you Ben Bernanke!

Financial Analysis

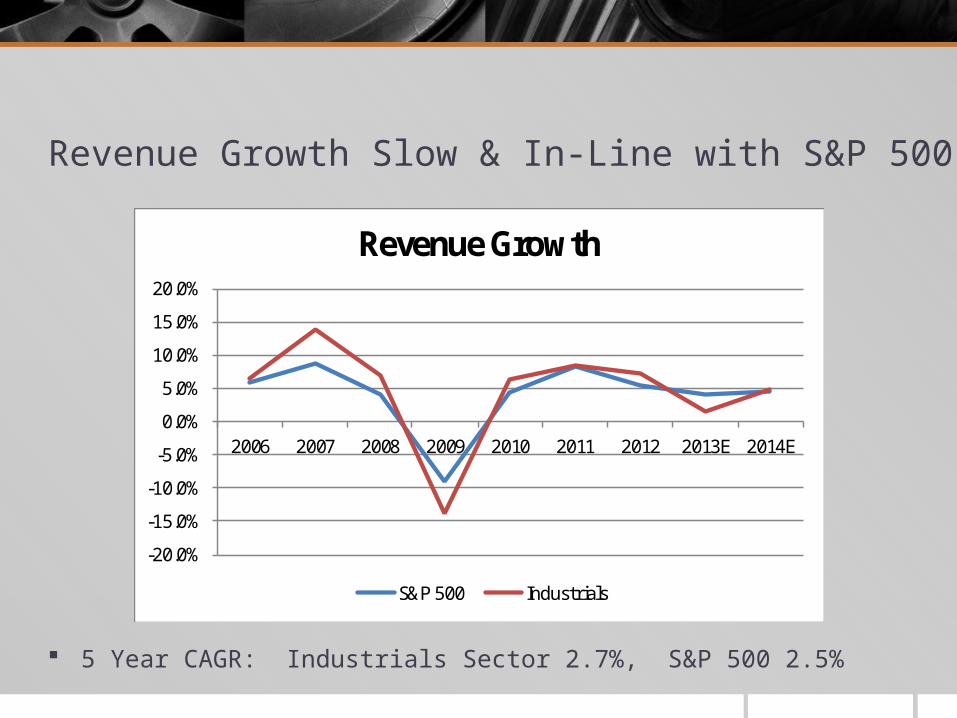

Revenue Growth Slow & In-Line with S&P 500

5 Year CAGR: Industrials Sector 2.7%, S&P 500 2.5%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Revenue Growth

S&P 500 Industrials

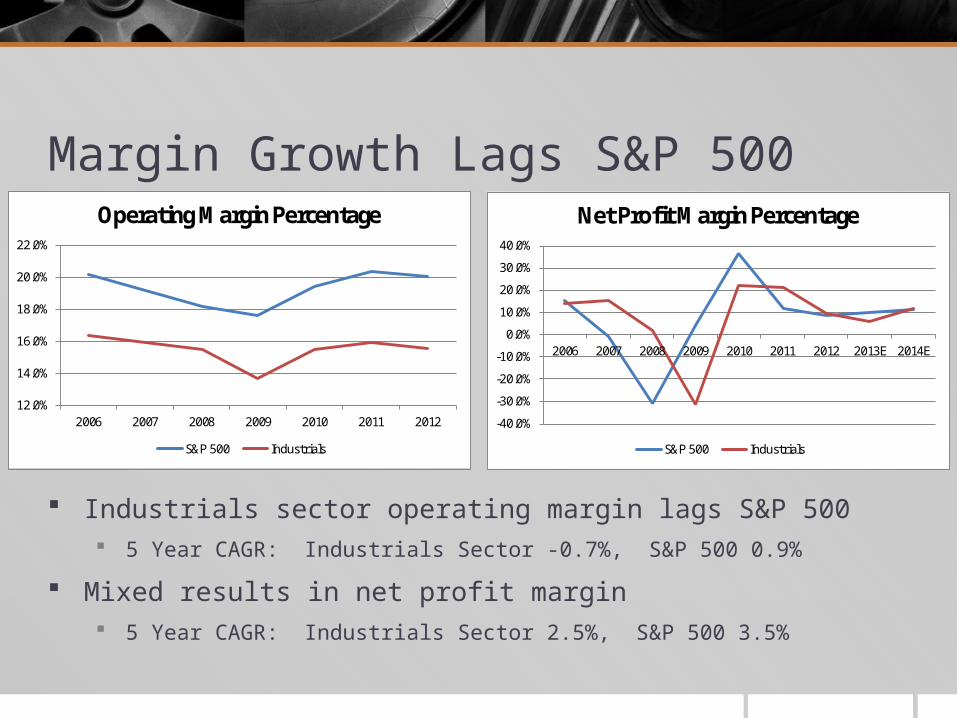

Margin Growth Lags S&P 500

Industrials sector operating margin lags S&P 500 5 Year CAGR: Industrials Sector -0.7%, S&P 500 0.9%

Mixed results in net profit margin 5 Year CAGR: Industrials Sector 2.5%, S&P 500 3.5%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

2006 2007 2008 2009 2010 2011 2012

Operating Margin Percentage

S&P 500 Industrials

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Net Profit Margin Percentage

S&P 500 Industrials

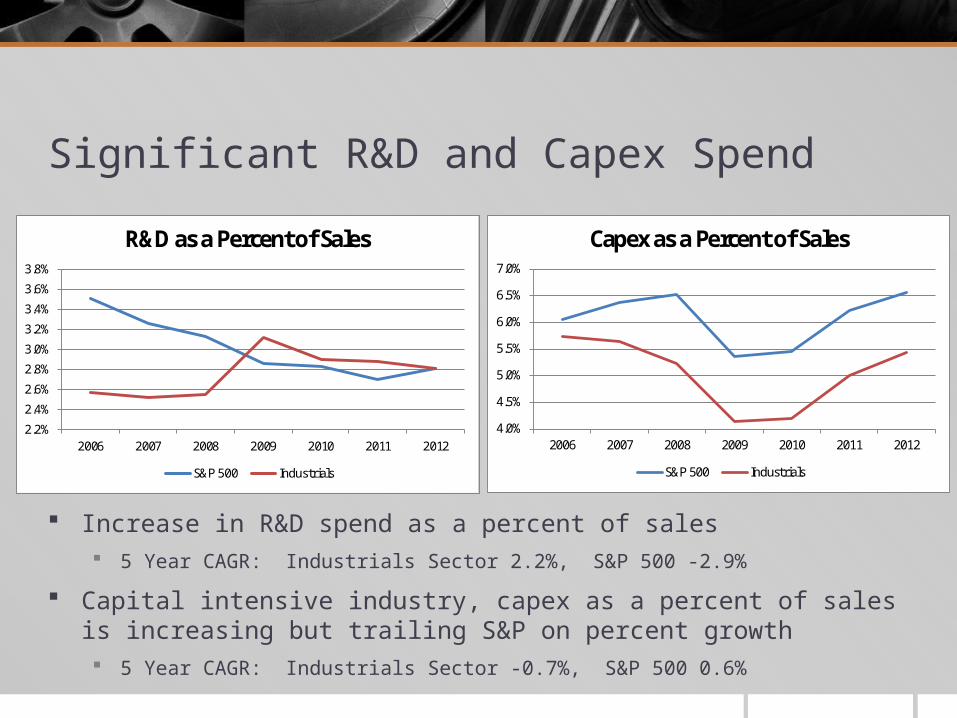

Significant R&D and Capex Spend

Increase in R&D spend as a percent of sales 5 Year CAGR: Industrials Sector 2.2%, S&P 500 -2.9%

Capital intensive industry, capex as a percent of sales is increasing but trailing S&P on percent growth 5 Year CAGR: Industrials Sector -0.7%, S&P 500 0.6%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

3.6%

3.8%

2006 2007 2008 2009 2010 2011 2012

R&D as a Percent of Sales

S&P 500 Industrials

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

2006 2007 2008 2009 2010 2011 2012

Capex as a Percent of Sales

S&P 500 Industrials

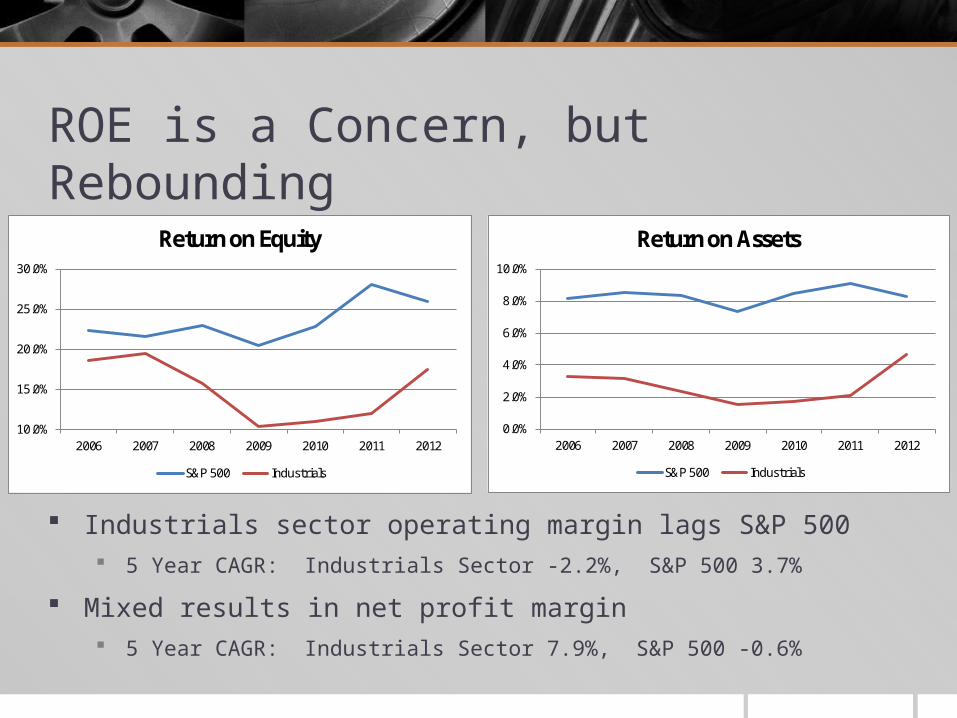

ROE is a Concern, but Rebounding

Industrials sector operating margin lags S&P 500 5 Year CAGR: Industrials Sector -2.2%, S&P 500 3.7%

Mixed results in net profit margin 5 Year CAGR: Industrials Sector 7.9%, S&P 500 -0.6%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012

Return on Equity

S&P 500 Industrials

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2006 2007 2008 2009 2010 2011 2012

Return on Assets

S&P 500 Industrials

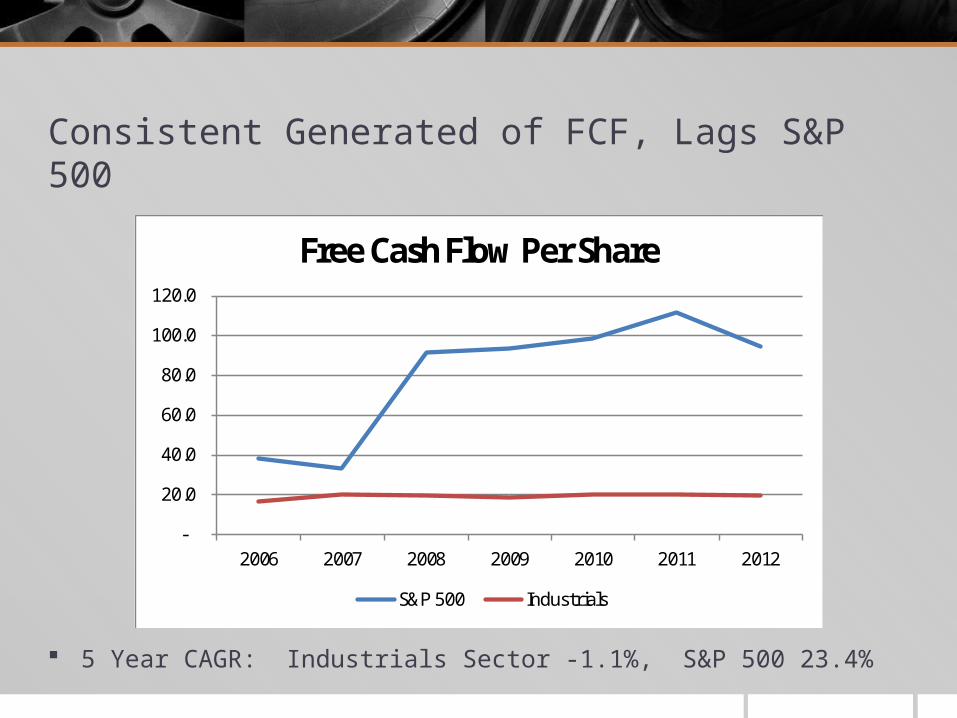

Consistent Generated of FCF, Lags S&P 500

5 Year CAGR: Industrials Sector -1.1%, S&P 500 23.4%

-

20.0

40.0

60.0

80.0

100.0

120.0

2006 2007 2008 2009 2010 2011 2012

Free Cash Flow Per Share

S&P 500 Industrials

Valuation Analysis

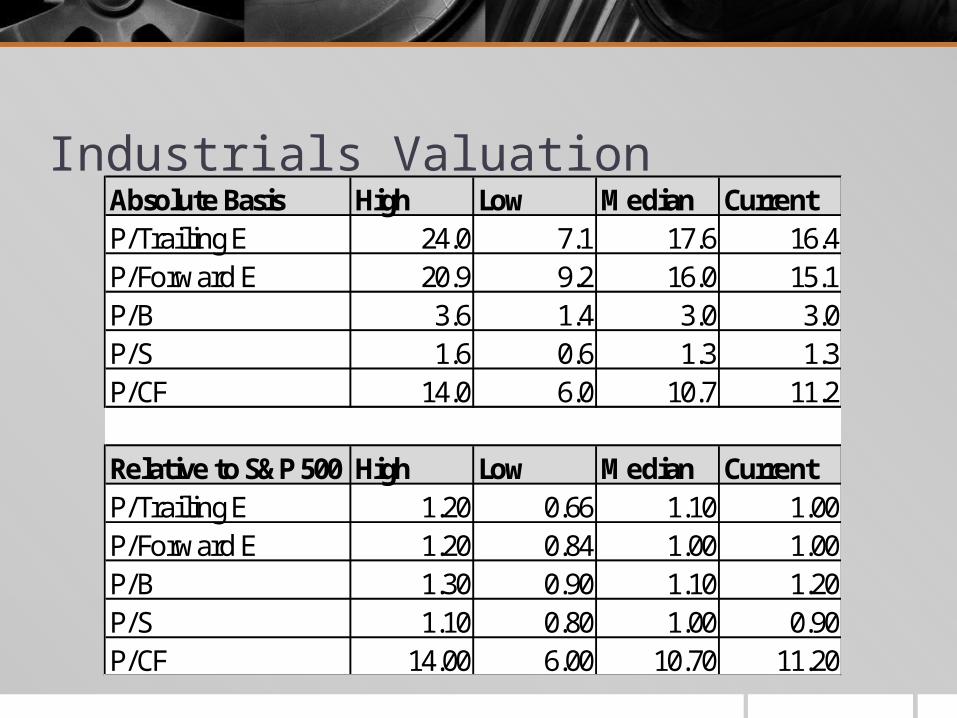

Industrials ValuationAbsolute Basis High Low Median CurrentP/Trailing E 24.0 7.1 17.6 16.4P/Forward E 20.9 9.2 16.0 15.1P/B 3.6 1.4 3.0 3.0P/S 1.6 0.6 1.3 1.3P/CF 14.0 6.0 10.7 11.2

Relative to S&P 500 High Low Median CurrentP/Trailing E 1.20 0.66 1.10 1.00P/Forward E 1.20 0.84 1.00 1.00P/B 1.30 0.90 1.10 1.20P/S 1.10 0.80 1.00 0.90P/CF 14.00 6.00 10.70 11.20

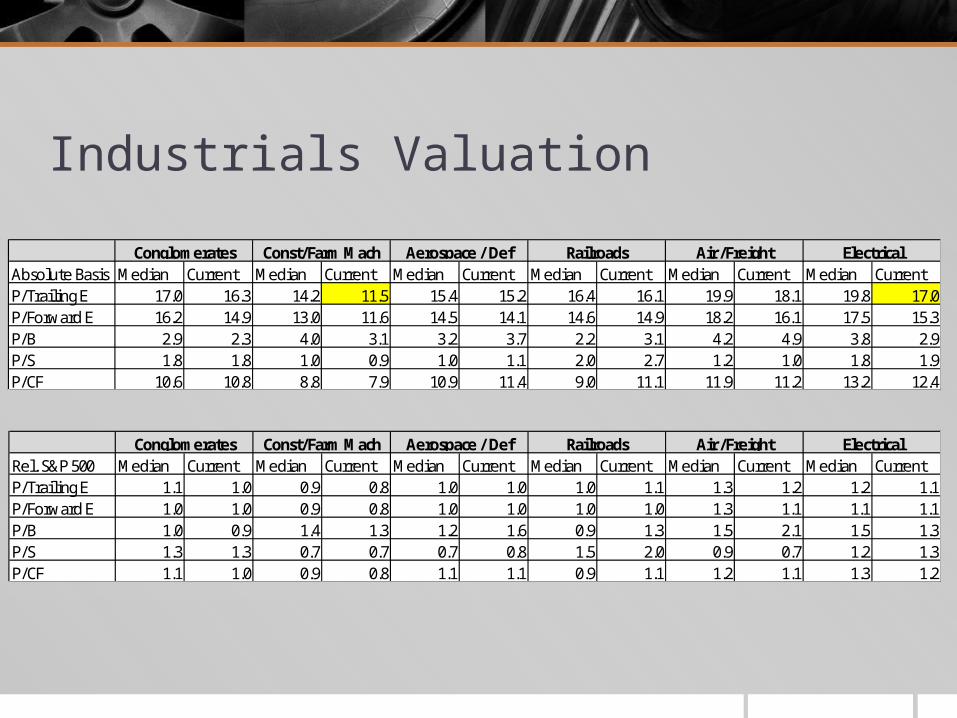

Industrials Valuation

Absolute Basis Median Current Median Current Median Current Median Current Median Current Median CurrentP/Trailing E 17.0 16.3 14.2 11.5 15.4 15.2 16.4 16.1 19.9 18.1 19.8 17.0P/Forward E 16.2 14.9 13.0 11.6 14.5 14.1 14.6 14.9 18.2 16.1 17.5 15.3P/B 2.9 2.3 4.0 3.1 3.2 3.7 2.2 3.1 4.2 4.9 3.8 2.9P/S 1.8 1.8 1.0 0.9 1.0 1.1 2.0 2.7 1.2 1.0 1.8 1.9P/CF 10.6 10.8 8.8 7.9 10.9 11.4 9.0 11.1 11.9 11.2 13.2 12.4

Railroads Air /Freight ElectricalAerospace / DefConst/Farm MachConglomerates

Rel. S&P 500 Median Current Median Current Median Current Median Current Median Current Median CurrentP/Trailing E 1.1 1.0 0.9 0.8 1.0 1.0 1.0 1.1 1.3 1.2 1.2 1.1P/Forward E 1.0 1.0 0.9 0.8 1.0 1.0 1.0 1.0 1.3 1.1 1.1 1.1P/B 1.0 0.9 1.4 1.3 1.2 1.6 0.9 1.3 1.5 2.1 1.5 1.3P/S 1.3 1.3 0.7 0.7 0.7 0.8 1.5 2.0 0.9 0.7 1.2 1.3P/CF 1.1 1.0 0.9 0.8 1.1 1.1 0.9 1.1 1.2 1.1 1.3 1.2

Railroads Air /Freight ElectricalAerospace / DefConst/Farm MachConglomerates

Recommendation

Recommendation Currently -234bps underweight

We recommend no change in weighting of industrials

Reasons for concern Slow global growth

GDP forecasts

Economy is still early in recovery phase

Foreign political uprisings

Low growth potential – valuation suggests sector is inline

Why we may be wrong Recent housing recovery

Possible energy independence (lower production costs = higher margins)

Faster economic expansion

Consumer sentiment

Questions?