Embed Size (px)

Citation preview

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 1/21

GLOBAL EMERGING MARKET STRA

EEEmmmeeerrrgggiii

AAsssseett AAlllloocc

Global E

Infl

Africa Emerging Capital (AEC) AssetFebruary 2011Olivier M. Lumenganeso

[email protected] Nyon – Switzerland

EGY

ggg CCCaaapppiiitttaaalll

ttiioonn,, wwiisshhiinngg ttoo sseeiizzee AAf f rriiccaann eemmeerrggiinngg ooppppoorrttuunnii

erging Markets Stra

tionary Exuberance

Allocation

Page 1

ttiieess

egy

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 2/21

GLOBAL EMERGING MARKET STRATEGY Page 2

Global Emerging Markets StrategyInflationary Exuberance

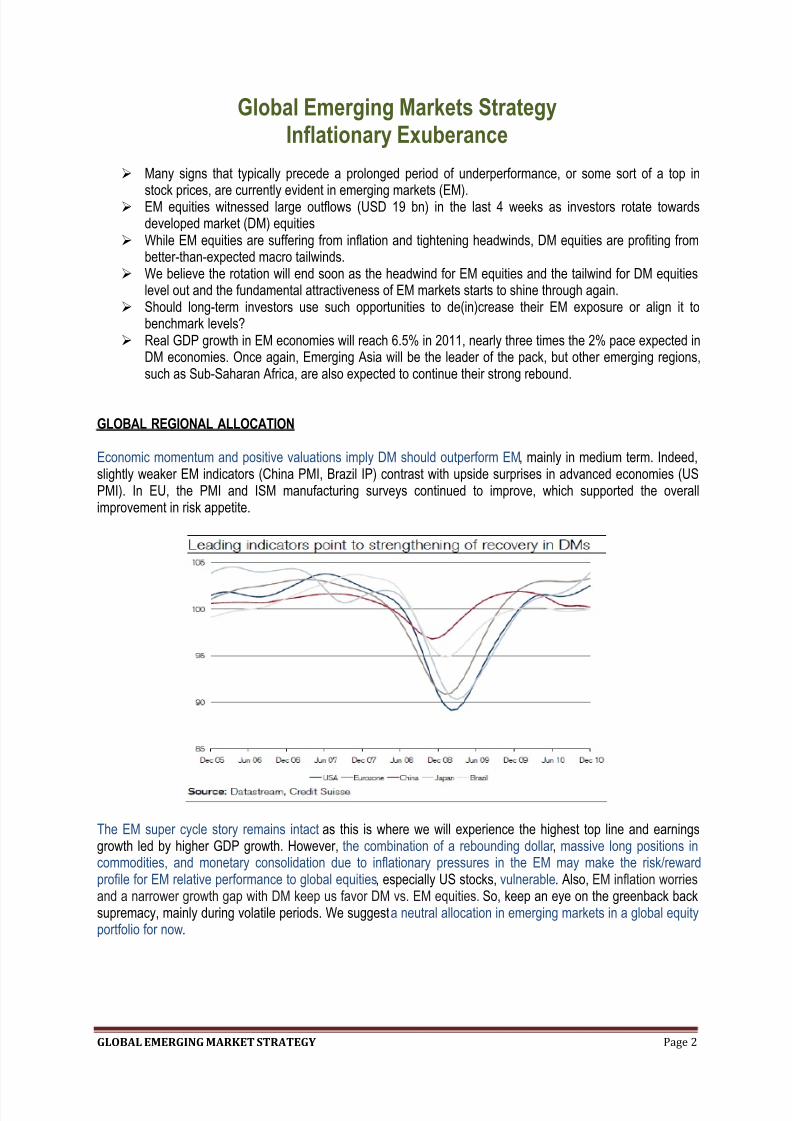

Many signs that typically precede a prolonged period of underperformance, or some sort of a top in

stock prices, are currently evident in emerging markets (EM). EM equities witnessed large outflows (USD 19 bn) in the last 4 weeks as investors rotate towardsdeveloped market (DM) equities

While EM equities are suffering from inflation and tightening headwinds, DM equities are profiting frombetter-than-expected macro tailwinds.

We believe the rotation will end soon as the headwind for EM equities and the tailwind for DM equitieslevel out and the fundamental attractiveness of EM markets starts to shine through again.

Should long-term investors use such opportunities to de(in)crease their EM exposure or align it tobenchmark levels?

Real GDP growth in EM economies will reach 6.5% in 2011, nearly three times the 2% pace expected inDM economies. Once again, Emerging Asia will be the leader of the pack, but other emerging regions,such as Sub-Saharan Africa, are also expected to continue their strong rebound.

GLOBAL REGIONAL ALLOCATION

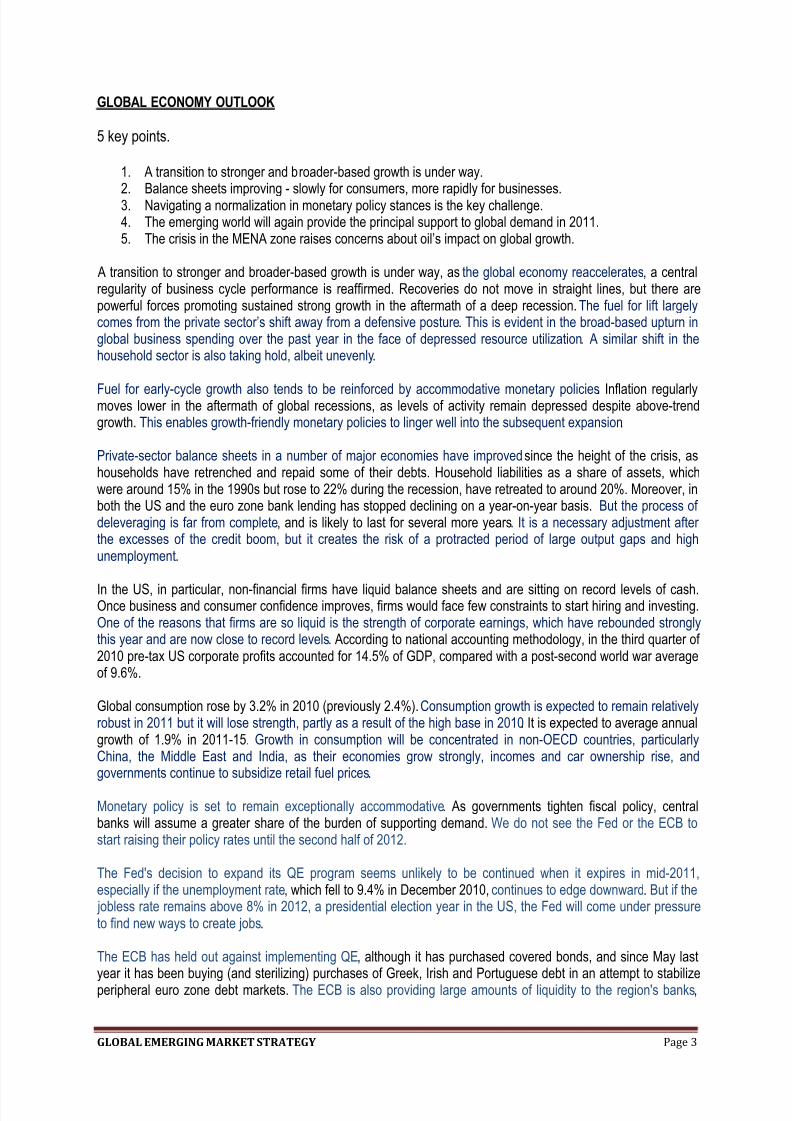

Economic momentum and positive valuations imply DM should outperform EM, mainly in medium term. Indeed,slightly weaker EM indicators (China PMI, Brazil IP) contrast with upside surprises in advanced economies (USPMI). In EU, the PMI and ISM manufacturing surveys continued to improve, which supported the overallimprovement in risk appetite.

The EM super cycle story remains intact as this is where we will experience the highest top line and earningsgrowth led by higher GDP growth. However, the combination of a rebounding dollar , massive long positions incommodities, and monetary consolidation due to inflationary pressures in the EM may make the risk/rewardprofile for EM relative performance to global equities, especially US stocks, vulnerable. Also, EM inflation worriesand a narrower growth gap with DM keep us favor DM vs. EM equities. So, keep an eye on the greenback backsupremacy, mainly during volatile periods. We suggest a neutral allocation in emerging markets in a global equityportfolio for now.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 3/21

GLOBAL EMERGING MARKET STRATEGY Page 3

GLOBAL ECONOMY OUTLOOK

5 key points.

1. A transition to stronger and broader-based growth is under way.

2.

Balance sheets improving - slowly for consumers, more rapidly for businesses.3. Navigating a normalization in monetary policy stances is the key challenge.4. The emerging world will again provide the principal support to global demand in 2011.5. The crisis in the MENA zone raises concerns about oil’s impact on global growth.

A transition to stronger and broader-based growth is under way, as the global economy reaccelerates, a centralregularity of business cycle performance is reaffirmed. Recoveries do not move in straight lines, but there arepowerful forces promoting sustained strong growth in the aftermath of a deep recession. The fuel for lift largelycomes from the private sector’s shift away from a defensive posture. This is evident in the broad-based upturn inglobal business spending over the past year in the face of depressed resource utilization . A similar shift in thehousehold sector is also taking hold, albeit unevenly.

Fuel for early-cycle growth also tends to be reinforced by accommodative monetary policies. Inflation regularlymoves lower in the aftermath of global recessions, as levels of activity remain depressed despite above-trendgrowth. This enables growth-friendly monetary policies to linger well into the subsequent expansion.

Private-sector balance sheets in a number of major economies have improved since the height of the crisis, ashouseholds have retrenched and repaid some of their debts. Household liabilities as a share of assets, whichwere around 15% in the 1990s but rose to 22% during the recession, have retreated to around 20%. Moreover, inboth the US and the euro zone bank lending has stopped declining on a year-on-year basis. But the process of deleveraging is far from complete, and is likely to last for several more years. It is a necessary adjustment after the excesses of the credit boom, but it creates the risk of a protracted period of large output gaps and highunemployment.

In the US, in particular, non-financial firms have liquid balance sheets and are sitting on record levels of cash.Once business and consumer confidence improves, firms would face few constraints to start hiring and investing.One of the reasons that firms are so liquid is the strength of corporate earnings, which have rebounded stronglythis year and are now close to record levels. According to national accounting methodology, in the third quarter of 2010 pre-tax US corporate profits accounted for 14.5% of GDP, compared with a post-second world war averageof 9.6%.

Global consumption rose by 3.2% in 2010 (previously 2.4%). Consumption growth is expected to remain relativelyrobust in 2011 but it will lose strength, partly as a result of the high base in 2010. It is expected to average annualgrowth of 1.9% in 2011-15. Growth in consumption will be concentrated in non-OECD countries, particularlyChina, the Middle East and India, as their economies grow strongly, incomes and car ownership rise, andgovernments continue to subsidize retail fuel prices.

Monetary policy is set to remain exceptionally accommodative. As governments tighten fiscal policy, centralbanks will assume a greater share of the burden of supporting demand. We do not see the Fed or the ECB tostart raising their policy rates until the second half of 2012.

The Fed's decision to expand its QE program seems unlikely to be continued when it expires in mid-2011,especially if the unemployment rate, which fell to 9.4% in December 2010, continues to edge downward. But if the jobless rate remains above 8% in 2012, a presidential election year in the US, the Fed will come under pressureto find new ways to create jobs.

The ECB has held out against implementing QE, although it has purchased covered bonds, and since May lastyear it has been buying (and sterilizing) purchases of Greek, Irish and Portuguese debt in an attempt to stabilizeperipheral euro zone debt markets. The ECB is also providing large amounts of liquidity to the region's banks ,

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 4/21

GLOBAL EMERGING MARKET STRATEGY Page 4

and we expect it to continue to do so in 2011. If conditions in peripheral euro zone bond markets do not becomeless stressed in 2011, the ECB may begin large-scale government bond purchases.

The Bank of Japan announced its own, much smaller, QE program in early October, while some members of themonetary policy committee of the Bank of England have been arguing in favor of expanding the UK's QEprogram.

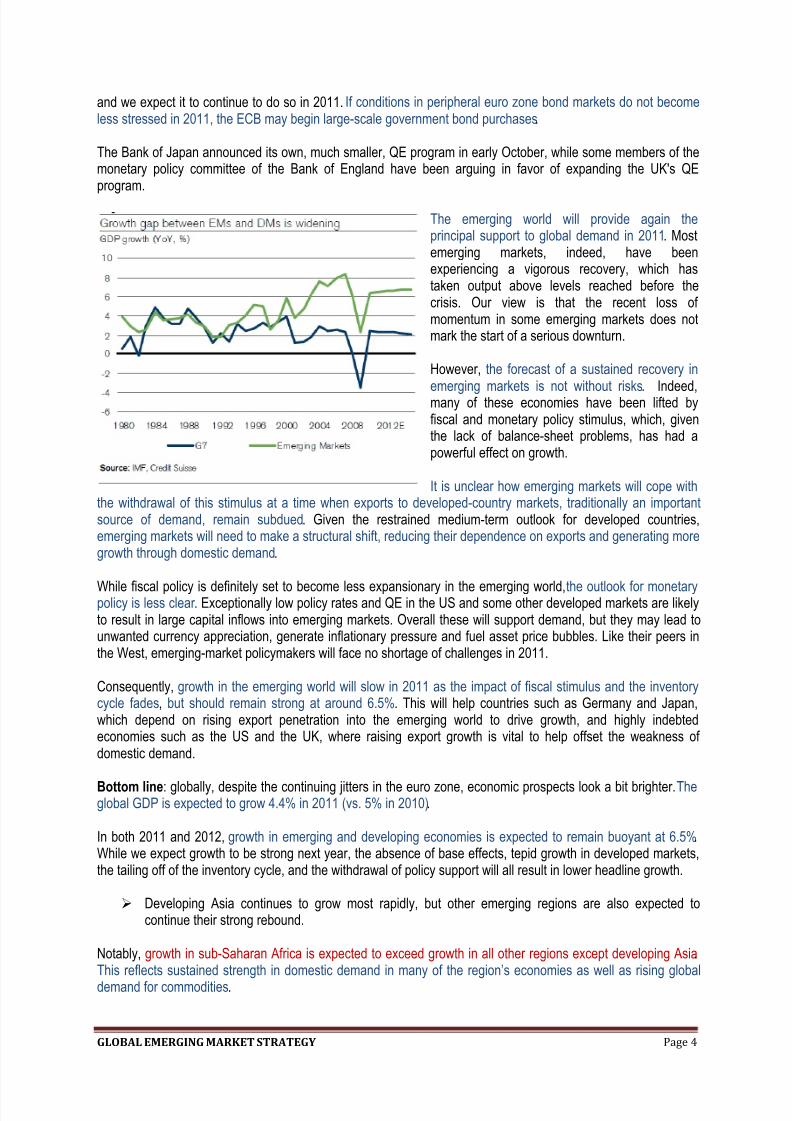

The emerging world will provide again theprincipal support to global demand in 2011. Mostemerging markets, indeed, have beenexperiencing a vigorous recovery, which hastaken output above levels reached before thecrisis. Our view is that the recent loss of momentum in some emerging markets does notmark the start of a serious downturn.

However, the forecast of a sustained recovery in

emerging markets is not without risks. Indeed,many of these economies have been lifted byfiscal and monetary policy stimulus, which, giventhe lack of balance-sheet problems, has had apowerful effect on growth.

It is unclear how emerging markets will cope withthe withdrawal of this stimulus at a time when exports to developed-country markets, traditionally an importantsource of demand, remain subdued. Given the restrained medium-term outlook for developed countries,emerging markets will need to make a structural shift, reducing their dependence on exports and generating moregrowth through domestic demand.

While fiscal policy is definitely set to become less expansionary in the emerging world, the outlook for monetarypolicy is less clear . Exceptionally low policy rates and QE in the US and some other developed markets are likelyto result in large capital inflows into emerging markets. Overall these will support demand, but they may lead tounwanted currency appreciation, generate inflationary pressure and fuel asset price bubbles. Like their peers inthe West, emerging-market policymakers will face no shortage of challenges in 2011.

Consequently, growth in the emerging world will slow in 2011 as the impact of fiscal stimulus and the inventorycycle fades, but should remain strong at around 6.5%. This will help countries such as Germany and Japan,which depend on rising export penetration into the emerging world to drive growth, and highly indebtedeconomies such as the US and the UK, where raising export growth is vital to help offset the weakness of domestic demand.

Bottom line: globally, despite the continuing jitters in the euro zone, economic prospects look a bit brighter. Theglobal GDP is expected to grow 4.4% in 2011 (vs. 5% in 2010).

In both 2011 and 2012, growth in emerging and developing economies is expected to remain buoyant at 6.5%.While we expect growth to be strong next year, the absence of base effects, tepid growth in developed markets,the tailing off of the inventory cycle, and the withdrawal of policy support will all result in lower headline growth.

Developing Asia continues to grow most rapidly, but other emerging regions are also expected tocontinue their strong rebound.

Notably, growth in sub-Saharan Africa is expected to exceed growth in all other regions except developing Asia.This reflects sustained strength in domestic demand in many of the region’s economies as well as rising global

demand for commodities.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 5/21

GLOBAL EMERGING MARKET STRATEGY Page 5

EM Asia will likely grow a robust 8.4% in 2011 (vs. 9.3% in 2010). China and India will again lead theregion, with growth expected to be 9.6% and 8.5%, respectively.

Importantly, as was the case in 2010, strong GDP growth in EM Asia will be a case of “no country left behind.The ASEAN (Indonesia, Malaysia, Philippines, Thailand, and Vietnam) will come out with 5.5% of GDPgrowth.

The growth message for 2011 in EMEA is that energy exporters will again outperform. We forecast2011 EMEA growth at 4.3%. We see the GCC, Russia and some oil exporters in Sub-Saharan Africa asgrowing above potential, in part because we see oil prices rising moderately, and in part because mostof these countries will not need to consolidate fiscally.

In 2009 and to some extent 2010, energy exporters used their oil stabilization funds/future generation fundsto counteract the impact of the global economic crisis. Now it is time to rebuild those funds. Countries withIMF programs (particularly Latvia, Romania and Ukraine) will continue with fiscal consolidation. Goingforward, some countries in EMEA EM will also see a need to accelerate structural reform, modernization, anddiversification away from energy in order to create a more sustainable growth structure.

Growth in LATAM should remain at or above potential in 2011. Real GDP growth in the region cameat 5.9%oya in 2010. Importantly, the 4.3% growth forecast for LATAM as a whole for 2011 suggests thatthe regional pace of growth will remain again above potential this year.

LATAM’s ability to maintain positive growth momentum despite the global slowdown is likely related to thefact that growth in most countries in the region is being driven by a strong recovery in domestic demand,while the growth contribution from net trade is already negative. Obviously, Latin America is not totallyimmune to the deceleration in global growth, which partly explains the lower growth projections penciled infor some countries for 2011, Mexico is the prime example, given its close economic links to the US.

The crisis in the MENA zone raises concerns about oil’s impact on global growth. The turmoil in North African

countries is a local rather than global problem that does not justify a change in our overall bullish view. It doeshave implications, though, for sector and region allocations. However, it raises, first, upside risks to commodityprices, reinforcing our bullish view on commodity sectors especially Energy. Second, steep increases inpurchases of agricultural commodities by vulnerable North African countries are putting further upward pressureon agricultural commodity prices, exacerbating the inflation threat within EM.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 6/21

GLOBAL EMERGING MARKET STRATEGY Page 6

EMERGING EQUITY MARKETS STRATEGY

Neutral

We keep a positive, but moderate, view on emerging markets for 2011 .We are market weight on the asset in a global portfolio for 2011.

Fundamentals remain solid

Supports: i) global recovery; ii) ample liquidity, with the Fed on hold in 2011; iii) a structurally weak dollar; iv) domesticgrowth secular story; v)solid earnings momentum and attractive valuations.

The risks: i) the scale of monetary tightening in GEMs, although real rates are negative in many countries; ii) the EUsovereign crisis.

The aftermath of Fed easing: 1993, 2005?

We believe the bull market entered its third year in late-October. Average Year 3 gains in the early phase of global recovery(as now) are c.50%. The best calendar year parallels are 1993 (+71%) and 2005 (+30%).

Regions

We are Overweight Asia (the growth area in GEMs). We suggest being Neutral EMEA (low valuations and benign interestrates) and Underweight LATAM (lower earnings momentum and aggressive monetary tightening).

Markets

We also prefer to play countries with attractive valuations and sustainable growth. We prefer the larger markets at theexpense of the smaller markets, with the exception of Indonesia, and Malaysia. We resist the temptation of Taiwan, whichhave one of the weakest 2011 earnings forecasts in the emerging markets universe. We extend our Frontiers, mainly in Africa.

Overweight: Indonesia, Malaysia, Russia;Neutral: Brazil, China, Frontier Africa, Korea, South Africa, Mexico, Thailand, Turkey;Underweight: Czech Rep, Hungary, India, Taiwan.

Sectors

We retain a high-beta cyclical bias, but with a preference for domestics over global cyclicals.

Overweight: Consumer Discretionary, Financials, Industrials. Materials and Energy are a Neutral.

Economic perspectives: real GDP growth in EM economies will reach 6.5% in 2011, nearly three times the 2%pace expected in DM economies. Once again, Emerging Asia will be the leader of the pack, with growth expectedto reach 8.4% amid the strong support from China’s 9.2% forecast for next year.

Where are we in the cycle, however? Data show that the emerging markets composite lead indicator is currentlyabove trend and in danger of rolling over. Indeed, the current state of the lead indicator is above trend &falling and could conceivably end up below trend. Does this mean a dip in economic activity is imminent? Not necessarily.

First, globally, we don’t expect a double dip as the economic growth slowdown has bottomed. Second, up-to-date economic data in the form of PMIs suggest that activity has been surprising on the

upside. Furthermore, we have seen unconditional support by the Fed to promote growth and reflate.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 7/21

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 8/21

GLOBAL EMERGING MARKET STRATEGY Page 8

For equity investors, controls designed to reduce the effective carry in fixed income markets are ok. Broader capital controls which reduce the ability of equity investors to buy and sell would be negative as they reduceliquidity and increase volatility.

Anti-asset inflation policies: central banks are targeting asset prices in EM to counter asset inflation. Thesepolicies introduce economic and sector specific risks. Note how poorly real estate stocks have performed in EMdespite low interest rates.

Trade wars: high US unemployment, China’s large current account surplus and polarized politics in the USincrease the risk of a trade war.

Economic risks

Uncertain outlook for commodities: our commodities and energy underweight is driven by a combination of long term economic cycles and a potential inflection point in the growth of Chinese material demand. The timingis complicated by the large influence of financial investors on commodity markets. The timing risk in a bearishview on commodity companies is high. Industrial metal prices rallied since May while global leading indicators fell.

Correlation of commodities to risk assets (equities) is high today. Momentum in a world of zero interest rates is anattractive attribute. An UW commodity call is unlikely to work at this point. When it does eventually the correctionmay prove to be violent as financial investors exit.

Unintended consequences of QE2: if QE2 results in a sharp increase in commodity prices it may choke-off growth and ultimately be counterproductive.

Peripheral Europe sovereign stress: Greek, Irish and Portuguese bond spreads to German bunds are at recordhighs. Sovereign stress could disrupt risk appetite as it did in Q2’10.

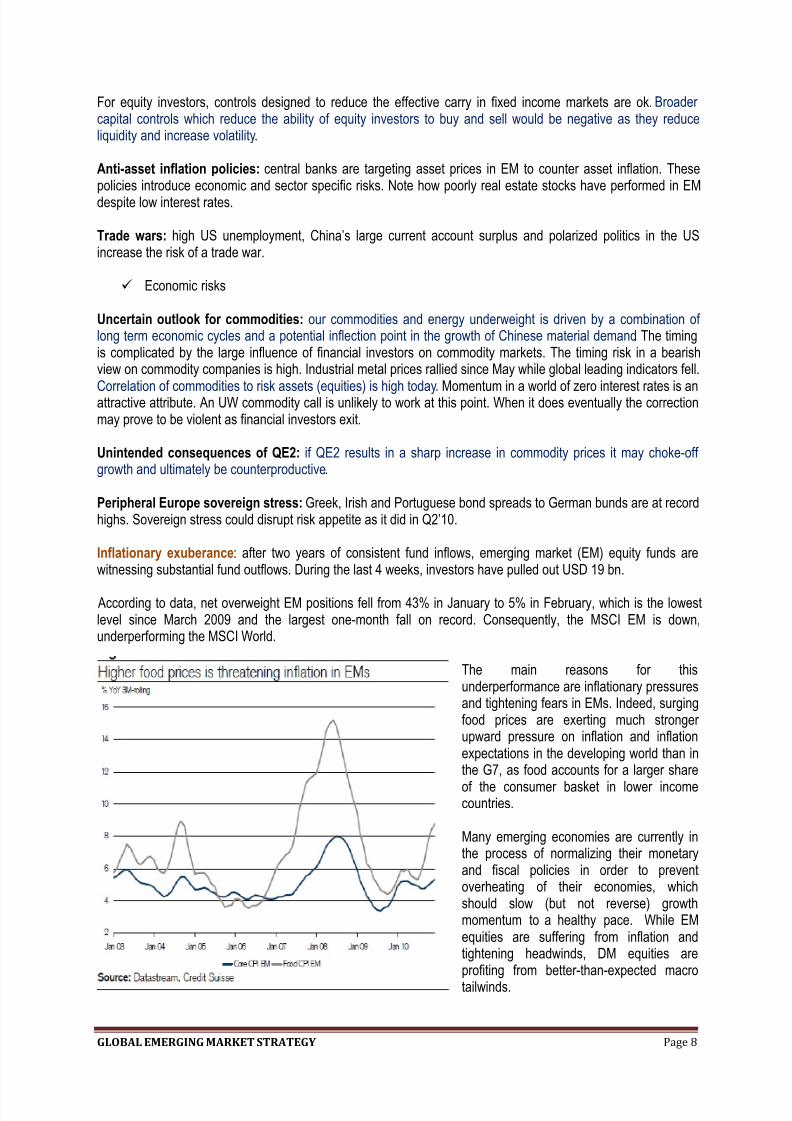

Inflationary exuberance: after two years of consistent fund inflows, emerging market (EM) equity funds arewitnessing substantial fund outflows. During the last 4 weeks, investors have pulled out USD 19 bn.

According to data, net overweight EM positions fell from 43% in January to 5% in February, which is the lowestlevel since March 2009 and the largest one-month fall on record. Consequently, the MSCI EM is down,underperforming the MSCI World.

The main reasons for thisunderperformance are inflationary pressuresand tightening fears in EMs. Indeed, surgingfood prices are exerting much stronger upward pressure on inflation and inflationexpectations in the developing world than inthe G7, as food accounts for a larger share

of the consumer basket in lower incomecountries.

Many emerging economies are currently inthe process of normalizing their monetaryand fiscal policies in order to preventoverheating of their economies, whichshould slow (but not reverse) growthmomentum to a healthy pace. While EMequities are suffering from inflation andtightening headwinds, DM equities areprofiting from better-than-expected macro

tailwinds.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 9/21

GLOBAL EMERGING MARKET STRATEGY Page 9

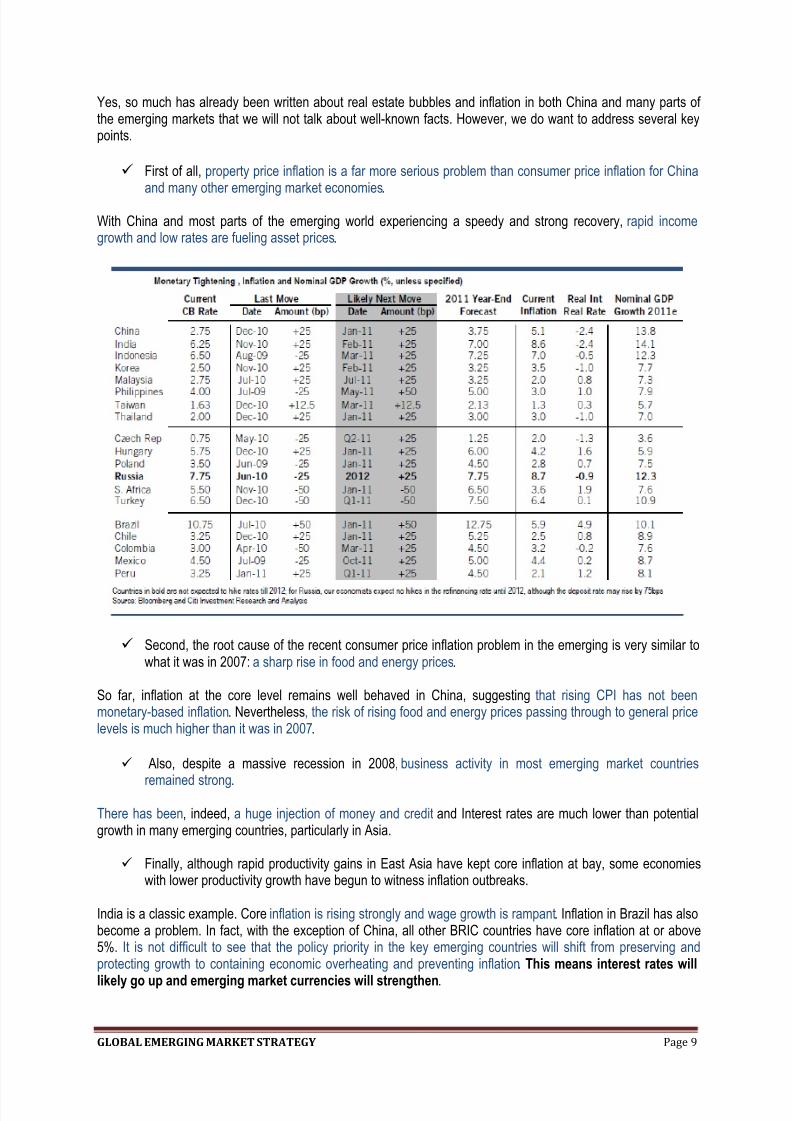

Yes, so much has already been written about real estate bubbles and inflation in both China and many parts of the emerging markets that we will not talk about well-known facts. However, we do want to address several keypoints.

First of all, property price inflation is a far more serious problem than consumer price inflation for Chinaand many other emerging market economies.

With China and most parts of the emerging world experiencing a speedy and strong recovery, rapid incomegrowth and low rates are fueling asset prices.

Second, the root cause of the recent consumer price inflation problem in the emerging is very similar towhat it was in 2007: a sharp rise in food and energy prices.

So far, inflation at the core level remains well behaved in China, suggesting that rising CPI has not beenmonetary-based inflation. Nevertheless, the risk of rising food and energy prices passing through to general pricelevels is much higher than it was in 2007.

Also, despite a massive recession in 2008, business activity in most emerging market countries

remained strong.

There has been, indeed, a huge injection of money and credit and Interest rates are much lower than potentialgrowth in many emerging countries, particularly in Asia.

Finally, although rapid productivity gains in East Asia have kept core inflation at bay, some economieswith lower productivity growth have begun to witness inflation outbreaks.

India is a classic example. Core inflation is rising strongly and wage growth is rampant. Inflation in Brazil has alsobecome a problem. In fact, with the exception of China, all other BRIC countries have core inflation at or above5%. It is not difficult to see that the policy priority in the key emerging countries will shift from preserving andprotecting growth to containing economic overheating and preventing inflation. This means interest rates will

likely go up and emerging market currencies will strengthen.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 10/21

GLOBAL EMERGING MARKET STRATEGY Page 10

Bottom-line: on the one hand, central banks in emerging countries are tightening while the Federal Reserve isengaged in QE2. On the other hand, banking systems in the developing world are much healthier than in the US;correspondingly credit is booming in many emerging economies while it has yet to recover in America. So, shouldinvestors be concerned about marginal tightening in emerging economies or should they be focused on the healthof banking systems in the developing nations versus the US?

In general, we believe emerging markets will continue to have robust growth potential driven by strong domesticdemand and investments. Domestic consumption will increasingly drive economic growth. Even though the U.S.dollar remains weak relative to emerging market currencies, there could be a significant rebound sometime in2011 as the US economy shows signs of gradual recovery. While this would not derail a long term structuraluptrend in EM assets, this will likely bring episodes of relative underperformance vis-à-vis of the developedmarket assets, mainly the US ones. More capital controls are likely to be implemented by EM countries if foreigndirect investment flows continue to disrupt their exchange rates. Las, but not least, inflation is under upwardpressure in emerging economies and there will be further policy tightening in these countries. In contrast, the Fedis still preoccupied with high unemployment and continues to favor easy money policies. Policy tightening andthe resultant liquidity squeeze in emerging economies will ensue a period of share price underperformancerelative to their U.S. counterparts. We are short emerging markets relative to the S&P 500 in a global

portfolio allocation.

MATURE EMERGING MARKETS

Despite a recovery in global risk taking, mature EM continues to transit through a period of consolidation. This is,to a great extent, the result of a perception that inflation is accelerating and central banks are somewhat behindthe curve. EM spreads, on the other hand, were a touch lower.

Emerging Asia: strong growth in Asia not only creates strong demand for food, but also generates other inflationary pressures that spill over to the emerging world. In a world where Asian (and increasinglyother regions) currencies are relatively sticky, abundant global liquidity turns into very expansionary

capital flows. In EMEA, there is a combination of active restrictive monetary policy and MENA politics. Ongoing

developments in North Africa are a reminder that political overhaul is also a risk with which investors inthe region need to reckon.

Latin America: Brazil and Peru continue to impose restrictions to reduce appreciation pressures. Wesee limited risk of similar measures in the rest of the region. High beta countries seem to be rushing tothe market to benefit from good liquidity and increased risk appetite.

Unfolding events in the MENA zone lead to a period of increasing instability in the region. Uncertainty isincreasingly breeding extreme caution from investors, holding back, at least in the short term, FDI and portfolioflows, with non-negligible effects on growth and the financing of large current account deficits (notably in Egypt).

At the same time, governments are likely to resort to expansionary fiscal measures to absorb popular anger through hiking wages and raising subsidies, adding to existing budget rigidities and elevating fiscal risks. Thisnaturally weighs on the credit profiles of some of the countries in the region. Accordingly, North African marketsshould remain under pressure.

We are moderately positive on emerging markets for 2011. The supports are the following:

Global recovery

Stronger US and Chinese growth are positive for GEM. The beneficiaries of stronger US and Chinese growthhave been: Mexico, Korea and Taiwan. Within sectors, this has coincided with a shift into Exporters (Technology

and Industrials) and Commodity sectors (Energy, Materials) from sectors that are dependent upon domesticgrowth (Consumer, Financials, Health Care, Telecoms and Utilities).

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 11/21

GLOBAL EMERGING MARKET STRATEGY Page 11

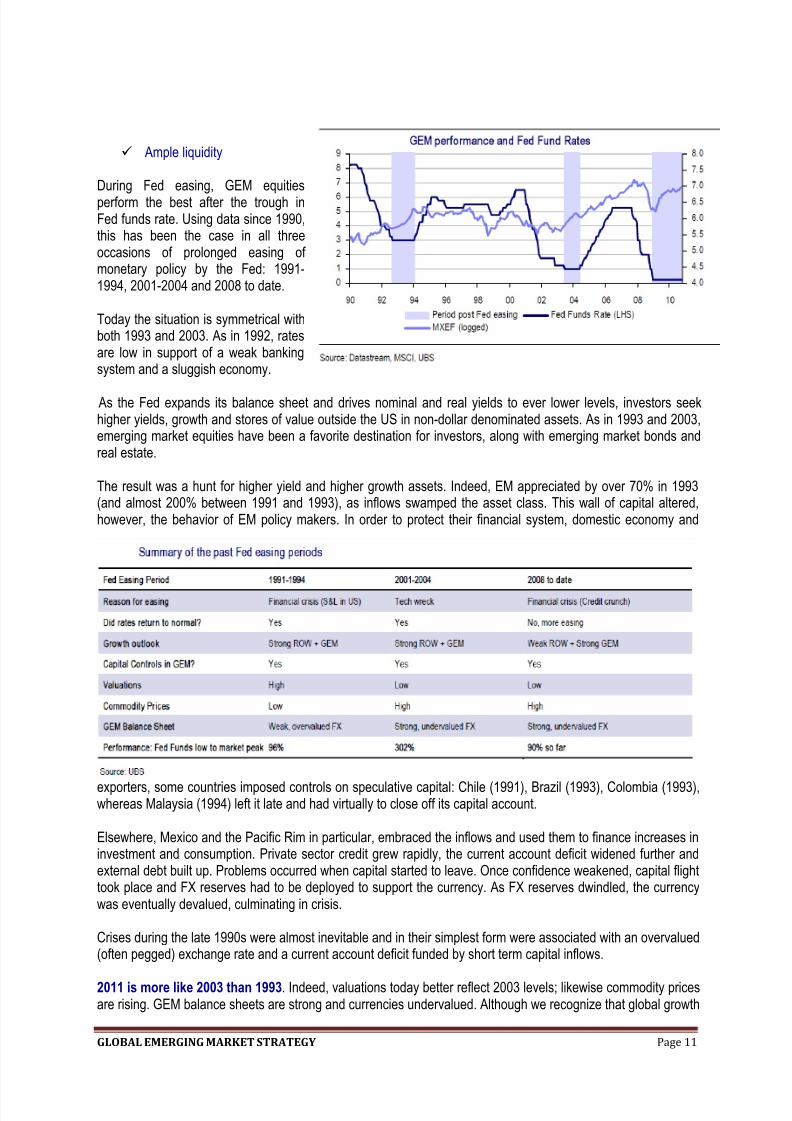

Ample liquidity

During Fed easing, GEM equitiesperform the best after the trough inFed funds rate. Using data since 1990,this has been the case in all threeoccasions of prolonged easing of monetary policy by the Fed: 1991-1994, 2001-2004 and 2008 to date.

Today the situation is symmetrical withboth 1993 and 2003. As in 1992, ratesare low in support of a weak bankingsystem and a sluggish economy.

As the Fed expands its balance sheet and drives nominal and real yields to ever lower levels, investors seekhigher yields, growth and stores of value outside the US in non-dollar denominated assets. As in 1993 and 2003,emerging market equities have been a favorite destination for investors, along with emerging market bonds andreal estate.

The result was a hunt for higher yield and higher growth assets. Indeed, EM appreciated by over 70% in 1993(and almost 200% between 1991 and 1993), as inflows swamped the asset class. This wall of capital altered,however, the behavior of EM policy makers. In order to protect their financial system, domestic economy and

exporters, some countries imposed controls on speculative capital: Chile (1991), Brazil (1993), Colombia (1993),whereas Malaysia (1994) left it late and had virtually to close off its capital account.

Elsewhere, Mexico and the Pacific Rim in particular, embraced the inflows and used them to finance increases ininvestment and consumption. Private sector credit grew rapidly, the current account deficit widened further andexternal debt built up. Problems occurred when capital started to leave. Once confidence weakened, capital flighttook place and FX reserves had to be deployed to support the currency. As FX reserves dwindled, the currencywas eventually devalued, culminating in crisis.

Crises during the late 1990s were almost inevitable and in their simplest form were associated with an overvalued(often pegged) exchange rate and a current account deficit funded by short term capital inflows.

2011 is more like 2003 than 1993. Indeed, valuations today better reflect 2003 levels; likewise commodity pricesare rising. GEM balance sheets are strong and currencies undervalued. Although we recognize that global growth

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 12/21

GLOBAL EMERGING MARKET STRATEGY Page 12

today is more fragile, Fed easing is always very positive for GEM assets. Check for the aftermath of Fed easing,however.

Unlike 1994, when the Fed hiked interest rates in 2004, there were no dislocations in Emerging Markets.Currencies were fundamentally inexpensive and well supported. The current global macro backdrop is favorablefor high yield and high growth plays. With the prospect of further capital controls, the likelihood is that capitalmoves into debt instruments of longer maturity and eventually equities.

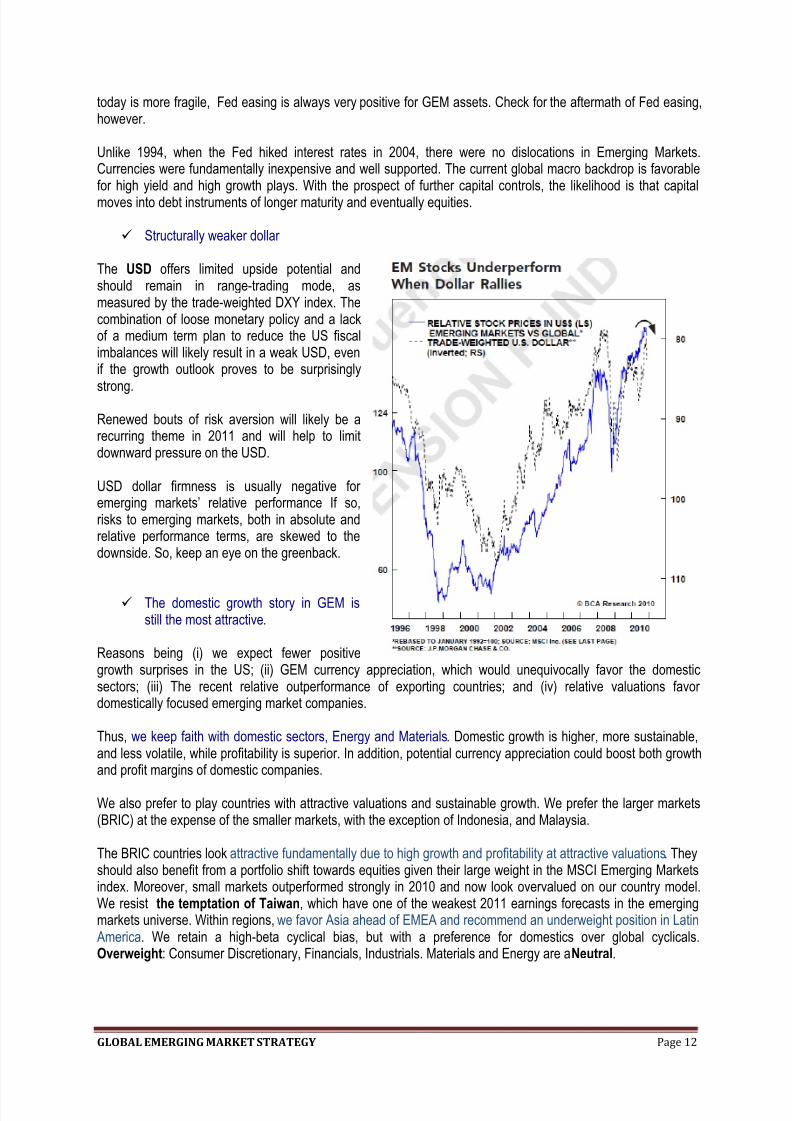

Structurally weaker dollar

The USD offers limited upside potential andshould remain in range-trading mode, asmeasured by the trade-weighted DXY index. Thecombination of loose monetary policy and a lackof a medium term plan to reduce the US fiscalimbalances will likely result in a weak USD, evenif the growth outlook proves to be surprisingly

strong.

Renewed bouts of risk aversion will likely be arecurring theme in 2011 and will help to limitdownward pressure on the USD.

USD dollar firmness is usually negative for emerging markets’ relative performance If so,risks to emerging markets, both in absolute andrelative performance terms, are skewed to thedownside. So, keep an eye on the greenback.

The domestic growth story in GEM isstill the most attractive.

Reasons being (i) we expect fewer positivegrowth surprises in the US; (ii) GEM currency appreciation, which would unequivocally favor the domesticsectors; (iii) The recent relative outperformance of exporting countries; and (iv) relative valuations favor domestically focused emerging market companies.

Thus, we keep faith with domestic sectors, Energy and Materials. Domestic growth is higher, more sustainable,and less volatile, while profitability is superior. In addition, potential currency appreciation could boost both growthand profit margins of domestic companies.

We also prefer to play countries with attractive valuations and sustainable growth. We prefer the larger markets(BRIC) at the expense of the smaller markets, with the exception of Indonesia, and Malaysia.

The BRIC countries look attractive fundamentally due to high growth and profitability at attractive valuations. Theyshould also benefit from a portfolio shift towards equities given their large weight in the MSCI Emerging Marketsindex. Moreover, small markets outperformed strongly in 2010 and now look overvalued on our country model.We resist the temptation of Taiwan, which have one of the weakest 2011 earnings forecasts in the emergingmarkets universe. Within regions, we favor Asia ahead of EMEA and recommend an underweight position in Latin America. We retain a high-beta cyclical bias, but with a preference for domestics over global cyclicals.Overweight: Consumer Discretionary, Financials, Industrials. Materials and Energy are a Neutral.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 13/21

GLOBAL EMERGING MARKET STRATEGY Page 13

Solid earnings momentum and attractive valuation

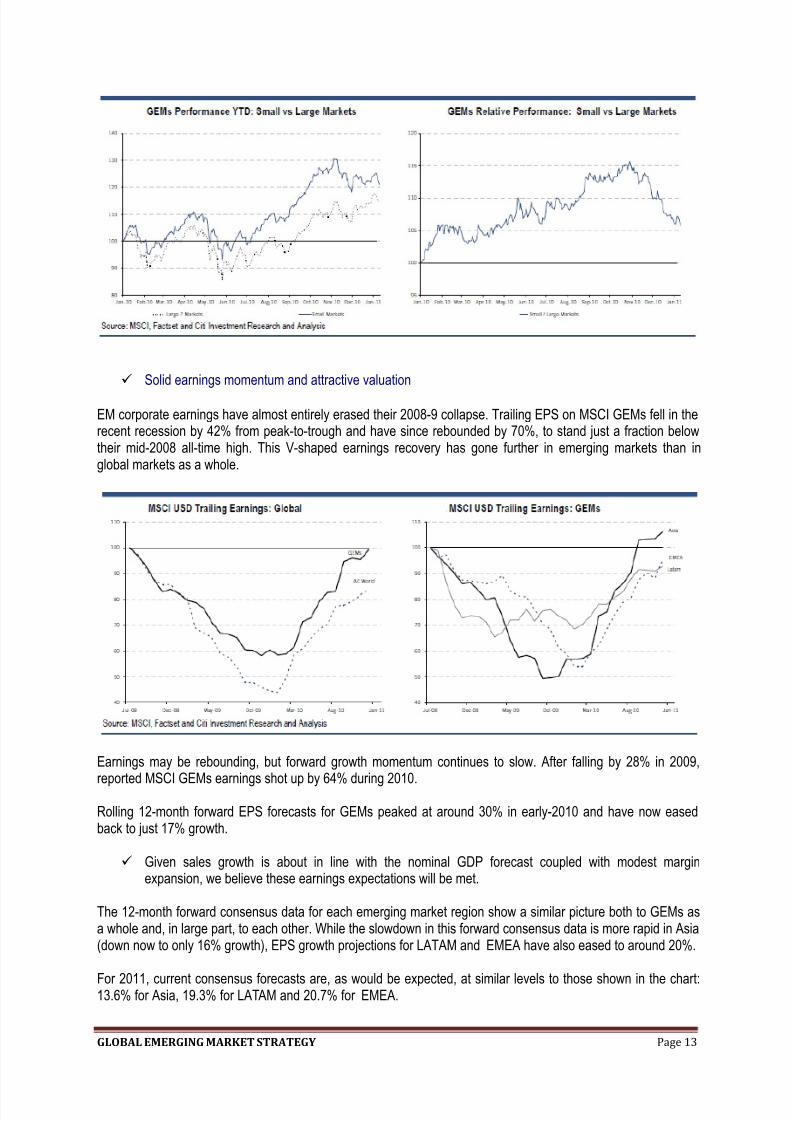

EM corporate earnings have almost entirely erased their 2008-9 collapse. Trailing EPS on MSCI GEMs fell in therecent recession by 42% from peak-to-trough and have since rebounded by 70%, to stand just a fraction belowtheir mid-2008 all-time high. This V-shaped earnings recovery has gone further in emerging markets than inglobal markets as a whole.

Earnings may be rebounding, but forward growth momentum continues to slow. After falling by 28% in 2009,

reported MSCI GEMs earnings shot up by 64% during 2010.

Rolling 12-month forward EPS forecasts for GEMs peaked at around 30% in early-2010 and have now easedback to just 17% growth.

Given sales growth is about in line with the nominal GDP forecast coupled with modest marginexpansion, we believe these earnings expectations will be met.

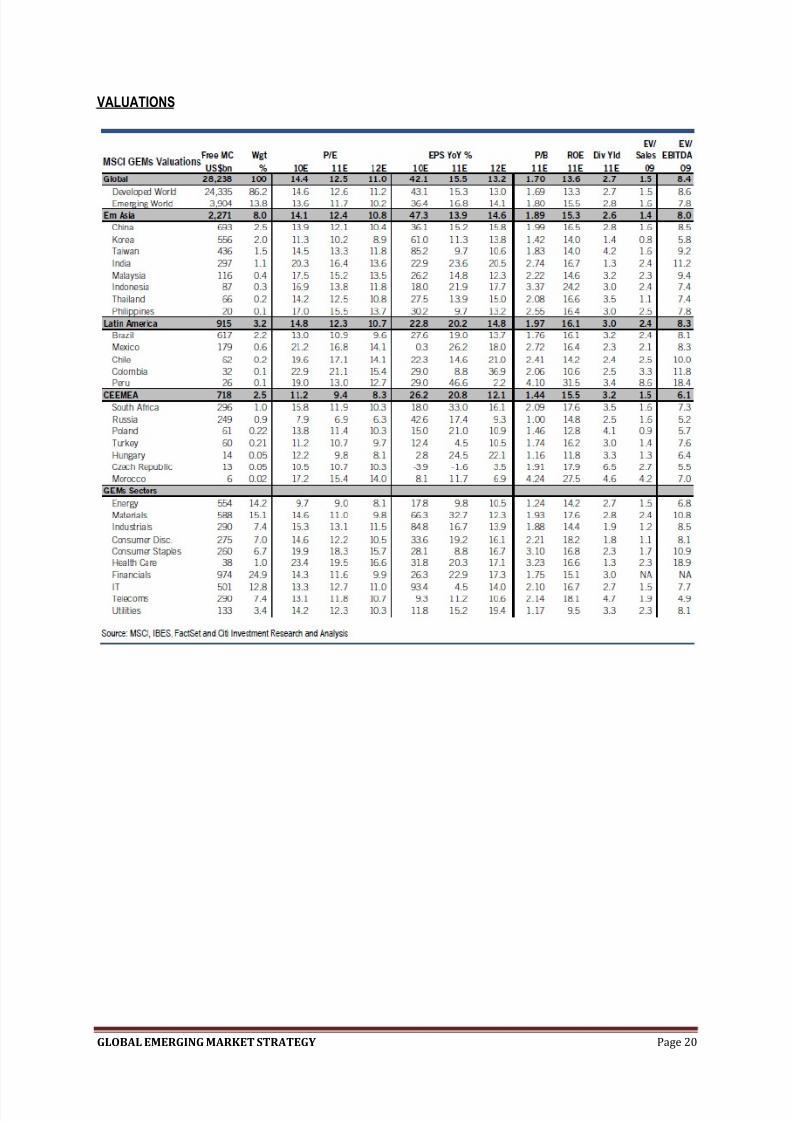

The 12-month forward consensus data for each emerging market region show a similar picture both to GEMs asa whole and, in large part, to each other. While the slowdown in this forward consensus data is more rapid in Asia(down now to only 16% growth), EPS growth projections for LATAM and EMEA have also eased to around 20%.

For 2011, current consensus forecasts are, as would be expected, at similar levels to those shown in the chart:13.6% for Asia, 19.3% for LATAM and 20.7% for EMEA.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 14/21

GLOBAL EMERGING MARKET STRATEGY Page 14

Switching to sectors, Technology is the only sector expected to post a YoY decline in earnings next year. Although the Telecoms sector is largely in an ex-growth phase, growth in EMEA is surprisingly strong. Thestrongest growth is reserved for the Financials, Materials and Utilities sectors. Growth prospects elsewhere arebroadly in line with the GEM aggregate.

Dividends for GEM aggregate are expected to grow by 17% and 22% in 2010 and 2011, respectively. Stronggrowth forecasts in the Materials sector come on the back of a steep decline seen in 2009. Furthermore it isexpected to be the strongest grower of dividends in 2011 supported by earnings. We expect big increases individends for the Healthcare sector in both 2010 and 2011 too.

GEM free cash flow (FCF) yields are foreseen at 0.6% and 3.0% in 2010 and 2011. Korea is still forecasted to beFCF negative in 2010 but is expected to give positive yield for 2011. Telecoms are expected to post the strongestFCF yields in both 2010 and 2011, with EMEA leading from the front. All the regions are expected to be cashgenerative in 2011.

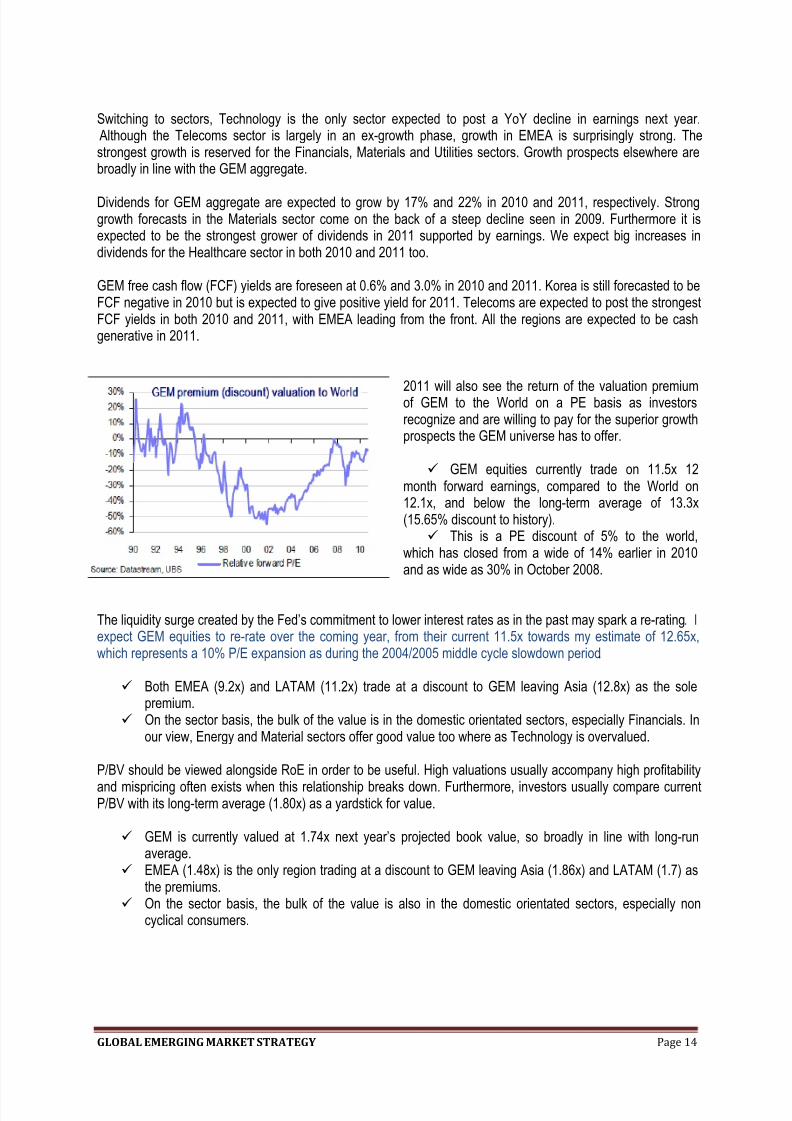

2011 will also see the return of the valuation premiumof GEM to the World on a PE basis as investorsrecognize and are willing to pay for the superior growthprospects the GEM universe has to offer.

GEM equities currently trade on 11.5x 12month forward earnings, compared to the World on12.1x, and below the long-term average of 13.3x(15.65% discount to history). This is a PE discount of 5% to the world,

which has closed from a wide of 14% earlier in 2010and as wide as 30% in October 2008.

The liquidity surge created by the Fed’s commitment to lower interest rates as in the past may spark a re-rating . Iexpect GEM equities to re-rate over the coming year, from their current 11.5x towards my estimate of 12.65x,which represents a 10% P/E expansion as during the 2004/2005 middle cycle slowdown period.

Both EMEA (9.2x) and LATAM (11.2x) trade at a discount to GEM leaving Asia (12.8x) as the solepremium.

On the sector basis, the bulk of the value is in the domestic orientated sectors, especially Financials. Inour view, Energy and Material sectors offer good value too where as Technology is overvalued.

P/BV should be viewed alongside RoE in order to be useful. High valuations usually accompany high profitability

and mispricing often exists when this relationship breaks down. Furthermore, investors usually compare currentP/BV with its long-term average (1.80x) as a yardstick for value.

GEM is currently valued at 1.74x next year’s projected book value, so broadly in line with long-runaverage.

EMEA (1.48x) is the only region trading at a discount to GEM leaving Asia (1.86x) and LATAM (1.7) asthe premiums.

On the sector basis, the bulk of the value is also in the domestic orientated sectors, especially noncyclical consumers.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 15/21

GLOBAL EMERGING MARKET STRATEGY Page 15

EXTENDING THE FRONTIERS

Frontier markets are likely to perform well in 2011 as they are regarded as a higher “beta” play to the large emergingmarkets.

Frontier markets are small/illiquid emerging markets that are not included in the main MSCI Emerging Markets Index.

With so much interest in emerging markets, eventually there may be some room for some of this underperformance byfrontier markets to unwind. We may likely see spillover of liquidity from large emerging markets to smaller and illiquid“frontier markets.”

This also requires that risk appetite remains strong or continues to rise, given the nature of frontier markets.

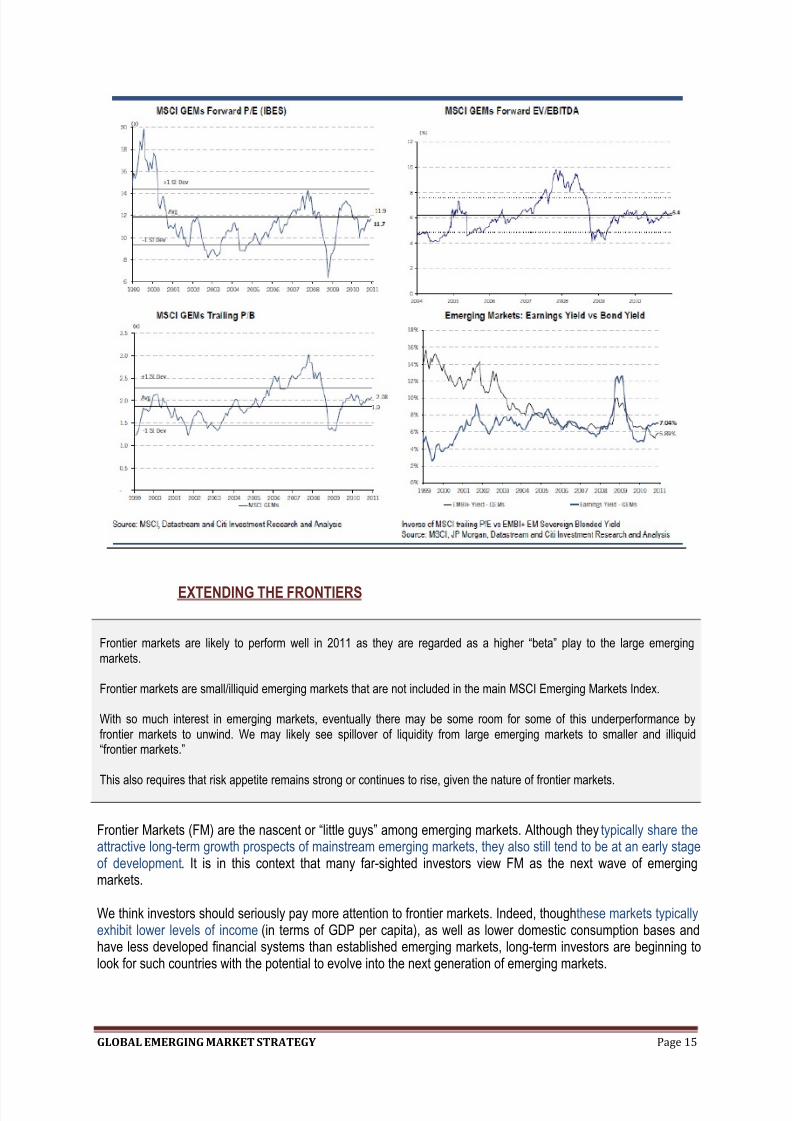

Frontier Markets (FM) are the nascent or “little guys” among emerging markets. Although they typically share theattractive long-term growth prospects of mainstream emerging markets, they also still tend to be at an early stageof development. It is in this context that many far-sighted investors view FM as the next wave of emergingmarkets.

We think investors should seriously pay more attention to frontier markets. Indeed, though these markets typicallyexhibit lower levels of income (in terms of GDP per capita), as well as lower domestic consumption bases andhave less developed financial systems than established emerging markets, long-term investors are beginning tolook for such countries with the potential to evolve into the next generation of emerging markets.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 16/21

GLOBAL EMERGING MARKET STRATEGY Page 16

So just as the GDP per capita in China between 1980 and 2010 jumped thirteen-fold, from 313 USdollars to 4,336 dollars, so too do many frontier markets today: from Bulgaria and Kazakhstan to Kenya.They have the potential to graduate into tomorrow's emerging markets.

Which countries qualify as frontier markets? Frontier markets can be found across the globe.

Many of the African countries like Ghana, Botswana and Tanzania are prime examples of frontier markets.

In fact, most African frontier markets exhibit a number of long-term structural growth drivers: for instance, young, large and growing populations, enormous technological catch-up potential, big outputgaps and consumer markets that are still in their infancy.

And given improving economic and political governance, as well as growing access to internationalfunding through capital markets, many African frontier markets today offer very interesting long-termeconomic opportunities.

But frontier markets can also be found in other regions of the world.

Eastern European countries such as Croatia or Romania, both supported by the prospect of EUaccession, are becoming increasingly attractive as frontier investment destinations.

Further east, the former Soviet satellite states such as the energy-rich states of Kazakhstan or Uzbekistan arealso becoming noticed as frontier markets.

In Latin America, countries such as Bolivia and Peru with natural resources are the ones attractingattention,

while countries such as

Vietnam and Mongolia are capturing investors' interest in Asia.

And in the Gulf region, with its vast oil and gas wealth, and loosening investment restrictions, countriessuch as Lebanon, Jordan and Qatar are popping up on investors' radar screens.

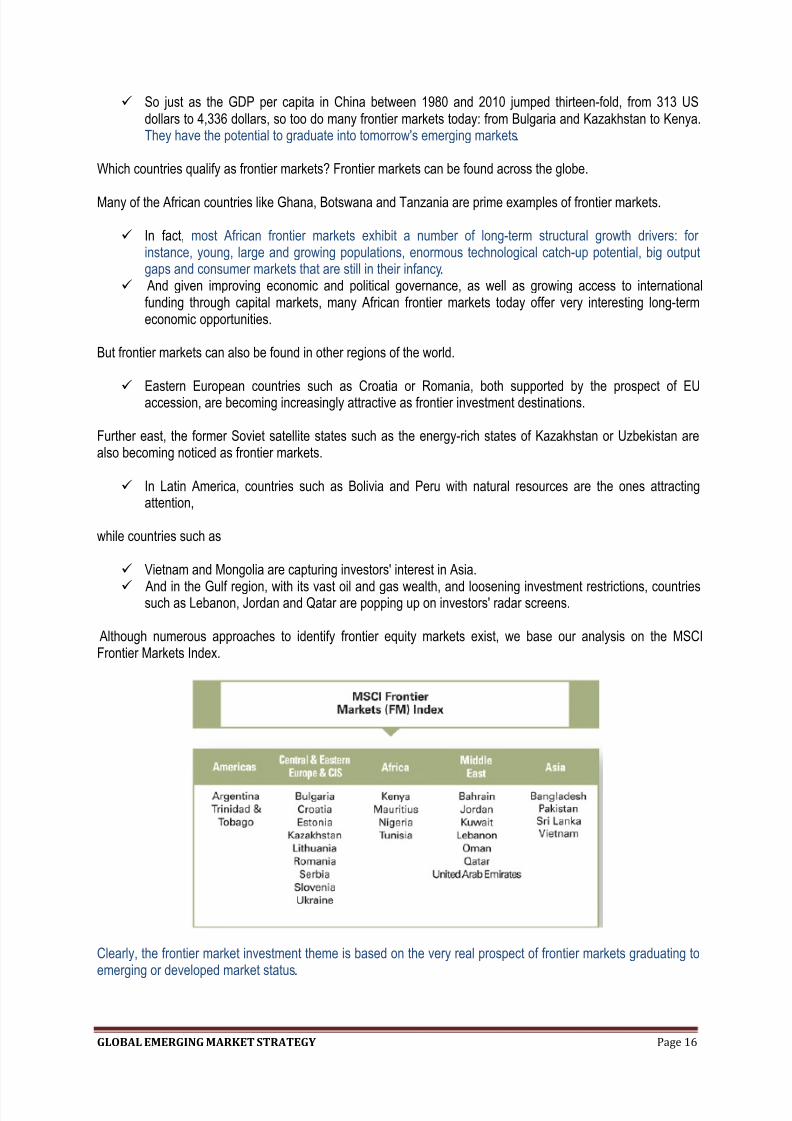

Although numerous approaches to identify frontier equity markets exist, we base our analysis on the MSCIFrontier Markets Index.

Clearly, the frontier market investment theme is based on the very real prospect of frontier markets graduating toemerging or developed market status.

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 17/21

GLOBAL EMERGING MARKET STRATEGY Page 17

Examples of this trend include South Korea and Taiwan, both today having similar economic growthprofiles of developed nations after having been some of the poorer nations in the world 20 years ago.

But we should also note that countries can also be demoted (and fall back to frontier status).

For instance, in 2009, Argentina lost its emerging market status after it implemented capital controls thatreduced the ability to convert foreign currencies into the local currency.

Similarly, in 2008 Pakistan was also demoted back to frontier market status for restricting daily declinesin its stock market at the peak of the financial crisis.

So, while the frontier market investment theme is based on the very real trend that these economies mature toemerging market status, Argentina and Pakistan show that there are exceptions to this trend.

We highlight several factors we think are drivers of the investment potential of frontier markets:

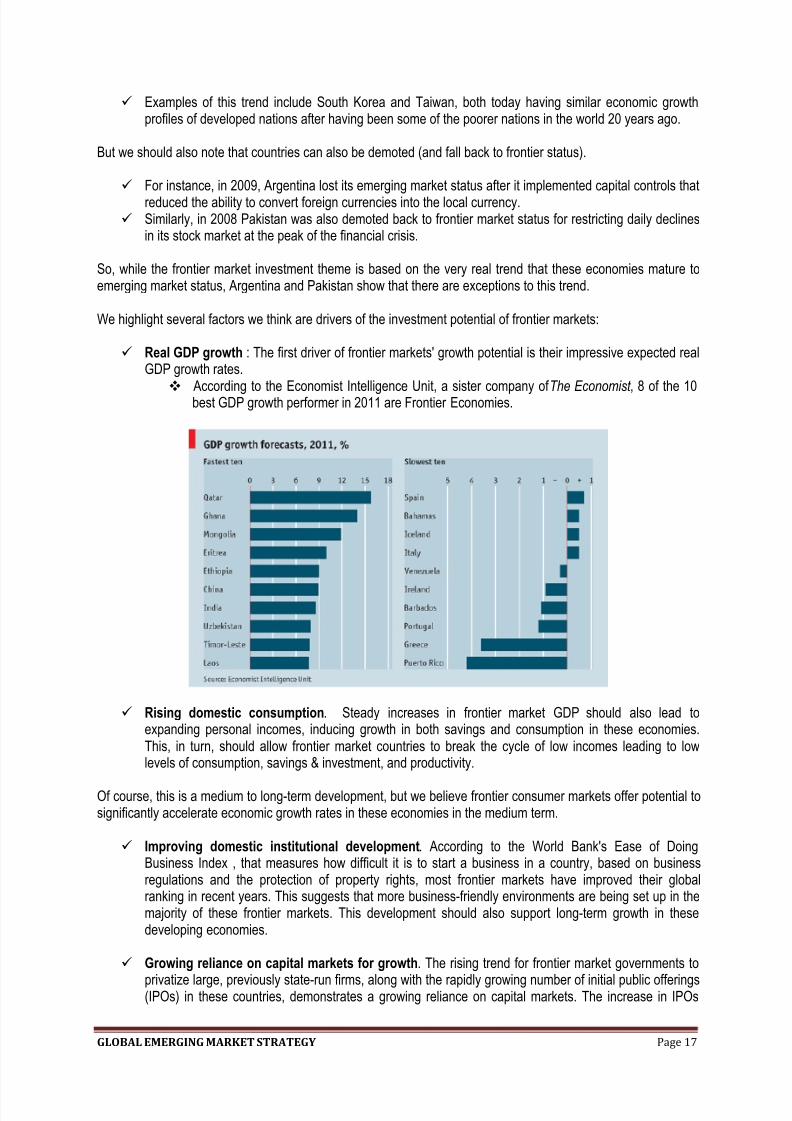

Real GDP growth : The first driver of frontier markets' growth potential is their impressive expected realGDP growth rates.

According to the Economist Intelligence Unit, a sister company of The Economist , 8 of the 10best GDP growth performer in 2011 are Frontier Economies.

Rising domestic consumption. Steady increases in frontier market GDP should also lead toexpanding personal incomes, inducing growth in both savings and consumption in these economies.This, in turn, should allow frontier market countries to break the cycle of low incomes leading to lowlevels of consumption, savings & investment, and productivity.

Of course, this is a medium to long-term development, but we believe frontier consumer markets offer potential tosignificantly accelerate economic growth rates in these economies in the medium term.

Improving domestic institutional development. According to the World Bank's Ease of DoingBusiness Index , that measures how difficult it is to start a business in a country, based on businessregulations and the protection of property rights, most frontier markets have improved their globalranking in recent years. This suggests that more business-friendly environments are being set up in themajority of these frontier markets. This development should also support long-term growth in thesedeveloping economies.

Growing reliance on capital markets for growth. The rising trend for frontier market governments to

privatize large, previously state-run firms, along with the rapidly growing number of initial public offerings(IPOs) in these countries, demonstrates a growing reliance on capital markets. The increase in IPOs

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 18/21

GLOBAL EMERGING MARKET STRATEGY Page 18

has, in turn, also boosted the overall equity market capitalization of the frontier universe and is starting tobring those countries and companies to the attention of more international investors.

But FM remain by definition more risky than their emerging market counterparts. First, despite the improvementsmade by frontier markets with respect to improving their institutional framework, economic and politicalgovernance remains weaker than in emerging and developed markets. The lack of suitable institutionalframeworks in many of these countries also makes it more difficult for the private sector to thrive, and also leavesthe broader economy more vulnerable to financial shocks and political unrest.

Second, frontier equity markets still tend to be very small and unsophisticated. Listed companies on mostfrontier market stock exchanges are still few in number and small in size. The five largest frontier countries bymarket capitalization are the UAE (USD 104 bn), Qatar (USD 102 bn), Kuwait (USD 100 bn), Argentina (USD 49bn) and Nigeria (USD 41 bn). But even these larger frontier markets appear tiny when one compares them to theUSD 992 bn market capitalization of the Swiss equity market and the USD 13 trillion of the US equity market.Moreover, 15 of the 25 frontier markets included in the MSCI Frontier Markets Index have a market capitalizationof less than USD 20 bn. This lower liquidity makes it more difficult to find sellers when markets fall, makinginvestments in frontier markets disproportionately sensitive to changes in capital flows and financial risk appetite.

Investors should need to be aware of four key operational challenges that relate to frontier markets. Research onfrontier markets is far less readily available than it is for the developed and emerging market space, whichleaves economic and valuation data sparse and perhaps less reliable. Also, some frontier markets limitforeign trading in local markets, which further restricts investments in these markets. Corporate governance,transparency and financial reporting standards in frontier markets are also likely to be weaker than indeveloped markets. And finally, trading and settlement systems may not be as sophisticated as those of larger markets, leaving more room for transaction errors.

Although these risks do cloud short-term visibility for these markets, better management and mitigation of theabove mentioned risks is likely to be key to ensuring lower risk premiums for frontier markets in the medium term.

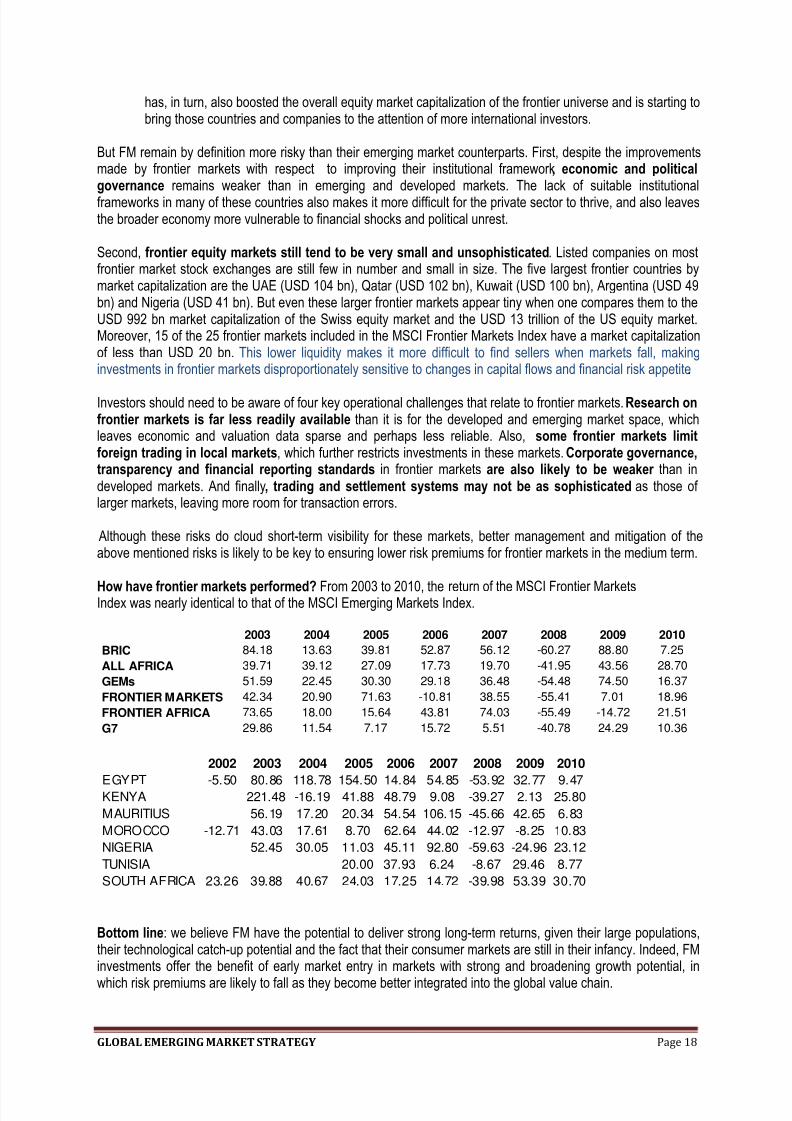

How have frontier markets performed? From 2003 to 2010, the return of the MSCI Frontier MarketsIndex was nearly identical to that of the MSCI Emerging Markets Index.

Bottom line: we believe FM have the potential to deliver strong long-term returns, given their large populations,their technological catch-up potential and the fact that their consumer markets are still in their infancy. Indeed, FMinvestments offer the benefit of early market entry in markets with strong and broadening growth potential, in

which risk premiums are likely to fall as they become better integrated into the global value chain.

2003 2004 2005 2006 2007 2008 2009 2010

BRIC 84.18 13.63 39.81 52.87 56.12 -60.27 88.80 7.25

ALL AFRICA 39.71 39.12 27.09 17.73 19.70 -41.95 43.56 28.70

GEMs 51.59 22.45 30.30 29.18 36.48 -54.48 74.50 16.37

FRONTIER MARKETS 42.34 20.90 71.63 -10.81 38.55 -55.41 7.01 18.96

FRONTIER AFRICA 73.65 18.00 15.64 43.81 74.03 -55.49 -14.72 21.51

G7 29.86 11.54 7.17 15.72 5.51 -40.78 24.29 10.36

2002 2003 2004 2005 2006 2007 2008 2009 2010

EGYPT -5.50 80.86 118.78 154.50 14.84 54.85 -53.92 32.77 9.47

KENYA 221.48 -16.19 41.88 48.79 9.08 -39.27 2.13 25.80

MAURITIUS 56.19 17.20 20.34 54.54 106.15 -45.66 42.65 6.83

MOROCCO -12.71 43.03 17.61 8.70 62.64 44.02 -12.97 -8.25 10.83

NIGERIA 52.45 30.05 11.03 45.11 92.80 -59.63 -24.96 23.12

TUNISIA 20.00 37.93 6.24 -8.67 29.46 8.77

SOUTH AFRICA 23.26 39.88 40.67 24.03 17.25 14.72 -39.98 53.39 30.70

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 19/21

GLOBAL EMERGING MARKET STRATEGY Page 19

And although equity investments in these markets are (still) subject to higher risk and uncertainty relative to moremature markets, we believe risk premiums are likely to fall as these economies continue to be more closely linkedinto the global value chain, as regulatory frameworks continue to improve, and as market access also further improves. We believe investments in frontier markets should be allocated to a satellite part of a diversifiedportfolio only, and investors should be willing and able to tolerate higher market volatility and temporarydistortions than is typical in established markets.

Given the higher investment risk and limited investable vehicles for frontier markets, we recommend thatinvestors gain exposure to frontier markets through specialized frontier market funds or structured products onindexes. For more sophisticated and risk tolerant investors, individual companies in frontier markets canoffer very interesting opportunities (although investment restrictions may apply in some instances).

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 20/21

GLOBAL EMERGING MARKET STRATEGY Page 20

VALUATIONS

8/6/2019 Inflationary Exuberance - GEMs Strategy

http://slidepdf.com/reader/full/inflationary-exuberance-gems-strategy 21/21

GLOBAL EMERGING MARKET STRA

AAAf f f rrriiicccaaa E

AAsssseett AAlllloocc

Specialists in African emer

Africa Emerging Capital Asset Allspecialized in providing multi-ass

managers (private and/or institutiwith a special focus on African ma We develop investment strategy adriving the global economy in gencomprehensive forecasting approahelp clients make sound and confi

Our vision is to become an acceptopportunities in growing, emergin

We commit to offer client drivenwith each client to address specifieach risk profile and investment h

We combine the spirit and visioninstitute without compromising th

Africa Emerging Capital (AEC) [email protected]

1260 Nyon - Switzerland Reference N°: 2011/05872Federal registration N°: CH-550-108792

EGY

mmmeeerrrgggiiinnnggg CCCaaapppiiitttaaalll

ttiioonn,, wwiisshhiinngg ttoo sseeiizzee AAf f rriiccaann eemmeerrggiinngg ooppppoorrttuunnii

ing markets

ocation is an independent investment research ant class top-down and bottom-up allocations, and i

onal) around the world in general, on emerging mrkets.

nd recommendations by identifying key structuraleral, and African economies in particular, utilizingches and indicators, analytic foundations, and madent investment decisions.

ed and sought-after investment advisor company rg and frontier Africa.

esearch and service, by establishing strong and inc needs by offering investment decision-making porizon.

f an entrepreneurial firm with the analytical rigore highest levels of client service.

Allocation

1-6

Page 21

ttiieess

d consultancy firm,deas to investment

arkets in particular,

and cyclical themesrigorous and

rket experience to

egarding

teractive relationshipocess that match

of a research