Embed Size (px)

Citation preview

Information and Liquidity of Over-the-Counter Securities:

Evidence from Public Registration of Private Debt

Song Han

Federal Reserve Board

Alan G. Huang

University of Waterloo

Madhu Kalimipalli

Wilfrid Laurier University

Ke Wang

Federal Reserve Board

This version: June 10, 2017

Preliminary. Comments Welcome.

Abstract

The Rule 144A private debt represents a significant and growing segment of the U.S. bond market.

A large fraction of 144A bond issues carry registration rights and are subsequently publicly

registered. We examine the market liquidity effects of enhanced information induced by the public

registration of private debt. Using the regulatory version of TRACE data for the period 2002-2013,

we find that following public registration of 144A bond, liquidity cost of trading these bonds

measured by dealer-specific effective bid-ask spreads narrow. The spread reduction is larger for

issues with higher ex-ante information asymmetry. Our results are consistent with existing

theories that financial transparency reduces information risk and thus improves market

liquidity.

Keywords: Rule 144A bond, broker-dealers, public registration, liquidity, information disclosure

JEL Classifications: G12, G14

The views expressed herein are completely our own and do not necessarily reflect the views of the Federal Reserve

Board or its staff. We acknowledge discussants and participants at the Third Ontario Universities Accounting and

Finance Symposium, 2017 Annual Meeting of the Mid-West Finance Association, and 2017 Annual Fixed Income

and Financial Institutions Conference, University of South Carolina for their helpful comments. (Accepted for

presentation at the 2017 European Finance Association Meetings, Mannheim, and Summer School on Liquidity in Financial Markets and Institutions, Washington University in St. Louis)

2

1. Introduction

A wide range of corporate securities and derivatives are traded in the over-the-counter

(OTC) market, where market-makers and investors search for trading counterparties and bargain

over trade terms. Theories show that asymmetric information among traders about issuer’s

financial conditions is one of major factors contributing to search frictions and market liquidity in

trading these securities (e.g., Duffie 2012). In practice, the extreme cases of Iliquidity episodes

include trading halts of specific securities due to lack of information, for example, when a firm

fails tofile periodic public reports. Trading conditions may also deteriorate sharply across the broad

market when the information risk becomes too high, as occurred during the recent financial crisis.

In this paper, we provide a quantitative analysis of how asymmetric information in

corporate finance impacts the trading liquidity in the market for corporate bonds—an OTC market

that has received a great deal of attention in recent years. Our focus on the informational effect

contributes to this growing literature, because most existing studies examine the impact on bond

liquidity of opacity in trading activities and market fragmentation.1 Our premise is the following.

The standard OTC theory implies that greater public disclosures of an issuer’s financial conditions

should improve the market liquidity of the issuer’s bonds, because public disclosure reduces the

extent of information asymmetry among traders (see, for example, Diamond and Verrecchia, 1991,

Easley, Hvidkjaer, and O’Hara 2002, Greenstone, Oyer, and Vissing-Jorgensen 2006).

We examine the liquidity effect on OTC securities of information disclosure in the context

of the public registration of the Rule 144A corporate bonds. Adopted in 1990, the Rule 144A

provided a safe harbor from the public registration requirements of the Securities Act (1933) for

resales of restricted securities to “qualified institutional buyers” (or QIBs), which generally are

large financial institutions and other accredited investors.2 Interestingly, while the Rule 144A

bonds are issued at “dark exclusively to QIBs,” many of them carry registration rights and are

1 Typical for an OTC market, corporate bond trading is generally opaque. Several studies find that trading costs have

declined after increased post-trade transparency on transaction information (Bessembinder, Maxwell, and

Venkataraman (2006), Edwards, Harris and Piwowar (2007), Goldstein and Hotchkiss (2007), and Goldstein,

Hotchkiss and Sirri (2007)). A large literature has examined the role of information asymmetry among traders in the

market liquidity of equity trading. See, for example, Glosten and Milgrom (1985), Glosten and Harris (1988),

Madhavan, Richardson, and Roomans (1997), and Huang and Stoll (1997). 2 Specifically, QIBs are the following financial entities: 1) an institution (e.g., an insurance company, investment

company or pension plan) that owns or invests at least $100 million in securities of non-affiliates; 2) a bank or savings

and loan (S&L) association that meets condition 1) and also has an audited net worth of at least $25 million; 3) a

broker or dealer registered under the Exchange Act, acting for its own account or for that of QIBs that own and invest

at least $10 million in securities of non-affiliates; or 4) an entity whose equity holders are all QIBs.

3

subsequently publicly registered.3 As required by the securities law, issuers need to disclose their

financial conditions as part of the public registration. Importantly, public registrations generally

entail an offer of new public bonds to exchange for the target Rule 144A bonds, where the terms

of the new bonds are mostly identical to those of the exchanged ones. As such, the 144A public

registrations don’t accompany changes in the issuer’s fundamentals such as leverage, allowing us

to better identify the informational effects on OTC trading liquidity.

Assessing the liquidity effect of the Rule 144A public registration can help shed light on

the informational effects for the broad bond markets. First, since its inception, Rule 144A corporate

bonds have quickly become an important source of corporate financing. For example, according

to the Fixed Income Securities Database (FISD), between 1990 and 2013, Rule 144A bonds

account for 20 percent of the total corporate bonds issued by U.S. firms, with the growth

particularly strong since the recent financial crisis.4 Second, secondary market volumes of 144A

bonds are also sizable, representing nearly 20 percent of the average trading volumes of all

corporate bonds (FINRA,,2014).5 To the best of our knowledge, we provide a first comprehensive

study on the market liquidity effects of Rule 144A public registration, which sheds light on the

general issue of the information effects on OTC trading.

We find that liquidity improves following public registration of 144A bonds and that the

improvement is larger for issues with higher ex-ante information asymmetry. Our analysis takes

advantage of the comprehensive version of the Trade Reporting and Compliance Engine (TRACE)

data for the period 2002-2013. The data contain transactions of all bonds reported to the Finance

Industry Regulatory Authority (FINRA), including those that previously were not disseminated to

the public, among which are Rule 144A bonds.6

To begin, we examine the change of trading costs following the public registration. Our

main measure for trading costs is the round-trip costs of trading (RTC). Following, for example,

3 Extant literature provides a wide range of estimates on the extent of exercises of these registration rights. Depending

on the sample used, over 30-90% of the 144A bonds are publicly registered in the few months following issuance.

See, e.g., Livingston and Zhou (2002), Huang and Ramirez (2010), and Craig (2012). 4 Specifically, out of the total $20.7 trillion of corporate debt issued during 1990-2013, $4.1 trillion was Rule 144A

debt. Also, 144A bond issuance as a share of total U.S. corporate bond issuance rose from 23.40 percent during pre-

crisis period ( 1999-2006) to 37.62 percent in post-crisis period (2010-2013). 5 Dan Caplinger, “How Rule 144A Created a Shadow Financial Market.” Motley Fool, 7/3/2015

(https://www.fool.com/investing/brokerage/2015/07/03/how-rule-144a-created-a-shadow-financial-market.aspx). 6 This regulatory data for this study is provided by FINRA to the Federal Reserve Board under a data sharing

agreement. Note that FINRA phased in public disseminations of non-Rule 144A from July 2002 to February 2005,

and started to disseminate Rule 144A transactions to the public on June 30, 2014, with 18 months of time lag.

4

Goldstein, Hotchkiss, and Sirri (2007), the RTC measure is the difference of transaction prices

between a dealer’s sale to a customer and a dealer’s purchase from another customer for the same

security on the same day. Since we observe the identification of the broker-dealers intermediating

each trade, we are able to compute dealer-bond specific RTC, which is closer to the true dealer-

specific effective bid-ask spread. OTC markets such as the Rule 144A market are often

characterized by sporadic trading and traders’ specific portfolio needs, making trade size-based

measures such as Amihud’s (1989) price impact measure less desirable. Using RTC as the liquidity

measure avoids such pitfall.

We search 144A bond registrations by matching bond specific attributes, combined with

validation of registration-key words in bond prospectuses. A Rule 144A bond becomes registered

mostly through an exchange offer in which the debtor issues registered public securities to tender

for the 144A bond. For every 144A bond, we search the FISD database to locate a public bond

subsequently issued that matches key characteristics of the 144A bond. We then validate the

matching by searching exchange offer-related key words in the prospectus of the public bond. Our

results show that on average, registration reduces RTC by 3.3 (5.0) basis points 100 (30) days

around the registration, or about 12 (19) percent of its pre-registration level.

We then conduct three sets of difference-in-difference (DID) analysis to address the

identification concern that the changes in trading liquidity around the public registration may be

attributable to factors other than changes in information environment regarding the 144A issuer’s

financial conditions. We take comfort in that 144A public registrations are not associated with

capital structure and funding changes, because the new public bond offered to replace the existing

144A bonds is identical to the tendered bond except the security legend. Even so, other factors, such

as market conditions, may change around the registrations and in turn affect bond liquidity.

Addressing this concern, we contrast the change in trading liquidity of bonds that are more likely

to experience changes in information environment with that of other control bonds. The premise is

that if the information disclosure matters for trading liquidity, then the public registration effects

should be stronger among issuers with greater information risk pre-registration.

The three sets of DID analysis are as follows. Firstly, focusing on the 144A bonds

experiencing public registrations, we contrast those issued by firms with public equities with those

by private firms. Because public firms disclose regularly their financial conditions, public

registration of their 144A bonds may have relatively less information content, when compared to

5

to 144A registrations of private firms. Secondly, we use an issue-specific proxy for the extent of

possible changes in information risk. Specifically, following the recent literature of SEC filing

analysis (e.g., Li 2008, Loughran and McDonald 2013, Ertugrul et al. 2015), we use three metrics

from bond prospectus to measure ex-ante information asymmetry of a public issue: total word

count, count of uncertainty words, and file size. This school of literature finds evidence for

“information obfuscation,” where issuers tend to hide adverse information through lengthy filings

(Bloomfield 2002). Lastly, we construct a matched sample of public (non-144A) bonds as our

control group. We expect the 144A debt registration for public firms to informationally less

prominent. For each 144A bonds experiencing public registration, we find a set of public bonds

with same industry, credit rating, callability, remaining bond maturity, and bond issue size. We

compare the changes in RTC between the 144A bond and its matched public bond around the

registration event. Overall, these three sets of DID analysis find that the RTC measure of bid-ask

spreads decreases post registration, and it is more so for firms with high information asymmetry

pre-public registrations. These findings suggest that increased corporate information disclosure

associated with public registration improve the market liquidity of OTC securities.

Measuring the impact of registration on bond pricing, we find that yields on average

decrease by 16 basis points and daily returns decrease by 3 basis points following registration,

consistent with previous empirical studies on 144A bonds. We also find that trading activities are

subdued following public registration, based on both trading volume and frequency of trading,

regardless of more retail investors entering the market; and that bond dealers tend to reduce their

net positions following public registration of 144A bonds. Since registration is an expected event,

some institutional traders may have reasons to trade 144A bonds ahead of registration time more

actively. Although post- registration, retail investors can enter the market, as they might behave

more like “busy-and-hold” investors, we tend to observe less active trading activity. However, if

we measure liquidity in terms of trading costs such as effective bid-ask spread, we still conclude

liquidity improves after registration. In a public bond market setting, Goldstein, Hotchkiss and

Sirri (2007) finds that enhanced transparency is not associated with greater trading volume, which

is consistent with our findings.

Overall, this paper contributes to the empirical literature showing that public disclosure

reduces liquidity costs for OTC securities. Following public registration of 144A bond, bid-ask

spreads narrow, and more so for firms with higher ex-ante information asymmetry. We believe

6

our paper is the first to identify the relationship between financial information asymmetry and

liquidity cost based on bond transaction data. It also complements empirical studies on bond

liquidity with detailed examination on Rule 144A bonds, which are often omitted in earlier

literature using TRACE database since the dissemination of this type of bonds is only recent

and our regulatory version of data contains all 144A bond transactions reported in TRACE but

not disseminated before.7 The rest of the paper is organized as follows. Section 2 discusses our

contributions to the literature. Section 3 describes our data, sample construction, and liquidity

measures. Section 4 presents our main empirical results on the impact of registration to liquidity

and trading activity. Section 5 provides additional robustness tests and other findings regarding to

yields and trading activities. Section 6 concludes.

2. Related Work

Our paper contributes to three related strands of literature that are summarized below.

2.1 Studies on Public Disclosure, Liquidity and Asset Pricing in OTC Markets

Our paper contributes to the broad literature on the effect of corporate information

disclosure on market liquidity and asset prices. A key insight of this literature, including standard

market microstructure theory, is that the market liquidity of traded securities reflects the risk of

asymmetric information about the issuer’s financial health (e.g., Glosten and Milgram 1985,

Diamond and Verrecchia 1991, and many others).

More specifically, our paper is more closely related to the strand of literature of how public

disclosure of corporate information in OTC markets affects liquidity and asset prices. Most of these

studies focus on OTC stocks. In particular, studies have found that market liquidity and asset prices

in the OTC stocks improve following mandatory disclosure requirements, because higher quality

financial reporting and better disclosure can reduce information asymmetry (e.g., Healy, Hutton,

and Palepu 1999, and Leuz and Verrecchia 2000, Easley, Hvidkjaer, and O’Hara 2002, Greenstone,

Oyer, and Vissing-Jorgensen 2006, Brüggemann, Kaul, Leuz, and Werner 2016).8 White (2016)

7 As of June 2014, FINRA (Financial Industry Regulatory Authority) started releasing 144A transaction data on

TRACE . 8 For example, Greenstone, Oyer, and Vissing-Jorgensen (2006) analyze the effects of mandatory disclosure

requirement using 1964 Securities Acts Amendments in U. S. equity markets and find the Amendments created $3.2

7

using a proprietary database of transaction-level OTC shows that the typical OTC investment

return is severely negative and that investor outcomes worsen for OTC stocks that have weaker

disclosure-related eligibility requirements. A number of recent studies also examine liquidity of

OTC equities per se and have similar findings on information effects. For example, different market

tiers of information disclosure are related to liquidity in both the OTC markets (Davis, Van Ness

and Van Ness 2016) and the Pink Sheet markets (Jiang, Petroni and Wang 2016). Ang, Shatuber

and Tetlock (2013) find that there is an illiquidity premium among OTC stocks and that the

premium is largest among stocks held predominantly by retail investors and those not disclosing

financial information in the OTC stocks.

Our paper is also related to the impact of corporate disclosure in the bond market. Duffie

and Lando (2001) theorize that imperfect accounting information due to infrequent accounting

disclosure contributes to the relatively elevated yield spreads of short-term corporate bonds, an

aspect that has been found puzzling for some time in studies of the term structure of corporate bond

yield spreads. Examining only corporate bond prices, Yu (2005) empirically verifies the prediction

of Duffie and Lando (2001) that firms with better information disclosure rankings tend to have

lower credit spreads, and that the transparency effect is especially large among short-term bonds.

Tang (2012) examines how proprietary costs of mandatory disclosure influence the decision to

exclude registration rights in private debt placements, and finds that, at the industry level,

industries dominated by players with “product differentiation strategy” have a larger proportion of

private placements without registration rights than product markets dominated by players with

“low cost strategy.”

A number of studies, also mostly on equity trading, assess the quantitative importance of

information risk on market liquidity by estimating the information component in bid-ask spreads—

a common measure for trading cost. For example, it is documented that the adverse selection risk

associated with information asymmetry among market participants about issuers’ financial

conditions leads to higher bid-ask spread (e.g., Huang and Stoll, 1987; Glosten and Harris, 1988;

Madhavan, Richardson, and Roomans,1997). An exception to these equity studies, Han and Zhou

(2014) estimate the information asymmetric components of corporate bond trading bid-ask spreads

to $6.2 billion of value for shareholders of the OTC firms in their sample. Brüggemann, Kaul, Leuz, and Werner

(2016) analyze a comprehensive sample of more than 10,000 U.S. OTC stocks and find that OTC firms that are subject

to stricter regulatory regimes and disclosure requirements have higher market quality (higher liquidity and lower crash

risk).

8

and examine the pricing implications of informed trading and its ability to predict corporate

defaults. They find that microstructure measures of information asymmetry seem to capture adverse

selection in corporate bond trading reasonably well.

Rule 144A debt has peculiarities. Bolton, Santos, and Scheinkman (2012) argue that the

disclosure exemption in the “dark” markets such as 144A allows informed “qualified” institutional

investors to exploit their information advantage. They explain that shadow financial sector exists

because they prevent dissemination of valuable information about asset values, and hence cream-

skim most valuable assets away from public, transparent, exchanges in turn leading to reduced

access of retail investors to the most lucrative investments. In terms of improving the post-

registration transparency, 144A debt registration can also be resemble “going public” exercise

using debt. However, the major difference of the 144A registration is that it doesn’t involve any

effective changes in firm’s funding or leverage. This factor helps our identification, separating our

study from previous studies on the information effects of bond IPOs (e.g., Datta, Datta and Patel

1997, 1999, 2000; Cai, Helwege and Warga 2007; Datta, Datta and Raman 2000).

Overall, our finding of positive effects of public disclosure on the corporate bond liquidity

is consistent with previous empirical evidence that information transparency generally improves

market liquidity.

2.2 Studies on Corporate Bond Market Liquidity

Our study also brings a new empirical angle toward the understanding of the corporate

bond market liquidity, a research area that has drawn growing attention in recent years. Previous

studies have examined the role of trading opacity and market fragmentation in the corporate bond

market liquidity. For example, in terms of trading opacity, studies find that TRACE dissemination

of transaction information results in lower transaction costs (e.g., Bessembinder, Maxwell, and

Venkataraman 2006, Edwards, Harris and Piwowar 2007, Goldstein and Hotchkiss 2007, and

Goldstein, Hotchkiss and Sirri 2007).9 Similarly, Green, Hollifield, and Schurhoff (2007a, 2007b)

and Green, Li and Schurhoff (2011) find positive effects of trade dissemination on transaction

9 Specifically, Bessembinder, Maxwell and Venkataraman (2006) report a 50% reduction in institutional trade

execution costs upon introduction of TRACE for bonds eligible for TRACE transaction reporting, in addition to a

liquidity externality of another 20% reduction of trade execution costs for non-TRACE bonds. Goldstein, Hotchkiss

and Sirri (2007) finds that enhanced transparency is not associated with greater trading volume, which is consistent

with our findings.

9

information in the municipal bond market. In terms of market fragmentation, Huang, Sun, Yao

and Yu (2015) show that liquidity clienteles affect corporate bond prices, and specifically, both

the level and volatility of liquidity premia are substantially attenuated among corporate bonds

heavily held by investors with a weak preference for liquidity. Recent studies also debate on

whether bond market liquidity increases or not in recent years following the recent financial crisis

and post-crisis regulations including the Volcker Rule and Dodd-Frank Act (e.g., Adrian, Fleming,

Shachar and Vogt 2105, Trebbi and Xiao 2015, Bao, O’Hara and Zhou 2016, Dick-Nielsen and

Rossi 2016, Anderson and Stulz 2017).

2.3 Studies on 144A securities

Our paper also complements existing studies on 144A securities by focusing on the

liquidity effects of information transparency on corporate financial conditions brought by public

registration of private debt. Previous studies on 144A corporate bonds generally examine their

yield premium compared to public bonds. For example, in an earlier study, Fenn (2000) documents

that among high-yield issuers between 1996 and 1997, yield premium for 144A bonds relative to

their public counterparts vanishes over time before registration so that registration does not have

much information value. Follow-up studies expand the data to include investment-grade issues and

draw different conclusions regarding yield premium of private issues. These studies find that Rule

144A debt on average has higher yield than their public counterparts (e.g., Livingston and Zhou

2002, Chaplinsky and Ramchand 2004, Craig 2012).

The majority of above studies conjecture that investors in 144A bonds generally require

higher yield because of lower liquidity and higher degree of information opaqueness in the private

debt market. Our paper is the first to provide direct evidence on the liquidity factor. Because our

liquidity measure is based on intra-day transaction data at the dealer-bond level, we provide a more

accurate proxy for trading cost. In addition, our DID approach better helps identify the information

disclosure effects from other factors that may potentially be associated with the changes in

liquidity conditions.

Our paper also relates to corporate finance studies on the 144A securities market examining

the choice between public bonds and 144A private issuance. These include, for example, the 144A

debt issuance by foreign firms where 144A market is fast replacing the public debt market for high

yield and non-rated international issues (e.g., Miller and Puthenpurackal 2002, Huang and Ramirez

10

2010, Gao 2011, Huang, Kalimipalli, Nayak and Ramchand 2016), and the role of corporate

governance, market timing, and market competition in the decision of public vs. private debt or

equity financing (Arena and Howe 2009, Barry, Mann, Mihov, and Rodríguez 2008). The

empirical evidence is broadly consistent with the notion that costs associated with mandatory

disclosure regulation have an economically significant impact on the financing choice between

public and private financing.

Our paper complements a recent study on 144A securitized (collateralized) securities by

Hollifield, Neklyudov and Spatt (2014), who also examine market liquidity using transaction data.

Their focus is the role of dealers in a network setting in liquidity provision, and they find that

central dealers receive relatively lower spreads than peripheral dealers, with the centrality discount

stronger for 144A securitizations.

3. Data and Sampling

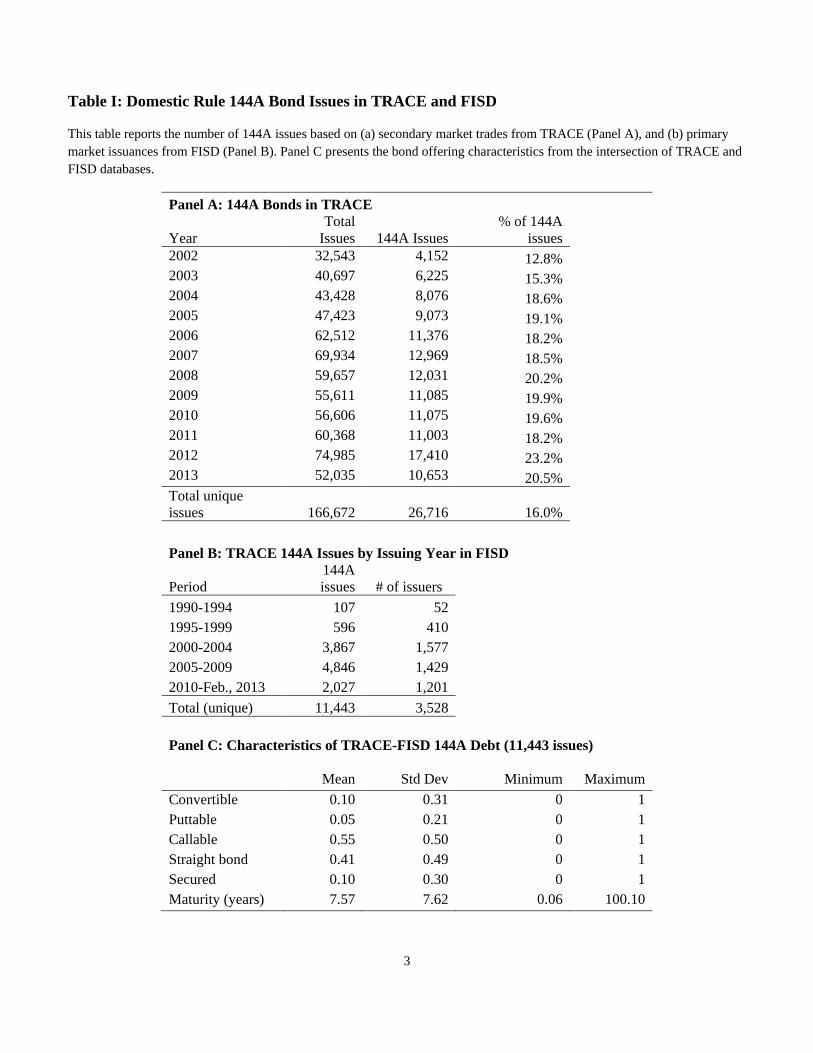

3.1 Rule 144A Bonds in TRACE and FISD

Our study focuses on the 144A bond issues that are subsequently registered as public

bonds. We use Mergent’s Fixed Income Securities Database (FISD) and the Trade Reporting and

Compliance Engine (TRACE) to construct our initial sample. To start, we use FISD’s 144A

indicator to extract the corporate 144A bonds issued from 1990 (the inception of Rule 144A bonds)

to 2013. We then examine 144A bond trading using transaction level data provided by the FINRA

using the regulatory version of the TRACE data. Our TRACE data covers the period of July, 2002

to February, 2013, and contains corporate bond transactions for both publicly and non-publicly

disseminated bonds; the latter include144A bonds which were issued to QIBs.10

We follow Dick-Nielsen (2009) and Dick-Nielsen et al. (2012) to filter the raw TRACE

data for cancelled trades, erroneous entries, reversals, duplicated reports, as well as trades with

non-positive prices or non-positive volumes. We present the summary statistics of the final 144A

TRACE data in Table 1. Panel A of Table I lists the number of bond issues classified into 144A

10 FINRA began to release to the public Rule 144A transactions on June 30, 2014. However, the public version of

TRACE has a very limited coverage of Rule 144A transactions for earlier years as of 2015. In addition, the regulatory

version of TRACE contains dealer ids which are necessary to construct our liquidity measures. To ensure accuracy,

we double check the TRACE 144A bonds with those from FISD.

11

and non-144A categories using the 144A flag in the TRACE data. We observe that during the 2002

to 2013 sample period, 12% to 23% of bonds traded each year in the market are 144A bonds. In

our entire secondary trading sample of TRACE data, there are 26,716 unique issues, or 16% of all

bonds, that are issued as 144A bonds. Panel A of Table 1 indicates that 144A bonds is a significant

portion of the bond universe in TRACE.

[Table I about here.]

We rely on FISD for bond characteristics. Intersecting FISD with TRACE bonds in Panel

A of Table I based on issue CUSIP and restricting bond issuers to be corporations domiciling in

U.S. leaves us with 11,443 Rule 144A bond issues from 3,528 issuers. Panel B of Table I lists the

number of these bonds by their origination year. We observe that 144A bonds with reported trades

in TRACE during 2002-2013 are mostly issued during those years or slightly prior to year 2002.

Panel C of Table I shows the primary market bond characteristics of the TRACE-FISD

Rule 144A bonds. While most bonds are non-convertible, non-puttable and non-secured, more

than half of the issues are callable. The average offering maturity of these bonds is 7.57 years, or

medium to long-term.

3.2 Public Registration of Ru1e 144A Bonds

Previous studies, such as Livingston and Zhou (2002) and Huang and Ramirez (2010),

search company filings in EDGAR to identify subsequent registration of 144A bonds. We instead

mainly use a matching sample approach to identify 144A registration events. The information on

the 144A registration rights clause or the exercise of the rights is not readily available. However,

Rule 144A securities become registered mostly through an exchange offer in which the debtor

issues registered public securities (with a new CUSIP) to tender for the 144A securities.11 The

prospectus for the 144A issues typically states that the new bonds issued pursuant to such an offer

will be substantially identical to the 144A bonds for which they may be exchanged in several

attributes, such as coupon rate, maturity date, security (collateral), and restrictive covenants.

Therefore, for every 144A bond, we search the FISD database to see if we can find a public bond

that matches key characteristics of the 144A bond, and we treat the matched bond as the

11 An alternative, but seldom used, procedure is to register the 144A bonds using a shelf registration. Comparing to

the exchange offer approach, the shelf registration can be more burdensome to the issuers because the likely holders

of securities at the future date of the registration must be included in the prospectus—a requirement that makes it

onerous for a broader investor base in the longer run.

12

corresponding registered bonds and its issuance date as the registration date.

Specifically, our matching criteria are as follows: (i) the public bond is issued by the same

borrower zero day to five years (inclusive) after the date of the 144A issuance; (ii) the difference

in the dates of maturity of the two bonds is no greater than 30 days; iii) the difference in the offering

amount of the two bonds is no greater than 5 percent; (iv) the two bonds have the same coupon

rate and same coupon type (fixed or variable);12 (v) the two bonds have the same security condition

(secured or not); and (vi) the two bonds have the same “straight” characteristic (straight bond or

not, where straight bond is defined as non-convertible, non-puttable, and non-callable). From Panel

C of Table I, we note that 10% of the 144A bonds are secured and 41% of the 144A bonds are

straight.

The matching process yields 2,749 bonds for the universe of 11,443 bonds in Panel B of

Table I, i.e., about 25% of the TRACE-FISD 144A bonds are subsequently registered. This

percentage is in line with 30% reported in Craig (2012) and 40% of investment grade bonds

reported in Livingston and Zhou (2002), who, unlike us, rely on Thompson SDC, EDGAR filings,

and Bloomberg data to identify registration.13

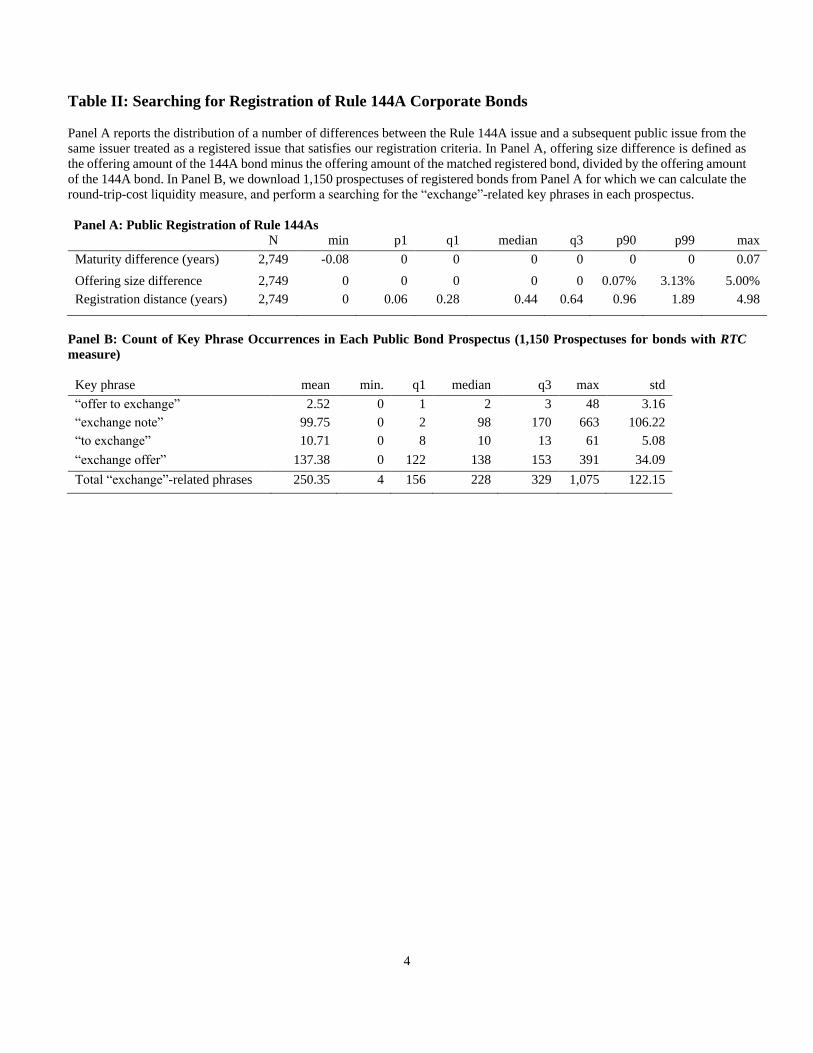

Panel A of Table II provides the characteristics of the registration. More than 99% of the

matched pairs have exactly the same maturity, and more than 75% (90%) of the matched pairs

have exactly the same (less than 0.1% difference in) the offering amount. The slight differences in

the offering amount in the right tail of the distribution may be due to early payment such as sinking

fund. More than half the registrations take place within half a year of 144A issuance, and more

than 95% of the registrations take place within a year. Even though we allow for five years to

search for potential registration, these results indicate that the registration, if any, takes place

quickly.

[Table II about here.]

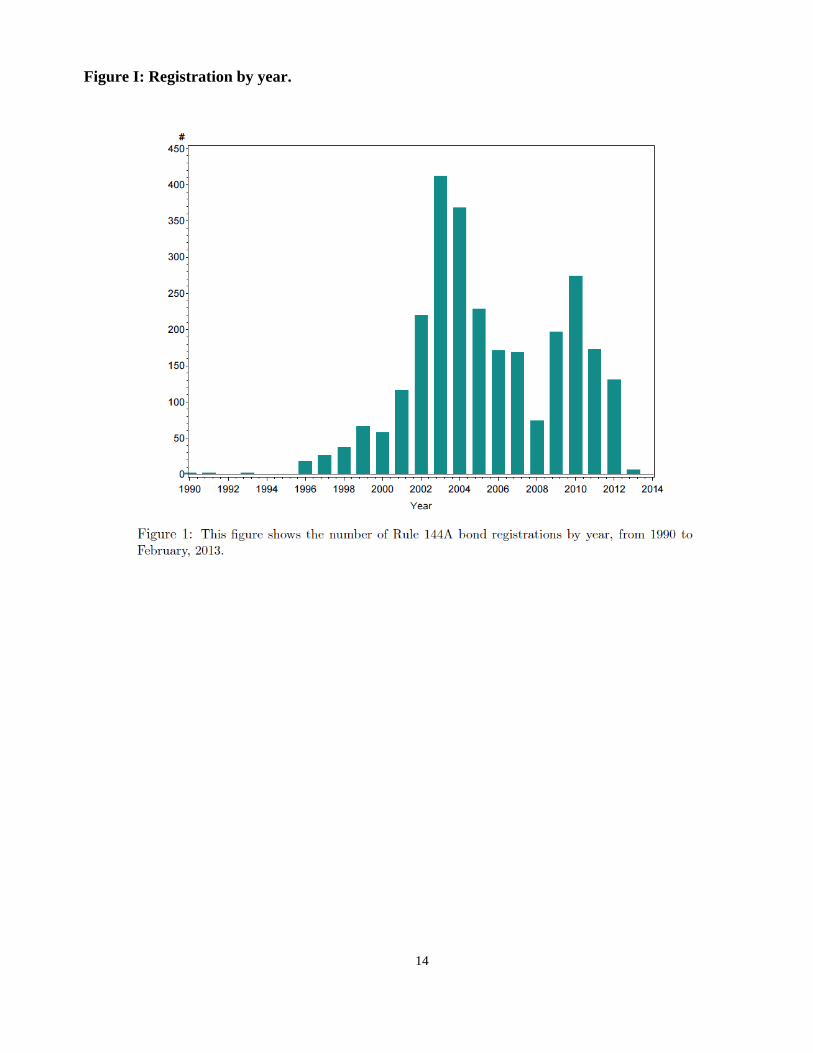

Figure 1 shows the number of registrations by year. Before 1996, registrations were scant

(partly due to the lack of Rule 144A bonds). The number of registrations increased steadily since

12 We impose condition iv) because maintaining the same coupon rate is one motivation for Rule 144A bonds to be

registered. Livingston and Zhou (2002) document that for Rule 144A bonds with the registration-rights clause, a

failure to register would in most cases result in an increase in the coupon rate, and hence issuers are motivated to

register the bond to avoid the increase of coupon rate when a registration-rights clause exists. 13 Some authors report that for subsets of 144A bonds, the registration rate is much higher. For example, Huang and

Ramirez (2000) document that the registration rate for all 144A convertible debt issues is about 88% for the sample

period of 1996 to 2004. Note that in Panel C of Table I we identify that convertible debt issues only consists of 10%

of all domestic 144A debt issues for our sample period.

13

1996, only to peak in 2003 to reach 412 registrations. The recent financial crisis only deterred

registration briefly in 2008, and registration activities since 2009 returned to normal level

comparable with previous periods. We also note that there are far fewer registration events before

the TRACE availability year of 2002. There are 2,487 or 90% of the registrations on or after 2002.

Therefore, it is suitable to use TRACE data to examine the effect of registration.

[Figure 1 about here.]

We provide further validation of the registration events identified above by examining the

EDGAR filings of the registered bonds. Specifically, we employ machine searching of bond

prospectuses to ensure that the matched procedure that we used above indeed produces registered

bonds of 144As. In registering a public bond for the 144A bond, the issuer makes an exchange

offer. To prepare key words for machine reading, we first read a number of bond prospectuses. We

note that the following four phrases appear frequently in the exchange-offer prospectuses: “offer

to exchange”, “exchange offer”, “exchange note”, “to exchange.” We hence count the number of

appearance of these phrases in bond prospectuses to verify that the pairs that we identified in Table

II are indeed 144As and their exchange offers.

Out of the 2,749 matched bond pairs, we are able to download 1,150 prospectuses from the

SEC’s EDGAR website for those issues that we can calculate the bid-ask spread measure of round-

trip cost (to be elaborated in the next section).14 Panel B of Table II provides the summary statistics

of the above key words in these prospectuses. 98.2% (99.7%) of the prospectuses contains at least

fifty (five) occurrences of the aforementioned exchange-related phrases; and the minimum number

of occurrences of those key words in a prospectus is four times. Out of the four key phrases,

perhaps not surprisingly, “exchange offer” and “exchange note” make the most frequent

appearance, each appearing on average 100 or more times in a prospectus. These results suggest

that our filtering of 144A registration is highly effective. We keep all of the matched pairs in our

sample, but note that our results are robust to excluding the registered issues whose prospectuses

have fewer than fifty occurrences of the exchange-related phrases.

In untabulated results, we also investigate whether there is a change of registration

activities after 2008 (inclusive), since year 2008 witnessed not only the financial crisis, but also a

regulatory reform on Rule 144A debt. Prior to 2008, non-affiliate QIBs (i.e., QIBs that are not in

a relationship of control with the issuer) can freely trade 144As after a two-year holding period

14 These prospectuses appear in the form of 424 or S-4.

14

when the bond issuers meet certain public-information disclosure requirement. After 2008, the

SEC halved the holding period to one year, and all the disclosure requirements are lifted. In other

words, after 2008 non-affiliate QIBs only need to hold 144A bonds for a year before they can

freely resell the bond to anyone. Such regulatory change may also affect how market accepts 144A

bonds. In our sample, post 2008, there are 2,887 144A offerings; out of which, 855, or 29.6% of

144As are subsequently registered. Out of that sample, time to registration has a higher median

value of 0.56 years. Hence, there is no discernible difference in the registration rate before and

after 2008.

3.3 Liquidity Cost Measures

Our research goal is to investigate the impact of financial information disclosure of bond

issues on the liquidity cost of trading as these bonds transfer from 144A to public bonds. Among

the prevailing bond trading liquidity measures, the most relevant and suited to our empirical

enquiry is DRT (dealer round-trip) liquidity measure used in Goldstein et al. (2007). The DRT

metric is based on transaction prices of opposite sides of trades matched by the same dealer and

the same trading volume.Hence we construct a “round-trip cost” measure of liquidity (RTC) as

follows and develop our main results of liquidity cost comparison before and after 144A bonds’

public registration based on this RTC measure. We will discuss results using other bond trading

liquidity measures in Section 5 under further robustness checks.

For each bond in our sample, we search for matched trading pairs within the same day for

the same dealer15 and the same trading volume at the opposite trading sides, taking only dealer to

customer trades into consideration. That is, for each trade in which a customer sells (buys) a bond

to a dealer, we attempt to find a subsequent trade in which the same dealer sells (buys) the bond

with the same amount to another customer within the same day. If we find such a pair, we estimate

the bid-ask spread that the dealer charges to the customers as the difference between the pair of

buy-sell prices.16 Formally, we define this “round-trip cost” (RTC), for each pair of trades as:

𝑅𝑇𝐶 =𝑃𝑎𝑠𝑘 − 𝑃𝑏𝑖𝑑

100

15 To construct such dealer-specific liquidity cost measure, we need dealer ID information for each trades, which is

provided by FINRA to Federal Reserve as part of the regulatory version of TRACE data. 16 In case there are multiple trades that match the original trade in terms of trading volume, trading parties (dealer),

trading sides, and trading day, we select the trade with the closest transaction time.

15

where 𝑃𝑎𝑠𝑘 (𝑃𝑏𝑖𝑑) is the ask (bid) price per $100 par. We define normalized version of liquidity

cost RCT_pct as 𝑃𝑎𝑠𝑘−𝑃𝑏𝑖𝑑

(𝑃𝑎𝑠𝑘+𝑃𝑏𝑖𝑑)/2 . This round-trip cost measure is essentially the bid-ask spread

charged by the same dealer implied from the buy and sell transactions intermediated by the specific

dealer at a specific trading volume. Larger RTC indicates worse liquidity, or equivalently, larger

transaction cost for trading the bond.

We take simple average to aggregate the RTC measures by trading day, bond, and/or

dealer. For example, for each bond and dealer pair, we calculate daily RTC as the average of the

RTCs of all pairs of trades we could identify for the dealer. Daily RTC for each bond is then

averaged across dealers and used as the sample liquidity measure. Clearly, the availability of RTC

depends on whether there exist at least two opposite-side trades on the same bond with the same

volume intermediated by the same dealer on the same day. Although in calculating RTC we do not

cover all of the transactions by disregarding trades without following off-setting same-day trades

by the same dealer, it is known common practice in bond market that dealers do cover the trades

within a short-time period if they are pure market makers.17

Using RTC has advantages in our setting. One advantage of using RTC measure is that we

can separate transactions with different trading volumes while calculating liquidity costs of trade.

As well-documented in bond liquidity literature, unlike stock trading, large trading size is most

likely associated with small transaction cost. With 144A bonds’ public registration, retail investors

begin to trade these bonds, so naturally the average trading size will become smaller after

registration, causing larger transaction costs per trade, if we do not control away the trading size

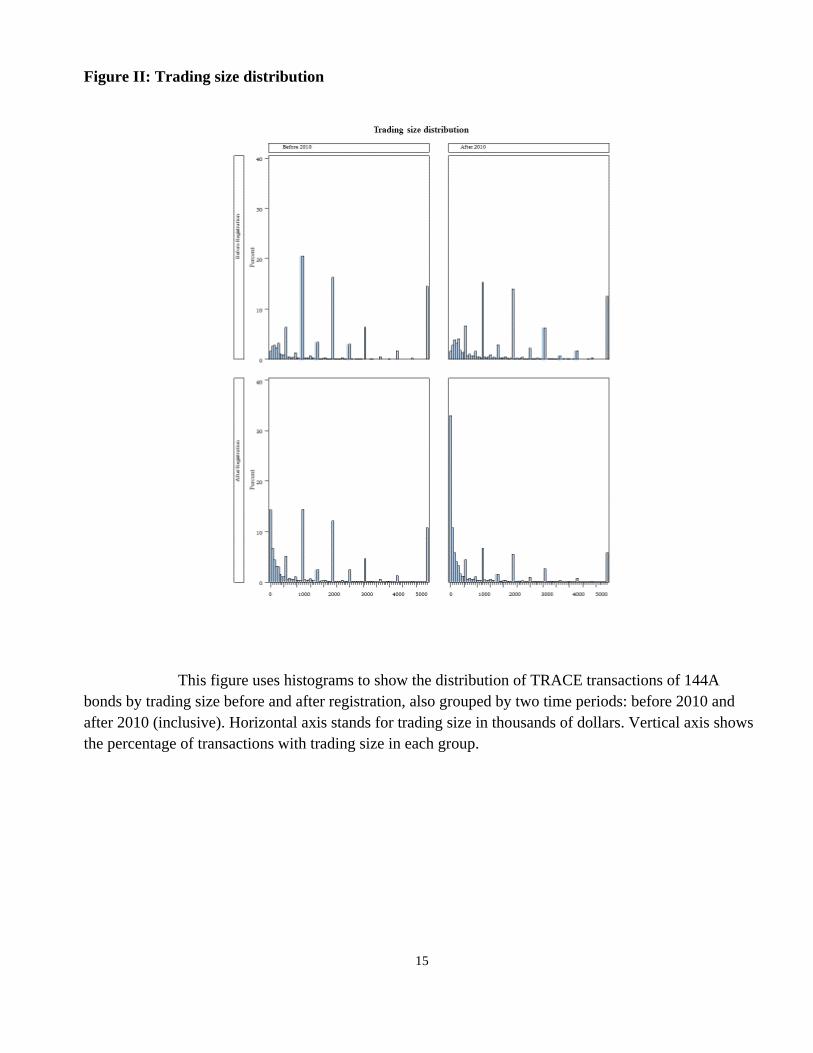

change. Figure 2 shows histogram of trading size distribution before and after registration. Clearly

after registration, larger percentage of trades have transaction size lower than $1mil. We also

observe such change is more significant since 2010, may be due to some regulation changes that

affect bond trading. In contrast to RTC which requires two sides of trade must have the same

trading volume, some other common liquidity measures, such as Roll’s measure, and measures

based on price dispersion such as half-spreads or min-max spreads, all pool transactions with

different trading volumes together while calculating liquidity. The price impact measure of

liquidity, Amihud measure, although commonly used in equity market hasbeen criticized for

17 Roll’s measure, requiring at least three trades on the same bond within the day, is another widely used liquidity

measure. In contrast, RTC requires at minimum two trades.

16

measuring bond liquidity, as it employs trading size as the denominator. So these other measures

of liquidity have potential to overestimate the illiquidity costs post-registration due to subdued

trading activity arising from small transactions, rendering them less suitable for our study.

[Figure 2 about here.]

Another advantage of choosing RTC as the liquidity measure is that in general, it is less

contaminated by intra-day price volatility although during very volatile days, fundamental price

movements may also affect RTC. The impact of volatility on RTC measured is likely to be smaller

compared to other liquidity measures.

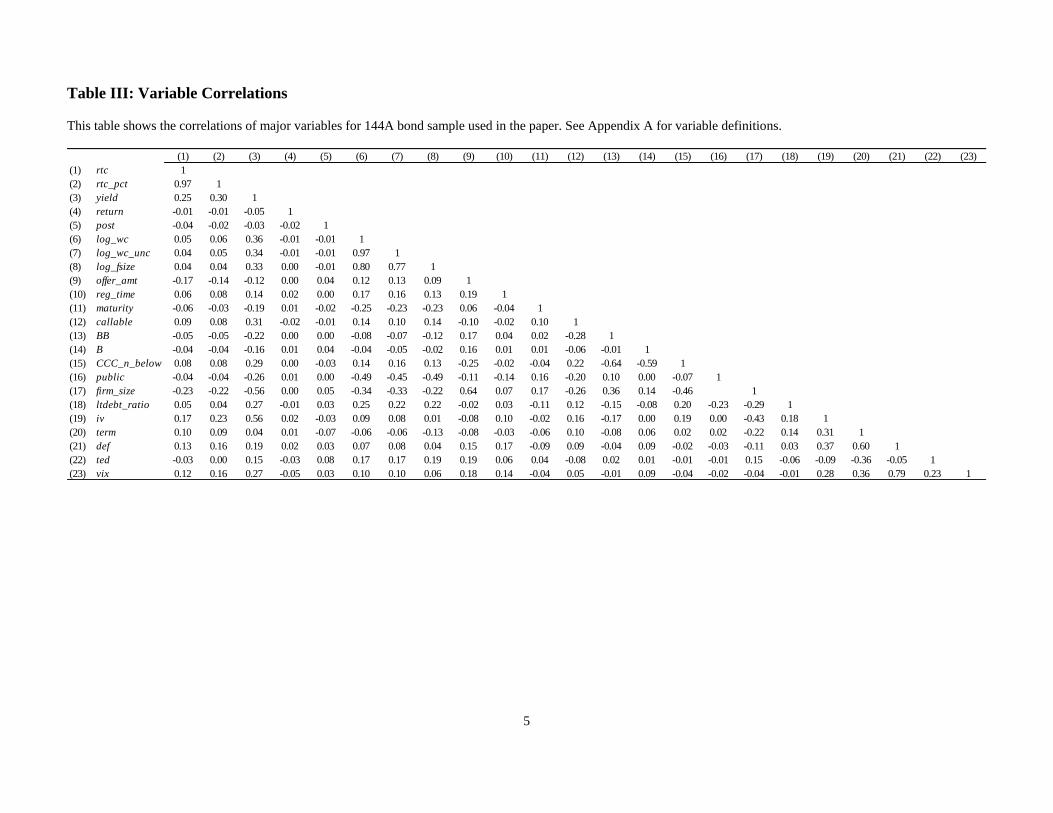

3.4 Sample Correlations

We use 100 trading days around registration as our primary event window. For the 2,487

matched registered bonds after 2002, we are able to calculate the round-trip-cost of 1,734 bond

pairs, or more than two thirds of the sample. Table III shows the correlations among the major

variables used in the paper. The registration indicator variable, post, which takes the value of zero

(one) for the transaction time before (post and including) registration, is negatively correlated with

RTC. The variable post is also negatively correlated with yield. The table also reports that,

consistent with conventional wisdom, RTC is negatively correlated with bond offering amount,

firm size, and whether the issuing firm is a public firm or not, and is positively correlated with

firm’s leverage and stock return volatility. These results suggest that dealers provide liquidity to

high information asymmetry issues.

[Table III about here.]

4. Empirical Analysis on 144A Bond Liquidity Around Registration

4.1 Overview of Liquidity Change around Registration

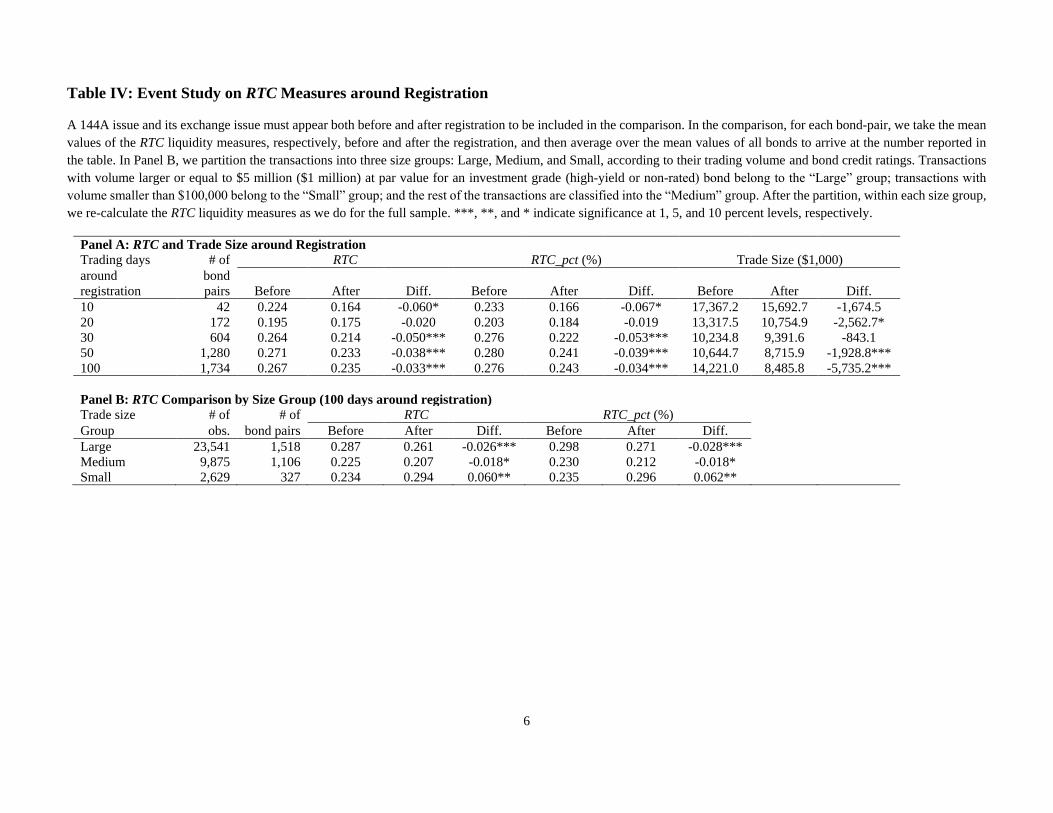

We first examine RTC changes around registration by applying traditional mean-of-mean

approach in event studies. For example, in the comparison of RTC liquidity measures, we take the

mean values of the RTC for each bond-pair, respectively, during specific window periods before

and after the registration, and then average over the mean values of all bonds. This way, each bond

has an equal weight regardless of its trading frequency. Panel A of Table IV offers the comparison

of RTC pre- and post-registration. It shows that RTC decreases after registration regardless of event

17

time window. From windows 30 to 100 days, the differences of RTC and RCT_pct pre- and post-

registration are all significant, and the reduction of RTC ranges from 12 to24%, which is

economically significant.

[Table IV about here.]

The last columns of Panel A of Table IV compares the trade size before and after the

registration, and shows that the average trade size drops after registration, echoing the trading size

distribution in Figure 2. This prompts us to examine the change in RTC conditional on trade size.

Based on trading volume and prevalent bond credit ratings, we partition transactions into three size

groups: Large, Medium, and Small. Transactions with par-value volume larger or equal to $5

million ($1 million) of an investment grade (high-yield or non-rated) bond belong to the “Large”

group; transactions with volume smaller than $100,000 belong to the “Small” group; and the rest

of the transactions are classified into the “Medium” group. After the partition, within each size

group, we re-calculate the RTC liquidity measures as we do for the full sample. Panel B of Table

IV shows that large trades dominate the sample, accounting for around two thirds of the trade

observations. Small trades account for less than 10% of the trades. Noticeably, the reduction of

RTC post-registration occurs mostly for the large trade-size group, and less conspicuously for the

medium trade-size group.

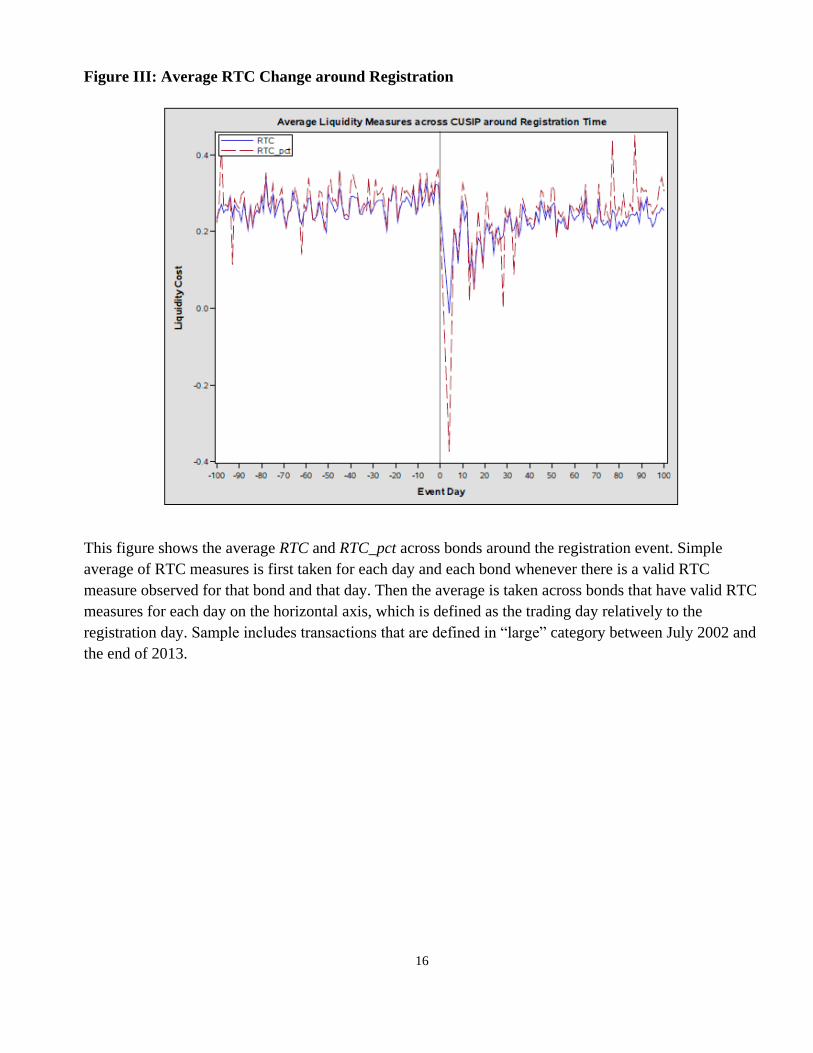

Figure 3 visualizes the decrease of RTC after registration by plotting the average RTC

measures across bonds along [-100,100] trading day window around the registration date, using

only the “Large” transactions in the sample. Plots of other liquidity measures that we checked,

such as Roll’s measure, half-spreads, also demonstrate similar patterns within the “Large”

transaction group, but no obvious change is identified for “Small” transaction group, as transaction

size may intervene with liquidity cost reduction.

[Figure 3 about here.]

4.2 Baseline Regressions of RTC

We then test the univariate results above in regressions that control for both bond cross-

sectional characteristics variables and time-varying macroeconomic variables. In examining the

change of RTC following the public registration, we employ the following baseline regression

specification based on the extant bond liquidity literature:

18

RTCi,t = α + β0 posti + β1 (issue-characteristics)i,t + β2 (firm-characteristics)i,t

+ β3 (aggregate variables)i,t +errori,t (1)

for a given bond issue i at day t. The dependent variables are either of two liquidity measures i.e.

RTC or RTC_pct, and that β1, β2, and β3 refer to regressions coefficients. Our main focus in

Equation (1) is post, the registration indicator. Other regression covariates consist of issue-specific

attributes (offering amount, time to registration, maturity, ratings, and callability dummy), issuer-

specific characteristics (whether the firm is a public firm or not, firm-size, leverage, idiosyncratic

stock return volatility), 18 and aggregate bond market credit and liquidity risk factors (term-

structure slope, default, funding liquidity, and VIX). We control for year fixed effects and

clustering effects by issuer and employ heteroscedasticy adjustments in all regressions. Equation

(1) is our baseline regression to evaluate the effects of registration.

Models (1) and (5) present the results for RTC and RTC_pct, respectively, using bond

transactions 100-days around registration. They first confirm the casual correlation results that we

reported earlier that RTC is negatively related to bond offering amount, firm size and credit rating,

and positively related to stock return volatility, reflecting the conventional wisdom that higher-

quality issue or issuer has better liquidity. Consistent with Table IV, we note that post is negatively

related to RTC and RTC_pct. After controlling for issue- and issuer-specific characteristics and the

macro variables, the effect of post on RTC is economically significant. Registration of 144A debt

reduces RTC by 0.02 (Models 5 and 7), or about 8% of its pre-registration level. The loading of

post on RTC_pct is however not significant. In untabulated results wefind that post is significantly

and negatively related to RTC_pct when we only control for the macro variables and issue- or

issuer-characteristics. Thus, it appears that the insignificance of post on RTC_pct in Table V is

caused by potential multicollinearity.

[Table V about here.]

4.3 DID Analysis: the Impact of Information Asymmetry to Bond Liquidity

The results above show that overall, there is a reduction of liquidity cost in trading after a

144A bond becomes public registered. However, these findings on the changes in trading liquidity

18 56% of the observations are from private firms and therefore will have missing values for issuer-specific

characteristics. To preserve observations, private issuer characteristics are set to zero. Results are qualitatively the

same otherwise.

19

around the public registration may be attributable to factors other than changes in information

environment regarding the 144A issuer’s financial conditions. We take comfort in that 144A public

registrations are not associated with capital structure and funding changes, because new public

bonds offered to tender the existing 144A bonds are identical to the tendered bonds except the

restricted securities legend. Even so, other factors, such as market conditions, trading information

transparency regulated by FINRA TRACE reporting requirement, may change around the

registrations and in turn affect bond liquidity.

To pin down the impact of financial information disclosure to liquidity cost, we use a

difference-in-differences (DID) approach to identify the liquidity change caused by enhanced

financial information disclosure. We conduct three sets of DID analysis in this section. In our first

two DID tests, we contrast the change in trading liquidity of bonds that more likely experience

changes in information environment with that of other control bonds. The premise is that if the

information disclosure matters for trading liquidity, then the public registration effects should be

stronger among issuers with greater information risk pre-registration. Our hypothesis is that the

RTC measure of bid-ask spread decreases more for firms with high information asymmetry pre-

public registrations. The findings would suggest that increased corporate information associated

with public registration improve the market liquidity of OTC securities.

First, focusing on the 144A bonds experiencing public registrations, we contrast those

issued by firms with public securities with those by private firms. Because public firms disclose

regularly their financial conditions, public registrations of their 144A bonds may have relatively

less information content, comparedto 144A registrations of private firms. Second, we use an issue-

specific proxy for the extent of possible changes in information risk. Specifically, we use word

count or file size of bond prospectus as alternative proxy for ex-ante information asymmetry

associated with public registration. The information obfuscation theory postulated by Bloomfield

(2002) states that issuers tend to hide adverse information through lengthy filings. Recent studies

on 10-K filings and debt and equity IPO prospectuses generally support this notion (e.g., Li 2008,

You and Zhang 2009, Loughran and McDonald 2013, and Ertugrul et al. 2015). Third, we construct

a matched sample of public (non-144A) bonds as our control group. For each 144A bond

experiencing public registration, we find a public bond with same industry, credit rating,

callability, remaining bond maturity, and bond issue size. We then compare the changes in their

trading liquidity around the registration event.Our third DID analysis employs a matched sample

20

approach to check if our identified changes is due to contemporaneous market changes rather than

the bond registration itself.

4.3.1 DID Results on Information Asymmetry: Public vs. Private Firms

Our focus is on the information asymmetry effects of the registration. As previously

discussed, we first differentiate bonds issued by public and private firms. Public firms, via their

SEC-mandated information disclosures, have less degree of information asymmetry to investors

relative to private firms. A large fraction of US 144A bonds are issued by private firms. Earlier we

showed that intersecting FISD with TRACE leaves us with 11,443 US 144A bond issues from

3,528 issuers (Table I); a further intersecting with Compustat reduces the universe to 3,835 issues

from 1,573 issuers. In other words, only about 35% of 144As are issued by public firms. In our

registration sample of 2,487 matched bond pairs, we find that only 55% are issued by public firms.

To examine whether information asymmetry is a channel for the effect of registration on

liquidity, we focus on the interaction term of post times one of our information asymmetry

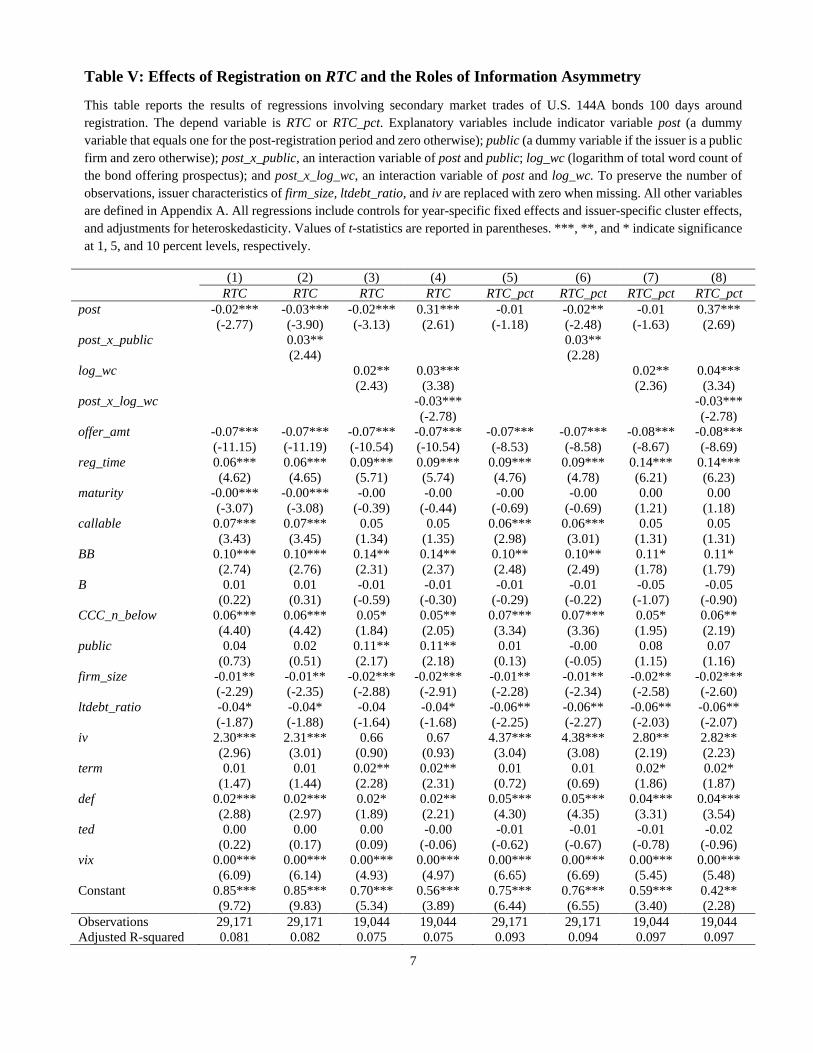

measures. Models (2) and (6) of Table V present the results using public, our public firm dummy,

as the information asymmetry measure. We note that the interaction term, post_x_public, loads

positively on liquidity measures of RTC and RTC_pct. Recall our earlier results that bond

registration per se leads to reduction in RTC. Models (2) and (6) of Table V indicate that the

reduction in RTC through bond registration is weaker (stronger) in public (private) issuers. The

overall reduction in the bid-ask spread in the event of registration of RTC is moderated by public-

issuer—in fact, the net reduction of RTC via post for public-issuers, which equals the sum of

coefficients of post and post_x_public, is close to zero or slightly positive, suggesting that the

reduction in RTC takes place mostly in private issuers. We note similar results for RTC_pct. Hence,

Models (2) and (6) of Table V provide evidence for the role of information asymmetry via private

firm as a channel for the effect of 144A registration on liquidity.

4.3.2 DID results on Information Asymmetry: Bond Prospectuses

In the previous section, the measure public captures the issuer-level of information

asymmetry but not the granular issue level. The challenge of the latter lies in the fact that about

half of the bonds are issued by private issuers. One way to get information about the issuer and

issue by the private issuer is through bond prospectus. A growing literature examines how firms

21

disclose the information in their financial reports such as 10-Ks and prospectuses such as IPO

prospectuses. Li (2008) finds that 10-K reports are harder to read when earnings are lower; and

You and Zhang (2009) find that more complex 10-Ks have a delayed investor reaction to 10-K

filings over the 12 months following the filing date. Recently, Ertugrul et al. (2015) investigate the

impact of a firm’s 10-K readability and ambiguous tone on its borrowing costs of bank loans, and

find that firms with larger 10-K file sizes and a higher proportion of uncertain and weak modal

words in 10-Ks have stricter loan contract terms and greater future stock price crash risk. In the

equity IPO setting, Loughran and McDonald (2013) examine the tone of initial IPO prospectus

and find the uncertain language makes it more difficult for investors to precisely assimilate the

value-relevant information. The literature generally suggests that disclosure documents that are

longer or contain more uncertain words are more difficult to read and interpret. The inherent idea

is “information obfuscation,” where it is postulated that issuers tend to hide adverse information

through lengthy filings (Bloomfield, 2002).

Consistent with the above literature, we use the following three dimensions of prospectus

to measure ex-ante information asymmetry of a public issue: the logarithm of the total number of

word count of the prospectus (log_wc), the logarithm of the total number of “uncertainty” word

count of the prospectus (log_wc_unc), and the logarithm of file size (log_fsize). 19 Based on the

extant literature, larger values of these measures indicate higher degree of information asymmetry.

It should be noted that these prospectus metrics serve as information asymmetry gauge for firms

that are already in the disclosure category. They allow us to differentiate, in an ex ante sense, the

level of information asymmetry among the issuers. As discussed earlier, we downloaded 1,150

bond prospectuses for bonds that we can calculate RTC, and calculate these prospectus measures.

Models (3)-(4) and (7)-(8) of Table V present the information asymmetry results using

log_wc. We first verify in Models (3) and (7) that log_wc is positively related to RTC and RTC_pct;

that is, higher information asymmetry, as proxied by larger values of log_wc, induces larger bond

bid-ask spreads. For our focus of interaction variable between post and log_wc, we note that it

loads negatively on liquidity measures of RTC and RTC_pct. These results are consistent with

those with public, in that they both indicate that bid-ask spread decreases more for high-

information asymmetry issues. The coefficient estimates of the post and log_wc interaction term

19 The “uncertainty” word list is from Loughran and McDonald (2011). File size is in kilobytes. In measuring the file

size, all prospectuses are converted to text file.

22

(post_x_log_wc) is about the same as those of log_wc, indicating that the information asymmetry

effect of registration is about the same as the main information asymmetry effect itself. Thus, the

evidence suggests that the channel of information asymmetry is an important consideration in the

reduction of bid-ask spread in Rule 144A bond registrations.

4.3.3 DID Results Using a Matched-Sample Approach

Our results above refer to the same bond undergoing a registration event. However, these

results may be due to contemporaneous market changes rather than the bond registration itself. To

further identify that our results are indeed from the registration event, we construct a control

sample of non-event bond trades (trades from bonds that do not have a registration event) and

compare these to event bond trades. We call the sample used in the previous section the treatment

sample—it contains bond trades for all of registered bonds pre- and post-registration. We construct

the match sample based on the following procedure. First, we select only trades of non-144A-

transformed public bonds, and further restrict that the bond trades have a vintage life of at least

one year (trade date at least one year after the bond issuance date).20 Out of this sample, we then

we select a control bond-month for each treatment bond-month based on the following criteria: (i)

the control issue and the treatment issue must have at least one bond transaction during the same

month; (ii) they must have the same average rounded credit rating using the ratings from the three

rating agencies during the month; (iii) they must be matched on callability; (iv) the issuers of the

control and treatment issues must be from the same industry group (either industrial, finance, or

utility); and (iv) the control issue should be the most similar, in terms of bond maturity at

transaction time and offer amount, to the treatment issue, based on an aggregated decile rank for

each of these dimensions. We pick only the non-duplicate control bond-month. In summary, we

form a control sample that is matched on transaction month, current credit rating, callability,

industry, remaining bond maturity, and bond issue size.

Following the above procedure, we identify the control issue-month for each treatment

issue-month, where “treatment” refers to the 144A-registration sample used earlier. We then

aggregate variables of both treatment and control issues at the monthly level and evaluate the

20 The second condition ensures that even if, in the not-too-likely scenario, the public bond that we chose may be from

a Rule 144A exchange-issue that we failed to identify, the trade time has well passed the registration date, and the

effect of its registration should be sufficiently small.

23

differences of variables before and after the registration of the treatment issue. We employ a

standard difference-in-difference approach: the first level of difference is the value of the variable

of the treatment issue-month minus the value of the variable of the control issue-month, and the

second level of difference is the difference of the first level differences before and after the

registration event.

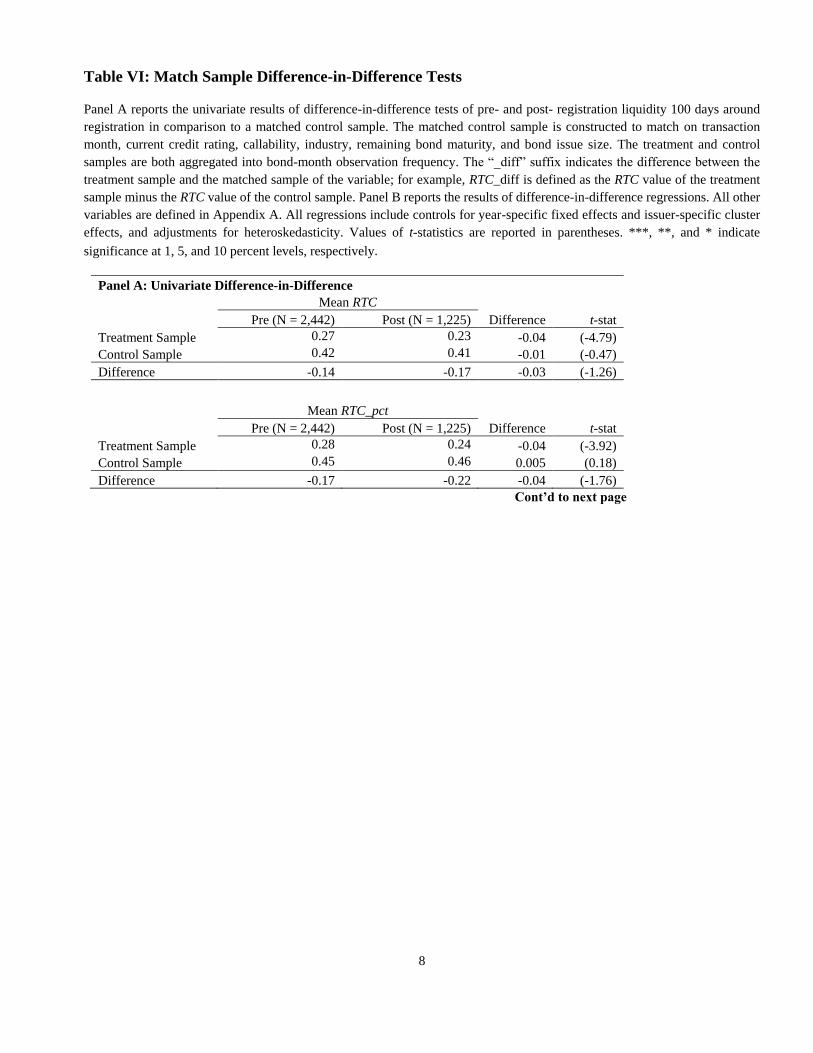

Panel A of Table VI reports the univariate statistics of liquidity differences for our baseline

sample. Prior to registration, we observe that RTC and RTC_pct differences tend to be negative,

indicating that Rule 144A issues have higher bid-ask spread than the match public bonds. These

results are consistent with the extant literature (e.g., Fenn 2000, Huang et al. 2017). After the

registration, the differences of the above variables all become smaller; RTC (RTC_pct) difference

decreases from -0.14 (-0.17) before registration to -0.17 (-0.22) after registration. Thus, compared

to a control group, registration leads to reduction in RTC. These results corroborate the patterns

that we identified in Table V.

[Table VI about here.]

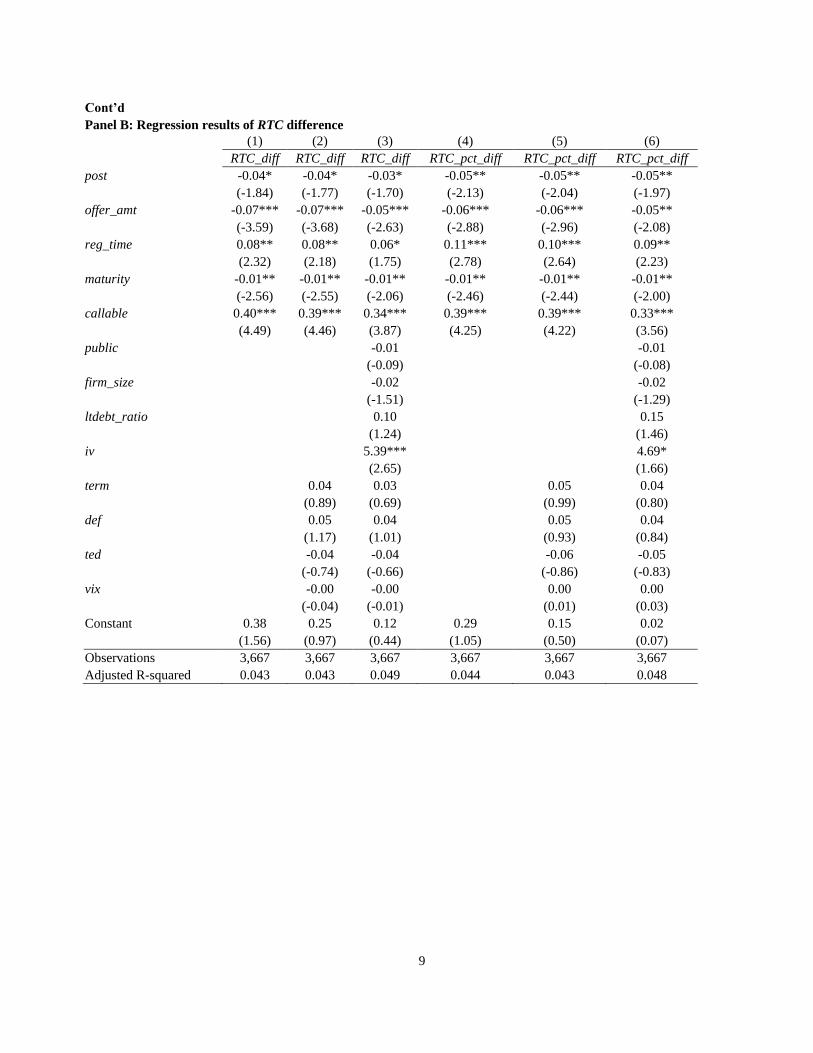

Panel B of Table VI further reports the difference-in-difference regression results. We

regress the first-level difference of the variable of interest on the registration event variable post.

Consistent with Table V, we observe that post significantly and negatively loads on both RTC and

RTC_pct. Hence, the univariate results in Panel A are corroborated with multivariate controls of

issue- and issuer-traits and macro variables. In sum, Table VI further confirms the information

disclosure impact on liquidity in private debt registrations.

5 Robustness Checks and Discussion

5.1 Robustness Checks

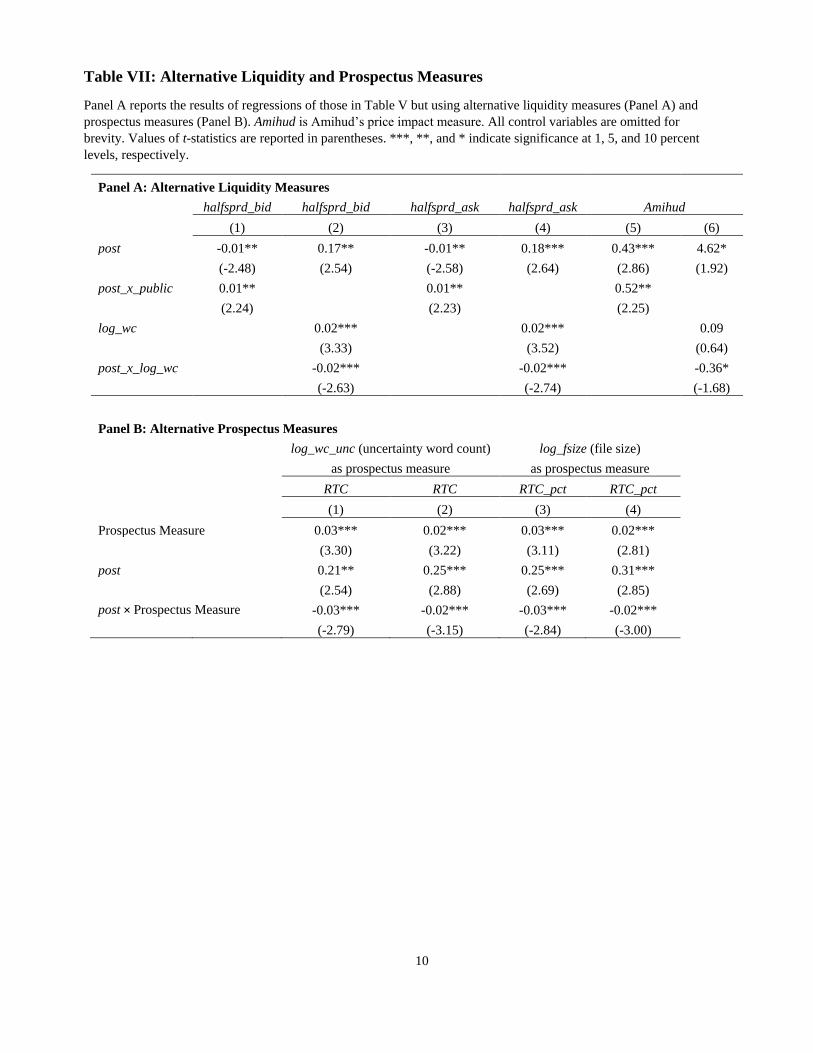

We carry out a number of robustness checks. First, Panel A of Table VII uses the alternative

illiquidity measures of half spreads. The half spread measures break bid-ask spread into the bid

and ask sides. We define halfsprd_bid (halfsprd_ask) as the difference between the mean bond

prices from trades where customers sell (buy) the bond to (from) dealers and the mean bond prices

from interdealer trades, normalized by the mean price in interdealer trades. This measure does not

require transaction mapping to the same dealers or same trading volume, and is therefore less

restrictive. We also construct an Amihud’s (2002) price impact measure that is defined in our

24

context as the percentage change in bond price between two consecutive trades divided by the

dollar trading volume of the first transaction. The results show that for these alternative illiquidity

measures, the interaction term post_x_public remains significantly positive, while post_x_log_wc

remains significantly negative.21

[Table VII about here.]

Panel B of Table VII uses alternative prospectus measures of uncertainty word count and

file size in the regressions of RTC and RTC_pct. Again, we find that both measures load positively,

their interaction terms with post load negatively, and the coefficient estimates on the interaction

terms are about the same magnitude as those of the counterpart prospectus measures. These results

are highly consistent with those of log_wc, and confirm the information asymmetry effect on

liquidity during 144A registration.

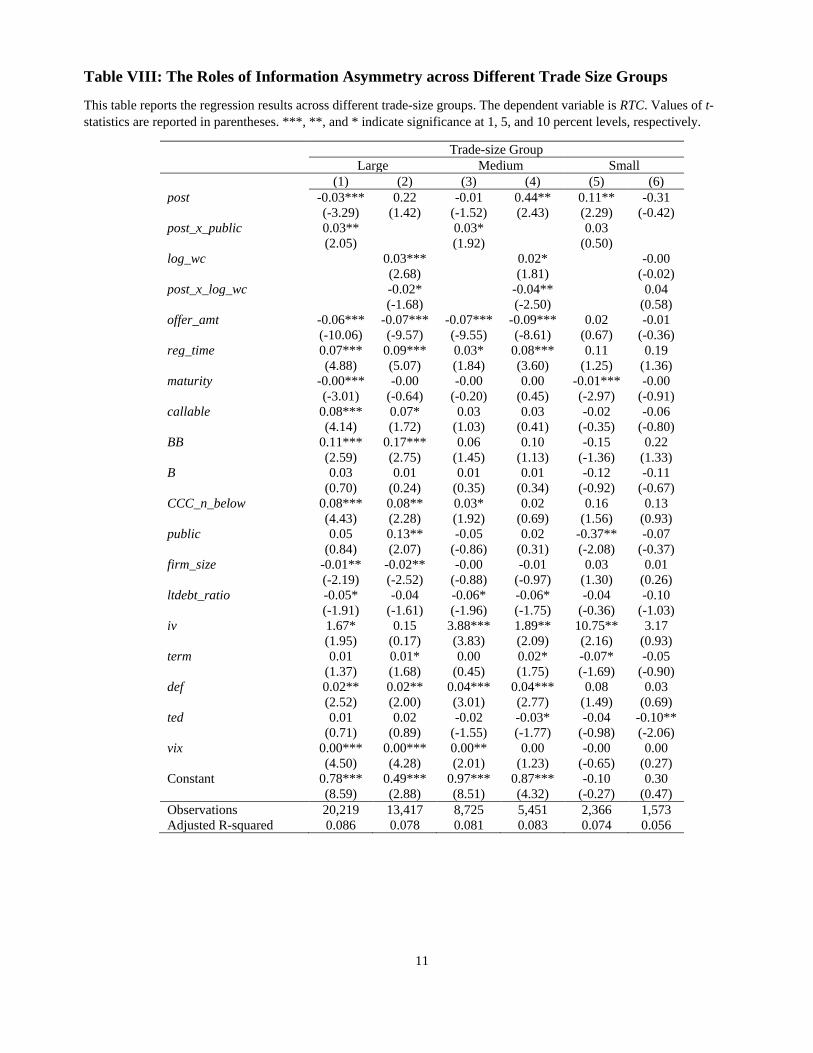

Table VIII presents the results with different trade-size groups. We find that post_x_public

remains significantly positive for large and medium trade-size groups, but becomes insignificant

for small trade-size group. Similarly, post_x_log_wc remains significantly negative for large and

medium trade-size groups, but becomes insignificant for small trade-size group. These results echo

the patterns of RTC reduction in Table IV, where we found that the reduction in RTC cluster in

large and medium trade-size groups, which nonetheless account for 90% of all trades.

[Table VIII about here.]

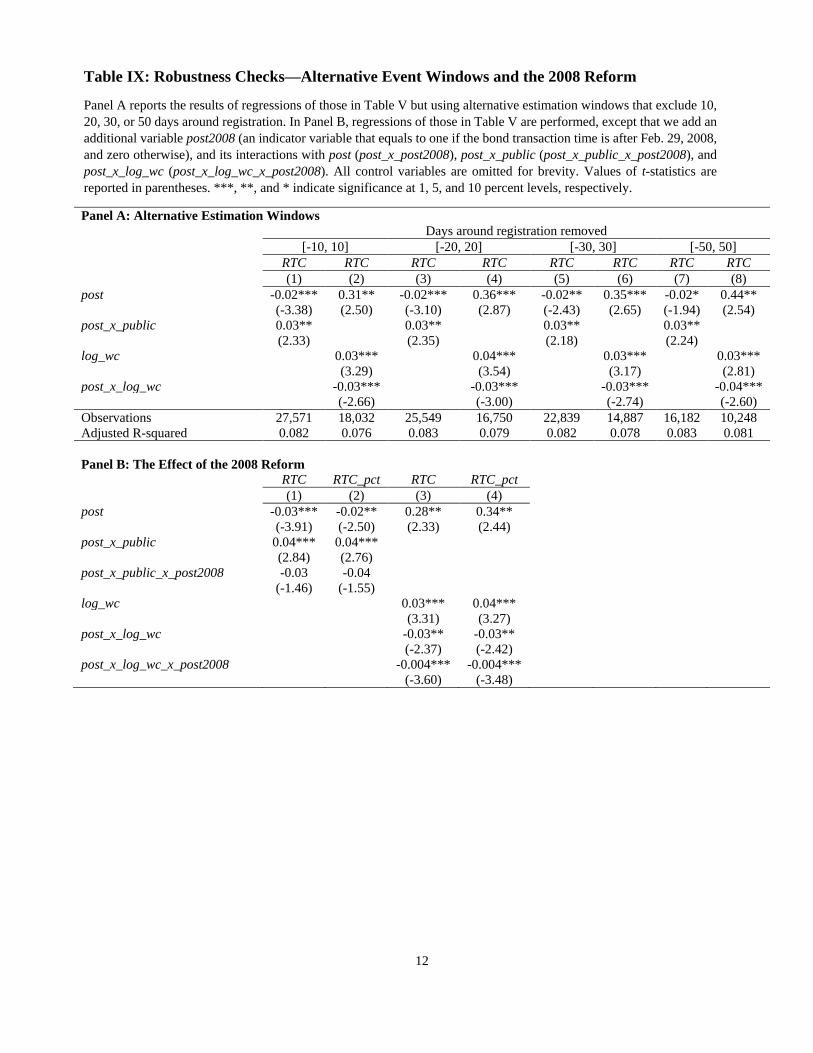

Panel A of Table IX further uses alternative event windows. As suggested in Table IV, we

find trades closely around registration are scant. For example, using 10 days around registration

we are only able to identify 42 Rule 144A-registered bond pairs for our entire sample period;

widening this estimation window to 100 days increases the number of bond pairs to 1,734, or 40

times of more bonds. In untabulated results, we find that trading frequency ramps up to exhibit a

hump shape with the peak at around 50 days after registration. Since there is no “real” issuance of

a new bond, it is plausible that it takes time for public investors to become aware of the exchanged,

registered bond. To test whether the information asymmetry effect is robust to this ramping-up of

trade, we exclude the ramping-up period by using alternative estimation windows that exclude 10,

21 The sign of post on the Amihud price impact measure (Amihud) is significantly positive, which would inadvertently

indicate that liquidity deteriorates per se post registration. We, however, find that this is driven by the dominator of

trade size in Amihud -post registration, the decrease in trade size (documented earlier in Table IV) leads to higher

values of Amihud. Hence, size-related liquidity measures such as Amihud should be interpreted with caution in our

context.

25

20, 30, or 50 days around registration. Panel A of Table IX again confirms that both post_x_public

and post_x_log_wc retain the same significance for these alternative estimation windows.

[Table IX about here.]

Panel B of Table IX presents the results of a potential structural break in 2008. Prior to

2008, non-affiliate (affiliate) QIBs can freely trade 144As after a two- (one-) year holding period

when the bond issuers meet certain public-information disclosure requirement. After 2008, the

SEC halved the holding period to one year, and all the disclosure requirements are removed. We

use a dummy variable for the adoption of the new reform time of Feb. 29, 2008, and interact the

dummy variable with post_x_public and post_x_log_wc, respectively, to form a triple interaction

variable. Panel B shows that the significance of post_x_public and post_x_log_wc on RTC and

RTC_pct remain intact. The triple interaction term of post_x_public and post-2008 dummy is

insignificant; and while the triple interaction term of post_x_log_wc and post-2008 dummy is

significantly negative, as expected, the magnitude of its coefficient estimate is just about one

tenth of that of post_x_log_wc itself. Overall, the results suggest that the 2008 reform has no or

only weak effect to the information asymmetry impact on liquidity in private debt registrations.

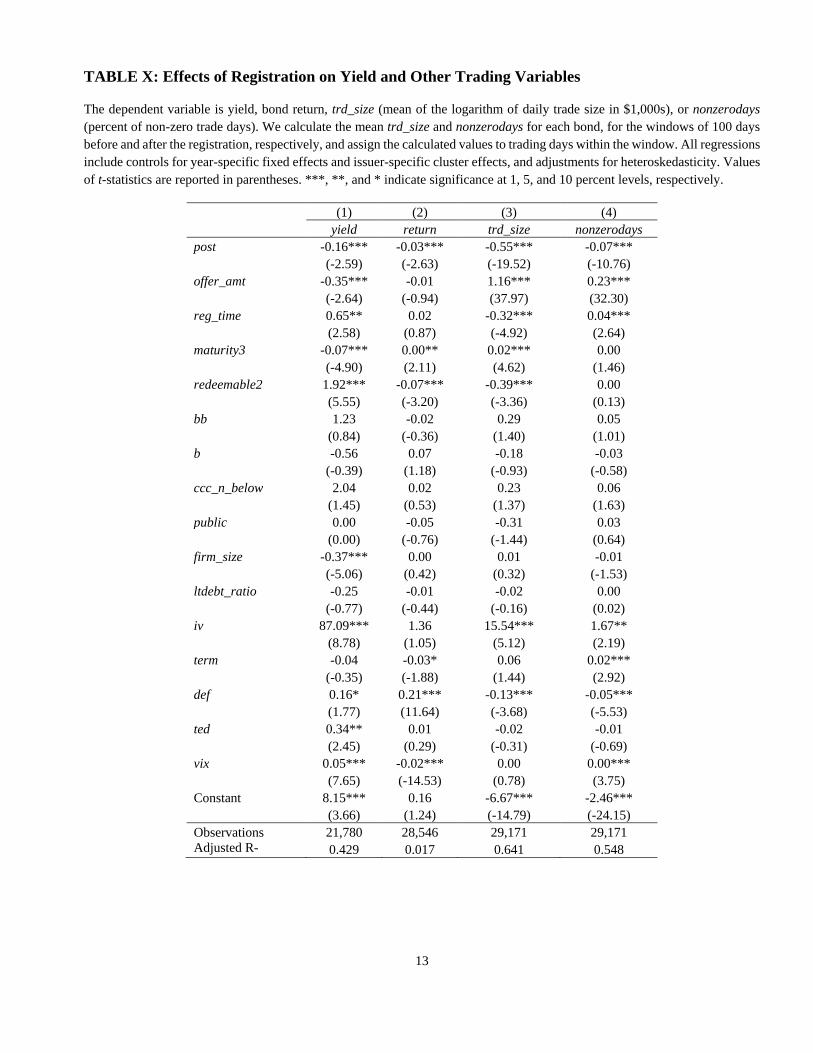

5.2 The Effect of Registration on Yield and Bond Returns

We finally examine the pricing effect of registration. We use two proxies for bond pricing:

the bond yield-to-maturity reported by TRACE, and bond returns. Following the literature (e.g.,

Bessembinder, Kahle Maxwell and Xu 2009), we define bond returns as the daily average price

minus the previous daily average price, divided by the previous daily average price times 100; this

ratio is further divided by the number of calendar days between for the two price dates. The bond

return variable thus measures daily returns. The first two columns of Table X presents the

regression results of yield and returns regressed on post for the event windows 100 days, after

controlling for issue- and issuer-specific variables and macro variables. We’ve shown in previous

sections that registration leads to lower bid-ask spread and degree of information asymmetry, and

we hence expect yield and returns to decrease posted registration. As expected, Table X

unequivocally shows that post is significantly negatively related to both yield and returns. The

relation is economically significant too. For example, the registration of 144A debt reduces the

yield by 16 bps, or reduces daily returns by 3 bps. In untabulated results, we can report that the

reduction of yield increases notably as we shorten the estimation window. For example, the

26

reduction increases to 124 bps if we use 20-day estimation window. Also not tabulated, we find

that the yield results also hold for the difference-in-difference sample. Overall, these results

indicate that registration does achieve the desired effect of lowering the price paid by investors.

[Table X about here.]

5.3 Further Discussion: Trading Frequency and Size

Earlier we documented that there is a decrease in trade size post registration. This is

plausibly due to the change of investor base post-registration. Pre-registration traders of 144As

consist of largely QIBs (for short-vintage 144As the only traders are QIBs), which are relatively

large institutional investors. In contrast, post registration the investor base is expanded to include

all public investors. Retail and non-QIB investors likely trade in smaller amounts and less

frequently than do QIBs. While our RTC measures of liquidity only consider the round trip trades

between dealers and customers, retail and non-QIB investors likely account for a much larger part

of customers in the post- versus pre- registration.

The remaining columns in Table X shows the effect of registration in regards to trading

size and trading frequency. We consider two such measures of each bond for the period of 100

days before and after registration: the logarithm of average daily dollar trade size (in $1,000s), and

the percentage of non-zero trading days. We restrict the sample, as before, to one that we can

calculate RTC to main sample consistency, and calculate one value of each measure for the bond

pre- and post-registration, respectively. Table X shows that both measures experience a drop after

registration, consistent with the conjecture that the introduction of retail and non-QIB customers

post registration results in smaller and less frequent trades. These results are consistent with

Goldstein, Hotchkiss and Sirri (2007), who find that enhanced transparency is not associated with

greater trading volume.

6. Summary and Conclusions

Rule 144A debt represents a significant and growing segment of the total U.S. debt market,

and a large portion of 144A debt issues carry registration rights and hence are subsequently publicly

registered. Though 144A debt issuance market has grown substantially over time, little is however

known about the post-registration effects of that market. In this paper, we examine the post-

registration effects of private Rule 144A debt and shed light on how public registration affects the

27

underlying liquidity.

We use broker-dealer’s round-trip-cost (RTC) to measure the underlying liquidity of the

144A bond market. We find that the registration of Rule 144A bonds leads to decreasing trading

costs. Specifically, our results show that on average registration reduces RTC by about 12 percent

of its pre-registration level in 100 days around the registration. Registration lowers bid-ask spread

or equivalently, improves liquidity and lowers transaction costs of trades.

We examine the robustness of our results using a number of difference-in-difference

approaches, by contrasting registered bonds between public and private firms, and between high

and low ex-ante information asymmetry issues as embodied in bond offering prospectuses, and also

by a matched sample of purely public bonds. We find that the registration-related RTC reduction

is larger for issues with higher ex-ante information asymmetry. In addition, the reduction of RTC

is accompanied by reductions in bond yield and returns. Overall our findings suggest

information transparency on corporate financial conditions contributes to better market liquidity of

corporate bonds in the OTC markets.

28

REFERENCES

Adrian, Tobias, Michael Fleming, Or Shachar, and Vogt, Erik, (2015). Has U.S. Corporate Bond Market

Liquidity Deteriorated? Introduction to a Series on Market Liquidity: Part2, FRBNY Blog paper.

Anand, Amber, Paul Irvine, Andy Puckett, and Kumar Venkataraman, (2013). "Institutional Trading and

Stock Resiliency: Evidence from the 2007-2009 Financial Crisis." Journal of Financial

Economics, 108 (3): 773-97.

Anderson, Mike, and René M. Stulz, (2017). Is post-crisis bond liquidity lower? Fisher College of Business

Working Paper Series.

Ang, Andrew, Assaf A. Shtauber and Paul C. Tetlock, (2013). "Asset Pricing in the Dark: The Cross-Section

of OTC Stocks." Review of Financial Studies, 26 (12): 2985-3028.

Arena, Matteo P. and John S. Howe, (2009). "Takeover Exposure, Agency, and the Choice between Private

and Public Debt," Journal of Financial Research, 32(2): 1475-6803.

Barry, C., Mann, S., Mihov, V., Rodríguez, M., (2008). "Corporate debt issuance and the historical level of

interest rates". Financial Management 37, 413–430.

Bao, Jack, Maureen O’Hara, and Alex Zhou,(2016). The Volcker Rule and Market-Making in Times of Stress,

Federel Reserve Board Working paper.

Bessembinder, Hendrik, William Maxwell, and Kumar Venkataraman (2006). "Market Transparency,

Liquidity Externalities, and Institutional Trading Costs in Corporate Bonds." Journal of Financial

Economics, 82 (2): 251-88.

Bolton, Patrick, Tano Santos, and Jose A. Scheinkman, (2012). "Shadow Finance," Working paper, Princeton

University.

Bulsiewicz, James G., (2015). "Institutional Industrial Trades and the Cross-section of Returns." Working

Paper.

Bushee, Brian, and Christian Leuz,(2005). Economic Consequences of SEC Disclosure Regulation: Evidence

from the OTC Bulletin Board, Journal of Accounting and Economics, 39: 233 - 264.

Brüggemann, Ulf, Aditya Kaul, Christian Leuz, Ingrid M. Werner (2013). The Twilight Zone:

OTC Regulatory Regimes and Market Qquality, NBER working paper.

Cai, Fang, Song Han, and Dan Li, (2012). "Institutional herding in the corporate bond market." Working Paper.

Cai, Nianyun, Jean Helwege, Arthur Warga,(2007). "Underpricing in the Corporate Bond Market". Review of

Financial Studies; 20 (6): 2021-2046

Chaplinsky, S., and Ramchand, L. (2004). "The Impact of SEC Rule 144A on Corporate Debt Issuance by

International Firms." Journal of Business, 77, 1073-1098.

Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam (2011). "Recent Trends in Trading Activity and

Market Quality." Journal of Financial Economics, 101 (2): 243-63.

29

Craig, Karen Ann (2012). "Liquidity in the 144A Debt Market." Trace: Tennessee Research and Creative

Exchange.

Das, Sanjiv, Madhu Kalimipalli, and Subhankar Nayak (2014). "Did CDS trading improve the market for

corporate bonds?" Journal of Financial Economics, 111 (2): 495-525.

Datta, S., M. Iskandar-Datta, and A. Patel. (1997). The Pricing of Initial Public Offers of Corporate Straight

Debt. Journal of Finance 52:379–96.

Datta, S., Iskandar-Datta, M. and Patel, A.,(1999). The Market's Pricing of Debt IPOs. Journal of Applied

Corporate Finance, 12: 86–91