Embed Size (px)

Citation preview

1

INFORMATIONAL EFFICIENCY OF

FUTURES MARKET IN INDIA

A thesis submitted to Pondicherry University in partial fulfillment of the

requirement for the award of the degree of

DOCTOR OF PHILOSOPHY

IN

COMMERCE

By

BABU JOSE

Under the Guidance of

Dr. D. LAZAR

Associate Professor

DEPARTMENT OF COMMERCE

SCHOOL OF MANAGEMENT

PONDICHERRY UNIVERSITY

PONDICHERRY-605 014

NOVEMBER-2011

2

MEMBERS OF DOCTORAL COMMITTEE

DR.K.CHANDRASEKHARA RAO

Professor & Head

Department of Banking Technology

Pondicherry University

DR. P.DHANAVANTHAN

Professor & Head

Department of Statistics

Pondicherry University

3

Dr. D. Lazar

Associate Professor

Department of Commerce

School of Management

Pondicherry University

Pondicherry-605 014

Certificate

This is to certify that the PhD thesis entitled “INFORMATIONAL EFFICIENCY

OF FUTURES MARKET IN INDIA” submitted to Pondicherry University for the

award of the degree of Doctor of Philosophy in Commerce by Babu Jose is the

bonafide research work carried out by him independently under my guidance and

supervision in the Department of Commerce. I also certify that this has not been

previously submitted for the award of any degree or associateship to any other

University or Institution.

Dr. D. Lazar

Associate Professor

Countersigned

Dean Head

School of Management Department of Commerce

Place:

Date:

4

BABU JOSE

Research Scholar- PhD (Full Time)

Department of Commerce

School of Management

Pondicherry University

Pondicherry-605 014

Declaration

I, Babu Jose hereby declare that the thesis entitled, “Informational Efficiency of

Futures Market in India” submitted to Pondicherry University, Pondicherry for the

award of the Degree of Doctor of Philosophy in Commerce is my original work and

it has not been previously submitted either in part or whole to this or any other

University for the award of any degree.

Babu Jose

Place:

Date:

5

to Him.................

who always

strengthen me

6

Acknowledgement

I bow before the God almighty for his special blessings on me from the beginning to

the completion of this study.

I am deeply indebted to Dr. Daniel Lazar, Associate Professor, Dept. of Commerce,

Pondicherry University, my Guide and Supervisor, for his timely supervision, strict

instruction and unconditional support for the successful Completion of this study. I

admire his motivation to keep me in the right track and his selfless assistance in

bringing out this work in the best way possible. I thank him meticulously for going

through all the pages and giving timely corrections, even the minute ones which

helped me a lot to do this research in the proper manner. I admire and cherish his

availability, encouragement, competence and scholarship.

I do thank Honorable Vice Chancellor Prof. J.A.K. Tareen, Prof. M. Ramadass,

Dean SOM , Dr. Malabika Deo, Professor & Head, Dept of Commerce, Pondicherry

University for giving me the opportunity to take up this study. I express my sincere

gratitude to My Doctoral Committee Members Dr. K.C. Chandrasekhara Rao,

Professor & Head, Dept. of Banking Technology, Dr. P. Dhanavanthan, Professor

& Head, Dept. of Statistics, Pondicherry University for their encouragement, keen

interest on the work, apt guidelines and strict monitoring which helped me a lot in the

course of this research.

With sentiment of joy and gratitude I express my sincere thanks to Mr. Sunil Paul,

Research Scholar, Dept. of Economics, Pondicherry University, Mr. Lagesh,

Research Scholar, Dept. of Economics, Hyderabad University, Dr. Sony Thomas,

Faculty, IIM Kozhikode, Dr. S. Shijin, Assistant Professor, Dept. of Commerce,

Pondicherry University and Mrs. Deepthi for their concern, kindness and selfless

help for the completion of my work. . I thank Bro. Benny Thadathil M.Ss.Cc, Mr.

Shinto Thomas and Mr. Vivek who helped me in the proof reading of the thesis.

7

I would like to thank Prof. P.Palanichamy, Prof. P. Natarajan, Dr. Velmurugan, Dr.

Shanmugasundaram, Sri. S. Aravanan and Mr. K.B. Nidheesh for their personal

encouragement and help during the research period. I take this opportunity to thank

Mrs. Savithri, office manager and Mr. Ammayiappan, Office Assistants, Dept. of

Commerce, for their personal help and cooperation during the research period.

It is great pleasure for me to thank, Meghanathan, Immanuel, Yazeer, Minija, Safir

Pasha , Mahindra Panday, Dharani and all other co-research scholars in the Dept.

of Commerce and of other Depts. for their co-operation, love, encouragement and

healthy personal relationship. I also thank my dear friends and teachers, Shaji. K.P,

Manoj. M, Joshy K.P, Hari Das, Sebastian.P.M, Dr. Madhusoodhana, Jose. M.V,

Rajesh and Raveesh for their motivating support and life long relationship they

rendered to me.

I avail this opportunity to express my sincere thanks to my wife Sindhu who is always

with me and her co-operating attitude, helping mentality and level of personal

understanding which helped me lot to balance my research and personal life in a

healthy manner. It is the time to sincerely thank my family members especially

Father, Mother, Sister, Brother-in-law, and all members of Thadathil and

Pinakkattu Family, without their consistent prayer, help and support, it would not

have been possible for me to get success in my personal and academic life.

Babu Jose

8

CONTENTS

Chapter Title Page

No.

CERTIFICATE

DECLARATION

DEDICATION

ACKNOWLEDGEMENT

CONTENTS

LIST OF TABLES

LIST OF FIGURES AND GRAPHS

ABBREVIATIONS

I INTRODUCTION 18-46

1.1 Preamble............................................................................ 19

1.2 Risk Management............................................................... 20

1.3 Derivatives........................................................................ 20

1.4 Forms of Derivatives......................................................... 21

1.5 Types of Derivatives......................................................... 22

1.6 Derivatives Market in India............................................... 25

1.7 Indian Futures & Options Markets..................................... 26

1.8 Futures and Options Trading at NSE................................. 27

1.9 Factors Influencing the price of Futures............................ 33

1.10 Relationship between Spot and Futures Markets.............. 34

1.11 Role of Trade Volume and Market Depth to Explain the

Market Movement............................................................

36

1.12 Risk management through Futures.................................... 38

1.13 Volatility and Lead Lag in Futures Market....................... 40

1.14 Development of Futures Markets in India......................... 41

1.15 Informational Efficiency of Futures Markets....................

43

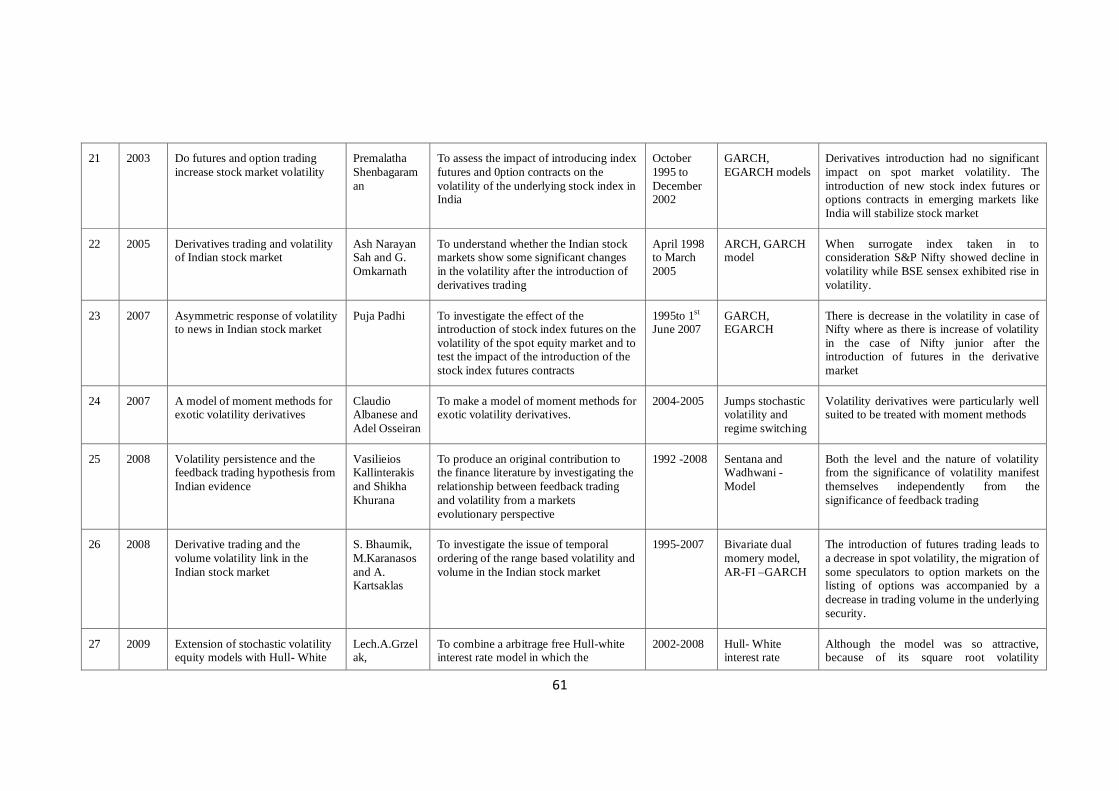

II REVIEW OF LITERATURE 47-112

2.1 Introduction....................................................................... 69

9

2.2 Reviews on Relationship between Futures and Spot

Market................................................................................

70

2.3 Reviews on determinates on Futures Market................ 88

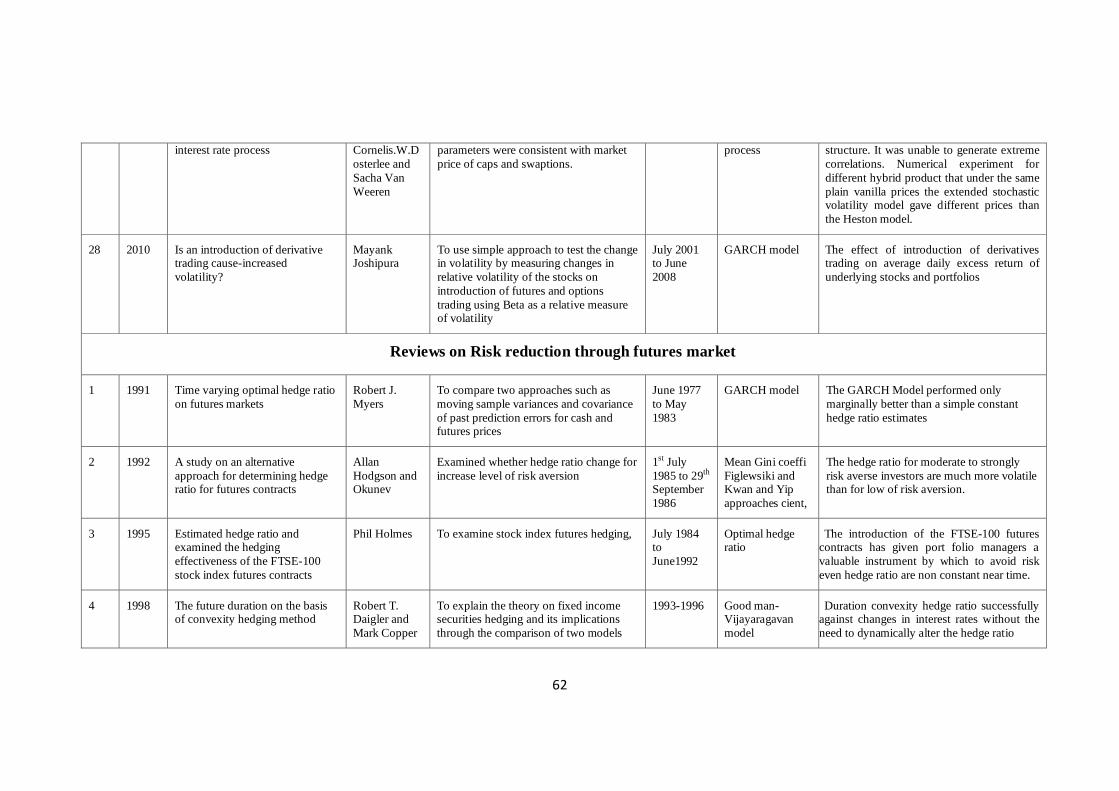

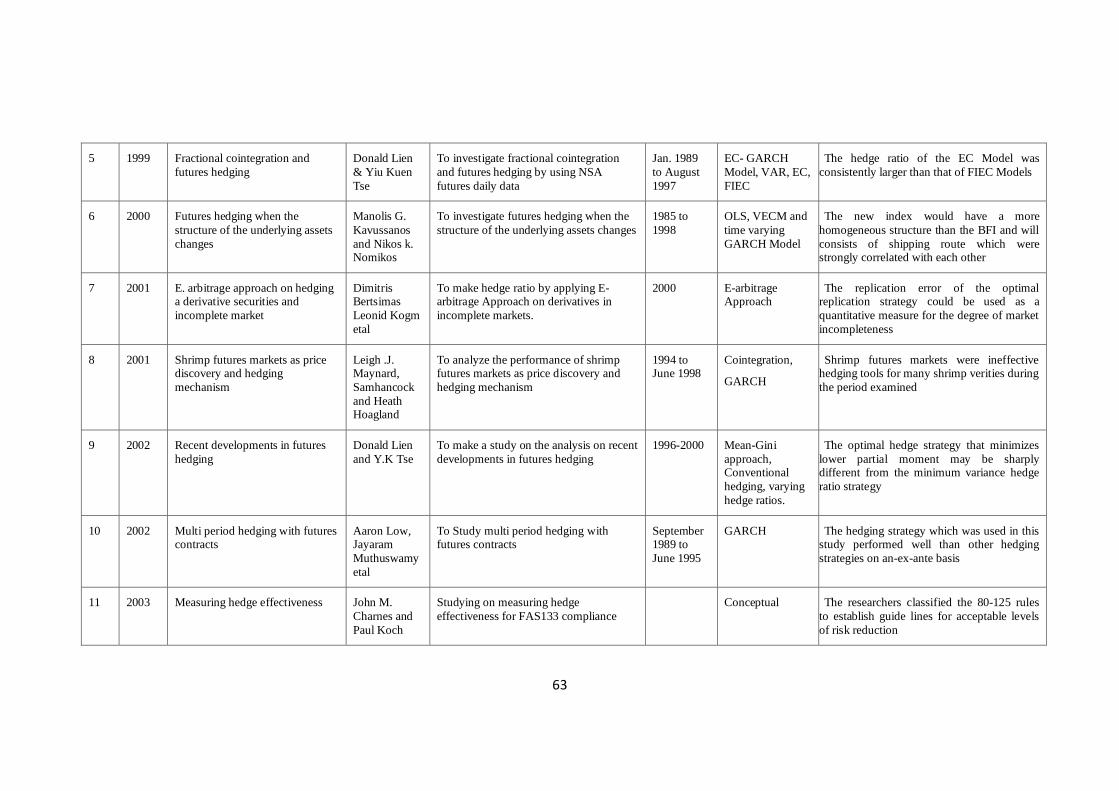

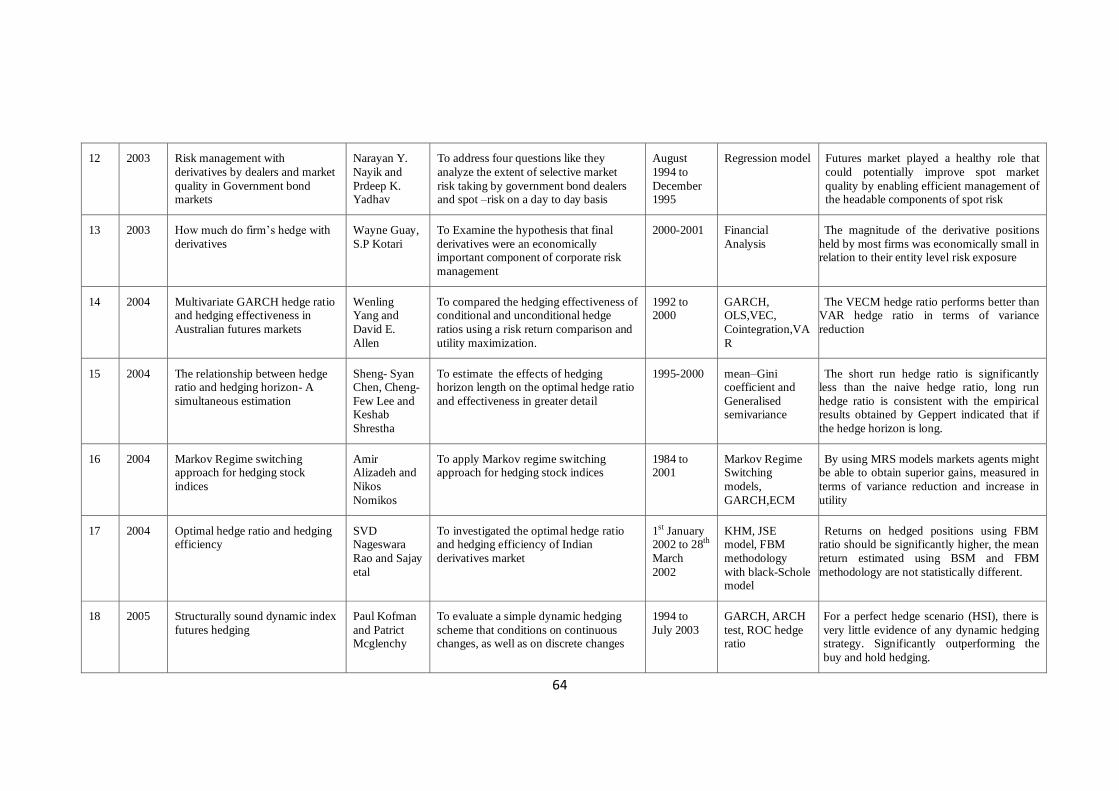

2.4 Reviews on Risk Reduction through Futures Market........ 98

2.5 Research Gap.................................................................... 112

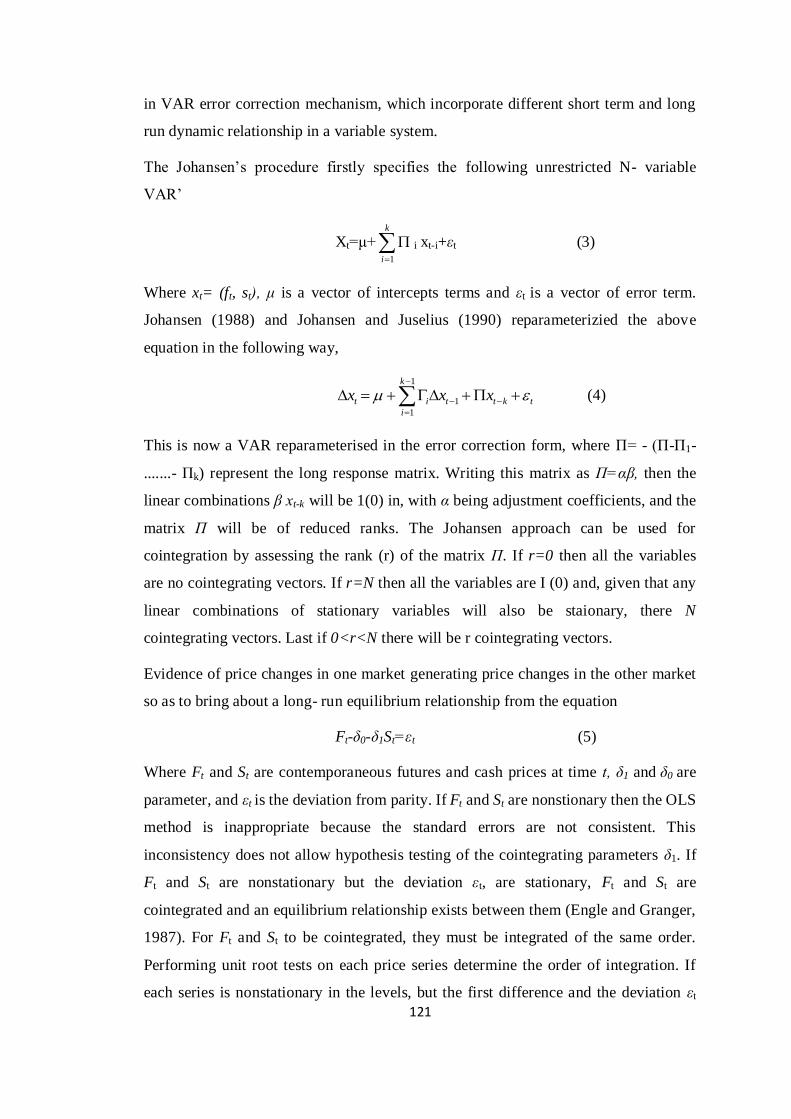

III METHODOLOGY 113-135

3.1 Introduction....................................................................... 114

3.2 Objectives of the Study...................................................... 114

3.3 Null Hypothesis of the Study............................................ 115

3.4 Significance of the Study................................................... 115

3.5 Scope of the Study............................................................. 116

3.6 Data and Methodology....................................................... 117

3.7 Period of the Study............................................................. 118

3.8 Limitations of the Study..................................................... 119

3.9 Econometrics Models used in the Study............................ 119

3.10 Reader’s Guide 135

IV DYNAMIC RELATIONSHIP BETWEEN FUTURES AND

SPOT MARKET IN INDIA

136-163

4.1 Introduction....................................................................... 137

4.2 Variables and Methodology.............................................. 140

4.3 Steps of Analysis............................................................... 141

4.4 Rationale of the Study........................................................ 141

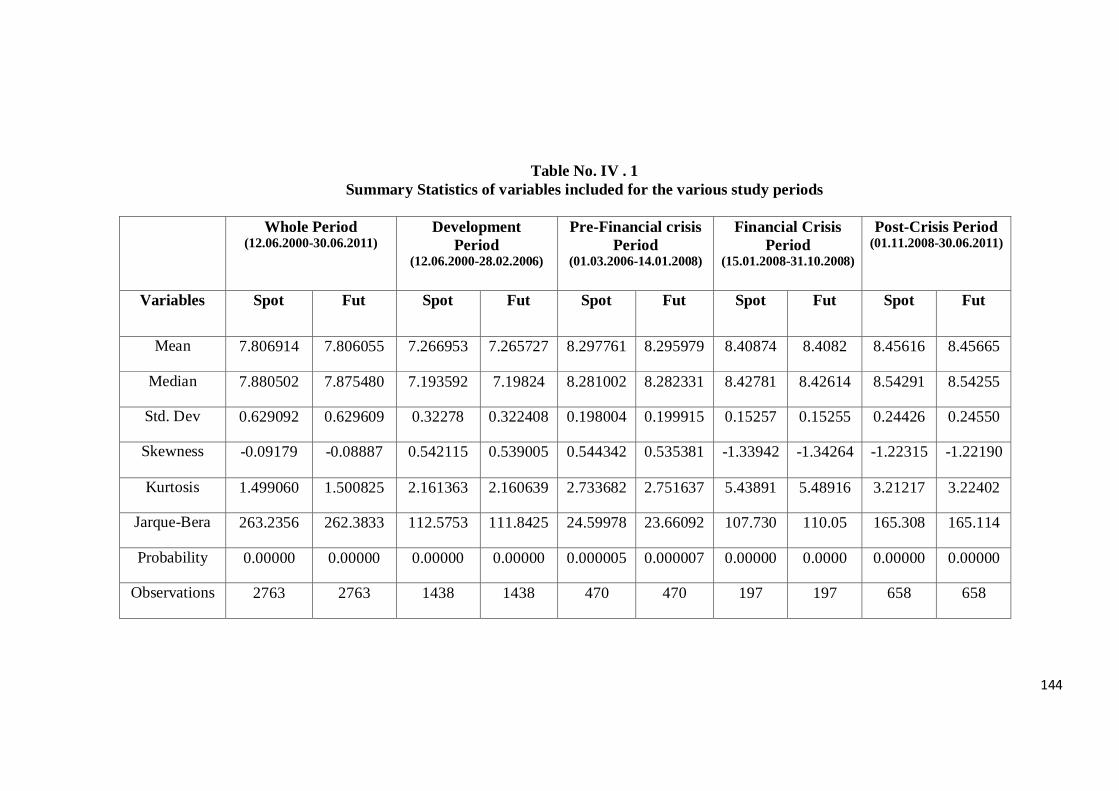

4.5 Results from Summary Statistics....................................... 142

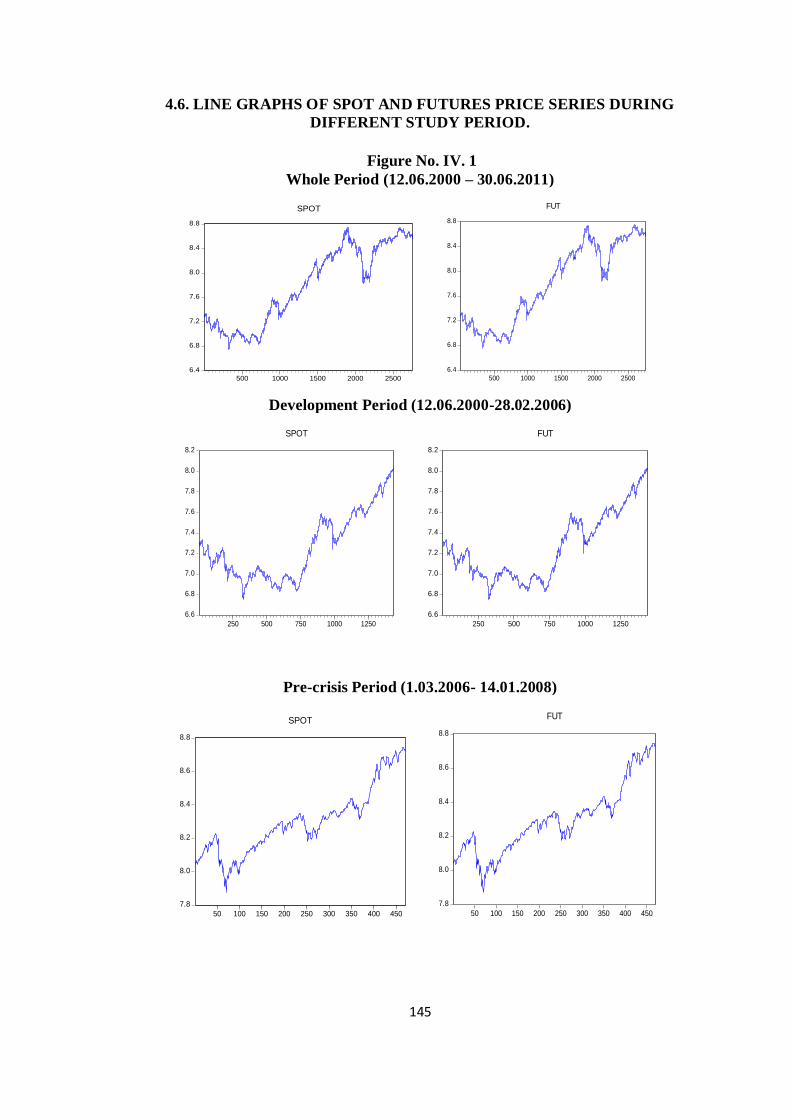

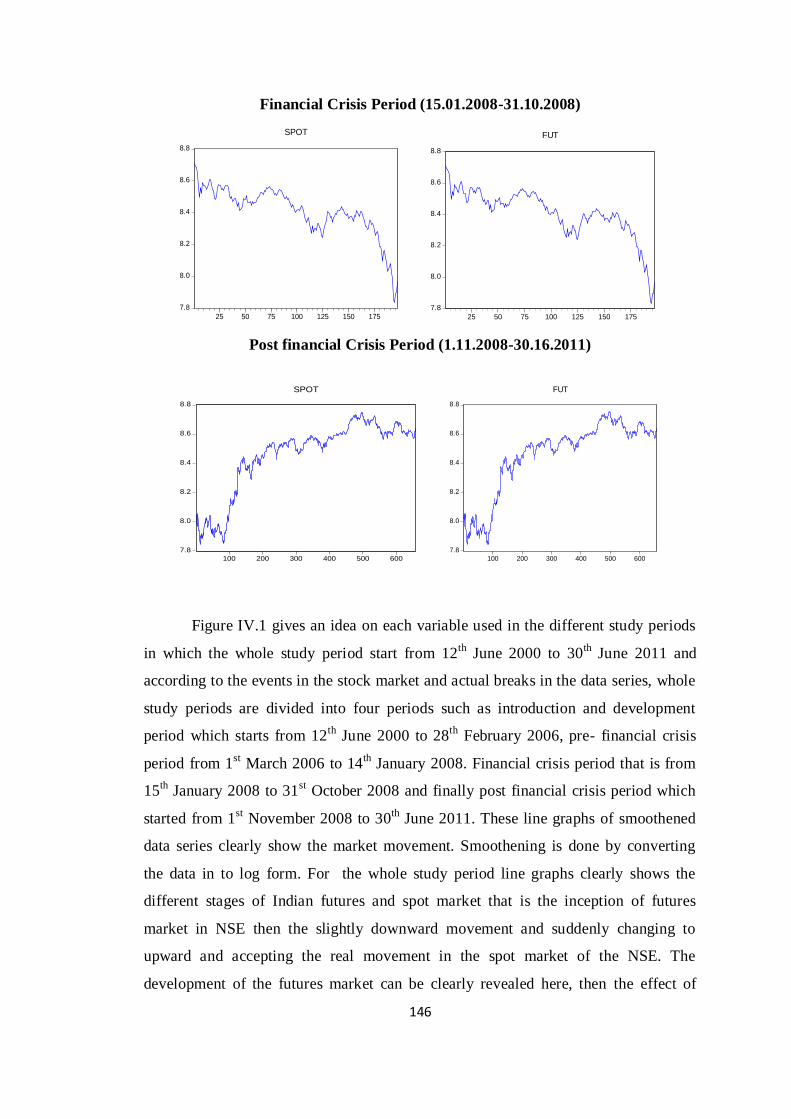

4.6 Line Graphs of Spot and Futures Price Series during

different Study Period......................................................

145

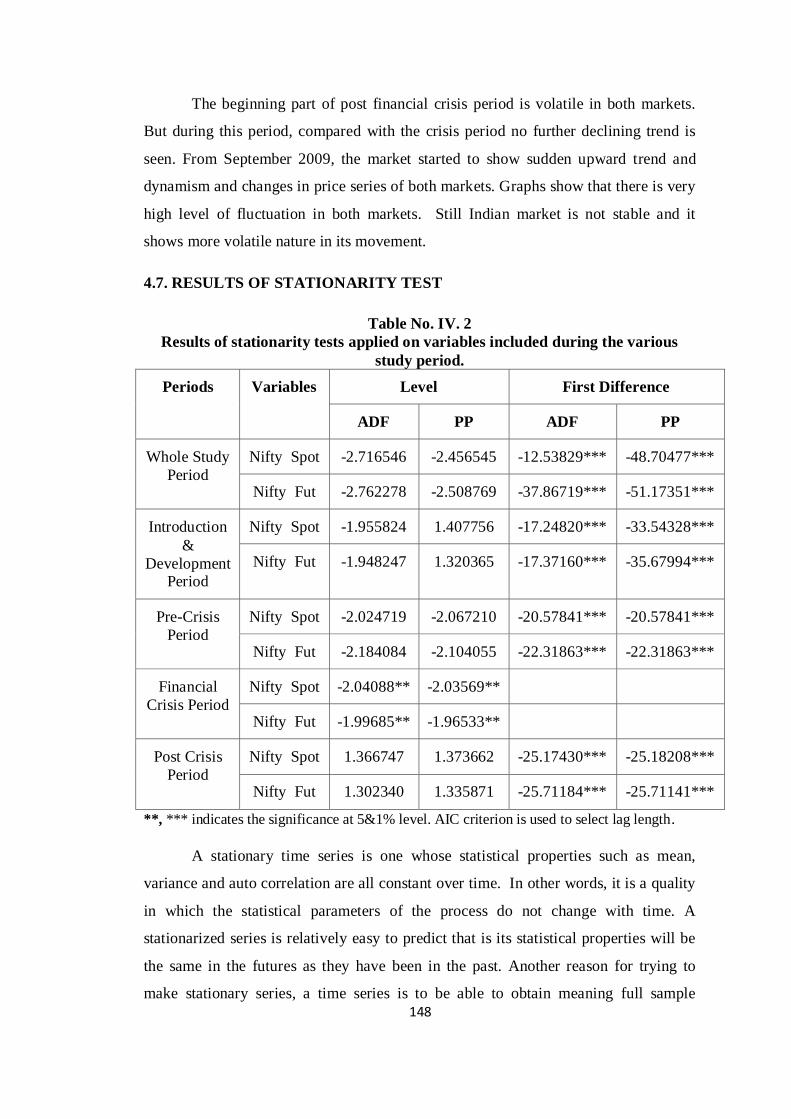

4.7 Results of Stationarity Test............................................... 148

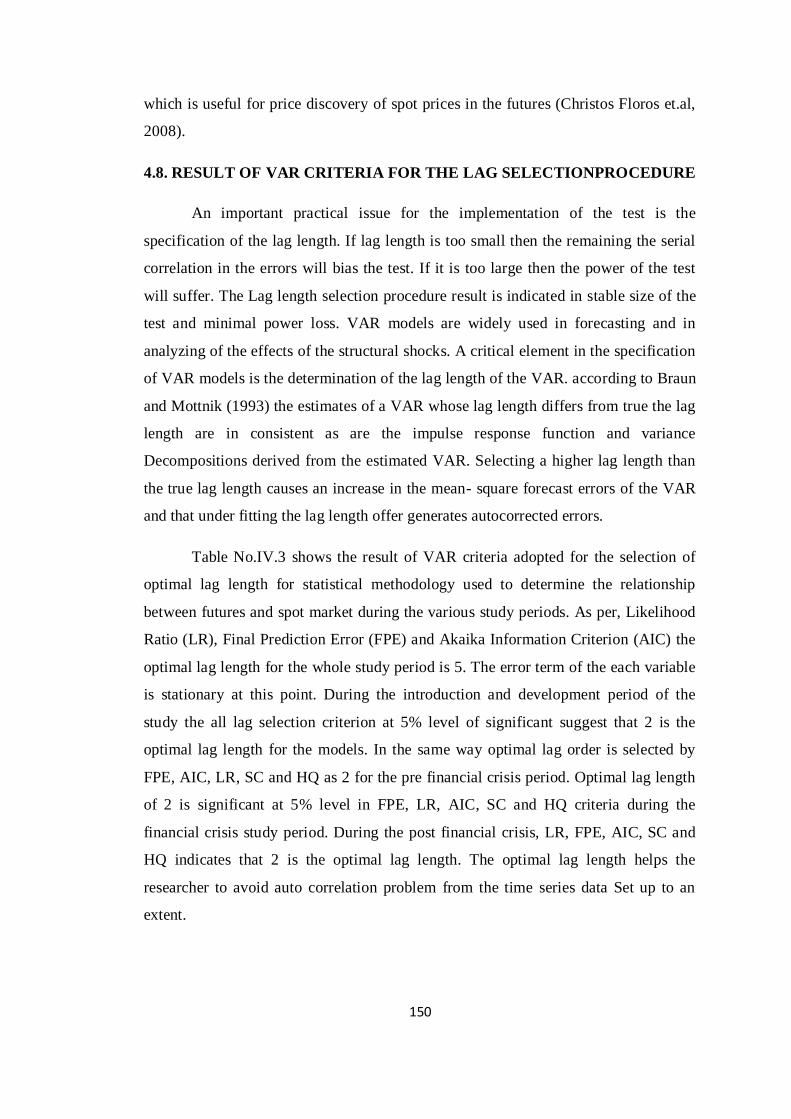

4.8 Result of VAR Criteria for the Lag Selection Procedure... 150

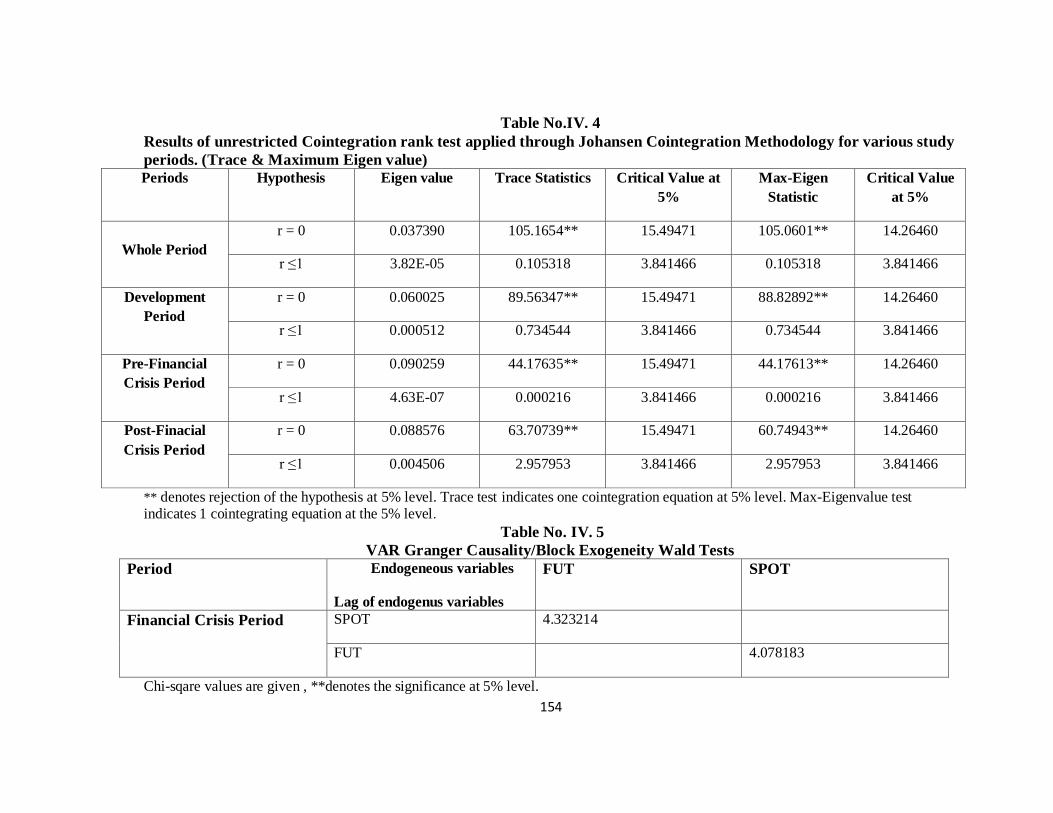

4.9 Long term Relationship between Futures and Spot

Market in India...................................................................

152

4.10 Short term Relationship between Spot and Futures

Market in India...................................................................

155

4.11 Causal Relationship between Spot and Futures Market in

India.................................................................................

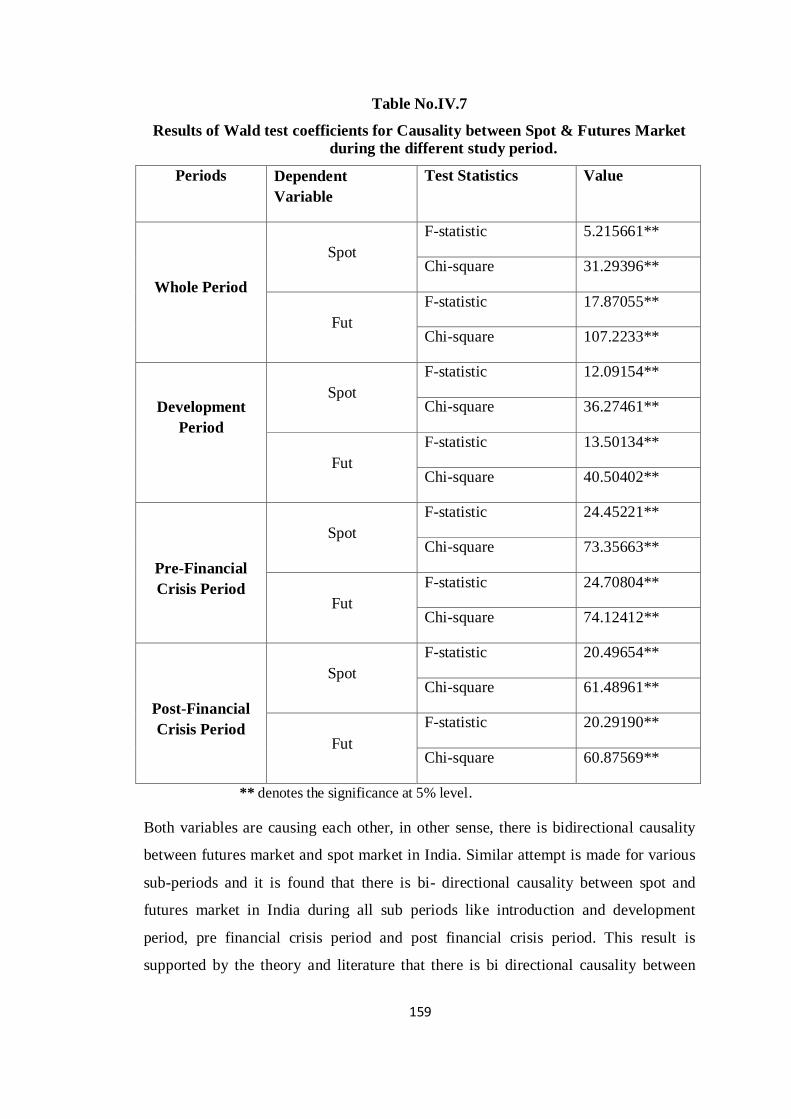

158

10

4.12 Conclusion.......................................................................

161

V DETERMINANTS OF FUTURES MARKET IN INDIAN 164-231

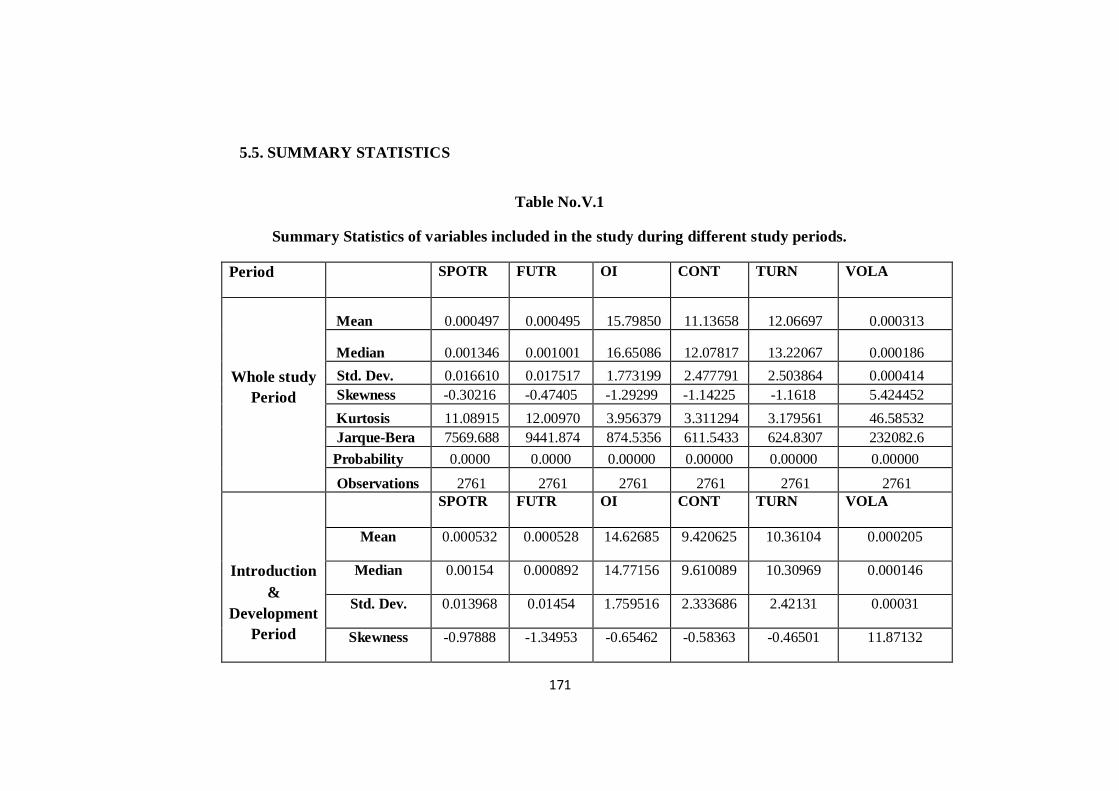

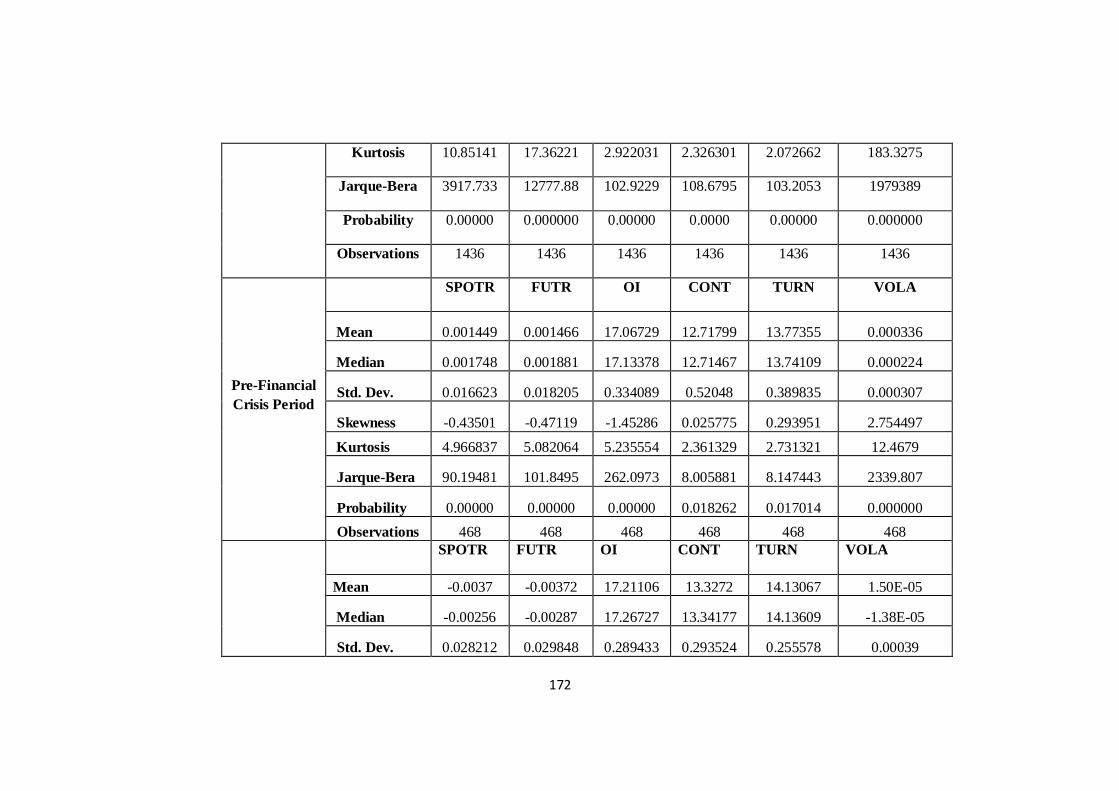

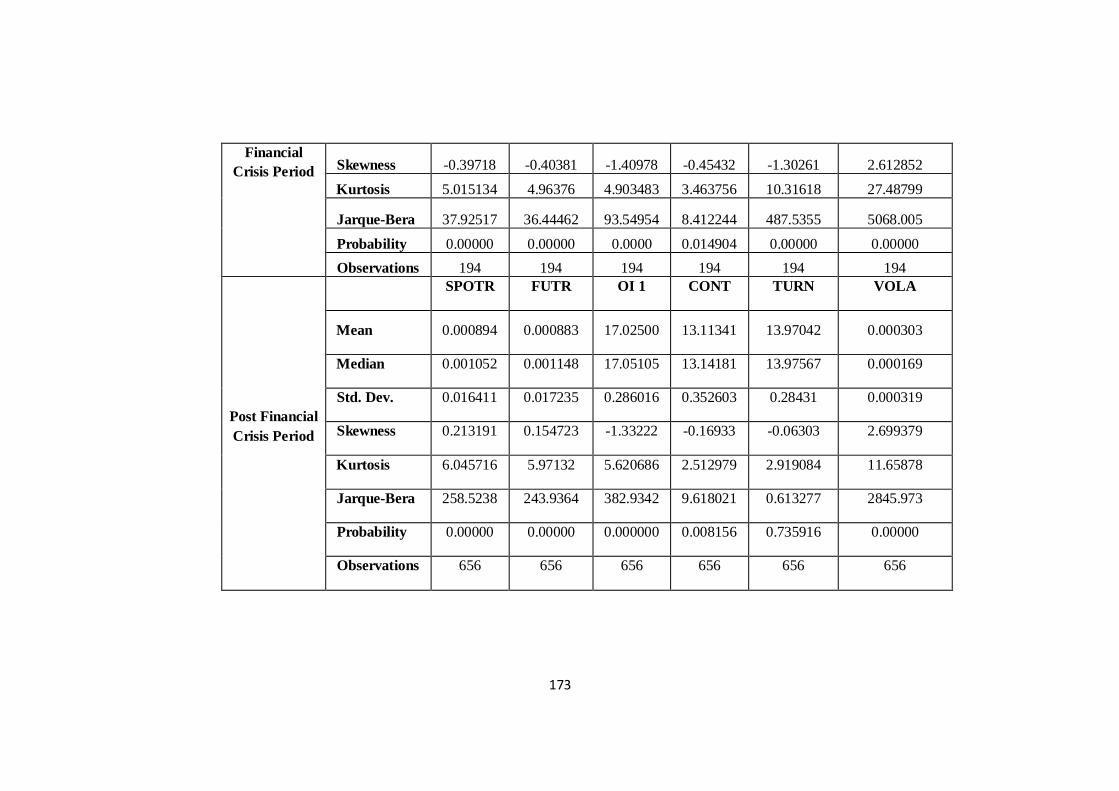

5.1 Introduction....................................................................... 165

5.2 Variables and Methodology............................................ 167

5.3 Steps for Analysis............................................................... 168

5.4 Rationale of the Study..................................................... 169

5.5 Summary Statistics......................................................... 171

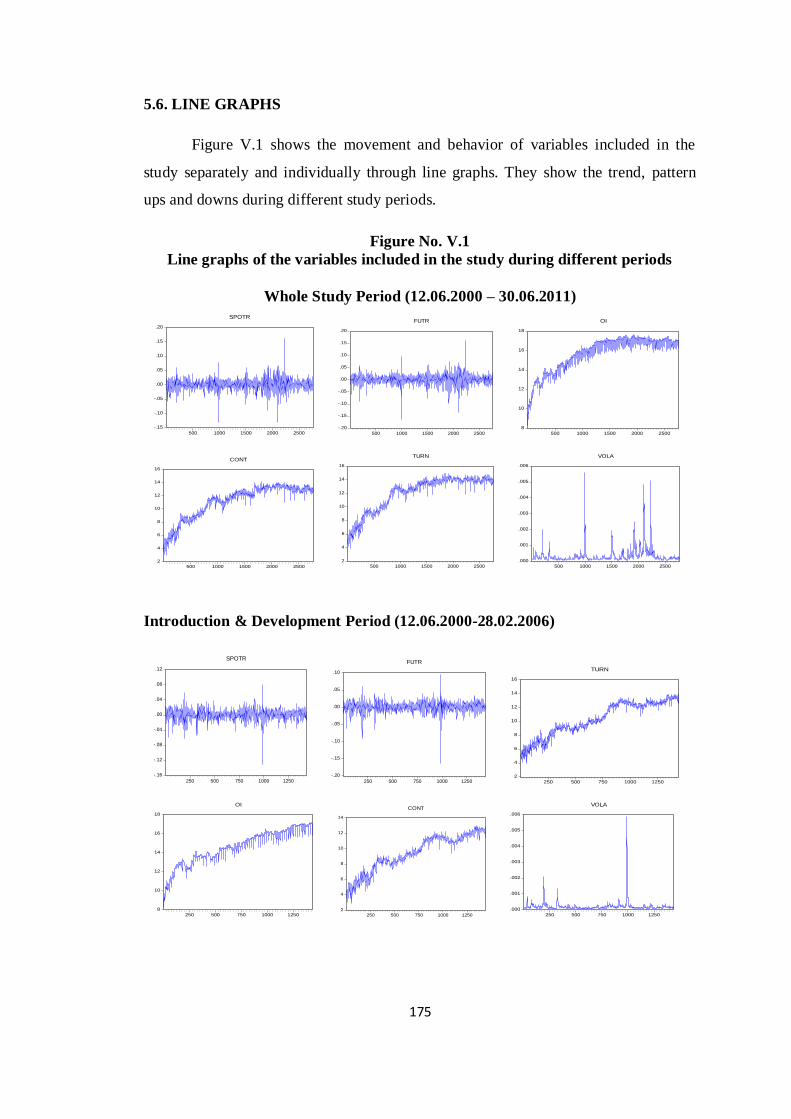

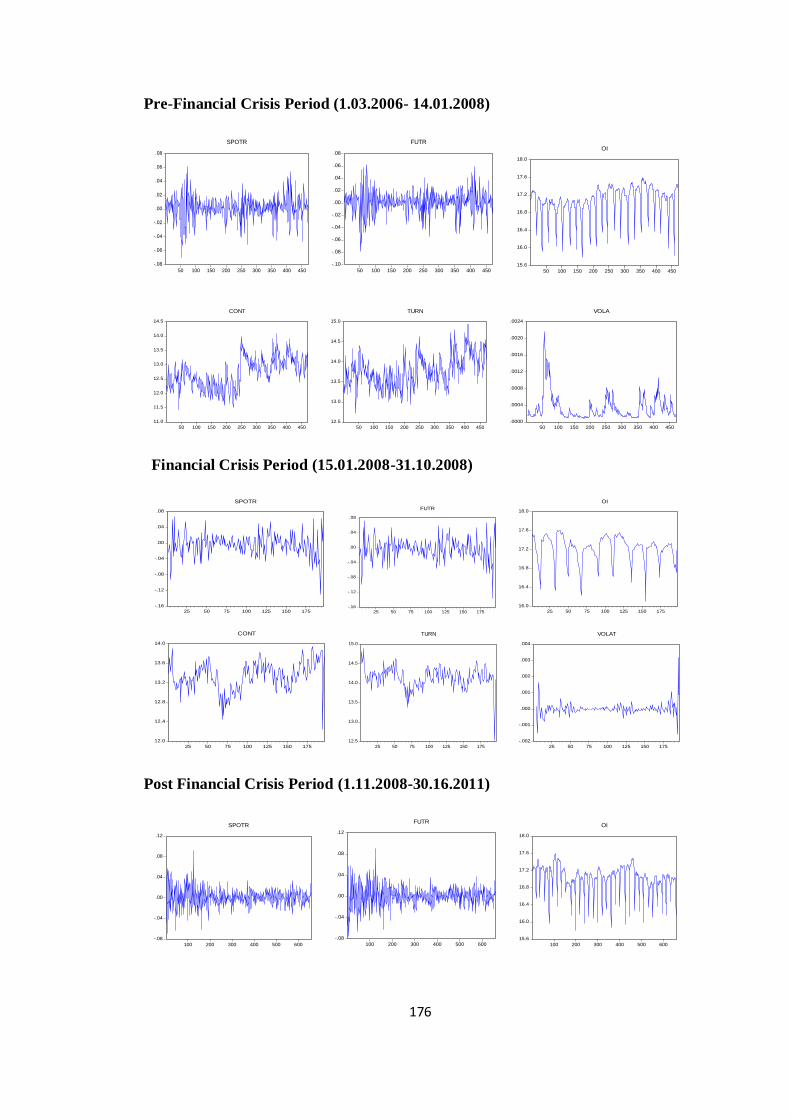

5.6 Line Graphs..................................................................... 175

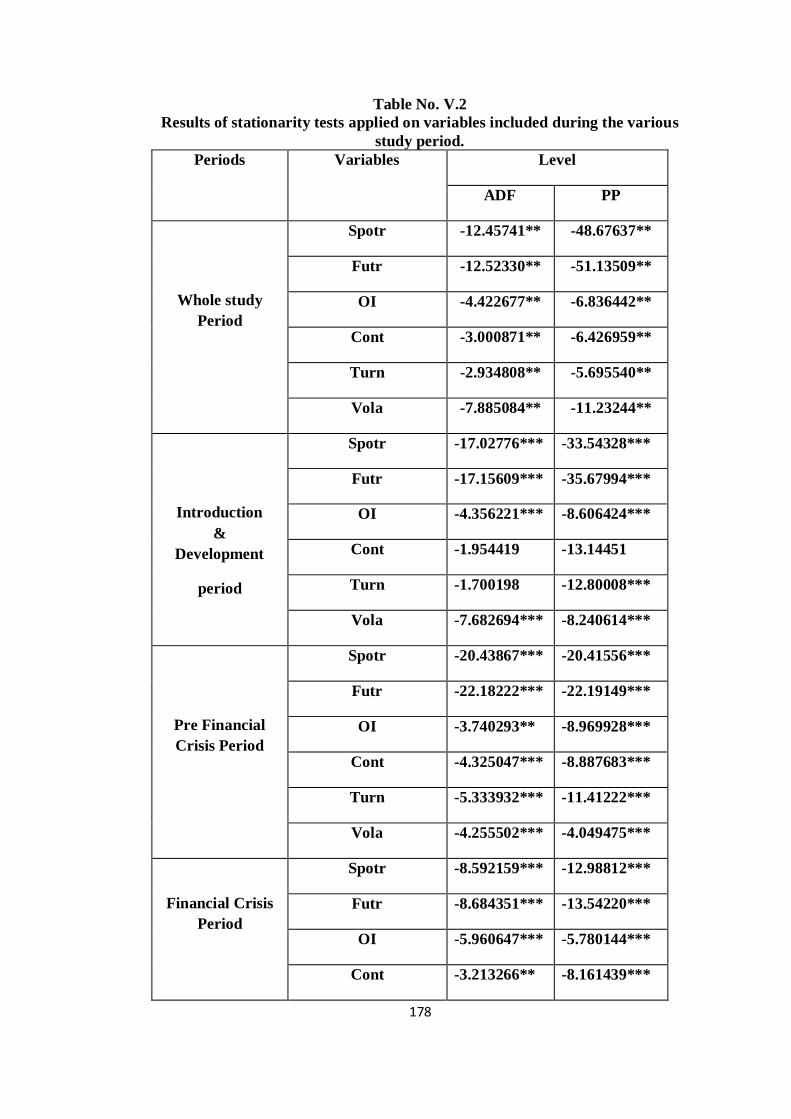

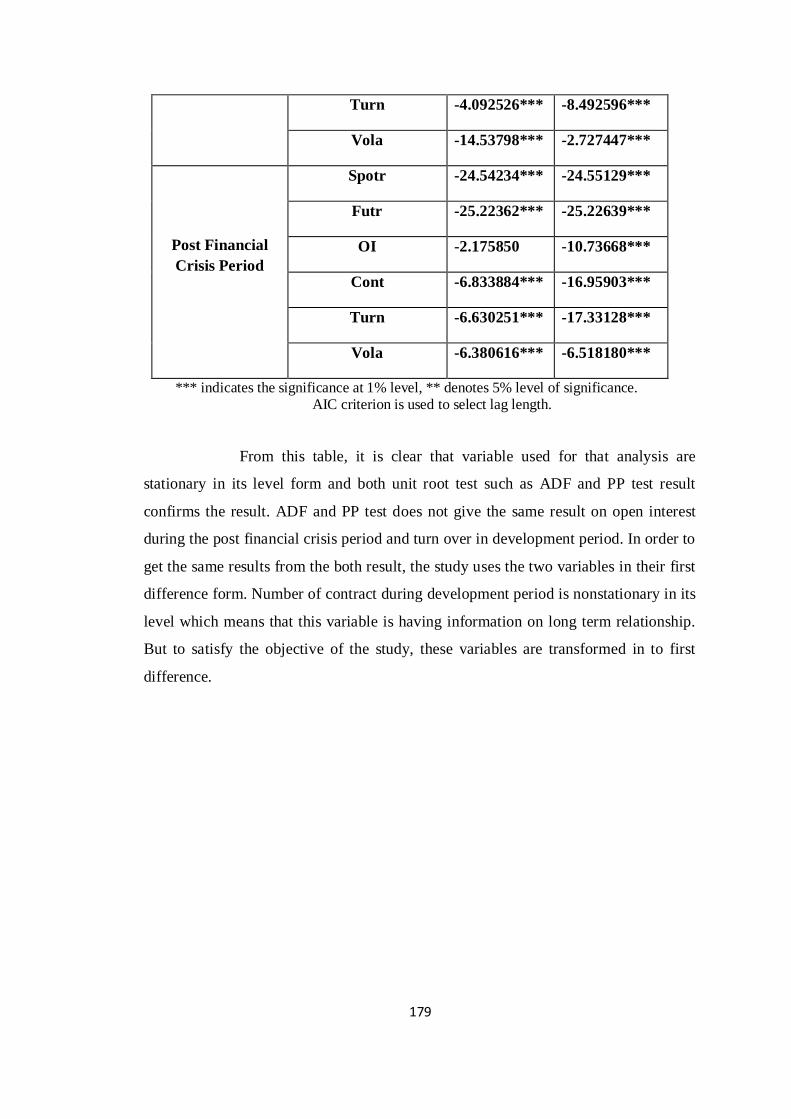

5.7 Stationarity of Variables................................................. 177

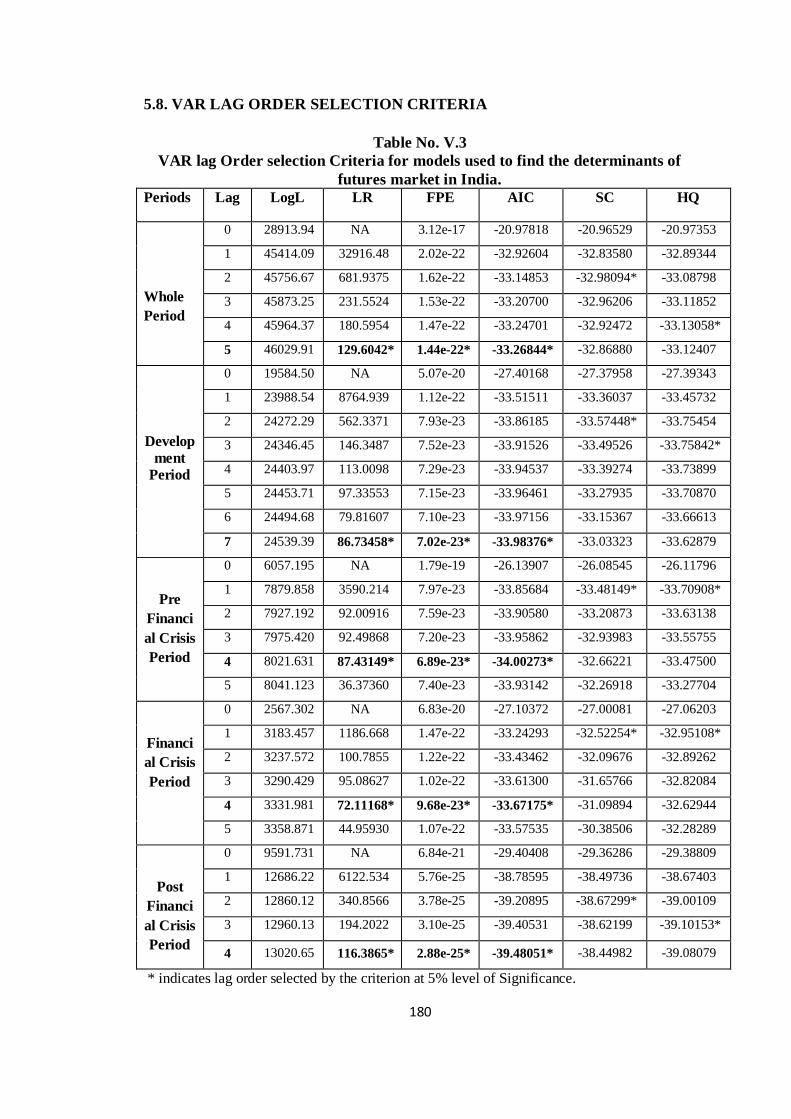

5.8 VAR Lag Order Selection Criteria................................... 180

5.9 Determinants of Futures Market in India.......................... 181

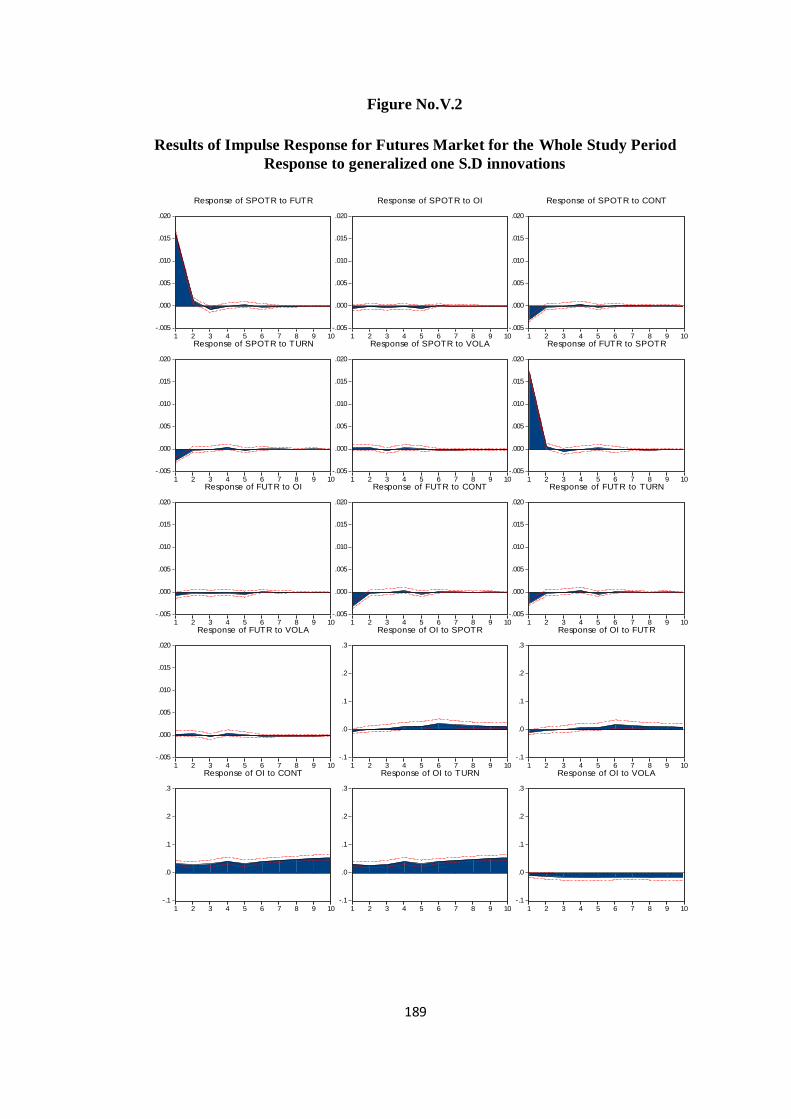

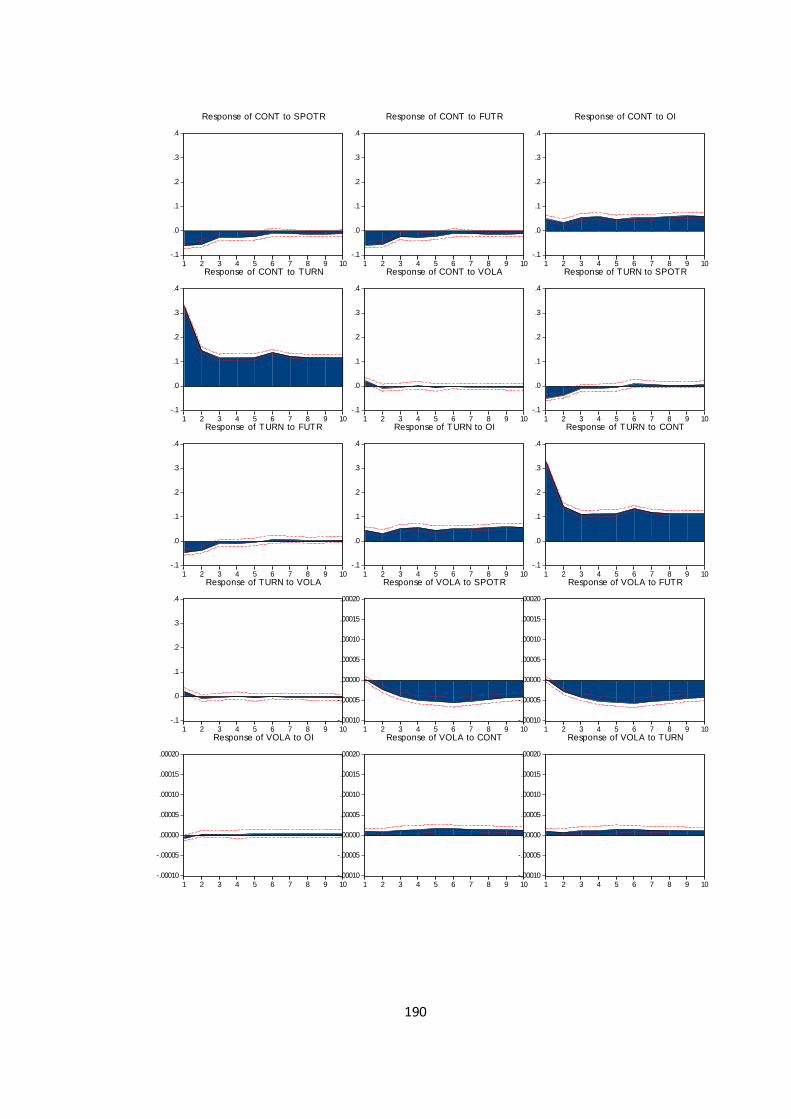

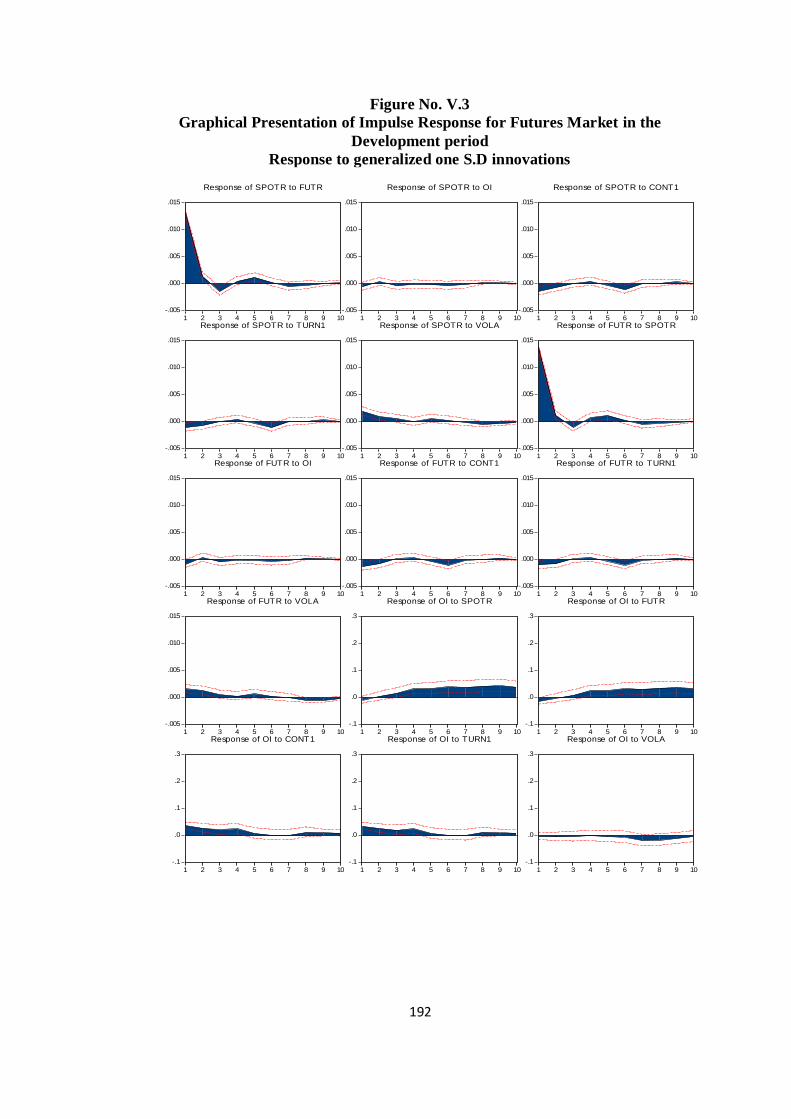

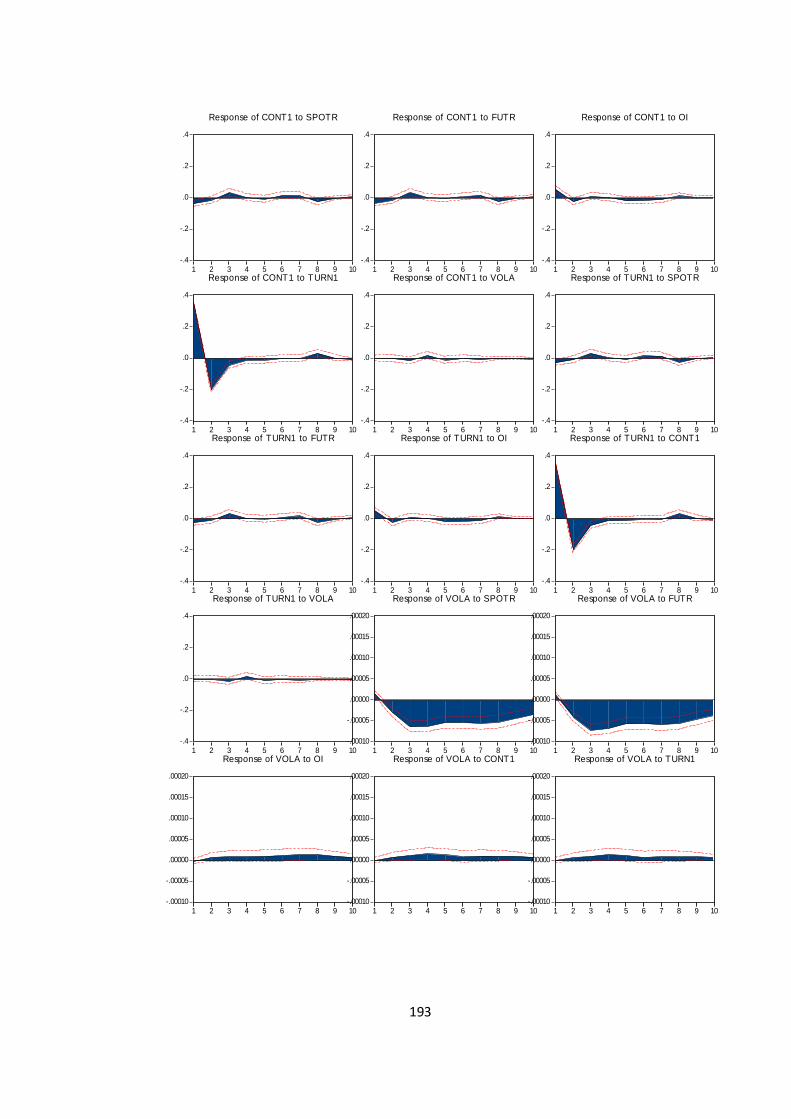

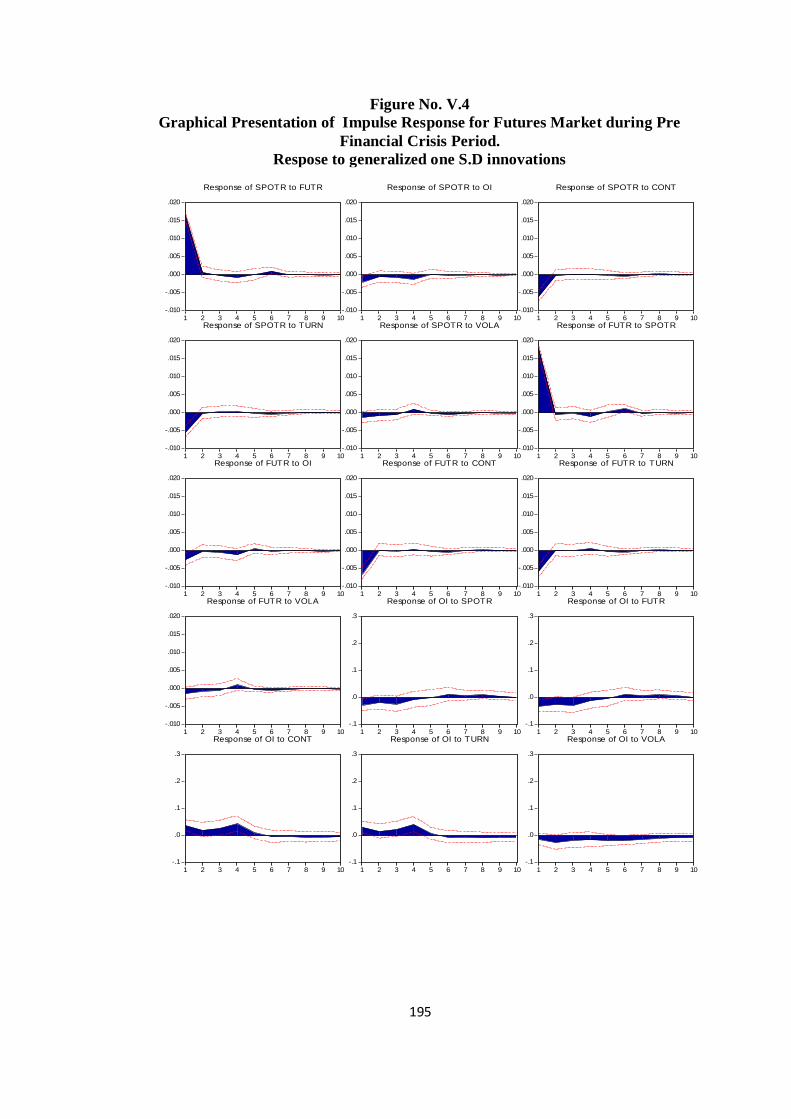

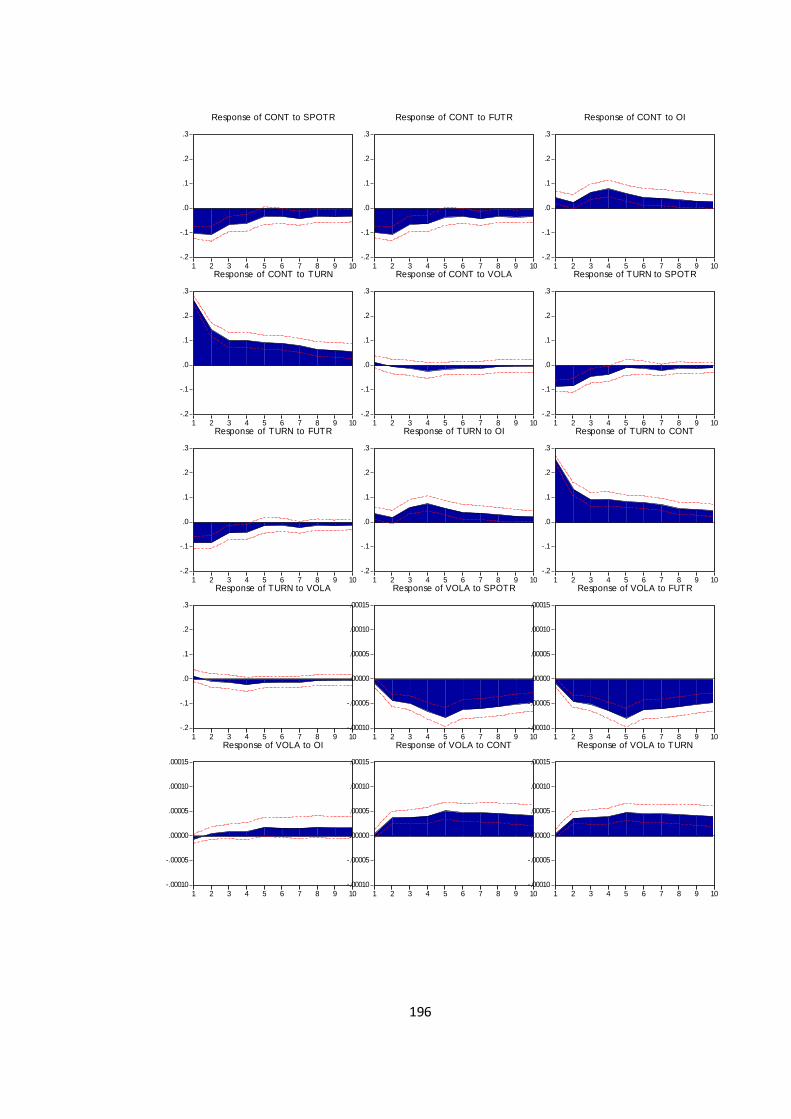

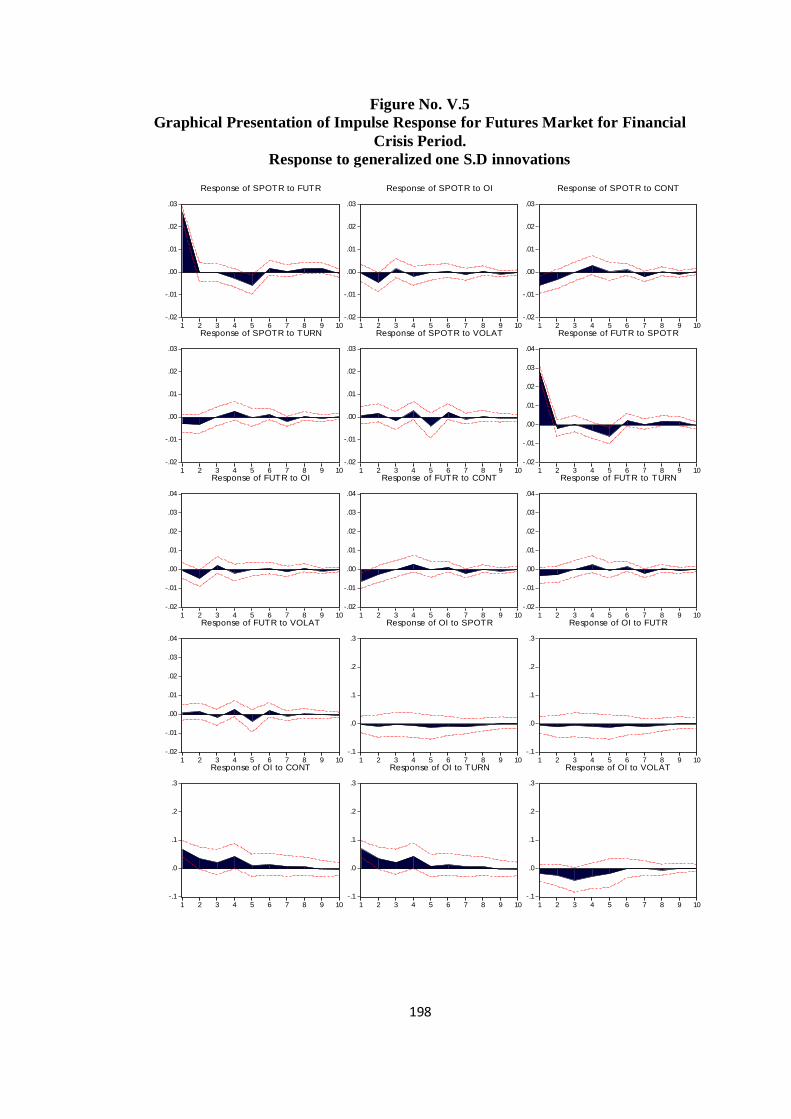

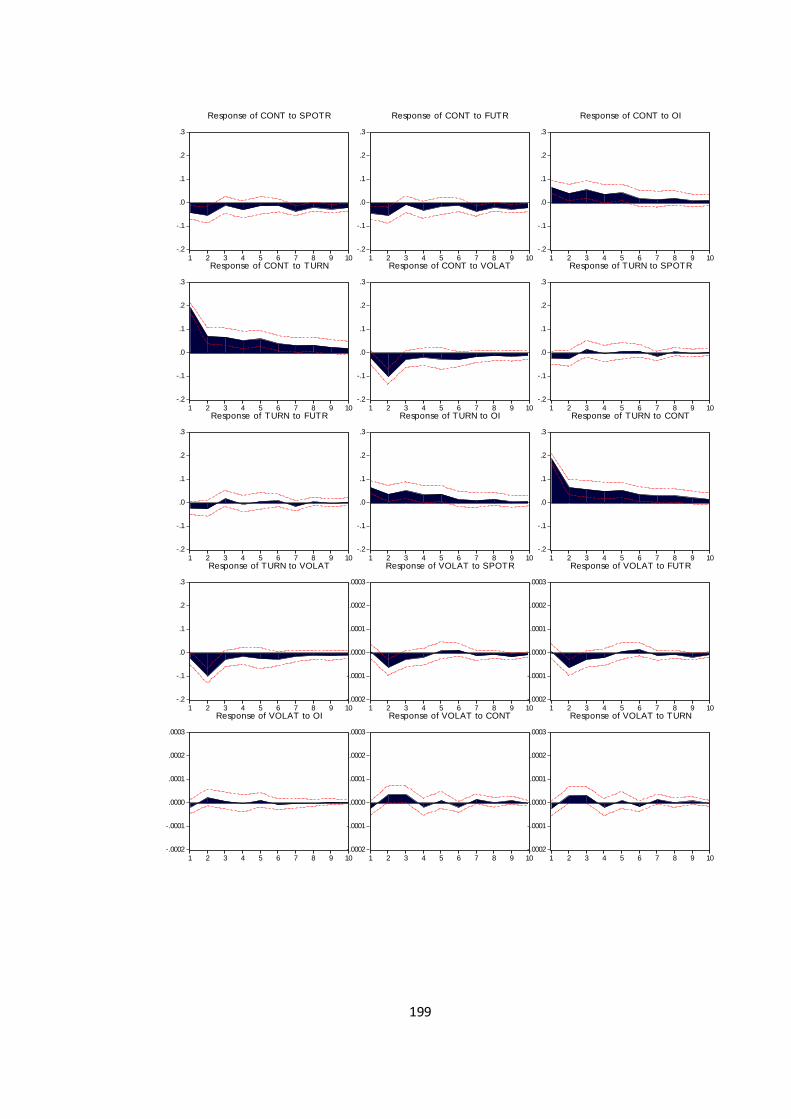

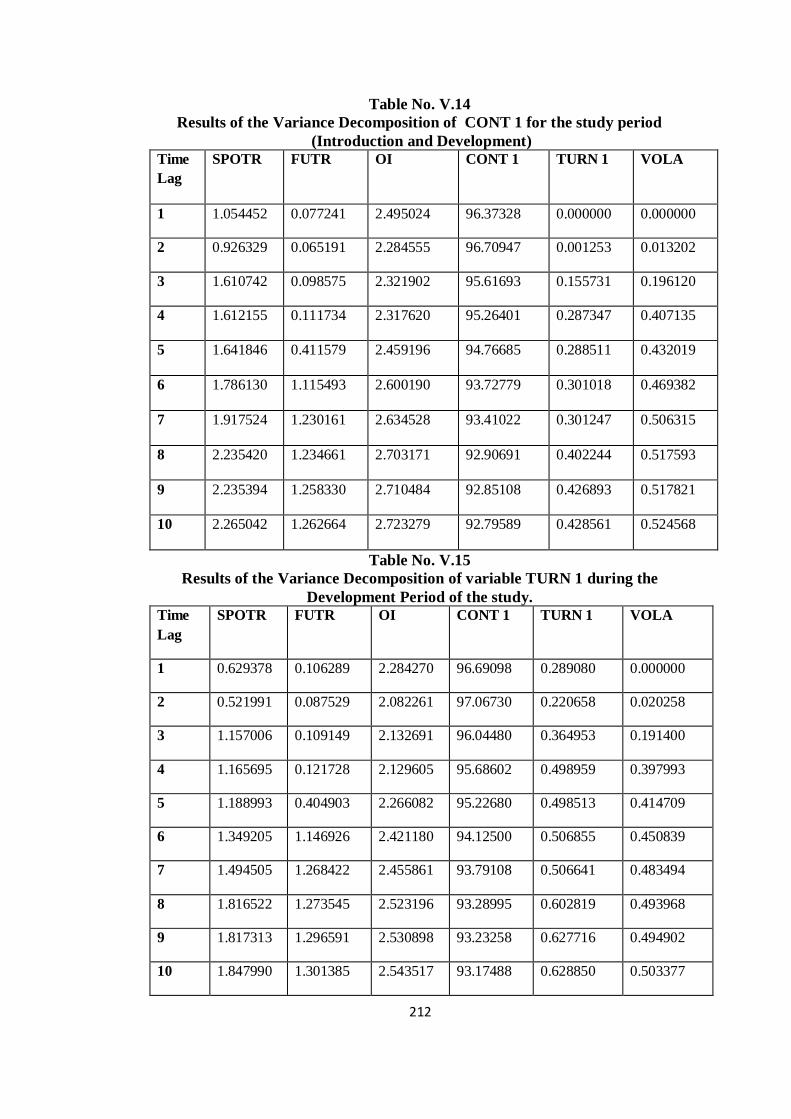

5.10 Time Profile of Shocks.................................................... 188

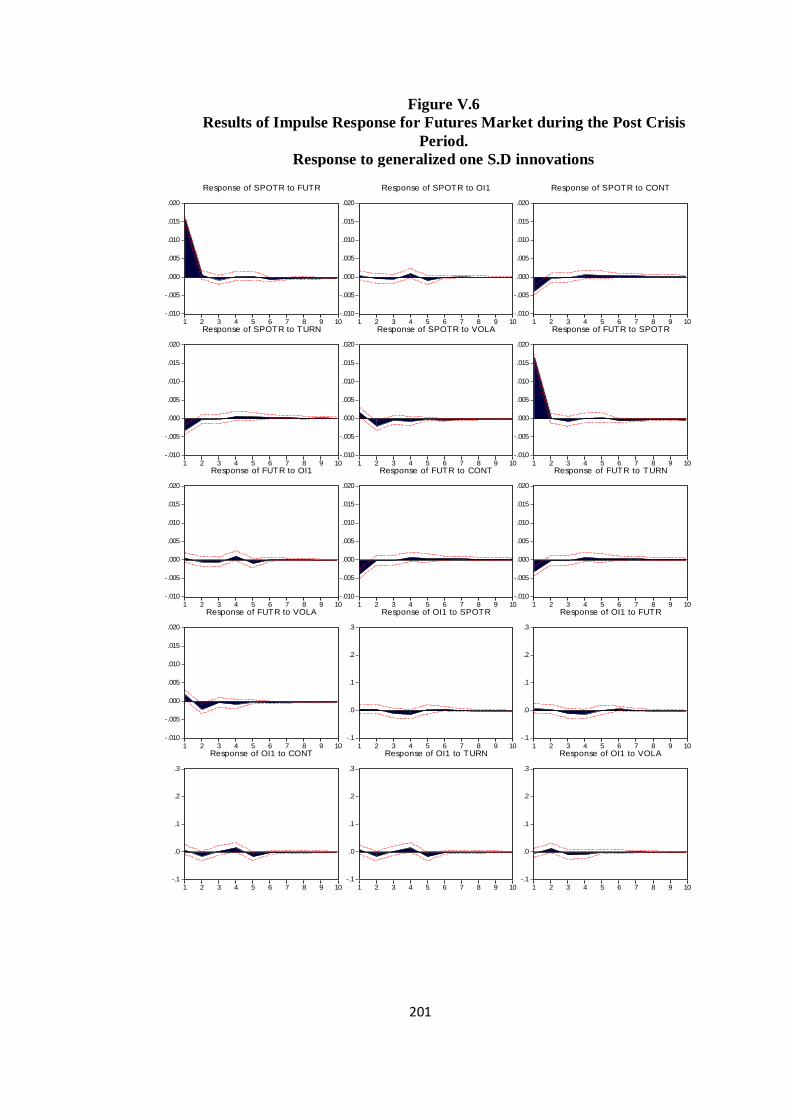

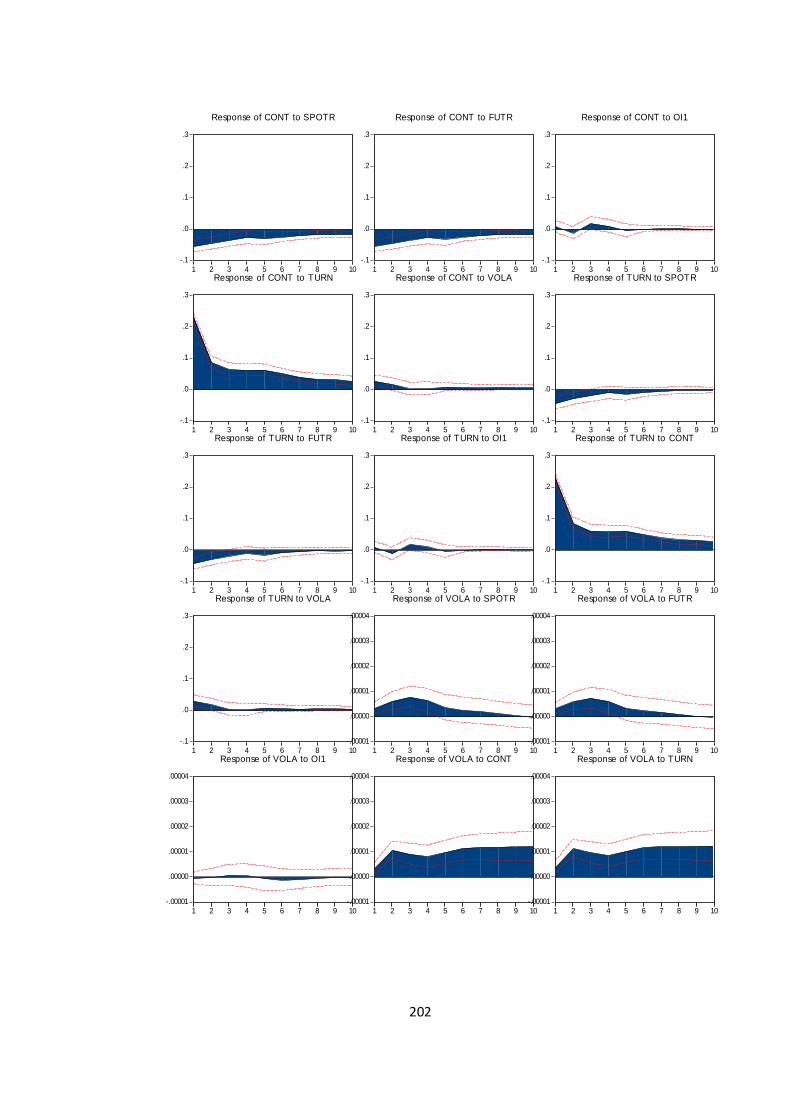

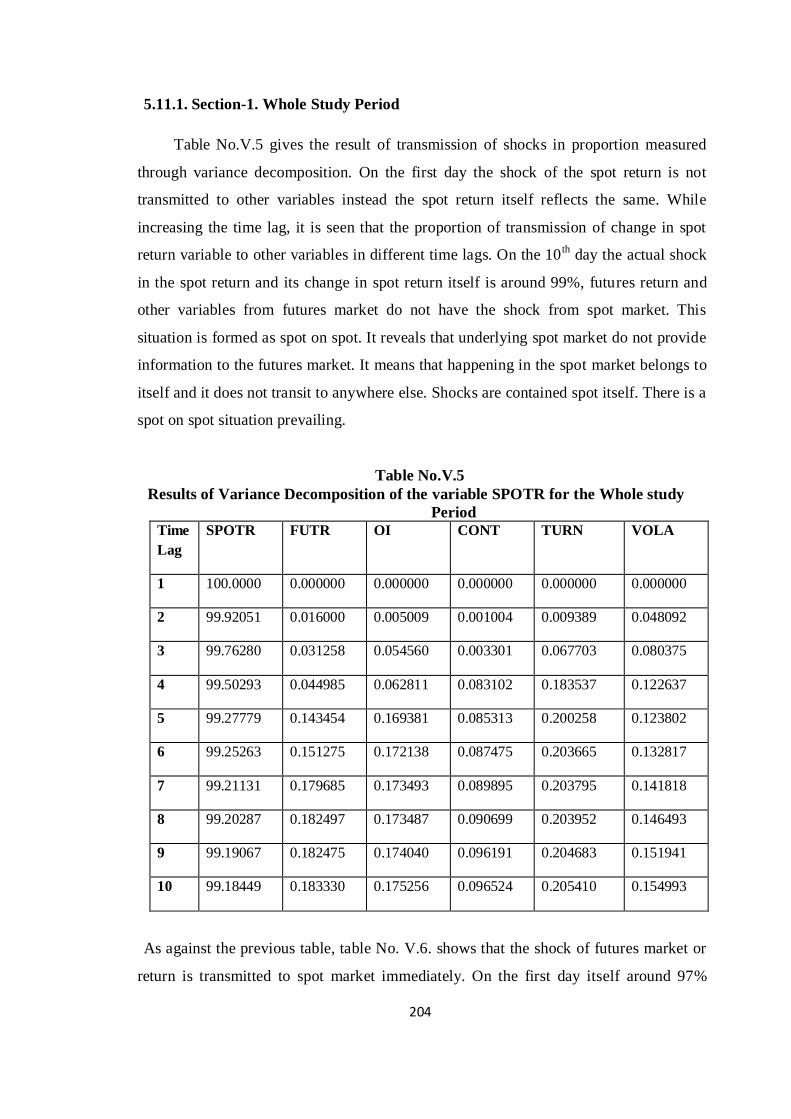

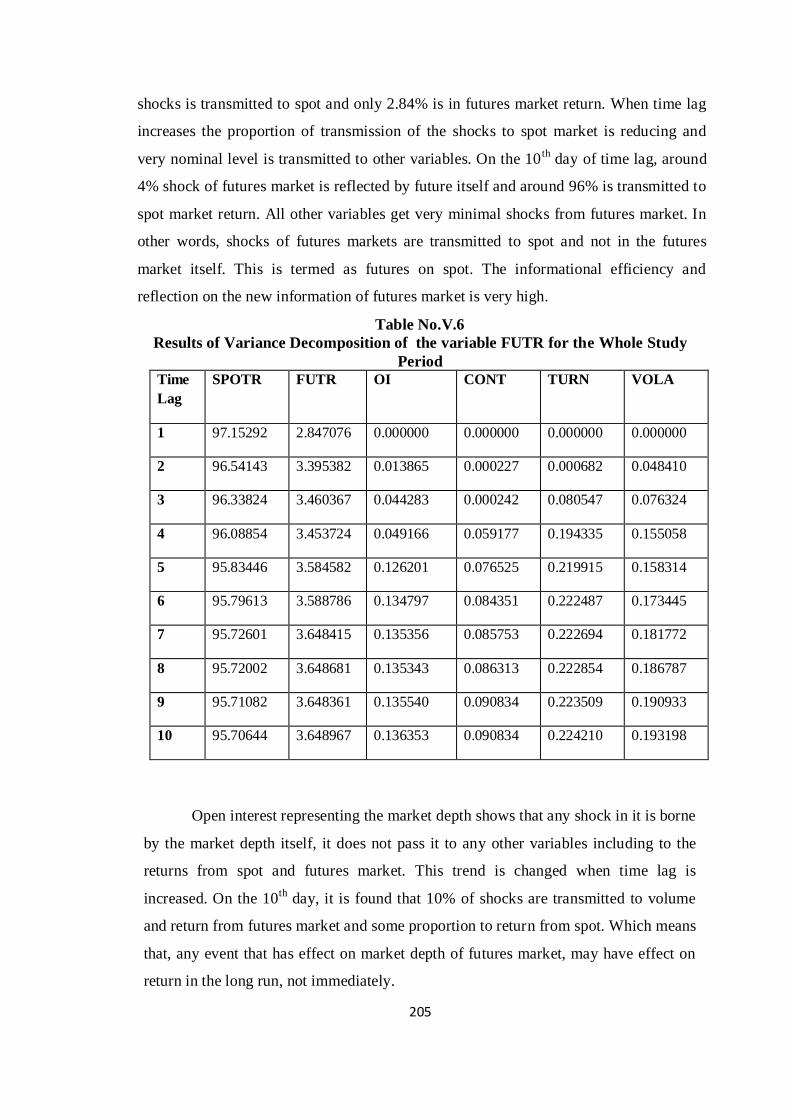

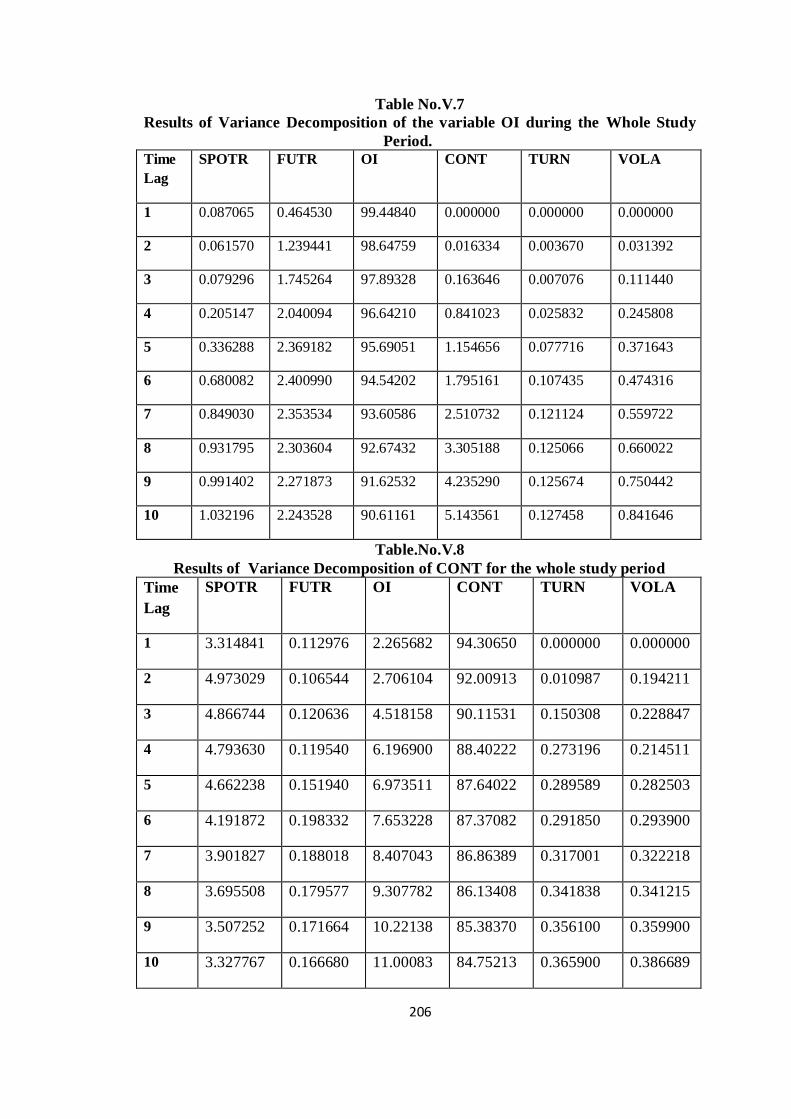

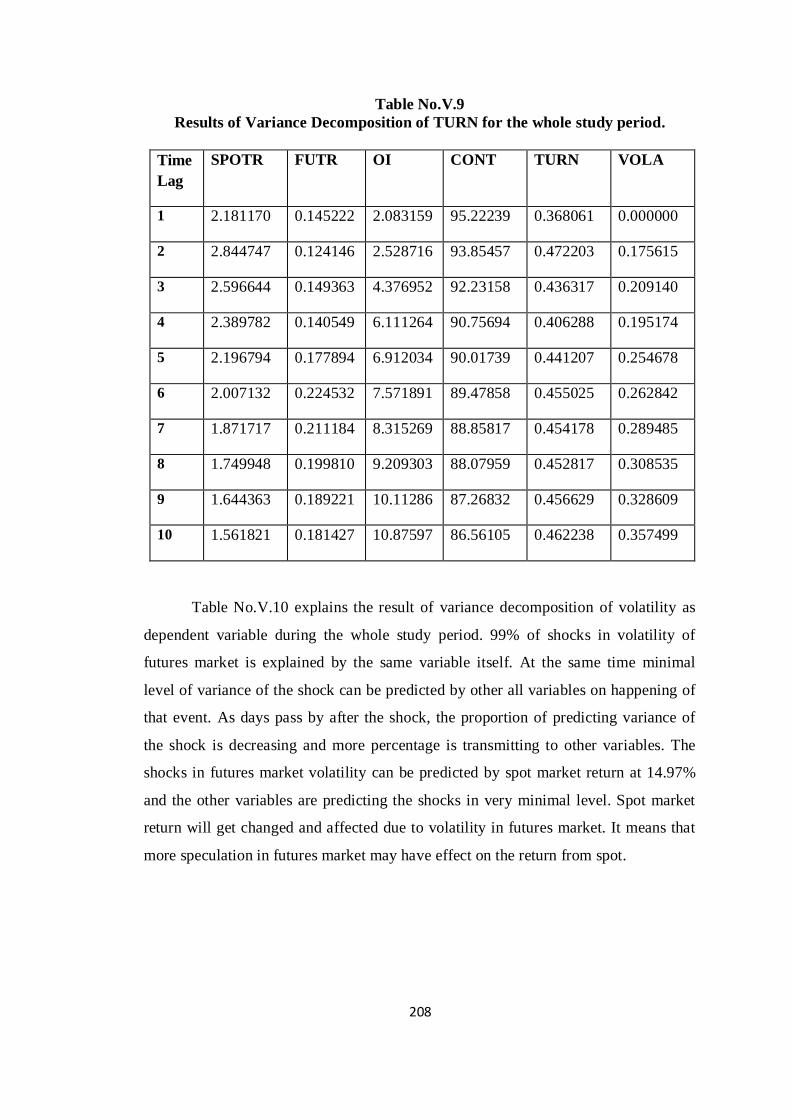

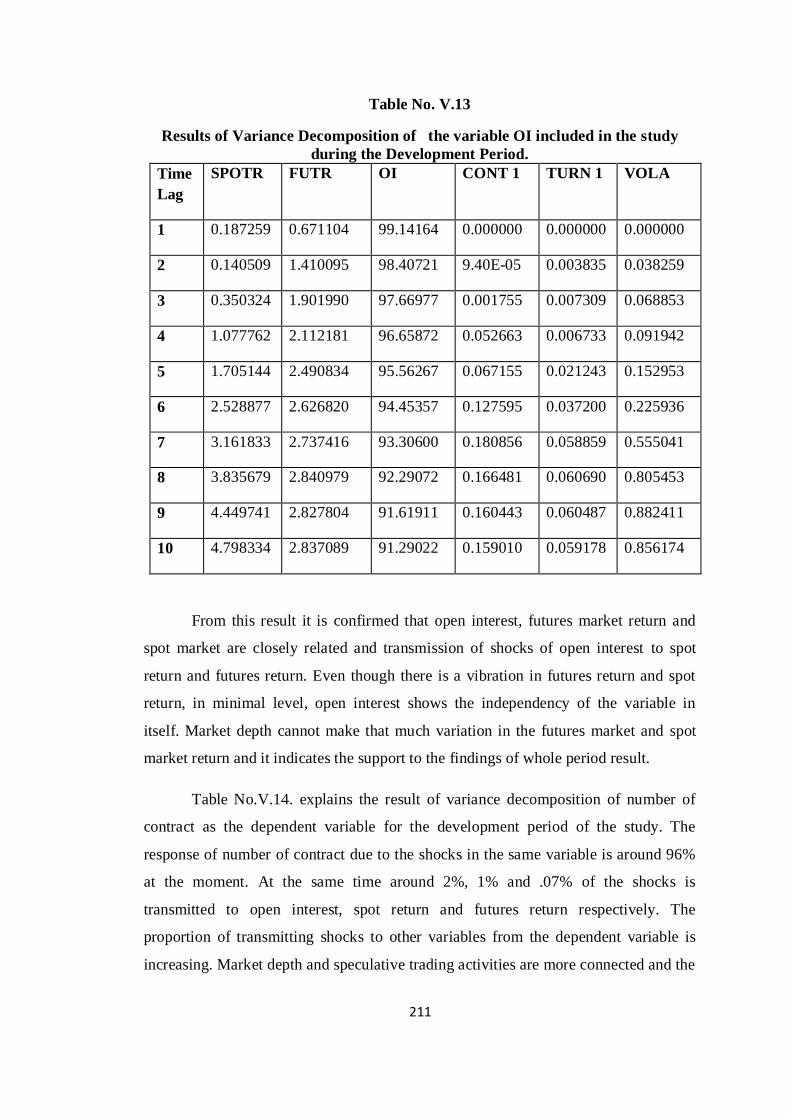

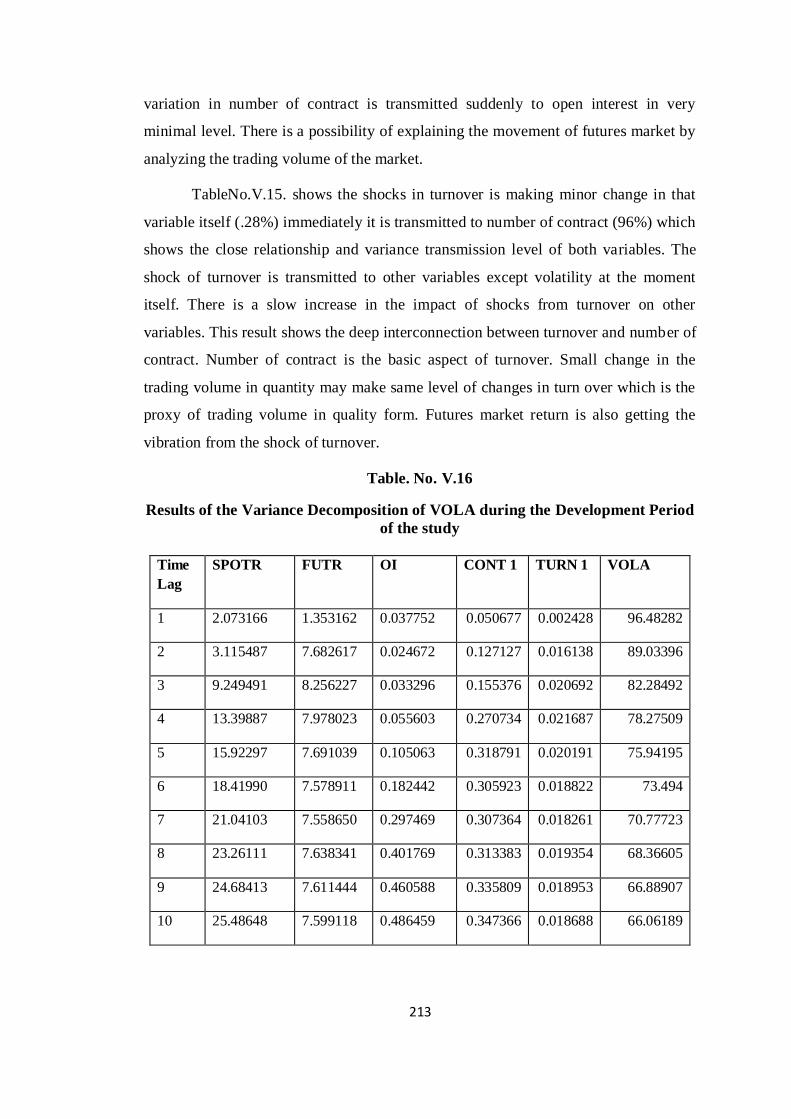

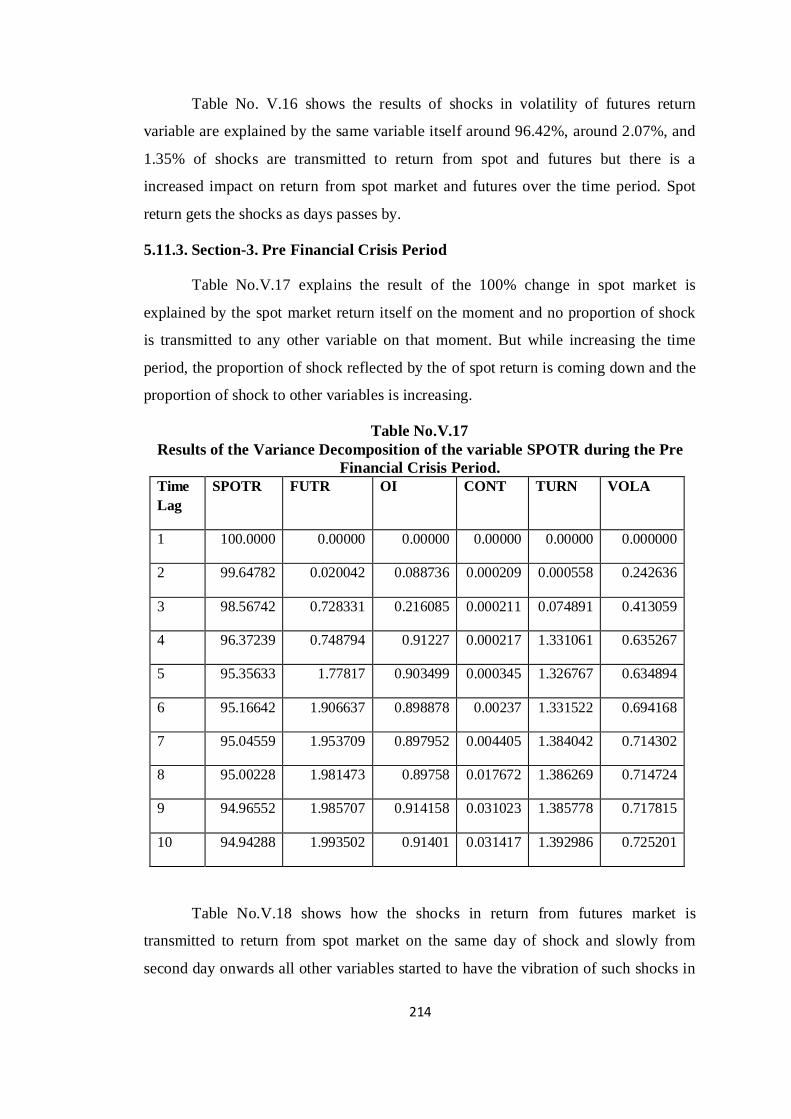

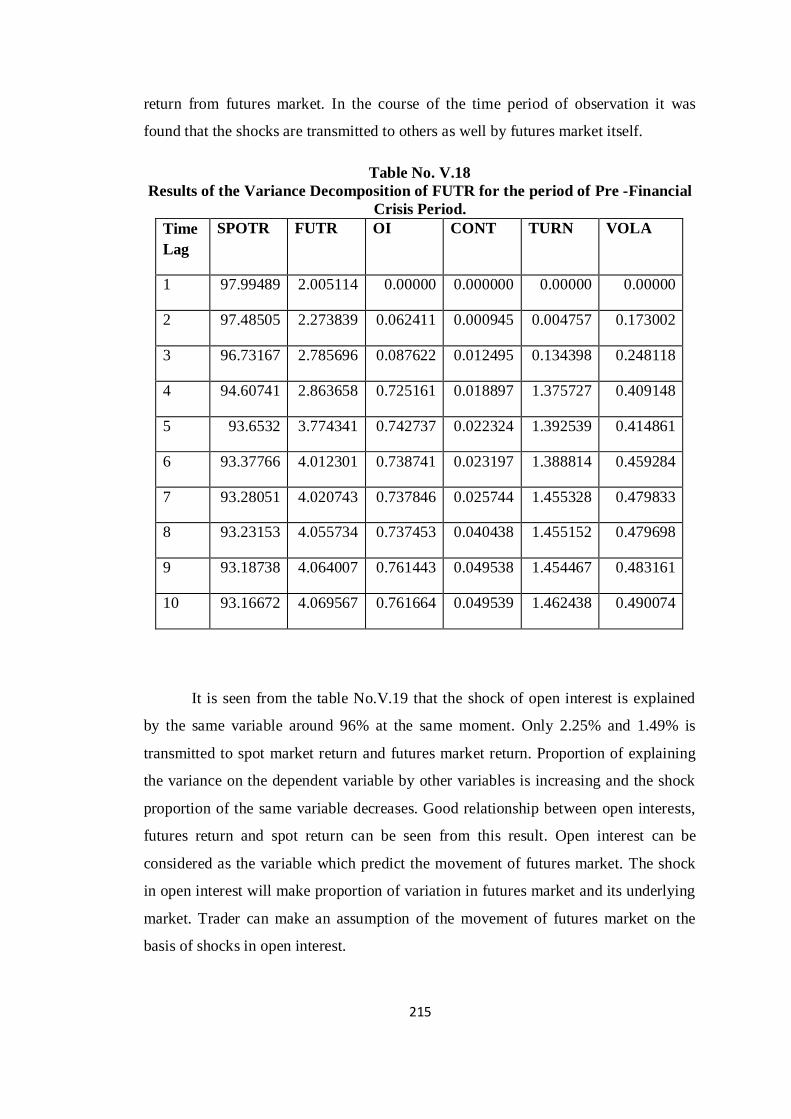

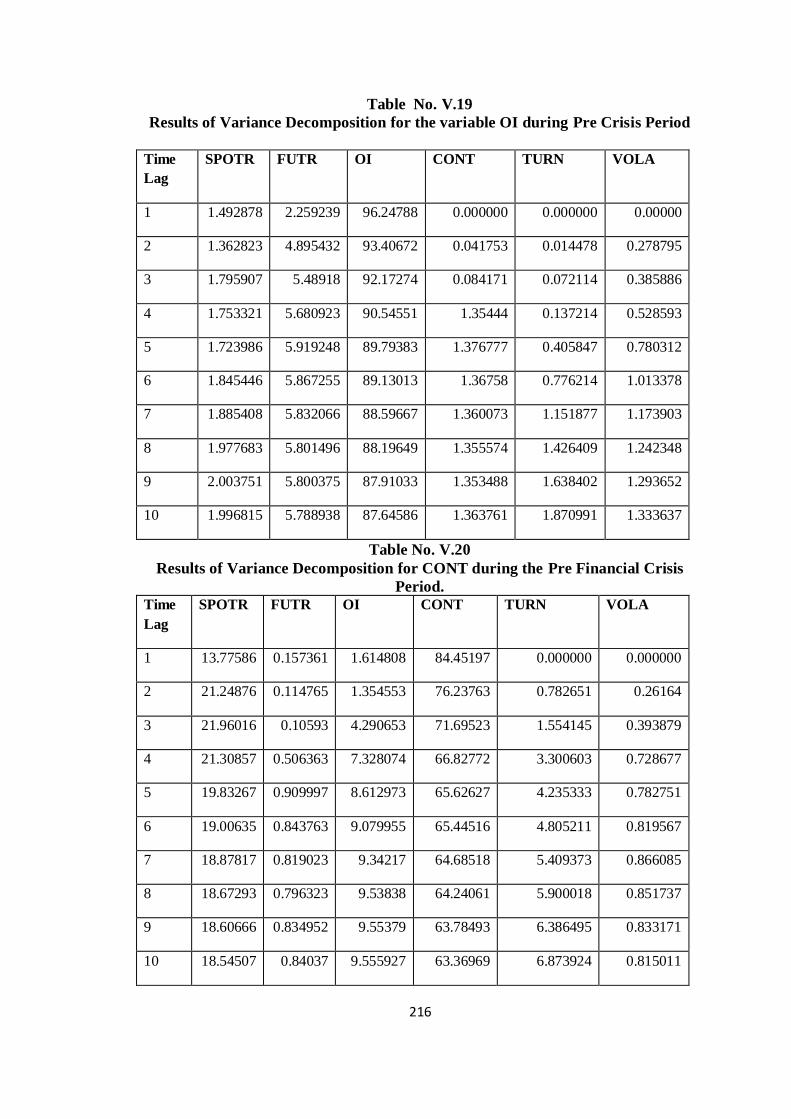

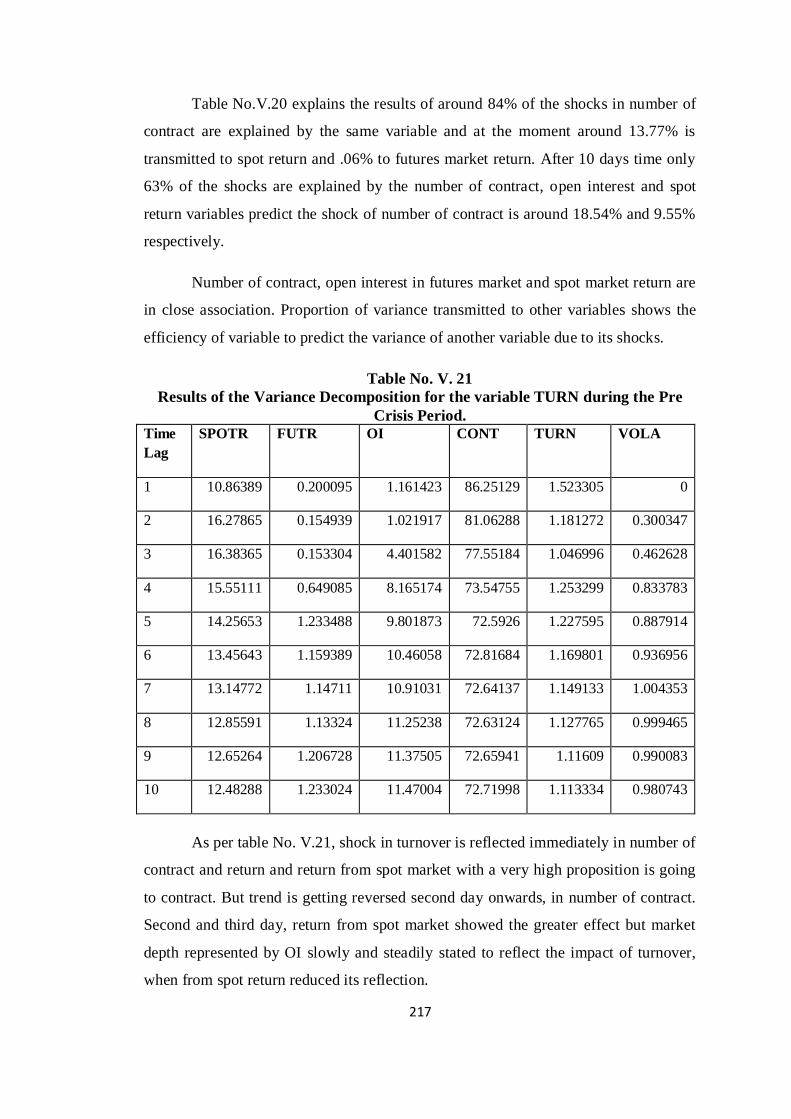

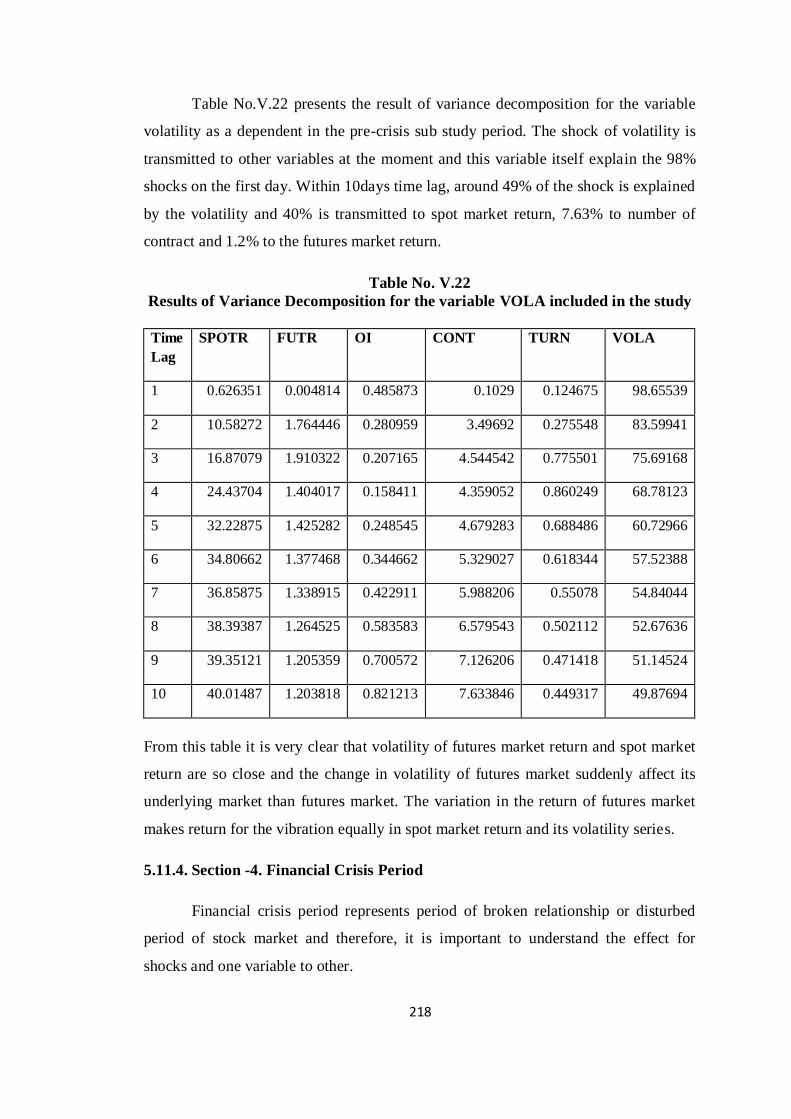

5.11 Proportion and Transmission of Shocks.......................... 203

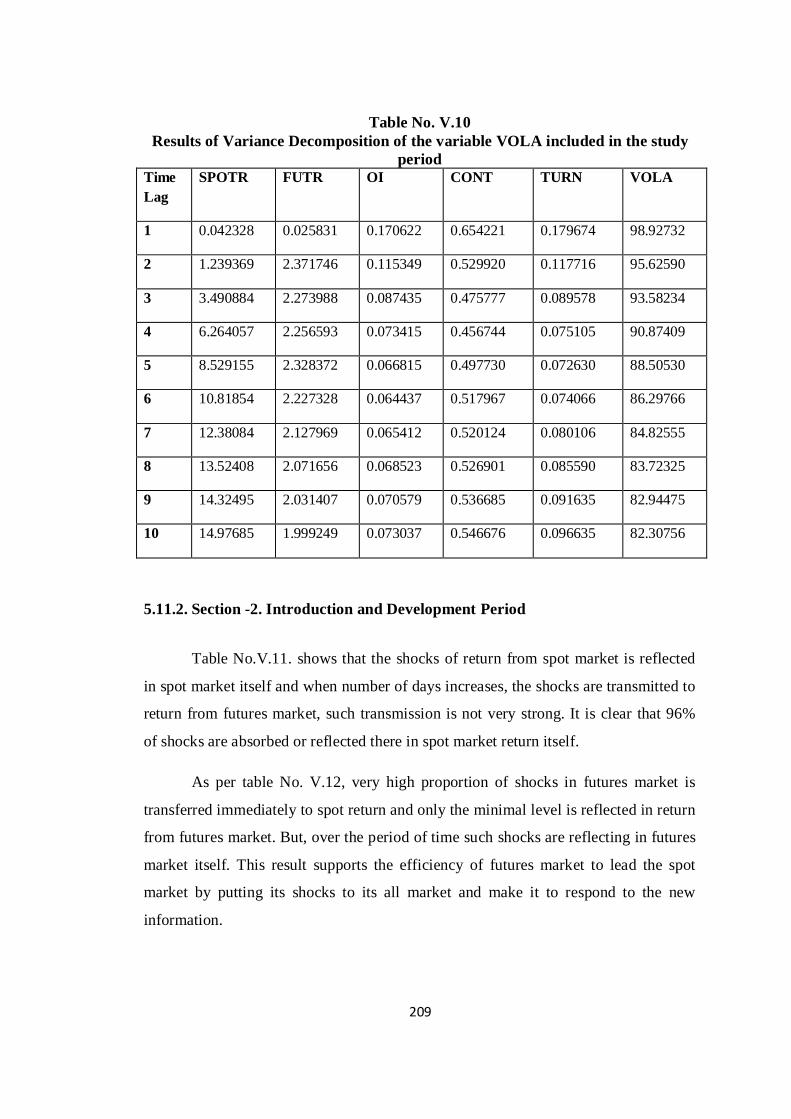

5.12 Conclusion......................................................................

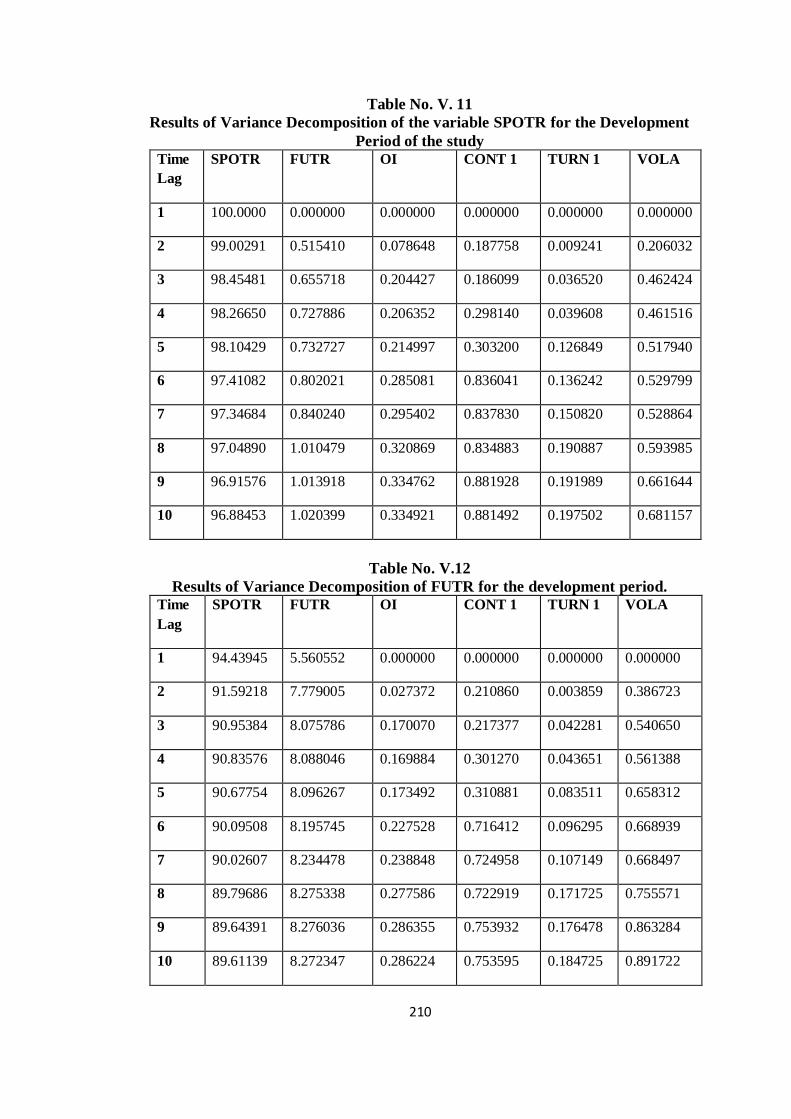

229

VI RISK REDUCTION EFFICIENCY OF FUTURES

MARKET IN INDIA

232-256

VI.1 Introduction................................................................... 233

VI.2 Variables used in the Study.............................................. 236

VI.3 Methodology Adopted..................................................... 237

VI.4 Rationale for the Analysis ........................................... 238

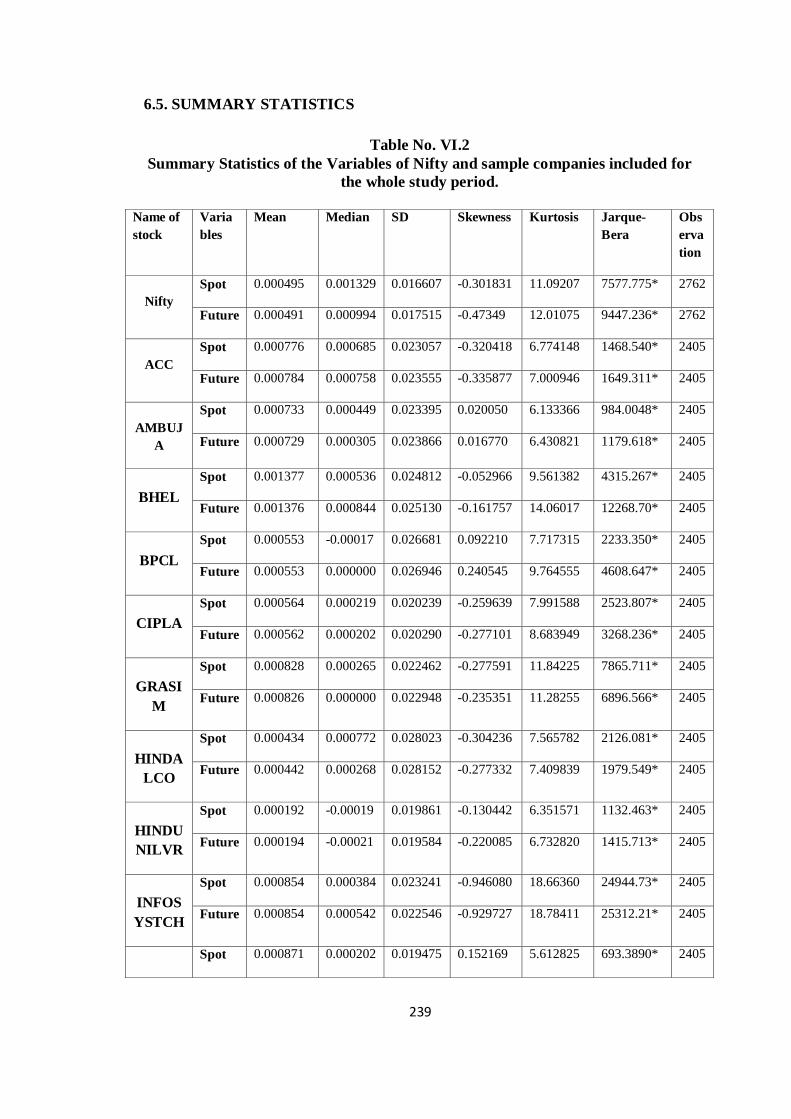

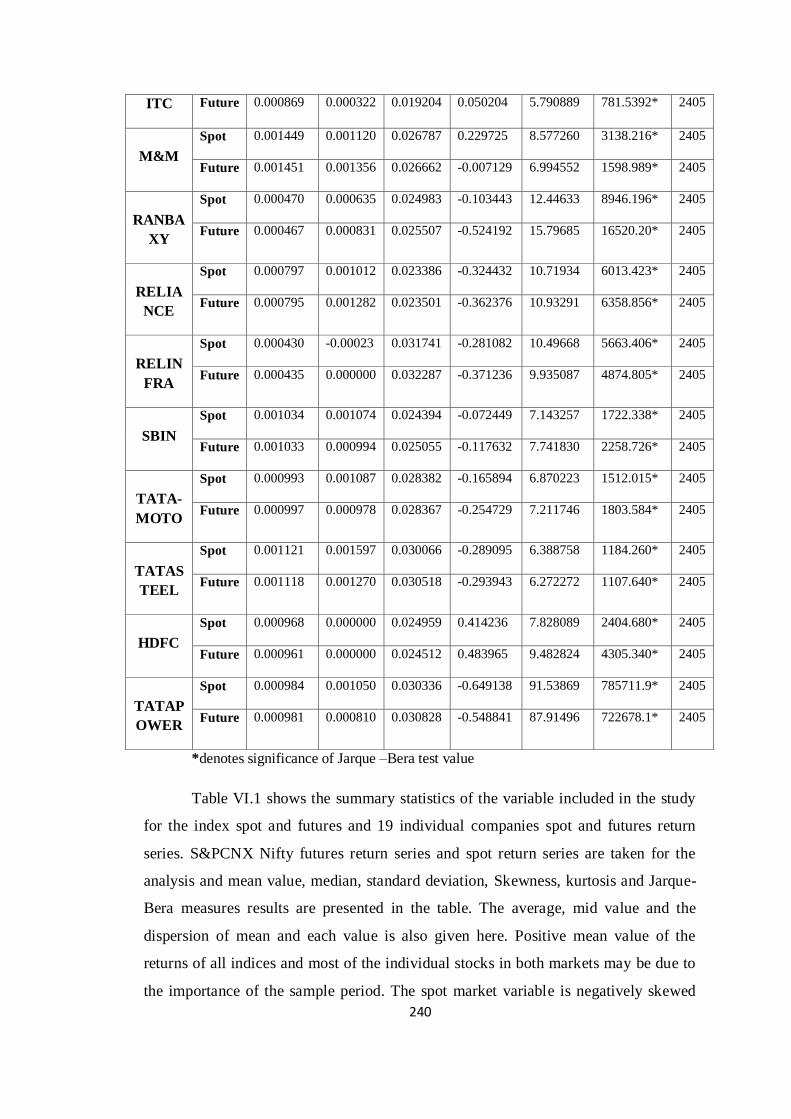

VI.5 Summary Statistics......................................................... 239

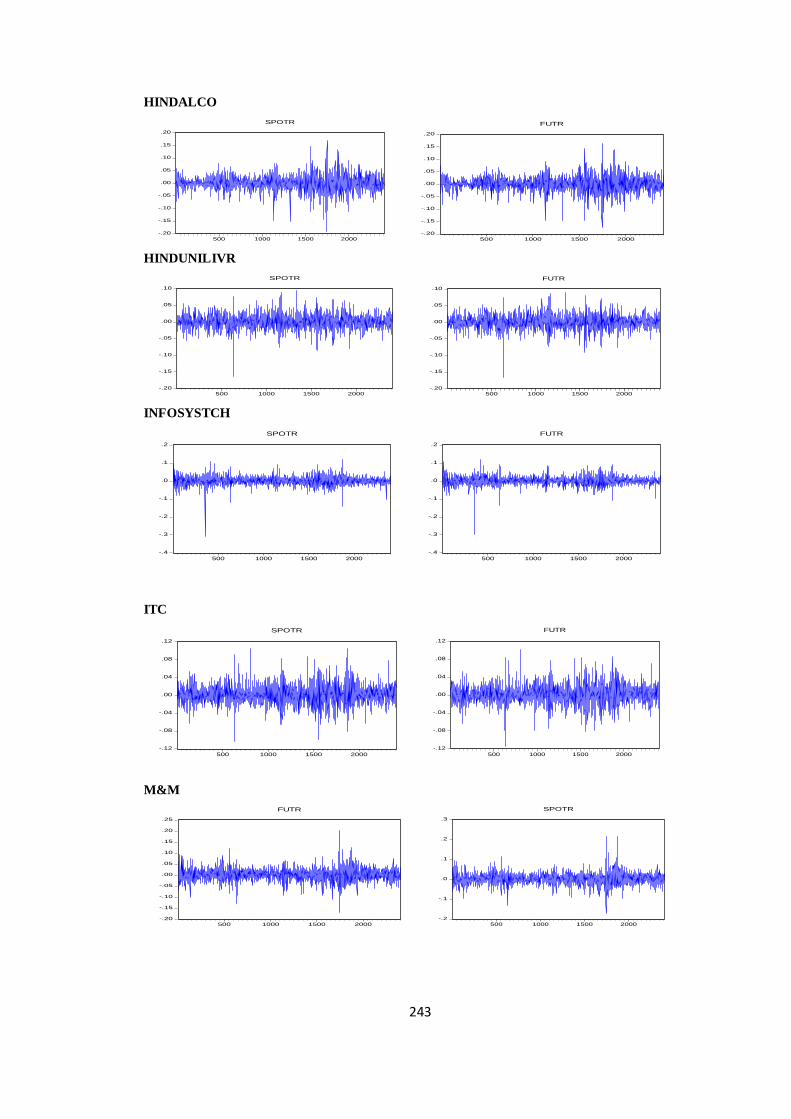

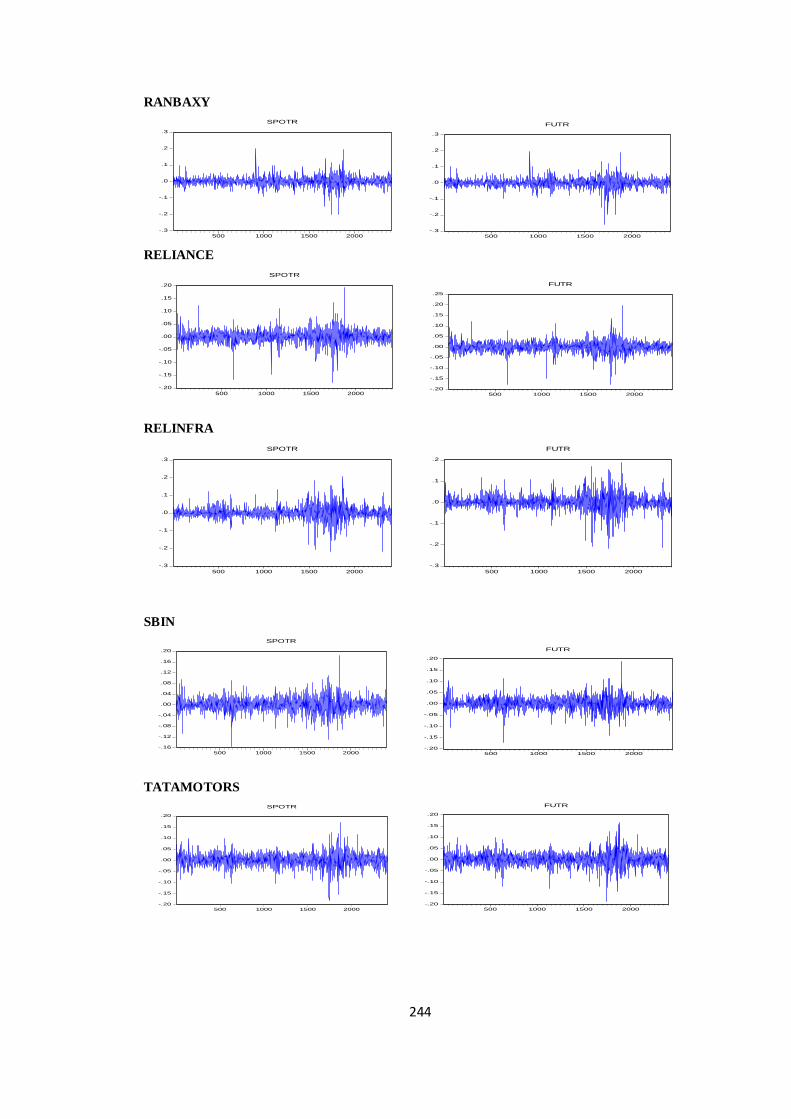

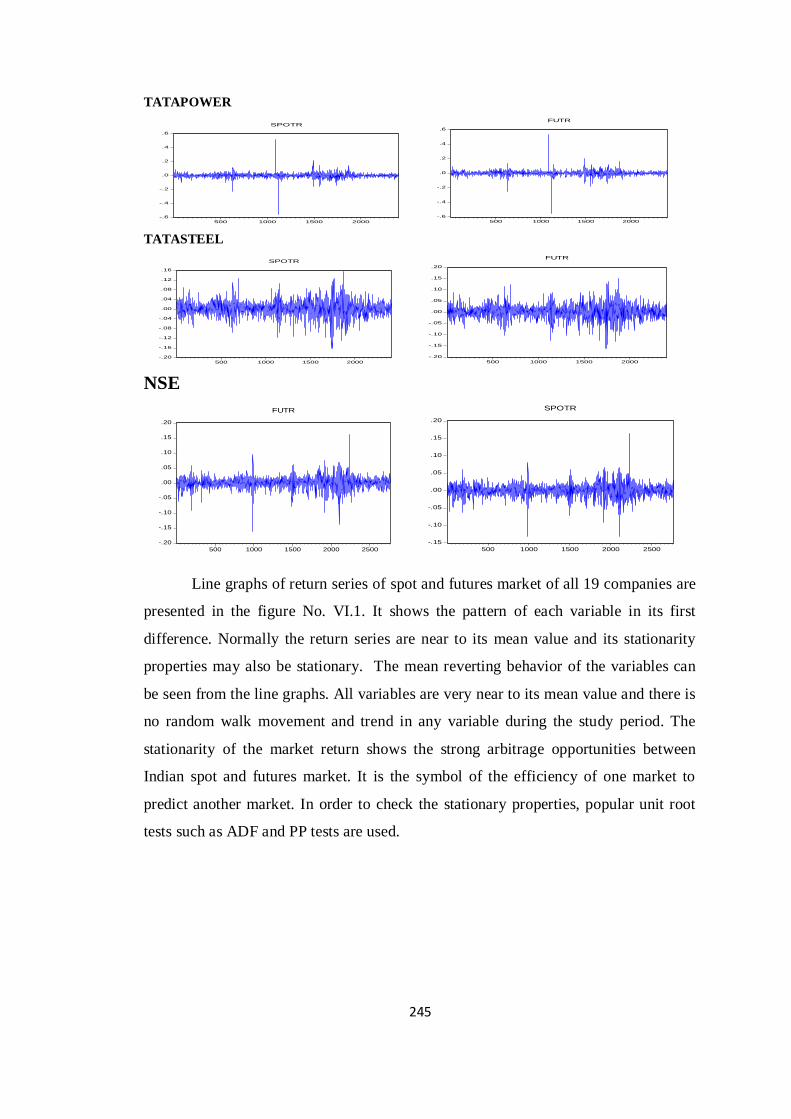

VI.6 Line Graphs....................................................................... 241

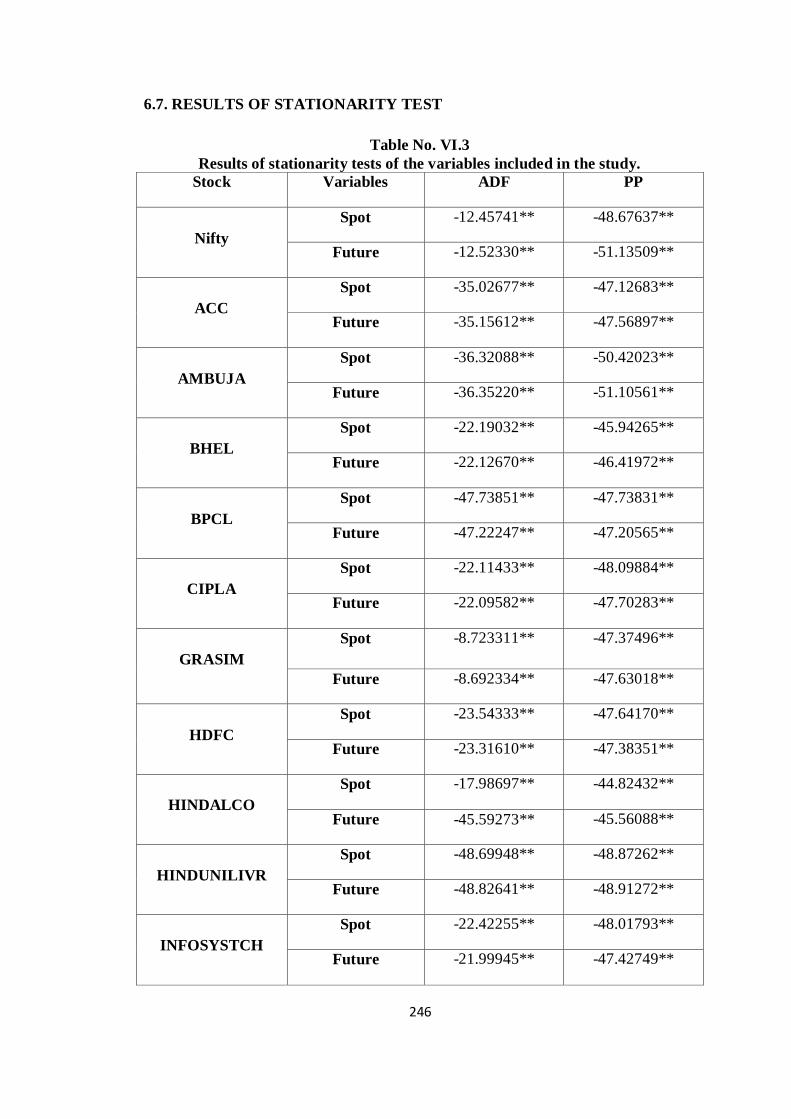

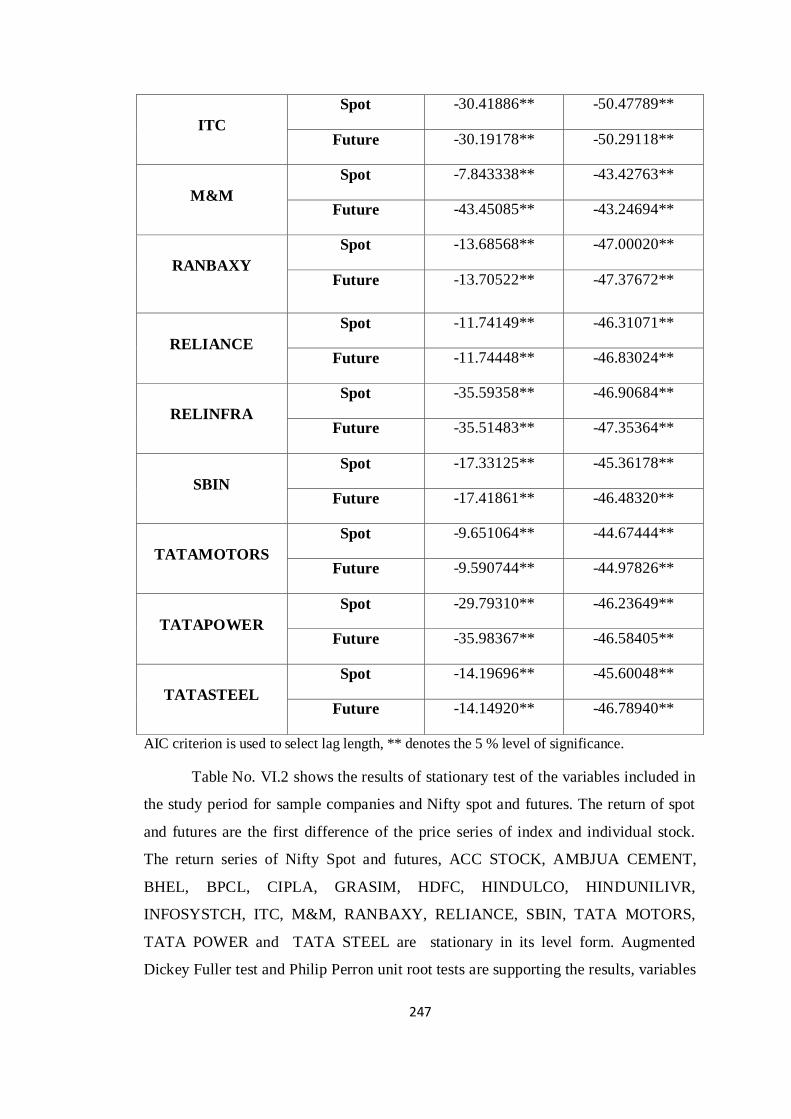

VI.7 Results of Stationarity Test................................................ 246

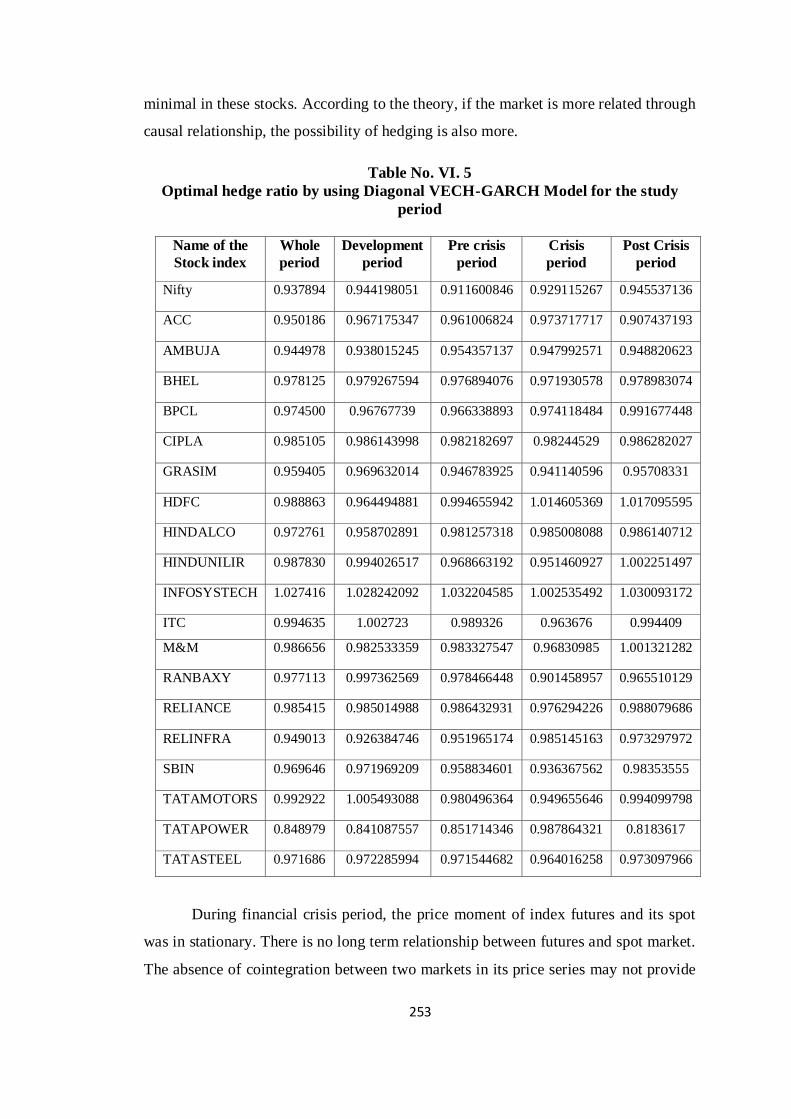

VI.8 Results of Optimal Hedge Ratio by using Diagonal VEC-

GARCH model............................................................

248

VI.9 Conclusion .................................................................. 255

VII FINDINGS AND SUGGESTIONS

257-266

VII.1 Introduction.................................................................. 258

VII.2 Long Term Relationship between Indian Futures and

Spot Market..................................................................

258

VII.3 Short Run Relationship between Indian Futures and

Spot Market..................................................................

259

VII.4 Lead –Lag Relationship between Futures and Spot 260

11

Market in India............................................................

VII.5 Determinants of Futures Market in India .................. 260

VII.6 Positive Relationship between Futures Market and its

Determinants..............................................................

261

VII.7 Negative Relationship between Futures Market and

its Determinants............................................................

262

VII.8 The existence of Shock and Responses of Indian

Futures and Spot Market.............................................

262

VII.9 Proportion and transmission of shocks and responses

of futures and spot market.........................................

263

VII.10 Risk reduction efficiency of futures market in India.... 263

VII.11 Summary..................................................................... 264

VII.12 Suggestions................................................................... 264

SCOPE FOR FURTHER RESEARCH

BIBLIOGRAPHY

APPENDIX

266-267

268-290

12

LIST OF TABLES

Table

No.

Title Page

No.

I.1 Forward Vs Future Contracts.................................................................. 22

1.2 Major Futures Exchanges: Year ended 31 December 2010..................... 26

I.3 NSE Futures and Options Monthly Settlement Statistics........................ 28

I.4 Relationship between Open Interest and Price...................................... 37

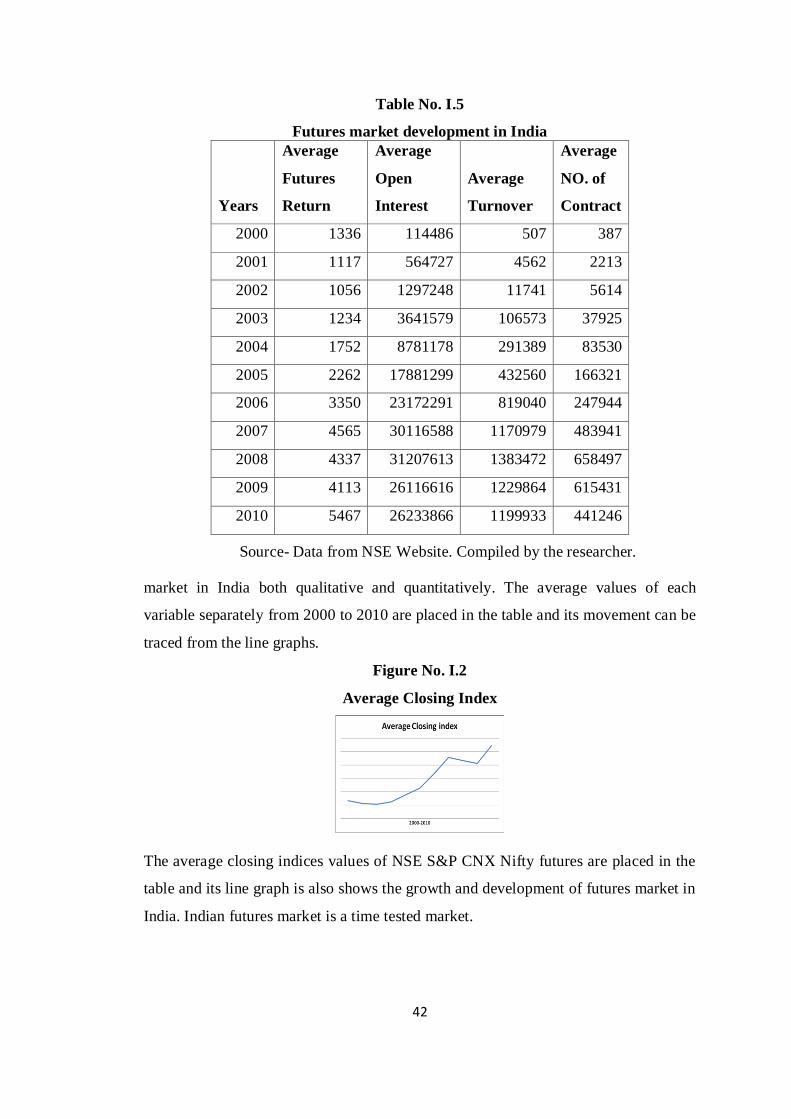

I.5 Futures Market Development in India...................................................... 42

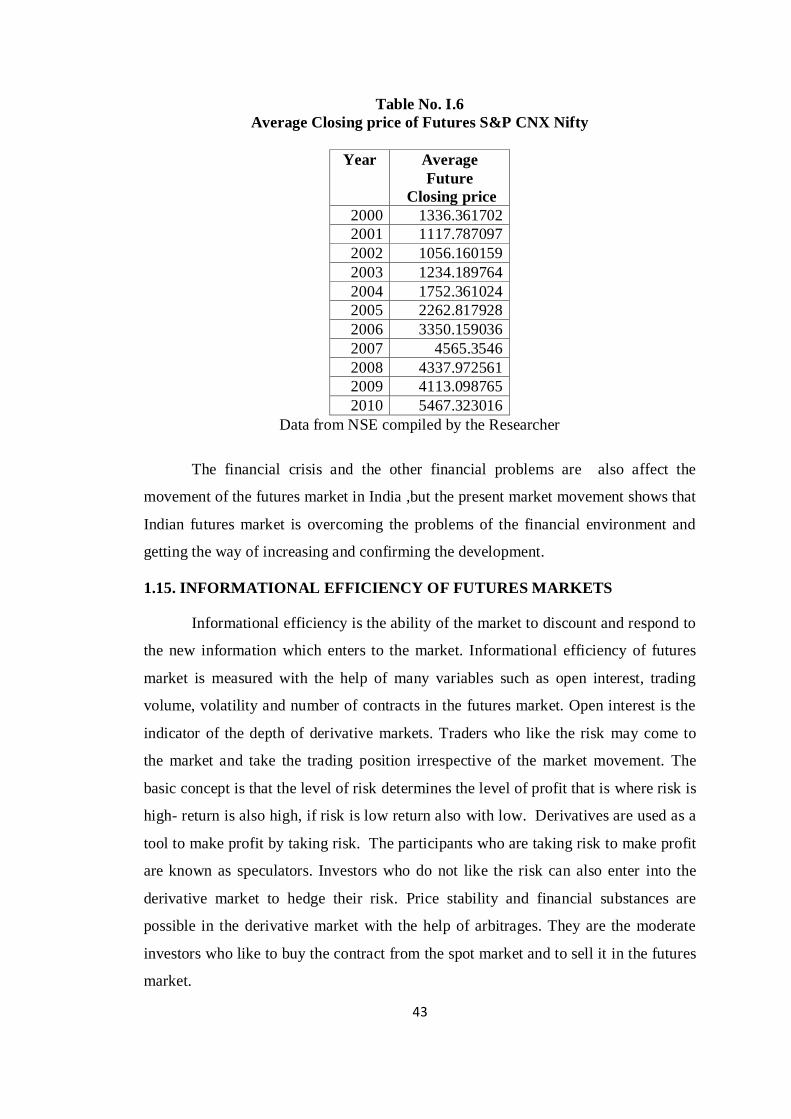

I.6 Average Closing Price of Futures S&P CNX Nifty................................. 43

II.1 Review of Literature................................................................................. 48

IV.1 Summary Statistics of Variables included for the various Study Periods 144

IV.2 Results of Stationarity Tests applied on variables included during the

various Study Period............................................................................... 148

IV.3 Results of VAR Criteria adopted for Selection of Lag Length for

models used to determine the relationship between Spot and Futures

during different Study Periods.................................................................

151

IV.4 Results of Unrestricted Cointegration Rank Test applied through

Johansen Cointegration Methodology for various Study Periods. (Trace

& Maximum Eigen value)........................................................................

154

IV.5 VAR Granger Causality/Block Exogeneity Wald Tests........................... 154

IV.6 Results of Normalized Cointegration Vector Error Correction Model

applied to determine the Short Term Relationship between Spot and

Futures Market during different Study Period.........................................

156

IV.7 Results of Wald Test coefficients for Causality between Spot & Futures

Market during the different Study Period............................................... 159

V.1 Summary Statistics of variables included in the study during different

Study Periods............................................................................................

171

V.2 Resuts of Stationarity Tests applied on variables included during the

various Study Period................................................................................

178

V.3 VAR lag Order Selection Criteria for models used to find the

determinants of Futures Market in India...................................................

180

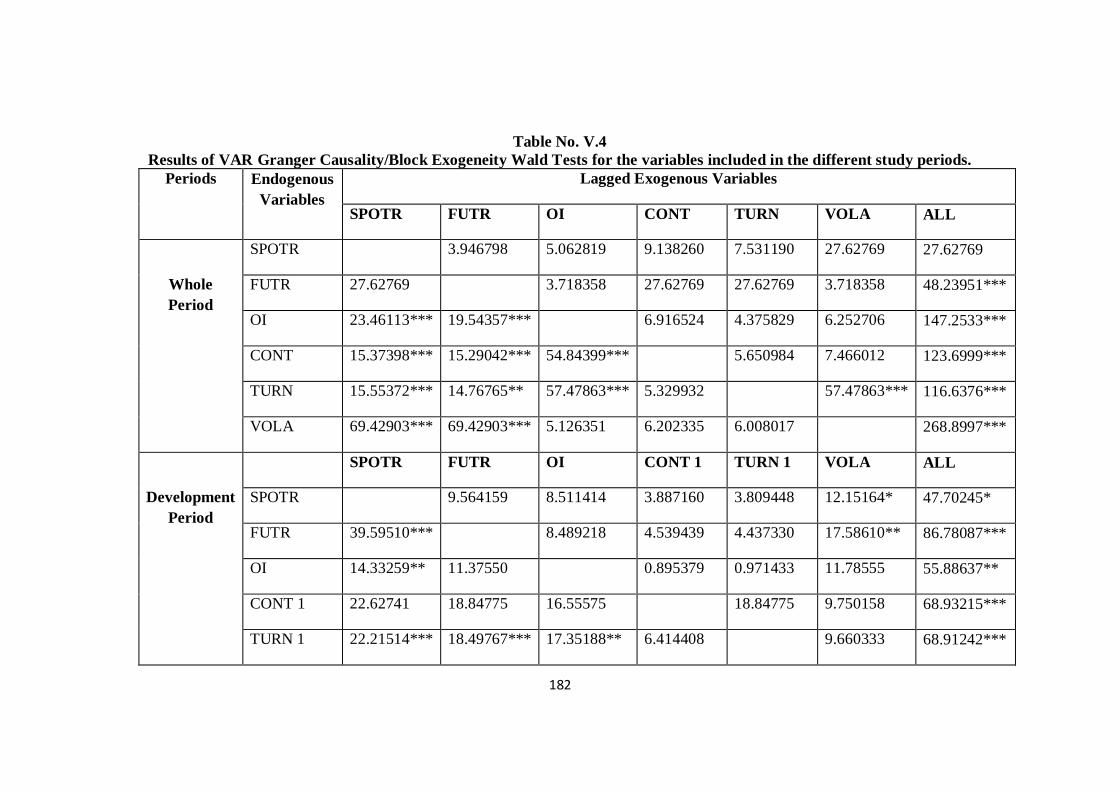

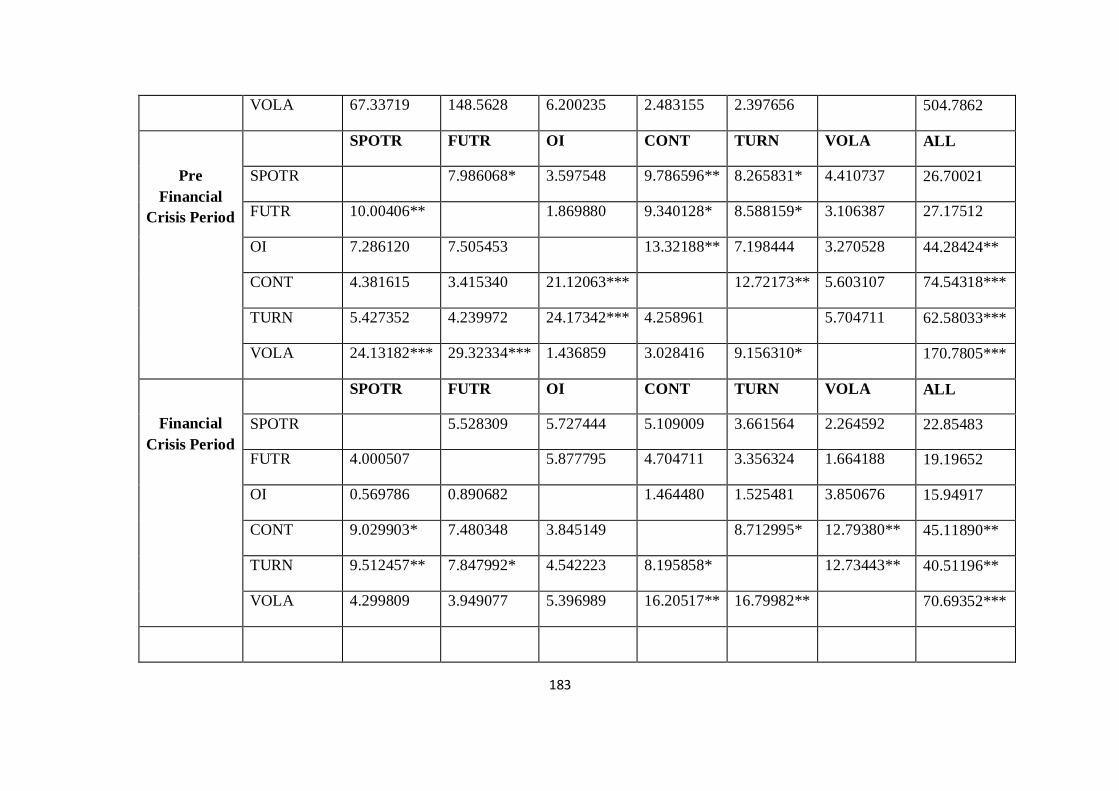

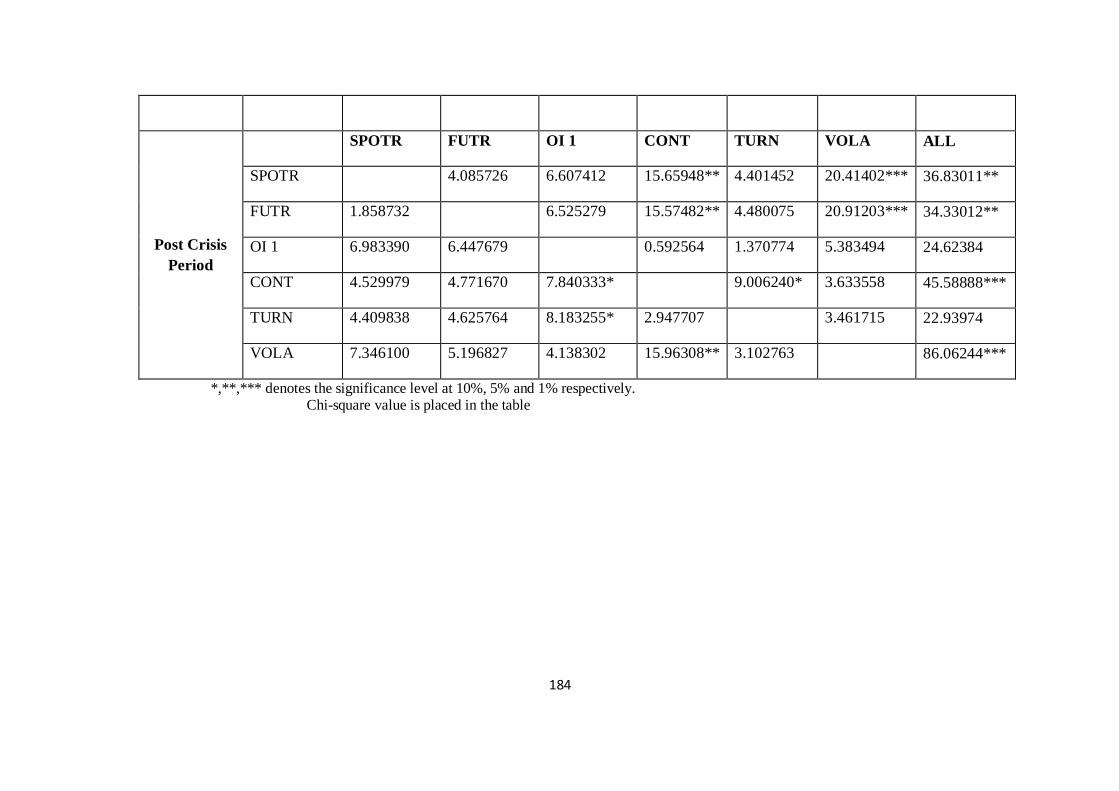

V.4 Results of VAR Granger Causality/Block Exogeneity Wald Tests for

the variables included in the different Study Periods...............................

182

V.5 Results of Varience Decomposition of the variable SPOTR for the

Whole Study Period.................................................................................

204

V.6 Results of Variance Decomposition of the variable FUTR for the

Whole Study Period.................................................................................

205

13

V.7 Results of Variance Decoposition of the variable OI during the Whole

Study Period.............................................................................................

206

V.8 Results of Variance Decomposition of CONT for the Whole Study

Period......................................................................................................

206

V.9 Results of Variance Decomposiotion of TURN for the Whole Study

Period.......................................................................................................

208

V.10 Results of Variance Decomposition of the variable VOLA included in

the Study Period.......................................................................................

209

V.11 Results of Variance Decomposition of the variable SPOTR for the

Development Period of the Study............................................................

210

V.12 Results of Variance Decomposition of FUTR for the Development

Period........................................................................................................

210

V.13 Results of Variance Decomposition of the variable OI included in the

study during the Development Period.....................................................

211

V.14 Results of the Variance Decomposition of CONT 1 for the study

Period (Introduction and Development).................................................

212

V.15 Results of the Variance Decomposition of variable TURN 1 during the

Development Period of the Study...........................................................

212

V.16 Results of the Variance Decomposition of VOLA during the

Development Perid of the Study..............................................................

213

V.17 Results of the Variance Decompositionof the variable SPOTR during

the Pre Financial Crisis Period..................................................................

214

V.18 Results of the Variance Decomposition of FUTR for the period of Pre

Financial Crisis Period.............................................................................

215

V.19 Results of Variance Decomposition for the variable OI during Pre

Crisis Period.............................................................................................

216

V.20 Results of Variance Decomposition for CONT during the Pre Financial

Crisis Period.............................................................................................

216

V.21 Resultsof the Variance Decompositionfor the variable TURN during

the Pre Crisis Period................................................................................

217

V.22 Results of Variance Decomposition for the variable VOLA included in

the Study.................................................................................................

218

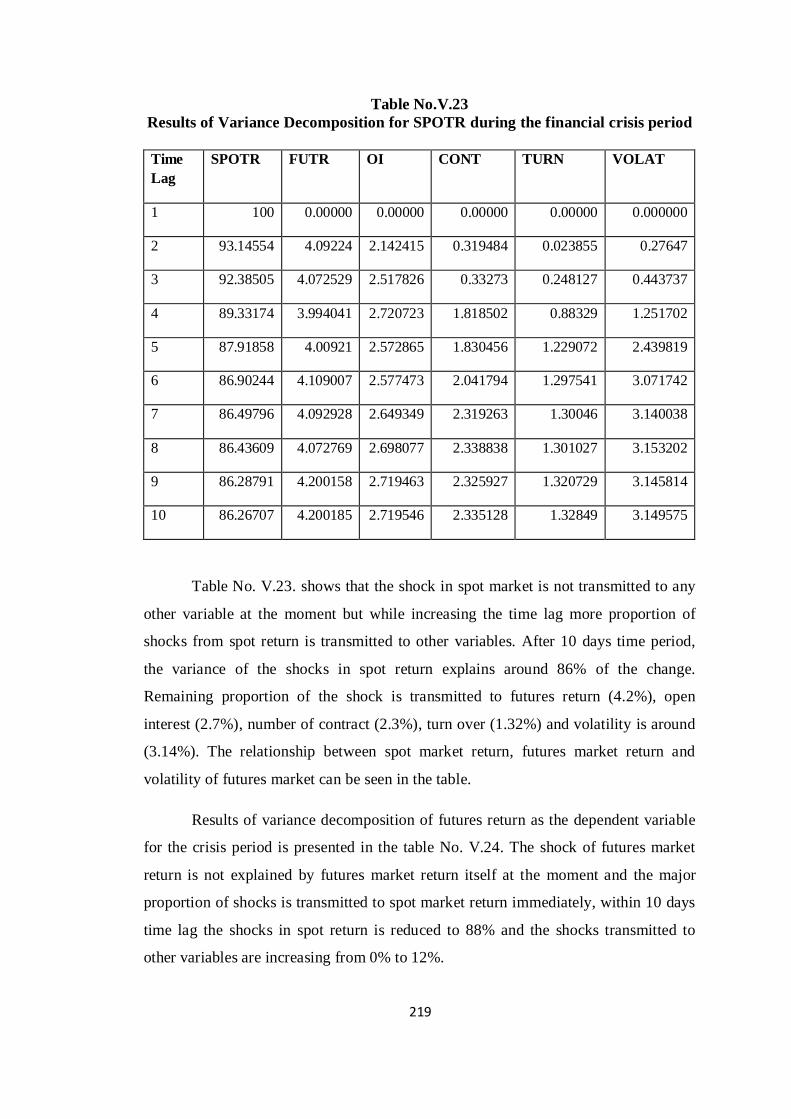

V.23 Results of Variance Decomposition for SPOTR during the Financial

Crisis Period..............................................................................................

219

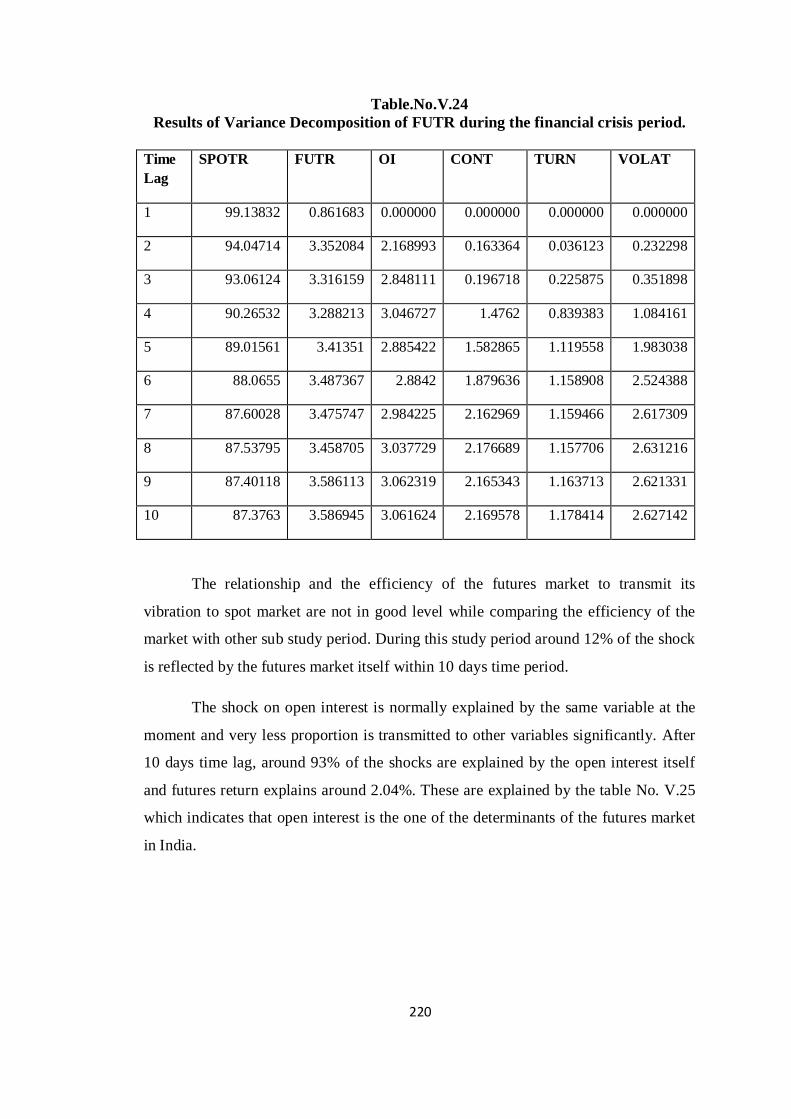

V.24 Results of Variance Decomposition of FUTR during the Financial

Crisis Period.............................................................................................

220

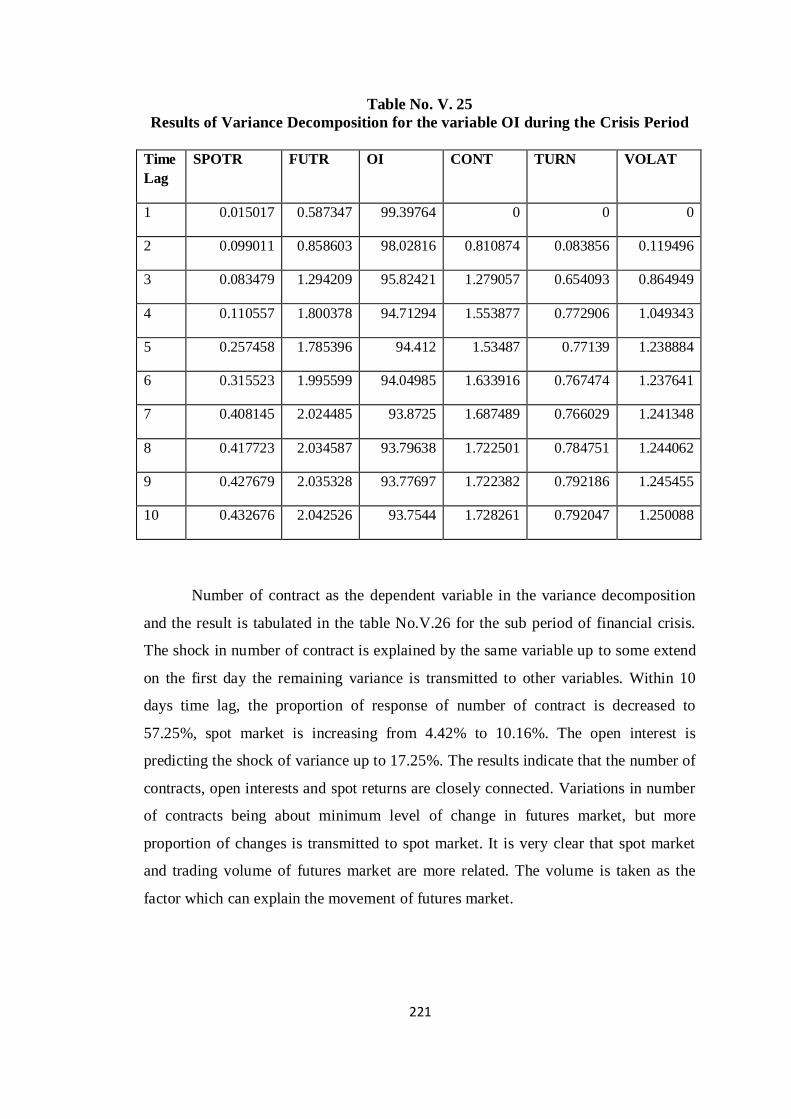

V.25 Results of Variance Decomposition for the variable OI during the

Crisis Peirod.............................................................................................

221

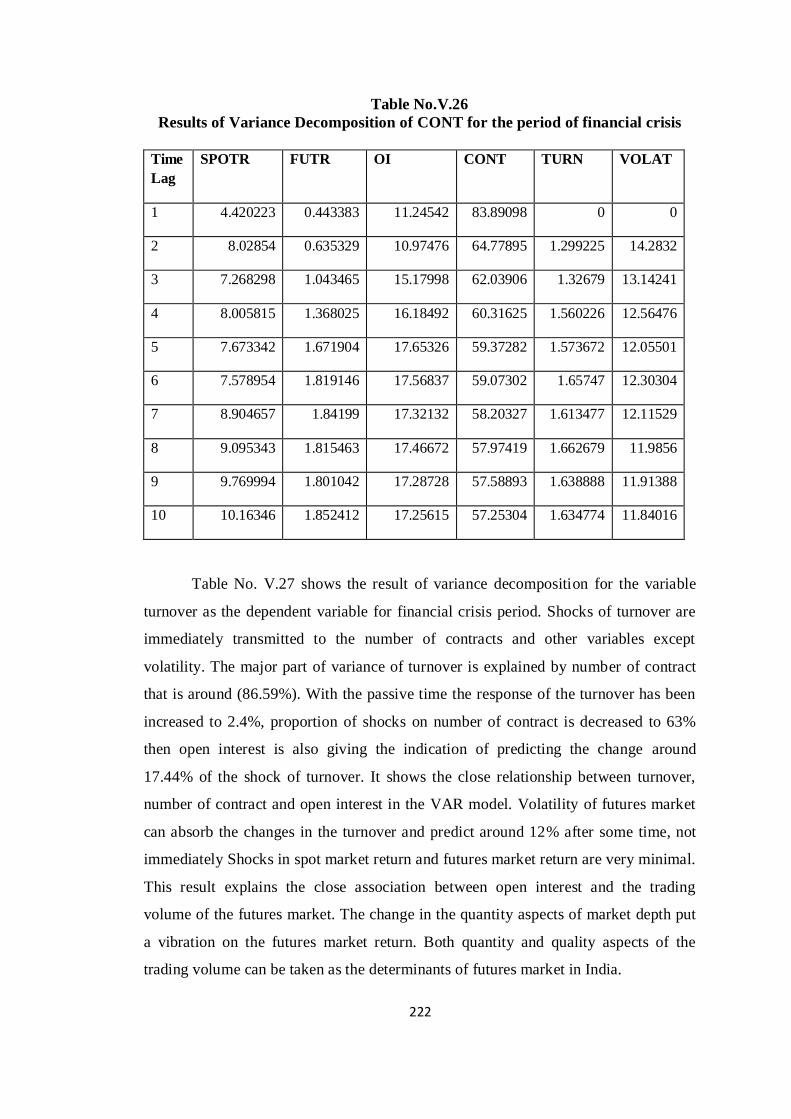

V.26 Resultsof Variance Decomposition of CONT for the Period of

Financial Crisis.........................................................................................

222

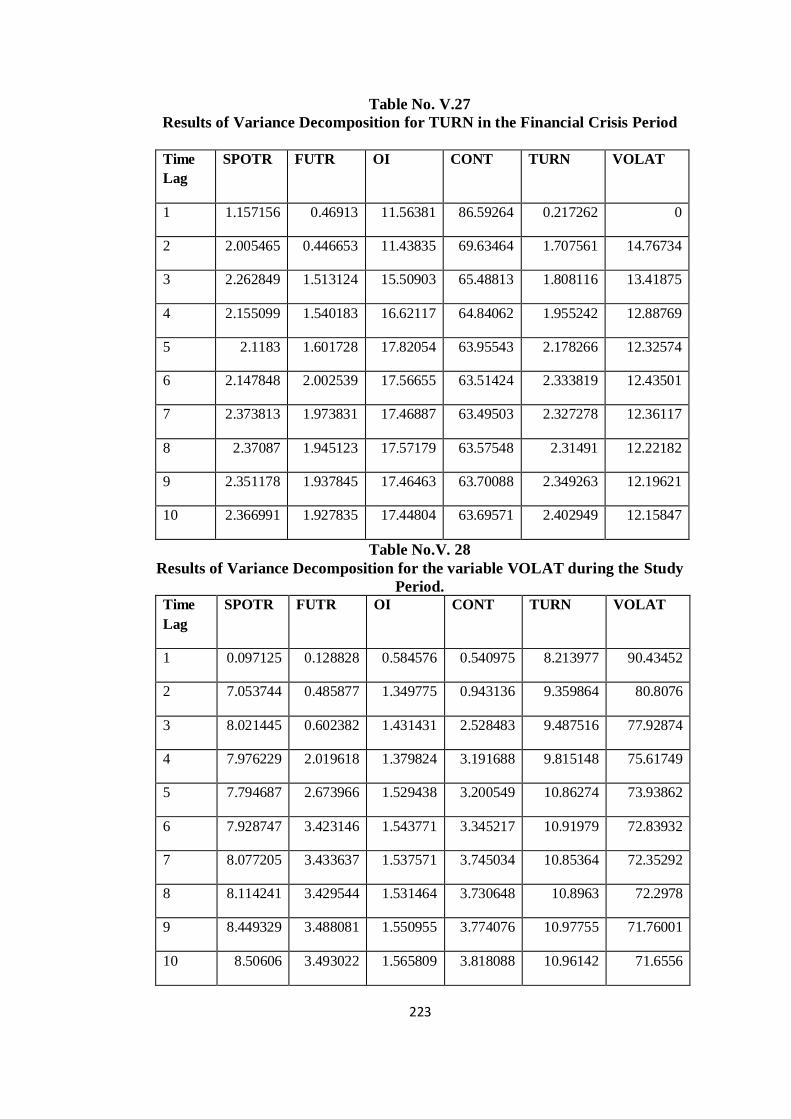

14

V.27 Results of Variance Decomposition for TURN in the Financial Crisis

Period.......................................................................................................

223

V.28 Results of Variance Decomposition for the variable VOLAT during

the Study Period.......................................................................................

223

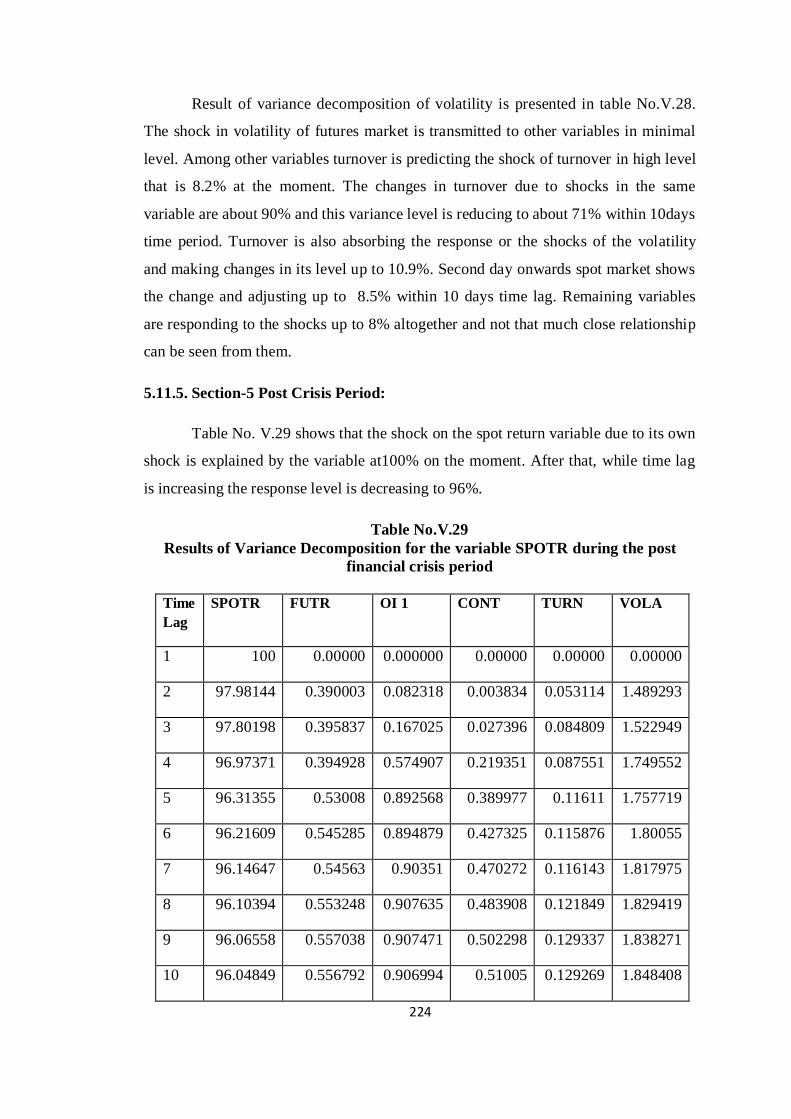

V.29 Results of Variance Decomposition for the variable SPOTR during the

Post Financial Crisis Period......................................................................

224

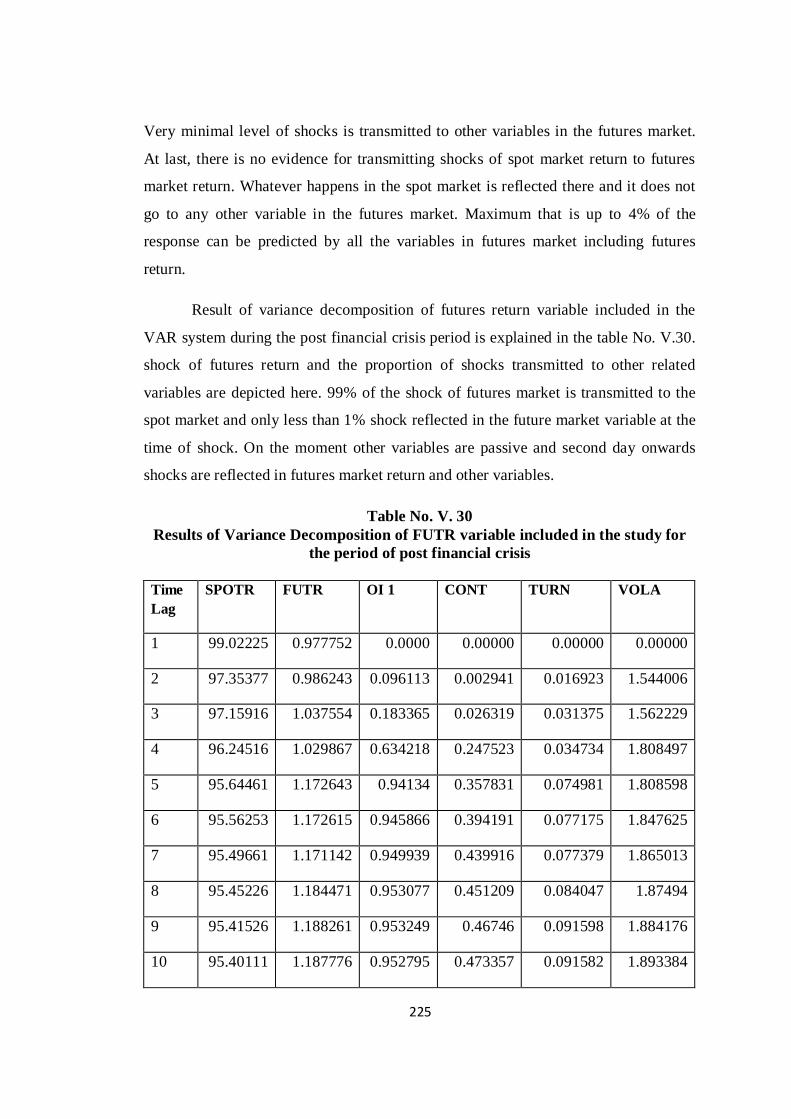

V.30 Results of Variance Decomposition of FUTR variable included in the

Study for the Period of Post Financial Crisis...........................................

225

V.31 Resutls of Variance decomposition for OI 1 during the Post Financial

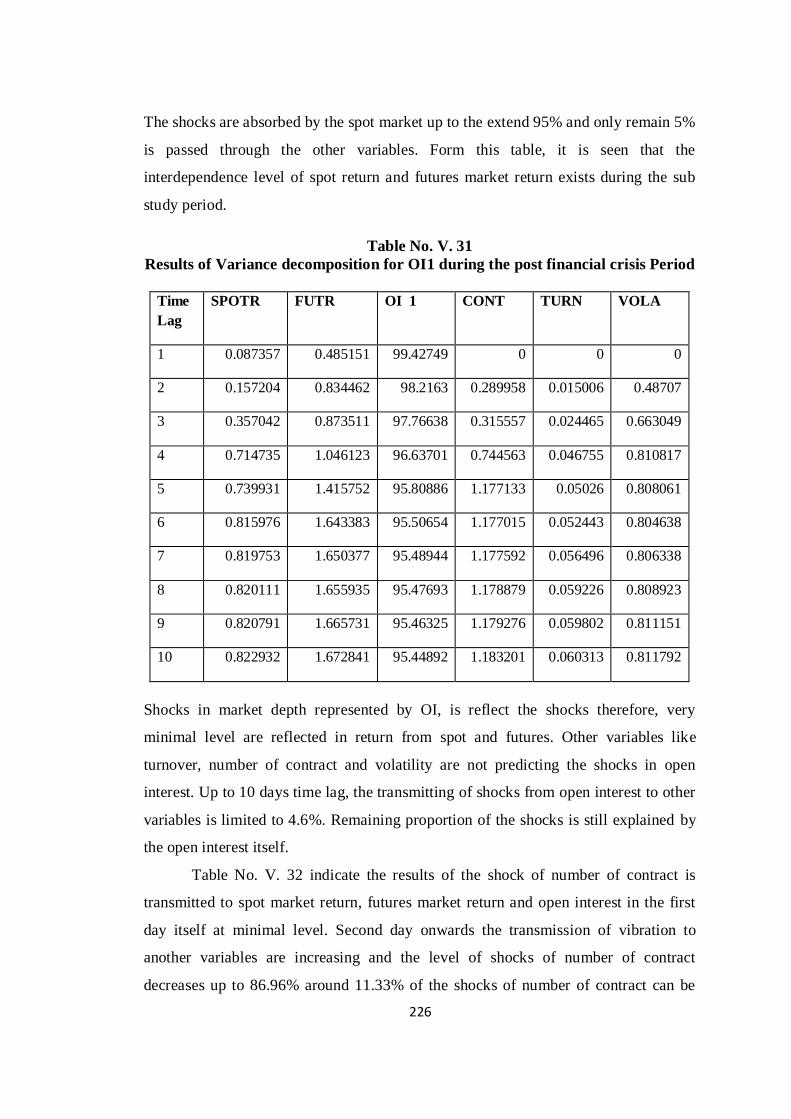

Crisis Period.............................................................................................

226

V.32 Results of Variance decomposition of the variabel CONT in the Post

Financial crisis peiod................................................................................

227

V.33 Results of Variance Decompositionfor the variabel TURN in the Post

Crisis Period............................................................................................

228

V.34 Results of Variance Decomposition for the variable VOLA during the

Post Crisis Period......................................................................................

228

VI.1 List of Individual Stock included in the sample of the Study.................. 236

VI.2 Summary Statistics of the Variables of Nifty and Sample Companies

included for the Whole Study Period........................................................

239

VI.3 Results of Stationarity Tests of the variables included in the Study........ 246

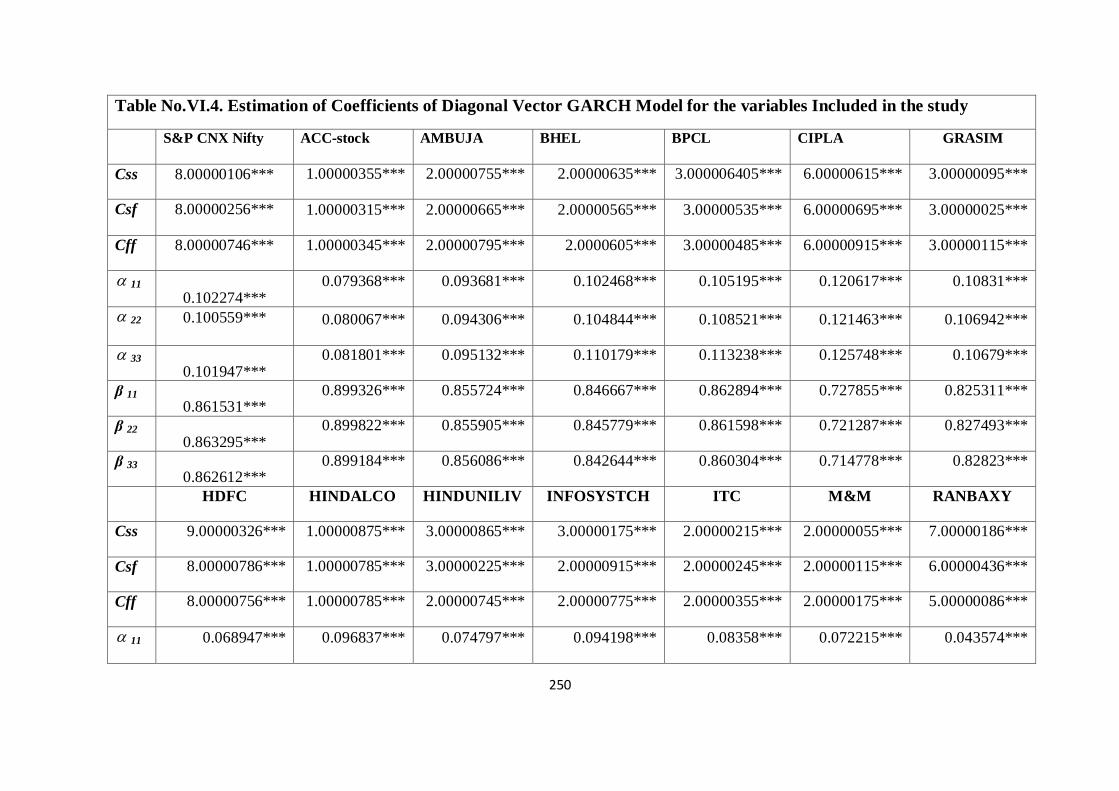

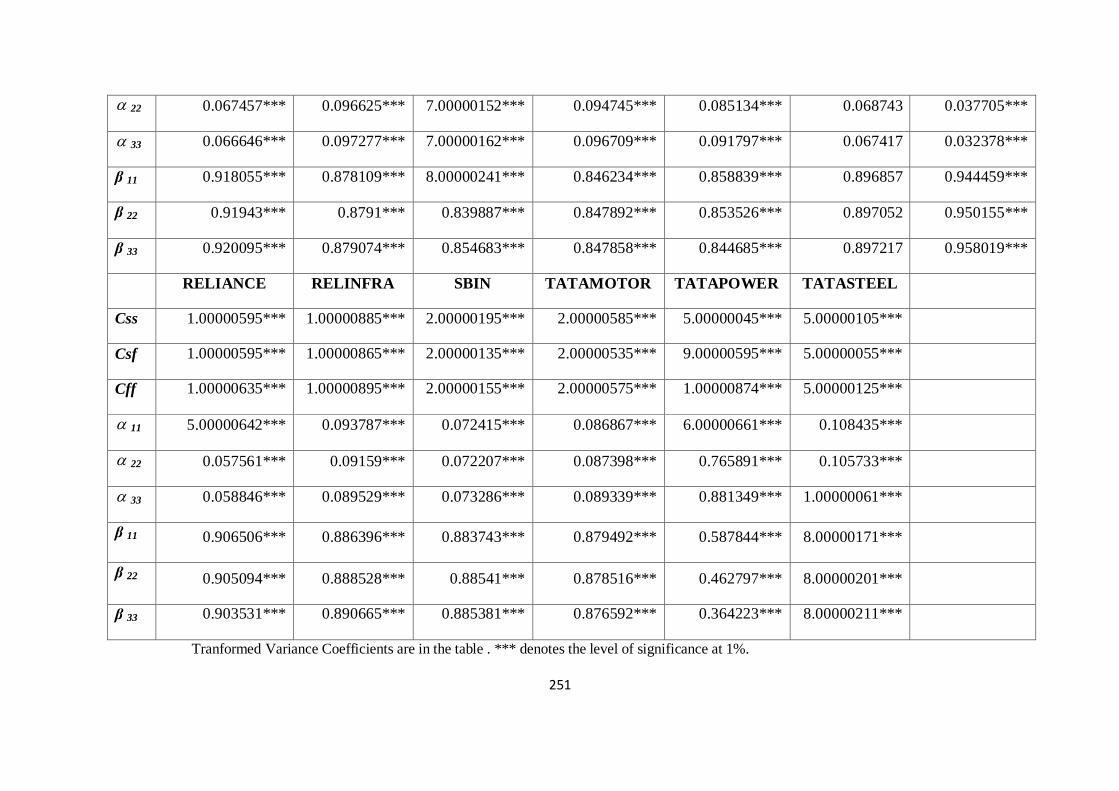

VI.4 Estimation of Coefficients of Diagonal Vector GARCH Model for the

variables included in the Study................................................................

250

VI.5 Optimal Hedge Ratio by using Diagonal VECH-GARCH Model for the

Study Period.............................................................................................

253

15

LIST OF FIGURES

Figure

No.

Title Page

No.

I.1 Line Graphs .............................................................................. 41

I.2 Average Closing Index.................................................................... 42

IV.1 Line graphs of spot and futures price series during different study

period..................................................................................................

145

V.1 Line graphs of the variables included in the study during different

periods. .............................................................................................

175

V.2 Results of Impulse Response for Futures Market for the Whole

Study Period Respose to generalized one S.D innovations...............

189

V.3 Graphical Presentation of Impulse Response for Futures Market in

the Development Period Respose to generalized one S.D

innovations.............

192

V.4 Graphical Presentation of Impulse Response for Futures Market

during Pre Financial Crisis Period.Respose to generalized one S.D

innovations......................................................................................

195

V.5 Graphical Presentation of Impulse Response for Futures Market

for Financial Crisis Period.Respose to generalized one S.D

innovations.....

198

V.6 Results of Impulse Response for Futures market during the Post

Crisis Period. Response to generalized one S.D. innovations.

201

VI.1 Line Graphs of the variables included in the study period........... 241

16

ABBREVIATIONS

S&P Standard and Poor

ARMA Autoregressive Moving Average

FTSE Index of London Stock Exchange

NYSE New York Stock Exchange

VAR Vector Auto Regressive

GARCH Generalized Auto Regressive Conditional Heteroskedastisity

NASDAQ National Association of Securities Dealers Automated

Quotations

E-GARCH Exponential Generalized Auto Regressive Conditional

Heteroskedastisity

NSE National Stock Exchange

BSE Bombay Stock Exchange

OLS Ordinary Least Square

ISE International Security Exchange

WPC Weighted Period Contribution

TAIFEX Taiwan Futures Exchange

ARCH Autoregressive conditional heteroskedasticity

TDEX Texas Data Exchange

ARDL Auto Regressive Distribution Lag

DCC-GARCH Dynamic Conditional Correlation Generalized Auto Regresive

Conditional Heteroskedastisity

IGARCH Integrated Generalized Autoregressive Conditional

Heteroskedasticity

GJR Glosten-Jagannathan-Runkle GARCH

APARCH The Asymmetric Power Autoregressive conditional

Heteroskedasticity

EC Error Correction

VECM Vector Error Correction model

HSIF Hang Seng Index Futures

HSFI Hang Seng Finance Index

RSGC Regime Switching Gambel-Clayton

17

ADF Augmented Dickey Fuller Test

LPM lower partial moment

SWARCH Switching Autoregressive conditional heteroskedasticity

FUTR Futures Return

VOL Volatility

OI Open Interest

TURN Turnover

CONT Number of Contract

SPOTR Spot return

LR Likelihood Ratio

FPE Final Prediction Error

AIC Akaika Information Criterion

FUT Futures Index

SPOT Spot Index

PP Philip Perron Test

SC Schwarz information criterion

HQ Hannan-Quinn information criterion

ACC The Associated Cement Companies Limited

BPCL Bharat Petroleum Corporation Limited

CIPLA Cipla Limited

BHEL Bharat Heavy Electricals Limited

ITC ITC Limited

M&M Mahindra & Mahindra Limited

SBIN State Bank of India Limited

HDFC Housing Development Finance Corporation Limited

RELINFRA Reliance Infrastructure Ltd

18

Chapter -I

Introduction

19

CHAPTER –I

INTRODUCTION

1.1. PREAMBLE

Investment is a vital part of the basic behavior of civilized society. In the

financial environment, investment is essentially the process of depositing the money

with the dual objective of having regular income and capital appreciation. Stock

market satisfies both the objectives very systematically and effectively. Regular

income from the perspective of dividend or interest and capital appreciation is the

price changes in the basic value of the shares. Investors are of different types like risk

lovers and risk evaders. Risk evaders do not like to be active in the market and they

are willing to wait to get high return from their minimal investment money after a

long period. Risk lovers are the real players in the stock market. They expect more

return with low risk. Portfolio construction is one of the strategies to make more profit

and to reduce the risk. The beginning of derivatives would be traced from a distant

past when investors in foreign nation especially Europe, US and some developed

Asian nations started to think about alternative ways to make more profit from the

existing investments.

Derivatives are the contracts or assets whose values are changed on the basis

of the changes in the underlying assets. Primarily derivatives markets are identified

for price discovery, arbitrage and risk protection or risk reduction. There are many

products such as futures, options and swaps in the derivatives markets. Among these

products futures are more popular in India. Futures market is the market which

basically depends on the spot market. Theoretically, both the spot and futures market

must move together and adjust or respond to the information and events in a similar

manner. Ideally there is perfect relationship between spot and futures markets. It is

paradoxical that, in practice such close relationship is not evident in Indian spot and

futures markets as per researches done. It is interesting to note that most of the time

futures markets lead the spot market and very rarely spot market leads futures

markets. Literature indicates that futures market is leading the spot market because of

20

high trading volume, multiple trading patterns, less transaction cost, high leverage and

less restriction in short sales.

1.2. RISK MANAGEMENT

Risk is the inherited element of investment and the complementary aspects of

return. People like or dislike risk, it cannot be avoided from the investment process

due to the positive relationship with them. While risk increases return is also

increasing and risk reduction indicates the trend of decrease in return. Investors

always make strategies to get maximum return from minimum level of risk. It makes

the investment process interesting. There are many ways to reduce risk and make

maximum return. Investment portfolio and hedging strategies are so popular among

the risk reduction strategies.

Derivatives are the tool which has been introduced with an aim of enhancing

price discovery, arbitrage and hedging process. Risk of the spot market can be

managed through the hedging process in futures market. Hedgers are the one of the

participants in the derivatives market. Managing or controlling risk is the aim of these

traders in spot and futures market. In order to reduce the risk the traders offset their

investment in the opposite investment strategy. The traders who hedge their

investment by taking opposite position of spot in the futures market are known as

hedgers. In other words, making an investment to reduce the risk of adverse price

movements in an asset is the process of hedging. A hedge consists of taking an

offsetting position in a related security like futures contract. Investors use hedging

strategy when they are unsure of what the market will do. A perfect hedge reduces the

investment risk to nothing. It is important to note that if both markets are integrated

then there is a chance of hedging. According to the empirical result of the studies,

Indian spot market and future market are integrated, hence there is a possibility of

hedging between Indian spot and futures markets.

1.3. DERIVATIVES

The derivatives were in practice in post-1970 period due to growing instability

in the financial markets. These products are initially drawn as hedging devices against

fluctuations in commodity prices and linked product. Derivative is a product or

contract which does not have any value on its own that means, it derives its value

21

from some underlying products. Derivatives base may be an asset, or an index, or

even a phenomenon. They do not have an independent existence of their own. In

recent years, derivatives products become very popular and the emergence of the

market for derivative products like forwards, futures, options and swaps can be taken

as to the willingness of risk-averse economic agents to guard themselves against

uncertainties which are arising out of fluctuations in asset prices. The financial

markets are underlined by high degree of volatility.

A common fact to use derivatives is to manage or control the risk of the

financial operation but speculators and arbitrageurs can seek profits from general

price changes or simultaneous price variations in different markets. In the case of

equity derivatives, options and futures on stock indices have gained much popularity

than on individual stocks, especially among institutional investors who are major

users of index-linked derivatives. By using derivative products, it is possible to

transfer price risks fully or partially through blocking in assets prices. The financial

derivatives have been grown up due to the different factors such as high volatility of

assets prices in financial markets, increased integration of national and international

financial markets, development and use of more sophisticated risk management tools,

availability of many choices of risk management strategies and innovations in the

derivatives markets.

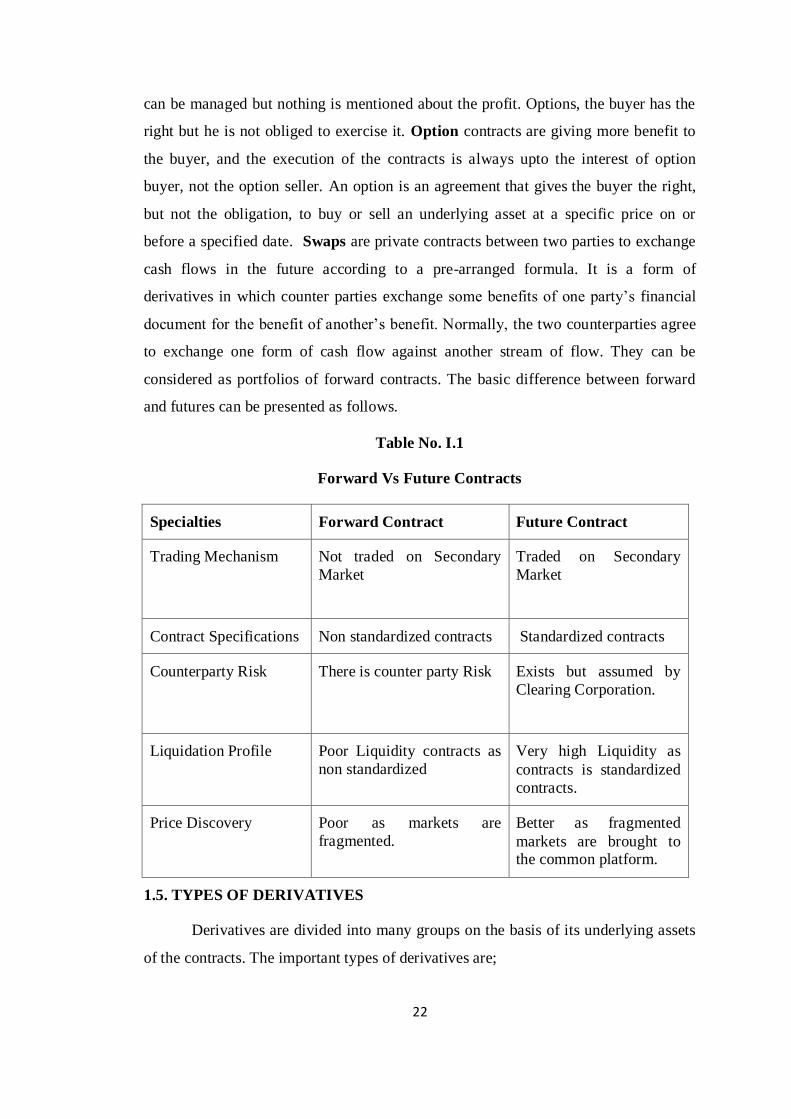

1.4. FORMS OF DERIVATIVES

Normally derivatives contracts are classified on the basis of its privilege and

right which are handled by the parties of contracts. Derivatives are the contracts on

the basis of underlying assets and their values are varied due to the change in the

value of underlying assets. These contracts are made with some privileges either to

the buyer or to the seller and these contracts are authorized or not, how these are

framed, are the basis to be considered to form the derivatives. There are mainly four

forms of derivatives such as forward, futures, options and swaps. Forward is the

basis of derivatives which contains a promise between two parties to buy or sell their

assets on a particular date with the agreed price. It is not authorized and there is no

guarantee for the execution. The same form of contract is done within the authorized

agency like stock exchanges is known as futures. In simple word, futures are the

standardized form of forward contract. Here only one side is protected that is risk and

22

can be managed but nothing is mentioned about the profit. Options, the buyer has the

right but he is not obliged to exercise it. Option contracts are giving more benefit to

the buyer, and the execution of the contracts is always upto the interest of option

buyer, not the option seller. An option is an agreement that gives the buyer the right,

but not the obligation, to buy or sell an underlying asset at a specific price on or

before a specified date. Swaps are private contracts between two parties to exchange

cash flows in the future according to a pre-arranged formula. It is a form of

derivatives in which counter parties exchange some benefits of one party’s financial

document for the benefit of another’s benefit. Normally, the two counterparties agree

to exchange one form of cash flow against another stream of flow. They can be

considered as portfolios of forward contracts. The basic difference between forward

and futures can be presented as follows.

Table No. I.1

Forward Vs Future Contracts

Specialties Forward Contract Future Contract

Trading Mechanism Not traded on Secondary

Market

Traded on Secondary

Market

Contract Specifications Non standardized contracts Standardized contracts

Counterparty Risk There is counter party Risk Exists but assumed by

Clearing Corporation.

Liquidation Profile Poor Liquidity contracts as

non standardized

Very high Liquidity as

contracts is standardized

contracts.

Price Discovery Poor as markets are

fragmented.

Better as fragmented

markets are brought to the common platform.

1.5. TYPES OF DERIVATIVES

Derivatives are divided into many groups on the basis of its underlying assets

of the contracts. The important types of derivatives are;

23

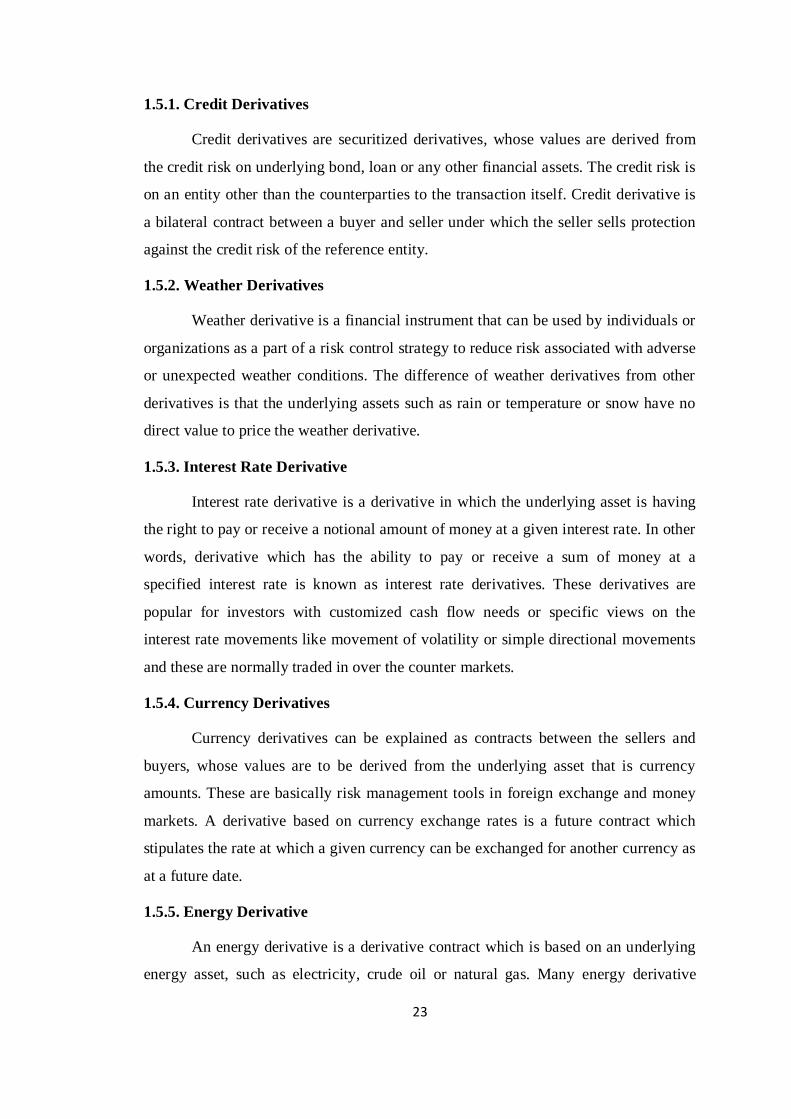

1.5.1. Credit Derivatives

Credit derivatives are securitized derivatives, whose values are derived from

the credit risk on underlying bond, loan or any other financial assets. The credit risk is

on an entity other than the counterparties to the transaction itself. Credit derivative is

a bilateral contract between a buyer and seller under which the seller sells protection

against the credit risk of the reference entity.

1.5.2. Weather Derivatives

Weather derivative is a financial instrument that can be used by individuals or

organizations as a part of a risk control strategy to reduce risk associated with adverse

or unexpected weather conditions. The difference of weather derivatives from other

derivatives is that the underlying assets such as rain or temperature or snow have no

direct value to price the weather derivative.

1.5.3. Interest Rate Derivative

Interest rate derivative is a derivative in which the underlying asset is having

the right to pay or receive a notional amount of money at a given interest rate. In other

words, derivative which has the ability to pay or receive a sum of money at a

specified interest rate is known as interest rate derivatives. These derivatives are

popular for investors with customized cash flow needs or specific views on the

interest rate movements like movement of volatility or simple directional movements

and these are normally traded in over the counter markets.

1.5.4. Currency Derivatives

Currency derivatives can be explained as contracts between the sellers and

buyers, whose values are to be derived from the underlying asset that is currency

amounts. These are basically risk management tools in foreign exchange and money

markets. A derivative based on currency exchange rates is a future contract which

stipulates the rate at which a given currency can be exchanged for another currency as

at a future date.

1.5.5. Energy Derivative

An energy derivative is a derivative contract which is based on an underlying

energy asset, such as electricity, crude oil or natural gas. Many energy derivative

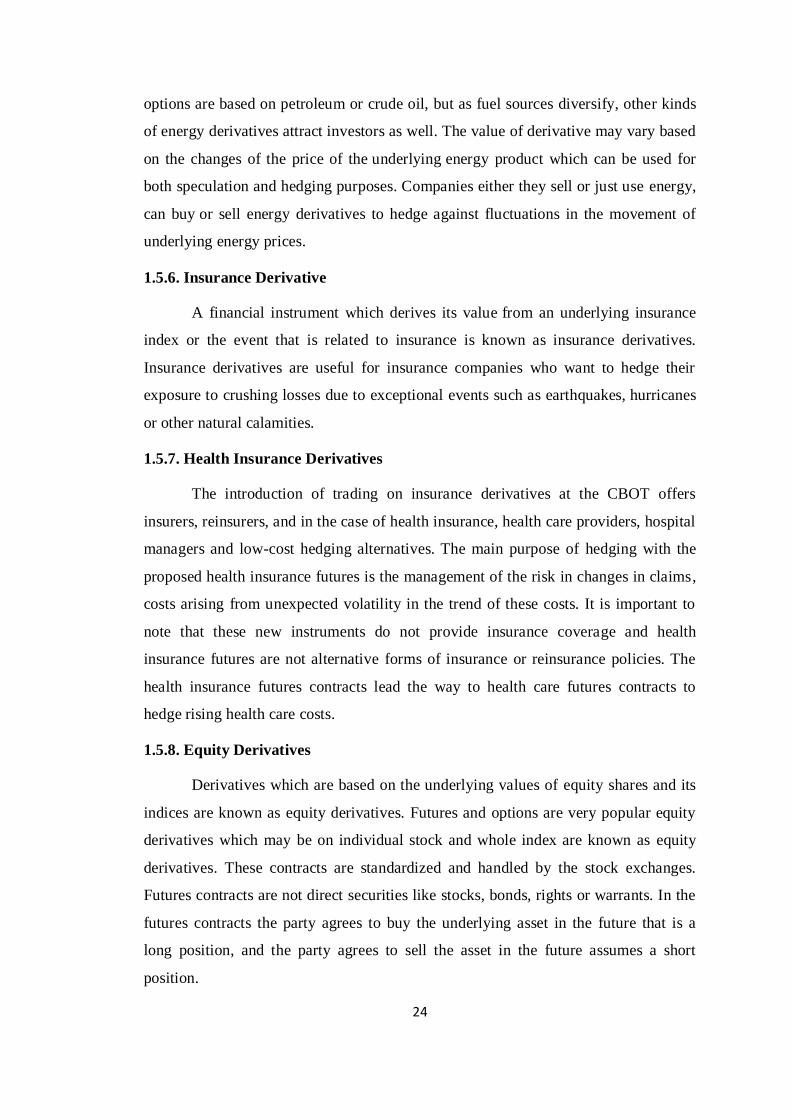

24

options are based on petroleum or crude oil, but as fuel sources diversify, other kinds

of energy derivatives attract investors as well. The value of derivative may vary based

on the changes of the price of the underlying energy product which can be used for

both speculation and hedging purposes. Companies either they sell or just use energy,

can buy or sell energy derivatives to hedge against fluctuations in the movement of

underlying energy prices.

1.5.6. Insurance Derivative

A financial instrument which derives its value from an underlying insurance

index or the event that is related to insurance is known as insurance derivatives.

Insurance derivatives are useful for insurance companies who want to hedge their

exposure to crushing losses due to exceptional events such as earthquakes, hurricanes

or other natural calamities.

1.5.7. Health Insurance Derivatives

The introduction of trading on insurance derivatives at the CBOT offers

insurers, reinsurers, and in the case of health insurance, health care providers, hospital

managers and low-cost hedging alternatives. The main purpose of hedging with the

proposed health insurance futures is the management of the risk in changes in claims,

costs arising from unexpected volatility in the trend of these costs. It is important to

note that these new instruments do not provide insurance coverage and health

insurance futures are not alternative forms of insurance or reinsurance policies. The

health insurance futures contracts lead the way to health care futures contracts to

hedge rising health care costs.

1.5.8. Equity Derivatives

Derivatives which are based on the underlying values of equity shares and its

indices are known as equity derivatives. Futures and options are very popular equity

derivatives which may be on individual stock and whole index are known as equity

derivatives. These contracts are standardized and handled by the stock exchanges.

Futures contracts are not direct securities like stocks, bonds, rights or warrants. In the

futures contracts the party agrees to buy the underlying asset in the future that is a

long position, and the party agrees to sell the asset in the future assumes a short

position.

25

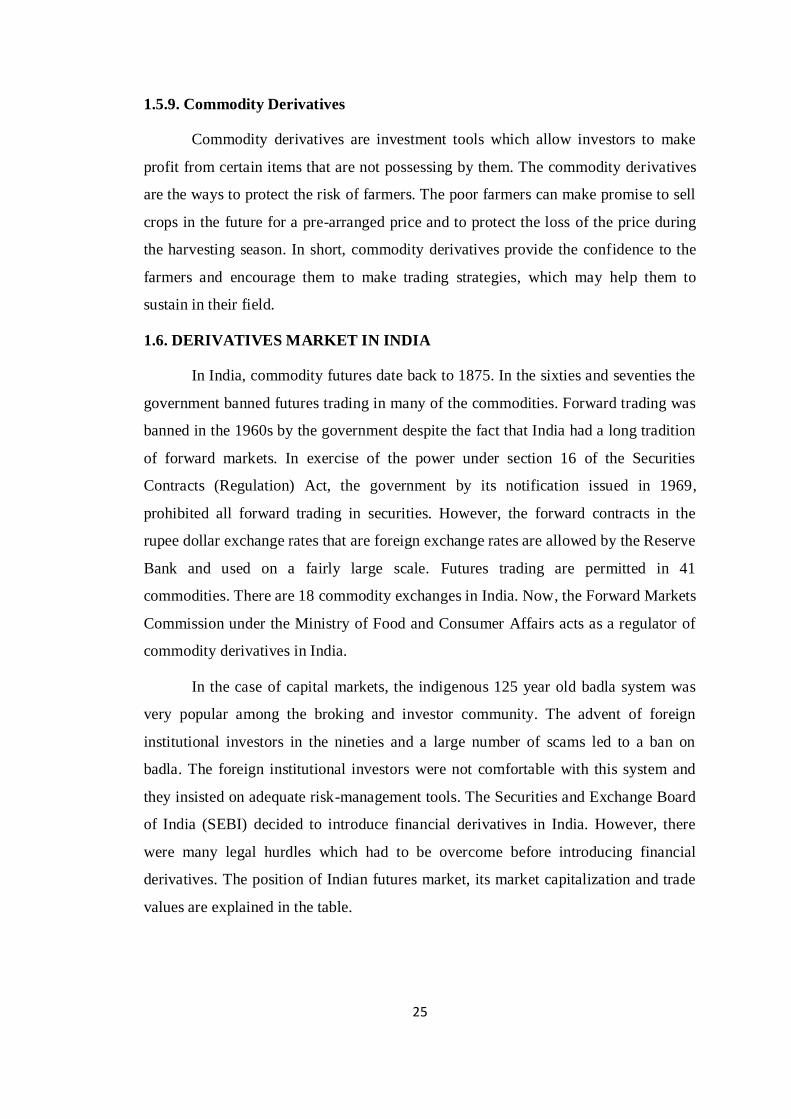

1.5.9. Commodity Derivatives

Commodity derivatives are investment tools which allow investors to make

profit from certain items that are not possessing by them. The commodity derivatives

are the ways to protect the risk of farmers. The poor farmers can make promise to sell

crops in the future for a pre-arranged price and to protect the loss of the price during

the harvesting season. In short, commodity derivatives provide the confidence to the

farmers and encourage them to make trading strategies, which may help them to

sustain in their field.

1.6. DERIVATIVES MARKET IN INDIA

In India, commodity futures date back to 1875. In the sixties and seventies the

government banned futures trading in many of the commodities. Forward trading was

banned in the 1960s by the government despite the fact that India had a long tradition

of forward markets. In exercise of the power under section 16 of the Securities

Contracts (Regulation) Act, the government by its notification issued in 1969,

prohibited all forward trading in securities. However, the forward contracts in the

rupee dollar exchange rates that are foreign exchange rates are allowed by the Reserve

Bank and used on a fairly large scale. Futures trading are permitted in 41

commodities. There are 18 commodity exchanges in India. Now, the Forward Markets

Commission under the Ministry of Food and Consumer Affairs acts as a regulator of

commodity derivatives in India.

In the case of capital markets, the indigenous 125 year old badla system was

very popular among the broking and investor community. The advent of foreign

institutional investors in the nineties and a large number of scams led to a ban on

badla. The foreign institutional investors were not comfortable with this system and

they insisted on adequate risk-management tools. The Securities and Exchange Board

of India (SEBI) decided to introduce financial derivatives in India. However, there

were many legal hurdles which had to be overcome before introducing financial

derivatives. The position of Indian futures market, its market capitalization and trade

values are explained in the table.

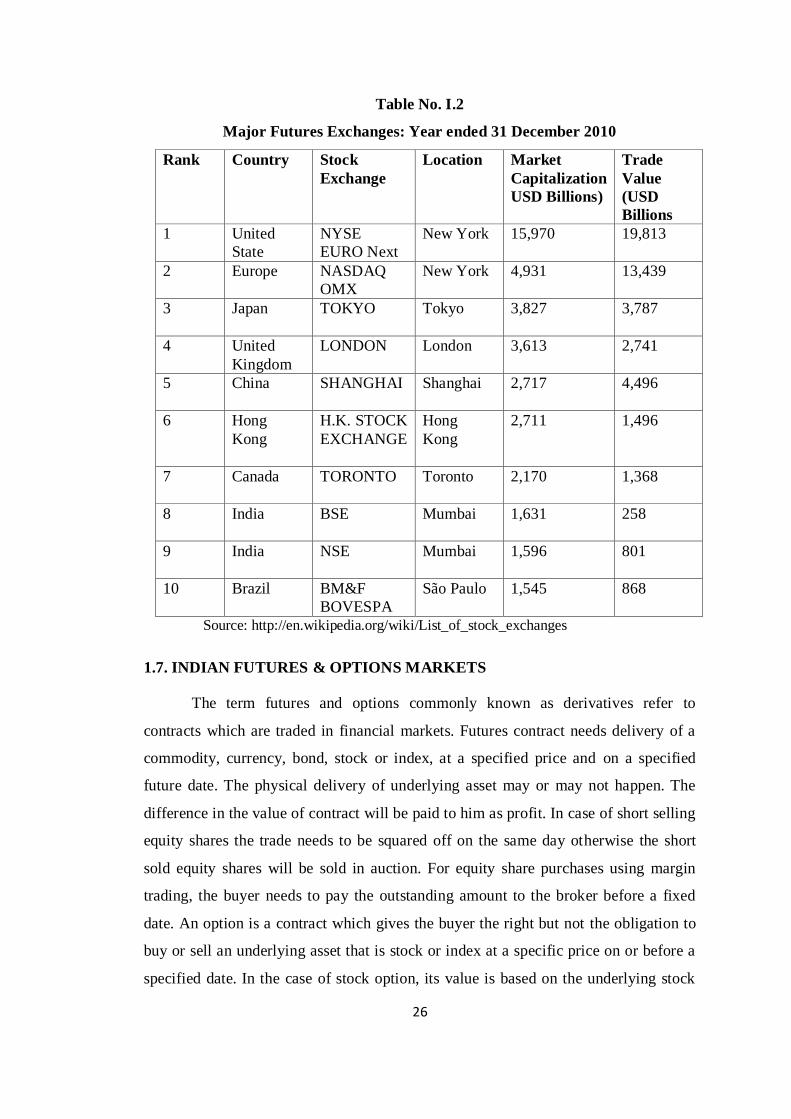

26

Table No. I.2

Major Futures Exchanges: Year ended 31 December 2010

Rank Country Stock

Exchange

Location Market

Capitalization

USD Billions)

Trade

Value

(USD

Billions

1 United

State

NYSE

EURO Next

New York 15,970 19,813

2 Europe NASDAQ

OMX

New York 4,931 13,439

3 Japan TOKYO

Tokyo 3,827 3,787

4 United

Kingdom

LONDON London 3,613 2,741

5 China SHANGHAI

Shanghai 2,717 4,496

6 Hong

Kong

H.K. STOCK

EXCHANGE

Hong

Kong

2,711 1,496

7 Canada TORONTO

Toronto 2,170 1,368

8 India BSE

Mumbai 1,631 258

9 India NSE

Mumbai 1,596 801

10 Brazil BM&F

BOVESPA

São Paulo 1,545 868

Source: http://en.wikipedia.org/wiki/List_of_stock_exchanges

1.7. INDIAN FUTURES & OPTIONS MARKETS

The term futures and options commonly known as derivatives refer to

contracts which are traded in financial markets. Futures contract needs delivery of a

commodity, currency, bond, stock or index, at a specified price and on a specified

future date. The physical delivery of underlying asset may or may not happen. The

difference in the value of contract will be paid to him as profit. In case of short selling

equity shares the trade needs to be squared off on the same day otherwise the short

sold equity shares will be sold in auction. For equity share purchases using margin

trading, the buyer needs to pay the outstanding amount to the broker before a fixed

date. An option is a contract which gives the buyer the right but not the obligation to

buy or sell an underlying asset that is stock or index at a specific price on or before a

specified date. In the case of stock option, its value is based on the underlying stock

27

and an index option the value of which is based on the underlying index. Options are

traded in the same way like stocks. They can be bought and sold just like any other

security. In case of options, the buyer pays only the premium amount and not the

value of the entire contract. The commission for the Options, however, will be based

on the value of the underlying assets. In Indian context, futures and options are very

popular among the derivatives products and it is mostly traded in Bombay Stock

Exchange and National Stock Exchange. Even though both markets are very popular,

on the basis of trade value of stock exchanges, the NSE (801USD Billion) is far better

than the BSE (258 USD Billion). On the basis of market capitalization, BSE performs

better way than the NSE as per the statistics of December 2010. On the basis of trade

value, NSE is the representative of Indian futures market.

1.8. FUTURES AND OPTIONS TRADING AT NSE

In India, at the National Stock Exchange, index futures trading were

introduced in the year 2000. Index Options trading was also made available in the

year 2001. Stock futures were introduced on 9th

Nov 2001. F&O index contracts are

available in Nifty, Junior Nifty, Bank Nifty, CNX IT and CNX 100. For individual

securities, F&O contracts are available in 223 scrips, starting from Aban Offshore to

Zee Entertainment Enterprises Limited. The contracts are traded as lots which mean a

contract will have certain fixed number of instruments. Stock futures are available for

most of the Nifty and Junior Nifty stocks. The stocks are chosen from amongst the top

500 stocks in terms of average daily market capitalization and average daily traded

value in the previous six months on a rolling basis. The market wide position limit in

the stock shall not be less than Rs.50 cores. The market wide position limit shall be

valued taking the closing prices of stocks in the underlying cash market on the date of

expiry of contract in the month.

28

Table No.I.3.

NSE futures and options monthly settlement statistics

Month

Index stock / Futures Index/ stock options

Total MTM

Settlement

Final

settlement

Premium

Settlement

Exercise

settlement

Apr-10 3295.1 83.05 794.96 105.02 4278.13

May-10 7062.3 203.46 1037.3 152.05 8455.11

Jun-10 5116.6 47.7 944.81 200.51 6309.61

Jul-10 3381.5 56.91 795.88 132.91 4367.19

Aug-10 3466.4 49.21 932.3 127.23 4575.14

Sep-10 4175.4 105 1623.1 314.46 6217.96

Oct-10 6684.6 181.99 1123.7 162.82 8153.11

Nov-10 10170 191.04 1052.9 183.16 11597.1

Dec-10 7242.4 77.04 1011.8 223.71 8554.95

Jan-11 6458 160.13 1074.2 165.35 7857.69

Feb-11 6202.9 359.05 1247 151.72 7960.66

Mar-11 4032.7 76.04 1065.5 199.97 5374.22

Apr-11 3503.7 103.6 872.7 56.18 4536.18

May11 5450.1 126.34 932 76.71 6585.15

Jul-11 4008.2 151.75 882.49 61.16 5103.6

All Figures are in Crores, Sources –NSE website

The market wide position limit of open position in terms of the number of underlying

stock on futures and option contracts on a particular underlying stock shall be 20% of

the number of shares held by non-promoters in the relevant underlying security.

1.8.1. Settlement

Settlement can be done in physical delivery or cash settlement basis and it is

the process of finalizing the contract in a closing manner. NSCCL (National

Securities Clearing Corporation Limited) is the clearing and settlement agency for all

deals executed on the Derivatives segment of NSE. It acts as legal counter-party to all

deals on futures and option segment of NSE's and guarantees settlement. A Clearing

29

Member of NSCCL has the responsibility of clearing and settlement of all deals

executed by Trading Members on NSE.

1.8.2. Final Settlement

On the expiry date of the futures contracts, the NSCCL marks all positions of

trading members to the final settlement price and the profit loss is settled in the form

of cash. The final settlement profit or loss is computed as the difference between trade

price or the previous day's settlement price and the final settlement price of the

relevant futures contract. Final settlement loss or profit amount is debited or credited

to the relevant clearing member’s bank account on T+1day formula.

1.8.3. Settlement Period

The period between the trade date and the settlement date. In other words the

number of days between the trade date and the settlement date. The trade date is the

day on which investors agree on the security transaction, while the settlement date is

the day where securities transfer from one to another and settlement is made.

Different types of transactions have different settlement periods. The month in which

the underlying assets of futures contact are delivered to the contract holder is known

as settlement month and the date on which payment is made to settle a trade that is the

date on which either cash or a security must be in the hands of the broker to satisfy the

conditions of a security transaction is the settlement date, then the risk that a trade will

not settle that is the risk that one party will deliver and the counterparty will not be

able to pay is the settlement risk. The another important term which is so close to the

term settlement is the settlement price which is the official closing price for a future

set by the clearing house at the end of each trading day. Settlement prices are used to

determine both margin calls and invoice prices for deliveries.

1.8.4. Clearing Members

Clearing Members of NSCCL has the responsibility of clearing and

settlement of all deals executed by Trading Members on NSE. Primarily the functions

like settlement and risk management are performed by the clearing members. In the

settlement function the actual settlement that is only fund settlement is performed and

the margins are settled to reduce the risk.

30

1.8.5. Clearing Bank

NSCCL has made net work of 13 clearing banks which are required to operate

and maintain clearing accounts with any of the empanelled clearing banks at the

designated clearing bank branches. The clearing accounts are to be used exclusively

for clearing & settlement operations. In the NSE trading settlement schedule, the

settlement of trades is on T+1 working day basis. Trading members with a funds pay-

in obligation are required to have clear funds in their basic clearing account on or

before 10.30 a.m. on the settlement day and after that the payout of amount is credited

to the primary clearing account of the members. Daily mark to market settlement

system is followed. The positions of the trader in the futures contracts are marked-to-

market to the daily settlement price of the futures contracts at the end of each trading

day. The profit or loss as the difference between the current and previous day closing

price is transferred into clients account or to suffer the losses. Trading members are

responsible to collect and settle the profits or loss from the trading members through

the settlement system.

1.8.6. Traders of Futures Contract

Futures traders are traditionally considered in one of two groups such as

hedgers, who have an interest in the underlying asset and are seeking to hedge out the

risk of price changes, and speculators those who seek to make a profit by predicting

market moves and opening a derivative contract related to the asset. In other words,

the investor is seeking exposure to the asset in a long futures or the opposite effect

through a short futures contract. Hedgers typically include producers and consumers

of a commodity or the owner of an asset or assets subject to certain influences such as

an interest rate.

Both hedge and speculative notions involves a separately managed account

whose investment objective is to track the performance of a stock index. The Portfolio

manager normally manages cash inflows in an easy and cost effective manner by

investing in stock index futures. This gains the portfolio exposure to the index which

is consistent with the fund or account investment objective that without having to buy

an appropriate proportion of each of the individual in stocks. Futures market claims

social utility by providing the transfer of risk, increased liquidity and time preferences

to the traders. In real life, the actual delivery rate of the underlying goods specified in

31

futures contracts is very low, it indicates that the hedging or speculating benefits of

the contracts can be had largely without holding the contract until expiry and

delivering the goods.

1.8.7. Stock Index Futures

It is the futures which are framed on the basis of the individual stock which is

available for trading in the market. In simple term stock index future is a futures

contract on individual stock index. It is confirmed that markets in stock index futures

is the baskets of securities which provide an apt trading medium for uniformed

liquidity traders who wish to trade portfolios in the market. This future can be used to

speculate on the future direction of the stock market or to hedge a portfolio of

securities against normal market movements.

1.8.8. Stock Index Futures Contract

These are contracts which are traded in terms of number of contracts in the

futures markets. It is a standardized contract which is traded on a futures exchange in

the form of buying or selling a certain underlying instrument at a certain date in the

future, at a specified agreed price.

1.8.9. Volatility

The measure in the change of price on a financial instrument over time is

known as volatility. It explains the amount of uncertainty or risk about the size of

variations in an asset’s value. Normally volatility is expressed in yearly terms which

can either be measured by using the statistical measures like standard deviation or

variance between returns from that same security or market index. A higher volatility

indicates that an asset’s value can potentially be varied over a larger range of values,

in other words, the price of the assets can change dramatically over a short period in

either direction. Beta is one of the measures of relative volatility of a specific asset to

the market. Volatility can be estimated by the annualized standard deviation of daily

change in price and the price moves up and down rapidly over short time periods, it is

said that high volume of volatility.

1.8.10. Futures Margin

A margin is posted by the trader to minimize credit risk to the stock exchange.

Normally 5-15% of the value of contract is the margin of the futures contracts. To

32

minimize counterparty risk to traders, trades executed on regulated futures exchanges

which are guaranteed by clearing houses. The clearing house becomes the buyer to

each seller, and the seller to each buyer, so that in the event of a counterparty default

the clearer assumes the risk of loss.

There are different types of margins such as Clearing Margin which are

distinct from customer margins that individual buyers and sellers of futures and

options contracts are required to deposit with brokers, Customer Margin for which

Futures Commission Merchants are responsible for overseeing customer margin

accounts. This margin is determined on the basis of market risk and contract value,

Initial Margin which is calculated on the basis of maximum estimated change in

contract value within a trading day. Initial margin is set by the exchange. If a position

involves an exchange-traded product, the amount or percentage of initial margin is set

by the exchange concerned, Maintenance Margin which is set of minimum margin

per outstanding futures contract that a customer must maintain in his margin account,

Margin-Equity Ratio that is a term used by speculators those who are representing

the amount of their trading capital that is being held as margin at any particular time.

The low margin requirements of futures results in substantial leverage of the

investment. However, the exchanges require a minimum amount that varies

depending on the contract and the trader. The broker may set the requirement higher,

but may not set it lower, Performance Bond Margin in which the amount of money

deposited by both a buyer and seller of a futures contract or an options seller to ensure

performance of the term of the contract and finally Return on Margin which is often

used to judge performance, because it represents the gain or loss compared to the

exchange’s perceived risk as reflected in required margin.

1.8.11. Pricing of Futures Contracts

The price of a futures contract is determined through arbitrage process if the

underlying asset is in supply. This is normally for stock index futures, index futures,

treasury bond futures and futures on physical commodities. When the deliverable

commodity does not exist the futures price cannot be fixed by arbitrage and there is

only one force which is simple supply and demand for the asset in the future to set the

price during this time.

33

The forward price contains the expected future value of the underlying

discounted at the risk free rate. The value of the future F(t), will be found by

compounding the present value S(t) at time t to maturity T by the rate of risk-free

return. When the deliverable commodity is not in plentiful supply, rational pricing

cannot be applied. The price of the futures is determined by today's supply and

demand for the underlying asset in the futures. In a deep and liquid market, supply

and demand would be expected to balance out at a price which represents an unbiased

expectation of the future price of the actual asset and so be given by the simple

relationship.

1.9. FACTORS INFLUENCING THE PRICE OF FUTURES

The prices of index futures and on individual shares generally follow the price

development in the underlying asset. The difference in the price between the

underlying asset and the future, also called the basis, is fundamentally determined by

the current supply and demand in the future. Arbitrage between the equity market and

futures market will, however, ensure that price effects from the market expectations

are adjusted so that the basis essentially reflects the money market rate. The futures

price is determined by many factors such as the market price of the underlying asset ,

the money market rate and expected dividend on the underlying asset during the life

of the future supply or demand, movement of futures market and the other aspects of

futures market like number of contract and trade volume of futures contract. A

theoretical price of an index future may be decided based on the reasoning that the

index future serves as a substitute for a share portfolio that is based on the index

constituents. Regardless of the choice of investment the investor will achieve a capital

gain or a capital loss.

The holder of a futures contract will not receive any dividend payments from

the shares in the portfolio but equally he does not have to tie up funds in the shares as

the shareholder. The holder of a futures contract may thus achieve a payoff by using

the excess liquidity elsewhere in the money market. Since the size of this difference in

investment return is time sensitive, the difference between the futures price and the

index value will narrow towards futures expiry date and will be eliminated at expiry.

Returns in the form of dividend payments are relatively limited, and historically they

have underperformed the money market rate, which is why index futures are generally

34

priced higher than the index value. The pricing of futures on individual shares follows

the same principles as for index futures for buying the share. The buyer of a future

therefore does not tie up liquidity in the share, but does not receive dividends. The

price of a future on an individual share will generally be higher than the price of the

underlying share. The expected dividend on a single share may influence the price of

the future at the time when dividend is actually paid, by which the price of the share is

higher than the price of the future.

1.10. RELATIONSHIP BETWEEN SPOT AND FUTURES MARKETS

The relationship of the spot and futures markets is the basic element of price

discovery process. The price discovery process is the process of determining the price

of an asset in the marketplace through the interactions of buyers and sellers. In other

words it is a method of determining the price for a specific commodity or

security through basic supply and demand factors related to the market. The price

discovery takes place continuously in the modern and dynamic market. The price will

sometimes fall below the duration average and sometimes exceed the average as a

result of the noise due to uncertainties. Price discovery involves number of buyers and

sellers, market mechanism, information about the markets and risk management

mechanism. Actually, price discovery helps to find the exact price for a commodity or

a share of a company. The price discovery is used in speculative markets which help

the traders, manufacturers, exporters, farmers, refineries, governments, consumers,

and speculators.

Price discovery process begins to favor the more competitive markets, leaving

attractive trading exchanges with fewer participants and effectively redundant in price

determination. Price discovery predominantly originates in the local markets. It

originates primarily from the stock exchanges. Many research works suggested that a

lead-lag relationship of up to 30 minutes from futures price to the spot price.

Fleming, Ostdick and Whaley, (1996) observed that the market with the lowest

trading cost will react more quickly to new information.

Information transmission or price discovery is an indication of the relative

market efficiencies of related assets. There are three approaches to study the price

discovery of assets such as the lead lag relationship between the price of notional

market or between different securities, examination of the role of volatility in the

35

price discovery process and to study how information is transferred among different

markets. It is argued that price discovery occurs mainly in the spot market which is

dominated by foreign and domestic institutional investors (Bohl, Salm and Schuppli,

2010). The aim of security market design is optimal price discovery, so the choice of

market structure will heavily on the best market. Increased volatility in futures prices

will have consequences for hedging, arbitrage strategies and margin requirements.

Cost of trading, combined with the nature of new information, has relationship

between futures and cash markets. Futures price may temporarily contain more

information until such information flows from futures to cash price. Price discovery

refers to the process through markets converge towards the efficiency price of the

underlying assets. At any point in time there is a flow of new information into assets

markets and market prices for the assets concerned readjusted to such new flows.

Literally, when two markets for the same assets are faced with the same

information arriving simultaneously, the two markets should react at the same time in

a similar fashion. If the two markets do not react at the same time, then one market

will lead the other. When such a lead lag relation appears in case of price adjustment,

the leading market is considered as contributing a price discovery function for that

sector. In early times, it has been observed that the spot market has a greater speed of

assimilation of new information that comes to the market and has predictive power for

the futures price movements in the underlying assets. Normally futures market

incorporates new information more quickly than the spot markets, primarily because

of their inherent high leverage and low transaction cost. Price discovery function

implies the presence of an equilibrium relation binding the two prices together. In

other words, it is said that there is common factor or an unobservable efficient price

that drives both the spot and futures prices. Another arguments in price discovery is

that the existence of long run relationship. The share of price discovery originating in

futures markets has important implication for hedgers and arbitragers. Imperfect

trading specification of the futures contracts may be responsible for the violation of

the common notion that an asset which involves zero investment will always be an

efficient price discovery vehicle. In developed markets, new information is

incorporated in too quickly. Trading halt consistently help to reduce price dispersion

and enhance the efficiency of the price discovery process. When trading is halted due

36

to significant pending news release, the efficiency of the price discovery process is

enhanced by the halt.

1.11. ROLE OF TRADE VOLUME AND MARKET DEPTH TO EXPLAIN

THE MARKET MOVEMENT

Futures market movement is closely associated with spot market movement.

The price variations and the trade volume of the both market may have high level of

role to decide the efficiency of futures and spot market. Open interest is the variable

of market depth of futures market. The outstanding number of contracts which are not

settled is an open interest and it shows the depth of the market movement.

1.11.1. Open Interest

In simple terms open Interest is the total number of futures or option contracts

that are not closed or delivered on the particular day or the number of buy market

orders before the market opens. It applies primarily to the futures market and is often

used to confirm trends and trend reversals for futures and options contracts. Open

interest measures the flow of money into the futures market. For each seller of a

futures contract there must be a buyer of that contract. Thus a seller and a buyer

combine to create only one contract. Open interest provides useful information that

should be considered while entering a contract position. If both parties in the

transaction are closing positions then the open interest decreases accordingly. If they

are in opening positions then the open interest goes up accordingly. One way to use

open interest is to look at it relation to the volume of contracts traded. When the

volume exceeds the existing open interest on a given day, this suggests that trading in

that option was exceptionally high that day. Open interest provides information to

determine whether there is unusually high or low volume for any particular contract.

It is mostly used as an indication of the strength of the market, but is not the same as

volume which is also often used as a strength indicator.

The movement of open interest with other variables can be taken as the

indicator of the futures market. An increase in open interest along with an increase in

price is confirmed an upward trend. Similarly, an increase in open interest along with

a decrease in price confirms a downward trend. In the other context, an increase or

decrease in prices while open interest remains flat or declining may indicate a

37

possible trend reversal. The relationship between the prevailing price trend and open

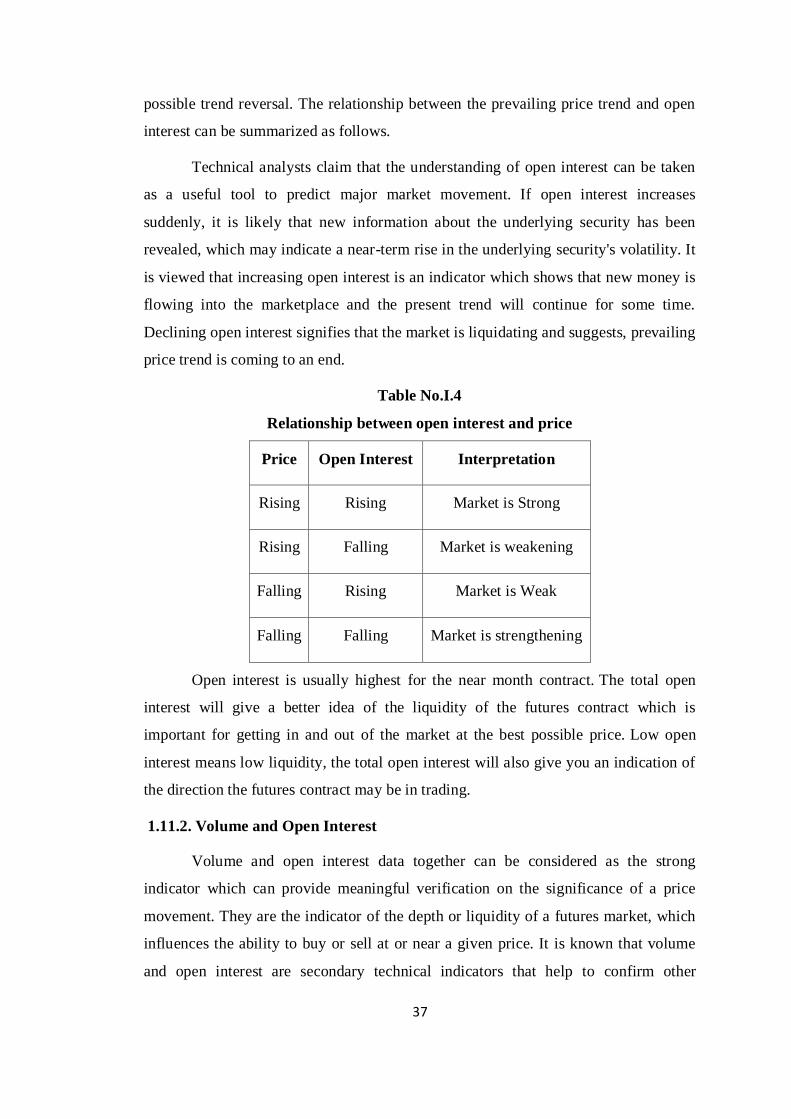

interest can be summarized as follows.

Technical analysts claim that the understanding of open interest can be taken

as a useful tool to predict major market movement. If open interest increases

suddenly, it is likely that new information about the underlying security has been

revealed, which may indicate a near-term rise in the underlying security's volatility. It

is viewed that increasing open interest is an indicator which shows that new money is

flowing into the marketplace and the present trend will continue for some time.

Declining open interest signifies that the market is liquidating and suggests, prevailing

price trend is coming to an end.

Table No.I.4

Relationship between open interest and price

Price Open Interest Interpretation

Rising Rising Market is Strong

Rising Falling Market is weakening

Falling Rising Market is Weak

Falling Falling Market is strengthening

Open interest is usually highest for the near month contract. The total open

interest will give a better idea of the liquidity of the futures contract which is

important for getting in and out of the market at the best possible price. Low open

interest means low liquidity, the total open interest will also give you an indication of

the direction the futures contract may be in trading.

1.11.2. Volume and Open Interest

Volume and open interest data together can be considered as the strong

indicator which can provide meaningful verification on the significance of a price

movement. They are the indicator of the depth or liquidity of a futures market, which

influences the ability to buy or sell at or near a given price. It is known that volume

and open interest are secondary technical indicators that help to confirm other

38

technical signals on the charts. If an upside price breakout is accompanied by heavy

volume that is a strong signal that the market may want to continue to move higher

because it indicates more traders jumped on the rising prices. A general trading rule is

that, if both volume and open interest are increasing, then the trend will probably

continue in its present direction. If volume and open interest are declining, this can be

interpreted as a signal that the current trend may be about to end.

It is utilized that three dimensional approach to market analysis which

includes a study on price, volume and open interest. Among these three elements,

price is the most important. However, volume and open interest provide important

secondary confirmation of the price action on a chart and often provide a lead

indication of an impending change of trend. Volume represents the total amount of

trading activity or contracts that have changed hands in a given commodity market for

a single trading day. The greater the amount of trading during a market session the

higher will be the trading volume. Another way to analyze these terms is that the

volume represents a measure of intensity or pressure behind a price trend. The greater

the volume, it can be expected the existing trend to continue rather than reverse. It is

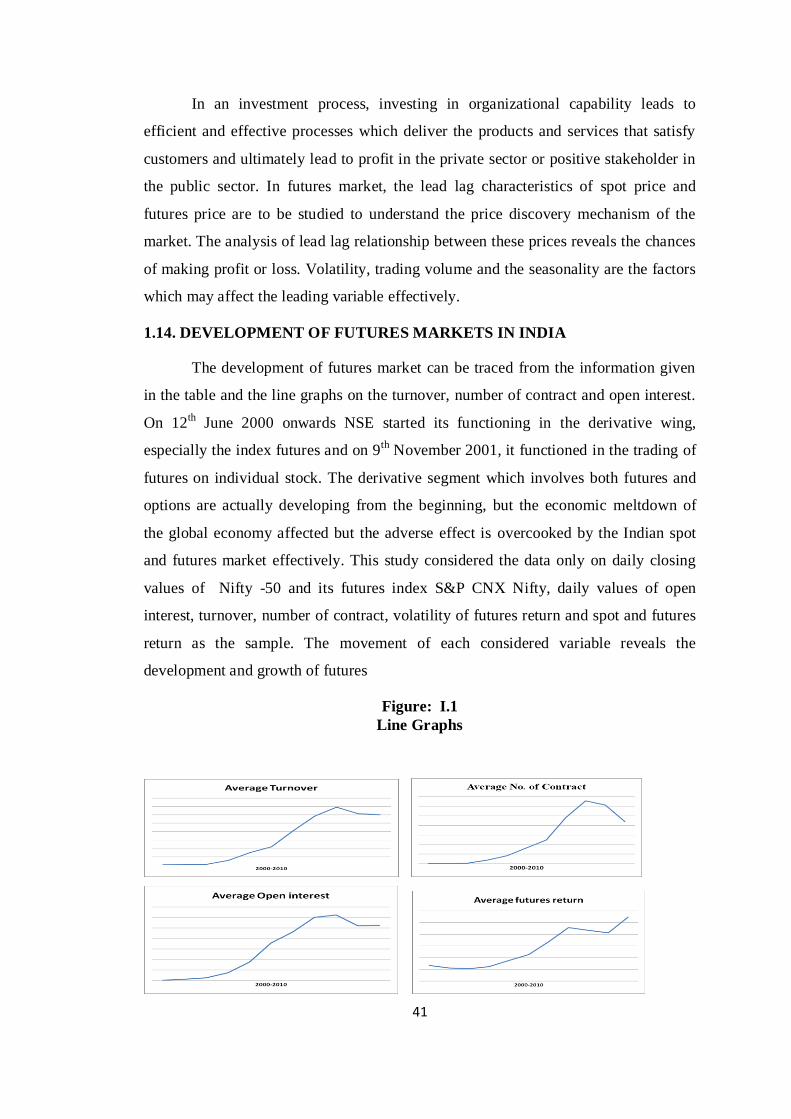

believed that volume precedes price, meaning that the loss of upside price pressure in

an uptrend or downside pressure in a downtrend will show up in the volume figures.

Where volume measures the pressure or intensity behind a price trend, open interest

measures the flow of money into the futures market. For each seller of a futures

contract there must be a buyer of that contract. Thus, a seller and a buyer combine to

create only one contract.

1.12. RISK MANAGEMENT THROUGH FUTURES

The main aim of the introduction of futures is to control and reduce risk in the

price movement. Further this can be used to manage the systemic risk, vested in the

investment in assets or securities. Increasing or decreasing the equity exposure of a

portfolio is popular with the help of Index Futures. Index funds are the funds which

imitate replicate index with an objective to generate the return equivalent to the Index.

The hedge terminology of the futures is used to reduce risk. Long hedge, short hedge,

cross hedge and the hedge ratios are the terms commonly used in the hedging process.

Derivatives can be considered a form of insurance in hedging, which is a

technique that attempts to reduce risk. They allow the risk related to the price of the

39

underlying asset to be transferred from one party to another. Hedging occurs when an

individual or institution buys an asset, such as a commodity or a bond that has coupon

payments or a stock that pays dividends and sells it using a futures contract.

Risk management strategy is applied in controlling or reducing chances of loss

from the variation in the prices of commodities, currencies, or securities. In other

words, hedging is a transfer of risk without buying insurance policies. It employs

many techniques, by taking equal and opposite positions in two different markets,

such as cash and futures markets, further it is used to protect one's capital against

effects of inflation through investing in financial instruments like bonds, shares or real

estate. Hedging is very popular in forex futures market due to the importance of

neutralizing the effect of currency fluctuations on sales income.

1.12.1. Hedge Ratio

The value of the proportion of a position that is hedged to the value of the

entire position is known as hedge ratio. It is a ratio which is comparing the value of a

position protected through a hedge with the size of the entire position itself. Hedge is

comparing the value of futures contracts purchased or sold to the value of the cash

commodity being hedged.

1.12.2. Minimum Variance Hedge Ratio

Minimum Variance Hedge Ratio is the ratio of futures contracts to a specific

spot position that minimizes the variance of the profit from the overall hedged

position and is invariant to the cost of the hedge. One problem with using futures

contracts to hedge a portfolio of spot assets is that perfect futures contracts may not

exist, so a perfect hedge cannot be achieved. A variation on the theme might go as

follows. Although there exists a futures market for an underlying asset, that futures

market is so illiquid that it is functionally useless. Thus, we need to find ways to use

sub-optimal contracts, contracts that are highly correlated with the underlying asset

and who have a similar variance. This is achieved using the minimum variance hedge

ratio. The minimum variance hedge ratio is the ratio of futures position relative to the

spot position that minimizes the variance of the position. If the spot and future

positions are perfectly correlated, then a 1:1 hedge ratio results of a perfect hedge.

The minimum variance hedge ratio can be calculated by dividing the covariance of

40

futures and spot by variance of futures. In short the minimum variance hedge ratio is

the ratio that minimizes the basic risk and it involves making a second investment

which will pay off if the first investment loses money. Hedging aims to deal with

situations where an investor predicts a company's stock will do well in relation to

rivals in the same industry. To achieve this, the investor needs to find a way of

making profit when the company does better than its rivals, but minimizing losses

when the entire industry performs badly. The solution is to hedge by buying stock in

one company, but shorting stock in rival companies. Shorting means to borrow stock,

sell it now, then buy it back and return it to the lender at a later date. This means that

the investor will profit if the stock price falls. The theory behind this form of hedging

is that if the first company does well on its own merits, the investor will make a profit.

If the entire industry does badly, the investor will have made some money by shorting

the second company, which minimizes the losses on the first company's stock. In this

context investor can make profit by making short sale in his investment.

The investor will face very low level of risk if the hedge ratio is very high. It

can be applied to any pair of investments whose performance is in some way related,

including factors such as currency exchange rates or commodity prices. The apt

method of estimating the hedge ratio may vary from situation to situation, but the