Embed Size (px)

DESCRIPTION

IDFC

Citation preview

Microsec Research

- On a restructuring mode- On a restructuring mode

Theme for growth

• Branch expansion• Capital Infusion• Restructuring the balance sheet profile

Analyst - Sanjeev JainPhone - 033-6651-2121Email Id - [email protected]

0116th April 2014

Infrastructure Development

BuyPRICE TARGET – INR148

Initiating Coverage Report

fInance company ltD.

Microsec Research02

Contents Pages

16th April 2014

Microsec Research

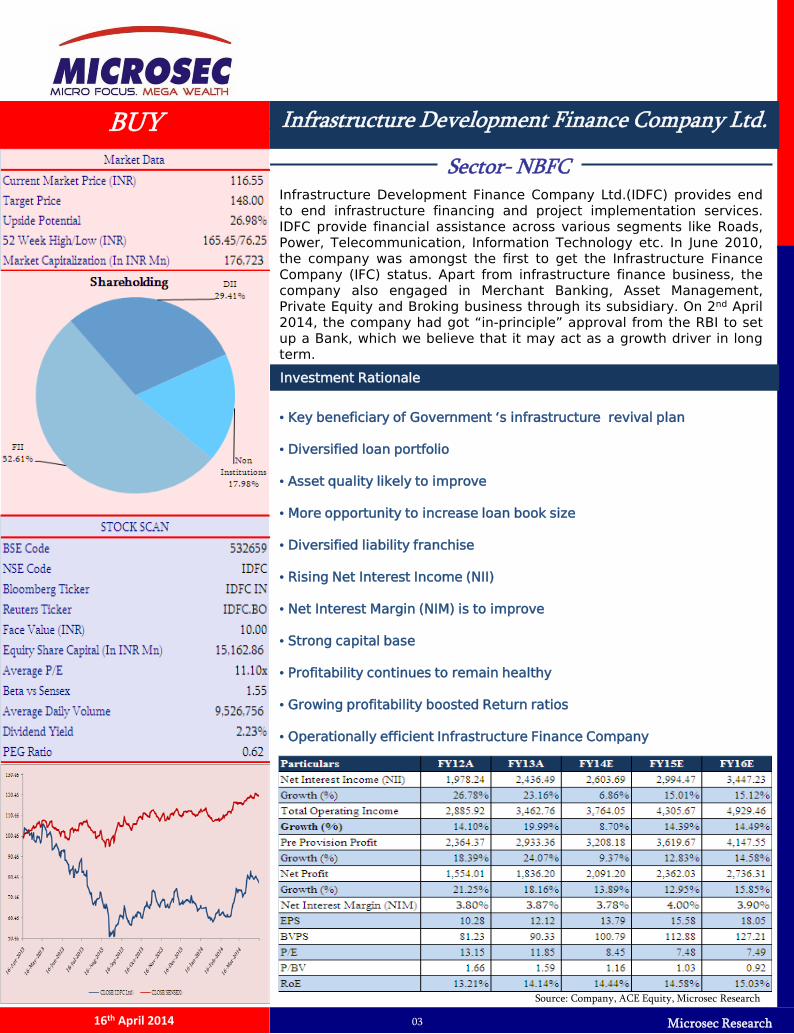

BUY Infrastructure Development Finance Company Ltd.

03

Infrastructure Development Finance Company Ltd.(IDFC) provides endto end infrastructure financing and project implementation services.IDFC provide financial assistance across various segments like Roads,Power, Telecommunication, Information Technology etc. In June 2010,the company was amongst the first to get the Infrastructure FinanceCompany (IFC) status. Apart from infrastructure finance business, thecompany also engaged in Merchant Banking, Asset Management,Private Equity and Broking business through its subsidiary. On 2nd April2014, the company had got “in-principle” approval from the RBI to setup a Bank, which we believe that it may act as a growth driver in longterm.

Sector- NBFC

Investment Rationale

• Key beneficiary of Government ‘s infrastructure revival plan

• Diversified loan portfolio

• Asset quality likely to improve

• More opportunity to increase loan book size

• Diversified liability franchise

• Rising Net Interest Income (NII)

• Net Interest Margin (NIM) is to improve

• Strong capital base

• Profitability continues to remain healthy

• Growing profitability boosted Return ratios

• Operationally efficient Infrastructure Finance Company

16th April 2014

Source: Company, ACE Equity, Microsec Research

Microsec Research04

Company Background IDFC was incorporated on January 30, 1997 on the recommendations of the ExpertGroup on Commercialization of Infrastructure Projects and was listed on the stockexchange (BSE & NSE) in August 2005. Since its inception, the company has beenproviding loan to Infrastructure projects and also engaged in the business of MerchantBanking, Asset Management, Private Equity and Broking business through its subsidiary.It is a conglomerate of 10 direct subsidiaries and 11 indirect subsidiaries. IDFCFoundation includes three Joint Ventures and two trusts. As on 31st December 2014, thecompany’s average Assets Under Management (AUM) was stood at INR52597 crores andits balance sheet crossed over INR70000 crores. The company has received manyawards and recognition over the last few years. Recently, the company had got “in-principle” approval from the RBI to set up bank, which we believe that it may act as agrowth driver in long term.

2008

2009

2005

Listed in BSE & NSE

Acquired the AMC business ofStandard Chartered Bank inIndia

Became part of Nifty 50

Classified as an Infrastructure FinanceCompany (IFC)

Entered into strategic partnership between IDFC &Natixis Global Asset Management

20112014

Got in-principle nod to set up Bank

Milestones

Source: Company, Microsec Research

16th April 2014

Microsec Research05

IDfc BusIness

structure

corporate Investment

BankIng

alternatIve asset management

puBlIc market asset

managementIDfc founDatIon

project fInance

fIxeD Income & treasury

Investment BankIng

securItIes & Investment research

prIvate equIty

Infrastructure

real estate

mutual funD

government aDvIsory &

program support servIces

polIcy aDvocacy

capItal BuIlDIng InItIatIve

communIty engagement

Source: Company, Microsec Research

16th April 2014

Microsec Research06

Board of Directors & Management

• EXECUTIVE CHAIRMANDr. Rajiv B. Lall

• MANAGING DIRECTOR & CEOVikram Limaye

• ADVISOR- PROJECT FINANCEA.K.T. Chari

• GROUP CHIEF FINANCIAL OFFICERSunil Kakar

• CHIEF RISK OFFICERSadashiv S. Rao

• MANAGING PARTNER & CEOM.K. Sinha

• MANAGING PARTNER & CIOSatish Mandhana

• VICE CHAIRMAN, IDFC MUTUAL FUNDNaval Bir Kumar

• GROUP HEAD – PROJECT FINANCE & PRINCIPAL INVESTMENTSVinayak Mavinkurve

• GROUP HEAD-PROJECT FINANCESanjay Grewal

• CEO - IDFC FOUNDATIONCherian Thomas

• GROUP HEAD- HUMAN RESOURCES & CORPORATE SERVICESAnimesh Kumar

• General Counsel and Group Head-Legal & ComplianceDr. Rajeev Uberoi

• Head - Fixed Income & TreasuryK. Rajagopal

• GROUP HEAD - NEW INITIATIVESAjay Mahajan

• Chief Operating OfficerAvtar Monga

Source: Company, Microsec Research

16th April 2014

Microsec Research

Economy Review & Outlook

07

The Indian economy is witnessing a challenging phase on the growth aspect. Thedecelerated Indian GDP growth at 4.7% in Q3FY14, clearly reflected the unfavorableenvironment of the Indian economy. A persistent high inflation which led to high interestrates has jeopardized the Indian economy which in turn affected the entire capitalintensive industry. The weakened domestic economic conditions combined with theGovernment policy paralysis have stalled a number of big infrastructure projects frombeing implemented, which has posed big challenges to the Indian Banks as well asInfrastructure finance companies. Consequently, the financial of Indian companies hasbeen affected and dented their ability to repay their loan, which has been clearlyreflected in the loan books of Indian Banks as well as NBFCs specially infrastructurefinance companies.

However, India recorded a trade deficit of 8.1 billion USD in February 2014 as comparedto 9.93 billion USD in January 2014, it was mainly, due to a sharp decline in imports ledby a fall in gold imports.

On the fiscal deficit front, the Government has targeted FY14 fiscal deficit at 4.6%. Inorder to achieve this, the Government has revised its FY14 planned expenditure downby ~(14%) to INR475532 crores, whereas, Net tax revenue collection revised down by~(5.4%) to INR836026 crores and non tax revenue collection up by ~12% to INR193226crores. However, the slower growth rate of Indian economy along with the poorperformance of Indian corporate and the vulnerable INR against major currencies haveweakened the revenue outlook for the rest of the year.

A lower fiscal deficit happens is generally good for the nation, however, it is important tosee that on what front (Revenue or Expenditure) the Government has taken the measureto do so. The current scenario, a reduction in planned expenditure may impact thebusiness growth of the Indian capital intensive industry as well as BFSI.

There is a need for a fast solution of the issue of stalled projects in which the Banks andNBFCs have a significant exposure. The new Government should focus on theinvestment front and should come out with attractive schemes like subvention oninterest rate on timely payment of loan or fast execution of projects, setting up sectorwise interest rates etc, for the respective manufacturer that may help removing thebottlenecks of the supply side. Consequently, the nation’s Current Account Deficit (CAD)and Fiscal Deficit may come down which may not only help in rupee appreciation againstthe USD but also improve the balance sheet of Indian corporate as well as Indian Banks.

Need of the hour

We believe moderate global economic recovery and the measures taken by thegovernment is likely to revive domestic growth. Inflation, Current Account Deficit (CAD)and Fiscal Deficit have shown some improvement. Indian rupee may appreciate owing tovarious steps being taken by the Government and the RBI. The steps taken for therevival of investment, including progressive infrastructure de-bottlenecking is likely toincrease capacity expansion and improve the ability of Indian companies to repay theirloan. The infrastructure finance companies as well as Banks which are better placed arelikely to generate better business and returns as the economy shows resilience of all themeasures being taken.

Outlook

16th April 2014

Microsec Research08

Weak Industrial Production

0.1%

India’s WPI Inflation

4.68%

India’s CPI Inflation

8.1%

India’s Fiscal Deficit India’s Trade Deficit

India’s GDP growth rate

16th April 2014

Microsec Research09

Government of India 10 year bond yieldINR vs. Dollar

India's Manufacturing PMI Trend

15th April 201415th April 2009

49.66

8.95

60.23

6.65

15th April 2009 15th April 2014

16th April 2014

Source: Company, Bloomberg, ADB, Microsec Research

Microsec Research

Investment Rationale

Key beneficiary of Government‘s infrastructure revival plan

10

The past couple of years has been challenging for the Indian economy. Domestic savingsand investments have plummeted and also, private investment in infrastructure hascome to a standstill. It is mainly, because of the number of headwinds from domesticand global front. Number of big infrastructure projects has been stuck due togovernment policy uncertainties. However this time round, the Government andregulator have taken number of measures to boost the economy, which is likely togenerate capacity expansion. Moreover, we believe, whichever government will comeinto power after the ongoing Lok Sabha election may try to improve the economicgrowth by boosting infrastructure sectors, which may not only improve the confidence ofthe big players but also improve the financial health of the Indian Banks and NBFCs. Thecompanies which are in better shape are likely to generate better returns. IDFCbehemoth business structure and diversified business portfolio positions it to take thestanding opportunity at that time.

During 12th five year plan, the Government has set a target of 1 trillion USD ofinvestment of large projects in infrastructure across various segments like Telecom,Roads, Power etc and expected half of which may come from private players. However,due to the global and domestic headwinds along with policy uncertainties has erodedthe confidence of private players to bet on this sector, which has affected the financial ofIndian Banks and NBFCs. However, IDFC’s strong risk management ability and wellunderstanding of emerging challenges and opportunities helped the company tomaintain its financials.

We believe, the new and stable government may try to pull out the confidence of privateplayers by coming out with the investor friendly scheme related to fast execution ofprojects and also try to fulfill the committed investment as per the 12th five year plan.Consequently, it may improve the cash flows in the sector and improve the financial ofIndian Banks and Infrastructure financing companies.

As IDFC’s has an unmatched knowledge of the sector and also, its is one of the leadinginfrastructure financing companies may reap a huge benefit going forward.

Government’s 12th Five Year Plan (2012-17) USD Billion

16th April 2014

Microsec Research11

Diversified loan portfolio

IDFC’s diversified loan portfolio makes the companies more vibrant and dynamic.Its diversified loan book helps the company to increase its risk absorptioncapacity by hedging against the risk of slowdown in specific sectors unlike itspeers REC, PFC which are focused only on power sector. IDFC’s has anunmatched knowledge and presence across the various segment like Energy,Transportation, Telecom etc, which gives the company more opportunity toexpand its business across these segments as per the performance of thesectors.

IDFC’s Diversified loan portfolio (31st December 2013)

Product wise OS disbursement as on 31st December 2013 (INR Crs.)

Source: Company, ACE Equity, Microsec Research

16th April 2014

Microsec Research12

Despite challenging environment over the past few years, wherein, the IndianBanks as well as NBFCs are suffering from asset quality problems, IDFC has beenable to improve its asset quality. In FY13, the company has reported 15 and10bps improvement in its GNPA and NNPA to 0.15% and 0.05% respectively.However, in Q3FY14, owing to the poor economic growth, the company hasreported 0.65% and 0.50% GNPA and NNPA respectively. We are not seeing anyupside in its NPA level from here back by the expectation of revival in theeconomy couple with the fast execution of stalled projects after the formation ofnew government and also the Banking business will give it opportunity to focusmore towards less riskier and retail segment . The company may improve itsGNPA and NNPA going forward. Its GNPA and NNPA may go down to 0.62% and0.45% in FY16E. The company’s strong and diversified business model and wellunderstanding of emerging challenges and opportunities couple with strong riskmanagement with in-depth analysis of borrowers’ profile may enable it toimprove its asset quality.

Asset quality likely to improve

IDFC’s asset quality trend Quarterly asset quality trend

Asset quality comparison with the company’s peer

Source: Companies, Microsec Research

16th April 2014

Microsec Research13

IDFC’s advance growth rate

As on 31st December 2013, IDFC has a leverage (Asset/Networth) of 4.59xwhich gives much room to the company to expand their loan book size and alsoimpress the credit rating agency. However, slowdown in the economy and thecompany’s conservative approach for the loan financing has lowered itsadvance growth rate. As on 31st March 2013, the company’s total advancestood at INR56618 crores, grew by 14% YoY. We anticipate 1% YoY growth inadvance for FY14E due to the company’s conservative approach and slowdownin the economy. We believe economy may start improving from the last quarterof the current financial year and also, the new and stable government may tryto boost the infrastructure sector which may help the company to expand theirloan book size. For FY16E, we anticipate ~22% YoY growth in its loan book.

More opportunity to increase loan book size

IDFC’s impressive leverage multiples

Source: Company, ACE Equity, Microsec Research

16th April 2014

Microsec Research14

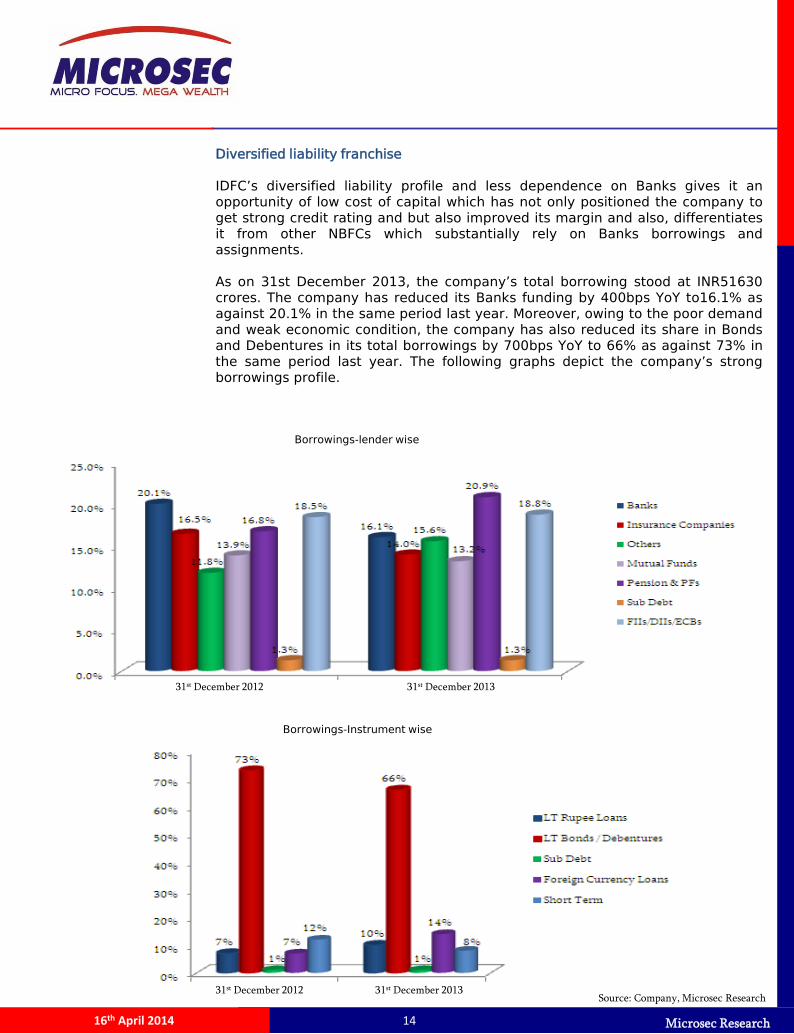

Diversified liability franchise

IDFC’s diversified liability profile and less dependence on Banks gives it anopportunity of low cost of capital which has not only positioned the company toget strong credit rating and but also improved its margin and also, differentiatesit from other NBFCs which substantially rely on Banks borrowings andassignments.

As on 31st December 2013, the company’s total borrowing stood at INR51630crores. The company has reduced its Banks funding by 400bps YoY to16.1% asagainst 20.1% in the same period last year. Moreover, owing to the poor demandand weak economic condition, the company has also reduced its share in Bondsand Debentures in its total borrowings by 700bps YoY to 66% as against 73% inthe same period last year. The following graphs depict the company’s strongborrowings profile.

Source: Company, Microsec Research31st December 2012 31st December 2013

Borrowings-lender wise

Borrowings-Instrument wise

31st December 2012 31st December 2013

16th April 2014

Microsec Research15

IDFC has consistently maintained its Net Interest Income (NII) growth rate overthe past few years. The company has reported ~25% CAGR growth in its NIIover the period of FY11-13. However, in 9MFY14, the company has reported~6% YoY growth in its NII. It was mainly, because of the slowdown in theeconomy which led to mounted pressure on the company to take conservativeapproach to give loans.

We anticipate ~15% CAGR growth of NII over the period of FY14-16. Thecompany’s strong business model, diversified funding mix and the expectationof revival in the economy going forward supported our valuation.

Rising Net Interest Income (NII)

Source: Company, Ace Equity, Microsec Research

IDFC’s NII growth trend

Interest Income/Total Assets is on the rise

16th April 2014

Microsec Research16

Net Interest Margin (NIM) is to improve

Source: Company, Ace Equity, Microsec Research

IDFC’s diversified funding mix helps it to mobilizefunds at competitive rates. Inexpensive liabilities mixhas enabled the company to maintain its NIMhealthy from the last few years. However, this timeround there is marginal pressure on company’s NIMdue to high rate of interest led by high inflation.

We believe the company’s cost of funding (whichcomprises of Pension & PFs (~21%), FIIs/DIIs/ECBs(~19%), Banks (~16%), Insurance Companies(~14%), Others (~16%) and Mutual Funds (~13%) oftotal funding mix as on December 31, 2013) is likelyto decline backed by the expectation of downsidereversal in the monetary policy cycle couple with INRappreciation against major currencies. Thecompany’s diversified loan portfolio and funding mixmay aid margin going forward. We anticipate thatcompany may maintain its margin of 3.9% over thenext couple of years.

Net Interest Margin Trend

Rolling 12 months reported Net Interest Margin trend

16th April 2014

Microsec Research17

Strong capital base

Source: Company, Ace Equity, Microsec Research

IDFC is in well position to support its growth trajectory. As on 31st December2013, its Capital Adequacy Ratio (CAR) stood at 24.80% out of which, Tier-1capital strongly stood at 22.50% which is well above the benchmark regulatoryrequirement and also it is the highest amongst its peers. The company activelymanages its capital to meet regulatory norms and current and future businessneeds considering the risks in its businesses, expectation of rating agencies,share holders and investors, and the available options of raising capital.

Well capitalized NBFC Highest CAR amongst its peers

% of Top 10 shareholders

16th April 2014

Microsec Research18

Source: Company, Microsec Research

IDFC had reported a strong growth in its Total Incomeand its profitability over the past few years. Thecompany’s Total Income has grown at a CAGR of ~17to INR3473 crores over the period of FY11-13.Whereas, Operating Profit and Profit After Tax (PAT)have grown at a CAGR of ~21% and ~20%respectively over the same period. The company’scustomised business model coupled with stable assetquality and deep understanding and strong relationwith the corporate acted as positive factors.

We anticipate ~12% and ~14% CAGR growth in itstotal income and PAT respectively over the period ofFY13-16.

Profitability continues to remain healthy

IDFC’s Total Income is on the rise

Operating Profit to grow at a CAGR of ~12% over FY13-16 Profitability to grow at a CAGR of ~14% over FY13-16

16th April 2014

Microsec Research19

In the present challenging environment, wherein, macro and micro economicenvironment led to higher stress, IDFC has managed well and kept return ratioshealthy. In December 2013, its Return on Assets (ROA) and Return on Equity(ROE) stood at 2.9% and 14.4% respectively. The company’s diversified loanportfolio which has helped it to improve its profitability and also, its activemanagement of current and future business needs considering the risks in itsbusinesses were the core reason of this achievement.

We anticipate company’s ROE and ROA of 14.58% and 3.03% for FY15E and15.03% and 2.98% for FY16E respectively. However, there may be a pressure oncompany’s ROE and ROA after starting of its banking business, which is expectedto start just after 18-20 months time frame from now.

Business size to grow at a CAGR of ~12% over FY13-16

Healthy Return Ratios

Growing profitability boosted Return ratios

Source: Company, ACE Equity. Microsec Research

16th April 2014

Microsec Research20

Cost/Income ratio

Profitability/employee (INR lakhs) is on the rise

Employee Cost/Operating Expenses is likely to stable Business/employee (INR Crs.) is on the rise

Assets/employee is on the rise (INR Crs.)

Source: Company, Ace Equity, Microsec Research

Net Profit per employee is on the rise (INR Crs.)

Operationally efficient Infrastructure Finance Company

IDFC has well managed its cost which is clearly reflectedin its Cost/Income ratio. In FY13, the company hasreported 278bps improvement in its operatingCost/Income ratio to 15.29%. We believe the company’sforay into the new banking business which is expected tostart just after 18-20 months may push up its cost. Weanticipate 15.93% and 15.86% of its Cost/Income ratiofor FY15E and FY16E respectively.

Beside this, the company’s behemoth business structure,diversified business portfolio coupled with selectiveapproach for loan finance and skillful employees haveboosted its employees productivity and profitability. Thefollowing graphs depicts the productivity and profitabilityper employee of the company.

16th April 2014

Microsec Research21

Source: Companies, Ace Equity, Microsec ResearchNote:- All figures are as on 31st March 2013, Valuations and Return Summary prices are as on 16th April 2014.

Peers Analysis

We believe, post the commencement of banking business, IDFC’s credit profile may be benefited in the longterm, as the company will have the options for the transition of its loan book over the various segments.Moreover, going forward revival in the economy (as expected) will also help the company’s financials.

16th April 2014

Microsec Research22

Valuation and Recommendation

P/BV Band

Notwithstanding challenging environment wherein, macro and micro economicenvironment led to higher stress, IDFC has managed to keep return ratios healthy. Thecompany’s 3 year average (FY11-13) ROE and ROA were 13.30% and 2.9% respectively.However, in December 2013, its Return on Assets (ROA) and Return on Equity (ROE)improved to 2.9% and 14.4% respectively. The company’s diversified loan portfolio and itsactive management of current and future business needs has helped it to maintain healthyreturns.

At the CMP of INR116.55, the stock is trading at TTM P/BV of 1.29x. The current valuationsof 1.03x FY15E and 0.92x FY16E Book Value looks attractive. We recommend a BUY on thestock with a target price of INR148 (1.16x FY16E BV) with an upside potential of ~27%from the current level with an investment horizon of 12-18 months.

Source: Company, ACE Equity, Microsec Research

Valuation is inexpensive and looks attractive

16th April 2014

Microsec Research23

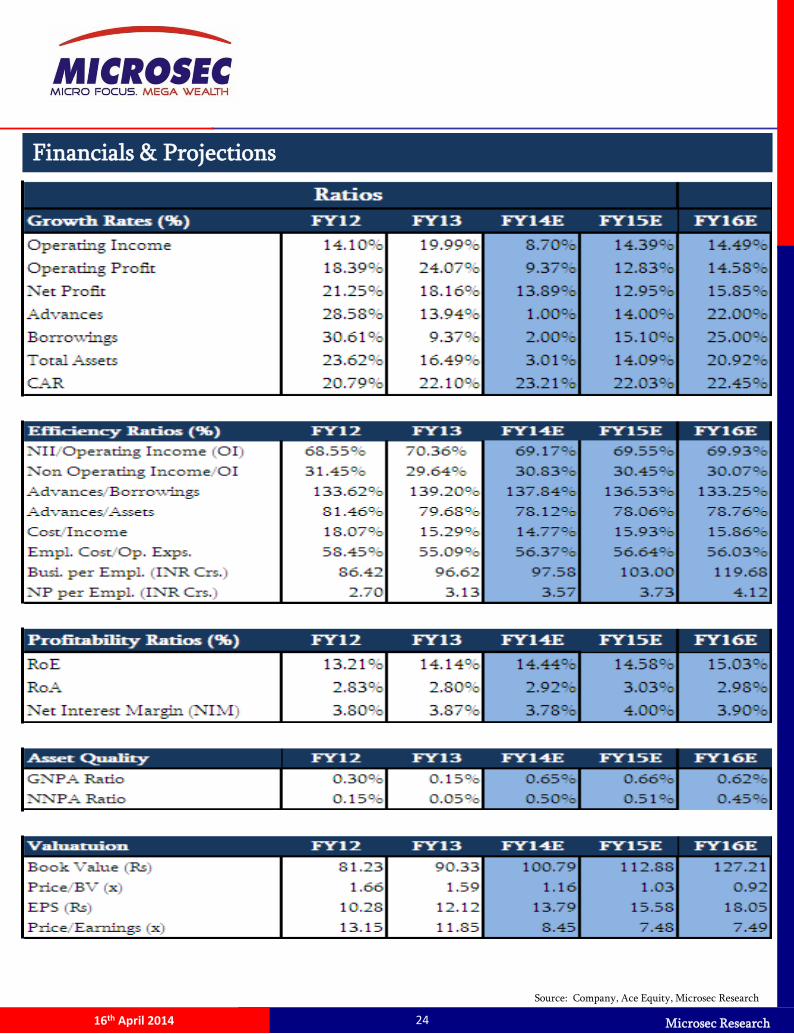

Financials & Projections

Source: Company, Ace Equity, Microsec Research

16th April 2014

Microsec Research24

Financials & Projections

Source: Company, Ace Equity, Microsec Research

16th April 2014

Microsec Research

Key Concerns The Banks and other financial institutions are also present in the infrastructuresector. The company may face huge competition which may force it to reduce itslending rate, if Banks start increase their foothold in this segment.

Further delay in the execution of stalled projects and slowdown in the economy mayact as a vicious cycle on investment in Capex, which may affect the company’sfinancials and also, increase risk on its asset quality.

Company’s investment banking and other capital market related business may beaffected, if there may slowdown in the capital markets going forward.

2516th April 2014

Microsec Research26

Recommendation

Strong Buy >20%

Buy between 10% and 20%

Hold between 0% and 10%

Underperform between 0% and -10%

Sell < -10%

Expected absolute returns (%) over 12 months

MICROSEC RESEARCH IS ALSO ACCESSIBLE ON BLOOMBERG AT <MCLI>

Microsec Research: Phone No.: 91 33 6651-2121 Email: [email protected]

Ajay Jaiswal: President, Investment Strategies, Head of Research: [email protected]

Fundamental Research

Name Sectors Designation Email ID

Nitin Prakash Daga IT, Telecom & Entertainment VP-Research [email protected]

Sutapa Roy Economy Research Analyst [email protected]

Sanjeev Jain BFSI Research Analyst [email protected]

Neha Majithia Metal, Mineral & Mining Research Analyst [email protected]

Soumyadip Raha Oil & Gas Executive Research [email protected]

Saroj Singh Auto, cement Executive Research [email protected]

Pooja Saraf FMCG, Textiles ,Cons. Goods Research Analyst [email protected]

Anandarup Goswami Midcaps Research Executive [email protected]

Khusboo Jaiswal Midcaps Research Executive [email protected]

Ajoy Mukherjee Pharmaceuticals, Agrochemicals Research Analyst [email protected]

Technical & Derivative Research

Vinit Pagaria Derivatives & Technical Senior VP [email protected]

Ranajit Kumar Saha Technical Research Sr. Manager [email protected]

Institutional Desk

Abhishek Sharma Institutional Desk Dealer [email protected]

PMS Division

Siddharth Sedani PMS Research VP [email protected]

Research-Support

Subhabrata Boral Research Support Asst. Manager Technology [email protected]

16th April 2014

Microsec Research3114th April 2014

Microsec Research

35

7th December’ 2010 28