Embed Size (px)

Citation preview

INITIAL PUBLIC OFFERING

APRIL 2006

PLETHICO PHARMACEUTICALS LIMITED

2

Disclaimer Statement

This presentation has been prepared by PLETHICO PHARMACEUTICALS LIMITED (“PPL” or “the Company”) solely for providing information about them. The information contained in this presentation has not been independently verified by Anand Rathi Securities Pvt Limited (“ARSPL”). No representation or warranty, express or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of such information or opinions contained herein. Neither the Company nor any of its respective affiliates, advisers or representatives nor ARSPL shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

The information contained in this presentation is only current as of its date. Certain statements made in this presentation may not be based on historical information or facts and may be "forward-looking statements", including those relating to the Company’s general business plans and strategy, its future financial condition and growth prospects, and future developments in its industry and its competitive and regulatory environment. Actual results may differ materially from these forward-looking statements due to a number of factors, including future changes or developments in the Company’s business, its competitive environment, information technology and political, economic, legal and social conditions in India.

This communication is for general information purposes only, without regard to specific objectives, financial situations and needs of any particular person. Please note that investments in securities are subject to risks including loss of principal amount. ARSPL does not accept any liability whatsoever, direct or indirect, that may arise from the use of the information herein.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares in the Company. ARSPL may from time to time perform investment banking or other services for, or solicit investment banking or other business from, any entity mentioned in this presentation.

3

Agenda

1. Issue Summary

2. Overview

3. Growth Strategy

4. Expansion Project

4

Issue Summary

5

Issue Summary

Total Issue Size Rs. 1100 Mn

Issue to Public Rs. 1100 Mn

of which QIB Portion (60%) Upto [●] Equity Shares

aggregating to Rs.660 Mn

of which Non-Institutional Portion(10%) Upto [●] Equity Shares aggregating to

Rs. 110 Mn

of which Retail Portion (30%) Upto [●] Equity Shares aggregating to

Rs. 330 Mn

Equity Shares O/s prior to the issue 3,04,00,000

Equity Shares O/s after the issue 34,328,572 at lower end and 34,066,667 at the higher end of the price band

6

Issue Summary

• Price Band Rs. 280 to Rs. 300 per Equity Share.

• Issue Size Rs. 1100 Million

• Minimum Application 20 Equity shares and multiples thereof

Issue opens April 10, 2006 -Monday

Issue closes April 17, 2006 -Monday

• Listing on BSE & NSE

• BRLM Anand Rathi Securities Private Limited

• Syndicate Member Enam Securities Private Limited

• Registrar to the Issue Intime Spectrum Registry Limited

7

Overview

8

Mission & Vision

Mission

To provide quality healthcare products at affordable prices driven by the highest

standards of ethics and human values.

Vision

To be a global healthcare company by the year 2010, offering products of

highest quality, backed by State-of-the-Art Manufacturing and R & D facilities, to

have a strong presence in the area of consumer healthcare business and

Nutraceuticals, both in the domestic as well as the International market.

9

Background - Company

The group started operations way back in 1963

Plethico was incorporated in 1991 to undertake manufacture of Formulations and undertake focused marketing of ethical/ prescriptions market

Focused on innovation and pioneered introduction of: Doxycycline based unique anti-biotic formulation

Co-trimoxazole based unique anti-bacterial formulation

Introduced for the first time in India, novel ayurvedic / herbal preparation (Single Herb Methi extract)

Adopted the “Branded Generic” model for marketing allopathic formulations in India in the prescriptions market

10

Background - Company

The company has presence in niche segments like

Herbal & Nutraceuticals preparations including Food

supplements

OTC / Consumer Products

NDDS

11

Background - Company

Operations in 45 countries including India

Export targets at the semi-regulated / un-regulated markets of

Eastern Europe

Common Wealth of Independent States (CIS)

Africas

South East Asian (SEA) nations

Gulf Co-operation Council (GCC)

Latin American Countries (LAC)

Over 150 sales representatives and front line-managers are employed in markets outside India

12

Sales Turnover

Break up of Total Turnover

68%

32%

Export Domestic

Countrywise Export Break up

31%

48%

13%

8%

Africa CIS LAC SEA GCC

Domestic Break Up

90%

10%

Contract Manufacturing Domestic OTC

DomesticTurnover

69%

31%

Herbal /NutraceuticalsAllopathic/Disposables

13

Fully Integrated State of Art Manufacturing Units

Can Cater to High Capacity Production of Tablets, Capsules, Liquid Orals, Eye / Ear drops, Injectables, Ointments & Creams.

MANGALIA PLANT

Manufacturing Facilities

KALARIA PLANT

Centralized humidity & temperature controlled warehousing

Plant built and installed as per cGMP norms

14

Backward Integration

Backward Integration by installation of State of the art:

“Klockner Hansell GMBH” machinery for manufacturing Lozenges

“Aoki Japan” machine for PET bottles.

Entry into regulated markets with herbal products requires augmenting the quality of herbal remedies vis a vis; herbal remedies exported to Non Regulated Countries. Hence the Company has decided to undertake Organic Farming.

RussiaKazakhstanMoldovaGeorgia

TurkmenistanUkraineUzbekistanTajikistanKyrgyzstanAzerbaijanLatviaLithuania

Slovakia

Ivory CoastDR CongoBenin

SudanUgandaKenyaEthiopiaEritreaSouth AfricaNigeria

CameroonSierra Leone

PeruChileEcuadorColombiaVenezuela

KuwaitYemenDubai

A TRULY GLOBAL REACH

VietnamPapua New GuineaMalaysiaCambodiaPhilippines

El SalvadorNicaraguaCosta RicaPanamaGuatemala

Caribbean

Sri Lanka

16

Growth Strategy

The Company has invested in future growth by building a two pronged

investment footprint.

“Organic growth footprint” - Build robust facilities which will comply to world

standards and

“Inorganic Growth footprint” - Invest strategically into strong setup’s either a

Marketing & Distribution outfit (called M&D Strategy)

Manufacturing cum M&D outfit (Called MM&D Strategy).

Backward Integration

Always gave due importance to R & D Activities.

17

The Company has entered into various overseas alliances with strategic partners

across continents.

Common Wealth of Independent States (CIS) Nations:

MoU with Rezlov Limited, a pharmaceutical marketing & distribution (M&D) chain for the

following countries. The stake held by the Company is as under:

Kazakhstan – 75%

Kyrgyzstan – 75%

Moldova – 63%

Russia – 51%

Ukraine – 51%

Azerbaijan – 51%

Overseas Investments

18

Africa

MoU signed for:

Kenya – Plethico Africa Ltd - for setting up of world class

manufacturing unit with liquid and ointment plant, allowing

access to COMESA Countries (Common Market For Eastern &

Southern Africa)

Cambodia – Agreement with Tricon Holdings Limited in

Cambodia for manufacturing and distribution operations

Overseas Investments

19

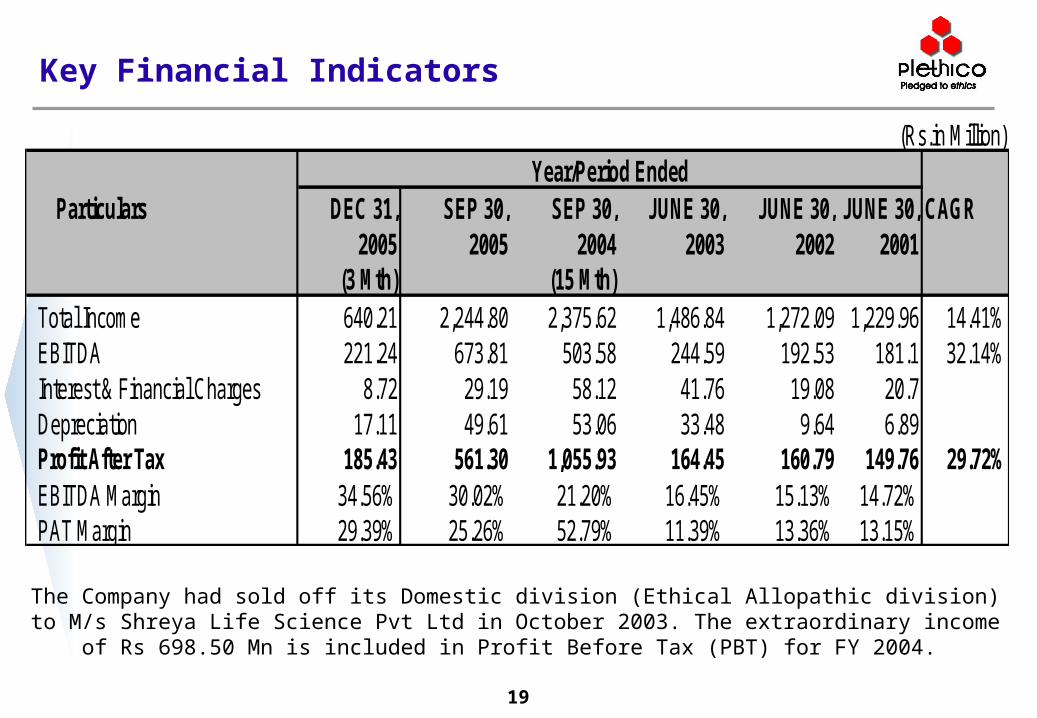

Key Financial Indicators

The Company had sold off its Domestic division (Ethical Allopathic division) to M/s Shreya Life Science Pvt Ltd in October 2003. The extraordinary income of Rs 698.50 Mn is included in Profit Before Tax

(PBT) for FY 2004.

(Rs.in Million)

Particulars DEC 31, SEP 30, SEP 30, JUNE 30, JUNE 30, JUNE 30, CAGR2005 2005 2004 2003 2002 2001

(3 Mth) (15 Mth)Total Income 640.21 2,244.80 2,375.62 1,486.84 1,272.09 1,229.96 14.41%EBITDA 221.24 673.81 503.58 244.59 192.53 181.1 32.14%Interest & Financial Charges 8.72 29.19 58.12 41.76 19.08 20.7Depreciation 17.11 49.61 53.06 33.48 9.64 6.89Profit After Tax 185.43 561.30 1,055.93 164.45 160.79 149.76 29.72%EBITDA Margin 34.56% 30.02% 21.20% 16.45% 15.13% 14.72%PAT Margin 29.39% 25.26% 52.79% 11.39% 13.36% 13.15%

Year/Period Ended

20

Key Financial Indicators

(Rs in Million)

Particulars DEC 31, SEP 30, SEP 30, JUNE 30, JUNE 30, JUNE 30,2005 2005 2004 2003 2002 2001

(3 mth) (15 Mth)

Capital Employed 3,434.35 3,301.29 2,608.55 1,597.50 1,497.88 1,056.11 Net Block (Including Capital WIP) 969.27 985.64 989.96 908.22 715.77 404.18 Working Capital 1,204.02 1,144.77 764.88 640.00 737.09 581.60 Net Worth 2,808.87 2,623.43 2,083.79 1,060.41 906.91 766.43 Borrowings 625.48 677.86 524.76 537.09 590.97 289.68 Return on Net Worth 26.40% 21.40% 50.67% 15.51% 17.73% 19.54%Earning Per Share (Weighted Average) 6.10 73.86 138.94 21.64 21.16 19.71

Year/Period Ended

CAGR of Networth for 2001-2005 is 30.03%

Debt Equity for Dec 31, 2005 (3 Months) is at 0.27

Growth Strategy

22

Increased focus on Herbals

FY 03

2%2% 3%13%

80%

HNOD - her bal / netr aceutical OT C Comestr ic

HNE - Her bal / nutr aceutical E xpor t

ADCm - Al lopathic Domestr ic Contr act m,anuf actur ing

AE - Al lopathic/ disposables E xpor t

AD - Al lopathic / disposables Domestic Br anded

FY 053%

48%

28%

21%0%

FY 03

23

Growth Initiatives

NDDS for diabetes and cancer patients

Current submission rate of 55-60 registration dossiers per month for exports

Thrust on East Europe, GCC and SEA countries

Increase in confectionary products and entry into foot care and oral care segments in domestic

Setting up manufacturing JV in Kenya

One of the differentiating features for export marketing -Invested over Rs 1Bn in Rezlov group of cos. to gain majority stake -To exercise control over the customers of M&D cos.

Domestic reach:

field force to increase from 100 to 500 over 2 years

24

Growth Initiatives (Contd…)

Increased focus on herbals, OTC and nutraceuticals

Topline growth

Organic

- Increase in confectionary products and entry into foot care and oral care segments in domestic

- Thrust on East Europe, GCC and SEA countries

Inorganic

- Rs 280m of issue proceeds planned for company / brand acquisition

25

Expansion Project

Project Particulars Cost (Rs million)I Upgradation of Kalaria Plant for UK MHRA compliance 257.10 II Setting up of a plant in Jammu & Kashmir (J&K) which is WHO 308.80

GMP compliant & undertaking Organic FarmingIII Setting-up of Research and Development & F&D Centre 131.50 IV Acquiring a stake in a OTC / Domestic herbal / Nutraceutical 280.00

Company or a BrandV Setting up a Corporate Office in Mumbai 194.00 VI Working Capital Requirement 275.00

TOTAL CAPITAL EXPENDITURE 1,446.40

Particulars Cost (Rs million)I Proceeds of the issue 1,100.00 II Internal Accruals [ ]

Total [ ]

Expansion Project

Means Of Finance

26

Summary

Non infringing model of Business

State of art manufacturing units in Indore possessing capability of manufacturing all possible dosage forms.

Strong formulation development technique including NDDS like effervescent tablets.

Strong M&D tie up in Russia, CIS & Cambodia

Strong management team and motivated workforce

Foray into Backward Integration for cultivating essential critical herbs for captive consumption thus enabling high end finger printing technology for herbal formulations

Strong system oriented company

Product list exceeding 400, transcending more than 39 therapeutic categories exporting to more than 45 countries across the globe

27

THANK YOU

Q&A

PLETHICO PHARMACEUTICALS LIMITED