Embed Size (px)

Citation preview

CONFIDENTIAL

Doug Ladd

Chief Marketing Officer

EndoChoice, Inc.

Innovation in Health Care

CONFIDENTIAL 2

Has Health Care Consumerism Come of Age?

CONFIDENTIAL 3

CONFIDENTIAL

Business in Brief: Castlight Health Health IT company based in San Francisco, CA; raised $100M Series D funding,

$181M total

Targets companies with self-insured health plans, charges them monthly fee based on number of employees and dependents covered

Platform enables consumers to compare quality, cost of services provided by doctors, labs, and hospitals

Employer clients include Life Technologies, Allegis Group; data partners include Leapfrog Group

Has Health Care Consumerism Come of Age?

4

Platform Supports Consumer Decision-Making

Source: Castlight Health, available at: www.castlighthealth.com; Advisory Board interviews and analysis.

• Provider, Service Cost

• Comparison Pricing

• Benefits Information

• Quality Scores

• Patient Satisfaction

• Access, Convenience

• Provider Credentials

Consumer Friendly Interface Pricing Information

Provider Search

61% Consumers report changing

their decision on where to get

care based on Castlight data

Light-Years Beyond “Hospital Compare”

CONFIDENTIAL

Health Plans Venturing (Back) into the Provider Space

5

Getting Closer to the Patient to Manage Cost and Quality

1) Operating loss in fiscal year 2011.

Humana acquires more than 200

ambulatory centers across 42 states

with the purchase of Concentra

WellPoint adds 26 clinics near Los

Angeles with the acquisition of the

health plan CareMore

Cigna expands its medical group

over two years to service 25 primary

and urgent care locations across

Arizona

Source: Kaiser Health News, “Managed Care Enters The Exam Room As Insurers Buy Doctor Groups,” available at: http://www.kaiserhealthnews.org/Stories/2011/July/01/unitedhealth-insurers-buy-doctors-groups.aspx, accessed April 1, 2011; The Advisory Board Company, available at: http://www.advisory.com/Daily-Briefing/2012/05/03/Highmark-UPMC-reach-18-month-deal, accessed May 10, 2012; Advisory Board interviews and analysis.

Case in Brief: Highmark

• Pittsburgh-based insurer announced

acquisition of West Penn Allegheny

Health System in June 2011

• Deal is only first step in a larger

strategy to grow in the provider

space through the purchase of

physicians and hospitals

Payers Expand into Primary

Care Also Expanding into Inpatient

Care?

• 5 hospitals

• $51.7M annual

operating loss1

• Recently closed ED

West Penn

Allegheny

CONFIDENTIAL

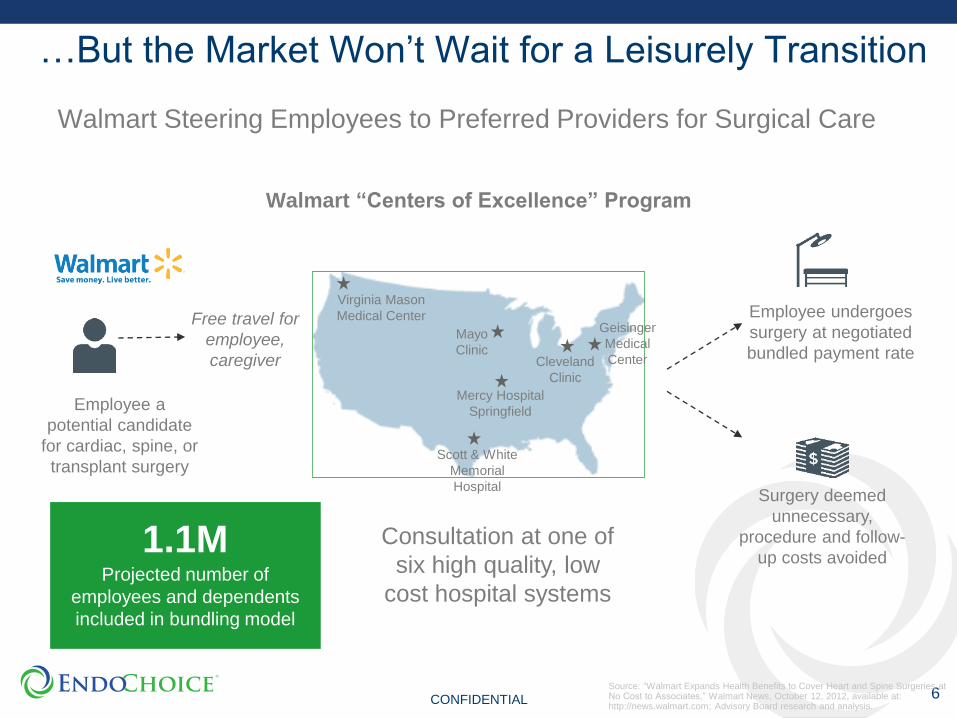

…But the Market Won’t Wait for a Leisurely Transition

6

Walmart Steering Employees to Preferred Providers for Surgical Care

Walmart “Centers of Excellence” Program

Source: “Walmart Expands Health Benefits to Cover Heart and Spine Surgeries at No Cost to Associates,” Walmart News, October 12, 2012, available at: http://news.walmart.com; Advisory Board research and analysis.

Employee a

potential candidate

for cardiac, spine, or

transplant surgery

Consultation at one of

six high quality, low

cost hospital systems

Employee undergoes

surgery at negotiated

bundled payment rate

Surgery deemed

unnecessary,

procedure and follow-

up costs avoided

Free travel for

employee,

caregiver Cleveland

Clinic

Scott & White

Memorial

Hospital

Virginia Mason

Medical Center

Mercy Hospital

Springfield

Geisinger

Medical

Center

Mayo

Clinic

1.1M Projected number of

employees and dependents

included in bundling model

CONFIDENTIAL

Employees Shouldering More of the Cost Burden

7

Shifting Responsibility to Employees via High-Deductible Health Plans

Source: “Employer Health Benefits: 2011 and 2012 Annual Surveys,” Kaiser Family Foundation and Health Research & Educational Trust, Buntin M, et al., “Healthcare Spending and Preventive Care in High-Deductible and Consumer-Directed Health Plans,” American Journal of Managed Care, March 2011, 222-230; Advisory Board research and analysis.

1) High-deductible health plan with savings option, defined as a health plan with a deductible of at least $1,000 for single coverage and $2,000 for family coverage.

2) Consumer directed/driven health plans. 3) High-deductible health plan/consumer-directed health plan.

Percent of Total Employees Covered by HDHP/SO1

2009-2012

Household Health Care

Spending Growth 2004-2005

Total health

care Outpatient Inpatient Emergency

Departments

Prescription

Drug

Select Large Employers Moving to 100%

CDHP2

HDHP/CDHP3 Control

$21

$10 ($1) $4

$7

$106

$56

$35

$4 $11

8%

13%

17% 19%

2009 2010 2011 2012

CONFIDENTIAL

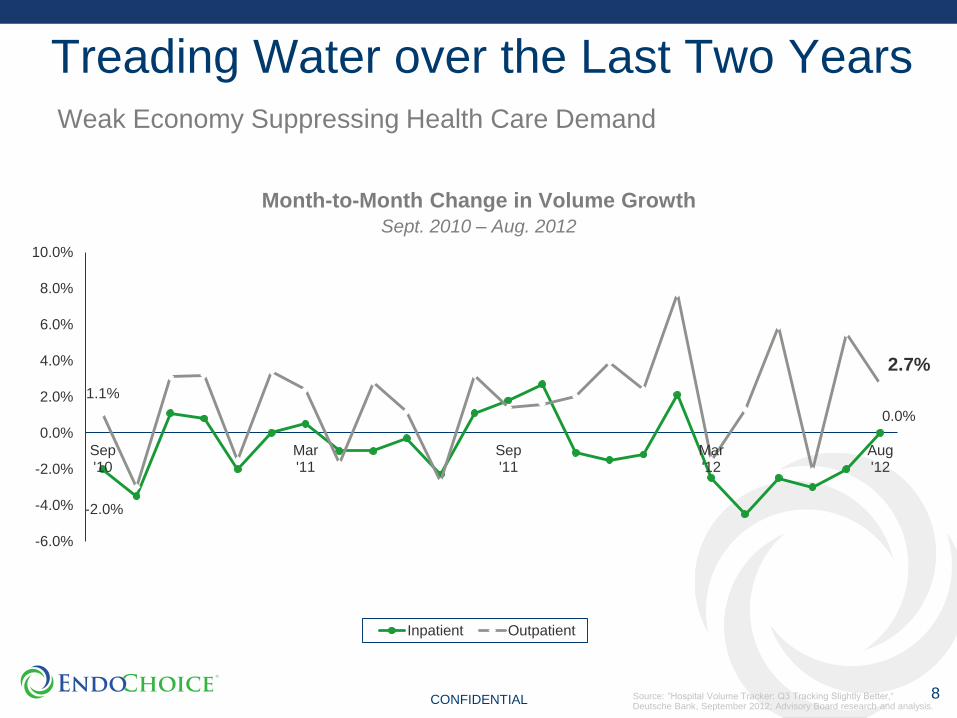

Treading Water over the Last Two Years

8 Source: “Hospital Volume Tracker: Q3 Tracking Slightly Better,“ Deutsche Bank, September 2012; Advisory Board research and analysis.

Month-to-Month Change in Volume Growth

Sept. 2010 – Aug. 2012

-2.0%

0.0%

1.1%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Sep'10

Mar'11

Sep'11

Mar'12

Aug'12

Inpatient Outpatient

2.7%

Weak Economy Suppressing Health Care Demand

CONFIDENTIAL

ACO Transformation Taking Hold

9

Groundswell of Providers Beginning to Transform Business Model

CONFIDENTIAL

Getting Serious About Transformation

10 Source: 2012 Growth Survey, Marketing and Planning Leadership Council; Advisory Board research and analysis.

Payment Reform Initiatives Planned to Launch between 2012 and 2015

n=53 Hospital and Hospital System

Planning Executives

46%

8%

50%

38%

21%

48%

7%

76%

55%

7%

Shared Savings Program Pioneer ACO Bundled Payments Risk-Based Contracts withPrivate Payers

None of the above

Freestanding Hospitals Multi-Hospital Systems

CONFIDENTIAL

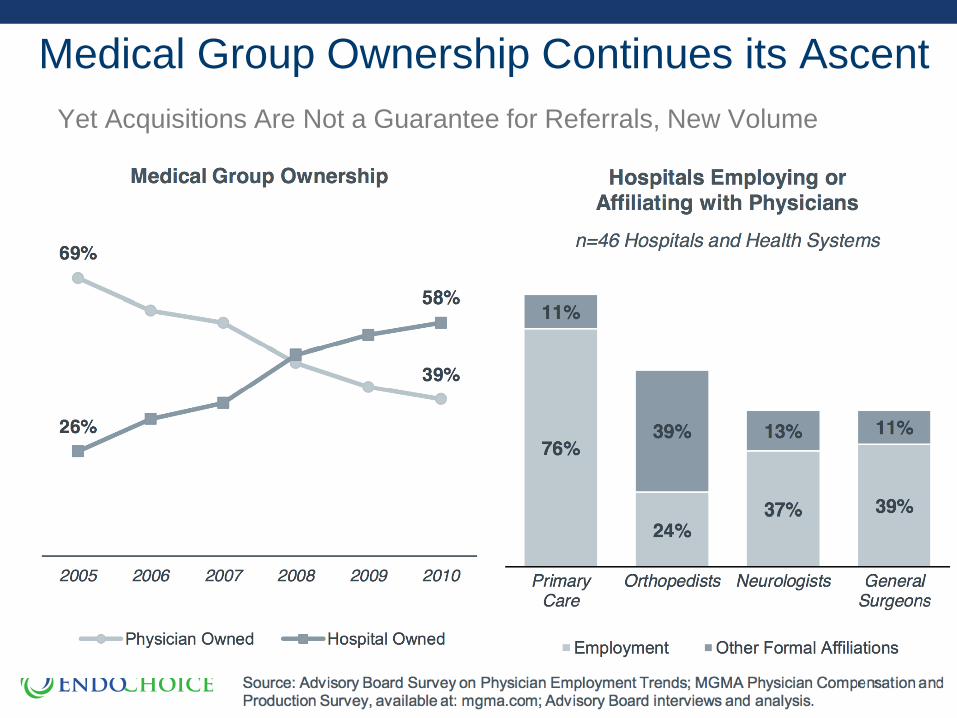

Medical Group Ownership Continues its Ascent

11

Yet Acquisitions Are Not a Guarantee for Referrals, New Volume

CONFIDENTIAL

Implications

Patients will play a larger role in decision making

Capitated agreements will be coming back

Innovation…in technology and care mechanisms will be rewarded

…if they reduce the cost of care

12

CONFIDENTIAL

Frost & Sullivan Analysis of Successful Medical Innovations

Review of the most successful IPOs of medical technology companies revealed they delivered on at least one of five key insights:

Catch Cancer Sooner

Reduce Patient Pain and Anxiety

Shift Site of Care to Less Expensive Venues

Eliminate the Need for General Anesthesia

De-Skill the Procedure…enable the less skilled to perform better

Do any of these and you reduce the cost of care

13

CONFIDENTIAL

Health Care Market Model

14

Minute

Clinics

Endoscopy General

Surgery

Pla

nn

ing

Urgent

High

Routine

Low Complexity

Trauma

CONFIDENTIAL

The Frequency of Problems and ‘Solving Costs’ Guides How Decisions are Made

15

Ad-Hoc

Experts

Patterns

Rules-Based

Decision Trees

Fre

qu

en

cy

Low

Low

High

High Solving Cost

CONFIDENTIAL

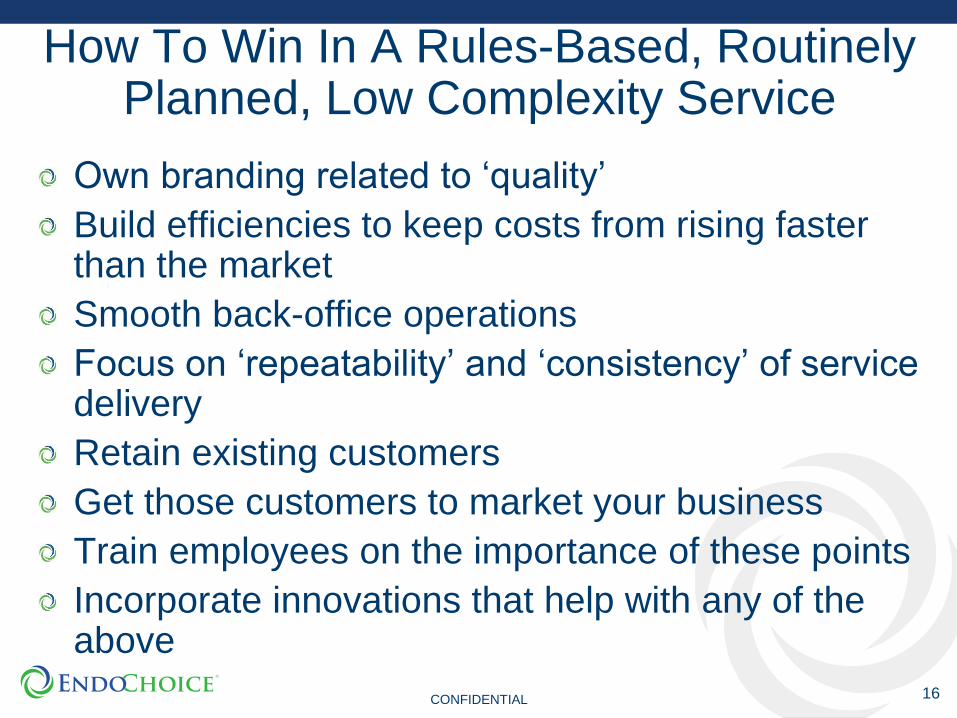

How To Win In A Rules-Based, Routinely Planned, Low Complexity Service

Own branding related to ‘quality’

Build efficiencies to keep costs from rising faster than the market

Smooth back-office operations

Focus on ‘repeatability’ and ‘consistency’ of service delivery

Retain existing customers

Get those customers to market your business

Train employees on the importance of these points

Incorporate innovations that help with any of the above

16

CONFIDENTIAL

Thank You

17

![MERKI MINICATALOGUE2013 [Mode de compatibilité] · C1 IST/702-avec réglage de niveau C1 IST/703-avec réglage de niveau ... C1 RMD/181M * C1 RMD/100M* C1 RMD/102M* C1 RMD/101M*](https://img.pdfslide.net/doc/110x75/5b87a8ef7f8b9aaf728bdd63/merki-minicatalogue2013-mode-de-compatibilite-c1-ist702-avec-reglage-de.jpg)