Embed Size (px)

Citation preview

Innovations in nebulized delivery

John Pritchard

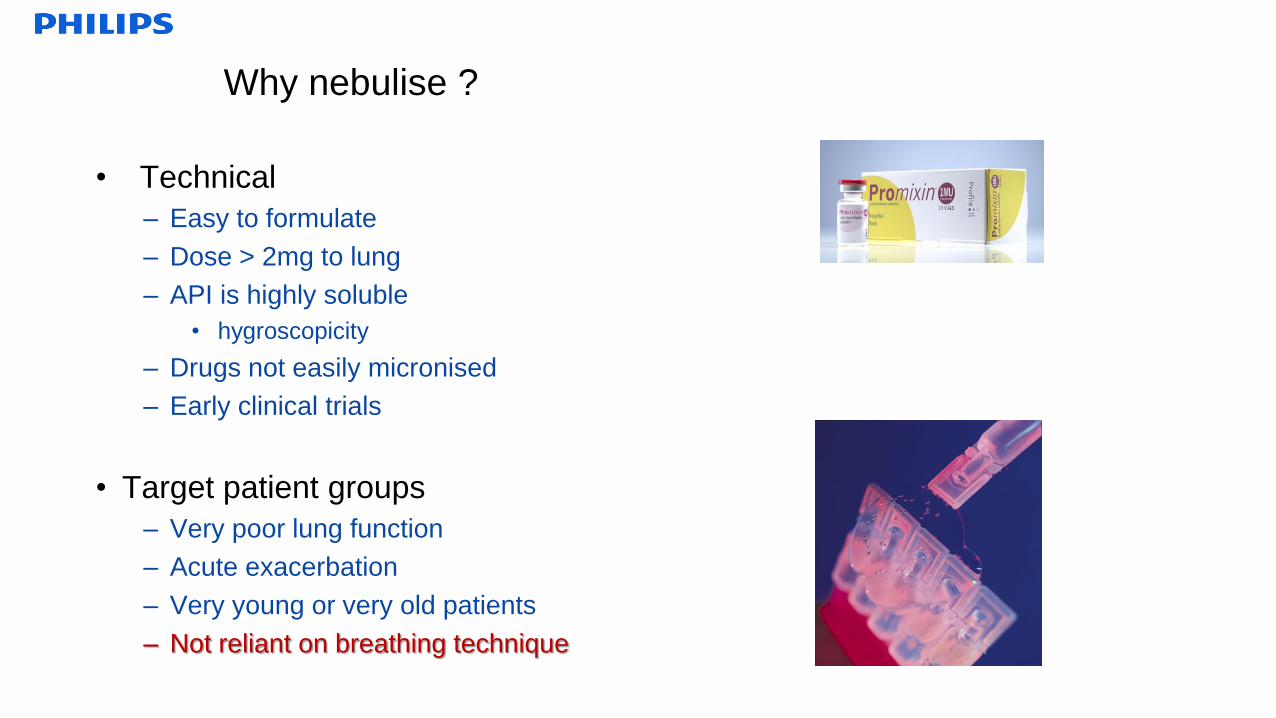

Why nebulise ?

• Technical

– Easy to formulate

– Dose > 2mg to lung

– API is highly soluble

• hygroscopicity

– Drugs not easily micronised

– Early clinical trials

• Target patient groups

– Very poor lung function

– Acute exacerbation

– Very young or very old patients

– Not reliant on breathing technique

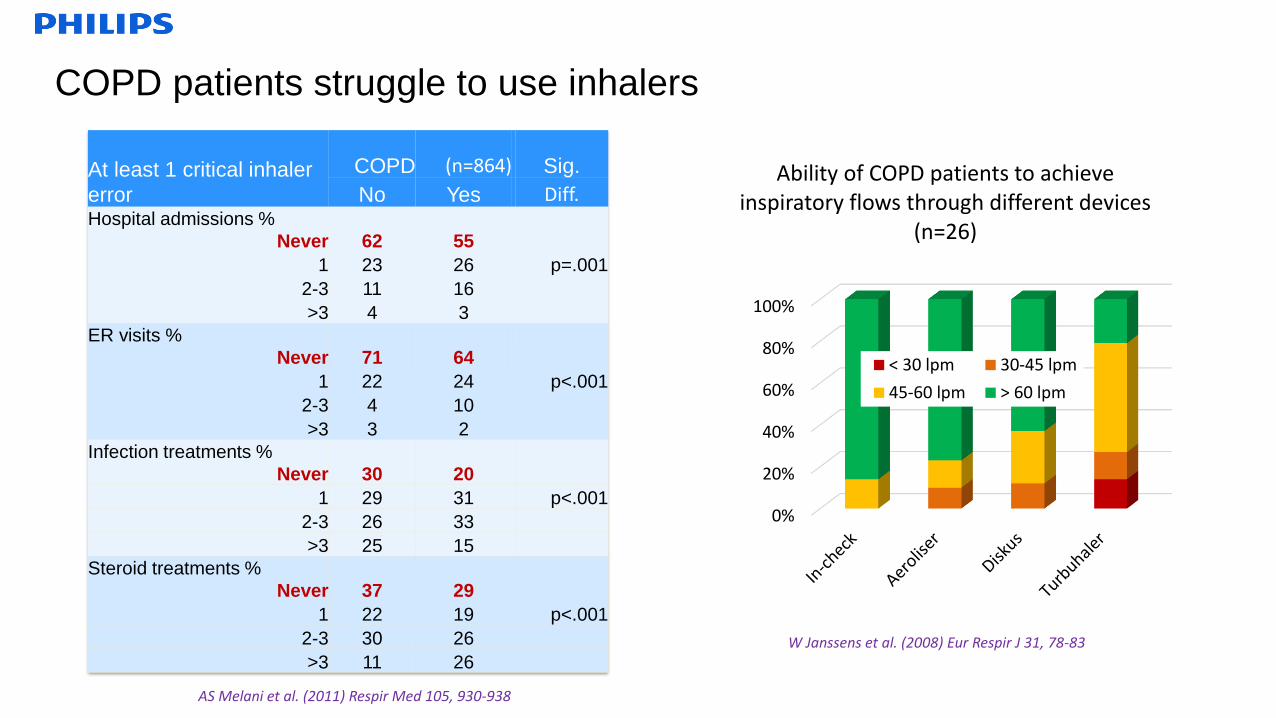

COPD patients struggle to use inhalers

At least 1 critical inhaler

error

COPD (n=864) Sig.

No Yes Diff.Hospital admissions %

Never 62 55

1 23 26 p=.001

2-3 11 16

>3 4 3

ER visits %

Never 71 64

1 22 24 p<.001

2-3 4 10

>3 3 2

Infection treatments %

Never 30 20

1 29 31 p<.001

2-3 26 33

>3 25 15

Steroid treatments %

Never 37 29

1 22 19 p<.001

2-3 30 26

>3 11 26

AS Melani et al. (2011) Respir Med 105, 930-938

W Janssens et al. (2008) Eur Respir J 31, 78-83

0%

20%

40%

60%

80%

100%

Ability of COPD patients to achieve inspiratory flows through different devices

(n=26)

< 30 lpm 30-45 lpm

45-60 lpm > 60 lpm

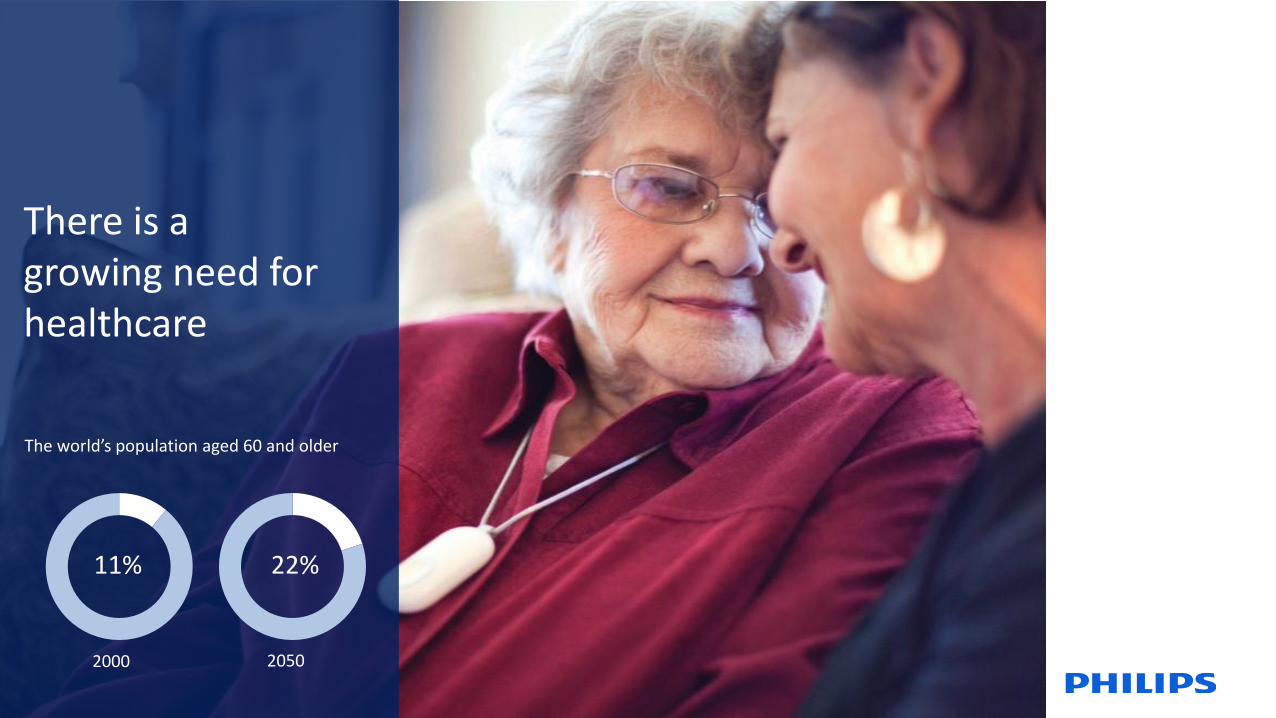

There is a growing need for healthcare

The world’s population aged 60 and older

2000 2050

11% 22%

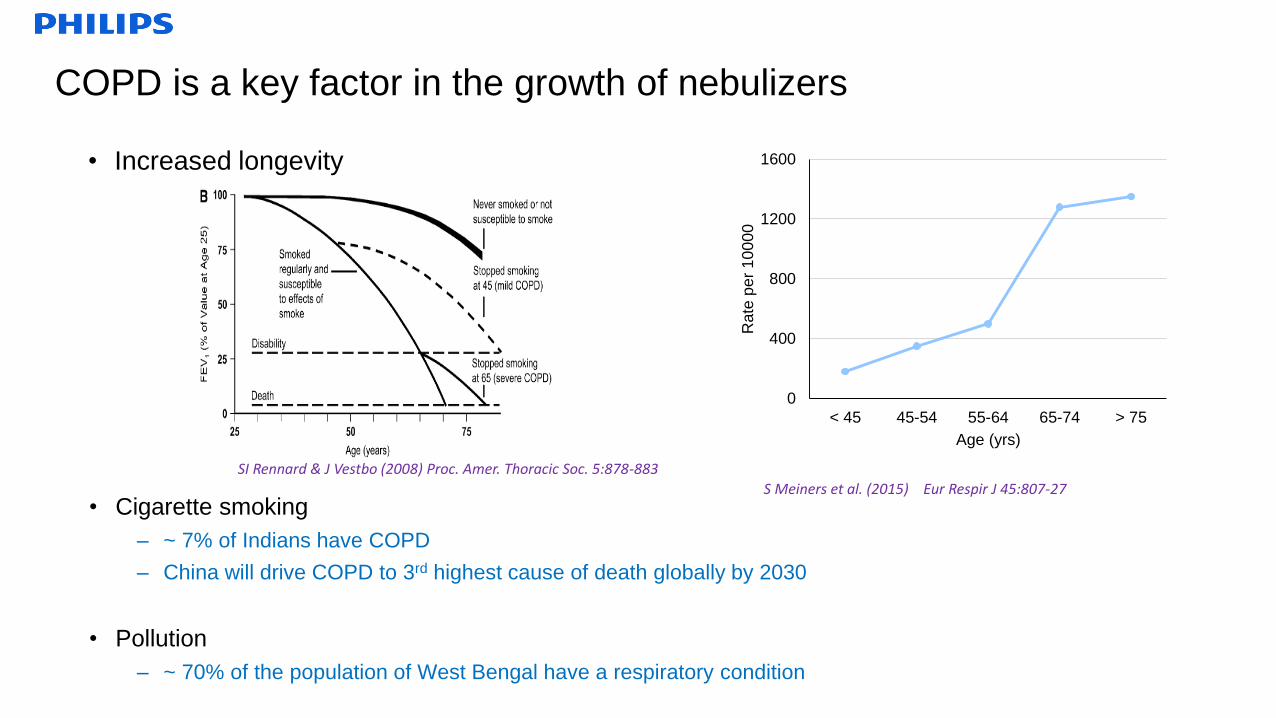

COPD is a key factor in the growth of nebulizers

• Increased longevity

• Cigarette smoking

– ~ 7% of Indians have COPD

– China will drive COPD to 3rd highest cause of death globally by 2030

• Pollution

– ~ 70% of the population of West Bengal have a respiratory condition

SI Rennard & J Vestbo (2008) Proc. Amer. Thoracic Soc. 5:878-883

0

400

800

1200

1600

< 45 45-54 55-64 65-74 > 75

Rate

pe

r 1

00

00

Age (yrs)

S Meiners et al. (2015) Eur Respir J 45:807-27

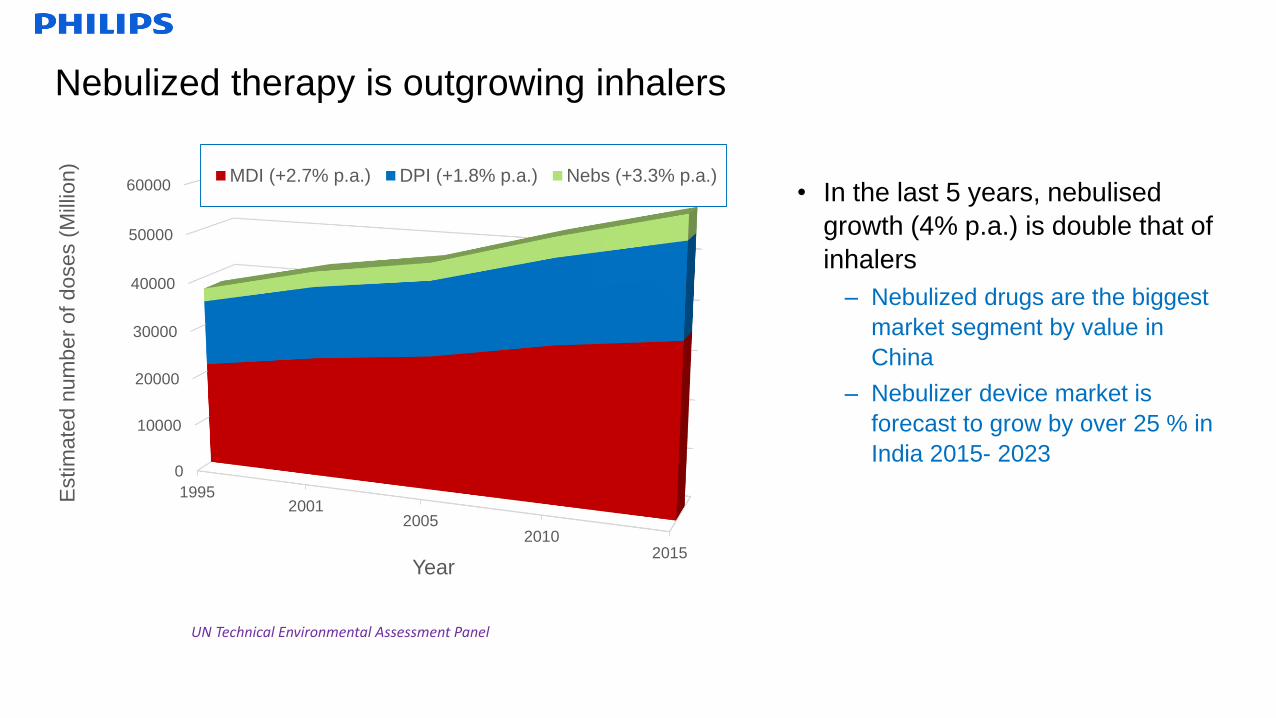

Nebulized therapy is outgrowing inhalers

• In the last 5 years, nebulised

growth (4% p.a.) is double that of

inhalers

– Nebulized drugs are the biggest

market segment by value in

China

– Nebulizer device market is

forecast to grow by over 25 % in

India 2015- 20230

10000

20000

30000

40000

50000

60000

19952001

20052010

2015

Estim

ate

d n

um

be

r of doses (

Mill

ion)

Year

MDI (+2.7% p.a.) DPI (+1.8% p.a.) Nebs (+3.3% p.a.)

UN Technical Environmental Assessment Panel

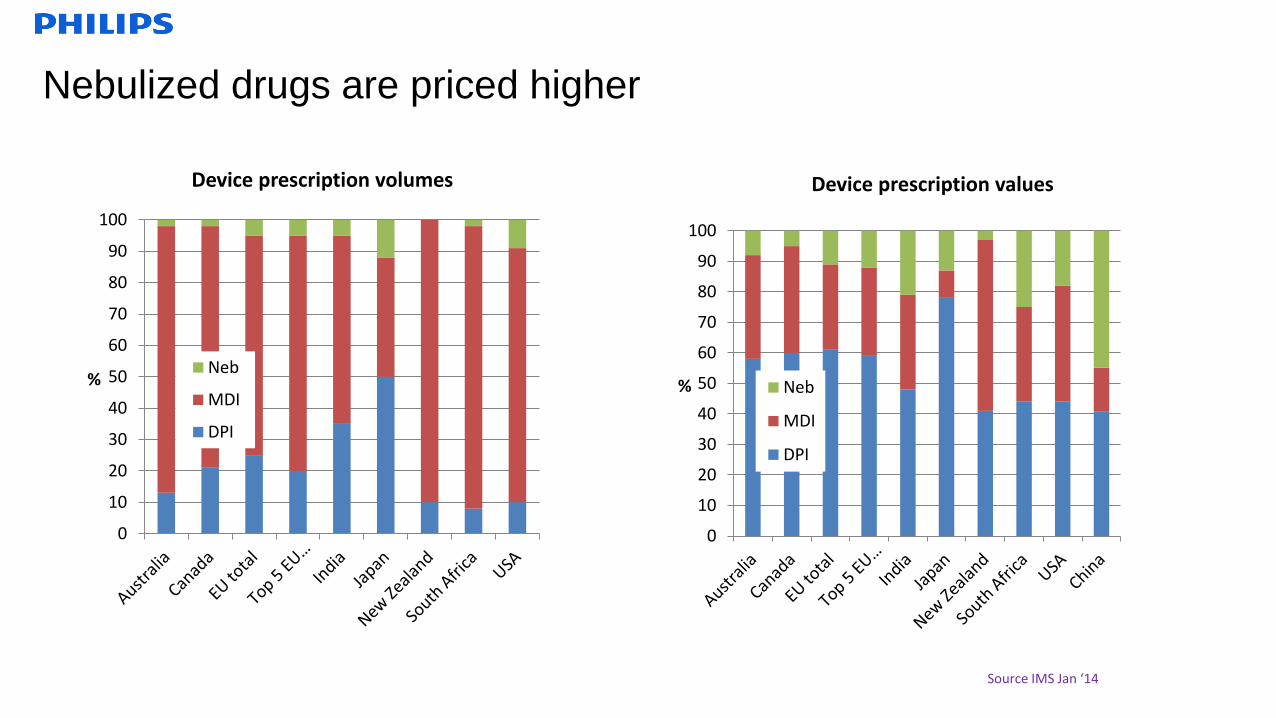

Nebulized drugs are priced higher

0

10

20

30

40

50

60

70

80

90

100

%

Device prescription volumes

Neb

MDI

DPI

Source IMS Jan ‘14

0

10

20

30

40

50

60

70

80

90

100

%

Device prescription values

Neb

MDI

DPI

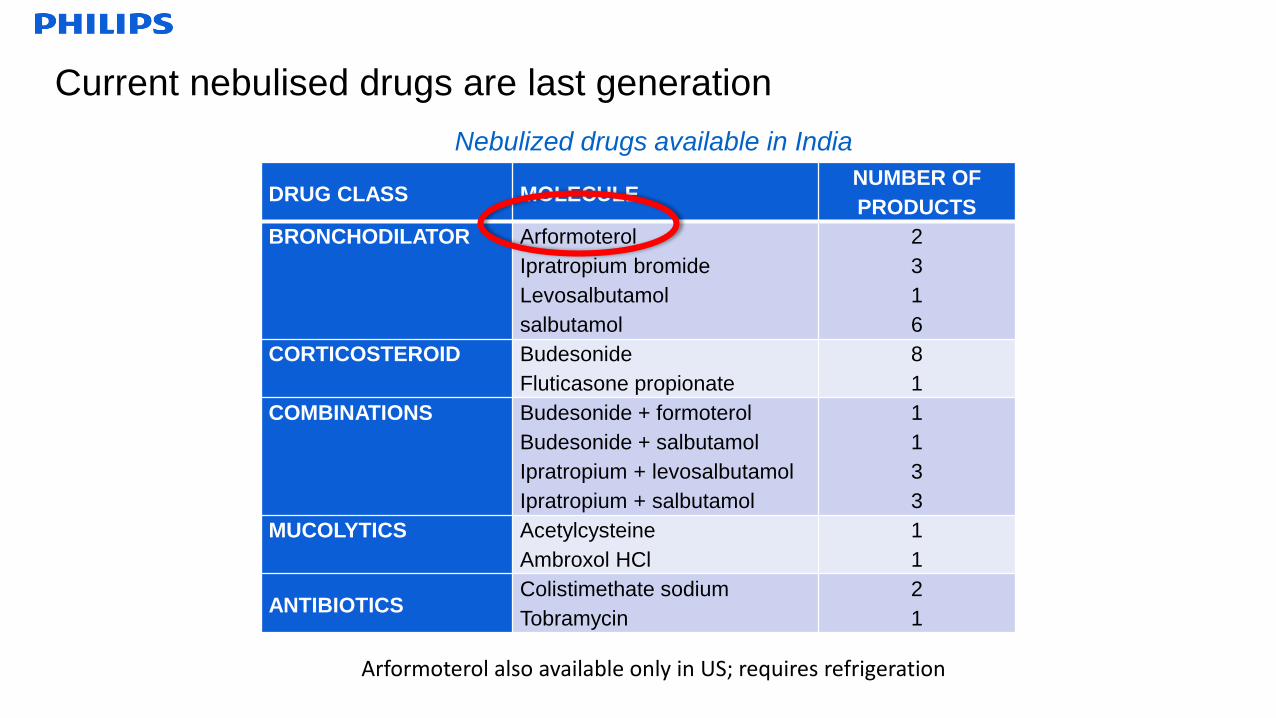

Current nebulised drugs are last generation

Nebulized drugs available in India

DRUG CLASS MOLECULENUMBER OF

PRODUCTS

BRONCHODILATOR Arformoterol

Ipratropium bromide

Levosalbutamol

salbutamol

2

3

1

6

CORTICOSTEROID Budesonide

Fluticasone propionate

8

1

COMBINATIONS Budesonide + formoterol

Budesonide + salbutamol

Ipratropium + levosalbutamol

Ipratropium + salbutamol

1

1

3

3

MUCOLYTICS Acetylcysteine

Ambroxol HCl

1

1

ANTIBIOTICSColistimethate sodium

Tobramycin

2

1

Arformoterol also available only in US; requires refrigeration

2

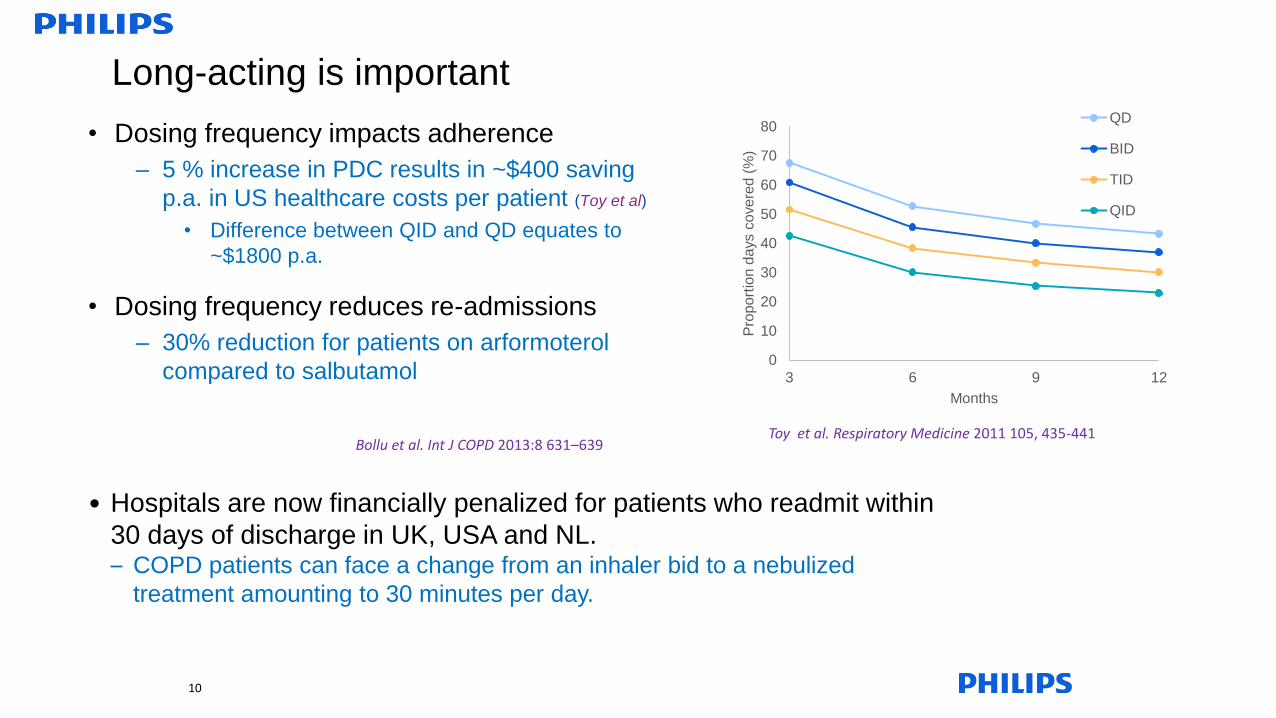

Long-acting is important

210

0

10

20

30

40

50

60

70

80

3 6 9 12

Pro

po

rtio

n d

ays c

ove

red

(%

)

Months

QD

BID

TID

QID

Toy et al. Respiratory Medicine 2011 105, 435-441Bollu et al. Int J COPD 2013:8 631–639

• Hospitals are now financially penalized for patients who readmit within

30 days of discharge in UK, USA and NL.– COPD patients can face a change from an inhaler bid to a nebulized

treatment amounting to 30 minutes per day.

• Dosing frequency impacts adherence

– 5 % increase in PDC results in ~$400 saving

p.a. in US healthcare costs per patient (Toy et al)

• Difference between QID and QD equates to

~$1800 p.a.

• Dosing frequency reduces re-admissions

– 30% reduction for patients on arformoterol

compared to salbutamol

2

There is no shortage of new drugs !

• Within the next couple of years, from major pharma companies there will be at least:

– 7 LAMA, 5 LABA, 7 ICS, 12 LABA/ICS, 5 LABA/LAMA

– Only ~ 1/3 in MDI format

• There are many more products being developed in growth markets

– Cipla offer 28 different products in over 100 countries including LABA/LAMA/ICS

• Few companies have addressed the nebulized segment

a) Develop a new molecule

b) Change the development paradigm

c) “Beyond the inhaler”

11

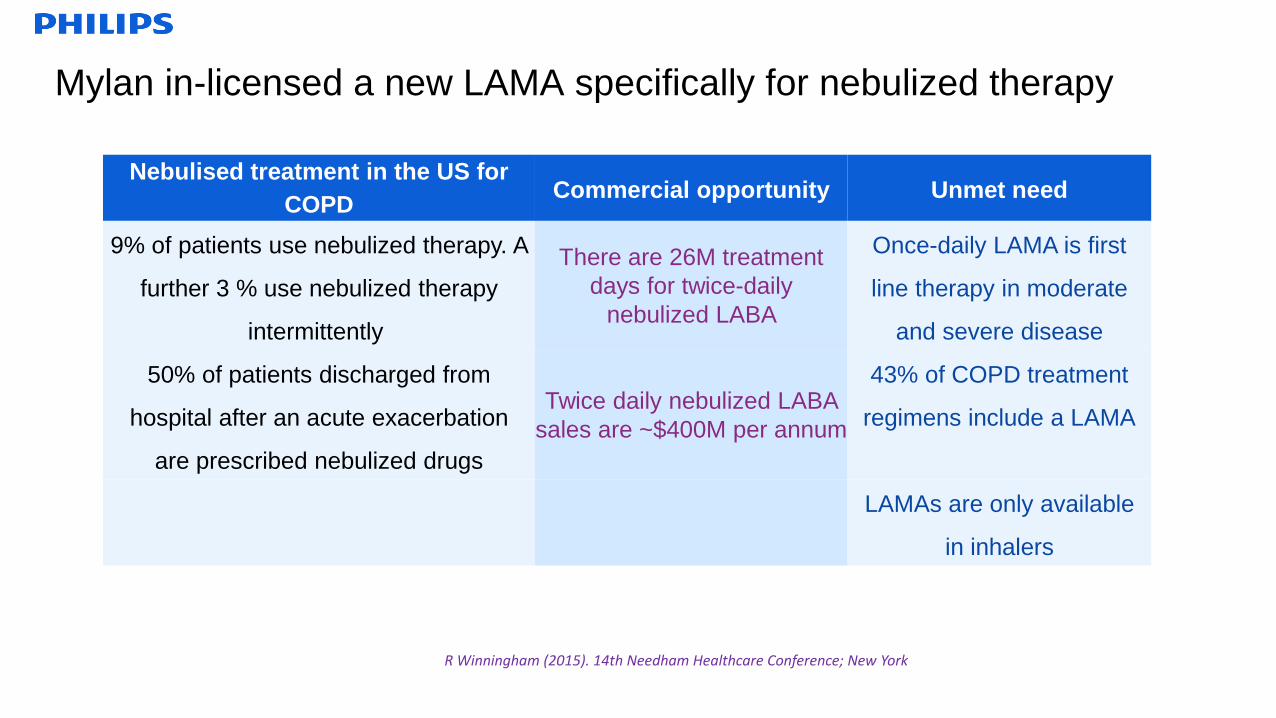

Mylan in-licensed a new LAMA specifically for nebulized therapy

Nebulised treatment in the US for

COPDCommercial opportunity Unmet need

9% of patients use nebulized therapy. A

further 3 % use nebulized therapy

intermittently

There are 26M treatment

days for twice-daily

nebulized LABA

Once-daily LAMA is first

line therapy in moderate

and severe disease

50% of patients discharged from

hospital after an acute exacerbation

are prescribed nebulized drugs

Twice daily nebulized LABA

sales are ~$400M per annum

43% of COPD treatment

regimens include a LAMA

LAMAs are only available

in inhalers

R Winningham (2015). 14th Needham Healthcare Conference; New York

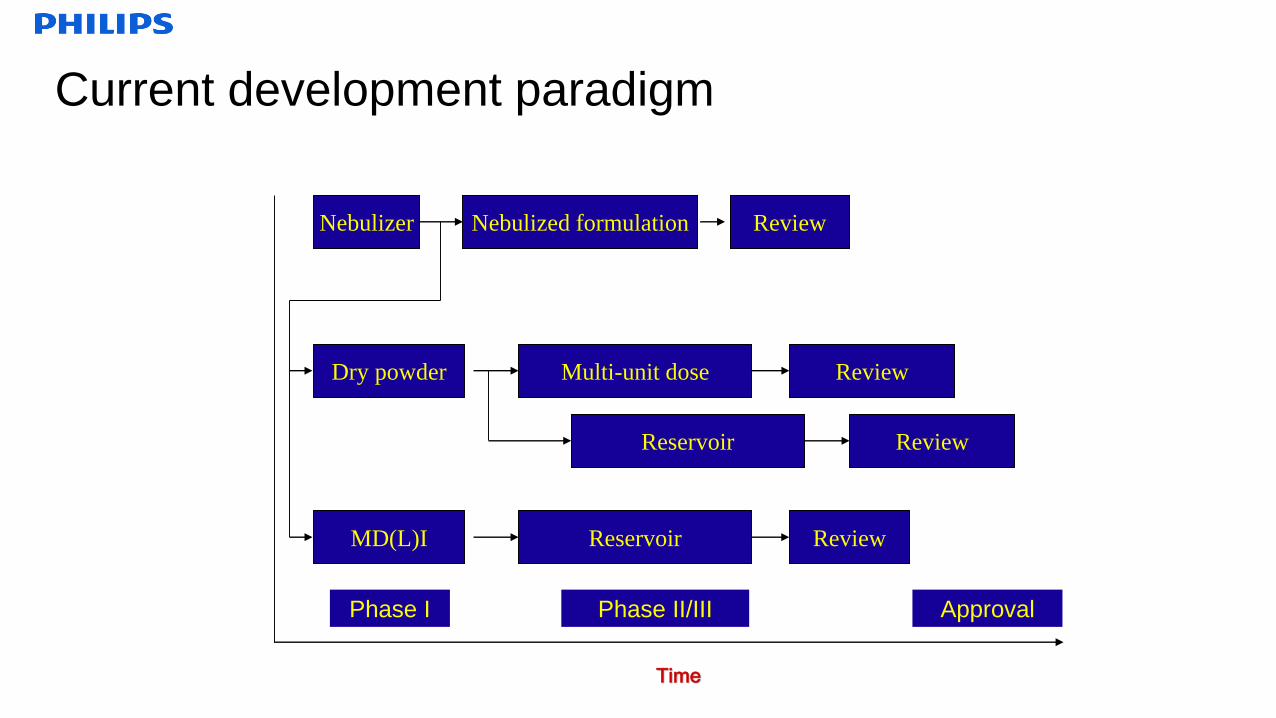

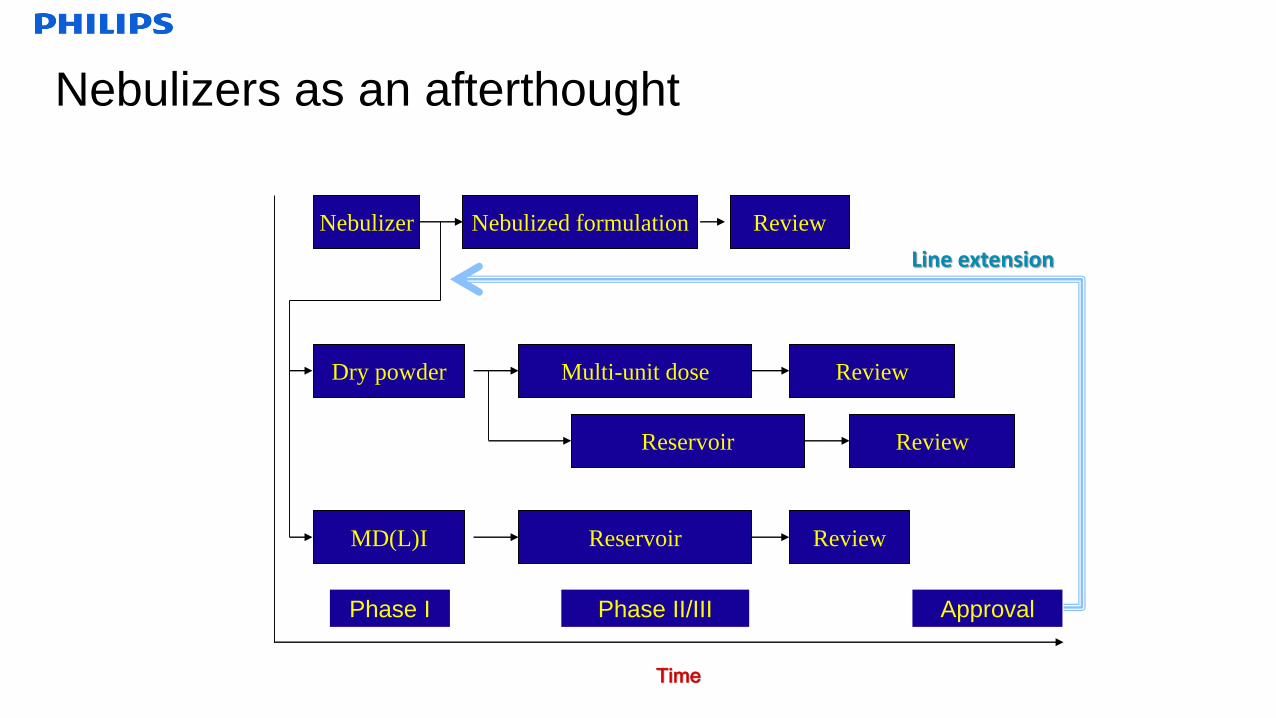

Current development paradigm

Time

Nebulizer

MD(L)I

Dry powder

Phase I ApprovalPhase II/III

ReviewNebulized formulation

Multi-unit dose Review

Reservoir Review

ReviewReservoir

Nebulizers as an afterthought

Time

Nebulizer

MD(L)I

Dry powder

Phase I ApprovalPhase II/III

ReviewNebulized formulation

Multi-unit dose Review

Reservoir Review

ReviewReservoir

Line extension

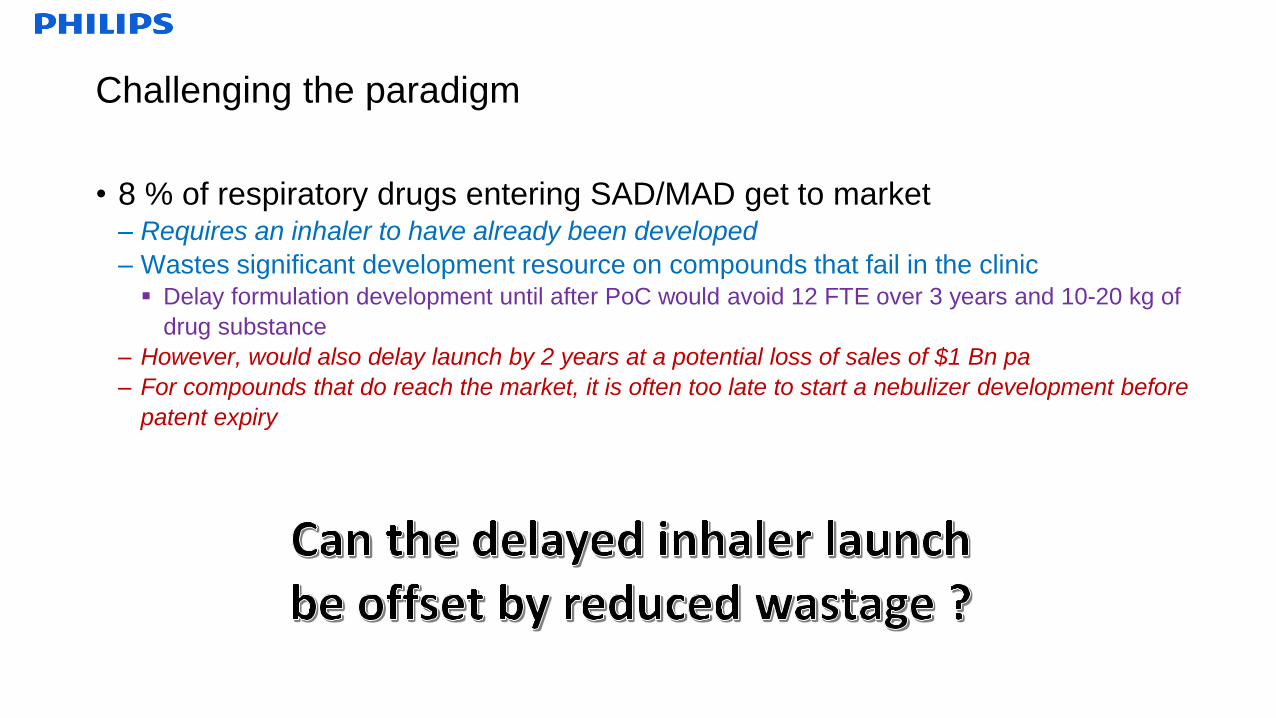

Challenging the paradigm

• 8 % of respiratory drugs entering SAD/MAD get to market– Requires an inhaler to have already been developed

– Wastes significant development resource on compounds that fail in the clinic Delay formulation development until after PoC would avoid 12 FTE over 3 years and 10-20 kg of

drug substance

– However, would also delay launch by 2 years at a potential loss of sales of $1 Bn pa

– For compounds that do reach the market, it is often too late to start a nebulizer development before

patent expiry

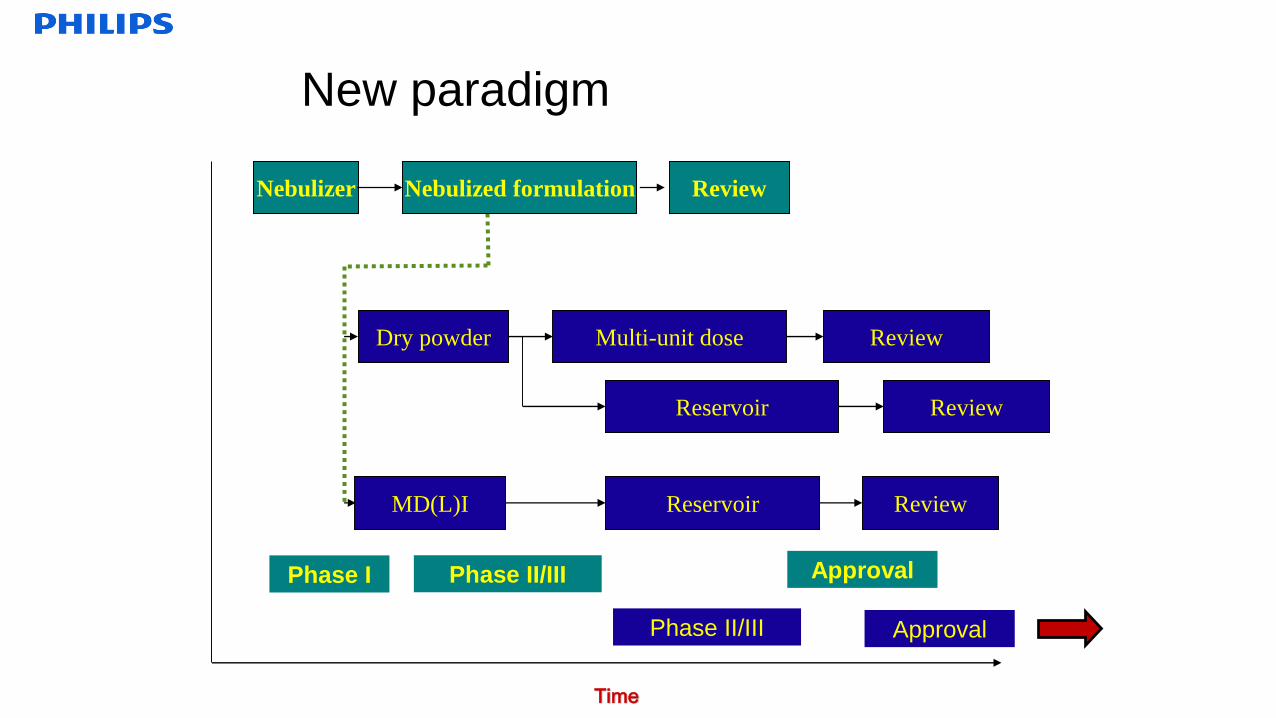

New paradigm

Time

Nebulizer

MD(L)I

Dry powder

Phase I ApprovalPhase II/III

ReviewNebulized formulation

Multi-unit dose Review

Reservoir Review

ReviewReservoir

Phase II/III Approval

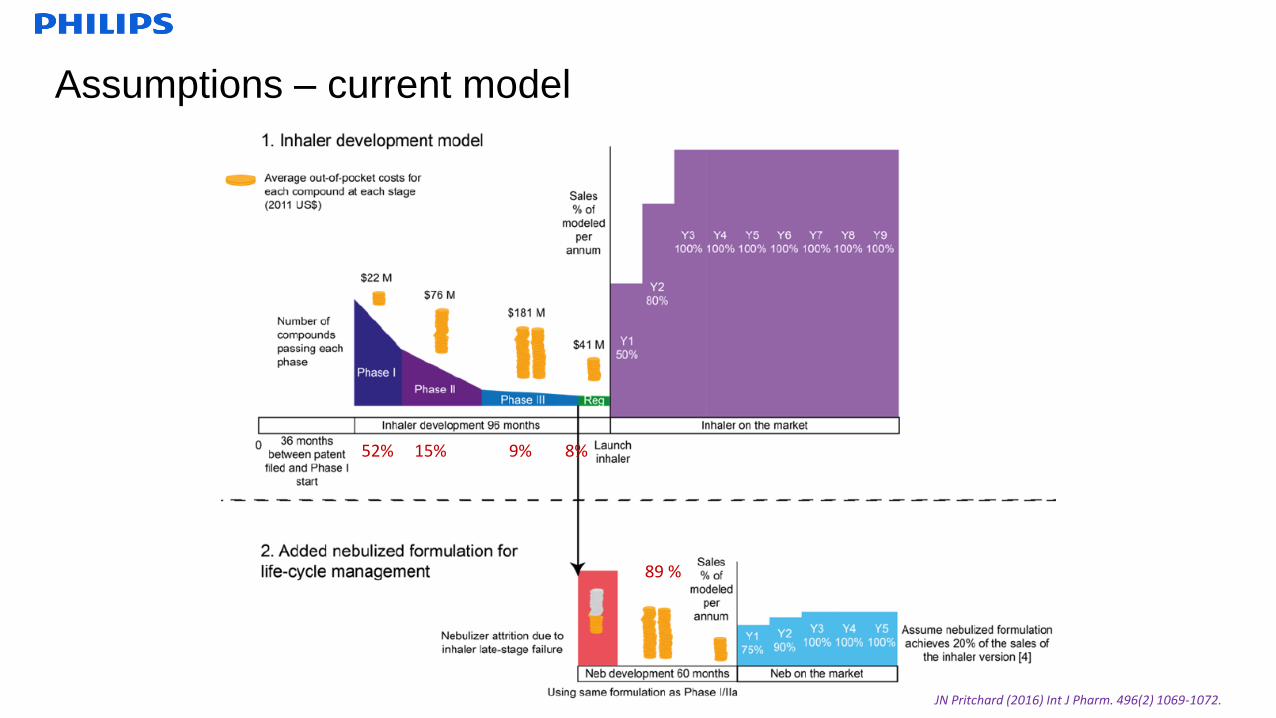

Assumptions – current model

JN Pritchard (2016) Int J Pharm. 496(2) 1069-1072.

52% 15% 9% 8%

89 %

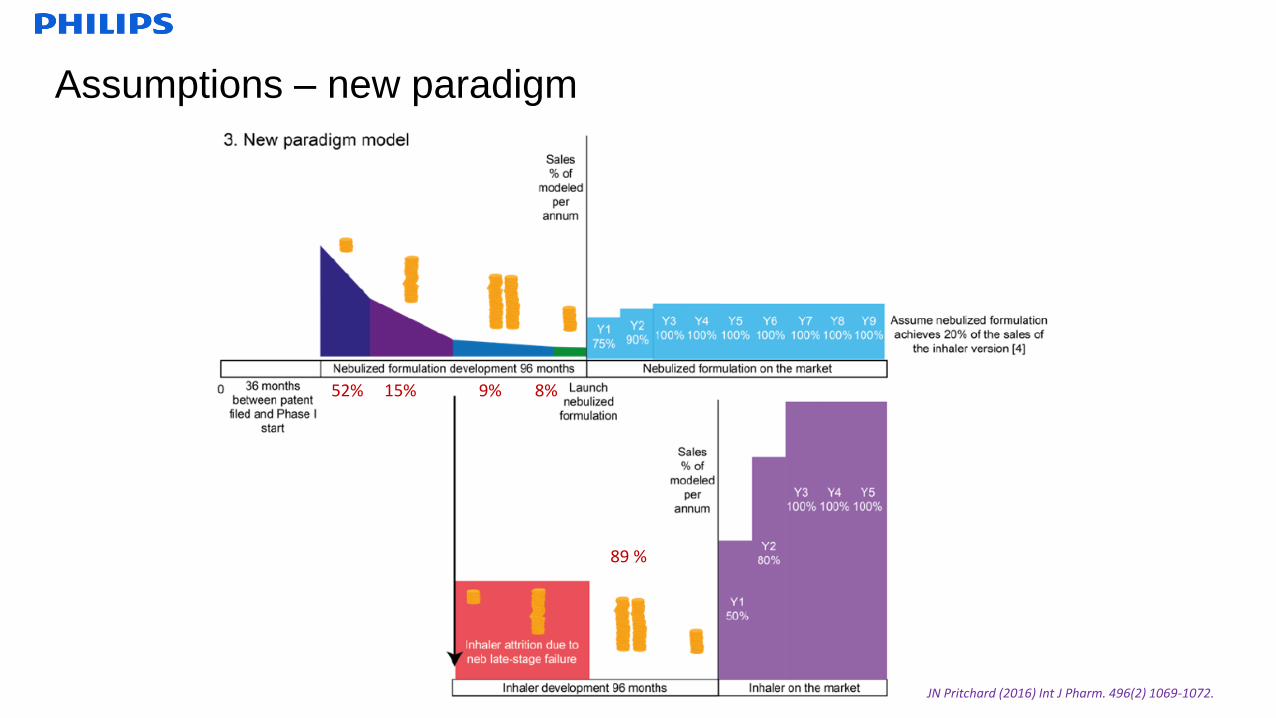

Assumptions – new paradigm

JN Pritchard (2016) Int J Pharm. 496(2) 1069-1072.

52% 15% 9% 8%

89 %

21J Pritchard (2016) Respiratory Drug Delivery 2016, 497-502

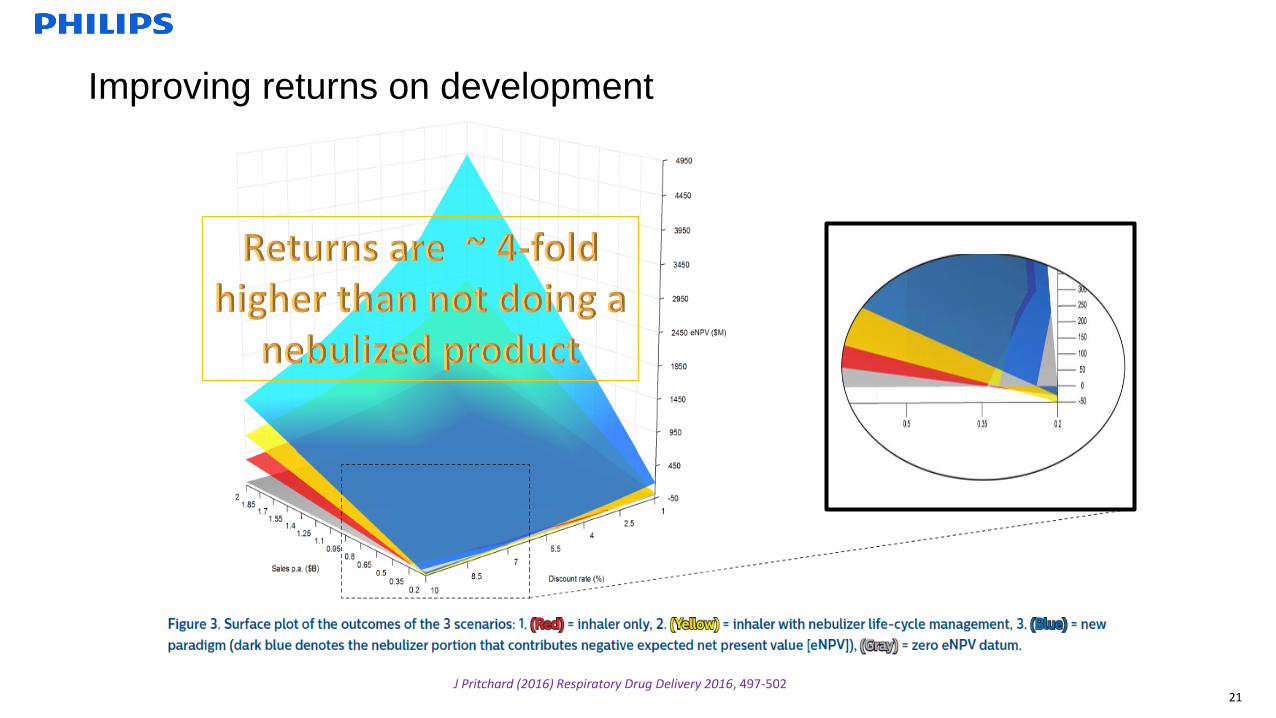

Improving returns on development

Changing the paradigm - to realise the value of nebulized drugs

• 8 % of respiratory drugs entering SAD/MAD get to market– Requires an inhaler to have already been developed

– Wastes significant development resource on compounds that fail in the clinic Delay formulation development until after PoC would avoid 12 FTE over 3 years and 10-20 kg of

drug substance

– However, would also delay launch by 2 years at a potential loss of sales of $1 Bn pa

– For compounds that do reach the market, it is often too late to start a nebulizer development before

patent expiry

Pritchard Int J Pharm 2015, 496:1069–72

• Take the FTIM nebulised formulation right through to market

– Treats the severe patients Underserved today

Most consuming of healthcare resource

• Financial penalties for readmission following exacerbation

Easiest to demonstrate efficacy and pharmacoeconomic benefit

– Improves bottom line ~ $8M saved in development costs (@4*PhI) & ~ $7M increased sales profit p.a.

.... but from a historic perspective

• Cost of Goods– Device

• US: minimum $ 30, typically $ 100, eFlow $ 1500, iNeb $ 3000

• India: range from $15 to > $1000

– Delivery efficiency can be poor if not breath-actuated

• Variable performance from different nebulisers– Multiple devices need to be covered during clinical programme

– Device specific registration and promotion

• Restricted formulary

– Increased sales and marketing costs

• Hardware is not patient-friendly– Transportation, cleanliness (microbiology), delivery time

– Pharmaceutical discharge to the environment

– Maintenance

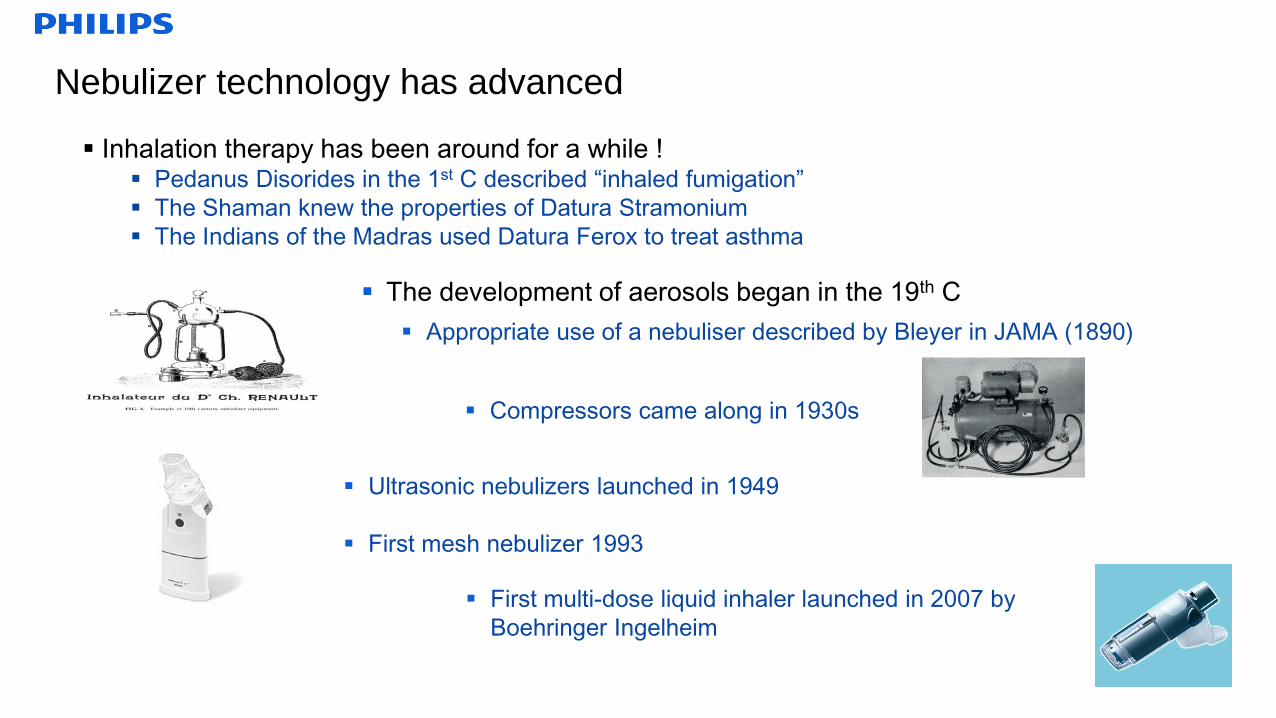

The development of aerosols began in the 19th C

Appropriate use of a nebuliser described by Bleyer in JAMA (1890)

Nebulizer technology has advanced

Inhalation therapy has been around for a while ! Pedanus Disorides in the 1st C described “inhaled fumigation”

The Shaman knew the properties of Datura Stramonium

The Indians of the Madras used Datura Ferox to treat asthma

Compressors came along in 1930s

Ultrasonic nebulizers launched in 1949

First mesh nebulizer 1993

First multi-dose liquid inhaler launched in 2007 by

Boehringer Ingelheim

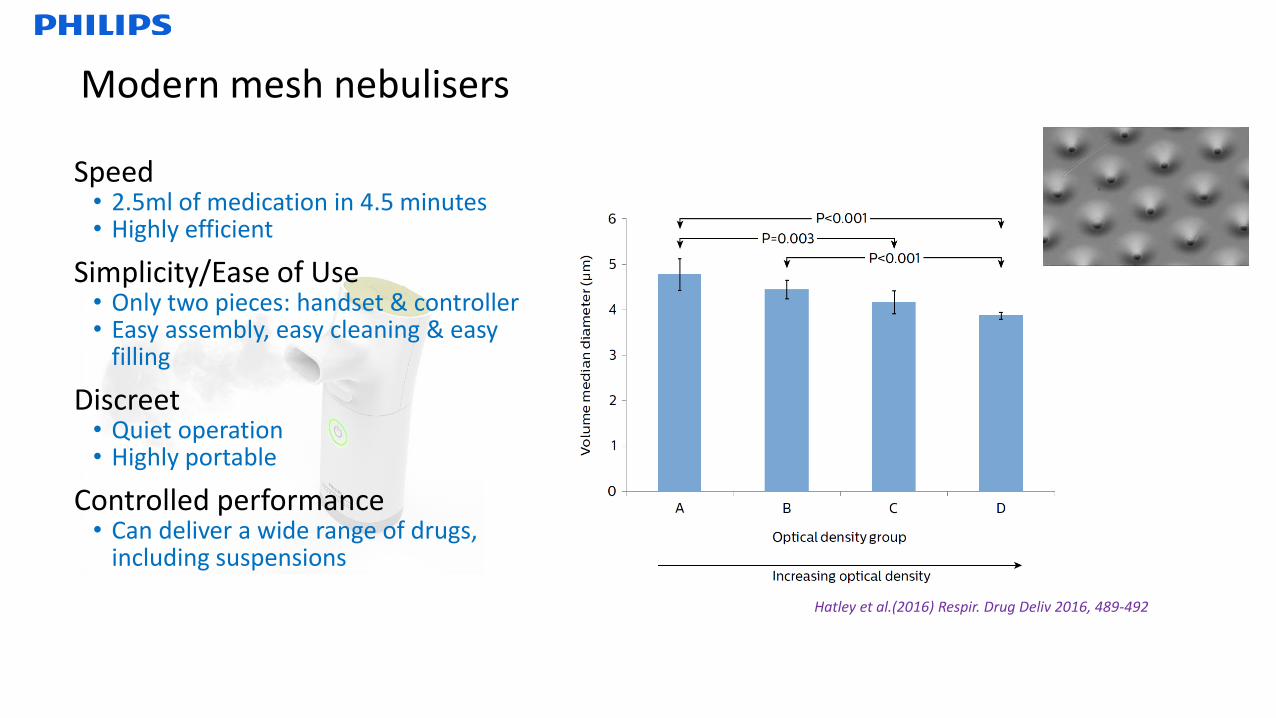

Modern mesh nebulisers

Hatley et al.(2016) Respir. Drug Deliv 2016, 489-492

Speed• 2.5ml of medication in 4.5 minutes • Highly efficient

Simplicity/Ease of Use• Only two pieces: handset & controller • Easy assembly, easy cleaning & easy

filling

Discreet• Quiet operation • Highly portable

Controlled performance• Can deliver a wide range of drugs,

including suspensions

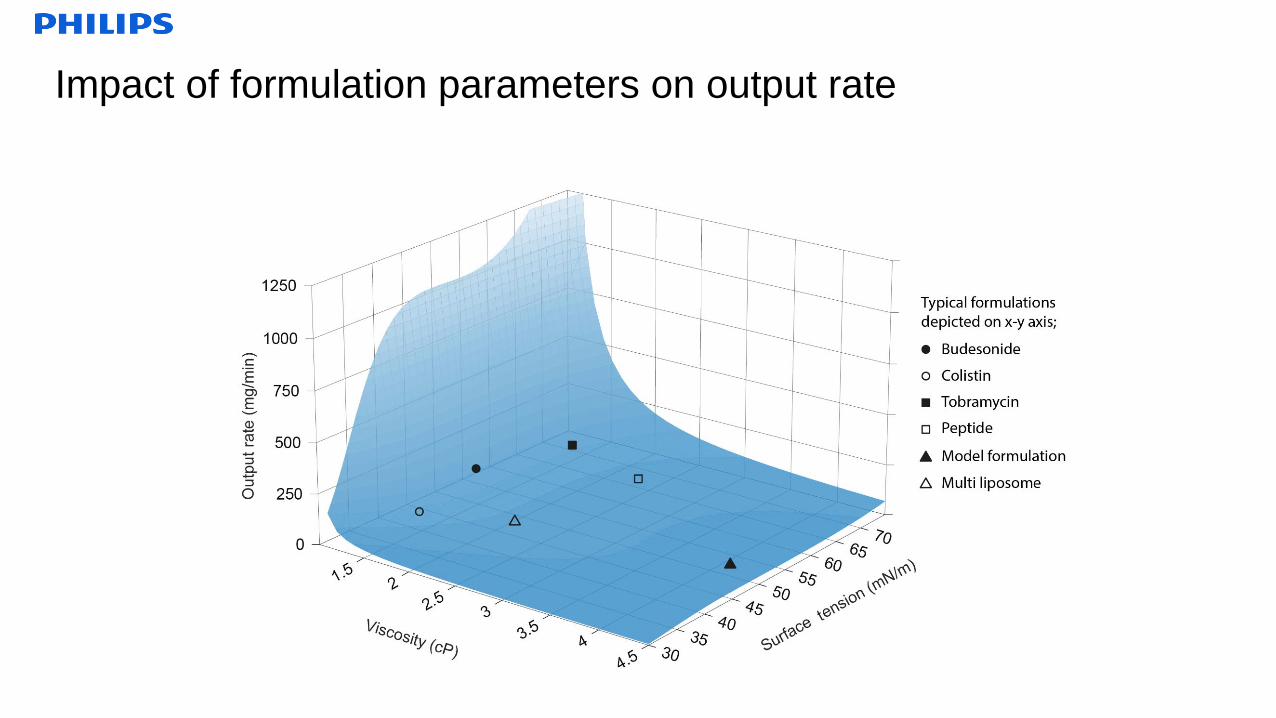

Impact of formulation parameters on output rate

10

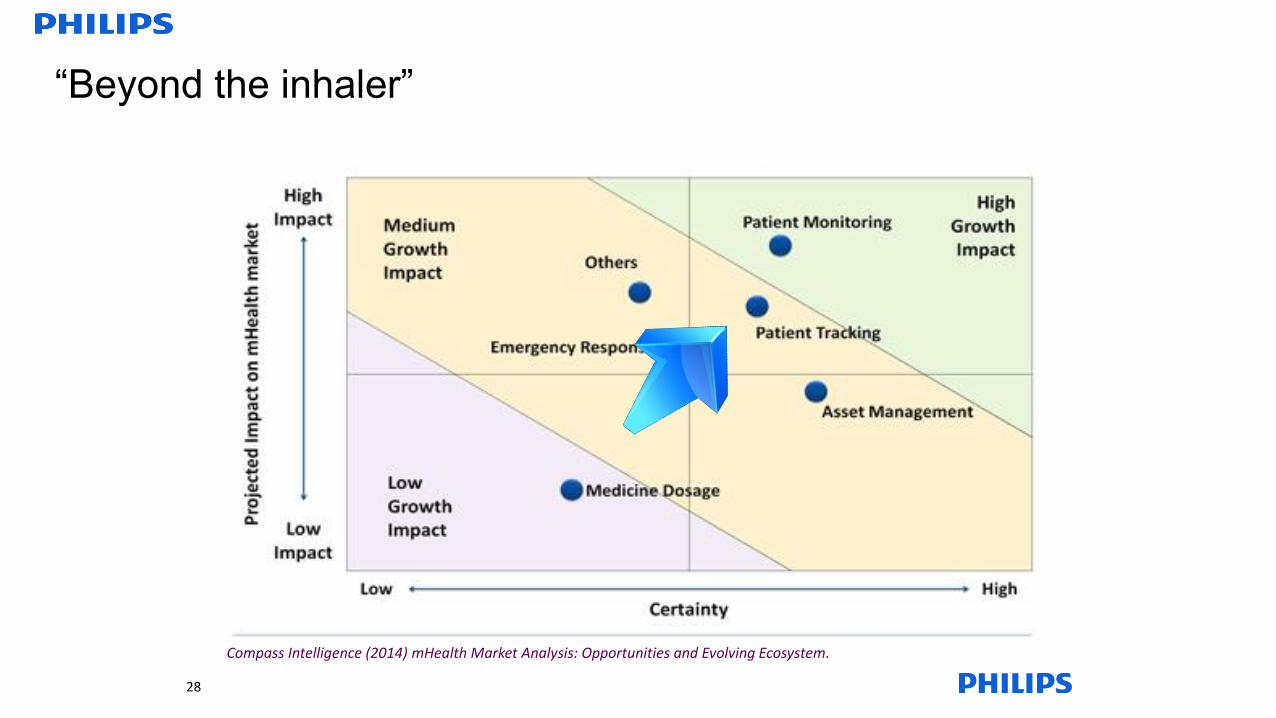

“Beyond the inhaler”

Compass Intelligence (2014) mHealth Market Analysis: Opportunities and Evolving Ecosystem.

28

Device Training Sustaining

Match inhaler to

patient

Use the patient’s

“language”

Electronic

instruction

Forgiving of poor

technique

Check inspiratory

manoeuvre

Check adherence and

reminders

16

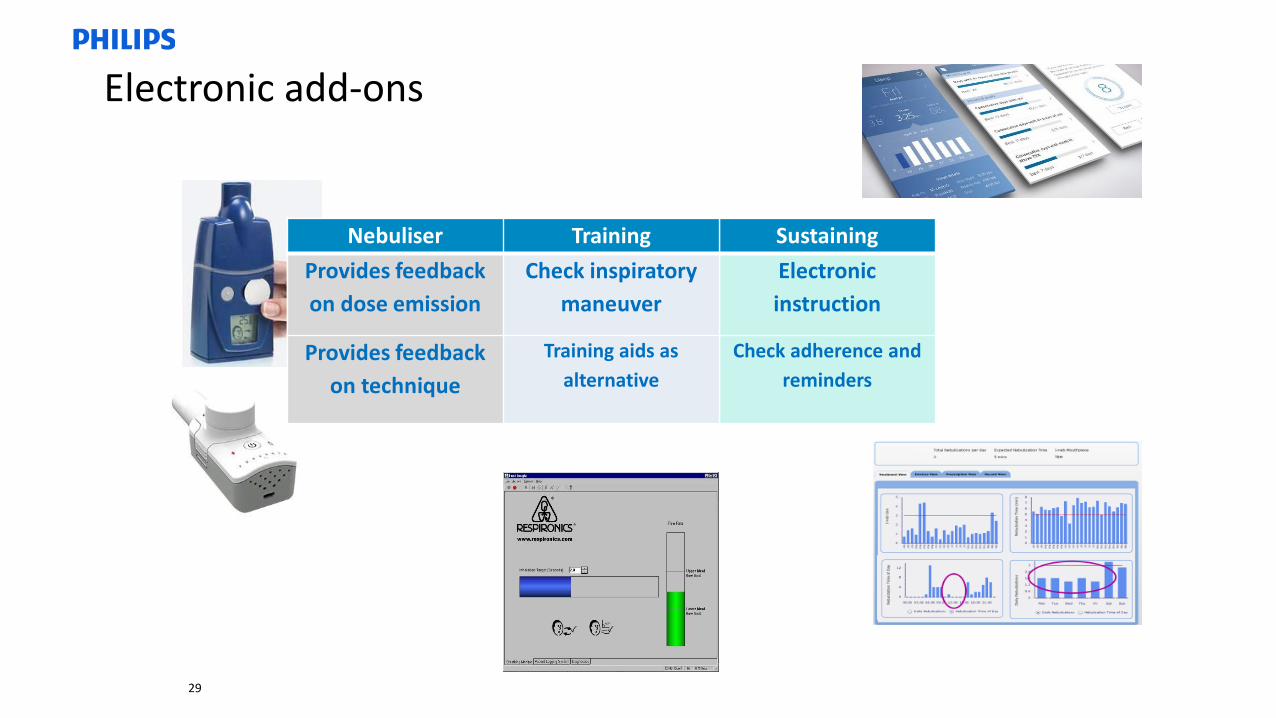

Electronic add-ons

Nebuliser

Provides feedback

on dose emission

Provides feedback

on technique

Nebuliser Training

Provides feedback

on dose emission

Check inspiratory

maneuver

Provides feedback

on technique

Training aids as

alternative

29

Redressing the drawbacks

• Delivery inefficiency

– Breath-actuation

– Low residual volume

• HeteroHomogeneous performance from different nebulisers

– Now regarded as drug-device combinations, other than for well-characterized, prescribed drugs

which have had prior approval from CDER eg. Salbutamol, ipratropium bromide, sodium

cromoglycate.

• For the review of the device component, a manufacturer may either submit a “device module” as component of the

NDA or IND or submit a separate 510(k).

– Tighter controls on device performance

• Hardware is not patient-friendly

– Battery-powered devices

– Simple construction

– Short treatment times

– Low maintenance

– Adherence management

.

Summary

• Despite drawbacks in performance, the

nebulizer drug market has outgrown the

inhaler market, and is currently growing faster

• Driven by Asian markets and by COPD

increasing

• There is a lack of long-acting drugs available

in nebulized form

• Bring the nebulized version to market first to

avoid missing the opportunity

• The technology has advanced

• Look “beyond the inhaler” to provide additional

protection

N B U R