Embed Size (px)

Citation preview

Innovative Analytics for Traditional, Social, and Text Data Dr. Gerald Fahner, Senior Director Analytic Science, FICO

Big Data – the Fuel “is high-volume, high-velocity and high-variety information assets that demand cost-effective, innovative forms of information processing for enhanced insight and decision making.”

Gartner

Machine Learning - the Engine “is a scientific discipline that explores the construction and study of algorithms that can learn from data. Such algorithms operate by building a model from example inputs and using that to make predictions or decisions, rather than following strictly static program instructions. Machine learning is closely related to and often overlaps with computational statistics; a discipline that also specializes in prediction-making.”

Wikipedia

Hot Trends in Predictive Analytics

Big Data and Machine Learning can help you to

Predict consumer behavior more accurately

To unlock this value requires domain expertise to build

Comprehensible models for justifiable decisions

Big data-driven

learning

Domain expertise

Deeper Insights - Stronger Predictions – Better Decisions

Balance Number Crunching With Expertise Domain Expert – the Driver

Informing Origination Risk Score Development by Machine Learning

Improving Insurance Fraud Model With Social Network Variables

Evaluating Predictive Power of Text Data for a Peer Lending Network

Case Studies

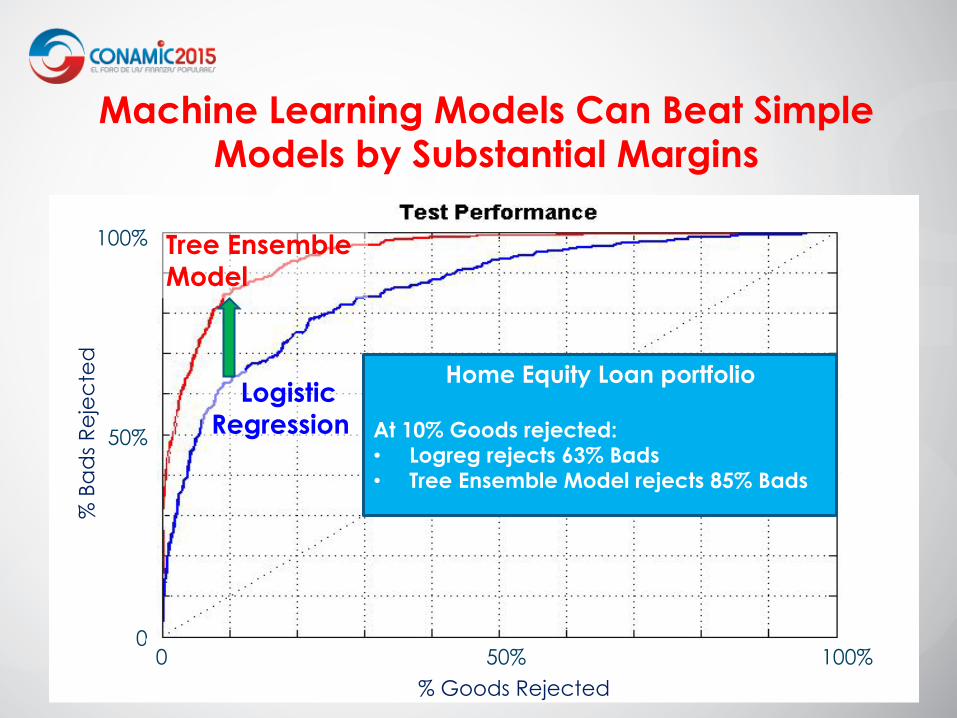

Tree Ensemble Model

Logistic Regression

100%

50%

0

% B

ad

s R

eje

cte

d

0 50% 100% % Goods Rejected

Home Equity Loan portfolio

At 10% Goods rejected: • Logreg rejects 63% Bads • Tree Ensemble Model rejects 85% Bads

Machine Learning Models Can Beat Simple Models by Substantial Margins

Training Data Prediction Function

Predictors

Ou

tco

me

s

Tree 1

Tree 2

Tree 200

Combine predictions

from 200 trees

Tree Ensemble Model

Predictors

Random Forest

Gradient Boosting

?

Scored!

New case

Sco

re

Anatomy of a Tree Ensemble Model

-2-1

01

2

-2-1

01

2-10

-5

0

5

10

Noisy training samples

Predictive relationship from which data were generated (“ground truth”)

Ou

tco

me

s

Predictors

Demonstration Problem

Tree 1

Weighted Average

-2-1

01

2

-2-1

01

2-10

-5

0

5

10

Stochastic Gradient Boosting 1’st Tree

Tree 1

Tree 5 Weighted Average

-2-1

01

2

-2-1

01

2-10

-5

0

5

10

Stochastic Gradient Boosting 5 Trees

Tree 1

Tree 200

Weighted Average

-2-1

01

2

-2-1

01

2-10

-5

0

5

10

Stochastic Gradient Boosting 200 Trees

2

11

1

3 2

5 11

7

1

3 2

5 11

7

1

2

11

1

3 2

5 11

7

1

3

5

7

1

3 2

5 11

7

3

5

7

1

3 2

5 11

7

1

3 2

5 11

7

1

3 2

5 11

7

1

3 2

5 11

7

6

4 10

12 13 6

8 9

4

13 6

8 9

8 9

4

13 6

8 9 8 9

4 10

12 13

10

12 13 6

8 9

4 10

12 13 6

8 9

10

12 4 10

12 13 6

10

12

4 10

12 13 6

8 9

4 10

12 13 6

8 9

4 10

12 13 6

8 9

Direct Inspection Yields a Black Box

DEBTINC 1.00 DELINQ 0.49 VALUE 0.45 CLAGE 0.40 DEROG 0.34 LOAN 0.25 CLNO 0.24 MORTDUE 0.23 NINQ 0.23 JOB 0.20 YOJ 0.20 REASON 0.07

Variable Importance Relative to most

important variable

Interaction Test Statistics Whether a variable interacts

with other variables

DEBTINC 0.029 VALUE 0.022 CLNO 0.014 CLAGE 0.013 DELINQ 0.010 YOJ 0.008 MORTDUE 0.007 LOAN 0.007 DEROG 0.006 JOB 0.006

Useful Diagnostic Information

Input/Output Simulation Create Deeps Insight Into Black Box

x1

)...( 1121 Pxxx

Condition values of all other predictors to data

Black box model (already trained)

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2 -8 -6 -4 -2 0 2 4 6 8

Sweep through range of Score as

function of

?

Non-intuitive Associations Can Lead to Unjustifiable Credit Decisions

Associa'on … (a,er controlling for all else) … Could lead to decision

Loan Applica'on: Consumers with 10% debt ra4o have lower risk score than consumers with 30% debt ra4o

Applicant is rejected because her debt ra4o is not high enough(!?)

Mortgage Lending: Consumers without previous mortgage have lower risk score than consumers with previous mortgage

Applicant can’t get a mortgage because he doesn’t have a mortgage(!?)

Practical Pitfalls Hindering Deployment of Machine Learning Models

PROS

Highly accurate fit to data

Discovery of unexpected associa4ons

Automated, produc4ve analysis

CONS

Hard to impose domain exper4se

Vulnerable to data limita4ons

May capture non-‐intui4ve associa4ons

Pros and Cons of Machine Learning Models for Credit Scoring

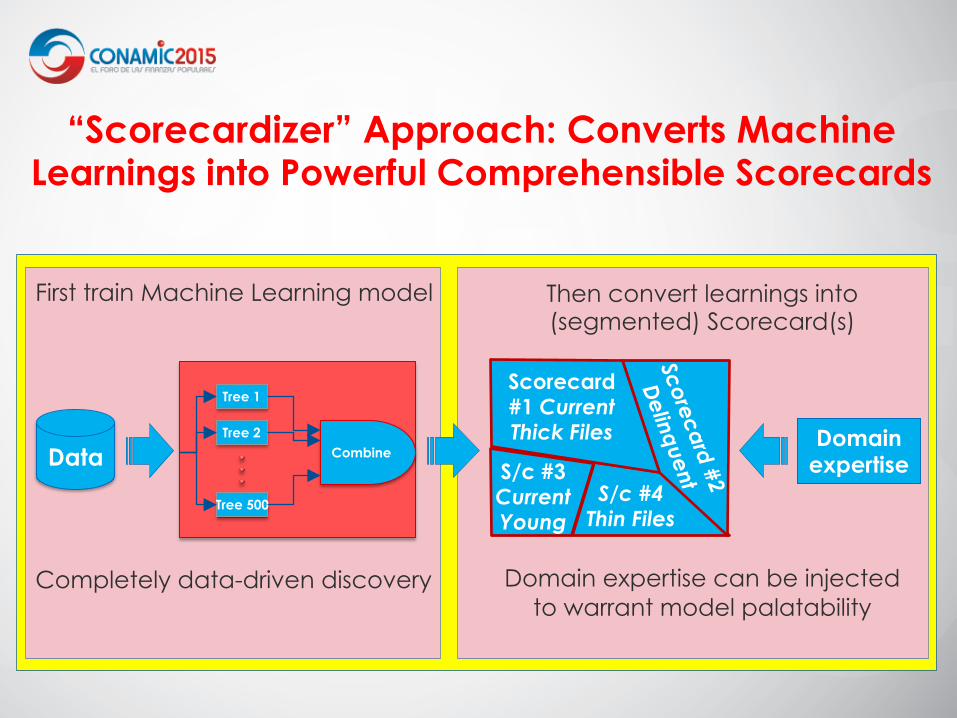

Then convert learnings into (segmented) Scorecard(s)

Domain expertise can be injected to warrant model palatability

First train Machine Learning model Completely data-driven discovery

Tree 1

Tree 2

Tree 500

Combine

Scorecard #1 Current Thick Files

S/c #4 Thin Files

S/c #3 Current Young

Domain expertise

“Scorecardizer” Approach: Converts Machine Learnings into Powerful Comprehensible Scorecards

Data

• In well-defined domains (e.g. credit scoring), can codify expertise

• Scorecardizer hooks into a database of expert rules, which enables fully automatic construction of palatable models – Manual refinement of the “end product” by domain experts is

still possible before deployment

Some examples of codified expertise

• Everything else equal:

– Score must not increase with higher Debt Ratio

– Score must not decrease with Applicant Age above 60 years

– For current accounts, a history of delinquency is bad

– For 2-cycle delinquents, history of mild delinquency can be good (these have shown their capacity to recover)

Can We Automate Expertise?

100

50

0

% B

ads

Rej

ecte

d

S/c #1 S/c #2 S/c #3 S/c #4 S/c #5

Scorecard segmentation discovered by Scorecardizer

Age of oldest credit line

Value of Current Property

5-fold cross-validated AUC

Tree Ensemble: incomprehensible 0.96

Scorecardizer: 5 comprehensible segmented scorecards

0.94

Single comprehensible scorecard 0.91

Results for Home Equity Loan Portfolio

0 50 100 % Goods Rejected

Informing Origination Risk Score Development by Machine Learning

Improving Insurance Fraud Model With Social Network Variables

Evaluating Predictive Power of Text Data for a Peer Lending Network

Case Studies

Florida $1 Million in

worker’s compensation fraud ring

New York $279 Million in

insurance fraud ring

20

Insurance Fraud and Networks

Predicting Fraud with Traditional and Network Data

Age Income Credit Score

Fraud

Adam 21 7,000 680 0

Beth 36 3,200 744 0

Carl 62 9,000 803 1

Dave 32 4,250 713 0

Eva 49 800 720 0

Customer-specific predictors

Traditional fraud score

Adam

Eva

Carl

Beth

Dave

Money transfer connection Similar address connection

Network variables

Predict

Combine

22

Enhancing Data with Network Variables

Age Income Credit Score

Adam 21 7,000 680

Beth 36 3,200 744

Carl 62 9,000 803

Dave 32 4,250 713

Eva 49 800 720

Avg. Age of Connections

# Money Transfers in Network per Month

Fraud

23 2 0

45 3 0

21 7 1

37 3 0

55 4 0

Variables derived from network • Graph algorithms • Feature generation • Feature evaluation • Feature selection

0

10

20

30

40

50

60

70

80

90

100

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

% D

ete

cte

d

% Reviewed

Boosting Auto Insurance Fraud Detection with Network Information

After adding network variables

Traditional variables only

+14%

24

Variable Importance Top 10 Variables

Rank Variable Name

1 Car Model

2 Total Paid Amount in Network

3 Policy Holder Occupation

4 Pre-accident Vehicle Value

5 Total # Payments in Network

6 # Phantom Vehicles in Network

7 ZIP Code of Policy Holder

8 Size of Network

9 Repairable Flag

10 Type of Accident

Network Variables

Informing Origination Risk Score Development by Machine Learning

Improving Insurance Fraud Model With Social Network Variables

Evaluating Predictive Power of Text Data for a Peer Lending Network

Case Studies

Call center records, claims, public records, collector notes, emails, blogs, social data, freeform comments, reviews, webpages, product descriptions,

transcribed phone calls, news articles…

Is there predictive value? How can we leverage it for comprehensible

models and justifiable decisions?

Semantic Scorecards & Topic Analysis

Ubiquitous Text Data Can Be Predictive and Yield New Insights

Hi, thanks for considering my request. I’m a student in Southern California. I have a great credit score. I will use this loan to pay my rent, books and tuition expenses. I’ve secured a part time job. My federal loans take care of all the rest. Thanks! Last summer we’ve extended our business for second-hand furniture into Southern Florida. We’ve been growing nice there. We need $4,000 to do enlarge showroom. Expecting to double sales thereafter. Sincerely, D.J. I need this loan to pay off higher rate credit card debt - fixed rate at 15%, that’s the only card I use.

Structured origination information

Generate traditional variables Extract keywords and topics

“Semantic Scorecard”: Combine traditional variables and text-based features in a comprehensible model

Prospect ID #5340164: “I need this loan to pay off higher rate credit card debt - fixed rate at 15%, that’s the only card I use”

Origination Risk for Peer-to-Peer Lending Network

Associated Loan Descriptions

Predictive Value of Text Data

Winner: Regular and text data Runner-up: Regular data only For comparison: Text data only

0 100

% Goods Rejected

100

0

% B

ads

Rej

ecte

d

Traditional variables (black) Keywords indicating elevated risk (red) Keywords indicating reduced risk (green)

Rank Variable Name

1 Credit Bureau Grade 2 Inquiries During Last 6 Months 3 Monthly Income 4 Months Since Last Record 5 need 6 Revolving Credit Balance 7 baby 8 Loan Purpose 9 business

10 would 11 Revolving Line Utilization 12 qualify 13 Length of Employment 14 sincerely 15 credit

Rank Variable Name

16 provided 17 sales 18 job 19 open 20 stable 21 payday 22 card 23 www 24 Open Credit Lines 25 Total Credit Lines 26 shop

Top Predictors From Automatic Variable Selection Lead to Unjustifiable Decisions

debt, free, consolidating, consolidated, card, credit, revolving, paying, payoff, sooner, quicker, clear, accumulated,

accrued, completely, …

business, equipment, sales, capital, store, marketing, experience, location, expand,

owner, retail, advertising, partner, inventory, products, profit, shop, restaurant, ...

Reduced risk topic: “Credit card consolidation”

Elevated risk topic: “Business-related items”

Gained New Insights Into Risk Topics Results Using “Latent Dirichlet Allocation”

• Machine learning, text- and social network analytics can yield deeper insights and stronger predictions, by combining traditional and novel data sources.

• Yet to make more profitable and justifiable decisions requires careful results interpretation and robust, explainable models.

• Domain expertise, combined with special methods and tools supporting interpretation, are of utmost importance for harnessing the potential of big data and machine learning.

Discussion