Embed Size (px)

Citation preview

Inside Brazil: The Leading Auto

Manufacturers and Suppliers

Augusto Amorim

© 2012 R. L. Polk & Co. All rights reserved. 2

Brazil Beyond Soccer and Carnival

World Soccer Cup winner five times

World’s 6th largest light vehicle producer

World’s most popular Carnival

World’s 4th largest light vehicle market

© 2012 R. L. Polk & Co. All rights reserved. 3

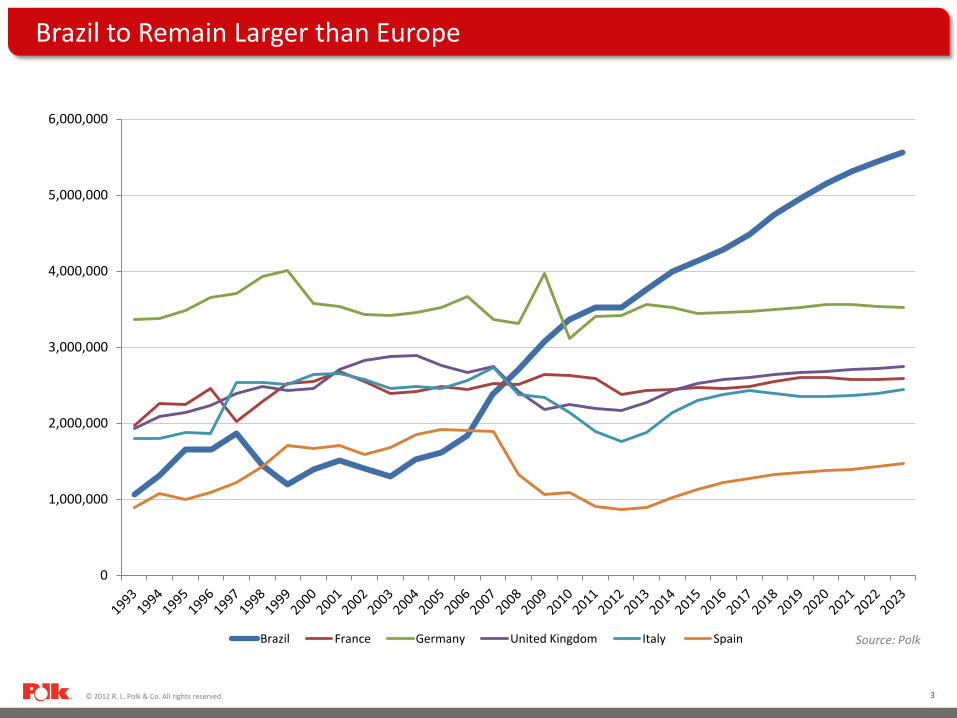

Brazil to Remain Larger than Europe

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Brazil France Germany United Kingdom Italy Spain Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 4

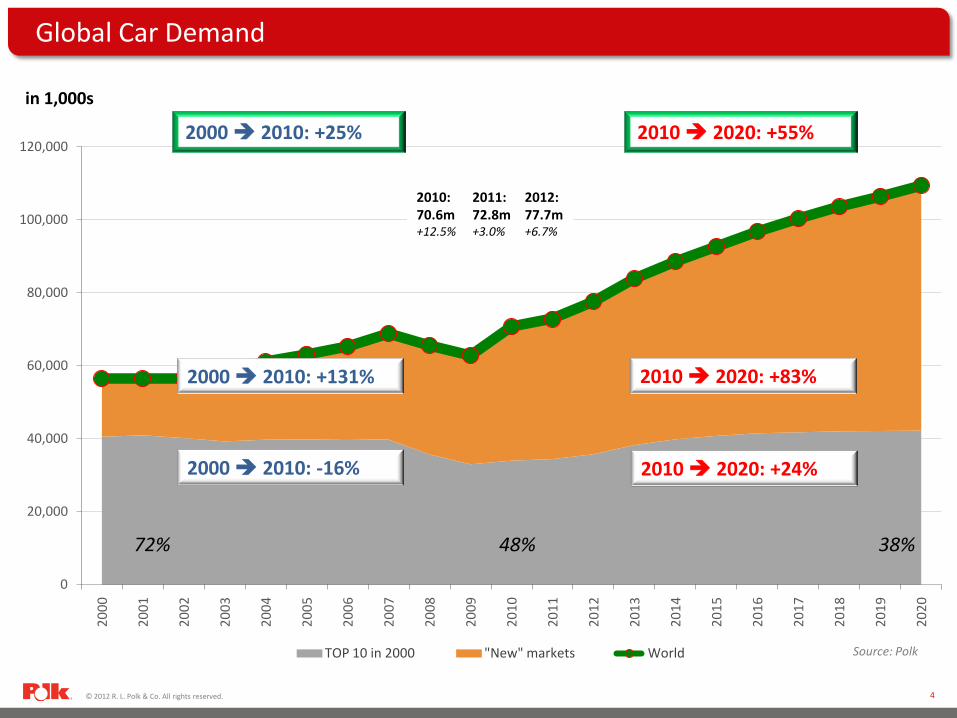

Global Car Demand

0

20,000

40,000

60,000

80,000

100,000

120,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

TOP 10 in 2000 "New" markets World

2000 2010: +25% 2010 2020: +55%

in 1,000s

72% 48% 38%

2000 2010: +131% 2010 2020: +83%

2000 2010: -16% 2010 2020: +24%

2010: 70.6m +12.5%

2011: 72.8m +3.0%

2012: 77.7m +6.7%

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 5

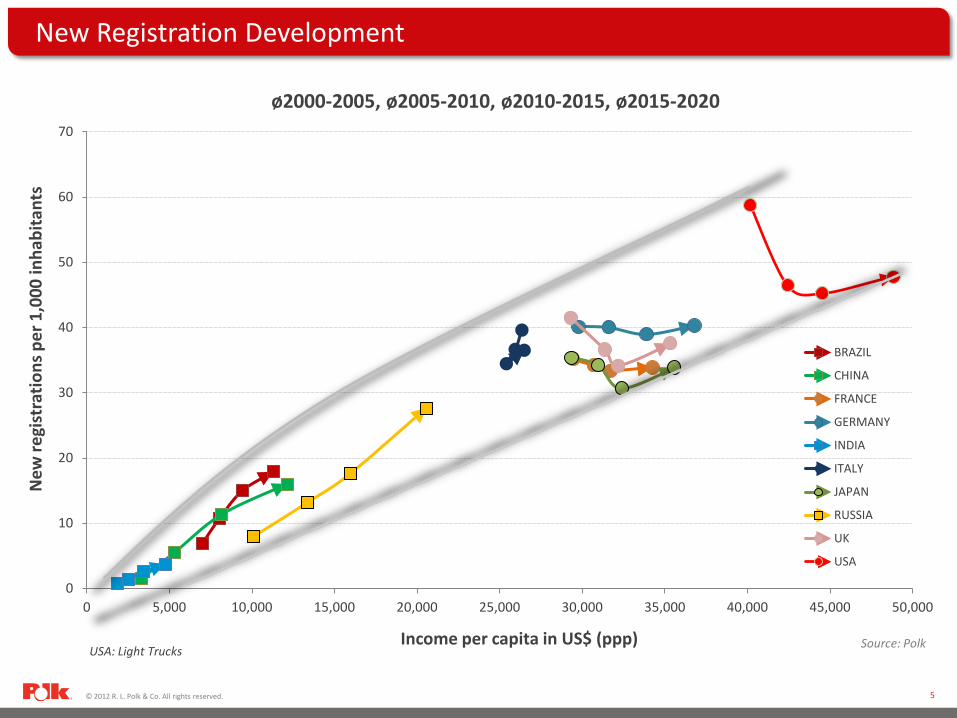

0

10

20

30

40

50

60

70

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

BRAZIL

CHINA

FRANCE

GERMANY

INDIA

ITALY

JAPAN

RUSSIA

UK

USA

ø2000-2005, ø2005-2010, ø2010-2015, ø2015-2020

New Registration Development

USA: Light Trucks

New

regi

stra

tions

per

1,0

00 in

habi

tant

s

Income per capita in US$ (ppp) Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 6

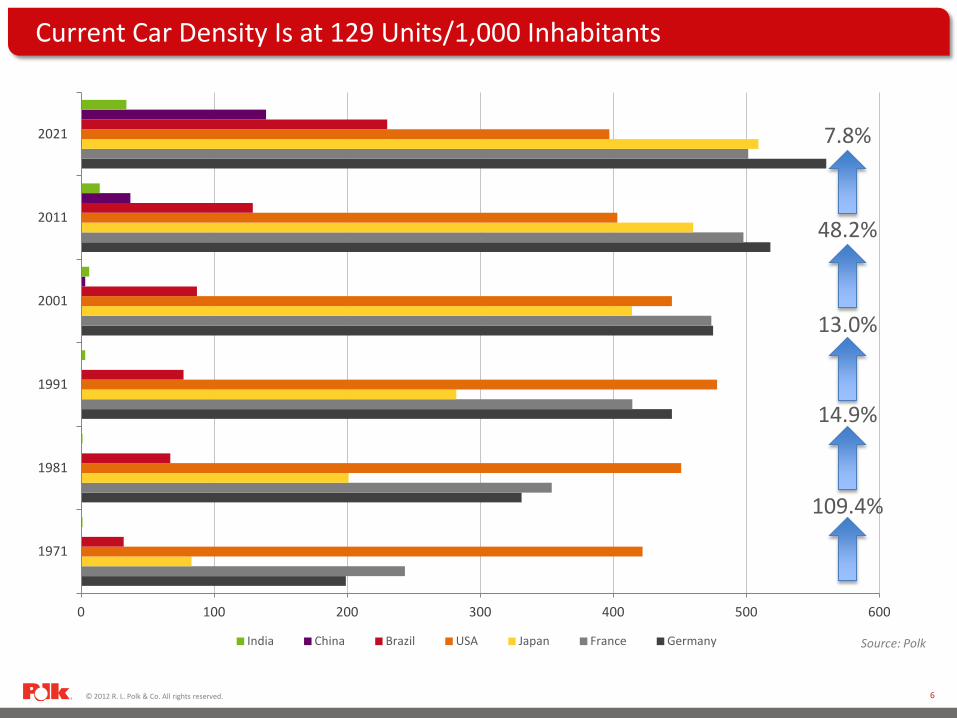

Current Car Density Is at 129 Units/1,000 Inhabitants

0 100 200 300 400 500 600

1971

1981

1991

2001

2011

2021

India China Brazil USA Japan France Germany

109.4%

13.0%

48.2%

14.9%

7.8%

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 7

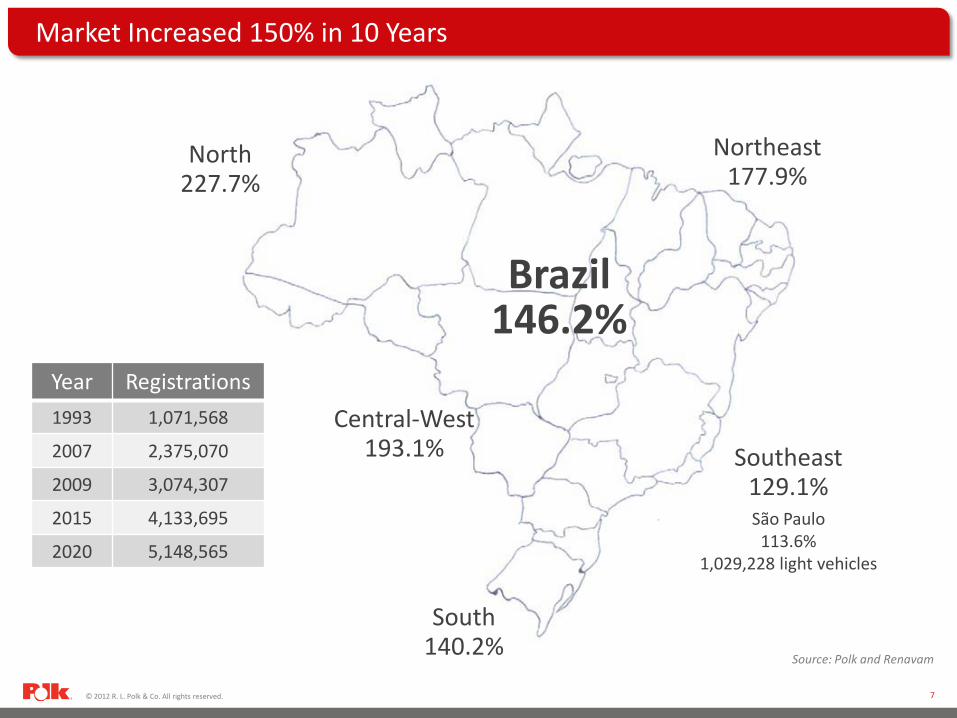

Market Increased 150% in 10 Years

Brazil 146.2%

Northeast 177.9%

South 140.2%

Central-West 193.1%

North 227.7%

Southeast 129.1% São Paulo

113.6% 1,029,228 light vehicles

Year Registrations 1993 1,071,568

2007 2,375,070

2009 3,074,307

2015 4,133,695

2020 5,148,565

Source: Polk and Renavam

© 2012 R. L. Polk & Co. All rights reserved. 8

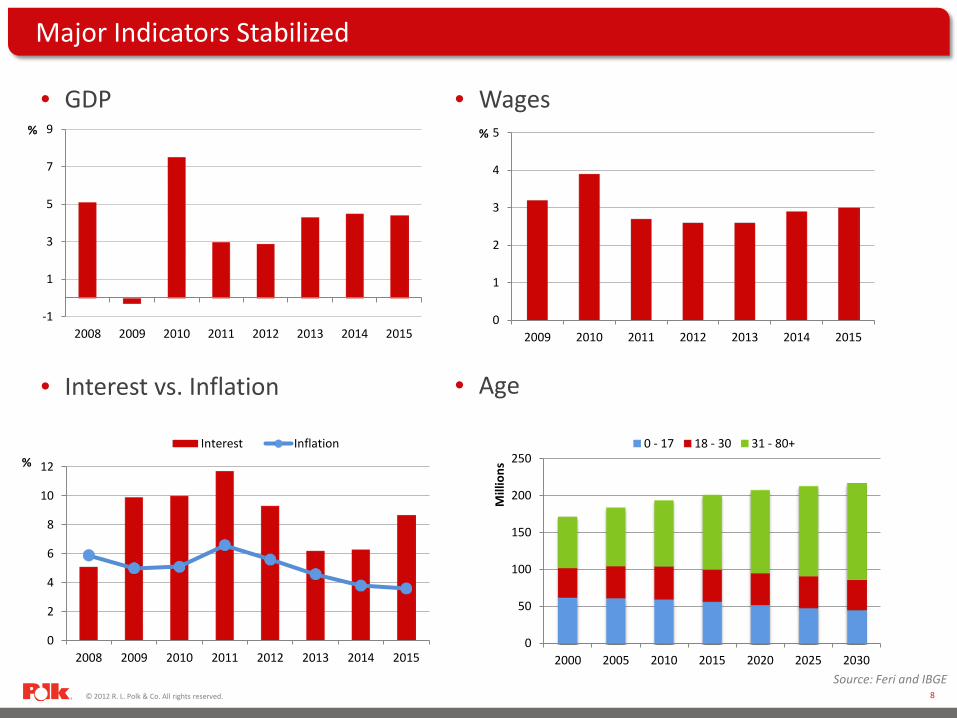

Major Indicators Stabilized

• GDP

• Interest vs. Inflation

• Wages

• Age

-1

1

3

5

7

9

2008 2009 2010 2011 2012 2013 2014 2015

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013 2014 2015

Interest Inflation

0

1

2

3

4

5

2009 2010 2011 2012 2013 2014 2015

0

50

100

150

200

250

2000 2005 2010 2015 2020 2025 2030

Mill

ions

0 - 17 18 - 30 31 - 80+

%

%

%

Source: Feri and IBGE

© 2012 R. L. Polk & Co. All rights reserved. 9

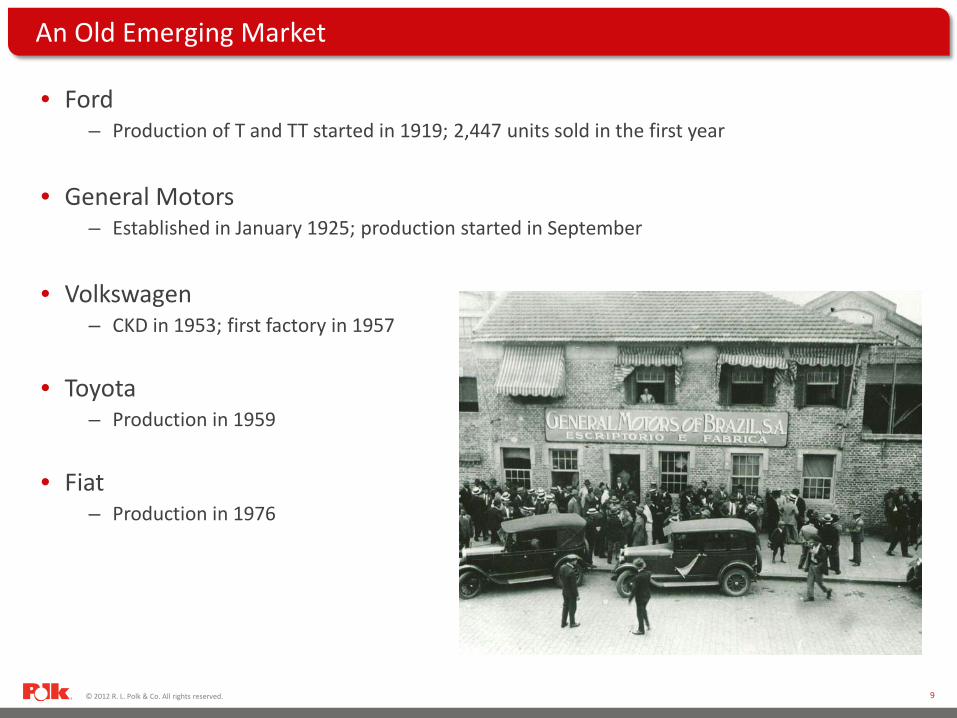

An Old Emerging Market

• Ford – Production of T and TT started in 1919; 2,447 units sold in the first year

• General Motors

– Established in January 1925; production started in September

• Volkswagen – CKD in 1953; first factory in 1957

• Toyota – Production in 1959

• Fiat

– Production in 1976

© 2012 R. L. Polk & Co. All rights reserved. 10

The Big 4 Perceived as Brazilian Brands

• Gurgel

– Production between 1975 and 1993

– Volkswagen powertrain until 1987. Own engine from then on

– Fiberglass body

– 25% of production exported to 40 countries

– Bankruptcy in 1993

• Troller

– Production started in 1997 as RF Sport

– Name changed to T4

– Failure of Pantanal pick-up truck

– Ford bought in 2007 for estimated US$ 220 million

– 19 dealerships

– 1,274 units in 2011

• Agrale

– Founded in 1962 as a tractor producer

– Introduction of trucks in 1982

– Motorcycles between 1983 and 2006

– Marruá developed in 2005 for military and civil use

– 750 units sold until February 2012

© 2012 R. L. Polk & Co. All rights reserved. 11

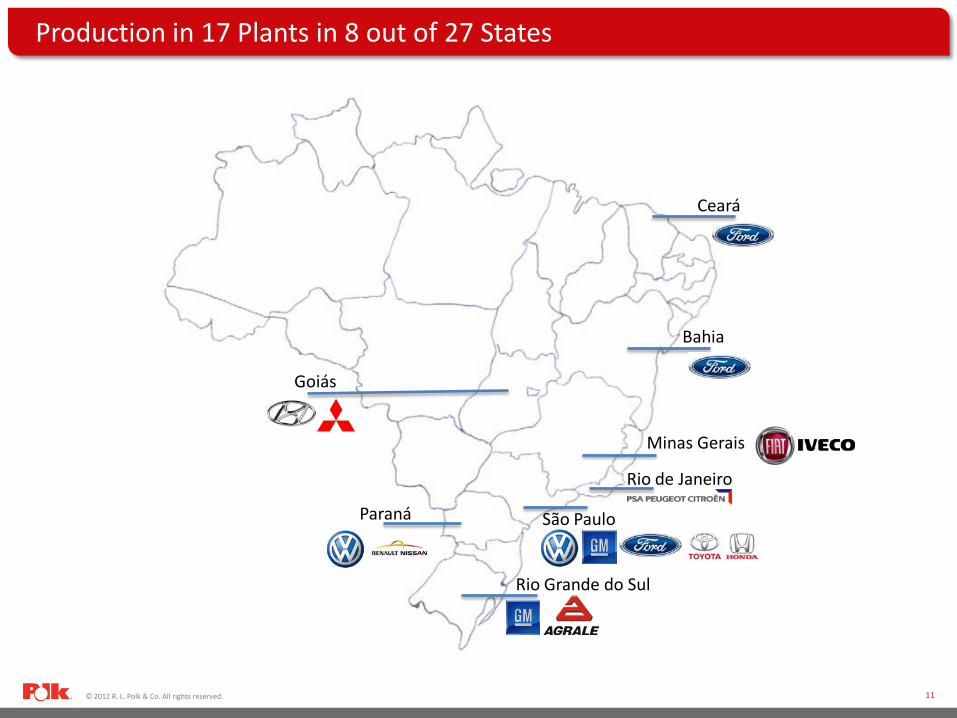

São Paulo

Production in 17 Plants in 8 out of 27 States

Bahia

Rio Grande do Sul

Paraná

Goiás

Minas Gerais

Rio de Janeiro

Ceará

© 2012 R. L. Polk & Co. All rights reserved. 12

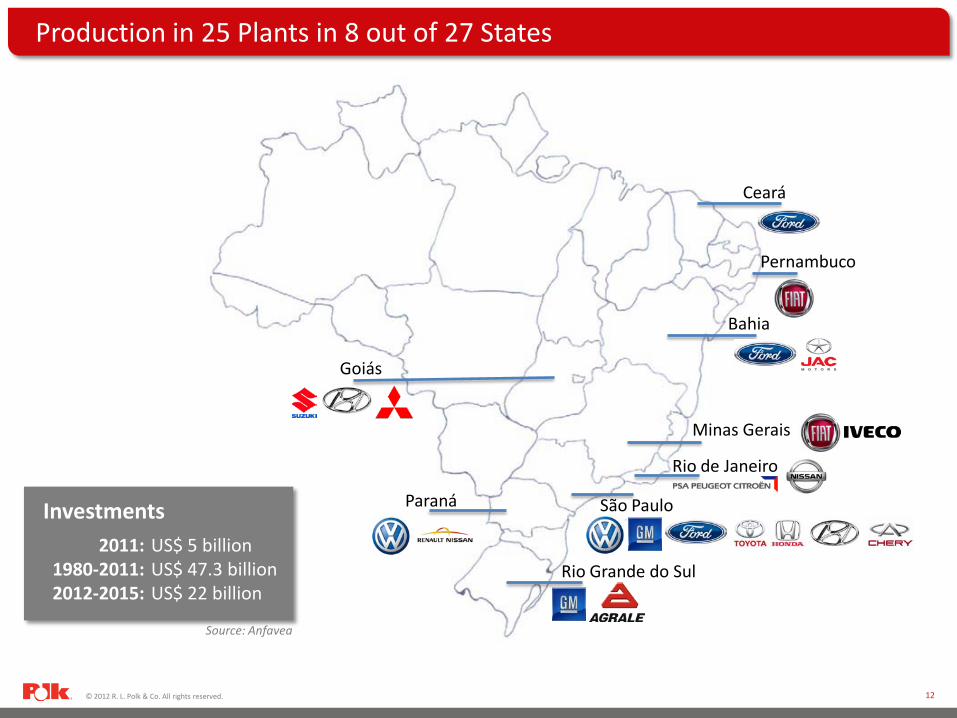

Production in 25 Plants in 8 out of 27 States

Bahia

Rio Grande do Sul

Paraná

Goiás

Minas Gerais

Rio de Janeiro

São Paulo

Pernambuco

Source: Anfavea

Ceará

Investments 2011: US$ 5 billion 1980-2011: US$ 47.3 billion 2012-2015: US$ 22 billion

© 2012 R. L. Polk & Co. All rights reserved. 13

High International Presence Among Suppliers

500 suppliers 60% latent capacity

© 2012 R. L. Polk & Co. All rights reserved. 14

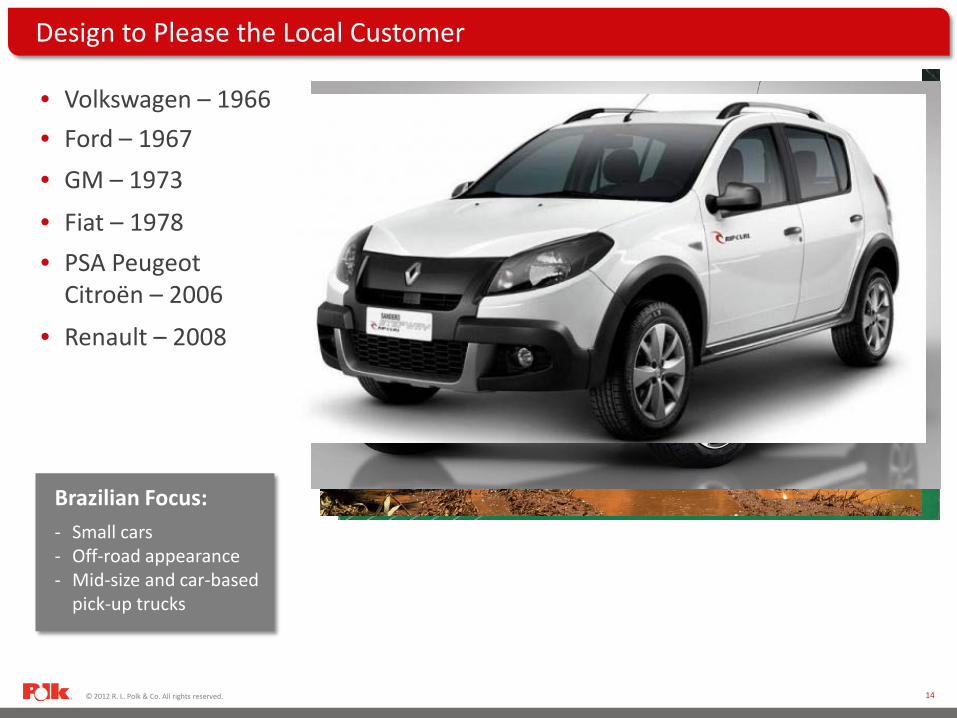

Design to Please the Local Customer

• Volkswagen – 1966 • Ford – 1967 • GM – 1973

• Fiat – 1978

• Renault – 2008

• PSA Peugeot Citroën – 2006

Brazilian Focus: - Small cars - Off-road appearance - Mid-size and car-based

pick-up trucks

© 2012 R. L. Polk & Co. All rights reserved. 15

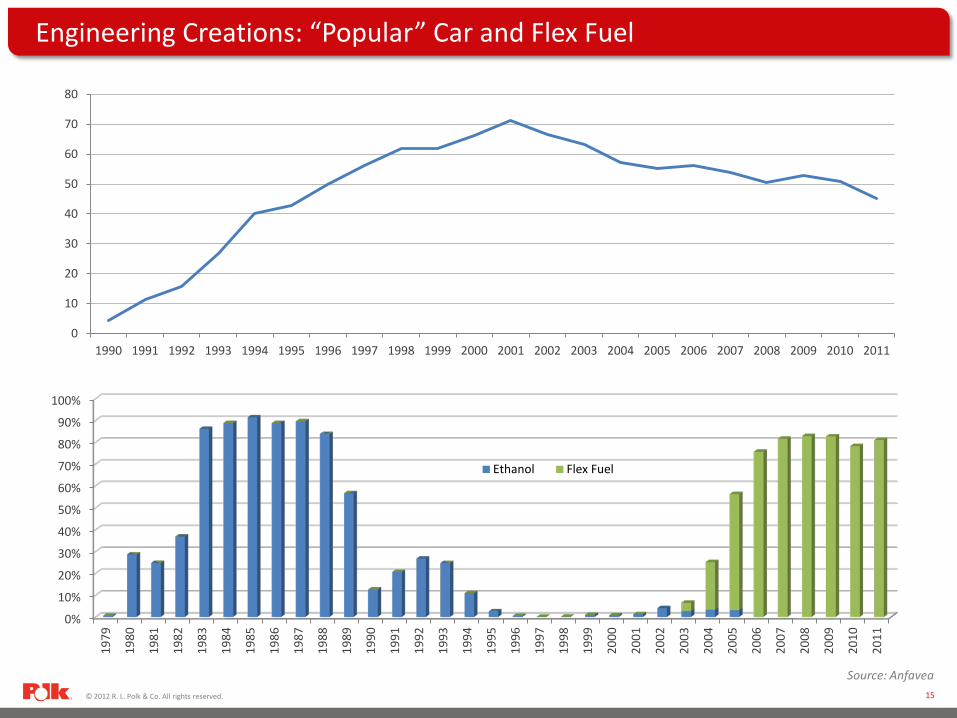

Engineering Creations: “Popular” Car and Flex Fuel

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Ethanol Flex Fuel

0

10

20

30

40

50

60

70

80

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: Anfavea

© 2012 R. L. Polk & Co. All rights reserved. 16

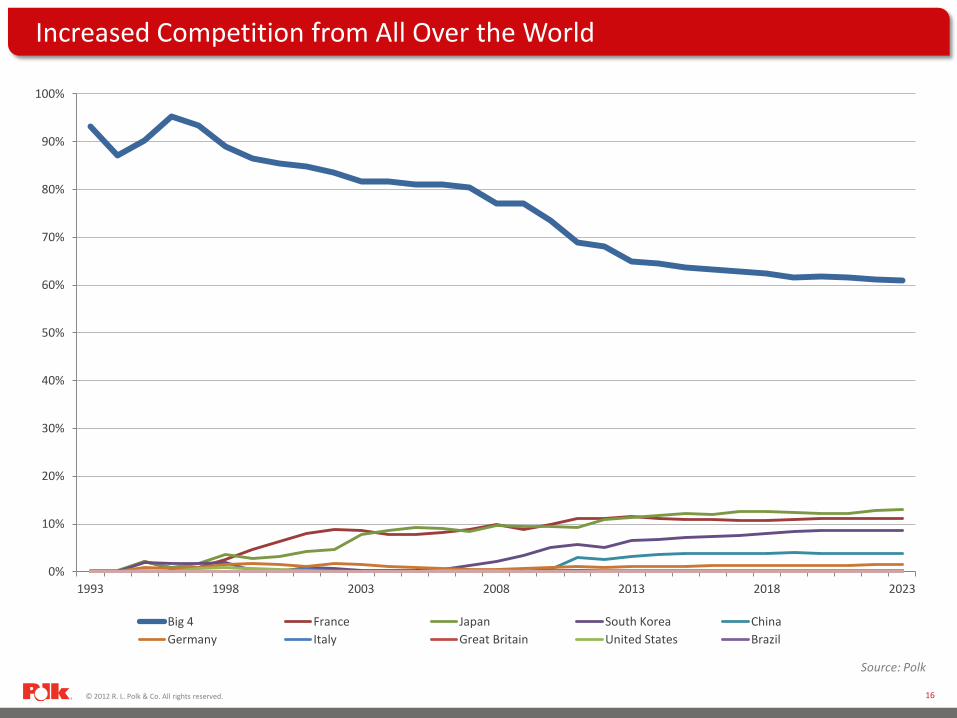

Increased Competition from All Over the World

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1993 1998 2003 2008 2013 2018 2023

Big 4 France Japan South Korea China Germany Italy Great Britain United States Brazil

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 17

0

5

10

15

20

25

Fiat VW Chevrolet Ford Renault

2011 2012 2013

LV: Top 5 Makes Have 75% of the Market

Source: Polk

22.5% 20.2% 16.8% 8.5% 6.2%

© 2012 R. L. Polk & Co. All rights reserved. 18

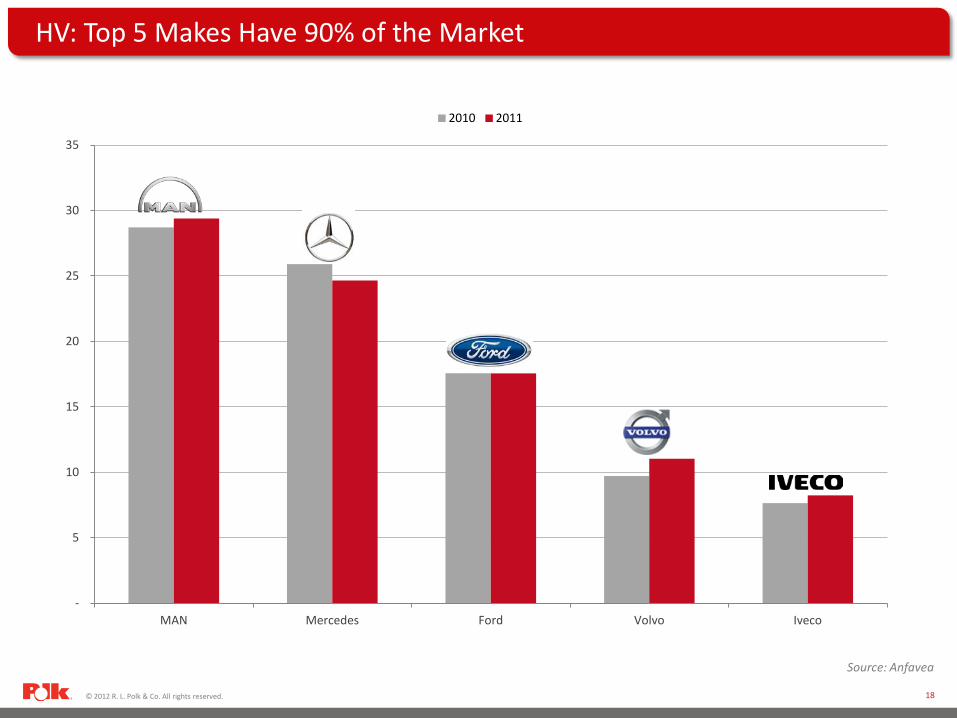

-

5

10

15

20

25

30

35

MAN Mercedes Ford Volvo Iveco

2010 2011

HV: Top 5 Makes Have 90% of the Market

Source: Anfavea

© 2012 R. L. Polk & Co. All rights reserved. 19

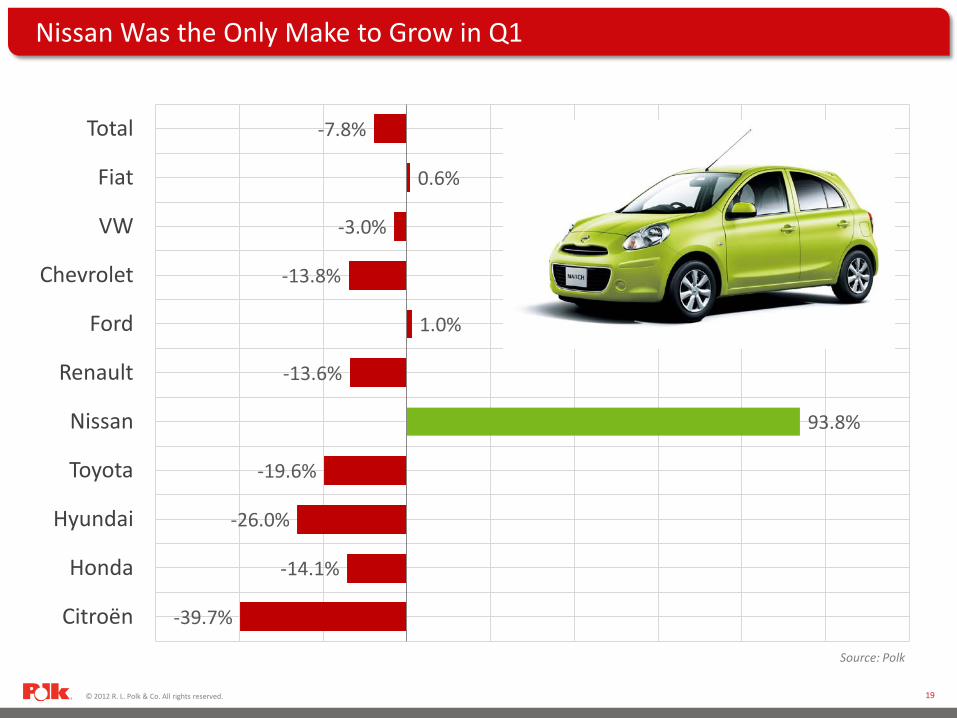

Nissan Was the Only Make to Grow in Q1

-7.8%

0.6%

-3.0%

-13.8%

1.0%

-13.6%

93.8%

-19.6%

-26.0%

-14.1%

-39.7%

Total

Fiat

VW

Chevrolet

Ford

Renault

Nissan

Toyota

Hyundai

Honda

Citroën

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 20

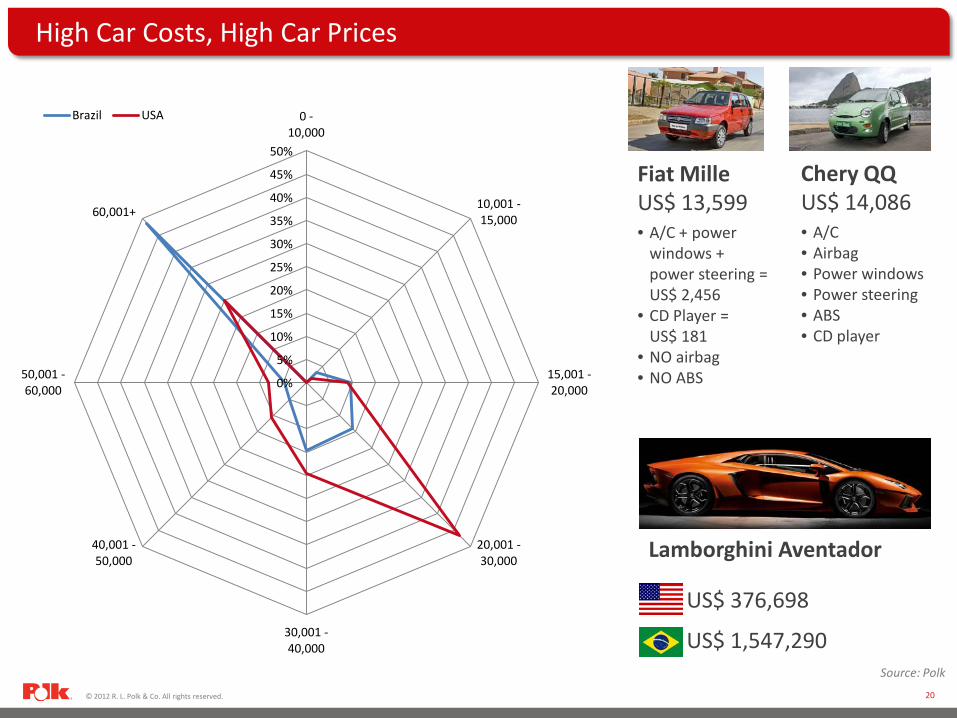

High Car Costs, High Car Prices

Fiat Mille US$ 13,599 • A/C + power

windows + power steering = US$ 2,456

• CD Player = US$ 181

• NO airbag • NO ABS

Chery QQ US$ 14,086 • A/C • Airbag • Power windows • Power steering • ABS • CD player

US$ 376,698

US$ 1,547,290

Lamborghini Aventador

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0 - 10,000

10,001 - 15,000

15,001 - 20,000

20,001 - 30,000

30,001 - 40,000

40,001 - 50,000

50,001 - 60,000

60,001+

Brazil USA

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 21

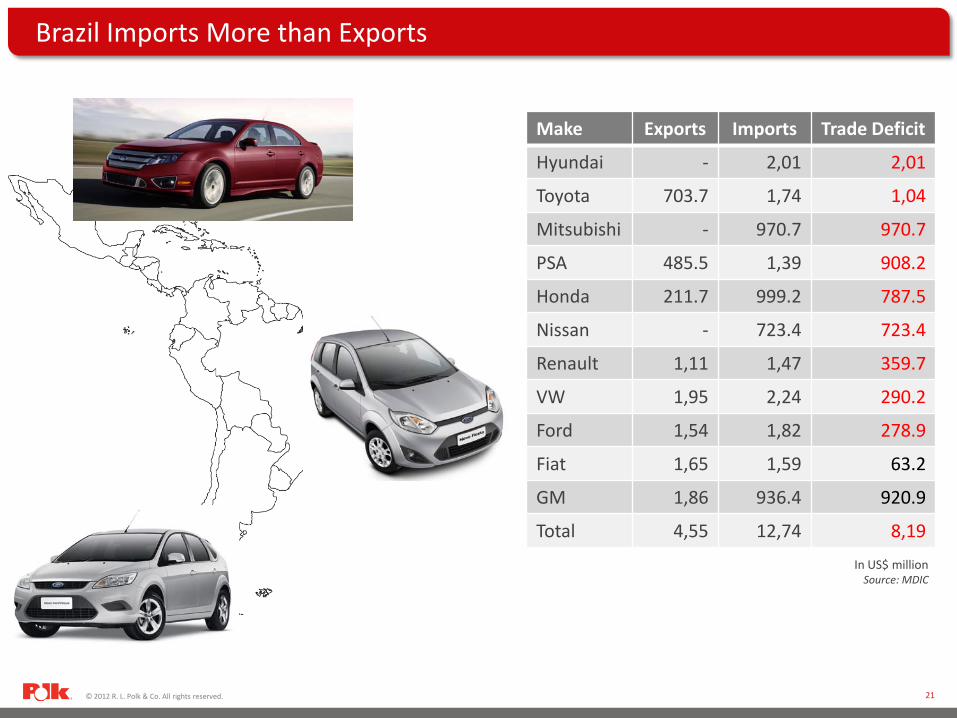

Brazil Imports More than Exports

Make Exports Imports Trade Deficit

Hyundai - 2,01 2,01

Toyota 703.7 1,74 1,04

Mitsubishi - 970.7 970.7

PSA 485.5 1,39 908.2

Honda 211.7 999.2 787.5

Nissan - 723.4 723.4

Renault 1,11 1,47 359.7

VW 1,95 2,24 290.2

Ford 1,54 1,82 278.9

Fiat 1,65 1,59 63.2

GM 1,86 936.4 920.9

Total 4,55 12,74 8,19

In US$ million Source: MDIC

© 2012 R. L. Polk & Co. All rights reserved. 22

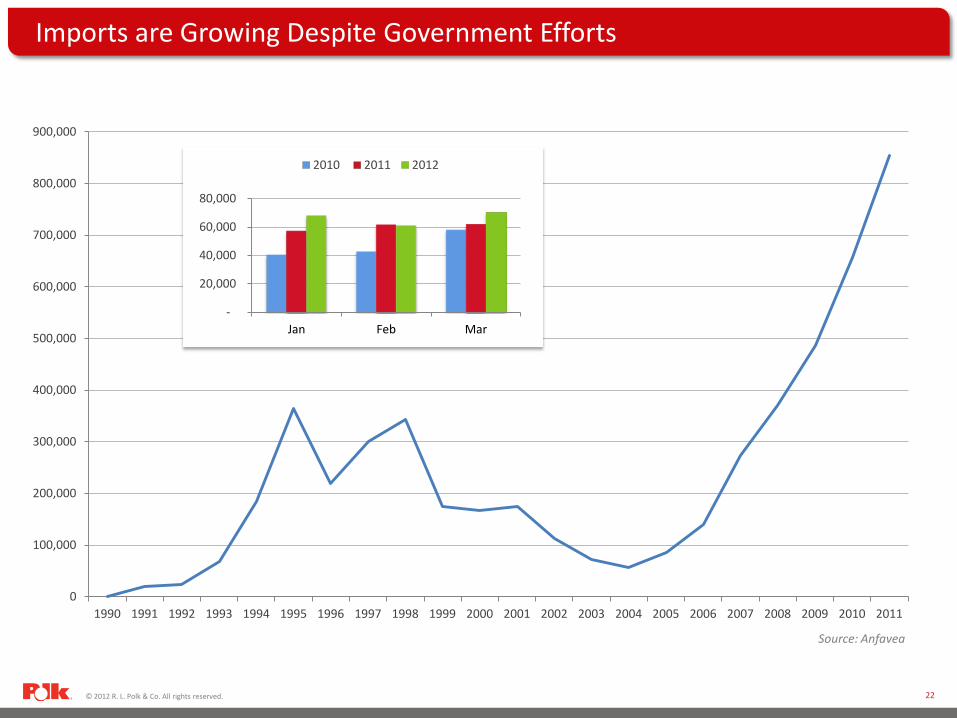

Imports are Growing Despite Government Efforts

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

-

20,000

40,000

60,000

80,000

Jan Feb Mar

2010 2011 2012

Source: Anfavea

© 2012 R. L. Polk & Co. All rights reserved. 23

New Policies to Shape Future of the Industry

• Free trade agreement with Mexico reviewed – US$ 1.45 billion between March 2012 and March 2013

– US$ 1.56 billion between April 2013 and March 2014

– US$ 1.64 billion between April 2014 and March 2015

• New rules to pay less IPI between 2013 and 2017

– Invest 0.15% of revenues in R&D; 0.5% from 2015 onwards

– Invest 0.5% of revenues in engineering and industrial technology; 1% from 2015 onwards

– 8 out of 12 production steps must happen in Brazil; 10 out of 12 from 2016 onwards

– 25% of the line-up must have fuel consumption tag; 100% from 2017 onwards

• Local content

– 55% for OEMs already producing in Brazil – Newcomers have 3 years to reach same level

© 2012 R. L. Polk & Co. All rights reserved. 24

Thank you!

Augusto Amorim Lead Analyst – South America Forecasting

248.728.7436 [email protected]

For more information please visit:

www.polk.com/forecast

Any use of this material including reproduction, modification, distribution or republication without the prior written consent of R. L. Polk & Co. is strictly prohibited.