Embed Size (px)

Citation preview

METROPOLITAN CONDO OUTLOOK WINTER 2015

Insights Into the Apartment Condominium Market in Eight Large Canadian Metropolitan Areas.

About Genworth CanadaGenworth MI Canada Inc. (TSX: MIC) through its subsidi-ary, Genworth Financial Mortgage Insurance Company Canada (Genworth Canada), is the largest private residen-tial mortgage insurer in Canada. The Company provides mortgage default insurance to Canadian residential mort-gage lenders, making homeownership more accessible to first-time homebuyers. Genworth Canada differentiates itself through customer service excellence, innovative processing technology, and a robust risk management framework. For almost two decades, Genworth Canada has supported the housing market by providing thought leader-ship and a focus on the safety and soundness of the mort-gage finance system. As at December 31, 2014, Genworth Canada had $5.8 billion total assets and $3.3 billion total shareholders’ equity.

Find out more at www.genworth.ca.

PrefaceThis report from The Conference Board of Canada and Genworth Canada offers an in-depth analysis of the con-dominium market for eight large Canadian census metro-politan areas (CMAs). The report covers a wide range of condominium market statistics, such as starts, completions, absorptions, and prices. The main goal of this publication is to analyze the recent trends in the condo market in each of the eight CMAs, as well as where each of the eight markets is heading over the next five years.

The eight census metropolitan areas covered are Québec City, Montréal, Ottawa, Toronto, Calgary, Edmonton, Vancouver, and Victoria.

This report is published twice a year, in summer and winter.

Metropolitan Condo Outlook: Insights Into the Apartment Condominium Market in Eight Large Canadian Metropolitan Areasby Jane McIntyre and Robin Wiebe

About The Conference Board of CanadaWe are:

� The foremost independent, not-for-profit, applied

research organization in Canada.

� Objective and non-partisan. We do not lobby

for specific interests.

� Funded exclusively through the fees we charge

for services to the private and public sectors.

� Experts in running conferences but also at con-

ducting, publishing, and disseminating research;

helping people network; developing individual

leadership skills; and building organizational

capacity.

� Specialists in economic trends, as well

as organizational performance and public

policy issues.

� Not a government department or agency,

although we are often hired to provide

services for all levels of government.

� Independent from, but affiliated with, The

Conference Board, Inc. of New York, which

serves nearly 2,000 companies in 60 nations

and has offices in Brussels and Hong Kong.

©2015 The Conference Board of Canada*Published in Canada • All rights reservedAgreement No. 40063028*Incorporated as AERIC Inc.

®The Conference Board of Canada and the torch logo are registered trademarks of The Conference Board, Inc.

Forecasts and research often involve numerous assumptions and data sources, and are subject to inherent risks and uncertainties. This information is not intended as specific investment, accounting, legal, or tax advice.

Contents

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Metropolitan Insights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Québec City . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Montréal. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Ottawa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Toronto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Calgary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Edmonton. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Vancouver . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Victoria. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Definitions and Concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Standard Geographical Classification (SGC) 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Metropolitan Areas With Their Component Census Subdivisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

The Conference Board of Canada/Genworth Canada

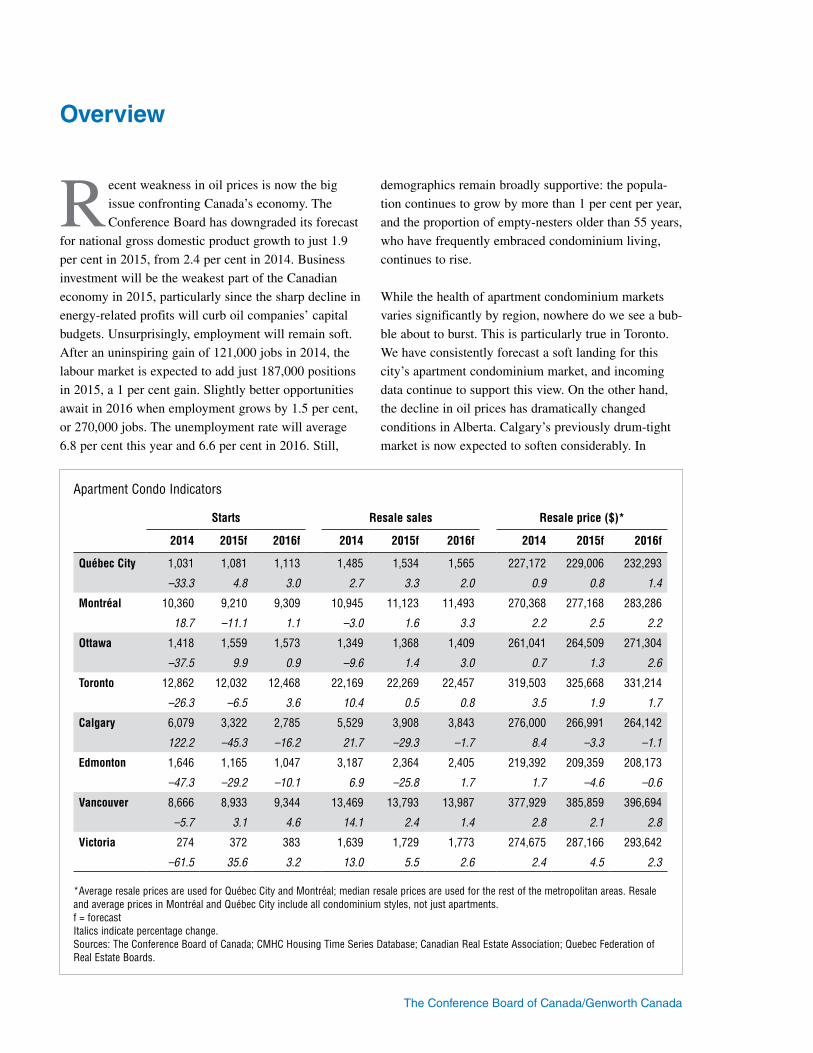

Recent weakness in oil prices is now the big

issue confronting Canada’s economy. The

Conference Board has downgraded its forecast

for national gross domestic product growth to just 1.9

per cent in 2015, from 2.4 per cent in 2014. Business

investment will be the weakest part of the Canadian

economy in 2015, particularly since the sharp decline in

energy-related profits will curb oil companies’ capital

budgets. Unsurprisingly, employment will remain soft.

After an uninspiring gain of 121,000 jobs in 2014, the

labour market is expected to add just 187,000 positions

in 2015, a 1 per cent gain. Slightly better opportunities

await in 2016 when employment grows by 1.5 per cent,

or 270,000 jobs. The unemployment rate will average

6.8 per cent this year and 6.6 per cent in 2016. Still,

demographics remain broadly supportive: the popula-

tion continues to grow by more than 1 per cent per year,

and the proportion of empty-nesters older than 55 years,

who have frequently embraced condominium living,

continues to rise.

While the health of apartment condominium markets

varies significantly by region, nowhere do we see a bub-

ble about to burst. This is particularly true in Toronto.

We have consistently forecast a soft landing for this

city’s apartment condominium market, and incoming

data continue to support this view. On the other hand,

the decline in oil prices has dramatically changed

conditions in Alberta. Calgary’s previously drum-tight

market is now expected to soften considerably. In

Overview

Apartment Condo Indicators

Starts Resale sales Resale price ($)*

2014 2015f 2016f 2014 2015f 2016f 2014 2015f 2016f

Québec City 1,031 1,081 1,113 1,485 1,534 1,565 227,172 229,006 232,293

–33.3 4.8 3.0 2.7 3.3 2.0 0.9 0.8 1.4

Montréal 10,360 9,210 9,309 10,945 11,123 11,493 270,368 277,168 283,286

18.7 –11.1 1.1 –3.0 1.6 3.3 2.2 2.5 2.2

Ottawa 1,418 1,559 1,573 1,349 1,368 1,409 261,041 264,509 271,304

–37.5 9.9 0.9 –9.6 1.4 3.0 0.7 1.3 2.6

Toronto 12,862 12,032 12,468 22,169 22,269 22,457 319,503 325,668 331,214

–26.3 –6.5 3.6 10.4 0.5 0.8 3.5 1.9 1.7

Calgary 6,079 3,322 2,785 5,529 3,908 3,843 276,000 266,991 264,142

122.2 –45.3 –16.2 21.7 –29.3 –1.7 8.4 –3.3 –1.1

Edmonton 1,646 1,165 1,047 3,187 2,364 2,405 219,392 209,359 208,173

–47.3 –29.2 –10.1 6.9 –25.8 1.7 1.7 –4.6 –0.6

Vancouver 8,666 8,933 9,344 13,469 13,793 13,987 377,929 385,859 396,694

–5.7 3.1 4.6 14.1 2.4 1.4 2.8 2.1 2.8

Victoria 274 372 383 1,639 1,729 1,773 274,675 287,166 293,642

–61.5 35.6 3.2 13.0 5.5 2.6 2.4 4.5 2.3

*Average resale prices are used for Québec City and Montréal; median resale prices are used for the rest of the metropolitan areas. Resale and average prices in Montréal and Québec City include all condominium styles, not just apartments.f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; CMHC Housing Time Series Database; Canadian Real Estate Association; Quebec Federation of Real Estate Boards.

2 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

Edmonton, the market was not as strained, but slow-

ing is also expected. Vancouver’s apartment market is

improving, but remains burdened by high inventories

of unsold units and subject to the vagaries of offshore

demand. An improving job market in Victoria will sup-

port healthier demand for all forms of housing. Soft

economies are limiting residential demand in Ottawa,

Montréal, and Québec City. Apartment markets in the

latter two areas look overbuilt. Since many condomin-

iums are sold to first-time buyers, the tightening of

mortgage rules over the past few years has probably

crimped demand for these units.

All cities are expected to enjoy population increases

during the next few years. Toronto is forecast to enjoy

the largest absolute increase, of at least 100,000 resi-

dents per year. Meanwhile, Victoria has the largest

share of 55-plus residents, at 35 per cent, but growth

in this population segment will be strongest in Calgary

and Edmonton.

Mixed economic conditions will produce varying hous-

ing market outcomes. Real GDP will probably decline

in Calgary and Edmonton this year, while advancing

1.5 per cent or more elsewhere. Toronto (2.8 per cent)

and Vancouver (2.7 per cent) are expected to see rela-

tively strong growth this year. Employment conditions

will follow a similar pattern. Unsurprisingly, job mar-

kets in Calgary and Edmonton will weaken. Elsewhere,

gains are expected to range from 0.4 per cent in Ottawa

to 1.8 per cent in Toronto.

Apartment sales rose in most cities last year, led by

a 22 per cent gain in Calgary. Volumes declined in

Montréal and Ottawa. For 2015, the suddenly weak

economic conditions in Calgary and Edmonton will

pull sales sharply lower, with modest increases in other

cities. A 5.5 per cent hike in Victoria leads expected

gainers, although this city’s volume remains well off

its peak years in the mid-2000s. Sales will inch higher

in Toronto.

Active listings rose everywhere last year except

Edmonton and Victoria, which both saw double-digit

percentage losses. Listings rose 22 per cent in Calgary,

but no other city had an increase above 10 per cent.

In 2015, the Alberta cities are forecast to see listings

swell as their markets slow. In the other six cities, most

changes will be modest, although listings are forecast

to drop 11 per cent in Ottawa. Last year’s listings gains

were at least partially responsible for a falling sales-to-

active-listing ratio in our three easternmost cities and

Calgary. Edmonton’s ratio rose sharply for the second

straight year, but will surrender these gains this year.

Calgary’s ratio is also expected to drop significantly.

Toronto’s ratio jumped nearly 3 percentage points on

the strength of a healthy sales gain. Montréal, Québec

City, and Ottawa were buyers’ markets last year; the

rest enjoyed balanced conditions. For 2015, we expect

balanced markets in Toronto, Vancouver, and Victoria.

Buyers’ conditions will prevail elsewhere. Price chan-

ges will be similarly mixed. The median apartment

price will decline in both Calgary and Edmonton, and

the average price will rise only fractionally in Québec

City. Ottawa’s price growth will also be languid.

Average apartment price growth will accelerate in

Montréal, but this seems due to aggressive incentives

being offered to sell new units. Victoria’s median price

will rise the fastest among our eight cities, as it finally

shakes off past declines. Prices will advance roughly

2 per cent in both Toronto and Vancouver.

Although absorption of new units rose in 2014 in five

of our eight markets and was above the previous dec-

ade’s average in six of the eight, even a small dip in

the pace of new-unit take-up could quickly result in a

big inventory run-up. Indeed, inventories of apartment

condominiums and units under construction are high

in many markets, notably Toronto, where builders will

cut starts this year. Montréal is already oversupplied,

and so starts will drop there as well. Alberta’s softening

economy will sharply curtail starts in Calgary and

Edmonton. Gains are expected in Québec City, Ottawa,

Vancouver, and Victoria, but starts in these four cities

will remain well off peak levels.

Rising apartment prices will lift monthly mortgage

charges everywhere except the Alberta cities. Victoria’s

relatively large price gain will boost this charge by

7.3 per cent, the biggest increase among our cities.

Where carrying charges rise, they will do so faster than

incomes, lifting their relative bite. This year’s ratio of

carrying costs to incomes will be highest in Vancouver,

at 21.6 per cent, and lowest, 9.8 per cent, in Edmonton.

Winter 2015—Metropolitan Condo Outlook | 3

The Conference Board of Canada/Genworth Canada

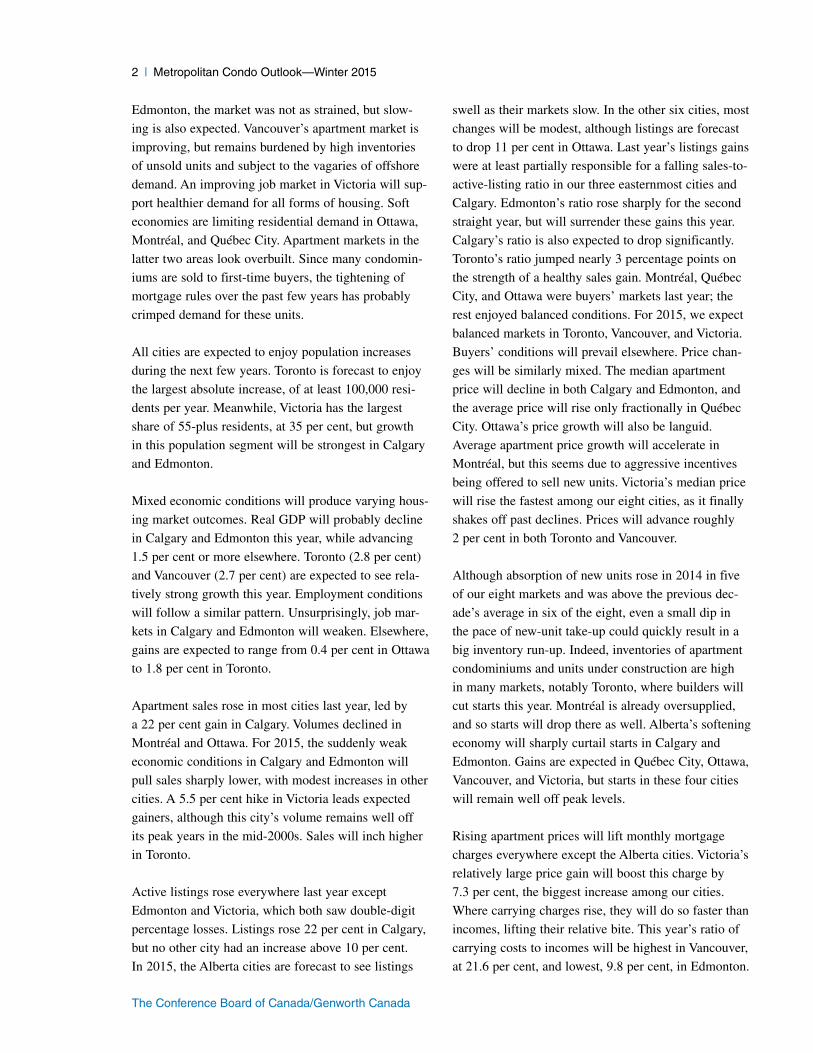

U nit sales of apartment condominiums are expected to rise by 3.3 per cent this year, up for the second year in a row. This growth fol-

lows several years of declining sales, as buyers dealt with tighter mortgage rules and slower economic growth. Resale price growth will be modest in 2015, but will strengthen to 1.4 per cent next year as demand grows and the market tightens. Although rising inventories have kept builders at bay for the past couple of years, the new apartment con-dominium market is also expected to see increased activity this year, with starts up 4.8 per cent.

Unit sales of existing apartment condominiums

increased 2.7 per cent in 2014, after falling in five of

the six previous years. The downturn in the resale mar-

ket had been driven by slower economic growth and

tighter mortgage rules. Buyers also felt the pinch of

deteriorating affordability after several years of strong

price growth. Indeed, by 2013, the average price of a

condominium in the Québec City resale market topped

$225,000, a near doubling in just 10 years. However,

while sales fell, strong prices kept sellers interested.

Active listings jumped an average of 29.2 per cent per

year from 2010 to 2013, lowering the sales-to-active-

listings ratio to 5.6 per cent, down from 19 per cent in

2009 and its lowest level since 1999. Accordingly,

the resale market moved from a sellers’ position

to a buyers’ one.

With the resale market in buyers’ territory, price growth

finally began to soften in 2013 and 2014, down to an

annual average of 1.5 per cent. At the same time, eco-

nomic growth and employment improved. As a result,

buyers came back to Québec City’s resale apartment

condominium market last year. Even though active list-

ings began falling in the second quarter of 2014, they

still increased by 5.4 per cent for the year as a whole.

As a result, the sales-to-active-listings ratio was roughly

the same as in 2013.

Metropolitan Insights

Québec City

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

5001,0001,5002,0002,5003,000

0102030405060

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

4 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

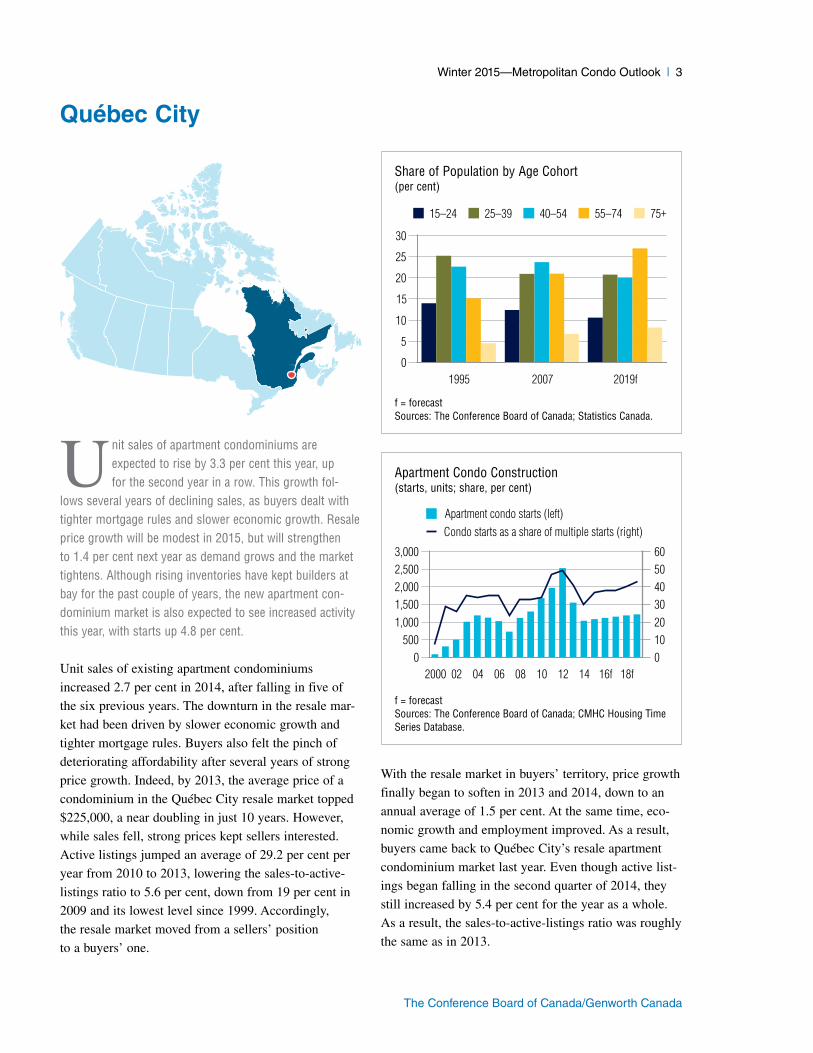

Unit sales continued to be strong through the fourth

quarter of 2014. But with weaker employment growth

forecast for 2015, unit sales of apartment condomin-

iums are expected to slow through the first six months

of this year, before rising again in the last half, to finish

the year up 3.3 per cent in 2015. Meanwhile, another

year of modest price increases (resale condominium

prices are forecast to grow by only 0.8 per cent), will

further discourage sellers from entering the market.

Active listings are expected to fall by 4.3 per cent

this year.

As the economy gains momentum next year, unit sales

are expected to rise further, growing by an average of

2.1 per cent annually over 2016 to 2019. But as sell-

ers contend with still-high inventory levels, listings are

forecast to drop by 10.4 per cent in 2016 and by 8 per

cent on an average annual basis from 2017 to 2019.

This will push the sales-to-active-listings ratio back

up to 9 per cent by 2019. In turn, price growth will

improve to an average of 2.1 per cent per year through

2016–19.

In the new apartment condominium market, starts

reached a record 2,530 units in 2012, following an

average annual increase of 28.9 per cent since 2008.

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Quebec Federation of Real Estate Boards.

2001 03 05 07 09 11 13 15f 17f 19f10

12

14

16

18

20

1,000

1,200

1,400

1,600

1,800

2,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Quebec Federation of Real Estate Boards.

2000 02 04 06 08 10 12 14 16f 18f5

10

15

20

25

30

0

4

8

12

16

20

Sales-to-active-listings ratio (left)Average price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.050.100.150.200.250.300.35

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−1

01234567

Winter 2015—Metropolitan Condo Outlook | 5

The Conference Board of Canada/Genworth Canada

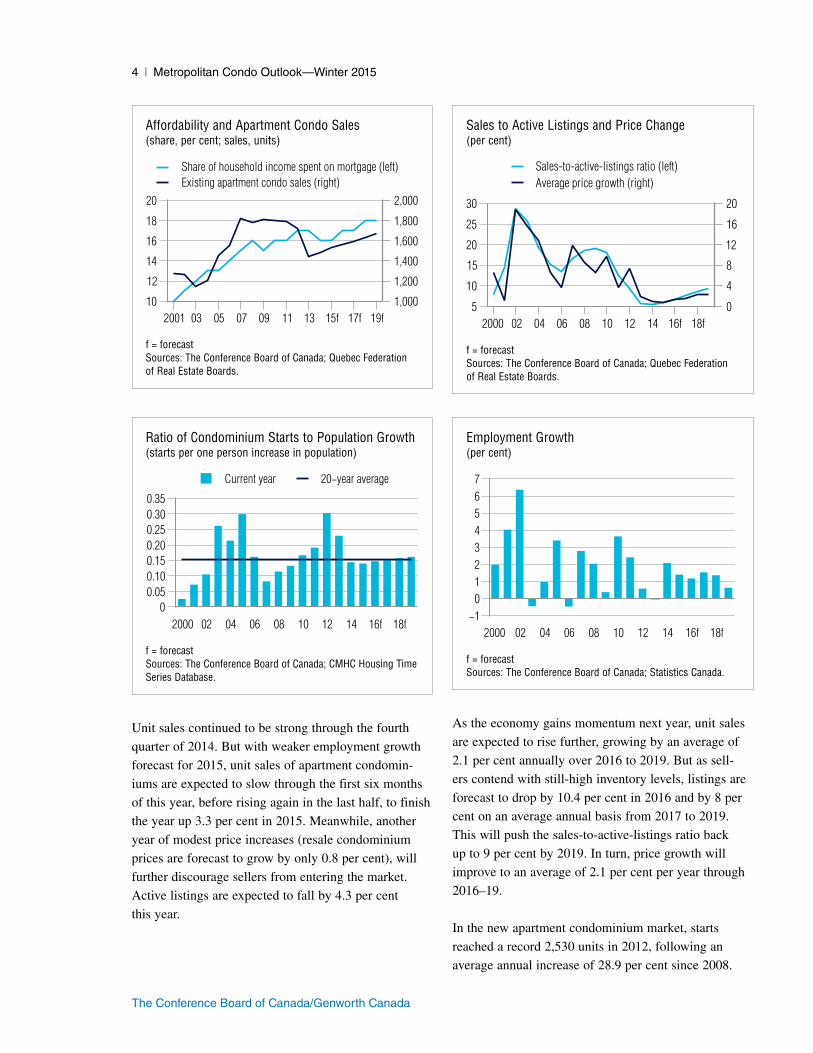

Even though absorptions rose at the same time, supply

still outstripped demand. As a result, inventories began

to rise rapidly. In response, builders reduced starts of

apartment condominiums by 38.9 per cent in 2013 and

a further 33.3 per cent last year, bringing them back

down to just over 1,000 units last year, closer to their

long-term average. Inventories subsequently began to

fall in 2014, even as absorptions slipped as well.

Builders finished off 2014 by increasing starts of apart-

ment condominiums in the last quarter of the year.

With inventories still on a downward trend and demand

picking up in the resale market, starts are expected to

rise modestly through the rest of this year as well. In

total, starts are forecast to increase by 4.8 per cent in

2014 and by 3 per cent in 2016. Although absorptions

are expected to fall this year and next, they will still

outnumber completions. Accordingly, inventories will

continue to edge down. Stable economic conditions will

help keep builders in the new apartment condominium

market through the following few years. Starts are

expected to rise by an average of 3 per cent annually

from 2017 to 2019, modest enough to keep inventories

in check.

Resale Condominium Apartment Market

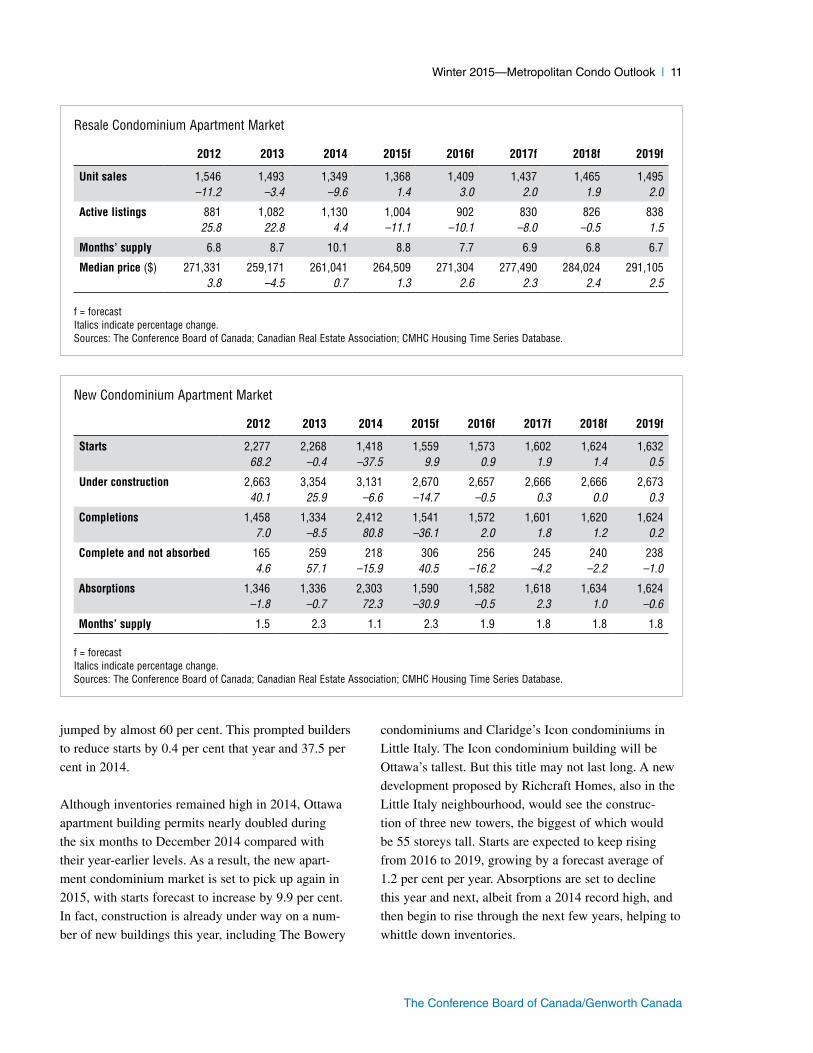

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 1,725 1,446 1,485 1,534 1,565 1,597 1,630 1,669–3.8 –16.2 2.7 3.3 2.0 2.0 2.1 2.4

Active listings 1,533 2,145 2,261 2,164 1,939 1,740 1,592 1,51228.0 40.0 5.4 –4.3 –10.4 –10.3 –8.5 –5.0

Months’ supply 10.7 17.8 18.3 16.9 14.9 13.1 11.7 10.9

Average price ($) 220,860 225,195 227,172 229,006 232,293 235,812 241,507 247,0927.4 2.0 0.9 0.8 1.4 1.5 2.4 2.3

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Quebec Federation of Real Estate Boards; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 2,530 1,546 1,031 1,081 1,113 1,150 1,183 1,21828.6 –38.9 –33.3 4.8 3.0 3.3 2.9 2.9

Under construction 1,664 1,558 928 1,043 1,020 1,018 1,018 1,02414.5 –6.4 –40.4 12.4 –2.2 –0.2 0.0 0.6

Completions 2,620 1,756 1,722 1,078 1,122 1,150 1,183 1,20772.8 –33.0 –1.9 –37.4 4.1 2.5 2.8 2.0

Complete and not absorbed 640 692 595 290 205 193 193 19891.3 8.1 –14.0 –51.3 –29.4 –5.6 0.0 2.3

Absorptions 2,044 2,127 1,778 1,320 1,181 1,159 1,180 1,20243.3 4.0 –16.4 –25.8 –10.5 –1.9 1.9 1.9

Months’ supply 3.8 3.9 4.0 2.6 2.1 2.0 2.0 2.0

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Quebec Federation of Real Estate Boards; CMHC Housing Time Series Database.

6 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

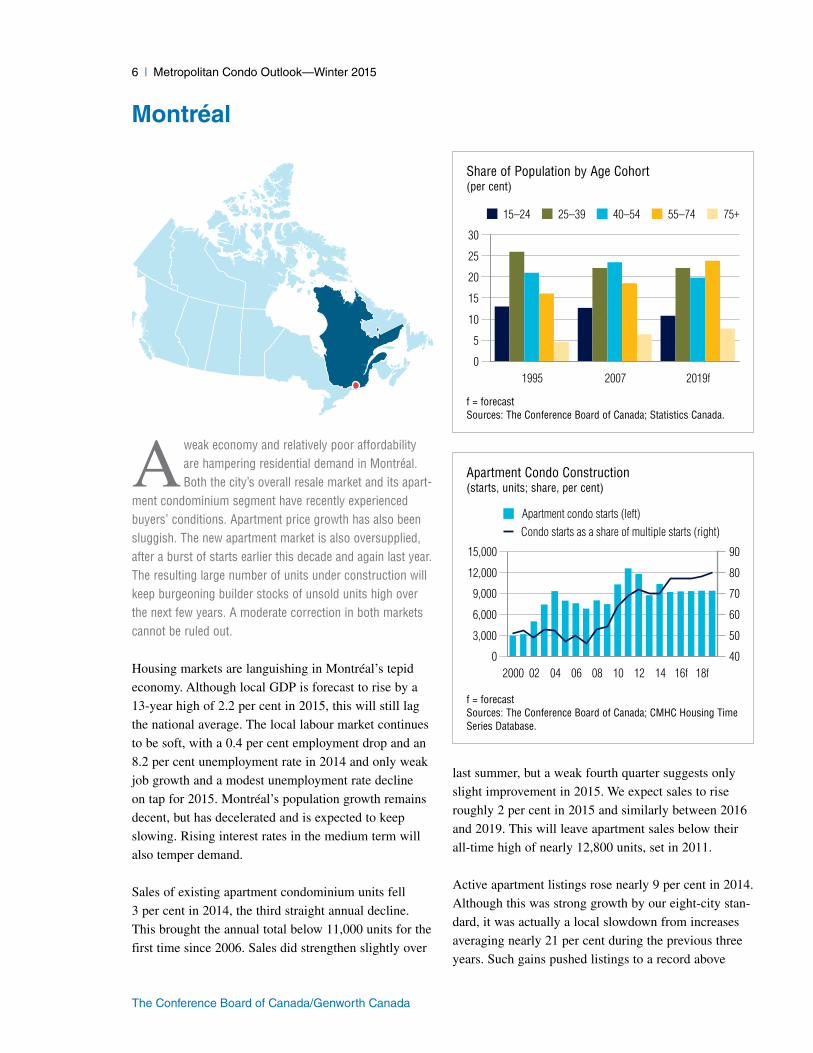

A weak economy and relatively poor affordability are hampering residential demand in Montréal. Both the city’s overall resale market and its apart-

ment condominium segment have recently experienced buyers’ conditions. Apartment price growth has also been sluggish. The new apartment market is also oversupplied, after a burst of starts earlier this decade and again last year. The resulting large number of units under construction will keep burgeoning builder stocks of unsold units high over the next few years. A moderate correction in both markets cannot be ruled out.

Housing markets are languishing in Montréal’s tepid

economy. Although local GDP is forecast to rise by a

13-year high of 2.2 per cent in 2015, this will still lag

the national average. The local labour market continues

to be soft, with a 0.4 per cent employment drop and an

8.2 per cent unemployment rate in 2014 and only weak

job growth and a modest unemployment rate decline

on tap for 2015. Montréal’s population growth remains

decent, but has decelerated and is expected to keep

slowing. Rising interest rates in the medium term will

also temper demand.

Sales of existing apartment condominium units fell

3 per cent in 2014, the third straight annual decline.

This brought the annual total below 11,000 units for the

first time since 2006. Sales did strengthen slightly over

last summer, but a weak fourth quarter suggests only

slight improvement in 2015. We expect sales to rise

roughly 2 per cent in 2015 and similarly between 2016

and 2019. This will leave apartment sales below their

all-time high of nearly 12,800 units, set in 2011.

Active apartment listings rose nearly 9 per cent in 2014.

Although this was strong growth by our eight-city stan-

dard, it was actually a local slowdown from increases

averaging nearly 21 per cent during the previous three

years. Such gains pushed listings to a record above

Montréal

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

3,000

6,000

9,000

12,000

15,000

40

50

60

70

80

90

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

Winter 2015—Metropolitan Condo Outlook | 7

The Conference Board of Canada/Genworth Canada

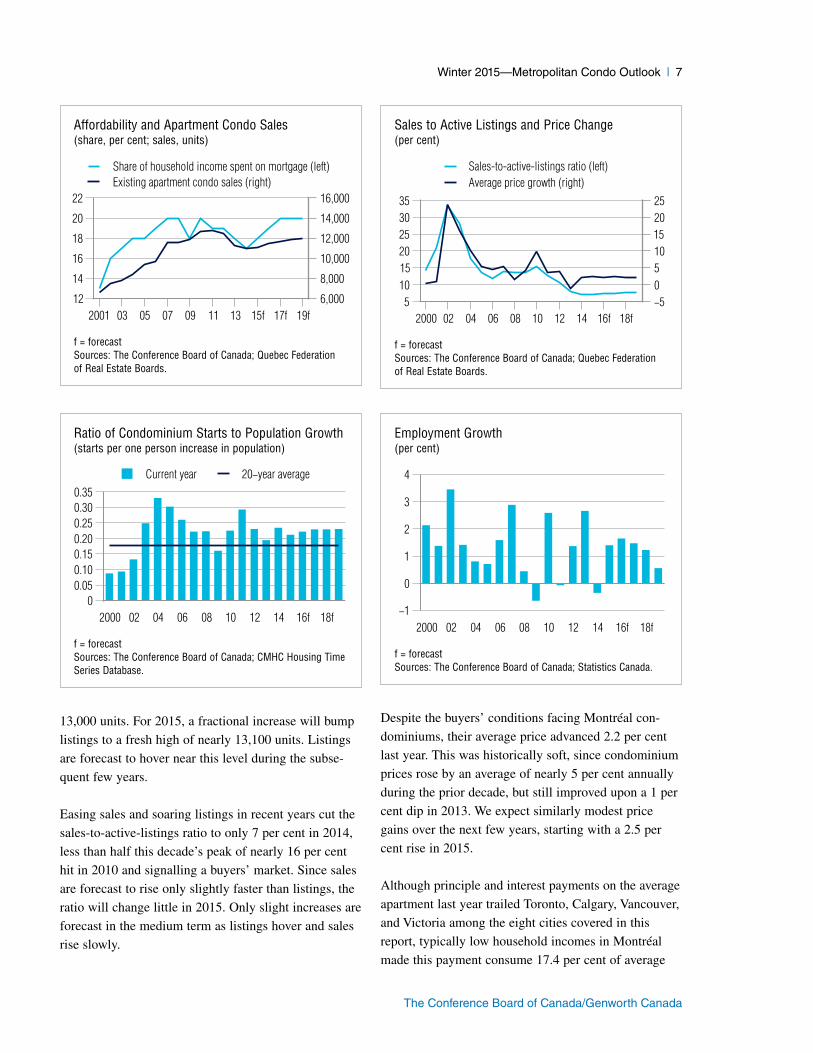

13,000 units. For 2015, a fractional increase will bump

listings to a fresh high of nearly 13,100 units. Listings

are forecast to hover near this level during the subse-

quent few years.

Easing sales and soaring listings in recent years cut the

sales-to-active-listings ratio to only 7 per cent in 2014,

less than half this decade’s peak of nearly 16 per cent

hit in 2010 and signalling a buyers’ market. Since sales

are forecast to rise only slightly faster than listings, the

ratio will change little in 2015. Only slight increases are

forecast in the medium term as listings hover and sales

rise slowly.

Despite the buyers’ conditions facing Montréal con-

dominiums, their average price advanced 2.2 per cent

last year. This was historically soft, since condominium

prices rose by an average of nearly 5 per cent annually

during the prior decade, but still improved upon a 1 per

cent dip in 2013. We expect similarly modest price

gains over the next few years, starting with a 2.5 per

cent rise in 2015.

Although principle and interest payments on the average

apartment last year trailed Toronto, Calgary, Vancouver,

and Victoria among the eight cities covered in this

report, typically low household incomes in Montréal

made this payment consume 17.4 per cent of average

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Quebec Federation of Real Estate Boards.

2001 03 05 07 09 11 13 15f 17f 19f12

14

16

18

20

22

6,000

8,000

10,000

12,000

14,000

16,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Quebec Federation of Real Estate Boards.

2000 02 04 06 08 10 12 14 16f 18f5

101520253035

−50510152025

Sales-to-active-listings ratio (left)Average price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.050.100.150.200.250.300.35

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−1

0

1

2

3

4

8 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

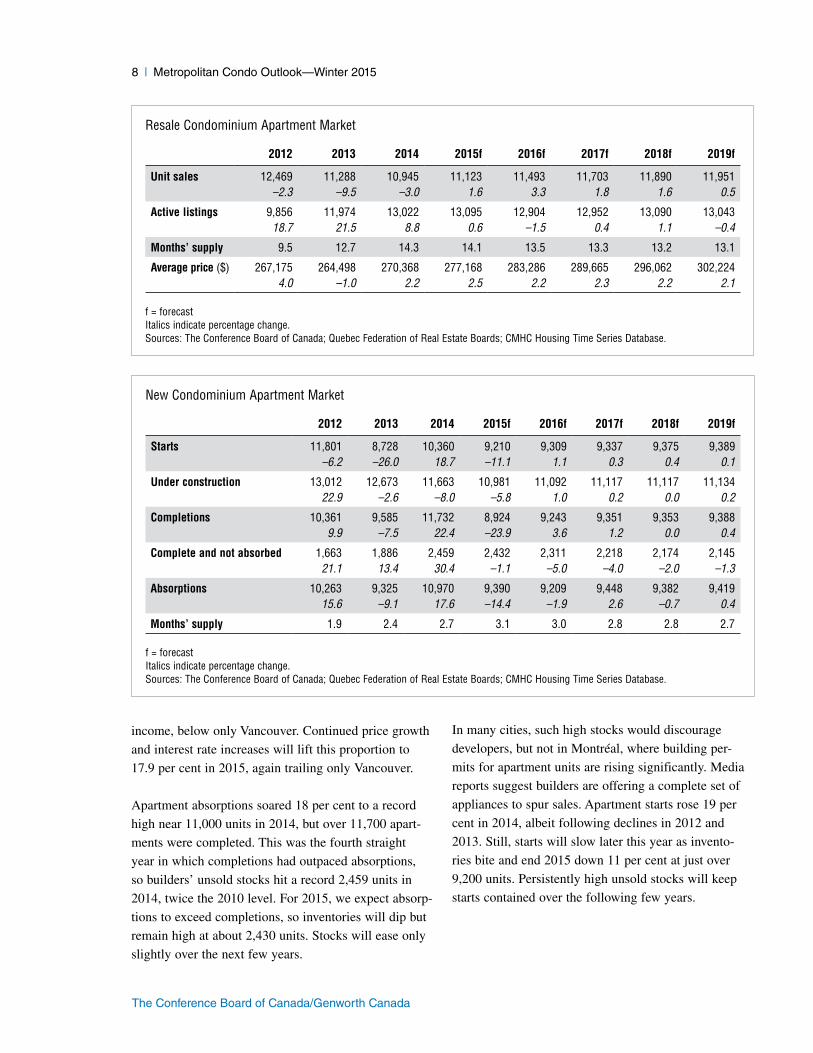

income, below only Vancouver. Continued price growth

and interest rate increases will lift this proportion to

17.9 per cent in 2015, again trailing only Vancouver.

Apartment absorptions soared 18 per cent to a record

high near 11,000 units in 2014, but over 11,700 apart-

ments were completed. This was the fourth straight

year in which completions had outpaced absorptions,

so builders’ unsold stocks hit a record 2,459 units in

2014, twice the 2010 level. For 2015, we expect absorp-

tions to exceed completions, so inventories will dip but

remain high at about 2,430 units. Stocks will ease only

slightly over the next few years.

In many cities, such high stocks would discourage

developers, but not in Montréal, where building per-

mits for apartment units are rising significantly. Media

reports suggest builders are offering a complete set of

appliances to spur sales. Apartment starts rose 19 per

cent in 2014, albeit following declines in 2012 and

2013. Still, starts will slow later this year as invento-

ries bite and end 2015 down 11 per cent at just over

9,200 units. Persistently high unsold stocks will keep

starts contained over the following few years.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 12,469 11,288 10,945 11,123 11,493 11,703 11,890 11,951–2.3 –9.5 –3.0 1.6 3.3 1.8 1.6 0.5

Active listings 9,856 11,974 13,022 13,095 12,904 12,952 13,090 13,04318.7 21.5 8.8 0.6 –1.5 0.4 1.1 –0.4

Months’ supply 9.5 12.7 14.3 14.1 13.5 13.3 13.2 13.1

Average price ($) 267,175 264,498 270,368 277,168 283,286 289,665 296,062 302,2244.0 –1.0 2.2 2.5 2.2 2.3 2.2 2.1

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Quebec Federation of Real Estate Boards; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 11,801 8,728 10,360 9,210 9,309 9,337 9,375 9,389–6.2 –26.0 18.7 –11.1 1.1 0.3 0.4 0.1

Under construction 13,012 12,673 11,663 10,981 11,092 11,117 11,117 11,13422.9 –2.6 –8.0 –5.8 1.0 0.2 0.0 0.2

Completions 10,361 9,585 11,732 8,924 9,243 9,351 9,353 9,3889.9 –7.5 22.4 –23.9 3.6 1.2 0.0 0.4

Complete and not absorbed 1,663 1,886 2,459 2,432 2,311 2,218 2,174 2,14521.1 13.4 30.4 –1.1 –5.0 –4.0 –2.0 –1.3

Absorptions 10,263 9,325 10,970 9,390 9,209 9,448 9,382 9,41915.6 –9.1 17.6 –14.4 –1.9 2.6 –0.7 0.4

Months’ supply 1.9 2.4 2.7 3.1 3.0 2.8 2.8 2.7

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Quebec Federation of Real Estate Boards; CMHC Housing Time Series Database.

Winter 2015—Metropolitan Condo Outlook | 9

The Conference Board of Canada/Genworth Canada

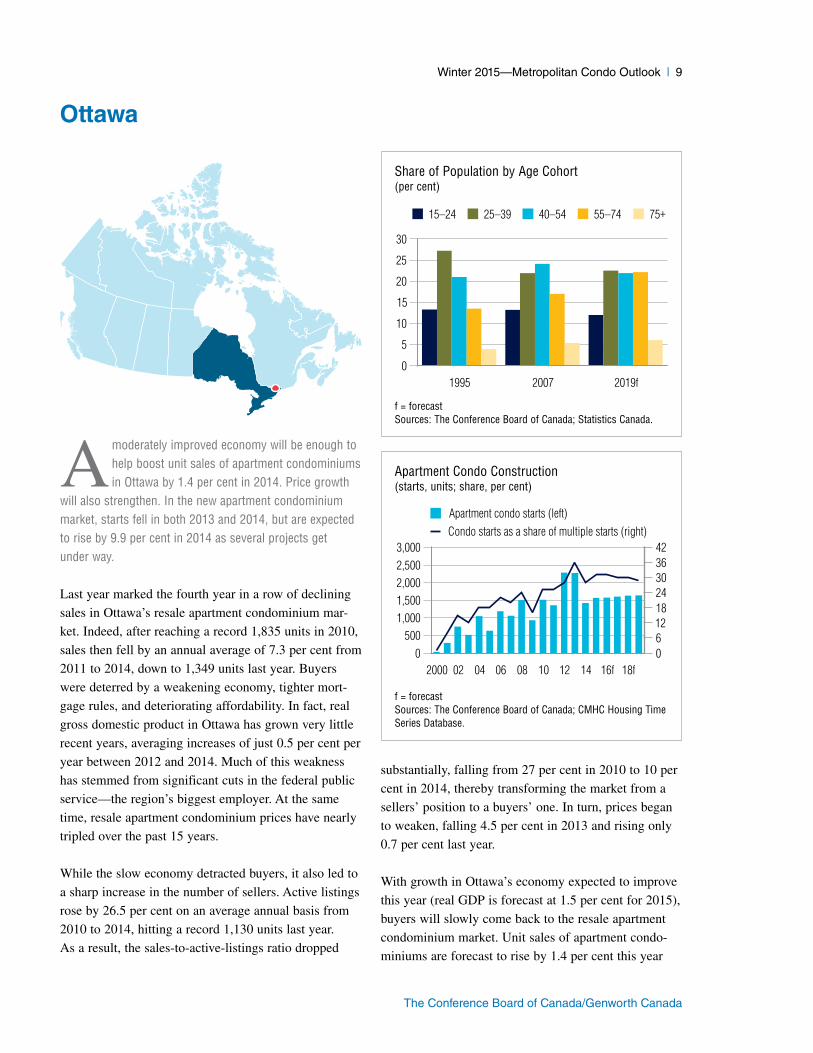

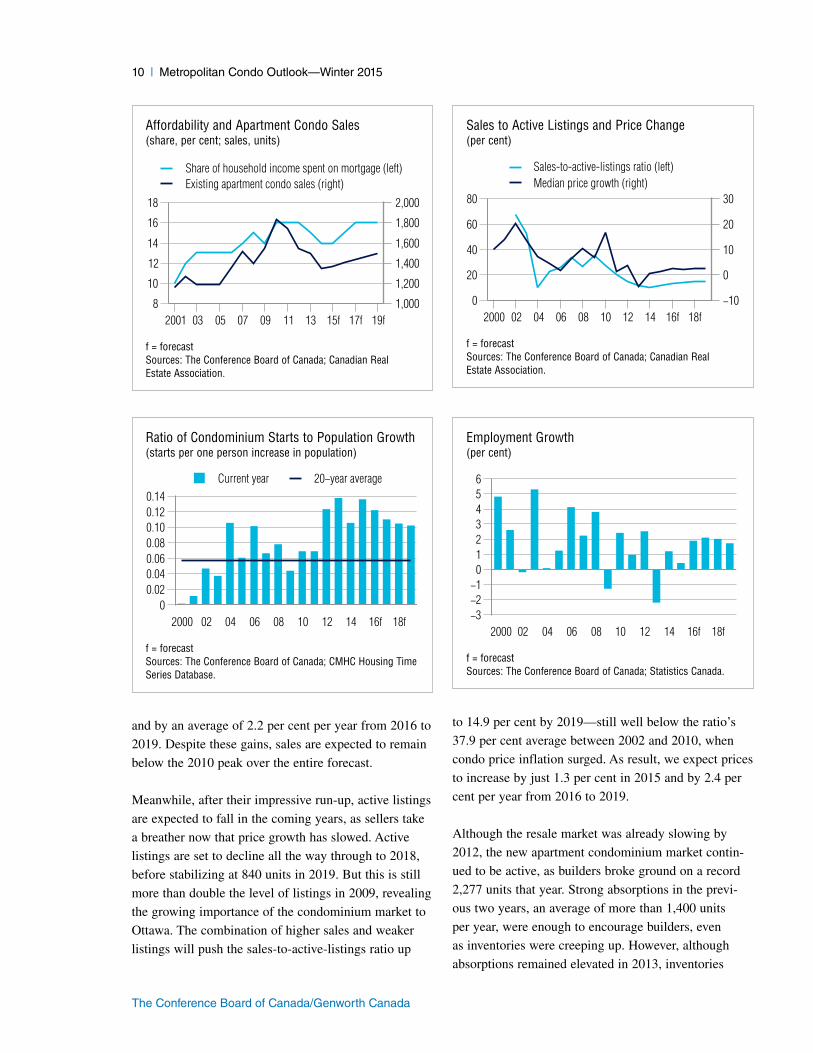

A moderately improved economy will be enough to help boost unit sales of apartment condominiums in Ottawa by 1.4 per cent in 2014. Price growth

will also strengthen. In the new apartment condominium market, starts fell in both 2013 and 2014, but are expected to rise by 9.9 per cent in 2014 as several projects get under way.

Last year marked the fourth year in a row of declining

sales in Ottawa’s resale apartment condominium mar-

ket. Indeed, after reaching a record 1,835 units in 2010,

sales then fell by an annual average of 7.3 per cent from

2011 to 2014, down to 1,349 units last year. Buyers

were deterred by a weakening economy, tighter mort-

gage rules, and deteriorating affordability. In fact, real

gross domestic product in Ottawa has grown very little

recent years, averaging increases of just 0.5 per cent per

year between 2012 and 2014. Much of this weakness

has stemmed from significant cuts in the federal public

service—the region’s biggest employer. At the same

time, resale apartment condominium prices have nearly

tripled over the past 15 years.

While the slow economy detracted buyers, it also led to

a sharp increase in the number of sellers. Active listings

rose by 26.5 per cent on an average annual basis from

2010 to 2014, hitting a record 1,130 units last year.

As a result, the sales-to-active-listings ratio dropped

substantially, falling from 27 per cent in 2010 to 10 per

cent in 2014, thereby transforming the market from a

sellers’ position to a buyers’ one. In turn, prices began

to weaken, falling 4.5 per cent in 2013 and rising only

0.7 per cent last year.

With growth in Ottawa’s economy expected to improve

this year (real GDP is forecast at 1.5 per cent for 2015),

buyers will slowly come back to the resale apartment

condominium market. Unit sales of apartment condo-

miniums are forecast to rise by 1.4 per cent this year

Ottawa

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

5001,0001,5002,0002,5003,000

06121824303642

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

10 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

and by an average of 2.2 per cent per year from 2016 to

2019. Despite these gains, sales are expected to remain

below the 2010 peak over the entire forecast.

Meanwhile, after their impressive run-up, active listings

are expected to fall in the coming years, as sellers take

a breather now that price growth has slowed. Active

listings are set to decline all the way through to 2018,

before stabilizing at 840 units in 2019. But this is still

more than double the level of listings in 2009, revealing

the growing importance of the condominium market to

Ottawa. The combination of higher sales and weaker

listings will push the sales-to-active-listings ratio up

to 14.9 per cent by 2019—still well below the ratio’s

37.9 per cent average between 2002 and 2010, when

condo price inflation surged. As result, we expect prices

to increase by just 1.3 per cent in 2015 and by 2.4 per

cent per year from 2016 to 2019.

Although the resale market was already slowing by

2012, the new apartment condominium market contin-

ued to be active, as builders broke ground on a record

2,277 units that year. Strong absorptions in the previ-

ous two years, an average of more than 1,400 units

per year, were enough to encourage builders, even

as inventories were creeping up. However, although

absorptions remained elevated in 2013, inventories

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f8

10

12

14

16

18

1,000

1,200

1,400

1,600

1,800

2,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f0

20

40

60

80

−10

0

10

20

30

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.020.040.060.080.100.120.14

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−3−2−1

0123456

Winter 2015—Metropolitan Condo Outlook | 11

The Conference Board of Canada/Genworth Canada

jumped by almost 60 per cent. This prompted builders

to reduce starts by 0.4 per cent that year and 37.5 per

cent in 2014.

Although inventories remained high in 2014, Ottawa

apartment building permits nearly doubled during

the six months to December 2014 compared with

their year-earlier levels. As a result, the new apart-

ment condominium market is set to pick up again in

2015, with starts forecast to increase by 9.9 per cent.

In fact, construction is already under way on a num-

ber of new buildings this year, including The Bowery

condominiums and Claridge’s Icon condominiums in

Little Italy. The Icon condominium building will be

Ottawa’s tallest. But this title may not last long. A new

development proposed by Richcraft Homes, also in the

Little Italy neighbourhood, would see the construc-

tion of three new towers, the biggest of which would

be 55 storeys tall. Starts are expected to keep rising

from 2016 to 2019, growing by a forecast average of

1.2 per cent per year. Absorptions are set to decline

this year and next, albeit from a 2014 record high, and

then begin to rise through the next few years, helping to

whittle down inventories.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 1,546 1,493 1,349 1,368 1,409 1,437 1,465 1,495–11.2 –3.4 –9.6 1.4 3.0 2.0 1.9 2.0

Active listings 881 1,082 1,130 1,004 902 830 826 83825.8 22.8 4.4 –11.1 –10.1 –8.0 –0.5 1.5

Months’ supply 6.8 8.7 10.1 8.8 7.7 6.9 6.8 6.7

Median price ($) 271,331 259,171 261,041 264,509 271,304 277,490 284,024 291,1053.8 –4.5 0.7 1.3 2.6 2.3 2.4 2.5

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 2,277 2,268 1,418 1,559 1,573 1,602 1,624 1,63268.2 –0.4 –37.5 9.9 0.9 1.9 1.4 0.5

Under construction 2,663 3,354 3,131 2,670 2,657 2,666 2,666 2,67340.1 25.9 –6.6 –14.7 –0.5 0.3 0.0 0.3

Completions 1,458 1,334 2,412 1,541 1,572 1,601 1,620 1,6247.0 –8.5 80.8 –36.1 2.0 1.8 1.2 0.2

Complete and not absorbed 165 259 218 306 256 245 240 2384.6 57.1 –15.9 40.5 –16.2 –4.2 –2.2 –1.0

Absorptions 1,346 1,336 2,303 1,590 1,582 1,618 1,634 1,624–1.8 –0.7 72.3 –30.9 –0.5 2.3 1.0 –0.6

Months’ supply 1.5 2.3 1.1 2.3 1.9 1.8 1.8 1.8

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

12 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

T oronto’s decent economic prospects, its rapid population growth, and the desirability of living downtown or near public transit routes all suggest

that a severe correction in Toronto’s apartment condomin-ium market is unlikely. While the large number of units under construction poses a risk, new-unit take-up exceeded completions last year and is expected to match them this year. Resale volumes are solid and prices continue to rise. A soft landing remains our call for this market segment, although brief periods of inflation-adjusted price drops are possible.

Toronto’s economy remains healthy and should be

buoyed by U.S. economic recovery and the softer

Canadian dollar. Its GDP growth is forecast to hit a

five-year high of 2.8 per cent this year, spurring faster

employment growth. Population hikes have averaged

nearly 94,000 people annually over the past five years

and are expected to exceed 100,000 annually starting in

2015. Moreover, the population of condo-loving empty-

nesters aged 55 or more rose an average of 3.3 per cent

annually over the past decade, twice the pace of overall

population growth. Resulting healthy condominium

demand will be amplified in 2015 by persistently low

mortgage interest rates.

Forecasts of a collapsing apartment condominium

market were not fulfilled in 2014 as sales of existing

units rose 10 per cent. Last year’s 22,169 transactions

approached Toronto’s all-time high of 22,900 units in

2011. And sales picked up in last year’s second half,

setting a healthy stage for 2015. Sales are indeed fore-

cast to inch higher in 2015, then average 1.4 per cent

annual growth between 2016 and 2019. This will lift

apartment sales to a fresh record in 2018.

The number of active apartment listings rose for the

fifth straight year in 2014, although the last two annual

gains have been below 1 per cent. Still, these increases

lifted listings to a record high of 6,200 units. For 2015,

Toronto

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecast Sources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f5,000

10,000

15,000

20,000

25,000

30,000

30

40

50

60

70

80

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

Winter 2015—Metropolitan Condo Outlook | 13

The Conference Board of Canada/Genworth Canada

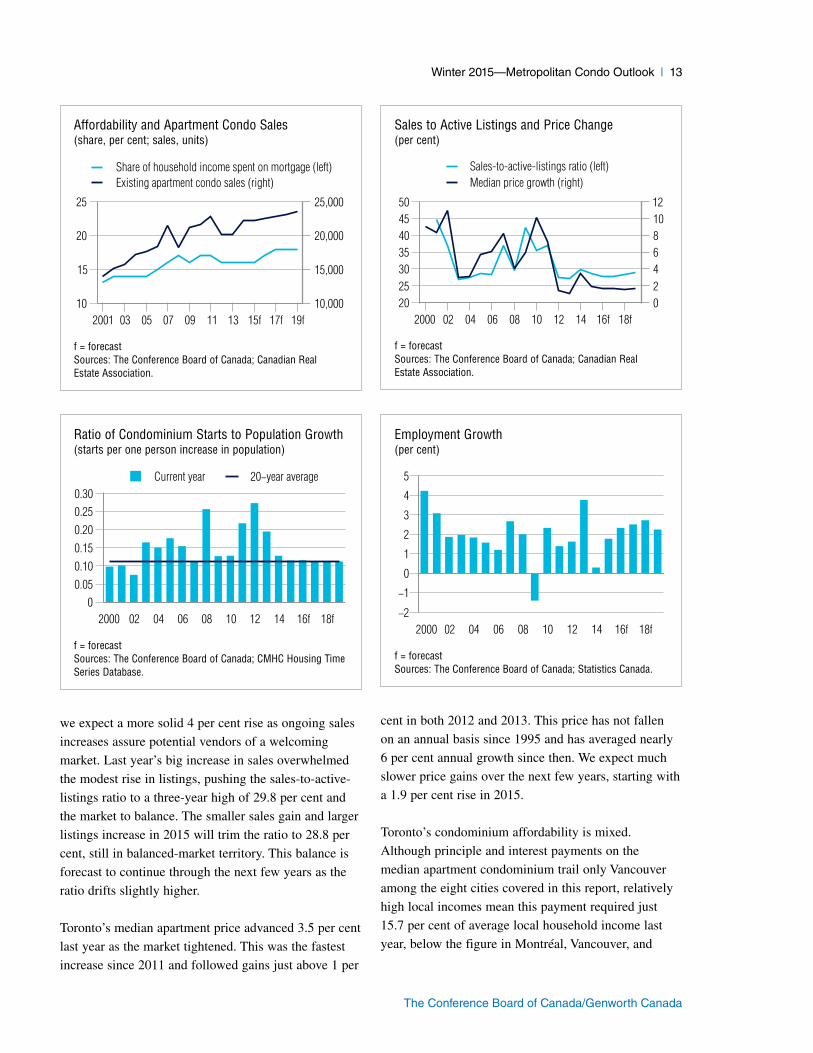

we expect a more solid 4 per cent rise as ongoing sales

increases assure potential vendors of a welcoming

market. Last year’s big increase in sales overwhelmed

the modest rise in listings, pushing the sales-to-active-

listings ratio to a three-year high of 29.8 per cent and

the market to balance. The smaller sales gain and larger

listings increase in 2015 will trim the ratio to 28.8 per

cent, still in balanced-market territory. This balance is

forecast to continue through the next few years as the

ratio drifts slightly higher.

Toronto’s median apartment price advanced 3.5 per cent

last year as the market tightened. This was the fastest

increase since 2011 and followed gains just above 1 per

cent in both 2012 and 2013. This price has not fallen

on an annual basis since 1995 and has averaged nearly

6 per cent annual growth since then. We expect much

slower price gains over the next few years, starting with

a 1.9 per cent rise in 2015.

Toronto’s condominium affordability is mixed.

Although principle and interest payments on the

median apartment condominium trail only Vancouver

among the eight cities covered in this report, relatively

high local incomes mean this payment required just

15.7 per cent of average local household income last

year, below the figure in Montréal, Vancouver, and

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f10

15

20

25

10,000

15,000

20,000

25,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f20253035404550

024681012

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.050.100.150.200.250.30

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−2

−1

0

1

2

3

4

5

14 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

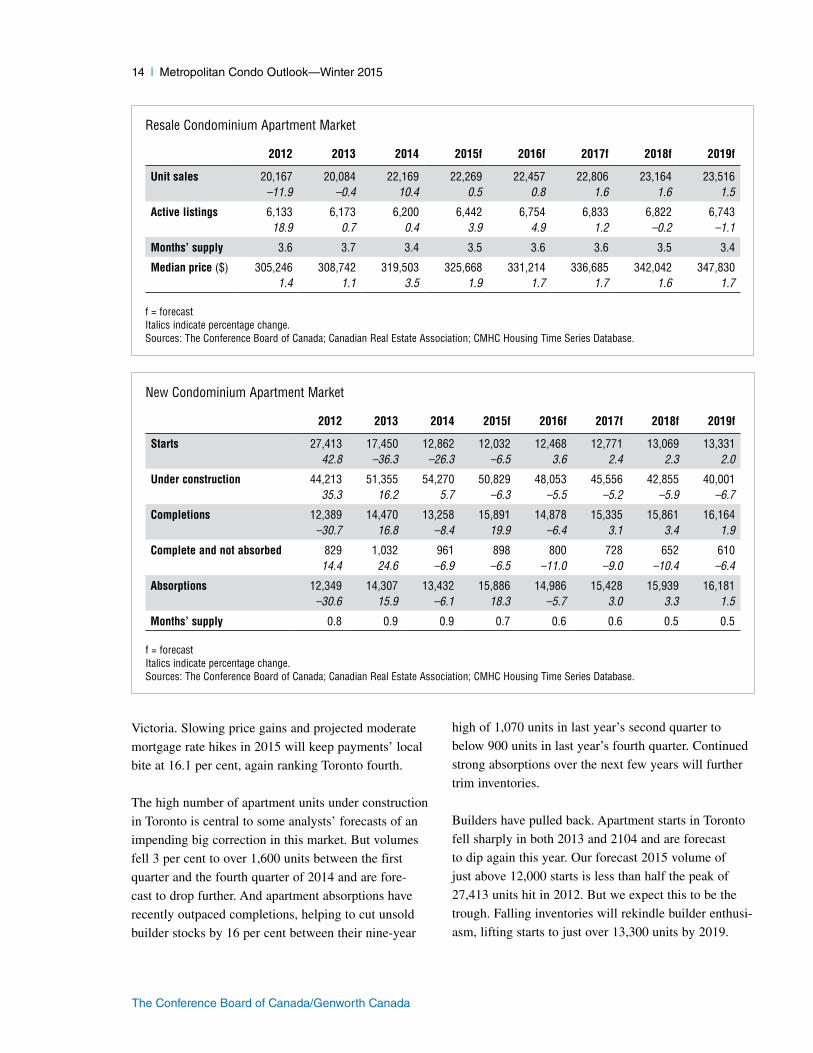

Victoria. Slowing price gains and projected moderate

mortgage rate hikes in 2015 will keep payments’ local

bite at 16.1 per cent, again ranking Toronto fourth.

The high number of apartment units under construction

in Toronto is central to some analysts’ forecasts of an

impending big correction in this market. But volumes

fell 3 per cent to over 1,600 units between the first

quarter and the fourth quarter of 2014 and are fore-

cast to drop further. And apartment absorptions have

recently outpaced completions, helping to cut unsold

builder stocks by 16 per cent between their nine-year

high of 1,070 units in last year’s second quarter to

below 900 units in last year’s fourth quarter. Continued

strong absorptions over the next few years will further

trim inventories.

Builders have pulled back. Apartment starts in Toronto

fell sharply in both 2013 and 2104 and are forecast

to dip again this year. Our forecast 2015 volume of

just above 12,000 starts is less than half the peak of

27,413 units hit in 2012. But we expect this to be the

trough. Falling inventories will rekindle builder enthusi-

asm, lifting starts to just over 13,300 units by 2019.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 20,167 20,084 22,169 22,269 22,457 22,806 23,164 23,516–11.9 –0.4 10.4 0.5 0.8 1.6 1.6 1.5

Active listings 6,133 6,173 6,200 6,442 6,754 6,833 6,822 6,74318.9 0.7 0.4 3.9 4.9 1.2 –0.2 –1.1

Months’ supply 3.6 3.7 3.4 3.5 3.6 3.6 3.5 3.4

Median price ($) 305,246 308,742 319,503 325,668 331,214 336,685 342,042 347,8301.4 1.1 3.5 1.9 1.7 1.7 1.6 1.7

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 27,413 17,450 12,862 12,032 12,468 12,771 13,069 13,33142.8 –36.3 –26.3 –6.5 3.6 2.4 2.3 2.0

Under construction 44,213 51,355 54,270 50,829 48,053 45,556 42,855 40,00135.3 16.2 5.7 –6.3 –5.5 –5.2 –5.9 –6.7

Completions 12,389 14,470 13,258 15,891 14,878 15,335 15,861 16,164–30.7 16.8 –8.4 19.9 –6.4 3.1 3.4 1.9

Complete and not absorbed 829 1,032 961 898 800 728 652 61014.4 24.6 –6.9 –6.5 –11.0 –9.0 –10.4 –6.4

Absorptions 12,349 14,307 13,432 15,886 14,986 15,428 15,939 16,181–30.6 15.9 –6.1 18.3 –5.7 3.0 3.3 1.5

Months’ supply 0.8 0.9 0.9 0.7 0.6 0.6 0.5 0.5

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

Winter 2015—Metropolitan Condo Outlook | 15

The Conference Board of Canada/Genworth Canada

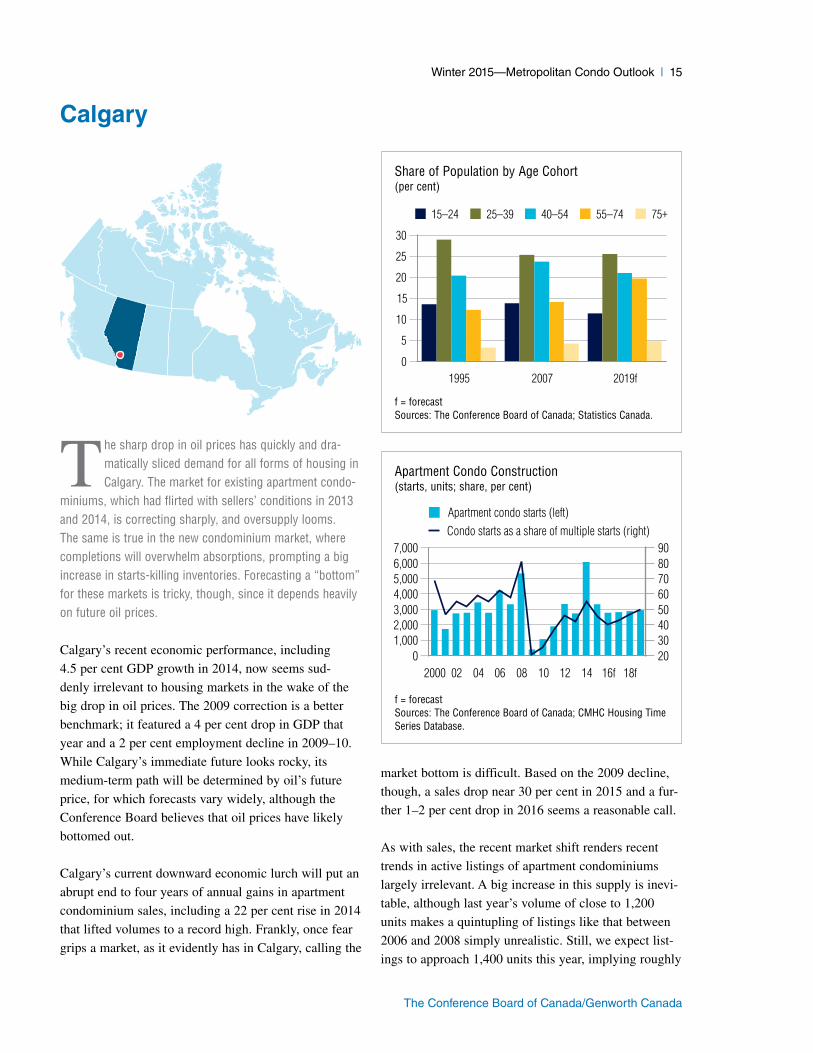

T he sharp drop in oil prices has quickly and dra-matically sliced demand for all forms of housing in Calgary. The market for existing apartment condo-

miniums, which had flirted with sellers’ conditions in 2013 and 2014, is correcting sharply, and oversupply looms. The same is true in the new condominium market, where completions will overwhelm absorptions, prompting a big increase in starts-killing inventories. Forecasting a “bottom” for these markets is tricky, though, since it depends heavily on future oil prices.

Calgary’s recent economic performance, including

4.5 per cent GDP growth in 2014, now seems sud-

denly irrelevant to housing markets in the wake of the

big drop in oil prices. The 2009 correction is a better

benchmark; it featured a 4 per cent drop in GDP that

year and a 2 per cent employment decline in 2009–10.

While Calgary’s immediate future looks rocky, its

medium-term path will be determined by oil’s future

price, for which forecasts vary widely, although the

Conference Board believes that oil prices have likely

bottomed out.

Calgary’s current downward economic lurch will put an

abrupt end to four years of annual gains in apartment

condominium sales, including a 22 per cent rise in 2014

that lifted volumes to a record high. Frankly, once fear

grips a market, as it evidently has in Calgary, calling the

market bottom is difficult. Based on the 2009 decline,

though, a sales drop near 30 per cent in 2015 and a fur-

ther 1–2 per cent drop in 2016 seems a reasonable call.

As with sales, the recent market shift renders recent

trends in active listings of apartment condominiums

largely irrelevant. A big increase in this supply is inevi-

table, although last year’s volume of close to 1,200

units makes a quintupling of listings like that between

2006 and 2008 simply unrealistic. Still, we expect list-

ings to approach 1,400 units this year, implying roughly

Calgary

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

1,0002,0003,0004,0005,0006,0007,000

2030405060708090

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

16 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

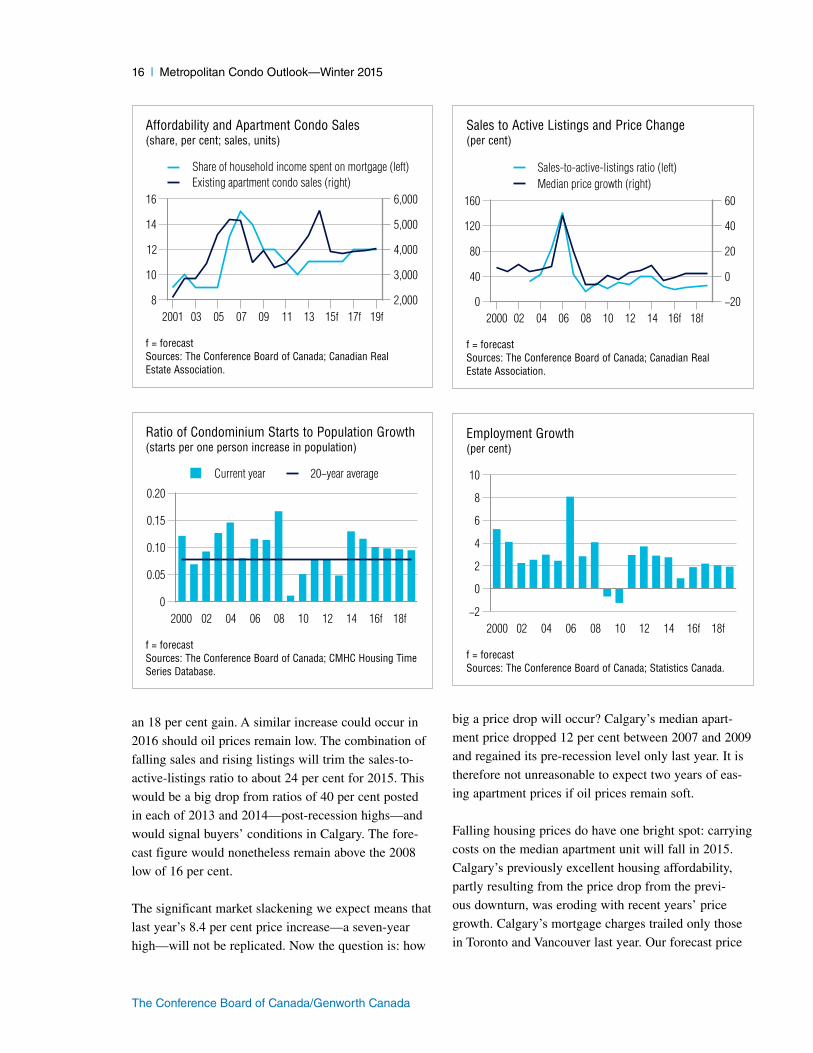

an 18 per cent gain. A similar increase could occur in

2016 should oil prices remain low. The combination of

falling sales and rising listings will trim the sales-to-

active-listings ratio to about 24 per cent for 2015. This

would be a big drop from ratios of 40 per cent posted

in each of 2013 and 2014—post-recession highs—and

would signal buyers’ conditions in Calgary. The fore-

cast figure would nonetheless remain above the 2008

low of 16 per cent.

The significant market slackening we expect means that

last year’s 8.4 per cent price increase—a seven-year

high—will not be replicated. Now the question is: how

big a price drop will occur? Calgary’s median apart-

ment price dropped 12 per cent between 2007 and 2009

and regained its pre-recession level only last year. It is

therefore not unreasonable to expect two years of eas-

ing apartment prices if oil prices remain soft.

Falling housing prices do have one bright spot: carrying

costs on the median apartment unit will fall in 2015.

Calgary’s previously excellent housing affordability,

partly resulting from the price drop from the previ-

ous downturn, was eroding with recent years’ price

growth. Calgary’s mortgage charges trailed only those

in Toronto and Vancouver last year. Our forecast price

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f8

10

12

14

16

2,000

3,000

4,000

5,000

6,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f0

40

80

120

160

−20

0

20

40

60

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.05

0.10

0.15

0.20

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−2

0

2

4

6

8

10

Winter 2015—Metropolitan Condo Outlook | 17

The Conference Board of Canada/Genworth Canada

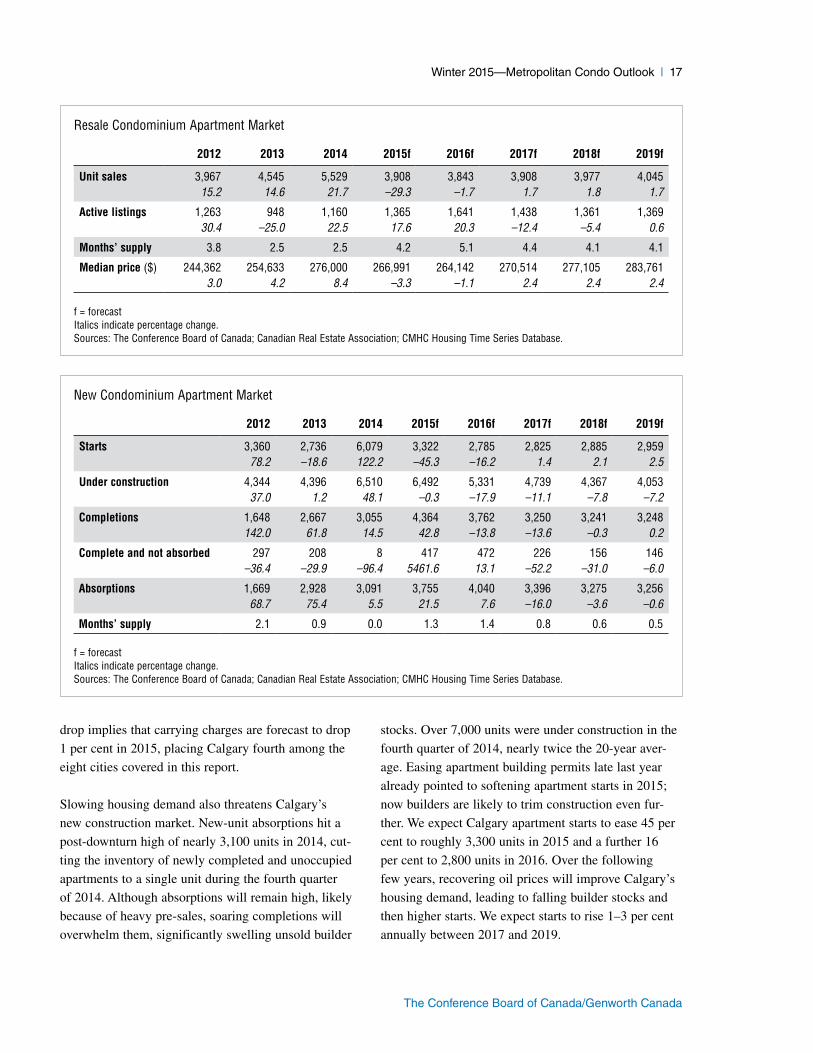

drop implies that carrying charges are forecast to drop

1 per cent in 2015, placing Calgary fourth among the

eight cities covered in this report.

Slowing housing demand also threatens Calgary’s

new construction market. New-unit absorptions hit a

post-downturn high of nearly 3,100 units in 2014, cut-

ting the inventory of newly completed and unoccupied

apartments to a single unit during the fourth quarter

of 2014. Although absorptions will remain high, likely

because of heavy pre-sales, soaring completions will

overwhelm them, significantly swelling unsold builder

stocks. Over 7,000 units were under construction in the

fourth quarter of 2014, nearly twice the 20-year aver-

age. Easing apartment building permits late last year

already pointed to softening apartment starts in 2015;

now builders are likely to trim construction even fur-

ther. We expect Calgary apartment starts to ease 45 per

cent to roughly 3,300 units in 2015 and a further 16

per cent to 2,800 units in 2016. Over the following

few years, recovering oil prices will improve Calgary’s

housing demand, leading to falling builder stocks and

then higher starts. We expect starts to rise 1–3 per cent

annually between 2017 and 2019.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 3,967 4,545 5,529 3,908 3,843 3,908 3,977 4,04515.2 14.6 21.7 –29.3 –1.7 1.7 1.8 1.7

Active listings 1,263 948 1,160 1,365 1,641 1,438 1,361 1,36930.4 –25.0 22.5 17.6 20.3 –12.4 –5.4 0.6

Months’ supply 3.8 2.5 2.5 4.2 5.1 4.4 4.1 4.1

Median price ($) 244,362 254,633 276,000 266,991 264,142 270,514 277,105 283,7613.0 4.2 8.4 –3.3 –1.1 2.4 2.4 2.4

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 3,360 2,736 6,079 3,322 2,785 2,825 2,885 2,95978.2 –18.6 122.2 –45.3 –16.2 1.4 2.1 2.5

Under construction 4,344 4,396 6,510 6,492 5,331 4,739 4,367 4,05337.0 1.2 48.1 –0.3 –17.9 –11.1 –7.8 –7.2

Completions 1,648 2,667 3,055 4,364 3,762 3,250 3,241 3,248142.0 61.8 14.5 42.8 –13.8 –13.6 –0.3 0.2

Complete and not absorbed 297 208 8 417 472 226 156 146–36.4 –29.9 –96.4 5461.6 13.1 –52.2 –31.0 –6.0

Absorptions 1,669 2,928 3,091 3,755 4,040 3,396 3,275 3,25668.7 75.4 5.5 21.5 7.6 –16.0 –3.6 –0.6

Months’ supply 2.1 0.9 0.0 1.3 1.4 0.8 0.6 0.5

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

18 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

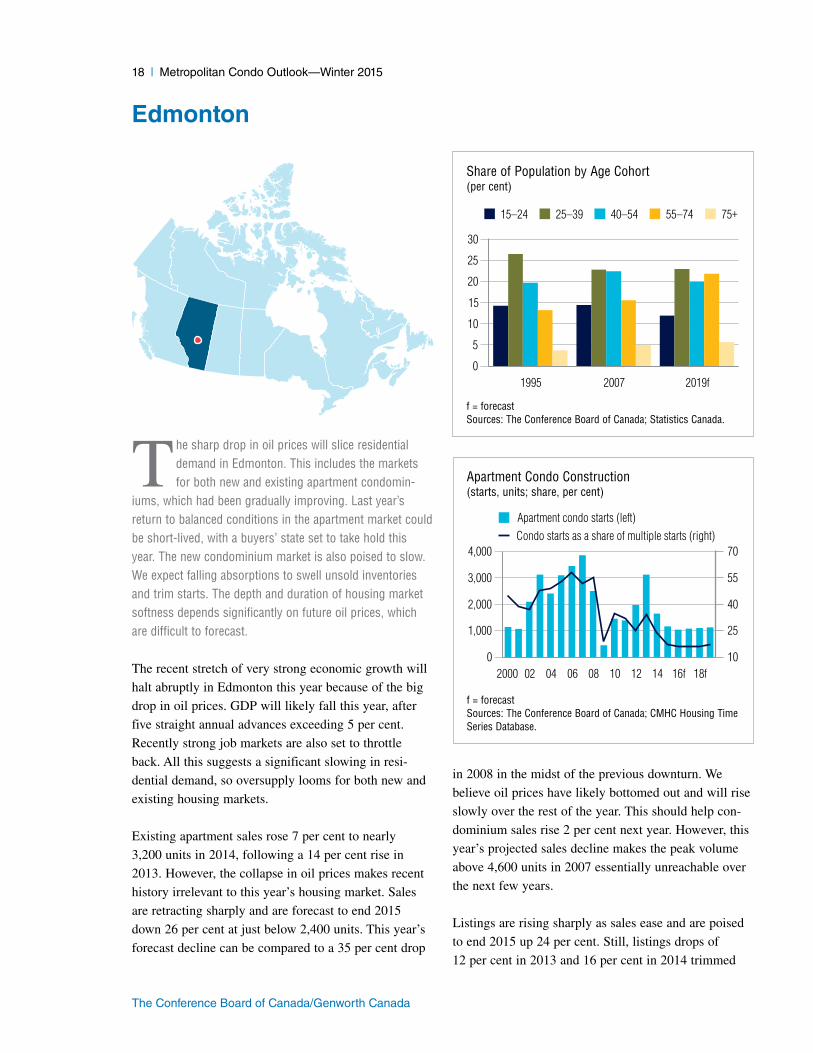

T he sharp drop in oil prices will slice residential demand in Edmonton. This includes the markets for both new and existing apartment condomin-

iums, which had been gradually improving. Last year’s return to balanced conditions in the apartment market could be short-lived, with a buyers’ state set to take hold this year. The new condominium market is also poised to slow. We expect falling absorptions to swell unsold inventories and trim starts. The depth and duration of housing market softness depends significantly on future oil prices, which are difficult to forecast.

The recent stretch of very strong economic growth will

halt abruptly in Edmonton this year because of the big

drop in oil prices. GDP will likely fall this year, after

five straight annual advances exceeding 5 per cent.

Recently strong job markets are also set to throttle

back. All this suggests a significant slowing in resi-

dential demand, so oversupply looms for both new and

existing housing markets.

Existing apartment sales rose 7 per cent to nearly

3,200 units in 2014, following a 14 per cent rise in

2013. However, the collapse in oil prices makes recent

history irrelevant to this year’s housing market. Sales

are retracting sharply and are forecast to end 2015

down 26 per cent at just below 2,400 units. This year’s

forecast decline can be compared to a 35 per cent drop

in 2008 in the midst of the previous downturn. We

believe oil prices have likely bottomed out and will rise

slowly over the rest of the year. This should help con-

dominium sales rise 2 per cent next year. However, this

year’s projected sales decline makes the peak volume

above 4,600 units in 2007 essentially unreachable over

the next few years.

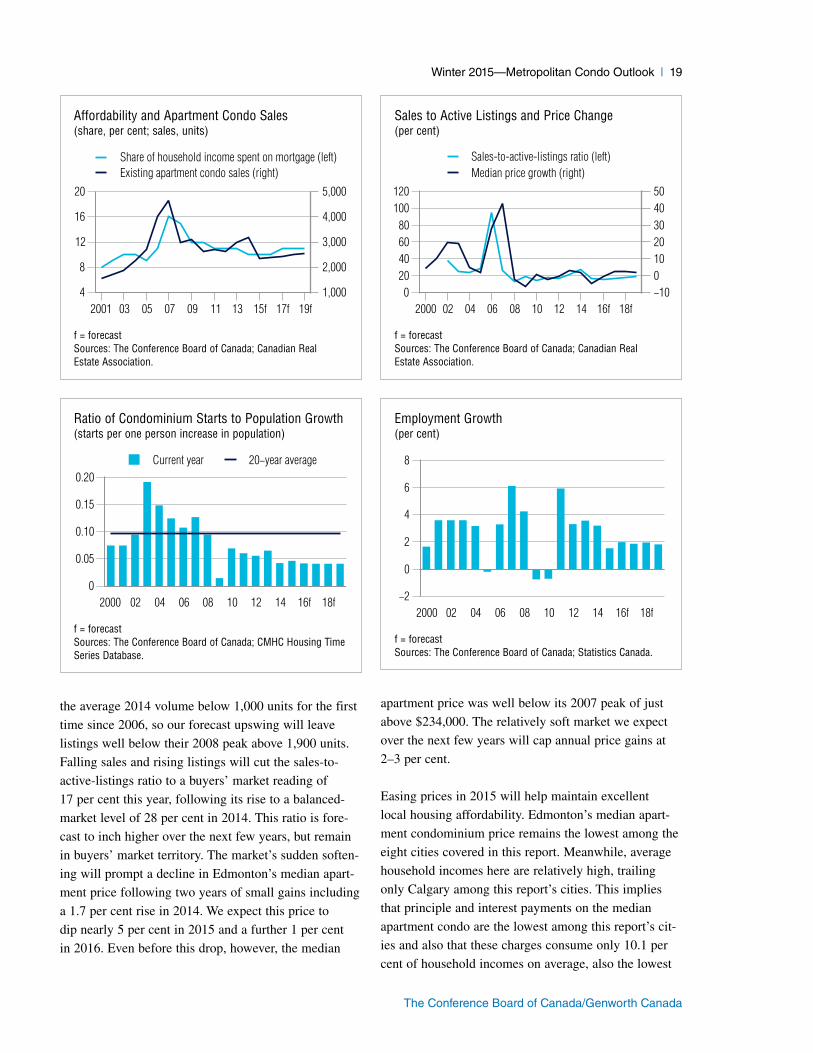

Listings are rising sharply as sales ease and are poised

to end 2015 up 24 per cent. Still, listings drops of

12 per cent in 2013 and 16 per cent in 2014 trimmed

Edmonton

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

1,000

2,000

3,000

4,000

10

25

40

55

70

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

Winter 2015—Metropolitan Condo Outlook | 19

The Conference Board of Canada/Genworth Canada

the average 2014 volume below 1,000 units for the first

time since 2006, so our forecast upswing will leave

listings well below their 2008 peak above 1,900 units.

Falling sales and rising listings will cut the sales-to-

active-listings ratio to a buyers’ market reading of

17 per cent this year, following its rise to a balanced-

market level of 28 per cent in 2014. This ratio is fore-

cast to inch higher over the next few years, but remain

in buyers’ market territory. The market’s sudden soften-

ing will prompt a decline in Edmonton’s median apart-

ment price following two years of small gains including

a 1.7 per cent rise in 2014. We expect this price to

dip nearly 5 per cent in 2015 and a further 1 per cent

in 2016. Even before this drop, however, the median

apartment price was well below its 2007 peak of just

above $234,000. The relatively soft market we expect

over the next few years will cap annual price gains at

2–3 per cent.

Easing prices in 2015 will help maintain excellent

local housing affordability. Edmonton’s median apart-

ment condominium price remains the lowest among the

eight cities covered in this report. Meanwhile, average

household incomes here are relatively high, trailing

only Calgary among this report’s cities. This implies

that principle and interest payments on the median

apartment condo are the lowest among this report’s cit-

ies and also that these charges consume only 10.1 per

cent of household incomes on average, also the lowest

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f4

8

12

16

20

1,000

2,000

3,000

4,000

5,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f0

20406080

100120

−1001020304050

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.05

0.10

0.15

0.20Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−2

0

2

4

6

8

20 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

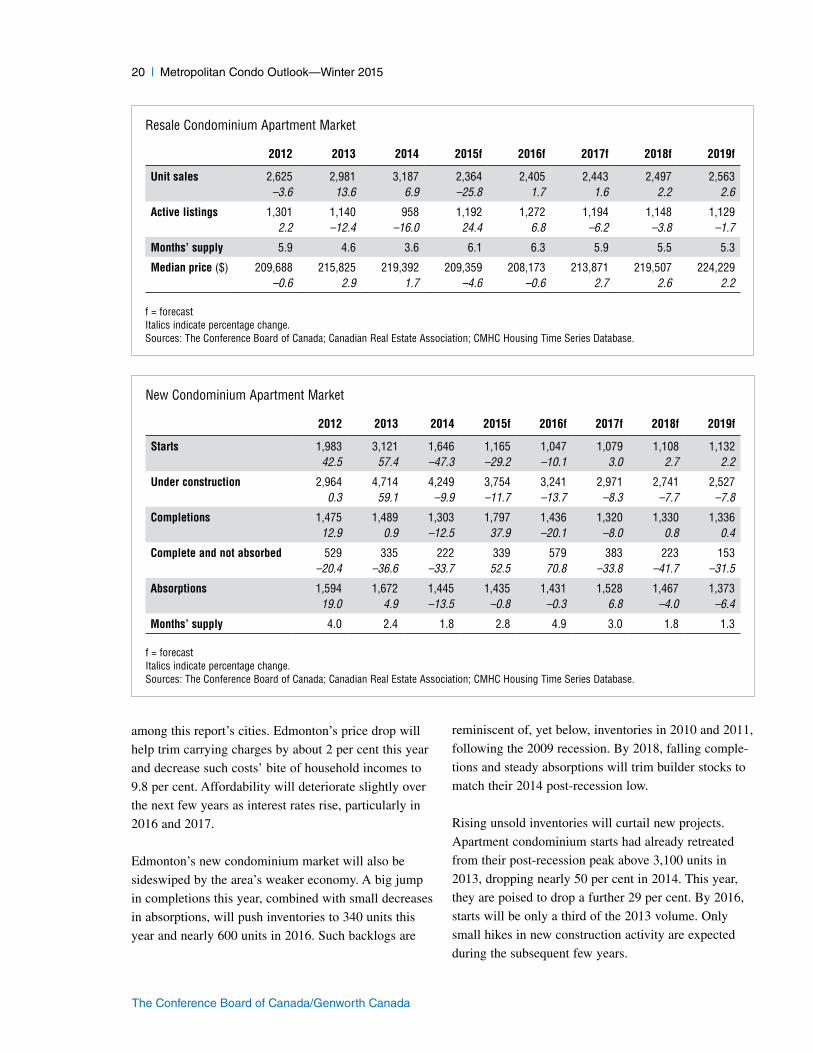

among this report’s cities. Edmonton’s price drop will

help trim carrying charges by about 2 per cent this year

and decrease such costs’ bite of household incomes to

9.8 per cent. Affordability will deteriorate slightly over

the next few years as interest rates rise, particularly in

2016 and 2017.

Edmonton’s new condominium market will also be

sideswiped by the area’s weaker economy. A big jump

in completions this year, combined with small decreases

in absorptions, will push inventories to 340 units this

year and nearly 600 units in 2016. Such backlogs are

reminiscent of, yet below, inventories in 2010 and 2011,

following the 2009 recession. By 2018, falling comple-

tions and steady absorptions will trim builder stocks to

match their 2014 post-recession low.

Rising unsold inventories will curtail new projects.

Apartment condominium starts had already retreated

from their post-recession peak above 3,100 units in

2013, dropping nearly 50 per cent in 2014. This year,

they are poised to drop a further 29 per cent. By 2016,

starts will be only a third of the 2013 volume. Only

small hikes in new construction activity are expected

during the subsequent few years.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 2,625 2,981 3,187 2,364 2,405 2,443 2,497 2,563–3.6 13.6 6.9 –25.8 1.7 1.6 2.2 2.6

Active listings 1,301 1,140 958 1,192 1,272 1,194 1,148 1,1292.2 –12.4 –16.0 24.4 6.8 –6.2 –3.8 –1.7

Months’ supply 5.9 4.6 3.6 6.1 6.3 5.9 5.5 5.3

Median price ($) 209,688 215,825 219,392 209,359 208,173 213,871 219,507 224,229–0.6 2.9 1.7 –4.6 –0.6 2.7 2.6 2.2

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 1,983 3,121 1,646 1,165 1,047 1,079 1,108 1,13242.5 57.4 –47.3 –29.2 –10.1 3.0 2.7 2.2

Under construction 2,964 4,714 4,249 3,754 3,241 2,971 2,741 2,5270.3 59.1 –9.9 –11.7 –13.7 –8.3 –7.7 –7.8

Completions 1,475 1,489 1,303 1,797 1,436 1,320 1,330 1,33612.9 0.9 –12.5 37.9 –20.1 –8.0 0.8 0.4

Complete and not absorbed 529 335 222 339 579 383 223 153–20.4 –36.6 –33.7 52.5 70.8 –33.8 –41.7 –31.5

Absorptions 1,594 1,672 1,445 1,435 1,431 1,528 1,467 1,37319.0 4.9 –13.5 –0.8 –0.3 6.8 –4.0 –6.4

Months’ supply 4.0 2.4 1.8 2.8 4.9 3.0 1.8 1.3

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

Winter 2015—Metropolitan Condo Outlook | 21

The Conference Board of Canada/Genworth Canada

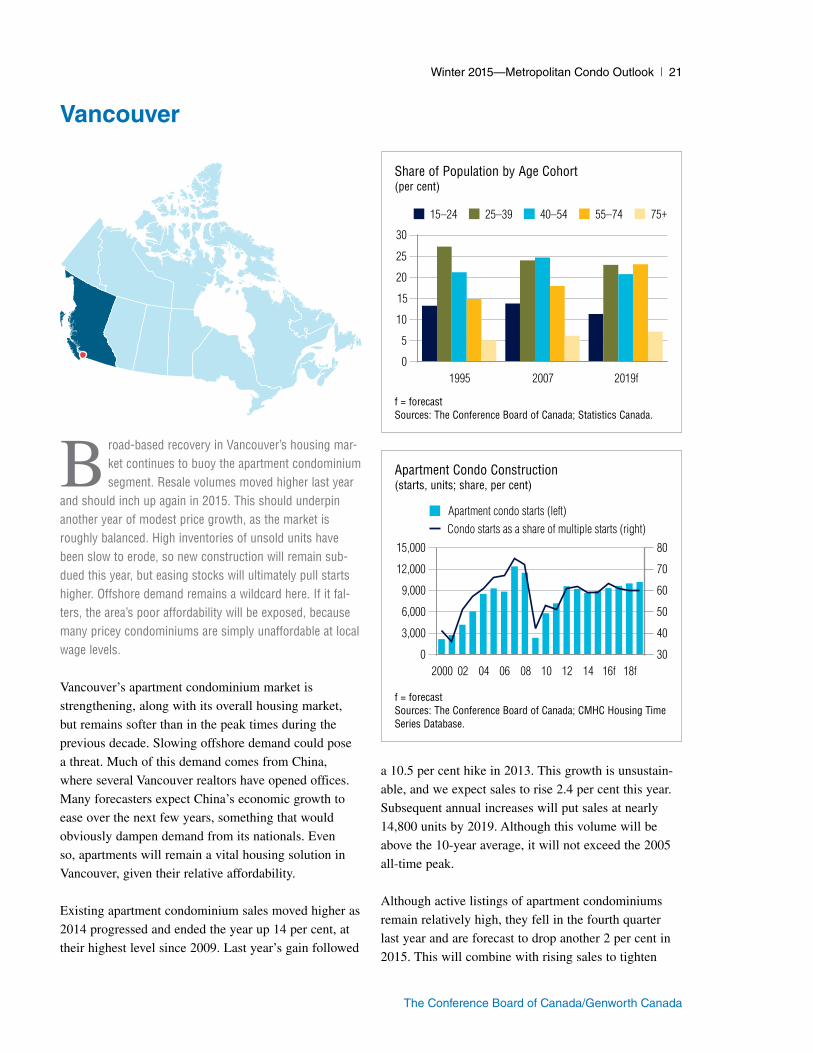

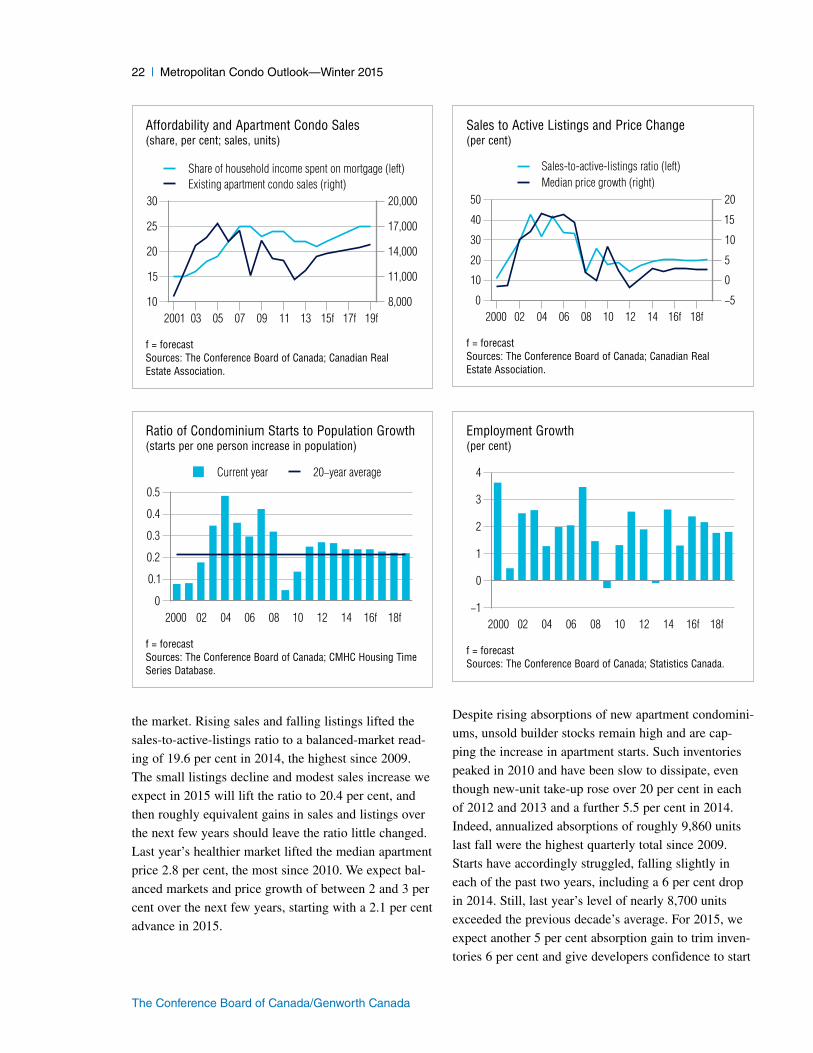

B road-based recovery in Vancouver’s housing mar-ket continues to buoy the apartment condominium segment. Resale volumes moved higher last year

and should inch up again in 2015. This should underpin another year of modest price growth, as the market is roughly balanced. High inventories of unsold units have been slow to erode, so new construction will remain sub-dued this year, but easing stocks will ultimately pull starts higher. Offshore demand remains a wildcard here. If it fal-ters, the area’s poor affordability will be exposed, because many pricey condominiums are simply unaffordable at local wage levels.

Vancouver’s apartment condominium market is

strengthening, along with its overall housing market,

but remains softer than in the peak times during the

previous decade. Slowing offshore demand could pose

a threat. Much of this demand comes from China,

where several Vancouver realtors have opened offices.

Many forecasters expect China’s economic growth to

ease over the next few years, something that would

obviously dampen demand from its nationals. Even

so, apartments will remain a vital housing solution in

Vancouver, given their relative affordability.

Existing apartment condominium sales moved higher as

2014 progressed and ended the year up 14 per cent, at

their highest level since 2009. Last year’s gain followed

a 10.5 per cent hike in 2013. This growth is unsustain-

able, and we expect sales to rise 2.4 per cent this year.

Subsequent annual increases will put sales at nearly

14,800 units by 2019. Although this volume will be

above the 10-year average, it will not exceed the 2005

all-time peak.

Although active listings of apartment condominiums

remain relatively high, they fell in the fourth quarter

last year and are forecast to drop another 2 per cent in

2015. This will combine with rising sales to tighten

Vancouver

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

3,000

6,000

9,000

12,000

15,000

30

40

50

60

70

80

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

22 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

the market. Rising sales and falling listings lifted the

sales-to-active-listings ratio to a balanced-market read-

ing of 19.6 per cent in 2014, the highest since 2009.

The small listings decline and modest sales increase we

expect in 2015 will lift the ratio to 20.4 per cent, and

then roughly equivalent gains in sales and listings over

the next few years should leave the ratio little changed.

Last year’s healthier market lifted the median apartment

price 2.8 per cent, the most since 2010. We expect bal-

anced markets and price growth of between 2 and 3 per

cent over the next few years, starting with a 2.1 per cent

advance in 2015.

Despite rising absorptions of new apartment condomini-

ums, unsold builder stocks remain high and are cap-

ping the increase in apartment starts. Such inventories

peaked in 2010 and have been slow to dissipate, even

though new-unit take-up rose over 20 per cent in each

of 2012 and 2013 and a further 5.5 per cent in 2014.

Indeed, annualized absorptions of roughly 9,860 units

last fall were the highest quarterly total since 2009.

Starts have accordingly struggled, falling slightly in

each of the past two years, including a 6 per cent drop

in 2014. Still, last year’s level of nearly 8,700 units

exceeded the previous decade’s average. For 2015, we

expect another 5 per cent absorption gain to trim inven-

tories 6 per cent and give developers confidence to start

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f10

15

20

25

30

8,000

11,000

14,000

17,000

20,000

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f0

10

20

30

40

50

−5

0

5

10

15

20

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.1

0.2

0.3

0.4

0.5

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−1

0

1

2

3

4

Winter 2015—Metropolitan Condo Outlook | 23

The Conference Board of Canada/Genworth Canada

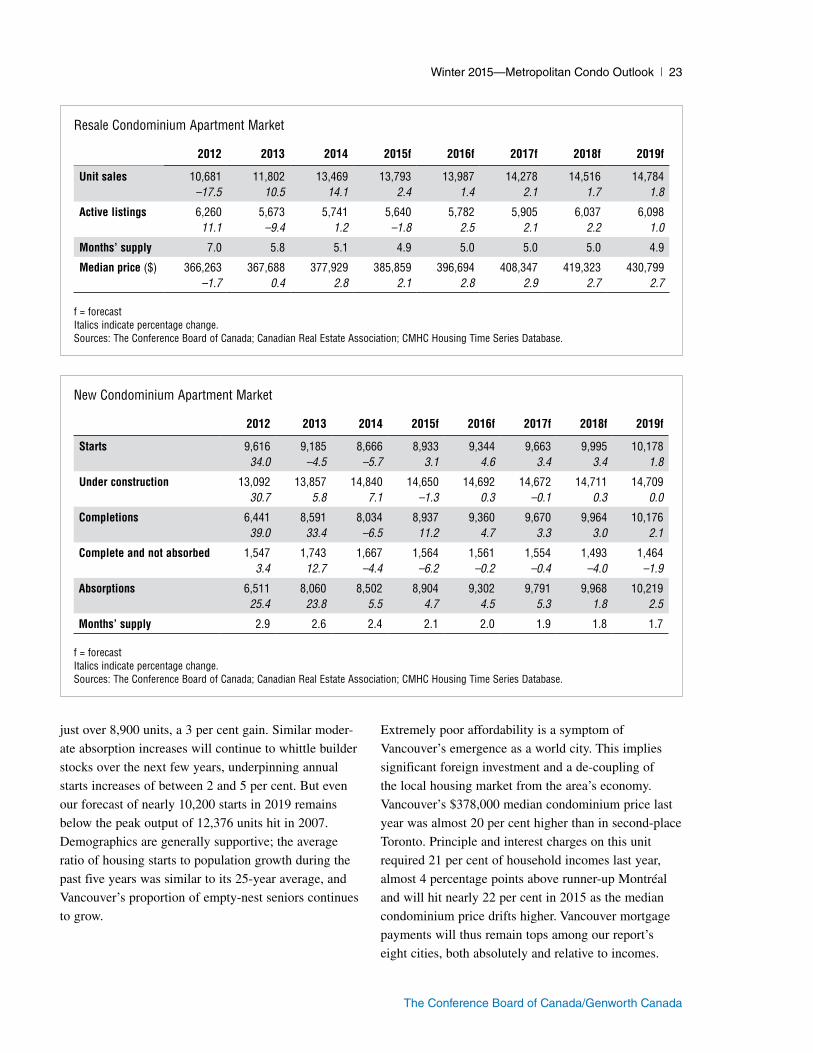

just over 8,900 units, a 3 per cent gain. Similar moder-

ate absorption increases will continue to whittle builder

stocks over the next few years, underpinning annual

starts increases of between 2 and 5 per cent. But even

our forecast of nearly 10,200 starts in 2019 remains

below the peak output of 12,376 units hit in 2007.

Demographics are generally supportive; the average

ratio of housing starts to population growth during the

past five years was similar to its 25-year average, and

Vancouver’s proportion of empty-nest seniors continues

to grow.

Extremely poor affordability is a symptom of

Vancouver’s emergence as a world city. This implies

significant foreign investment and a de-coupling of

the local housing market from the area’s economy.

Vancouver’s $378,000 median condominium price last

year was almost 20 per cent higher than in second-place

Toronto. Principle and interest charges on this unit

required 21 per cent of household incomes last year,

almost 4 percentage points above runner-up Montréal

and will hit nearly 22 per cent in 2015 as the median

condominium price drifts higher. Vancouver mortgage

payments will thus remain tops among our report’s

eight cities, both absolutely and relative to incomes.

Resale Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Unit sales 10,681 11,802 13,469 13,793 13,987 14,278 14,516 14,784–17.5 10.5 14.1 2.4 1.4 2.1 1.7 1.8

Active listings 6,260 5,673 5,741 5,640 5,782 5,905 6,037 6,09811.1 –9.4 1.2 –1.8 2.5 2.1 2.2 1.0

Months’ supply 7.0 5.8 5.1 4.9 5.0 5.0 5.0 4.9

Median price ($) 366,263 367,688 377,929 385,859 396,694 408,347 419,323 430,799–1.7 0.4 2.8 2.1 2.8 2.9 2.7 2.7

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

New Condominium Apartment Market

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Starts 9,616 9,185 8,666 8,933 9,344 9,663 9,995 10,17834.0 –4.5 –5.7 3.1 4.6 3.4 3.4 1.8

Under construction 13,092 13,857 14,840 14,650 14,692 14,672 14,711 14,70930.7 5.8 7.1 –1.3 0.3 –0.1 0.3 0.0

Completions 6,441 8,591 8,034 8,937 9,360 9,670 9,964 10,17639.0 33.4 –6.5 11.2 4.7 3.3 3.0 2.1

Complete and not absorbed 1,547 1,743 1,667 1,564 1,561 1,554 1,493 1,4643.4 12.7 –4.4 –6.2 –0.2 –0.4 –4.0 –1.9

Absorptions 6,511 8,060 8,502 8,904 9,302 9,791 9,968 10,21925.4 23.8 5.5 4.7 4.5 5.3 1.8 2.5

Months’ supply 2.9 2.6 2.4 2.1 2.0 1.9 1.8 1.7

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Canadian Real Estate Association; CMHC Housing Time Series Database.

24 | Metropolitan Condo Outlook—Winter 2015

The Conference Board of Canada/Genworth Canada

T his year, Victoria’s first employment gains since 2012 may finally signal sustained, albeit modest, improvement for an apartment condominium mar-

ket previously shackled by a soft economy, tepid population growth, and poor affordability. The apartment resale market firmed in 2014 and is expected to strengthen further this year. Transactions will remain muted by recent standards though, and prices will stay below their peak. On the new construction side, last year’s big drop in starts will eventu-ally trim high inventories and allow modest construction increases over the next few years.

Victoria’s flat GDP and falling employment have

limited demand for all forms of housing. But modest

economic and job growth, along with the persistence

of relatively low interest rates, should finally improve

consumer interest; this, combined with the clearing of

apartment condominium inventory backlogs following a

large decline in starts last year, suggests this market has

finally bottomed. Shoots of recovery will emerge this

year and then strengthen.

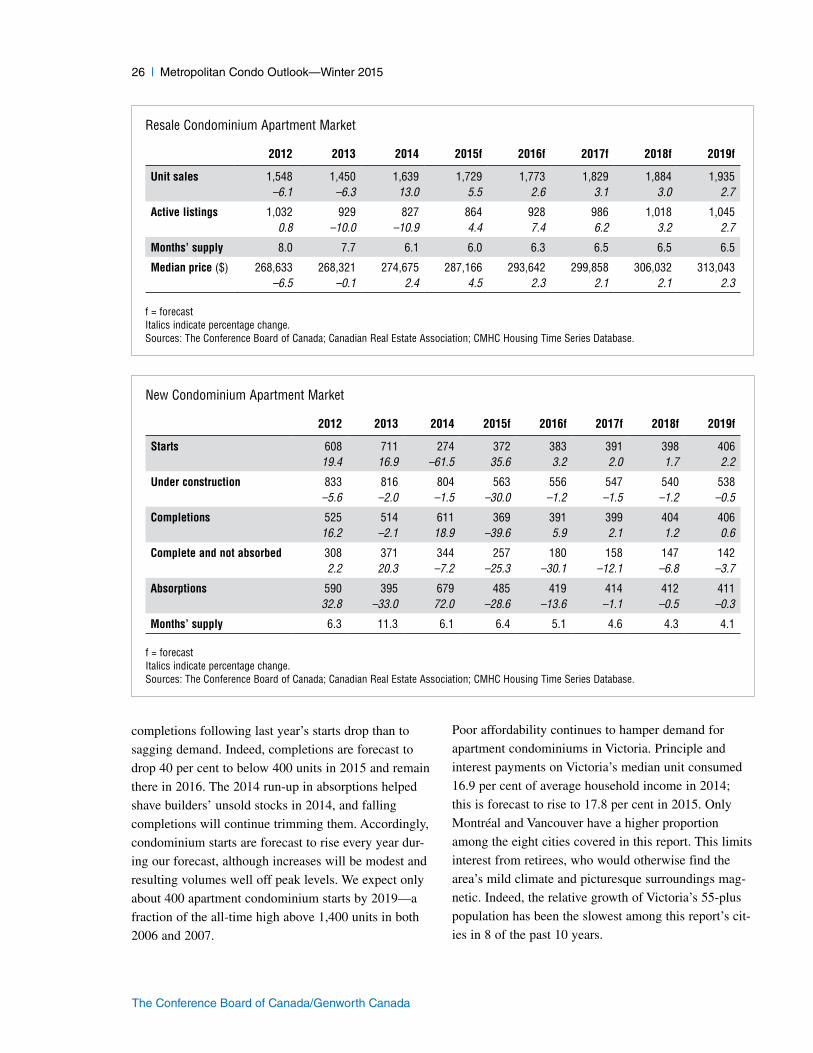

Existing apartment condominium sales shook off four

straight annual declines to rise 13 per cent in 2014.

Sales strengthened throughout the year, and fourth-

quarter volumes were the highest quarterly level in

over three years. Despite these gains, last year’s total of

1,639 sales remained well off the 2,400-unit peak hit in

2007. We expect sales to rise a further 5 per cent this

year and by an average of roughly 3 per cent annually

thereafter. This would put 2019 transactions just above

the annual average of nearly 1,900 units traded here

during the past decade.

The falling number of active apartment listings in 2013

was likely due mainly to the expiry of listings or their

withdrawal from the market by frustrated potential

vendors. But rising sales failed to prevent a further

11 per cent drop last year. We think listings will rise

Victoria

Share of Population by Age Cohort(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

1995 2007 2019f0

5

10

15

20

25

30

15–24 25–39 40–54 55–74 75+

Apartment Condo Construction(starts, units; share, per cent)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

300

600

900

1,200

1,500

0

20

40

60

80

100

Apartment condo starts (left)Condo starts as a share of multiple starts (right)

Winter 2015—Metropolitan Condo Outlook | 25

The Conference Board of Canada/Genworth Canada

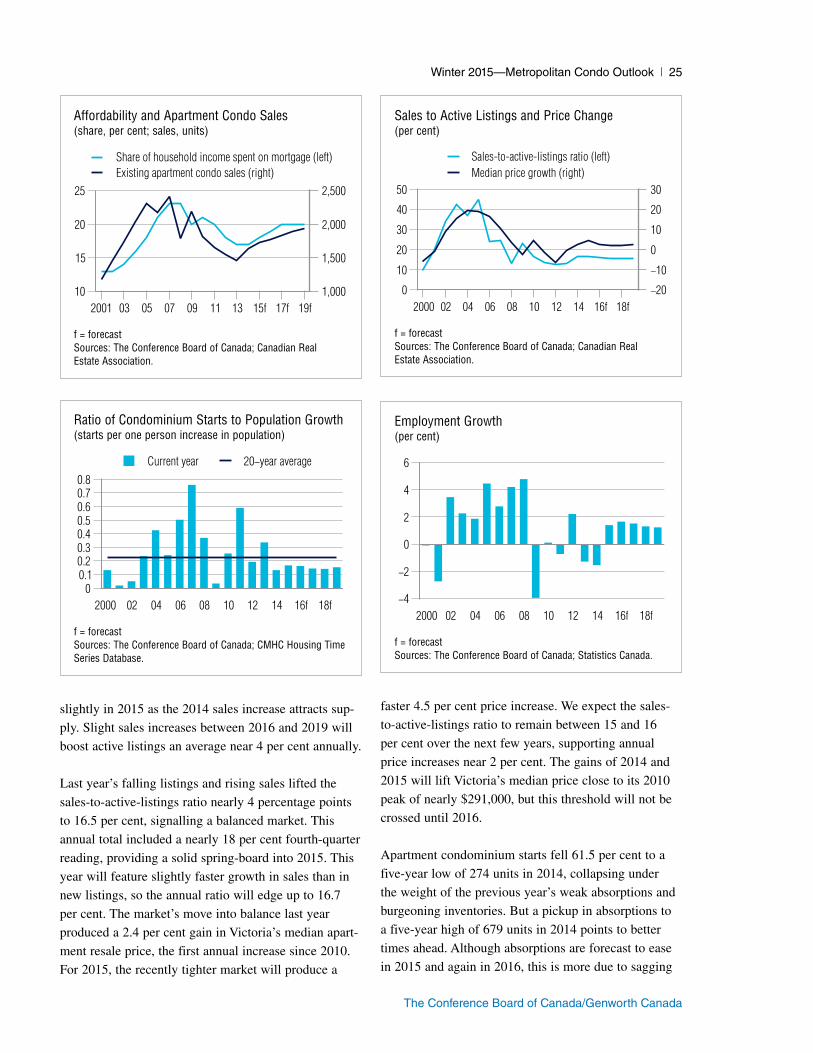

slightly in 2015 as the 2014 sales increase attracts sup-

ply. Slight sales increases between 2016 and 2019 will

boost active listings an average near 4 per cent annually.

Last year’s falling listings and rising sales lifted the

sales-to-active-listings ratio nearly 4 percentage points

to 16.5 per cent, signalling a balanced market. This

annual total included a nearly 18 per cent fourth-quarter

reading, providing a solid spring-board into 2015. This

year will feature slightly faster growth in sales than in

new listings, so the annual ratio will edge up to 16.7

per cent. The market’s move into balance last year

produced a 2.4 per cent gain in Victoria’s median apart-

ment resale price, the first annual increase since 2010.

For 2015, the recently tighter market will produce a

faster 4.5 per cent price increase. We expect the sales-

to-active-listings ratio to remain between 15 and 16

per cent over the next few years, supporting annual

price increases near 2 per cent. The gains of 2014 and

2015 will lift Victoria’s median price close to its 2010

peak of nearly $291,000, but this threshold will not be

crossed until 2016.

Apartment condominium starts fell 61.5 per cent to a

five-year low of 274 units in 2014, collapsing under

the weight of the previous year’s weak absorptions and

burgeoning inventories. But a pickup in absorptions to

a five-year high of 679 units in 2014 points to better

times ahead. Although absorptions are forecast to ease

in 2015 and again in 2016, this is more due to sagging

Affordability and Apartment Condo Sales(share, per cent; sales, units)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2001 03 05 07 09 11 13 15f 17f 19f10

15

20

25

1,000

1,500

2,000

2,500

Share of household income spent on mortgage (left)Existing apartment condo sales (right)

Sales to Active Listings and Price Change(per cent)

f = forecastSources: The Conference Board of Canada; Canadian Real Estate Association.

2000 02 04 06 08 10 12 14 16f 18f0

10

20

30

40

50

−20

−10

0

10

20

30

Sales-to-active-listings ratio (left)Median price growth (right)

Ratio of Condominium Starts to Population Growth(starts per one person increase in population)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2000 02 04 06 08 10 12 14 16f 18f0

0.10.20.30.40.50.60.70.8

Current year 20−year average

Employment Growth(per cent)

f = forecastSources: The Conference Board of Canada; Statistics Canada.

2000 02 04 06 08 10 12 14 16f 18f−4

−2

0

2

4

6