Embed Size (px)

Citation preview

Institutional Presentation

November/December 2010

Success Track Record

Foundation Strengthening/Expansion

10.6%

1983 1986 1989 1992 1995 1996 1997 1998 1999 2000 2001 2002

9.8%

10.0%

8.4%

6.5%

11010698

63

3524

17

(1) EBITDA Margin excludes extraordinary expenses.

ProprietaryTechnology

Startup ofMicrosiga

Franchising System

ISO 9001

Argentina

ISO 9001: 2000(Franchises)

MexicoFocus on

Managementand results

Growth in Margin

Gro

ss R

eve

nu

e(R

$ M

illio

n)

and

EBIT

DA

Mar

gin

(%)

¹

CMMI 12.4%

IPO

13.9%

392

247

173

18.4%

490

21.9%

2004 2005 2006 2007 2008

Acquisition

Acquisition

Midbyte and BCSAcquisitions

760

20.6%

33x EBITDA11x Revenue

2009

12.4%

126

2003

3

25.2%1,080

LTM

Operating Leverage1,205

GROWTH:17x EBITDA

8,5x Revenue

Cross-Selling

Structure of Business Model

(1) Does not include close to 5,000 employees of our franchises(2) Includes Infrastructure, HR BPO, Education and Service Desk

CoreSynergies Synergies

TOTVS Customer Service and Relationship

Software – Base and New Clients ServicesExpanded Business

Technology

ERP CRMBusiness

Intelligence

VerticalModules

Consulting

Value-Added Service2

4

TOTVS

74 Full TOTVS Distribution Channels

+ 26,200 customers~ 5,000 direct employees¹

Flexible Technology

Digital TV

7th worldwide in ERP-Suite* and 1st in growth

5

184

210

216

280

308

360

848

1,145

1,366

2,414

5,183

Epicor (USA)

Cegid (FRA)

Exact (NED)

Unit4 (NED)

TOTVS (BRA)

Lawson (USA)

Microsoft (USA)

Infor (USA)

Sage (UK)

Oracle (USA)

SAP (GER)

Source: Gartner - ERP Software, Worldwide, 2009

Market Update

-6.6%

0.8%

-12.3%

-1.3%

8.6%

-7.0%

-4.7%

-12.8%

-5.3%

-11.2%

-9.6%

*Licenses e Maintenance Revenues, in US$ million 2008 vs. 2009 Evolution

ERP-Suite Worldwide Ranking 2009

15.0%

26.8%

31.2%

27.0%

Market Share – Leadership in Latin America

6

Market Update

GARTNER (2009 – full year)

Source: Gartner – Market Share ERP Software, Worldwide, 2009

A

B

#4 Portugal

#1 Brazil#3 Argentina#3 Mexico

Others

Market Share – Absolute leader in Brazil

Source: IDC Latin America Semiannual ERM Applications Tracker 2009

7

Market Update

IDC (2009)

32.9%34.4%

37.9%

42.7%

33.2% 34.1%32.0%

29.9%

10.5%8.8% 8.3% 7.3%

2006 2007 2008 2009

A

B

GARTNER (2009)

1.7%1.1%

6.8%

24.4%

49.1%

16.9%A

B

CD

Source: Gartner – Market Share ERP Software. Worldwide. 2009

Others

Fundamentals and Business Model

8

TOTVS’ Differentials

Software = Basic Need

Underpenetrated Market

Environment

Macro / Market Changes

Target Market

Technology &

Product

Distribution

Licenses

Maintenance

Services

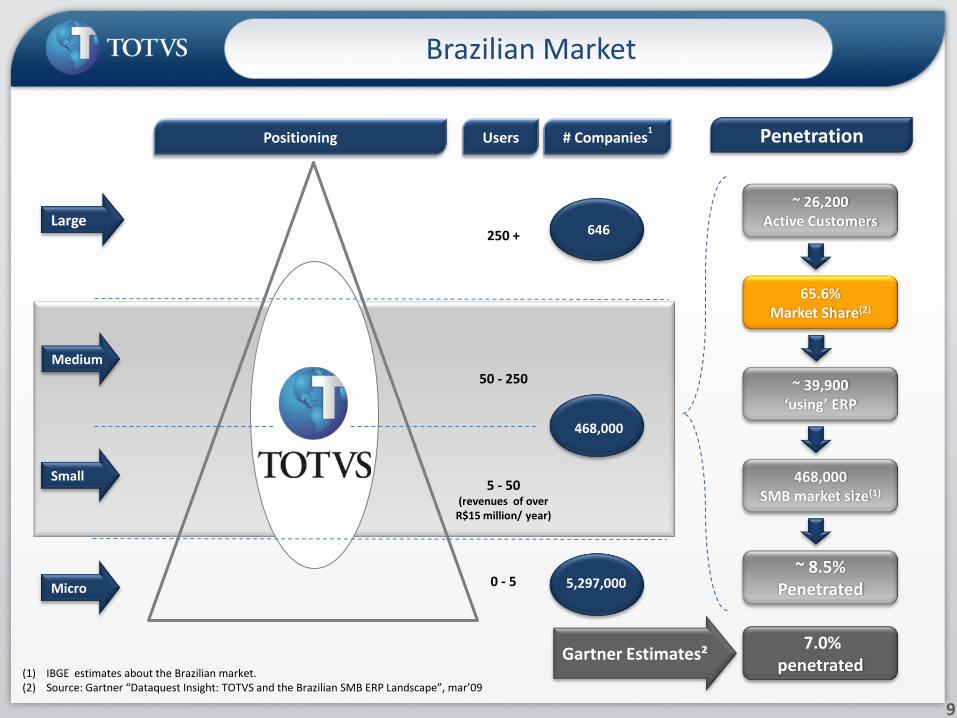

(1) IBGE estimates about the Brazilian market. (2) Source: Gartner “Dataquest Insight: TOTVS and the Brazilian SMB ERP Landscape”, mar’09

646

468,000

5,297,000

250 +

50 - 250

0 - 5

Large

Medium

Small

Micro

5 - 50(revenues of over

R$15 million/ year)

9

Brazilian Market

Positioning Users # Companies1

~ 26,200Active Customers

65.6%Market Share(2)

~ 39,900‘using’ ERP

468,000SMB market size(1)

~ 8.5%Penetrated

Penetration

Gartner Estimates²7.0%

penetrated

Revenue/Business Model

New Customers

Base Customers

NewCustomers

BasicImplementation

Base Customers

New Licenses

New Modules

Consultingand

VAS+

Licenses

Services

Maintenance

New Licenses

CorporateModel

TOTVS’ Business

10

Updates Upgrades(New version)

Help-desk

0.34 0.34 0.34 0.34 0.34 0.34 0.341.00

0.34

2.00

Y0 Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8

Traditional model Corporate model

Recurring Fees by Metric1 new licensesold per year

Y0 Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12… …

Diversified client base

Datasul and RM Sistemas contributed to diversify even more the company’s client base

(1) Based on TOTVS Brazil 2009 revenue.

Client Breakdown by Sector 1 Revenue Concentration 1

11-100 Largest

12%

Others82%

10 Largest

6%

11

TOTVS’ Business

Manufacturing39%

Services16%

Distribution and Logistics

12%

FinancialServices

8%

Construction and projects

7%

Others18%

Série 1

Segment and Size Approach

TOTVS 1 Services

TOTVS –Digital TV

Seri

es

T

TOTV

S A

grib

usi

ne

ss

TOTV

S M

anu

fact

uri

ng

TOTV

S Ed

uca

tio

nal

TOTV

S H

eal

th

TOTV

S C

on

stru

ctio

n &

Pro

ject

s

TOTV

S Fi

nan

cial

Se

rvic

es

TOTV

S Le

gal

TOTV

S Se

rvic

es

TOTV

S D

istr

ibu

tio

n &

Lo

gist

ics

TOTV

S R

eta

il

Seri

es

1Se

rie

s C

TOTVS Manufaturing1 TOTVS 1 Retail

Seri

es

3 TOTVS 3 RetailTOTVS

Manufacturing 3

12

Offering by Segment Offering by Size

Definition

Series 3

Series 1

Series T

TOTVS 1 Health

Size

Complexity

Segment Facts

13

+1,110 extractive and processing customers, +1,000 metal and plastic, +1,400 capital goods

Manufacturing

+900 department stores, +140 supermarkets, +280 building materials distributorsRetail

2,300 services providers, 400 Utilities providers, 470 travel and passengers transportationServices

12 million lives, +9,700 beds, medical registers to 35 specialties

Health

7 out of 10 top law firms, 10,000 lawyers

Legal

50 out of 100 Brazilian biggest comps. and 20 international builders, 450engineering and design customers Construction

and Projects

+200 sugar cane producers = 50% national crop, 120 grain producers,

1.5 million hectaresAgribusiness

+1,600 wholesaler distributors, 20% of shippers customers use our CRM

Distribution and Logistics

22k portfolios, 4k funds, 120k/dayconsumer credit transactions, R$1.5

trillion assets under custody, LA Financial Market Top provider

Financial Services

+700 Brazilian institutions, +1.5 million students, choice of 67% of the

consolidating groups Educational

Comprehensive Portfolio

14

TOTVS product architecture and platform

15

Technology

16

Innovative Model with Results

SaaS

PaaS

IaaS

Application

Framework

Middleware

Database

Op. System

Hardware

TCP/IP Protocol

Vanguard Growth Profitability

Public / Private Cloud

Series 1 Cloud

Series T Corporate Model

(iSaaS)byYouESB

byYouECM

Datacenter &Service Desk

17

Distribution

Presence and Dominance

Other Geographies

Latin America

Subsidiaries

Products only

Franchises

►1 Branch + 1 Franchise, Portugal

►1 Franchise, Angola

►+50 clients, over 8 countries

►Gartner: TOTVS’ ERP Market Share: 31.2% in 2009 - 1st company!

►IDC: TOTVS’ SMB Market Share: 34.25% in 2009 vs. 29.7% in 2008 – 1st company!

►Products over 15 countries

►Excluding Brazil:

+400 clients, +300 direct employees

+13 Full TOTVS distribution channels

Brazil Latin America

►Distribution Channels: 6 Branches + 52 Franchisees

►≈40 complementary channels working with TOTVS distribution network

►+27,000 clients

►49.1% Market share (Gartner)

►42.7% Market share (IDC)

►+4,700 Direct employees

18

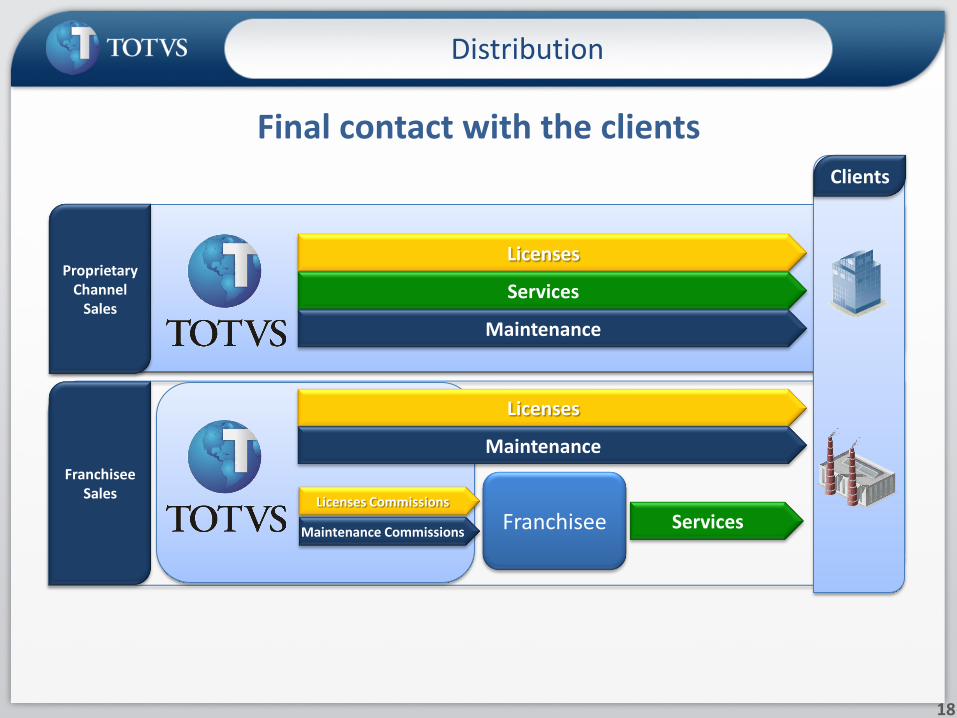

Distribution

Final contact with the clients

Franchisee

Licenses

Services

Maintenance

Services

Licenses

Maintenance

Licenses Commissions

Maintenance Commissions

Proprietary Channel

Sales

FranchiseeSales

Clients

Results 3Q10

Operational Highlights

Financials Highlights

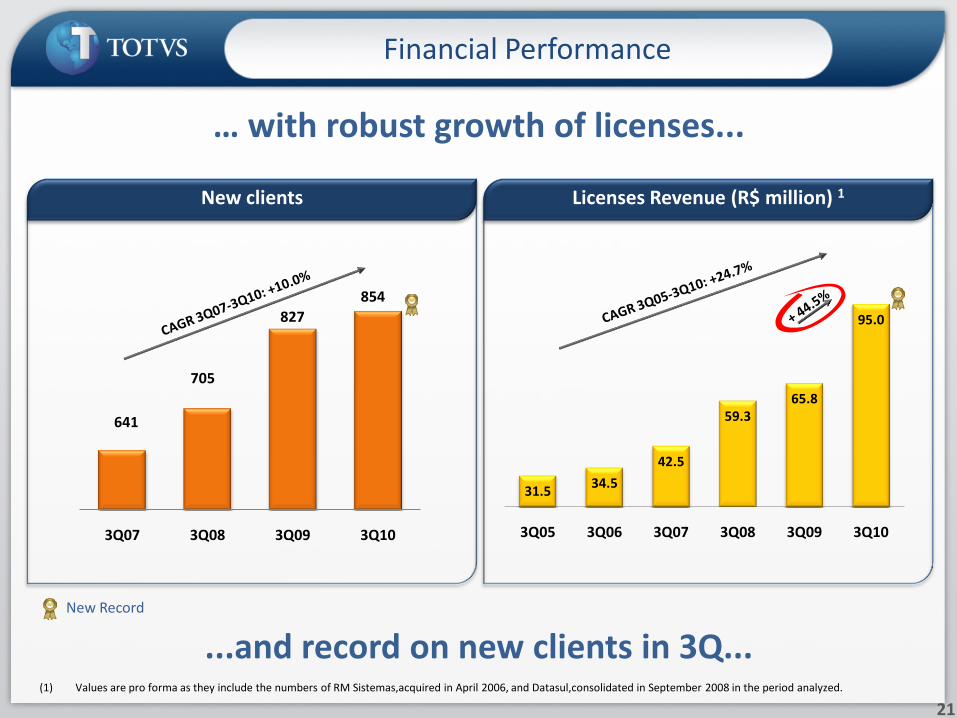

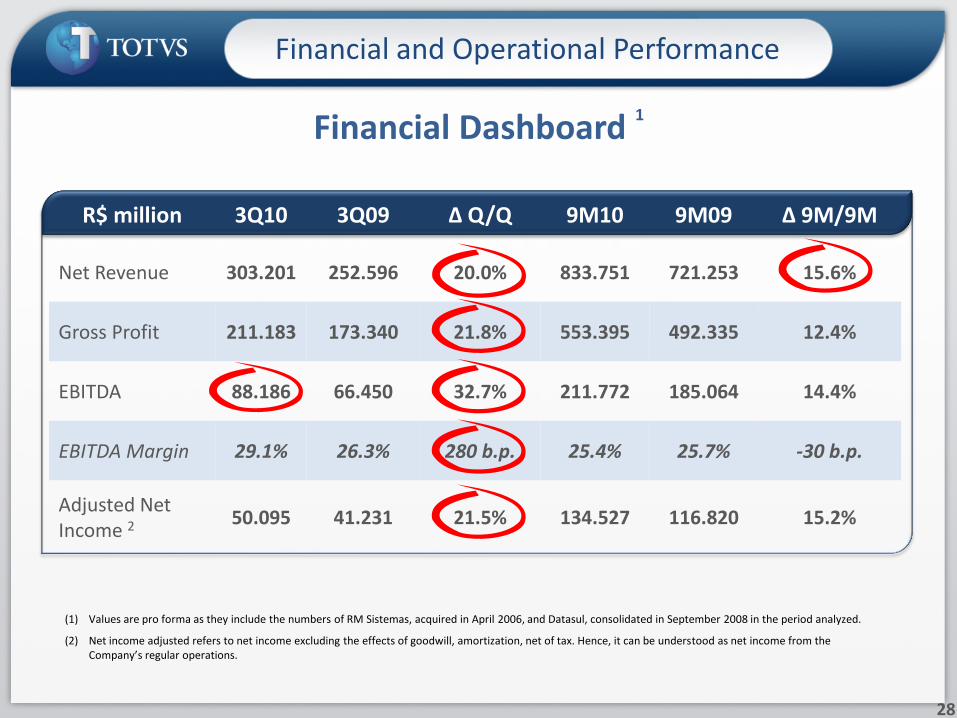

► Net Revenue: historical record, reached R$303.201 million, a 20.0% over 3Q10.

► Licenses Fees Revenue: historical record, 44.5% over 3Q09.

► Services Revenue: 7.6% growth (3Q10 vs. 3Q09).

► Maintenance Fees Revenue: historical record, R$140.125 million. Growth of 13.7% over

3Q09.

► EBITDA: R$88.186 million record in 3Q10, a 32.7% growth against 3Q09.

► Margin: 29.1% record in the quarter, 280 b.p. over 3Q09.

► Adjusted Net Income: R$50.095 million in 3Q10, 21.5% over 3Q09.

► 854 new clients in 3Q10, 14.6% growth over 2Q10, new historical record.

► Licenses sales to 4,523 clients (new + base) in the quarter, 5.5% over 2Q10.

► Acquisition of FDES ( Development Franchises).

► Sale of state of Paraná customer portfolio, allowing 2 “Full TOTVS” franchises creation in

the region.

► 306,870 share issuance for 15% of debentures conversion .

Recent Events

19th consecutive quarter of double-digit organic growth...

19

Gross and Net Revenue (R$ million) 1

120.2

136.2

168.5

218.6

252.6

303.2

136.5152.2

187.6

242.6

276.1

328.8

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

Net Revenue Gross Revenue

...presenting a consistent revenue growth

(1) Values are pro forma as they include the number of RM Sistemas, acquired in April 2006, and Datasul, consolidated in September 2008 in the period analyzed.

Financial Performance

20

344.2

397.4

477.4

611.4

721.3

833.8

386.5

444.6

529.5

680.9

788.4

913.4

9M05 9M06 9M07 9M08 9M09 9M10

Net Revenue Gross Revenue

New Record

31.534.5

42.5

59.365.8

95.0

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

… with robust growth of licenses...

(1) Values are pro forma as they include the numbers of RM Sistemas,acquired in April 2006, and Datasul,consolidated in September 2008 in the period analyzed.

Financial Performance

21

New clients

...and record on new clients in 3Q...

641

705

827

854

3Q07 3Q08 3Q09 3Q10

Licenses Revenue (R$ million) 1

New Record

… and services / maintenance improvements.

70.375.2

88.4

108.1

123.3

140.1

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

34.8

42.5

56.6

75.2

87.1 93.7

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

Maintenance Revenue (R$ million) 1Services Revenue (R$ million) 1

Financial Performance

22

New Record

(1) Values are pro forma as they include the numbers of RM Sistemas, acquired in April 2006, and Datasul,consolidated in September 2008 in the period analyzed.

2005 2006 2007 2008 2009

530.3

940.8

734.0

611.9

23.8%

24.6%

51.6%

27.3%

24.0%

48.7%

23.3%

29.4%

47.3%44.9%

30.3%

24.8%

1,080.3

23.1%

30.7%

46.2%

Gross Revenue (R$ million) 1

Gross Revenue Breakdown

Financial Performance

23

3Q09 3Q10

44.7%

31.5%

28.5%

42.6%

23.8%

28.9%

328.8

276.1

(1) Values are pro forma as they include the numbers of RM Sistemas,acquired in April 2006, and Datasul,consolidated in September 2008 in the period analyzed.

Licenses Services Maintenance

87.9109.0

12.2%

13.1%

9M09 9M10

32.339.3

12.8% 13.0%

3Q09 3Q10

8.110.0

3.2% 3.3%

3Q09 3Q10

536.2622.0

9M09 9M10

(1) Excluding depreciation, amortization expenses and non –recurring expenses.

Costs and Expenses Dashboard ¹

17.5 18.5

6.9%6.1%

3Q09 3Q10

57.0 54.7

7.9%

6.6%

9M09 9M10

20.424.5

2.8%2.9%

9M09 9M10

186.1 215.0

3Q09 3Q10

R&D (R$ million) x R&D / NR

Marketing Expenses (R$ million) x Mkt. Exp. / NRG&A (R$ million) x G&A / NR

Costs and Expenses ¹ (R$ million)

Financial Performance

24

423 494

628

718

825

526

629

796

955

1,101

3Q06 3Q07 3Q08 3Q09 3Q10

Operational Leverage

Financial Performance

25

EBITDA - 12M (R$ million)1 and 2

Costs and ExpensesEBITDANet Revenue

G&A / NR 1

14.7%

12.1%

9.7%

8.6%

6.9%6.1%

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

(1) Values are pro forma as they include the numbers of RM Sistemas,acquired in April 2006, and Datasul,consolidated in September 2008 in the period analyzed.(2) Last 12 months.

18.1%

17.0%

22.1%

20.0%

19.2%

20.8%

20.4%

22.4%

21.9%

22.2%

21.0%

21.3%

20.3%

22.1%

26.2%

24.4%

26.3%

24.0%

23.4%

23.2%

29.1%

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

EBITDA and Margin

Financial Performance

26

EBITDA and Margin (R$ million) 1

New Record

21.826.1

37.0

44.4

66.5

88.2

18.1%19.2%

21.9%

20.3%

26.3%

29.1%

0,10

0,15

0,20

0,25

0,30

0

20

40

60

80

100

120

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10

EBITDA EBITDA Margin

EBITDA Margin Behavior 1

(1) Values are pro forma as they include the numbers of RM Sistemas,acquired in April 2006, and Datasul,consolidated in September 2008 in the period analyzed.

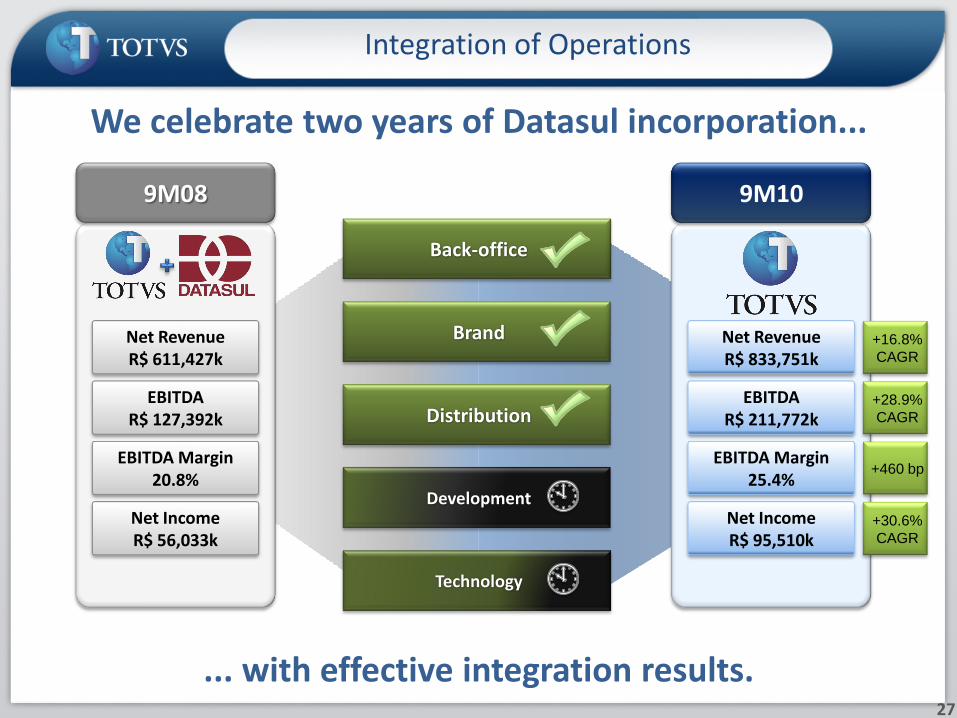

Integration of Operations

9M08

Net RevenueR$ 611,427k

Net RevenueR$ 833,751k

EBITDAR$ 127,392k

Net IncomeR$ 56,033k

EBITDAR$ 211,772k

Net IncomeR$ 95,510k

EBITDA Margin20.8%

EBITDA Margin25.4%

Brand

Distribution

Development

Technology

9M10

Back-office

We celebrate two years of Datasul incorporation...

... with effective integration results.27

+28.9%

CAGR

+460 bp

+30.6%

CAGR

+16.8%

CAGR

R$ million 3Q10 3Q09 Δ Q/Q 9M10 9M09 Δ 9M/9M

Net Revenue 303.201 252.596 20.0% 833.751 721.253 15.6%

Gross Profit 211.183 173.340 21.8% 553.395 492.335 12.4%

EBITDA 88.186 66.450 32.7% 211.772 185.064 14.4%

EBITDA Margin 29.1% 26.3% 280 b.p. 25.4% 25.7% -30 b.p.

Adjusted Net Income 2 50.095 41.231 21.5% 134.527 116.820 15.2%

Financial Dashboard 1

Financial and Operational Performance

28

(1) Values are pro forma as they include the numbers of RM Sistemas, acquired in April 2006, and Datasul, consolidated in September 2008 in the period analyzed.

(2) Net income adjusted refers to net income excluding the effects of goodwill, amortization, net of tax. Hence, it can be understood as net income from the Company’s regular operations.

29

Fundamentals

TOTVS Success Equation...

...Based on strong fundamentals.

The material that follows is a presentation of general background information about TOTVS activities as of the date of the presentation

in November 2010.

It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to potential

investors.

This presentation may contain statements that express management’s expectations and/or forecasts about future events.

These expectations and/or forecasts involve risks and uncertainties that could cause actual results to differ materially from those

projected in such forward-looking statements. Therefore, the future results of the company may differ from current expectations and

readers must not base their expectations exclusively on the information presented herein.

No representation or warranty, express or implied, is made concerning, and no reliance should be placed on the accuracy, fairness, or completeness of the information presented herein.

This document does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase any securities.

Neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever.

Contacts

www.totvs.com/ir

QUESTIONS

Safe harbor

30