Embed Size (px)

Citation preview

Instructor Kurt Rosentreter,

CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM

www.facebook.com/kurtismycfo www.linkedin.com/in/kurtrosentreter @KurtRosentreter

The Financial Planning Process

The Various Segments of a Plan

Segments Addressed in this presentation: ◦ Goal planning

◦ Cash flow management

◦ Understanding insurance – life & disability

◦ Tax planning

◦ Estate planning

◦ Income tax planning

What is a “financial plan”? What is wealth management”? How do I differentiate between a financial

advisor, financial planner, portfolio manager, insurance agent or chief guru of money? ◦ What do their designations mean?

If I need a financial plan do I need to buy investment or insurance products?

How do I pay for financial advice or products?

1. Establish the client/planner engagement 2. Gather data and set goals/expectations 3. Develop financial strategies 4. Implement agreed upon financial solutions 5. Monitor effectiveness of solutions annually 6. Follow up and rebalancing strategies as

needed through life.

Facts Assumptions Client values and preferences

Present alternatives Discuss pros/cons of each Make recommendations Discuss resistance / acceptance Modify recommendation if necessary

A process related to addressing goals such as: •Retirement planning •Insurance needs analysis •Children’s savings •Estate planning •Debt strategies •Real estate •Tax planning

Comprehensiveness

Accuracy

Reasonableness / Attainability

Affordable

Timely

Balanced

Developed in partnership

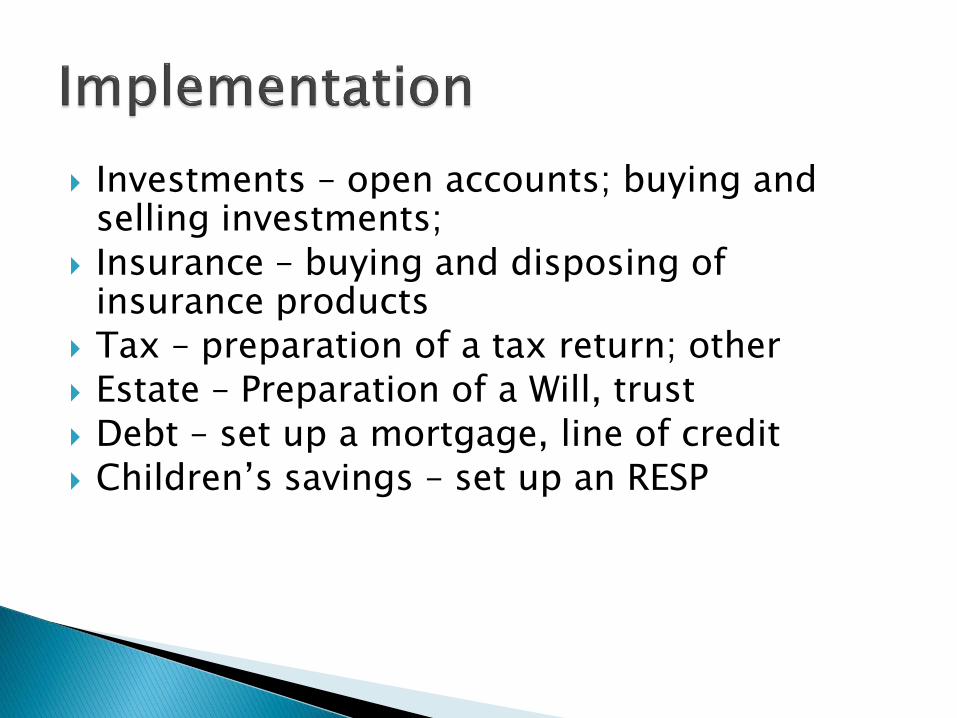

Investments – open accounts; buying and selling investments;

Insurance – buying and disposing of insurance products

Tax – preparation of a tax return; other Estate – Preparation of a Will, trust Debt – set up a mortgage, line of credit Children’s savings – set up an RESP

Key Points Planning vs. implementation Have a plan before you implement Set timing

Deadlines

Who does the implementation? Need for third party specialists

Is implementation paid for? Communication during implementation

Client knowledge, preferences, pace

Advisor limitations Documentation

Review progress ◦ Absolute (vs. goals) ◦ Relative Peers

Other

Frequency of Monitoring ◦ Depends on need Investments – regularly

Estate – every few years

Changes in personal circumstances

Changing tax and legal environments

Economic changes

Changes to Goals

Changes to timelines

Key: pro-action & communication

Transition of your approach to financial management: ◦ Areas of your finances

◦ Strategies (e.g. max RRSP)

◦ Solutions (e.g. prep your own T1)

◦ Products (mutual funds)

◦ Costs

◦ Advisors

◦ Attitude

Why? ◦ This is the point of the exercise ◦ Creates focus ◦ Deals with conflicts ◦ Creates accountability ◦ Provides a measuring stick ◦ Treats your personal finances like a business ◦ Greater likelihood of success

Define your Goals ◦ Write them down

◦ Each family member write down their own

Prioritize / tradeoffs

Time line to achieve

Desired, acceptance, not acceptable range

Measure progress against your goals ◦ Annually

Integrate your planning to consider all goals at once

Evolve your finances as your goals evolve

Good financial advisors track progress of your financial goals

No need to budget unless warning signs ◦ Creeping Debt

Categorize: core fixed, core variable, discretionary and luxury

Save for big ticket items: renos, gifts, vacations & vehicles

Watching timing issues – eg. Bonuses

Have a cushion built up – emergency fund

Know financial impact of major changes: maternity leave, job change, second property, etc.

Spending money involves financial tradeoffs to reach various goals:

1. Proper life & disability insurance

2. Pay off high cost debt

3. RESPs

4. RRSPs

5. TFSAs

6. Pay off low cost debt

7. Invest outside of registered accounts

8. Pay off tax deductible debt

Health and dental insurance

Life insurance

Disability insurance

Critical Illness insurance

Travel insurance

Safety Net Needs

Term Insurance, Disability Insurance, Critical Illness

Insurance, Long term care insurance, Travel insurance

Maximize Wealth Potential - Universal Life Insurance / IRP Net Worth Enhancement

- Term to 100 Insurance

- Corporate Owned Permanent Insurance

Inter-generational - Estate Tax Life Insurance

- Business Succession Life

Insurance

- Cottage Life Insurance

Start up

Career

Minimal

Wealth

Early Stage

Career

Wealth

Creation

Advanced

Career

Wealth

Management

Retired

Wealth

Preservation &

Transfer

Understanding who you are dealing with : ◦ Training

◦ Licensing

◦ E&O

◦ Independents vs. Dedicated

Relationship with insurance companies

◦ Commissions How it works

How it can vary but what you buy

◦ Philosophies – two key types

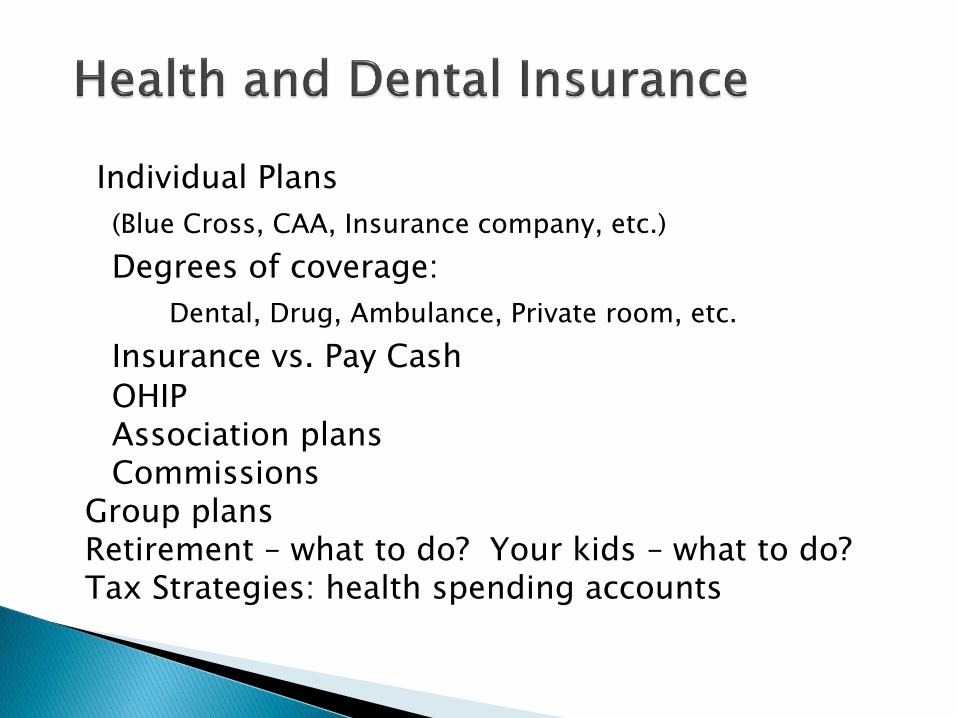

Individual Plans

(Blue Cross, CAA, Insurance company, etc.)

Degrees of coverage:

Dental, Drug, Ambulance, Private room, etc.

Insurance vs. Pay Cash

OHIP Association plans Commissions Group plans Retirement – what to do? Your kids – what to do? Tax Strategies: health spending accounts

Why do you need life insurance? ◦ Protect dependants

◦ Enhance estate values

◦ Create liquidity

The changing priority of insurance needs as you age: 30’s, 50’s, 70’s

Characteristics of Life Insurance

Policy owner, life insured, premium payer

Joint life (last to die, first to die)

Beneficiary designation

Policy reinstatement

Ratings

Life Insurance Needs

Amount ◦ Completing a Needs Analysis

Considerations

Group coverage

Mortgage insurance

Sale of Home

Family chipping in

Length of Period of Insurance Needs

Term Life Insurance

Features ◦ Renewable

◦ Convertible

◦ Premium frequency

◦ T10 vs. T20

◦ T100 vs. UL

◦ Private coverage vs. Employer group coverage

◦ Joint vs. individual life coverage

◦ AD&D

Permanent Life Insurance Features ◦ Universal Life vs. Whole Life ◦ Cash value ◦ Investment side fund & investing options ◦ Surrender charges ◦ Policy loans ◦ Non forfeiture options

Cash surrender value APL Extended term insurance Reduced paid up insurance

◦ Level cost

Planning Points ◦ Too little at 40 and too much at 55 ◦ Buying insurance within your master plan Buying rationally, not emotionally

◦ Dangers of employer group insurance ◦ Limitations of mortgage insurance ◦ Old policies ◦ Buying policies on children ◦ Buying policies in retirement ◦ Pricing of term vs. permanent coverage ◦ Understanding agent economics Term vs. Permanent commissions

Transferring old policies

Beware concept selling.

Definition ◦ Vs. critical illness insurance ◦ Vs. long term care insurance ◦ Vs. Worker’s Compensation Insurance ◦ Vs. CPP disability benefit

Occupation Classification Any occ, regular occ, own occ

Elimination period Two years or age 65 for benefit payment Benefit maximum Pre-tax and after-tax Guaranteed renewable Riders (e.g. inflation, return of premium)

Definition ◦ Vs. disability insurance

Purposes ◦ Pay for medical needs ◦ Continue existing quality of life

Characteristics ◦ Range of diseases covered ◦ Return of premium rider

If you budget only goes so far…

Typical Canadian: Credit card, web purchase for a week or two, employer

group plan coverage.

Challenges of this approach: Pre-existing conditions

Limited coverage

Rising cost

Alternatives Tailor made coverage; long term fixed purchase.

Freezing of Accounts

Wills and Probation

The Three Taxation Periods

Length of Time until Windup

Amount of work

– Selling real estate, closing accounts, paying bills, Will probate and tax returns, final wishes, contracts, disputes, legal liability

The role players:

– Executor

– Guardian

– Trustee

– External experts: lawyer and accountant

Do you have an up to date Will? Where are the Wills?

Do you have a copy?

Prepared by a lawyer?

Reviewed by a tax expert I hope?

No do-it-yourself Will

All of the kids or none of the kids as Executors ◦ Are trust companies a good idea? ◦ Pay Executors ◦ Joint Executors with back ups

Guardians should not be money trustees ◦ Story of Brother

Two Wills, maybe three

Are trust companies a good idea for Executor?

Don’t leave one asset to many people

Read the Will out loud to kids.

Spousal remarriage estate issues

Children’s inheritance clause – beware family home facts

Don’t create a great Will and mess it up with joint ownership, beneficiary designations and gifting.

Know What to Do Action Plan:

◦ Understand who the advisors are now; meet them all; evaluate them all; make sure passive spouse knows them; make sure they offer the right services; make sure they are the right age.

◦ Wind down a complicated net worth now.

◦ Have a plan for the non-financial assets.

What to Do with Key Assets In Your Estate What to do with various assets:

Family home

Cottage

Old life insurance policies

RRSPs and RRIFs

Pensions

Certificates in the safety deposit box

Action Plan: Have a plan before death.

How much income tax is due at death?

House

Cottage

Rental property

RRSPs or RRIFs

Cash, bonds and GICs

Equity Investments

Business

On first death versus second death

How to reduce this income tax at death? Joint ownerships (spouse and kids)

Designated beneficiaries

Gifting

Life insurance

Tax planning each year with taxable income levels (e.g rrif).

Charitable giving

How will costs be paid? Assets or life insurance

What are the other costs of an estate? Probate fees

Legal fees

Trustee fees

Executor fees

Accounting fees

Valuation fees

Real estate commissions

What is probate?

When is it necessary?

Probate Fee Planning and an Estate Joint ownership – pros/cons

Gifting – pros/cons

Second Will for assets without probate – pros/cons

Incorporation – pros/cons

Trust – pros/cons

Joint ownership of assets ◦ Bank accounts, real estate, investments

◦ Practical reasons to do it

◦ Tax issues

◦ Estate benefits and pitfalls

◦ Legal considerations

Gifting of assets ◦ Bank accounts, real estate, investments

◦ Practical reasons to do it

◦ Tax issues

◦ Estate benefits and pitfalls

◦ Legal considerations

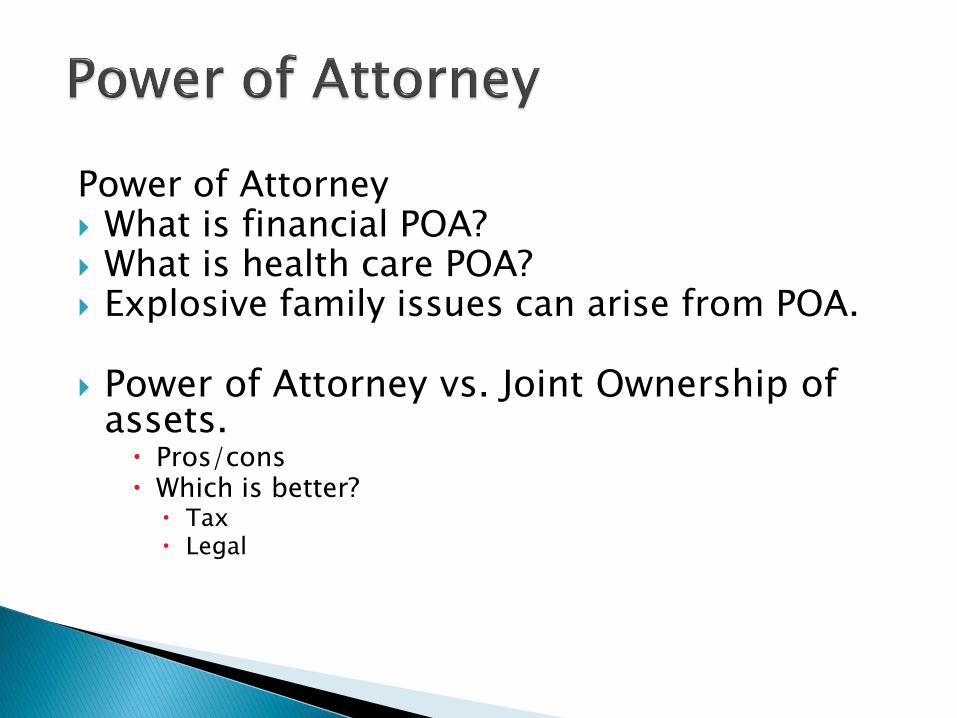

Power of Attorney What is financial POA? What is health care POA? Explosive family issues can arise from POA.

Power of Attorney vs. Joint Ownership of

assets. Pros/cons Which is better? Tax Legal

Methods ◦ Cash ◦ Appreciated Assets ◦ Annuity ◦ Life Insurance ◦ Foundation ◦ Donor Advised Funds

Before Death and at death

In-sync with rest of financial plan.

Tax Planning Tips Planning review vs. return preparation April vs. December Good debt vs. bad debt Equalizing net worth with spouse (PRL

strategy) Permanent life insurance as a tax shelter Asset based investment fees, not

commissions Self employed vs employee Tax smart investing

Use of corporations for the self employed Defer income tax

Income split

Access to the capital gains exemption

Salary vs. dividend options

Write off medical costs

Professional corporation vs. holding companies

Preserve OAS in retirement

Reduce costs on death to next generation.

Measuring Results

Judge your personal finances just like you are judged in your career.

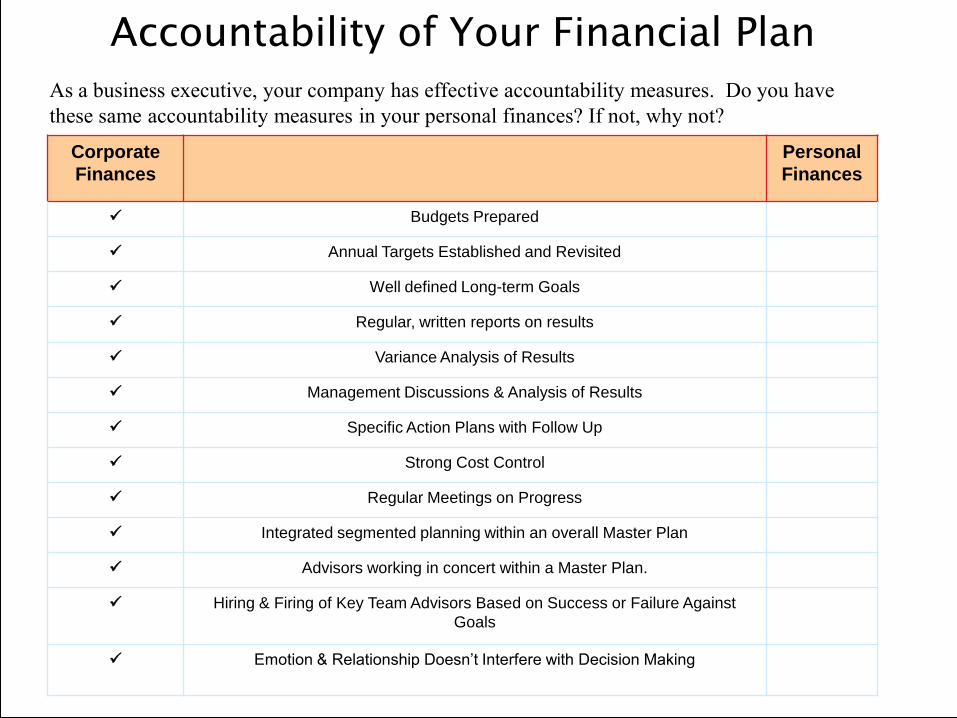

Accountability of Your Financial Plan

As a business executive, your company has effective accountability measures. Do you have

these same accountability measures in your personal finances? If not, why not?

Corporate

Finances

Personal

Finances

Budgets Prepared

Annual Targets Established and Revisited

Well defined Long-term Goals

Regular, written reports on results

Variance Analysis of Results

Management Discussions & Analysis of Results

Specific Action Plans with Follow Up

Strong Cost Control

Regular Meetings on Progress

Integrated segmented planning within an overall Master Plan

Advisors working in concert within a Master Plan.

Hiring & Firing of Key Team Advisors Based on Success or Failure Against

Goals

Emotion & Relationship Doesn’t Interfere with Decision Making

Think comprehensively about your money.

Demand value and service and expertise.

Evolve your strategies as you evolve.

Document everything.

Get second opinions.

Kurt Rosentreter, CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM

Senior Financial Advisor, Manulife Securities Incorporated

Certified Financial Planner, Manulife Securities Insurance Inc.

416.628.5761 Ext 230 [email protected] www.kurtismycfo.com

Follow Kurt on:

www.facebook.com/kurtismycfo

www.linkedin.com/in/kurtrosentreter

@KurtRosentreter

Next Session we will continue our integrated planning approach and cover: ◦ Managing debt

◦ Financial planning for children

◦ Real estate planning

◦ Retirement planning

◦ Investing

The opinions expressed are those of the author and may not necessarily reflect those of: Manulife Securities Incorporated or Manulife Securities Insurance Inc.

Manulife Securities Incorporated is a member of the Canadian Investor Protection Fund

CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM Chartered Professional Accountant association finance

instructor for the last ten years (Ontario, B.C., Manitoba). Twenty-five years of personal finance industry experience. Past co-founder of the $2 Billion Investment Counsel practice

at one of Canada’s Big Four CA Firms. National best selling author of seven personal finance books. Senior Financial Advisor, Manulife Securities Incorporated. Certified Financial Planner, Manulife Securities Insurance Inc. Instructor / Speaker to more than 500 audiences on matters

of personal finance. Regular commentator on money for CBC, CTV, Globe, Post,

Star, various radio and magazines. Regular contributor as an expert in the Financial Facelift

column for The Globe and Mail. www.KurtismyCFO.com

Instructor Kurt Rosentreter,

CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM

www.facebook.com/kurtismycfo www.linkedin.com/in/kurtrosentreter @KurtRosentreter

The Financial Planning Process

Segments addressed in this presentation: ◦ Risk Management

◦ Retirement planning

◦ Costs of raising children

◦ Real estate planning

◦ Personal investing strategies

1. Establish the client/planner engagement 2. Gather data and set goals/expectations 3. Develop financial strategies 4. Implement agreed upon financial solutions 5. Monitor effectiveness of solutions annually 6. Follow up and rebalancing strategies as

needed through life.

Examples of Major Financial Risks: Lawsuit against your career / business

Heart attack and unable to work

Divorce ◦ Child’s divorce

Car accident and liability

Company in trouble fast

Premature unemployment

Out of money at age 85

Exceptional stock market losses at age 55

Scenario analysis ◦ Net worth today; what must it be in X years? ◦ Estimate costs, investment returns, savings levels ◦ Don’t forget about car purchases, vacations, child costs,

healthcare, end of life care.

Annual re-visitation of progress / results Most folks under-estimate what is needed Goals should not be how to fit your lifestyle into your pension Key: don’t head blindly into retirement

Resources: ◦ Government benefits ◦ Investments RRSP Other

◦ Small business ◦ Real estate ◦ Your spouse’s assets and incomes

Expenses: ◦ “normalize” your previous year’s expenses to get an

estimate of future costs ◦ Fixed costs, variable costs, discretionary costs, occasional

costs.

Few people fully retire under 60 anymore

More people starting businesses or working part time to age 65-70.

WHY? Cost of living is higher

Cost of specific healthcare is higher

Living longer requires more money

Sandwich generation situation

You should have no debt (usually by 55) You should not plan to buy more expensive

real estate to live in You should not still be funding your

children’s expenses You should not be an aggressive stock

market investor with your savings. You should know if you can afford to retire,

and what it will cost to live in 30 years.

You should not start giving large lumps of money to the kids

You should not rush to put the real estate as jointly owned with the kids

You should monitor your spending levels within your income potential.

You should examine worst case scenarios with investment returns.

How Your Retirement Is Affected By Real Estate Decisions

Timing to buy your first home

◦ Dangers of money gifts from parents

◦ Use of the HBP

Mortgage type and payments

Extra money: pay mortgage vs. pay RRSP vs. fun stuff

Renovations and bigger homes

Second properties – affordability

Real estate downsizing

Prioritizing real estate in your master plan.

How Your Retirement is Affected By Those You Love

Cost of having children Private school

Post secondary ($40,000 per child per Bachelor degree.)

How many children?

Financial assistance to elderly parents What will it cost?

Siblings of different economic means

16

Private school

Post secondary education

Weddings

Cars

New home purchases

Other

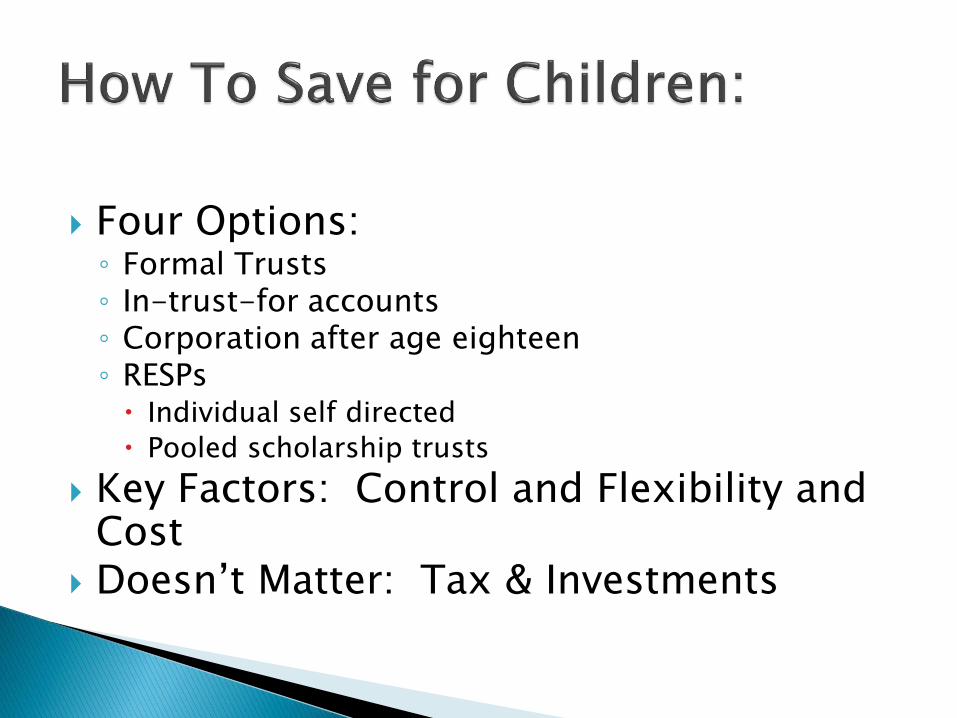

Four Options: ◦ Formal Trusts ◦ In-trust-for accounts ◦ Corporation after age eighteen ◦ RESPs Individual self directed

Pooled scholarship trusts

Key Factors: Control and Flexibility and Cost

Doesn’t Matter: Tax & Investments

Contribution limit of $50,000 per child ◦ Most parents put in max of $2,500

Level that $500 CESG grant is maximized

Key Points About RESPs: ◦ Can catch up missed years and grant money

◦ Grandparents should not own the plan

◦ Beware time limit

◦ Money in ITF accounts can move to RESP.

Buying your first home – the largest purchase of your life Balance financial and personal goals

Financial: wait until deposit is larger Financial: Better to avoid the Home Buyer’s Plan Financial: Repay the HBP in 5 not 15 Financial: Risk of buying a condo as a stepping stone

Owning a home first, and then getting married Beware different divorce results for common law

Wedding gifts from parents to help with home ownership – avoiding pitfalls

Weekly mortgage payments are best. Buying vs. renting

Biggest problem for 60 year olds today How much real estate is too much? Mortgage free by what age? Will you downsize?

For sure?

How much will you free up?

Can you handle condo maintenance fees?

Reverse mortgages The cottage The commercial property Buying versus renting in old age

1. Have a financial plan first Investing should flow from your broader plan.

Focus on goals

Set targets, savings levels, return expectations

Run from any advisor who doesn’t get this.

2. Limit your stock market exposure Convince me why you need any?

Less with age

Less in the “new” stock market

Less if you don’t understand

Why advisors may be biased to the stock market

3. Stick with high quality securities A. Fixed income: GIC’s and government bonds

B. Equity: Blue chip stocks, ETF’s, no load funds

C. Avoid: labour funds, tax shelters, small cap stocks, most mutual funds, IPO’s, wrap programs.

4. Rebalancing twice a year A. Sell growth / keep core positions

B. Rebalance back to original plan

C. Rebalance for stage of life

5. Do it Yourself or Hire an Honest Advisor Can you be a do-it-yourselfer?

Time commitment / personal interest

Honest advisor:

Four documents: proposal letter, financial plan, Investment Policy Statement, annual results letter

Education

Disclosure

Fee based is the best way to go for equities, commission based for bonds

Don’t blindly trust the way you trust an MD.

6. Stay on top of results A. Have advisors demonstrate what they will do to

monitor results (qual and quant)

B. Understand their investing philosophy – do you agree?

C. Semi-annual face to face meeting

D. Compare results against indexes and peers – give 3 to 5 years before replacing underperformance

E. Know impact of fees and taxes – two main drags on performance.

Think comprehensively about your money.

Demand value and service and expertise.

Evolve your strategies as you evolve.

Document everything.

Get second opinions.

Kurt Rosentreter, CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM

Senior Financial Advisor, Manulife Securities Incorporated

Certified Financial Planner, Manulife Securities Insurance Inc.

416.628.5761 Ext 230 [email protected] www.kurtismycfo.com

Follow Kurt on:

www.facebook.com/kurtismycfo

www.linkedin.com/in/kurtrosentreter

@KurtRosentreter

The opinions expressed are those of the author and may not necessarily reflect those of: Manulife Securities Incorporated or Manulife Securities Insurance Inc. Manulife Securities Incorporated is a member of the Canadian Investor Protection Fund

CPA, CA, CFP, CLU, TEP, FMA, CIMA, FCSI, CIM Chartered Professional Accountant association finance

instructor for the last ten years (Ontario, B.C., Manitoba). Twenty-five years of personal finance industry experience. Past co-founder of the $2 Billion Investment Counsel practice

at one of Canada’s Big Four CA Firms. National best selling author of seven personal finance books. Senior Financial Advisor, Manulife Securities Incorporated. Certified Financial Planner, Manulife Securities Insurance Inc. Instructor / Speaker to more than 500 audiences on matters

of personal finance. Regular commentator on money for CBC, CTV, Globe, Post,

Star, various radio and magazines. Regular contributor as an expert in the Financial Facelift

column for The Globe and Mail. www.KurtismyCFO.com