Embed Size (px)

Citation preview

Insurance Regulation and Supervision

For bank Supervisors

17 October 2012

Su Hoong Chang

Agenda

Global Perspective & Financial Stability

Raising the (Regulatory) Bar

Cross-sectoral risk transfers &

Emerging Trends

2

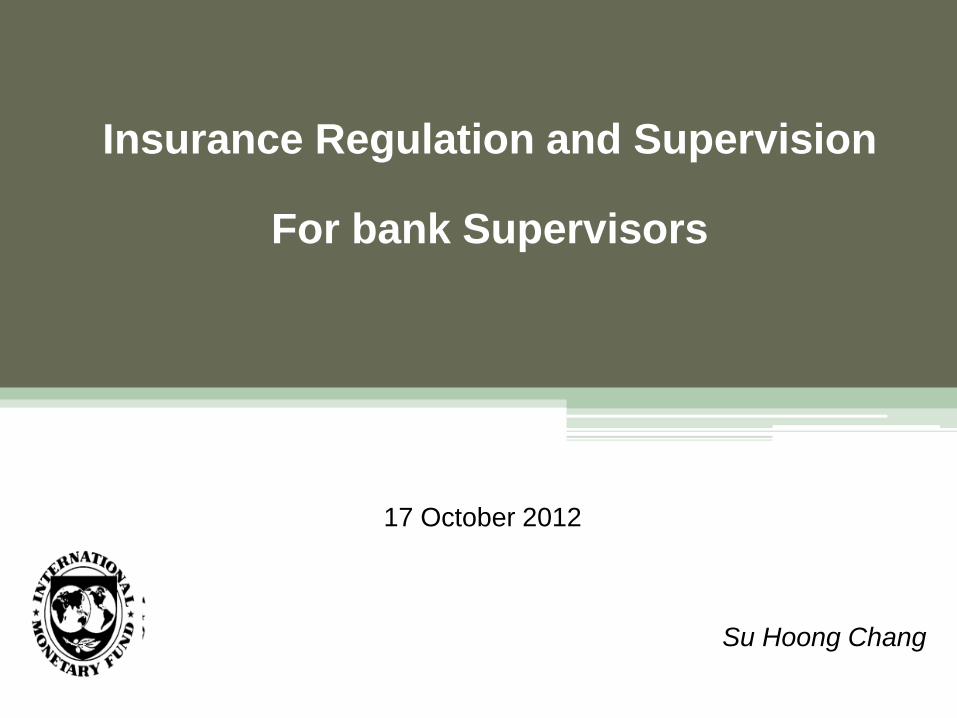

Global Insurance Market - 2011

3

Premiums

in US$ billions

Insurance density

Premiums per capita

in US$

Insurance

penetration

As % of GDP

Premiums Life General Life General

Advanced

Markets

3,897

(85%)

2,168 1,544 5.01 3.57

Emerging

Markets

700

(15%)

62 56 1.42 1.30

Source: Swiss Re - World Insurance Market in 2011, Sigma 3/2012

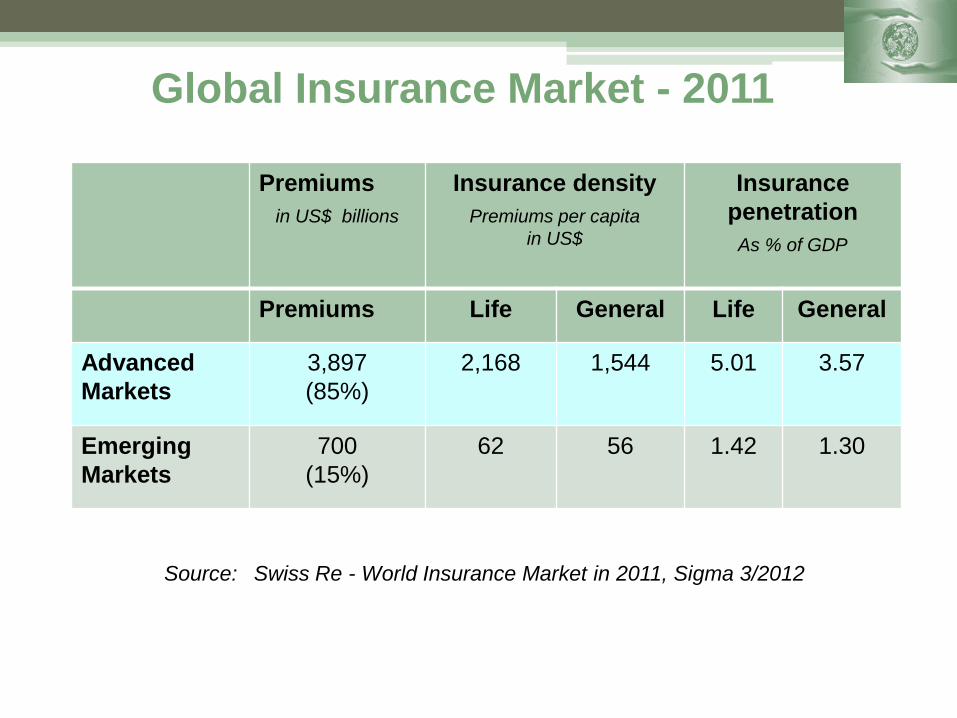

Insurance and Financial Stability

4

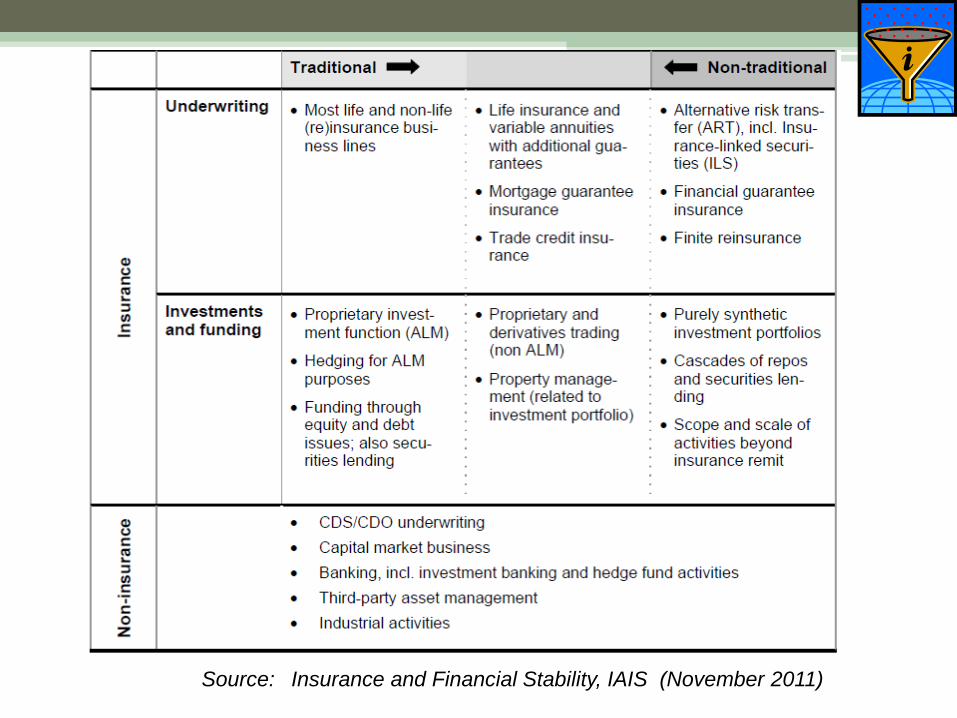

“Total insurance assets represent approximately one third

of the banking industry’s assets” (Next slide)

“The 25 largest insurers in the world combine US$10.7

trillion in total assets”.

“The reinsurance sector is smaller” – total assets of 10 largest

reinsurers < the top primary insurer

“Insurers engaged in traditional insurance activities were

largely not a concern from a systemic risk perspective”

However, NTNI activities may amplify or contribute to

systemic risks

The systemic impact of insurers is “ultimately an empirical

issue”

Source: Insurance and Financial Stability, IAIS (November 2011)

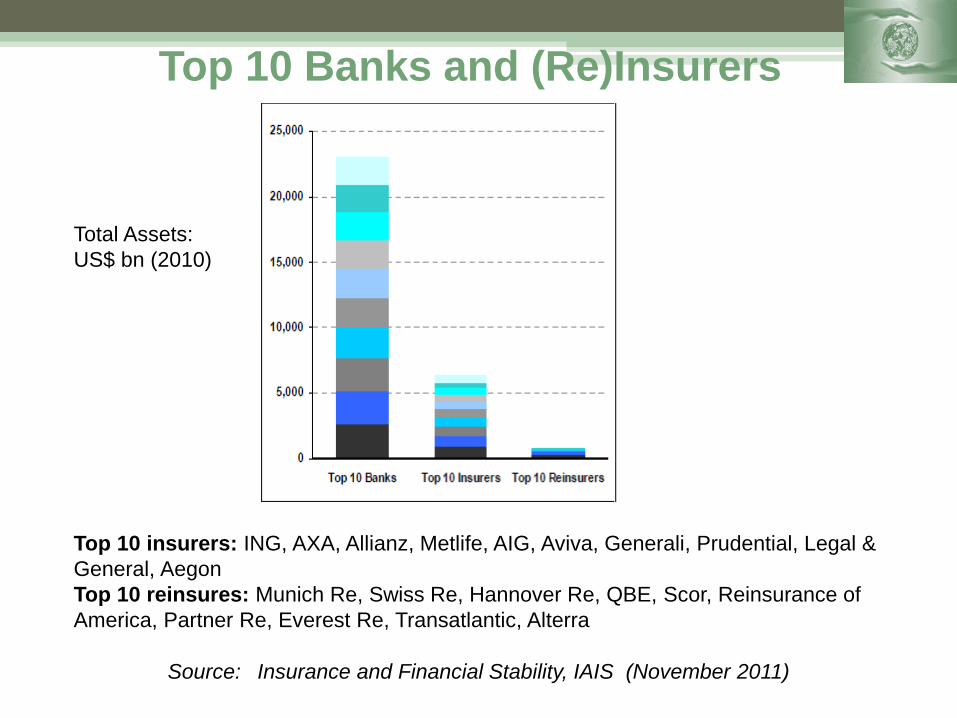

Top 10 Banks and (Re)Insurers

5 Source: Insurance and Financial Stability, IAIS (November 2011)

Top 10 insurers: ING, AXA, Allianz, Metlife, AIG, Aviva, Generali, Prudential, Legal &

General, Aegon

Top 10 reinsures: Munich Re, Swiss Re, Hannover Re, QBE, Scor, Reinsurance of

America, Partner Re, Everest Re, Transatlantic, Alterra

Total Assets:

US$ bn (2010)

6

Source: Insurance and Financial Stabilty, IAIS (November 2011)

Source: Insurance and Financial Stability, IAIS (November 2011)

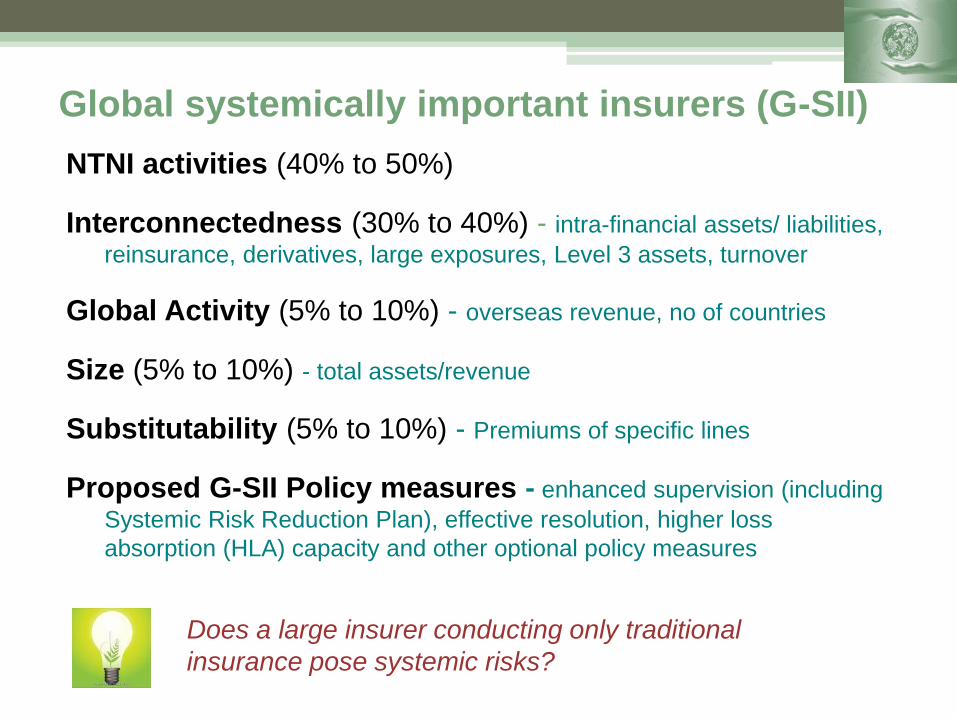

Global systemically important insurers (G-SII)

NTNI activities (40% to 50%)

Interconnectedness (30% to 40%) - intra-financial assets/ liabilities,

reinsurance, derivatives, large exposures, Level 3 assets, turnover

Global Activity (5% to 10%) - overseas revenue, no of countries

Size (5% to 10%) - total assets/revenue

Substitutability (5% to 10%) - Premiums of specific lines

Proposed G-SII Policy measures - enhanced supervision (including

Systemic Risk Reduction Plan), effective resolution, higher loss

absorption (HLA) capacity and other optional policy measures

7

Does a large insurer conducting only traditional

insurance pose systemic risks?

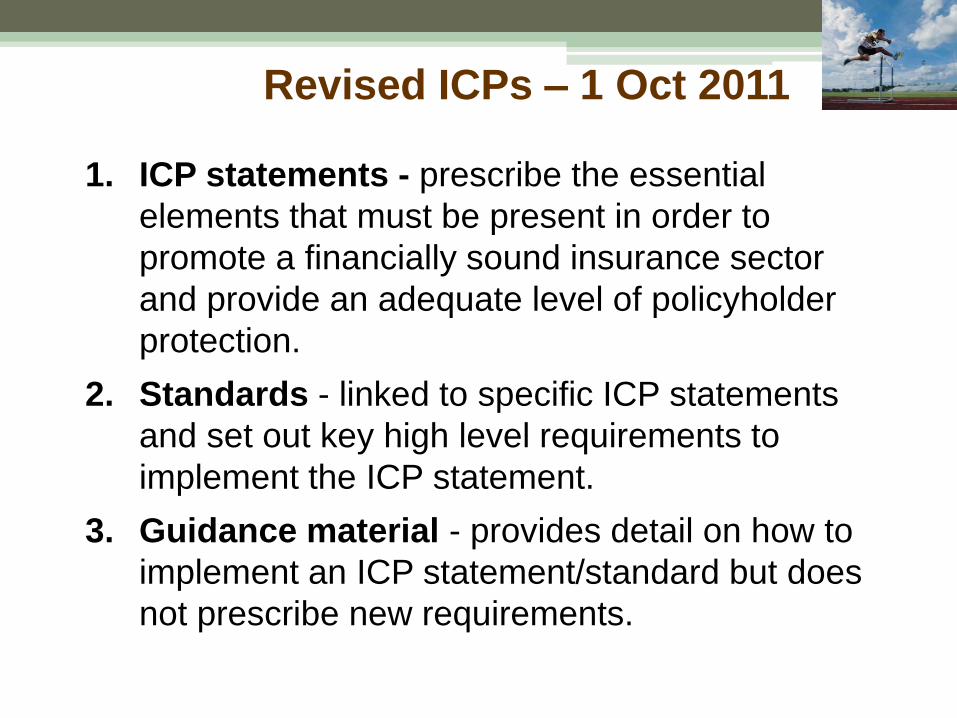

Revised ICPs – 1 Oct 2011

1. ICP statements - prescribe the essential

elements that must be present in order to

promote a financially sound insurance sector

and provide an adequate level of policyholder

protection.

2. Standards - linked to specific ICP statements

and set out key high level requirements to

implement the ICP statement.

3. Guidance material - provides detail on how to

implement an ICP statement/standard but does

not prescribe new requirements.

8

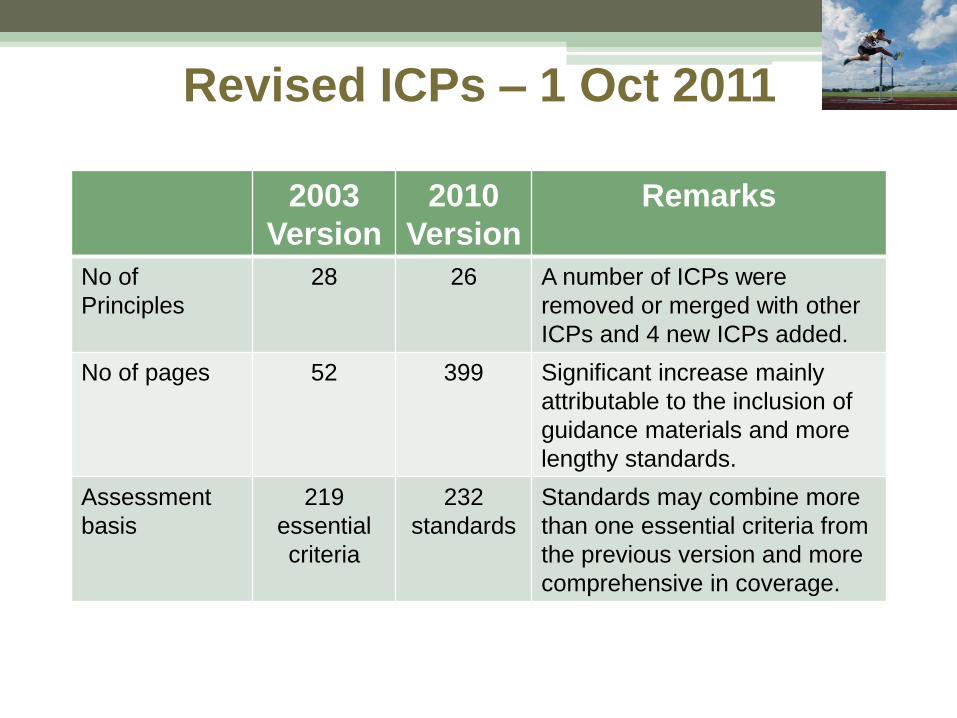

Revised ICPs – 1 Oct 2011

9

2003

Version

2010

Version

Remarks

No of

Principles

28 26 A number of ICPs were

removed or merged with other

ICPs and 4 new ICPs added.

No of pages 52 399 Significant increase mainly

attributable to the inclusion of

guidance materials and more

lengthy standards.

Assessment

basis

219

essential

criteria

232

standards

Standards may combine more

than one essential criteria from

the previous version and more

comprehensive in coverage.

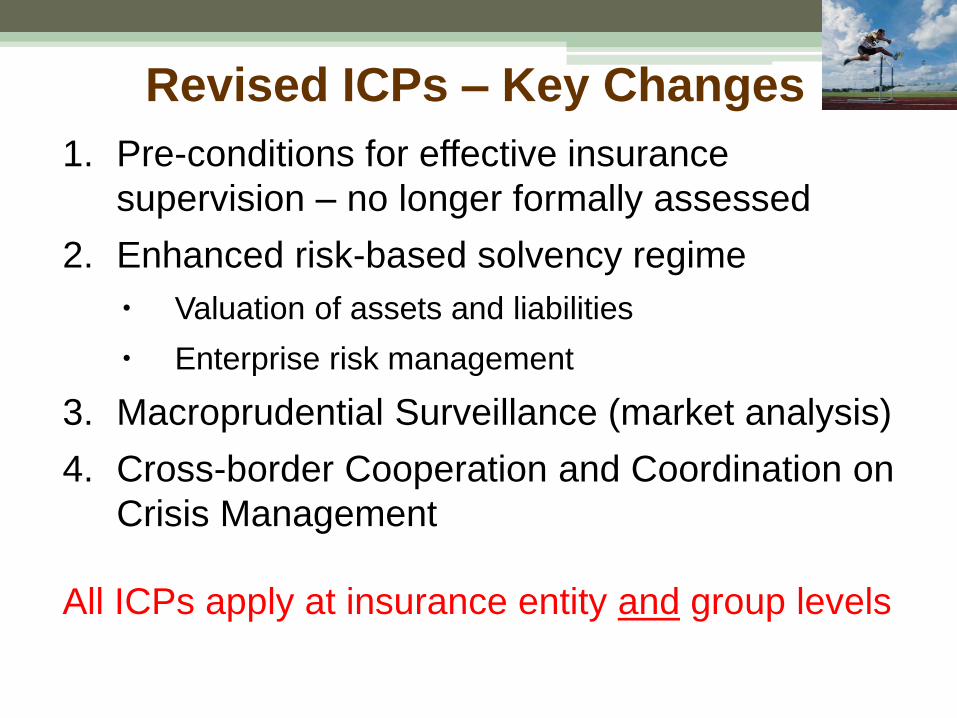

Revised ICPs – Key Changes

1. Pre-conditions for effective insurance

supervision – no longer formally assessed

2. Enhanced risk-based solvency regime

Valuation of assets and liabilities

Enterprise risk management

3. Macroprudential Surveillance (market analysis)

4. Cross-border Cooperation and Coordination on

Crisis Management

All ICPs apply at insurance entity and group levels

10

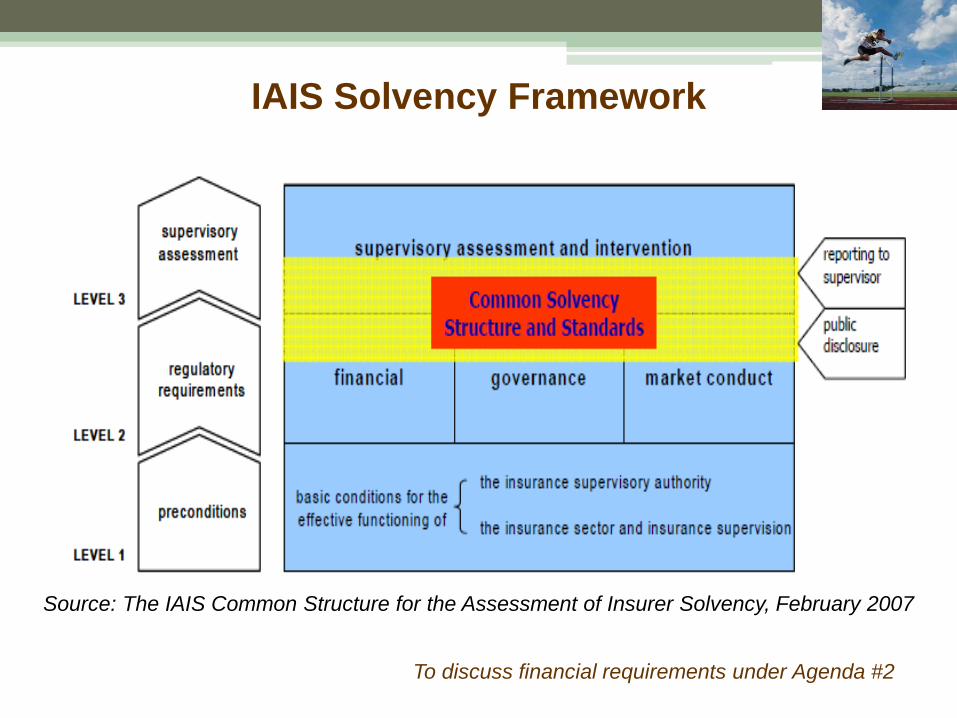

IAIS Solvency Framework

11

Source: The IAIS Common Structure for the Assessment of Insurer Solvency, February 2007

To discuss financial requirements under Agenda #2

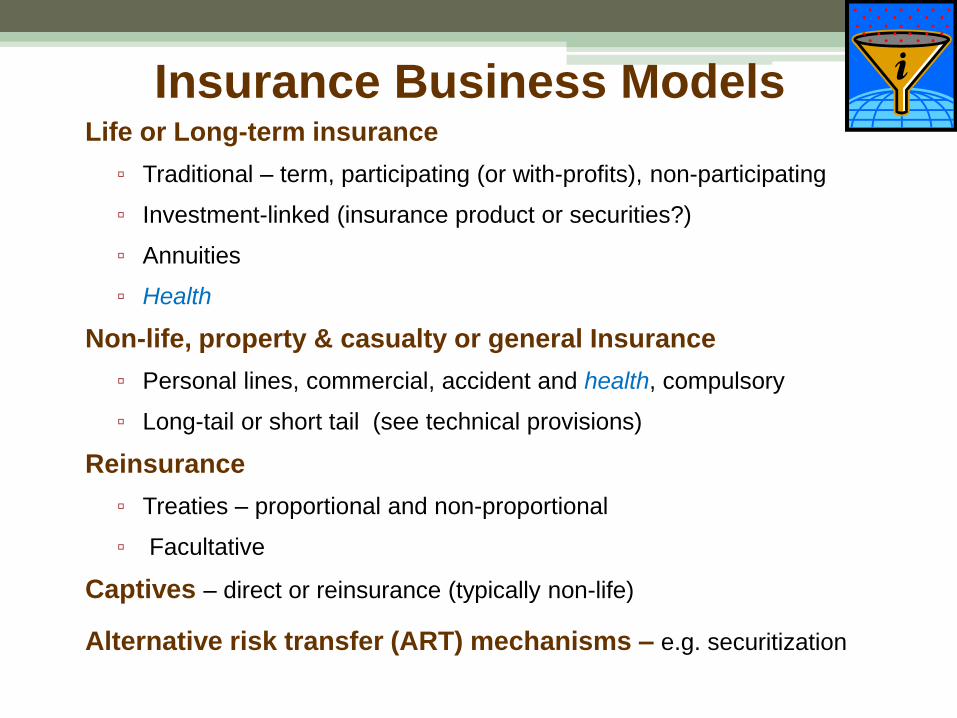

Insurance Business Models Life or Long-term insurance

▫ Traditional – term, participating (or with-profits), non-participating

▫ Investment-linked (insurance product or securities?)

▫ Annuities

▫ Health

Non-life, property & casualty or general Insurance

▫ Personal lines, commercial, accident and health, compulsory

▫ Long-tail or short tail (see technical provisions)

Reinsurance

▫ Treaties – proportional and non-proportional

▫ Facultative

Captives – direct or reinsurance (typically non-life)

Alternative risk transfer (ART) mechanisms – e.g. securitization

12

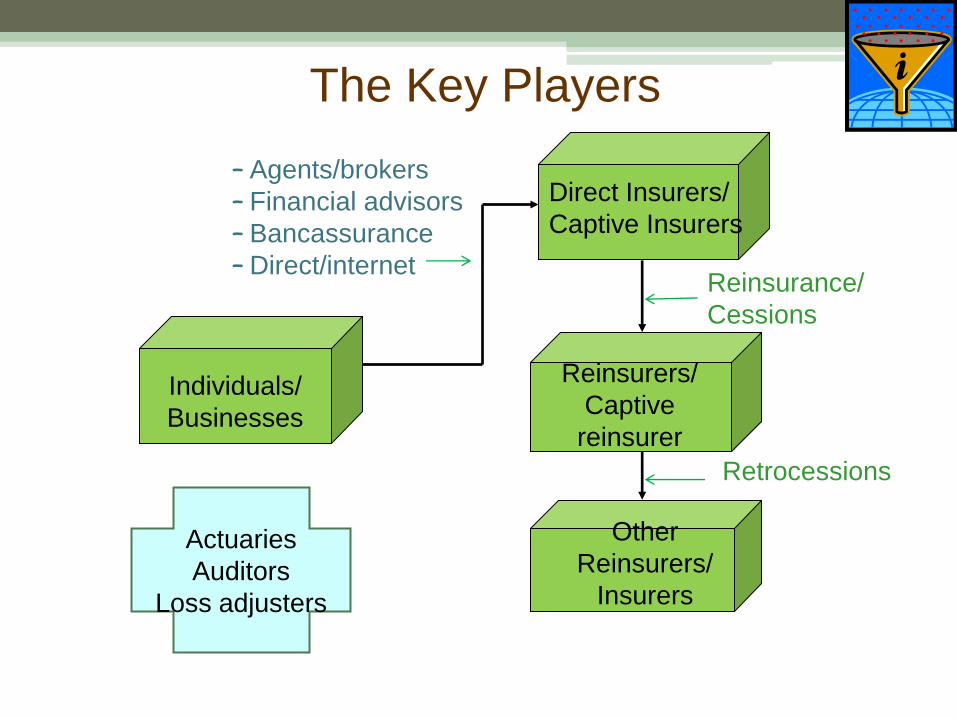

The Key Players

– Agents/brokers

– Financial advisors

– Bancassurance

– Direct/internet

Retrocessions

Individuals/

Businesses

Direct Insurers/

Captive Insurers

Reinsurers/

Captive

reinsurer

Other

Reinsurers/

Insurers

Reinsurance/

Cessions

Actuaries

Auditors

Loss adjusters

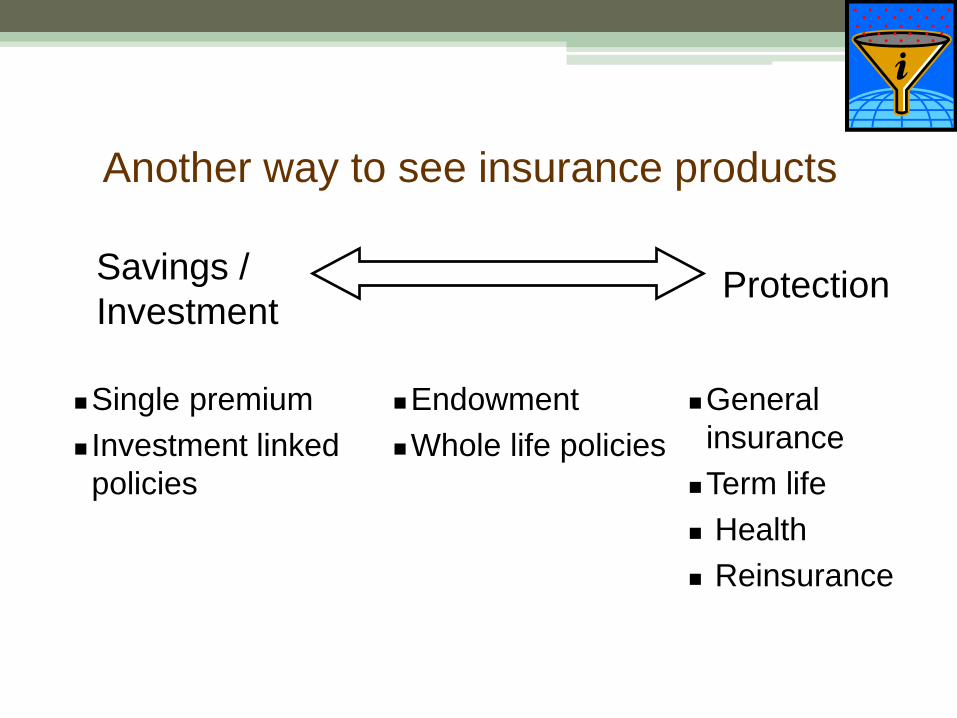

Another way to see insurance products

14

Savings /

Investment Protection

Single premium

Investment linked

policies

Endowment

Whole life policies

General

insurance

Term life

Health

Reinsurance

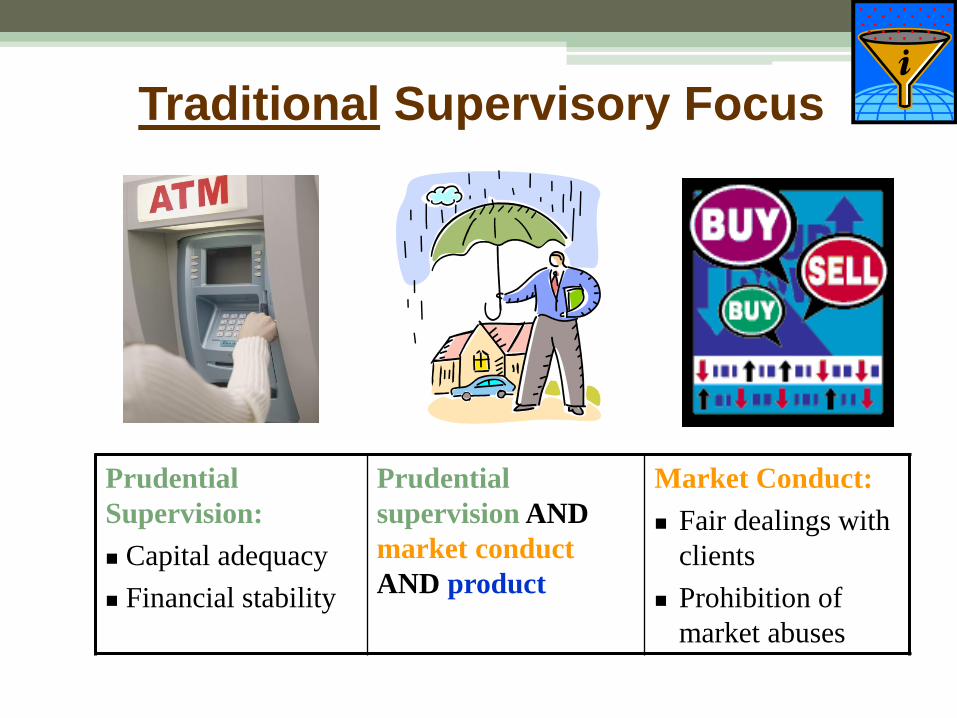

Traditional Supervisory Focus

15

Prudential

Supervision:

Capital adequacy

Financial stability

Prudential

supervision AND

market conduct

AND product

Market Conduct:

Fair dealings with

clients

Prohibition of

market abuses

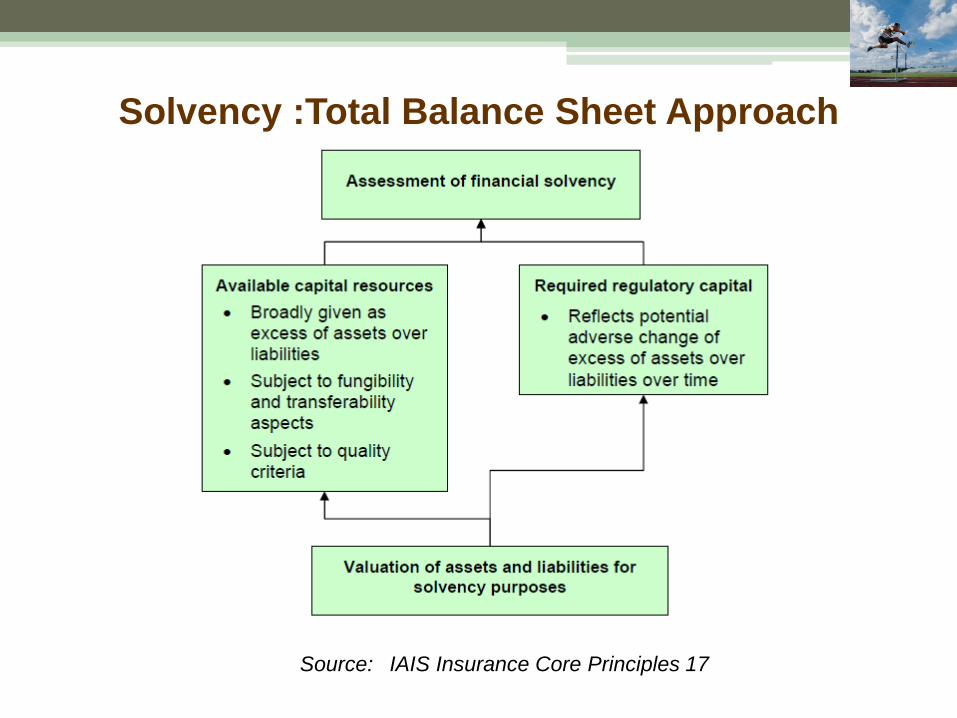

Solvency :Total Balance Sheet Approach

16 Source: IAIS Insurance Core Principles 17

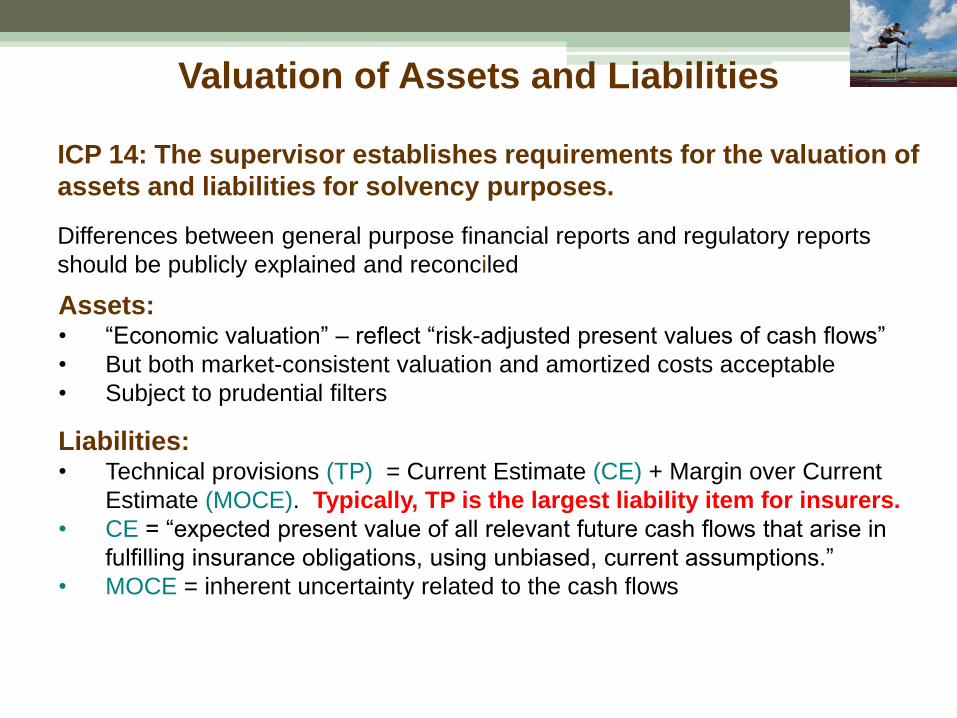

Valuation of Assets and Liabilities

ICP 14: The supervisor establishes requirements for the valuation of

assets and liabilities for solvency purposes.

17

Differences between general purpose financial reports and regulatory reports

should be publicly explained and reconciled

Assets: • “Economic valuation” – reflect “risk-adjusted present values of cash flows”

• But both market-consistent valuation and amortized costs acceptable

• Subject to prudential filters

Liabilities: • Technical provisions (TP) = Current Estimate (CE) + Margin over Current

Estimate (MOCE). Typically, TP is the largest liability item for insurers.

• CE = “expected present value of all relevant future cash flows that arise in

fulfilling insurance obligations, using unbiased, current assumptions.”

• MOCE = inherent uncertainty related to the cash flows

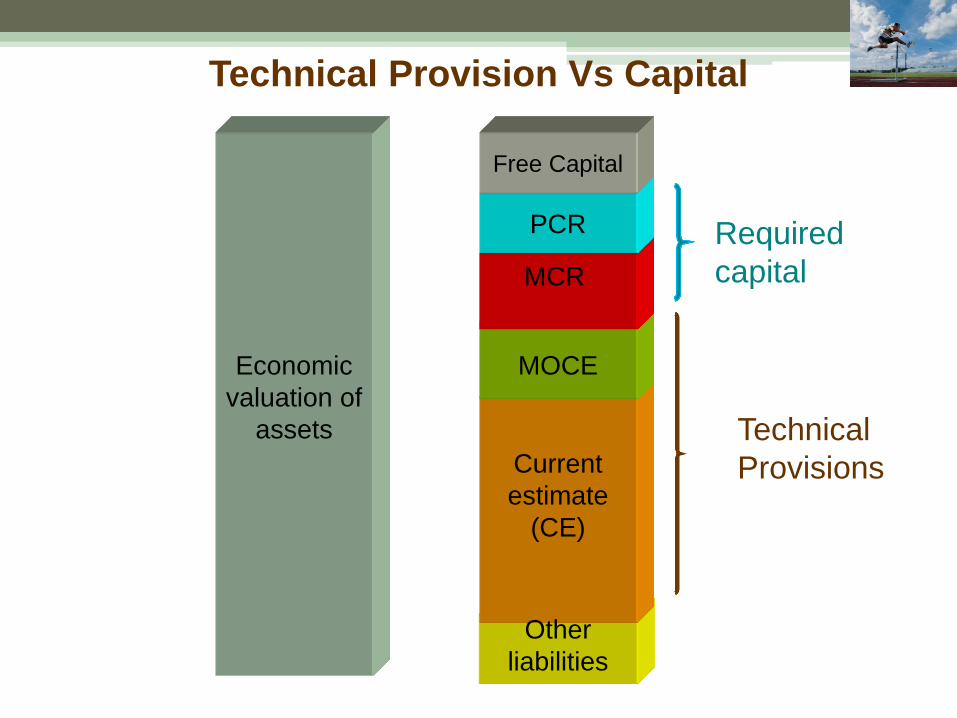

Technical Provision Vs Capital

18

Current

estimate

(CE)

MOCE

MCR

PCR

Technical

Provisions

Required

capital

Other

liabilities

Free Capital

Economic

valuation of

assets

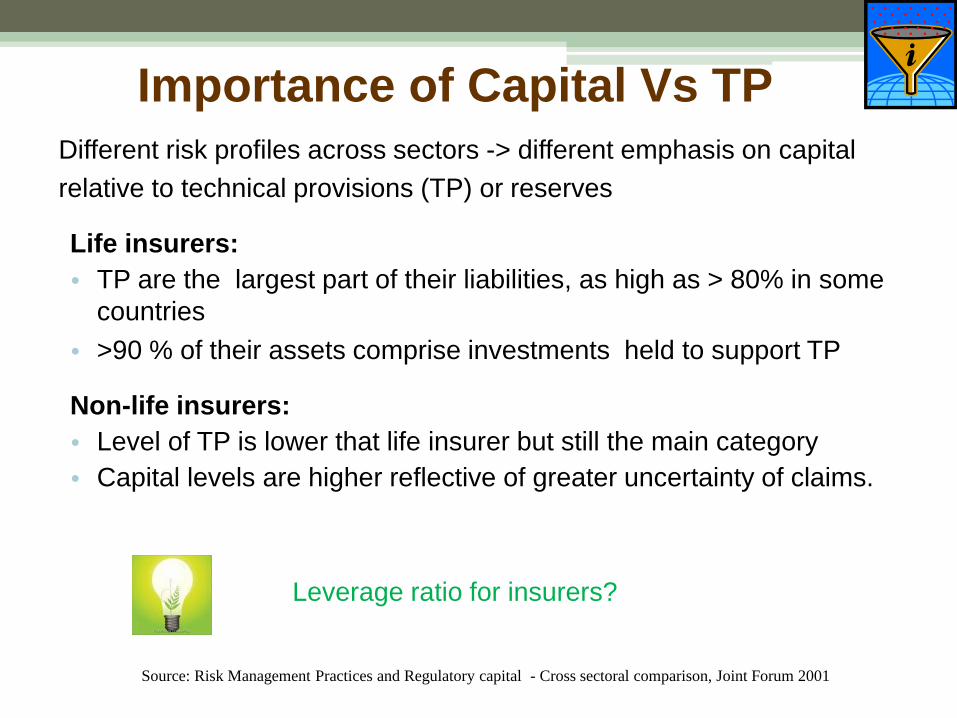

Importance of Capital Vs TP

Different risk profiles across sectors -> different emphasis on capital

relative to technical provisions (TP) or reserves

Life insurers:

• TP are the largest part of their liabilities, as high as > 80% in some

countries

• >90 % of their assets comprise investments held to support TP

Non-life insurers:

• Level of TP is lower that life insurer but still the main category

• Capital levels are higher reflective of greater uncertainty of claims.

19 Source: Risk Management Practices and Regulatory capital - Cross sectoral comparison, Joint Forum 2001

Leverage ratio for insurers?

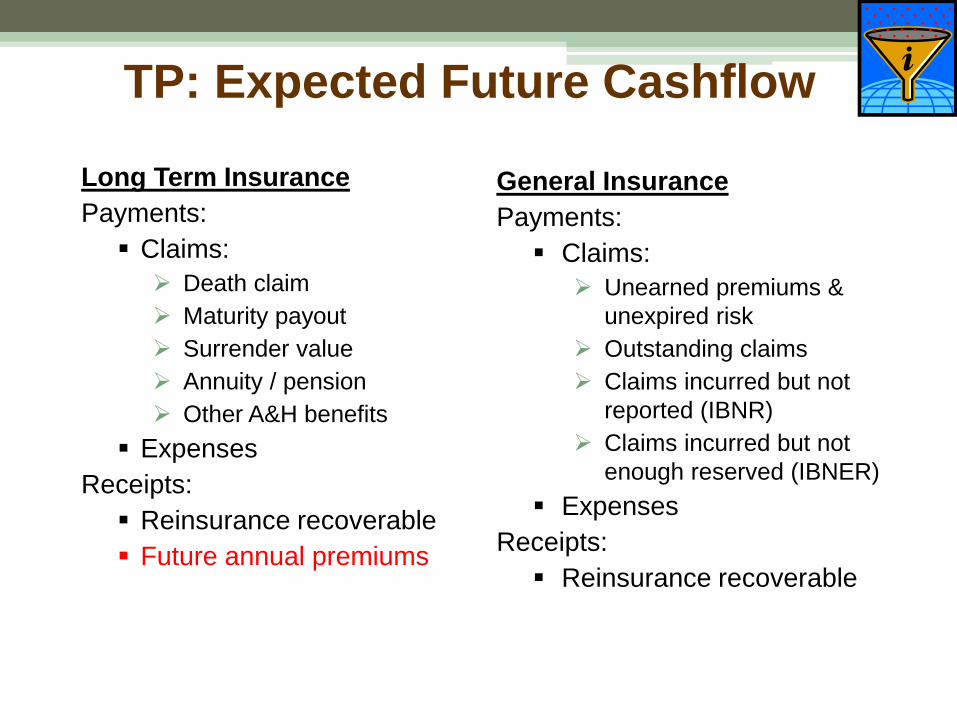

TP: Expected Future Cashflow

20

Long Term Insurance

Payments:

Claims:

Death claim

Maturity payout

Surrender value

Annuity / pension

Other A&H benefits

Expenses

Receipts:

Reinsurance recoverable

Future annual premiums

General Insurance

Payments:

Claims:

Unearned premiums &

unexpired risk

Outstanding claims

Claims incurred but not

reported (IBNR)

Claims incurred but not

enough reserved (IBNER)

Expenses

Receipts:

Reinsurance recoverable

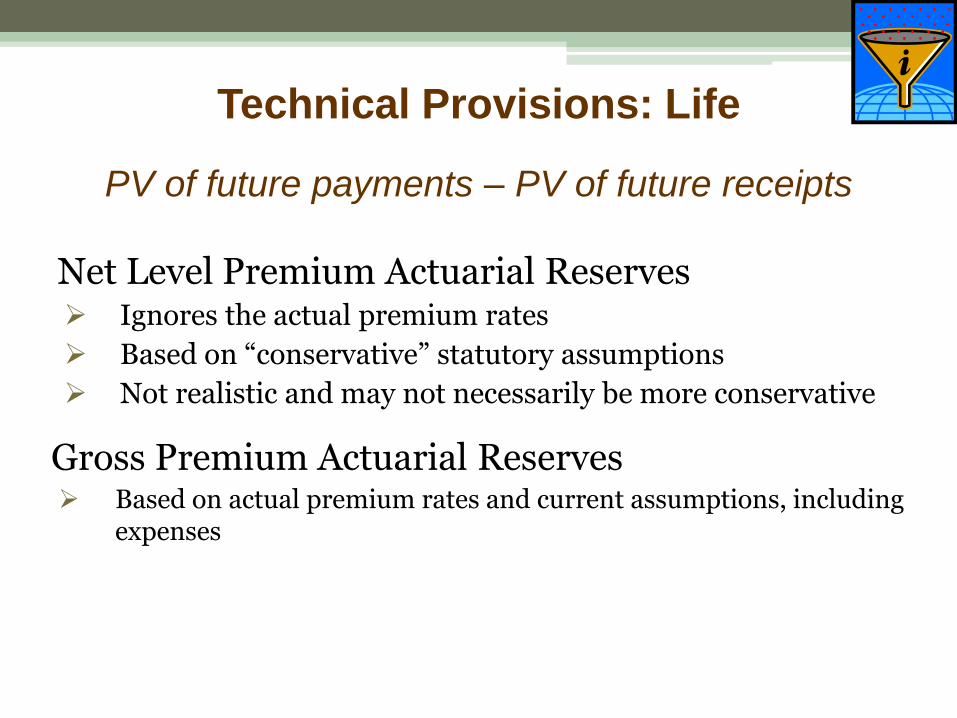

Technical Provisions: Life

Net Level Premium Actuarial Reserves Ignores the actual premium rates

Based on “conservative” statutory assumptions

Not realistic and may not necessarily be more conservative

Gross Premium Actuarial Reserves Based on actual premium rates and current assumptions, including

expenses

21

PV of future payments – PV of future receipts

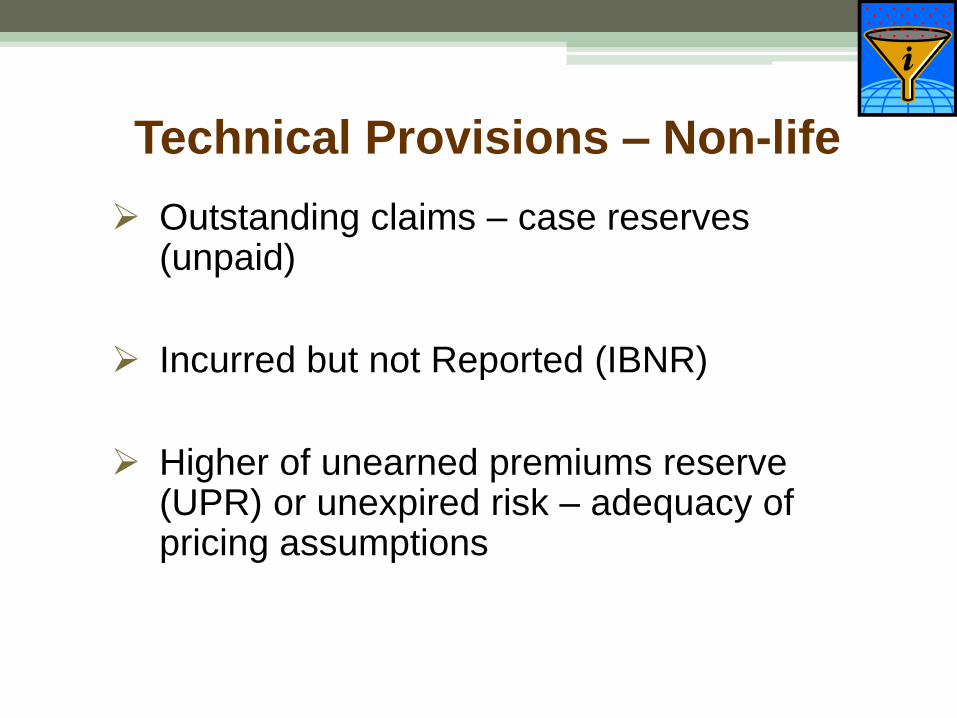

Technical Provisions – Non-life

Outstanding claims – case reserves (unpaid)

Incurred but not Reported (IBNR)

Higher of unearned premiums reserve (UPR) or unexpired risk – adequacy of pricing assumptions

22

23

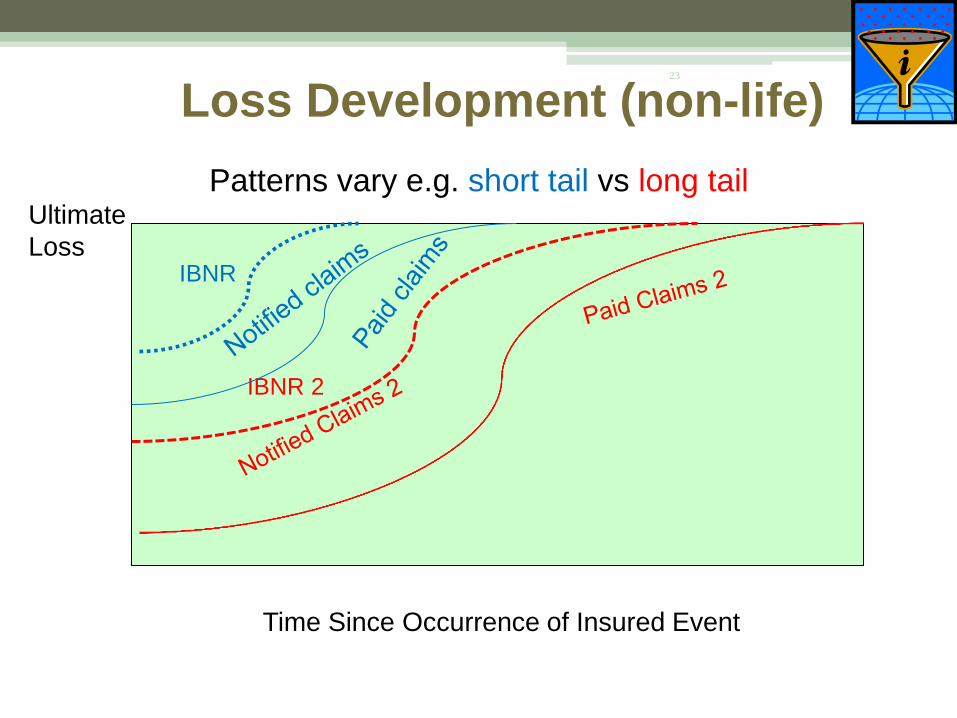

Loss Development (non-life)

Time Since Occurrence of Insured Event

Ultimate

Loss

IBNR 2

Patterns vary e.g. short tail vs long tail

IBNR

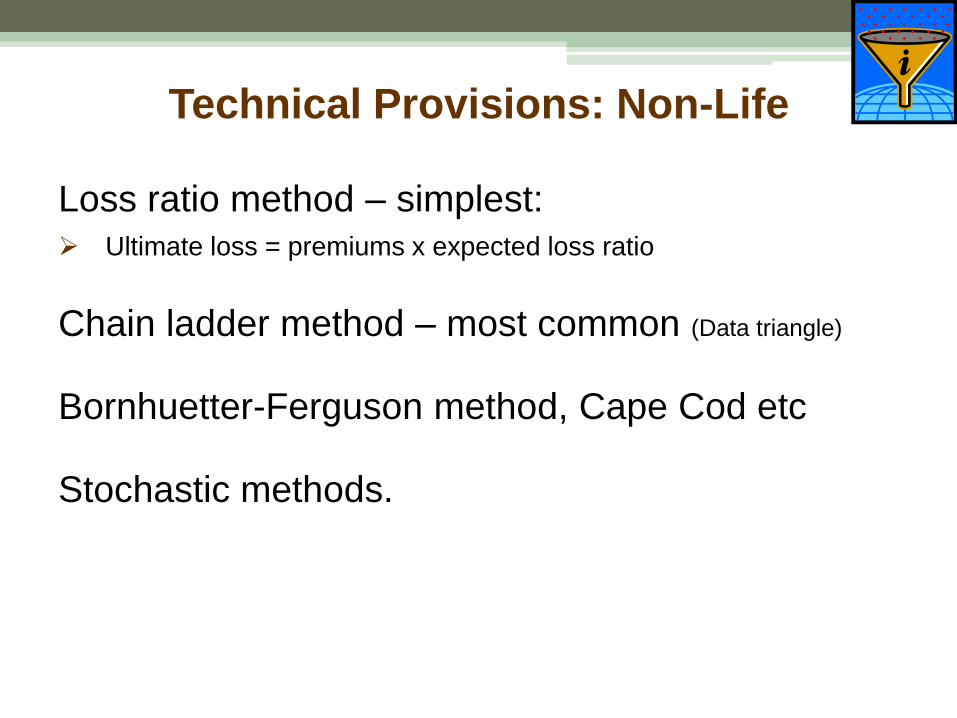

Technical Provisions: Non-Life

24

Loss ratio method – simplest:

Ultimate loss = premiums x expected loss ratio

Chain ladder method – most common (Data triangle)

Bornhuetter-Ferguson method, Cape Cod etc

Stochastic methods.

25

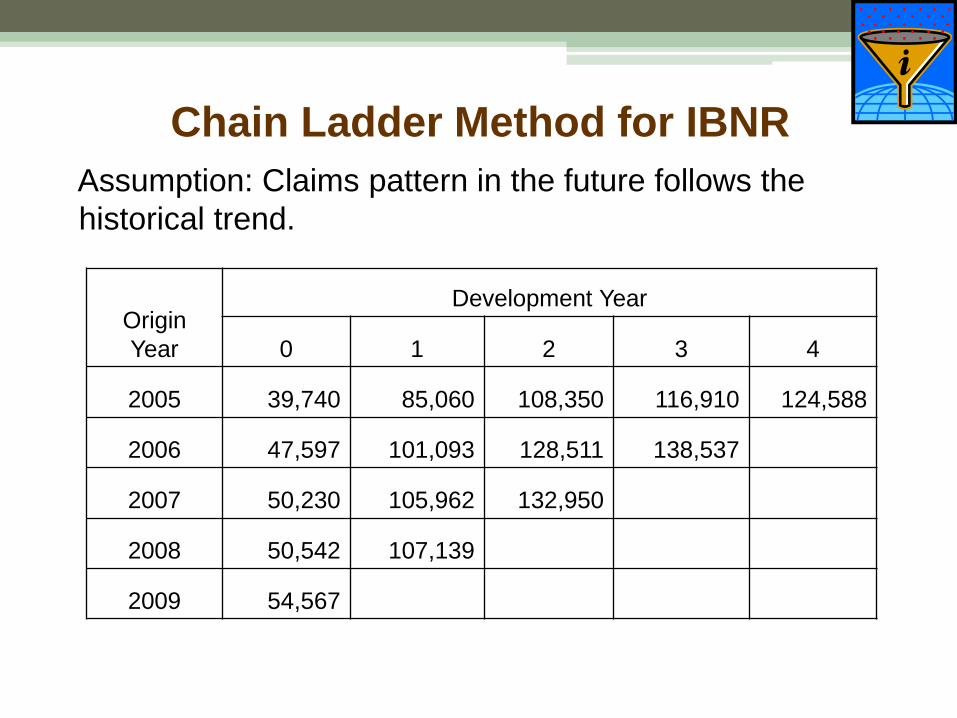

Assumption: Claims pattern in the future follows the

historical trend.

Origin

Year

Development Year

0 1 2 3 4

2005 39,740 85,060 108,350 116,910 124,588

2006 47,597 101,093 128,511 138,537

2007 50,230 105,962 132,950

2008 50,542 107,139

2009 54,567

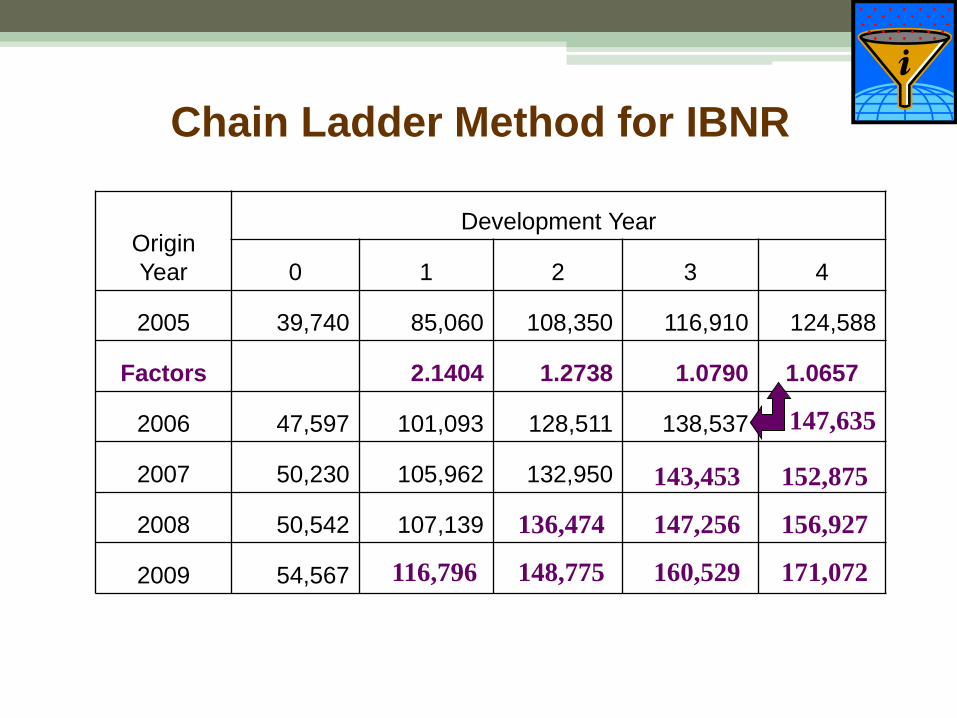

Chain Ladder Method for IBNR

26

Chain Ladder Method for IBNR

Origin

Year

Development Year

0 1 2 3 4

2005 39,740 85,060 108,350 116,910 124,588

Factors 2.1404 1.2738 1.0790 1.0657

2006 47,597 101,093 128,511 138,537

2007 50,230 105,962 132,950

2008 50,542 107,139

2009 54,567 116,796

136,474

148,775

143,453

147,256

160,529

152,875

156,927

171,072

147,635

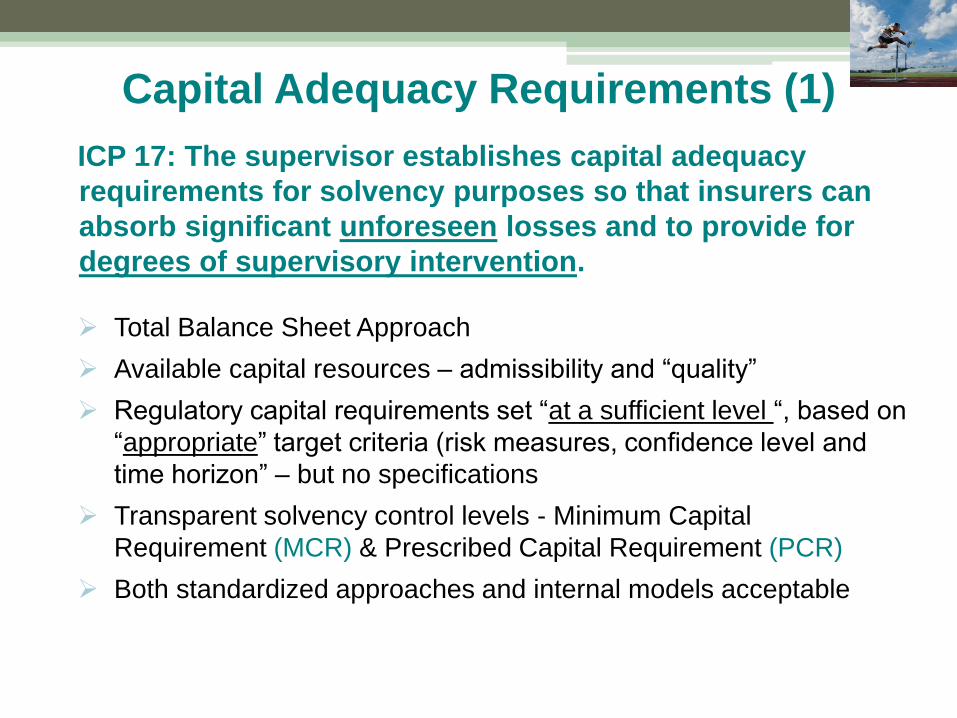

Capital Adequacy Requirements (1)

27

ICP 17: The supervisor establishes capital adequacy

requirements for solvency purposes so that insurers can

absorb significant unforeseen losses and to provide for

degrees of supervisory intervention.

Total Balance Sheet Approach

Available capital resources – admissibility and “quality”

Regulatory capital requirements set “at a sufficient level “, based on

“appropriate” target criteria (risk measures, confidence level and

time horizon” – but no specifications

Transparent solvency control levels - Minimum Capital

Requirement (MCR) & Prescribed Capital Requirement (PCR)

Both standardized approaches and internal models acceptable

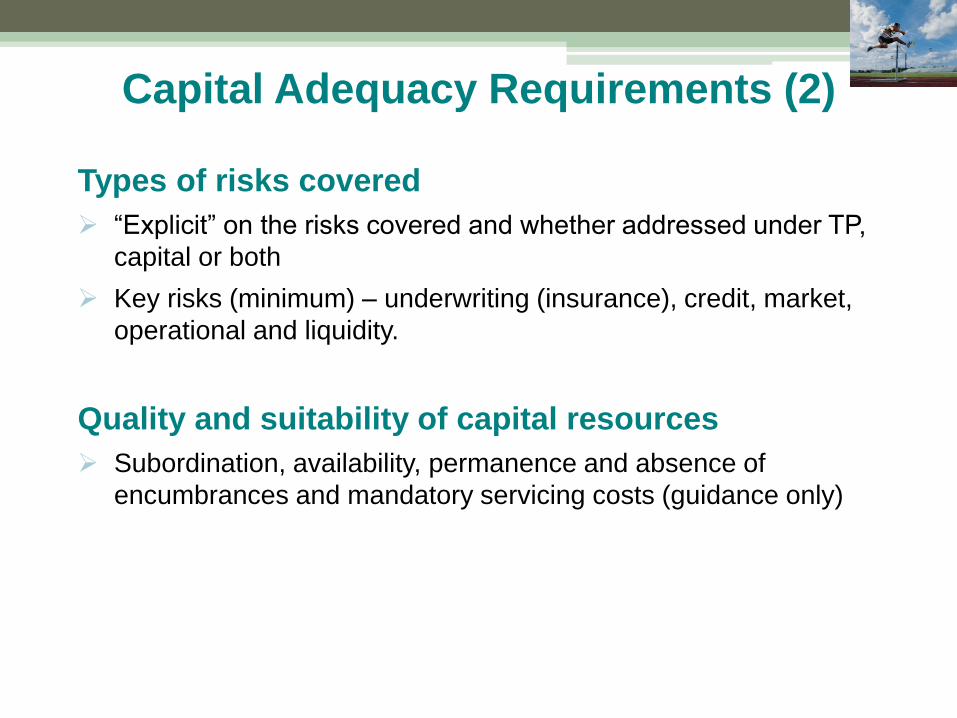

Capital Adequacy Requirements (2)

28

Types of risks covered

“Explicit” on the risks covered and whether addressed under TP,

capital or both

Key risks (minimum) – underwriting (insurance), credit, market,

operational and liquidity.

Quality and suitability of capital resources

Subordination, availability, permanence and absence of

encumbrances and mandatory servicing costs (guidance only)

Cross-sectoral Risk Transfers

• Repos, securities lending, CDS

• Liquidity swaps – banks and insurers

• Transfers to the capital markets

29

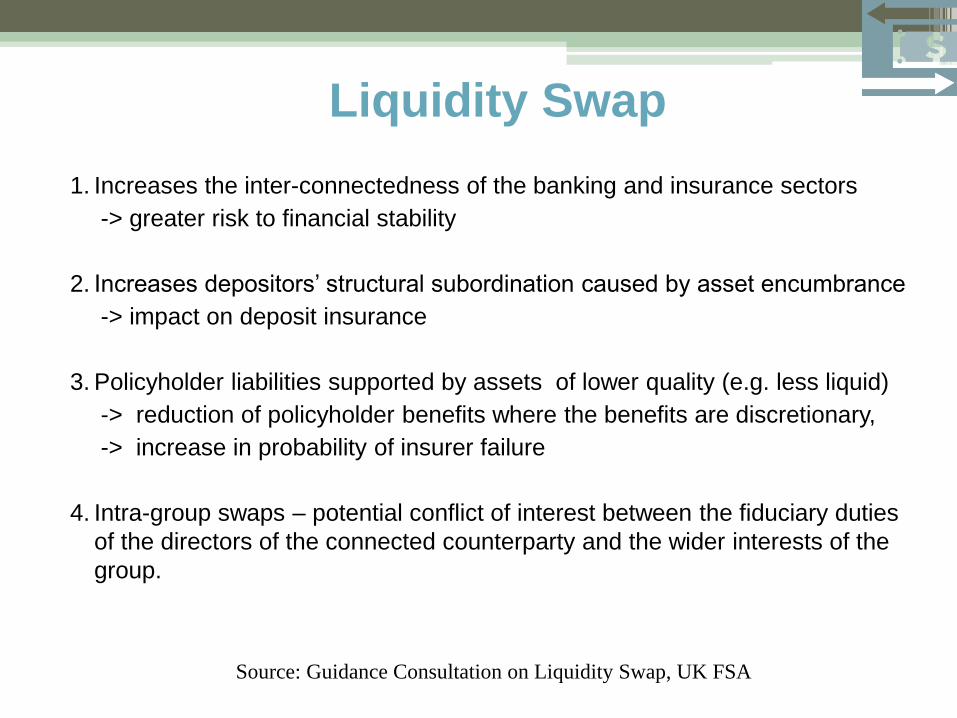

Liquidity Swap

1. Increases the inter-connectedness of the banking and insurance sectors

-> greater risk to financial stability

2. Increases depositors’ structural subordination caused by asset encumbrance

-> impact on deposit insurance

3. Policyholder liabilities supported by assets of lower quality (e.g. less liquid)

-> reduction of policyholder benefits where the benefits are discretionary,

-> increase in probability of insurer failure

4. Intra-group swaps – potential conflict of interest between the fiduciary duties

of the directors of the connected counterparty and the wider interests of the

group.

30 Source: Guidance Consultation on Liquidity Swap, UK FSA

Risk transfers to capital market

Industry Loss Warranties

Derivatives • P&C cat derivative (OTC) • Mortality/longevity swaps • Exchanged traded cat contracts • Weather derivatives

Securitization • P&C cat bonds • Extreme mortality bonds • Embedded value securitisation • AXXX/XXX securitisation • Life settlement securitisation

31

Insurable interest?

Source: Swiss Re sigma 4/2009

Other Emerging Issues

• Treatment of sovereign assets

• De-risking by insurers – unintended

assets reallocation from equities to bonds

• Trend towards investment-linked products

and investment horizon of life insurers ->

role of insurers as long-term investors

• Increase frequency and severity of natural

catastrophe – impact on non-life insurers

32

Thank You