Embed Size (px)

Citation preview

Insurance Surveyors and Loss Assessors

Contents:

1. About this handbook

2. Insurance Surveyors

3. Frequently Asked Questions

4. Policyholder Servicing TATs

5. If you have a grievance

1. About this book

This handbook is designed by the InsuranceRegulatory and Development Authority (IRDA) asa guide on Insurance Surveyors and gives genericinformation only. No Information given hereinreplaces or overrides the relevant provisions of theI n s u r a n c e A c t , 1 9 3 8 a n dRegulations/guidelines/circulars issued by IRDAin this regard.

Please approach a duly licensed surveyor orInsurance Company registered with IRDA forspecific information regarding a claim on policy orfor any other additional information.

2

2. Insurance Surveyors and Loss Assessors

Section 64 UM of the Insurance Act, 1938, mandateslicensing of Surveyors and Loss Assessors (SLA) forsettlement of losses above Rs.20000/- reported under apolicy of general insurance. Further, the said section has alsolaid down the qualification requirements for grant of licenceto act as SLA.

IRDA Surveyor Regulations, 2000 & IRDA Surveyors(Amendment) Regulations, 2013

The enactment of IRDA Act, 1999, authorized IRDA tolicence eligible persons to act as Surveyor and LossAssessors (SLA). IRDA framed the Insurance Surveyors &Loss Assessors (Licensing, professional requirements &code of conduct) Regulations, 2000 under powers vestedunder Section 42D, 64 UM and 114A of the Insurance Act,1938 and section 26 of IRDA Act, 1999. The saidregulations, specifies the eligibility criteria, training andexamination requirements for grant of licence to applicantsto act as Surveyor and Loss Assessors. The said regulationsalso specify the Duties and Responsibilities & Code ofConduct for surveyors licensed by IRDA. The Code ofConduct specifies the professional and ethical requirementsfor conduct of their professional work. It elaborates on the

3

code which, inter alia, stipulates that a surveyor and lossassessor shall behave ethically and with integrity inprofessional pursuits, shall strive for objectivity inprofessional and business judgment, act impartially whenacting on instructions from an insurer in relation to apolicyholder’s claim under a policy issued by that insurer,conduct himself with courtesy and consideration to allpeople with whom he comes into contact during the courseof his work.

Licenses are issued to both individuals andfirms/companies to act as Surveyor and Loss Assessors.There are eight areas in which surveyors could be licensed towork, depending on their qualifications. These are Fire,Motor, Miscellaneous, Engineering, Marine cargo, MarineHull, Loss of Profit and Crop Insurance.

The IRDA is empowered to take regulatory action againstsurveyors for misconduct and/or violation of Act andRegulatory provisions. These regulations were amended inthe year 2013 to bring further additional criteria for grant oflicence to act as Surveyors and Loss Assessors includingmandatory training and other requirements for grant ofboth fresh and renewal licence. Further, the amendedregulations also allows a policyholder to appoint a surveyorto assess a claim under a policy of general insurance, inwhich case the expenses towards professional fees (surveyfees) have to be borne by him. The said amended regulations

4

were notified in the official gazette in March 2013 andplaced in the IRDA website www.irda.gov.in under thelink surveyors.

Further the IRDA (Protection of Policyholders’Interests) Regulations, 2002 also stipulates the timelimit for appointment of surveyors, which is 72 hoursfrom date of intimation of claim to insurers/occurrence of the event resulting in loss or damage andsubmission of survey report by surveyors, which is onemonth from the date of appointment by insurer.

The said regulation casts responsibility on thepolicyholder to co-operate with the surveyor andprovide him with all the information/ documents toenable him to assess the loss.

Delay, if any, in the submission of the report by thesurveyor should be communicated to the insurer andinsured.

5

3. FAQ’S

1. Is it mandatory for an insurer to appointsurveyor for each and every loss reported undera policy of general insurance?

2. What is the need to engage an InsuranceSurveyor?

3. What will happen if I am not in a position tofurnish the details required by the surveyor?

4. Can the surveyor delay submission of his reportbeyond 30 days?

No. It is not mandatory for an insurer to appoint asurveyor for each and every loss reported by a policyof general insurance. Only where the estimated lossexceeds Rs.20,000/-, the insurers are mandated toappoint a licensed surveyor to assess and settle theloss.

The need for the engagement of a surveyor is forassessing the loss/damage suffered without any biasor prejudice and by a professional/expert in thefield.

If you are unable to furnish all particulars requiredby surveyor for assessment of the damage/loss,there will be delay in assessment of the claim.

In exceptional circumstances, there could be a delayin submission of survey report by a surveyor,

6

beyond 30 days from the date of his appointment, inwhich case he has to necessarily seek extension oftime from insurer. However, in no case, the time limitfor submission of report can exceed a period of 6months from the date of his appointment.

Yes. Wherever the insurer finds the surveyor’s reportincomplete in any respect, he can ask the surveyor tofurnish additional report within 15 days of receipt ofthe original report. In such a case, the surveyor shallfurnish the additional report within 3 weeks of thereceipt of such communication.

This is a false notion that surveyors are therepresentatives of insurance companies and so theyfavour insurers. A surveyor and loss assessor shall actimpartially and maintain confidentiality, neutralitywithout jeopardizing the liability of the insurer andthe claim of the insured.

5. Can the insurer ask additional report fromSurveyor?

6. Since the surveyors are appointed by theinsurance company, do they favour insurancecompanies?

7

7. Who can become a surveyor and loss assessor?What is the procedure for obtaining a surveyorlicence?

8. What are the documents to be submitted by anapplicant for grant of surveyor licence?

Section 64 UM of the Insurance Act, 1938 stipulatesthe requisite qualification for grant of licence to actas Surveyor and Loss Assessor.

In order to obtain a licence to act as surveyor and lossassessor; those persons who possess one or more ofthe qualification set out in Section 64UM of theInsurance Act, 1938 can enroll with IRDA as atrainee, undergo practical training for one yearunder A’ or ‘B’ categorized Surveyor in thosedepartments enrolled with IRDA. Upon completionof practical training and passing of surveyorexamination conducted by Insurance Institute ofIndia (Mumbai), one can apply for licence fromIRDA. The Authority on being satisfied with theeligibility of applicant, shall grant a licence whichshall remain valid for a period of five years from thedate of issue.

The following are the documents to be submitted forgrant of licence to an individual to act as Surveyorand Loss Assessor:

8

• Application form – Form 1AF

• Copies of educational qualification certificates dulynotarized

• Copy of mark sheet

• Copies of four quarterly reports

• Training completion certificate

• Demand draft for Rs.5000/- drawn on any bankpayable at Hyderabad in favour of IRDA

• Affidavit on Rs.10 stamp paper

Yes. It is possible for an applicant to submit hisapplication for grant of surveyor licence through anonline portal i.e. [email protected] (linkavailable from www.irda.gov.in) and upload allrequired documents in the portal in soft form. Thesaid portal provides an end to end solution andenables the applicant to know the status ofapplication from submission till its approval andgrant of licence by IRDA.

9. Is it possible for an applicant to submit anapplication for surveyor licence and otherrequired documents in soft form? Is there anonline portal for submission of applications? Isthere any system to know my status ofapplication?

9

10. How do I know whether the surveyor appointedis an authorized person to take up theassignment of loss assessment or not?

11. Is the loss amount assessed by surveyor bindingon insurer/s?

12. What is the time limit for the insurer to take adecision on the claim, after submission ofsurveyor report or additional survey report bythe surveyor and loss assessor?

The list of licensed and categorized surveyors andloss assessors is placed in the IRDA website i.e.www.irda.gov.in from which one can know whetherthe surveyor appointed is a licensed Surveyor or not.

No. The insurers are not bound by the loss amountassessed by the surveyor. The insurer has the right topay or settle any claim at any amount different fromthe amount assessed by the appointed surveyor.

An insurer has to take a decision on the claim within30 days of receipt of surveyor report or additionalsurvey report by the surveyor. The insurer musteither offer a settlement of claim or give reasons forrejection of a claim in writing.

10

13. Can a policyholder claim interest in case of anydelay in settlement of claim?

Once an offer of claim settlement given by insurer isaccepted by a policyholder in writing, claimsettlement amounts should be disbursed within 7days from the date of acceptance by policyholder. Incase of any delay in disbursement of the claimamount, the insurer is liable to pay interest @ 2% rateabove the bank rate prevalent on 1st April of thatfinancial year.

11

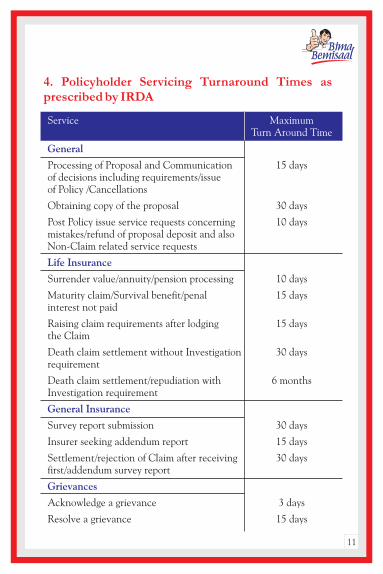

4. Policyholder Servicing Turnaround Times asprescribed by IRDA

12

5. If you have a grievance:

The Consumer Affairs Department of the InsuranceRegulatory and Development Authority (IRDA) hasintroduced the Integrated Grievance Management System(IGMS) which is an online system for registration andtracking of grievances. You must register your grievancefirst with the insurance company and in case you are notsatisfied with its disposal by the company, you may escalate itto IRDA through IGMS by accessing www.igms.irda.gov.in.In case you are not able to access the insurer’s grievancesystem directly, IGMS also provides you a gateway toregister your grievance with the insurer.

Apart from registering your grievance through IGMS ( i.e.,web) , you have several channels for grievanceregistration—through e-mail ([email protected]),through letter ( address your letter to Consumer AffairsDepartment, Insurance Regulatory and DevelopmentAuthority, 3rd Floor, Parishram Bhavan, Basheerbagh,Hyderabad:4) or simply call IRDA Call Centre at Toll Free155255 through which IRDA shall, free of cost, registeryour complaints against insurance companies as well as helptrack its status. The Call Centre assists by filling up thecomplaints form on the basis of the call. Wherever required,it will facilitate in filing of complaints directly with theinsurance companies as the first port of call by givinginformation relating to the address, telephone number,

13

website details, contact number, e-mail id etc. of theinsurance company. IRDA Call Centre offers a truealternative channel for prospects and policyholders, withcomprehensive tele-functionalities, serving as a 12 hours x 6days service platform from 8 AM to 8 PM, Monday toSaturday in Hindi, English and various Indian languages.

When a complaint is registered with IRDA, it facilitatesresolution by taking it up with the insurance company. Thecompany is given 15 days’ time to resolve the complaint. Ifrequired, IRDA carries out investigations and enquiries.Further, wherever applicable, IRDA advises thecomplainant to approach the Insurance Ombudsman interms of the Redressal of Public Grievances Rules, 1998.

![No. 6288. LAND SURVEYORS ACT 1958.1958. Land Surveyors. No. 6288 837 No. 6288. LAND SURVEYORS ACT 1958. An Act to consolidate the Law relating to Surveyors. [30th September, 1958.]](https://img.pdfslide.net/doc/110x75/5e94498d234c4b210e568874/no-6288-land-surveyors-act-1958-1958-land-surveyors-no-6288-837-no-6288.jpg)

![Policyholder: 1[ABC Company]](https://img.pdfslide.net/doc/110x75/61fb14eb2e268c58cd59ef53/policyholder-1abc-company.jpg)