Embed Size (px)

Citation preview

Integrated sustainability analysis of biorefinery concepts Nils Rettenmaier | IFEU

Nils Rettenmaier | IFEU - 12/02/2014

● Goal: Multi-criteria evaluation of BIOCORE’s sustainability impacts ● vs. petrochemical product portfolios and vs. biomass-based alternatives

● Challenge: No standardised overall methodology available ● Approach: Comprehensive and streamlined sustainability assessment

● All major aspects of sustainability covered ● Set of existing state-of-the-art assessment methodologies used ● LCA, economic and social assessment harmonised between sister projects ● Individual assessments are based on the same system boundaries

INTEGRATED SUSTAINABILITY ASSESSMENT METHODOLOGY

Settings for sustainability benchmarking

Integrated assessment of sustainability

Environmental assessment

Economic assessment

Social / legal / policy assessment

SWOT & biomass competition analysis

Nils Rettenmaier | IFEU - 12/02/2014

● Scenario-based assessment: ● Industrial-scale 150 kt biorefinery in 2025 (mature technology)

● Generic, life cycle-oriented comparison (no case studies): ● Bio-based product portfolios vs. conventional product portfolios ● Screening procedure applied to select among possible combinations

INTEGRATED SUSTAINABILITY ASSESSMENT SETTINGS & DEFINITIONS

Nils Rettenmaier | IFEU - 12/02/2014

● Combination of two methodologies ● Screening Life Cycle Assessment (LCA)

• well-established methodology • global/regional environmental impacts

● ‘Life Cycle Environmental Impact Assessment’ (LC-EIA) • newly developed methodology • local environmental impacts

ENVIRONMENTAL ASSESSMENT METHODOLOGY

Nils Rettenmaier | IFEU - 12/02/2014

● Environmental benefits can be achieved, depending on: ● Product portfolio

• Need to valorise all fractions • High-quality CIMV Organosolv

lignin not to be used for energy • Size of smallest intermediate

matters: avoid C1/C2 molecules ● Technical implementation

• Large impact of biomass con-version: energy-intensive CIMV process ( residual heat !)

• Heat integration and energy use in DSP are crucial

• Favourable conditions needed ● Provision of lignocellulosic

biomass less important • Rice straw burning avoided (+)

ENVIRONMENTAL ASSESSMENT HIGHLIGHTS: SCREENING LCA

Nils Rettenmaier | IFEU - 12/02/2014

● Biomass feedstock deter-mines local environmental impacts (at generic level): ● Comparably low risks

associated with lignocellulose • Least impacts: agro-residues • Low impacts: perennial crops

● Biomass conversion less important than provision ● Brownfield site causes less

impacts than greenfield site ● Local environmental impacts

depend on specific location ● Can act as showstoppers ● Have to be tackled at an early

stage in order to create saver environment for investment

ENVIRONMENTAL ASSESSMENT HIGHLIGHTS: LIFE CYCLE-EIA

©T. E. Reiners

Provision of wheat straw vs. ploughing in

Type of risk

Affected environmental factors Soil Ground

water Surface water

Plants / Biotopes

Animals Climate / Air

Land-scape

Human health and recreation

Bio-diversity

Soil erosion neutral neutral Soil compaction neutral neutral neutral neutral neutral

Loss of soil organic matter

neutral neutral neutral neutral

Soil chemis-try / fertiliser neutral neutral

Eutrophi-cation neutral neutral neutral neutral neutral neutral

Nutrient leaching neutral

Water demand neutral neutral neutral neutral

Weed control / pesticides neutral neutral neutral neutral neutral

Loss of landscape elements

neutral neutral neutral neutral neutral neutral

Loss of habitat types neutral /

positive1 neutral / positive1 neutral /

positive1 Loss of species neutral /

positive1 neutral / positive1 neutral /

positive1

Nils Rettenmaier | IFEU - 12/02/2014

● Economic assessment ● Newly developed methodology for economic evaluation of biorefineries

which works with limited input data (e.g. no sizing of equipment). • Estimation of capital expenditures (CAPEX) based on the sum of the calculated

rated power of all equipment of the whole plant. • Operating expenditures (OPEX) partly calculated directly (e.g. utilities and

operating materials), partly based on standard literature.

● Market analysis ● Product fact sheets incl. product prices ● Analysis of green premium prices

ECONOMIC ASSESSMENT & MARKET ANALYSIS METHODOLOGY

Nils Rettenmaier | IFEU - 12/02/2014

● Profitability depending on: ● Product portfolio

• Lignin & C5 valorisation needed • Ethanol to be avoided • Green Premium prices paid ?

● Technical implementation • Favourable conditions needed

● Feedstock • Hardwood or SRC poplar more

profitable than straw ● Capacity

• 500 kt rice straw unit profitable (not the case for 150 kt unit)

● IRR-threshold of 25% not surpassed in std. scenarios

● Additional incentives needed ● Price support (< biofuels) ● Investment support (CAPEX)

ECONOMIC ASSESSMENT & MARKET ANALYSIS HIGHLIGHTS: COST OF MANUFACTURE

Nils Rettenmaier | IFEU - 12/02/2014

● Fact sheets available for all BIOCORE products

● Green Premium prices possible for selected BIOCORE products: ● May significantly improve

biorefinery’s profitability ● +10 to 20% paid for bio-

based intermediates, plastics and polymers

● Level decreases towards end of the supply chain

● Additional effects possible if feedstock is non-GMO and/or non-food crop

ECONOMIC ASSESSMENT & MARKET ANALYSIS HIGHLIGHTS: MARKET ANALYSIS

Nils Rettenmaier | IFEU - 12/02/2014

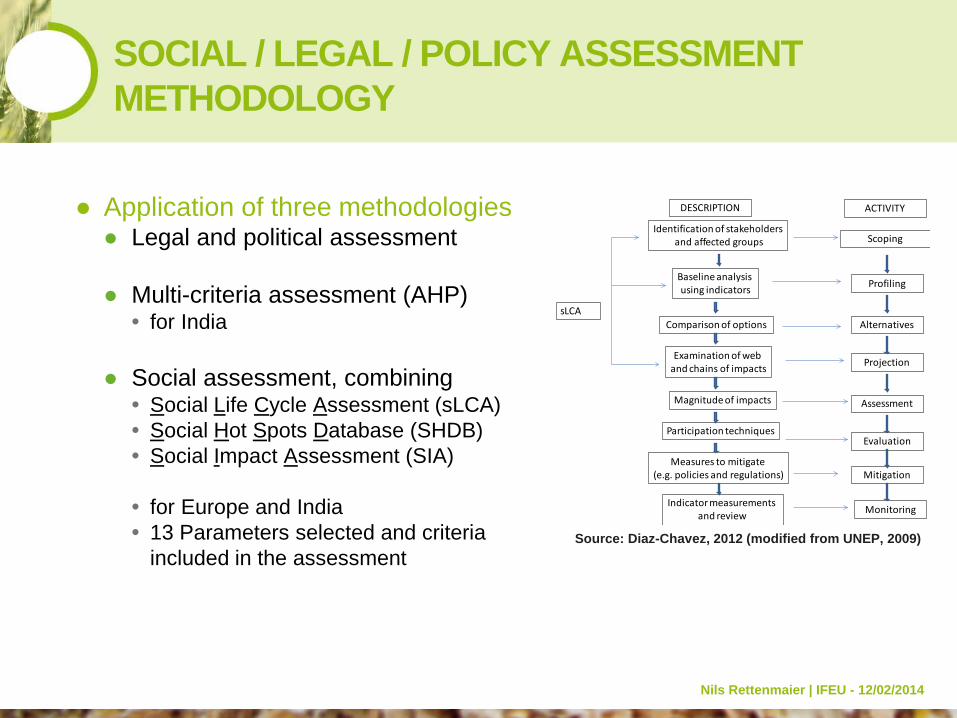

● Application of three methodologies ● Legal and political assessment

● Multi-criteria assessment (AHP)

• for India

● Social assessment, combining • Social Life Cycle Assessment (sLCA) • Social Hot Spots Database (SHDB) • Social Impact Assessment (SIA)

• for Europe and India • 13 Parameters selected and criteria

included in the assessment

SOCIAL / LEGAL / POLICY ASSESSMENT METHODOLOGY

Profiling

Scoping

Assessment

Projection

Mitigation

Evaluation

Monitoring

Identification of stakeholdersand affected groups

Baseline analysis using indicators

AlternativesComparison of options

Examination of web and chains of impacts

Magnitude of impacts

Participation techniques

Measures to mitigate (e.g. policies and regulations)

Indicator measurements and review

ACTIVITYDESCRIPTION

sLCA

Source: Diaz-Chavez, 2012 (modified from UNEP, 2009)

Nils Rettenmaier | IFEU - 12/02/2014

● Europe: ● Different policy and regu-

latory instruments in place at EU and national level

● No mandatory social criteria in the RED

● No sustainability framework for lignocellulosic feedstock ”RED2” for solid biomass !

● Standards needed, e.g. for bio-based carbon content CEN TC 411 ongoing

● Policy changes a problem for some stakeholders

SOCIAL / LEGAL / POLICY ASSESSMENT HIGHLIGHTS: POLICY ASSESSMENT

Source: Diaz-Chavez, 2012

Nils Rettenmaier | IFEU - 12/02/2014

● Conclusions: ● Skilled workforce to be

attracted to remote areas ● Job creation:

• mainly in biomass production / extraction and transport

• less in production and conversion due to high tech

• reported by stakeholders, not quantified

● Health and safety: regulations need to consider new paths & products

● Producers’ willingness to sell biomass unclear (fair share?)

● Rural development a high benefit for alternative uses of biomass and dedicated crops

SOCIAL / LEGAL / POLICY ASSESSMENT HIGHLIGHTS: SOCIAL ASSESSMENT

No Parameter Characteristics/ Criteria

Type Impact Risk Benefit

1 Production of feedstock Incentives B + H

Barriers B - L

2 Identification of stakeholders along the supply chain

Producers (farmers) Regulators Business Traders Research

B + H

3 Policies and regulations National

B + H

Enforcement B - L

5 Land use tenure Land ownership rights B N

6 Community participation Community participation D + H

8 Rural development and infrastructure

Roads

B - L

Water (availability and quality) for the local population

D N

9 Job creation and wages Labour involved on feedstock production

D + & - L H

Labour involved in production D + L

Wages paid according to national/regional regulation (minimum wage)

D N L

Rural development D + H

10 Gender equity Inclusion of women D

11 Labour conditions ILO conventions including - Child labour - Right to organise - Indigenous rights - Forced labour

D + & - L H

12 Health and safety Compliance with health and safety regulations at the different supply chains

D L M

13 Competition with other sectors Competition of residues use for biorefinery and impact on other industries and sectors that affects negatively

D + & - M M

Source: Diaz-Chavez, 2013

Nils Rettenmaier | IFEU - 12/02/2014

● Application of two methodologies ● SWOT (strengths, weaknesses,

opportunities and threats) analysis • Capture further sustainability aspects

not covered by other assessments • Identify „hot spots“ • Collect stakeholder perceptions

● Biomass competition analysis • Address direct and indirect land use

change (LUC) impacts • Set zero in LCA and other assessments

to only evaluate the impacts of the BIOCORE concept (which would be superposed by competition effects)

• Therefore separate analysis

SWOT & BIOMASS COMPETITION ANALYSIS METHODOLOGY

Nils Rettenmaier | IFEU - 12/02/2014

● Biomass provision ● Techn. potential not realisable:

• Insufficient infrastructure • Ownership structure • Competition with tradition. uses

● (Too) high residue extraction = risk for soil fertility

● Stem wood & residues not specifiable once pelletised

● Biomass conversion

● Lack of consistent and sufficiently developed legislative framework ● Certification systems needed to avoid fraud with allegedly “bio-based”

products, especially if green premium prices are paid ● Marked still depends on political support ● Efforts needed to achieve public acceptance

SWOT & BIOMASS COMPETITION ANALYSIS HIGHLIGHTS: SWOT ANALYSIS

Success factors Failure factors Internal factors

Strengths Providing an alternative to the increasingly

scarce fossil carbon sources Contribution to rural development: Job and

income creation in rural areas (agriculture and forestry, logistics, processing)

Runs on non-food biomass: No direct competition to food

Runs on residues (straw): No direct competition for land use

Weaknesses Only debarked hardwood is suitable Softwood can be used as pellets only Infrastructure not yet fully available Scarcity of land in Europe, except for

eastern Europe Some created jobs are only seasonal jobs

External factors

Opportunities Higher energy- and resource security for EU Making farmers biorefinery shareholders

could facilitate cooperation and rural development

Threats Higher biomass prices affect other biomass

users Indirect effects on land use patterns:

Increased demand for cultivated biomass because of higher efficiency (c.f. the current situation of German biogas industry, which operates using maize silage)

In case of biomass import: long transport and associated burdens, lower transparency regarding sustainability issues

Small scale ownership structure put a hurdle on mobilisation

Nils Rettenmaier | IFEU - 12/02/2014

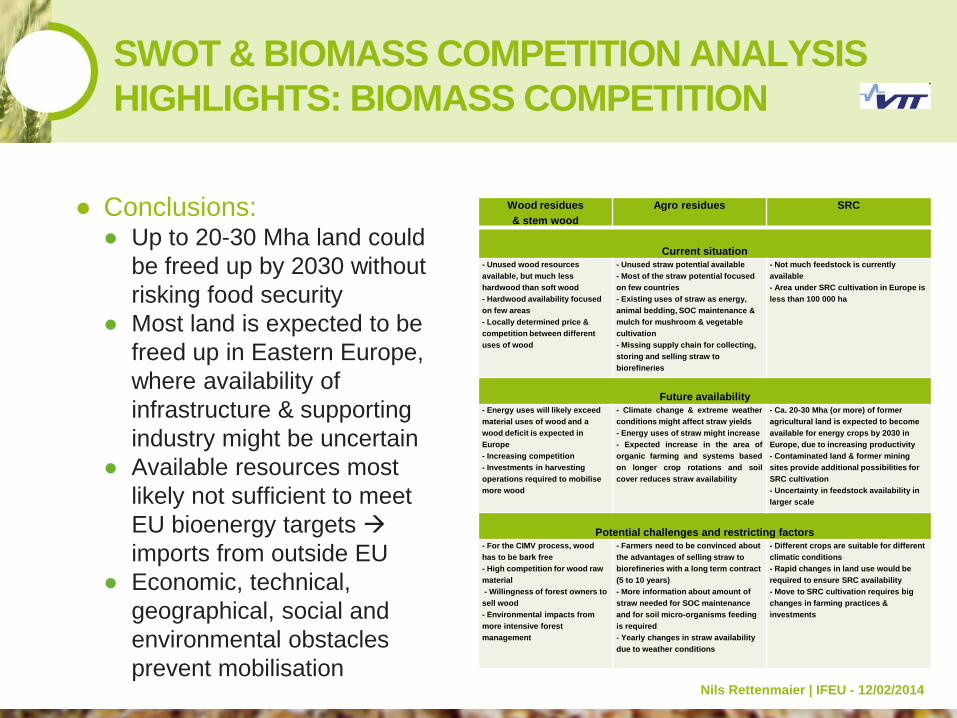

● Conclusions: ● Up to 20-30 Mha land could

be freed up by 2030 without risking food security

● Most land is expected to be freed up in Eastern Europe, where availability of infrastructure & supporting industry might be uncertain

● Available resources most likely not sufficient to meet EU bioenergy targets imports from outside EU

● Economic, technical, geographical, social and environmental obstacles prevent mobilisation

SWOT & BIOMASS COMPETITION ANALYSIS HIGHLIGHTS: BIOMASS COMPETITION

Wood residues & stem wood

Agro residues SRC

Current situation

- Unused wood resources available, but much less hardwood than soft wood - Hardwood availability focused on few areas - Locally determined price & competition between different uses of wood

- Unused straw potential available - Most of the straw potential focused on few countries - Existing uses of straw as energy, animal bedding, SOC maintenance & mulch for mushroom & vegetable cultivation - Missing supply chain for collecting, storing and selling straw to biorefineries

- Not much feedstock is currently available - Area under SRC cultivation in Europe is less than 100 000 ha

Future availability - Energy uses will likely exceed material uses of wood and a wood deficit is expected in Europe - Increasing competition - Investments in harvesting operations required to mobilise more wood

- Climate change & extreme weather conditions might affect straw yields - Energy uses of straw might increase - Expected increase in the area of organic farming and systems based on longer crop rotations and soil cover reduces straw availability

- Ca. 20-30 Mha (or more) of former agricultural land is expected to become available for energy crops by 2030 in Europe, due to increasing productivity - Contaminated land & former mining sites provide additional possibilities for SRC cultivation - Uncertainty in feedstock availability in larger scale

Potential challenges and restricting factors - For the CIMV process, wood has to be bark free - High competition for wood raw material - Willingness of forest owners to sell wood - Environmental impacts from more intensive forest management

- Farmers need to be convinced about the advantages of selling straw to biorefineries with a long term contract (5 to 10 years) - More information about amount of straw needed for SOC maintenance and for soil micro-organisms feeding is required - Yearly changes in straw availability due to weather conditions

- Different crops are suitable for different climatic conditions - Rapid changes in land use would be required to ensure SRC availability - Move to SRC cultivation requires big changes in farming practices & investments

Nils Rettenmaier | IFEU - 12/02/2014

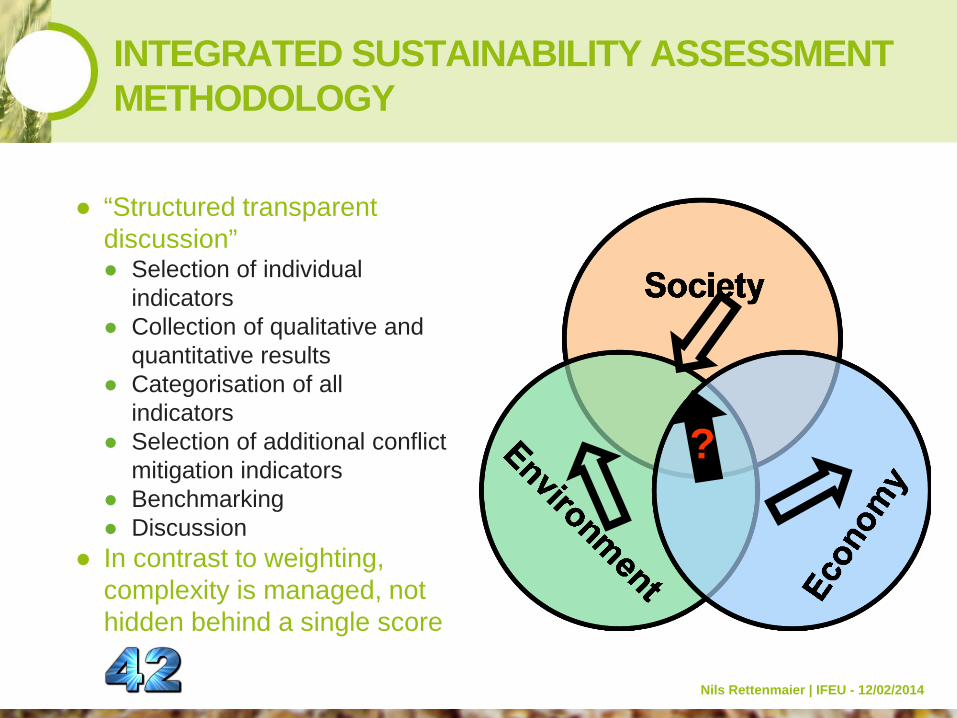

● “Structured transparent discussion” ● Selection of individual

indicators ● Collection of qualitative and

quantitative results ● Categorisation of all

indicators ● Selection of additional conflict

mitigation indicators ● Benchmarking ● Discussion

● In contrast to weighting, complexity is managed, not hidden behind a single score

INTEGRATED SUSTAINABILITY ASSESSMENT METHODOLOGY

?

Nils Rettenmaier | IFEU - 12/02/2014

INTEGRATED SUSTAINABILITY ASSESSMENT HIGHLIGHTS

Indicator Unit or subcateg. Whe

at s

traw

(X

yl /

IA)

Whe

at s

traw

(X

yl /

etha

nol)

Whe

at s

traw

(E

than

ol /

IA)

Whe

at s

traw

(S

HF

etha

nol)

Whe

at s

traw

(E

than

ol to

PV

C)

Whe

at s

traw

(F

allb

ack

optio

ns)

Whe

at s

traw

(C

atal

ytic

xyl

itol)

Whe

at s

traw

(IA

m

ater

ial r

ecyc

ling)

Whe

at s

traw

(S

traw

pow

ered

)

Whe

at s

traw

(L

igni

n to

ene

rgy)

Har

dwoo

d (X

yl /

IA)

Pop

lar S

RC

(X

yl /

IA)

Mis

cant

hus

(Xyl

/ IA

)

Whe

at s

traw

, Ind

ia

(Xyl

/ IA

)

Ric

e st

raw

, Ind

ia

(Xyl

/ IA

)

Ric

e st

raw

, Ind

ia

500

kt (X

yl /

IA)

Dire

ct c

ombu

stio

n (W

heat

stra

w)

Syn

fuel

(W

heat

stra

w)

Whe

at e

than

ol

Bee

t eth

anol

Mai

ze e

than

ol

Triti

cale

dire

ct

com

bust

ion

Rap

e se

ed

biod

iese

l

Mai

ze b

ioga

s

Maturity - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 0 0 + + + 0 + +Availability of infrastructure for logistics and storage

- - - - - - - - - - - - - - - - - - - - - 0 0 0 0 0 0

Use of GMOs - - - - - - - - 0 - - - - - - - - - - - - - - - 0 0 0 0 0 0 0 0Risk of explosions and fires - 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 - 0 0 0 0 0 0

Development of legislatory framework and bureaucratic hurdles

- - - - - - - - - - - - - - - - - 0 - - - - 0 - 0

Feedstock flexibility of conversion technologies

- + + + + + + + + + + + + + + + + + + - - - + - +

Resource depletion: energy GJ / t biomass (dry)-14 -4 17 16 14 12 -23 -11 -15 -9 -22 -16 -15 -14 -10 -10 -18 -3 -11 -1 -5 -7 -14 -12

Climate change t CO2 eq. / t biomass (dry) -0,9 -0,5 0,3 0,2 0,2 0,5 -1,3 -0,8 -0,7 -0,4 -1,5 -1,2 -1,1 -0,9 -1,0 -1,0 -1,0 -0,1 -0,7 -0,1 -0,2 -0,3 -0,7 -0,4Terrestrial acidification kg SO2 eq. / t biomass (dry) -0,3 0,7 5,2 4,9 4,9 1,5 6,3 -0,1 1,0 0,9 -2,6 -1,5 -1,1 -0,3 -2,9 -2,9 0,5 1,0 1,6 0,0 3,4 3,3 5,9 2,3Marine eutrophication kg N eq. / t biomass (dry) -4,3 -4,3 1,4 1,7 1,6 N/D -5,6 -4,4 -1,8 -4,3 -6,2 -4,2 -3,7 -4,3 -4,4 -4,4 0,5 0,5 N/D N/D N/D 1,2 N/D N/DFreshwater eutrophication kg P eq. / t biomass (dry) -0,4 -0,4 0,1 0,1 0,1 N/D -0,4 -0,4 -0,1 -0,4 -0,6 -0,4 -0,3 -0,4 -0,3 -0,3 0,1 0,1 N/D N/D N/D 0,1 N/D N/DPhotochemical ozone formation kg NMVOC eq. / t biomass (dry) -1,9 -1,4 0,7 0,3 0,2 -0,5 -1,5 -1,7 -0,6 -0,5 -3,2 -2,5 -2,2 -1,9 -23,9 -23,9 -0,5 0,1 -0,8 -0,1 -0,1 1,0 0,3 -0,3Respiratory inorganics kg PM10 eq. / t biomass (dry) -0,7 -0,4 1,0 0,8 0,7 -0,1 0,8 -0,6 -0,1 -0,3 -1,3 -0,9 -0,7 -0,7 -18,1 -18,1 0,0 0,0 0,1 0,0 0,5 0,7 0,8 0,2Ozone depletion g R11 eq. / t biomass (dry) 2,4 1,9 2,9 2,8 2,9 -0,2 2,4 2,4 4,4 3,1 -1,1 0,3 0,4 2,4 -14,1 -14,1 5,7 2,3 3,6 -0,7 10,2 9,6 18,9 7,6Direct additional land use (ha · a) / t biomass (dry) 0 0 0 0 0 0 0 0 0 0 0 0,08 0,09 0 0 0 0 0 0,20 0,02 0,15 0,09 0,33 0,07Indirect land use (EU) (ha · a) / t biomass (dry) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 -0,01 0 0 N/D 0,0Indirect land use (SA) (ha · a) / t biomass (dry) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 -0,06 -0,02 -0,06 0 N/D 0,0Water - 0 0 0 0 0 0 0 0 0 0 0 0 - - 0 + + 0 0 0 - - 0 - -Soil - 0 0 0 0 0 0 0 0 0 0 0 + + 0 ++ ++ 0 0 - - - - - - - - - -Fauna - 0 0 0 0 0 0 0 0 0 0 0 + - 0 ++ ++ 0 0 - - - - - -Flora - 0 0 0 0 0 0 0 0 0 0 0 + 0 0 ++ ++ 0 0 - - - - - - - - -Landscape - 0 0 0 0 0 0 0 0 0 0 0 0 0 0 + + 0 0 0 0 0 0 0 0

Total capital investment Million € 150 144 156 149 161 123 136 157 138 144 158 158 147 N/D 146 284NPV (5%, no GP) Million € -159 -311 -629 -686 -852 -641 -96 -209 -114 -410 20 7 -131 N/D -229 110NPV (5%, incl. GP) Million € 6 -311 -464 -686 -787 -641 69 -38 51 -252 239 224 46 N/D -78 616Profit / loss (no GP) € / t biomass (dry) -11 -114 -324 -370 -459 -353 23 -40 12 -520 115 106 6 N/D -61 77Profit / loss (incl. GP) € / t biomass (dry) 123 -114 -114 -370 -328 -353 152 103 139 -458 263 253 147 N/D 75 147IRR (no GP) % N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 7% 6% N/A N/D N/A 11%IRR (incl. GP) % 6% N/A N/A N/A N/A N/A 12% 1% 10% N/A 24% 23% 10% N/D N/A 31%Price support (no GP, 25% IRR)

% 37% 56% 127% 159% 219% 238% 27% 42% 31% 84% 18% 19% 34% N/D 49% 11% N/D N/D 60%* 60%* 60%* N/D 40%* 70%*

Price support (no GP, 15% IRR)

% 25% 43% 108% 137% 191% 208% 17% 29% 20% 68% 8% 9% 22% N/D 36% 3% N/D N/D 60%* 60%* 60%* N/D 40%* 70%*

Price support (incl. GP, 25% IRR)

% 19% 56% 83% 159% 182% 238% 11% 23% 14% 53% 1% 2% 15% N/D 28% 0% N/D N/D 60%* 60%* 60%* N/D 40%* 70%*

Market access - 0 + 0 + + + + 0 0 0 0 0 0 0 0 0 0 - + + + 0 + +CO2 avoidance costs € / t CO2 eq. 294 793 N/A N/A N/A N/A 167 397 305 1194 107 135 218 N/D 314 70

Energy resource savings costs € / GJ 19 97 N/A N/A N/A N/A 9 29 15 50 7 10 16 N/D 32 7

Incentives + + + + + 0 + + + + ++ + + N/D ++ ++Barriers - - - - - 0 - - - - - - - N/D - -Producers (farmers) + + + + + + + + + + ++ + + N/D ++ ++Business + + + + + + + + + + ++ + + N/D ++ ++Traders + + + + + + + + + + + + + N/D + +Road 0 0 0 0 0 0 0 0 0 0 - + + N/D + +

Water (availability and quality) for the local population 0 0 0 0 0 0 0 0 0 0 0 - - N/D 0 0

Labour conditions (enforcement)

ILO conventions + + + + + 0 + + + + 0 0 0 N/D + +

Competition with other sectors Competition for residues - - - - - -- - - - - - 0 0 N/D - -Soci

ety

Econ

omy

Envi

ronm

ent

Tech

nolo

gy

N/D

N/D

Production of feedstock

Identification of stakeholders

Rural development and infrastructure

Standard Standard

N/D

Alternatives to BIOCOREStandard

BIOCORE scenarios BIOCORE scenarios

Nils Rettenmaier | IFEU - 12/02/2014

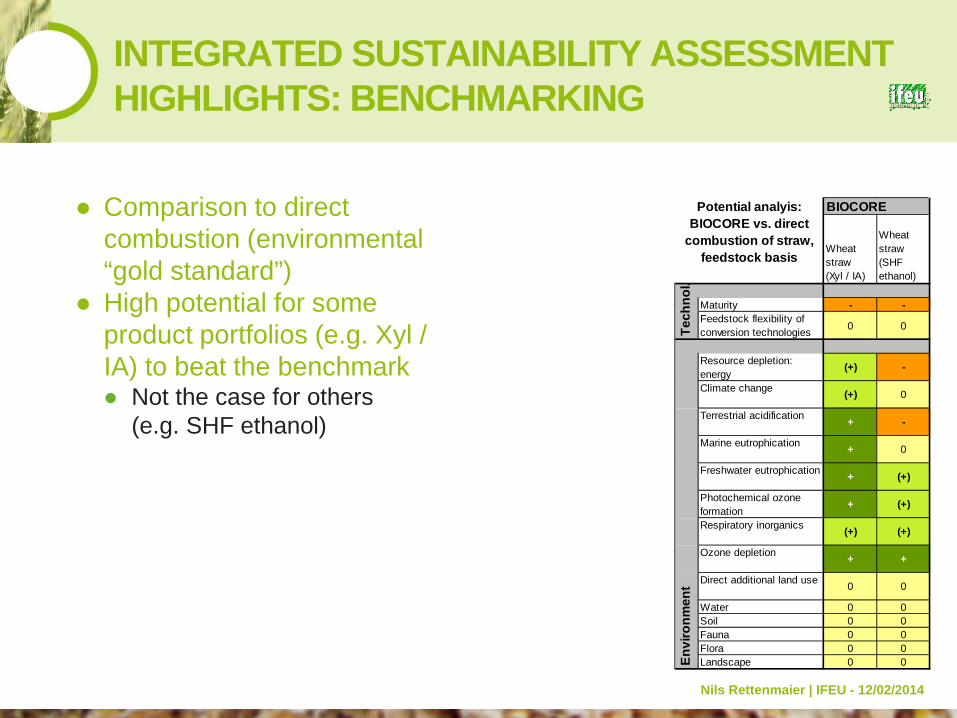

● Comparison to direct combustion (environmental “gold standard”)

● High potential for some product portfolios (e.g. Xyl / IA) to beat the benchmark ● Not the case for others

(e.g. SHF ethanol)

INTEGRATED SUSTAINABILITY ASSESSMENT HIGHLIGHTS: BENCHMARKING

BIOCORE

Wheat straw (Xyl / IA)

Wheat straw (SHF ethanol)

Maturity - -Feedstock flexibility of conversion technologies 0 0

Resource depletion: energy

(+) -

Climate change (+) 0

Terrestrial acidification + -

Marine eutrophication + 0

Freshwater eutrophication + (+)

Photochemical ozone formation

+ (+)

Respiratory inorganics (+) (+)

Ozone depletion + +

Direct additional land use 0 0

Water 0 0Soil 0 0Fauna 0 0Flora 0 0Landscape 0 0

Potential analyis:BIOCORE vs. direct

combustion of straw,feedstock basis

Tech

nol.

Envi

ronm

ent

Nils Rettenmaier | IFEU - 12/02/2014

● Major methodological advancements ● Comprehensive and streamlined integrated sustainability assessment

● Powerful decision support tool for the ex-ante evaluation and optimisation of complex (biorefinery) systems ● Capable of depicting the most promising options (all investigated scenarios

show advantages and disadvantages) ● It is important to consider the entire value chain

● Biomass conversion (product portfolio and optimum technical implementation) crucial in terms of economics and environment (LCA)

● Biomass provision important in terms of local environmental as well as social impacts

● Success of biorefineries not just a question of technology ● Many stakeholders involved (e.g. farmers/forest owners) ● Biomass availability is limited ● Political framework ● Legal framework

CONCLUSIONS

Nils Rettenmaier | IFEU - 12/02/2014

● Actively manage increasing biomass and land use competition to which biorefineries might contribute ● Biomass and land use allocation plans at national and European level ● Regional plans which include regulations for project planning and land /

resource allocation in order to minimize barriers for project development ● Mandatory sustainability criteria for bio-based materials (+ food & feed?)

● Create a level-playing field between all uses of biomass, especially between bioenergy & bio-based products ● The current policy framework (10% RE target in the transport sector and

multiple counting in the RED) leads to a misallocation of biomass and undesired effects (iRUC=indirect residue use competition)

● Current users of biomass in other sectors also require a level-playing field ● Ensure a stable investment climate: >100 M€ for a 150 kt biorefinery

● (One-time) investment support more attractive than pay-back via multiple counting (subject to frequent changes)

● Consider Equator principles (World Bank) for large investments

RECOMMENDATIONS… …FOR POLICY MAKERS

Nils Rettenmaier | IFEU - 12/02/2014

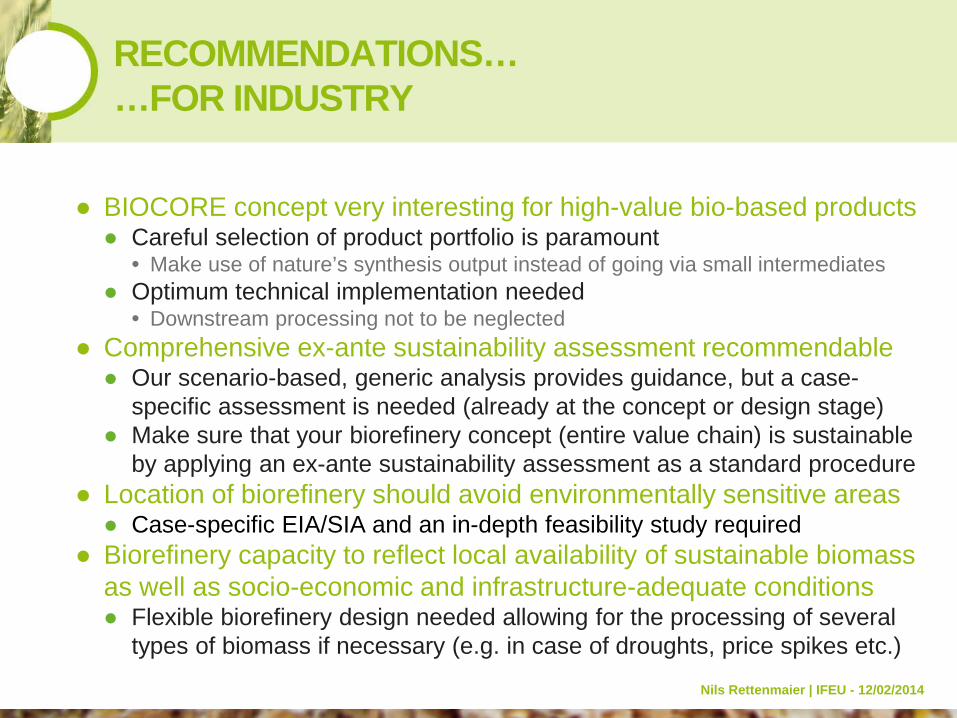

● BIOCORE concept very interesting for high-value bio-based products ● Careful selection of product portfolio is paramount

• Make use of nature’s synthesis output instead of going via small intermediates ● Optimum technical implementation needed

• Downstream processing not to be neglected ● Comprehensive ex-ante sustainability assessment recommendable

● Our scenario-based, generic analysis provides guidance, but a case-specific assessment is needed (already at the concept or design stage)

● Make sure that your biorefinery concept (entire value chain) is sustainable by applying an ex-ante sustainability assessment as a standard procedure

● Location of biorefinery should avoid environmentally sensitive areas ● Case-specific EIA/SIA and an in-depth feasibility study required

● Biorefinery capacity to reflect local availability of sustainable biomass as well as socio-economic and infrastructure-adequate conditions ● Flexible biorefinery design needed allowing for the processing of several

types of biomass if necessary (e.g. in case of droughts, price spikes etc.)

RECOMMENDATIONS… …FOR INDUSTRY

Nils Rettenmaier | IFEU - 12/02/2014

● Questions ? ● Don’t hesitate to ask !

● Acknowledgements ● All BIOCORE WP 7 partners

● The whole BIOCORE consortium

● This work was supported by the European Commission through the FP7 project “BIOCOmmodity REfinery” (“BIOCORE”, GA no. 241566)

THANK YOU FOR YOUR KIND ATTENTION

Contact: Nils Rettenmaier [email protected] +49-6221-4767-24

H. Keller M. Müller-Lind. G. Reinhardt

M. O‘Donohue R. Diaz-Chavez W. Kretschmer K. Scheurlen et al.

S. Piotrowski M. Carus J. Beckmann

S. Kapur S. Bhattacharjya I. Kumar

H. Pihkola T. Pajula