Embed Size (px)

DESCRIPTION

A report summarising the state of the market and practical guide for advertises looking to employ interactive solutions

Citation preview

The Outdoor Media Landscape is Changing Start

1Interactive Europe Foreword

A major quantitative and qualitative study of 9,000 Europeans across 6 markets Interactive Europe explores interactivity in the context of Out of Home. It seeks to understand the audience’s current behaviours as well as what they see themselves open to doing in the future.

In addition to providing brands with insight into the emerging opportunities and pitfalls to avoid, the findings confirm that the personalisation of technology and the interactive behaviours it facilitates are redefining Out of Home advertising’s role.

Ultimately, this new landscape is amplifying many of Out of Home’s traditional strengths, providing a world of new opportunities for brands to enjoy deeper engagement with consumers.

FOREWORDThe world is changing. Consumer behaviour and the expectation placed on brands is evolving, as is the way we interact with advertising.

From a brand owner’s perspective this report seeks to provide answers to several key questions:

What is interactive advertising?

Do I need to worry about interactivity now?

What does the audience think about interactive Out of Home?

What are the technologies to focus on and the pitfalls to avoid?

How does interactive Out of Home fit into my media mix – how does it work with social media?

What does the future look like for interactive Out of Home?

Nowadays, there is an array of digital technologies beyond the web, such as smartphones and tablets and social platforms like Twitter and Facebook. These new connected platforms and devices are enabling both consumers and brands to have deeper and more rewarding conversations.

As consumers divide their time between many different activities, brand owners now have to work harder to create an ongoing relationship. Brands are constantly looking to discover new ways to satisfy consumer demands and interests in order to improve the advertising experience.

Finding new ways of reaching, informing and entertaining audiences through Out of Home advertising is no different. Interaction via Out of Home formats combines the very best in audience delivery methods with the creative opportunities that large, public blank canvas’ can provide.

Out of Home advertising has benefited from an explosion of relevant interactive technologies from Quick Read (QR) codes to Near Field Communication (NFC), further enhancing what has always been an essentially interactive medium. Technologies such as Augmented Reality (AR) are also allowing advertisers to experiment with traditional billboards and to think about using Out of Home in different and more creative ways.

You will see from the insights contained within this report that interactivity is taking many forms and that smart devices in particular are unlocking the potential, however, our definition extends beyond new technologies and includes anything that invites the consumer to ‘get involved’ and interact.

As this report finds, a successfully activated interactive Out of Home campaign is one that targets audiences at the right time, with the right technology whilst offering consumers the right rewards for engaging with a brand.

WHAT IS INTERACTIVE ADVERTISING?The marketing applications for interactive advertising are evolving as rapidly as the technologies themselves. The worldwide web originally offered something that many other platforms initially could not easily compete with, the ability to provide an instant, consumer initiated conversation with a brand with little more than a mouse click.

SUN

2Interactive Europe What is interactive advertising?

3Interactive Europe What is interactive advertising?

4Interactive Europe 1. Out of Home – a mass medium

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

SECTION 01

OUT OF HOMEA MASS MEDIUM

5Interactive Europe 1. Out of Home – a mass medium

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

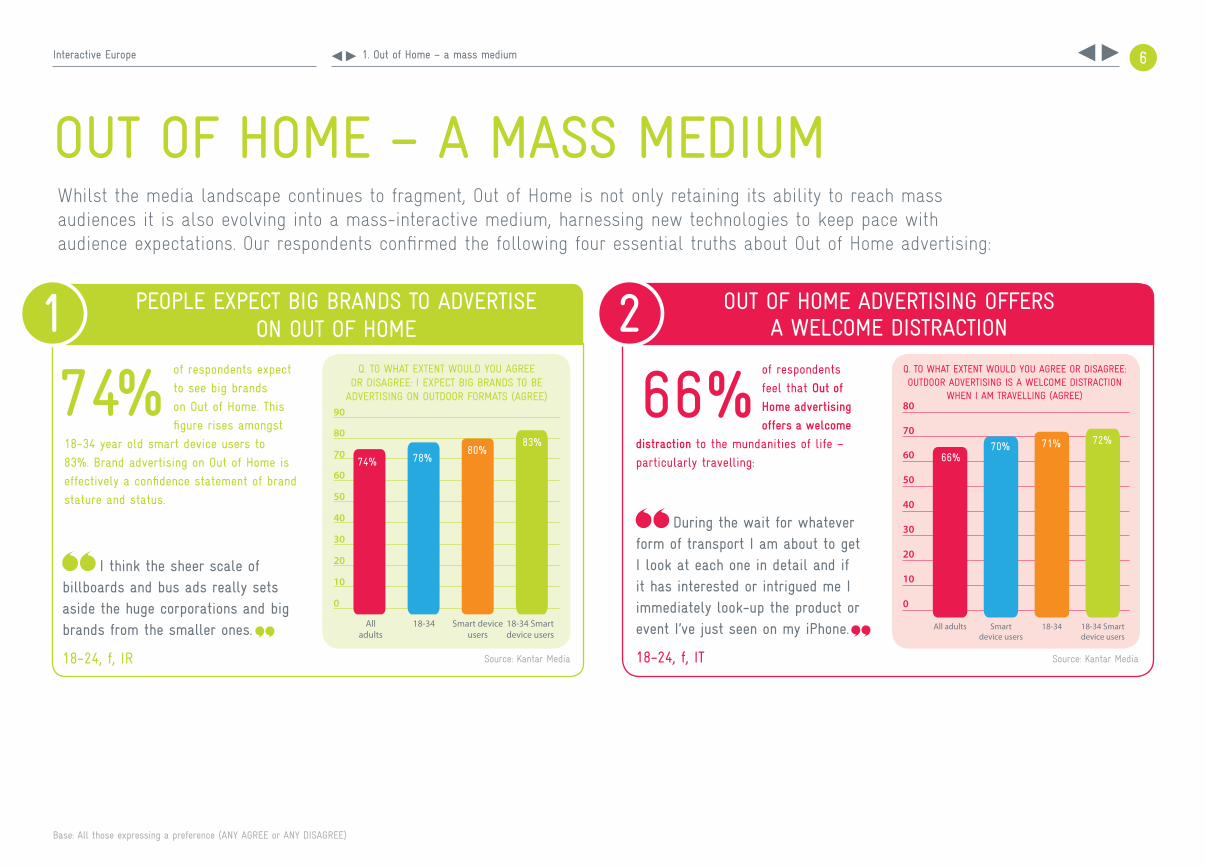

During the wait for whatever form of transport I am about to get I look at each one in detail and if it has interested or intrigued me I immediately look-up the product or event I’ve just seen on my iPhone.

18-24, f, IT

I think the sheer scale of billboards and bus ads really sets aside the huge corporations and big brands from the smaller ones.

18-24, f, IR

OUT OF HOME – A MASS MEDIUMWhilst the media landscape continues to fragment, Out of Home is not only retaining its ability to reach mass audiences it is also evolving into a mass-interactive medium, harnessing new technologies to keep pace with audience expectations. Our respondents confirmed the following four essential truths about Out of Home advertising:

21

74%of respondents expect to see big brands on Out of Home. This figure rises amongst

18-34 year old smart device users to 83%. Brand advertising on Out of Home is effectively a confidence statement of brand stature and status.

of respondents feel that Out of

Home advertising

offers a welcome

distraction to the mundanities of life – particularly travelling:

0

10

20

30

40

70

50

80

60

All adults Smart device users

18-34 Smart device users

18-34

66%70% 71% 72%

PEOPLE EXPECT BIG BRANDS TO ADVERTISE ON OUT OF HOME

OUT OF HOME ADVERTISING OFFERS A WELCOME DISTRACTION

0

10

20

30

40

70

50

80

60

All adults

18-34 18-34 Smart device users

Smart device users

74% 78%80%

Q. TO WHAT EXTENT WOULD YOU AGREE OR DISAGREE: I EXPECT BIG BRANDS TO BE

ADVERTISING ON OUTDOOR FORMATS (AGREE) 90

83%

66%Q. TO WHAT EXTENT WOULD YOU AGREE OR DISAGREE: OUTDOOR ADVERTISING IS A WELCOME DISTRACTION

WHEN I AM TRAVELLING (AGREE)

Source: Kantar Media Source: Kantar Media

6Interactive Europe 1. Out of Home – a mass medium

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

3

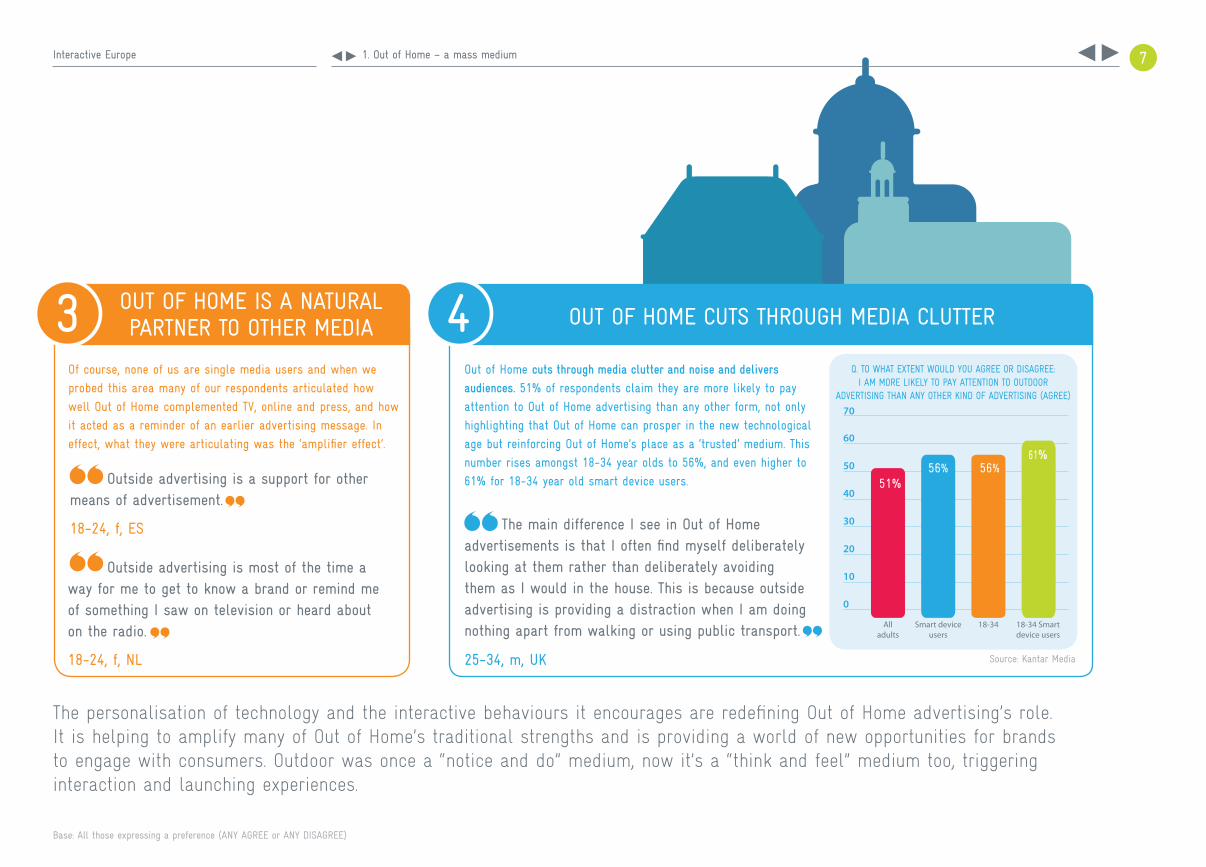

Outside advertising is a support for other means of advertisement.

18-24, f, ES

Outside advertising is most of the time a way for me to get to know a brand or remind me of something I saw on television or heard about on the radio.

18-24, f, NL

The personalisation of technology and the interactive behaviours it encourages are redefining Out of Home advertising’s role. It is helping to amplify many of Out of Home’s traditional strengths and is providing a world of new opportunities for brands to engage with consumers. Outdoor was once a “notice and do” medium, now it’s a “think and feel” medium too, triggering interaction and launching experiences.

Out of Home cuts through media clutter and noise and delivers

audiences. 51% of respondents claim they are more likely to pay attention to Out of Home advertising than any other form, not only highlighting that Out of Home can prosper in the new technological age but reinforcing Out of Home’s place as a ‘trusted’ medium. This number rises amongst 18-34 year olds to 56%, and even higher to 61% for 18-34 year old smart device users.

Of course, none of us are single media users and when we probed this area many of our respondents articulated how well Out of Home complemented TV, online and press, and how it acted as a reminder of an earlier advertising message. In effect, what they were articulating was the ‘amplifier effect’.

The main difference I see in Out of Home advertisements is that I often find myself deliberately looking at them rather than deliberately avoiding them as I would in the house. This is because outside advertising is providing a distraction when I am doing nothing apart from walking or using public transport.

25-34, m, UK

OUT OF HOME IS A NATURAL PARTNER TO OTHER MEDIA OUT OF HOME CUTS THROUGH MEDIA CLUTTER

0

10

20

30

40

70

50

60

All adults

Smart device users

18-34 Smart device users

18-34

51%56% 56%

61%

Q. TO WHAT EXTENT WOULD YOU AGREE OR DISAGREE:I AM MORE LIKELY TO PAY ATTENTION TO OUTDOOR

ADVERTISING THAN ANY OTHER KIND OF ADVERTISING (AGREE)

4

Source: Kantar Media

7Interactive Europe 1. Out of Home – a mass medium

8Interactive Europe 2. Do I need to worry about this now?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

SECTION 02

DO I NEED TO WORRY ABOUT THIS NOW?

9Interactive Europe 2. Do I need to worry about this now?

DO I NEED TO WORRY ABOUT THIS NOW?

Digital tools like YouTube, Twitter and blogs have enabled the public to become content creators, rather than passive consumers.

In response, more and more advertisers are inviting consumers to get involved with their campaigns through incentivisation and participation and are already using interactive mechanisms in all forms of advertising.

The mass use of smart mobile devices and the essential need to be connected to the online world is bringing added strength to the Out of Home medium. Mobile devices are rapidly becoming the dominant digital format versus desk bound machines. Gartner forecasts 104 million tablets will be sold worldwide in 2012. By 2015, sales are forecast to rise to 326 million units, surpassing the number of laptops sold annually. Over the same period of time, smartphone sales will have risen from 450 million a year to 1.1 billion.

In a word, yes. The media landscape has changed significantly in the last decade and the pace of change is accelerating. Advertisers’ concerns about fragmenting audiences have been intensified by the multitude of platforms now available for people to watch, read, listen and take-part in.

And why is this important and relevant? Well, as we know from Exterion Media’s “Europe on the Move” 2011 study www.europeonthemove.com, people are not only using their smart devices to go online and search as a consequence of seeing an Out of Home ad, interactivity is also one of the many ways that advertisers can fulfil audience expectations and stimulate imaginations.

Interactivity on Out of Home campaigns allows brands to make an emotional connection with the consumer in a public space and at a time when consumer action is possible.

Smartphone and tablet owners represent 56% of the population surveyed. The smart device audience is younger and more male than average, with 64% of 18-24 year olds and 60% of men owning a smart device.

The smart device audience accounts for at least half the Out of Home audience in every European market surveyed, with penetration highest in the UK.

64%UK

57%SPAIN NETHERLANDS

56%

54%IRELAND

53%ITALY

50%FRANCE

WHO ARE SMART DEVICE USERS?

Source: Kantar MediaBase: All respondents

10Interactive Europe 2. Do I need to worry about this now?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)Base: All those expressing a preference

WHAT ARE PEOPLE USING THEIR SMARTPHONES/ TABLETS FOR?

Smart device owners are taking full advantage of the technology at their fingertips and are spending their time out of home accessing the internet. It would appear that all smart device users, especially younger groups (18-34), have a hunger for information and a need to be entertained. Accessing the internet (80%), using social networks (67%) and playing games (53%) are among the top functions used on smart devices.

Perhaps unsurprisingly, younger audiences are more open to interaction. They instinctively understand the relationship between brand custodians and themselves and are willing participants in the brand/consumer relationship. They can act as trend setters for campaigns and help to amplify messages via their social networks. And while they may not be able to predict the future, they can give us insights into what they like and what they are prepared to use and do.

Source: Kantar MediaBase: All those expressing a preference

Accessing the internet

Using social networks

Taking photographs/or shooting videos

Listening to music

Conducting an online search

Playing games

Downloading apps

Instant Messaging (eg BBM)

Watching video content

Uploading photos

Making a purchase

Other

Smartphone/tablet users 18-34 year oldsSmartphone/tablet users 35-55 year olds

8074

6748

6453

5346

6460

5341

5444

5344

28

38

35

19

4

27

26

15

8

SMART DEVICE OWNERS MAKE FULL USE OF THE TECHNOLOGY WHILE OUT OF THE HOME

Q. YOU SAY YOU OWN A SMARTPHONE OR TABLET DEVICE, WHICH OF THE FOLLOWING HAVE YOU USED YOUR DEVICE FOR IN THE PAST WEEK?

40

11Interactive Europe 2. Do I need to worry about this now?

MAKING PURCHASES

As well as going online to find out more information about the ads they are seeing, smart device users are more open to making purchases through their mobile devices.

Here you see that 53% of all respondents agree with the statement ‘mobile technology allows me to make purchases more easily’ – compared to 68% of smart device users. The numbers rise when we analyse the numbers for Early Adopters (people who agree with the statement “I like to buy gadgets as soon as they come out”) and Technology Advocates (“I like telling other people about new technologies”) and it is these audiences in particular we can look to to identify future trends.

0

10

20

30

40

70

80

90

50

60

All adults Smart device users Early adoptersTech advocates

53%

68%

74%

86%

MOBILE TECHNOLOGY ALLOWS PEOPLE TO MAKE

PURCHASES MORE EASILY WHEN OUT AND ABOUT

Q. TO WHAT EXTENT WOULD YOU AGREE OR DISAGREE: MOBILE TECHNOLOGY ALLOWS ME TO MAKE PURCHASES

EASIER WHEN OUT AND ABOUT (AGREE)

All figures represent the percentage of respondents who expressed an opinion

I use QR codes that I find on posters that directly link me to the event or the website. I have used twitter to try and win products that were advertised on billboards. I have also used deal apps etc. I think nearly every product or service could integrate social media into their campaigns and make their message interactive.

18-24, f, IR

So, what are the implications for brands considering interactive Out of Home? Well, the media savvy consumer welcomes it.

of smart device users would feel more positive about a brand that invites interaction. 71%

Source: Kantar MediaBase: All those expressing a preference (ANY AGREE or ANY DISAGREE)

12Interactive Europe 2. Do I need to worry about this now?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

RECEPTIVE AUDIENCE

While the media landscape has changed so too has the “path to purchase” as we knew it. The changes in lifestyles and the ways in which people have embraced technology have fundamentally changed the traditional media model.

People drop in and out of “shopper mode” no matter where they are in their daily journey, facilitated by their smartphone or tablet. In fact, 74% of smart device users have taken some sort of action as a direct response to an Out of Home advertising campaign, outperforming non-users in every response category, even those in which smart device technology is not an important enabler. Most strikingly, smart device owners are more likely to think about brands after having seen an Outdoor advert, suggesting that this group is more attuned and receptive to interacting with brands outdoors.

Technology Advocates, who are crucial in increasing awareness of interactive possibilities, show an even higher response rate of 83%.

Q. THINKING ABOUT WHEN YOU ARE OUT OF THE HOME, WHICH OF THE FOLLOWING HAVE YOU EVER USED YOUR SMART DEVICE TO DO?

Source: Kantar MediaBase: All urban audiences; Technology Advocates

(3.934) Smart device users (5,051)

Went online to get more information

39%32%

33%27%

Mentioned/spoke to someone

about it

32%29%Thought about it

26%22%

Went somewhere

32%28%

Considered buying the product

23%20%

Bought a product

28%22%

Sought more information

18%17%

Went online to buy product

16%15%

Responded to a special offer

Technology AdvocatesSmart device users

13Interactive Europe 2. Do I need to worry about this now?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

NIKE ‘#MAKE IT COUNT’ CAMPAIGNNike is a great example of a brand embracing interaction. January 2012 marked the beginning of a very important year, not just for the cream of the sporting crop but for everyone. To celebrate Nike launched a campaign which saw top UK athletes make their pledges for the forthcoming year whilst inspiring people to make their own pledges under the hashtag #makeitcount and be part of the movement.

14Interactive Europe 2. Do I need to worry about this now?

Portraits of Nike-sponsored athletes appeared across Exterion Media’s 100 LCD digital screens at Westfield Stratford City London retail mall, while the athletes’ own handwriting brought to life their personal pledge. The athlete’s twitter handle sat on the execution along with the “Make It Count” hashtag to encourage online participation. Photographed by top photographer Adam Hinton, the campaign featured action portraits in posters, press and online.

The campaign ran across a multitude of digital Out of Home formats, on roadside, underground and at Westfield, in proximity to Nike stores. Large-scale impactful sites were used to inspire Londoners to pledge, including banners, bus mega-rears and mega 6 sheets. Cover-wraps also ran on Metro and Sport

newspapers, the latter made interactive through Blippar’s interactive mobile and tablet app.

In addition, the campaign featured a digital in-store experience starring members of the public at the flagship Nike stores in Oxford Street and Westfield Stratford City London. Shoppers were photographed alongside their handwritten “Make it Count” pledges to create bespoke Nike portraits in the style of the elite athlete posters which were displayed onscreen around the stores. At Westfield Stratford, in an exclusive partnership with Exterion Media, shoppers’ pledges were also broadcast on a number of digital screens across the retail centre. In total 280 people had their pledge messages displayed on LCDs and #makeitcount has been tweeted over 64,000 times to date.

Nick Ashley, Partner and Head of Client Leadership at Mindshare, explains, “Nike have always been at the forefront of developments in digital outdoor. We are delighted to have collaborated with Exterion Media to have delivered another first where London shoppers can see their individual pledges broadcast to thousands of other shoppers in real-time. If that’s not an incentive to keep your commitment, I don’t know what is. Outdoor neatly complemented the other media choices with its ability to drive rapid cover and awareness. And because of the stature of the chosen formats, they were instrumental in facilitating conversations, involvement and 2012 pledges from the public, both in-situ and also via their social networks”.

Ultimately interactive Out of Home enables marketers to get consumers involved in brands in ways they would not traditionally have been able to do. It puts the consumer in the driving seat, giving them the control that their smart devices offer. With the right incentive, consumers spend longer discovering brands for themselves which in turn ensures a more vested interest in products and services, promotes brand loyalty and continuously attracts new consumers to the category. The Out of Home interaction makes consumers feel more positively about a brand and can re-introduce fun to the equation.

15Interactive Europe 2. Do I need to worry about this now?

16Interactive Europe 3. What does the audience think about interactive Out of Home?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

WHAT DOES THE AUDIENCE THINK ABOUT INTERACTIVE OUT OF HOME?

SECTION 03

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

17Interactive Europe 3. What does the audience think about interactive Out of Home?

Base: All those expressing a preference

WHAT DOES THE AUDIENCE THINK ABOUT INTERACTIVE OUT OF HOME?

This is an audience bombarded with a proliferation of media channels and platforms – television, radio, press and internet. But, as they spend so much time out of the home it is outdoor advertising that reaches them while they are energetic, stimulated and on the path to purchase.

In line with previous studies, our respondents told us that the public nature of Out of Home makes ads more difficult to avoid, but that its less intrusive nature means it’s more accepted. Throughout, respondents’ expressed the notion that brands that use Out of Home are showing consumers more respect by not intruding on them.

They also told us that Out of Home reaches them when they are in the right frame of mind to be influenced by ads - when out and about (42% think about products they need to buy when Out of Home).

The outdoor audience are the people brands and advertisers want to reach – a highly mobile group who are technologically savvy, high income earners and interested in what brands have to offer. They are socially informed, on trend and consequently more receptive to brand messages and interacting with advertising.

I always feel billboards and buses are a great way to advertise. They are larger than life and very striking and eye catching. 25-34, f UK

Outdoor advertising allows us to “choose” the moment in which we want to receive information about the different brands and products of the advertisers. In this sense, perhaps this type of “street” advertising causes me more “friendliness”, a good advertising campaign in the street makes me remember it. 18-24, m ES

18Interactive Europe 3. What does the audience think about interactive Out of Home?

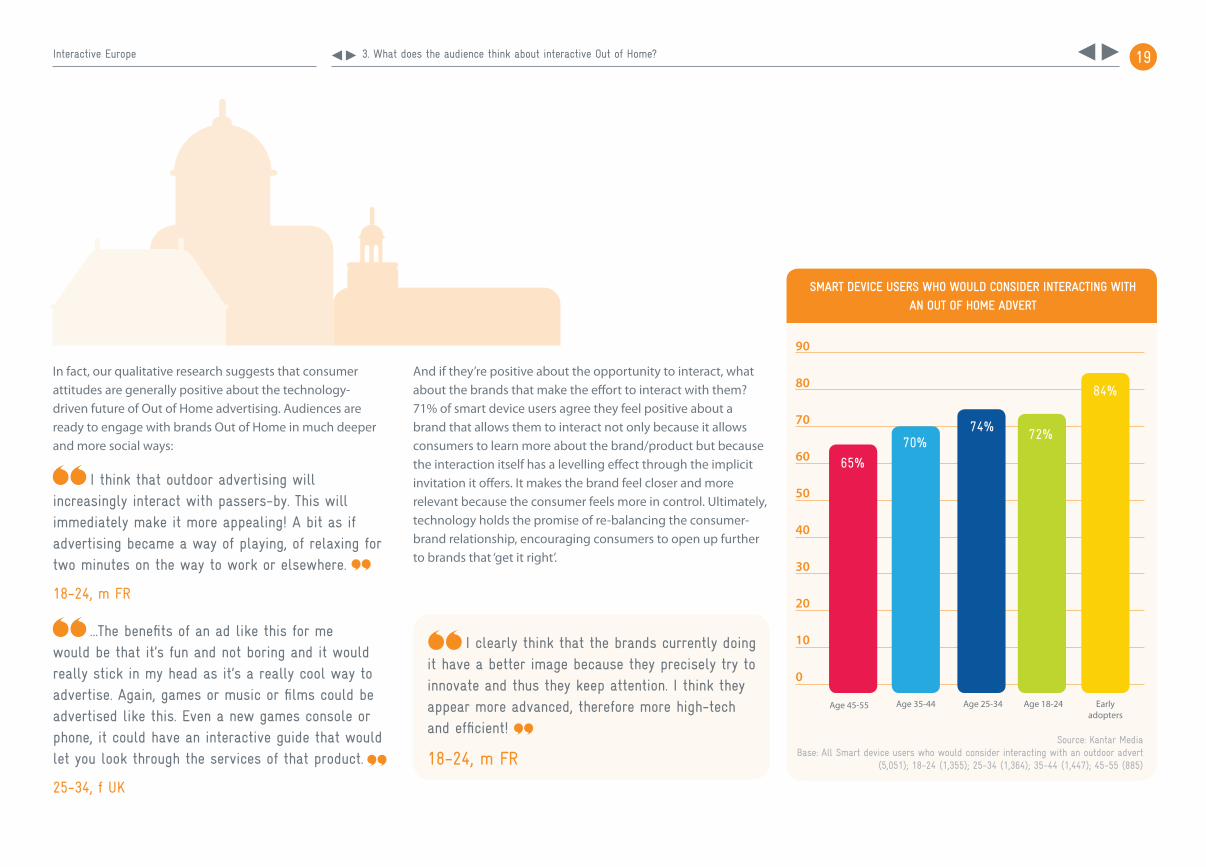

In fact, our qualitative research suggests that consumer attitudes are generally positive about the technology-driven future of Out of Home advertising. Audiences are ready to engage with brands Out of Home in much deeper and more social ways:

I think that outdoor advertising will increasingly interact with passers-by. This will immediately make it more appealing! A bit as if advertising became a way of playing, of relaxing for two minutes on the way to work or elsewhere.

18-24, m FR

…The benefits of an ad like this for me would be that it’s fun and not boring and it would really stick in my head as it’s a really cool way to advertise. Again, games or music or films could be advertised like this. Even a new games console or phone, it could have an interactive guide that would let you look through the services of that product.

25-34, f UK

0

10

20

30

40

70

80

90

50

60

Age 45-55 Age 35-44 Age 18-24Age 25-34 Early adopters

SMART DEVICE USERS WHO WOULD CONSIDER INTERACTING WITH

AN OUT OF HOME ADVERT

65%

70%72%74%

84%

And if they’re positive about the opportunity to interact, what about the brands that make the effort to interact with them? 71% of smart device users agree they feel positive about a brand that allows them to interact not only because it allows consumers to learn more about the brand/product but because the interaction itself has a levelling effect through the implicit invitation it offers. It makes the brand feel closer and more relevant because the consumer feels more in control. Ultimately, technology holds the promise of re-balancing the consumer-brand relationship, encouraging consumers to open up further to brands that ‘get it right’.

I clearly think that the brands currently doing it have a better image because they precisely try to innovate and thus they keep attention. I think they appear more advanced, therefore more high-tech and efficient!

18-24, m FRSource: Kantar Media

Base: All Smart device users who would consider interacting with an outdoor advert (5,051); 18-24 (1,355); 25-34 (1,364); 35-44 (1,447); 45-55 (885)

19Interactive Europe 3. What does the audience think about interactive Out of Home?

On QR Codes: I tried to scan one because it caught my attention and I found it interesting, but it didn’t work, I don’t know whether because of the incompatibility of my phone or my lack of skill but I was pretty frustrated.

25-34, f ES

BUT DON’T LET THEM DOWN

Brands have to deliver on the expectations they generate. Our respondents were very clear; if you provoke their curiosity, you had better not let them down! Our study found that if people are persuaded to interact and are not sufficiently rewarded, the effect can be negative.

Time and time again our respondents fed back that in order to utilise interactive Out of Home to its full potential, not only must the activity resonate with the overall brand or campaign message it must also give the participant something of value.

Asking consumers to find out about a brand, product or service by providing them with a QR Code, web link or NFC tag is only half the journey. In other words, a simple link to the company website is not going to achieve the level of engagement that may have been anticipated and could in fact be counterproductive!

Those brands that have managed to follow some simple rules (see Nike case study pages 14-15) have gone far beyond simply facilitating interaction. They have managed to prompt engagement through a suitable incentive and have also extended the user’s brand journey which in turn offers a more rewarding and immersive relationship for both brand and consumer. The main message from our respondents was – What’s In It For

Me? What pay-off do I get from interacting with ads? What is the consumer benefit?

I don’t think I would interact with a commercial soon or often. Because there is not a real win-win situation, what do I get out of it? If I want to know more it is just as easy to go online and search it myself.

18-24, f NL

20Interactive Europe 3. What does the audience think about interactive Out of Home?

And the benefits of successful engagement are clear – brands that do it right will reap the rewards. For example, 55%1 of all respondents with a social media profile have used social media to share information about promotions or offers whilst Out of Home. 74%2 of Early Adopters (who have a social media profile and are smart device users) shared promotions with their friends strongly indicating that this type of behaviour is only set to continue.

Based on our qualitative discussions with respondents, we have identified two core incentives that should be considered by brands looking not only to inspire consumers to take that initial step to interact but also to continue to engage with the brand beyond simple fact finding and data retrieval:

The brand advertised this way would win a lot of points in my eyes, because it shows that it is innovative, up-to-date, fun... And the fact that they offer a touch screen game like this, which get people very hooked, would make me have a very positive image of the advertised brand and product.

25-34, f ES

2 consumers benefit from an experience eg a game or video/music content

ENTERTAINMENT VALUE

I like the idea of scanning in to win something or to access something exclusive to those aware enough to do so.

25-34, f ES

I have scanned QR codes before for restaurants or shops! I scanned them to get my bearings …If by scanning a QR code, I can get a discount or access special offers, I would indeed be interested to scan them.

25-34, f ES

1 consumers benefit from promotions or discountsMONETARY VALUE

1. All who have a social media profile (6,710). 2. All who are Early Adopters have a social media profile and have a smart device (1,302)

21Interactive Europe 3. What does the audience think about interactive Out of Home?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

SHAKING-UP THE HAPPINESS WITH COKE

22Interactive Europe 3. What does the audience think about interactive Out of Home?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

The future of communication is moving at break-neck speed, there is an explosion of channels and it is still growing at a phenomenal pace. Consumers are well and truly overloaded. They don’t have time for irrelevant and complex messages from brands. It doesn’t matter what the channel, we need to keep the message simple, engaging and involving if we are to win their hearts and minds. The findings from Exterion Media’s Interactive Europe survey reinforce all of these core messages which we intuitively know to be true, we’ve all experienced the gimmicks, the ideas that make it far too difficult to bother taking the message and lack of relevance. The case for the power of outdoor is well and truly made and understood, but what we’re still learning is where and how to maximise adding technology, QR Codes, Facebook and Twitter to capitalise on the

consumers wish to find out more, engage more and deepen brand relevance.

In Ireland, Coca-Cola are hooked on the power of outdoor and invest heavily in the medium across multiple formats. However, what was truly innovative was the outdoor campaign Coca-Cola ran to bring to life the holiday season for the brand over Christmas. They undertook a major brand generosity initiative and dispensed 50,000 ‘free’ cans of Coke using 6 sheet mini can dispensers across key shopping centre locations. All the consumer had to do was wave their hand across the dispenser to get a free can of Coke. It was a terrific initiative that really utilised the power of engagement using outdoor.

We’ve already heard that consumers think positively about brands that make an effort to interact with them, so long as the incentive is clear. Coca-Cola is one such brand that recently launched a successful interactive campaign with Exterion Media in Dublin. Orliath Blaney explains more:

Orlaith Blaney, CEO, McCann Erickson, Ireland

23Interactive Europe 3. What does the audience think about interactive Out of Home?

24Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

WHAT ARE THE TECHNOLOGIES TO FOCUS ON AND THE PITFALLS TO AVOID?

SECTION 04

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

25Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

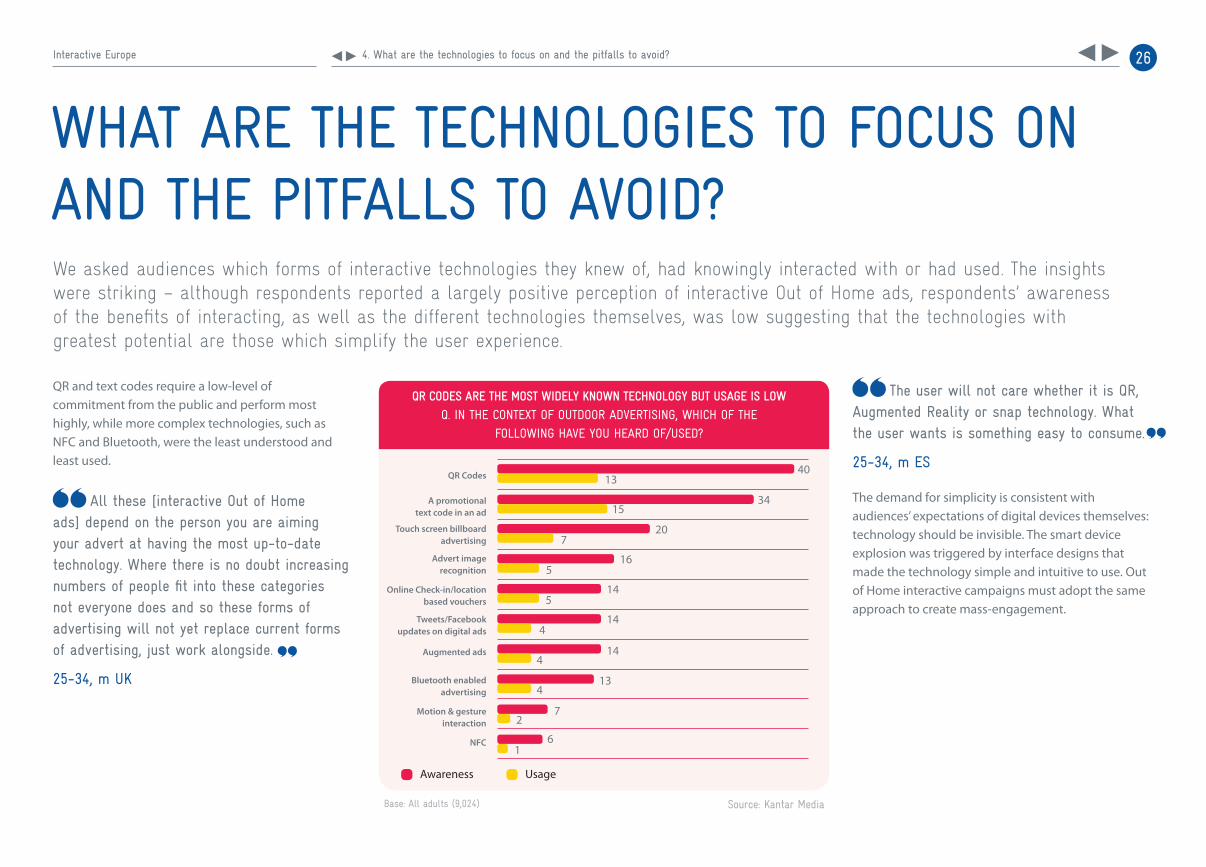

We asked audiences which forms of interactive technologies they knew of, had knowingly interacted with or had used. The insights were striking – although respondents reported a largely positive perception of interactive Out of Home ads, respondents’ awareness of the benefits of interacting, as well as the different technologies themselves, was low suggesting that the technologies with greatest potential are those which simplify the user experience.

All these [interactive Out of Home ads] depend on the person you are aiming your advert at having the most up-to-date technology. Where there is no doubt increasing numbers of people fit into these categories not everyone does and so these forms of advertising will not yet replace current forms of advertising, just work alongside.

25-34, m UK

The user will not care whether it is QR, Augmented Reality or snap technology. What the user wants is something easy to consume.

25-34, m ES

QR and text codes require a low-level of commitment from the public and perform most highly, while more complex technologies, such as NFC and Bluetooth, were the least understood and least used.

The demand for simplicity is consistent with audiences’ expectations of digital devices themselves: technology should be invisible. The smart device explosion was triggered by interface designs that made the technology simple and intuitive to use. Out of Home interactive campaigns must adopt the same approach to create mass-engagement.

WHAT ARE THE TECHNOLOGIES TO FOCUS ON AND THE PITFALLS TO AVOID?

26Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

Base: All adults (9,024) Source: Kantar Media

QR Codes

A promotional text code in an ad

Touch screen billboard advertising

Advert image recognition

Online Check-in/location based vouchers

Tweets/Facebook updates on digital ads

Augmented ads

Bluetooth enabled advertising

Motion & gesture interaction

NFC

Awareness Usage

4013

3415

207

144

165

144

145

134

2

61

QR CODES ARE THE MOST WIDELY KNOWN TECHNOLOGY BUT USAGE IS LOW

Q. IN THE CONTEXT OF OUTDOOR ADVERTISING, WHICH OF THE FOLLOWING HAVE YOU HEARD OF/USED?

7

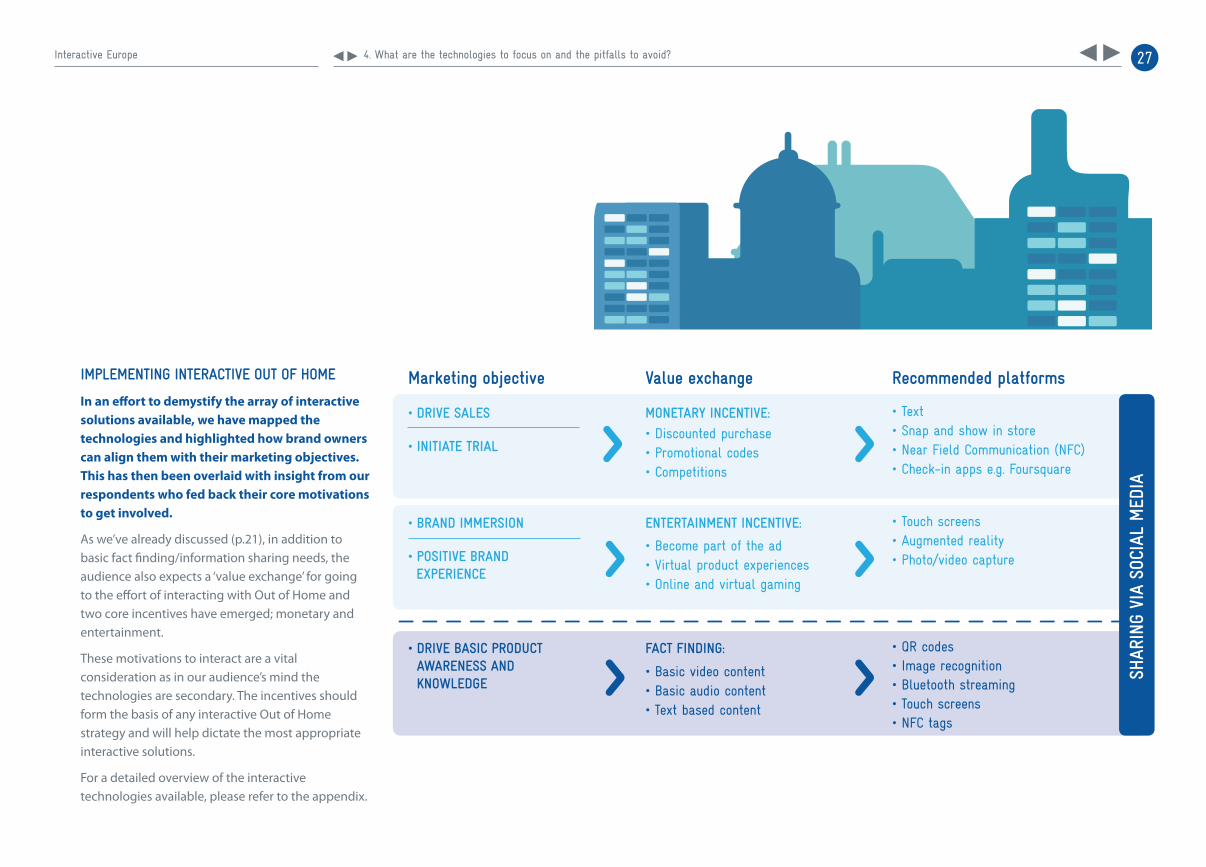

IMPLEMENTING INTERACTIVE OUT OF HOME

In an effort to demystify the array of interactive solutions available, we have mapped the technologies and highlighted how brand owners can align them with their marketing objectives. This has then been overlaid with insight from our respondents who fed back their core motivations to get involved.

As we’ve already discussed (p.21), in addition to basic fact finding/information sharing needs, the audience also expects a ‘value exchange’ for going to the effort of interacting with Out of Home and two core incentives have emerged; monetary and entertainment.

These motivations to interact are a vital consideration as in our audience’s mind the technologies are secondary. The incentives should form the basis of any interactive Out of Home strategy and will help dictate the most appropriate interactive solutions.

For a detailed overview of the interactive technologies available, please refer to the appendix.

MONETARY INCENTIVE:

ENTERTAINMENT INCENTIVE:

FACT FINDING:

• DRIVE SALES

• INITIATE TRIAL

• Become part of the ad• Virtual product experiences• Online and virtual gaming

• Basic video content• Basic audio content• Text based content

• BRAND IMMERSION

• POSITIVE BRAND EXPERIENCE

• DRIVE BASIC PRODUCT AWARENESS AND KNOWLEDGE

• Discounted purchase• Promotional codes• Competitions

Marketing objective Value exchange

• Touch screens • Augmented reality• Photo/video capture

• QR codes• Image recognition• Bluetooth streaming• Touch screens• NFC tags

• Text• Snap and show in store • Near Field Communication (NFC)• Check-in apps e.g. Foursquare

Recommended platforms

SHAR

ING

VIA

SOCI

AL M

EDIA

27Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

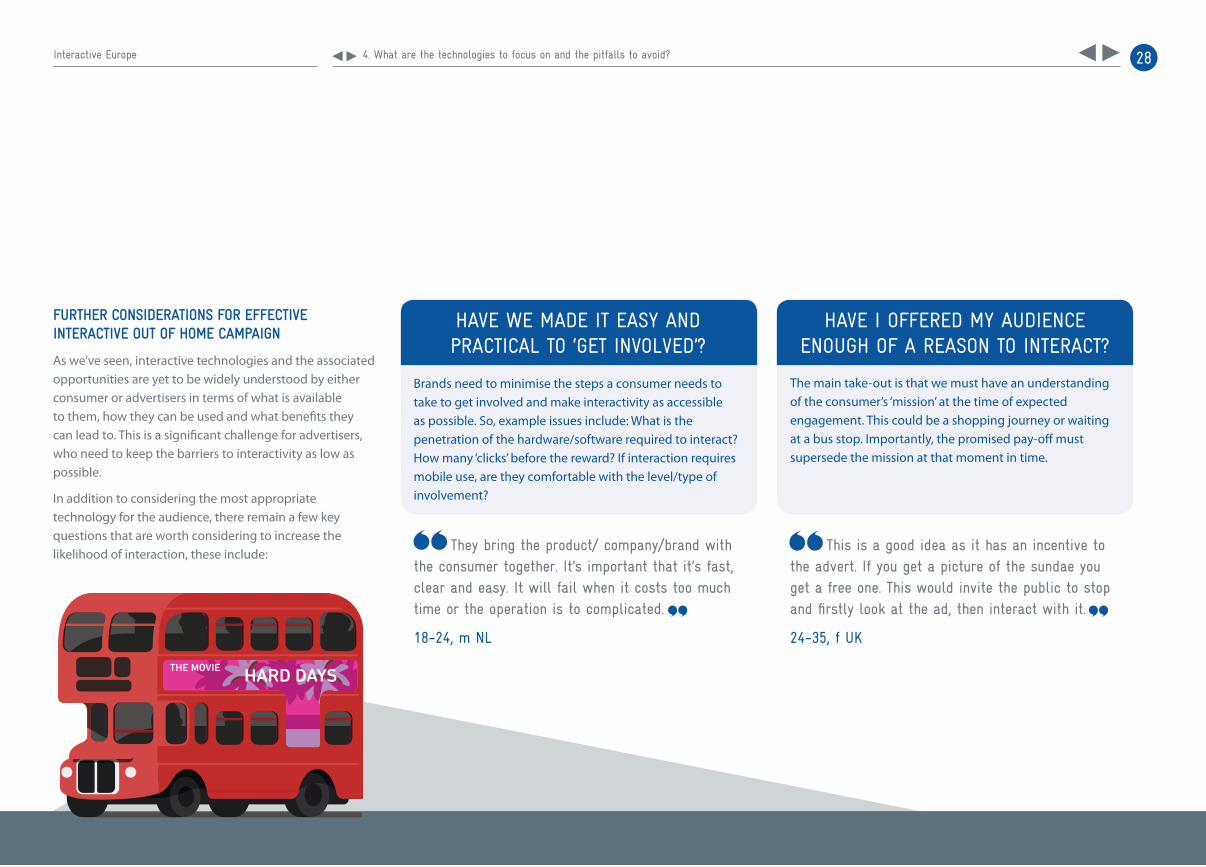

FURTHER CONSIDERATIONS FOR EFFECTIVE INTERACTIVE OUT OF HOME CAMPAIGN

As we’ve seen, interactive technologies and the associated opportunities are yet to be widely understood by either consumer or advertisers in terms of what is available to them, how they can be used and what benefits they can lead to. This is a significant challenge for advertisers, who need to keep the barriers to interactivity as low as possible.

In addition to considering the most appropriate technology for the audience, there remain a few key questions that are worth considering to increase the likelihood of interaction, these include:

They bring the product/ company/brand with the consumer together. It’s important that it’s fast, clear and easy. It will fail when it costs too much time or the operation is to complicated.

18-24, m NL

This is a good idea as it has an incentive to the advert. If you get a picture of the sundae you get a free one. This would invite the public to stop and firstly look at the ad, then interact with it.

24-35, f UK

Brands need to minimise the steps a consumer needs to take to get involved and make interactivity as accessible as possible. So, example issues include: What is the penetration of the hardware/software required to interact? How many ‘clicks’ before the reward? If interaction requires mobile use, are they comfortable with the level/type of involvement?

HAVE WE MADE IT EASY AND PRACTICAL TO ‘GET INVOLVED’?

The main take-out is that we must have an understanding of the consumer’s ‘mission’ at the time of expected engagement. This could be a shopping journey or waiting at a bus stop. Importantly, the promised pay-off must supersede the mission at that moment in time.

HAVE I OFFERED MY AUDIENCE ENOUGH OF A REASON TO INTERACT?

28Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

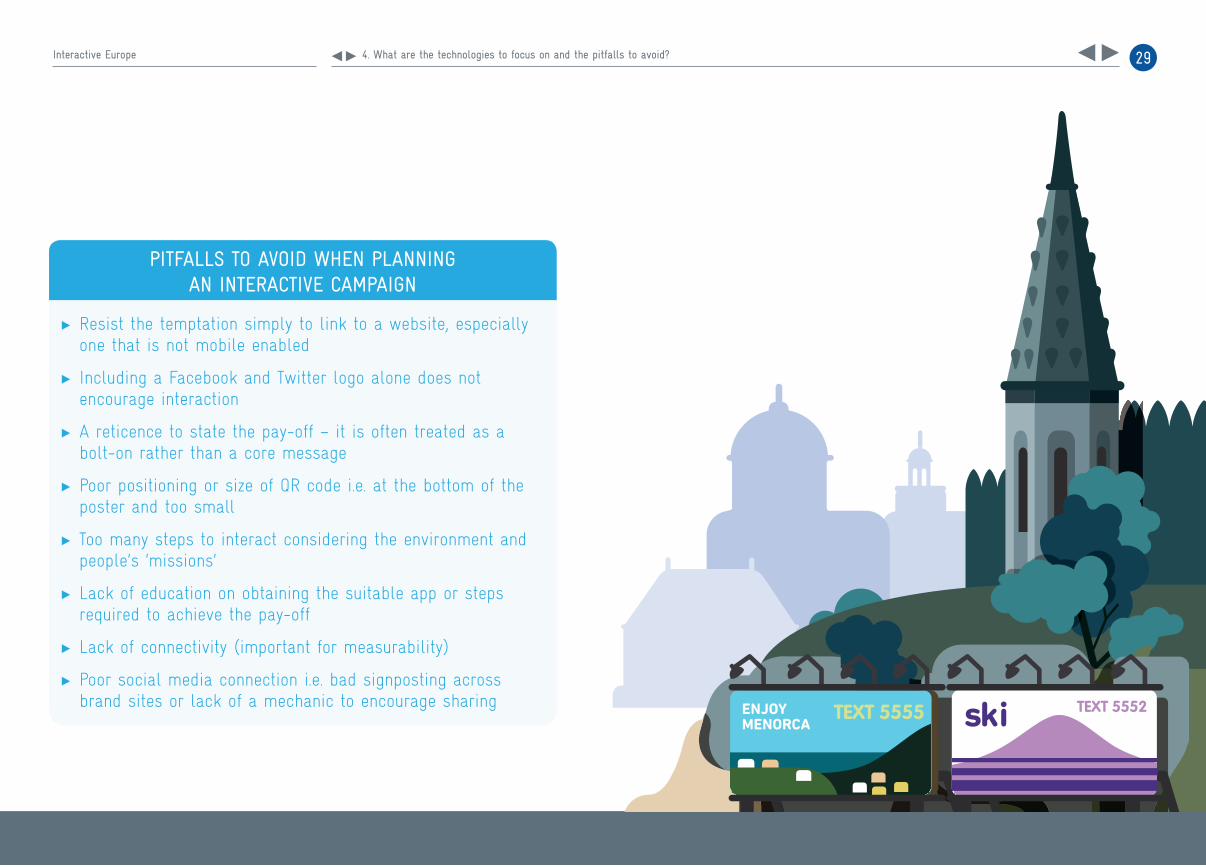

PITFALLS TO AVOID WHEN PLANNING AN INTERACTIVE CAMPAIGN

Resist the temptation simply to link to a website, especially one that is not mobile enabled

Including a Facebook and Twitter logo alone does not encourage interaction

A reticence to state the pay-off – it is often treated as a bolt-on rather than a core message

Poor positioning or size of QR code i.e. at the bottom of the poster and too small

Too many steps to interact considering the environment and people’s ‘missions’

Lack of education on obtaining the suitable app or steps required to achieve the pay-off

Lack of connectivity (important for measurability)

Poor social media connection i.e. bad signposting across brand sites or lack of a mechanic to encourage sharing

29Interactive Europe 4. What are the technologies to focus on and the pitfalls to avoid?

30Interactive Europe 5. How does this fit into my media mix?

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

143143

HOW DOES THIS FIT INTO MY MEDIA MIX?

SECTION 05

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

31Interactive Europe 5. How does this fit into my media mix?

HOW DOES THIS FIT INTO MY MEDIA MIX?

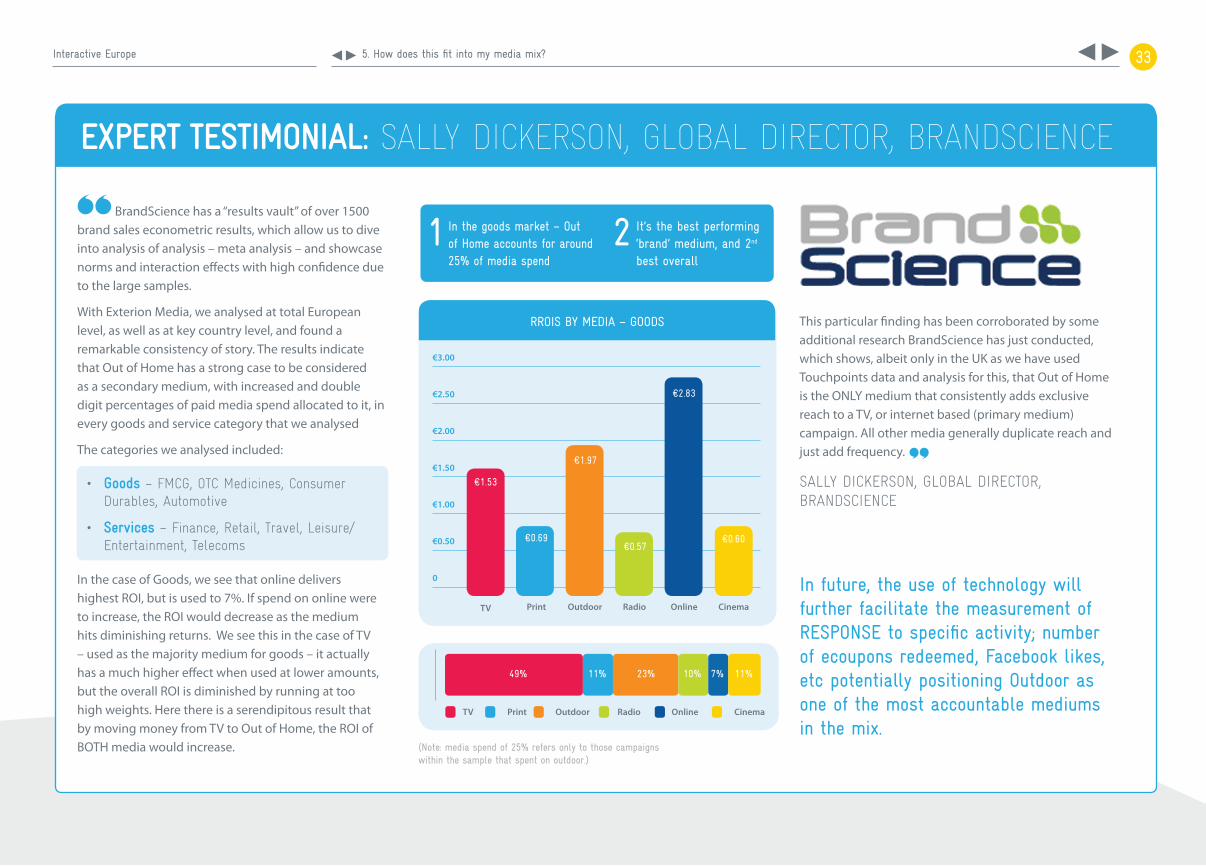

In 2011 Exterion Media conducted a meta analysis of previously conducted econometric studies that proved that Out of Home should be a significant part of an advertiser’s marketing mix to optimise ROI.

The study commissioned through BrandScience, Omnicom Media Group’s business and marketing effectiveness consultancy, proved the effectiveness of Out of Home advertising across Exterion Media’s European markets in delivering a return on investment. In the goods category, the study proved that Out of Home is the best performing ‘brand’ medium, and second best overall behind the Internet, so given the lead medium for goods is usually TV or press, the suggestion is that Out of Home should always be considered as a core secondary medium. For brands in the services category, Out of Home advertising is on a par with radio, press and cinema, only marginally behind TV and online.

Consumers have a very good understanding of power of outdoor advertising and the halo effect it can have on other forms of advertising for the same brand.

As the marketplace becomes ever more complex and competitive the need to maximise return on investment through efficient and effective marketing and advertising becomes increasingly critical.

Outdoor advertising makes me think of other ads I’ve seen, notably on TV, and that produces certain continuity, a bit like “brainwashing”. I know, it’s rather an extreme term but what I mean by that is that they keep banging on about the same things so that in the end you give in to temptation.

18-24, f FR

One Outdoor ad that did catch my eye though was the Gordon’s Gin ad that has Gordon Ramsay pouring the gin over his head. That made me smile because I love the TV advert!!

18-24, f UK

Outside ads are most of the time a way for me to get to know a brand or to remind me of something I saw on television or heard about on the radio.

18-24, f NL

32Interactive Europe 5. How does this fit into my media mix?

SALLY DICKERSON, GLOBAL DIRECTOR, BRANDSCIENCE

BrandScience has a “results vault” of over 1500 brand sales econometric results, which allow us to dive into analysis of analysis – meta analysis – and showcase norms and interaction effects with high confidence due to the large samples.

With Exterion Media, we analysed at total European level, as well as at key country level, and found a remarkable consistency of story. The results indicate that Out of Home has a strong case to be considered as a secondary medium, with increased and double digit percentages of paid media spend allocated to it, in every goods and service category that we analysed

The categories we analysed included:

• Goods – FMCG, OTC Medicines, Consumer Durables, Automotive

• Services – Finance, Retail, Travel, Leisure/Entertainment, Telecoms

In the case of Goods, we see that online delivers highest ROI, but is used to 7%. If spend on online were to increase, the ROI would decrease as the medium hits diminishing returns. We see this in the case of TV – used as the majority medium for goods – it actually has a much higher effect when used at lower amounts, but the overall ROI is diminished by running at too high weights. Here there is a serendipitous result that by moving money from TV to Out of Home, the ROI of BOTH media would increase.

This particular finding has been corroborated by some additional research BrandScience has just conducted, which shows, albeit only in the UK as we have used Touchpoints data and analysis for this, that Out of Home is the ONLY medium that consistently adds exclusive reach to a TV, or internet based (primary medium) campaign. All other media generally duplicate reach and just add frequency.

In future, the use of technology will further facilitate the measurement of RESPONSE to specific activity; number of ecoupons redeemed, Facebook likes, etc potentially positioning Outdoor as one of the most accountable mediums in the mix.

In the goods market – Out of Home accounts for around 25% of media spend

It’s the best performing ‘brand’ medium, and 2nd best overall

1 2

0

€0.50

€1.00

€1.50

€2.00

€2.50

€3.00

TV Print Radio Online CinemaOutdoor

€1.53

€0.69

€1.97

€0.57

€2.83

€0.60

(Note: media spend of 25% refers only to those campaigns within the sample that spent on outdoor.)

RROIS BY MEDIA – GOODS

Print Radio OnlineOutdoorTV Cinema

49% 11% 23% 10% 7% 11%

EXPERT TESTIMONIAL: SALLY DICKERSON, GLOBAL DIRECTOR, BRANDSCIENCE

33Interactive Europe 5. How does this fit into my media mix?

34Interactive Europe 6. Out of Home’s Interactive Future

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

OUT OF HOME’S INTERACTIVE FUTURE

SECTION 06

ForewordSection oneSection twoSection threeSection fourSection fiveSection sixConclusion

35Interactive Europe 6. Out of Home’s Interactive Future

OUT OF HOME’S INTERACTIVE FUTURE

The personalisation of technology and the interactive behaviours it encourages are redefining Out of Home advertising’s role. It is helping to amplify many of its traditional strengths and is providing a world of new opportunities for brands to engage with consumers.

Ultimately, however, audience power will determine the effectiveness of Out of Home and secure its place in the advertising mix. And there are three key factors driving this dynamic:

Ads on TV, I often skip them, they go on too long and they’re really there to push me to consume. On top of that, they arrive at a time when I’m with my family, and at that time I don’t want to remain stuck there for 15 minutes watching ads! In a magazine, it’s the same. If I buy magazines, it’s to read articles, not to look at advertising! Outdoors, advertising is less aggressive, more colourful, and if I don’t want to look at it, I just have to turn my head away.

25-34, f FR

As discussed earlier in this report media fragmentation and rapidly changing technologies have handed the power of choice to consumers. PVR technologies such as Sky+ make it possible for people to skip through whole TV ad breaks. It is this combined with a more expectant and demanding consumer that is challenging the traditional ‘push’ advertising model. Leading brands understand their advertising needs to work even harder to capture attention as well as offering a core benefit to consumers.

In this context Out of Home advertising will arguably play an even more important role as it is welcomed and more difficult to avoid. Indeed amongst key advertising targets such as the 18-34 age group 55% of those expressing a preference agreed that they were more likely to pay attention to Out of Home than any other form of advertising.

Outdoor has always complemented the likes of TV, online and press because of its ability to generate rapid awareness which in turn creates a ‘halo effect’ giving a brand greater stature, presence and therefore talk-ability.

THE BALANCE OF POWER1

1 A paradigm shift in the ‘balance of power’

2 The concept of invitation Vs intrusion

3 Out of Home complementary to social media

36Interactive Europe 6. Out of Home’s Interactive Future

When I am away from home, I believe that I am more receptive about a beautiful advertising than when I am at home in front of the TV or while I listen to the radio. It seems to be even and definitely less intrusive, because I am the one, who decides to dwell or not with it or to read something.

25-34, f IT

The main difference I see in Out of Home advertisements is that I often find myself deliberately looking at them rather than deliberately avoiding them as I would in the house. This is because outside advertising is not interrupting what I’m doing but providing a distraction when I am doing nothing but walking or using public transport.

25-34, m UK

It is questionable whether advertising that interrupts consumers can truly engage with them. Consumers told us that they are highly unlikely to stop watching a TV programme or reading a magazine to start interacting with an advertiser; the benefit would need to strongly outweigh the editorial content. However the welcome nature of Out of Home advertising is far more likely to elicit the desired response.

As our 2011 report ‘Europe on the Move’ showed, Outdoor audience behaviours and moods vary greatly, depending on the nature of the journey and time of the day. Advertisers that understand this tailor their messages accordingly and benefit from engagement with traditional creative treatments. If done correctly, including interactivity can only enhance this relationship.

INVITATION VS INTRUSION2

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

0

10

20

30

40

70

50

80

60

All adults Smart device users

18-34 Smart device users

18-34

66%70% 71% 72%

Q. TO WHAT EXTENT WOULD YOU AGREE OR DISAGREE: OUTDOOR ADVERTISING IS A WELCOME DISTRACTION WHEN I AM TRAVELLING (AGREE)

Source: Kantar Media

37Interactive Europe 6. Out of Home’s Interactive Future

Out of Home complementary to social media

Respondents are fundamentally receptive to the idea of advertising and brand interaction in a public environment. However, in the semi-public realm of social media, the role of brand advertising and engagement is still being negotiated between advertisers and users, as WPP CEO, Sir Martin Sorrell discussed in 2011:

I’m not sceptical about social media, I’m concerned about when you monetise it because by its nature it’s me talking to you electronically, digitally. If I’m talking to you and I send

you a commercial message how do you feel about that? If I say ‘buy this’ or ‘do that’, it’s not the right context. [But it’s] an extremely powerful way of building brands, building trust and building reputation”, such as by users recommending products to each other.

This said, the attitudinal data suggests that Out of Home, which has always been most effective when employed as a complementary medium (particularly for television) is now highly complementary for mobile and social media as it can trigger both digital exploration of brand messages and social media conversations.

The most common response amongst 18-24 year olds for doing something as a result of seeing an Out of Home advert was word of mouth. This is amplified by social networks with more than half of respondents in every age range other than 45-55 year olds accessing social networking websites.

The only time I do it is if it’s part of a competition or promotional campaign i.e. I have something to get out of it. I always think it’s a bit cheesy to “like” Heineken just because you happen to enjoy Heineken...I like a million things but if I was to “like” them all on Facebook it would take quite a while.

18-24, m IRE

I don’t really understand what liking or following a brand on Twitter/Facebook is supposed to achieve really.

18-24, m IRE

3

38Interactive Europe 6. Out of Home’s Interactive Future

0

10

20

30

40

70

50

60

Age 18-24

Technology advocates

Age 25-34

Early adopters

Age 45-55

Age 35-44

52% 60%

55%

50%

57% 56%

This social effect is consistent with a study of European social network users in 2011 by InSites Consulting, which found that “offline brand experiences are the best conversation starter on social media.”

I think this way of advertising is smart. If you can elicit an interaction, people talk about it and more people will know about it without even seeing the advertisement. For example a while ago I saw a poster of Mysteryland and then I talked about it to my friends and asked who is going to that festival and that we have to buy tickets etc.

18-24, m NL

Source: Kantar MediaAll smart device users with a social media profile (2,172)

ALL SMART DEVICE USERS WITH A SOCIAL MEDIA PROFILE

39Interactive Europe 6. Out of Home’s Interactive Future

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

CONCLUSIONAudiences want brands to engage them on the move. Despite the speed of change in terms of technology, public attitudes towards Out of Home interactivity are well-established and positive. The younger, more tech-savvy audiences are currently the most engaged and ready to experiment with brands on the move and this is indicative of general consumer behaviour in the future.

But audiences don’t want you to waste their time. They expect something of value in return for investing their time in exploring brands more deeply. They want to interact and engage with brands that are more fun and more rewarding. They are inclined to like brands more that have made an effort and done something smart and creative.

Audiences want brands to apply the same principles to interactivity that they always have Out of Home: if you understand who your audience is, what they’re doing on the move, how they feel as they go and what they’re looking for when they get there, they are ready for a conversation.

40Interactive Europe Conclusion

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

41Interactive Europe Conclusion

Andrea [email protected]

Virginie MassardFrancevirginie.massard@exterionmedia.frwww.exterionmedia.fr

Guy GrimmeltThe [email protected]

Anna ReevesInternational [email protected]

Agata Romo [email protected]

Simon HarringtonUnited Kingdomsimon.harrington@exterionmedia.co.ukwww.exterionmedia.co.uk

Antoinette O’CallaghanIrelandantoinette.ocallaghan@exterionmedia.iewww.exterionmedia.ie

ABOUT EXTERION MEDIA

Exterion Media’s core business is engaging and delivering valuable audiences for advertisers through a variety of formats and environments including transport, billboards, street furniture and retail. Exterion Media is also one of the leaders in digital Out-of-Home advertising.

With operations in Europe and China and partnerships worldwide, its advertising reaches 73% of the world’s population accounting for 91% of the worlds’ GDP. Exterion Media combines this unrivalled reach with deep audience insight and innovations in Out-of-Home advertising.

Exterion Media is owned by Platinum Equity, a leading private equity firm specialising in mergers, acquisitions and operations.

We have collected and analysed a significant amount of data – at both a pan European and individual country level – and would be happy to share these findings as well as other insights with you in more detail.

Please contact the relevant person below, they will be happy to discuss the insights in more detail.

Alternatively, visit www.interactiveeurope.com to download a copy of this report and access more content on the study.

CONTACTS

As a leading Out of Home advertising company, Exterion Media specialises in understanding the relationship between brands and audiences.

143143

143143

42Interactive Europe About Exterion Media

METHODOLOGYThe scope of the study covered six key Exterion Media markets – UK, Ireland, France, Spain, Italy and the Netherlands. The research was conducted by Kantar Media in autumn 2011, with fieldwork running from 19th October to 27th November 2011.

Prior to the main research a preparatory phase took place in order to generate and refine the themes and consumer understanding behind the study. This encompassed two qualitative discussions about Out of Home media conducted face-to-face. All of the participants in the discussions were Smartphone users, one group were 18-24 year olds and the other 25-34 years old.

The main study comprised both quantitative and qualitative elements. A total of 9,024 interviews were conducted, across all 6 countries, with adults aged 18-54 years who live in, work or visit an urban area at least three times a week. An urban area was defined as either a town or city. The interviews were conducted online amongst members of the Lightspeed Research online panel using Computer Aided Web Interviewing (CAWI). The questionnaire covered a wide variety of topics including smartphone ownership, attitudes to advertising and interaction with advertising, specifically Out of Home. The data

was weighted to the urban profiles of the 6 countries. A question was run on an omnibus study in each country to establish the size of the urban market and weighting.

The qualitative element ran at the same time using an online discussion forum – Kantar Media’s Arena. The Arena took part over 5 days and respondents were set various tasks as they progressed. All respondents within the qualitative sessions were Smartphone users and aged 18-35 years. Respondents discussed various aspects of Out of Home media with a focus on the role of technology, including some future facing concepts. Moderators in each country managed the discussion and set a series of tasks including exposure to some of the new and more creative treatments and interactive concepts. The process was partly deliberative beginning with an investigation of their interaction with Out of Home media, progressing through barriers to interaction and ended by evaluating some of the concepts and newer treatments including NFC, augmented reality and location based apps.

43Interactive Europe Methodology

A QUICK GUIDE TO INTERACTIVE TECHNOLOGIES

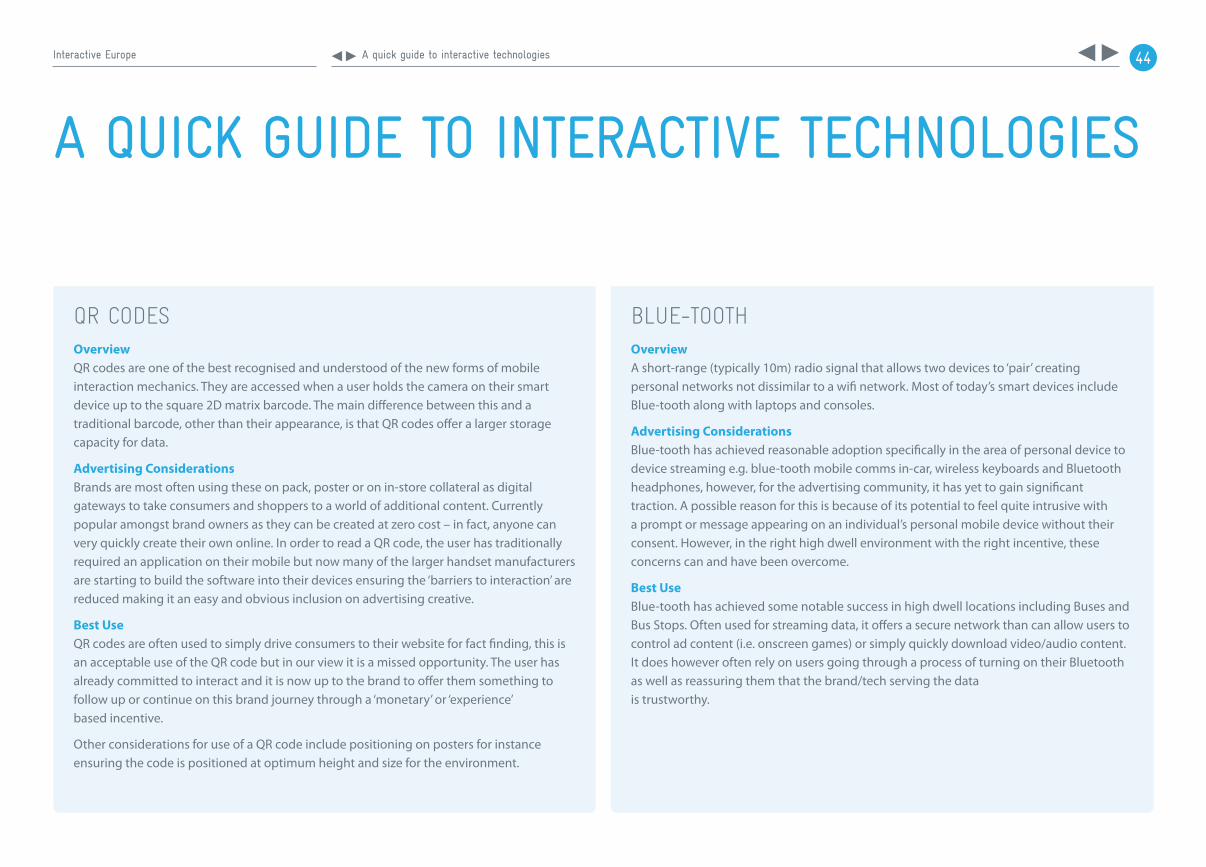

QR CODESOverview QR codes are one of the best recognised and understood of the new forms of mobile interaction mechanics. They are accessed when a user holds the camera on their smart device up to the square 2D matrix barcode. The main difference between this and a traditional barcode, other than their appearance, is that QR codes offer a larger storage capacity for data.

Advertising Considerations Brands are most often using these on pack, poster or on in-store collateral as digital gateways to take consumers and shoppers to a world of additional content. Currently popular amongst brand owners as they can be created at zero cost – in fact, anyone can very quickly create their own online. In order to read a QR code, the user has traditionally required an application on their mobile but now many of the larger handset manufacturers are starting to build the software into their devices ensuring the ‘barriers to interaction’ are reduced making it an easy and obvious inclusion on advertising creative.

Best Use QR codes are often used to simply drive consumers to their website for fact finding, this is an acceptable use of the QR code but in our view it is a missed opportunity. The user has already committed to interact and it is now up to the brand to offer them something to follow up or continue on this brand journey through a ‘monetary’ or ‘experience’ based incentive.

Other considerations for use of a QR code include positioning on posters for instance ensuring the code is positioned at optimum height and size for the environment.

BLUE-TOOTHOverviewA short-range (typically 10m) radio signal that allows two devices to ‘pair’ creating personal networks not dissimilar to a wifi network. Most of today’s smart devices include Blue-tooth along with laptops and consoles.

Advertising Considerations Blue-tooth has achieved reasonable adoption specifically in the area of personal device to device streaming e.g. blue-tooth mobile comms in-car, wireless keyboards and Bluetooth headphones, however, for the advertising community, it has yet to gain significant traction. A possible reason for this is because of its potential to feel quite intrusive with a prompt or message appearing on an individual’s personal mobile device without their consent. However, in the right high dwell environment with the right incentive, these concerns can and have been overcome.

Best UseBlue-tooth has achieved some notable success in high dwell locations including Buses and Bus Stops. Often used for streaming data, it offers a secure network than can allow users to control ad content (i.e. onscreen games) or simply quickly download video/audio content. It does however often rely on users going through a process of turning on their Bluetooth as well as reassuring them that the brand/tech serving the data is trustworthy.

44Interactive Europe A quick guide to interactive technologies

A QUICK GUIDE TO INTERACTIVE TECHNOLOGIES

NEAR FIELD COMMUNICATION (NFC)Overview Near Field Communication allows the transfer of data between a smart device with pre-installed NFC hardware and an NFC tag or NFC transmitter/receiver. It is generally a close proximity form of communication (around 4cm) and therefore is very dependent on the consumer presenting their device to receive or transmit data. This ‘physical opt-in’ principle makes it less intrusive than Blue-tooth and also more secure. They are widely viewed as one of the interactive technologies of the future as they offer one of the quickest and most versatile forms of data exchange with can relay everything from video to monetary transactions (e.g. via Google Wallet).

Advertising Considerations Japan has been using NFC successfully for several years and it is only the hardware manufacturers that have prevented NFC from reaching a reasonable level of penetration in the UK and the US, however, it is expected that by the end of 2012, over 50% of mobiles will include NFC technology.

Best UseNFC transmitters (hardware installed into advertising units) present a convenient way to transfer and view movie trailers or even purchase tickets. NFC tags are another form of NFC where a small amount of data in sticker is able to direct the user to exclusive content hosted online.

TOUCH SCREENSOverviewThanks to touch controlled technology such as the Iphone and other personal devices, touch screens are now a technology that we literally, come into contact with on a daily basis.

Advertising Considerations Most Out of Home touch screens are now ‘connected or online’ allowing remote access and control by the content provider which in turn allows consumers to access both online and bespoke locally hosted content. In essence, a touch screen can offer the functionality and therefore versatility for advertisers that your home computer can offer - the only difference being there is no mouse. This allows a huge array of content to be delivered instantly without the need for the consumer to do anything other touch the screen. This is the most immediate form of interactivity.

Best UseTouch screens rely on dwell time as unlike some forms of poster to mobile interactivity, most of the interaction occurs at the screen itself. Campaigns will require big and bold call to actions as consumers are still not familiar with the idea of being able to manipulate or delve further into content in this public way. Best uses can include the provision of location specific data, for instance: cinema times, availability and trailers or branded games with monetary reward to then take in-store.

45Interactive Europe A quick guide to interactive technologies

AUGMENTED REALITY (MOBILE AND NON MOBILE)OverviewOf all the interactive technologies augmented reality (AR) is the most impactful. In its most common form, it uses your phones camera or a camera built into an advertising hoarding to display whatever is in the camera’s view finder on screen at that given moment.

This of course is very simple, however, when the camera is presented with a stimulus that the software on the device recognises (i.e. a face, a flyer, building or logo), an image or action is overlaid, live, on your camera or via the screen giving the impression of a augmented reality.

Advertising ConsiderationsAR is one of the most engaging forms of interactive advertising – as such it offers some of the greatest experience related benefits. If this ‘wow’ factor can be combined with a monetary and social element then the potential for generating consumer involvement and affinity is exceptionally high. Of course AR is also one of more costly of the interactive mechanics and requires a bespoke application download - as yet, a dominant AR app provider is yet to establish themselves.

Best UseFun and immersion are key to AR campaigns. They can literally bring a product into a consumer’s home through a virtual experience. Automotive manufacturers have been the first to really grasp the potential of this technology along with some of the FMCG brands. AR also offers location specific experiences meaning that users have to search out the ads or are treated to special experiences in certain locations – this also adds to the magic which drives talk-ability and brand immersion.

SMS OR MOBILE MARKETING OverviewTexts require very little explanation however they are still a relevant and potential vehicle for interactivity as they offer a familiar, trusted platform that nearly everyone has access to all of the time. They are most often used to drive immediate sales based on consumer behaviour and can also be used to initiate a data connection over 3G allowing users to control or manipulate advertising content.

Advertising ConsiderationsText campaigns have fallen out of favour with many advertisers as many consumers have had at least one bad experience with unscrupulous text spammers. Again, like many of these technologies, with the right incentive and a very targeted and well managed system campaign, they can offer some relatively cost effective way to engage with your customers.

Best Use Mobile marketing is inexpensive, personal and based on previous consumer behaviour, can be exceptionally targeted. Mobile campaigns also have a very high redemption rate as by knowing your consumes previous buying behaviour, you can quickly target them during the decision making process. Categories such as retail and food have found text mechanics to work particularly well for them.

46Interactive Europe A quick guide to interactive technologies

MOBILE APPLICATIONS (IMAGE REC/CHECK IN) Overview Interactive technologies such as AR and Image Recognition apps like Google Goggles currently rely on users to obtain software in order to activate this interaction. This software is downloaded via the smart devices relative app store. Another interactive mechanic used by brands growing in popularity are brand check-ins. Four Square is the most well known of the check-in apps however Facebook also has a check-in function. We’ve also seen poster check-ins which again offers a reward each time you see a specific brand’s advertising.

Adverting Considerations The average user has around 65 apps on their phone, but over a week they will use just 15 (Source: Flurry 2012). Those apps that don’t deliver a specific communication function or browsing function must work very hard to ensure their product remains on the consumers standard repertoire.

Best Use Incorporating interactive elements into platforms that already have a good penetration (i.e. already owned and don’t require a download) offer the best opportunity to engage with customers. They’re both familiar and require no extra effort in terms of searching their app store and download.

PHOTO/VIDEO CAPTURE OverviewPhoto and video capture encompasses a range of different types of interactions. Some of the most common include inviting consumers to capture an image via their Smart device to either show in-store for discounts or to submit as part of a competition or be included as part of the campaign. This capitalises on consumers’ current willingness to snap or video their surrounding which ensures with the right incentive, involvement can be high.

Adverting Considerations Such campaigns clearly resonate with price sensitive, younger, mobile centric audiences and work most efficiently close to the point or purchase. It’s also important to build in a strong social media element as this type of interaction offers huge potential for sharing and therefore driving further and prolonged consumer involvement in the campaign and brand.

Best Use The ‘snap and show’. e.g. “take a photo of this ad and bring in store for you discount today” offers very tangible, measurable benefits for brands. A more experience oriented version of this is sending or having your image captured and then projected essentially making the consumer part of the ad. This often creates excellent social chatter and buzz as being part of the ad is often something to boast about.

47Interactive Europe A quick guide to interactive technologies

Base: All those expressing a preference (ANY AGREE or ANY DISAGREE)

48Interactive Europe A quick guide to interactive technologies

www.interactiveeurope.comtwitter: #InteractiveEurope

Return to start