Embed Size (px)

Citation preview

8/7/2019 Interest Rate Swaps: Pre-2008 Crisis

http://slidepdf.com/reader/full/interest-rate-swaps-pre-2008-crisis 1/1

THEEDGE malaysia | january 17, 2011capital 46derivatives world

• ArbitrageopportunitiesThe IRS market is closely linked to the in-

terest rate utures and orwards markets. Arbi-trageurs continuously trade between orwards,

utures and swaps resulting in the rates or thedierent derivatives within the same tenor tostay in close proximity.

Some important features ofinterest rate swapsBeore we go urther, it would be useul to un-derstand some important eatures o the IRS,such as:• Resetdates

These are pre-set dates when the oatingrate in the IRS will be reset tothe current rate. For exam-ple, an IRS that has one oat-ing leg paying three-monthLibor (say 5%) will be re-setevery three months at pre-de-termined dates. At these dates,the three-month Libor (which

was 5%) will be changed to thecurrent rate (say 4.8%).• FixedrateorswaprateIn a previous article, “Finan-cial Wizardry in Swaps theGreek case” ( March 8, 2010),the swap rate or a cross cur-rency swap was discussed. Inany fxed-or-oating swap,

the fxed rate to be paid by the fxed ratepayer will be such that it makes the swap“air”. In other words, at the inception o the swap, the price o the swap shouldideally be zero. Now, the price o the swapis simply the present value o its oatingand fxed cash ows. To make the pricezero, the fxed rate is adjusted to make thepresent value zero. This fxed rate is alsoknown as the swap rate or the at-market

swap rate.

New developmentsNow that we have a reasonable level o under-standing o the plain-vanilla interest rate swap,in the next article, we will study how the swapmarket changed ater the 2008 crisis, bring-ing about “basis risk” which was consideredinsignifcant beore but cannot aord to besidelined now.

JasvinJosenisaspecialistindevelopingmethodologiesorvaluationovariousderivativeproducts.Shehasover10years’experienceininvestmentbankingandtheinancialindustryinEuropeandAsia.Comments:[email protected]://derivativetimes.blogspot.com.

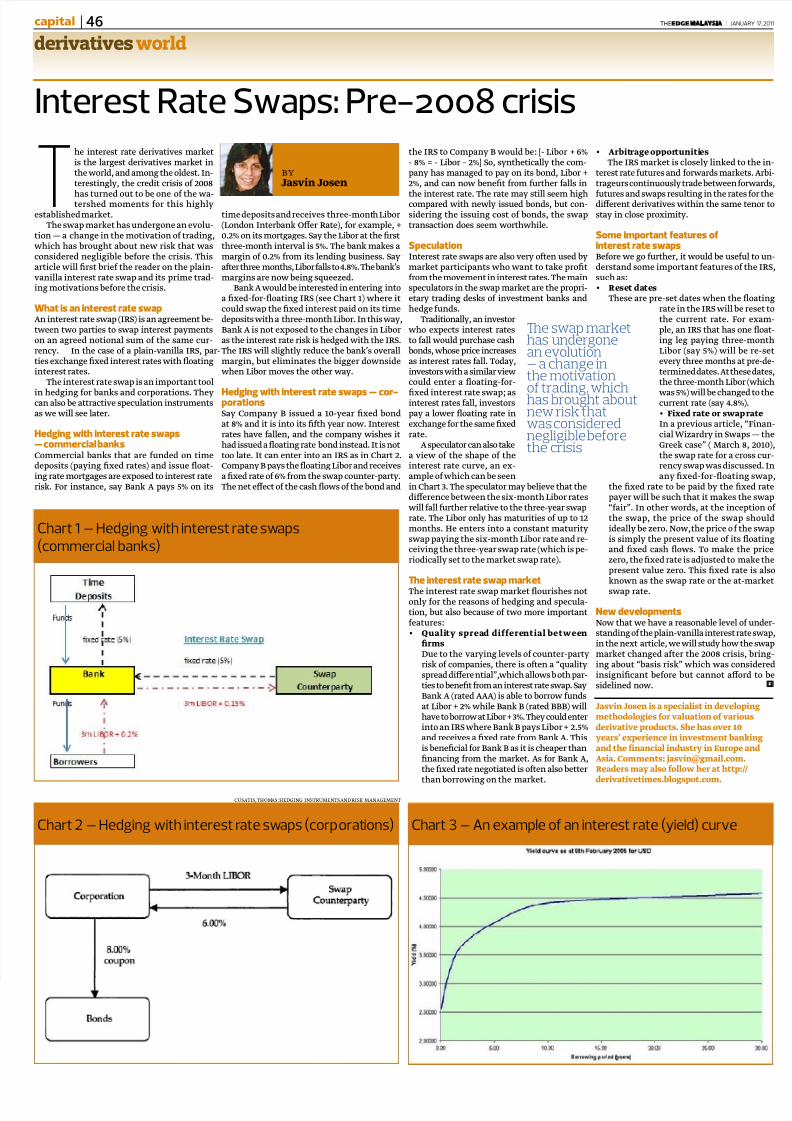

time deposits and receives three-month Libor(London Interbank Oer Rate), or example, +0.2% on its mortgages. Say the Libor at the frstthree-month interval is 5%. The bank makes amargin o 0.2% rom its lending business. Sayater three months, Libor alls to 4.8%. The bank’smargins are now being squeezed.

Bank A would be interested in entering intoa fxed-or-oating IRS (see Chart 1) where itcould swap the fxed interest paid on its timedeposits with a three-month Libor. In this way,Bank A is not exposed to the changes in Liboras the interest rate risk is hedged with the IRS.The IRS will slightly reduce the bank’s overallmargin, but eliminates the bigger downsidewhen Libor moves the other way.

Hedging with interest rate swaps cor-porationsSay Company B issued a 10-year fxed bondat 8% and it is into its fth year now. Interestrates have allen, and the company wishes ithad issued a oating rate bond instead. It is nottoo late. It can enter into an IRS as in Chart 2.Company B pays the oating Libor and receivesa fxed rate o 6% rom the swap counter-party.The net eect o the cash ows o the bond and

the IRS to Company B would be: [- Libor + 6%- 8% = - Libor – 2%] So, synthetically the com-pany has managed to pay on its bond, Libor +2%, and can now beneft rom urther alls in

the interest rate. The rate may still seem highcompared with newly issued bonds, but con-sidering the issuing cost o bonds, the swaptransaction does seem worthwhile.

SpeculationInterest rate swaps are also very oten used bymarket participants who want to take proftrom the movement in interest rates. The mainspeculators in the swap market are the propri-etary trading desks o investment banks andhedge unds.

Traditionally, an investorwho expects interest ratesto all would purchase cashbonds, whose price increasesas interest rates all. Today,investors with a similar viewcould enter a oating-or-

fxed interest rate swap; asinterest rates all, investorspay a lower oating rate inexchange or the same fxedrate.

A speculator can also takea view o the shape o theinterest rate curve, an ex-ample o which can be seenin Chart 3. The speculator may believe that thedierence between the six-month Libor rateswill all urther relative to the three-year swaprate. The Libor only has maturities o up to 12months. He enters into a constant maturityswap paying the six-month Libor rate and re-ceiving the three-year swap rate (which is pe-riodically set to the market swap rate).

Te interest rate swap market

The interest rate swap market ourishes notonly or the reasons o hedging and specula-tion, but also because o two more importanteatures:• Qualityspreaddifferentialbetween

frmsDue to the varying levels o counter-partyrisk o companies, there is oten a “qualityspread dierential”, which allows both par-ties to beneft rom an interest rate swap. SayBank A (rated AAA) is able to borrow undsat Libor + 2% while Bank B (rated BBB) willhave to borrow at Libor + 3%. They could enterinto an IRS where Bank B pays Libor + 2.5%and receives a fxed rate rom Bank A. Thisis benefcial or Bank B as it is cheaper thanfnancing rom the market. As or Bank A,the fxed rate negotiated is oten also betterthan borrowing on the market.

interet Rte swp: Pre-2008 cr

Cht 1 – Hedgig with iteest te swps(commecil bks)

Cht 3 – a exmple of iteest te (ield) cve

T

he interest rate derivatives marketis the largest derivatives market inthe world, and among the oldest. In-terestingly, the credit crisis o 2008

has turned out to be one o the wa-tershed moments or this highlyestablished market.

The swap market has undergone an evolu-tion a change in the motivation o trading,which has brought about new risk that wasconsidered negligible beore the crisis. Thisarticle will frst brie the reader on the plain-vanilla interest rate swap and its prime trad-ing motivations beore the crisis.

What is an interest rate swapAn interest rate swap (IRS) is an agreement be-tween two parties to swap interest paymentson an agreed notional sum o the same cur-rency. In the case o a plain-vanilla IRS, par-ties exchange fxed interest rates with oatinginterest rates.

The interest rate swap is an important tool

in hedging or banks and corporations. Theycan also be attractive speculation instrumentsas we will see later.

Hedging with interest rate swaps commercial banksCommercial banks that are unded on timedeposits (paying fxed rates) and issue oat-ing rate mortgages are exposed to interest raterisk. For instance, say Bank A pays 5% on its

byJasvinJosen

Te swap markethas undergonean evolution a change inthe motivation

of trading, whichhas brought aboutnew risk thatwas considerednegligible beforethe crisis

Cht 2 – Hedgig with iteest te swps (copotios)

Cusatis, thomas: hedging instruments and risk management