Embed Size (px)

Citation preview

1

5 December 2018

Interim ResultsHalf-year ended 27 October 2018

2

Cautionary statement

This document is solely for use in connection with a briefing on the group headed by Stagecoach Group plc (“the Group”).

This document contains forward-looking statements that are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries, sectors and markets in which the Group operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results to differ materially from those currently anticipated. No assurances can be given that the forward-looking statements in this presentation will be realised. The forward-looking statements reflect the knowledge and information available at the date of preparation.

This document is not a full record of the presentation because it does not include comments made verbally by Stagecoach Group management or by others.

3

ROSS PATERSONFINANCE DIRECTOR

4

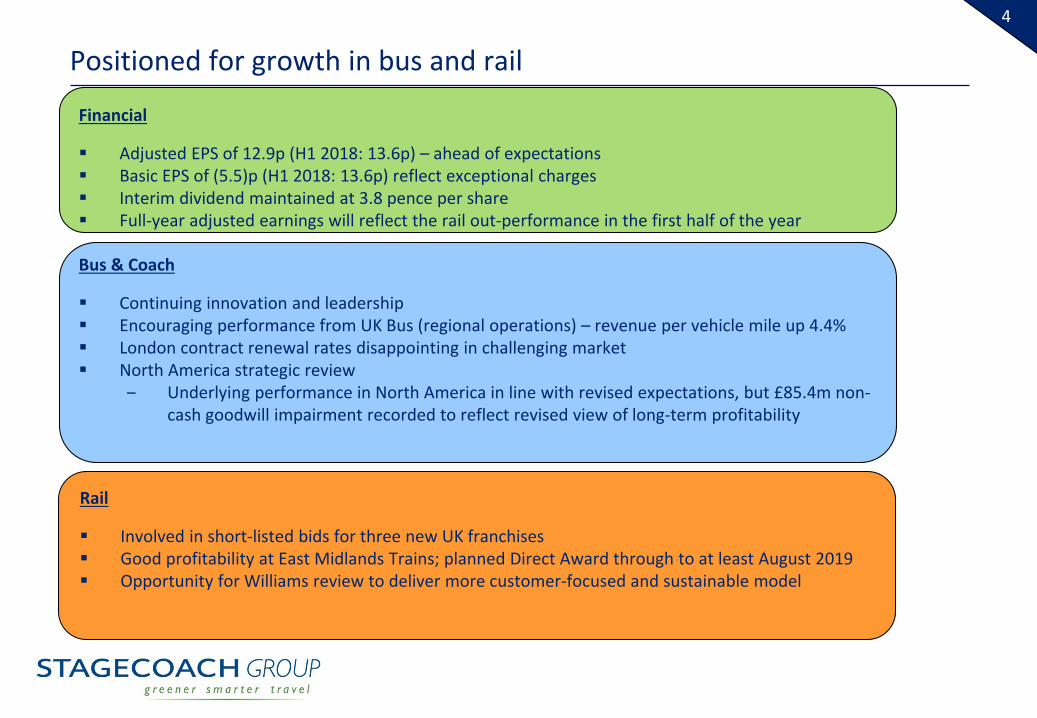

Positioned for growth in bus and rail

Financial

Adjusted EPS of 12.9p (H1 2018: 13.6p) – ahead of expectations Basic EPS of (5.5)p (H1 2018: 13.6p) reflect exceptional charges Interim dividend maintained at 3.8 pence per share Full-year adjusted earnings will reflect the rail out-performance in the first half of the year

Bus & Coach

Continuing innovation and leadership Encouraging performance from UK Bus (regional operations) – revenue per vehicle mile up 4.4% London contract renewal rates disappointing in challenging market North America strategic review

‒ Underlying performance in North America in line with revised expectations, but £85.4m non-cash goodwill impairment recorded to reflect revised view of long-term profitability

Rail

Involved in short-listed bids for three new UK franchises Good profitability at East Midlands Trains; planned Direct Award through to at least August 2019 Opportunity for Williams review to deliver more customer-focused and sustainable model

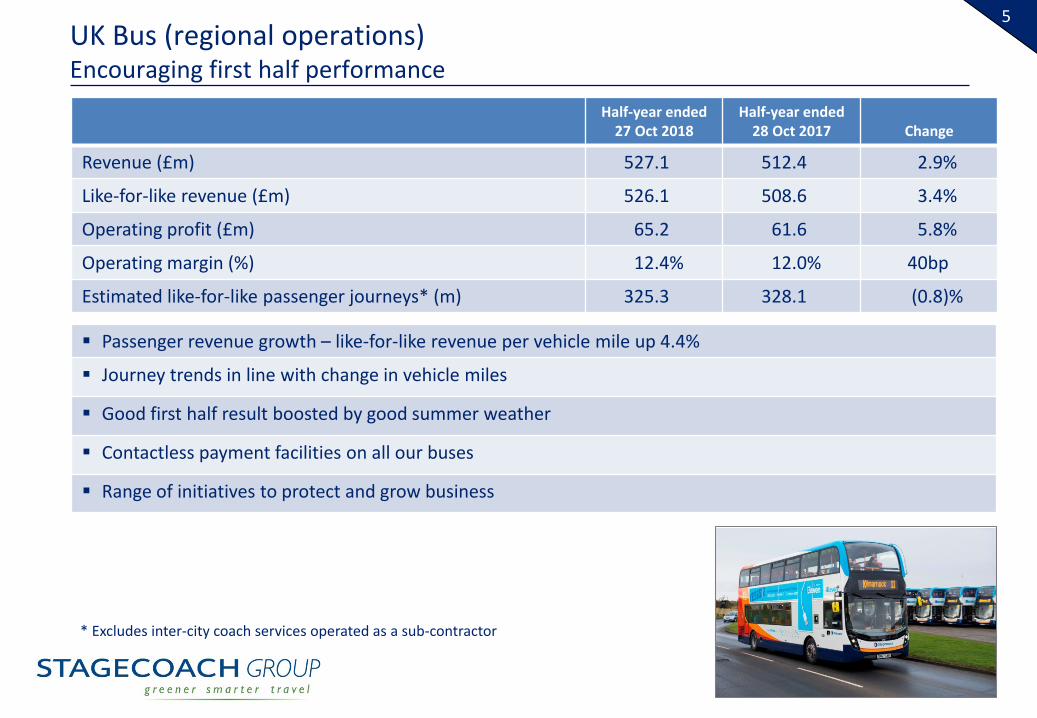

5UK Bus (regional operations)Encouraging first half performance

* Excludes inter-city coach services operated as a sub-contractor

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017 Change

Revenue (£m) 527.1 512.4 2.9%

Like-for-like revenue (£m) 526.1 508.6 3.4%

Operating profit (£m) 65.2 61.6 5.8%

Operating margin (%) 12.4% 12.0% 40bp

Estimated like-for-like passenger journeys* (m) 325.3 328.1 (0.8)%

Passenger revenue growth – like-for-like revenue per vehicle mile up 4.4%

Journey trends in line with change in vehicle miles

Good first half result boosted by good summer weather

Contactless payment facilities on all our buses

Range of initiatives to protect and grow business

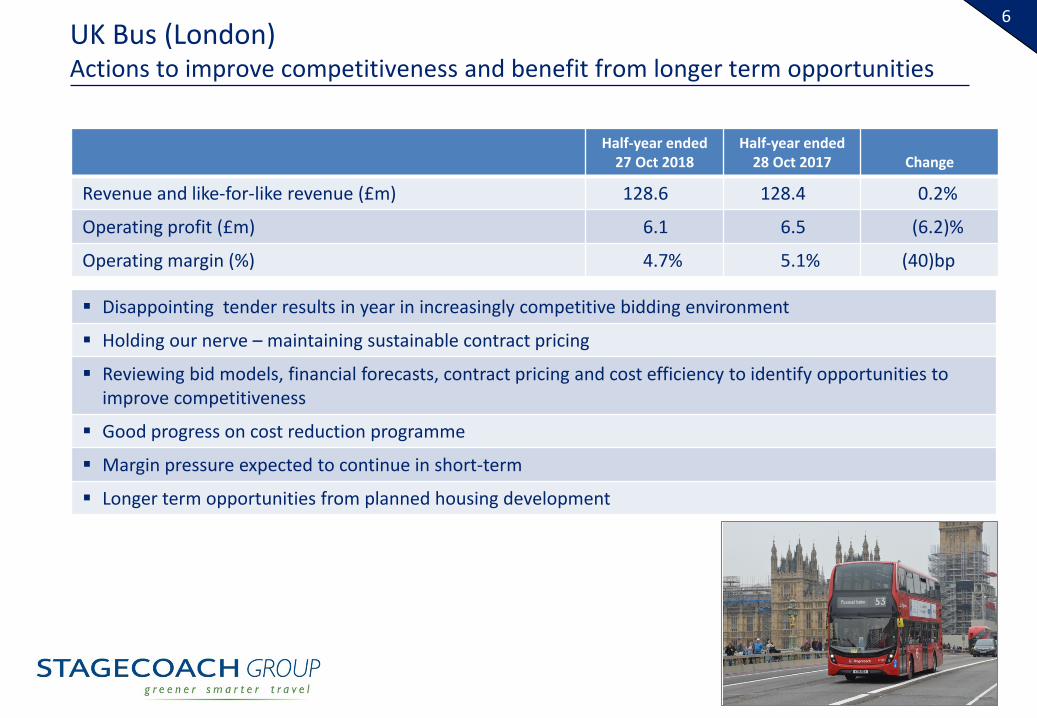

6UK Bus (London)Actions to improve competitiveness and benefit from longer term opportunities

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017 Change

Revenue and like-for-like revenue (£m) 128.6 128.4 0.2%

Operating profit (£m) 6.1 6.5 (6.2)%

Operating margin (%) 4.7% 5.1% (40)bp

Disappointing tender results in year in increasingly competitive bidding environment

Holding our nerve – maintaining sustainable contract pricing

Reviewing bid models, financial forecasts, contract pricing and cost efficiency to identify opportunities to improve competitiveness

Good progress on cost reduction programme

Margin pressure expected to continue in short-term

Longer term opportunities from planned housing development

7North AmericaFocused on new opportunities

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017 Change

Revenue (US$m) 323.3 333.9 (3.2)%

Like-for-like revenue (US$m) 323.9 333.9 (3.0)%

Operating profit (US$m) 21.2 27.6 (23.2)%

Operating margin (%) 6.6% 8.3% (170)bp

No significant change since September trading update in expected 2018/19 profit

Focus is on growing scheduled service (including megabus.com) and contract revenue business

Further reviewing cost base

Non-cash impairment charge of £85.4m, reflecting revised view of long-term profitability

Reviewing strategic options – in discussions regarding possible sale

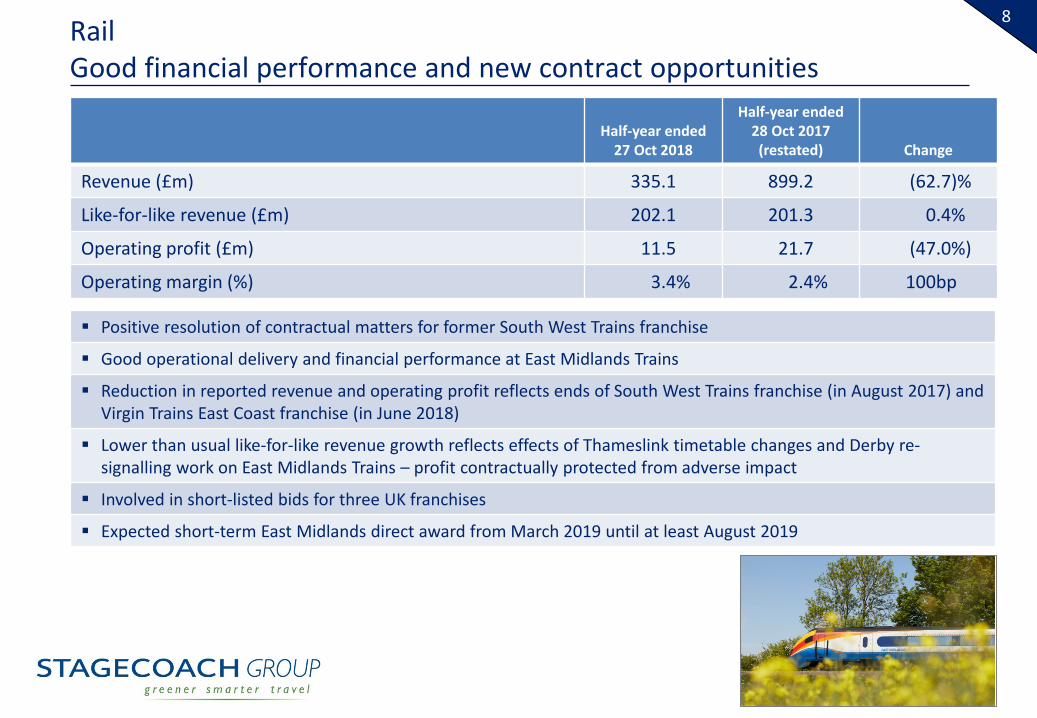

8RailGood financial performance and new contract opportunities

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017(restated) Change

Revenue (£m) 335.1 899.2 (62.7)%

Like-for-like revenue (£m) 202.1 201.3 0.4%

Operating profit (£m) 11.5 21.7 (47.0%)

Operating margin (%) 3.4% 2.4% 100bp

Positive resolution of contractual matters for former South West Trains franchise

Good operational delivery and financial performance at East Midlands Trains

Reduction in reported revenue and operating profit reflects ends of South West Trains franchise (in August 2017) and Virgin Trains East Coast franchise (in June 2018)

Lower than usual like-for-like revenue growth reflects effects of Thameslink timetable changes and Derby re-signalling work on East Midlands Trains – profit contractually protected from adverse impact

Involved in short-listed bids for three UK franchises

Expected short-term East Midlands direct award from March 2019 until at least August 2019

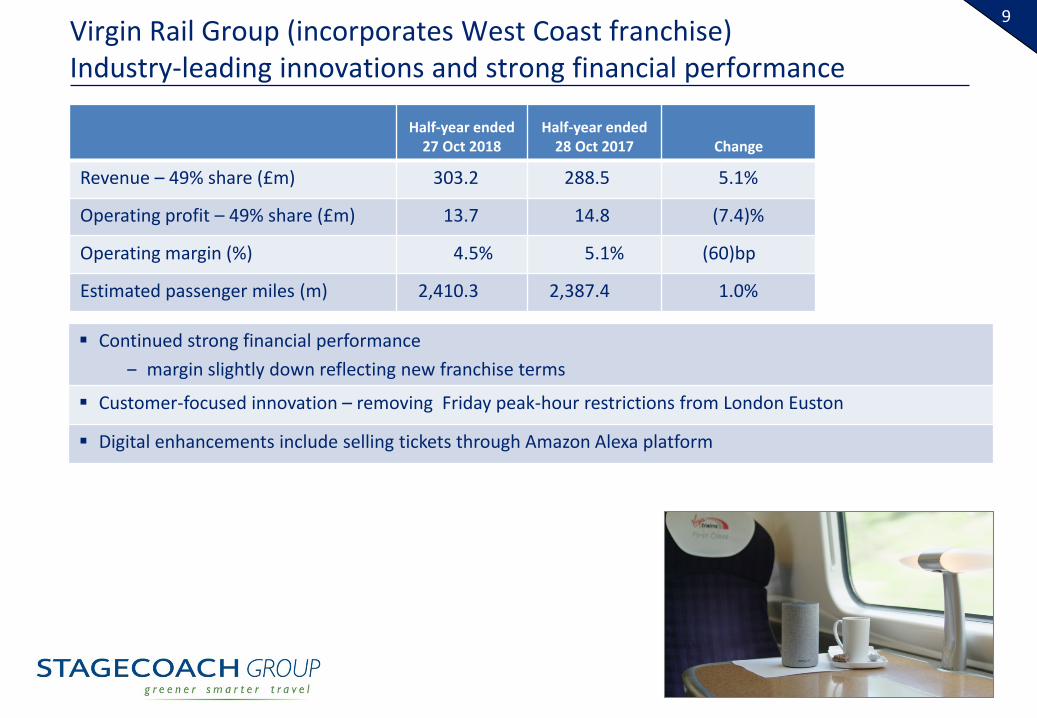

9Virgin Rail Group (incorporates West Coast franchise)Industry-leading innovations and strong financial performance

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017 Change

Revenue – 49% share (£m) 303.2 288.5 5.1%

Operating profit – 49% share (£m) 13.7 14.8 (7.4)%

Operating margin (%) 4.5% 5.1% (60)bp

Estimated passenger miles (m) 2,410.3 2,387.4 1.0%

Continued strong financial performance‒ margin slightly down reflecting new franchise terms

Customer-focused innovation – removing Friday peak-hour restrictions from London Euston

Digital enhancements include selling tickets through Amazon Alexa platform

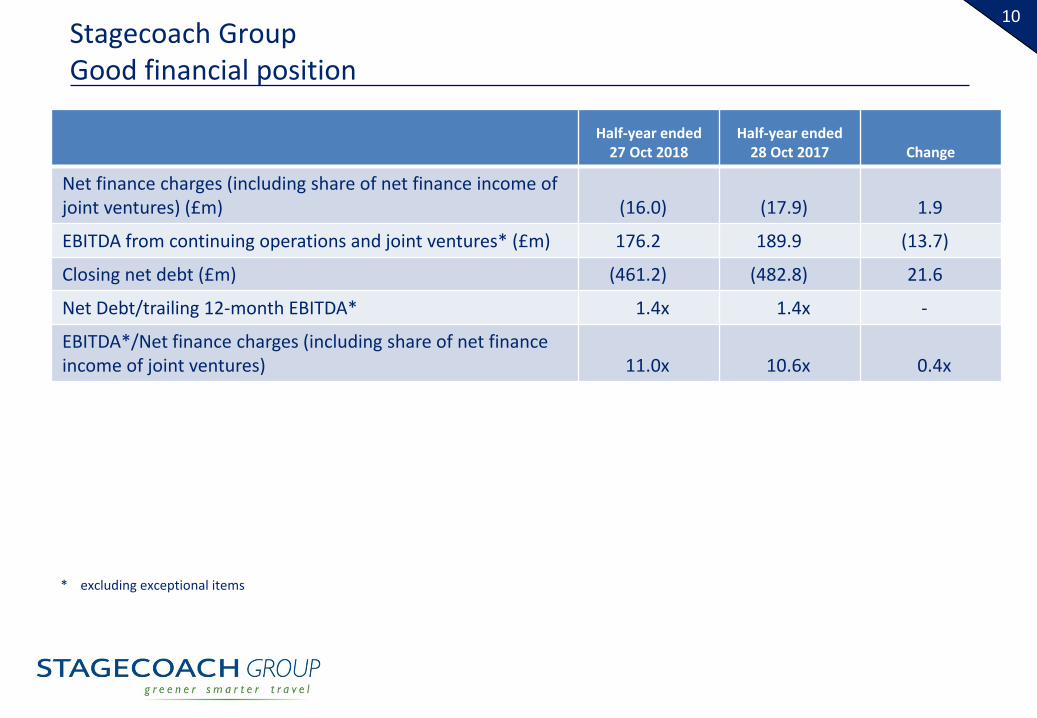

10Stagecoach GroupGood financial position

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017 Change

Net finance charges (including share of net finance income of joint ventures) (£m) (16.0) (17.9) 1.9

EBITDA from continuing operations and joint ventures* (£m) 176.2 189.9 (13.7)

Closing net debt (£m) (461.2) (482.8) 21.6

Net Debt/trailing 12-month EBITDA* 1.4x 1.4x -

EBITDA*/Net finance charges (including share of net finance income of joint ventures) 11.0x 10.6x 0.4x

* excluding exceptional items

11

MARTIN GRIFFITHSCHIEF EXECUTIVE

12

Overview

Good business fundamentals and strong financial position

Growth in core regional bus operations and well positioned in de-risked rail market

Clear understanding of changing dynamics and trends in our public transport markets

Focus on growing demand through data, technology, innovation + better policy

Leveraging technology and engaging with our people to make bus and rail services easier for customers, reduce costs and improve efficiency

Positive outlook from growing pressure on governments to address road congestion, air quality and maximise benefit of public transport to economy

13

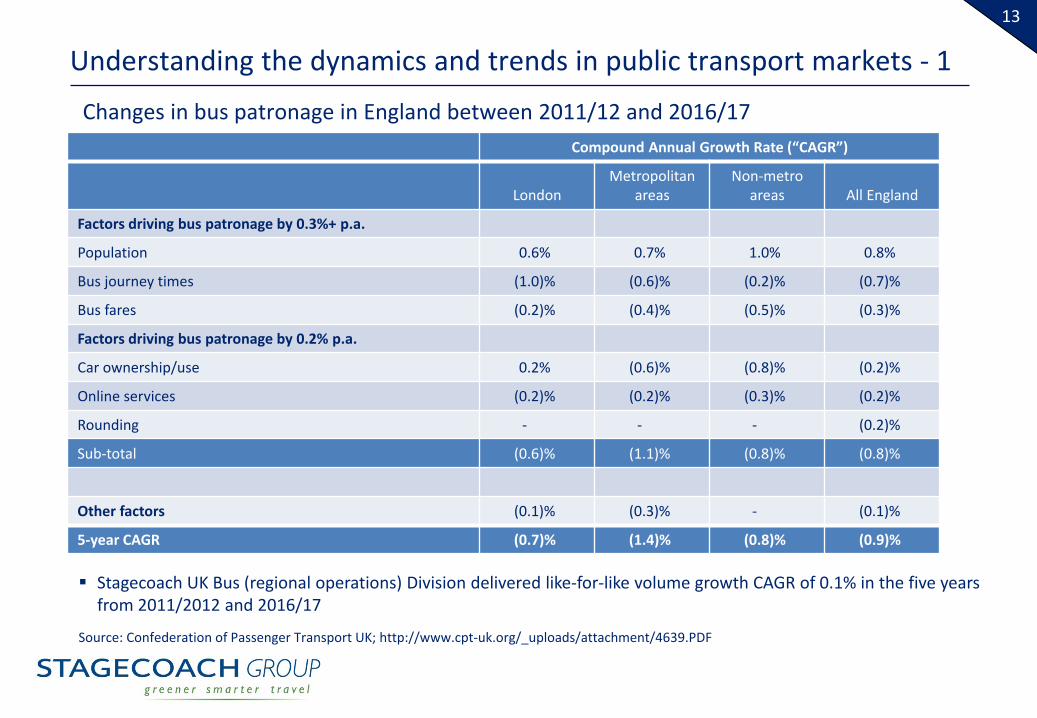

Understanding the dynamics and trends in public transport markets - 1

Compound Annual Growth Rate (“CAGR”)

LondonMetropolitan

areasNon-metro

areas All England

Factors driving bus patronage by 0.3%+ p.a.

Population 0.6% 0.7% 1.0% 0.8%

Bus journey times (1.0)% (0.6)% (0.2)% (0.7)%

Bus fares (0.2)% (0.4)% (0.5)% (0.3)%

Factors driving bus patronage by 0.2% p.a.

Car ownership/use 0.2% (0.6)% (0.8)% (0.2)%

Online services (0.2)% (0.2)% (0.3)% (0.2)%

Rounding - - - (0.2)%

Sub-total (0.6)% (1.1)% (0.8)% (0.8)%

Other factors (0.1)% (0.3)% - (0.1)%

5-year CAGR (0.7)% (1.4)% (0.8)% (0.9)%

Source: Confederation of Passenger Transport UK; http://www.cpt-uk.org/_uploads/attachment/4639.PDF

Changes in bus patronage in England between 2011/12 and 2016/17

Stagecoach UK Bus (regional operations) Division delivered like-for-like volume growth CAGR of 0.1% in the five years from 2011/2012 and 2016/17

14

Understanding the dynamics and trends in public transport markets - 2

Population growth is the biggest positive driver of bus patronage across England.

The biggest negative drivers of patronage are factors linked to road congestion: car ownership, increased bus journey times and higher bus fares

Public policy decisions have also negatively impacted bus use:

‒ Cuts to local authority supported services have reduced the scope of bus networks

‒ the Government’s decision to reduce the rate of Bus Service Operators Grant (fuel duty rebate) from April 2012 has increased bus operator costs and fares

Online services (e.g. online shopping and delivery services) have had a lesser adverse impact on bus use

The incremental impact from new taxi competition has been relatively modest

15

Future bus passenger trends: opportunities and risksOpportunities for growth

Measures to tackle road congestion and air quality, promote public transport

Stable public policy to minimise bus cost increases

Stabilisation/growth in tendered bus services ex-London

Further improvements in bus quality

Benefits of operator use of data to grow patronage

Increased car costs (fuel prices, insurance)

Creating new reasons to travel, particularly to town centres

Population growth and urbanisation

Risks of decline

Increased taxi competition

More use of online services

Greater flexible (and at home) working

16

Making our bus services easier for customers

Growth in new and refreshed inter-urban services by reflecting changing customer needs/expectations in product offer

Partnership with Deloitte digital arm to deliver radical simplification of passenger information, with prioritisation of digital

Brand strategy review to reconnect with customers and leverage strength of our market leading offer

Completion of roll-out of Britain’s biggest deployment of contactless technology on bus, with plans for QR code mobile ticketing on bus in 2019

17

Predictive demand analytics Partnership with CitySwifter to deliver more

accurate bus schedules, business intelligence, improved reliability and cost efficiencies

Trial on four major bus corridors into Oxford New schedules running since September 2018

focused initially on improving punctuality

Demand responsive transport (DRT) Detailed analysis of key criteria across global

DRT market initially identified four locations on Stagecoach network in England

Data used to redesign services to generate growth from existing and new travel demand

Commercial terms agreed for a strategic relationship with a technology provider

Innovation: using data to predict and manage transport demand

18

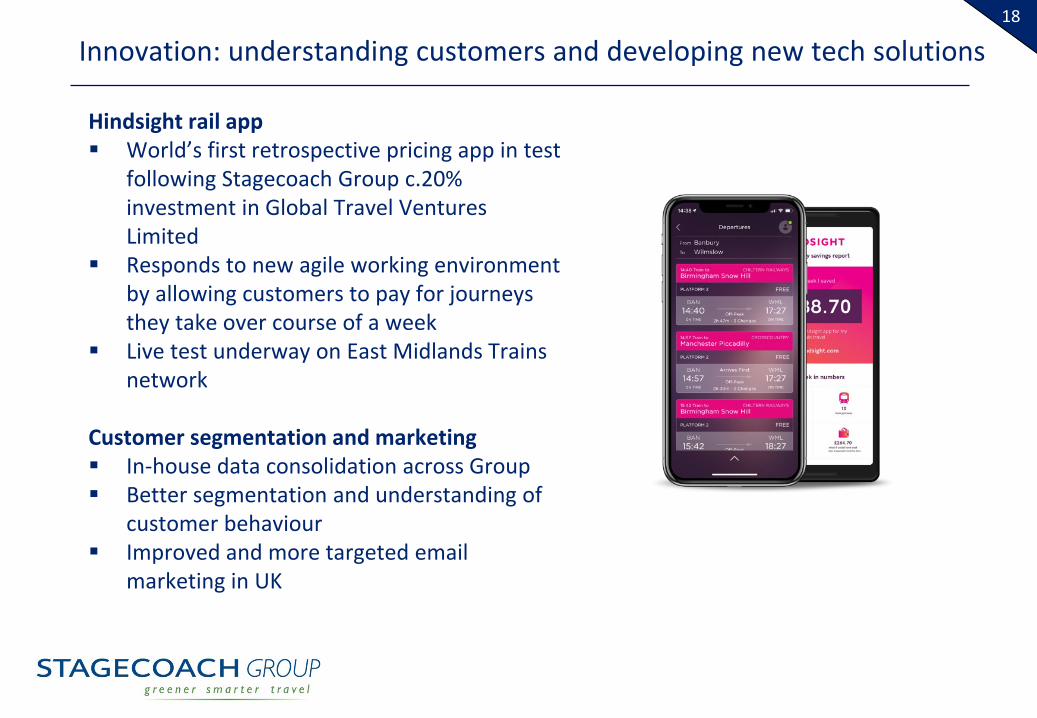

Innovation: understanding customers and developing new tech solutions

Hindsight rail app World’s first retrospective pricing app in test

following Stagecoach Group c.20% investment in Global Travel Ventures Limited

Responds to new agile working environment by allowing customers to pay for journeys they take over course of a week

Live test underway on East Midlands Trains network

Customer segmentation and marketing In-house data consolidation across Group Better segmentation and understanding of

customer behaviour Improved and more targeted email

marketing in UK

19

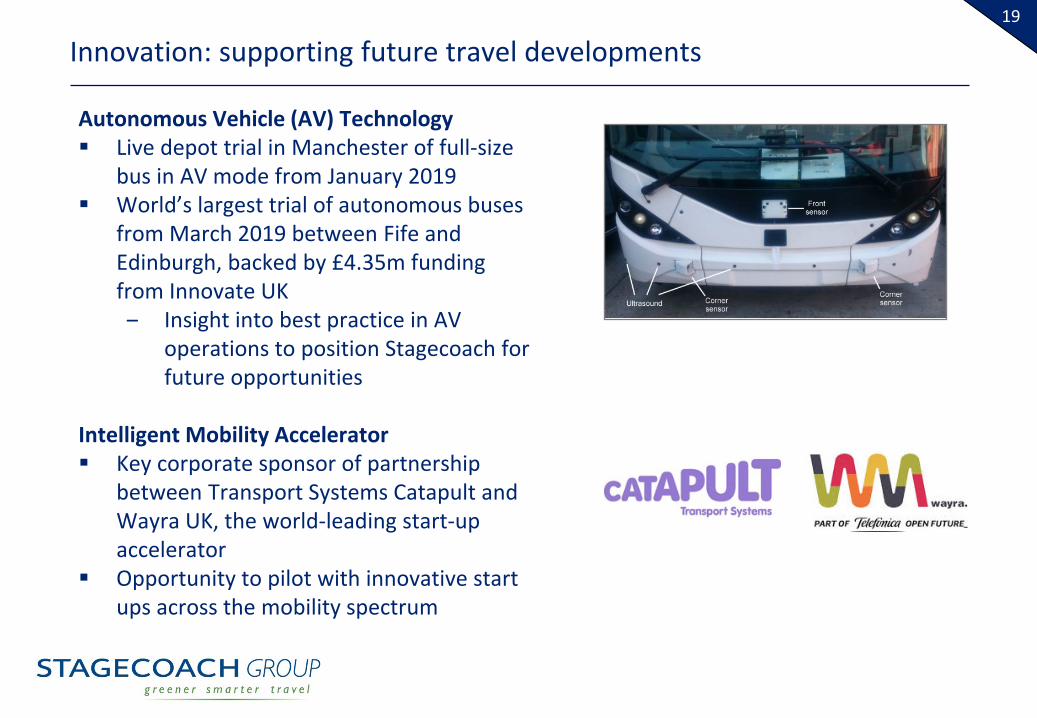

Innovation: supporting future travel developments

Autonomous Vehicle (AV) Technology Live depot trial in Manchester of full-size

bus in AV mode from January 2019 World’s largest trial of autonomous buses

from March 2019 between Fife and Edinburgh, backed by £4.35m funding from Innovate UK‒ Insight into best practice in AV

operations to position Stagecoach for future opportunities

Intelligent Mobility Accelerator Key corporate sponsor of partnership

between Transport Systems Catapult and Wayra UK, the world-leading start-up accelerator

Opportunity to pilot with innovative start ups across the mobility spectrum

20

Influencing transport policy

Urban Mobility Partnership Formed by Stagecoach Group and car

rental group, Enterprise Holdings Brings together key stakeholders to

develop practical policy solutions aimed at reducing congestion, improving air quality and making journeys easier in UK towns and cities

Initial policy proposals focus on mobility credits, planning and grey fleets

21

UK rail market and government policy review

Group well-positioned in UK rail market

‒ Three live contract bids both individually and with strong partners‒ Direct Award at East Midlands Trains through to at least August 2019

expected shortly‒ More than 20 years' experience of delivering benefits for customers,

taxpayers, investors Williams rail review presents opportunity for a more sustainable franchising

model and a successful railway for customers and taxpayers

22

Strong Group financial position and positive outlook

Disciplined capital investment across the business

Increase in expected 2018/19 adjusted earnings per share

Brexit risks evaluated and manageable

Opportunities from innovation, new initiatives and growing pressure on government to address congestion and air quality

23

INTERIM RESULTSHALF-YEAR ENDED 27 OCTOBER 2018

24

APPENDICES

25

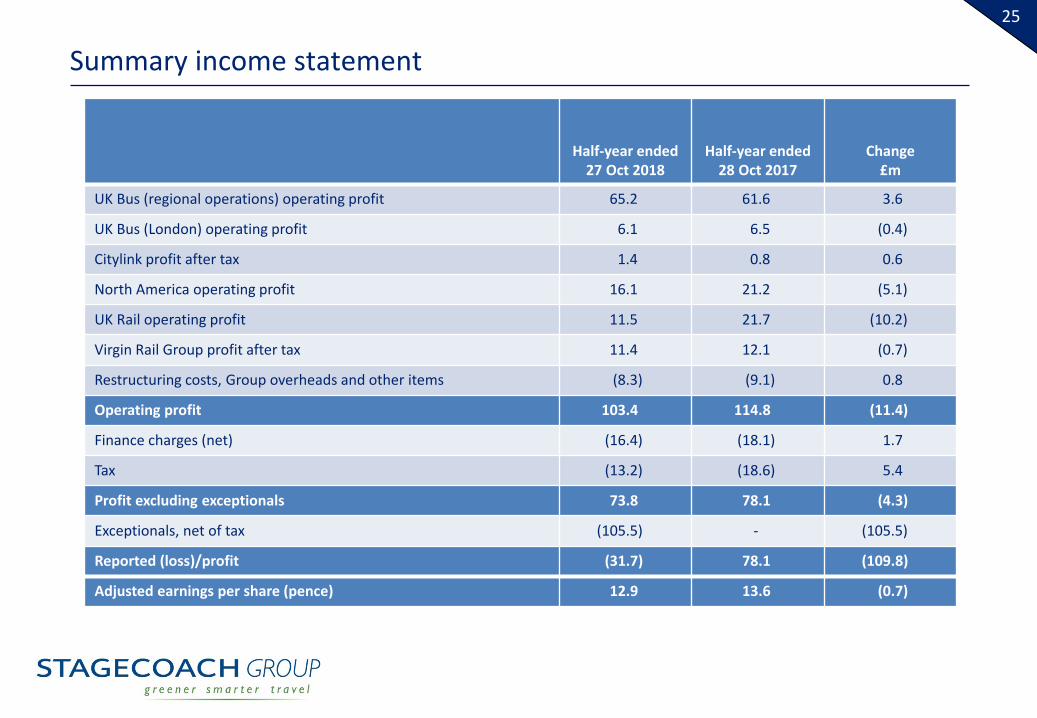

Summary income statement

Half-year ended27 Oct 2018

Half-year ended28 Oct 2017

Change£m

UK Bus (regional operations) operating profit 65.2 61.6 3.6

UK Bus (London) operating profit 6.1 6.5 (0.4)

Citylink profit after tax 1.4 0.8 0.6

North America operating profit 16.1 21.2 (5.1)

UK Rail operating profit 11.5 21.7 (10.2)

Virgin Rail Group profit after tax 11.4 12.1 (0.7)

Restructuring costs, Group overheads and other items (8.3) (9.1) 0.8

Operating profit 103.4 114.8 (11.4)

Finance charges (net) (16.4) (18.1) 1.7

Tax (13.2) (18.6) 5.4

Profit excluding exceptionals 73.8 78.1 (4.3)

Exceptionals, net of tax (105.5) - (105.5)

Reported (loss)/profit (31.7) 78.1 (109.8)

Adjusted earnings per share (pence) 12.9 13.6 (0.7)

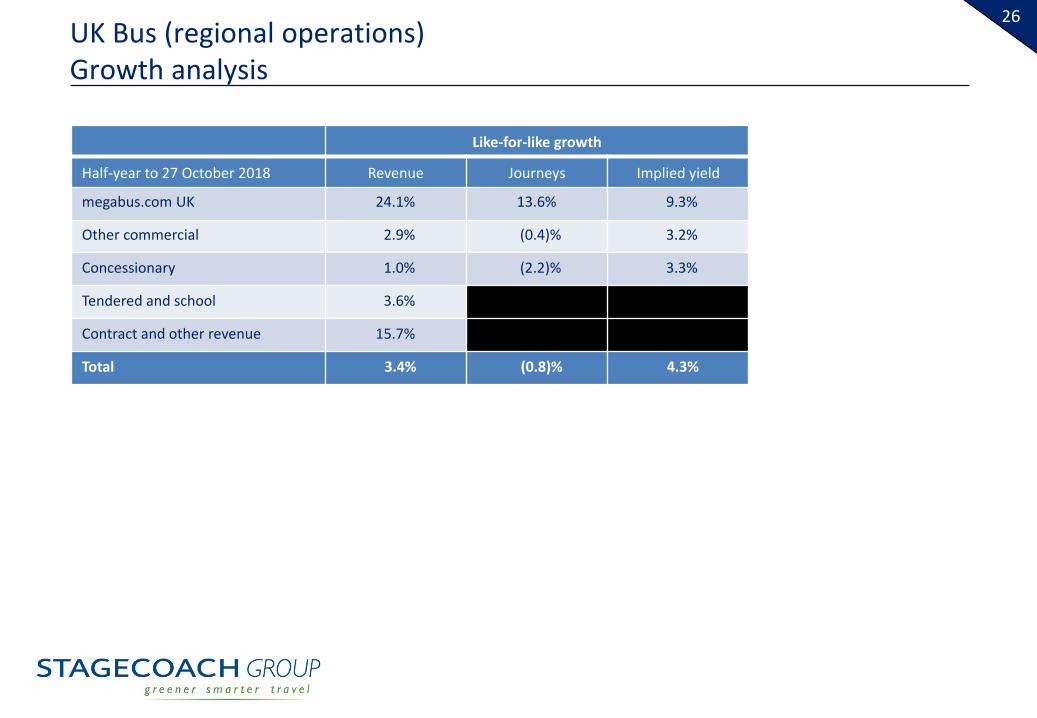

26UK Bus (regional operations)Growth analysis

Like-for-like growth

Half-year to 27 October 2018 Revenue Journeys Implied yield

megabus.com UK 24.1% 13.6% 9.3%

Other commercial 2.9% (0.4)% 3.2%

Concessionary 1.0% (2.2)% 3.3%

Tendered and school 3.6%

Contract and other revenue 15.7%

Total 3.4% (0.8)% 4.3%

27

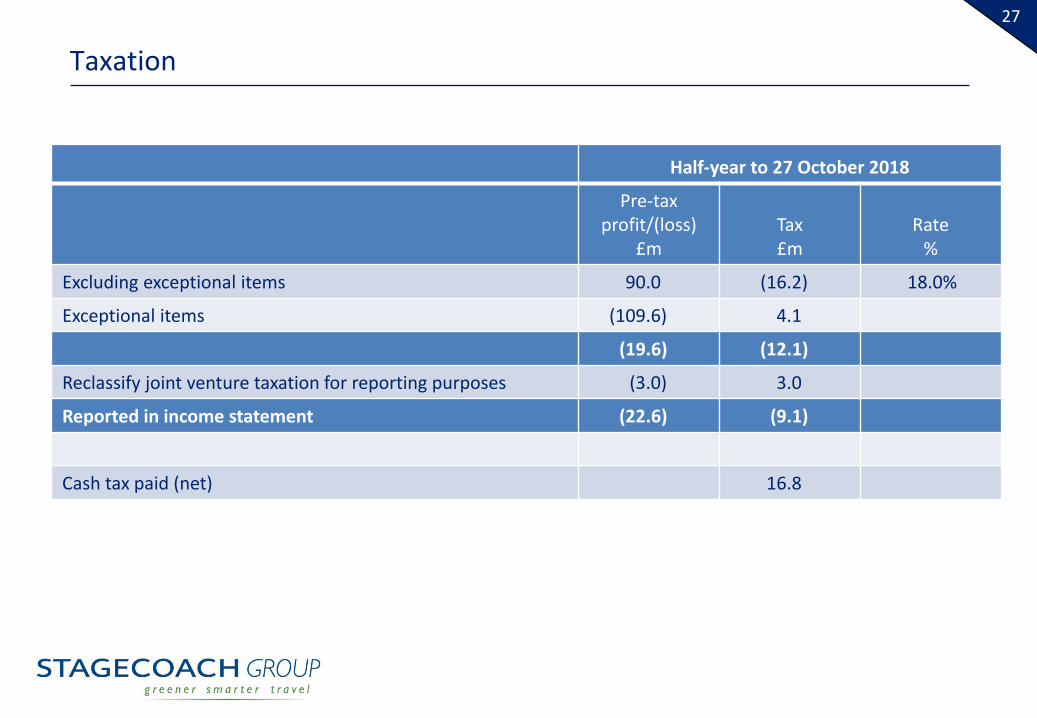

Taxation

Half-year to 27 October 2018

Pre-tax profit/(loss)

£mTax£m

Rate%

Excluding exceptional items 90.0 (16.2) 18.0%

Exceptional items (109.6) 4.1

(19.6) (12.1)

Reclassify joint venture taxation for reporting purposes (3.0) 3.0

Reported in income statement (22.6) (9.1)

Cash tax paid (net) 16.8

28

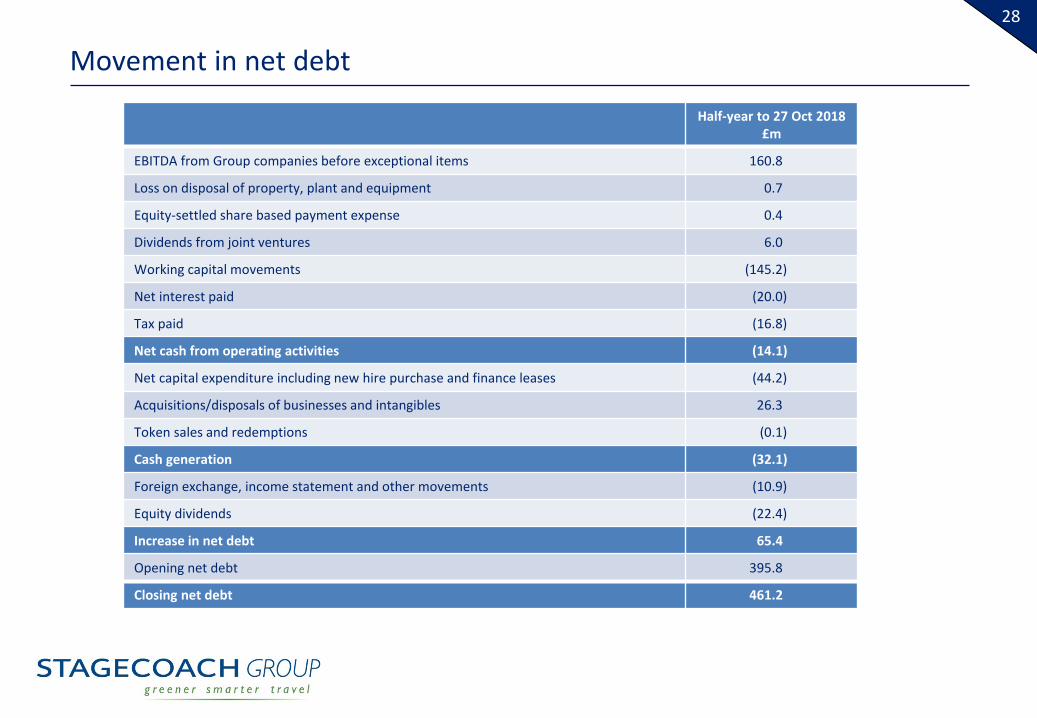

Movement in net debt

Half-year to 27 Oct 2018£m

EBITDA from Group companies before exceptional items 160.8

Loss on disposal of property, plant and equipment 0.7

Equity-settled share based payment expense 0.4

Dividends from joint ventures 6.0

Working capital movements (145.2)

Net interest paid (20.0)

Tax paid (16.8)

Net cash from operating activities (14.1)

Net capital expenditure including new hire purchase and finance leases (44.2)

Acquisitions/disposals of businesses and intangibles 26.3

Token sales and redemptions (0.1)

Cash generation (32.1)

Foreign exchange, income statement and other movements (10.9)

Equity dividends (22.4)

Increase in net debt 65.4

Opening net debt 395.8

Closing net debt 461.2

29

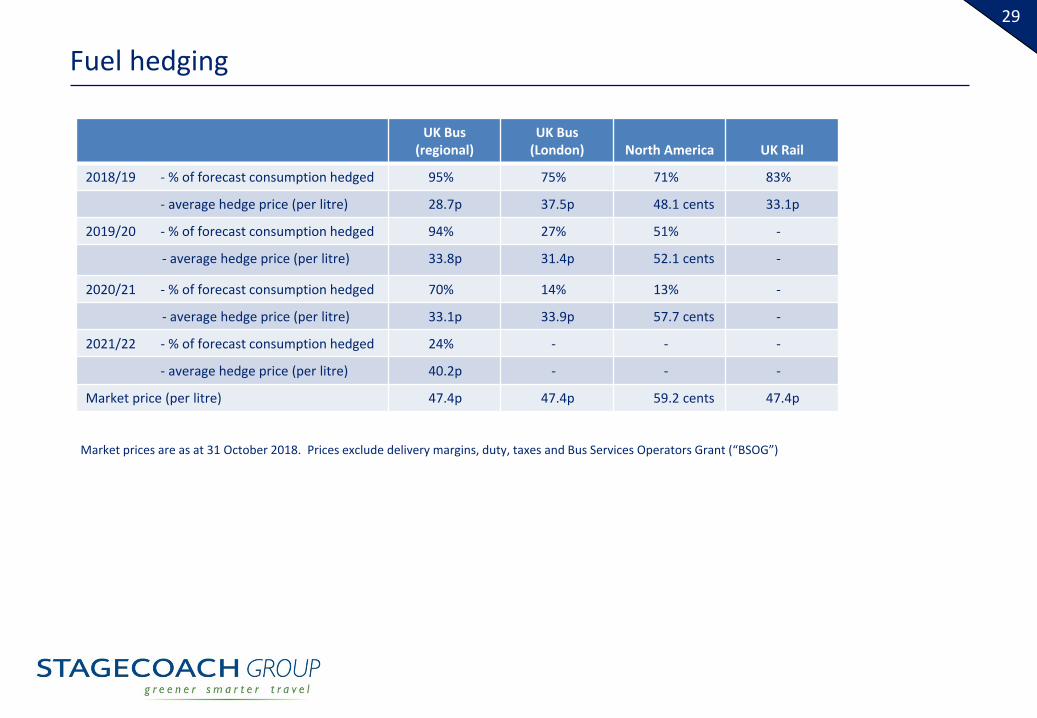

Fuel hedging

UK Bus(regional)

UK Bus (London) North America UK Rail

2018/19 - % of forecast consumption hedged 95% 75% 71% 83%

- average hedge price (per litre) 28.7p 37.5p 48.1 cents 33.1p

2019/20 - % of forecast consumption hedged 94% 27% 51% -

- average hedge price (per litre) 33.8p 31.4p 52.1 cents -

2020/21 - % of forecast consumption hedged 70% 14% 13% -

- average hedge price (per litre) 33.1p 33.9p 57.7 cents -

2021/22 - % of forecast consumption hedged 24% - - -

- average hedge price (per litre) 40.2p - - -

Market price (per litre) 47.4p 47.4p 59.2 cents 47.4p

Market prices are as at 31 October 2018. Prices exclude delivery margins, duty, taxes and Bus Services Operators Grant (“BSOG”)

30

Definitions

Like-for-like amounts are derived, on a constant currency basis, by comparing the relevant year-to-date amount with the equivalent prior year period for those businesses and individual operating units that have been part of the Group throughout both periods. Where the number of days differs between the current and prior year periods, the prior year amount is normalised for that when calculating like-for-like amounts.

Operating profit or loss for a particular business unit or division within the Group refers to profit or loss before net finance income/costs, taxation, non-controlling interests, non-software intangible asset amortisation, exceptional items and restructuring costs.

Operating margin for a particular business unit or division within the Group means operating profit or loss as a percentage of revenue.

Exceptional items means items which individually or, if of a similar type, in aggregate need to be disclosed by virtue of their nature, size or incidence in order to allow a proper understanding of the underlying financial performance of the Group.

Gross debt is borrowings as reported on the consolidated balance sheet, adjusted to exclude accrued interest and the effect of fair value hedges on the carrying value of borrowings.

Net debt (or net funds) is the net of cash/cash equivalents and gross debt.

TfL refers to Transport for London, a governmental body.

31

INTERIM RESULTSHALF-YEAR ENDED 27 OCTOBER 2018