Embed Size (px)

Citation preview

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1

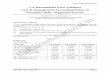

INTERMEDIATE EXAMINATION Syllabus 2016

Paper 10: COST & MANAGEMENT ACCOUNTING AND FINANCIAL MANAGEMENT (CMFM)

Time Allowed: 3 Hours Full Marks: 100

There are Sections A, B, C and D to be answered subject to instructions given against each. (Time allotted for Sections A and B shall be limited to a maximum of 50 minutes)

Section A 20 Marks

1. You are required to answer all the questions. Each question carries 1 mark. Instructions: Each question is followed by 4 Answer choices and only one is correct. You are

required to select the choice which according to you represents the correct answer.

20 X 1 = 20

a. Type of accounting which measures, reports and analyse non-financial and financial

information to help in decision making is called:

(i) Financial Accounting (ii) Management Accounting A (iii) Cost Accounting (iv) Green Accounting b. Which of the following is the main objective of financial management? (i) Revenue Maximisation (ii) Profit Maximisation (iii) Wealth Maximisation A (iv) Cost Minimisation c. In cost accounting, purpose of variance analysis is to: (i) understand reasons for variances. (ii) take remedial measures. (iii) improve future performance. (iv) All of the above A d. Which of the following forms of equity financing is especially designed for funding

High Risk & High Reward projects?

(i) ADR (ii) GDR (iii) FCCB (iv) Venture Capital A e. Absorption Costing is also known as: (i) Total Costing A (ii) Committed Costing (iii) Target Costing (iv) Discretionary Costing f. Which one of the following activities is outside the purview of financing decision in

financial management?

(i) Identification of the source of funds (ii) Measurement of the cost of funds

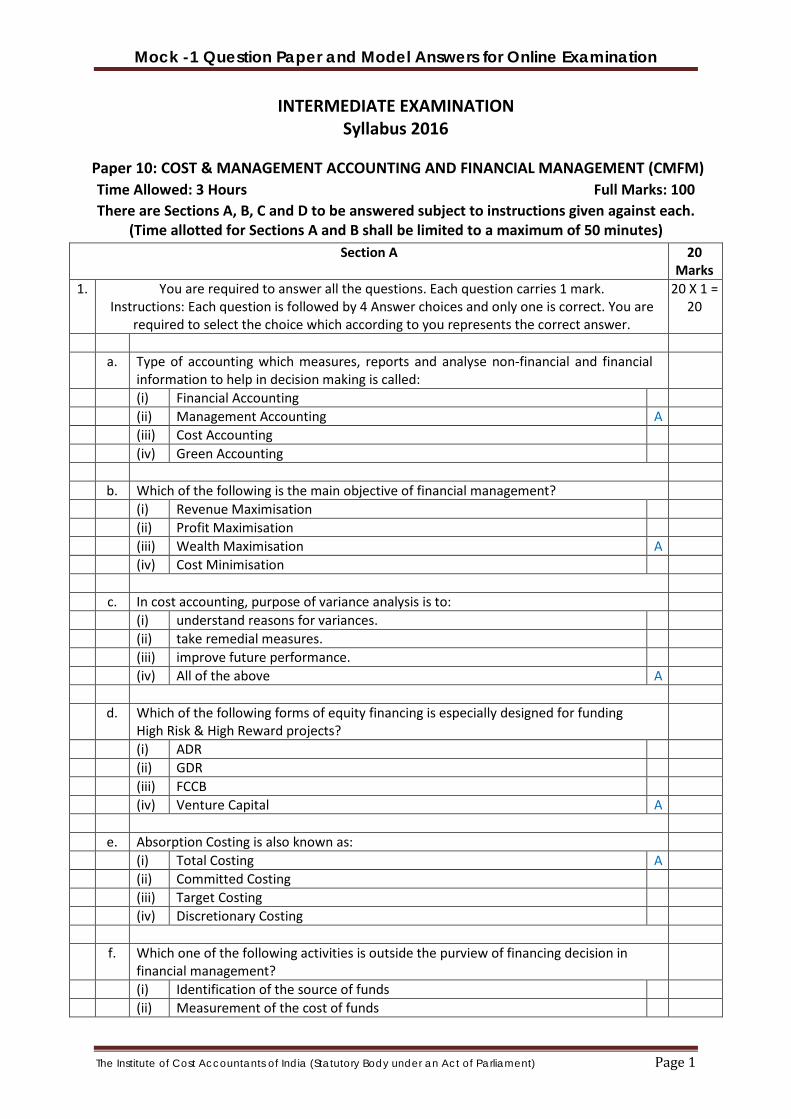

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 2

(iii) Deciding on the time of raising the funds (iv) Deciding on the utilization of the funds A g. Which one of the following is not to be considered for preparing a production budget? (i) The production plan of the organization (ii) The Sales Budget (iii) Research and Development Budget A (iv) Availability of Raw Materials h. In Net Profit Ratio, the denominator is: (i) Credit Sales (ii) Net Sales A (iii) Cost of Sales (iv) Cost of Goods Sold i. Which one of the following is not considered as a method of Transfer Pricing? (i) Negotiated Transfer Pricing (ii) Market Price Based Transfer Pricing (iii) Fixed Cost Based Transfer Pricing A (iv) Opportunity Cost Based Transfer Pricing j. A process through which loans and other receivables are underwritten and sold in a

form of asset is known as:

(i) Factoring (ii) Forfeiting (iii) Securitisation A (iv) Bill Discounting k. In a factory when production is increased within the relevant range then: (i) variable costs will vary on a per unit basis. (ii) variable costs will vary in total. A (iii) fixed costs will vary in total. (iv) fixed and variable cost stay the same in total. l. Which of the following is a Profitability Ratio? (i) Proprietary Ratio (ii) Debt-Equity Ratio (iii) Price-Earning Ratio A (iv) Fixed Asset Ratio m. The main objective of budgetary control is: (i) to define the goal of the firm (ii) to coordinate different departments A (iii) to plan to achieve its goals (iv) All of the above n. Which of the following does not help to increase Current Ratio? (i) Issue of Debentures to buy Stock (ii) Issue of Debentures to pay Creditors (iii) Sale of Investment to pay Creditors

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 3

(iv) Avail Bank Overdraft to buy Machine A o. What is the name of the method of pricing, when two separate pricing methods are

used to price transfer of products from one subunit to another?

(i) Dual pricing A (ii) Functional pricing (iii) Congruent pricing (iv) Optimal pricing p. The excess of Current Assets over Current Liabilities is called ____________ .

Fill in the blank from among the choices as below.

(i) Net Current Assets (ii) Net Working Capital (iii) Working Capital (iv) All of the above A

q. When are overhead variances recorded in a standard costing system? (i) When the goods are transferred out of work-in-progress. (ii) When the factory overhead is applied to work-in-progress. A (iii) When the cost of goods sold is recorded. (iv) When the direct labour is recorded.

r. Which of the following statements is correct? (i) A higher Receivable Turnover is not desirable. (ii) Interest Coverage Ratio depends upon Tax Rate. (iii) Increase in Net Profit Ratio means increase in Sales. (iv) Lower Debt-Equity Ratio means lower Financial Risk. A

s. Which of the following factors does not affect Learning Curve? (i) Method of Production (ii) Labour Strike (iii) Shut Down (iv) All of the above A t. Which of the following statements is correct? (i) A higher Receivable Turnover is not desirable. (ii) Interest Coverage Ratio depends upon Tax Rate. (iii) Increase in Net Profit Ratio means increase in Sales. (iv) Lower Debt-Equity Ratio means lower Financial Risk. A

Section B 20 Marks

2. You are required to answer all the questions. Each question carries 1 mark. Instructions: Each question is followed by a space where you are required to type your answer.

20 X 1 = 20

a. If EBIT = Rs. 1,00,000, Fixed Assets = Rs. 2,00,000, Sales = Rs. 10,00,000 and Variable

Cost = Rs. 7,00,000. Then, the Operating Leverage will be ______ .

Type your answer here 3

b. Fill up the blank below with an appropriate word.

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 4

Another name for the ‘Learning Curve is an _______ Curve’. Type your answer here Experience

c. Modigliani and Miller Hypothesis is a ______________ model. Fill up the blank above with an appropriate word.

Type your answer here Dividend

d. Fill up the blank below with appropriate word(s). __________ is that notional value at which goods and services are transferred between divisions in a decentralized organization.

Type your answer here Transfer Price

e. Debt Service Coverage Ratio indicates the liquidity of a firm in relation to its ability to meet projected daily expenditure from operations. Is the above statement true or false?

Type your answer here False

f. Match the statement under Column I with the most appropriate statement under Column II: Column I Column II Theory of Capital Structure (i) Indicator of Short-term solvency of a company

(ii) Gordon Model

Type your answer here Theory of capital structure - (ii) Gordon Model g. Standard Costing are applicable in Banking Industry.

Identify whether the above statement is true or false.

Type your answer here False h. Fill up the blank below with appropriate word(s).

Liquid ratio is the indicator of ______________ solvency of a company.

Type your answer here Short term i. Column I Column II

Distinctive feature of Learning curve

(i) Persons engaged in repetitive task will improve his performance over time.

(ii) on the principle of exception.

Type your answer here Distinctive feature of Learning curve (i) Persons engaged in repetitive task will improve his performance over time.

j. State whether the following statement is True or False:

Capital Budgetary Forecasts Returns on proposed long-term investments and compares profitability of different Investments and their cost of capital.

Type your answer here True k. State whether the following statement is True or False:

Management Accounting is largely based on estimates and as such total accuracy is not ensured under Management Accountancy.

Type your answer here True l. Who said “Value of share is worth the present value of its future Dividend rather than

its earnings”?

Type your answer here John Burr Williams

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 5

m. Which item in Column II is an appropriate match for the item in Column I?

Column I Column II

Difference between costs of two alternatives (i) Break-Even Analysis (ii) Differential Cost

Type your answer here (ii) Differential Cost n. Fill up the blank with appropriate word(s).

As per the Graham and Dodd Model, Market Price of share will ______ when company declares dividend rather than when it does not.

Type your answer here increase o. Under ______ costing, Fixed Costs are charged to Cost of Production.

Fill up the blank above with an appropriate word.

Type your answer here Absorption p. State whether the following statement is True or False:

A Depository Receipt in the US market is called American Depository Receipt (ADR).

Type your answer here True q. A firm has a capital of Rs. 10 lakhs, sales of Rs. 5 lakhs, gross profit of Rs. 2 lakhs and

expenses of Rs.1 lakh. What is the Net Profit Ratio?

Type your answer here 20% r. Net Present Value method cannot serve as the best decision criteria for selection of

projects when they are mutually exclusive. Do you Accept or Reject the sentence above?

Type your answer here Reject s. Other variables remaining constant, a hike in selling price per unit will_____ the Break

Even Point. Fill up the blank above with an appropriate word.

Type your answer here lower t. Identify the correctly matched pair of statements:

Column A Column B 1. Leverage (i) Raise Short Term Finance through Receivables 2. Stochastic Model (ii) Control Limits

Type your answer here Correctly matched pair: Column A, Item: 2. Stochastic Model Column B, Item: ii. Control Limits

Section C 40

Marks You are required to answer any 4 out of 6 questions in this section

Instructions: Each question is followed by a space where you are required to type your answer. 10 X 4 =

40

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 6

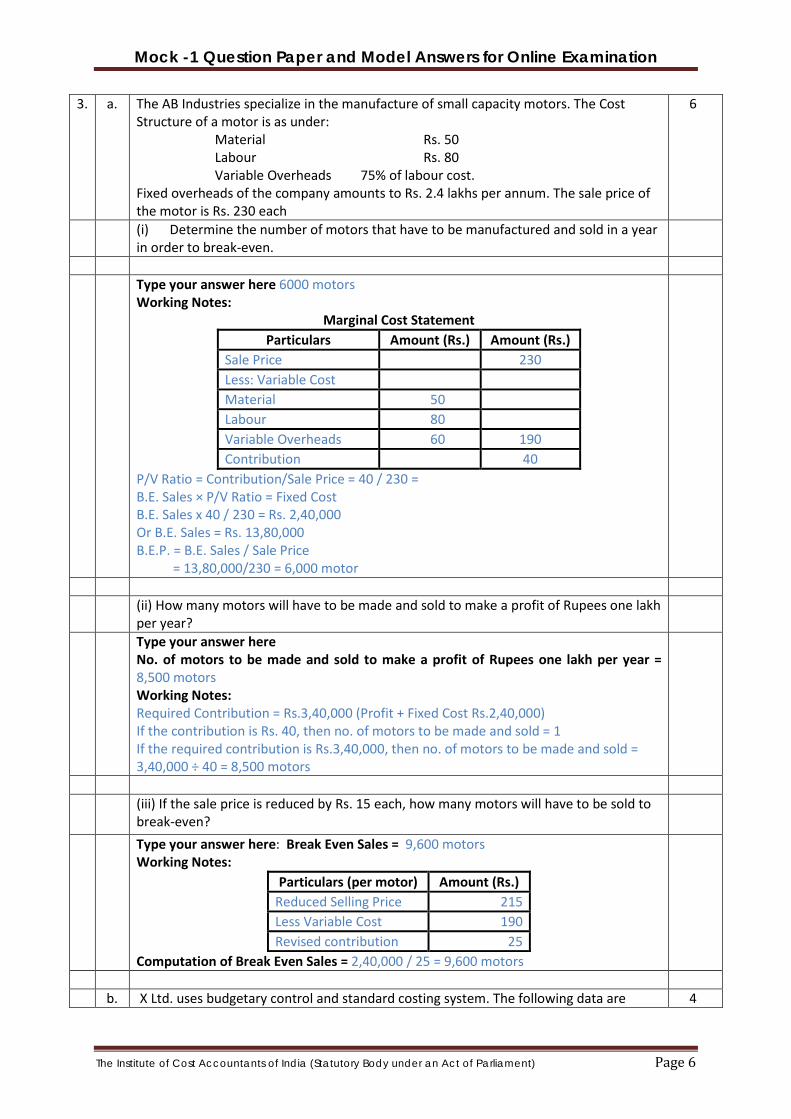

3. a. The AB Industries specialize in the manufacture of small capacity motors. The Cost Structure of a motor is as under:

Material Rs. 50 Labour Rs. 80 Variable Overheads 75% of labour cost.

Fixed overheads of the company amounts to Rs. 2.4 lakhs per annum. The sale price of the motor is Rs. 230 each

6

(i) Determine the number of motors that have to be manufactured and sold in a year in order to break-even.

Type your answer here 6000 motors

Working Notes: Marginal Cost Statement

Particulars Amount (Rs.) Amount (Rs.) Sale Price 230 Less: Variable Cost Material 50 Labour 80 Variable Overheads 60 190 Contribution 40

P/V Ratio = Contribution/Sale Price = 40 / 230 = B.E. Sales × P/V Ratio = Fixed Cost B.E. Sales x 40 / 230 = Rs. 2,40,000 Or B.E. Sales = Rs. 13,80,000 B.E.P. = B.E. Sales / Sale Price = 13,80,000/230 = 6,000 motor

(ii) How many motors will have to be made and sold to make a profit of Rupees one lakh

per year?

Type your answer here No. of motors to be made and sold to make a profit of Rupees one lakh per year = 8,500 motors Working Notes: Required Contribution = Rs.3,40,000 (Profit + Fixed Cost Rs.2,40,000) If the contribution is Rs. 40, then no. of motors to be made and sold = 1 If the required contribution is Rs.3,40,000, then no. of motors to be made and sold = 3,40,000 ÷ 40 = 8,500 motors

(iii) If the sale price is reduced by Rs. 15 each, how many motors will have to be sold to

break-even?

Type your answer here: Break Even Sales = 9,600 motors Working Notes:

Particulars (per motor) Amount (Rs.) Reduced Selling Price 215 Less Variable Cost 190 Revised contribution 25

Computation of Break Even Sales = 2,40,000 / 25 = 9,600 motors

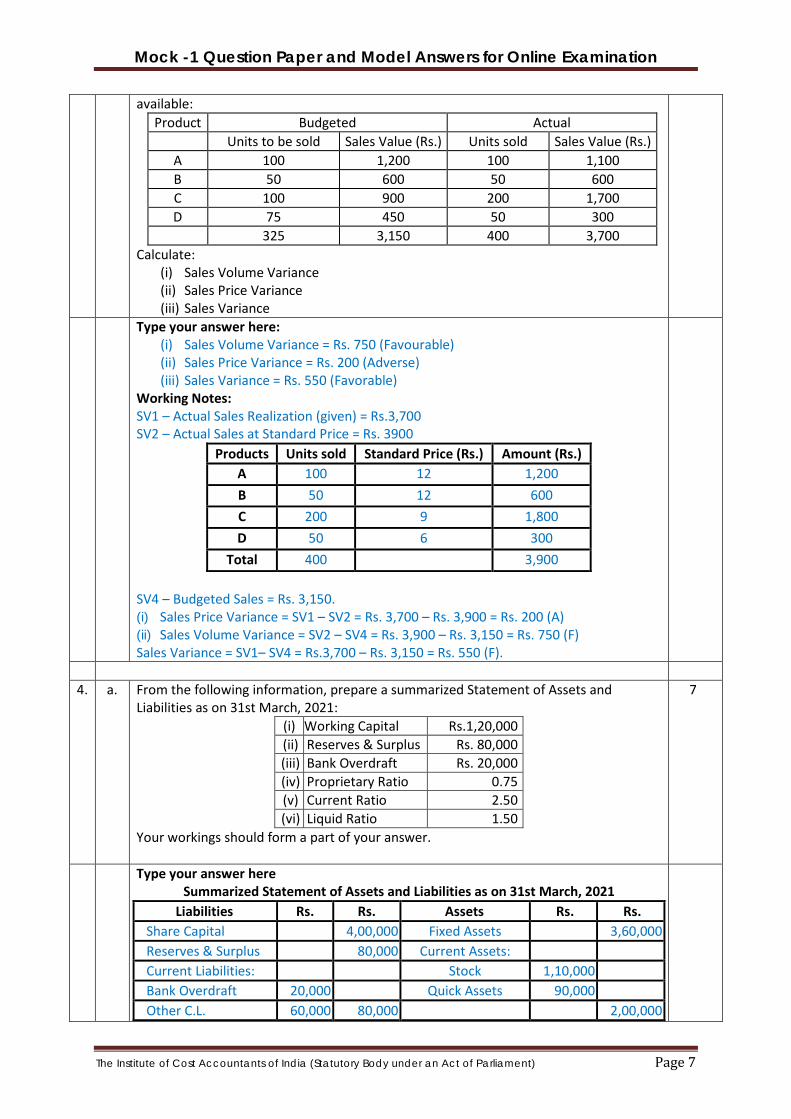

b. X Ltd. uses budgetary control and standard costing system. The following data are 4

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 7

available: Product Budgeted Actual

Units to be sold Sales Value (Rs.) Units sold Sales Value (Rs.) A 100 1,200 100 1,100 B 50 600 50 600 C 100 900 200 1,700 D 75 450 50 300 325 3,150 400 3,700

Calculate: (i) Sales Volume Variance (ii) Sales Price Variance (iii) Sales Variance

Type your answer here: (i) Sales Volume Variance = Rs. 750 (Favourable) (ii) Sales Price Variance = Rs. 200 (Adverse) (iii) Sales Variance = Rs. 550 (Favorable)

Working Notes: SV1 – Actual Sales Realization (given) = Rs.3,700 SV2 – Actual Sales at Standard Price = Rs. 3900

Products Units sold Standard Price (Rs.) Amount (Rs.) A 100 12 1,200

B 50 12 600

C 200 9 1,800

D 50 6 300

Total 400 3,900

SV4 – Budgeted Sales = Rs. 3,150. (i) Sales Price Variance = SV1 – SV2 = Rs. 3,700 – Rs. 3,900 = Rs. 200 (A) (ii) Sales Volume Variance = SV2 – SV4 = Rs. 3,900 – Rs. 3,150 = Rs. 750 (F) Sales Variance = SV1– SV4 = Rs.3,700 – Rs. 3,150 = Rs. 550 (F).

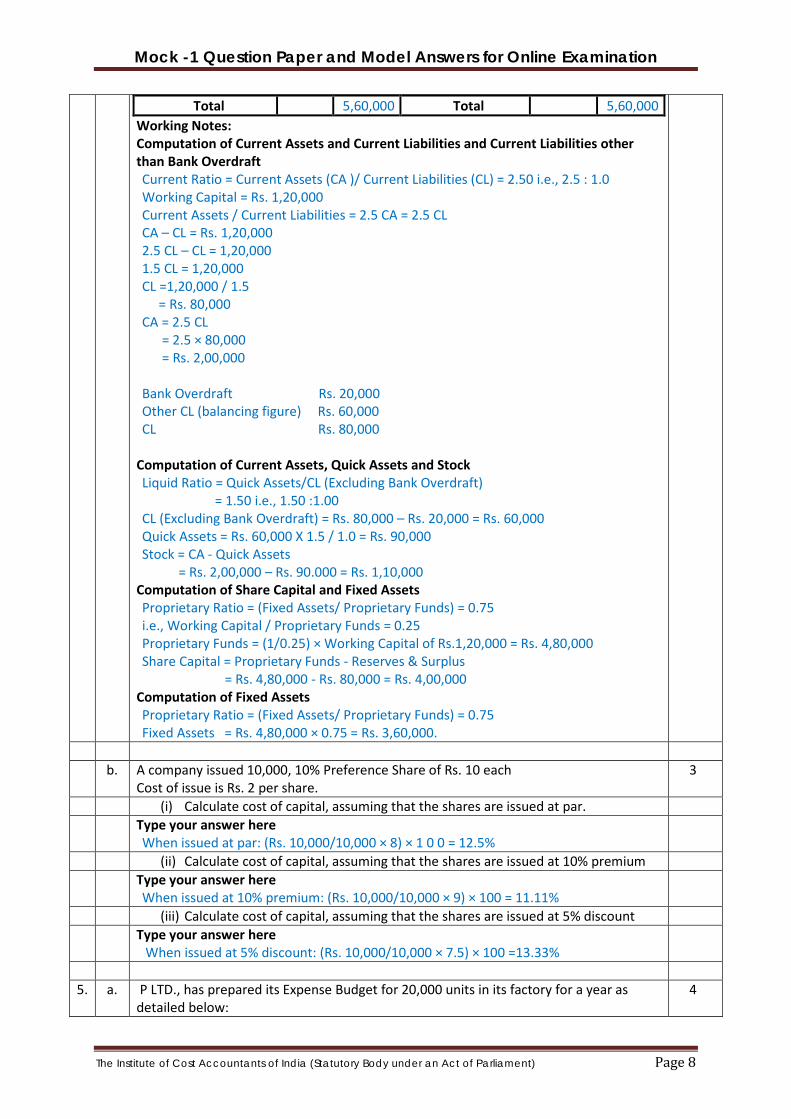

4. a. From the following information, prepare a summarized Statement of Assets and

Liabilities as on 31st March, 2021: (i) Working Capital Rs.1,20,000 (ii) Reserves & Surplus Rs. 80,000 (iii) Bank Overdraft Rs. 20,000 (iv) Proprietary Ratio 0.75 (v) Current Ratio 2.50 (vi) Liquid Ratio 1.50

Your workings should form a part of your answer.

7

Type your answer here Summarized Statement of Assets and Liabilities as on 31st March, 2021

Liabilities Rs. Rs. Assets Rs. Rs. Share Capital 4,00,000 Fixed Assets 3,60,000 Reserves & Surplus 80,000 Current Assets: Current Liabilities: Stock 1,10,000 Bank Overdraft 20,000 Quick Assets 90,000 Other C.L. 60,000 80,000 2,00,000

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 8

Total 5,60,000 Total 5,60,000 Working Notes: Computation of Current Assets and Current Liabilities and Current Liabilities other than Bank Overdraft Current Ratio = Current Assets (CA )/ Current Liabilities (CL) = 2.50 i.e., 2.5 : 1.0 Working Capital = Rs. 1,20,000 Current Assets / Current Liabilities = 2.5 CA = 2.5 CL CA – CL = Rs. 1,20,000 2.5 CL – CL = 1,20,000 1.5 CL = 1,20,000 CL =1,20,000 / 1.5 = Rs. 80,000 CA = 2.5 CL = 2.5 × 80,000 = Rs. 2,00,000 Bank Overdraft Rs. 20,000 Other CL (balancing figure) Rs. 60,000 CL Rs. 80,000

Computation of Current Assets, Quick Assets and Stock Liquid Ratio = Quick Assets/CL (Excluding Bank Overdraft) = 1.50 i.e., 1.50 :1.00 CL (Excluding Bank Overdraft) = Rs. 80,000 – Rs. 20,000 = Rs. 60,000 Quick Assets = Rs. 60,000 X 1.5 / 1.0 = Rs. 90,000 Stock = CA - Quick Assets = Rs. 2,00,000 – Rs. 90.000 = Rs. 1,10,000

Computation of Share Capital and Fixed Assets Proprietary Ratio = (Fixed Assets/ Proprietary Funds) = 0.75 i.e., Working Capital / Proprietary Funds = 0.25 Proprietary Funds = (1/0.25) × Working Capital of Rs.1,20,000 = Rs. 4,80,000 Share Capital = Proprietary Funds - Reserves & Surplus = Rs. 4,80,000 - Rs. 80,000 = Rs. 4,00,000

Computation of Fixed Assets Proprietary Ratio = (Fixed Assets/ Proprietary Funds) = 0.75 Fixed Assets = Rs. 4,80,000 × 0.75 = Rs. 3,60,000.

b. A company issued 10,000, 10% Preference Share of Rs. 10 each

Cost of issue is Rs. 2 per share. 3

(i) Calculate cost of capital, assuming that the shares are issued at par. Type your answer here

When issued at par: (Rs. 10,000/10,000 × 8) × 1 0 0 = 12.5%

(ii) Calculate cost of capital, assuming that the shares are issued at 10% premium Type your answer here

When issued at 10% premium: (Rs. 10,000/10,000 × 9) × 100 = 11.11%

(iii) Calculate cost of capital, assuming that the shares are issued at 5% discount Type your answer here

When issued at 5% discount: (Rs. 10,000/10,000 × 7.5) × 100 =13.33%

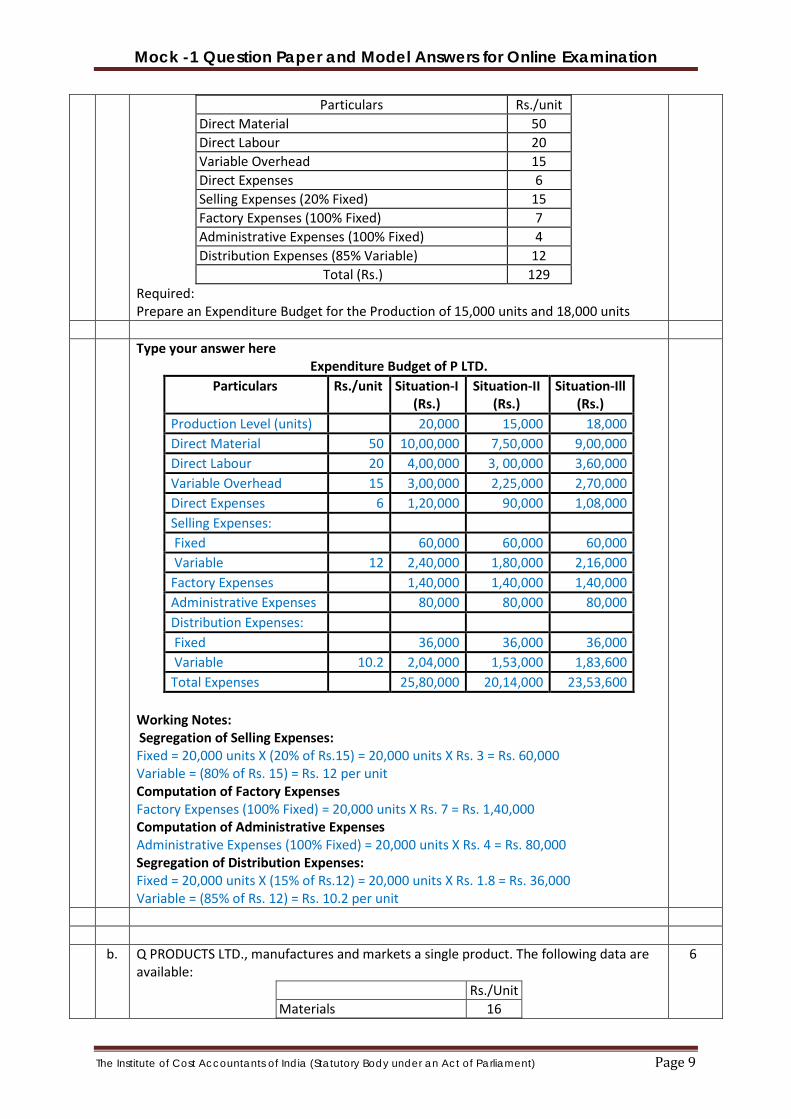

5. a. P LTD., has prepared its Expense Budget for 20,000 units in its factory for a year as

detailed below: 4

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 9

Particulars Rs./unit Direct Material 50 Direct Labour 20 Variable Overhead 15 Direct Expenses 6 Selling Expenses (20% Fixed) 15 Factory Expenses (100% Fixed) 7 Administrative Expenses (100% Fixed) 4 Distribution Expenses (85% Variable) 12

Total (Rs.) 129 Required: Prepare an Expenditure Budget for the Production of 15,000 units and 18,000 units

Type your answer here

Expenditure Budget of P LTD. Particulars Rs./unit Situation-I

(Rs.) Situation-II

(Rs.) Situation-Ill

(Rs.) Production Level (units) 20,000 15,000 18,000 Direct Material 50 10,00,000 7,50,000 9,00,000 Direct Labour 20 4,00,000 3, 00,000 3,60,000 Variable Overhead 15 3,00,000 2,25,000 2,70,000 Direct Expenses 6 1,20,000 90,000 1,08,000 Selling Expenses: Fixed 60,000 60,000 60,000 Variable 12 2,40,000 1,80,000 2,16,000 Factory Expenses 1,40,000 1,40,000 1,40,000 Administrative Expenses 80,000 80,000 80,000 Distribution Expenses: Fixed 36,000 36,000 36,000 Variable 10.2 2,04,000 1,53,000 1,83,600 Total Expenses 25,80,000 20,14,000 23,53,600

Working Notes: Segregation of Selling Expenses: Fixed = 20,000 units X (20% of Rs.15) = 20,000 units X Rs. 3 = Rs. 60,000 Variable = (80% of Rs. 15) = Rs. 12 per unit Computation of Factory Expenses Factory Expenses (100% Fixed) = 20,000 units X Rs. 7 = Rs. 1,40,000 Computation of Administrative Expenses Administrative Expenses (100% Fixed) = 20,000 units X Rs. 4 = Rs. 80,000 Segregation of Distribution Expenses: Fixed = 20,000 units X (15% of Rs.12) = 20,000 units X Rs. 1.8 = Rs. 36,000 Variable = (85% of Rs. 12) = Rs. 10.2 per unit

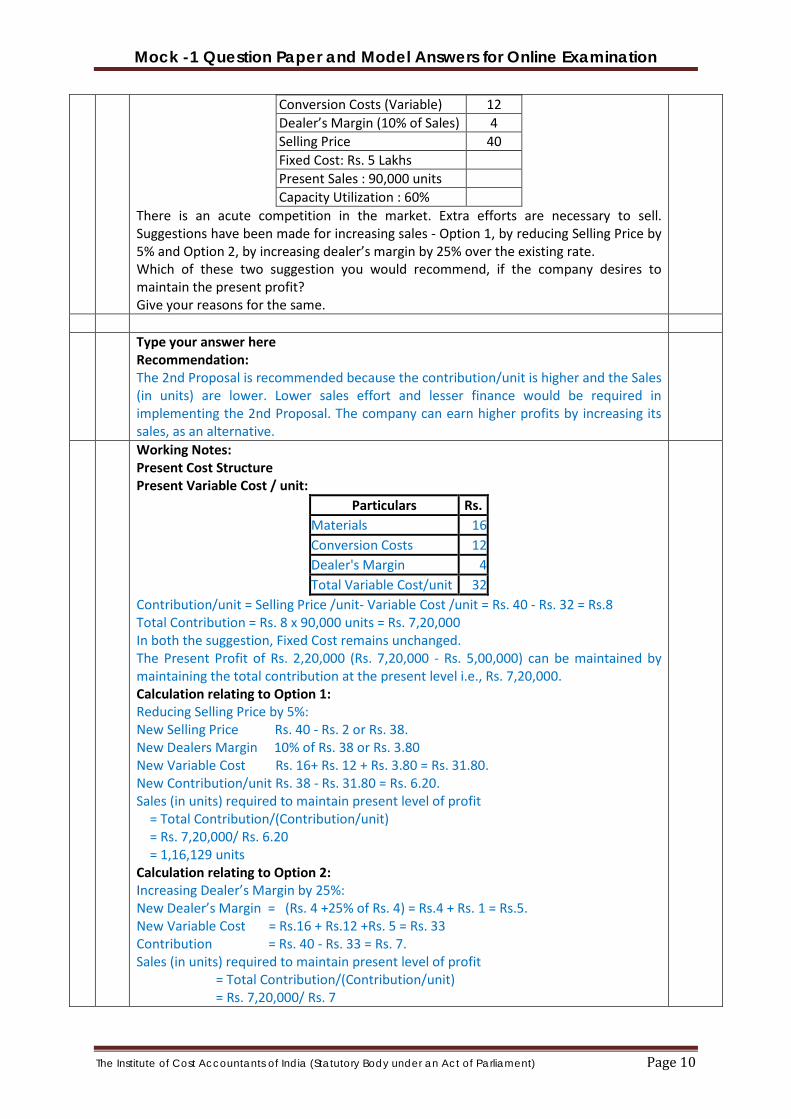

b. Q PRODUCTS LTD., manufactures and markets a single product. The following data are

available: Rs./Unit Materials 16

6

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 10

Conversion Costs (Variable) 12 Dealer’s Margin (10% of Sales) 4 Selling Price 40 Fixed Cost: Rs. 5 Lakhs Present Sales : 90,000 units Capacity Utilization : 60%

There is an acute competition in the market. Extra efforts are necessary to sell. Suggestions have been made for increasing sales - Option 1, by reducing Selling Price by 5% and Option 2, by increasing dealer’s margin by 25% over the existing rate. Which of these two suggestion you would recommend, if the company desires to maintain the present profit? Give your reasons for the same.

Type your answer here

Recommendation: The 2nd Proposal is recommended because the contribution/unit is higher and the Sales (in units) are lower. Lower sales effort and lesser finance would be required in implementing the 2nd Proposal. The company can earn higher profits by increasing its sales, as an alternative.

Working Notes: Present Cost Structure Present Variable Cost / unit:

Particulars Rs. Materials 16 Conversion Costs 12 Dealer's Margin 4 Total Variable Cost/unit 32

Contribution/unit = Selling Price /unit- Variable Cost /unit = Rs. 40 - Rs. 32 = Rs.8 Total Contribution = Rs. 8 x 90,000 units = Rs. 7,20,000 In both the suggestion, Fixed Cost remains unchanged. The Present Profit of Rs. 2,20,000 (Rs. 7,20,000 - Rs. 5,00,000) can be maintained by maintaining the total contribution at the present level i.e., Rs. 7,20,000. Calculation relating to Option 1: Reducing Selling Price by 5%: New Selling Price Rs. 40 - Rs. 2 or Rs. 38. New Dealers Margin 10% of Rs. 38 or Rs. 3.80 New Variable Cost Rs. 16+ Rs. 12 + Rs. 3.80 = Rs. 31.80. New Contribution/unit Rs. 38 - Rs. 31.80 = Rs. 6.20. Sales (in units) required to maintain present level of profit = Total Contribution/(Contribution/unit) = Rs. 7,20,000/ Rs. 6.20 = 1,16,129 units Calculation relating to Option 2: Increasing Dealer’s Margin by 25%: New Dealer’s Margin = (Rs. 4 +25% of Rs. 4) = Rs.4 + Rs. 1 = Rs.5. New Variable Cost = Rs.16 + Rs.12 +Rs. 5 = Rs. 33 Contribution = Rs. 40 - Rs. 33 = Rs. 7. Sales (in units) required to maintain present level of profit = Total Contribution/(Contribution/unit) = Rs. 7,20,000/ Rs. 7

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 11

= 1,02,857 units

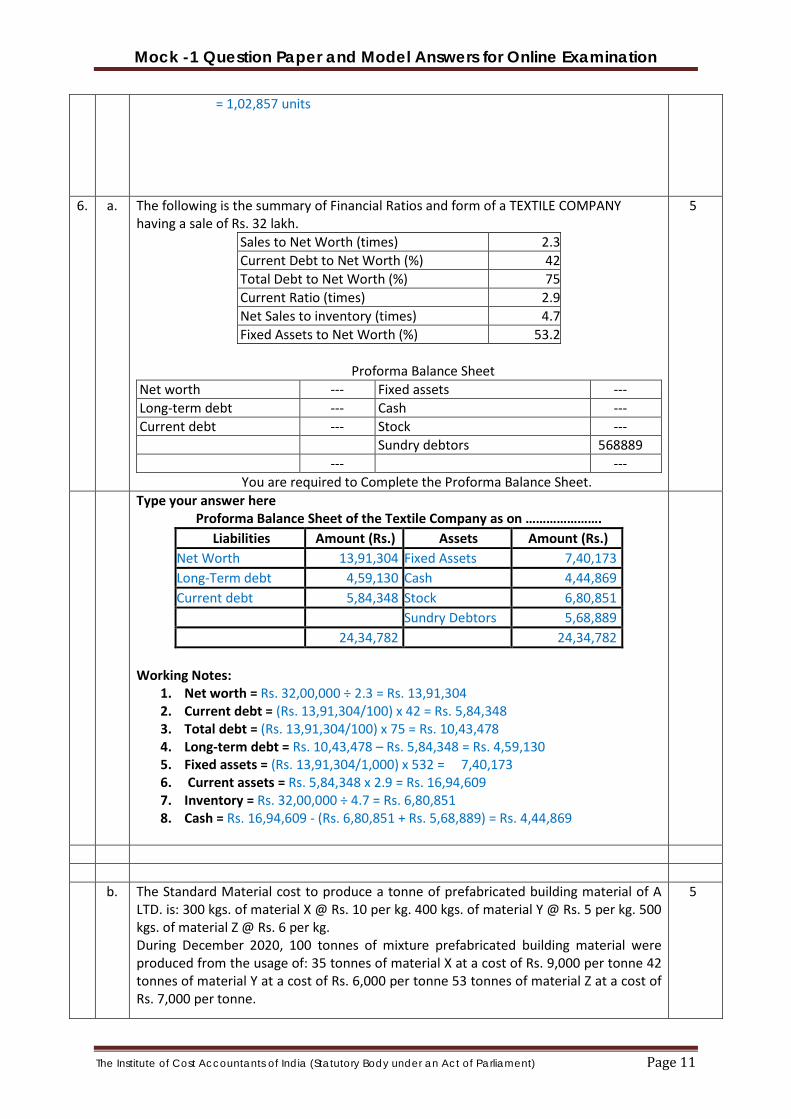

6. a. The following is the summary of Financial Ratios and form of a TEXTILE COMPANY having a sale of Rs. 32 lakh.

Sales to Net Worth (times) 2.3 Current Debt to Net Worth (%) 42 Total Debt to Net Worth (%) 75 Current Ratio (times) 2.9 Net Sales to inventory (times) 4.7 Fixed Assets to Net Worth (%) 53.2

Proforma Balance Sheet

Net worth --- Fixed assets --- Long-term debt --- Cash --- Current debt --- Stock --- Sundry debtors 568889 --- ---

You are required to Complete the Proforma Balance Sheet.

5

Type your answer here Proforma Balance Sheet of the Textile Company as on ………………….

Liabilities Amount (Rs.) Assets Amount (Rs.) Net Worth 13,91,304 Fixed Assets 7,40,173 Long-Term debt 4,59,130 Cash 4,44,869 Current debt 5,84,348 Stock 6,80,851 Sundry Debtors 5,68,889 24,34,782 24,34,782

Working Notes:

1. Net worth = Rs. 32,00,000 ÷ 2.3 = Rs. 13,91,304 2. Current debt = (Rs. 13,91,304/100) x 42 = Rs. 5,84,348 3. Total debt = (Rs. 13,91,304/100) x 75 = Rs. 10,43,478 4. Long-term debt = Rs. 10,43,478 – Rs. 5,84,348 = Rs. 4,59,130 5. Fixed assets = (Rs. 13,91,304/1,000) x 532 = 7,40,173 6. Current assets = Rs. 5,84,348 x 2.9 = Rs. 16,94,609 7. Inventory = Rs. 32,00,000 ÷ 4.7 = Rs. 6,80,851 8. Cash = Rs. 16,94,609 - (Rs. 6,80,851 + Rs. 5,68,889) = Rs. 4,44,869

b. The Standard Material cost to produce a tonne of prefabricated building material of A

LTD. is: 300 kgs. of material X @ Rs. 10 per kg. 400 kgs. of material Y @ Rs. 5 per kg. 500 kgs. of material Z @ Rs. 6 per kg. During December 2020, 100 tonnes of mixture prefabricated building material were produced from the usage of: 35 tonnes of material X at a cost of Rs. 9,000 per tonne 42 tonnes of material Y at a cost of Rs. 6,000 per tonne 53 tonnes of material Z at a cost of Rs. 7,000 per tonne.

5

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 12

(i) Calculate Total Material Cost Variance Type your answer here

Total Material Cost Variance: Standard Cost for Actual Quantity - Actual Cost = Rs. 8,00,000 – Rs. 9,38,000 = Rs. 1,38,000 (A) Working Notes:

Material Standard Actual Quantity

(Kg.) Rate (Rs.)

Amount (Rs.)

Quantity (Kg.)

Rate (Rs.)

Amount (Rs.)

X 30,000 10.00 3,00,000 35,000 9.00 3,15,000 Y 40,000 5.00 2,00,000 42,000 6.00 2,52,000 Z 50,000 6.00 3,00,000 53,000 7.00 3,71,000

Total 1,20,000 8,00,000 1,30,000 9,38,000

(ii) Calculate Total and Individual Material Price Variances Type your answer here

Material Price Variances: AQ (AP- SP) X : 35,000 (9-10) = Rs. 35,000 (Favourable) Y : 42,000 (6-5) = Rs. 42,000 (Adverse) Z : 53,000 (7-6) = Rs. 53,000 (Adverse) Total MPV = Rs. 60,000 (Adverse)

(iii) Calculate Total and Individual Material Usage Variances Type your answer here

Material Usage Variances: SP (AQ - SQ) X: 10 (35,000 - 30,000) = Rs. 50,000 (Adverse) Y: 5 (42,000 - 40,000) = Rs. 10,000 (Adverse) Z: 6 (53,000 - 50,000) = Rs. 18,000 (Adverse) Total MUV = Rs. 78,000 (Adverse)

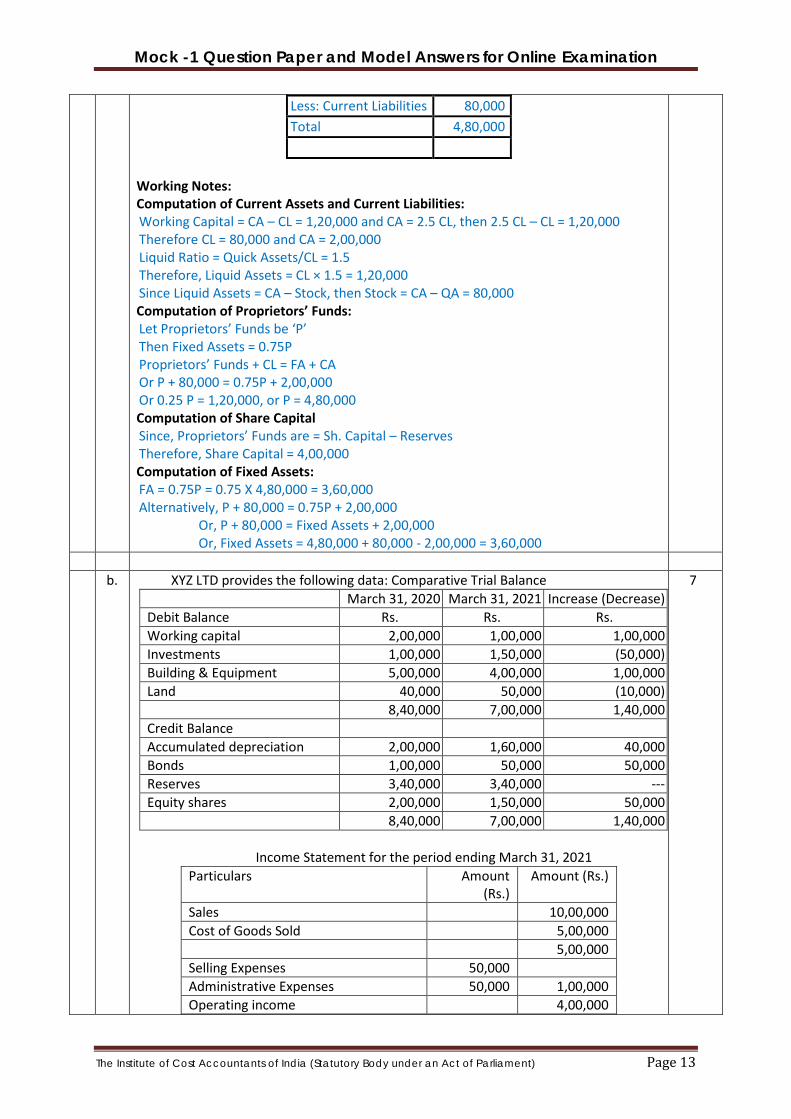

7. a. From the following information prepare a Statement of Proprietors’ Funds:

i. Current Ratio = 2.5:1 ii. Fixed Assets/Proprietors Funds = 0.75

iii. Liquid Ratio = 1.5 : 1 iv. Bank Overdraft = Rs. 10,000 v. Reserves and Surplus = Rs. 80,000

vi. Working Capital = Rs. 1,20,000

3

Type your answer here: Statement of Proprietors Fund

Particulars Rs. Proprietors Fund Share Capital 4,00,000 Reserves and Surplus 80,000 Total 4,80,000 Investment of Funds Fixed Assets 3.60,000 Stock 80,000 Other Current Assets 1,20,000

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 13

Less: Current Liabilities 80,000 Total 4,80,000

Working Notes: Computation of Current Assets and Current Liabilities: Working Capital = CA – CL = 1,20,000 and CA = 2.5 CL, then 2.5 CL – CL = 1,20,000 Therefore CL = 80,000 and CA = 2,00,000 Liquid Ratio = Quick Assets/CL = 1.5 Therefore, Liquid Assets = CL × 1.5 = 1,20,000 Since Liquid Assets = CA – Stock, then Stock = CA – QA = 80,000 Computation of Proprietors’ Funds: Let Proprietors’ Funds be ‘P’ Then Fixed Assets = 0.75P Proprietors’ Funds + CL = FA + CA Or P + 80,000 = 0.75P + 2,00,000 Or 0.25 P = 1,20,000, or P = 4,80,000 Computation of Share Capital Since, Proprietors’ Funds are = Sh. Capital – Reserves Therefore, Share Capital = 4,00,000 Computation of Fixed Assets: FA = 0.75P = 0.75 X 4,80,000 = 3,60,000 Alternatively, P + 80,000 = 0.75P + 2,00,000 Or, P + 80,000 = Fixed Assets + 2,00,000 Or, Fixed Assets = 4,80,000 + 80,000 - 2,00,000 = 3,60,000

b. XYZ LTD provides the following data: Comparative Trial Balance

March 31, 2020 March 31, 2021 Increase (Decrease) Debit Balance Rs. Rs. Rs. Working capital 2,00,000 1,00,000 1,00,000 Investments 1,00,000 1,50,000 (50,000) Building & Equipment 5,00,000 4,00,000 1,00,000 Land 40,000 50,000 (10,000)

8,40,000 7,00,000 1,40,000 Credit Balance Accumulated depreciation 2,00,000 1,60,000 40,000 Bonds 1,00,000 50,000 50,000 Reserves 3,40,000 3,40,000 --- Equity shares 2,00,000 1,50,000 50,000

8,40,000 7,00,000 1,40,000

Income Statement for the period ending March 31, 2021 Particulars Amount

(Rs.) Amount (Rs.)

Sales 10,00,000 Cost of Goods Sold 5,00,000

5,00,000 Selling Expenses 50,000 Administrative Expenses 50,000 1,00,000 Operating income 4,00,000

7

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 14

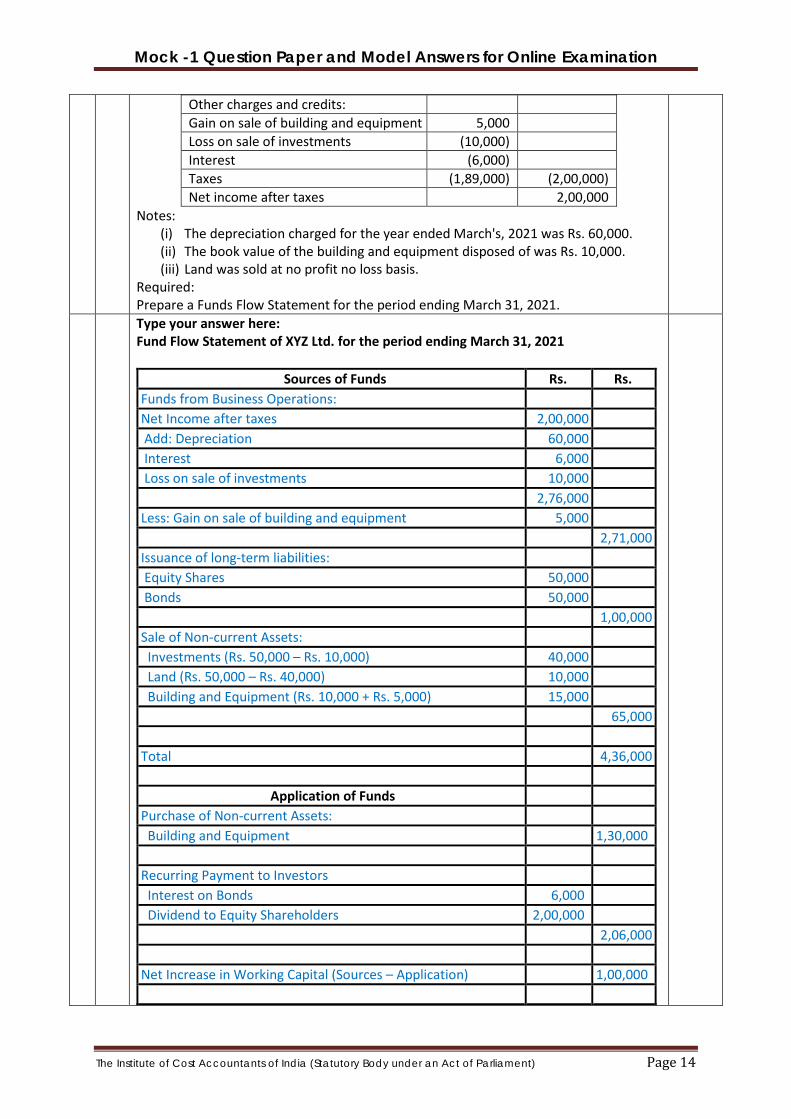

Other charges and credits: Gain on sale of building and equipment 5,000 Loss on sale of investments (10,000) Interest (6,000) Taxes (1,89,000) (2,00,000) Net income after taxes 2,00,000

Notes: (i) The depreciation charged for the year ended March's, 2021 was Rs. 60,000. (ii) The book value of the building and equipment disposed of was Rs. 10,000. (iii) Land was sold at no profit no loss basis.

Required: Prepare a Funds Flow Statement for the period ending March 31, 2021.

Type your answer here: Fund Flow Statement of XYZ Ltd. for the period ending March 31, 2021

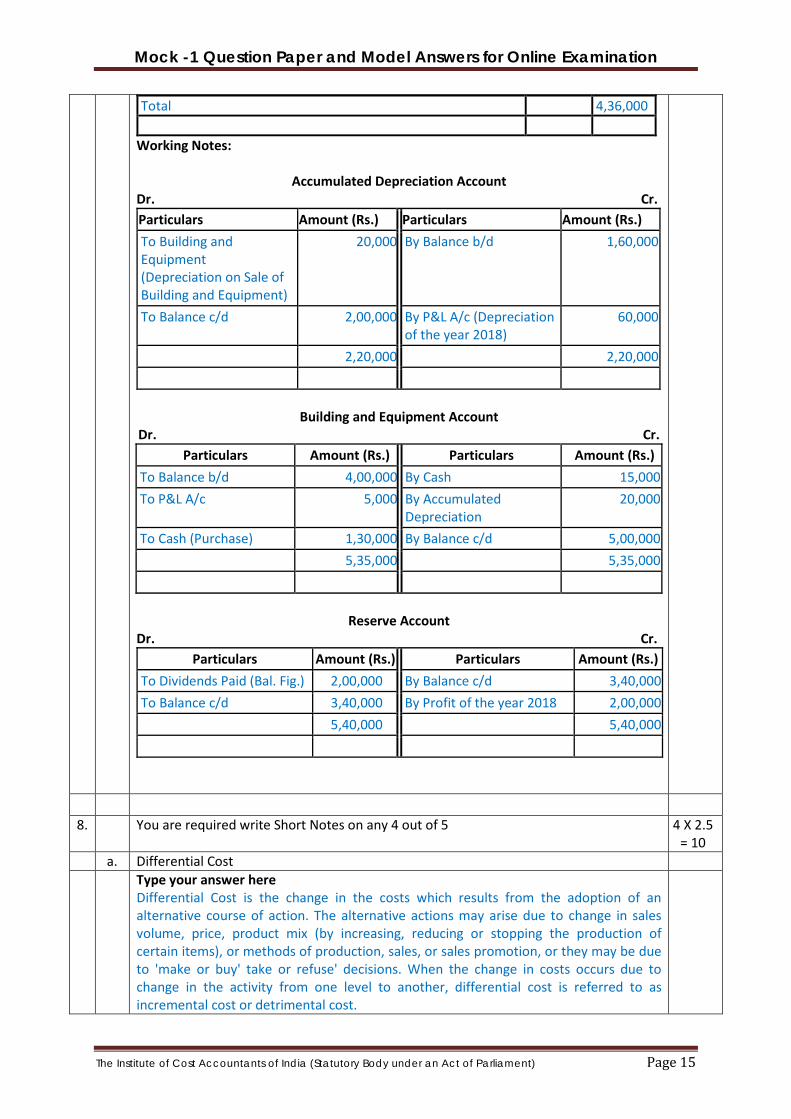

Sources of Funds Rs. Rs. Funds from Business Operations: Net Income after taxes 2,00,000 Add: Depreciation 60,000 Interest 6,000 Loss on sale of investments 10,000 2,76,000 Less: Gain on sale of building and equipment 5,000 2,71,000 Issuance of long-term liabilities: Equity Shares 50,000 Bonds 50,000 1,00,000 Sale of Non-current Assets: Investments (Rs. 50,000 – Rs. 10,000) 40,000 Land (Rs. 50,000 – Rs. 40,000) 10,000 Building and Equipment (Rs. 10,000 + Rs. 5,000) 15,000 65,000 Total 4,36,000

Application of Funds Purchase of Non-current Assets: Building and Equipment 1,30,000 Recurring Payment to Investors Interest on Bonds 6,000 Dividend to Equity Shareholders 2,00,000 2,06,000 Net Increase in Working Capital (Sources – Application) 1,00,000

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 15

Total 4,36,000

Working Notes:

Accumulated Depreciation Account Dr. Cr. Particulars Amount (Rs.) Particulars Amount (Rs.)

To Building and Equipment (Depreciation on Sale of Building and Equipment)

20,000 By Balance b/d 1,60,000

To Balance c/d 2,00,000 By P&L A/c (Depreciation of the year 2018)

60,000

2,20,000 2,20,000

Building and Equipment Account Dr. Cr.

Particulars Amount (Rs.) Particulars Amount (Rs.)

To Balance b/d 4,00,000 By Cash 15,000

To P&L A/c 5,000 By Accumulated Depreciation

20,000

To Cash (Purchase) 1,30,000 By Balance c/d 5,00,000

5,35,000 5,35,000

Reserve Account Dr. Cr.

Particulars Amount (Rs.) Particulars Amount (Rs.)

To Dividends Paid (Bal. Fig.) 2,00,000 By Balance c/d 3,40,000

To Balance c/d 3,40,000 By Profit of the year 2018 2,00,000

5,40,000 5,40,000

8. You are required write Short Notes on any 4 out of 5 4 X 2.5 = 10

a. Differential Cost Type your answer here

Differential Cost is the change in the costs which results from the adoption of an alternative course of action. The alternative actions may arise due to change in sales volume, price, product mix (by increasing, reducing or stopping the production of certain items), or methods of production, sales, or sales promotion, or they may be due to 'make or buy' take or refuse' decisions. When the change in costs occurs due to change in the activity from one level to another, differential cost is referred to as incremental cost or detrimental cost.

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 16

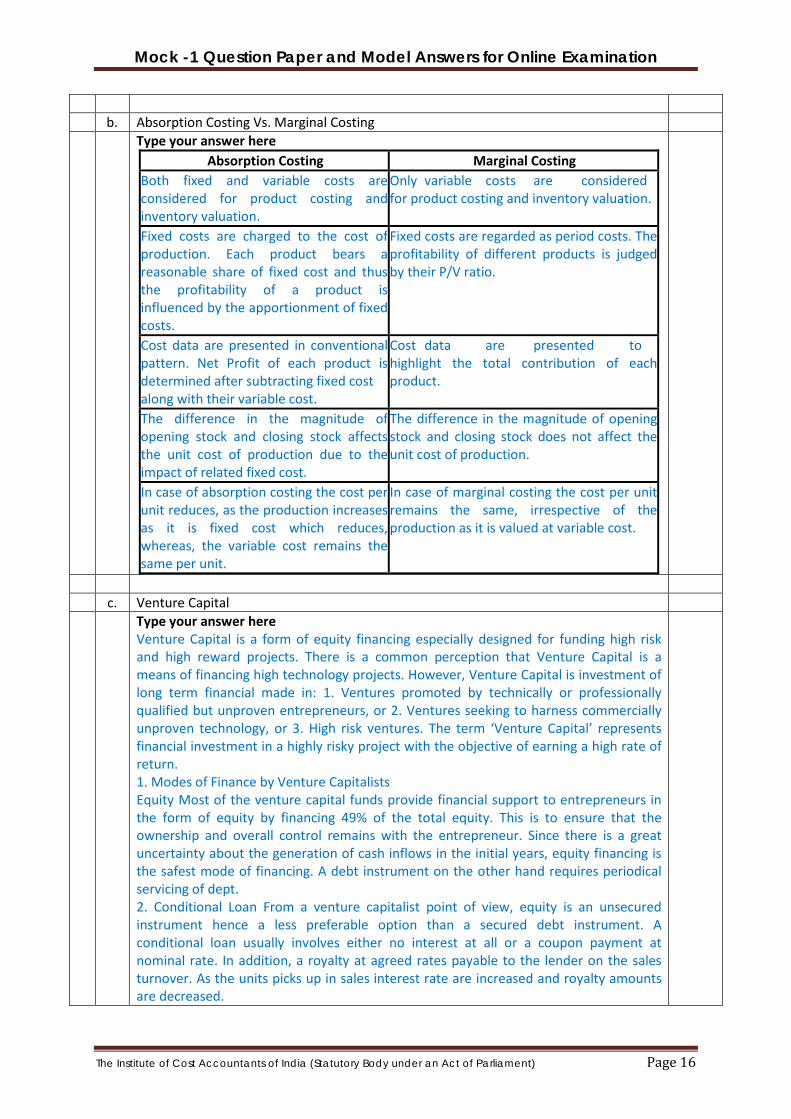

b. Absorption Costing Vs. Marginal Costing Type your answer here

Absorption Costing Marginal Costing Both fixed and variable costs are considered for product costing and inventory valuation.

Only variable costs are considered for product costing and inventory valuation.

Fixed costs are charged to the cost of production. Each product bears a reasonable share of fixed cost and thus the profitability of a product is influenced by the apportionment of fixed costs.

Fixed costs are regarded as period costs. The profitability of different products is judged by their P/V ratio.

Cost data are presented in conventional pattern. Net Profit of each product is determined after subtracting fixed cost along with their variable cost.

Cost data are presented to highlight the total contribution of each product.

The difference in the magnitude of opening stock and closing stock affects the unit cost of production due to the impact of related fixed cost.

The difference in the magnitude of opening stock and closing stock does not affect the unit cost of production.

In case of absorption costing the cost per unit reduces, as the production increases as it is fixed cost which reduces, whereas, the variable cost remains the same per unit.

In case of marginal costing the cost per unit remains the same, irrespective of the production as it is valued at variable cost.

c. Venture Capital Type your answer here

Venture Capital is a form of equity financing especially designed for funding high risk and high reward projects. There is a common perception that Venture Capital is a means of financing high technology projects. However, Venture Capital is investment of long term financial made in: 1. Ventures promoted by technically or professionally qualified but unproven entrepreneurs, or 2. Ventures seeking to harness commercially unproven technology, or 3. High risk ventures. The term ‘Venture Capital’ represents financial investment in a highly risky project with the objective of earning a high rate of return. 1. Modes of Finance by Venture Capitalists Equity Most of the venture capital funds provide financial support to entrepreneurs in the form of equity by financing 49% of the total equity. This is to ensure that the ownership and overall control remains with the entrepreneur. Since there is a great uncertainty about the generation of cash inflows in the initial years, equity financing is the safest mode of financing. A debt instrument on the other hand requires periodical servicing of dept. 2. Conditional Loan From a venture capitalist point of view, equity is an unsecured instrument hence a less preferable option than a secured debt instrument. A conditional loan usually involves either no interest at all or a coupon payment at nominal rate. In addition, a royalty at agreed rates payable to the lender on the sales turnover. As the units picks up in sales interest rate are increased and royalty amounts are decreased.

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 17

d. Debtors Turnover Ratio Type your answer here

This ratio ‘DTR’ indicates the speed at which the debtors are converted into cash. It is also called as ‘Receivables Turnover Ratio’. DTR = Credit Sales in a year / Average Account Receivable The term, average account receivable includes trade debtors and bills receivable. Average accounts receivables are computed by taking the average receivables in the beginning and at the end of the accounting year. The optimum ratio is dependent on the credit policy of the firm and credit period allowed to the customers. A lower ratio indicates poor collection from the debtors. The higher the ratio, better it is. Sometimes, we have to calculate the average collection period of debtors. In such a case, the formula would be; Average Collection Period = Days in a year / DTR Or Average Collection Period = (Debtors × Days in a year) / Credit Sales in a year. i.e., Debtors/Credit Sales per day. Significance of DTR: DTR or Debt Collection Period measures the quality of debtors since it indicates the speed with which money is collected from the debtor. A shorter collection period implies prompt payment by debtors. A longer collection period implies too liberal and inefficient credit collection performance. The credit policy should neither be too liberal nor too restrictive. The former will result in more blockage of funds and bad debts while the latter will cause lower sales which will reduce profits.

e. Performance Budgeting Type your answer here

Performance Budgeting: is synonymous with Responsibility Accounting, which means that the responsibility of various levels of management is predetermined in terms of output or result keeping in view the authority is vested with them. Performance budget is a budget that reflects the input of resources and the output of services for each unit of an organization. This type of budget is commonly used by the government to show the link between the funds provided to the public and the outcome of these services. Performance budgeting is a method of budgeting that provides the purpose and objectives for which funds are needed, costs of programs and related activities proposed to accomplish those objectives and outputs to be produced or services to be rendered under each program. Performance budgeting follows the validation that a relaxation of input controls and an increased flexibility enhances managers' performance as long as results are measured and managers are held responsible for their results. The major aim of performance budgeting is to improve the efficiency of public expenditure, by linking the funding of public sector organizations to the results they deliver. It adopts organized performance information (indicators, evaluations, program costings) to make this link. There is a good impact of performance budgeting on organizations in terms of improved prioritization of expenditure, and in improved service effectiveness. Performance budgeting is based on a classification of managerial level for the purpose of establishing a budget for each level. The individual in charge of that level should be made responsible and held accountable for its performance over a given period of time.

Section D 20

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 18

Marks You are required to answer all the questions in this section

Instructions: Each question is followed by a space where you are required to type your answer. 10 X

2 = 20 Marks

9. A MILLS LTD. has a number of machines that were used to make a product that the firm

has phased out of its operations. The products with long life cycles were considered company’s “cash cows” but they were becoming a thing of the past. The product had, predictably, failed to keep up with a market that demanded more for less. Heavily dependent on machines, this product had also faced a number of issues due to machine downtime. In the modern market, customers expect immediate gratification; an older model of machine, like the one A Mills has a history of crashes, which led to a supply disruption of the product. This added to the woes of the product, and it lost its lead to its competitors, who wasted no time in snapping up the customers. The revenue stream from the product soon became a trickle, till it finally stopped in 2020, when the lockdowns sounded a death knell for the long-suffering product. An existing machine was originally purchased one year ago for Rs. 5,00,000 and is being depreciated by applying straight line method and its remaining useful life is 4 years. No salvage value is expected at the end of the useful life. It can currently be sold for Rs.1,50,000. The machine can also be modified to produce another product at a cost of Rs.2,00,000. The modifications would not affect the useful life, or salvage value, and would be depreciated using the straight line method. If the firm does not modify the existing machine, it will have to buy a new machine at a cost of Rs. 4,40,000, (no salvage value) and the new machine would be depreciated over 4 years applying straight line method of depreciation. The engineers estimate that the cash operating costs with the new machine would be Rs. 25,000 per year less than with the existing machine. Cost of capital is 15 per cent and corporate tax rate is 35 per cent. However, modernizing an old machine, unlike full replacement, maintains the existing equipment’s footprint, saving plants from a sizable investment in space reconfiguration. Retrofits can be scheduled and executed over time, improving cash flow. You have been appointed as a financial advisor to the Company recently. The Board members of the company have asked you to quantitatively support your observations and suggest to the company whether the new machine should be bought, or the old equipment modified. Keep in mind, the older it gets, the higher the cost of maintenance is Outdated, old equipment often results to wasted time and productivity in the workplace. Assume straight line method of depreciation for tax purposes and loss on sale of existing machine can be claimed as short-term capital loss in the current year itself. [Given: PVIFA (15% 4 years) = 2.855]

a. Find the cost savings before and after tax. 2 Type your answer here

Cost Savings before tax = Rs. 25,000 Cost Savings after tax = Rs. 16,250 Working Notes: Cost Savings after tax = Cost Savings before tax X (1 – Corporate Tax Rate) = 16,250 (1 - 0.35) = 16,250

b. Is there any difference in the amount of depreciation pre and post-tax? 3

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 19

Type your answer here Difference in amount in Depreciation pre and post tax

A. Differential amount of depreciation before tax = Rs. 10,000 B. Differential amount of depreciation after tax = Rs. 3,500

Difference [(A) – (B) = Rs. 6,500 Working Notes: Computation of Depreciation of Old Machine: Original Cost: Rs. 5,00,000 Expected Life: 5 years Depreciation p.a. under SLM: Rs. 1,00,000 Computation of Depreciation of New Machine: Original Cost: Rs. 4,40,000 Expected Life: 4 years Depreciation p.a. under SLM: Rs. 1,10,000 Computation of Differential amount of Depreciation: Differential Depreciation before tax: Depreciation of New Machine – Depreciation of Old Machine = Rs. 1,10,000 – Rs. 1,00,000 = Rs. 10,000 Differential Depreciation after tax: Differential Depreciation before tax X Corporate Tax Rate = Rs. 10,000 X .035 = Rs. 3,500

c. Do you expect a savings or a loss to the company if it buys the new machine? 3 Type your answer here

Future savings (or loss) from buying the new machine: Savings of Rs. 56,386 Particulars Amount Before

Tax (Rs.) Amount After

Tax (Rs.) Cost Savings 25,000 16,250 Differential Depreciation (1,10,000 – 1,00,000) 10,000 3,500 Total Cash Advantage per year 19,750 PF of Future Savings from buying new machine 56,386

Working Notes: Computation of Present Value of Future Savings: Total Cash Advantage per year X Present Value Interest Factor of Annuity = 19,750 X 2.855 = Rs. 56,386

d. What option would you recommend for the company and why? 2 Type your answer here

Recommendation: It is recommended to the company not to but the new machine. The old machine should be modified. The cost of the new machine is higher than the expected savings from such machine. There shall be an excess cash outflow of Rs. 33,614 (i.e. Rs. 2,33,614 – Rs. 2,00,000) if the new machine is purchased instead of modifying the old machine. Working Notes:

Particulars Amount (Rs.) PF of Future Savings from buying new machine 56,386 Cash Inflow on Disposal of Old Machine 1,50,000 Cash Outflow on buying the New Machine 4,40,000 Adjusted Net Cash Flow on buying the New Machine 2,33,614 Cash Outflow for modification of Old Machine 2,00,000

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 20

10. The unforeseen pandemic of Covid-19 brought about quite a few changes in the consumption of the consumer goods in India. Millions of fitness and food videos shared on various social media platforms are a testament to this trend. This shift was also reflected in the home appliances that they purchased during the past year. In addition to that, a momentous growth in the purchase of electronic devices such as laptops, tablets and headphones among others during the past year was noticed. People also looked for more efficient devices as work-from-home became the new normal. As more and more people settled in their routines they looked for automating their home appliances in a bid to save time. An increasing number of customers are opting for COVID ACs with air purification functionalities and multi-functional refrigerators such as convertible refrigerators and curd makers. Demand for laptops and tablets in the past year have seen growth of nearly 200% on a pre and post lockdown basis. Office essentials such as printers have seen a 75% increase in searches for various kinds of printers (inkjet, ink tank and lasers). There is also a significant increase in demand for health and hygiene devices that help ensure the safety of consumers and their families with healthcare essentials such as IR Thermometers, Pulse Oxymeters, BP Monitors, etc. being the top verticals. The anticipated sales of Electronic Corporation Ltd, a seller of small parts for medical and screen-based devices, is Rs. 4,00,000 and unit selling price is Rs. 20 each. The per unit cost of direct material is Rs. 9, labour is Rs. 3 and other variable expenses are Rs. 3 per unit. The company is earning a net profit of 5% and to improve the profitability, various proposals are discussed at the Executive Committee Meeting of the company. Proposal A: The present administrative setup is on the regional basis and it was felt that centralization will reduce the fixed costs by Rs. 12,000. Maintaining multiple offices throughout the country, especially when work from home is a reality, without any major falls in employee efficiency, seems unnecessary. Proposal B: The Production Manager has agreed that he will try to work on a cost reduction programme which will reduce the cost by Rs. 1 per unit but there will be little impact on the quality which will be negligible to the customer. Proposal C: The Sales Manager opposed the two proposals and suggested that it may be possible to increase the number of units sold by 20%, provided the selling price is reduced by 5%, since the market is cut-throat and innovation is an everyday word. Electronics Corporation Ltd. has long-standing contracts with the majority of its customers, but a significant market share still belongs to its competitor. A fall in prices may be enough to propel the Company to a market leader, a position which its competitor currently enjoys, over a period of time. However, the company’s current profit margins are quite slim anyway. A price reduction may push it down further. Proposal D: Another Sales Manager proposed that the selling price be increased by 10% but the unit sales (no. of units sold) will be reduced by 5%.

a. Prepare a Statement of Cost, Profit and Sales based on the current scenario. 2

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 21

Type your answer here Statement of Estimated Cost, Profit and Sales

Particulars Per Unit (Rs.) Amount (Rs.) Amount (Rs.) Sales 20 4,00,000 Variable Costs

Direct Materials 9 1,80,000 Labour 3 60,000 Other variable Expenses 3 60,000 Total Variable Cost 15 3,00,000 Contribution 5 1,00,000 Total Fixed Cost 80,000 Estimated Profit 20,000

Working Notes: No. of units sold: Sales (Rs.) / Selling Price per unit = Rs. 4,00,000 / Rs. 20 per unit = 20,000 units Anticipated Profit: Profit is calculated @ 5% of Sales = 5% of Rs. 4,00,000 = Rs. 80,000 Total Fixed Cost: It is a balancing figure

b. What may be the impact on estimated profit if Proposal A or Proposal B is accepted? 3 Type your answer here

Impact on estimated profit upon acceptance of Proposal A: Accepting Proposal A will yield additional profit of Rs. 12,000. Impact on estimated profit upon acceptance of Proposal B: Accepting Proposal B will yield additional profit of Rs. 20,000. Working Notes:

Statement of Estimated Cost, Profit and Sales

Particulars Proposal A Proposal B

Amount (Rs.) Amount (Rs.) Sales (units) 20,000 20,000 Selling Price per unit (Rs.) 20 20 Variable Cost (Rs.) 15 14 Contribution / unit 5 6 Total Contribution (Rs.) 1,00,000 1,20,000 Less: Fixed Cost (Rs.) 68,000 80,000 Anticipated Net Profit (Rs.) 32,000 40,000 Estimated Profit (Rs.) 20,000 20,000 Increase (Decrease) in Profit (Rs.) 12,000 20,000

Computation for Proposal A: Revised Fixed Cost = Pre-Revised Fixed Cost – Proposed Reduction = Rs. 80,000 – Rs. 12,000 = Rs. 68,000 Computation for Proposal B: Revised Variable Cost per unit = Pre-Revised Variable Cost per unit – Reduction in Pre-Revised Variable Cost of Re. 1 per unit = Rs. 15 – Re. 1 = Rs. 14

c. What may be the impact on estimated profit if Proposal C or Proposal D is accepted? 3 Type your answer here

Impact on estimated profit upon acceptance of Proposal C: Accepting Proposal C will yield a reduction in estimated profit amounting to Rs. 4,000.

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 22

Impact on estimated profit upon acceptance of Proposal D: Accepting Proposal D will yield additional profit of Rs. 33,000. Working Notes:

Statement of Estimated Cost, Profit and Sales

Particulars Proposal C Proposal D

Amount (Rs.) Amount (Rs.) Sales (units) 24,000 19,000 Selling Price per unit (Rs.) 19 22 Variable Cost (Rs.) 15 15 Contribution / unit 4 7 Total Contribution (Rs.) 96,000 1,33,000 Less: Fixed Cost (Rs.) 80,000 80,000 Anticipated Net Profit (Rs.) 16,000 53,000 Estimated Profit (Rs.) 20,000 20,000 Increase (Decrease) in Profit (Rs.) (4,000) 33,000

Computation for Proposal C: Revised Sales (units) = Pre-Revised Sales (units) + 20% increase in Pre-Revised Sales (units) = 20,000 + 20% of 20,000 units = 24,000 units Revised Selling Price = Pre-Revised Selling Price – 5% reduction in Pre-Revised Selling Price = Rs. 20 – 5% of Rs. 20 = Rs. 19 Computation for Proposal D: Revised Sales (units) = Pre-Revised Sales (units) + 5% reduction in Pre-Revised Sales (units) = 20,000 - 5% of 20,000 units = 19,000 units Revised Selling Price = Pre-Revised Selling Price + 10% increase in Pre-Revised Selling Price = Rs. 20 + 10% of Rs. 20 = Rs. 22

d. Which proposal should be accepted? Also offer your comments on its acceptance and/or non-acceptance.

2

Type your answer here Proposal to be accepted: D

Proposal Impact on Estimated Profit

Comments Increase/Decrease Amount (Rs.)

A Increase 12,000 Not acceptable as it considers the present COVID19 Pandemic situation and does not consider Post-COVID19 situation

B Increase 20,000 Not acceptable as there may be some/little impact on quality resulting in marketing dangers

C Decrease 4,000 Not acceptable as it reduces the estimated profits and has a long term impact on profitability.

D Increase 33,000 Acceptable as the quality of the product remains same and it considers the possible reduction in

Mock -1 Question Paper and Model Answers for Online Examination

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 23

sales with an increase in selling price. However, such a move may benefit the competitors as they can re-price and re-position their products taking advantage of such increase in selling price by Electronics Corporation Ltd.

END