Embed Size (px)

Citation preview

GARLAND INDEPDENDENT SCHOOL DISTRICT Garland, Rowlett and Sachse

972.487.4651 PO Box 469026 Garland, TX 75046–9026

Phrases in (blue) are hyperlinks used by IA to review the audit and for the reader to know from where information came. This is IA Job # 16–53.

Internal Audit Department

Steven Martin, CPA/CFF, CGFM, CFE, CGMA, CIGI November 18, 2016 Director of Internal Audit

Independent Auditor’s Report

Follow–up Report to the March 30, 2016, Internal Control Audit of the Tax Office

To: Board of Trustees

Reference is made to the Internal Control Audit of the District’s Tax Office dated March 30,

2016, which included 19 findings and one observation, listed in Appendix Two, page 12. The

Internal Audit Charter, Board Policy CFC (Local) states, “The internal audit department shall

be responsible for appropriate follow–up on audit findings and recommendations. All

significant findings shall remain in an open issues file until cleared by the internal audit

department. The internal audit department shall issue periodic status reports to the Board with

copies issued to the Superintendent.”

The administration fully accepted and enacted 11 out of 19 recommendations. The original

audit focused on Tax Office internal control, which is largely a matter of judgment, taking into

account cost versus benefit. The administration is under no obligation to enact the remaining

recommendations unless the Board directs otherwise. Consequently, pending such direction

to the administration by the Board, this will conclude follow–up audits on the original Tax

Office audit.

The original audit included three main findings:

Separating accounting and treasury functions at the Tax Office

Creating an audit trail within the Tax Office

Employing separate contractors to manage tax records and receive credit card

payments.

The Tax Office created an audit trail as described herein in Appendix Two. However,

accounting and treasury functions still take place within one administrative unit, the Tax

Office, and the same contractor continues to manage tax records and receive tax payments.

Attached are the following appendixes:

Appendix One – Management’s Current Status per Management of each finding,

page 9

Appendix Two – Current Tax Office Tax Cash Handling Procedures, page 12

2

Appendix Three – Personnel with Governmental Data Services (GDS)(property tax

software) access, page 22

Appendix Four – Findings in the Original Report, page 23

Appendix Five – Management’s Response to Original Findings, page 41

Appendix Six – IA’s letter to management requesting a response, page 45

The original findings with management’s original responses, management’s reported current

status, and results of the current audit are as follows:

Tax Office

1) Lack of Separation of Duties –Tax Office – Recommendation rejected, minor

changed enacted, no reconciliations as proposed completed

Management’s original response – “The Tax Office has removed from GDS

the access the Director of Tax Services has to be able to post payments and

access the Tax Clerk Ill has to be able to make any adjustments. The Business

Office (hereinafter use to mean the finance and accounting functions of the

District) does have the ability to review a monthly reconciliation of the Dallas

Central Appraisal District (DCAD) tax roll to the data maintained in GDS

without a significant drain on resources. This will be implemented as soon as

feasible.”

Current Status per Management – “No change but plans are being made to

review the Dallas Central Appraisal District tax roll supplements that are

received monthly. This review will be made by staff not part of the Tax

Office.”

Current Audit – The original recommendation called for a physical separation

of Tax Office accounting and treasury responsibilities. This was rejected.

Instead, the administration countered by enacting changes in GDS access (see

Appendix Three). The Director of Tax Services cannot post payments and the

second-in-charge cannot make adjustments. A review by IA of the GDS

Access documents confirms these changes.

However the change is meaningless because the Director of Tax Services and

Tax Clerk III have the ability to change GDS access at any time.

Consequently, the original finding effect stands: Tax Office personnel have

access to cash and checks and also to accounting records. Assets may be

misappropriated and accounting records altered.

Furthermore, the Tax Office Director supervises the Tax Clerk III and

remaining four Tax Clerks all of whom have the ability to record tax

payments, and in addition to the Director, two Tax Clerks also have the ability

to make adjustments and refunds. Even if Tax Office personnel lacked the

ability to make changes to GDS access, because one administrative unit has

access to accounting records as well as incoming cash and checks, the District

continues to be in violation of TEA’s Financial Accountability System

3

Resource Guide (FASRG), Financial Accounting & Reporting Section 1.5.4.4

that states:

o Segregation of the responsibilities for billing property taxes and

services from collection and accounting

o Segregation of the responsibilities for maintaining detail accounts

receivable records from collections and general ledger posting

o Segregation of collection, control and deposit of funds activities from

maintaining accounting records

o Maintenance of the property tax assessment rolls by individuals not

engaged in any accounting or collection function

o If EDP is used, maintenance of the principle of segregation of duties

within processing activities

TEA FASRG Financial Accounting & Reporting Section 1.5.2.2 states,

“Persons who have authorized access to both assets and related accounting

records may be in a position to conceal shortages of the assets in the records.

If duties are properly segregated, persons who have authorized access to assets

will not also have access to related accounting records in which they might

conceal shortages.”

The FASRG internal control requirement is tempered by Section 1.5.1.3,

which states, “The application of control activities, such as segregation of

duties, is affected to some degree by the size of the school district. In

smaller school districts, control activities will be less formal than in larger

school districts. Additionally, certain types of control activities may not be

relevant in a smaller entity.”

However, “Educating 57,000 students across 71 campuses, Garland ISD

ranks as the second–largest district in Dallas County, fourth–largest in

Dallas–Fort Worth, 13th–largest in Texas, and is among the 70–largest in

America,” (161118 from GISD website Highlights _ Garland Independent

School District). Additionally, with 2016–2017 budgeted general funds

revenues of $462,406,099, GISD can hardly be called a small district,

(161118 2016–17_approved_budget_8–24–16).

Second, the original management response stated, “The Business Office

(hereinafter use to mean the finance and accounting functions of the District)

does have the ability to review a monthly reconciliation of the DCAD tax roll

to the data maintained in GDS without a significant drain on resources. This

will be implemented as soon as feasible.” However, pursuant to

management’s reported Current Status per Management, such reviews have

not yet been started.

Furthermore, although it is stated that the Business Office has the ability to

review monthly reconciliations of the DCAD tax roll to data maintained in

4

GDS, it is seen that no one in the Business Office has access to GDS (see

Appendix Three). The original report was issued in April 2016 and this

review is being conducted in November 2016. It appears in the last six

months no steps have been implemented to review said monthly

reconciliations.

2) Lack of Separation of Duties – GDS, contractor – Recommendation rejected, risk

accepted

Management’s original response – “The District has before used another

vendor for credit card and e-check services. PCI (Payment Card Industry)

compliance issues caused the District to switch back services to GDS. The Tax

Office contacted GDS to request a copy of the audit performed under

Statement on Standards for Attestation Engagements (SSAE) No. 16,

Reporting on Controls at a Service Organization. GDS has indicated that the

District's data resides on our servers and not in their hosted solution like most

of their clients. Some additional research will likely be necessary to determine

if we can rely on the controls in place at GDS and not split the services.”

Current Status per Management – “No change.”

Current Audit – GDS provided the District with an SSAE report on one of its

service organizations, not an SSAE report on itself as a service organization.

Subsequently, the District’s Chief Financial Officer provided the following

statement, “Per your request I had Denise Holmes calculate the percentage of

tax revenue received through GDS’s credit card and e–check services. For the

time period 9/1/2015 through 8/31/2016 the amount of tax collections from

GDS were $10,438,477. For the same time period the levy was $190,379,645.

This represents just over 5%. I believe the risk to the District is minimal given

the small percentage that GDS collects via their system. However, should that

amount increase I will certainly weigh the cost against the benefit of having a

third-party service engaged to collect credit card and e-check payments of

taxes.”

3) Lack of Testing and Reconciling of Taxes Receivable in GDS at the Beginning of the

Year and from One Month to the Next – Recommendation Accepted but not

Enacted After Six Months

Management’s original response – “The Tax Office, Business Office and

Budget Department will work on developing a way to randomly test data

received by the Dallas Central Appraisal District. Any reconciliation

performed will be reviewed by the Deputy Superintendent of Business.”

Current Status per Management – “A process is being developed whereby

data received from the DCAD and imported into the tax office software will

be reviewed by Budget and the CFO.”

Current Audit – The recommendation is process of being enacted but to date,

six months later, Business Office personnel still lack access to GDS, the

District’s tax software.

5

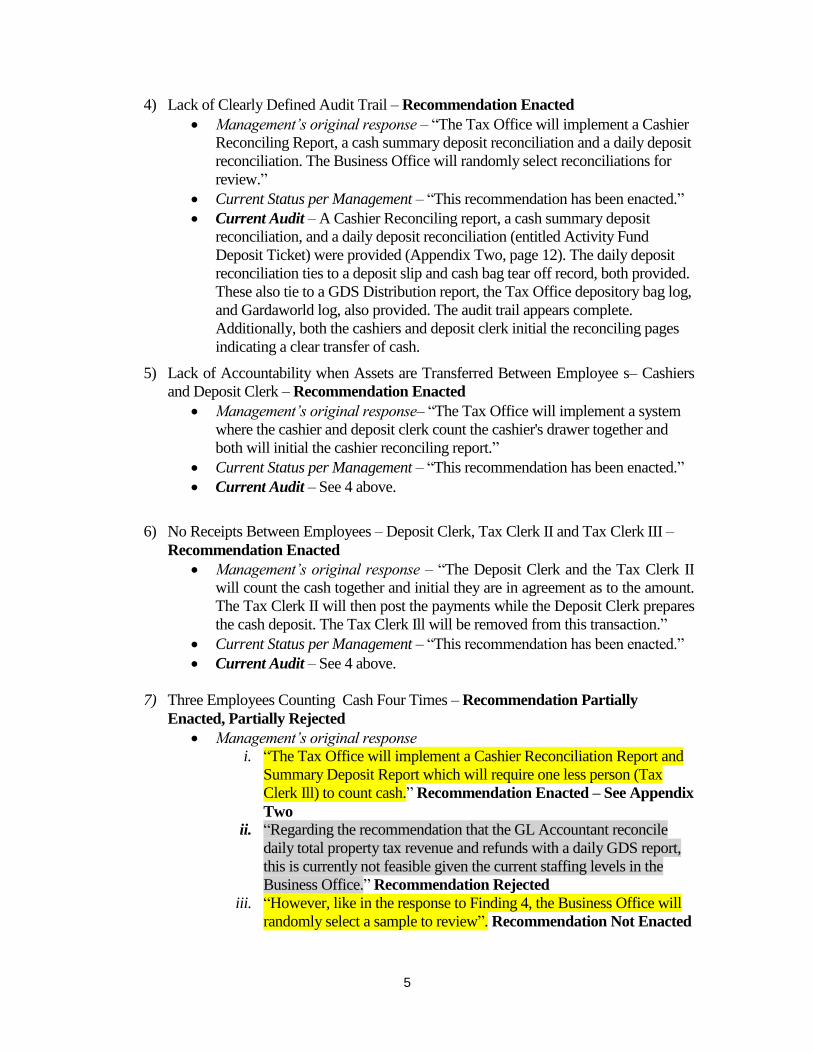

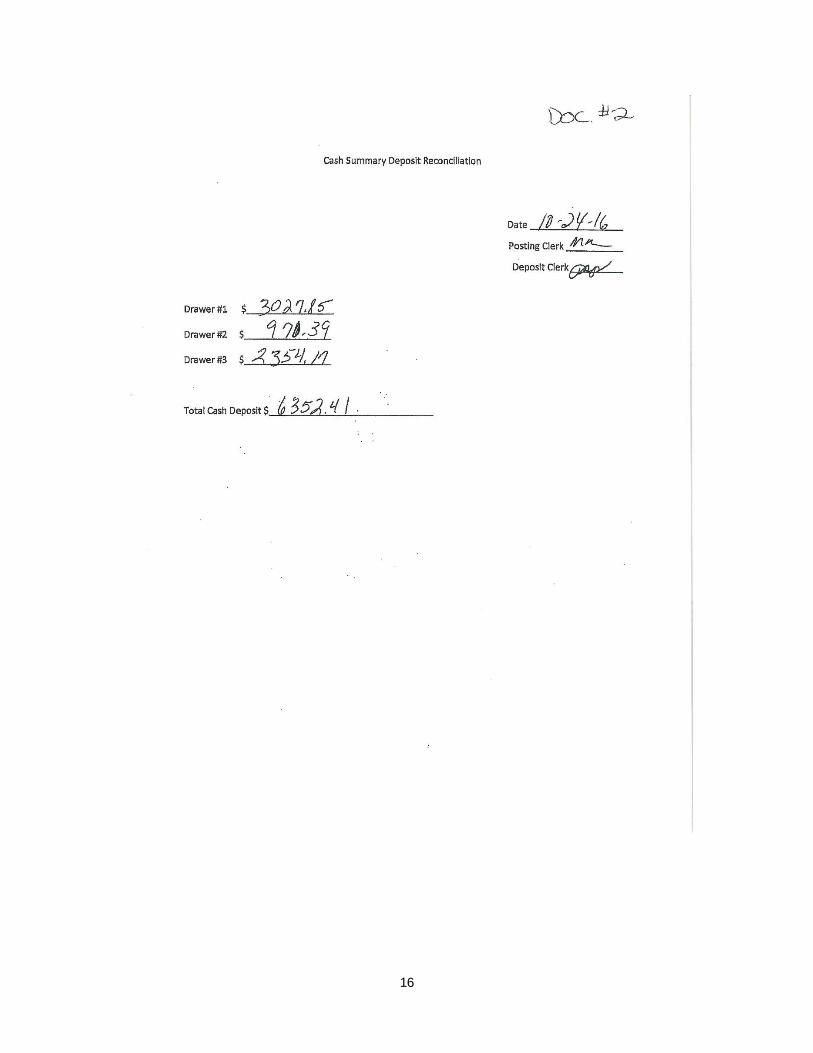

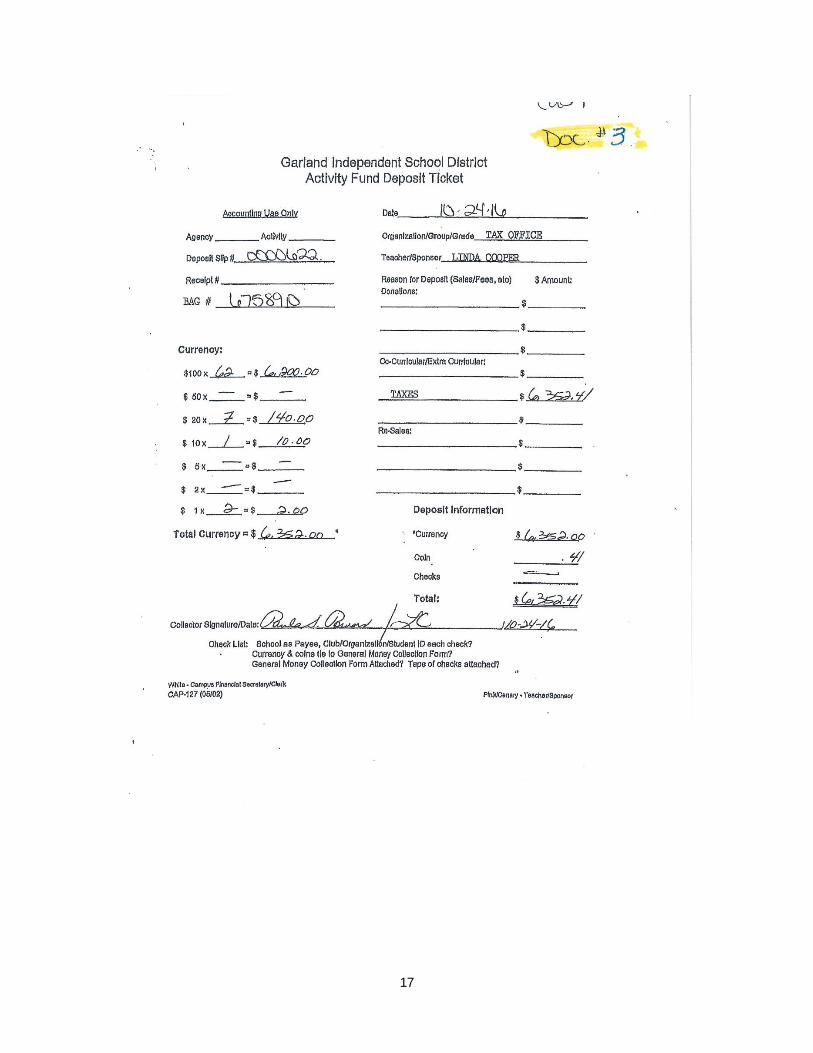

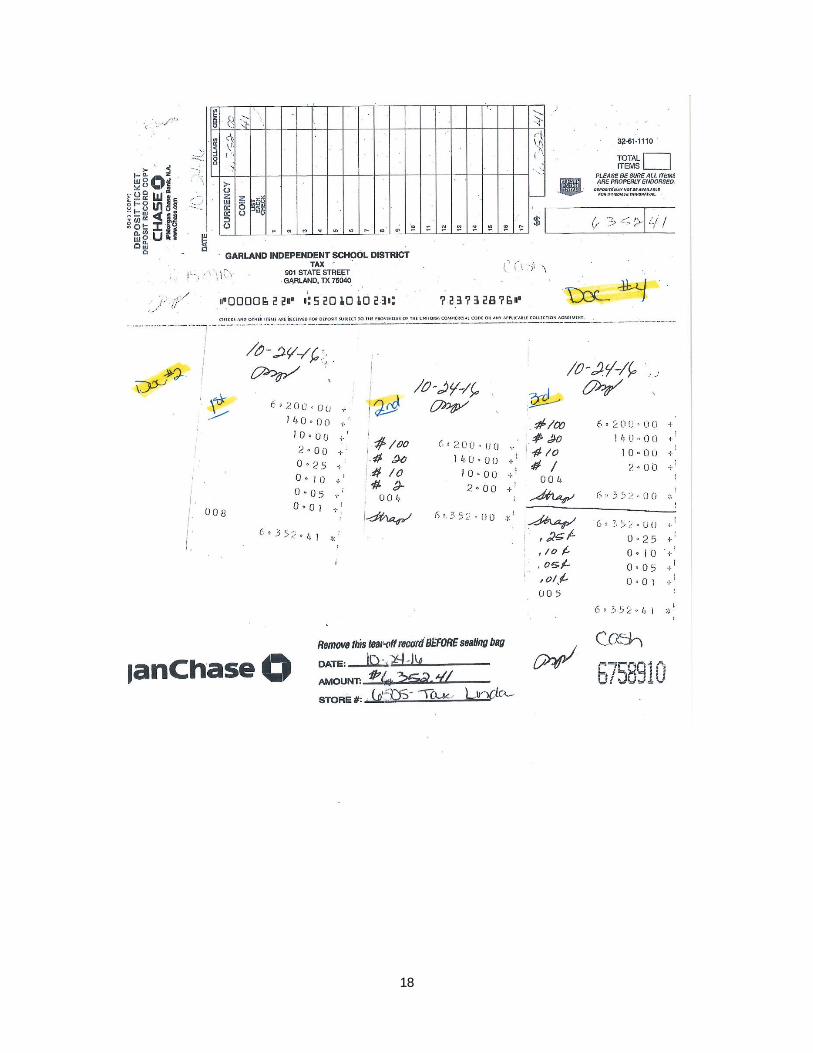

4) Lack of Clearly Defined Audit Trail – Recommendation Enacted

Management’s original response – “The Tax Office will implement a Cashier

Reconciling Report, a cash summary deposit reconciliation and a daily deposit

reconciliation. The Business Office will randomly select reconciliations for

review.”

Current Status per Management – “This recommendation has been enacted.”

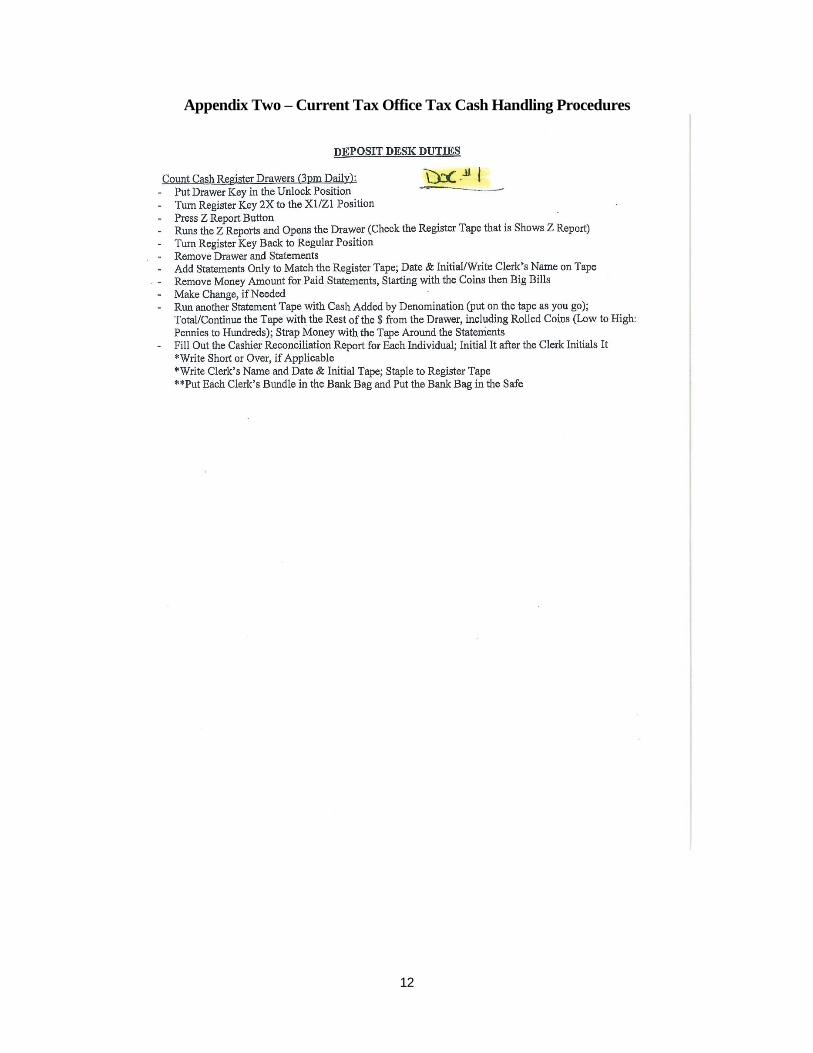

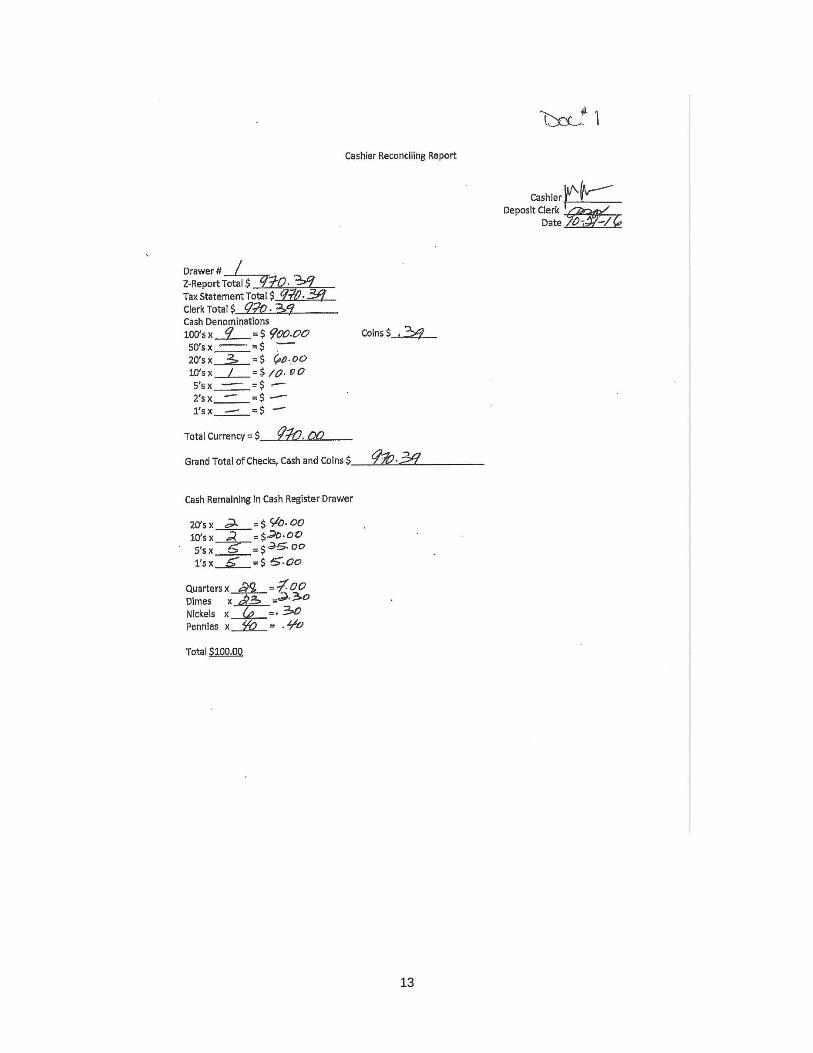

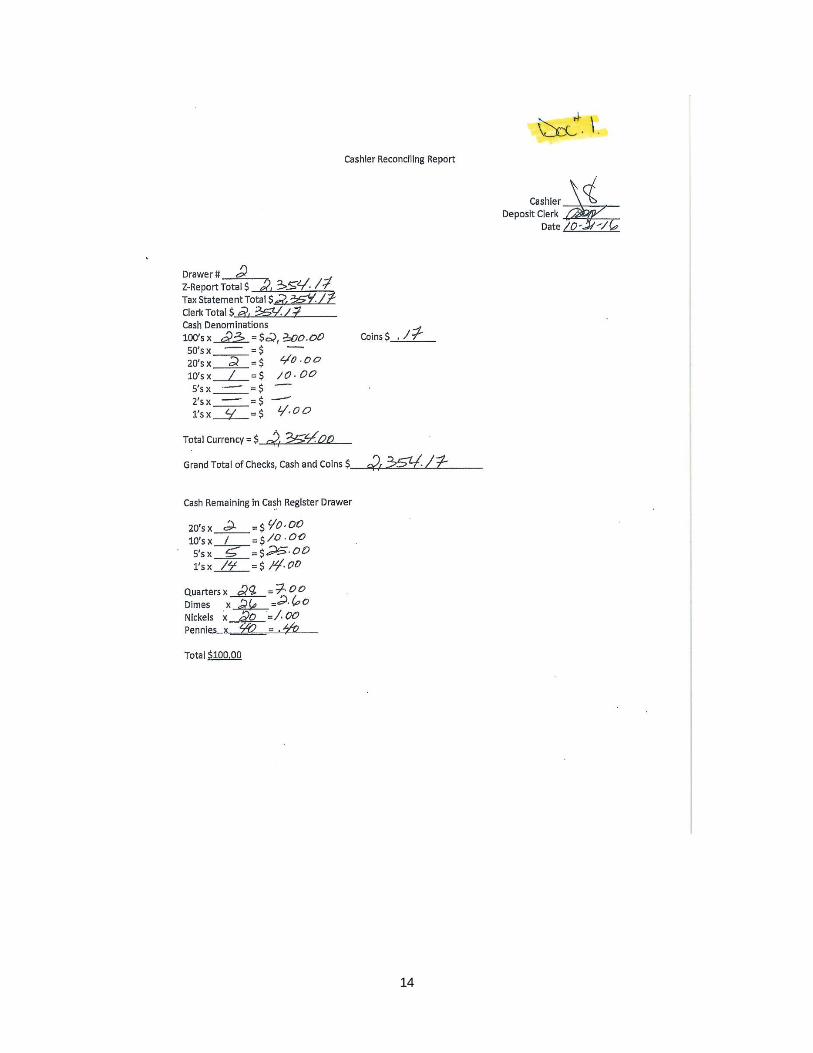

Current Audit – A Cashier Reconciling report, a cash summary deposit

reconciliation, and a daily deposit reconciliation (entitled Activity Fund

Deposit Ticket) were provided (Appendix Two, page 12). The daily deposit

reconciliation ties to a deposit slip and cash bag tear off record, both provided.

These also tie to a GDS Distribution report, the Tax Office depository bag log,

and Gardaworld log, also provided. The audit trail appears complete.

Additionally, both the cashiers and deposit clerk initial the reconciling pages

indicating a clear transfer of cash.

5) Lack of Accountability when Assets are Transferred Between Employee s– Cashiers

and Deposit Clerk – Recommendation Enacted

Management’s original response– “The Tax Office will implement a system

where the cashier and deposit clerk count the cashier's drawer together and

both will initial the cashier reconciling report.”

Current Status per Management – “This recommendation has been enacted.”

Current Audit – See 4 above.

6) No Receipts Between Employees – Deposit Clerk, Tax Clerk II and Tax Clerk III –

Recommendation Enacted

Management’s original response – “The Deposit Clerk and the Tax Clerk II

will count the cash together and initial they are in agreement as to the amount.

The Tax Clerk II will then post the payments while the Deposit Clerk prepares

the cash deposit. The Tax Clerk Ill will be removed from this transaction.”

Current Status per Management – “This recommendation has been enacted.”

Current Audit – See 4 above.

7) Three Employees Counting Cash Four Times – Recommendation Partially

Enacted, Partially Rejected

Management’s original response

i. “The Tax Office will implement a Cashier Reconciliation Report and

Summary Deposit Report which will require one less person (Tax

Clerk Ill) to count cash.” Recommendation Enacted – See Appendix

Two

ii. “Regarding the recommendation that the GL Accountant reconcile

daily total property tax revenue and refunds with a daily GDS report,

this is currently not feasible given the current staffing levels in the

Business Office.” Recommendation Rejected

iii. “However, like in the response to Finding 4, the Business Office will

randomly select a sample to review”. Recommendation Not Enacted

6

Current Status per Management – “The requested change has been enacted.”

Current Audit – Despite a request (161114 to CFO for requested items re

Follow up response) for reconciliations completed by the Business Office for

IA to review, none were provided, despite management’s original response

being made six months ago. Accordingly, it appears this part of the

recommendation, reconciling daily total property revenue and refunds with a

daily GDS report, will not be enacted, either daily or on an interim basis.

8) Tax Collector’s Bond to be approved by the Board – Recommendation Enacted

Management’s original response – “GISD Board Policy CG (Legal) reads

"The tax collector for the District shall be bonded in accordance with the law."

The District has a crime policy with National Union Fire Insurance Company

of Pittsburgh, Pa. (AIG). The policy provides $1,000,000 of employee theft

coverage subject to a $5,000 deductible. The Board approves the purchase of

insurance. However, we will ask General Counsel if the approval of the policy

meets the requirement of board policy and Tax Code §6.29 and make changes

as necessary.”

Current Status per Management – “The requested change has been made.”

Current Audit – Internal Audit witnessed the Board voting to approve the Tax

Director’s bond on June 28, 2016.

9) Cash Deposit Bags not used in Numerical Order – Recommendation Enacted

This was corrected during the original audit

10) No Point of Sale Receipt from either the Cash Registers or GDS – Recommendation

Enacted

Management’s original response– “The Tax Office has started printing a

duplicate register receipt to give to the taxpayer for the cash payments

received. Checks are posted to the taxpayer's account and a receipt is issued

from GDS.”

Current Status per Management– “No change.”

Current Audit – Response satisfactory

11) Board to approve $500 Refunds, not Give Notice for $2,500 Refunds –

Recommendation Enacted

Management’s original response – “The Tax Office will begin immediately to

present to the Board of Trustees all tax refunds in excess of $500.”

Current Status per Management – “No change.”

Current Audit – A review of the refunds submitted for Board approval on

November 7, 2016, showed several from $500 to $2,500. Additionally, a

review of the video of this meeting showed the Board approving the refunds.

12) No Support Provided to the Business Office for Adjustments in Oracle of Levy

Adjustments – Recommendation agreed to but not enacted

7

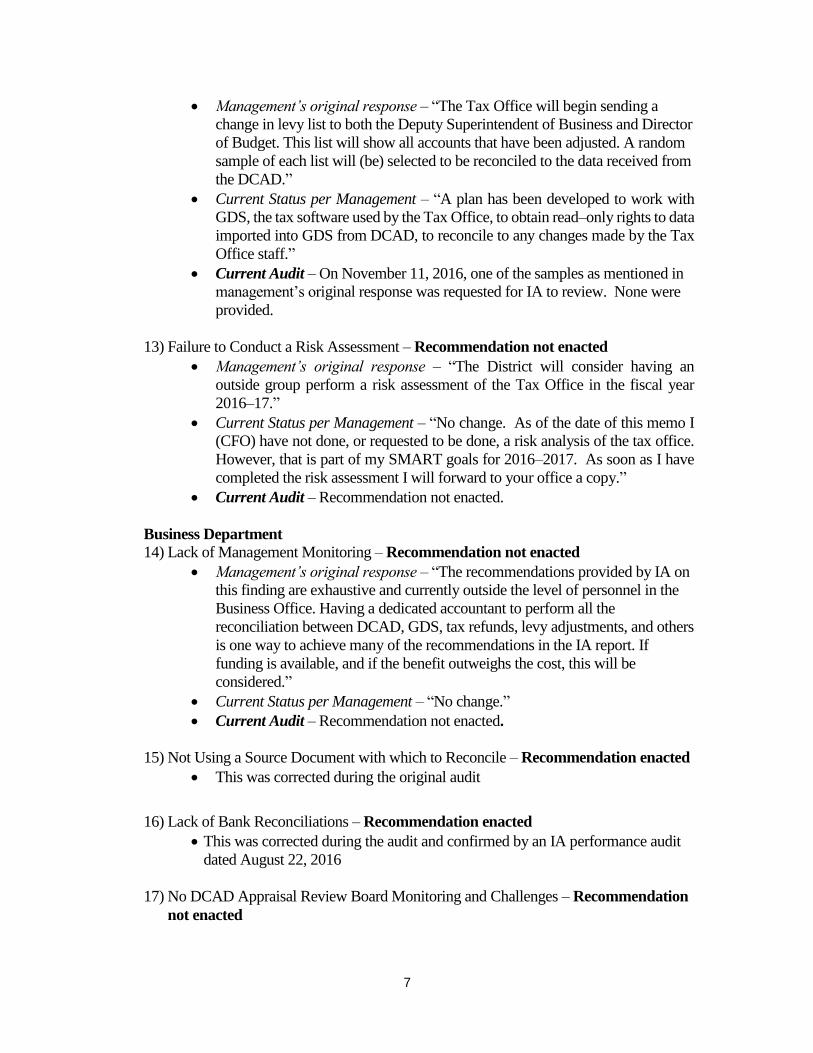

Management’s original response – “The Tax Office will begin sending a

change in levy list to both the Deputy Superintendent of Business and Director

of Budget. This list will show all accounts that have been adjusted. A random

sample of each list will (be) selected to be reconciled to the data received from

the DCAD.”

Current Status per Management – “A plan has been developed to work with

GDS, the tax software used by the Tax Office, to obtain read–only rights to data

imported into GDS from DCAD, to reconcile to any changes made by the Tax

Office staff.”

Current Audit – On November 11, 2016, one of the samples as mentioned in

management’s original response was requested for IA to review. None were

provided.

13) Failure to Conduct a Risk Assessment – Recommendation not enacted

Management’s original response – “The District will consider having an

outside group perform a risk assessment of the Tax Office in the fiscal year

2016–17.”

Current Status per Management – “No change. As of the date of this memo I

(CFO) have not done, or requested to be done, a risk analysis of the tax office.

However, that is part of my SMART goals for 2016–2017. As soon as I have

completed the risk assessment I will forward to your office a copy.”

Current Audit – Recommendation not enacted.

Business Department

14) Lack of Management Monitoring – Recommendation not enacted

Management’s original response – “The recommendations provided by IA on

this finding are exhaustive and currently outside the level of personnel in the

Business Office. Having a dedicated accountant to perform all the

reconciliation between DCAD, GDS, tax refunds, levy adjustments, and others

is one way to achieve many of the recommendations in the IA report. If

funding is available, and if the benefit outweighs the cost, this will be

considered.”

Current Status per Management – “No change.”

Current Audit – Recommendation not enacted.

15) Not Using a Source Document with which to Reconcile – Recommendation enacted

This was corrected during the original audit

16) Lack of Bank Reconciliations – Recommendation enacted

This was corrected during the audit and confirmed by an IA performance audit

dated August 22, 2016

17) No DCAD Appraisal Review Board Monitoring and Challenges – Recommendation

not enacted

9

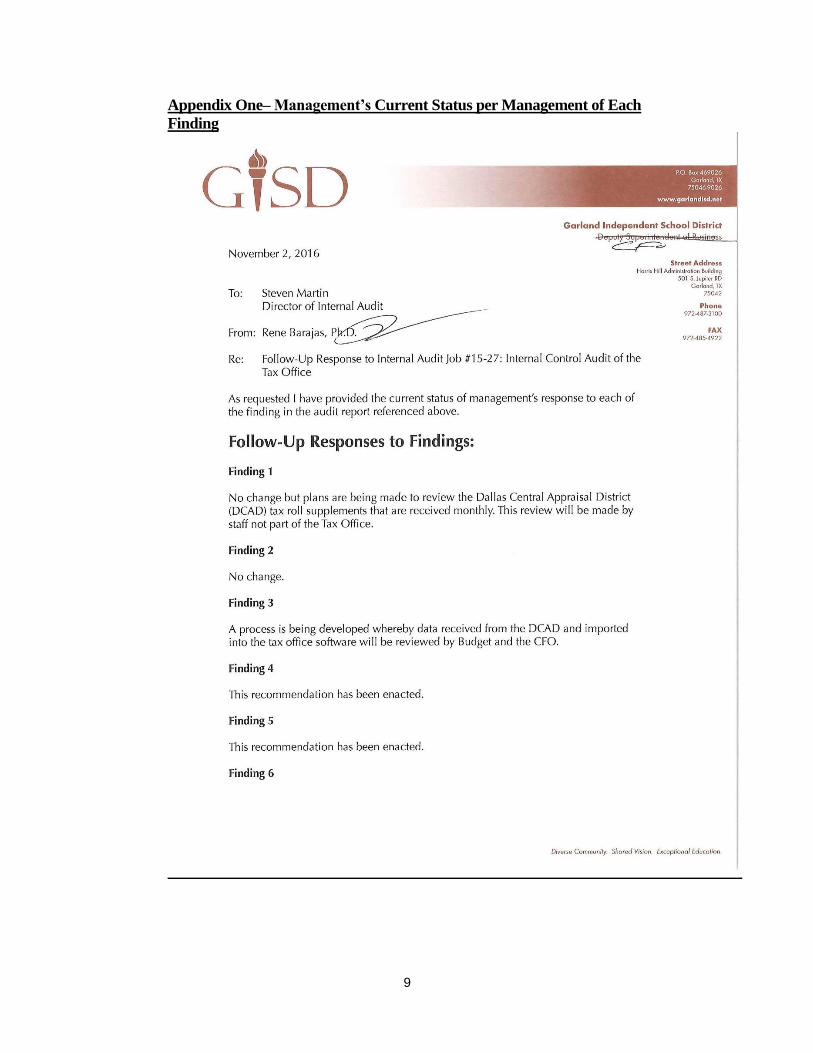

Appendix One– Management’s Current Status per Management of Each

Finding

10

11

12

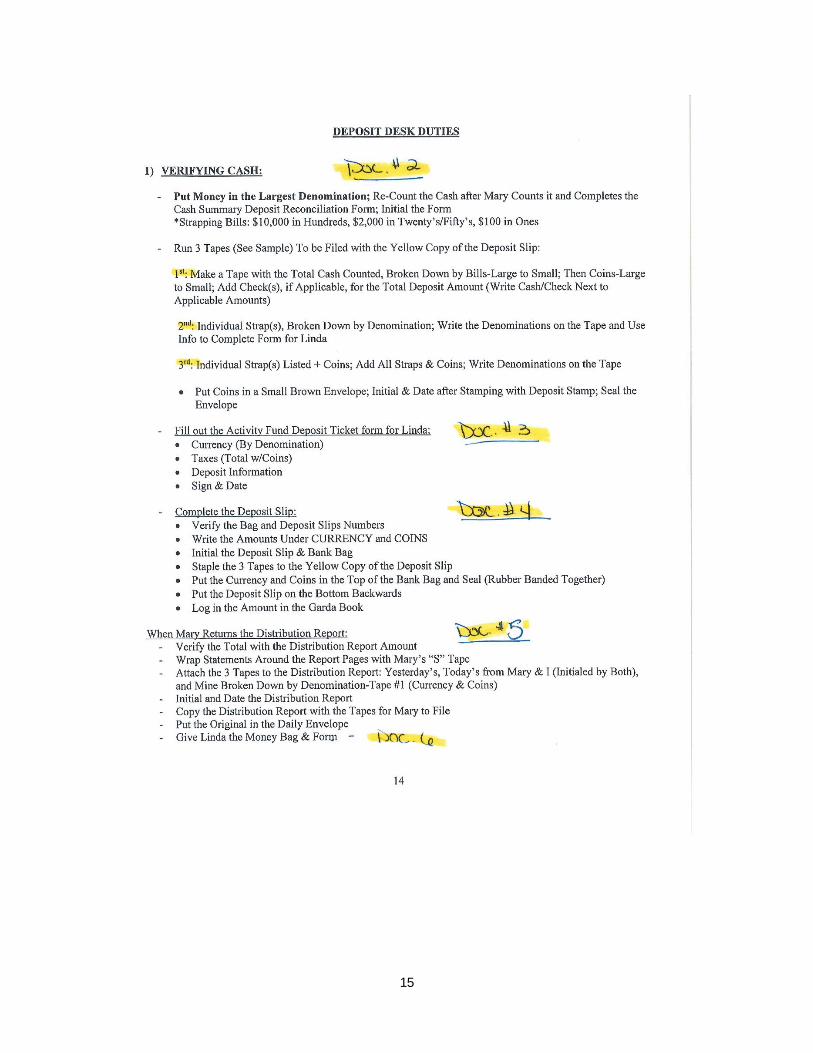

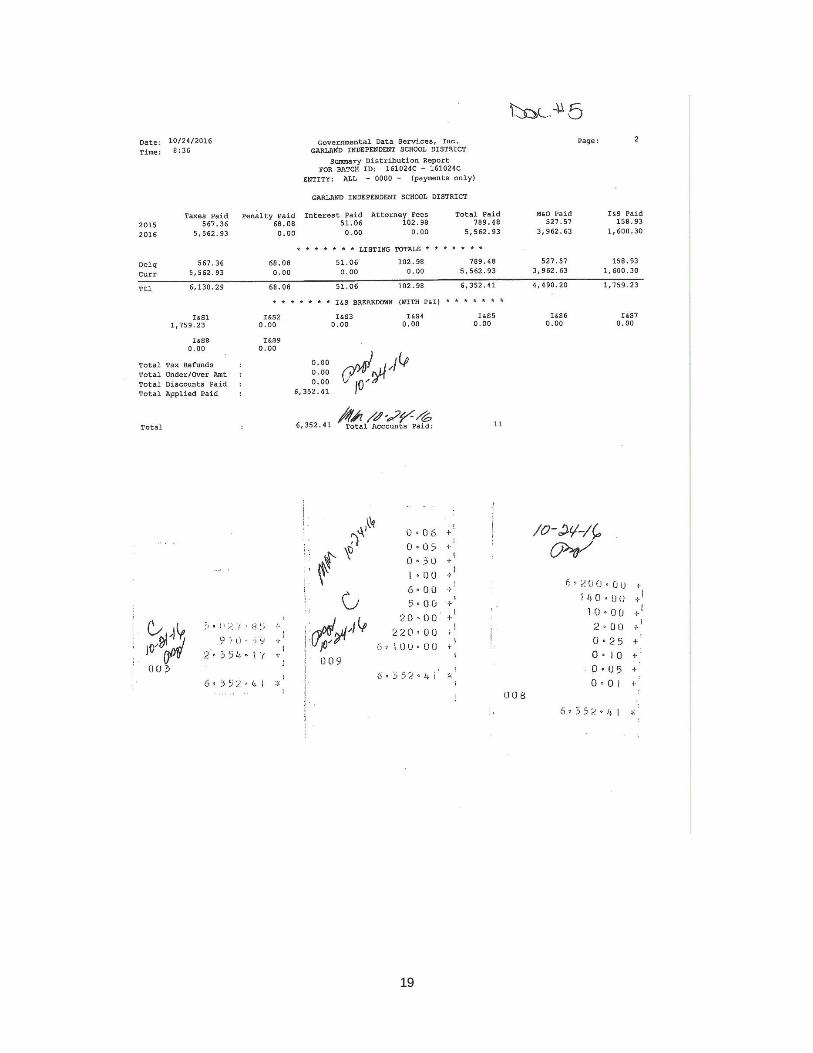

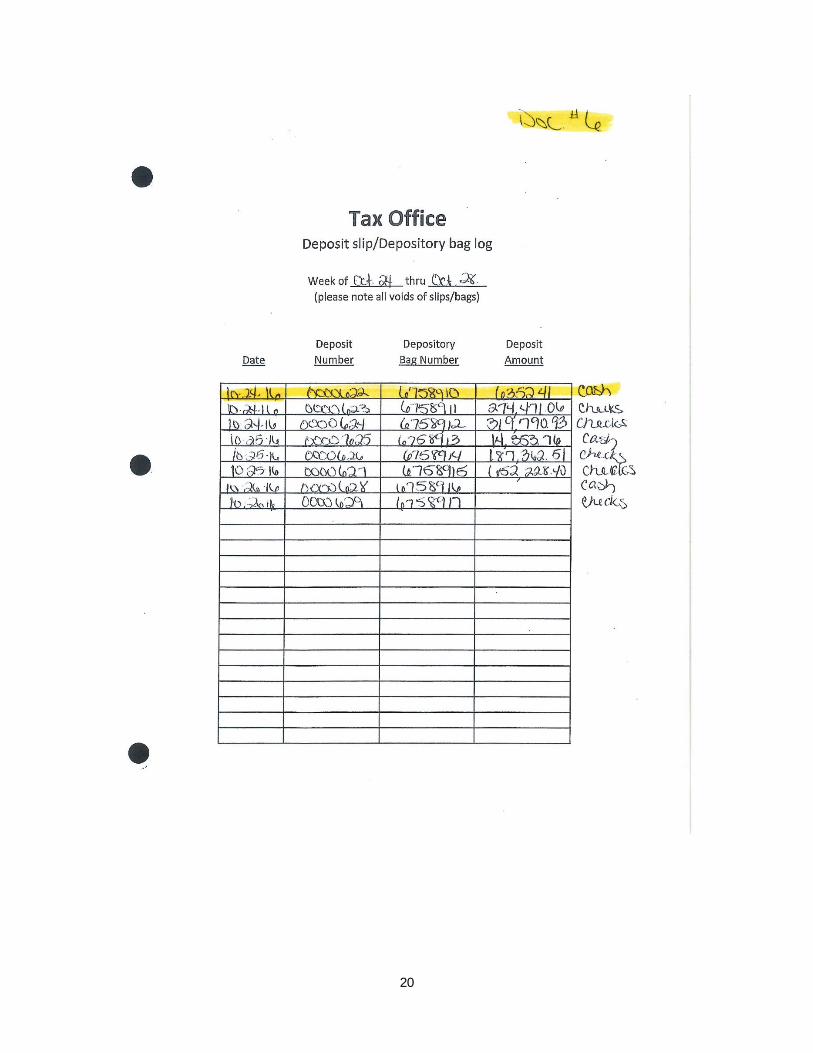

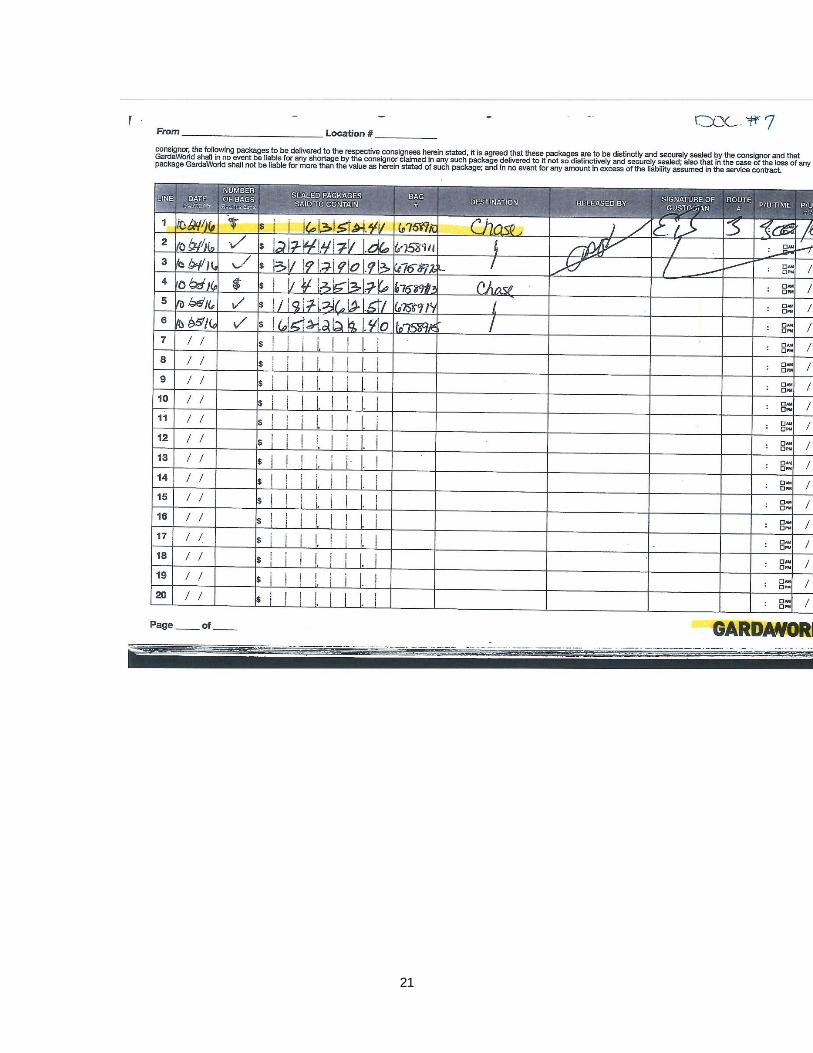

Appendix Two – Current Tax Office Tax Cash Handling Procedures

13

14

15

16

17

18

19

20

21

22

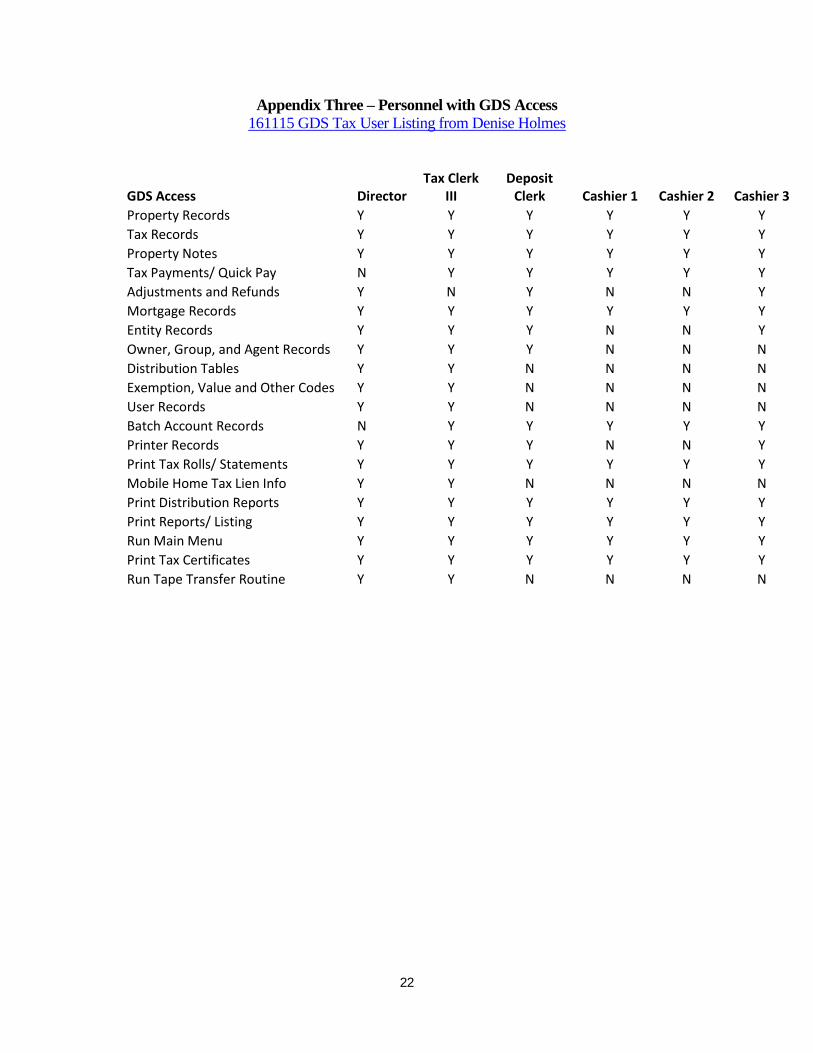

Appendix Three – Personnel with GDS Access

161115 GDS Tax User Listing from Denise Holmes

GDS Access Director Tax Clerk

III Deposit

Clerk Cashier 1 Cashier 2 Cashier 3

Property Records Y Y Y Y Y Y

Tax Records Y Y Y Y Y Y

Property Notes Y Y Y Y Y Y

Tax Payments/ Quick Pay N Y Y Y Y Y

Adjustments and Refunds Y N Y N N Y

Mortgage Records Y Y Y Y Y Y

Entity Records Y Y Y N N Y

Owner, Group, and Agent Records Y Y Y N N N

Distribution Tables Y Y N N N N

Exemption, Value and Other Codes Y Y N N N N

User Records Y Y N N N N

Batch Account Records N Y Y Y Y Y

Printer Records Y Y Y N N Y

Print Tax Rolls/ Statements Y Y Y Y Y Y

Mobile Home Tax Lien Info Y Y N N N N

Print Distribution Reports Y Y Y Y Y Y

Print Reports/ Listing Y Y Y Y Y Y

Run Main Menu Y Y Y Y Y Y

Print Tax Certificates Y Y Y Y Y Y

Run Tape Transfer Routine Y Y N N N N

23

Appendix Four – Findings in the Original Report

Tax Office

Lack of Separation of Duties – Tax Office

1) Criteria (Financial Accounting & Reporting, pdf page 529 & 547)

TEA FASRG Financial Accounting & Reporting Section 1.5.2.2 states, “Persons who

have authorized access to both assets and related accounting records may be in a

position to conceal shortages of the assets in the records. If duties are properly

segregated, persons who have authorized access to assets will not also have access to

related accounting records in which they might conceal shortages.”

Financial Accounting & Reporting Section 1.5.4.4 also states:

a. Segregation of the responsibilities for billing property taxes and services from

collection and accounting

b. Segregation of the responsibilities for maintaining detail accounts receivable

records from collections and general ledger posting

c. Segregation of collection, control and deposit of funds activities from

maintaining accounting records

d. Maintenance of the property tax assessment rolls by individuals not engaged

in any accounting or collection function

e. If EDP is used, maintenance of the principle of segregation of duties within

processing activities

Condition

Property taxes due the District are similar to a District bank account. The

management of District bank accounts involve a separation of duties in which one

person receives and deposits funds into the account, another writes the checks or

makes wire transfers, another records such receipts and payments in the District’s

books, and yet one more reconciles the bank account.

Yet such separation of duties are lacking at the Property Tax Office, where four

employees have access to make adjustments and issue refunds in GDS and have

access to cash and checks. The Director of Property Tax Services supervises the

issuances of tax bills, the receipt of cash and checks, the recording in the District’s tax

books (GDS software) as to what has been received, the write–offs of property taxes

due, and the write–down of property values.

The same cashiers that receive cash and check payments post such receipts to the Tax

Office’s accounting system of taxpayer accounts, GDS. Furthermore, the Director of

Tax Services, Tax Clerk III, and three Tax Clerks II have the ability to post

adjustments to individual taxpayer property valuations, upon which the tax due is

based, as well as to post refunds. The Director of Tax Services and the Tax Clerk III

supervise all four cashiers.

24

Per Gummelt, GDS Senior Programmer, adjustments to property values and tax due

can be made through GDS. The software also has the capability to track who makes

such entries (160302 email from Gummelt). The Director of Tax Services stated that

if unauthorized adjustments were made, there would be no red flags (160301 Denise

Holmes interview).

Effect

Tax Office personnel have access to cash and checks and also to accounting records.

Assets may be misappropriated and accounting records altered.

Cause

The same employees have access to cash, checks, and accounting records.

Recommendation

It is recommended that the accounting and treasury functions be functionally and

physically separated. One supervisor would supervise the receipt of cash and checks

while another would reconcile GDS to DCAD reports, provide such reconciliations

with supporting documentation to the Business Department for oversight, and

supervise property tax accounting and billing.

The supervisor of tax receipts and cashiers would not have the ability to make

adjustments in GDS but have read–only access in order to look up account

information. The supervisor of tax accounting and billing and related personnel could

make adjustments in GDS but not have access to cash and checks.

The current Tax Clerks would be separated between the accounting and treasury

functions. This separation of duties is not as efficient as having six people in one

office with overlapping duties, but it affords considerable more internal control. It is

probable additional personnel would need to be hired or more temporary personnel

used during the busy season.

2) Lack of Separation of Duties – GDS, contractor

Criteria (Financial Accounting & Reporting, pdf page 547)

TEA FASRG Financial Accounting & Reporting Section 1.5.4.4:

a. Segregation of the responsibilities for billing property taxes and services from

collection and accounting

b. Segregation of the responsibilities for maintaining detail accounts receivable

records from collections and general ledger posting

c. Segregation of collection, control and deposit of funds activities from

maintaining accounting records

d. Maintenance of the property tax assessment rolls by individuals not engaged

in any accounting or collection function

e. If EDP is used, maintenance of the principle of segregation of duties within

processing activities

25

Condition

GDS provides the annual tax roll data it downloads from the DCAD. It also provides

monthly tax data updates called “supplementals” (160201 Denise Holmes Interview).

GDS also processes credit and debit card payments, and electronic funds transfer

payments, on behalf of the District (GDS credit debit card agreement).

Effect

GDS has access to the District’s tax records, both the value of real estate and tax due,

and also to e–checks and credit card payments made to the District.

Cause

One vendor has access to both the District’s property tax records and property tax

payments.

Recommendation

Use a separate contractor from GDS, who provides original and monthly updated

accounting data, to collect credit card and e–check funds.

3) Lack of Testing and Reconciling of Taxes Receivable in GDS at the Beginning of the

Year and from One Month to the Next

Criteria (Financial Accounting and Reporting, pdf page 530)

TEA FASRG Financial & Accounting Reporting Section 1.5.2.3, Reconciliations and

Comparison of Assets with Records states, “The purpose of reconciliations and

comparisons of assets with records is to ensure that independent checks cover the

output of a system, either by maintenance of a separate independent control record

with which the processed data are reconciled or by direct comparison of the output

with the related assets. Monitoring is usually accomplished by reviewing

reconciliations or by participating in comparisons of assets. Examples of

reconciliations of assets with records are reconciliation of physical inventory to

accounting records and reconciliation of bank balance to general ledger balance.”

Financial & Accounting Resources Section 1.5.2.4, Analytical Review states, “The

purpose of analytical reviews is to evaluate summary information, usually resulting

from a series of transactions or processes, by comparing it with expected results.”

Condition

The certified property tax roll is provided by DCAD each July 25. The Tax Office

prints a PDF copy of such roll and monthly updates, but does not use this data for

either its tax calculations or invoicing. Instead, GDS also obtains such DCAD data

and downloads calculated taxpayer account data to the District’s servers, from which

invoices are mailed, payments recorded, and adjustments made. GDS also uploads to

the District monthly adjustments calculated from monthly DCAD updates. GDS is

not audited by an outside firm (160324 Gummelt regarding audit). The Tax Office

does not do analytical work or account testing to confirm the accuracy of GDS’s

26

calculation of taxes due, either at the beginning of or during the year (160330 Denise

Holmes).

Effect

The District is blindly relying on GDS to provide correct information. Although

DCAD is audited once every three years by the State Auditor, a similar audit is not

conducted on GDS. Accordingly, the property tax levies, either at the beginning of the

year or provided in monthly updates, could be incorrect or subject to fraud.

Cause:

The District does not in any way confirm or test that the data received each year and

then in monthly updates from GDS is correct.

Recommendation

GDS data received at the beginning of each school year should be sample tested for

correct tax levies. Additionally, analytical work should be conducted comparing taxes

due per GDS to an estimate by the Tax Office based on DCAD taxable amounts

multiplied by the District’s tax rate. Levy totals then on should be reconciled with

each monthly update supported by individual taxpayer account data including

payments, exemptions, overpayments, interest, and penalties. Such reconciliations

should be approved by either or both management outside of the Tax Office and the

Board.

4) Lack of Clearly Defined Audit Trail

Criteria (Financial Accounting & Reporting pdf page 14)

TEA FASRG Financial Accounting & Reporting, 1.1.3, Accounting Principles and

Policies, states, “The state board of education intent in prescribing these rules is to

cause the budgeting and financial accounting and reporting system of independent

school districts to conform with generally accepted accounting principles (GAAP)

established by the Governmental Accounting Standards Board (GASB) and the

Financial Accounting Standards Board (FASB) for accounting treatments not

specified in GASB pronouncements.”

Furthermore, Standards for Internal Control in the Federal Government, Appropriate

documentation of transactions and internal control, states, “Management clearly

documents internal control and all transactions and other significant events in a

manner that allows the documentation to be readily available for examination.”

GAAP and the Standards for Internal Control require what is commonly referred to as

an “audit trail,” in which supporting documents are clearly marked to indicate from

where they came.

27

Condition

The Tax Office’s deposit records for cash, checks, electronic checks, credit cards,

Remit system reports, and GDS reports saved for audits are not clearly marked.

Adding machine tapes are relied upon for reconciling without clearly detailing what is

being reconciled.

Effect

An auditor is unable to audit supporting documentation to GDS and Oracle entries

without explanation from Tax Office personnel.

Cause

Failure to clearly mark supporting documentation and their relation to each other,

journal entries, and deposits.

Recommendation

It is recommended that 1) cashier reconciling reports be used with clearly supported

supporting documents (Z–reports, bottom portion of tax bills, and a listing by

denomination of cash to deposit and remaining in the cash register drawer) and 2)

daily deposit summary reconciling reports be compiled with supporting documents

including the cashier reconciling reports, GDS Distribution reports, E–check and

Credit Card reports from the company GDS, Remit reports, copies of deposit slips, the

bottom portion of taxpayer bills, and Oracle screen shots.

The supporting documents filed in the vault should include a daily GDS reconciliation

with all supporting documents, and daily Cashier reconciliations, with all supporting

documents.

5) Lack of Accountability when Assets are Transferred Between Employees– Cashiers and

Deposit Clerk

Criteria (Financial Accounting & Reporting pdf page 540)

TEA FASRG Financial Accounting & Reporting, Section 1.5.4.2 Cash, Procedural

Controls, states, “Controls over the collection, timely deposit and recording of

collections in the accounting records in each collection location.”

Condition

Related to the lack of marking on Tax Office records, there is a lack of accountability

as assets, cash and checks, are transferred from one employee to another. When

Cashier drawers are taken to be counted, there is no receipt given to the Cashier.

Effect

Because there is no written agreement between the providing and receiving employees

when cash is transferred from one to another, there is a distinct lack of an audit trail as

to when responsibility is transferred, and if funds are missing, who should be held

responsible.

28

Cause

Lack of internal control and documentation regarding the transfer of an asset, cash and

checks.

Recommendation

A Cashier and the Deposit Clerk should count the Cashier’s drawer together,

reconciling on one page the Z–Report, tax bills, and cash/check count. When these

three items are reconciled and both the Cashier and Deposit Clerk agree, then both

should sign or initial the reconciliation page indicating agreement and that the Z–

Report, tax bills, and cash/checks have been relinquished from the Cashier to the

Deposit Clerk.

6) No Receipts Between Employees – Deposit Clerk and Tax Clerk II and then Tax Clerk

III

Criteria (Financial Accounting & Reporting pdf page 540)

TEA FASRG Financial Accounting & Reporting, Section 1.5.4.2 Cash, Procedurals

Controls, states, “Controls over the collection, timely deposit and recording of

collections in the accounting records in each collection location.”

Condition

When the Deposit Clerk leaves cash and checks for first a Tax Clerk II to count and

then a Tax Clerk III to count, there are no receipts documenting the asset transfer nor

do two parties count the cash and checks together.

Effect

There is a break in the audit trail and subsequently a break in the transfer of

responsibility between employees. Accordingly, if cash or checks come up missing,

there is no audit trail to assign responsibility.

Cause

Lack of internal control and documentation regarding the transfer of an asset, cash and

checks.

Recommendation

When the Deposit Clerk transfers cash and checks to another employee, both should

count the funds together and sign one form indicating the transfer is complete and

agreed to by both.

7) Three Employees Counting Cash Four Times

Criteria

District policy DFBB, (Local), states a reason for a term contract nonrenewal is “3)

Incompetency or inefficiency in the performance of duties.”

29

Condition

As documented in Appendix Five, Tax Office Work Flow, three Tax Office

employees count the same cash and checks four times.

Effect

Counting cash and checks four times wastes time and makes the cash and checks more

susceptible to loss by being exposed more than is necessary.

Cause

Three employees count the same cash and checks four times.

Recommendation

There is no need for three Tax Office employees to count cash. When cash was stolen

last summer from Tax Office receipts, it occurred after the last count, which could still

happen regardless of how many people count the cash. Each Cashier should count his

drawer with the Deposit Clerk, reconciling the Z–Report, cash and checks, and tax

bills, with each signing the Cashier Reconciliation Sheet. The Deposit Clerk should

then summarize the three Cashier Reconciliation Sheets on a Summary Deposit

Reconciliation Sheet which would also include checks and tax bills mailed in. The

total then would be reconciled to the cash and check deposit slips. These

reconciliation sheets, deposit slips, and tax bills would then be forwarded to the

Accounting side of the Treasury Office for posting to GDS, as well as to the Business

Office official who performs the daily GDS reconciliation as described below.

The Summary Deposit Reconciliation Sheet total would then be included in a Total

Property Tax Reconciliation Sheet which would also include payments made by e–

check and credit cards and refunds as evidenced by Blue Slips. The total funds

received would be reconciled to GDS Distribution Statements and print screen shots of

the funds being recorded in Oracle. The three reconciliation sheets would be filed at

the Treasury and Accounting divisions of the Tax Office, and with the General Ledger

Accountant. The GL Accountant would reconcile daily total property tax revenue and

refunds with a daily GDS report indicating how much in property taxes was due the

District (beginning balance, adjustments due to property value change, less payments,

add refunds, ending balance). This reconciliation would also take into account and

document adjustments made by the Tax Services Director to specific taxpayer

accounts including adjustments to property valuation due to supplemental reports and

the writing off of past due property taxes.

8) Tax Collector’s Bond to be approved by the Board

Criteria

Pursuant to District policy CG (Legal), “The tax collector for the District shall be

bonded in accordance with law. Tax Code 6.29,” (CG (Legal) Bonded Employees

and Officers). Tax Code 6.29 states, “the bond must be made payable to and must be

approved by the governing body of the unit in an amount determined by the governing

body,” (Tax Code Chapter 6 pdf page 38).

30

Condition

The tax collector for the District, Denise Holmes, has a $50,000 bond for the 2014–

2015 school year (Tax Collector's bond); however, Holmes stated that the Board

approved neither the bond nor the amount. The tax collector is in violation of District

policy and State law.

Cause

Failure to obtain Board approval of the bond and its amount.

Recommendation

The Director of Tax Services should at each annual renewal of her bond, obtain Board

approval of it and the amount. Such approval should be recorded in Board minutes.

9) Cash Deposit Bags not used in Numerical Order

Criteria (Financial Accounting & Reporting pdf page 543)

TEA FASRG Financial Accounting & Reporting, Section 1.5.4.2 Cash, Procedural

Controls, #31includes, “Controls and physical safeguards surrounding working (petty

cash) funds.” Additionally, Section 1.5.3, Exhibit 46, the Internal Control Checklist,

includes the use of prenumbered forms for receiving reports, purchase orders, and

payroll checks. Section 1.5.4.2 includes the use of prenumbered receipts for the

receipt of cash. The use of prenumbered cash bags, as with various forms, is a time–

tested addition to internal control, alerting accounting personnel and management if

sensitive forms or cash bags are missing or duplicated, indicating either error, fraud, or

theft.

Condition

Prior to the theft of $20,774 from the Tax Office that occurred from November 2014

to May 2015, Tax Office personnel did not use numbered cash deposit bags in

consecutive order (151019 interview of Cooper, Figueroa, Santos, Powers).

Effect

By not using consecutive cash bags and thus accounting in a log for all cash bags, it

would not be noticed if a particular cash bag was missing. For example, it would be

possible for a taxpayer to pay $2,000 in property taxes, and then for that amount to be

placed into a cash bag, yet that particular bag not given to the courier service. Then

the taxpayer’s account could be adjusted to show that no cash was due. Later a Tax

Office employee could secrete the bag out of the office. Because the bag numbers

listed in the courier logbook kept in the Tax Office were not in consecutive order, a

missing bag would not be noticed. Accordingly, not using cash bags in consecutive

order decreases internal control.

Cause

Failure to implement internal control provided by the cash bag manufacturer.

31

Recommendation

As can be seen in Appendix II – Interim Tax Office Recommendations – Internal

Audit previously made recommendations including the use of cash bags in numerical

order. It was seen on February 8, 2016, by reviewing the last three Garda log book

pages, that the cash bags are now being used in order (160208 received from Powers

pdf pages 5–7).

10) No Point of Sale Receipt from either the Cash Registers or GDS

Criteria (Financial Accounting and Reporting, pdf page 542)

TEA FASRG Financial Accounting & Reporting Section 1.5.4.2, states “Receipts

controlled by cash register, prenumbered receipts or other equivalent means if

payments are made in person (over the counter).”

Condition

As documented in Appendix Five – Tax Office Work Flow, no point of sale receipt

from the cash registers is provided to taxpayers.

Effect

A person making payment to an organization is an integral part of the internal control.

By receiving a receipt issued by the cash register, management has some assurance

that the total amount indicated on the cash registers reports are the sum of the cash

register receipts provided to taxpayers. If a taxpayer receives an incorrect receipt, he

or she is likely to notify District management.

Cause

Cash register receipts are not issued to taxpayers. Instead, when cash payments are

received, each cashier has his or her own receipt book from which a receipt is given to

a taxpayer. The amounts from the receipt books are not recorded in any journal for

comparison to cash register totals. When checks are received over the counter, the

cash register is not rang up. “Paid” is stamped on the taxpayer’s bill. There is no

journal entry to record the immediate receipt of checks. Instead, checks are laid aside

for entry into GDS, but this may not happen until much later after the check has been

received.

Recommendation

Cash register receipts should be issued to taxpayers for the receipt of cash and checks.

Although taxpayers are currently given handwritten receipts for cash, such receipts are

not included in any daily journal and, accordingly, are not included in any daily

reconciliation. Additionally, no receipt is currently given for checks and,

consequently, no immediate record is kept of such receipt. Instead, tax bills are

stamped “paid.” Furthermore, even if handwritten or spreadsheet journals of cash and

checks were maintained, they would not automatically tie to the cash registers as are

cash register receipts.

32

11) Board to approve $500 Refunds, not Given Notice for $2,500 Refunds

Criteria (TX Property Tax Code 2015 Edition, Section 31.11)

Texas Property Tax Code states, “If a taxpayer applies to the tax collector of a taxing

unit for a refund of an overpayment or erroneous payment of taxes, the collector for

the unit determines that the payment was erroneous or excessive, and the auditor for

the unit agrees with the collector’s determination, the collector shall refund the amount

of the excessive or erroneous payment from available current tax collections or from

funds appropriated by the unit for making refunds. However, the collector may not

make the refund unless:

a) in the case of a collector who collects taxes for one taxing unit, the governing

body of the taxing unit also determines that the payment was erroneous or

excessive and approves the refund if the amount of the refund exceeds:

i. $5,000 for a refund to be paid by a county with a population of two

million or more; or

ii. $500 for a refund to be paid by any other taxing unit;

b) in the case of a collector who collects taxes for more than one taxing unit, the

governing body of the taxing unit that employs the collector also determines

that the payment was erroneous or excessive and approves the refund if the

amount of the refund exceeds:

i. $5,000 for a refund to be paid by a county with a population of two

million or more; or

ii. $2,500 for a refund to be paid by any other taxing unit

TEA FASRG Financial Accounting & Reporting, Section 1.5.4.4, #41, includes as a

Procedural Control “Formally approved write–offs or other reductions of receivables

by senior officials not involved in the collection function.”

Condition

The Director of Tax Services stated that per Board policy, the Board is notified when

refunds are $2,500 or more (160201 Denise Holmes Interview). When asked to

provide the policy, Holmes emailed, “I can’t find a policy about refunds of $2,500

either. The property tax code, Sec. 31.11, speaks of refunds of $500 for collectors that

collect for one taxing unit needing approval. It is my understanding that we use to take

refunds of $500 or more to the Board years ago, but there started to be so many that

the dollar amount was increased to $2,500 when Jerry Jones was tax assessor. We

have continued with that amount since that time. Mr. Jones was two assessors before

me and retired in 2005” (160301email from Denise Holmes re Board Refunds).

Effect

State law has been violated for over ten years providing insufficient information to the

Board of Trustees to enact their duties.

Cause

Failure to abide by State law.

33

Recommendation

Follow State law and obtain Board of Trustees approval, not just notification, for

refunds of $500 or more.

12) No Support Provided to the Business Office for Adjustments in Oracle of Levy

Adjustments

Criteria (Financial Accounting and Reporting, pdf page 551)

Financial Accounting & Reporting Section 1.5.4.4, Revenues and Receivables,

Procedural Controls, Billing Remittance Verification, Property Taxes, Accounts

Receivable Recordkeeping, #44, states, “Reconciling the aggregate collections on

accounts receivable against postings to individual receivable accounts.”

Condition

The General Ledger Accountant monthly adjusts the amount due from property taxes

based upon an unsupported number provided by the Tax Office (Barron).

Effect

Changes may be made by either GDS or Tax Office personnel to taxpayer accounts

without oversight or reconciliation by the Business Office.

Cause

No support is provided by the Tax Office to the Business Office to support such

changes to taxpayer accounts.

Recommendation

A list of taxpayer accounts adjusted should be provided to the Business Office so that

they can sample test the changes with DCAD data.

13) Failure to Conduct a Risk Assessment

Criteria (Financial Accounting and Reporting, pdf page 524)

Financial Accounting & Reporting Section 1.5.1, Internal Control – Defined, includes

Risk Assessment as one of five interrelated components. Section 1.5.2 includes the

following definition:

Risk assessment is defined as the “entity’s identification, analysis, and management of

risks” relevant to the preparation of GAAP financial statements.

Risks can arise or change as a result of the following factors:

• Changes in operating environment

• New personnel

• New or revamped information systems

• Rapid growth

• New technology

34

New grant activities, building projects and other activities

• Organizational restructuring

• Accounting pronouncements

• Federal regulations

• School finance statutes

Condition

No Risk Assessment has been done by the Tax Office (160330 Denise Holmes).

Effect

A credible Risk Assessment leads to the design and use of credible Control Activities.

Cause

The Tax office is not following guidance per the Texas Education Agency’s Financial

Accountability System Resource Guide.

Recommendation

Conduct a Risk Assessment for approval by the Business Department, with

corresponding Control Activities, Information and Communications Systems, and

Business Department monitoring.

Business Department

14) Lack of Management Monitoring

Criteria (Financial Accounting and Reporting, pdf page 530–551)

TEA FASRG Financial Accounting & Reporting Section 1.5.2.3, Reconciliations and

Comparison of Assets with Records, states, “The purpose of reconciliations and

comparisons of assets with records is to ensure that independent checks cover the

output of a system, either by maintenance of a separate independent control record

with which the processed data are reconciled or by direct comparison of the output

with the related assets. Monitoring is usually accomplished by reviewing

reconciliations or by participating in comparisons of assets. Examples of

reconciliations of assets with records are reconciliation of physical inventory to

accounting records and reconciliation of bank balance to general ledger balance.”

Section 1.5.4.2, #39, includes as a Procedural Control, “Review and approval of all

reconciliations and investigation of unusual reconciling items by an official who is not

responsible for receipts and disbursements, including recording evidence of the review

and approval by signing the reconciliation.”

Furthermore, Section 1.5.4.4, #39, Revenues and Receivables, also includes as a

Procedural Control, “Monitoring taxes and fees collected by another unit of

government to assure timely receipt and subjecting amounts received to reviews for

reasonableness,” and #44, “Reconciling the aggregate collections on accounts

receivable against postings to individual receivable accounts.”

35

Condition

Nobody at the Business Office has access to GDS. Although daily GDS reports are

sent to the General Leger Accountant and an Accounting Specialist (who does the Tax

Office bank reconciliation) weekly, when asked if they do anything with them, the

reply was, “Not really, they get and keep them,” (Barron & Pate). The Accounting

Specialist said the daily GDS reports are “helpful to balance the Tax Office bank

account,” (160223 Alsabrook). At the beginning of the school year, the general and

debt service funds, Current Property Tax Levy accounts are debited and the related

Deferred Revenue Taxes Accounts credited ( Oracle beginning tax receivable entry).

No supporting documentation for Deferred Revenue Taxes is maintained; it is only a

balancing account.

At each month’s end, the General Ledger Accountant makes a forced entry in Oracle

to adjust the General and Debt Funds Property Taxes Current and Delinquent Funds to

the amounts shown on the monthly Tax Office Report provided to the Tax Office, as

supported by GDS (T account analysis of Jan 16 Tax Office entries sheet one). The

focus is on ensuring that the property tax receivable accounts, for both the general and

debt funds, current and delinquent accounts, ties to the GDS amounts. The offsetting

entries are to the related Deferred Revenue Taxes accounts (160321 pm Barron).

There are no supporting documents for the Deferred Revenue Taxes accounts (160321

Barron interview). The monthly adjustments to the Current and Delinquent Tax Levy

as shown in the monthly Tax Collection Reports presented to the Board are not

reviewed by the Business Office (160321 pm Baron interview pdf page 6). The

General Ledger Accountant stated that the Business Office does not monitor GDS

(160223 Barron).

The Tax Office monthly provides a spreadsheet including the certified taxable

valuation in July, and then supplemental valuations each month thereafter to the

Deputy Superintendent of Business. However, the reasons for increases and decreases

in such valuations are not reviewed (160330 Denise Holmes).

Effect

The Tax Office has no oversight by the Business Department.

Cause

The Business Department does not monitor taxes receivable, write–offs, payments,

and valuation changes.

Recommendation

No one was found to monitor the adjustments made by the Director of Tax Services or

the Tax Clerk III, both of whom have said they are able to make any adjustments to

taxpayer accounts. While write–offs of past due accounts of $500 were to have been

approved by the Board of Trustees, there is no administration monitoring that this

actually occurs (160223 Baron). In fact, the Director of Tax Services has only been

submitting write–offs of past due accounts of $2,500 or more in violation of State law.

36

Additionally, there is no monitoring of the necessity of any adjustments. Finally, no

evidence was seen that taxpayer accounts are reconciled monthly, with the total from

the beginning of month “A” compared to the beginning of month “B,” with revenue

totals as evidenced by deposits added, and decreases owed because of supplementary

reports, including “ceilings” and added exemptions included. Put simply, it is possible

for the Director of Tax Services or Tax Clerk III to write–down taxpayer account

balances without any oversight or knowledge of the administration. The Business

Department should exert oversight of the Tax Office.

15) Not Using a Source Document with which to Reconcile

Criteria (AU–00326 Audit Evidence)

“Appropriateness is the measure of the quality of audit evidence, that is, its relevance

and its reliability in providing support for, or detecting misstatements in, the classes of

transactions, account balances, and disclosures and related assertions. The auditor

should consider the sufficiency and appropriateness of audit evidence to be obtained

when assessing risks and designing further audit procedures. The quantity of audit

evidence needed is affected by the risk of misstatement (the greater the risk, the more

audit evidence is likely to be required) and also by the quality of such audit evidence

(the higher the quality, the less the audit evidence that may be required). Accordingly,

the sufficiency and appropriateness of audit evidence are interrelated.”

Condition

The Business Office’s General Ledger Accountant monthly reconciled Oracle entries

provided by the Tax Office to a Tax Office generated spreadsheet of taxes collected.

Although the General Ledger Accountant was not actively monitoring or auditing the

Tax Office, even the act of reconciling Oracle, the District’s books, should involve

using the best and most relevant evidence available, which in this instance is the Tax

Office’s software records, GDS, and not rely entirely on a Tax Office generated

spreadsheet.

Effect

Although the General Ledger Accountant had access to GDS reports and could have

reconciled to them, he reconciled to evidence that was not as relevant, a report

prepared by the Director of Tax Services. This meant that if the Tax Office report was

in error or fraudulently prepared, the General Ledger Accountant would have

perpetuated the error or fraud.

Cause

Failure to reconcile using the best and most relevant evidence available.

Recommendation

The recommendation by IA was made during the audit that the General Ledger

Accountant reconcile Oracle to GDS reports and not rely entirely on the Tax Office

37

spreadsheet. The General Ledger Accountant made this change during the audit.

(Barron)

16) Lack of Bank Reconciliations

Criteria (Financial Accounting and Reporting, pdf page 530–551)

TEA FASRG Financial Accounting & Reporting Section 1.5.2.3, Reconciliations and

Comparison of Assets with Records, states, “The purpose of reconciliations and

comparisons of assets with records is to ensure that independent checks cover the

output of a system, either by maintenance of a separate independent control record

with which the processed data are reconciled or by direct comparison of the output

with the related assets. Monitoring is usually accomplished by reviewing

reconciliations or by participating in comparisons of assets. Examples of

reconciliations of assets with records are reconciliation of physical inventory to

accounting records and reconciliation of bank balance to general ledger balance.”

Condition

The Bank of America account used by the District’s Tax Office was not reconciled

from November 2014 until July 2015 (Alsabrook interview). During this time, eight

Tax Office bank deposits were short of cash totaling $20,774 (people who participated

in deposits).

Effect

The first theft was followed by seven more, occurring over nine months, without

detection by the Business Department because the bank reconciliations were not

completed.

Cause

Bank accounts were not timely reconciled by the Business Department.

Recommendation

Bank reconciliations should be prepared in a timely manner. Per the Director of

Finance, this has been corrected, and bank reconciliations are being timely done.

Additionally, per the Board’s direction, IA is conducting quarterly performance audits

in 2016 regarding bank reconciliations.

17) No DCAD Appraisal Review Board Monitoring and Challenges

Criteria (TX Property Tax Code pdf page 248)

Texas Property Tax Code Section 41.03, Challenge by Taxing Unit states:

(a) A taxing unit is entitled to challenge before the appraisal review board:

(1) the level of appraisals of any category of property in the district or in any

territory in the district, but not the appraised value of a single taxpayer’s

property;

(2) an exclusion of property from the appraisal records;

(3) a grant in whole or in part of a partial exemption;

38

(4) a determination that land qualifies for appraisal as provided by Subchapter C,

D, E, or H, Chapter 23; or

(5) failure to identify the taxing unit as one in which a particular property is

taxable.

(b) If a taxing unit challenges a determination that land qualifies for appraisal under

Subchapter H, Chapter 23, on the ground that the land is not located in an aesthetic

management zone, critical wildlife habitat zone, or streamside management zone, the

taxing unit must first seek a determination letter from the director of the Texas Forest

Service.

Additionally, the fifth component of TEA mandated Internal Control activities is

Monitoring Activities (Appendix Thirteen, page 55).

Condition

No Business Department or Tax Department employee was found to monitor DCAD

Appraisal Review Board decisions as they relate to the District. Additionally, the

Director of Tax Services does not recall the District ever challenging a decision of the

DCAD Appraisal Review Board (60301 Denise Holmes interview).

Effect

Such ARB decisions may adversely affect the District’s tax base.

Cause

Lack of active monitoring.

Recommendation

A Business Department employee should be assigned the task of monitoring ARB

decisions and periodically reporting on same to the Deputy Superintendent of

Business, the Superintendent, and the Board, so an understanding is gained as to the

affect such decisions have on the District’s tax base and, if appropriate, to mount a

challenge.

Technology Department

(Note: both of the Technology Department findings were corrected during the course

of the audit)

18) No Off–Site Backup

Criteria (Financial Accounting and Reporting, pdf page 571)

Section 1.5.4.8, Information Technology, Procedural Controls, includes “Procedures

to protect against a loss of important files, programs or equipment.”

Condition

The production servers on which the District’s taxpayers account data are maintained

are only approximately ten feet from the server on which the data was daily backed

up. The data was not being saved off site.

39

Effect

If there was a fire, flood, explosion, tornado, or earthquake at the Dr. Marvin D.

Roden Technology Center, there would have been the possibility of the District’s

taxpayer data being lost, putting at risk millions of dollars of revenue (McGuire,

Network Engineer interview).

Cause

Lack of off–site backup of taxpayer account data.

Recommendation

Internal Audit made the recommendation when the issue was discovered and it was

corrected during the course of the audit. The server on which taxpayer data is stored is

now backed up on site for 35 days and also a tape is sent off–site which includes

taxpayer accounts, which is saved for seven days (email from McGuire weekly

backups being sent offsite).

19) Lack of Friday Backup until Monday

Criteria: (Financial Accounting and Reporting, pdf page 571)

Section 1.5.4.8, Information Technology, Procedural Controls, includes “Procedures

to protect against a loss of important files, programs or equipment.”

Condition

Although a daily backup was conducted on the District’s taxpayer accounts, it was set

for Monday through Friday, at 1:30 a.m. This meant that the work done on Fridays

was no backed up until early Monday morning.

Effect

This placed Tax Office work at risk of being lost over a period of three days, instead

of one.

Cause

Friday’s backup did not occur until after Saturday and Sunday.

Recommendation

This was changed during the audit so that the daily backups would occur on Saturday

mornings as well. (McGuire, Network Engineer interview). The in–house backup is

saved for 35 days. (160204 from McGuire regarding backups).

Observation

Tax Office Employee Placed on Administrative Leave after Theft Still has Access to GDS

As can be seen in Appendix 10 (page 44), a Tax Office employee, placed on administrative

leave since late last year because he/she was the last employee to handle District tax receipts

before they went missing, as of February 18, 2016, still had access to GDS, including the

40

ability to make adjustments and record refunds (160223 GDS Tax User Listing from Denise

Holmes pdf page 9).

41

Appendix Five – Management’s Response to Original Findings

42

43

44

45

Appendix Six – Request for Management Response