Embed Size (px)

Citation preview

Internal Controls Environment:A Tax PerspectiveA Tax Perspective

John Bennecke, Managing Director, Chicago Jennifer Lau, Senior Manager, Chicago

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 1

AgendaAgenda

Setting The Stage Current Tax Environment Current Tax Environment Tax Process / Risk Areas Examples

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 2

Setting The StageSetting The StageAs Corporations continue to evolve and expand into the ever changing global economy, they must continually update and transform theirglobal economy, they must continually update and transform their accounting and tax reporting environment to adjust to the changes.

Unfortunately while the accounting and tax compliance / financialUnfortunately, while the accounting and tax compliance / financial reporting requirements are running at warp speed to keep pace, the internal controls environment in many organizations has lagged and is struggling to catch-up.struggling to catch up.

The result is an organization with an alarming risk profile in one of the areas which presents a significant organizational risk internally andareas which presents a significant organizational risk, internally and externally .

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 3

In the NewsIn the News…The number of audit deficiencies continues to grow -

The PCAOB’s 2011 inspection reports will show an increase in audits found to have serious problems which includes a number of cases where “audit work wasn’t completely or properly conducted, p y p p y ,or the company’s financial statements were contradicted by other evidence.”“In the reports issued last year, the board found deficiencies in p y , f fnearly a third of audits examined at Big Four accounting firms.”

- Rapoport, Michael. “Audit Firms’ Work Deemed Deficient.” Wall Street Journal 17 September 2012: C3 PrintSeptember 2012: C3. Print

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 4

Current EnvironmentCurrent EnvironmentToday’s Internal Audit environment has changed dramatically f 2002from 2002:

Shift in focus from reporting and compliance requirements to strategic, operational and financial maturation of an organization’s processes

Reliance on Internal Audit to identify linkages between departments and mitigate the related exposures

Leveraging subject matter experts to gain in-depth knowledge of the various process areas

Expectation of collaboration between Internal Audit and the various pdepartments to further enhance process and control best practices

Leveraging internal audit work to gain external audit reliance

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 5

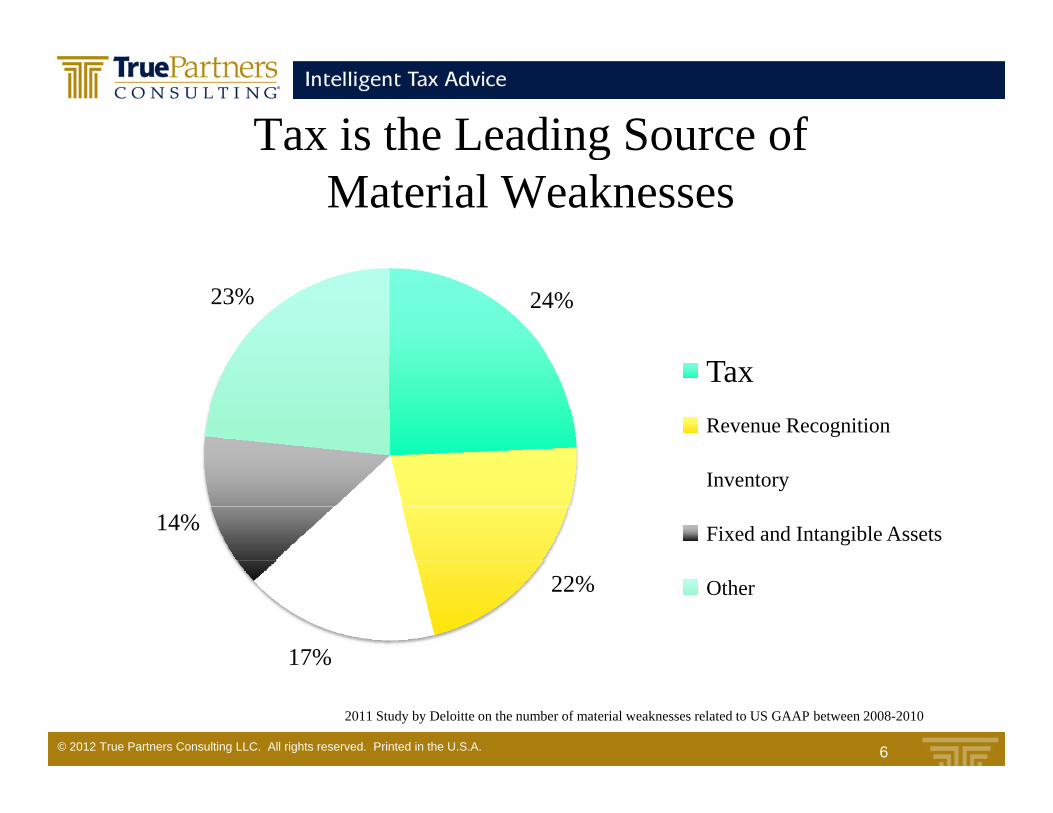

Tax is the Leading Source of s e e d g Sou ce oMaterial Weaknesses

24%23%

TaxRevenue Recognition

14%

Inventory

Fixed and Intangible Assets

22%

17%

Other

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 6

17%

2011 Study by Deloitte on the number of material weaknesses related to US GAAP between 2008-2010

Tax is the Leading Source of s e e d g Sou ce oMaterial Weaknesses

A review of financial statement disclosures reveals that the top 5 causes of tax material weaknesses1 are tt ib t d tattributed to:

Insufficient review by management (23%)Personnel (lack of training resource constrained) (22%) Personnel (lack of training, resource constrained) (22%)

Lack of general procedures or process (13%) Inadequate reconciliation (10%) Inadequate reconciliation (10%) Improper treatment/recording (10%)Note > All of these areas should be addressed in companies’ Controls Environment.

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 7

12011 Study by Deloitte on the number of material weaknesses related to US GAAP between 2008-2010

Internal Audit and TaxInternal Audit and TaxIn meetings with several Internal Audit Executives over the past several months, we have learned the following:

Internal Audit Departments typically rely on support outside of their function when it comes to Tax

Dedicated Internal Audit service providers many times need to partner with others to provide technical expertise with respect to Tax

Tax Departments typically rely on original SOX documentation Tax Departments typically rely on original SOX documentation from 2004/2005

Transactions many times create gaps in the internal control environmentenvironment

SOX documentation and controls remain static while the organizations have changed (reorganizations, staffing, roles and responsibilities )

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 8

responsibilities )

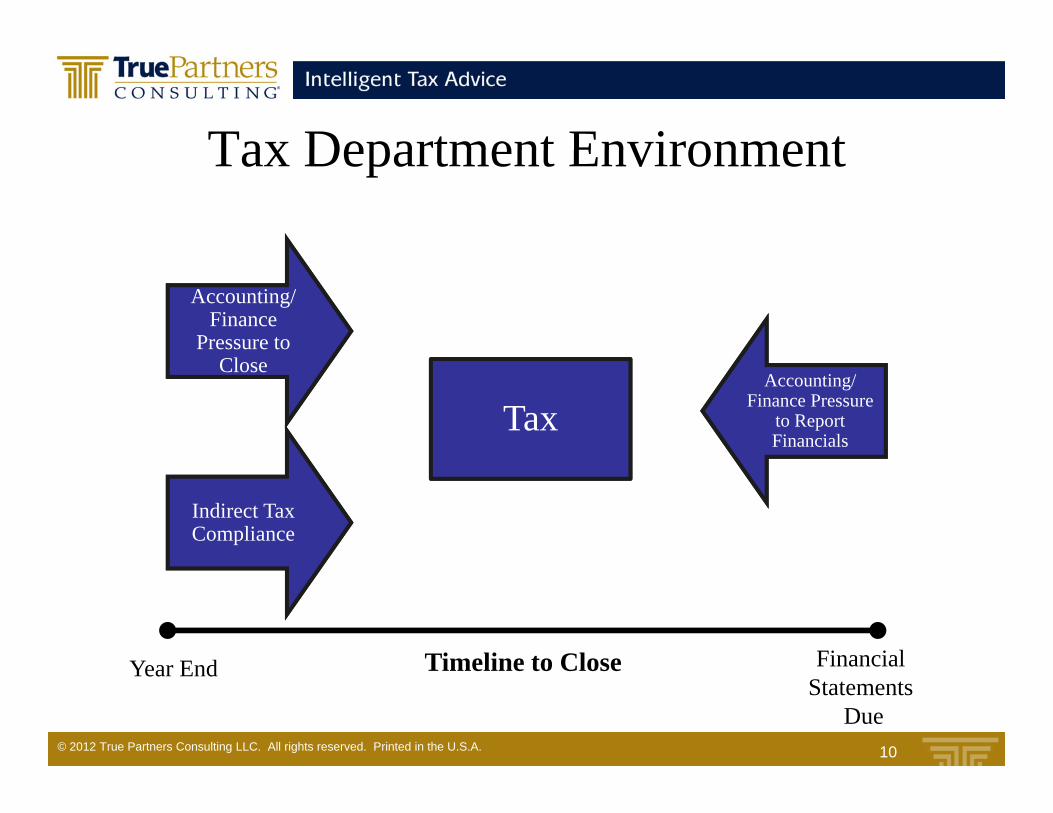

Tax Department EnvironmentTax Department Environment

Tax departments are facing a number of challenges:Tax departments are facing a number of challenges: Shorter financial close cycles Shortages of tax talent Increased transparency in financial/tax reporting Pressure to link value drivers with enablers Increased regulatory requirements Increased regulatory requirements Managing cost of functions Competing goals with Finance

Timing Timing Talent Communication Chain

Lower risk tolerance (Internal / External)

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 9

Lower risk tolerance (Internal / External)

Tax Department EnvironmentTax Department Environment

Accounting/ Finance

Pressure to

TaxAccounting/

Finance Pressure to Report Financials

Close

Indirect Tax Compliance

Timeline to CloseY E d Financial

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 10

Timeline to CloseYear End Financial Statements

Due

Tax Internal Control EnvironmentMacro Level

Tax Financial Reporting ( i i i )Financial (Provisioning)Financial

Reporting

T C li

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 11

Tax Compliance= key control

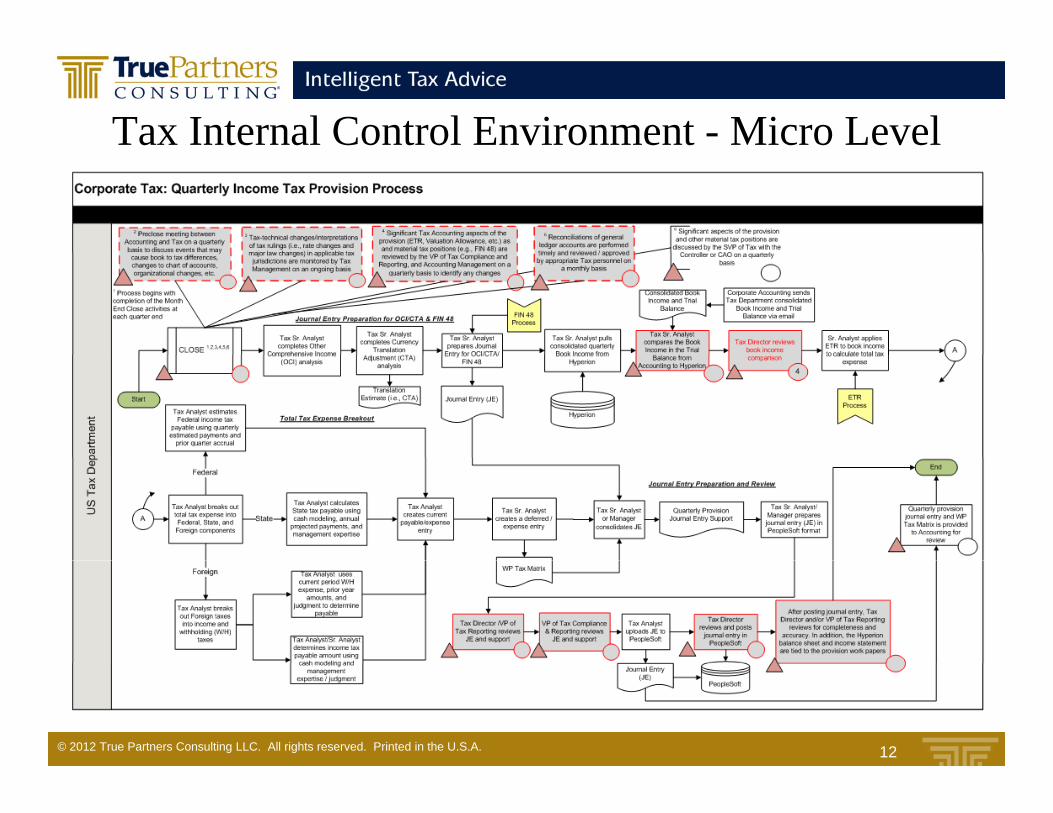

Tax Internal Control Environment - Micro Level

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 12

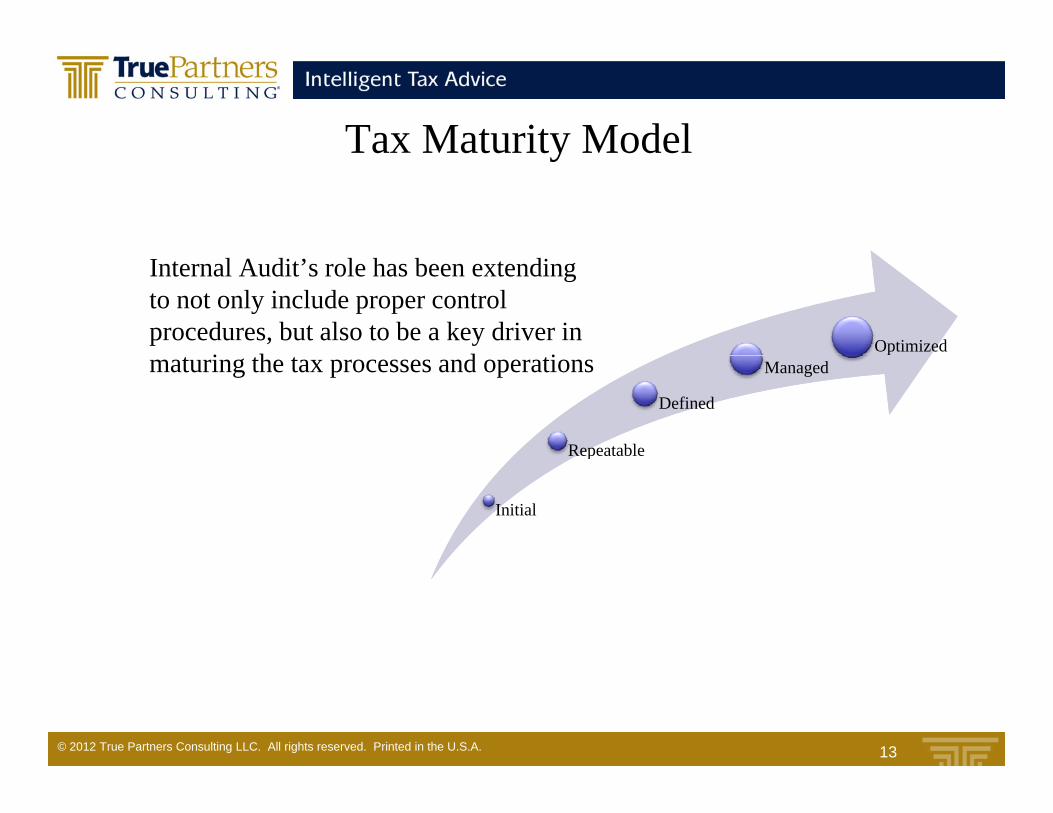

Tax Maturity ModelTax Maturity Model

Optimized

Internal Audit’s role has been extending to not only include proper control procedures, but also to be a key driver in

i h d i

Repeatable

Defined

Managedmaturing the tax processes and operations

Initial

p

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 13

Tax Maturity ModelInitial Repeatable Defined Managed Optimized

ople

Limited or outsourced tax department

Resources and knowledge limited to select

Adequate internal tax department staffing of critical functions within Tax

Leveraged tax department

Team efficiency maximized by leveraging knowledge and resources at the appropriate levels

Regularly evaluates the need to reorganize Tax Department to leverage / optimize strengths of team members

Tax Departmentorganizational structure is globally aligned with corporate strategy and

Peo limited to select

individuals

Limited in skill sets and industry knowledge

Leveraged tax department personnel and knowledge sharing

Strategic use of external resources

management

Strategic use of external resources

Undocumented and undefined policies and

Documented policies,procedures and controls

Clearly defined roles and responsibilities in accordance

Continual strengthening of existing controls and

Use of automated solutions, which may be leveraged

Proc

ess

undefined policies and processes

Ad hoc process and minimum controls

procedures and controls

Review policies, proceduresand controls on an annual basis and updated accordingly for changes

responsibilities in accordance with the existing tax department structure and within the appropriate process flows

existing controls and processes, to address any organizational / business changes

Create detailed process manuals and desktopprocedures

which may be leveraged across multiple process areas, such as compliance, financial reporting, mgmt reporting, etc.

Existing processes have the ability to tolerate changes toprocedures ability to tolerate changes to the company structure

nolo

gy

Spreadsheet dependant

Minimal internal use of available technology solutions

Use of standard templates and Excel spreadsheets

Spreadsheet maintenance performed annually and

Standardized workpapers designed across all tax processes (ex. integration of tax compliance and tax

i i i )

Implemented effective system and spreadsheet control procedures

Use of appropriate

Implement automated solutions to build in efficiencymitigate risk, and serve multiple strategic goals

Tech

n solutions performed annually and update accordingly, in coordination with company policy and procedures

provisioning) Use of appropriate technology tools, where applicable

Use of a department intranet, SharePoint solution, etc.

gic

Not strategically aligned within organization

Not strategically aligned within organization

Tax plays a role in executionof strategic initiatives and

Tax plays a role and isactively involved in strategic

Strategic alignment of Tax / Accounting / Finance

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 14

Stra

teg decisions organizational decisions Tax is proactive in

implementing solutions to adapt to the changing environment

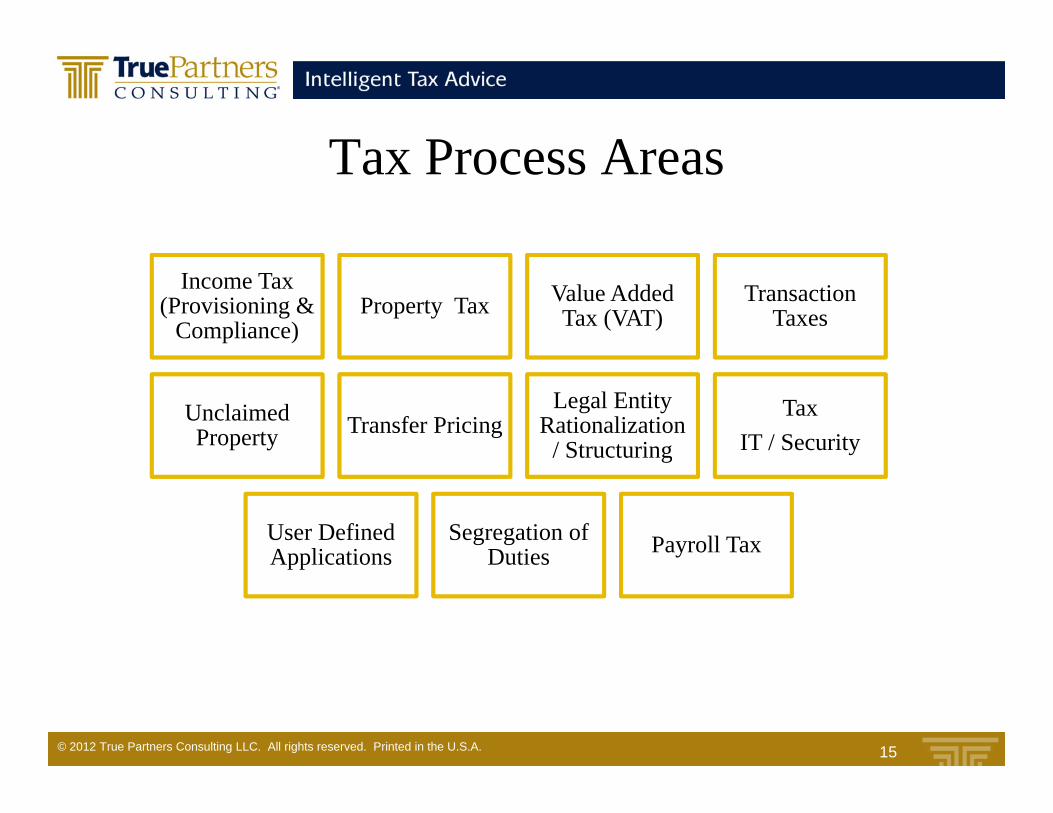

Ta Process AreasTax Process Areas

Income Tax (Provisioning &

Compliance)Property Tax Value Added

Tax (VAT)Transaction

Taxes

Unclaimed Property Transfer Pricing

Legal Entity Rationalization

/ Structuring

Tax IT / Securityg

User Defined Applications

Segregation of Duties Payroll Tax Applications Duties

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 15

Income Tax ProcessesIncome Tax Processes

Tax Financial Reporting (Provisioning)Tax Financial Reporting (Provisioning)• Annual/Quarterly Processes• Effective Tax Rate (ETR)• Return to Provision • Tax Basis Balance Sheet• Tax Basis Balance Sheet• ASC 740-10 (FIN 48)• Account Reconciliation• Journal Entries

Income Tax Compliance• Data Collection• Tax Return Preparation

A dit M t• Audit Management• Notice Management• Account Reconciliation• Journal Entries

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 16

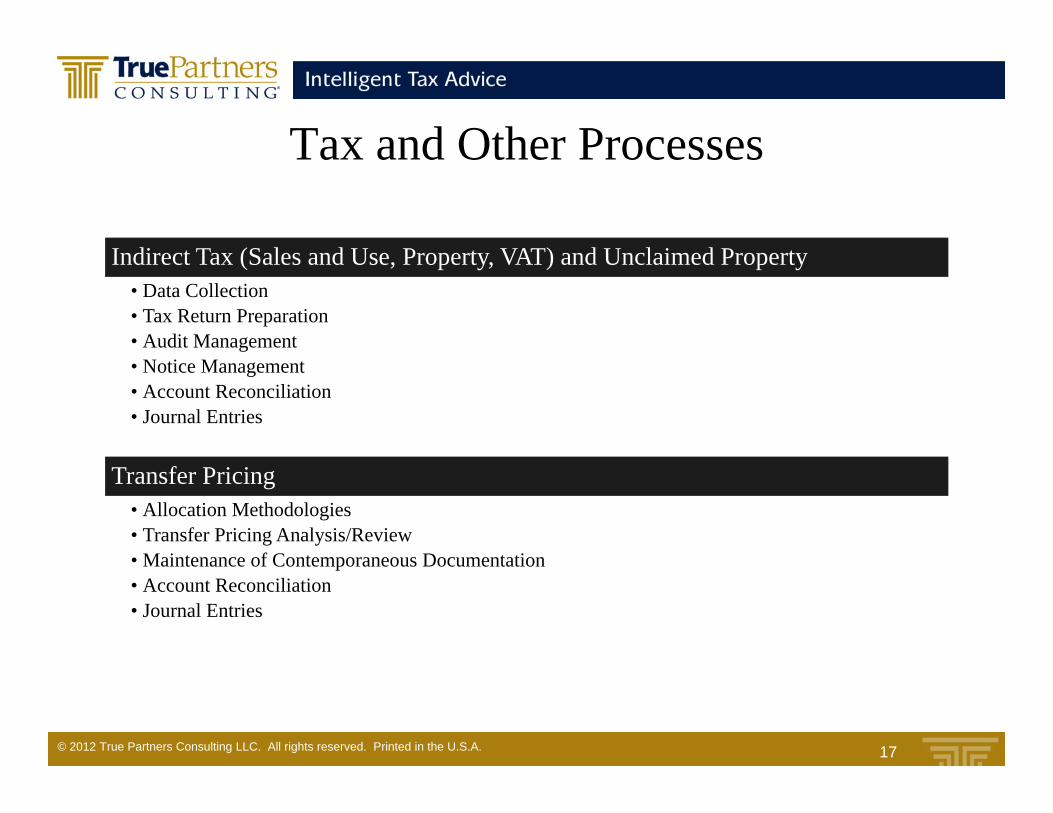

Tax and Other ProcessesTax and Other Processes

I di t T (S l d U P t VAT) d U l i d P tIndirect Tax (Sales and Use, Property, VAT) and Unclaimed Property• Data Collection• Tax Return Preparation• Audit Management• Notice Management• Account Reconciliation• Journal Entries

Transfer Pricing• Allocation Methodologies• Transfer Pricing Analysis/Review• Maintenance of Contemporaneous Documentation• Maintenance of Contemporaneous Documentation• Account Reconciliation• Journal Entries

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 17

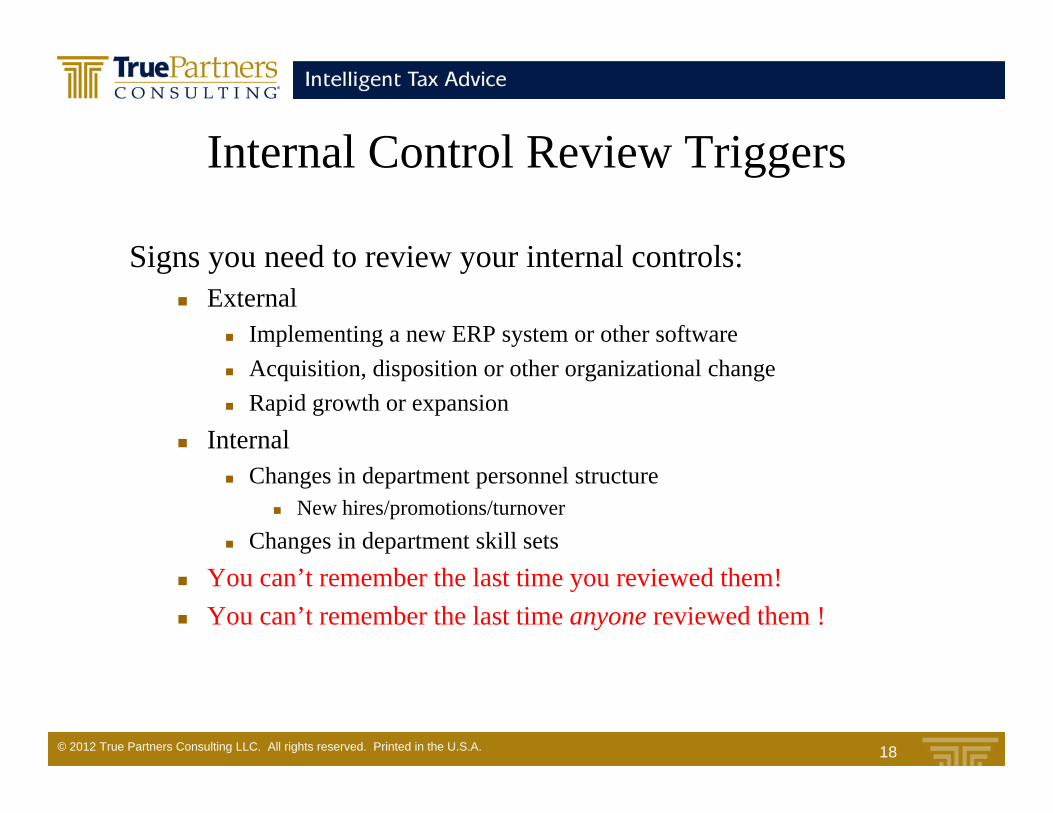

Internal Control Review TriggersInternal Control Review Triggers

Signs you need to review your internal controls:Signs you need to review your internal controls: External

Implementing a new ERP system or other software Acquisition, disposition or other organizational change Rapid growth or expansion

Internal Changes in department personnel structure

New hires/promotions/turnover Changes in department skill sets

You can’t remember the last time you reviewed them! You can’t remember the last time anyone reviewed them !

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 18

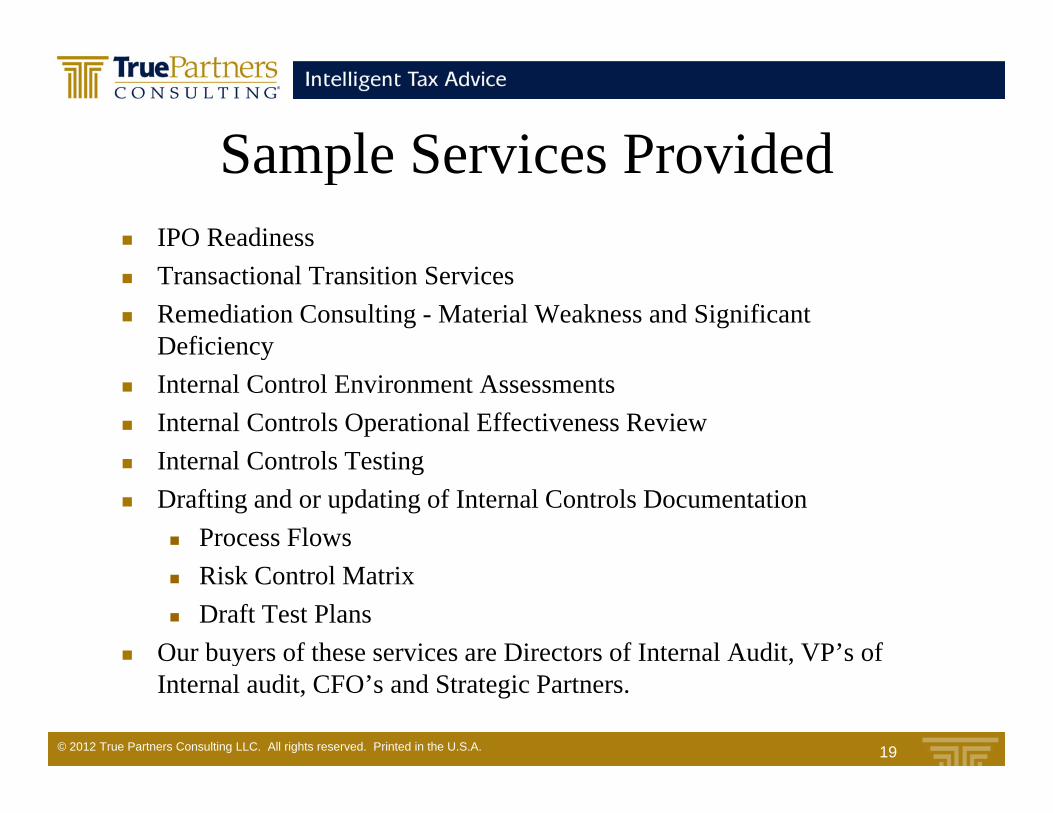

Sample Services ProvidedSample Services Provided IPO Readiness Transactional Transition Services Remediation Consulting - Material Weakness and Significant

Deficiencyy Internal Control Environment Assessments Internal Controls Operational Effectiveness Review

Internal Controls Testing Internal Controls Testing Drafting and or updating of Internal Controls Documentation

Process Flows Risk Control Matrix Draft Test Plans

Our buyers of these services are Directors of Internal Audit, VP’s of

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 19

y ,Internal audit, CFO’s and Strategic Partners.

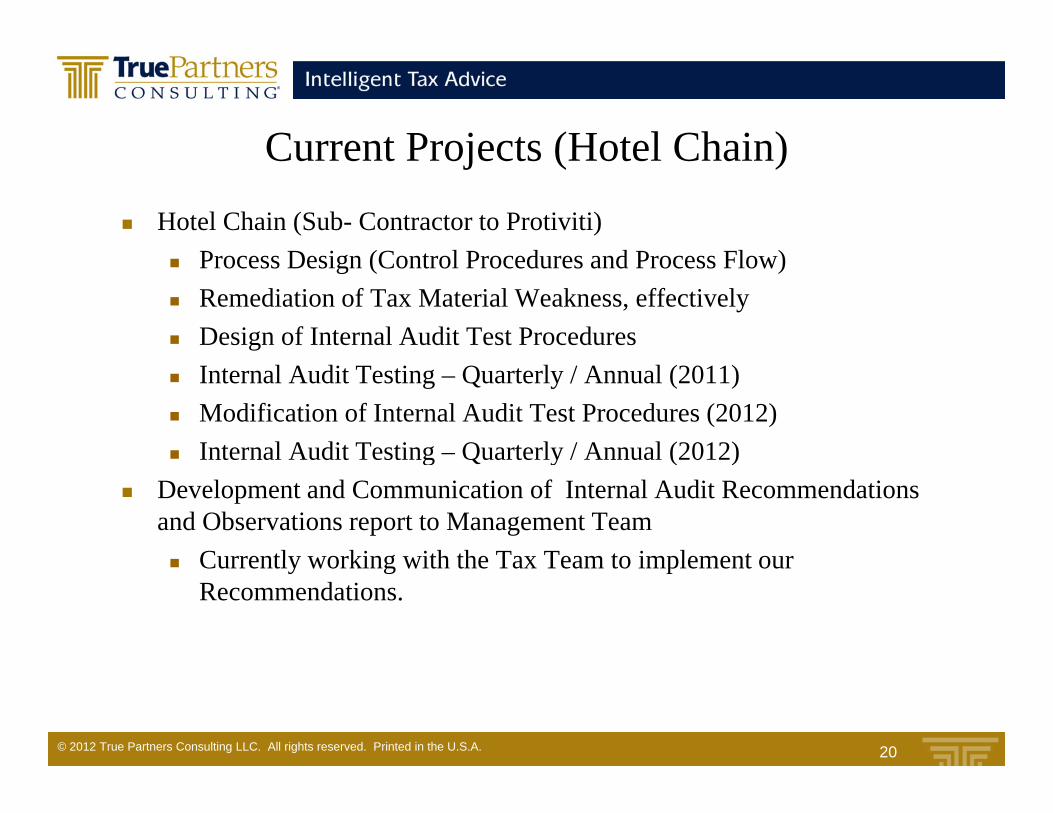

Current Projects (Hotel Chain)Current Projects (Hotel Chain) Hotel Chain (Sub- Contractor to Protiviti)

P D i (C t l P d d P Fl ) Process Design (Control Procedures and Process Flow) Remediation of Tax Material Weakness, effectively Design of Internal Audit Test Procedures Internal Audit Testing – Quarterly / Annual (2011) Modification of Internal Audit Test Procedures (2012) Internal Audit Testing – Quarterly / Annual (2012) Internal Audit Testing Quarterly / Annual (2012)

Development and Communication of Internal Audit Recommendations and Observations report to Management Team Currently working with the Tax Team to implement our Currently working with the Tax Team to implement our

Recommendations.

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 20

Current ProjectsCurrent Projects (Home and Security Products)

Home and Security Products Tax Process Design (Control Procedures and Process Flow)

R I l i f SOX d S i ff Re-Implementation of SOX, due to Spin off Tax Provision Automation, Integrated and an Integral component of

the Tax Control Environment. Integration of Tax Provision and Tax Compliance (OneSource) Member of the Internal Controls Management Team

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 21

C t t I f tiContact Information

John P. BenneckeManaging Director

[email protected] 312 235 3337P 312.235.3337

Jennifer LauJennifer LauSenior Manager

[email protected] 312.588.3410P 312.588.3410

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 22

Q ti ?Questions ?

© 2012 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A. 23