Embed Size (px)

Citation preview

International Air Transport – Outlook, The p ,Alliances , Strategies and the Privatization

of TAPof TAP

July 2011LISLIS

Some fundamentals

The airline business plays a key economic role for any country particularly for trade and tourismany country, particularly for trade and tourism

The airline business is highly competitive and has shown low overall profitability- which has benefited customers

New business models (e.g. regional airlines, low cost airlines) have expanded the business

A new age including global airline business models beckons – but there are many hurdles ahead, and bec o s but t e e a e a y u d es a ead, a doutcomes are debatable

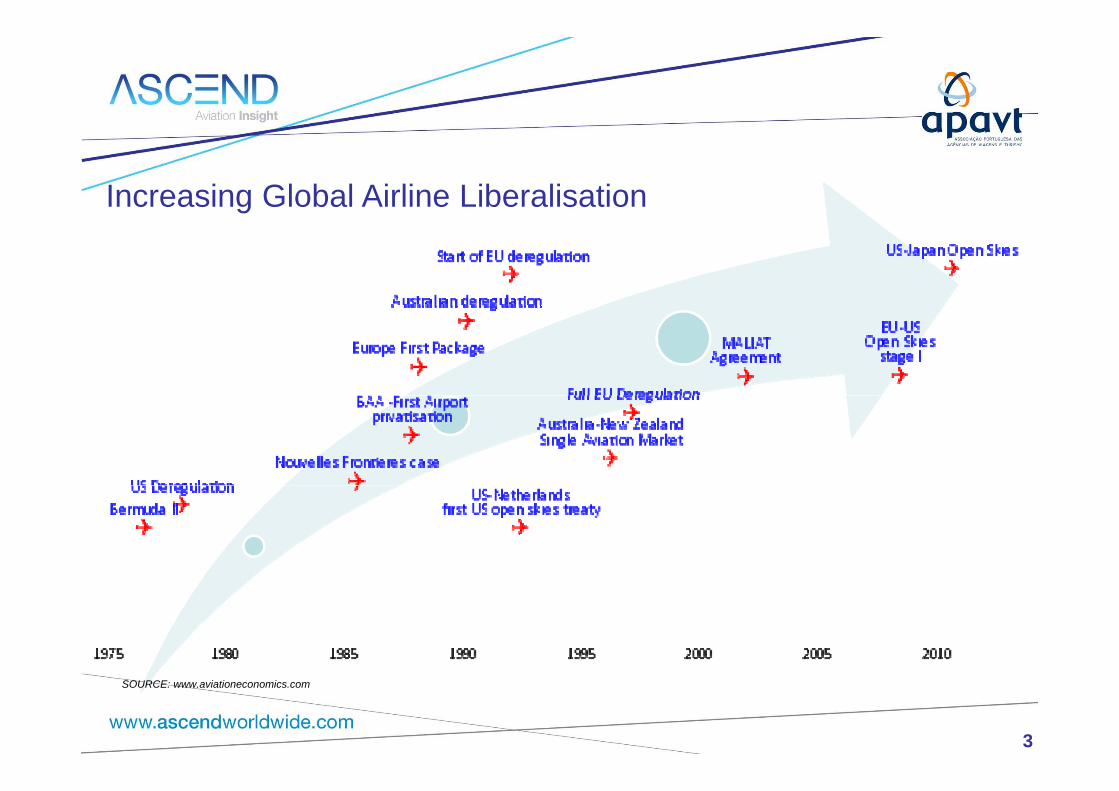

Increasing Global Airline Liberalisation

3

SOURCE: www.aviationeconomics.com

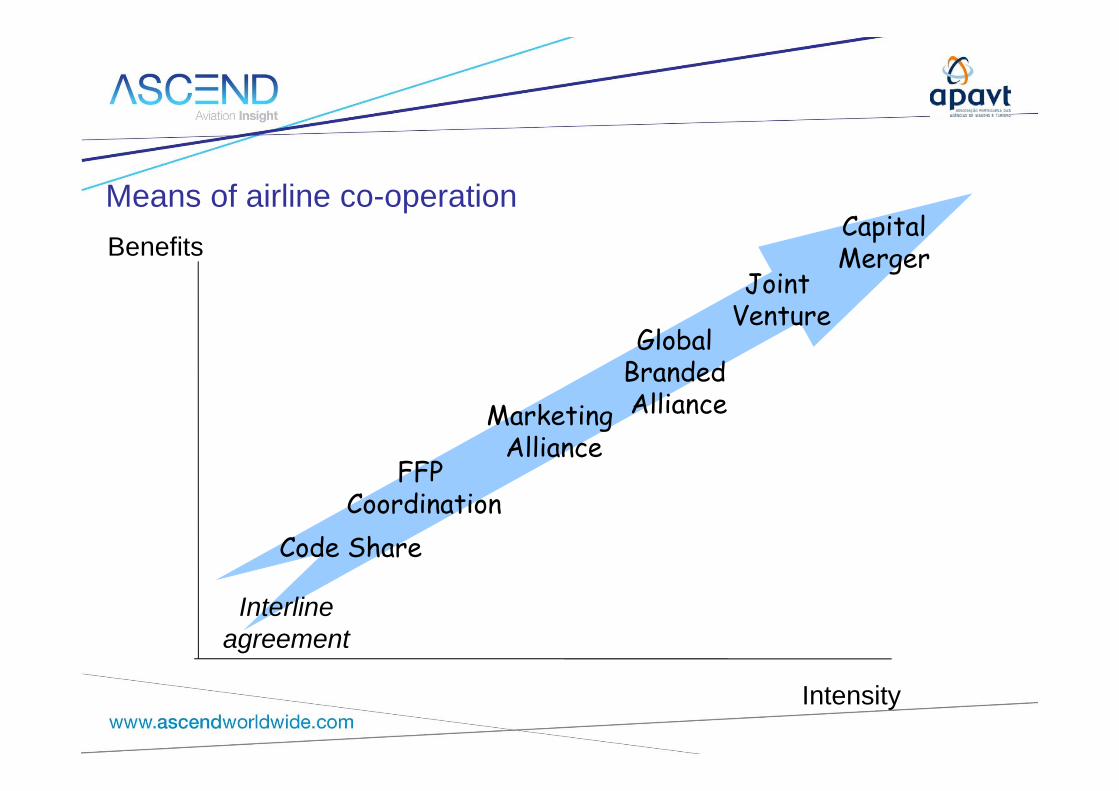

Means of airline co-operationC i l

BenefitsJoint

V

CapitalMerger

Global Branded Alli

Venture

FFP

Marketing Alliance

Alliance

Code ShareCoordination

Interlineagreement

Intensity

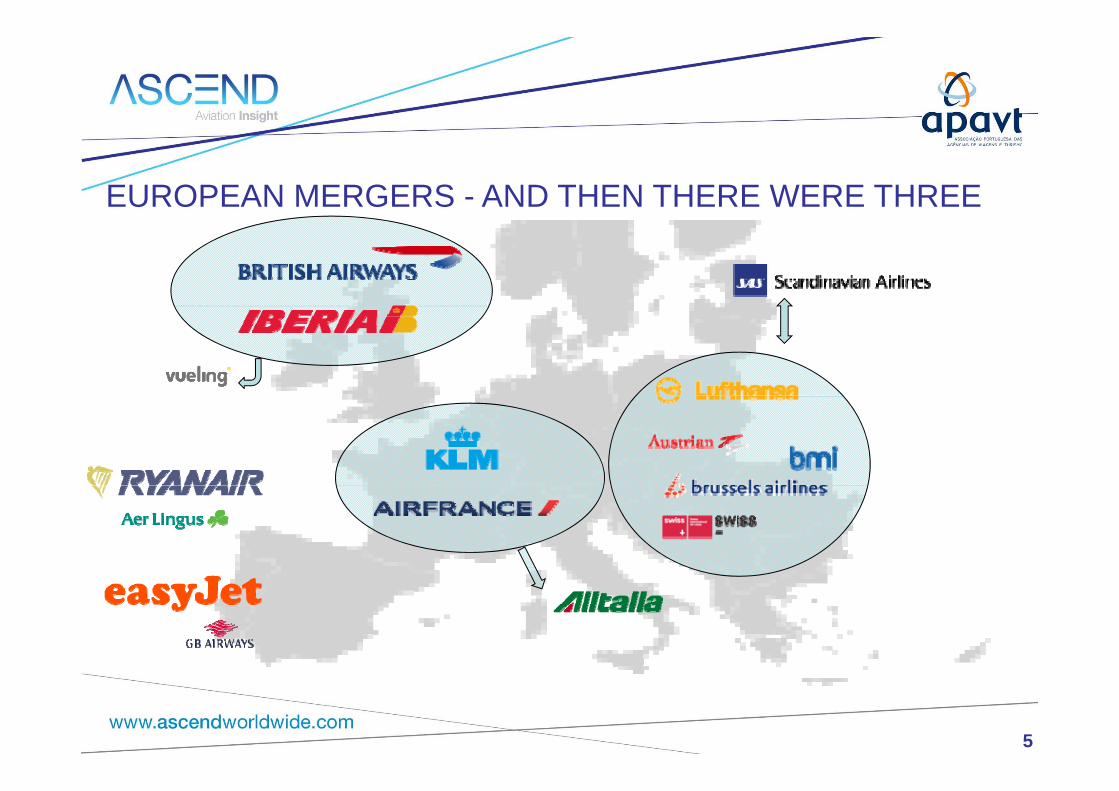

EUROPEAN MERGERS - AND THEN THERE WERE THREE

5

Global Branded Alliances

6

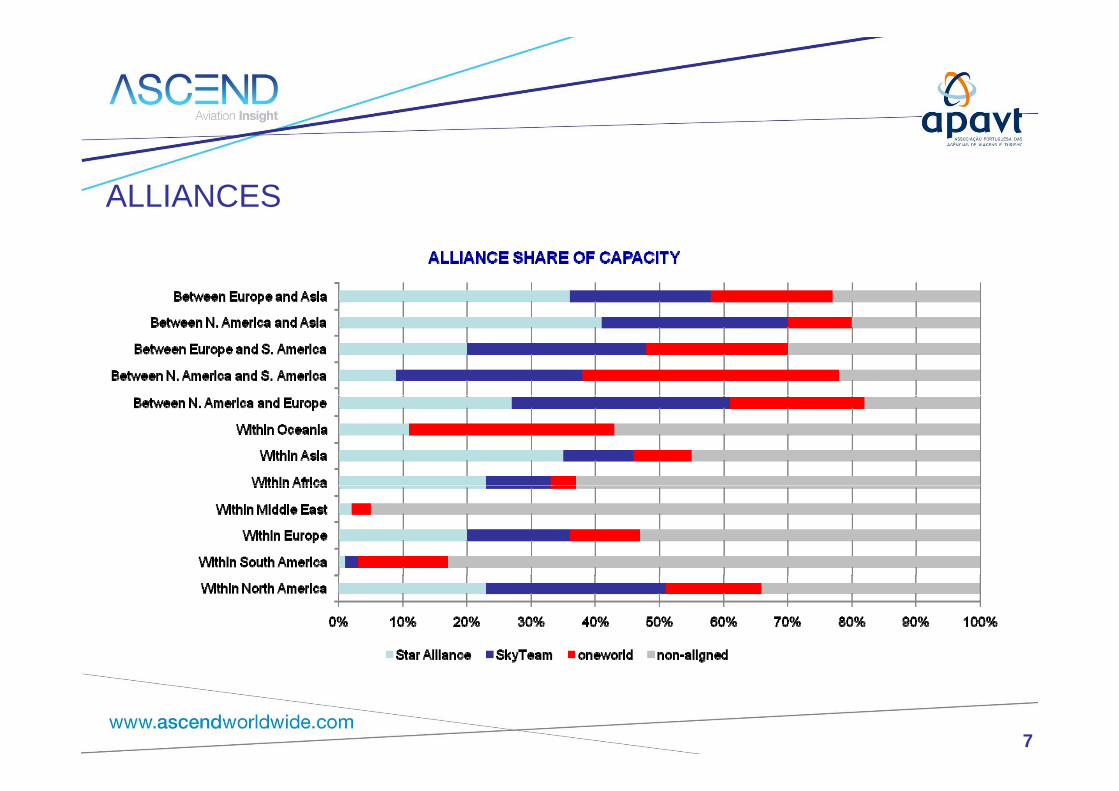

ALLIANCES

7

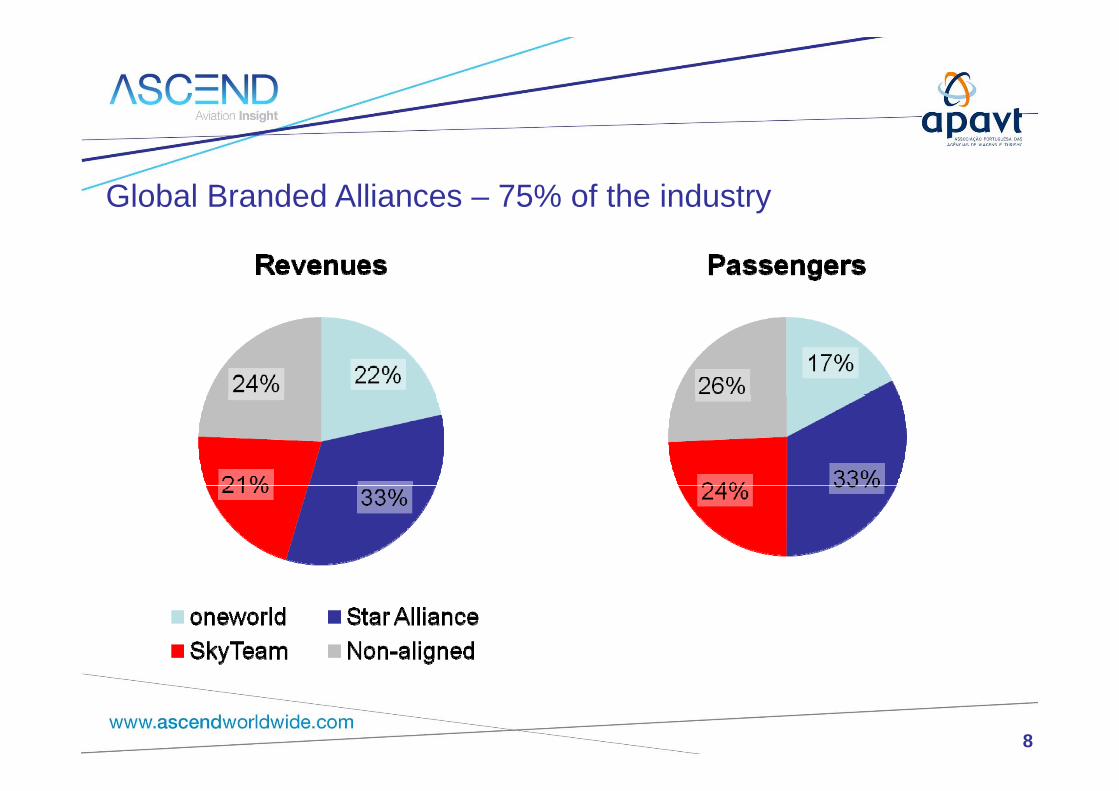

Global Branded Alliances – 75% of the industry

8

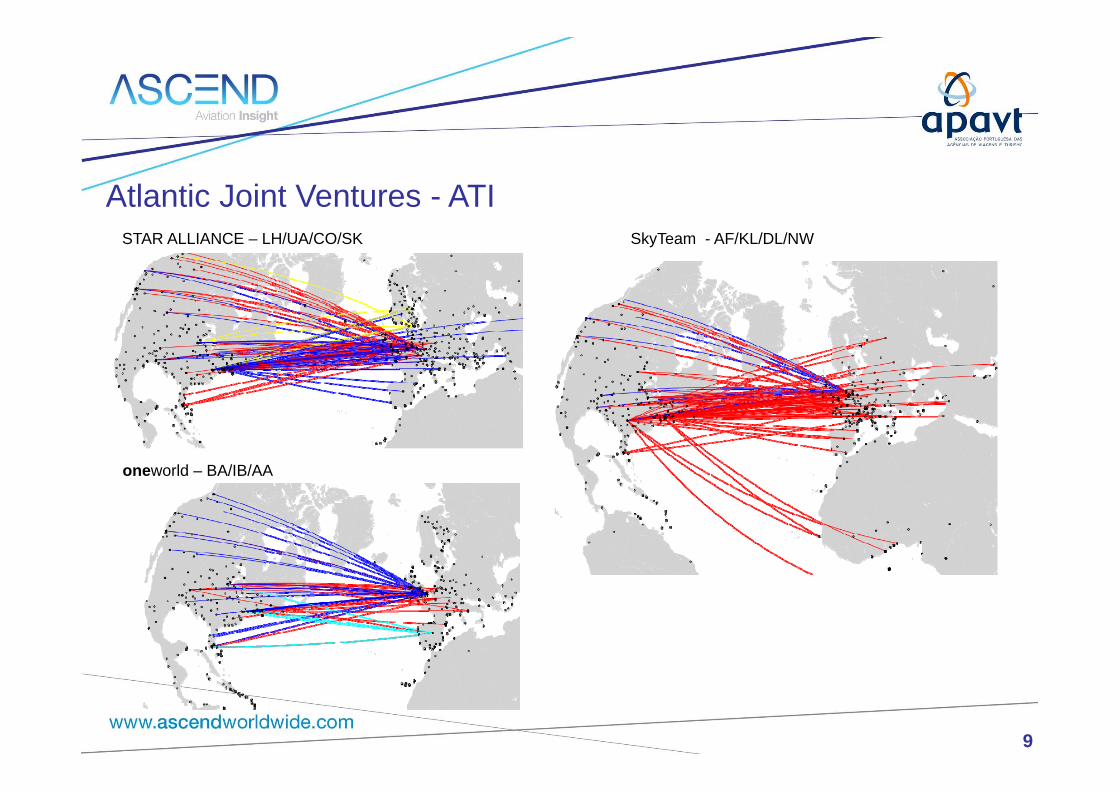

Atlantic Joint Ventures - ATISTAR ALLIANCE – LH/UA/CO/SK SkyTeam - AF/KL/DL/NW

oneworld – BA/IB/AA

9

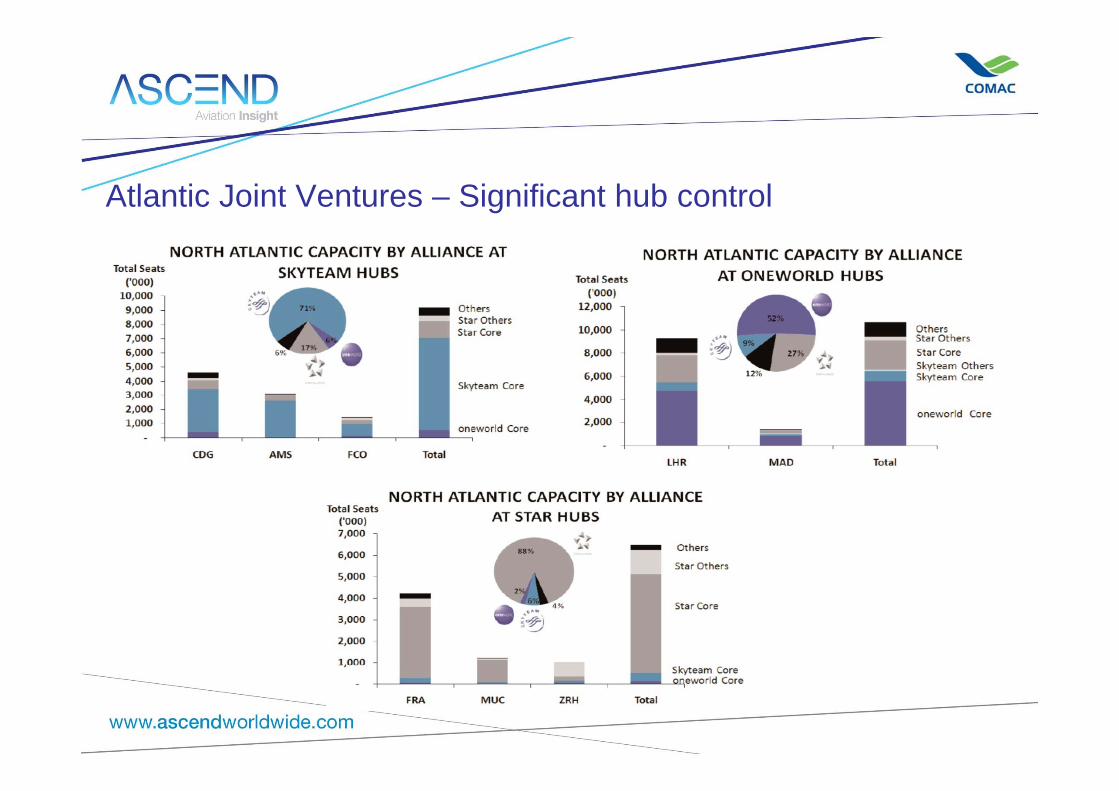

Atlantic Joint Ventures – Significant hub control

Consolidation – next steps

Immunised Joint Ventures (JV’s) on PacificAA-JL and UA-NH started April 2011AA JL and UA NH started April 2011Long standing DL- KE, DL-China? (but no open skies yet)

EU-Far East/Pacific Immunised JVsLong standing AF- KE. Long-standing BA-QFLH-NH proposedAF-China?, BA-JL ?

USA has signed 102 open skies agreements (more than half way there)Chi R i I di t t diChina, Russia, India outstanding

Truly global virtual JV networks?but still nation-based regulation...but still nation-based regulation.

THE EVOLVING LCC MODEL

Original Southwest model Point-to-point, short sector length, high frequency, no frills –p , g , g q y,

attract business away from cars and buses.

European extension (1 – e.g. Ryanair) Single aircraft type, high utilisation, secondary

airport destinations, emphasis on low cost above all, create traffic by fares stimulation. “We fly and the traffic will come”.y y (2 – e.g. easyJet/JetBlue). Single aircraft type, more primary

airports, undercut the legacy carriers to attract the business traveller “We fly to where people want to go but cheaply”traveller. We fly to where people want to go – but cheaply

Asian extension 24 hour operations telephone ticketing for non CC holders24 hour operations, telephone ticketing for non CC holders All developing ancillary revenues

12

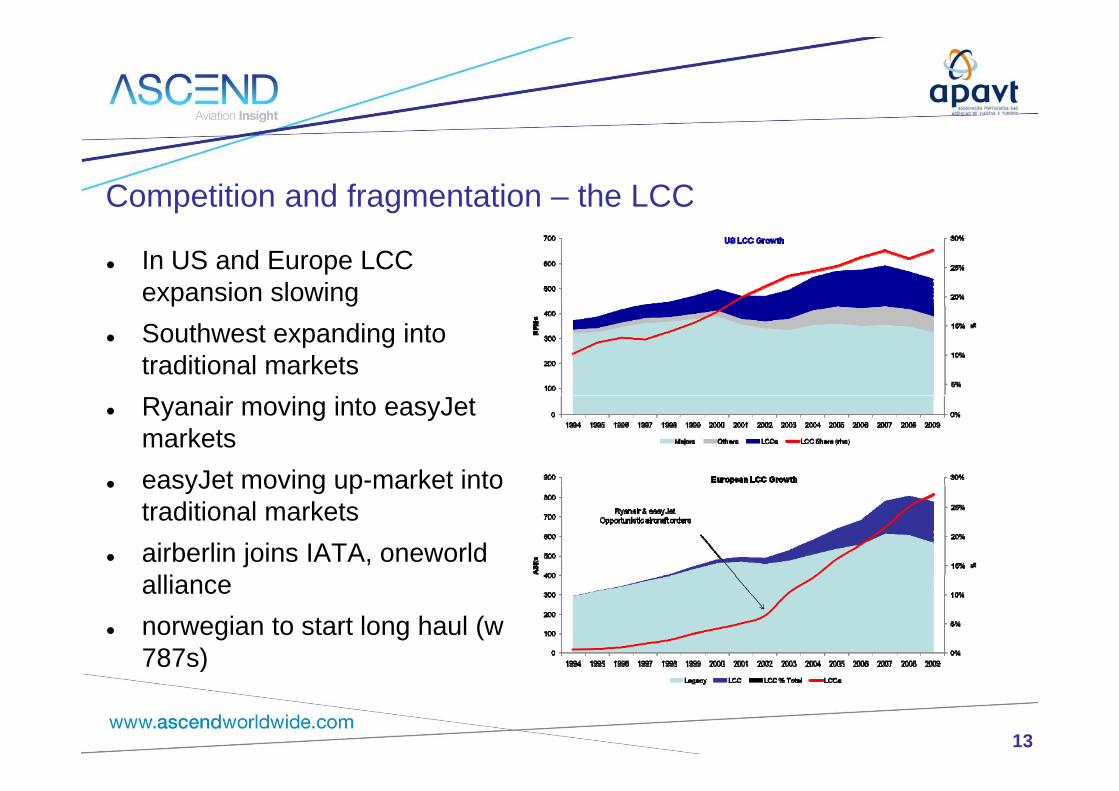

Competition and fragmentation – the LCC

In US and Europe LCC expansion slowing p g

Southwest expanding into traditional markets

Ryanair moving into easyJetmarkets

easyJet moving up-market into easyJet moving up market into traditional markets

airberlin joins IATA, oneworldllialliance

norwegian to start long haul (w 787s)

13

787s)

New competition - super-hubsEmirates

Gulf carriers developing 6th

freedom hubs Attacking established traffic flows

Europe-Far East, Europe-Africa, Kangaroo routeUS ME Af i A i

EtihadQatarUS-ME, Africa, AsiaAsia-Africa

European Airlines not currently an attractive investment

• Stagnant economies• Intense CompetitionIntense Competition• Fuel Price prospects uncertain• Current results weak

Financial results by Airline Region of registration (USDm)

500

-500

0N.

AmericaAsia

PacificEurope Latin

America2010Q12011Q1

-1500

-1000America Pacific America 2011Q1

-2000

Background on TAP markets

Brazil and Africa Markets showBrazil and Africa Markets show high growth potential for 2010-2014 (c.7%+ p.a.)

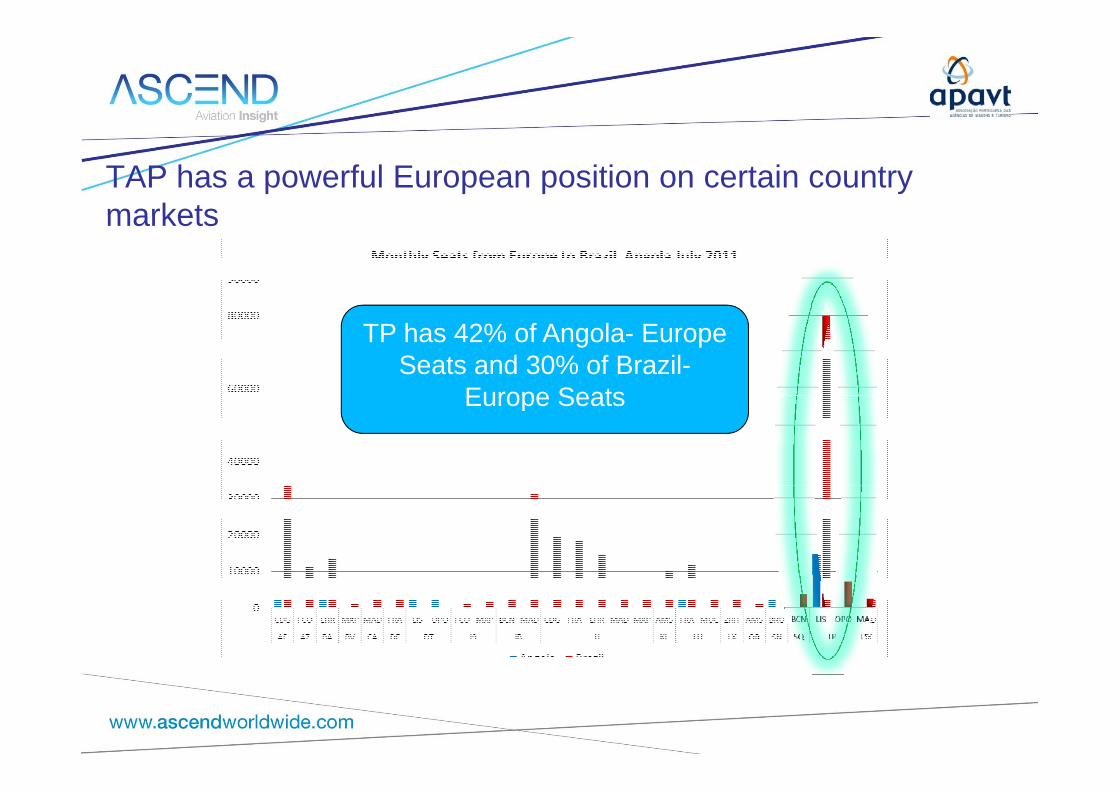

TAP has a powerful European position on certain country marketsmarkets

TP has 42% of Angola- Europe Seats and 30% of Brazil-

Europe SeatsEurope Seats

Outstanding Issues- LAN and TAM Merger?

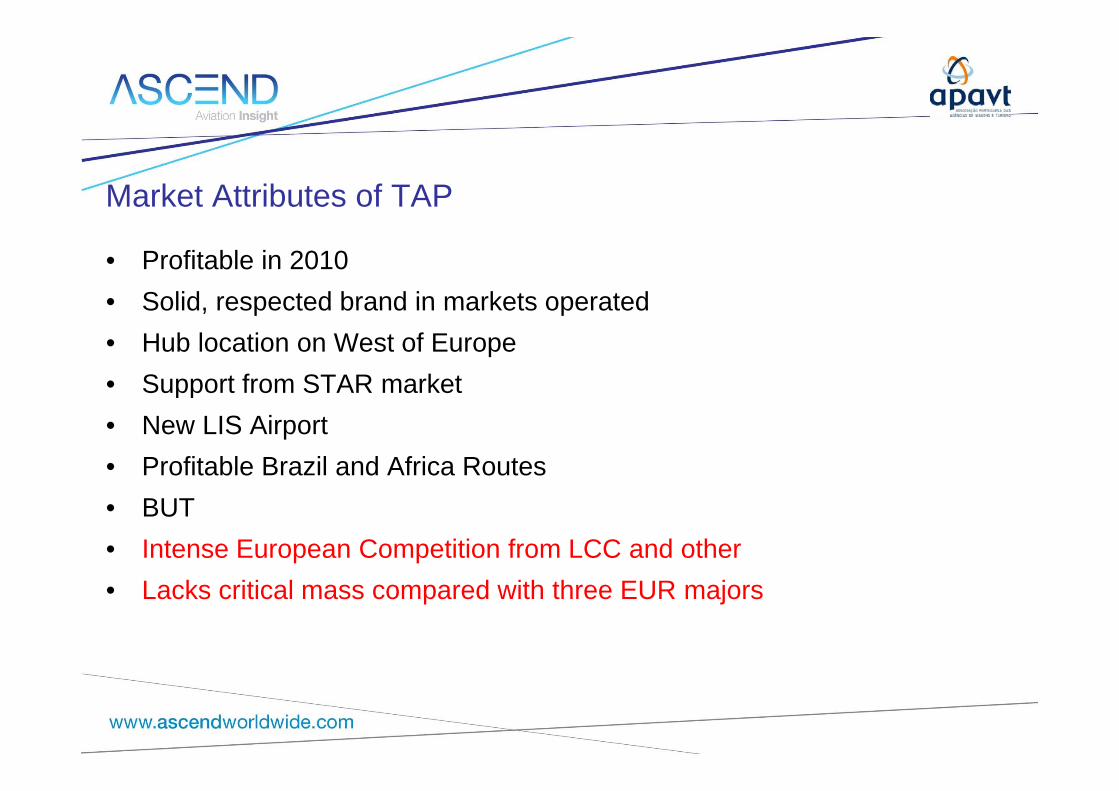

Market Attributes of TAP

• Profitable in 2010• Solid respected brand in markets operatedSolid, respected brand in markets operated• Hub location on West of Europe• Support from STAR marketpp• New LIS Airport• Profitable Brazil and Africa Routes• BUT• Intense European Competition from LCC and other• Lacks critical mass compared with three EUR majors

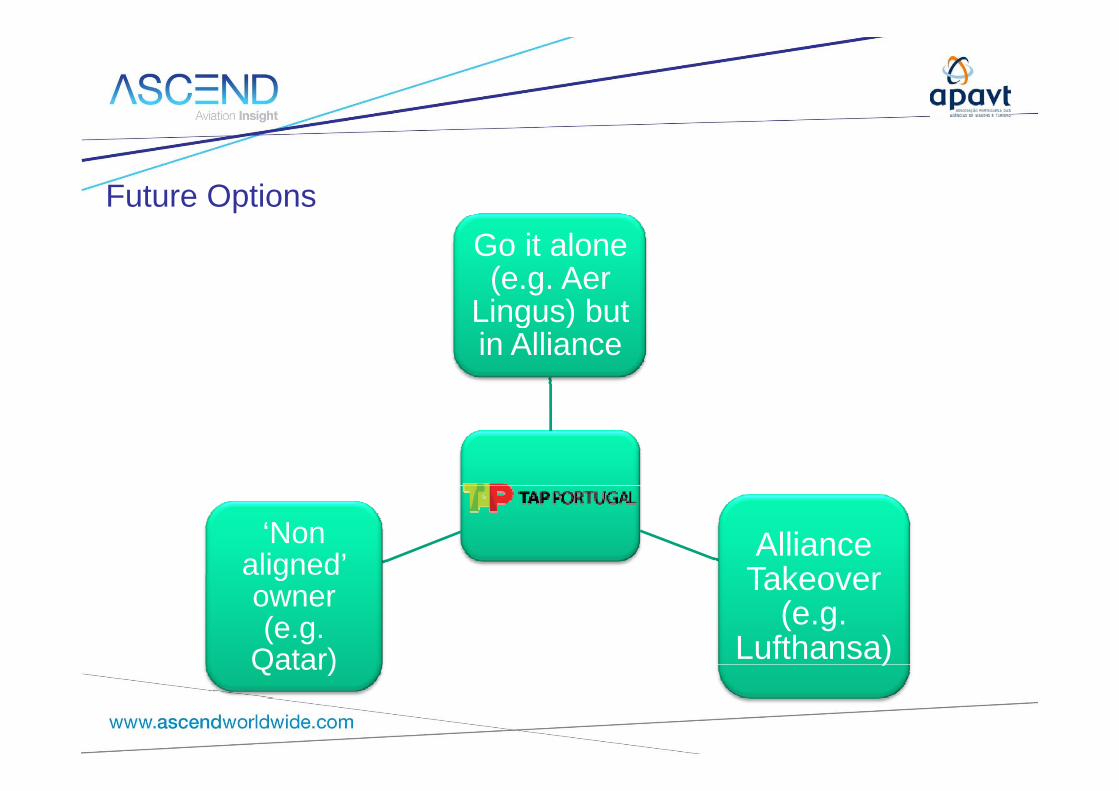

Future OptionsGo it alone (e.g. Aer

Lingus) butLingus) but in Alliance

Alliance Takeover

‘Non aligned’ Takeover

(e.g. Lufthansa)

gowner (e.g.

Qatar) )Qatar)

ASCEND - OFFICES & GLOBAL EXPERIENCE

Hong Kong New YorkLondonHong Kong New YorkLondon

Ascend Asia Ascend USAAscend – Head Office Ascend LondonAscend Asia

35/F Central Plaza,

18 Harbour Road,

Wanchai

Ascend USA441 Lexington Avenue

Suite 702,

New York,

Ascend – Head Office

Cardinal Point,

Newall Road,

Heathrow Airport

Ascend London

10 Fenchurch Avenue,

City of London,

EC3M 7Wanchai

Hong Kong

Tel +852 2813 6366

asia@ascendworldwide com

NY 10017

Tel +1 212 286 1692

Heathrow Airport

London, TW6 2AS

Tel +44 (0)20 8564 6700

uk@ascendworldwide com

EC3M 7

Tel +44 (0)20 8564 6700

uk@ascendworldwide com

21

The information contained in our databases and used in this presentation has been assembled from many sources, and whilst the utmost care has been taken to ensure accuracy, the information is supplied on the understanding that no legal liability whatsoever shall attach to Ascend, its subsidiaries, their officers, or employees in respect of any error or omission that may have occurred.