Embed Size (px)

Citation preview

IFRS

International Financial

Reporting Standards

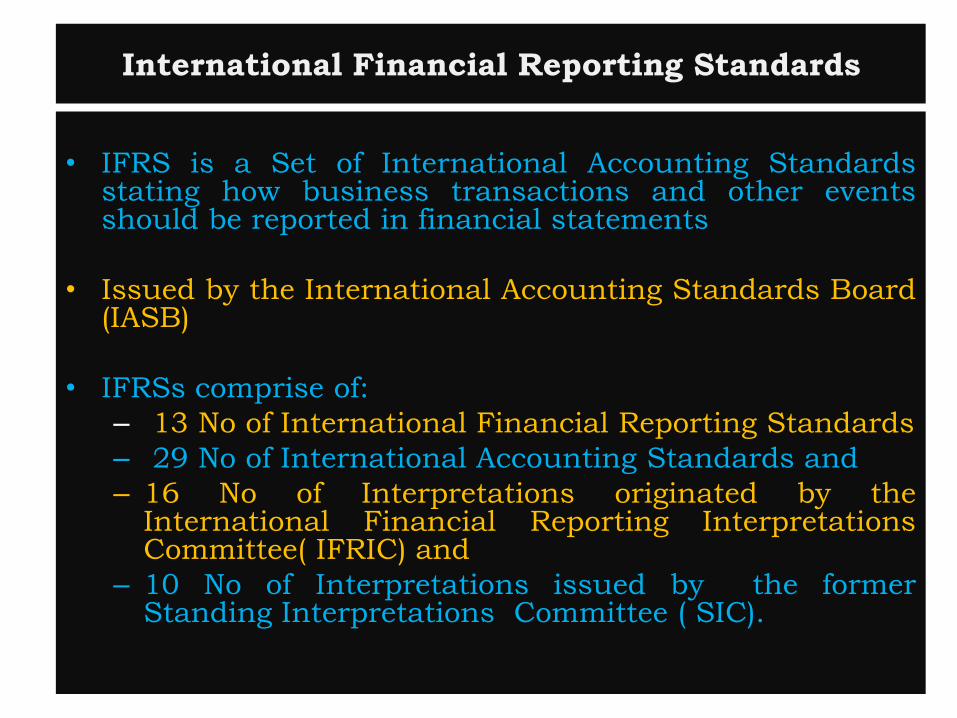

International Financial Reporting Standards

• IFRS is a Set of International Accounting Standards stating how business transactions and other events should be reported in financial statements

• Issued by the International Accounting Standards Board (IASB)

• IFRSs comprise of:

– 13 No of International Financial Reporting Standards

– 29 No of International Accounting Standards and

– 16 No of Interpretations originated by the International Financial Reporting Interpretations Committee( IFRIC) and

– 10 No of Interpretations issued by the former Standing Interpretations Committee ( SIC).

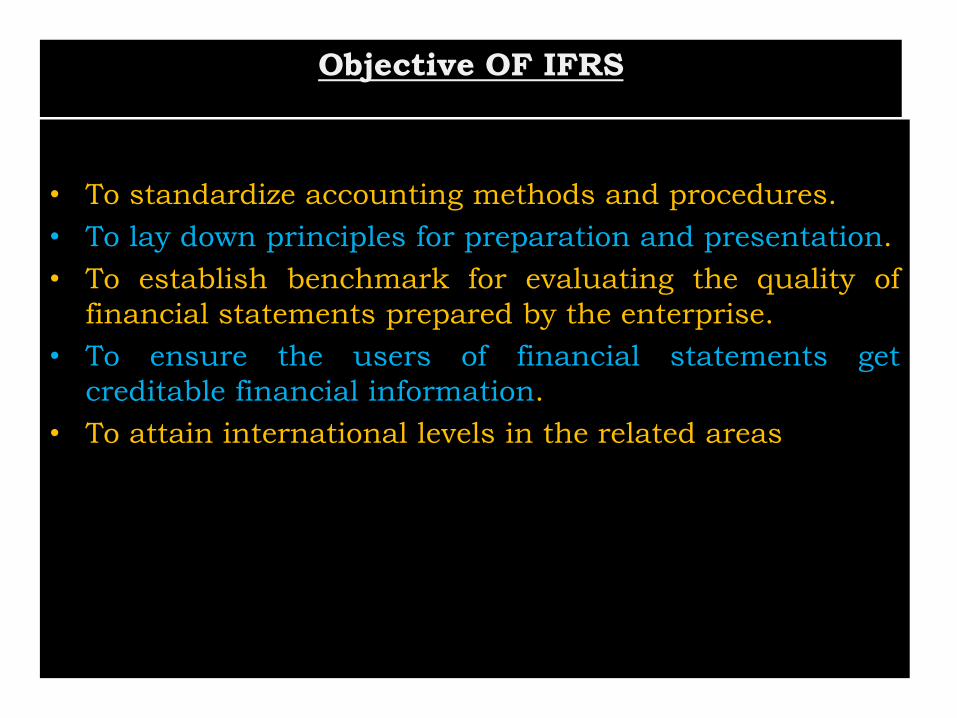

• To standardize accounting methods and procedures.

• To lay down principles for preparation and presentation.

• To establish benchmark for evaluating the quality of

financial statements prepared by the enterprise.

• To ensure the users of financial statements get

creditable financial information.

• To attain international levels in the related areas

Objective OF IFRS

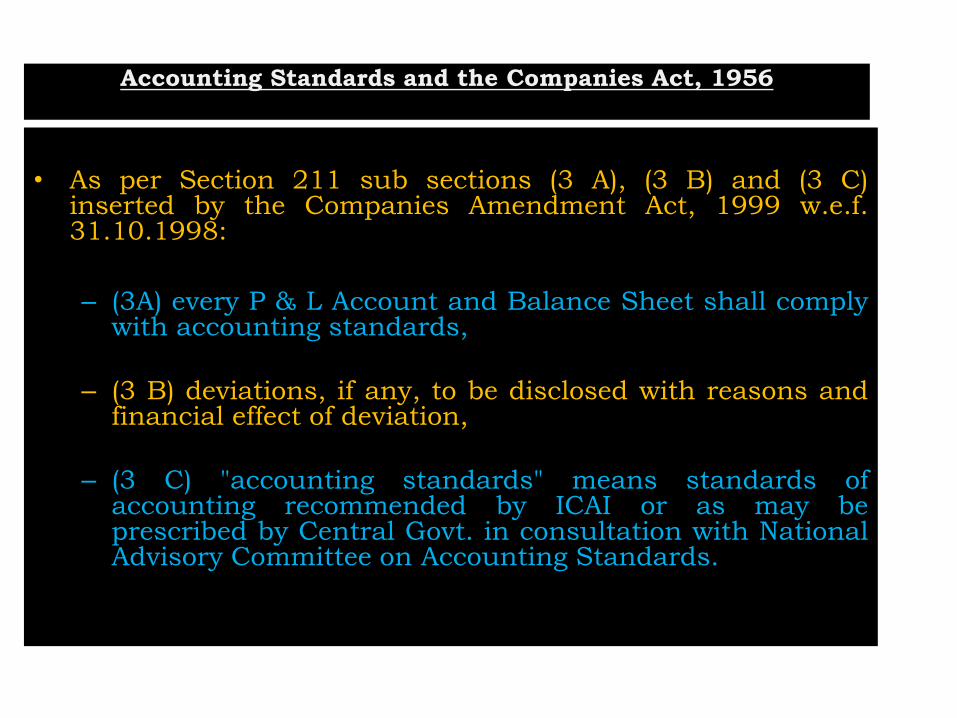

• As per Section 211 sub sections (3 A), (3 B) and (3 C)

inserted by the Companies Amendment Act, 1999 w.e.f. 31.10.1998:

– (3A) every P & L Account and Balance Sheet shall comply

with accounting standards,

– (3 B) deviations, if any, to be disclosed with reasons and financial effect of deviation,

– (3 C) "accounting standards" means standards of accounting recommended by ICAI or as may be prescribed by Central Govt. in consultation with National Advisory Committee on Accounting Standards.

Accounting Standards and the Companies Act, 1956

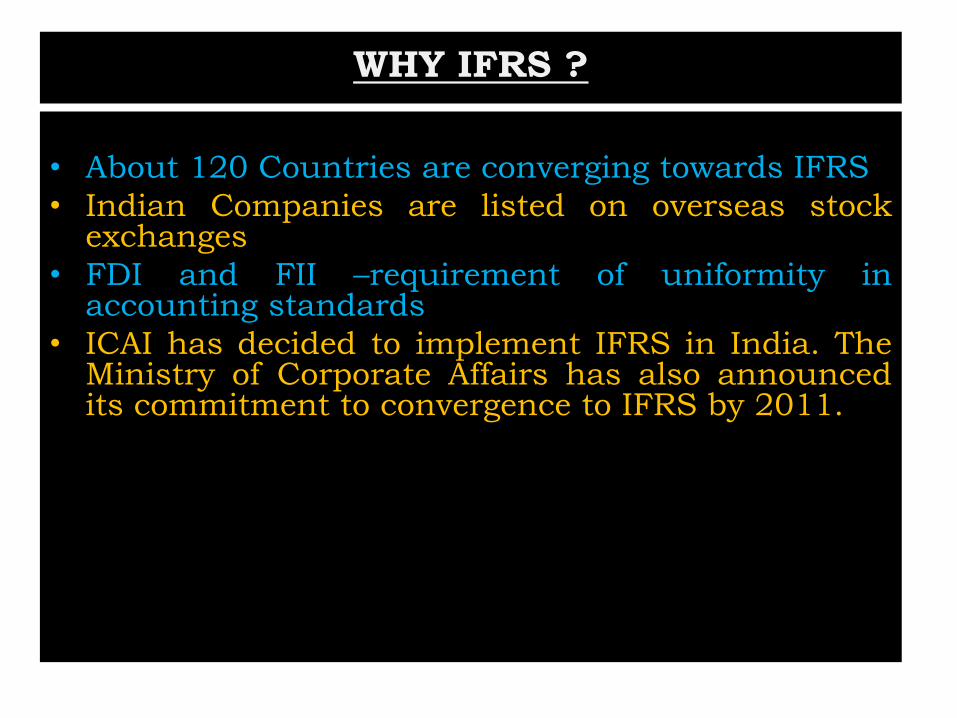

WHY IFRS ?

• About 120 Countries are converging towards IFRS

• Indian Companies are listed on overseas stock exchanges

• FDI and FII –requirement of uniformity in accounting standards

• ICAI has decided to implement IFRS in India. The Ministry of Corporate Affairs has also announced its commitment to convergence to IFRS by 2011.

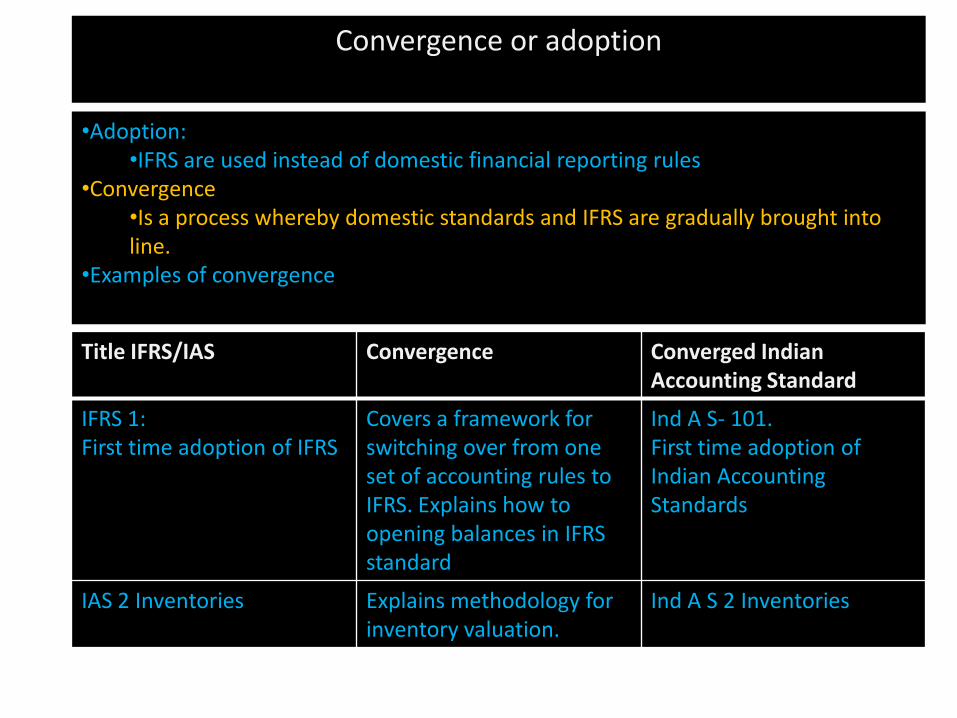

Convergence or adoption

•Adoption: •IFRS are used instead of domestic financial reporting rules

•Convergence •Is a process whereby domestic standards and IFRS are gradually brought into line.

•Examples of convergence

Title IFRS/IAS Convergence Converged Indian Accounting Standard

IFRS 1: First time adoption of IFRS

Covers a framework for switching over from one set of accounting rules to IFRS. Explains how to opening balances in IFRS standard

Ind A S- 101. First time adoption of Indian Accounting Standards

IAS 2 Inventories Explains methodology for inventory valuation.

Ind A S 2 Inventories

Convergence in India

Phase Target date for convergence with IFRS

Phase I

Companies with net worth more than Rs 1000 Cr and companies which are listed

1st April 2011

Phase II Companies having networth between Rs

500 Cr to Rs 1000 Cr

1st April 2013

Phase III Companies having net worth less than Rs

500 Cr

1st April 2014

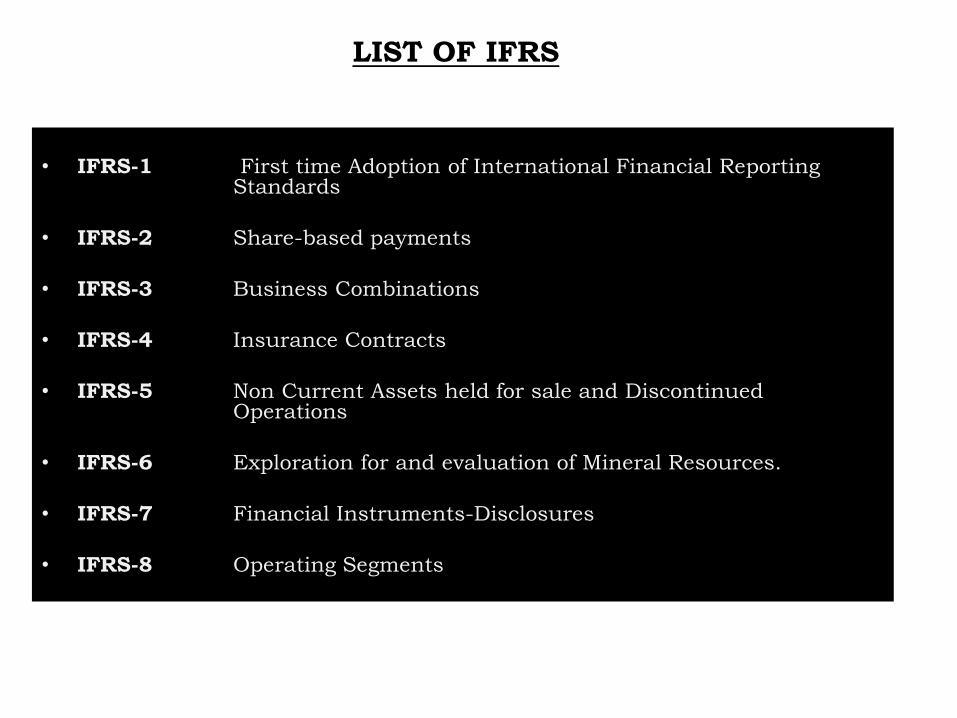

LIST OF IFRS

• IFRS-1 First time Adoption of International Financial Reporting Standards

• IFRS-2 Share-based payments

• IFRS-3 Business Combinations

• IFRS-4 Insurance Contracts

• IFRS-5 Non Current Assets held for sale and Discontinued Operations

• IFRS-6 Exploration for and evaluation of Mineral Resources.

• IFRS-7 Financial Instruments-Disclosures

• IFRS-8 Operating Segments

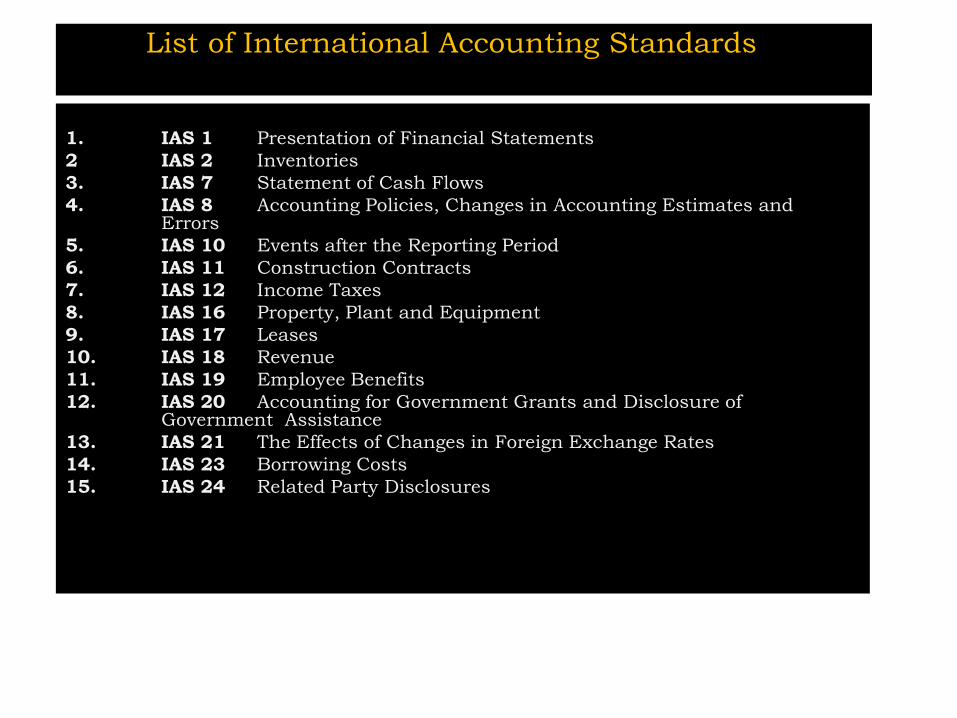

List of International Accounting Standards

1. IAS 1 Presentation of Financial Statements

2 IAS 2 Inventories

3. IAS 7 Statement of Cash Flows

4. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

5. IAS 10 Events after the Reporting Period

6. IAS 11 Construction Contracts

7. IAS 12 Income Taxes

8. IAS 16 Property, Plant and Equipment

9. IAS 17 Leases

10. IAS 18 Revenue

11. IAS 19 Employee Benefits

12. IAS 20 Accounting for Government Grants and Disclosure of Government Assistance

13. IAS 21 The Effects of Changes in Foreign Exchange Rates

14. IAS 23 Borrowing Costs

15. IAS 24 Related Party Disclosures

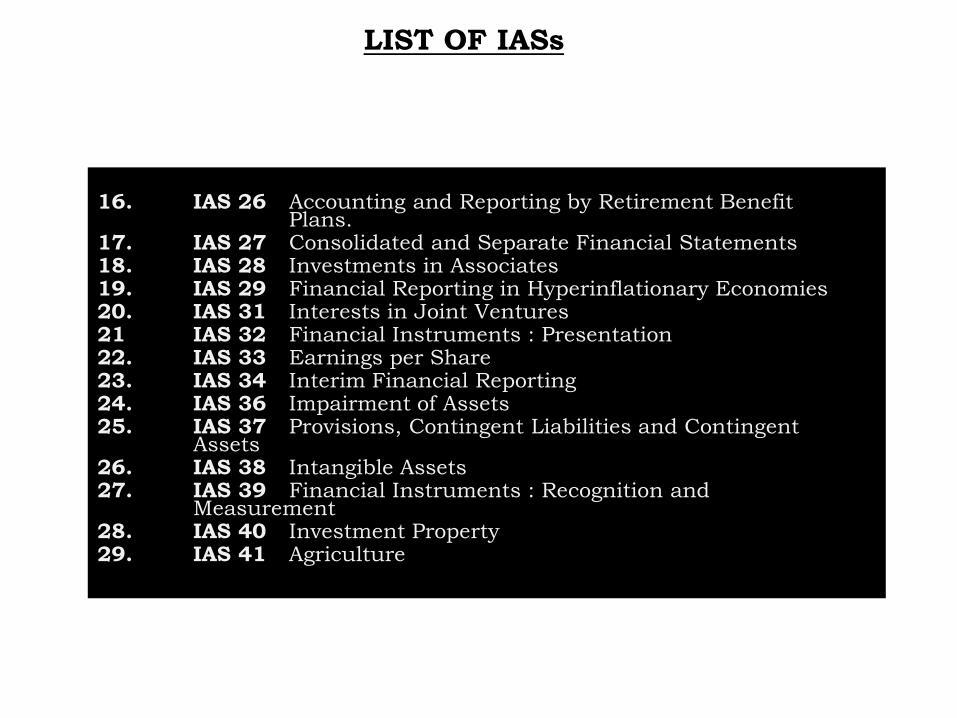

LIST OF IASs

16. IAS 26 Accounting and Reporting by Retirement Benefit

Plans. 17. IAS 27 Consolidated and Separate Financial Statements 18. IAS 28 Investments in Associates 19. IAS 29 Financial Reporting in Hyperinflationary Economies 20. IAS 31 Interests in Joint Ventures 21 IAS 32 Financial Instruments : Presentation 22. IAS 33 Earnings per Share 23. IAS 34 Interim Financial Reporting 24. IAS 36 Impairment of Assets 25. IAS 37 Provisions, Contingent Liabilities and Contingent

Assets 26. IAS 38 Intangible Assets 27. IAS 39 Financial Instruments : Recognition and

Measurement 28. IAS 40 Investment Property 29. IAS 41 Agriculture

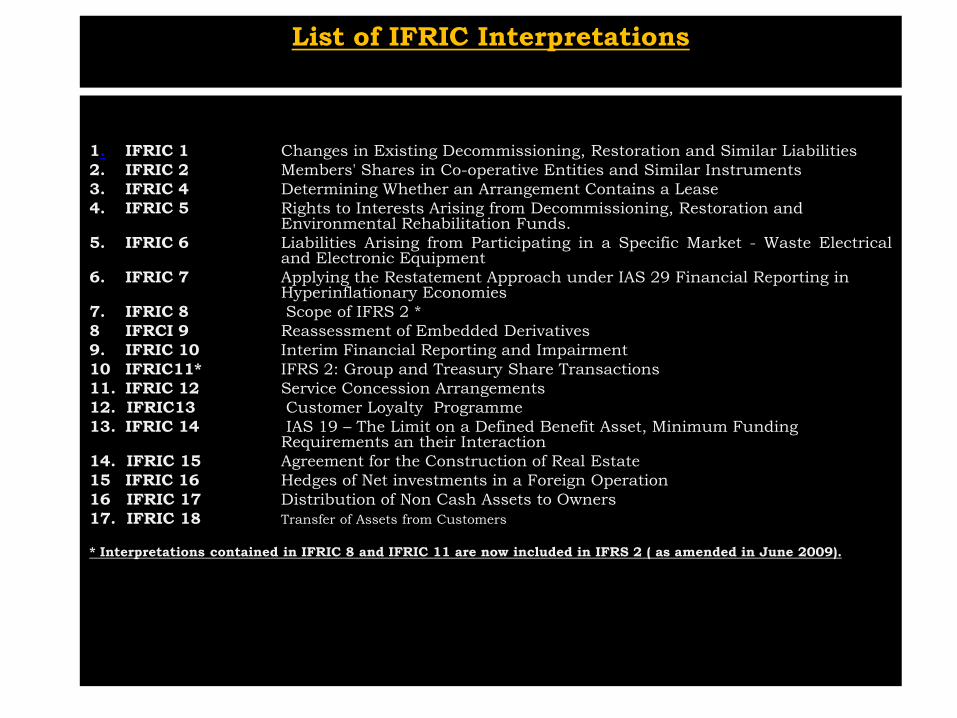

List of IFRIC Interpretations

1. IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

2. IFRIC 2 Members' Shares in Co-operative Entities and Similar Instruments

3. IFRIC 4 Determining Whether an Arrangement Contains a Lease

4. IFRIC 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Rehabilitation Funds.

5. IFRIC 6 Liabilities Arising from Participating in a Specific Market - Waste Electrical and Electronic Equipment

6. IFRIC 7 Applying the Restatement Approach under IAS 29 Financial Reporting in Hyperinflationary Economies

7. IFRIC 8 Scope of IFRS 2 *

8 IFRCI 9 Reassessment of Embedded Derivatives

9. IFRIC 10 Interim Financial Reporting and Impairment

10 IFRIC11* IFRS 2: Group and Treasury Share Transactions

11. IFRIC 12 Service Concession Arrangements

12. IFRIC13 Customer Loyalty Programme

13. IFRIC 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements an their Interaction

14. IFRIC 15 Agreement for the Construction of Real Estate

15 IFRIC 16 Hedges of Net investments in a Foreign Operation

16 IFRIC 17 Distribution of Non Cash Assets to Owners

17. IFRIC 18 Transfer of Assets from Customers

* Interpretations contained in IFRIC 8 and IFRIC 11 are now included in IFRS 2 ( as amended in June 2009).

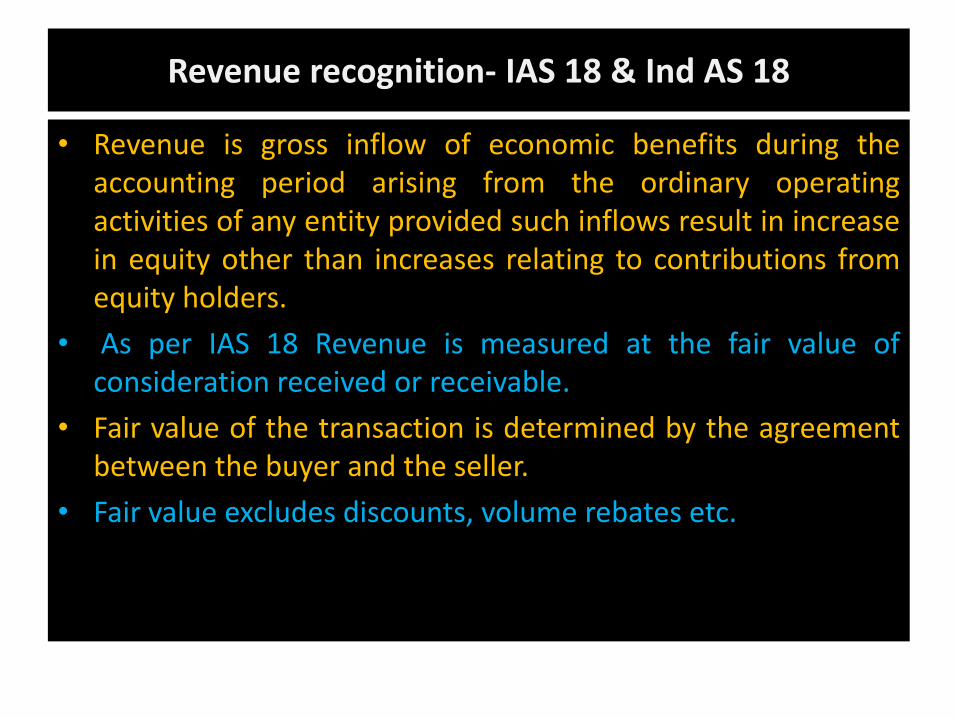

Revenue recognition- IAS 18 & Ind AS 18

• Revenue is gross inflow of economic benefits during the accounting period arising from the ordinary operating activities of any entity provided such inflows result in increase in equity other than increases relating to contributions from equity holders.

• As per IAS 18 Revenue is measured at the fair value of consideration received or receivable.

• Fair value of the transaction is determined by the agreement between the buyer and the seller.

• Fair value excludes discounts, volume rebates etc.

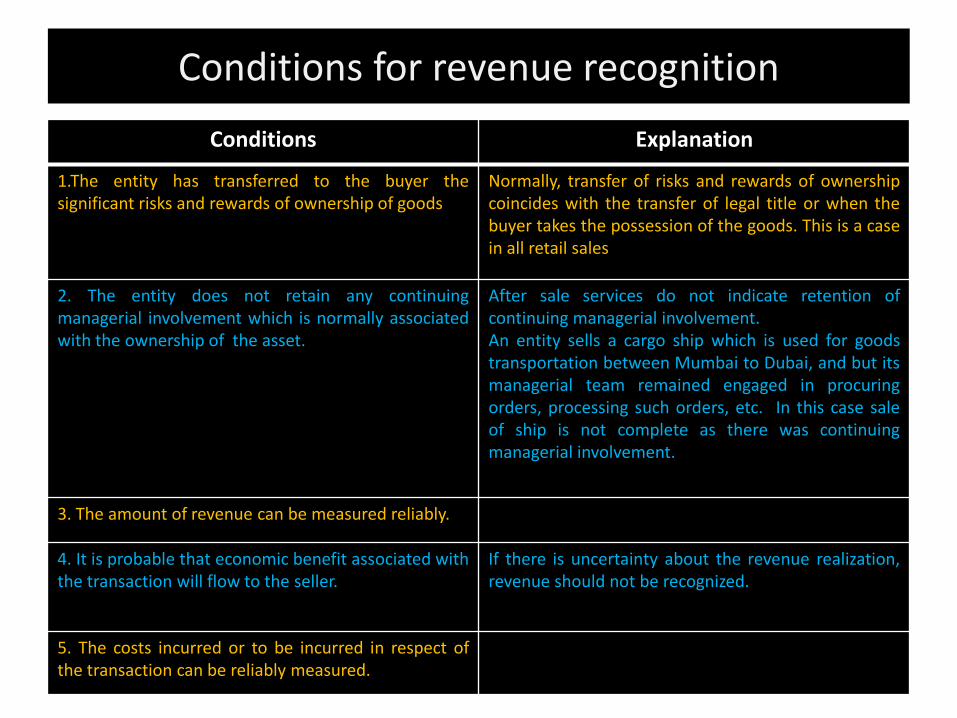

Conditions for revenue recognition

Conditions Explanation

1.The entity has transferred to the buyer the significant risks and rewards of ownership of goods

Normally, transfer of risks and rewards of ownership coincides with the transfer of legal title or when the buyer takes the possession of the goods. This is a case in all retail sales

2. The entity does not retain any continuing managerial involvement which is normally associated with the ownership of the asset.

After sale services do not indicate retention of continuing managerial involvement. An entity sells a cargo ship which is used for goods transportation between Mumbai to Dubai, and but its managerial team remained engaged in procuring orders, processing such orders, etc. In this case sale of ship is not complete as there was continuing managerial involvement.

3. The amount of revenue can be measured reliably.

4. It is probable that economic benefit associated with the transaction will flow to the seller.

If there is uncertainty about the revenue realization, revenue should not be recognized.

5. The costs incurred or to be incurred in respect of the transaction can be reliably measured.

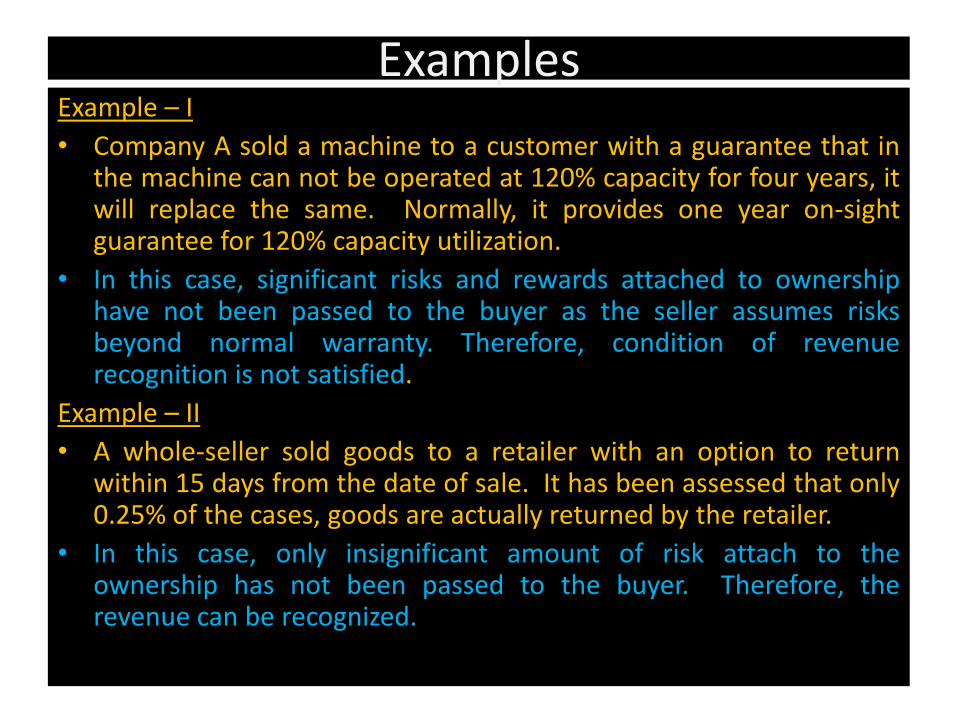

Examples Example – I

• Company A sold a machine to a customer with a guarantee that in the machine can not be operated at 120% capacity for four years, it will replace the same. Normally, it provides one year on-sight guarantee for 120% capacity utilization.

• In this case, significant risks and rewards attached to ownership have not been passed to the buyer as the seller assumes risks beyond normal warranty. Therefore, condition of revenue recognition is not satisfied.

Example – II

• A whole-seller sold goods to a retailer with an option to return within 15 days from the date of sale. It has been assessed that only 0.25% of the cases, goods are actually returned by the retailer.

• In this case, only insignificant amount of risk attach to the ownership has not been passed to the buyer. Therefore, the revenue can be recognized.

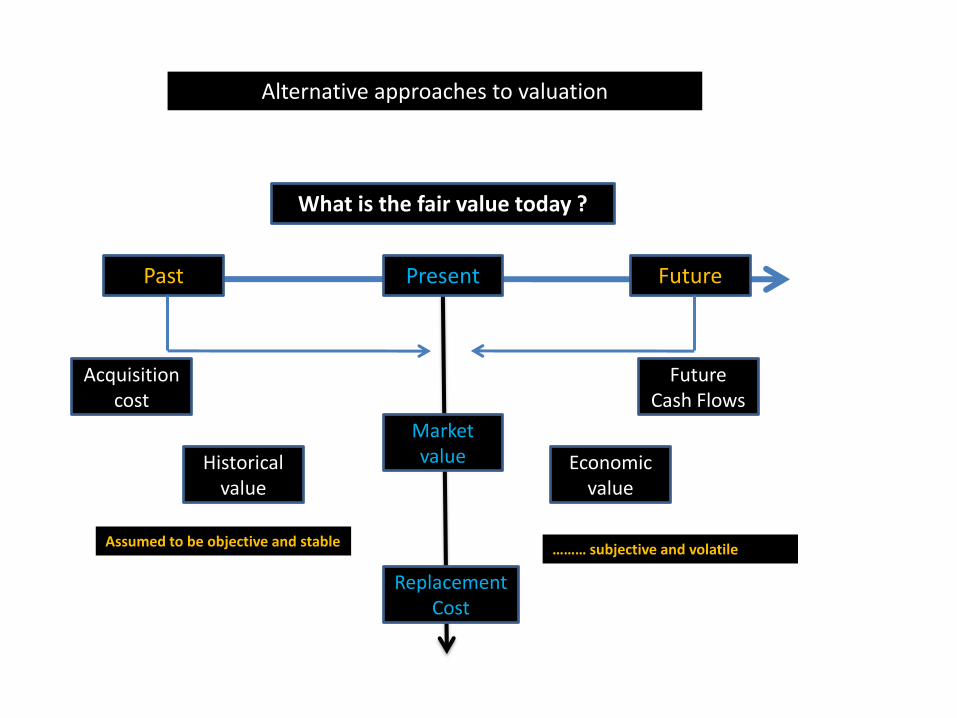

Past Future Present

What is the fair value today ?

Acquisition cost

Historical value

Future Cash Flows

Economic value

Market value

Assumed to be objective and stable ……… subjective and volatile

Replacement Cost

Alternative approaches to valuation

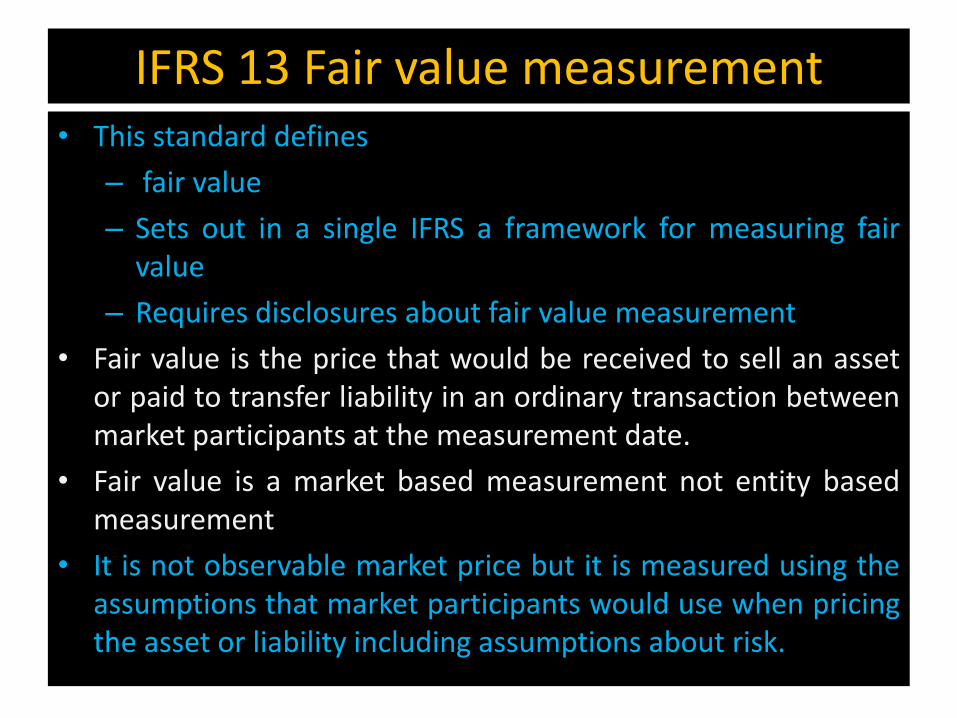

IFRS 13 Fair value measurement • This standard defines

– fair value

– Sets out in a single IFRS a framework for measuring fair value

– Requires disclosures about fair value measurement

• Fair value is the price that would be received to sell an asset or paid to transfer liability in an ordinary transaction between market participants at the measurement date.

• Fair value is a market based measurement not entity based measurement

• It is not observable market price but it is measured using the assumptions that market participants would use when pricing the asset or liability including assumptions about risk.

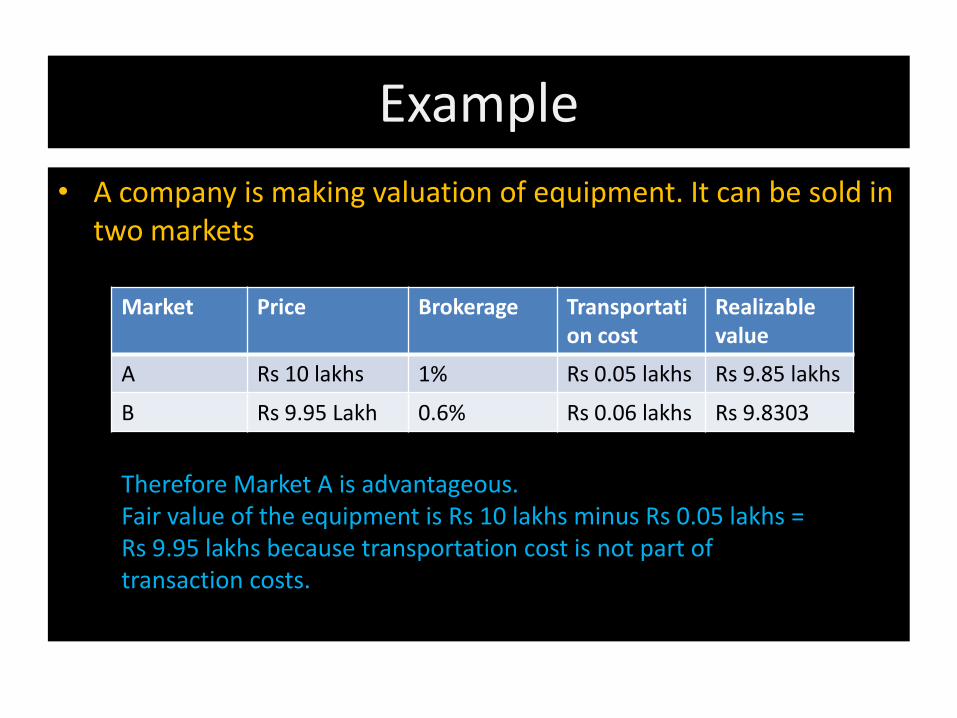

Example

• A company is making valuation of equipment. It can be sold in two markets

Market Price Brokerage Transportati

on cost Realizable value

A Rs 10 lakhs 1% Rs 0.05 lakhs Rs 9.85 lakhs

B Rs 9.95 Lakh 0.6% Rs 0.06 lakhs Rs 9.8303

Therefore Market A is advantageous. Fair value of the equipment is Rs 10 lakhs minus Rs 0.05 lakhs = Rs 9.95 lakhs because transportation cost is not part of transaction costs.

Thank you