Embed Size (px)

Citation preview

International Real Estate International Real Estate Portfolio StrategiesPortfolio Strategies

By Norm Miller, Director of the Real Estate Center at the UniverBy Norm Miller, Director of the Real Estate Center at the University of Cincinnati, sity of Cincinnati, Visitor at DePaul through June 2004 Visitor at DePaul through June 2004

[email protected]@sbcglobal.net

January 26January 26thth, 2004, 2004

PRRES 10PRRES 10thth ConferenceConferenceSponsored by Sponsored by

ThammasatThammasat University (Thank you Professor University (Thank you Professor NiputhNiputh JitprasonkJitprasonk))and theand the

ValuersValuers Association of Thailand (Thank you Director Association of Thailand (Thank you Director SoponSopon PornchokchaiPornchokchai))And Dr. And Dr. NarisNaris CaiyasootCaiyasoot, Rector of , Rector of ThammasatThammasat UniversityUniversity

Thank you for this invitation!! Thank you for this invitation!! ขอบคุณขอบคุณครับครับI am honored to participate.I am honored to participate.

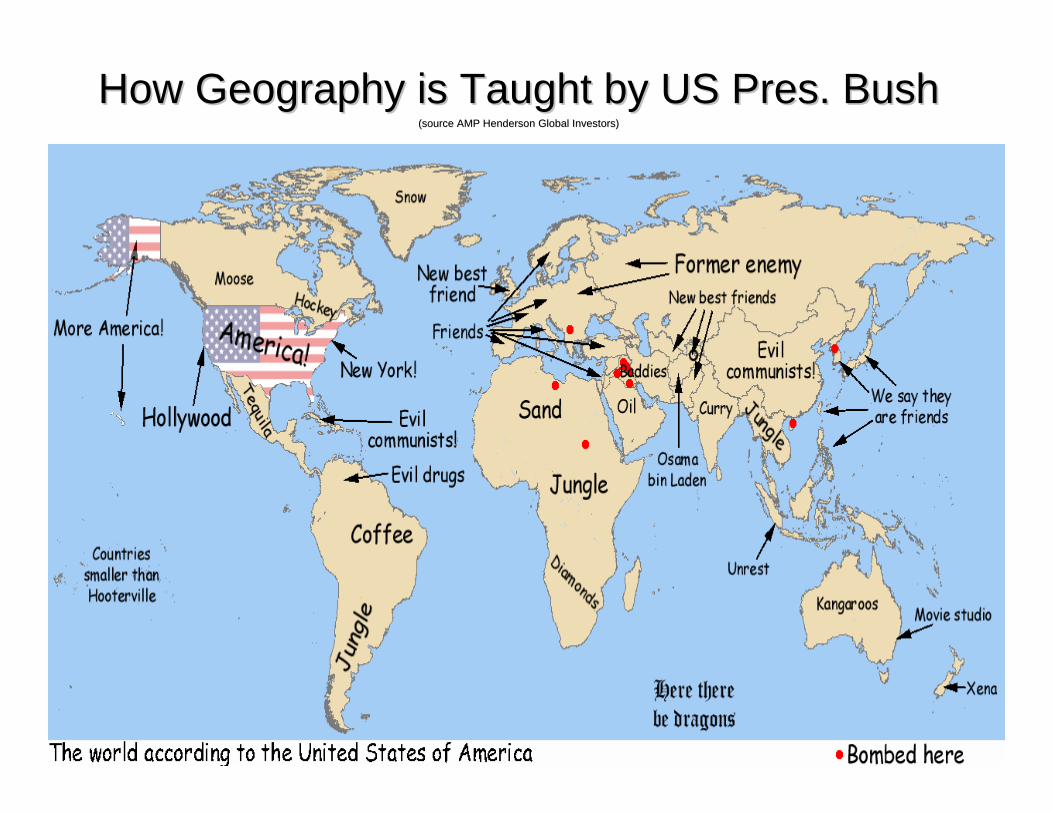

How Geography is Taught by US Pres. BushHow Geography is Taught by US Pres. Bush(source AMP Henderson Global Investors)(source AMP Henderson Global Investors)

Let’s quickly jump into some Let’s quickly jump into some interesting market evidence…. interesting market evidence…. Little Known Previously Secret Little Known Previously Secret Empirical Relationships Found Empirical Relationships Found

After Exhaustive Review After Exhaustive Review

Significant at the 5% levelSignificant at the 5% level

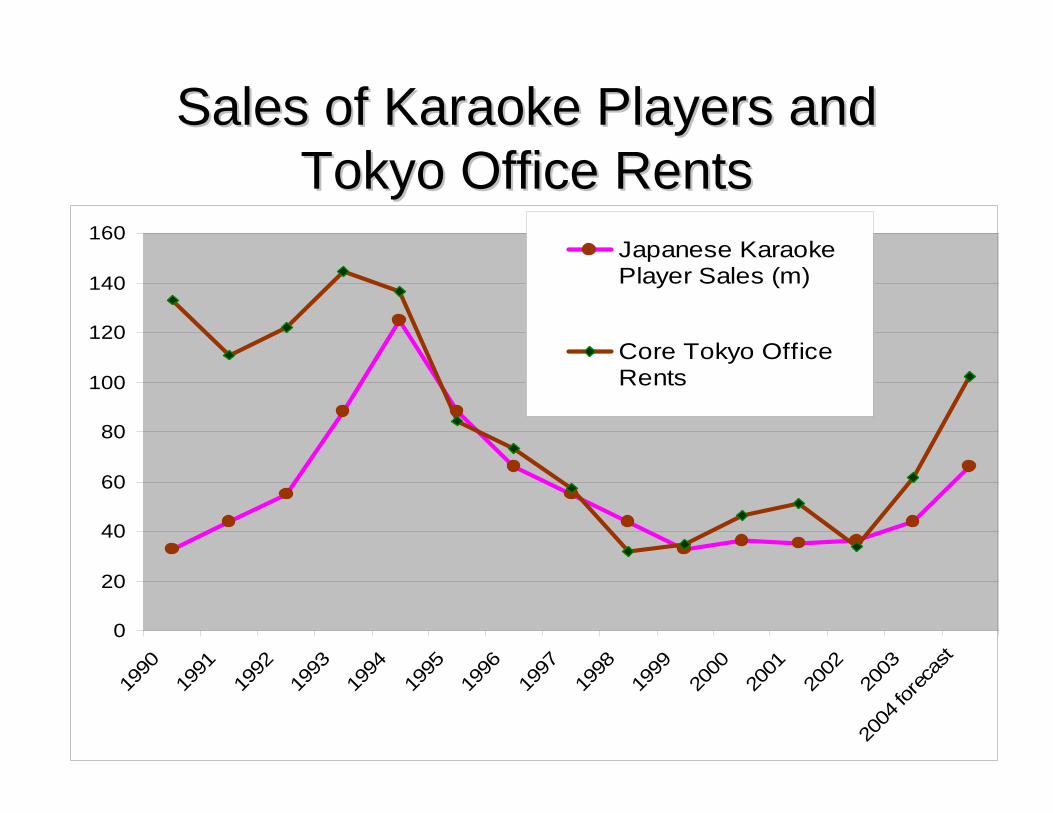

Sales of Karaoke Players and Sales of Karaoke Players and Tokyo Office RentsTokyo Office Rents

0

20

40

60

80

100

120

140

160

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

forec

ast

Japanese KaraokePlayer Sales (m)

Core Tokyo OfficeRents

There are others that we don’t have There are others that we don’t have time to review today such as time to review today such as

US “liberating” attacks on smaller US “liberating” attacks on smaller countries and the value of Real countries and the value of Real Estate in Cuba Estate in Cuba (negative correlation)(negative correlation)

The price of miniature Buddha's in The price of miniature Buddha's in Thailand and the rent on Class B Thailand and the rent on Class B retail space.retail space.

More seriously (but not totally seriously) today we will cover:More seriously (but not totally seriously) today we will cover:

The caseThe case for and against international real for and against international real estate investment with a review of some key estate investment with a review of some key studies (not too many)…studies (not too many)…The evidenceThe evidence in terms of returns and risks in terms of returns and risks (diversification).(diversification).A review of some investment advisor A review of some investment advisor approaches to international real estate.approaches to international real estate.A proposed strategy going forward.A proposed strategy going forward.Some direct investment criteria.Some direct investment criteria.Summary and conclusionsSummary and conclusions

Some research credits before we beginSome research credits before we beginResearch FirmsResearch Firms

DB Real EstateDB Real EstateGPR (Netherlands)GPR (Netherlands)DTZDTZIPD IPD Prudential (Prudential (LiangLiang, Gordon, , Gordon, LowreyLowrey))Jones Lang LaSalleJones Lang LaSalleHenderson Global (Henderson Global (PierzakPierzakand others)and others)RREEF now part of DBRREEF now part of DBColliers InternationalColliers InternationalIbbotson and Assoc.Ibbotson and Assoc.Ernst and YoungErnst and YoungDeloitte, Deloitte, ToucheTouche, , TohmatsuTohmatsu

Some Leading Authors Some Leading Authors PietPiet EicholtzEicholtz, Hans Van , Hans Van Opt’VeldOpt’Veld and GPRand GPRMartin Martin HoesliHoesli with Jon with Jon LekanderLekander and and WitoldWitoldWitkiewiczWitkiewiczPatrick Wilson and Ralf Patrick Wilson and Ralf ZurbrueggZurbrueggA.J. A.J. ZiobrowskiZiobrowskiGlenn MuellerGlenn MuellerDave Dave GeltnerGeltnerAndy BaumAndy BaumAddaeAddae--DapaahDapaahOnly authors who have treated me nicely will be mentioned Only authors who have treated me nicely will be mentioned ☺☺

The Case for Going GlobalThe Case for Going Global

Lower Portfolio Risks Through DiversificationLower Portfolio Risks Through Diversification–– Highly dependent on our return correlation Highly dependent on our return correlation

measures and our investment horizonmeasures and our investment horizonIncrease ReturnsIncrease Returns–– Highly dependent on our view of market Highly dependent on our view of market

efficiency, cycles and the ability to forecast trends efficiency, cycles and the ability to forecast trends as well as liquidity and transaction costsas well as liquidity and transaction costs

–– Note stated objectives versus exNote stated objectives versus ex--post realitypost realityLower Risks and Increase ReturnsLower Risks and Increase Returns

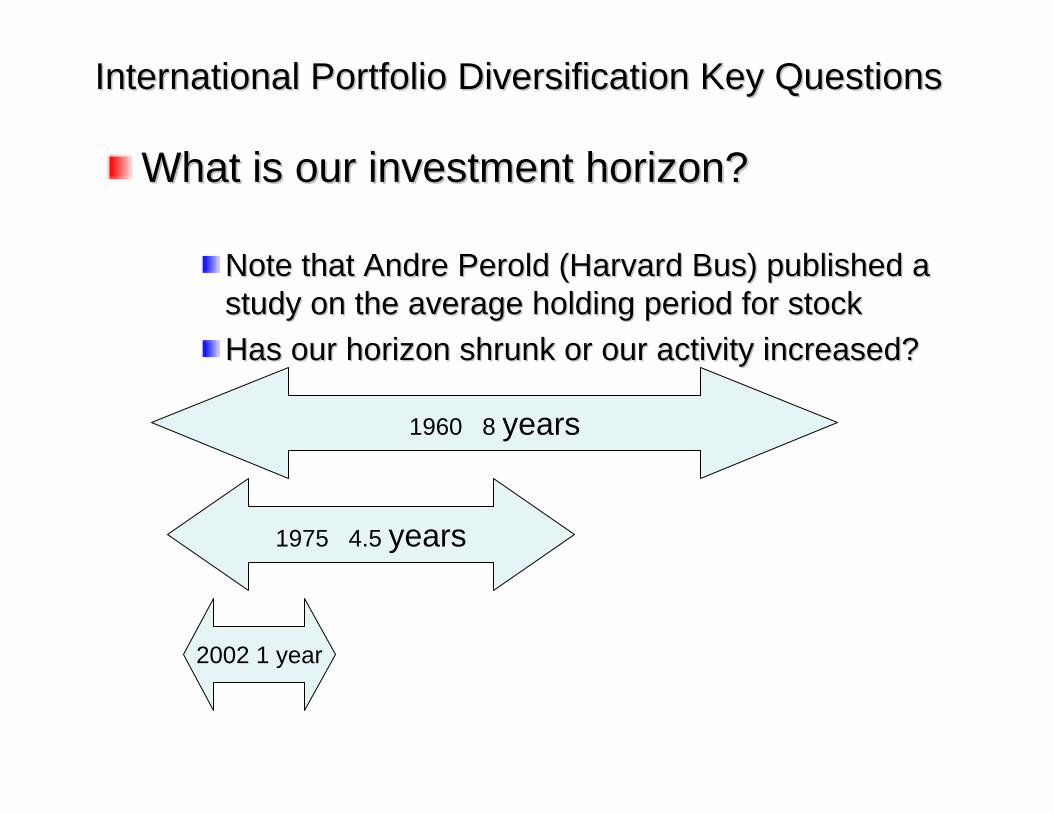

International Portfolio Diversification Key QuestionsInternational Portfolio Diversification Key Questions

What is our investment horizon?What is our investment horizon?–– Influences how quickly we judge performanceInfluences how quickly we judge performance

Do investors really care about risk?Do investors really care about risk?What is the appropriate horizon for What is the appropriate horizon for measuring correlations and how stable are measuring correlations and how stable are the correlations we use to judge the correlations we use to judge diversification?diversification?Is there enough data history?Is there enough data history?What is the appropriate portfolio? What is the appropriate portfolio? –– RE or All AssetsRE or All Assets

International Portfolio Diversification Key QuestionsInternational Portfolio Diversification Key Questions

What is our investment horizon?What is our investment horizon?

Note that Andre Note that Andre PeroldPerold (Harvard Bus) published a (Harvard Bus) published a study on the average holding period for stockstudy on the average holding period for stockHas our horizon shrunk or our activity increased?Has our horizon shrunk or our activity increased?

1960 8 years

1975 4.5 years

2002 1 year

Do investors really care about risk?Do investors really care about risk?Until the Tech stocks crashed in 1998 we saw that Until the Tech stocks crashed in 1998 we saw that when returns were high investors seemed to forget when returns were high investors seemed to forget about risk.about risk.

It can be difficult to remain objective It can be difficult to remain objective about risk until you get burned.about risk until you get burned.And remaining objective can be And remaining objective can be hard.hard.

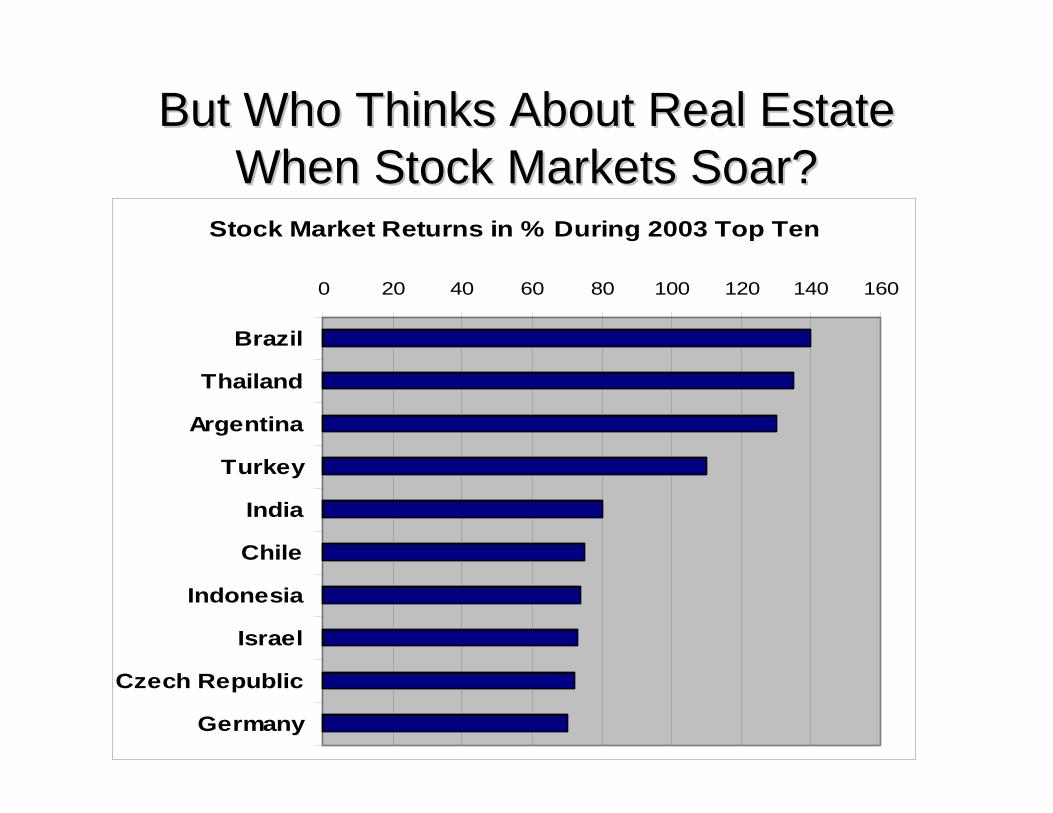

But Who Thinks About Real Estate But Who Thinks About Real Estate When Stock Markets Soar?When Stock Markets Soar?

Stock Market Returns in % During 2003 Top Ten

0 20 40 60 80 100 120 140 160

Brazil

Thailand

Argentina

Turkey

India

Chile

Indonesia

Israel

Czech Republic

Germany

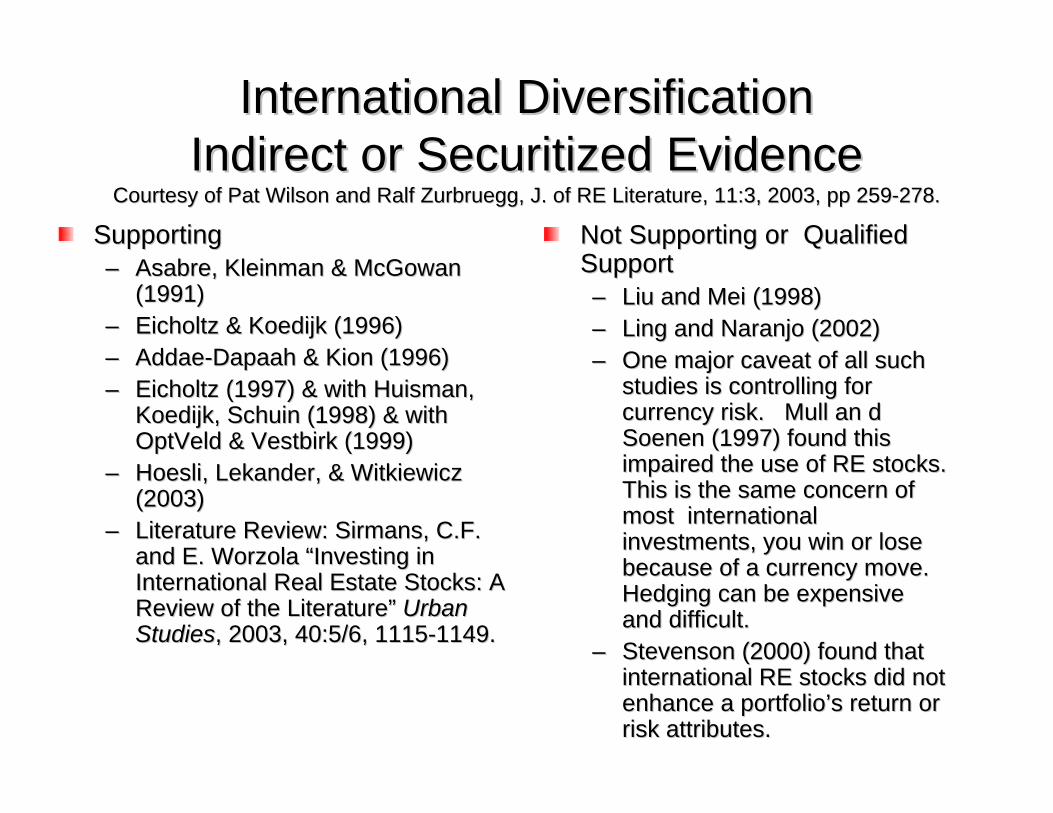

International Diversification International Diversification Indirect or Securitized EvidenceIndirect or Securitized Evidence

Courtesy of Pat Wilson and Ralf Courtesy of Pat Wilson and Ralf ZurbrueggZurbruegg, J. of RE Literature, 11:3, 2003, pp 259, J. of RE Literature, 11:3, 2003, pp 259--278.278.

Supporting Supporting –– AsabreAsabre, , KleinmanKleinman & McGowan & McGowan

(1991)(1991)–– EicholtzEicholtz & & KoedijkKoedijk (1996)(1996)–– AddaeAddae--DapaahDapaah & & KionKion (1996)(1996)–– EicholtzEicholtz (1997) & with (1997) & with HuismanHuisman, ,

KoedijkKoedijk, , SchuinSchuin (1998) & with (1998) & with OptVeldOptVeld & & VestbirkVestbirk (1999)(1999)

–– HoesliHoesli, , LekanderLekander, & , & WitkiewiczWitkiewicz(2003)(2003)

–– Literature Review: Literature Review: SirmansSirmans, C.F. , C.F. and E. and E. WorzolaWorzola “Investing in “Investing in International Real Estate Stocks: A International Real Estate Stocks: A Review of the Literature” Review of the Literature” Urban Urban StudiesStudies, 2003, 40:5/6, 1115, 2003, 40:5/6, 1115--1149.1149.

Not Supporting or Qualified Not Supporting or Qualified SupportSupport–– Liu and Liu and MeiMei (1998)(1998)–– Ling and Ling and NaranjoNaranjo (2002)(2002)–– One major caveat of all such One major caveat of all such

studies is controlling for studies is controlling for currency risk. Mull an d currency risk. Mull an d SoenenSoenen (1997) found this (1997) found this impaired the use of RE stocks. impaired the use of RE stocks. This is the same concern of This is the same concern of most international most international investments, you win or lose investments, you win or lose because of a currency move. because of a currency move. Hedging can be expensive Hedging can be expensive and difficult.and difficult.

–– Stevenson (2000) found that Stevenson (2000) found that international RE stocks did not international RE stocks did not enhance a portfolio’s return or enhance a portfolio’s return or risk attributes.risk attributes.

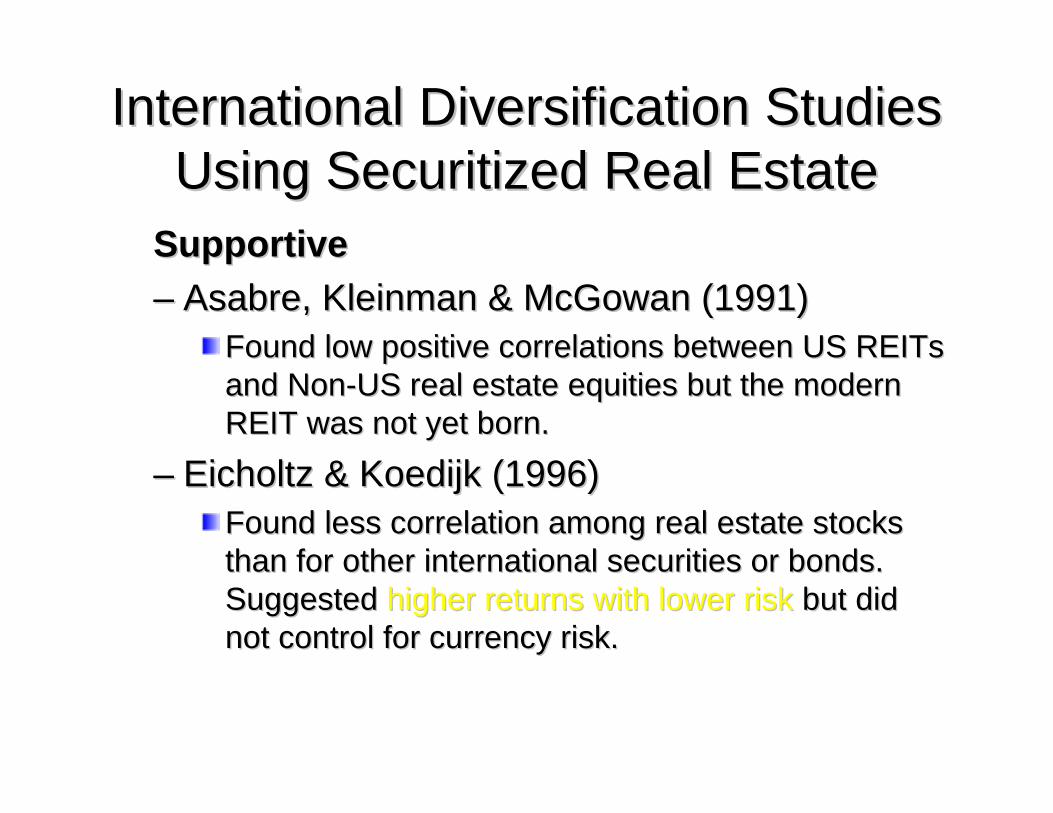

International Diversification Studies International Diversification Studies Using Securitized Real EstateUsing Securitized Real Estate

SupportiveSupportive–– AsabreAsabre, , KleinmanKleinman & McGowan (1991)& McGowan (1991)

Found low positive correlations between US Found low positive correlations between US REITsREITsand Nonand Non--US real estate equities but the modern US real estate equities but the modern REIT was not yet born.REIT was not yet born.

–– EicholtzEicholtz & & KoedijkKoedijk (1996)(1996)Found less correlation among real estate stocks Found less correlation among real estate stocks than for other international securities or bonds. than for other international securities or bonds. Suggested Suggested higher returns with lower riskhigher returns with lower risk but did but did not control for currency risk. not control for currency risk.

International Diversification Studies International Diversification Studies Using Securitized Real EstateUsing Securitized Real Estate

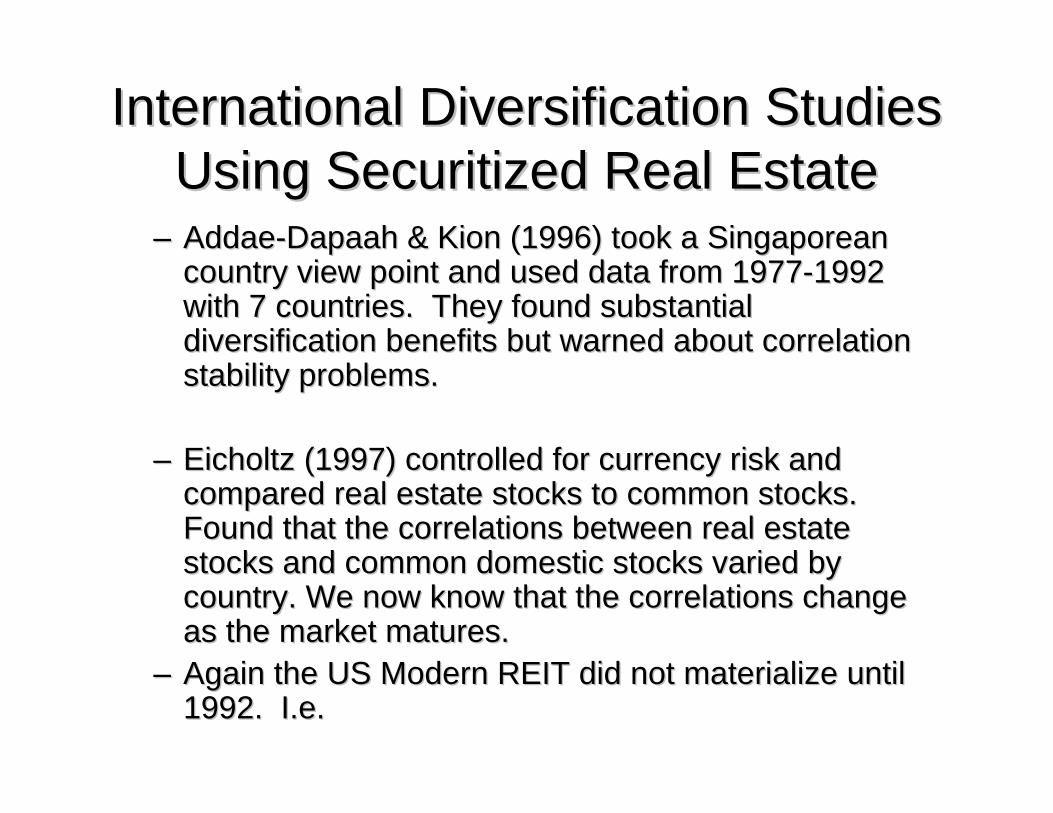

–– AddaeAddae--DapaahDapaah & & KionKion (1996) took a Singaporean (1996) took a Singaporean country view point and used data from 1977country view point and used data from 1977--1992 1992 with 7 countries. They found substantial with 7 countries. They found substantial diversification benefits but warned about correlation diversification benefits but warned about correlation stability problems.stability problems.

–– EicholtzEicholtz (1997) controlled for currency risk and (1997) controlled for currency risk and compared real estate stocks to common stocks. compared real estate stocks to common stocks. Found that the correlations between real estate Found that the correlations between real estate stocks and common domestic stocks varied by stocks and common domestic stocks varied by country. We now know that the correlations change country. We now know that the correlations change as the market matures. as the market matures.

–– Again the US Modern REIT did not materialize until Again the US Modern REIT did not materialize until 1992. I.e.1992. I.e.

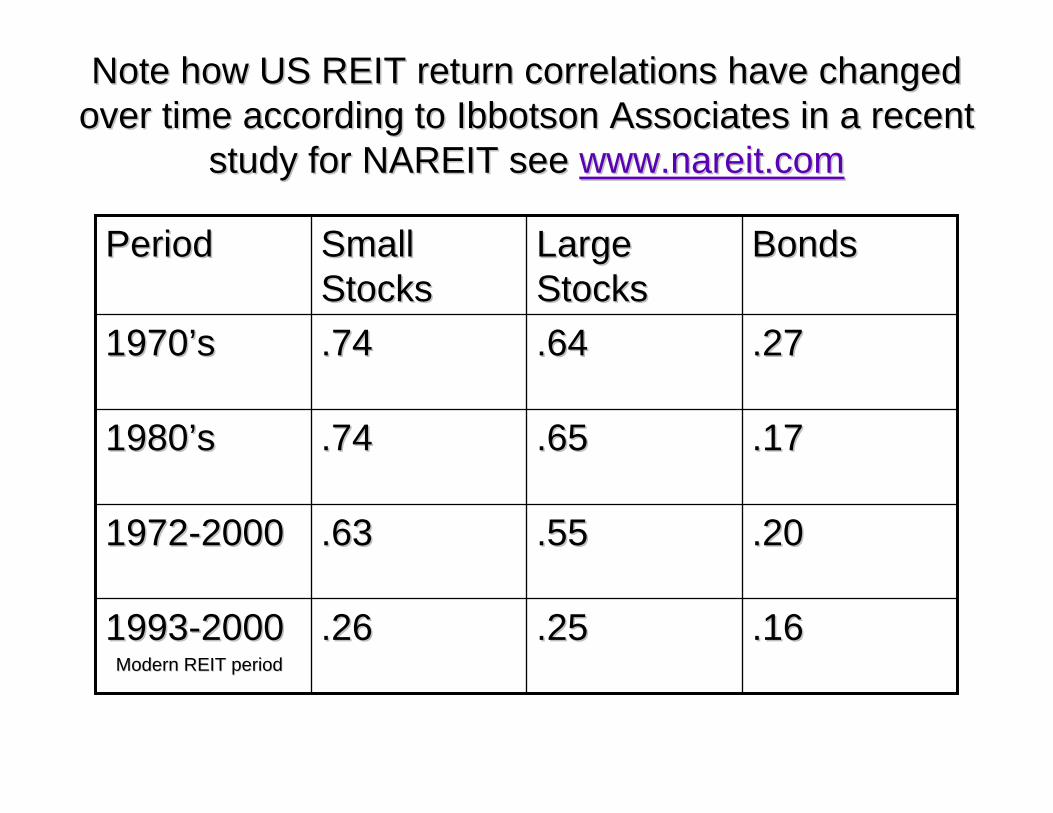

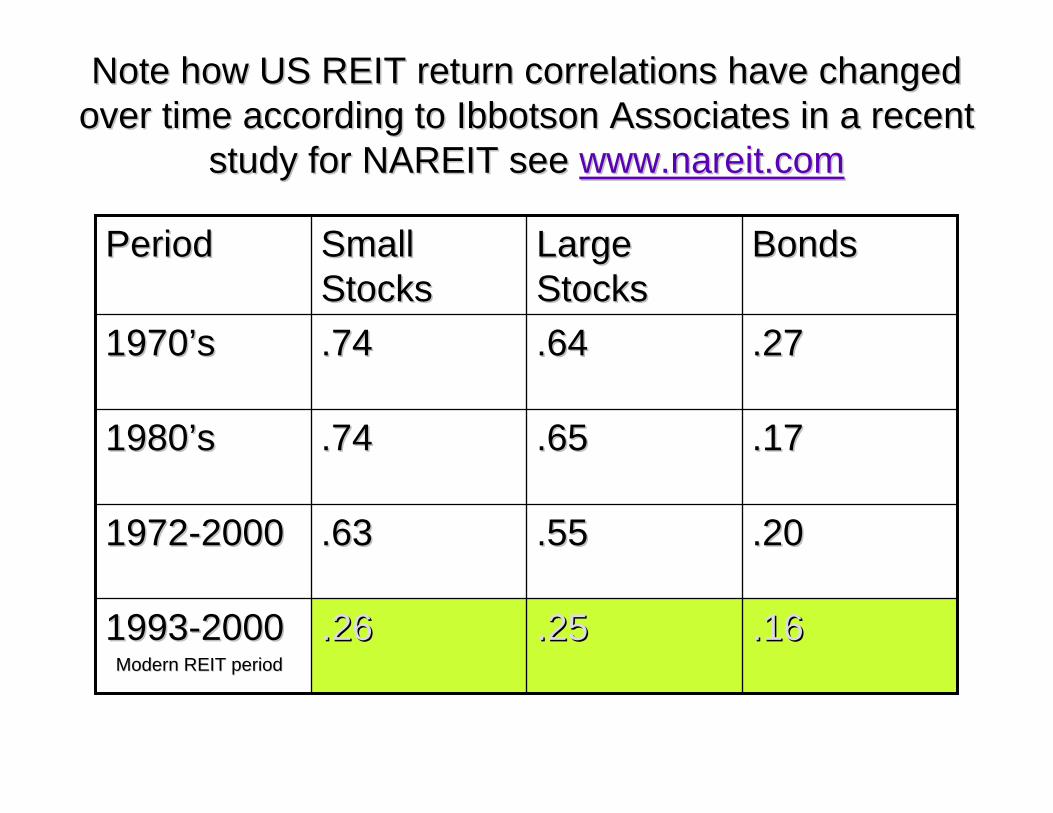

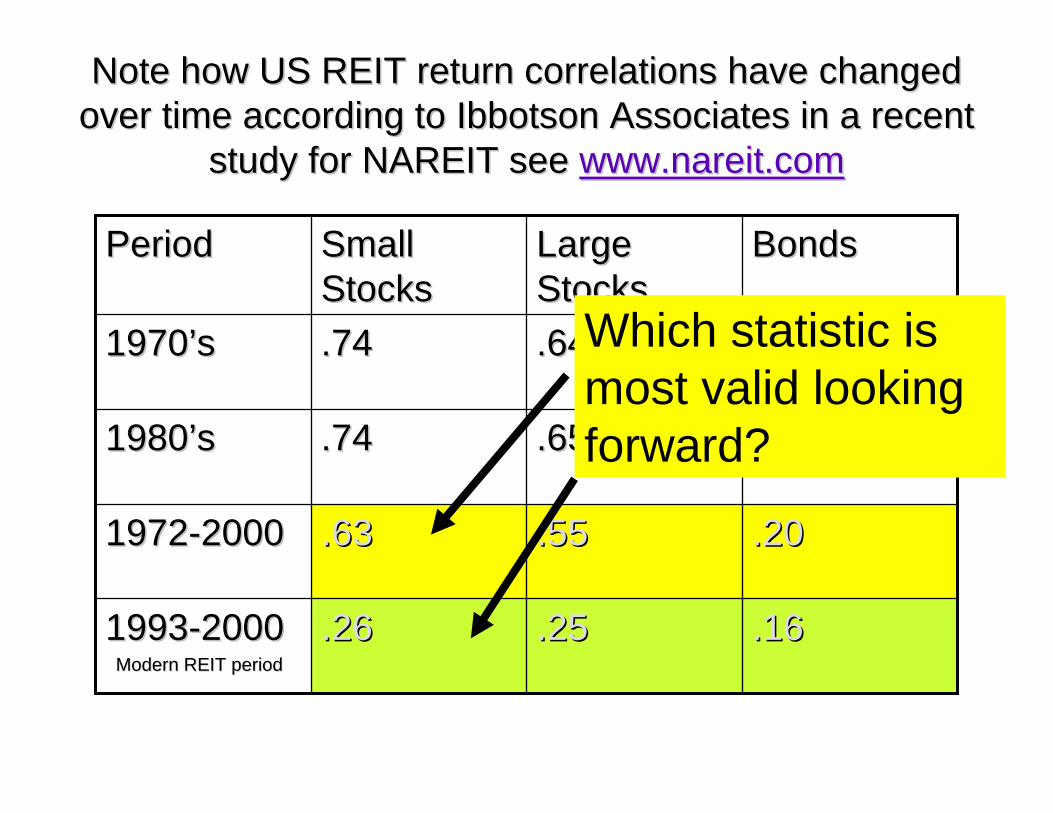

Note how US REIT return correlations have changed Note how US REIT return correlations have changed over time according to Ibbotson Associates in a recent over time according to Ibbotson Associates in a recent

study for NAREIT see study for NAREIT see www.nareit.comwww.nareit.com

.16.16.25.25.26.2619931993--20002000Modern REIT periodModern REIT period

.20.20.55.55.63.6319721972--20002000

.17.17.65.65.74.741980’s1980’s

.27.27.64.64.74.741970’s1970’s

BondsBondsLarge Large StocksStocks

Small Small StocksStocks

PeriodPeriod

Note how US REIT return correlations have changed Note how US REIT return correlations have changed over time according to Ibbotson Associates in a recent over time according to Ibbotson Associates in a recent

study for NAREIT see study for NAREIT see www.nareit.comwww.nareit.com

.16.16.25.25.26.2619931993--20002000Modern REIT periodModern REIT period

.20.20.55.55.63.6319721972--20002000

.17.17.65.65.74.741980’s1980’s

.27.27.64.64.74.741970’s1970’s

BondsBondsLarge Large StocksStocks

Small Small StocksStocks

PeriodPeriod

Note how US REIT return correlations have changed Note how US REIT return correlations have changed over time according to Ibbotson Associates in a recent over time according to Ibbotson Associates in a recent

study for NAREIT see study for NAREIT see www.nareit.comwww.nareit.com

.16.16.25.25.26.2619931993--20002000Modern REIT periodModern REIT period

.20.20.55.55.63.6319721972--20002000

.17.17.65.65.74.741980’s1980’s

.27.27.64.64.74.741970’s1970’s

BondsBondsLarge Large StocksStocks

Small Small StocksStocks

PeriodPeriod

Which statistic is most valid looking forward?

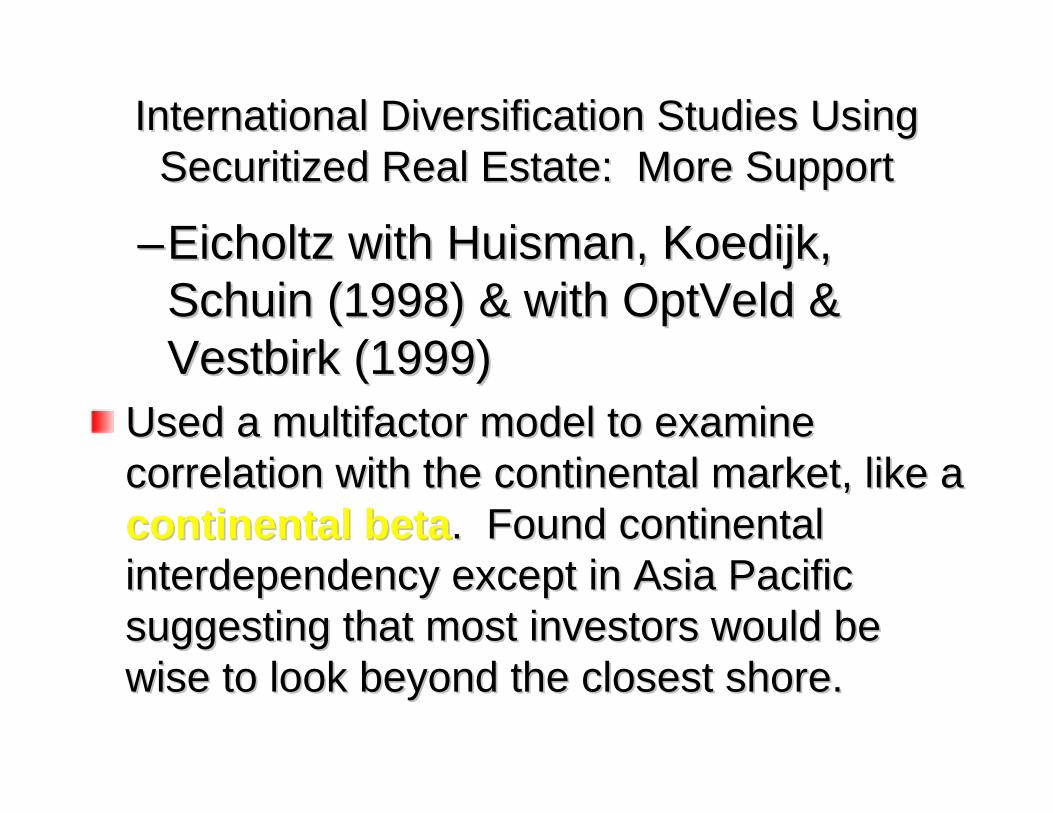

International Diversification Studies Using International Diversification Studies Using Securitized Real Estate: More SupportSecuritized Real Estate: More Support

––EicholtzEicholtz with with HuismanHuisman, , KoedijkKoedijk, , SchuinSchuin (1998) & with (1998) & with OptVeldOptVeld & & VestbirkVestbirk (1999)(1999)

Used a multifactor model to examine Used a multifactor model to examine correlation with the continental market, like a correlation with the continental market, like a continental betacontinental beta. Found continental . Found continental interdependency except in Asia Pacific interdependency except in Asia Pacific suggesting that most investors would be suggesting that most investors would be wise to look beyond the closest shore. wise to look beyond the closest shore.

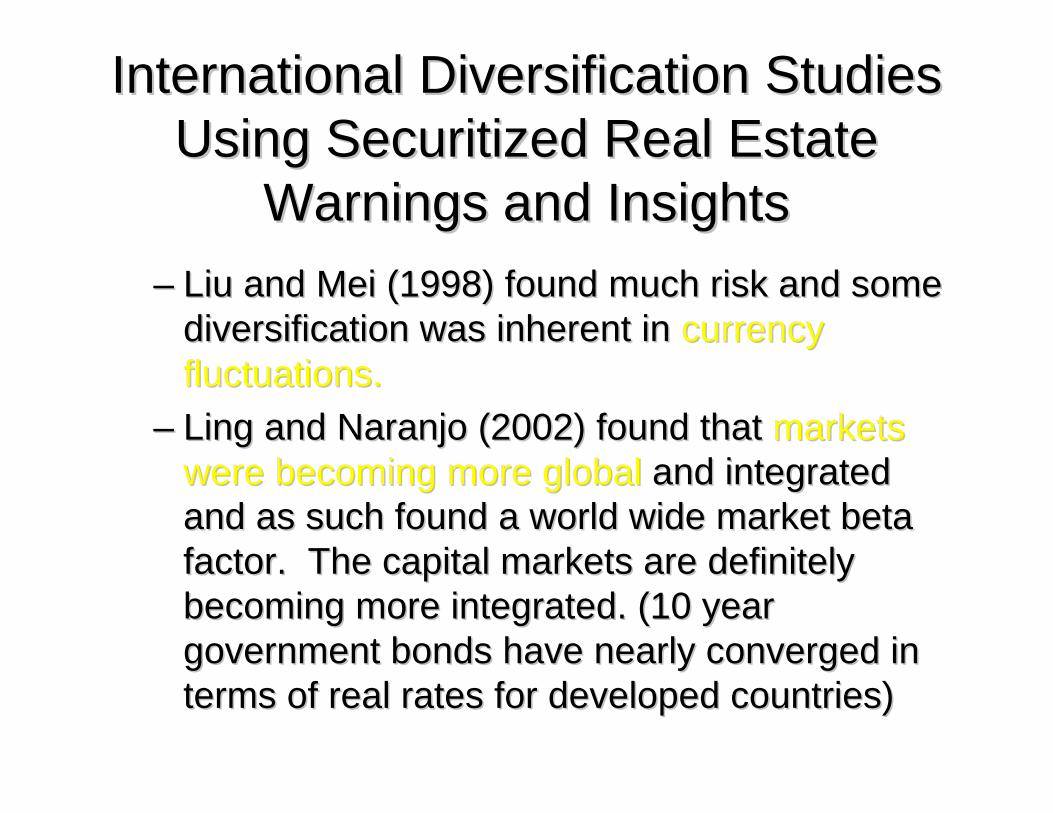

International Diversification Studies International Diversification Studies Using Securitized Real EstateUsing Securitized Real Estate

Warnings and InsightsWarnings and Insights–– Liu and Liu and MeiMei (1998) found much risk and some (1998) found much risk and some

diversification was inherent in diversification was inherent in currency currency fluctuations.fluctuations.

–– Ling and Ling and NaranjoNaranjo (2002) found that (2002) found that markets markets were becoming more globalwere becoming more global and integrated and integrated and as such found a world wide market beta and as such found a world wide market beta factor. The capital markets are definitely factor. The capital markets are definitely becoming more integrated. (10 year becoming more integrated. (10 year government bonds have nearly converged in government bonds have nearly converged in terms of real rates for developed countries) terms of real rates for developed countries)

Invest in global firms domestically based?Invest in global firms domestically based?–– Just buy Coca Cola or P&G?Just buy Coca Cola or P&G?–– Some US Some US REITsREITs are now becoming global and are now becoming global and

providing some international diversification. For providing some international diversification. For example these US based example these US based REITsREITs are starting to invest are starting to invest internationally:internationally:

Chelsea Property Corp (CPG) retailChelsea Property Corp (CPG) retailArchstoneArchstone Smith (ASN) residentialSmith (ASN) residentialShurgardShurgard (SHU) storage(SHU) storageAMB Property (AMB) industrialAMB Property (AMB) industrialPrologisPrologis (PLD) industrial(PLD) industrialFirst Industrial (FR) First Industrial (FR)

Still it is a small list with a small portion of Still it is a small list with a small portion of foreign foreign real estate!real estate!

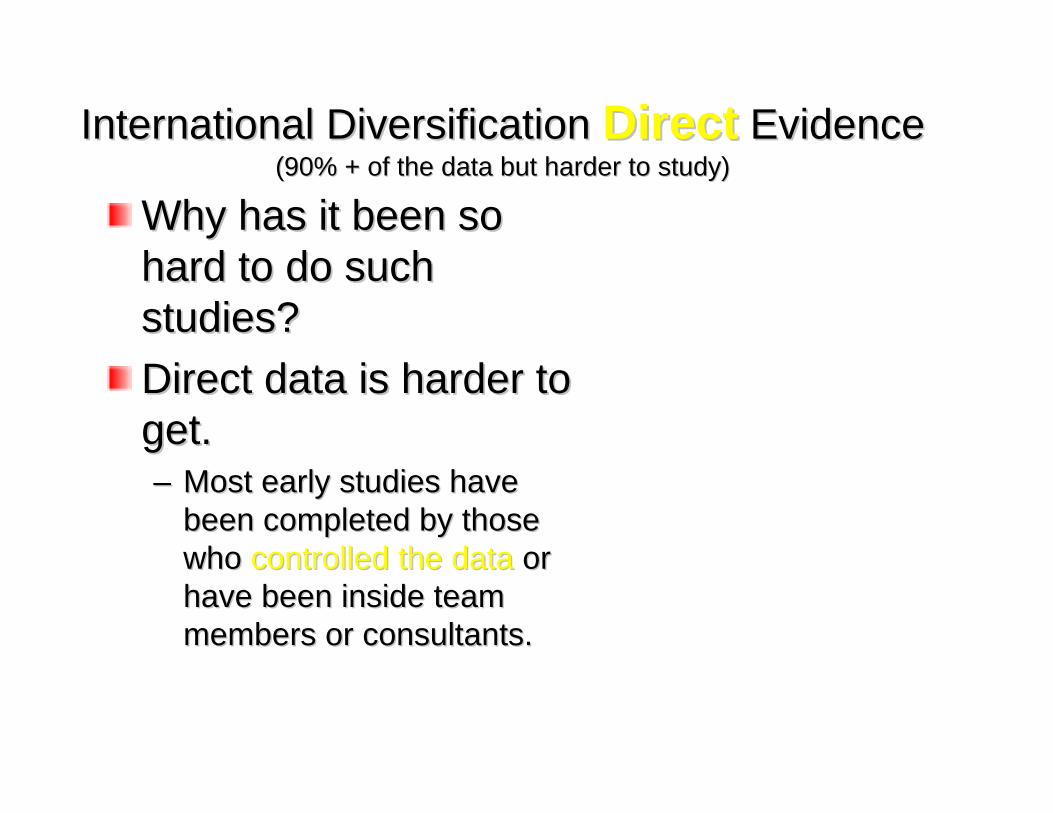

International Diversification International Diversification DirectDirect EvidenceEvidence(90% + of the data but harder to study)(90% + of the data but harder to study)

Why has it been so Why has it been so hard to do such hard to do such studies?studies?Direct data is harder to Direct data is harder to get. get. –– Most early studies have Most early studies have

been completed by those been completed by those who who controlled the datacontrolled the data or or have been inside team have been inside team members or consultants.members or consultants.

–– Major players Major players didn’t wantdidn’t want the the detailsdetails of their of their properties properties revealedrevealed so they only wanted so they only wanted aggregate data to be available.aggregate data to be available.

–– The The market wants transparency but notmarket wants transparency but not all the all the investment advisors.investment advisors.

What is the big concern with using direct What is the big concern with using direct data?data?Smoothing or understating true price Smoothing or understating true price volatilityvolatility based on infrequent appraisals and based on infrequent appraisals and biased appraisals that do not adjust fully to biased appraisals that do not adjust fully to current market conditions. (current market conditions. (GeltnerGeltner 1989+)1989+)–– Most studies today will unsmoothMost studies today will unsmooth the data and the data and

make assumptions about underlying risk.make assumptions about underlying risk.–– Data history is often too short and emerging Data history is often too short and emerging

markets need to reach a certain threshold, large markets need to reach a certain threshold, large enough to attract institutional investors before enough to attract institutional investors before the return trends stabilize.the return trends stabilize.

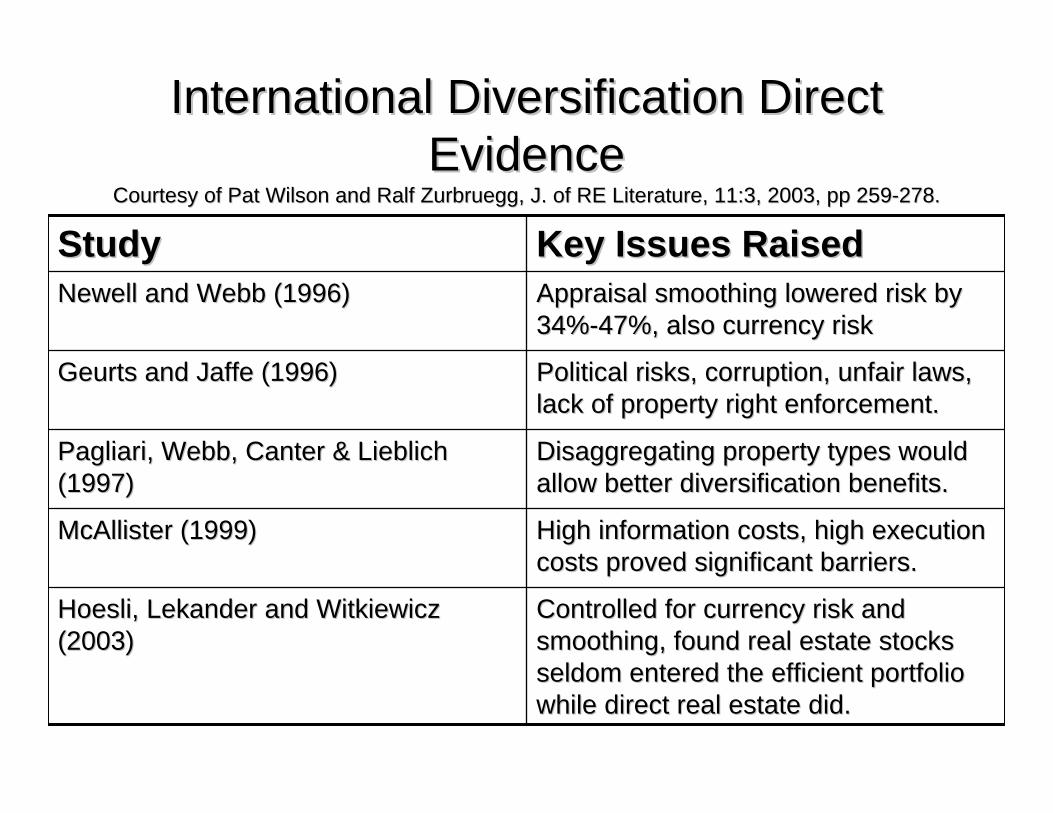

International Diversification Direct International Diversification Direct EvidenceEvidence

Courtesy of Pat Wilson and Ralf Courtesy of Pat Wilson and Ralf ZurbrueggZurbruegg, J. of RE Literature, 11:3, 2003, pp 259, J. of RE Literature, 11:3, 2003, pp 259--278.278.

Controlled for currency risk and Controlled for currency risk and smoothing, found real estate stocks smoothing, found real estate stocks seldom entered the efficient portfolio seldom entered the efficient portfolio while direct real estate did.while direct real estate did.

HoesliHoesli, , LekanderLekander and and WitkiewiczWitkiewicz(2003)(2003)

High information costs, high execution High information costs, high execution costs proved significant barriers.costs proved significant barriers.

McAllister (1999)McAllister (1999)

Disaggregating property types would Disaggregating property types would allow better diversification benefits.allow better diversification benefits.

PagliariPagliari, Webb, Canter & , Webb, Canter & LieblichLieblich(1997)(1997)

Political risks, corruption, unfair laws, Political risks, corruption, unfair laws, lack of property right enforcement.lack of property right enforcement.

GeurtsGeurts and Jaffe (1996)and Jaffe (1996)

Appraisal smoothing lowered risk by Appraisal smoothing lowered risk by 34%34%--47%, also currency risk47%, also currency risk

Newell and Webb (1996)Newell and Webb (1996)Key Issues RaisedKey Issues RaisedStudyStudy

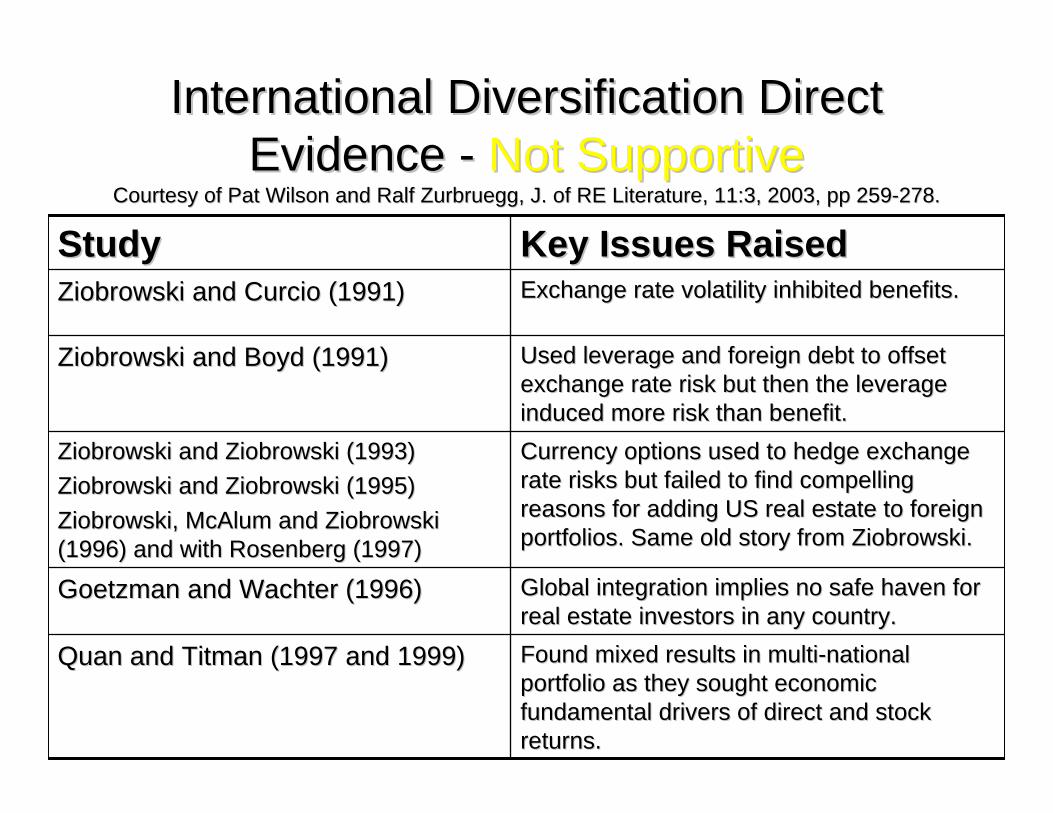

International Diversification Direct International Diversification Direct Evidence Evidence -- Not SupportiveNot Supportive

Courtesy of Pat Wilson and Ralf Courtesy of Pat Wilson and Ralf ZurbrueggZurbruegg, J. of RE Literature, 11:3, 2003, pp 259, J. of RE Literature, 11:3, 2003, pp 259--278.278.

Global integration implies no safe haven for Global integration implies no safe haven for real estate investors in any country.real estate investors in any country.

GoetzmanGoetzman and and WachterWachter (1996)(1996)

Found mixed results in multiFound mixed results in multi--national national portfolio as they sought economic portfolio as they sought economic fundamental drivers of direct and stock fundamental drivers of direct and stock returns.returns.

QuanQuan and Titman (1997 and 1999)and Titman (1997 and 1999)

Currency options used to hedge exchange Currency options used to hedge exchange rate risks but failed to find compelling rate risks but failed to find compelling reasons for adding US real estate to foreign reasons for adding US real estate to foreign portfolios. Same old story from portfolios. Same old story from ZiobrowskiZiobrowski..

ZiobrowskiZiobrowski and and ZiobrowskiZiobrowski (1993)(1993)ZiobrowskiZiobrowski and and ZiobrowskiZiobrowski (1995)(1995)ZiobrowskiZiobrowski, , McAlumMcAlum and and ZiobrowskiZiobrowski(1996) and with Rosenberg (1997)(1996) and with Rosenberg (1997)

Used leverage and foreign debt to offset Used leverage and foreign debt to offset exchange rate risk but then the leverage exchange rate risk but then the leverage induced more risk than benefit.induced more risk than benefit.

ZiobrowskiZiobrowski and Boyd (1991)and Boyd (1991)

Exchange rate volatility inhibited benefits.Exchange rate volatility inhibited benefits.ZiobrowskiZiobrowski and and CurcioCurcio (1991)(1991)Key Issues RaisedKey Issues RaisedStudyStudy

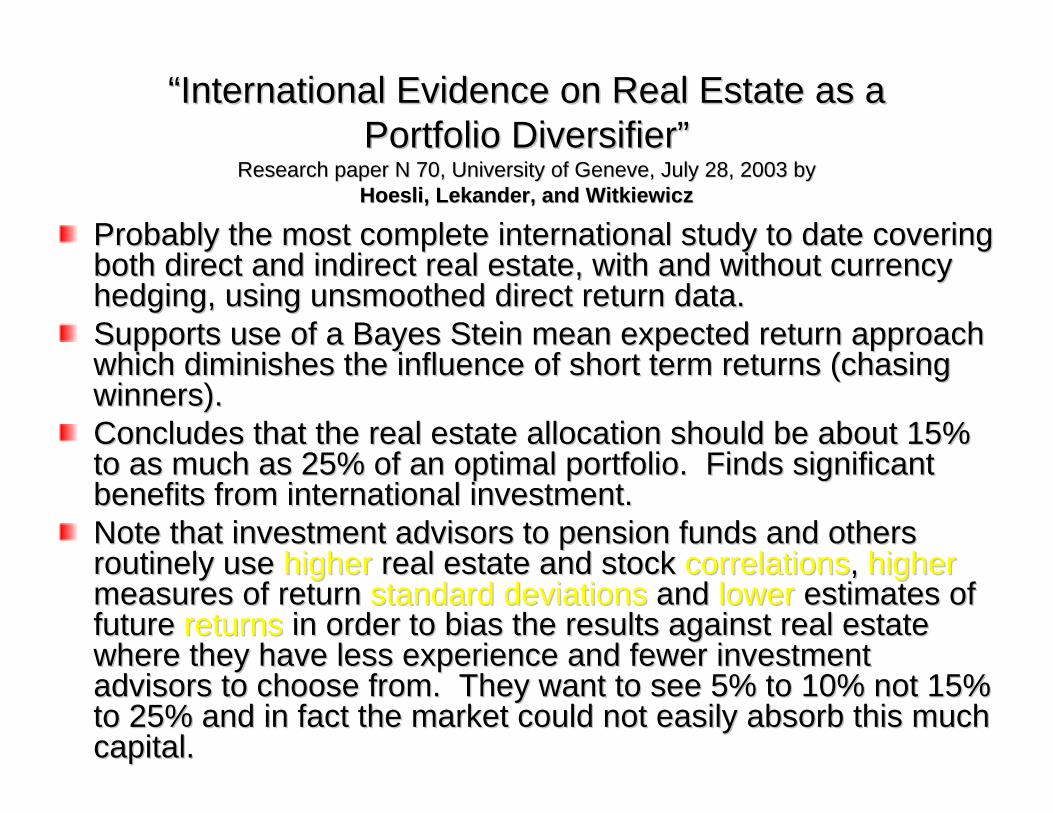

““International Evidence on Real Estate as a International Evidence on Real Estate as a Portfolio Diversifier”Portfolio Diversifier”

Research paper N 70, University of Research paper N 70, University of GeneveGeneve, July 28, 2003 by, July 28, 2003 byHoesliHoesli, , LekanderLekander, and , and WitkiewiczWitkiewicz

Probably the most complete international study to date covering Probably the most complete international study to date covering both direct and indirect real estate, with and without currency both direct and indirect real estate, with and without currency hedging, using unsmoothed direct return data.hedging, using unsmoothed direct return data.Supports use of a Supports use of a BayesBayes Stein mean expected return approach Stein mean expected return approach which diminishes the influence of short term returns (chasing which diminishes the influence of short term returns (chasing winners).winners).Concludes that the real estate allocation should be about 15% Concludes that the real estate allocation should be about 15% to as much as 25% of an optimal portfolio. Finds significant to as much as 25% of an optimal portfolio. Finds significant benefits from international investment.benefits from international investment.Note that investment advisors to pension funds and others Note that investment advisors to pension funds and others routinely use routinely use higherhigher real estate and stock real estate and stock correlationscorrelations, , higherhighermeasures of return measures of return standard deviationsstandard deviations and and lowerlower estimates of estimates of future future returnsreturns in order to bias the results against real estate in order to bias the results against real estate where they have less experience and fewer investment where they have less experience and fewer investment advisors to choose from. They want to see 5% to 10% not 15% advisors to choose from. They want to see 5% to 10% not 15% to 25% and in fact the market could not easily absorb this much to 25% and in fact the market could not easily absorb this much capital.capital.

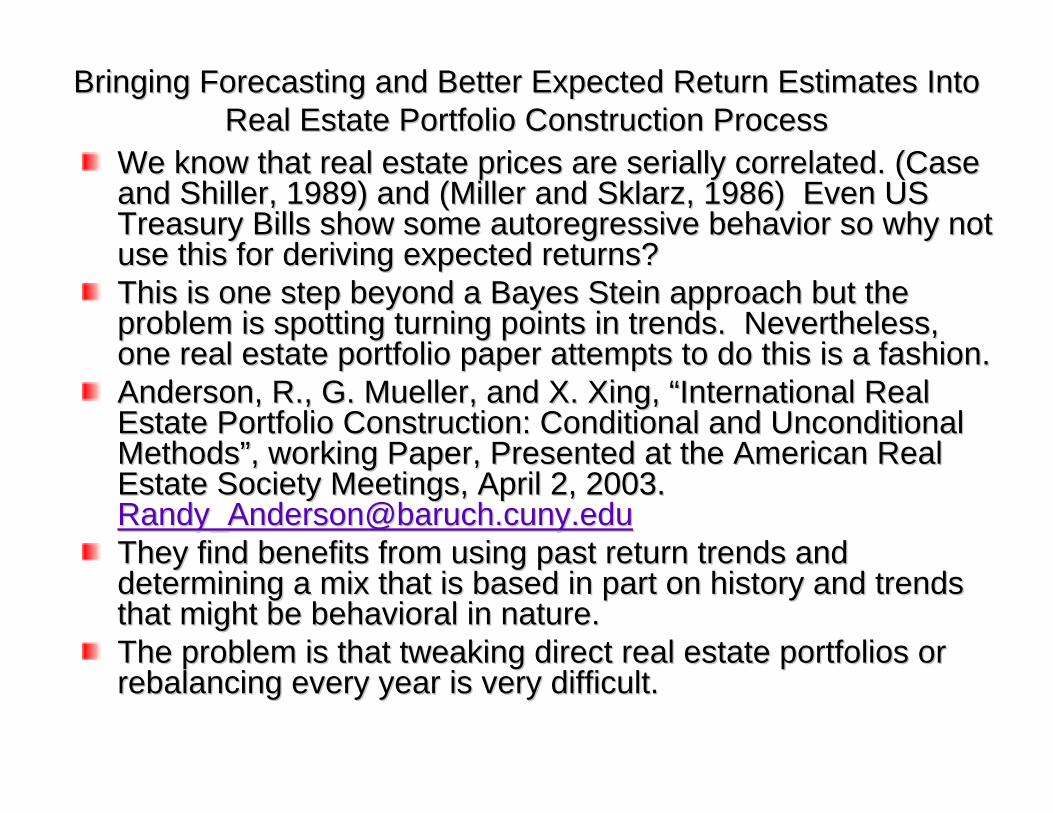

Bringing Forecasting and Better Expected Return Estimates Into Bringing Forecasting and Better Expected Return Estimates Into Real Estate Portfolio Construction ProcessReal Estate Portfolio Construction Process

We know that real estate prices are serially correlated. (Case We know that real estate prices are serially correlated. (Case and and ShillerShiller, 1989) and (Miller and , 1989) and (Miller and SklarzSklarz, 1986) Even US , 1986) Even US Treasury Bills show some autoregressive behavior so why not Treasury Bills show some autoregressive behavior so why not use this for deriving expected returns?use this for deriving expected returns?This is one step beyond a This is one step beyond a BayesBayes Stein approach but the Stein approach but the problem is spotting turning points in trends. Nevertheless, problem is spotting turning points in trends. Nevertheless, one real estate portfolio paper attempts to do this is a fashionone real estate portfolio paper attempts to do this is a fashion..Anderson, R., G. Mueller, and X. Xing, “International Real Anderson, R., G. Mueller, and X. Xing, “International Real Estate Portfolio Construction: Conditional and Unconditional Estate Portfolio Construction: Conditional and Unconditional Methods”, working Paper, Presented at the American Real Methods”, working Paper, Presented at the American Real Estate Society Meetings, April 2, 2003. Estate Society Meetings, April 2, 2003. [email protected][email protected] find benefits from using past return trends and They find benefits from using past return trends and determining a mix that is based in part on history and trends determining a mix that is based in part on history and trends that might be behavioral in nature. that might be behavioral in nature. The problem is that tweaking direct real estate portfolios or The problem is that tweaking direct real estate portfolios or rebalancing every year is very difficult.rebalancing every year is very difficult.

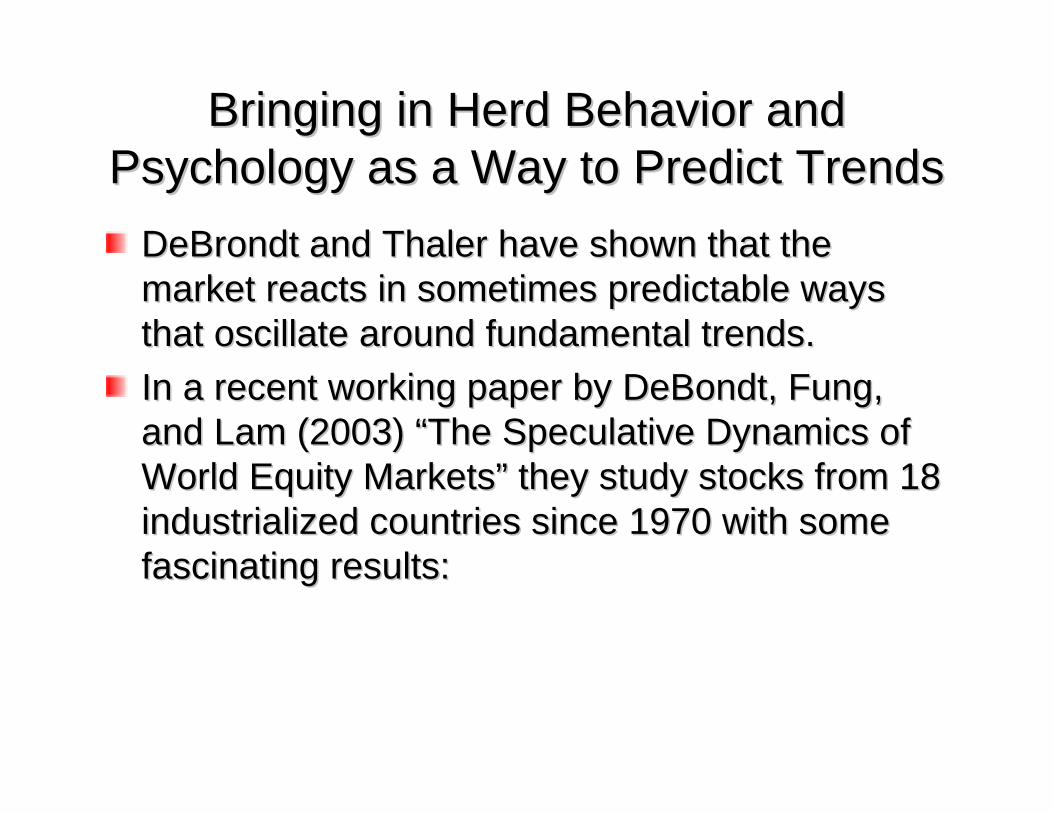

Bringing in Herd Behavior and Bringing in Herd Behavior and Psychology as a Way to Predict TrendsPsychology as a Way to Predict Trends

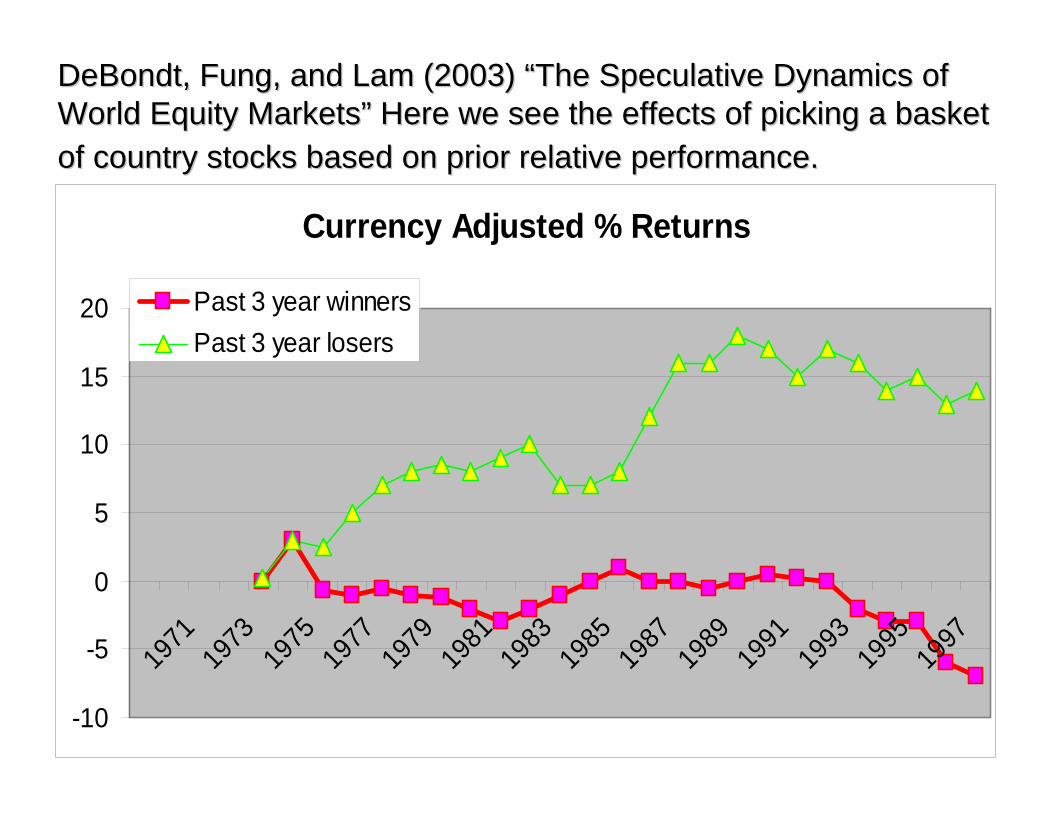

DeBrondtDeBrondt and and ThalerThaler have shown that the have shown that the market reacts in sometimes predictable ways market reacts in sometimes predictable ways that oscillate around fundamental trends. that oscillate around fundamental trends. In a recent working paper by In a recent working paper by DeBondtDeBondt, , FungFung, , and Lam (2003) “The Speculative Dynamics of and Lam (2003) “The Speculative Dynamics of World Equity Markets” they study stocks from 18 World Equity Markets” they study stocks from 18 industrialized countries since 1970 with some industrialized countries since 1970 with some fascinating results:fascinating results:

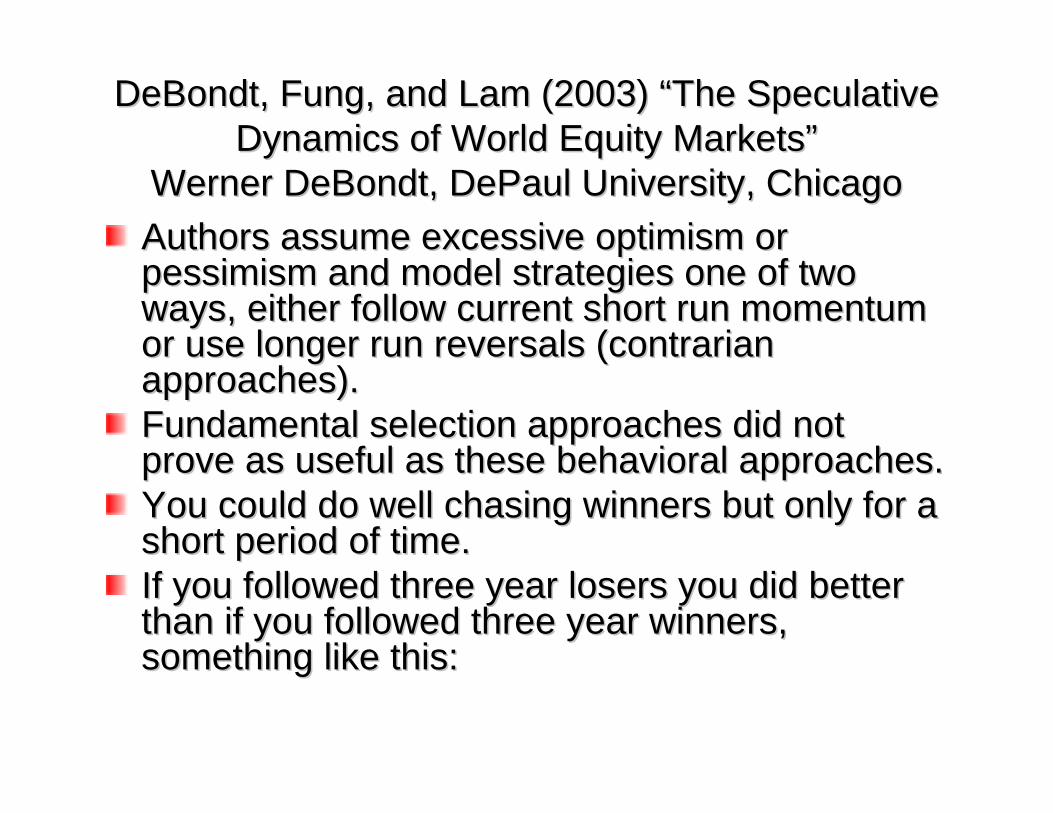

DeBondtDeBondt, , FungFung, and Lam (2003) “The Speculative , and Lam (2003) “The Speculative Dynamics of World Equity Markets”Dynamics of World Equity Markets”

Werner Werner DeBondtDeBondt, DePaul University, Chicago, DePaul University, ChicagoAuthors assume excessive optimism or Authors assume excessive optimism or pessimism and model strategies one of two pessimism and model strategies one of two ways, either follow current short run momentum ways, either follow current short run momentum or use longer run reversals (or use longer run reversals (contrariancontrarianapproaches).approaches).Fundamental selection approaches did not Fundamental selection approaches did not prove as useful as these behavioral approaches.prove as useful as these behavioral approaches.You could do well chasing winners but only for a You could do well chasing winners but only for a short period of time.short period of time.If you followed three year losers you did better If you followed three year losers you did better than if you followed three year winners, than if you followed three year winners, something like this:something like this:

DeBondtDeBondt, , FungFung, and Lam (2003) “The Speculative Dynamics of , and Lam (2003) “The Speculative Dynamics of World Equity Markets” Here we see the effects of picking a baskeWorld Equity Markets” Here we see the effects of picking a basket t of country stocks based on prior relative performance.of country stocks based on prior relative performance.

Currency Adjusted % Returns

-10

-5

0

5

10

15

20

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

Past 3 year winnersPast 3 year losers

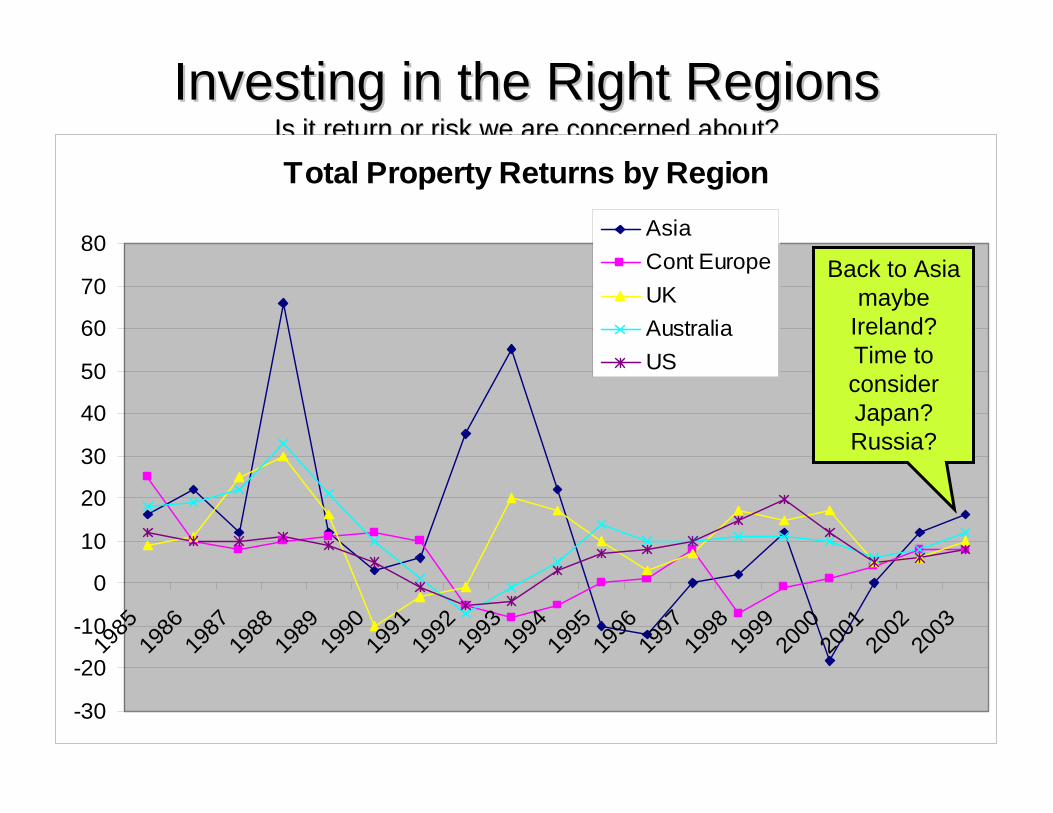

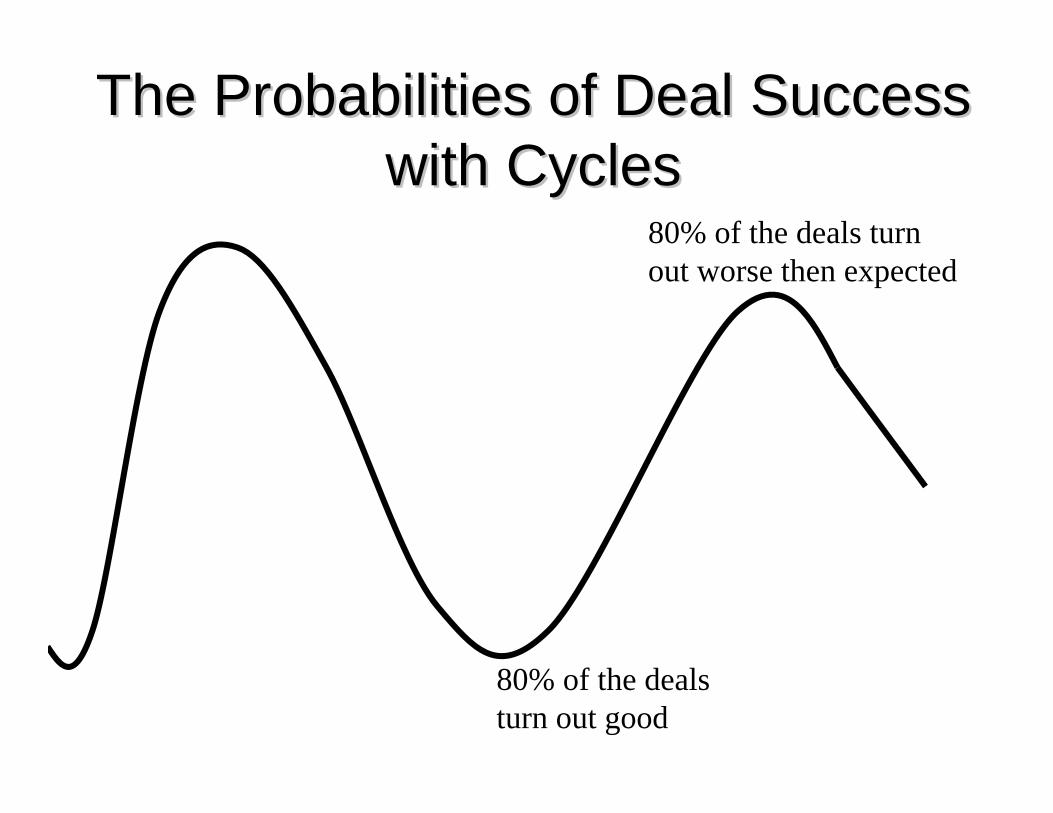

Cycles and Picking Winning Cycles and Picking Winning Countries or RegionsCountries or Regions

Can we apply Can we apply contrariancontrarian investing to investing to direct real estate or direct real estate or consider the consider the momentum of trends? momentum of trends? Is she on her way up or Is she on her way up or on her way down?on her way down?

Investing in the Right RegionsInvesting in the Right RegionsIs it return or risk we are concerned about?Is it return or risk we are concerned about?

Total Property Returns by Region

-30

-20

-10

0

10

20

30

40

50

60

70

80

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

AsiaCont EuropeUKAustraliaUS

Back to Asia maybe

Ireland? Time to consider Japan?Russia?

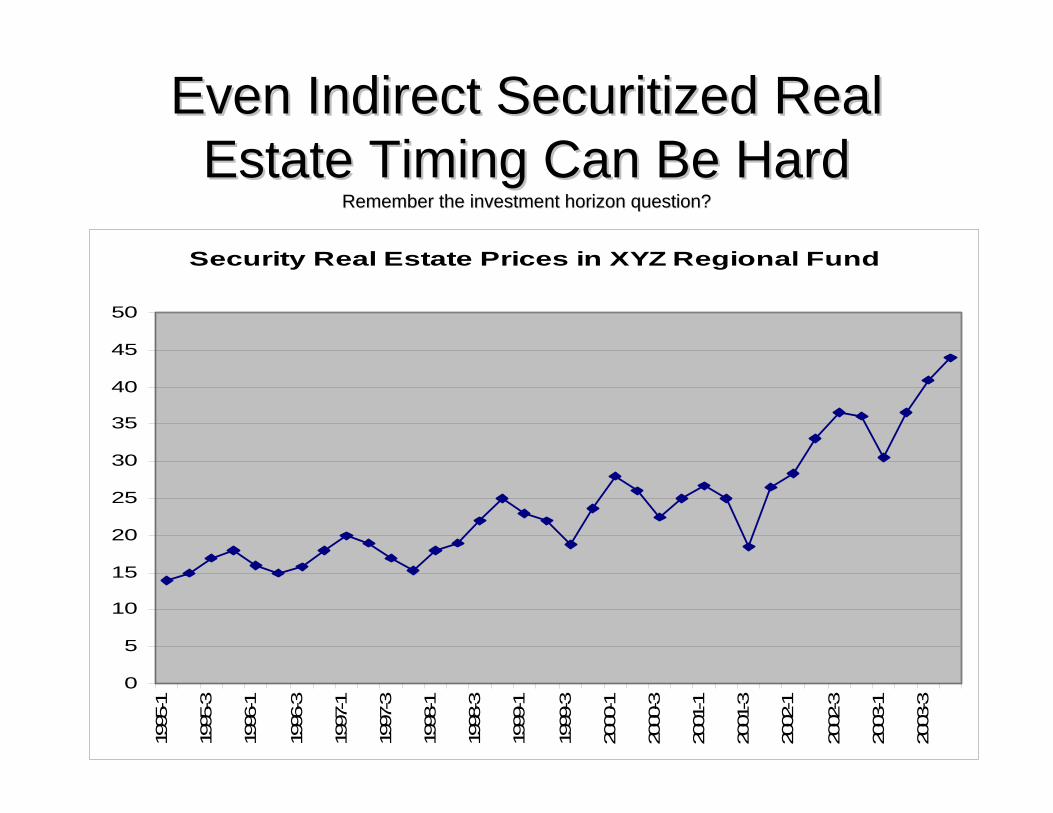

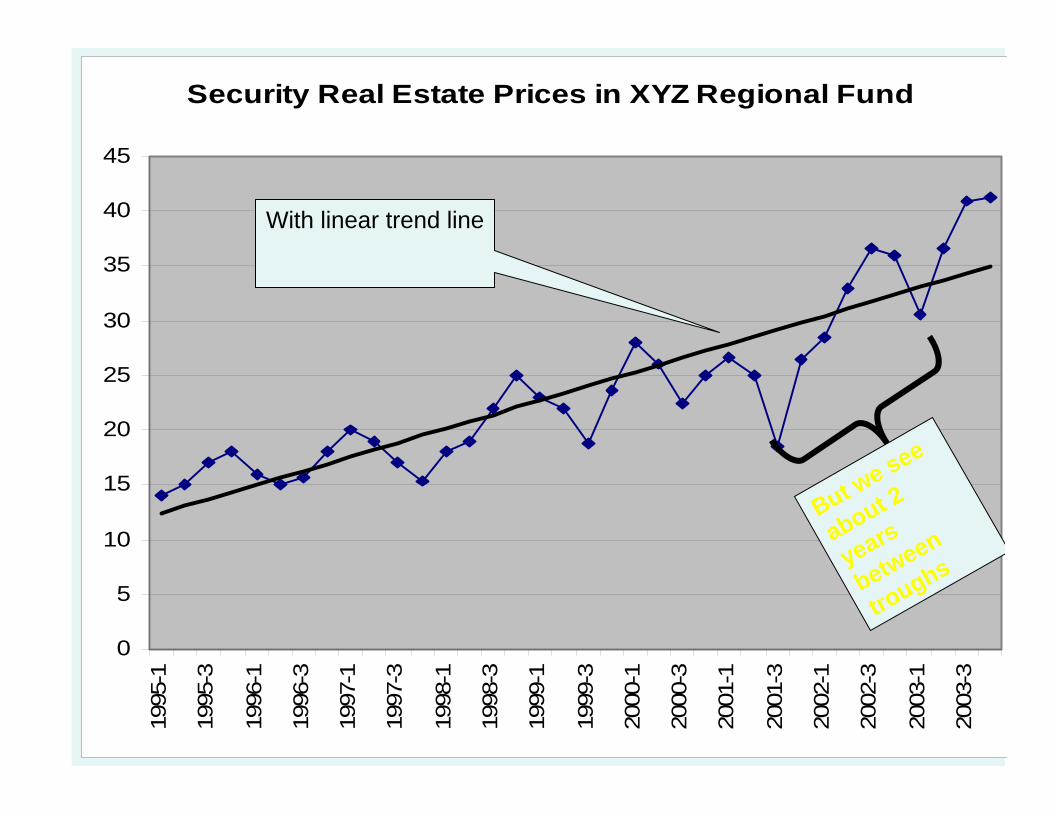

Even Indirect Securitized Real Even Indirect Securitized Real Estate Timing Can Be HardEstate Timing Can Be Hard

Remember the investment horizon question?Remember the investment horizon question?

Security Real Estate Prices in XYZ Regional Fund

0

5

10

15

20

25

30

35

40

45

50

1995

-1

1995

-3

1996

-1

1996

-3

1997

-1

1997

-3

1998

-1

1998

-3

1999

-1

1999

-3

2000

-1

2000

-3

2001

-1

2001

-3

2002

-1

2002

-3

2003

-1

2003

-3

Security Real Estate Prices in XYZ Regional Fund

0

5

10

15

20

25

30

35

40

4519

95-1

1995

-3

1996

-1

1996

-3

1997

-1

1997

-3

1998

-1

1998

-3

1999

-1

1999

-3

2000

-1

2000

-3

2001

-1

2001

-3

2002

-1

2002

-3

2003

-1

2003

-3

With linear trend line

But we see

about 2

years

between

troughs

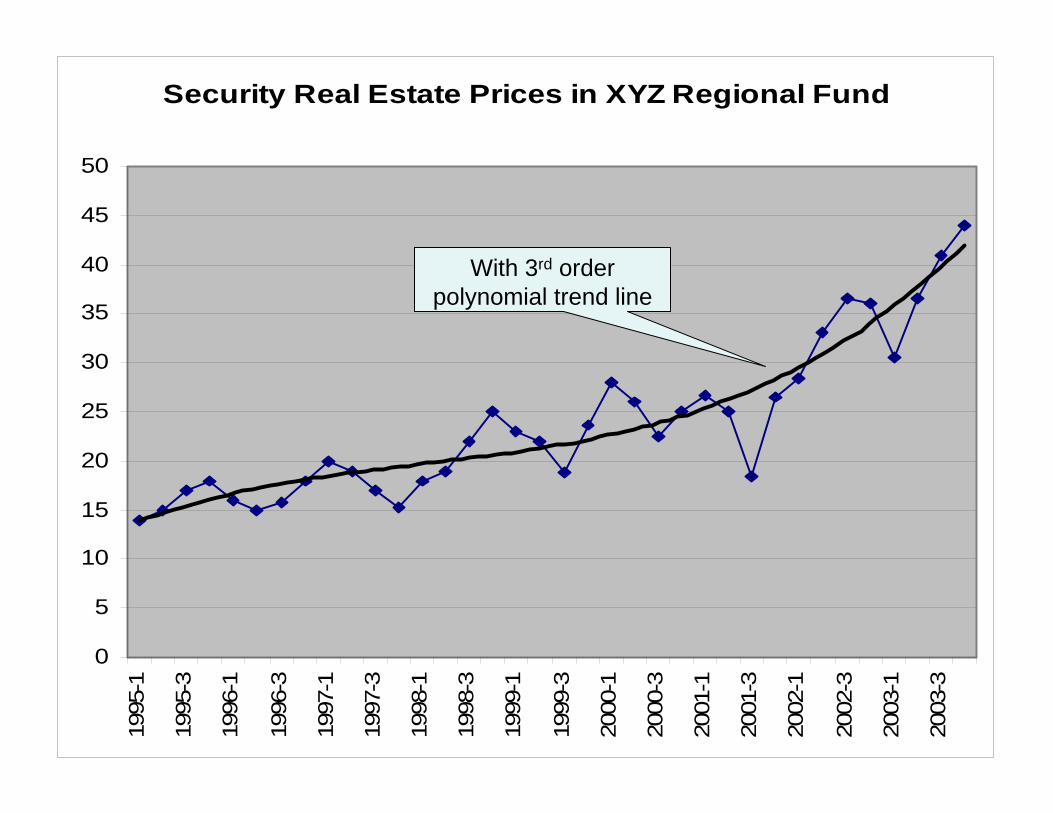

Security Real Estate Prices in XYZ Regional Fund

0

5

10

15

20

25

30

35

40

45

5019

95-1

1995

-3

1996

-1

1996

-3

1997

-1

1997

-3

1998

-1

1998

-3

1999

-1

1999

-3

2000

-1

2000

-3

2001

-1

2001

-3

2002

-1

2002

-3

2003

-1

2003

-3

With 3rd order polynomial trend line

80% of the deals turn out good

80% of the deals turn out worse then expected

The Probabilities of Deal Success The Probabilities of Deal Success with Cycleswith Cycles

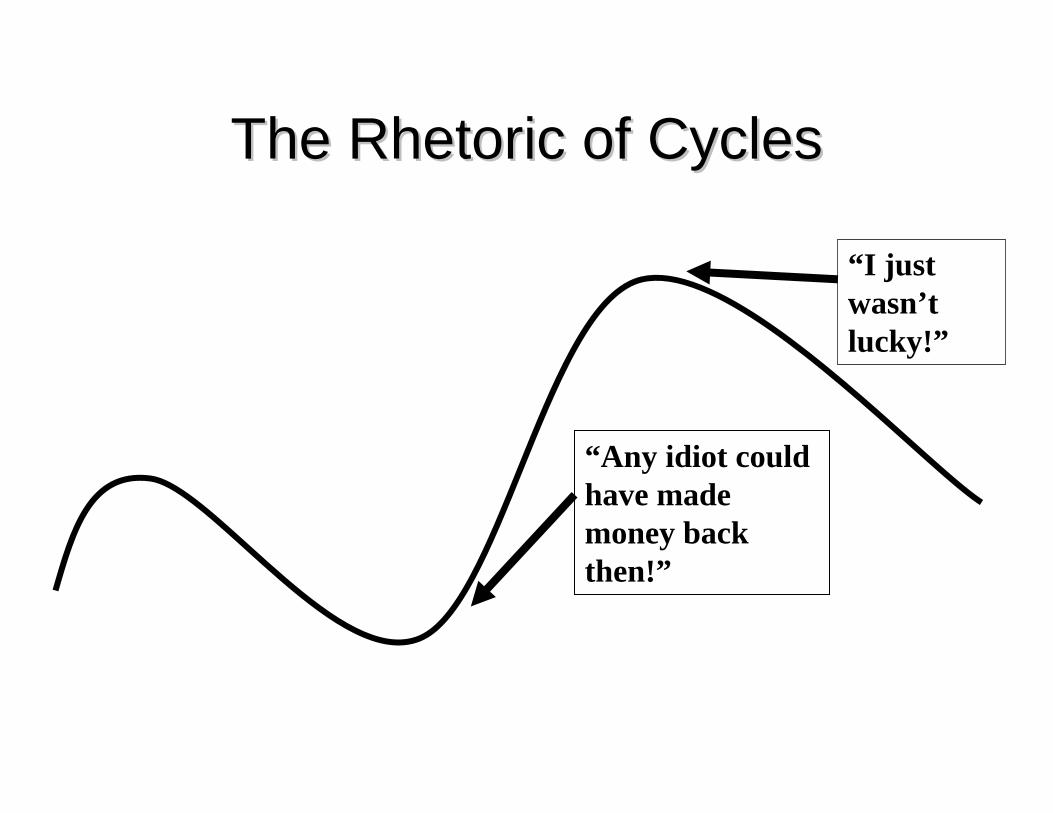

“Any idiot could have made money back then!”

“I just wasn’t lucky!”

The Rhetoric of CyclesThe Rhetoric of Cycles

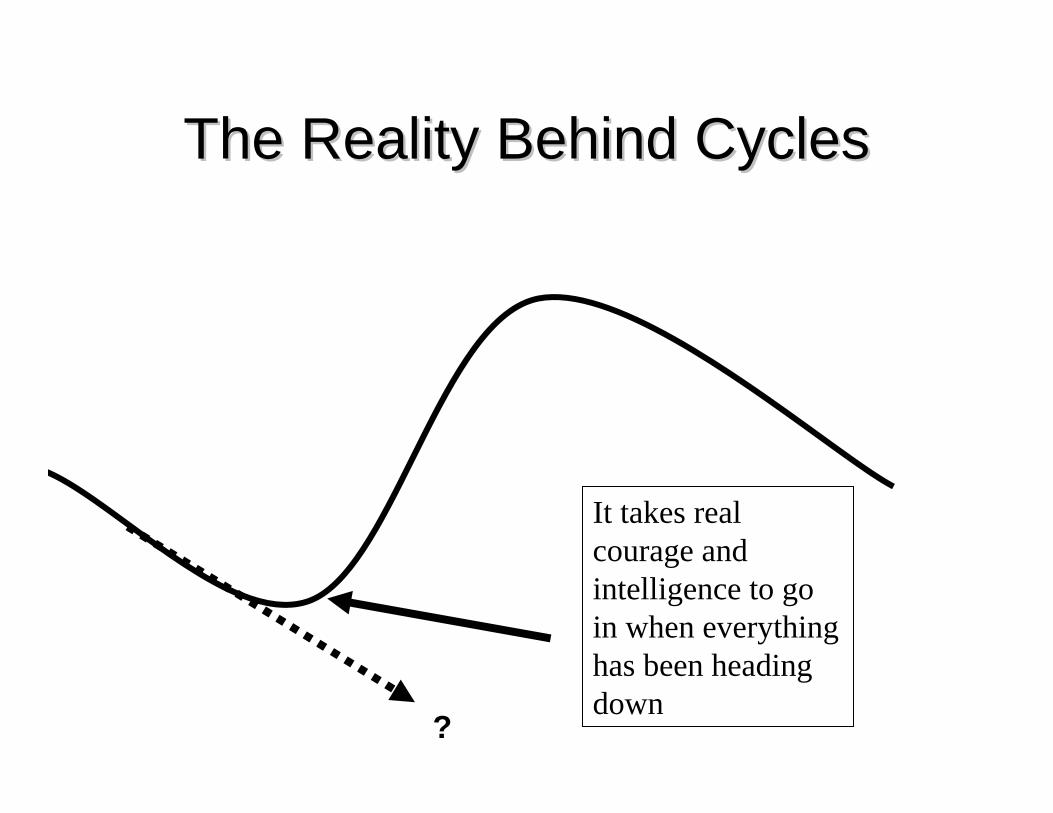

It takes real courage and intelligence to go in when everything has been heading down

The Reality Behind CyclesThe Reality Behind Cycles

?

How to go global?How to go global?Direct?Direct?–– Most big investment managers have a study Most big investment managers have a study

that shows the benefits of going global and they that shows the benefits of going global and they have a plan ready to show how they can put have a plan ready to show how they can put your money to work. All of them have no your money to work. All of them have no doubts about the benefits of going global.doubts about the benefits of going global.

–– We will look at some of their work in a moment.We will look at some of their work in a moment.

How to go global?How to go global?

Indirect? (Public securities)Indirect? (Public securities)––We did not have enough product until We did not have enough product until

recently to consider this question. recently to consider this question. And if you are in the US you must be willing to And if you are in the US you must be willing to ignore US return history and explain it away to ignore US return history and explain it away to want to go direct based on recent US real want to go direct based on recent US real estate performance…..estate performance…..

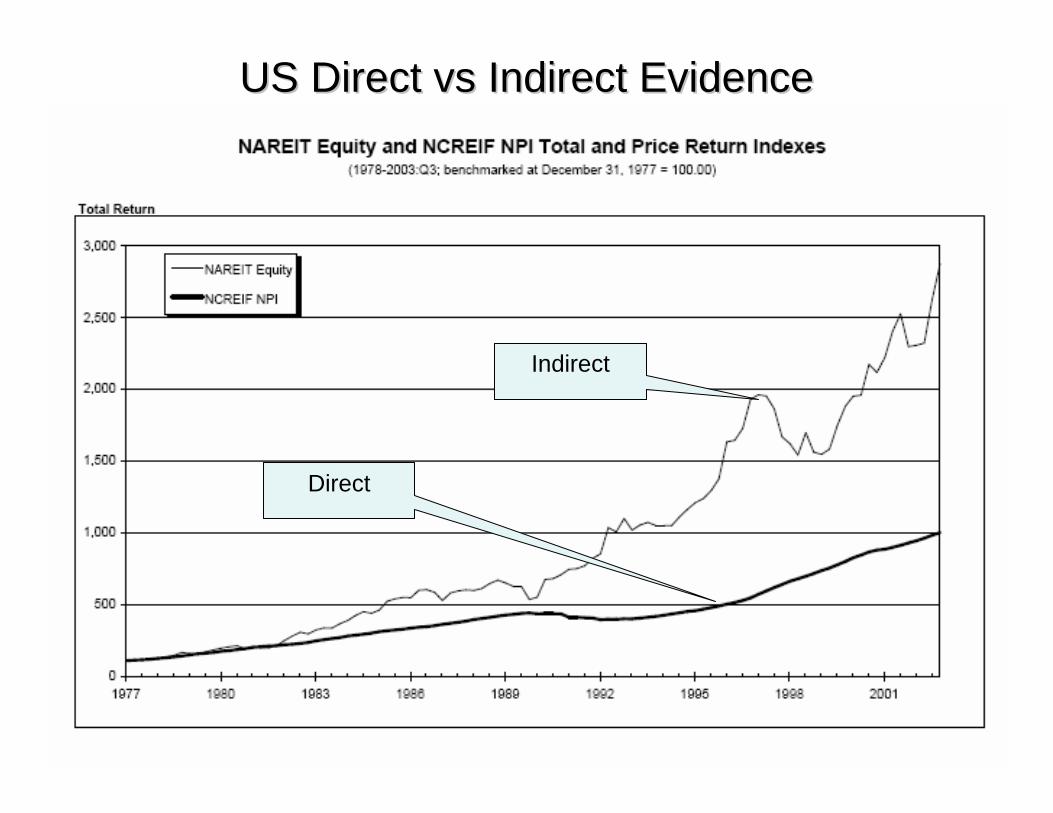

US Direct US Direct vsvs Indirect EvidenceIndirect Evidence

Direct

Indirect

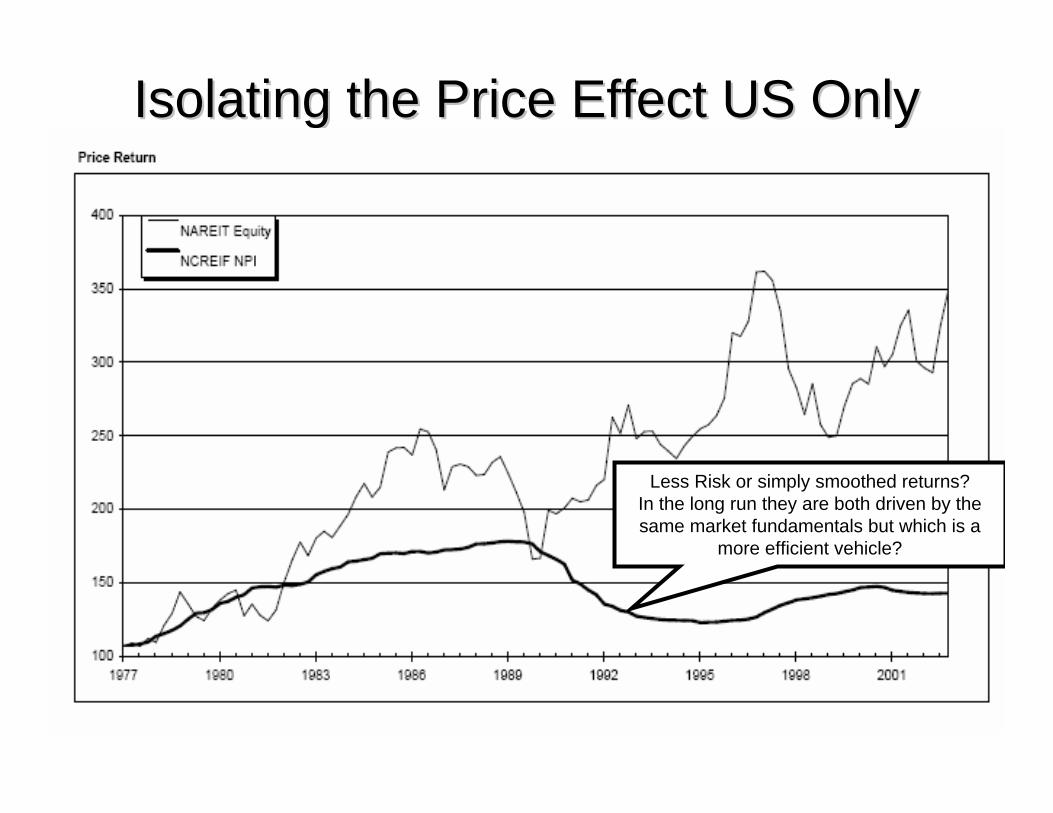

Isolating the Price Effect US OnlyIsolating the Price Effect US OnlyThrough 3Through 3rdrd Qtr 2003Qtr 2003

Less Risk or simply smoothed returns? In the long run they are both driven by the same market fundamentals but which is a

more efficient vehicle?

Going Global With Advice From:Going Global With Advice From:Global Henderson (London based)Global Henderson (London based)Prudential (NY/NJ Based)Prudential (NY/NJ Based)DB (RREEF) German and USDB (RREEF) German and USStrazsheimStrazsheim Global Advisors (CA US)Global Advisors (CA US)Jones Lang LaSalleJones Lang LaSalleEach approach will be briefly examinedEach approach will be briefly examinedMost rely heavily on GDP growth as the key Most rely heavily on GDP growth as the key variable variable –– of course supply should matter as well of course supply should matter as well ––but we do not have such data readily available but we do not have such data readily available except at the very local level.except at the very local level.

Going Global with Global HendersonGoing Global with Global Henderson

Use GDP driven rent forecasts and 6 risk Use GDP driven rent forecasts and 6 risk criteria: criteria: –– Default risk, legal risk, political (currency risk Default risk, legal risk, political (currency risk

and inflation), liquidity risk, and market and inflation), liquidity risk, and market transparency to devise risk premiums for transparency to devise risk premiums for foreign investors.foreign investors.

–– Selected risk premiums are shown on the Selected risk premiums are shown on the next slide.next slide.

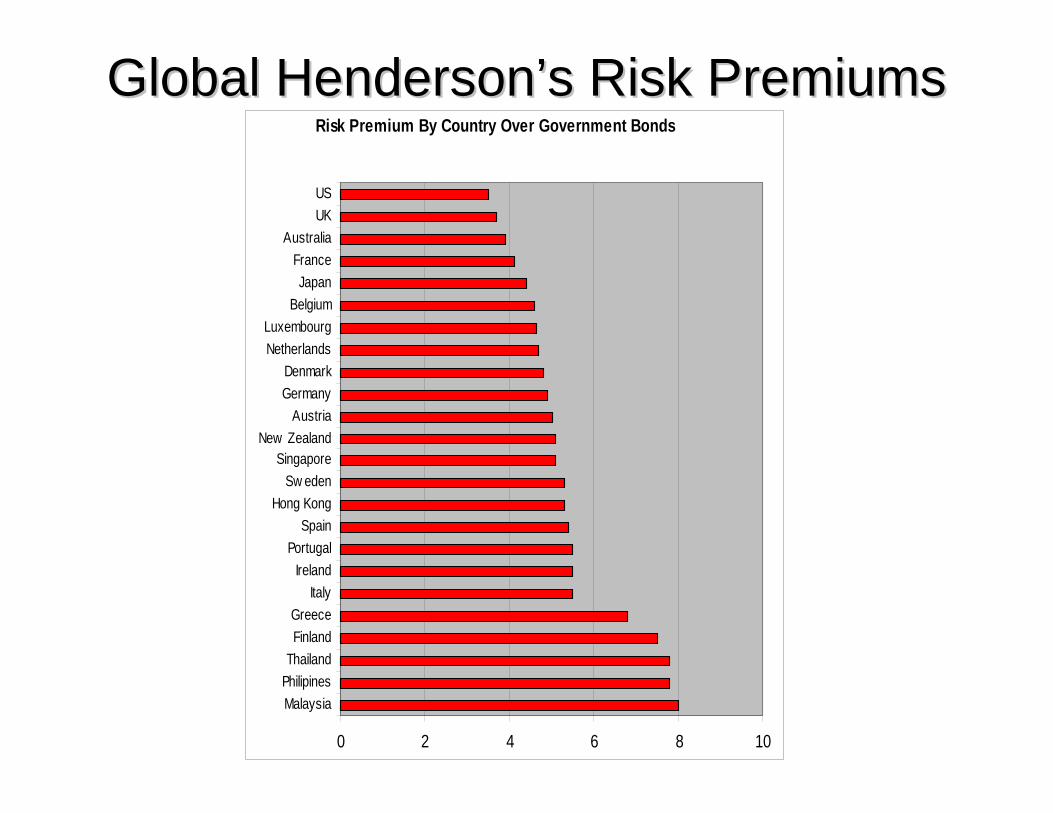

Global Henderson’s Risk PremiumsGlobal Henderson’s Risk PremiumsRisk Premium By Country Over Government Bonds

0 2 4 6 8 10

MalaysiaPhilipinesThailandFinlandGreece

ItalyIreland

PortugalSpain

Hong KongSw eden

SingaporeNew Zealand

AustriaGermanyDenmark

NetherlandsLuxembourg

BelgiumJapan

FranceAustralia

UKUS

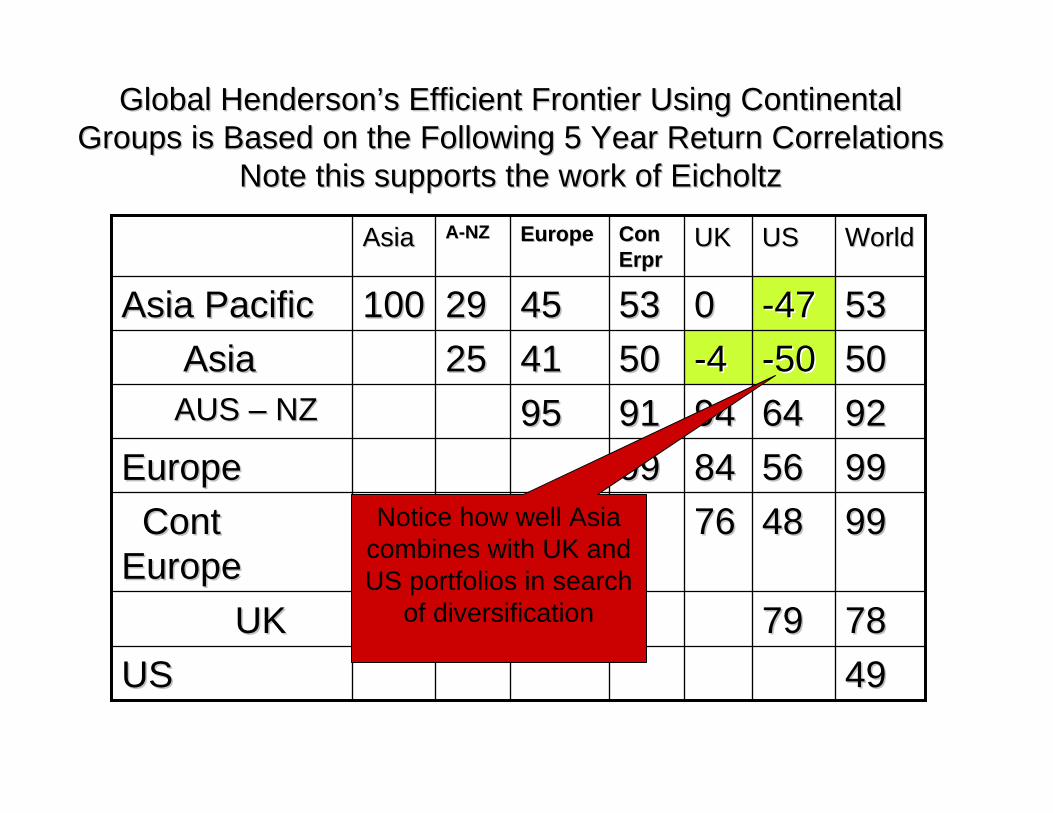

Global Henderson’s Efficient Frontier Using Continental Global Henderson’s Efficient Frontier Using Continental Groups is Based on the Following 5 Year Return CorrelationsGroups is Based on the Following 5 Year Return Correlations

Note this supports the work of Note this supports the work of EicholtzEicholtz

4949USUS78787979UKUK

999948487676Cont Cont EuropeEurope

9999565684849999EuropeEurope92926464949491919595AUS AUS –– NZNZ5050--5050--44505041412525AsiaAsia5353--474700535345452929100100Asia PacificAsia Pacific

WorldWorldUSUSUKUKCon Con ErprErpr

EuropeEuropeAA--NZNZAsiaAsia

Notice how well Asia combines with UK and US portfolios in search

of diversification

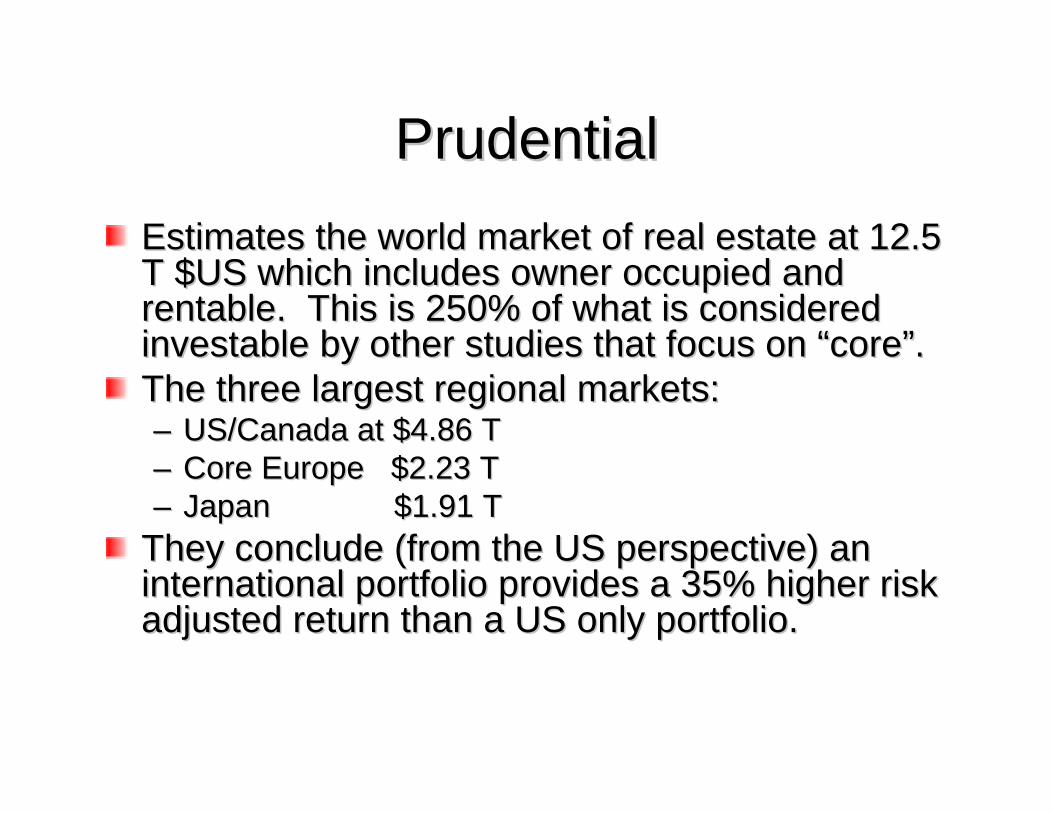

Prudential Prudential Estimates the world market of real estate at 12.5 Estimates the world market of real estate at 12.5 T $US which includes owner occupied and T $US which includes owner occupied and rentable. This is 250% of what is considered rentable. This is 250% of what is considered investableinvestable by other studies that focus on “core”. by other studies that focus on “core”. The three largest regional markets:The three largest regional markets:–– US/Canada at $4.86 TUS/Canada at $4.86 T–– Core Europe $2.23 TCore Europe $2.23 T–– JapanJapan $1.91 T $1.91 T

They conclude (from the US perspective) an They conclude (from the US perspective) an international portfolio provides a 35% higher risk international portfolio provides a 35% higher risk adjusted return than a US only portfolio.adjusted return than a US only portfolio.

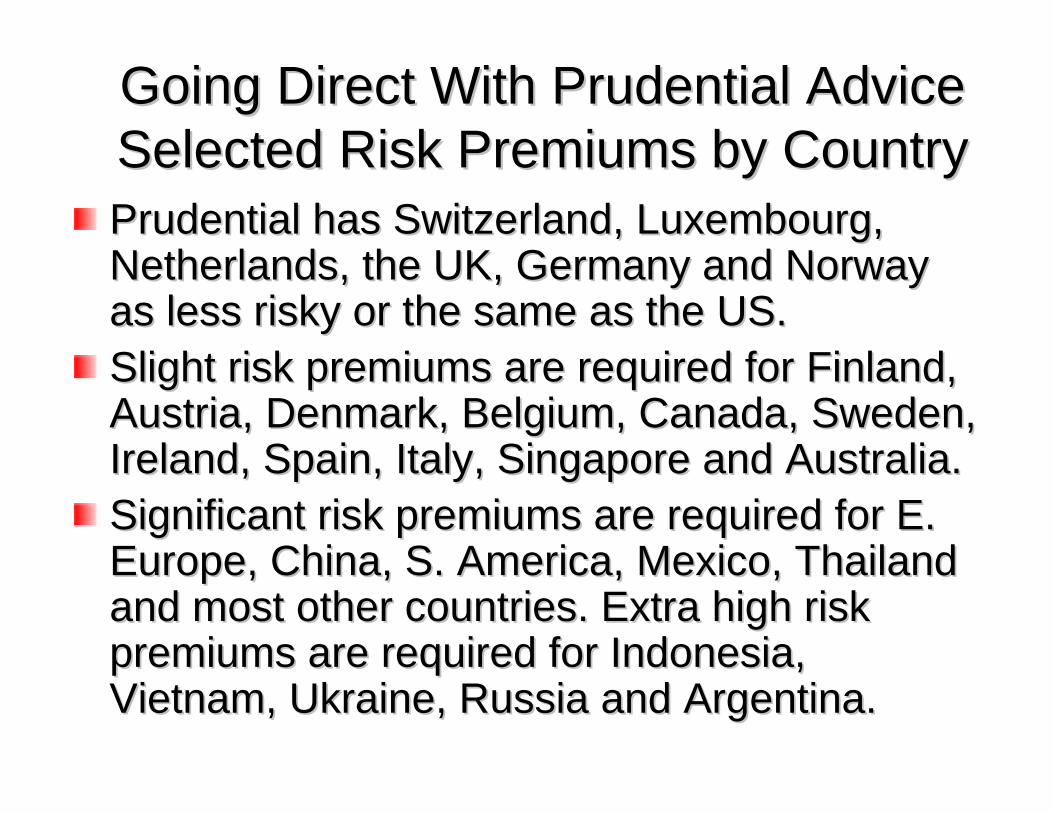

Going Direct With Prudential AdviceGoing Direct With Prudential AdviceSelected Risk Premiums by CountrySelected Risk Premiums by CountryPrudential has Switzerland, Luxembourg, Prudential has Switzerland, Luxembourg, Netherlands, the UK, Germany and Norway Netherlands, the UK, Germany and Norway as less risky or the same as the US.as less risky or the same as the US.Slight risk premiums are required for Finland, Slight risk premiums are required for Finland, Austria, Denmark, Belgium, Canada, Sweden, Austria, Denmark, Belgium, Canada, Sweden, Ireland, Spain, Italy, Singapore and Australia. Ireland, Spain, Italy, Singapore and Australia. Significant risk premiums are required for E. Significant risk premiums are required for E. Europe, China, S. America, Mexico, Thailand Europe, China, S. America, Mexico, Thailand and most other countries. Extra high risk and most other countries. Extra high risk premiums are required for Indonesia, premiums are required for Indonesia, Vietnam, Ukraine, Russia and Argentina.Vietnam, Ukraine, Russia and Argentina.

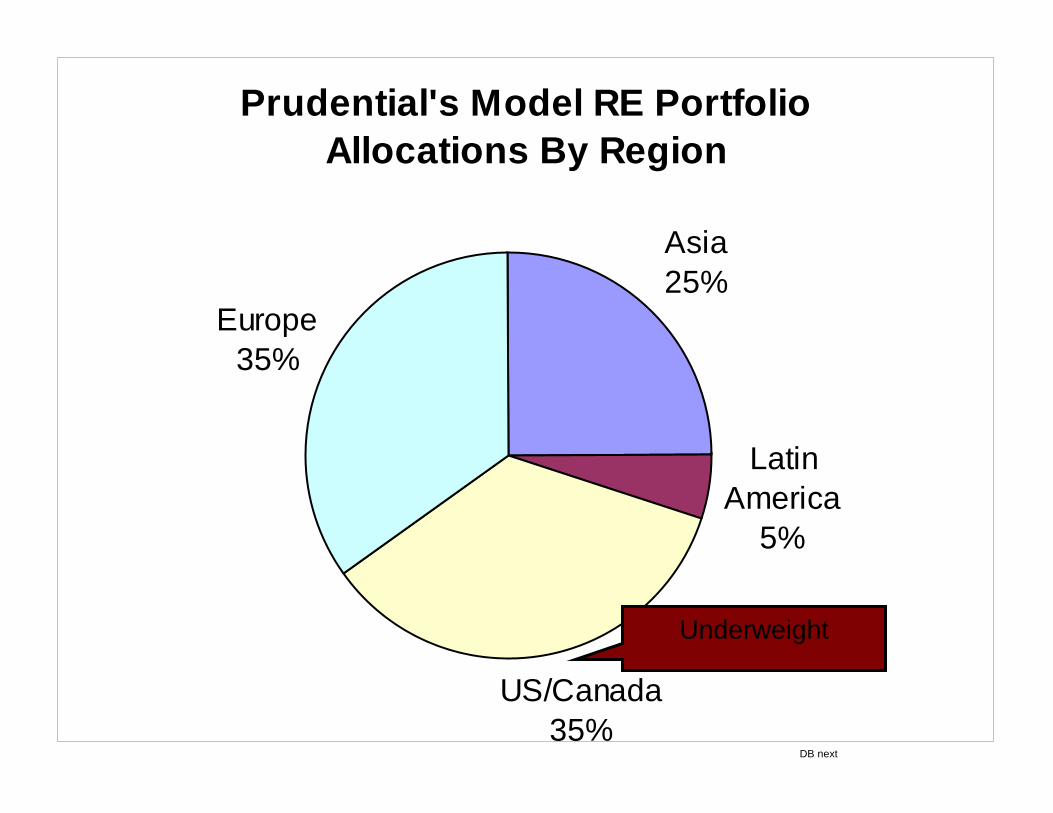

Prudential's Model RE Portfolio Allocations By Region

Asia25%

Latin America

5%

US/Canada35%

Europe35%

Underweight

DB next

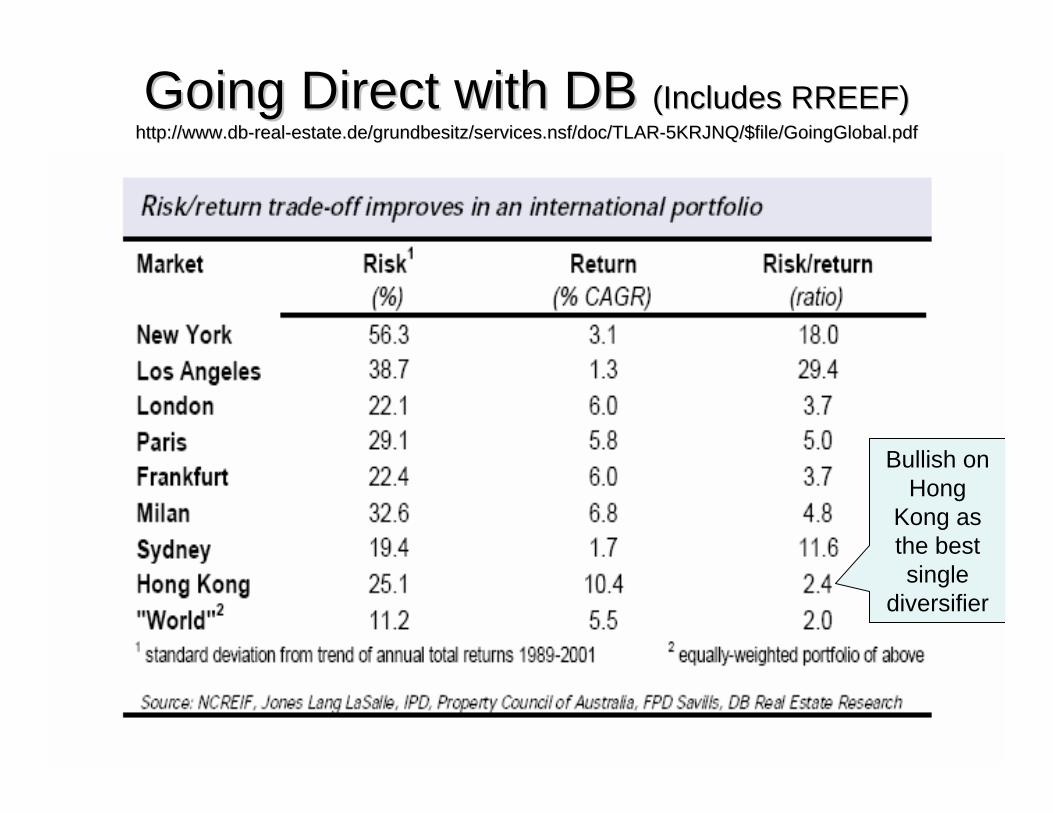

Going Direct with DB Going Direct with DB (Includes RREEF)(Includes RREEF)http://www.dbhttp://www.db--realreal--estate.de/grundbesitz/services.nsf/doc/TLARestate.de/grundbesitz/services.nsf/doc/TLAR--5KRJNQ/$file/GoingGlobal.pdf5KRJNQ/$file/GoingGlobal.pdf

Bullish on Hong

Kong as the best single

diversifier

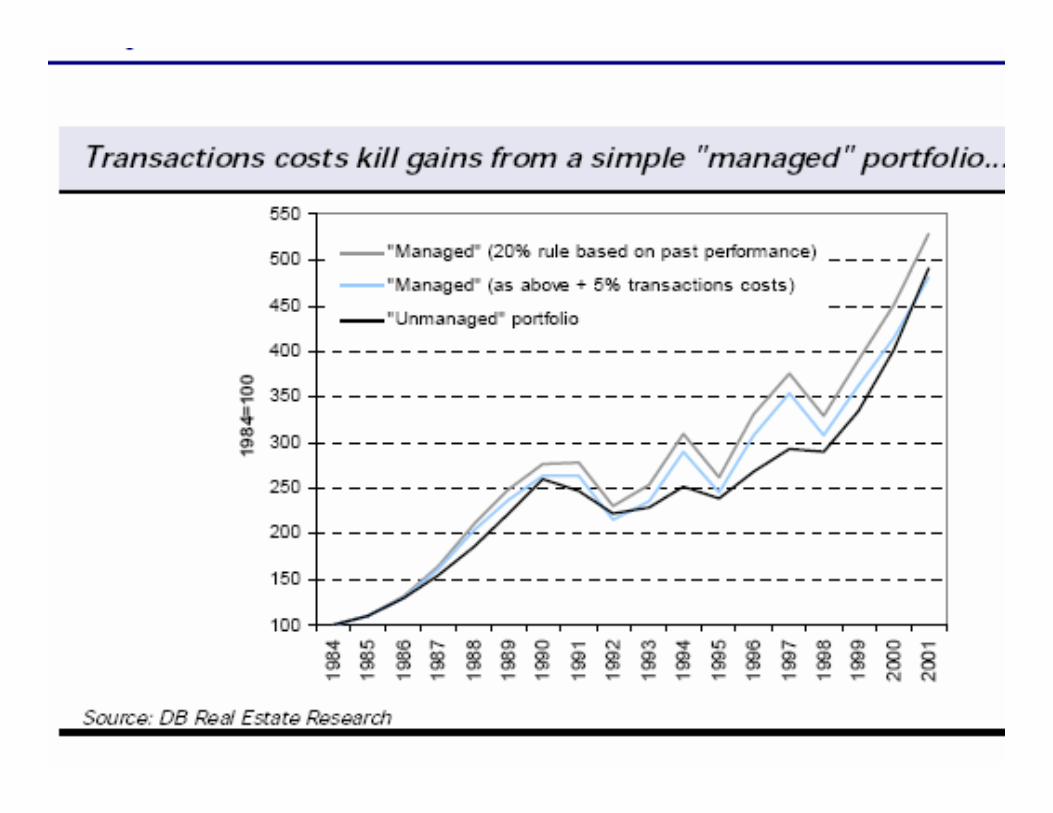

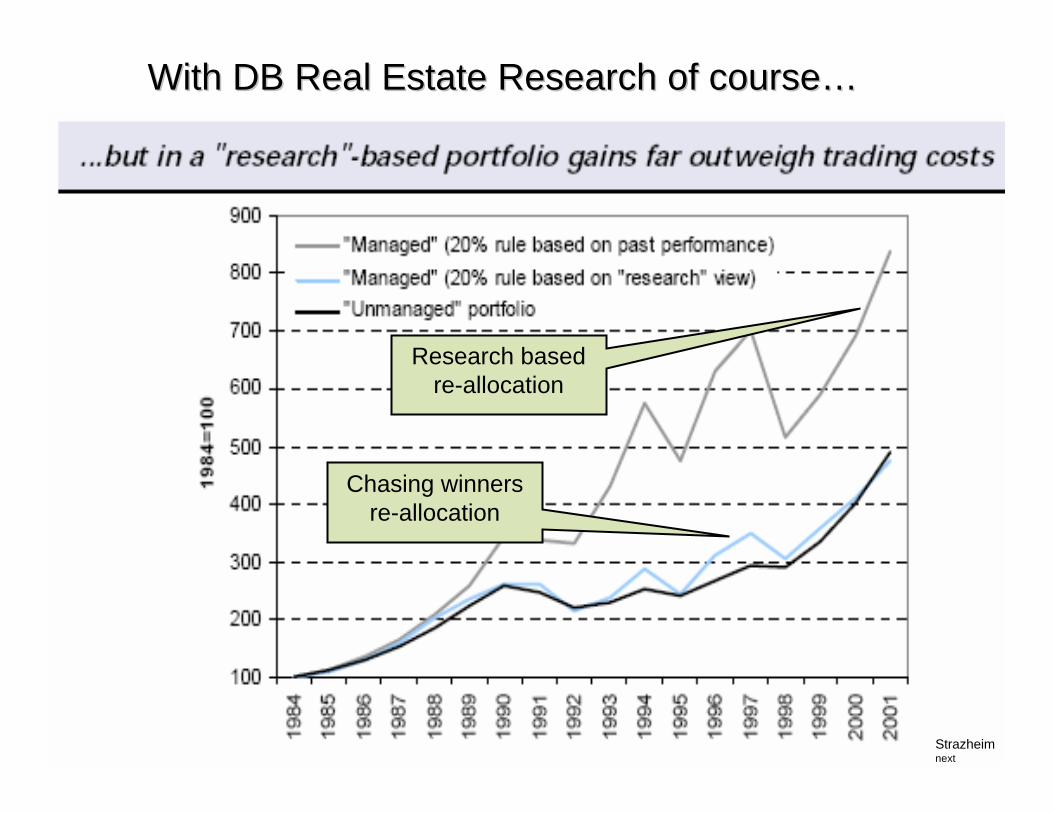

With DB Real Estate Research of course…With DB Real Estate Research of course…

Research based re-allocation

Chasing winners re-allocation

Strazheimnext

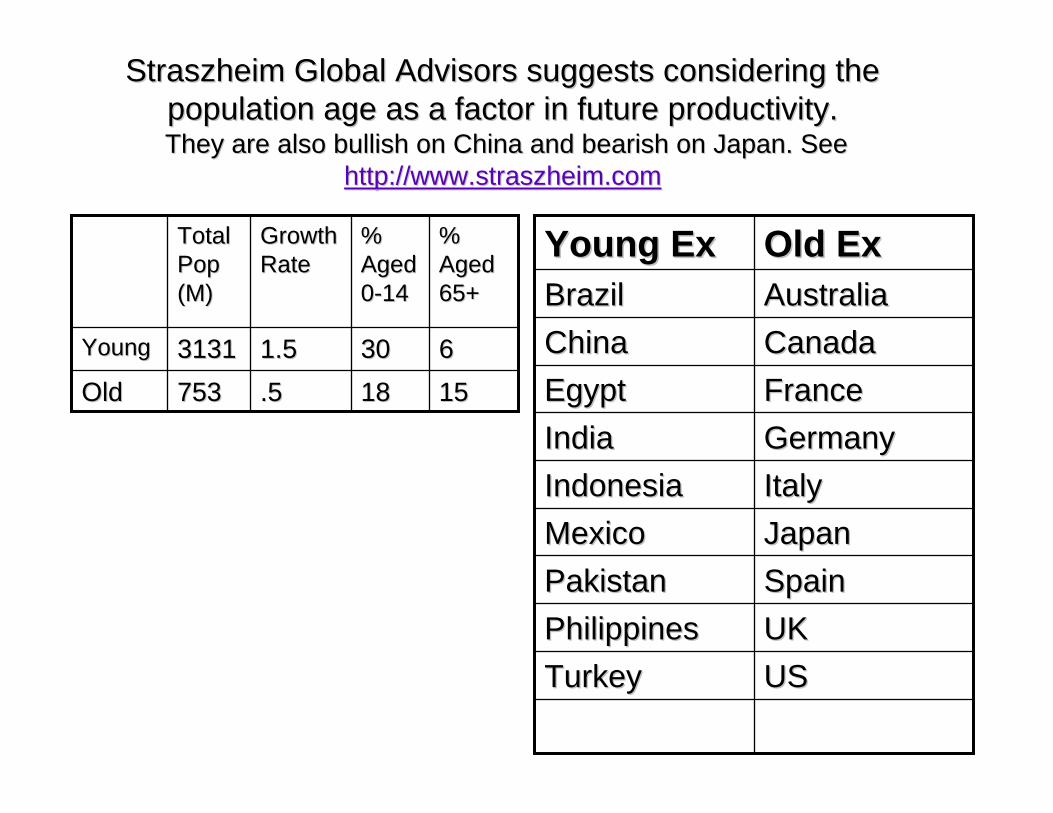

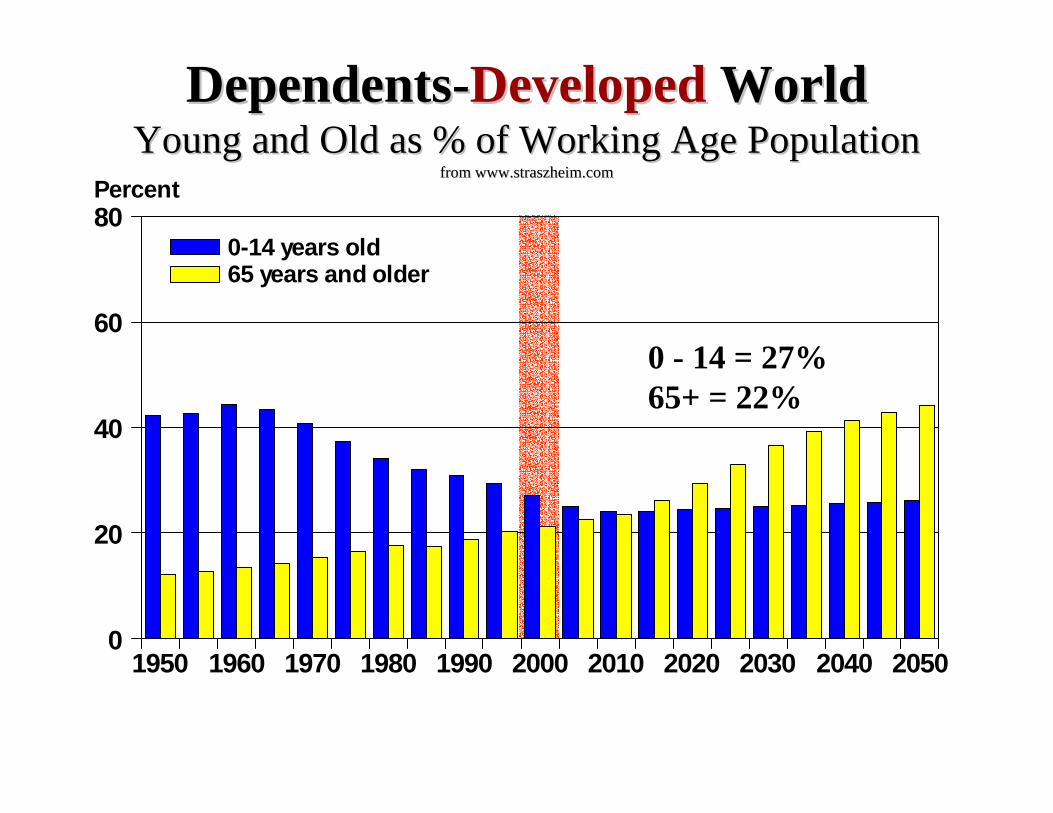

StraszheimStraszheim Global Advisors suggests considering the Global Advisors suggests considering the population age as a factor in future productivity.population age as a factor in future productivity.They are also bullish on China and bearish on Japan. See They are also bullish on China and bearish on Japan. See

http://www.straszheim.comhttp://www.straszheim.com

15151818.5.5753753OldOld6630301.51.531313131YoungYoung

% % Aged Aged 65+65+

% % Aged Aged 00--1414

Growth Growth RateRate

Total Total Pop Pop (M)(M)

USUSTurkeyTurkeyUKUKPhilippinesPhilippinesSpainSpainPakistanPakistanJapanJapanMexicoMexicoItalyItalyIndonesiaIndonesiaGermanyGermanyIndiaIndiaFranceFranceEgyptEgyptCanadaCanadaChinaChinaAustraliaAustraliaBrazilBrazilOld ExOld ExYoung ExYoung Ex

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent

0-14 years old65 years and older

0 -14 = 51%65+ = 8%

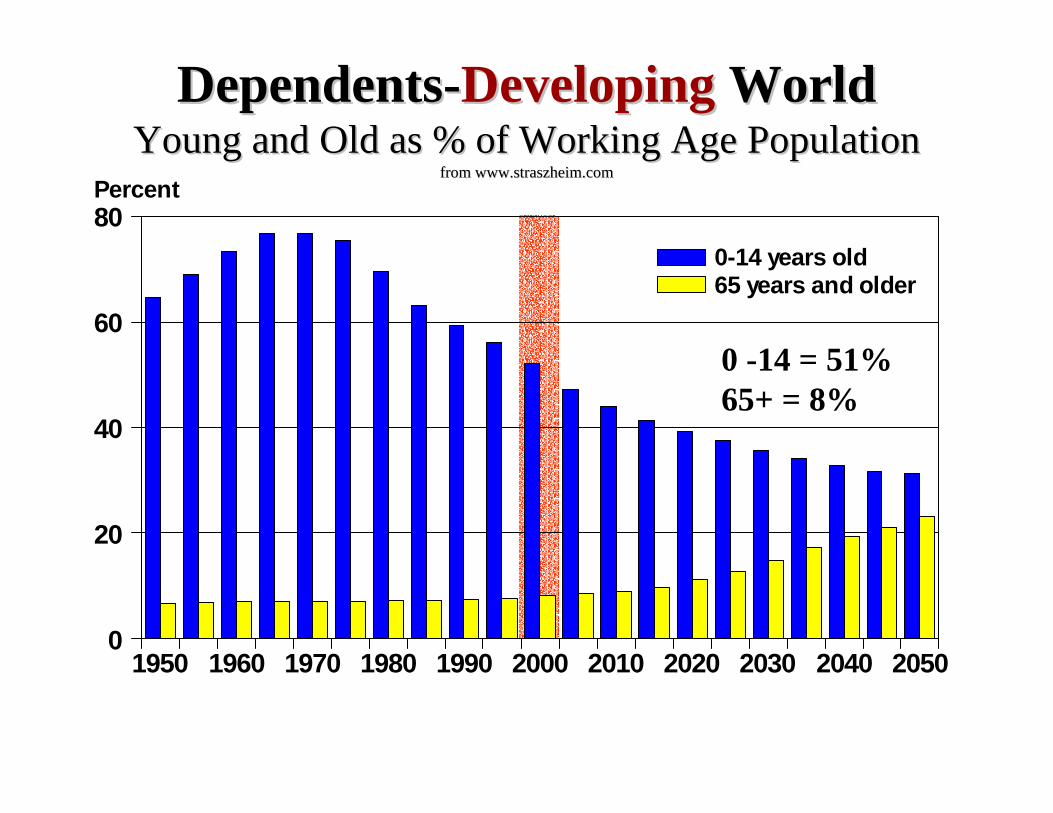

DependentsDependents--DevelopingDeveloping WorldWorldYoung and Old as % of Working Age PopulationYoung and Old as % of Working Age Population

from from www.straszheim.comwww.straszheim.com

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent

0-14 years old65 years and older

0 - 14 = 27%65+ = 22%

DependentsDependents--DevelopedDeveloped WorldWorldYoung and Old as % of Working Age PopulationYoung and Old as % of Working Age Population

from from www.straszheim.comwww.straszheim.com

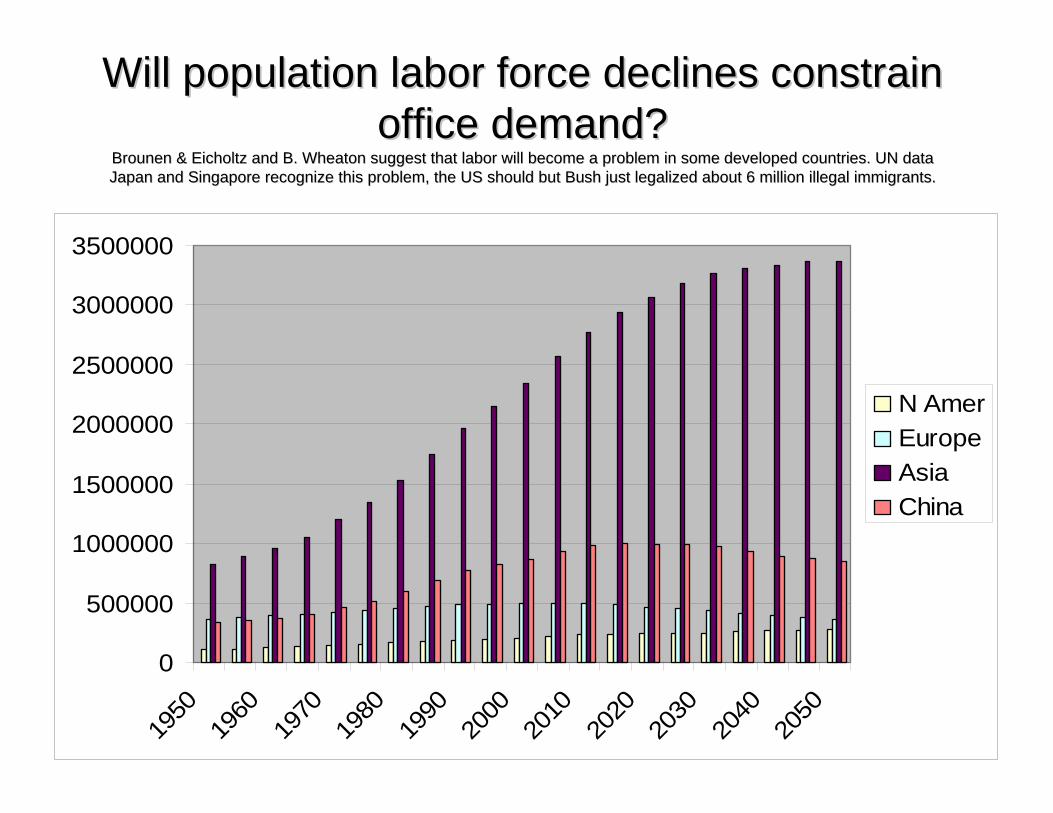

Will population labor force declines constrain Will population labor force declines constrain office demand?office demand?

BrounenBrounen & & EicholtzEicholtz and B. Wheaton suggest that labor will become a problem in someand B. Wheaton suggest that labor will become a problem in some developed countries. UN datadeveloped countries. UN dataJapan and Singapore recognize this problem, the US should but BuJapan and Singapore recognize this problem, the US should but Bush just legalized about 6 million illegal immigrants.sh just legalized about 6 million illegal immigrants.

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

N AmerEuropeAsiaChina

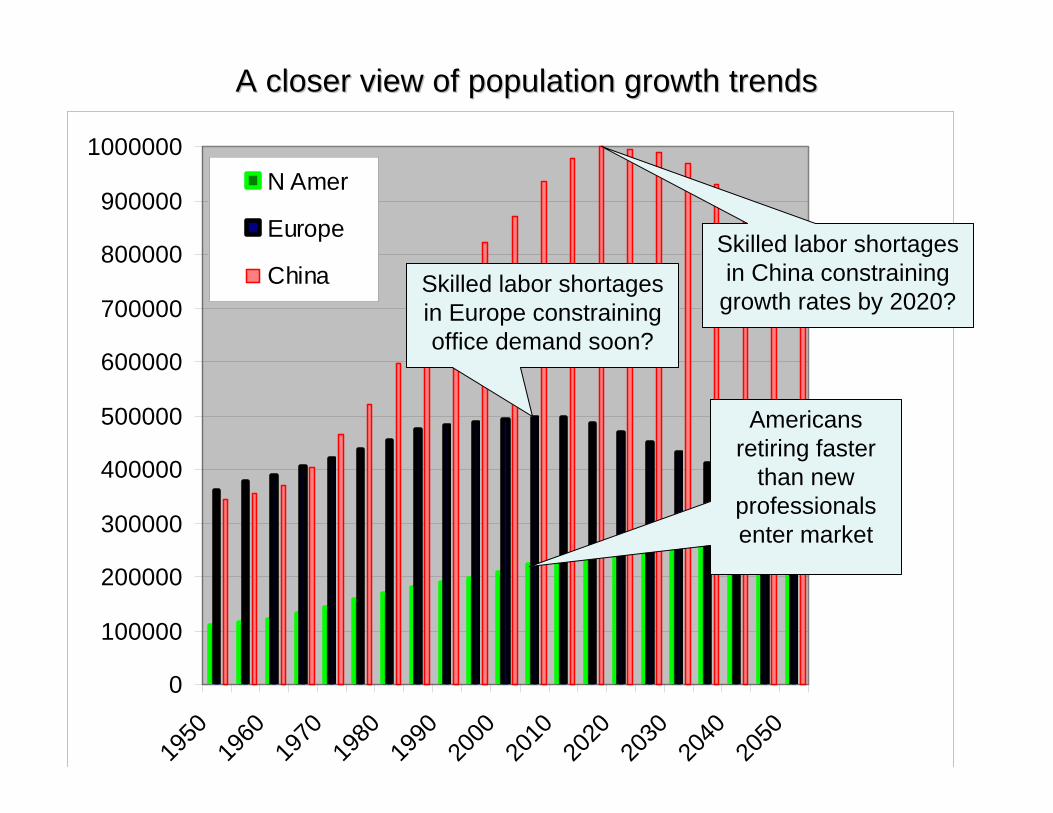

A closer view of population growth trendsA closer view of population growth trends

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

N Amer

Europe

China Skilled labor shortages in Europe constraining office demand soon?

Skilled labor shortages in China constraining growth rates by 2020?

Americans retiring faster

than new professionals enter market

Who looks out to 2020 anyway?Who looks out to 2020 anyway?

So let’s assume you are convinced So let’s assume you are convinced that there are benefits to that there are benefits to

international real estate investment.international real estate investment.

How about a reality check?How about a reality check?

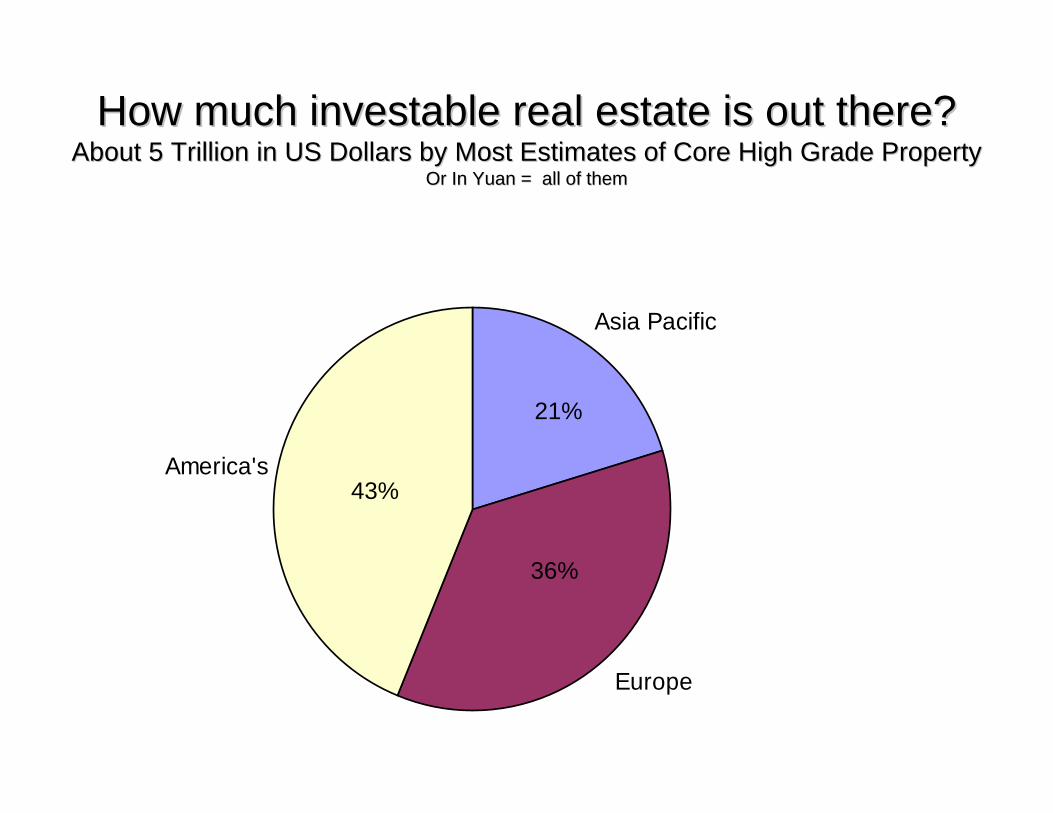

How much How much investableinvestable real estate is out there?real estate is out there?About 5 Trillion in US Dollars by Most Estimates of Core High GrAbout 5 Trillion in US Dollars by Most Estimates of Core High Grade Propertyade Property

Or In Yuan = all of themOr In Yuan = all of them

Asia Pacific

Europe

America's

21%

36%

43%

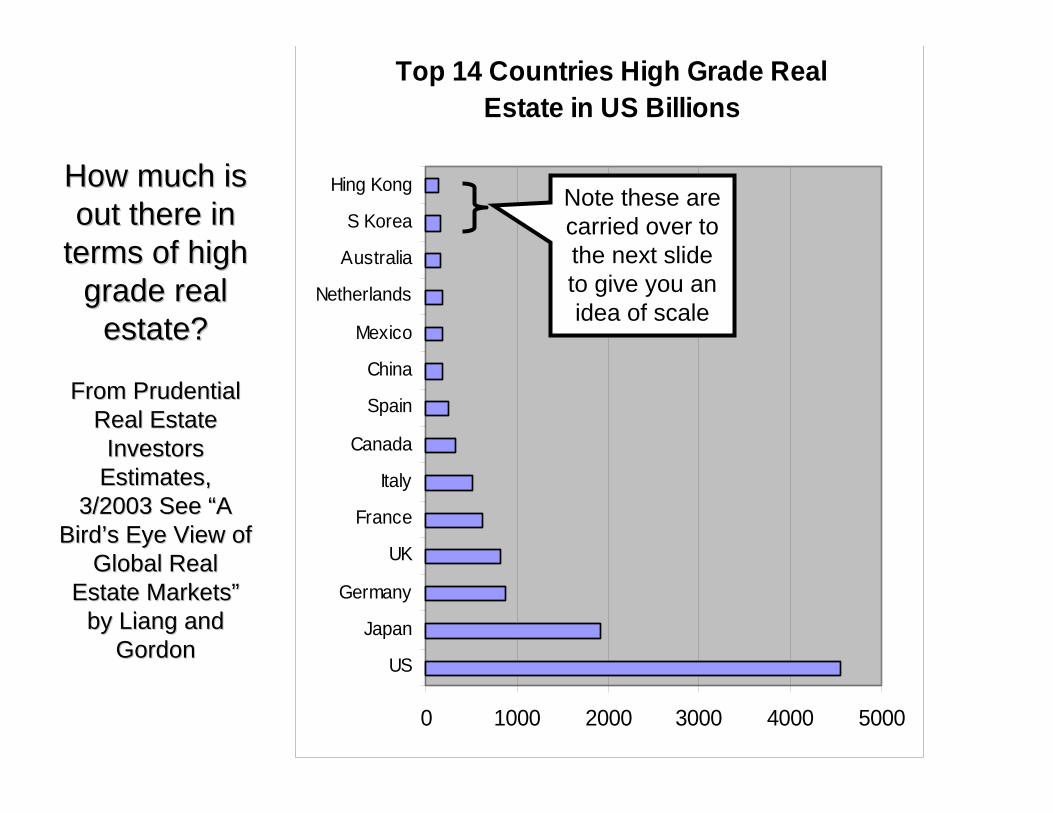

How much is How much is out there in out there in

terms of high terms of high grade real grade real

estate?estate?

From Prudential From Prudential Real Estate Real Estate Investors Investors

Estimates, Estimates, 3/2003 See “A 3/2003 See “A

Bird’s Eye View of Bird’s Eye View of Global Real Global Real

Estate Markets” Estate Markets” by by LiangLiang and and

GordonGordon

Top 14 Countries High Grade Real Estate in US Billions

0 1000 2000 3000 4000 5000

US

Japan

Germany

UK

France

Italy

Canada

Spain

China

Mexico

Netherlands

Australia

S Korea

Hing Kong Note these are carried over to the next slide to give you an idea of scale

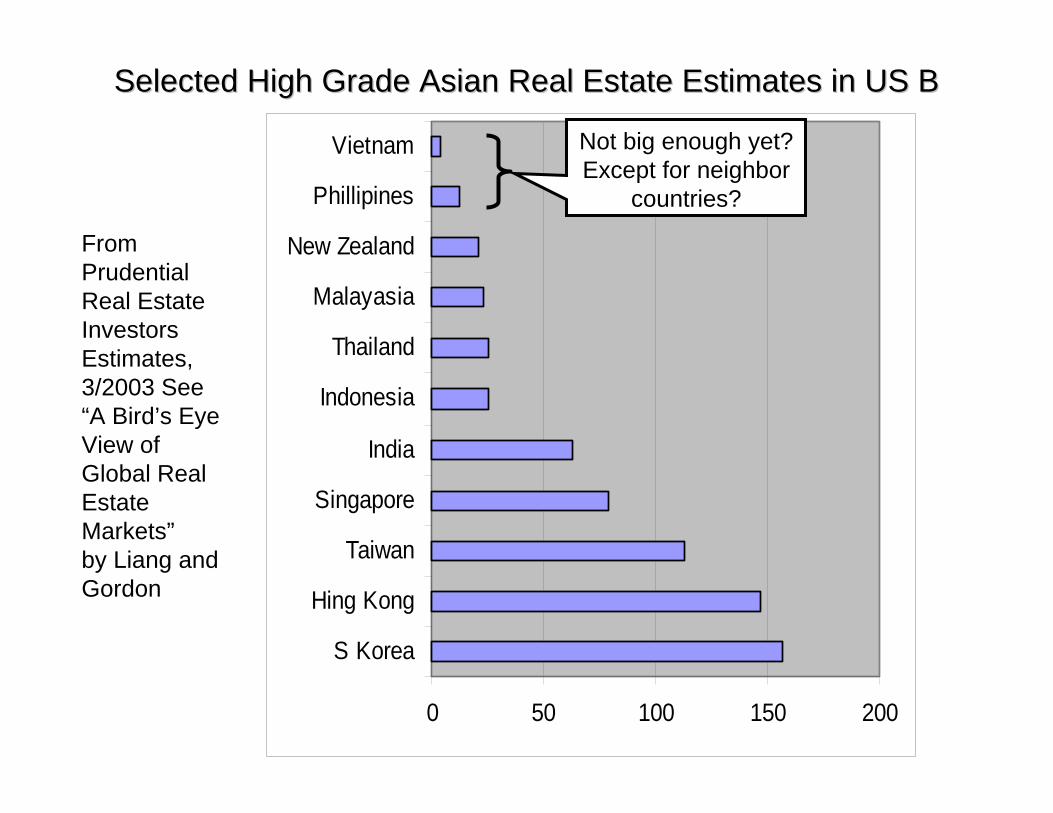

Selected High Grade Asian Real Estate Estimates in US BSelected High Grade Asian Real Estate Estimates in US B

0 50 100 150 200

S Korea

Hing Kong

Taiwan

Singapore

India

Indonesia

Thailand

Malayasia

New Zealand

Phillipines

Vietnam

From Prudential Real Estate Investors Estimates, 3/2003 See “A Bird’s Eye View of Global Real Estate Markets” by Liang and Gordon

Not big enough yet? Except for neighbor

countries?

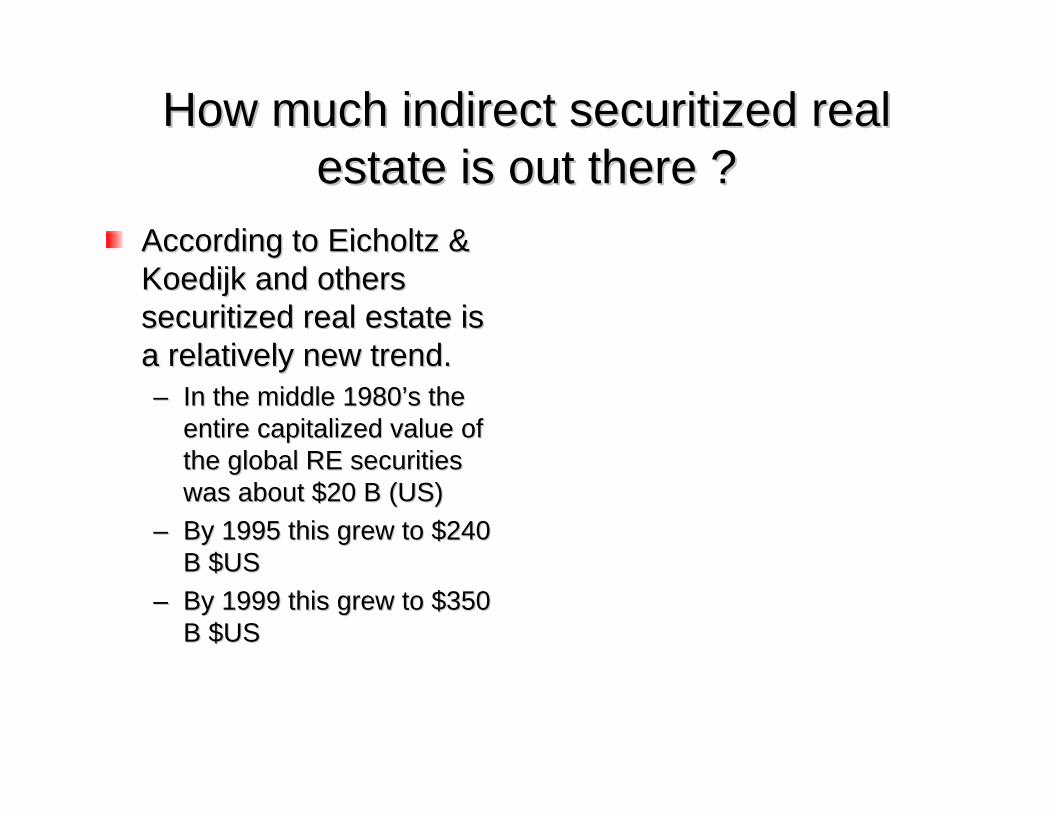

How much indirect securitized real How much indirect securitized real estate is out there ?estate is out there ?

According to According to EicholtzEicholtz & & KoedijkKoedijk and others and others securitized real estate is securitized real estate is a relatively new trend. a relatively new trend. –– In the middle 1980’s the In the middle 1980’s the

entire capitalized value of entire capitalized value of the global RE securities the global RE securities was about $20 B (US) was about $20 B (US)

–– By 1995 this grew to $240 By 1995 this grew to $240 B $USB $US

–– By 1999 this grew to $350 By 1999 this grew to $350 B $US B $US

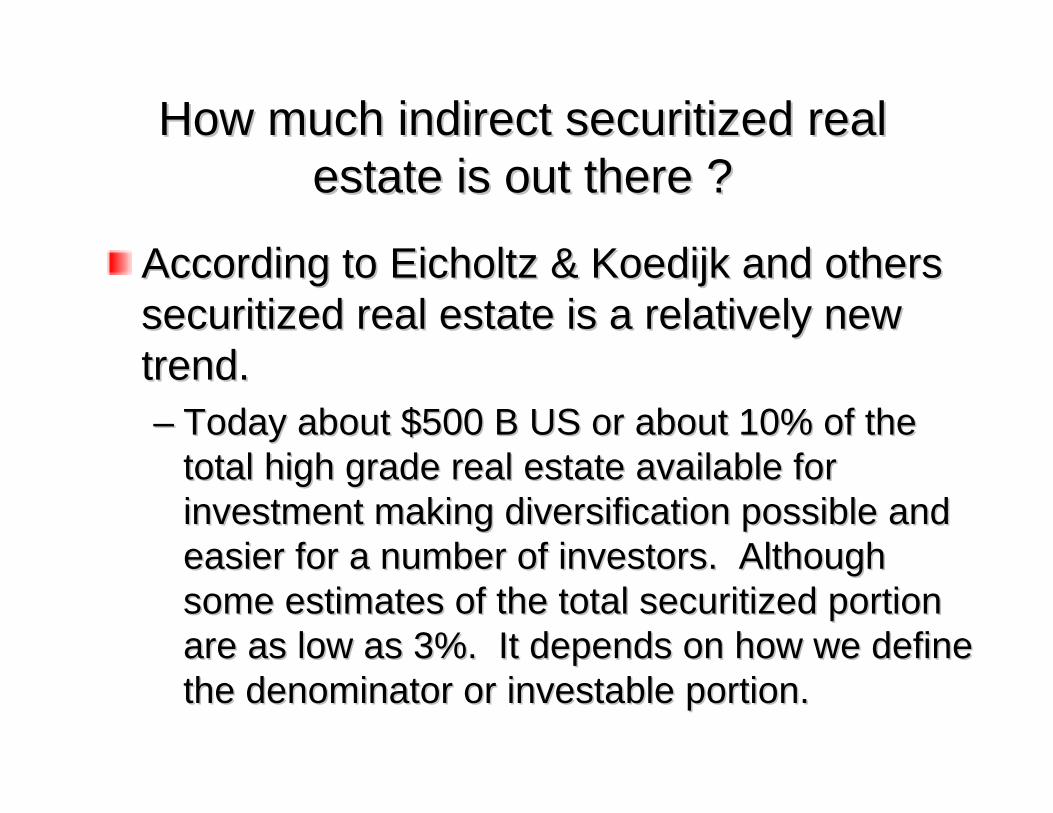

How much indirect securitized real How much indirect securitized real estate is out there ?estate is out there ?

According to According to EicholtzEicholtz & & KoedijkKoedijk and others and others securitized real estate is a relatively new securitized real estate is a relatively new trend. trend. –– Today about $500 B US or about 10% of the Today about $500 B US or about 10% of the

total high grade real estate available for total high grade real estate available for investment making diversification possible and investment making diversification possible and easier for a number of investors. Although easier for a number of investors. Although some estimates of the total securitized portion some estimates of the total securitized portion are as low as 3%. It depends on how we define are as low as 3%. It depends on how we define the denominator or the denominator or investableinvestable portion.portion.

Public or Indirect “Securitized” Real EstatePublic or Indirect “Securitized” Real EstateWhich countries offer Which countries offer REITsREITs (Real estate investment trusts) or REIT(Real estate investment trusts) or REIT--like securities?like securities?

from from www.realestateportfolio.comwww.realestateportfolio.com and Ernst and Youngand Ernst and Young

USUSAustraliaAustraliaBelgiumBelgiumBrazilBrazilCanadaCanadaEuropean Union European Union (proposed)(proposed)FranceFranceGermanyGermanyHong KongHong KongJapanJapan

KoreaKoreaLuxembourgLuxembourgMalaysiaMalaysiaNetherlandsNetherlandsPuerto RicoPuerto RicoSingaporeSingaporeSpainSpainTaiwanTaiwanTurkeyTurkeyOthers will certainly followOthers will certainly follow

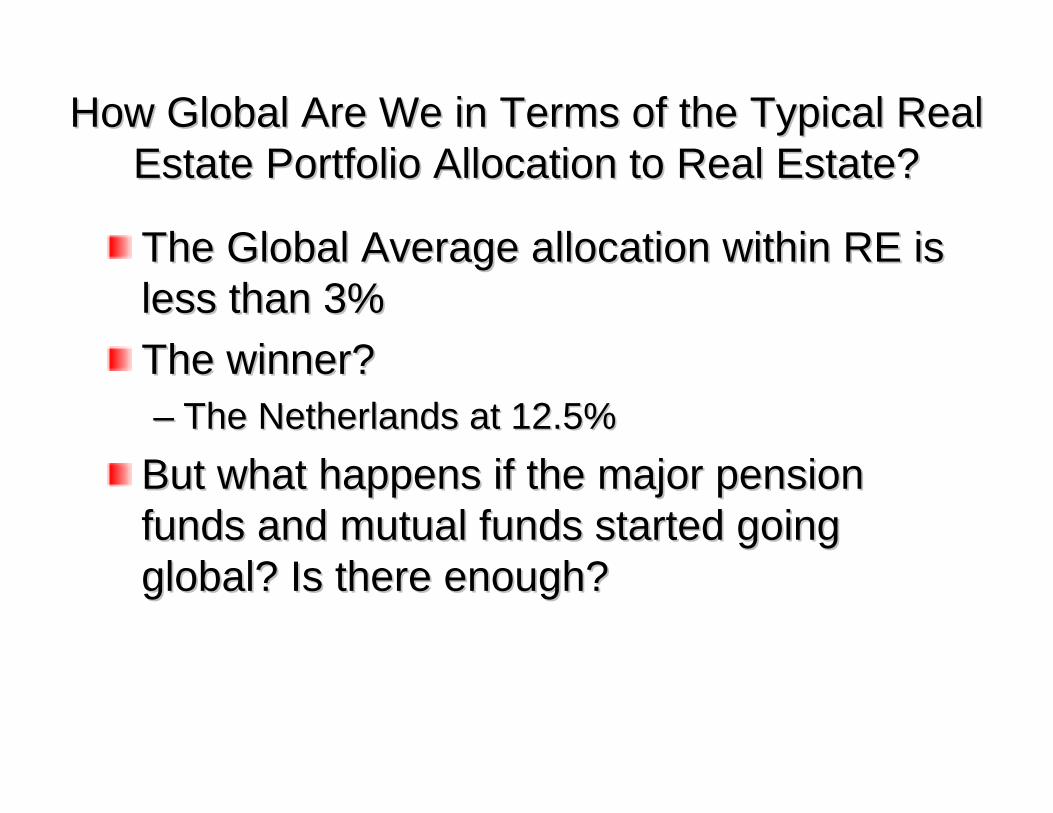

How Global Are We in Terms of the Typical Real How Global Are We in Terms of the Typical Real Estate Portfolio Allocation to Real Estate?Estate Portfolio Allocation to Real Estate?

The Global Average allocation within RE is The Global Average allocation within RE is less than 3%less than 3%The winner?The winner?–– The Netherlands at 12.5% The Netherlands at 12.5% But what happens if the major pension But what happens if the major pension funds and mutual funds started going funds and mutual funds started going global? Is there enough?global? Is there enough?

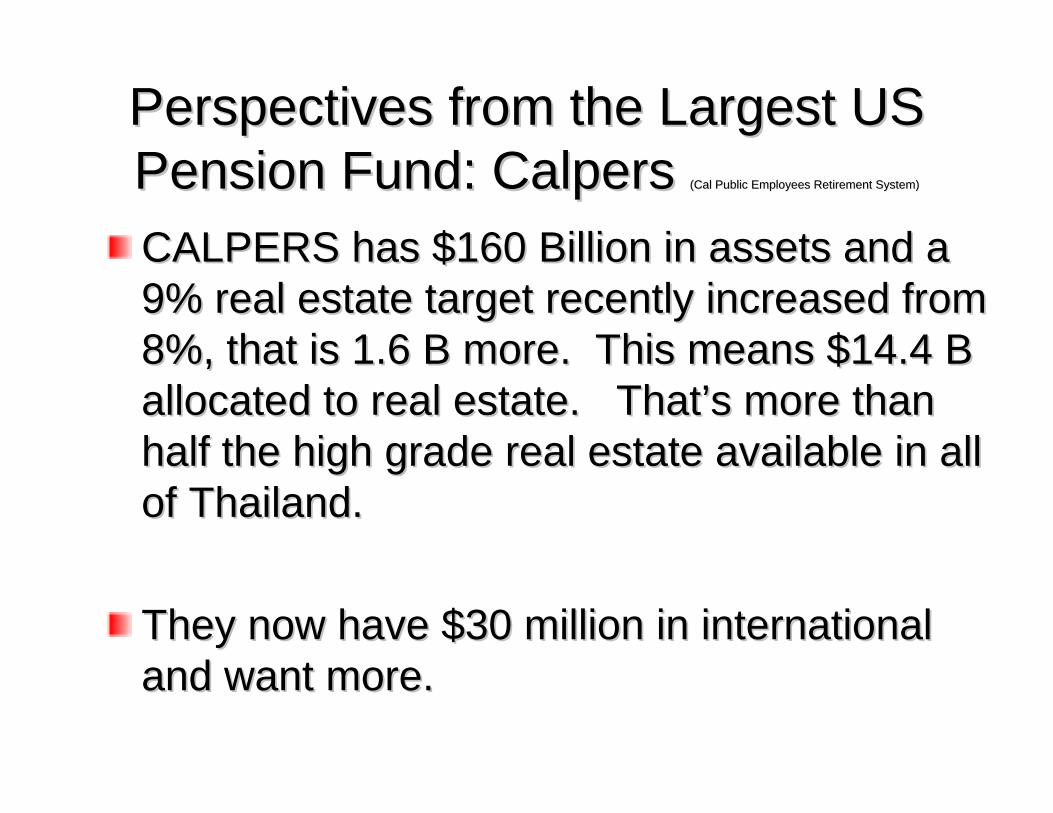

Perspectives from the Largest US Perspectives from the Largest US Pension Fund: Pension Fund: CalpersCalpers (Cal Public Employees Retirement System)(Cal Public Employees Retirement System)

CALPERS has $160 Billion in assets and a CALPERS has $160 Billion in assets and a 9% real estate target recently increased from 9% real estate target recently increased from 8%, that is 1.6 B more. This means $14.4 B 8%, that is 1.6 B more. This means $14.4 B allocated to real estate. That’s more than allocated to real estate. That’s more than half the high grade real estate available in all half the high grade real estate available in all of Thailand. of Thailand.

They now have $30 million in international They now have $30 million in international and want more. and want more.

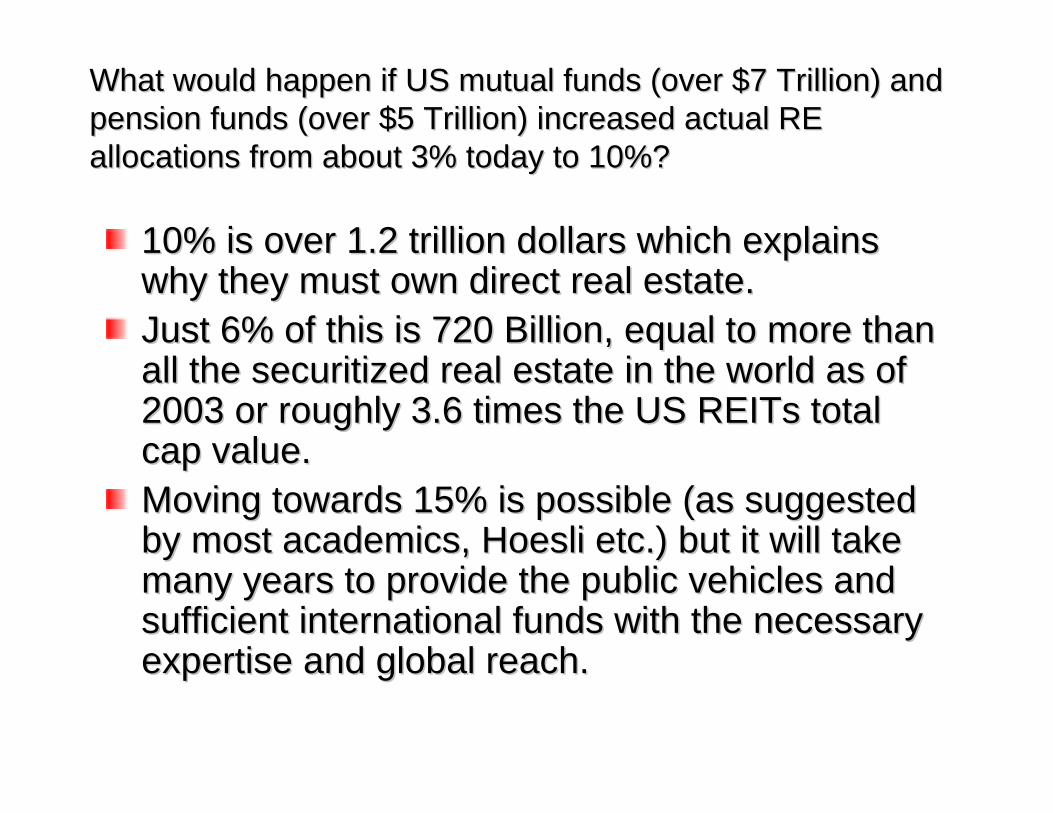

What would happen if US mutual funds (over $7 Trillion) and What would happen if US mutual funds (over $7 Trillion) and pension funds (over $5 Trillion) increased actual RE pension funds (over $5 Trillion) increased actual RE allocations from about 3% today to 10%?allocations from about 3% today to 10%?

10% is over 1.2 trillion dollars which explains 10% is over 1.2 trillion dollars which explains why they must own direct real estate.why they must own direct real estate.Just 6% of this is 720 Billion, equal to more than Just 6% of this is 720 Billion, equal to more than all the securitized real estate in the world as of all the securitized real estate in the world as of 2003 or roughly 3.6 times the US 2003 or roughly 3.6 times the US REITsREITs total total cap value.cap value.Moving towards 15% is possible (as suggested Moving towards 15% is possible (as suggested by most academics, by most academics, HoesliHoesli etc.) but it will take etc.) but it will take many years to provide the public vehicles and many years to provide the public vehicles and sufficient international funds with the necessary sufficient international funds with the necessary expertise and global reach.expertise and global reach.

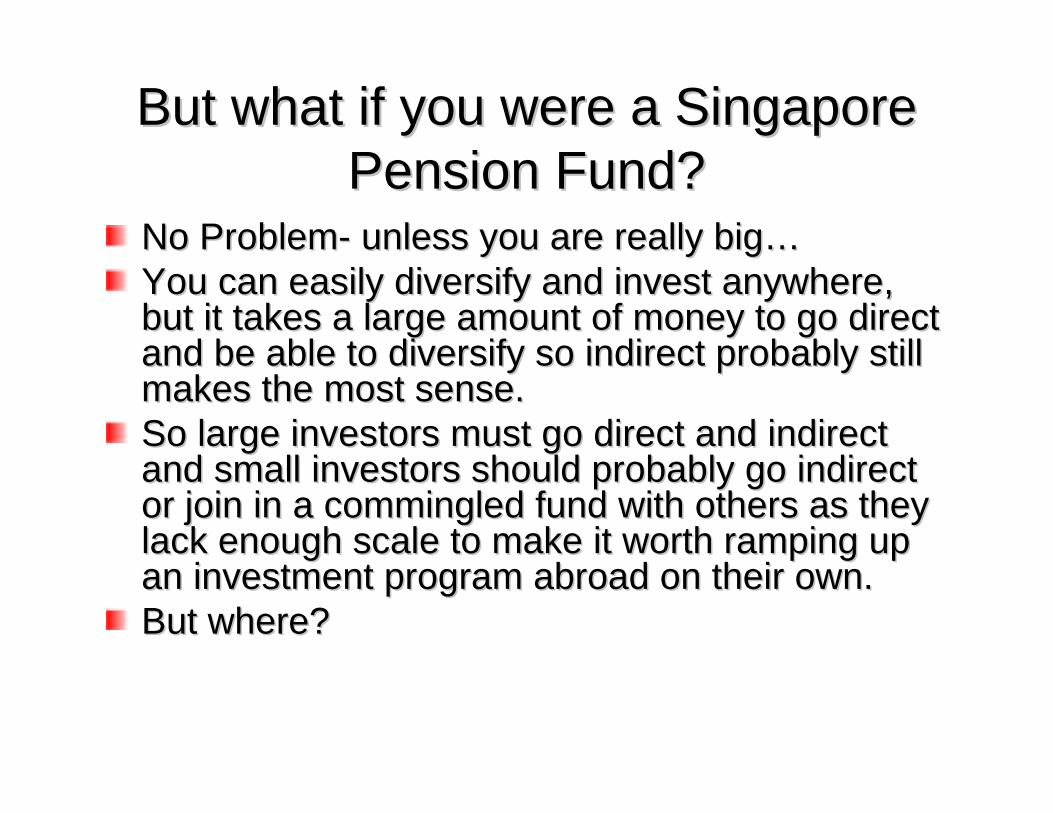

But what if you were a Singapore But what if you were a Singapore Pension Fund?Pension Fund?

No ProblemNo Problem-- unless you are really big…unless you are really big…You can easily diversify and invest anywhere, You can easily diversify and invest anywhere, but it takes a large amount of money to go direct but it takes a large amount of money to go direct and be able to diversify so indirect probably still and be able to diversify so indirect probably still makes the most sense.makes the most sense.So large investors must go direct and indirect So large investors must go direct and indirect and small investors should probably go indirect and small investors should probably go indirect or join in a commingled fund with others as they or join in a commingled fund with others as they lack enough scale to make it worth ramping up lack enough scale to make it worth ramping up an investment program abroad on their own.an investment program abroad on their own.But where?But where?

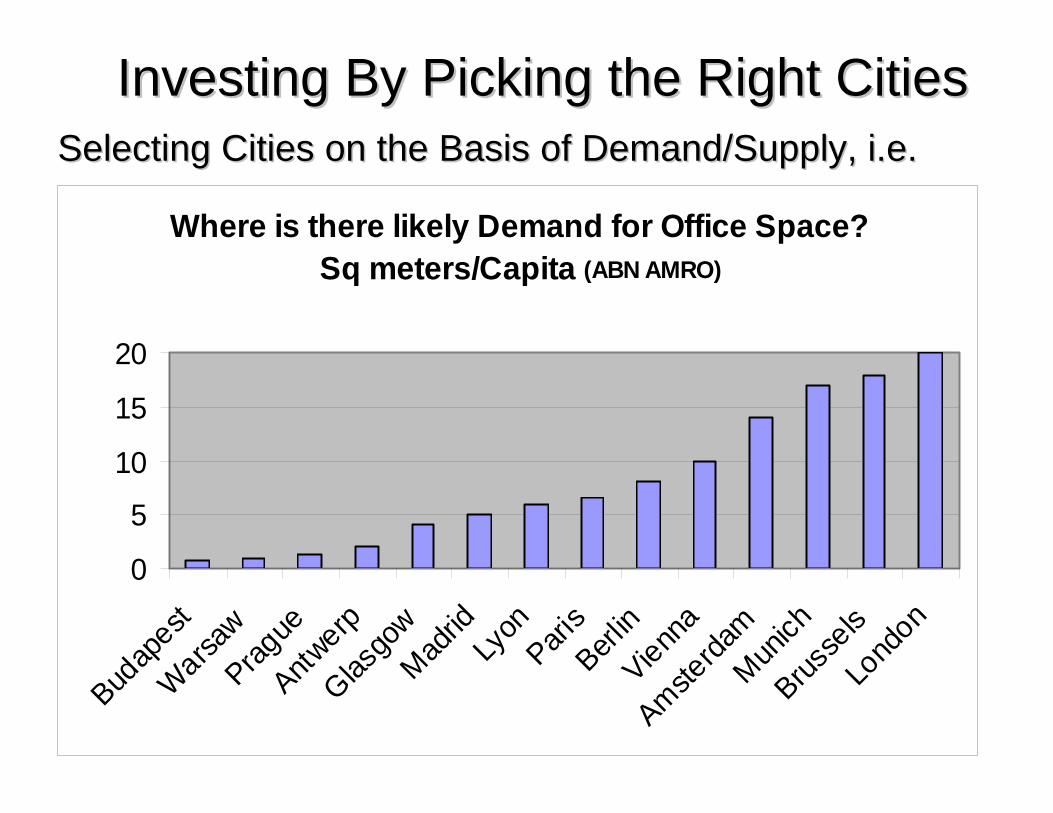

Investing By Picking the Right CitiesInvesting By Picking the Right CitiesSelecting Cities on the Basis of Demand/Supply, i.e.Selecting Cities on the Basis of Demand/Supply, i.e.

Where is there likely Demand for Office Space? Sq meters/Capita (ABN AMRO)

0

5

10

15

20

Budap

estWarsa

wPrag

ueAntw

erpGlas

gow

Madrid

Lyon

Paris

Berlin

Vienna

Amsterda

mMun

ichBrus

sels

Lond

on

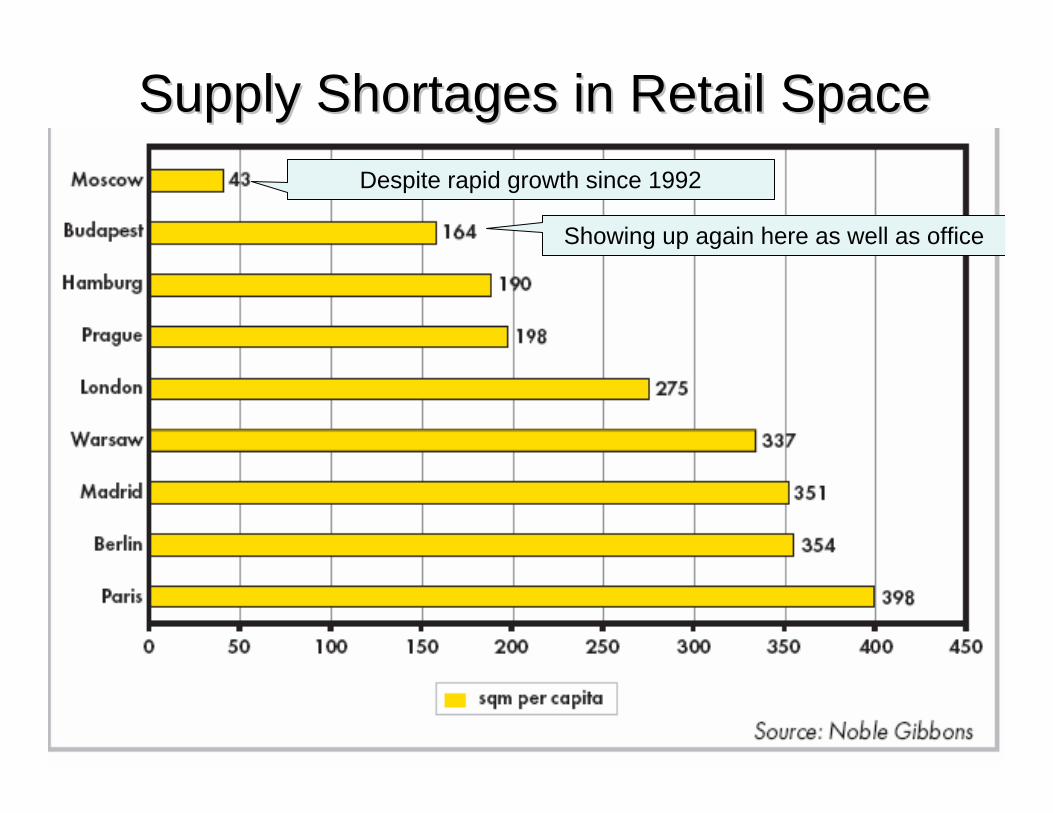

Supply Shortages in Retail SpaceSupply Shortages in Retail SpaceDespite rapid growth since 1992

Showing up again here as well as office

Or noting the loss of white collar Or noting the loss of white collar service jobs in Americaservice jobs in America

One countries loss is another’s gain.One countries loss is another’s gain.The internet and communication technology has The internet and communication technology has meant the death of distance for firms like IBM, meant the death of distance for firms like IBM, Microsoft, many Banks and Airline support staffMicrosoft, many Banks and Airline support staffEconomics teaches us that when there seems to Economics teaches us that when there seems to be a negative trend somewhere there will also be a negative trend somewhere there will also be a positive somewhere else.be a positive somewhere else.

According to A.T. Kearney the USA is losing According to A.T. Kearney the USA is losing 500,000 jobs a year right now to China, India, 500,000 jobs a year right now to China, India, Russia, and the Czech Republic. That suggests Russia, and the Czech Republic. That suggests new office demand in these markets.new office demand in these markets.

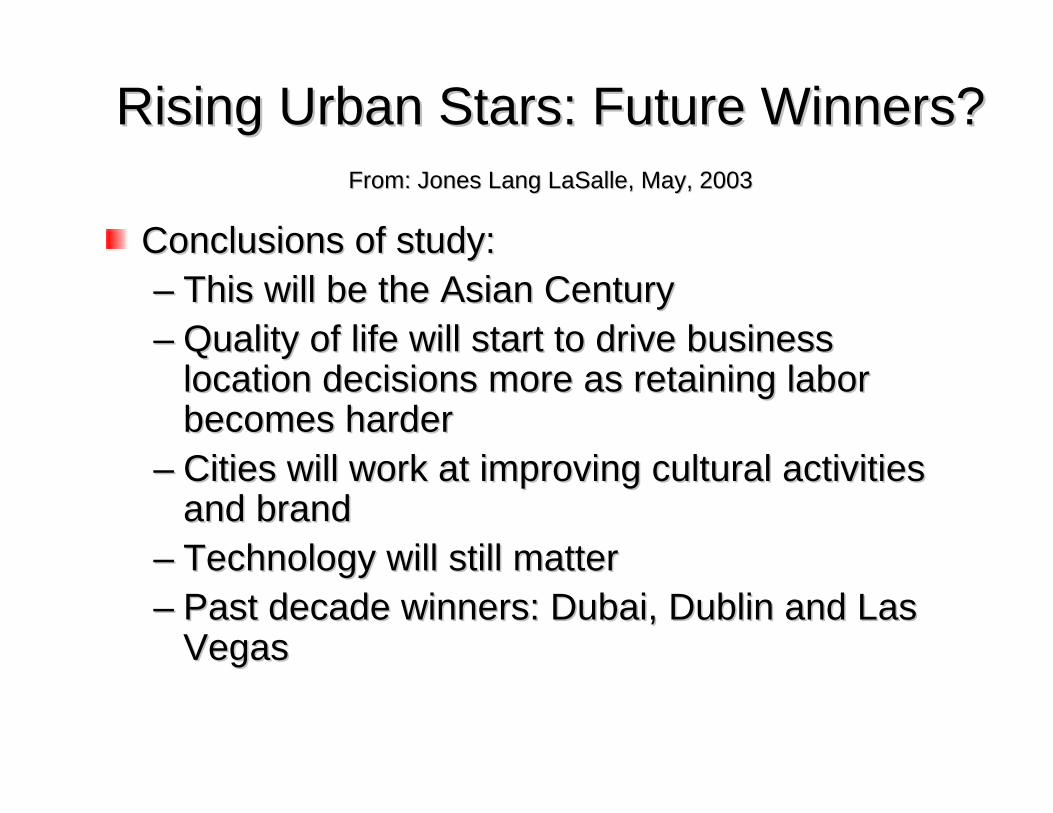

Rising Urban Stars: Future Winners?Rising Urban Stars: Future Winners?From: Jones Lang LaSalle, May, 2003From: Jones Lang LaSalle, May, 2003

Conclusions of study: Conclusions of study: –– This will be the Asian CenturyThis will be the Asian Century–– Quality of life will start to drive business Quality of life will start to drive business

location decisions more as retaining labor location decisions more as retaining labor becomes harderbecomes harder

–– Cities will work at improving cultural activities Cities will work at improving cultural activities and brandand brand

–– Technology will still matterTechnology will still matter–– Past decade winners: Dubai, Dublin and Las Past decade winners: Dubai, Dublin and Las

VegasVegas

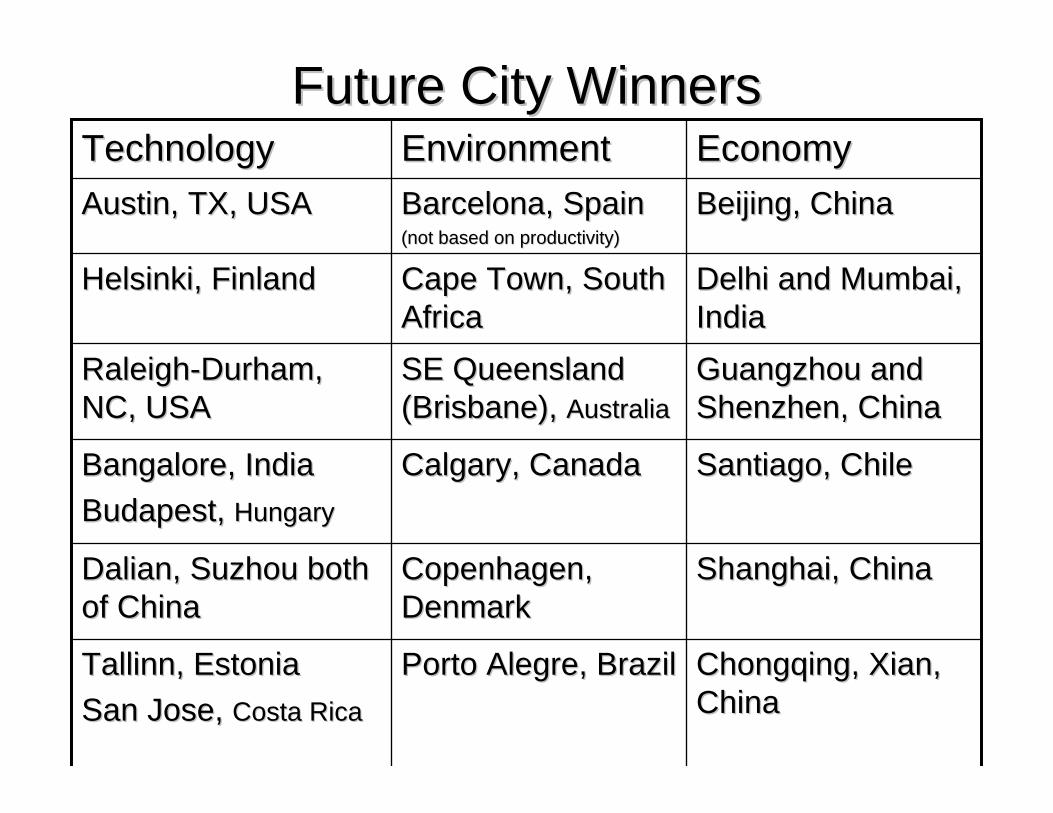

Future City WinnersFuture City Winners

ChongqingChongqing, Xian, , Xian, ChinaChina

Porto Porto AlegreAlegre, Brazil, BrazilTallinn, EstoniaTallinn, EstoniaSan Jose, San Jose, Costa RicaCosta Rica

Shanghai, ChinaShanghai, ChinaCopenhagen, Copenhagen, DenmarkDenmark

DalianDalian, , SuzhouSuzhou both both of Chinaof China

Santiago, ChileSantiago, ChileCalgary, CanadaCalgary, CanadaBangalore, IndiaBangalore, IndiaBudapest, Budapest, HungaryHungary

Guangzhou and Guangzhou and Shenzhen, ChinaShenzhen, China

SE Queensland SE Queensland (Brisbane), (Brisbane), AustraliaAustralia

RaleighRaleigh--Durham, Durham, NC, USA NC, USA

Delhi and Mumbai, Delhi and Mumbai, IndiaIndia

Cape Town, South Cape Town, South AfricaAfrica

Helsinki, FinlandHelsinki, Finland

Beijing, ChinaBeijing, ChinaBarcelona, SpainBarcelona, Spain(not based on productivity)(not based on productivity)

Austin, TX, USAAustin, TX, USAEconomyEconomyEnvironmentEnvironmentTechnologyTechnology

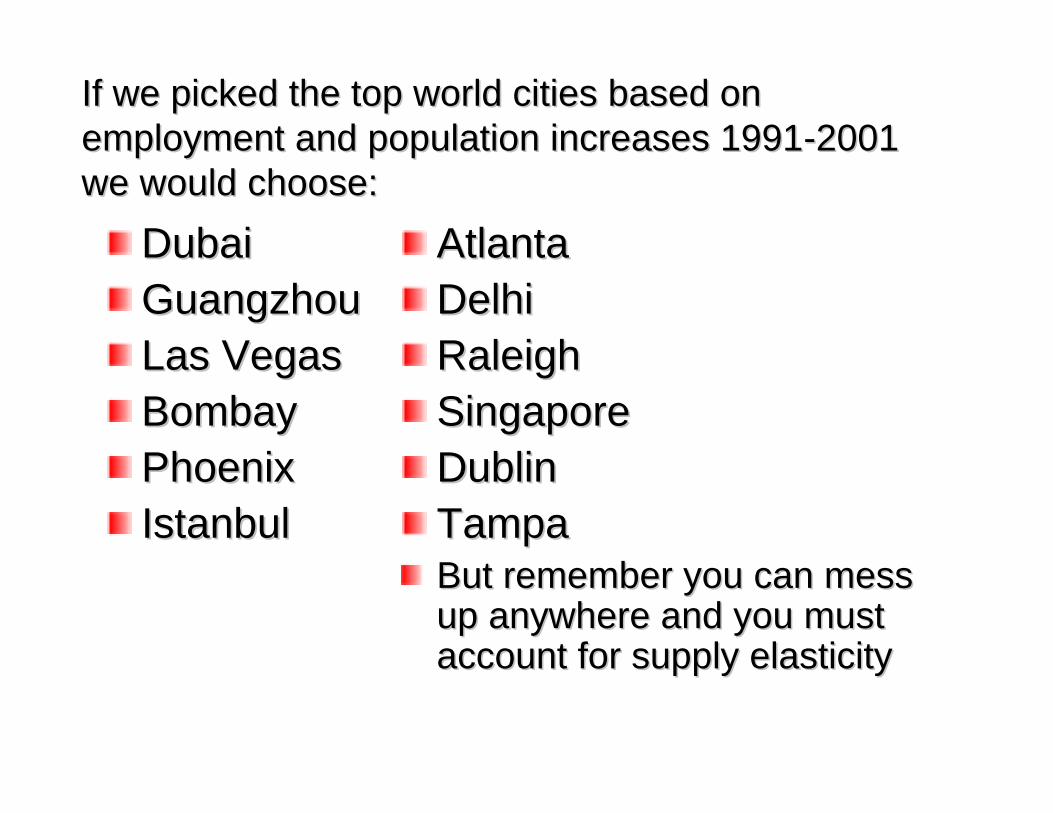

If we picked the top world cities based on If we picked the top world cities based on employment and population increases 1991employment and population increases 1991--2001 2001 we would choose:we would choose:

DubaiDubaiGuangzhouGuangzhouLas VegasLas VegasBombayBombayPhoenixPhoenixIstanbulIstanbul

AtlantaAtlantaDelhiDelhiRaleighRaleighSingaporeSingaporeDublinDublinTampaTampaBut remember you can mess But remember you can mess up anywhere and you must up anywhere and you must account for supply elasticityaccount for supply elasticity

Investing By Picking the Right Investing By Picking the Right CountriesCountries

Assuming you are allowed to “own” in foreign Assuming you are allowed to “own” in foreign countries.countries.You must consider currency risks, taxation, You must consider currency risks, taxation, corruption and property rights enforcement, local rule corruption and property rights enforcement, local rule nuances (lease tenant rights or residential squatter nuances (lease tenant rights or residential squatter rights) and local liquidity, and brokerage costs all in rights) and local liquidity, and brokerage costs all in addition to normal fundamentals of demand and addition to normal fundamentals of demand and supply trends, assuming there is market information supply trends, assuming there is market information (transparency).(transparency).Perhaps work ethic and productivity?Perhaps work ethic and productivity?

Currency RisksCurrency Risks

Malaysia, Malaysia, PhilipinesPhilipines and Thailand need to and Thailand need to develop currency future markets so that develop currency future markets so that hedging becomes possible, otherwise risk hedging becomes possible, otherwise risk premiums of 2% to 4% will be required by premiums of 2% to 4% will be required by foreign investors. foreign investors. Finland and Greece also have significant Finland and Greece also have significant currency risks.currency risks.Least risky markets: US, UK, Australia, Least risky markets: US, UK, Australia, and France.and France.

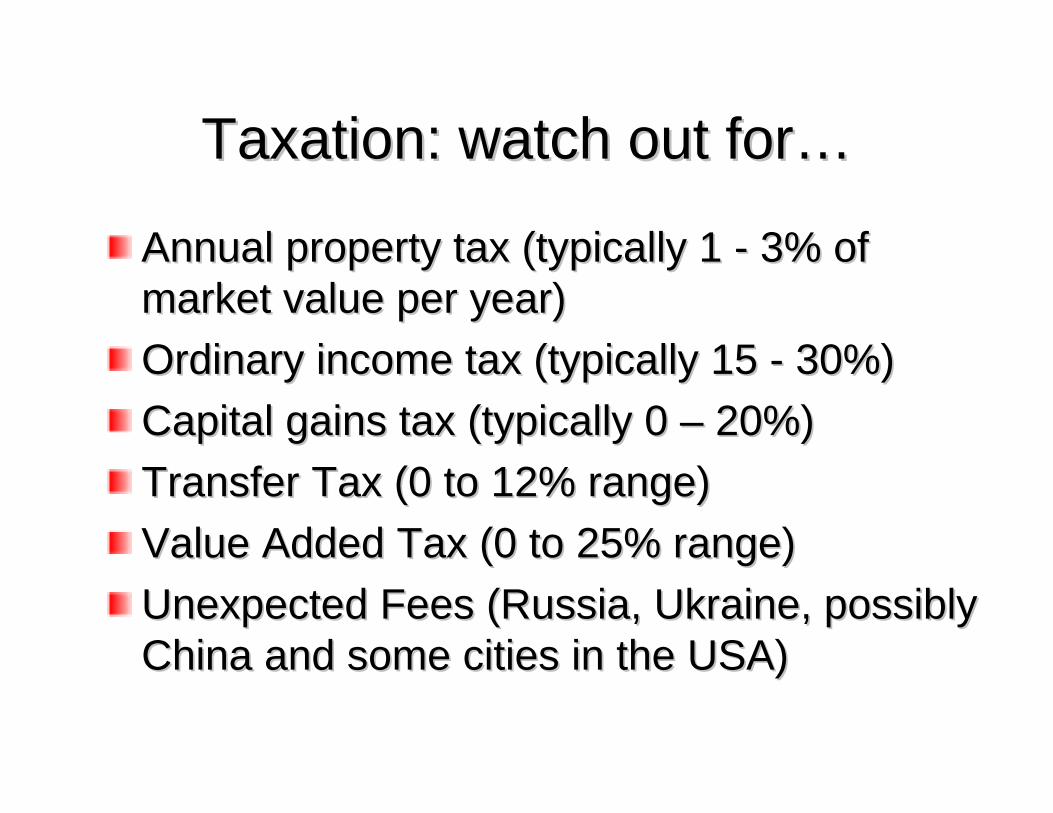

Taxation: watch out for…Taxation: watch out for…

Annual property tax (typically 1 Annual property tax (typically 1 -- 3% of 3% of market value per year)market value per year)Ordinary income tax (typically 15 Ordinary income tax (typically 15 -- 30%)30%)Capital gains tax (typically 0 Capital gains tax (typically 0 –– 20%)20%)Transfer Tax (0 to 12% range)Transfer Tax (0 to 12% range)Value Added Tax (0 to 25% range)Value Added Tax (0 to 25% range)Unexpected Fees (Russia, Ukraine, possibly Unexpected Fees (Russia, Ukraine, possibly China and some cities in the USA)China and some cities in the USA)

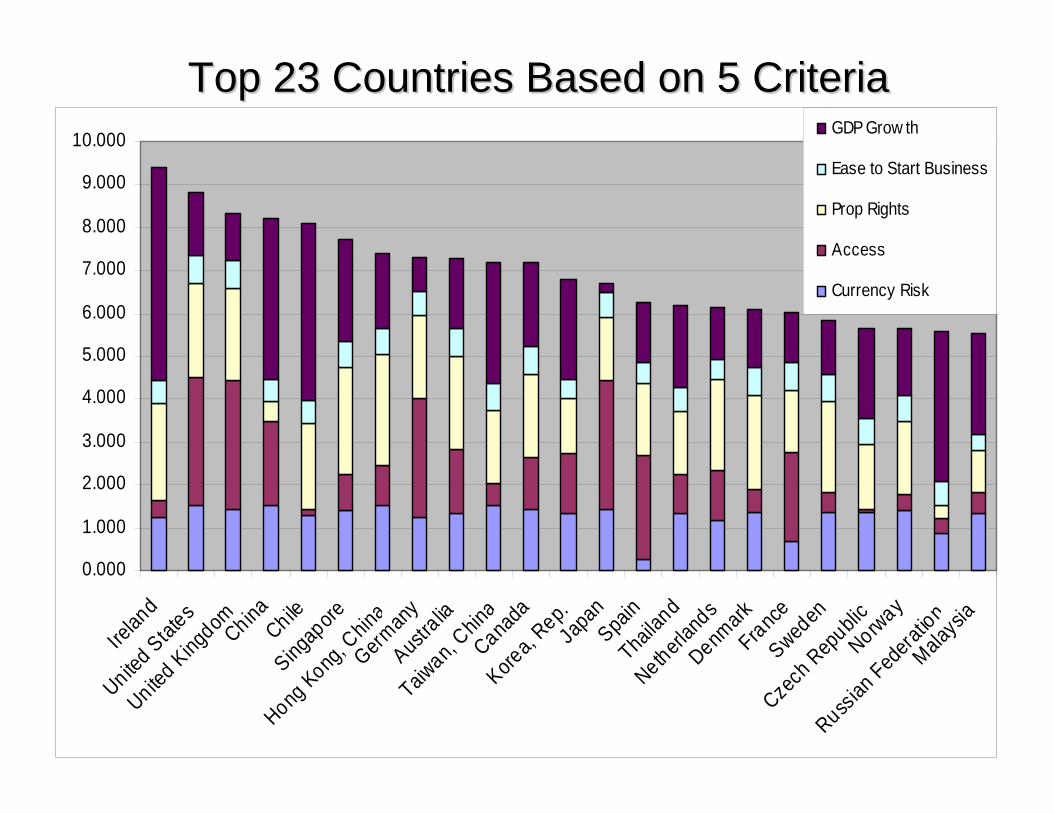

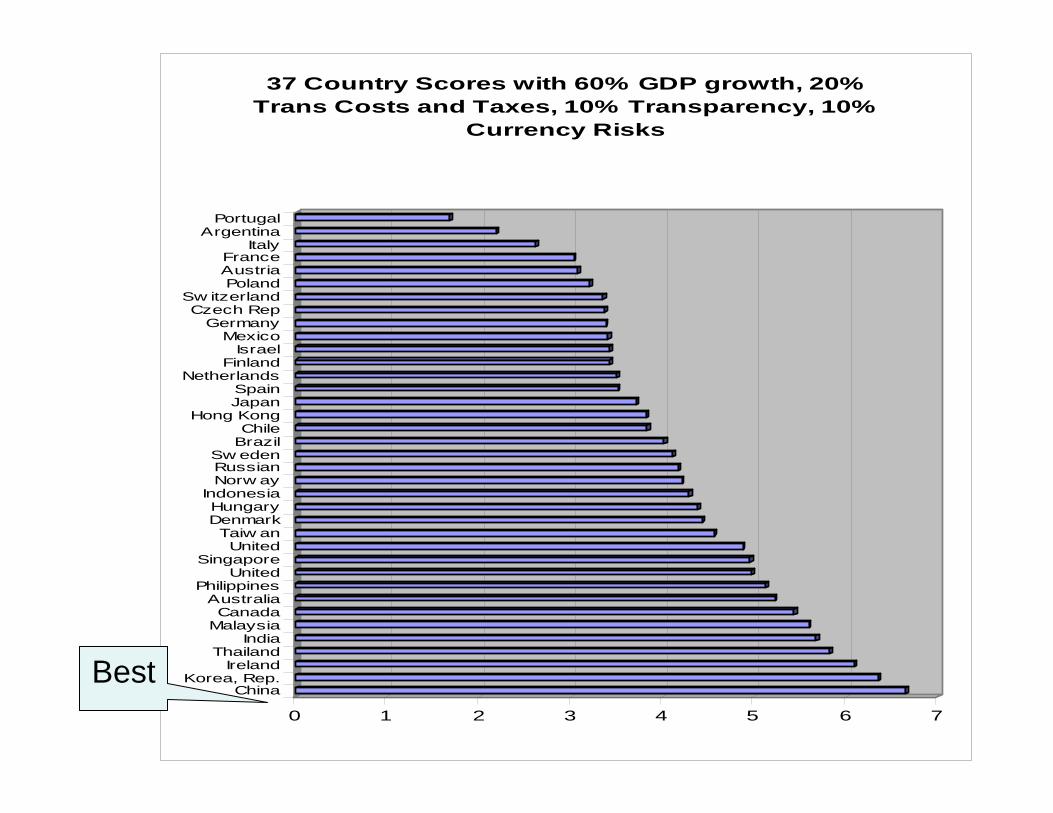

Using the following five criteria Using the following five criteria equally weightedequally weighted

GDP GrowthGDP GrowthCurrency Risk and TaxationCurrency Risk and TaxationProperty Rights EnforcementProperty Rights EnforcementEase to Start a Business (Regulation)Ease to Start a Business (Regulation)Access (measured by airport Access (measured by airport boardingsboardings))We get the following results as to where We get the following results as to where we should invest…we should invest…

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

Irelan

d

United Stat

es

United King

domChinaChile

Singap

ore

Hong Kong

, Chin

aGerm

any

Australia

Taiwan,

China

Canada

Korea,

Rep.Ja

pan

Spain

Thailan

dNetherl

ands

Denmark

FranceSwed

en

Czech

Republic

Norway

Russian

Federa

tion

Malaysi

a

GDP Grow th

Ease to Start Business

Prop Rights

Access

Currency Risk

Top 23 Countries Based on 5 CriteriaTop 23 Countries Based on 5 Criteria

0 1 2 3 4 5 6 7

ChinaKorea, Rep.

IrelandThailand

IndiaMalaysiaCanada

AustraliaPhilippines

UnitedSingapore

UnitedTaiw an

DenmarkHungary

IndonesiaNorw ayRussianSw eden

BrazilChile

Hong KongJapanSpain

NetherlandsFinland

IsraelMexico

GermanyCzech Rep

Sw itzerlandPolandAustriaFrance

ItalyArgentina

Portugal

37 Country Scores with 60% GDP growth, 20% Trans Costs and Taxes, 10% Transparency, 10%

Currency Risks

Best

0 1 2 3 4 5 6 7

China

Korea, Rep.

Ireland

Thailand

India

Malaysia

Canada

Australia

Philippines

United States

Singapore

United Kingdom

Taiw an

Denmark

Hungary

Indonesia

Norw ay

Russian Federation

Sw eden

Brazil

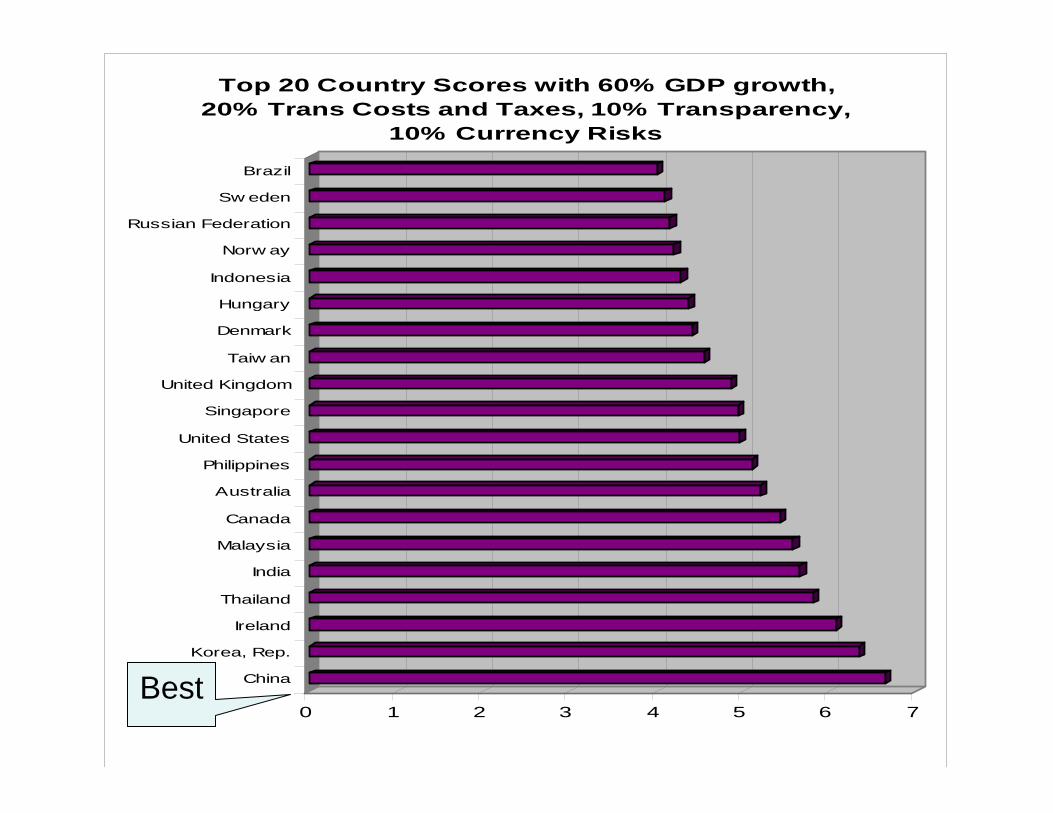

Top 20 Country Scores with 60% GDP growth, 20% Trans Costs and Taxes, 10% Transparency,

10% Currency Risks

Best

0 1 2 3 4 5 6 7

China

Korea, Rep.

Ireland

Thailand

India

Malaysia

Canada

Australia

Philippines

United States

Singapore

United Kingdom

Taiw an

Denmark

Hungary

Indonesia

Norw ay

Russian Federation

Sw eden

Brazil

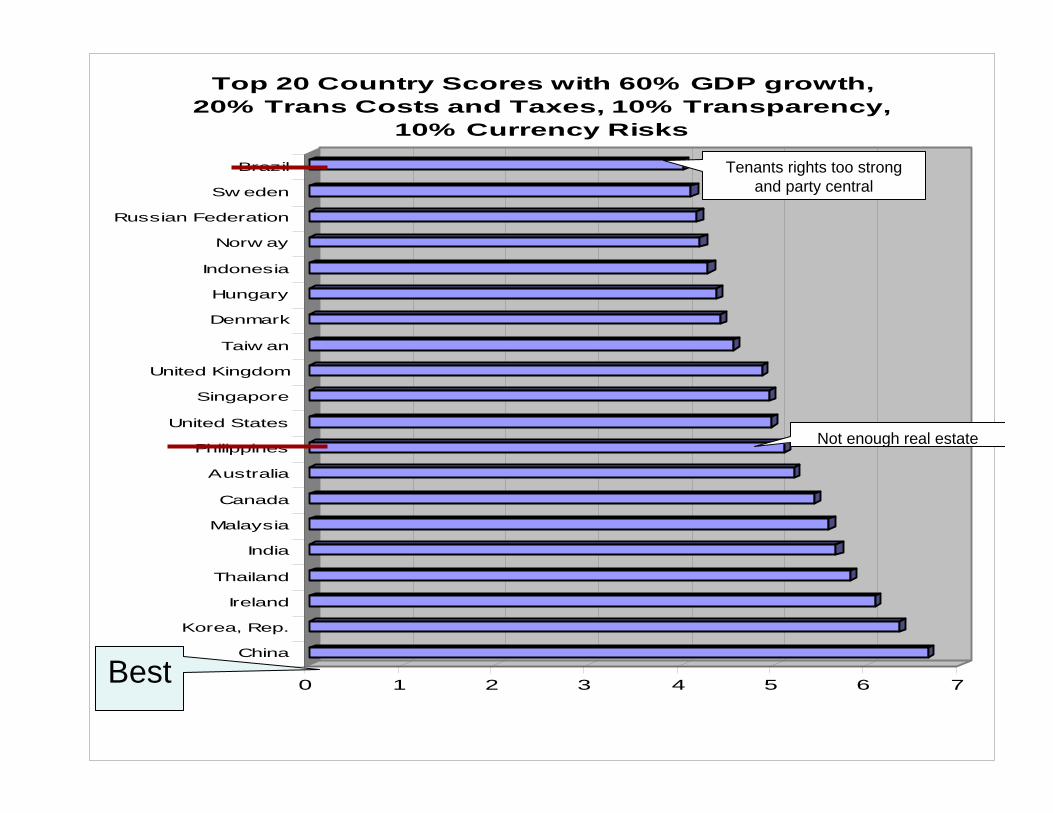

Top 20 Country Scores with 60% GDP growth, 20% Trans Costs and Taxes, 10% Transparency,

10% Currency Risks

Tenants rights too strong and party central

Not enough real estate

Best

In the absence of long term objective data In the absence of long term objective data explaining direct real estate returnsexplaining direct real estate returns

We will rely on arbitrary models with We will rely on arbitrary models with arbitrary weights, i.e. we could have used:arbitrary weights, i.e. we could have used:

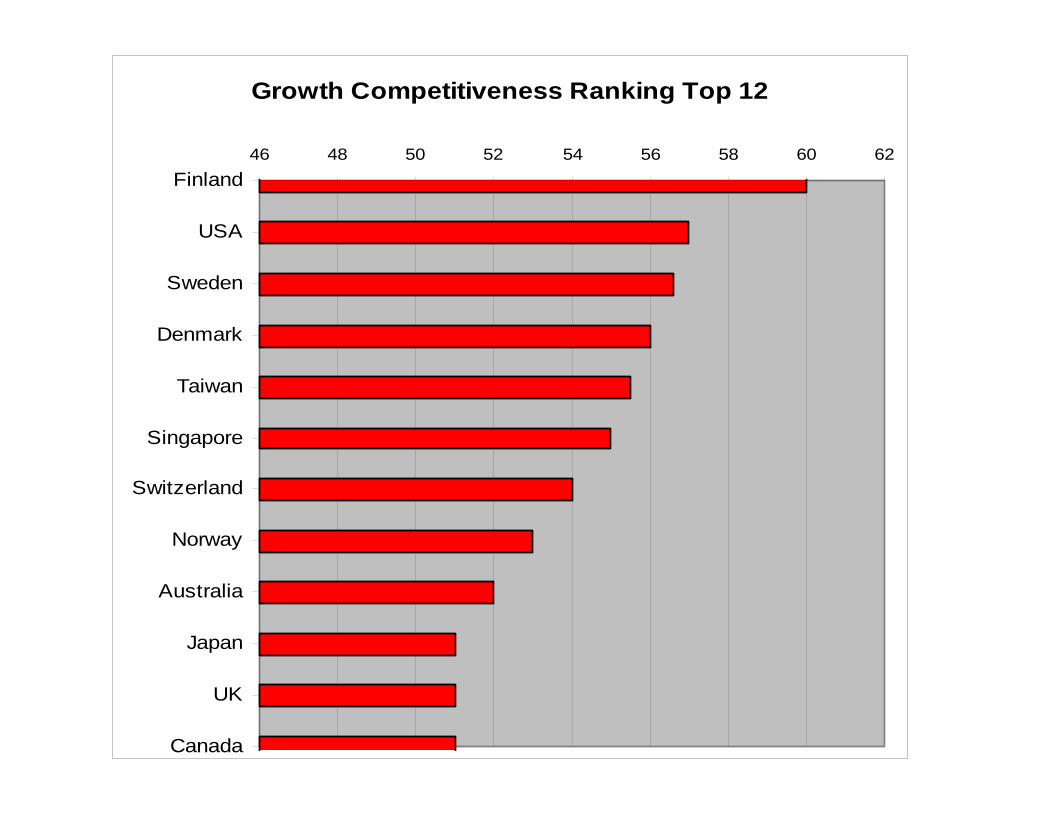

Growth Competitiveness Ranking Top 12

46 48 50 52 54 56 58 60 62Finland

USA

Sweden

Denmark

Taiwan

Singapore

Switzerland

Norway

Australia

Japan

UK

Canada

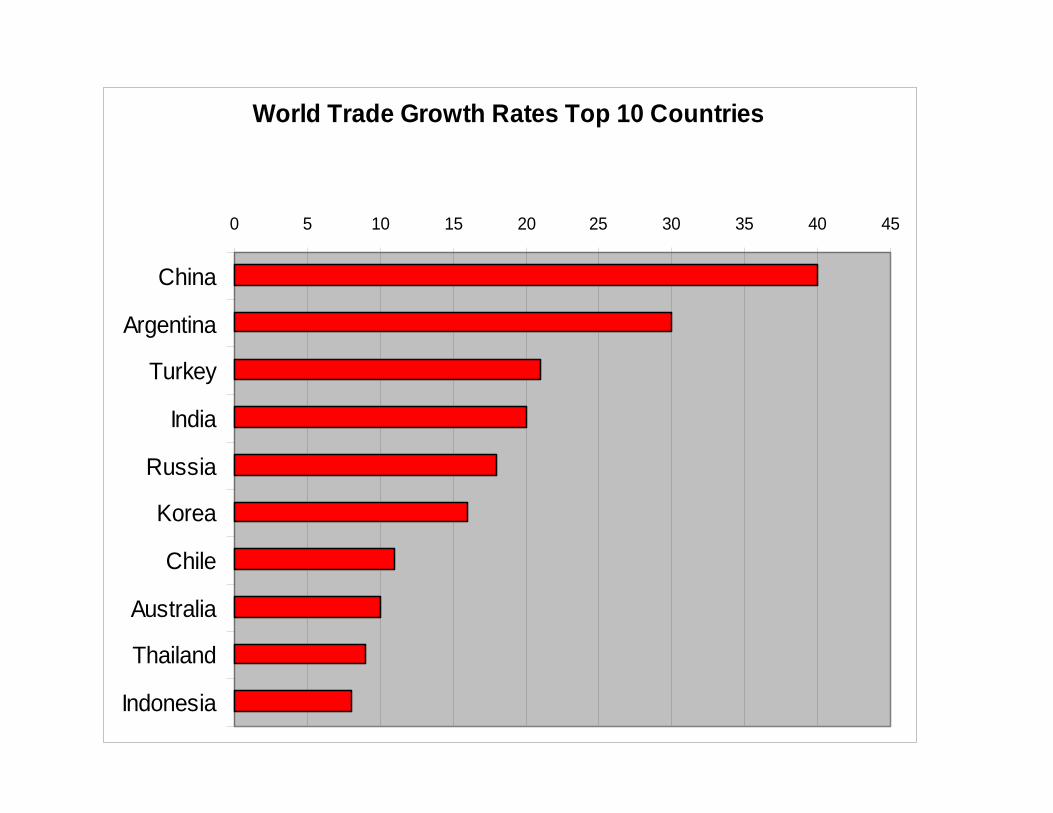

World Trade Growth Rates Top 10 Countries

0 5 10 15 20 25 30 35 40 45

China

Argentina

Turkey

India

Russia

Korea

Chile

Australia

Thailand

Indonesia

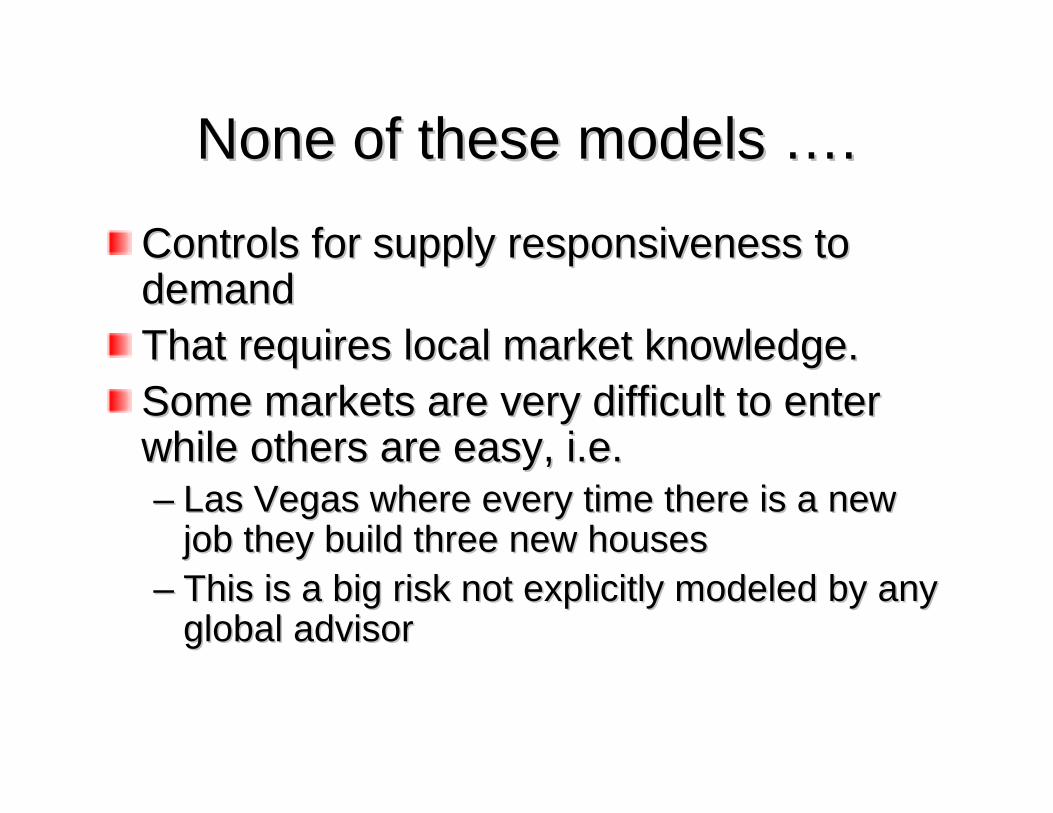

None of these models ….None of these models ….

Controls for supply responsiveness to Controls for supply responsiveness to demanddemandThat requires local market knowledge.That requires local market knowledge.Some markets are very difficult to enter Some markets are very difficult to enter while others are easy, i.e.while others are easy, i.e.–– Las Vegas where every time there is a new Las Vegas where every time there is a new

job they build three new housesjob they build three new houses–– This is a big risk not explicitly modeled by any This is a big risk not explicitly modeled by any

global advisorglobal advisor

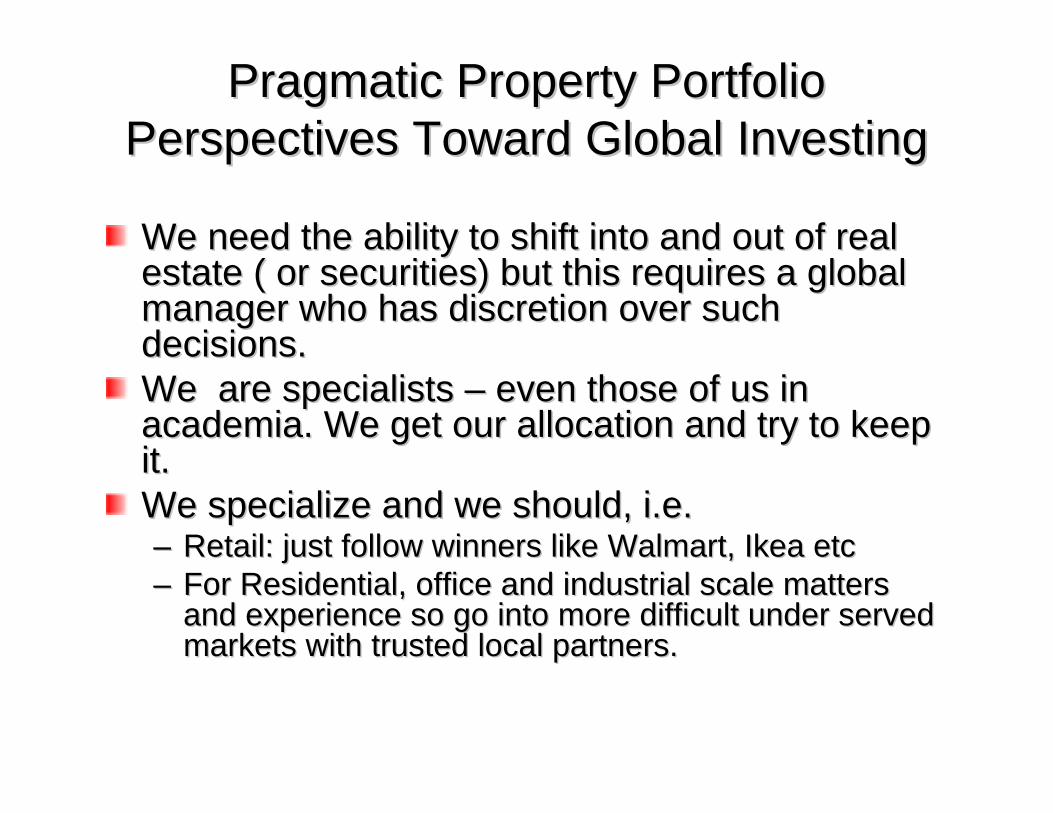

Pragmatic Property Portfolio Pragmatic Property Portfolio Perspectives Toward Global InvestingPerspectives Toward Global Investing

We need the ability to shift into and out of real We need the ability to shift into and out of real estate ( or securities) but this requires a global estate ( or securities) but this requires a global manager who has discretion over such manager who has discretion over such decisions. decisions. We are specialists We are specialists –– even those of us in even those of us in academia. We get our allocation and try to keep academia. We get our allocation and try to keep it.it.We specialize and we should, i.e.We specialize and we should, i.e.–– Retail: just follow winners like Retail: just follow winners like WalmartWalmart, Ikea etc, Ikea etc–– For Residential, office and industrial scale matters For Residential, office and industrial scale matters

and experience so go into more difficult under served and experience so go into more difficult under served markets with trusted local partners.markets with trusted local partners.

Developing Trusted RelationshipsDeveloping Trusted RelationshipsA prerequisite to local foreign direct A prerequisite to local foreign direct investment.investment.It makes no sense to go in and start from It makes no sense to go in and start from scratch a new business but rather to scratch a new business but rather to develop partnerships.develop partnerships.Subordinated contracts with preferred Subordinated contracts with preferred returns make the most sensereturns make the most sense–– Master leases (shift leasing and management)Master leases (shift leasing and management)–– Participating mortgages (equity like but without Participating mortgages (equity like but without

true ownership)true ownership)

Summary 1 of 3 Summary 1 of 3 The world is somewhat different since 1992 for American The world is somewhat different since 1992 for American REITS and for Western Europe with the EU (1992) and EU REITS and for Western Europe with the EU (1992) and EU currency (2002). It is also different since 1989 in the old currency (2002). It is also different since 1989 in the old Soviet block countries.Soviet block countries.Any yield at all would be good for Japanese InvestorsAny yield at all would be good for Japanese InvestorsA modest increase in pension fund allocations to A modest increase in pension fund allocations to international real estate, especially from the US, could international real estate, especially from the US, could quickly overwhelm the market. quickly overwhelm the market. Real estate has garnered increased investor interest recentlyReal estate has garnered increased investor interest recently

–– Aging populationAging population

–– A modest real estate allocation pays a disproportionate A modest real estate allocation pays a disproportionate share of current liabilities for pension fundsshare of current liabilities for pension funds

Summary 2 of 3Summary 2 of 3Strategic investors that want to be able to reStrategic investors that want to be able to re--balance or move in and out of markets will prefer balance or move in and out of markets will prefer securitized forms of real estate. This requires securitized forms of real estate. This requires the liquidity of a securitized vehicle.the liquidity of a securitized vehicle.Countries that wish to increase foreign Countries that wish to increase foreign investment must develop indirect or securitized investment must develop indirect or securitized vehicles and encourage greater penetration into vehicles and encourage greater penetration into core property segments. There is an important core property segments. There is an important role for governments to play in helping these role for governments to play in helping these markets evolve.markets evolve.For smaller investors securities are the only For smaller investors securities are the only reasonable way to diversify internationally.reasonable way to diversify internationally.

Summary 3 of 3Summary 3 of 3

For the largest investors indirect and direct For the largest investors indirect and direct is still necessary for achieving minimum is still necessary for achieving minimum diversification objectives.diversification objectives.No investment advisor nor academic has a No investment advisor nor academic has a very reliable forward looking model that very reliable forward looking model that spans the globe as no one is able to spans the globe as no one is able to forecast supply reaction to demand forecast supply reaction to demand without local knowledge.without local knowledge.

ConclusionsConclusionsThere will always There will always be global be global opportunities in opportunities in specialized sectors.specialized sectors.

–– You can still do You can still do well in weak well in weak markets and markets and make big make big mistakes in mistakes in strong markets.strong markets.

A final personal noteA final personal noteLook how global we are today….Look how global we are today….

ขอบคุณครับ

ReferencesReferencesAddaeAddae--DapaahDapaah, K. and C.B. , K. and C.B. KionKion “International Diversification of Property Stock: A Singaporean“International Diversification of Property Stock: A SingaporeanInvestor’s Viewpoint” Investor’s Viewpoint” Real Estate FinanceReal Estate Finance, 1996, 13:3, 54, 1996, 13:3, 54--66.66.Anderson, R., G. Mueller, and X. Xing, “International Real EstatAnderson, R., G. Mueller, and X. Xing, “International Real Estate Portfolio Construction: e Portfolio Construction: Conditional and Unconditional Methods”, working Paper, PresentedConditional and Unconditional Methods”, working Paper, Presented at the American Real Estate at the American Real Estate Society Meetings, April 2, 2003. Society Meetings, April 2, 2003. [email protected][email protected], R. J. and D. M. , R. J. and D. M. GeltnerGeltner “Price Discovery in the American and British Property Markets”,“Price Discovery in the American and British Property Markets”,Real Estate EconomicsReal Estate Economics, 1995, 23:1, pp 21, 1995, 23:1, pp 21--24.24.BrounenBrounen, D. and P. , D. and P. EicholtzEicholtz ““Demographics and the Office Market: An International InvestigatiDemographics and the Office Market: An International Investigationon””Working paper presented at ASSA meetings, San Diego, USA, Jan. 2Working paper presented at ASSA meetings, San Diego, USA, Jan. 2004.004.Chen, N. Roll and S.A. Ross, Chen, N. Roll and S.A. Ross, ““Economic Forces and the Stock MarketEconomic Forces and the Stock Market””, , Journal of BusinessJournal of Business, 1986, , 1986, Vol. 59, 383Vol. 59, 383--403.403.Chua, A., Chua, A., ““The Role of International Real Estate in Global Mixed Asset PortThe Role of International Real Estate in Global Mixed Asset Portfoliosfolios”” Journal of Real Journal of Real Estate Portfolio ManagementEstate Portfolio Management, 1999, 5:2, pp. 99, 1999, 5:2, pp. 99--112. 112. Conover, C. H. Friday and G. Conover, C. H. Friday and G. SirmansSirmans, , ““Diversification Benefits from Foreign Real Estate Diversification Benefits from Foreign Real Estate InvestmentsInvestments”” Journal of Real Estate Portfolio ManagementJournal of Real Estate Portfolio Management, 2002, January/April, 17, 2002, January/April, 17--25.25.CurcioCurcio, R. J. and A.J. , R. J. and A.J. ZiobrowskiZiobrowski, , ““Global Mixed Asset DiversificationGlobal Mixed Asset Diversification”” Global Finance JournalGlobal Finance Journal, , 1991, 2:3/4, pp. 2551991, 2:3/4, pp. 255--92.92.DD’’Arcy, E. and S. Lee Arcy, E. and S. Lee ““A Real Estate Portfolio Strategy for Europe: A Review of the OptA Real Estate Portfolio Strategy for Europe: A Review of the Optionsions””Journal of Real Estate Portfolio ManagementJournal of Real Estate Portfolio Management, 1998, 4:2, 113, 1998, 4:2, 113--23.23.DahlquistDahlquist, M. and C. Harvey, , M. and C. Harvey, ““Global Tactical Asset AllocationGlobal Tactical Asset Allocation””, , Emerging Markets QuarterlyEmerging Markets Quarterly, , 2001, 1:1, 62001, 1:1, 6--14.14.DamodaranDamodaran, A. , A. ““Country Risk and Company Exposure: Theory and PracticeCountry Risk and Company Exposure: Theory and Practice”” Journal of Applied Journal of Applied FinanceFinance, Fall/Winter 2003, pp. 7, Fall/Winter 2003, pp. 7--20.20.DeBrondtDeBrondt, W., A. , W., A. FungFung, and K. Lam, , and K. Lam, ““The Speculative Dynamics of World Equity MarketsThe Speculative Dynamics of World Equity Markets””DePaul University Working Paper, Department of Finance, College DePaul University Working Paper, Department of Finance, College of Business, 1 East Jackson, of Business, 1 East Jackson, Chicago, 60604, Nov. 2003. Chicago, 60604, Nov. 2003. [email protected]@depaul.edu

ReferencesReferencesDusanDusan IsakovIsakov, 1999, Is beta still alive? Conclusive evidence from the Swiss , 1999, Is beta still alive? Conclusive evidence from the Swiss stock stock market, The European Journal of Finance 5, 202market, The European Journal of Finance 5, 202--212.212.EichholtzEichholtz, P.M.A. David J. , P.M.A. David J. HartzellHartzell. . ““Property Shares, Appraisals and the Stock Property Shares, Appraisals and the Stock Market: An International PerspectiveMarket: An International Perspective””.. Journal of Property Finance and EconomicsJournal of Property Finance and Economics1996, 12: 1631996, 12: 163--178.178.EicholtzEicholtz, P. , P. ““Does International Diversification Work Better for Real Estate TDoes International Diversification Work Better for Real Estate Than for han for Stocks and Bonds?Stocks and Bonds?”” Financial Analyst JournalFinancial Analyst Journal, 1996, 52:1, 56, 1996, 52:1, 56--62.62.EicholtzEicholtz, P. , P. ““Real Estate Securities and Common Stocks: A First International Real Estate Securities and Common Stocks: A First International LookLook””Real Estate FinanceReal Estate Finance, 1997, 14:1, pp. 70, 1997, 14:1, pp. 70--74. 74. EicholtzEicholtz, P. , P. ““The Stability of the CovarianceThe Stability of the Covariance’’s of International Property Share s of International Property Share ReturnsReturns””, , Journal of Real Estate ResearchJournal of Real Estate Research, 1996, 11:2, pp. 149, 1996, 11:2, pp. 149--58.58.EicholtzEicholtz, P., and K.G. , P., and K.G. KoedijkKoedijk, , ““International Real Estate Securities IndexesInternational Real Estate Securities Indexes””,, Real Real Estate FinanceEstate Finance, 1996, 12: 4, pp. 42, 1996, 12: 4, pp. 42--50.50.EicholtzEicholtz, P., H. , P., H. OptOpt’’VeldVeld and S. and S. VestbirkVestbirk, , ““Going International: Liquidity and Pricing in Going International: Liquidity and Pricing in the Largest Public Property Marketsthe Largest Public Property Markets”” Real Estate FinanceReal Estate Finance, 1999, 16:3, pp. 74, 1999, 16:3, pp. 74--81. 81. EicholtzEicholtz, P., R. , P., R. HuismanHuisman, K. , K. KoedijkKoedijk and L. and L. SchuinSchuin, , ““Continental Factors in Continental Factors in International Real Estate ReturnsInternational Real Estate Returns”” Real Estate EconomicsReal Estate Economics, 1998, 26:3, pp. 493, 1998, 26:3, pp. 493--509.509.GeltnerGeltner, D. and N. Miller, , D. and N. Miller, Commercial Real Estate Analysis and InvestmentCommercial Real Estate Analysis and Investment, , Southwestern Pub. 2001.Southwestern Pub. 2001.GeurtsGeurts, T.G. and A.J. Jaffe, , T.G. and A.J. Jaffe, ““Risk and Real Estate Investment: An International Risk and Real Estate Investment: An International PerspectivePerspective”” Journal of Real Estate ResearchJournal of Real Estate Research, 1996, 11:2, pp. 117, 1996, 11:2, pp. 117--30.30.Gordon, J, and T Canter, “International Real Estate Securities: Gordon, J, and T Canter, “International Real Estate Securities: A Test of Capital A Test of Capital Markets Integration”, Markets Integration”, Journal of Real Estate Portfolio ManagementJournal of Real Estate Portfolio Management, 1999, 5:2, 161, 1999, 5:2, 161--170.170.Gordon, J, T Canter and J. Webb, “The Effects of International RGordon, J, T Canter and J. Webb, “The Effects of International Real Estate Securities eal Estate Securities on Portfolio Diversification”, on Portfolio Diversification”, Journal of Real Estate Portfolio ManagementJournal of Real Estate Portfolio Management, 1998, 4:2, , 1998, 4:2, 8383--91.91.

ReferencesReferencesHamelinkHamelink, F. and M. , F. and M. HoesliHoesli, “What Factors Determine International Real Estate Security , “What Factors Determine International Real Estate Security Returns?” Returns?” Stockholm Institute for Financial ResearchStockholm Institute for Financial Research, No. 7, 2002., No. 7, 2002.Henderson Global Investors Research Report, A. Schofield, ManagiHenderson Global Investors Research Report, A. Schofield, Managing Editor, “The Case for ng Editor, “The Case for Going Global” July, 2000. Going Global” July, 2000. [email protected]@henderson.comHoesliHoesli, Martin, Jon , Martin, Jon LekanderLekander and and WitoldWitold WitkiewiczWitkiewicz “International Evidence on Real Estate as a “International Evidence on Real Estate as a Portfolio Diversifier” October, 2002, working paper, University Portfolio Diversifier” October, 2002, working paper, University of Geneva, and Aberdeen Property of Geneva, and Aberdeen Property Investors, Investors, [email protected]@hec.unige.chJames D. Peterson and C. H. Hsieh, James D. Peterson and C. H. Hsieh, ““Do Common Risk Factors in the Returns on Shares and Do Common Risk Factors in the Returns on Shares and Bonds Explain Returns on Bonds Explain Returns on REITsREITs??””, , Property EconomicsProperty Economics, 25, 321, 25, 321--345.345.Kelly, J., T. Bellman and C. Kelly, J., T. Bellman and C. BastoniBastoni, , ““Rising Urban Stars Rising Urban Stars –– Uncovering Future WinnersUncovering Future Winners”” Jones Jones Lang LaSalle Research, May, 2003. Lang LaSalle Research, May, 2003. [email protected]@eu.joneslanglasalle.comKengKeng, Tan Yen , Tan Yen ““Inclusion of International Real Estate in Real Estate PortfoliosInclusion of International Real Estate in Real Estate Portfolios”” presented April, presented April, 2003, ARES, working paper, University of Western Sydney, 2003, ARES, working paper, University of Western Sydney, [email protected]@uws.edu.auKuhle,JKuhle,J., C. Walther and C. ., C. Walther and C. WurtzebachWurtzebach, , ““The Financial Performance of Property Investment The Financial Performance of Property Investment TrustsTrusts””, , Journal of Property Research, Journal of Property Research, 1986, 1, 671986, 1, 67--75. 75. LiangLiang, Y. and N. Gordon. , Y. and N. Gordon. ““A BirdA Bird’’s Eye View of Global Real Estate Marketss Eye View of Global Real Estate Markets””, Prudential Real , Prudential Real Estate Investors Research, March, 2003. Estate Investors Research, March, 2003. www.prei.comwww.prei.comLing, D. and A. Ling, D. and A. NaranjoNaranjo, , ““Commercial Real Estate Performance: A Cross Country AnalysisCommercial Real Estate Performance: A Cross Country Analysis””Journal of Real Estate Finance and EconomicsJournal of Real Estate Finance and Economics, 2002, 24:1/2, 119, 2002, 24:1/2, 119--42.42.Liu, C. and J. Liu, C. and J. MeiMei, , ““The Predictability of International Real Estate Markets, ExchangThe Predictability of International Real Estate Markets, Exchange Risks and e Risks and Diversification ConsequencesDiversification Consequences”” Real Estate EconomicsReal Estate Economics, 1998, 26:1, 3, 1998, 26:1, 3--39.39.Liu, Liu, HartzellHartzell, T. Grissom and , T. Grissom and W.GreigW.Greig, , ““The Composition of the Market Portfolio and Property The Composition of the Market Portfolio and Property Investment PerformanceInvestment Performance””, , Real Estate EconomicsReal Estate Economics, 1990, 18, 49, 1990, 18, 49--75.75.LowreyLowrey, C.F. , C.F. ““A Framework for Constructing International Real Estate PortfolioA Framework for Constructing International Real Estate Portfolioss””, Prudential Real , Prudential Real Estate Investors Research, February, 2002. Estate Investors Research, February, 2002. www.prei.comwww.prei.comLu, K.W. and J.P. Lu, K.W. and J.P. MeiMei, , ““The Return Distributions of Property Shares in Emerging MarketsThe Return Distributions of Property Shares in Emerging Markets””, , Journal of Real Estate Portfolio ManagementJournal of Real Estate Portfolio Management, 1999, 5:2, 145, 1999, 5:2, 145--60.60.McAllister, P. McAllister, P. ““Globalization, Integration and Commercial Property: Evidence froGlobalization, Integration and Commercial Property: Evidence from the U.K.m the U.K.””, , Journal of Property Investment and FinanceJournal of Property Investment and Finance, 1999, 17:1, 8, 1999, 17:1, 8--26.26.