Embed Size (px)

Citation preview

Internship report on Bank Alfalah

Internship Report: BANK ALFALAH LIMITED

SUBMITTED TO:

Internship CoordinatorIMS, BZU MULTAN

SUBMITTED BY: Natasha Rafiq

BB-08-11

BBA(HONS) 7TH Semester

Institute of Management Science, BZU Multan

Institute of management Sciences, BZU. Page 1

Internship report on Bank Alfalah

Acknowledgement

First of all I want to pay my gratitude to Almighty Allah who has enabled me to

successfully accomplish my internship in Bank Alfalah Limited.

I am very grateful to the whole team working over there in the organization that have

provided me the opportunity to explore the practical applications of the techniques and

methodologies concerned with the banking. All the department in charges and managers are very

kind and helping especially, Ma,am Qudsia Mazhar from Accounts Deptt, Mr. Amanullah Malik

from credit administration department have helped me a lot during my stay in the bank as an

internee.

Finally, I want to acknowledge Mr. Muhammad Saqib (Branch Manager) who has guided

me all the way through my internship time and stay in the organization for eight weeks. His

guidance leads me to the awareness of hidden aspects of the banking sector and practices.

Institute of management Sciences, BZU. Page 2

Internship report on Bank Alfalah

LIST OF CONTENTS

Institute of management Sciences, BZU. Page 3

Internship report on Bank Alfalah

Institute of management Sciences, BZU. Page 4

Internship report on Bank Alfalah

INTRODUCTION:

Following privatization, Bank Alfalah emerged as new identity of Habib Credit and

Exchange Bank with a revived purpose and commitment. Charged with the strength of Abu

Dhabi consortium and under the leadership of his Highness Sheikh Nahayan Mabarak Al -

Nayayan, the bank has already made significant conditions in building and strengthening both

corporate retail-banking sectors in Pakistan.

Designing the product portfolio of bank response to the customer’s preferences, the

product like Royal Profit, Royal Patriot and Royal Custodial are prime examples of quality and

innovation providing timely banking opportunities to customers of bank.

Assessment of the needs and wants of the customers is an on going process at Bank

Alfalah, which helps to continually develop new products and services. To continuously offer

courteous, professional and advanced banking solutions, the team of bank has recently been

rejuvenated by going though training programs with a focus on information technology.

To make their banking solutions become accessible to more and more people, they have

embarked upon a rapid expansion program, aiming to provide a networking that makes the

services available to any of their customers in all the major urban centers of Pakistan with a view

to go international in the future.

With their key indicators of progress already soaring to new heights, the bank is

committed to dedicate all its energies, resources and time to bring higher value and satisfaction

to their customers, employees and shareholders.

Institute of management Sciences, BZU. Page 5

Internship report on Bank Alfalah

The graph of bank is going up and up every year. The ratio of profit is increasing at good

percentage. The bank is serving the people at high level of standards by going according to the

wishes of the customers.

BRIEF HISTORY:

Bank of Credit & Commerce International (BCCI) was a Pakistan based bank, established by

Mr.Agha Hassan Abdi from UBL, in association with U.A.E and Europe. BCCI has its branches in 74

different countries of the world. It had its 3 branches in Pakistan. In 1991, the BCCI was banned, when it

was accused by European countries, that the bank was involved in some illegal operations with Gulf

countries. The major reason behind European accusation was that BCCI was of Islamic mode. Therefore,

the bank was closed due to international pressure. Then, its 3 Pakistani branches were taken over by the

Government of Pakistan, which were named as Habib Credit and Exchange Bank (HCEB) and these were

working as subsidiary of Habib Bank Limited.

Following the privatization in July 1997, Habib Credit and Exchange Band assumed the new

identity of Bank Alfalah on February 25, 1998. It is now Abu Dhabi based bank as the family of Sheikh

Nahayan Mubarik Al Nahayan purchased 70% of its shares and 30 % shares remained with Habib Bank

on behalf of Government of Pakistan.

It has its 362 branches in Pakistan. Alfalah has emerged as one of the leading commercial banks

in the financial sector of Pakistan. Charged with strength of Abu Dhabi group and under the leadership of

his highness Sheikh Nahayan Mubarak, minister of higher education and scientific research and

prominent member of Royal family. The bank is energized with vision, envisaging.

The bank has already made significant contribution in building and strengthening both corporate

and retail banks sector in Pakistan. Assessment of the needs and wants of customer is an on going process

at Bank Alfalah, which help to centennially develop new products of services. Designing the product

portfolio in response to royal patriot, royal custodial, Alfalah car finance, Alfalah rupee traveler

Institute of management Sciences, BZU. Page 6

Internship report on Bank Alfalah

cheques home loans are prime example of quality innovation providing timely banking

opportunities to customer. To continuously offer courteous, professional and advanced banking

going through training programs with focus to information technology has recently rejuvenated

solution the team of bank.

VISION STATEMENT:

“To be the premier organizations operating locally &

internationally that provides the complete range of financial

services to all segments under one roof”

MISSION STATEMENT :

“To develop & deliver the most innovative products, manage

customer experience, deliver quality service that contributes to

brand strength, establishes a competitive advantage and enhances

profitability, thus providing value to the stakeholders of the bank”.

CREDIT RATING :

Institute of management Sciences, BZU. Page 7

Internship report on Bank Alfalah

“The Bank Alfalah Limited's long term rating increased to AA in the long term and A1+ in the short term. These ratings have been assigned by PACRA, Pakistan's leading rating agency. These ratings denote better risk absorption capacity stemming from enhanced equity as well as well maintained credit portfolio.

PROUCTS & SERVICES: ATM

ONLINE

CREDIT CARD

CAR FINANCING

TREASURY & INVESTMENT

RUPEE TRAVELERS CHEQUE

FOREIGN TRADE & CORRESPONDENT BANKING

ATM(automatic teller machine):Bank Alfalah through its commitment to provide superior and

improved services to its valued customers, has unveiled a nationwide

network of ATMs. For your convenience, you now have access to

instantaneous cash availability, 24 hours a day, 7 days a week.

Our ATM network is geared up to exploit the latest technology, and is equipped to meet the

highest standards of security and efficiency.

Withdraw Cash

Use our convenient, user-friendly fast cash option

Make a Balance Inquiry.

Institute of management Sciences, BZU. Page 8

Internship report on Bank Alfalah

Get an instant printout of your account balances

Get a printout of your last transactions (Mini-statement) on the spot.

Change your PIN (Personal Identification Number).

Bank Alfalah is pleased to introduce 55 state of the art ATMs, deployed at the most

convenient and accessible locations. Bank Alfalah is a founder member of the 1-Link

Switch, thus making a countrywide network of ATMs available

Online: Bank Alfalah now offers the facility of on-line banking to its

customers through its countrywide network of branches.

Customers can use the ATMs or the banking counters of any

branch for day-to-day banking needs, irrespective of branch

where they maintain their accounts. For Corporate customers

centralized Cash Management facility is also offered through on-

line banking.

Credit Card: Bank Alfalah Credit Card is your partner everywhere and is

globally accepted and welcomed at locations displaying the

VISA logo. It is accepted at nearly 30 million merchants

and 1 million ATMs in more than 150 countries around the

globe and over 10,000 establishments in Pakistan.

Alfalah VISA let’s you pay for shopping, travel, entertainment, meals and much

more. Card members are facilitated through a number of promotions from time to

time. In addition, there are a number of strategic business partnerships with leading

local and international brands for purchase of home appliances at exciting Step-BY-

Step (SBS) monthly installment plan with free home delivery at lowest interest rates

Car Financing:

Institute of management Sciences, BZU. Page 9

Internship report on Bank Alfalah

Alfalah Car Financing is specially designed for you with easy affordable and flexible

installment plan. Lowest turnaround time, best rates and unmatched

convenience typically characterize this product. As one of the market

leaders, presently the focus remains on innovation and quality. For the

convenience of our customers we have initiated strategic partnerships with leading insurance

companies that offer our clients special high vale rates.

Treasury & Investment:

1. Money Market

a. Short term money market inter-bank trading.

b. Active Treasury Bills trading in secondary market.

c. Forward – forward inter-bank money market trading.

d. Money market linked lending to and borrowing from corporate clients

2. Foreign Exchange Market

a. Active trading in ready and forward USD/PKR.

b. Active quotations of foreign exchange rates in fifteen major currencies.

c. Information in respect of prevailing rates of most of the currencies of the world

for corporate clients and individuals.

d. Forward – Forward foreign exchange rates of USD/PKR.

e. Active swap trading in USD/PKR and other major currencies such as EUR, GBP,

JPY and CHF.

3. Investment

a. Active Investment in treasury bills (TBs)

b. Active Trading in Pakistan Investment Bonds (PIBs).

c. Active investment in Certificate of Investment (COIs)

Institute of management Sciences, BZU. Page 10

Internship report on Bank Alfalah

d. Active investment in Terms Finance Certificates (TFCs)

4. Government Securities

a. Efficient service for individuals and corporate clients for buying and selling

government securities on their appropriate requests

5. Custodianship

a. Investment Securities Portfolio Accounts of Customers for holding on their behalf

Treasury Bills, Pakistan Investment Bonds.

6. Financial Advisory Services

a. Briefing on current information available in market in respect of prevailing rates

of USD/PKR.

b. Briefing on current information available in market in respect of foreign exchange

rates of major foreign currencies.

o Future expectations and sentiments on major foreign currencies including Pak. Rs.

RUPEE TRAVELERS CHEQUE :

Bank Alfalah presents Rs.1,000, 5,000 and 10,000

denominations of travelers cheque, making it very convenient

to carry money while traveling or keeping your emergency cash safe. Bank Alfalah travelers

cheque are your best travel companion as they provide the most benefits that no other traveler’s

cheque offer. Alfalah TCs have unmatched security features Plus, you don't have to be an

account holder to avail these benefits! Free from the risk and hassle of carrying cash

Institute of management Sciences, BZU. Page 11

Internship report on Bank Alfalah

during travel, Bank Alfalah TCs ensure safe and smooth travel. An excellent combination that

no other TC can contest

Foreign Trade & Correspondent Banking:

Inspired by a challenging spirit and an unyielding desire to create

a sound and reliable networking of correspondent relationships, the bank

has placed great emphasis towards it growth. Accomplishing something

for the first time requires a special focus. It demands foreseeing

possibilities. In our endeavor, to do so, we successfully surmounted

problems and difficulties arising out of issues relating to weak economic conditions of the

economy and a continuous deteriorating status of country risk.

The incertitude and skepticism of the international banking community towards financial

institutions from emerging markets remained intact. Our persistence during the past four years

allowed us to make significant inroads into the arena of correspondent banking. Large

international banks, after critically evaluating us, agreed to enter into relationship.

During 2002 we added 81 banks to our network of correspondents, bringing the total number over 170. Of these relationships, there are now several banks that rank amongst, the top financial institutions in the world. Our geographical coverage now extends to over 100 countries, which is adequately compatible with our trade flows.

Our correspondents, during the year extended us unqualified support, which enabled us to undertake a healthy quantum of foreign trade business. There are many challenges ahead for the bank, in the coming year, our bank will not only continue to review its efforts on existing correspondents to make the relationship more beneficial, but will also add more correspondents to establish a comprehensive international networking to facilitate our customer’s transaction as well as the Bank’s proprietary needs. We have provided against the list of correspondents their world and country ranking. These ranking have been taken from The Bankers Almanac – July 2001 issue.

Institute of management Sciences, BZU. Page 12

Internship report on Bank Alfalah

We would like to emphasize that correspondent arrangements do not necessarily imply the existence of account relationship. We are in the process of rationalizing our current account relationships. We shall continue to open new accounts in various currencies based on our trade flows and business requirements.

JOB DESCRIPTION : I did my internship at Bank Alfalah Limited, Bosan Road Multan. There I worked in

different departments. I started up with Credit Department, where I learned about credit procedures of bank Alfalah under the supervision of credit manager Mr.

Amanullah Malik. This branch is just dealing for small and medium enterprise. Then I worked Accounts Department where I Worked under Mis Qudsia Mazhar . After

working in Accounts I worked in Account opening. The in charge of this department is Mr.Mazhar Abbas. Then I worked in remittances under the supervision of Mr.

Salman Safri. In last I worked in customer dealing area

Staff:

Name Designation:Mr. Saqib Branch manager

Mr.Amanullah MAlik Credit mangerMr.Nasir Riaz Operation manager

Mr.Mushtaq Bhutta Chief cash tellerMs Javeria Sadat Cash officer

Ms Qudsia Mazhar Account officerMr. Mazhar Abbas CRO

Ms Rabia HR in chargeMr.Salman Safri Remittances officer

Institute of management Sciences, BZU. Page 13

Internship report on Bank Alfalah

Account Opening Department :

During my stay in this section, I learnt how to open a new account? How to give

information to a new client? What are the requirements that should be filled before opening an

account and how to issue Cheque books?

Opening an Account

By opening an account at a bank a person becomes a customer of the bank. There are seven different types of accounts.

1. PLS / Saving Accounts

2. Current Account

3. Royal Profit

4. Basic Banking

5. Alfalah Kifayat

6. Alfalah Mahana Amdan

7. Alfalah Kmyab karobar

PLS / Saving Accounts:

Minimum account opening requirement of Rs. 5,000 only.

No restriction on number of withdrawals and number of deposits.

Profit on saving accounts is credited to the customer account on half-yearly basis.

Institute of management Sciences, BZU. Page 14

Internship report on Bank Alfalah

Current Account:

Non interest bearing checking account.

Minimum account opening requirement of Rs. 10,000 only.

Debit card can be used to withdraw cash and make purchases at thousands of outlets across Pakistan which provides access to funds 24 hours a day.

No restriction on number of withdrawals and on number of deposits

Royal Profit Account:

Minimum Deposit requirement of Rs. 50,000 only.

Higher returns on higher balances.

No restriction on number of withdrawals and on number of deposits.

Debit card can be used to withdraw cash and make purchases at thousands of outlets across Pakistan which provides access to funds 24 hours a day.

Profit is credited to the customer account on monthly basis.

Basic Banking account:

Initial deposit for account opening is Rs. 1,000 with no minimum balance requirement. Maximum 2 deposits & 2 withdrawals through cheque is allowed. No restriction on ATM withdrawal.

Any Pakistani resident can open this account. This account is for individual/joint customers only. Other customers like companies, corporate etc are not eligible for opening of this account.

Minimum balance requirement for opening this account is Rs. 10,000/- and no maximum limit

Institute of management Sciences, BZU. Page 15

Internship report on Bank Alfalah

Customers can withdraw funds whenever they like. There is no restriction on number of withdrawals.

Alfalah Mahana Amdan

Minimum placement limit is Rs. 100,000/- and maximum placement limit is Rs.15,000,000/-

Expected Rate of profit is 10% Per annum (as per PLS governing rules)

Profit will be automatically credited on the 1st working day of each month into customers Current/PLS/RP/BBA account

Free Personal Accident Insurance coverage up to the deposit amount or Rs. 1,500,000/- whichever is lower.

Customer can avail financing facility up to 90% of the deposit(as per banks policy)

Any Pakistani resident over the age of 18 can open this account

Alfalah Mahana Amdan term deposit can be maintained only at any one BAL branch with a maximum cap of Rs. 15 Million. An undertaking shall be obtained from the customer certifying that he/she is not availing Alfalah Mahana Amdan Term Deposit Receipt facility from any other BAL branch.(included in AOF)

Alfalah Mahana Amdan TDR will be issued for three years tenure with auto renewal facility of principal amount i.e. the facility will be renewed automatically on maturity (i.e. 3 years)

Alfalah Mahana Amdan TDR will be subject to Zakat, Withholding Tax as well as any other applicable taxes

Alfalah Kamyab Karobar:

Online Current Account

Bank Alfalah presents Alfalah Kamyab Karobar (KK) - a structured, branded, tier-based current account that caters to your banking needs & aspirations. This product will provide

Institute of management Sciences, BZU. Page 16

Internship report on Bank Alfalah

you the opportunity to enjoy free services alongside state of the art banking facilities, linked directly to the deposit balances in your KK account.

Alfalah KK Account can be opened with minimum deposit requirement of Rs 25,000, while the degree of free services will be dependent on the minimum thresholds of respective tier.Its will give you the power to choose from different tiers and avail banking facility from any of the Alfalah branches – PAN Pakistan.

KK Accounts have strategically been tailored into 3 different tiers, allowing you to choose the allotted free service to your benefit. The three tiers are as following:

Silver Gold Platinum

The unique tier based structure ensures that you can avail smooth & cost efficient facilities based on your current level of deposits i.e. Higher the deposit, higher the number of free services.

Some of the Salient features include (tier-based):

Free Online Transactions Free SMS Debit Alert (Subject to availability) Free PO/DD Free Accidental Cover( Valid for up to two People) Free cash deposit across Pakistan Gold VISA debit/ATM Card with every account

Institute of management Sciences, BZU. Page 17

Internship report on Bank Alfalah

Requirements of Account opening

These types of accounts can be opened.

i. Individual Accounts

1. Business Man

2. Student

3. House hold

4. Salary Person

ii. Sole Proprietorship Account

iii. Partnership Accounts

iv. Company Accounts

The requirements of these accounts are as follows

1. Individual Accounts

National Identity Card of the account holder.

If signatures of the account holder are very easy then three passport size photographs

NIC of Next to Kin

Reference (Introducer must be account holder of Alfalah bank limited and operate

account from last six month)

For Salary account

Same as above and also attach a letter from a company in which mention date of joining, designation and per month salary.

For student account

Same as above and also attach a letter by university, in which mentioned the degree

Institute of management Sciences, BZU. Page 18

Internship report on Bank Alfalah

program and session (To____ From____)

2. Sole Proprietorship Account

National Identity Card of the account holder.

If signatures of the account holder are very easy then three passport size

photographs

NIC of Next to Kin

Reference (Introducer must be account holder of Alfalah bank limited and

operate account from last six month)

Application on Business Letter pad.

Stamp of business. (Same Spell as Letter pad and also write proprietorship)

3. Partnership Accounts

National Identity Card of the Partnership.

If signatures of the account holder are very easy then three passport size photographs

NIC of Next to Kin

Reference (Introducer must be account holder of Alfalah bank limited and operate

account from last six month)

Application on Business Letter pad.

Stamp of business. (Same Spell as Letter pad and also write Partnership)

Copy of National Tax Number

Partnership deed

If Partnership register then Form C issue by Government.

4. Company Accounts

In this case the following documents are required

Institute of management Sciences, BZU. Page 19

Internship report on Bank Alfalah

Copies of NIC of Directors of the company

Certificate of incorporation of business

Certificate of commencement of business (In case of Public Limited Company)

Article and Memorandum of Association

Latest copy of Form-29

List of Directors

Copy of Board Resolution

Copy of National Tax Number

Procedure of opening the account

The procedure of opening the account is as follows.

Account Opening Form:

First of all, the customer fills the account opening form (AOF). Filling of account

opening form includes type of account, currency of account, name, address, signature of

customer and signature of introducer and attach a photocopy of national identity card.

He also signs an undertaking that he will follow the rules and regulations of the bank.

Introduction:

The signature and account number of the account holder introducing the account to the

new person is obtained on the account opening form. The operational manager of the

branch verifies it.

Specimen Signature Card:

The signature of the client is obtained on a specimen signature card (S.S Card). The card

is obtained with two signatures from the customer. Every time a cheque is received for

payment from the client, the signature on the cheque is verified by comparing it with S.S

Institute of management Sciences, BZU. Page 20

Internship report on Bank Alfalah

Card.

Requisition slip

A requisition slip for Chequebooks is also given to the customer. The customer fills it and gives it to the account opener.

Know Your Customer Form

Every account holder fills this form. The basic purpose of this form is to get some information about the customer.

Account Number:

When all the formalities are completed, an account number is allotted to the customer

and all the information is entered into the computer and register. Then that account

number is written on S.S Card and account opening form.

Depositing of amount in account:

The client deposit cash in the account. For this purpose cash pay-in-slip is used. The

minimum initial deposit is fixed for each account according to the nature of account.

If PLS / saving account the minimum requirement is Rs.5,000 only.

If Current account the minimum requirement is Rs.10,000 only.

Issuance of a Cheque Book:

After opening an account with the bank, the account holder makes a request in the name

of the bank for the issuance of chequebook. Such a request is known as Requisition Slip.

BAL issues chequebook of at least 10 leaves and maximum 50 leaves. When he used

this book completely then he can apply for another. This process takes a day because the

Institute of management Sciences, BZU. Page 21

Internship report on Bank Alfalah

Chequebooks come from Karachi head office.

Closing of accounts:

The procedure of closing of account is as follows.

First of all the customer gives the request to close the account.

His signatures are verified.

He withdraws all his money from his account but in case of current account Rs. 150

is deducted as a charge of closing the account.

A liability form is send to the credit department if he has taken a loan from the bank.

If he is cleared from all the liabilities then further proceeds are taken.

Permission is granted by the authorized person (the manager).

Account is closed in the computer system.

Hic specimen signature card is attached with the account opening form and marked

closed.

ClearingIn the clearing I Learned from MR Salman . The basic function of the clearing

department is to facilitate the customer; it provides them the services in collection of their

cheque in other banks. CLEARING actually means the transfer of funds from one branch of bank

Institute of management Sciences, BZU. Page 22

Internship report on Bank Alfalah

to the other branch of the same bank or the other bank on which the instrument is drawn, without

involving cash through State banks clearing house.

NIFT:

NIFT stands for National Institutional facilitation Technologies. Clearing House of SBP has

shifted a tiresome part of its work to a private institution named NIFT. NIFT collects cheque,

demand drafts, Pat orders, Travelers Cheque, etc. from all the branches of different banks within

city through its carriers and send them to the branches on which these are drawn for clearing.

After the branches approve the instruments drawn on them, NIFT prepares a sheet for each

branch showing the number for instruments and amount in its favor and drawn on it and sends it

to each branch. A similar sheet for each bank is also sent to clearing house of SBP where

accounts of banks are settled in the same manner.

The instruments are collected from the client. Following things are checked.

Cheque date (a cheque is valid for six months and it should not be post dated).

Title of Account

Amount in figures and words should be same

There should be no cutting and overwriting on the cheque.

Deposit should also match with the cheque.

Stamping Procedure:

In stamping procedure, the pay-in-slip counter foil the following three stamps are used. If

the cheque is for the same bank, and drawer and the payee both have the account in the same

bank, the simple bank stamp is used, and this stamp indicates the transfer of cheque from one

account to another account. This cheque is directly moves towards posting in computer terminal

where the computer operator debit one account and credit the account of another party. This

stamp is known as the Transfer stamp.

Institute of management Sciences, BZU. Page 23

Internship report on Bank Alfalah

If the cheque is received from other bank and drawer’s account is not in the bank then cheque

received stamp is used. This cheque is represented in the clearinghouse; date is also mentioned

on the stamp. If the cheque is from out of the city then it is send for the collection.

Stamping On Cheque:

After receiving the cheque and issuance of the counter foil to the client, stamping process

starts on the cheque; the following stamps can be used.

a) The name and branch name of the bank stamp is used on the front side of the cheque.

This stamp is used on all types of cheque. This stamp is known as crossing stamp.

b) The second stamp used is the clearing stamp on the front side of the cheque. It also

indicates the presenting date of the cheque. If the cheque is dishonored and deposited

again for clearing, the clearing stamp is used again with new date of presenting. So

the clearing stamp is necessary wherever the cheque is presented for clearing.

c) The third necessary stamp, which is the endorsement, indicates the paying bank to

“payees account credited”. It is the confirmation of outward clearing.

The whole clearing process requires about 2 days, after 2 days the customers’ account is

credited and the customer can make the transactions.

Remittance: Remittance is transfer of funds from one city to another city or within the city. For this purpose,

most commonly used instruments are

Institute of management Sciences, BZU. Page 24

Internship report on Bank Alfalah

1) Demand Draft

2) Pay Order

3) Telegraphic Transfer

4) Online Transaction

Demand Draft:

A demand draft is an instrument in writing drawn by one branch of a bank on another branch

of the same bank for a certain sum of money; payable on demand to the order of the payee

mention therein the draft.

Issuance of Demand Draft:

The customer makes a request to the banker for a demand draft. The banker gives him/her

an application form to fill and ask him to deposit the amount for which he needs draft. The client

mentioned the name of payee in the favor of which it is to be paid, the name of branch on which

it is drawn and amount of draft on the form and puts his signature on it. Afterwards, he deposits

the amount in cash with the bank. In case he is Account Holder of the same bank, he can give

cheque instead of cash upon which the banker transfers the amount from his account. When all

these formalities are fulfilled, banker issues him a demand draft. Bank takes charges for demand

draft that are different in different banks according to their schedules of charges.

Internal Process:

After issuing demand draft, bank sends a credit advice to the bank on which it is drawn.

Drawer bank after receiving credit advice gives credit to DD payable Account. When DD is

presented on the cash counter, bank pays cash against it after checking N.I.C of payee and debits

DD payable account. If DD is crossed amount is transferred into payees account. Posting is also

made in the computer terminals for the purpose of record of the bank.

Issuance of Duplicate DD:

Institute of management Sciences, BZU. Page 25

Internship report on Bank Alfalah

Bank can issue duplicate of demand draft on clients request after taking charges. The

charges are Rs 100.

Cancellation of DD:

In case, client wants to cancel the draft he has to make an application with his signature.

Banker checks the signature. Amount of draft is returned to client after deducting cancellation

charges. The cancellation charges are Rs 100.

Pay Order:

A pay order is an instrument in writing issued by bank for a certain sum of money

payable on demand to the order of the payee mention within the city, where as pay slip is used

for bank’s internal use.

Issuance of Pay Order:

The client makes a request to the banker for issuance of a pay order. The banker gives

him an application form to fill and ask him to deposit the amount for which he requires the pay

order. The client deposits the amount in cash with bank. If he is account holder of the same bank,

he can give cheque upon which amount is transferred from his account. After the fulfillment of

these entire requirements banker issue the pay order to the customer. Bank takes charges for

issuance of pay order, which varies from bank to bank. Bank Alfalah takes the following

flat charges.

Internal procedure:

Institute of management Sciences, BZU. Page 26

Internship report on Bank Alfalah

After issuing Pay order, banker gives credit Sundry creditors account. Posting is made in

the computer terminal. When Pay order is presented on cash counter bank makes payment

against it after checking N.I.C of payee and Sundry creditors account is debited. If it is crossed,

the amount is transferred into the payees account.

Cancellation and Duplicate issue:

The procedure for cancellation and duplicate issue of pay order is same as that of demand

draft and the charges are also same. The charges for both the services are Rs.100.

Tax:

Government of Pakistan has levied 0.3% advance tax on the issue of Pay orders and

demand drafts. If the customer submits tax exemption form to the bank, he is not charges tax.

But if customer does not submit form, he has to pay 0.3% tax on the amount of pay order or

demand draft.

Telegraphic Transfer:

Telegraphic Transfer is bank-to-bank, and branch-to-branch. The bank has settlement

with other banks according to which the banks can make the payments to the customer’s account

Institute of management Sciences, BZU. Page 27

Internship report on Bank Alfalah

mentioned by the other bank in the TELEX. In this case proper authentication is must for this

purpose.

Process:

Customer obtain a requisition slip and fills it properly

After filling the application from the concerning officer fills the TT form.

This Telegram is send to he required bank.

After receiving the telegram bank immediately makes the payment to the customer and

the vouchers sent to the issuing bank by ordinary mail.

Bank debits the account of the customer or receives cash including charges of the bank.

TT is made through codes. Bank sent telegrams with codes and in banking language

using the words test.

Online Transaction:

For branch-to-branch transfer of funds on the same day, previously TT was used. But

now banks have adopted a new system known as Online Transfer.

In online transactions cheque of different branches can be paid, for instance if a client has

taken Online Transaction facility and presents Multan’s cheque to Bank Alfalah Multan, he/she

can have payment from Karachi. If the cheque has been cleared from Multan Bank Alfalah, a

copy of cheque is made and is faxed to appropriate branch; the branch then checks the client’s

balance, date of cheque and signature of client. If the cheque is given clearance from the

respective branch then payment is made to client, the branch is then debited and the branch that

has made payment is credited.

Institute of management Sciences, BZU. Page 28

Internship report on Bank Alfalah

Accounts Department:Accounts department plays a major role in every bank. In Bank Alfalah the burden of the

accounts department is largely reduced because of computerization. The use of the computer

system increases the efficiency and pace of the bank’s work.

Following activities are carried out in the accounts department:

Bunches

Budgeting

Reports

Funds management

Activity checking

Reconciliation

Foreign exchange, old Account Contracts

Maintenance of fixed assets and calculation of their depreciation

Bunches:

In account office it’s daily work to maintain the bunches as below:

Cash Debit Bunch

o Current Account

o Saving Account

Cash Credit Bunch

o Current Account

o Saving Account

CLG Debit and CLG Credit Bunch

o Current Account and Saving Account Debit

o Current Account and Saving Account Credit

Institute of management Sciences, BZU. Page 29

Internship report on Bank Alfalah

Budgeting:

The main task performed by the accounting department is the preparation of the budget.

Budget is based on forecasting and their own inspiration for future, whereas forecasting is based

on past performance. This is one important task on the basis of which funds are allocated to

various branches and also the targets are determined. The targets determined Deposits,

Advances, and revenues. Every branch prepares its own budget for the fiscal year and then

budgets of all the branches across the country are consolidated at the head office in Karachi. In

this way a consolidated budget is also prepared.

Fiscal year of the bank starts from January to December. Accounting department starts

preparing the budget from October for the next year. Before the preparation of budget the bank

reviews its sources and funds it has and the uses of those sources.

The main sources of the bank are the follows:

Deposits, Capital, Borrowing from other banks, etc

The main uses of a bank are the follows:

Advances, Investment in securities, placement in inter-bank markets,

Other things, which are undertaken into account while formulating the budget, are:

Income, Expenses, etc.

The revenue target is fixed keeping in view the past performance. The cost of generating

these revenues is also estimated. Then budget of each branch is submitted to head office for

modifications and for approval. After the modification and approval the budget for a specific

branch is being set by the head office. Monthly budget meeting is held to analyze the monthly

performance by all the branch mangers with head office. The actual performance is compared

with the estimated and variance is calculated. Variance can be negative as well as positive. If

there is a negative variance, this shows management’s inefficiency in controlling its expenses or

Institute of management Sciences, BZU. Page 30

Internship report on Bank Alfalah

incompetence in achieving the desired revenue targets. Proper adjustments are made in the next

month’s target according to the previous month’s performance because sometimes the goals,

which are set by the head office, are unrealistic and unachievable.

Reports:

In Bank Alfalah many types of reports are being prepared. These are daily, weekly,

monthly, semiannual and annual reports. These are generated from the main frame and are used

for proper analysis. The following reports are generated daily from the main frame which are

being used by the accounts department for the preparation of their own reports:

Statement of affairs:

It includes information about assets, liabilities and their balance. Daily position of deposit

and advances are also calculated in this report.

Subsidiary Statement:

This is a detailed report, which includes all the information regarding the statement of affairs.

Income and Expenditure report:

It includes all the details regarding to both the heads of income and expenditure in detail.

Royal Profit Report:

It includes the details of the deposit of royal profit account.

Currency wise report (ccy):

It provides the details of all the deposits currency wise.

Institute of management Sciences, BZU. Page 31

Internship report on Bank Alfalah

Sub 66 Report:

It contains income, expenditure, general ledger accounts and their balances.

Now following are the reports, which are being prepared with the help of the above reports:

Daily position of advances and deposits:

This report is being sent to the head office daily in which the detail is given regarding the

new accounts of deposits and advances.

Statement of affairs:

This report includes assets and liabilities. Two copies of this report are made daily, one is

sent to the area office and one to the head office for analysis but the format is different for

both of them. Statement of Affairs also prepared at the weekend for the whole week as well

as at the end of a month.

Monthly Budget Review Report:

This report is made to review the performance of the month by calculating the variance. And

then if the variance is in negative, positive actions are taken and reasons will also be

mentioned in the report.

Funds Management:

Every bank in Pakistan has an account with State bank of Pakistan and has to maintain

5% of the total deposit in the account with the State bank. Funds management is done only

through the main branch. If the bank has so many branches in a single city then only the main

branch is responsible for the funds management. Daily a report was prepared and reported to

State bank.

Institute of management Sciences, BZU. Page 32

Internship report on Bank Alfalah

The important factors that affect the report are as follows:

Total Deposit (of all branches in a single city)

Opening Balance (closing balance of the previous day)

Inward Clearing

Outward clearing

Cheque issued by State Bank

Cheque Deposited

After all the calculations, a result is obtained which signifies the cash in hand of the respective day. If the cash in hand is sufficient to fulfill the needs of the State Bank, well and good otherwise if the cash is not sufficient then the other options are considered.

In case of shortage of funds, the main branch has the following options, which it can adopt.

1. TT from Head Office:

2. Cover from Head Office

3. Funds from Other banks

TT from Head Office:

One solution of the problem is to contact and inform head office about our respective

position and demand for funds. However the most frequent reason, why this practice is not

followed is that State bank has allowed only one TT free of cost for all the branches in Pakistan.

Therefore we first have to confirm head office that whether or not it is sending TT to

another branch of bank Alfalah. If the head office sends us the TT then it cannot send any other

TT to another branch of Bank Alfalah without charges. The charges are also not negligible for

Institute of management Sciences, BZU. Page 33

Internship report on Bank Alfalah

example the charges of TT for an amount of one hundred million are above 60,000. For

this specific reason the TT is not encouraged.

Cover from Head Office:

The most frequent option used is to inform Head office about the shortage and ask for

cover. The head office then maintains extra amount in its account with State bank. The extra

amount will be the shortage of main branch reported. The main branch will then pay interest to

the head office on a rate of 11.5% per day. The head office is paid on monthly basis.

Funds from Other banks:

In case of funds shortage another bank is contacted with whom the bank has settlement

for instance Emirates bank. If this option is taken the head office is informed

and the head office then pays to the Karachi branch of the respective bank from which funds are

taken.

Activity Checking:

Activity checking is the process of the entire banking, which has taken place. A report

known as activity report is prepared on daily basis. The report specifies every vouchering, which

has taken place. Sorting is made according to the mainframe-generated report. All the vouchers

are checked that whether they are properly posted or is there any transaction left to be posted.

This checking makes the working of the bank more efficient and avoids any loopholes.

Institute of management Sciences, BZU. Page 34

Internship report on Bank Alfalah

Reconciliation:

BAL prepares its reconciliation statements with

Head Office

State Bank of Pakistan

Head Office Reconciliation:

All the debit and credit entries of the main office account are recorded in the statement.

Then it is checked with physical vouchers and if there is any problem, they reconcile it. Head

office extract are statements sent by branches to the head office. They check the outstanding

entries, if there is any entry posted by branch but not by head office they will send their query to

the branch and branch will respond to that query by sending the required document. Head office

reconciliation is carried out in the head office; accounts department handles inquiries.

State Bank of Pakistan:

SBP maintains the account of every scheduled bank including bank Alfalah. The statement of

account reconciliation shows the entries that are passed during the month in both banks. Bank

Alfalah compares the statement with the ledger card of State bank of Pakistan in which all entries

are recorded done with SBP. If any amount debited by SBP and Bank Alfalah does not credit that

amount, it is added in the balance of the reconcile statement provided by the SBP to BAL.

Institute of management Sciences, BZU. Page 35

Internship report on Bank Alfalah

Maintenance of Fixed Assets and Calculation of their Depreciation:

Account department maintains the record of fixed assets. The accounts department calculates

the depreciation the assets by using straight-line method. Depreciation is the allocation of cost of

the asset over the useful life. Depreciation is accrued on monthly basis and charged at year-end.

Department prepares Asset purchase report and Asset sale report after six months.

Institute of management Sciences, BZU. Page 36

Internship report on Bank Alfalah

CREDITS DEPARTMENT :

The basic function of a bank is to receive deposits (at low rate of return) and to lend

money (at a high rate of return). So, the lending operations of a bank constitute a vital part of its

business. This department is the source of income and earnings for the bank. Bank’s funds

comprises mainly of money borrowed from numerous customers on various accounts such as

saving accounts, current accounts, fixed deposits etc. Whereas the major part of total income of a

bank is generated through the utilization of these funds.

The credit department is further divided into two departments, which are as follows:

Credit Marketing

Credit Administration

As this branch recently started its operations, that’s why credit facilities are not so

advanced. They are just advancing loans to small and medium enterprise.

Processing of Loan:

The banker must be very careful and ensure that his depositor’s money is advanced to

safe hands where risk of loss does not exist. When a customer requests his banker to facilitate

him with different credit facilities, the bankers first assess the credibility of customer and the

market conditions.

The elements of credibility, integrity, repayment, and market conditions help a banker in

arriving at a conclusion regarding the safety of advances.

Credibility:

Institute of management Sciences, BZU. Page 37

Internship report on Bank Alfalah

It is the most important factor in determining the safety of advances, for there is no

substitute for integrity, honesty and trustworthiness. A borrower’s character can indicate his

intention to repay the advance, since his honesty and integrity is of primary importance. If the

past record of the borrower shows that his integrity has been questionable then the banker

usually tries to avoid such a customer.

Repayment:

This is the management ability factor, which tells how successful a business has been in

the past, and what are the future possibilities are. Before advancing loan a banker must be

satisfied with the sources of the repayment of the funds.

Capital:

The bankers also check the capital of the borrower. This can be kept as a security of a

loan. In other words, if the businessman financial Position is sound, only then he can be landed.

CIB Report:

Bank cannot sanction any loan to a customer, until and unless it gets credit report form

CIB (Credit Information Bureau, SBP). Before making any decision about the client, bank needs

a CIB report. Therefore, first of all the bankers requests CIB to provide the credit report of the

client. This report indicates all the credit facilities outstanding (availed) by the client.

Credit Line Proposal (CLP):

After being satisfied with the credibility and integrity of the applicant, the processing of

loan application starts with the preparation of Credit Line Proposal (CLP). It has the vital and

most important task assigned to the credit officers in BAL.

In a CLP, every information regarding the client and his business is stipulated as follows:

Institute of management Sciences, BZU. Page 38

Internship report on Bank Alfalah

Total existing facilities (limit), their outstanding value and the securities that were

provided against these facilities.

Total proposed limit of credit and the securities provided against it. The credit officer

does the analysis and verification of these securities.

Regular Credit Limit:

But if the client wants to route a regular business with the bank, then he requests for

regular credit limit of credit facilities for a specific period. Following things should be

undertaken while preparing a CLP and also being mentioned in the CLP.

Customer’s background, his relationship with the bank (if he is an existing customer),

his relationships with other banks.

Purpose of facility and terms and conditions regarding the client.

Nature of his business and what are the market conditions and opportunities fro the

business.

Reciprocal business is also stipulated on the proposal, which means expected business

that would be routed through the bank for these facilities. Bank calculates his

profitability on the basis of this business.

Institute of management Sciences, BZU. Page 39

Internship report on Bank Alfalah

SWOT ANALYSISBAL is one of the fastest growing banks in Pakistan. In the light of these situations we can make

an analysis.

Strengths:

Bank has a belief in customer service

Backed by strong Abu Dhabi Consortium

Customers give suggestion for the improvement of bank and these suggestions are

listened carefully

.Environment is friendly.

Products are excellent

Modernized banks (online banking)

Fully computerized, each department has to own PC.

Weaknesses:

Although the bank is growing fast but it has some weaknesses which it should remove to make

itself further strong.

Less Advertisement

Slow in introducing new products

Gives its staff less benefits

They should advance their credit techniques in Bosan Road branch.

Institute of management Sciences, BZU. Page 40

Internship report on Bank Alfalah

Opportunities:

Extension of International network of the branches

Introduction of innovative products

Information technology

Establishing foreign branches

Growing market

Threats:

Uncertain economic conditions

Action taken by competitors

Bank Alfalah has major Business deposits. With change of political environment it may

affect the bank.

Institute of management Sciences, BZU. Page 41

Internship report on Bank Alfalah

Financial analysis

BANK ALFALAH LIMITEDINCOME STATEMENT

2009-2010

Particulars 2009 2010

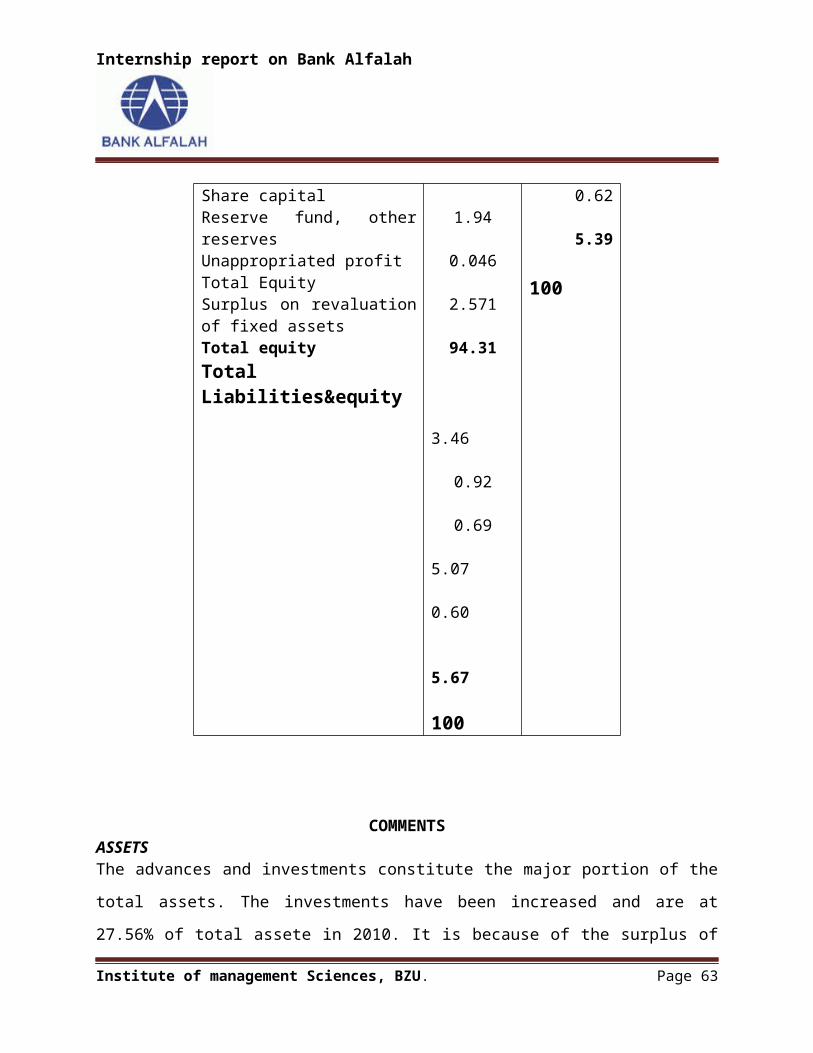

AssetsCash & balances with treasury bankBalances with other banksLending to financial institutionInvestmentsAdvances- net of provisionfixed assetsOther assetsTotal assetsLiabilitiesBills payableBorrowingDeposits & other accountSub ordinate loansDeferred tax liabilitiesOther liabilitiesTotal liabilitiesNet Assets

Presented byShare capitalReserve fund, other reservesUnappropriated profit

Surplus on revaluation of fixed assetsTotal Liabilities & equity

35,056,012

22,722,63914,947,43599,159,957188,042,43814,492,19414,649,380389,070,055

3,766,144 20,653,921 324,759,752 7,570,181 179,851 10,006,786 366,936,635 22,133,420

13,491,5633,587,9692,690,72819,770,2602,363,160

22,133,420

41,197,841

16,179,2556,497,556

113,425,861207,152,54614,204,55512,826,225

411,483,839

4,521,53313,700,124

354,015,3117,567,192

115,9199,258,216

389,178,29522,305,544

13,491,5633819,1332,415,860

19,726,5562,578,988

22,305,544

Institute of management Sciences, BZU. Page 42

Internship report on Bank Alfalah

389,070,055 411,483,839

BANK ALFALAH LIMITEDINCOME STATEMENT

2009-2010

Particulars 2009 2010

Mark up/interest incomeMinus: Mark up/interest expenseNet interest incomeMinus: ProvisionsNet mark up income after provisionPlus: non markup interest incomeGross incomeMinus: operating expense

Profit before taxationMinus: income taxProfit after taxation

35,561,31224,654,18010,907,1324,071,5276,835,6055,182,253

12,017,85811,001,542

1,016,316119,281897,035

37,530,25623,855,44813,674,8084,260,3839,414,4254,708,161

14,122,58612,753,841

1,368,745400,293968,452

Institute of management Sciences, BZU. Page 43

Internship report on Bank Alfalah

Vertical analysis of balance sheetBANK ALFALAH LIMITED

INCOME STATEMENT2009-2010

Particulars 2009In %

2010In %

AssetsCash & balances with treasury bankBalances with other banksLending to financial institutionInvestmentsAdvances- net of provisionfixed assetsOther assetsTotal assetsLiabilitiesBills payableBorrowingDeposits & other accountSub ordinate loansDeferred tax liabilitiesOther liabilitiesTotal liabilities

Presented byShare capitalReserve fund, other reservesUnappropriated profitTotal EquitySurplus on revaluation of fixed assetsTotal equityTotal Liabilities&equity

9.01

5.84 3.84 25.48 48.33 3.72 3.76 100

0.96 5.30 83.47 1.94 0.046 2.571 94.31

3.46 0.92 0.69 5.07 0.60

5.67 100

10.01

3.931.57

27.5650.343.453.11100

1.093.32

86.031.830.022.24

94.53

3.270.920.584.770.62

5.39 100

Institute of management Sciences, BZU. Page 44

Internship report on Bank Alfalah

COMMENTSASSETSThe advances and investments constitute the major portion of the total assets. The investments

have been increased and are at 27.56% of total assete in 2010. It is because of the surplus of

revaluation, which has resulted due to the increase in the value of government securities and

shares of public limited companies (where BAL had invested).

The portion of advances has increased by the year. This is a healthy sign and shows that the

business is expanding.

LIABILITIESOn the liability side, deposits and borrowings are the major accounts. The percentage of deposits

is increasing whereas percentage of borrowings decreasing.

Despite of the considerable increase of % (aprox.) in deposits, the decrease in % of deposits to

total liabilities is due to the increase in total liabilities resulted due to the increase in deposits

from other banks. Since, the bank is on its way to expansion and for the purpose of expansion it

needs to have borrowing. Therefore increase in total liabilities is not that much alarming.

Institute of management Sciences, BZU. Page 45

Internship report on Bank Alfalah

Vertical analysis of income

statements

BANK ALFALAH LIMITEDINCOME STATEMENT

2009-2010Particulars 2009 2010

Mark up/interest incomeMinus: Mark up/interest expenseNet interest incomeMinus: ProvisionsNet mark up income after provisionPlus: non markup interest incomeGross incomeMinus: operating expense

Profit before taxationMinus: income taxProfit after taxation

100.0069.3230.6811.4419.2414.5733.8130.93

2.880.332.55

100.0063.5736.4311.3525.0812.5437.6233.98

3.641.062.58

Institute of management Sciences, BZU. Page 46

Internship report on Bank Alfalah

Horizontal analysis BANK ALFALAH LIMITED

BALANCE SHEET2009-2010

Particulars 2010 2009

AssetsCash & balances with treasury bankBalances with other banksLending to financial institutionInvestmentsAdvances- net of provisionfixed assetsOther assetsTotal assetsLiabilitiesBills payableBorrowingDeposits & other accountSub ordinate loansDeferred tax liabilitiesOther liabilitiesTotal liabilities

Presented byShare capitalReserve fund, other reservesUnappropriated profitTotal Equity

Surplus on revaluation of fixed assetsTotal Liabilities&equity

117.52

73.1343.46

114.38110.1698.0187.55

105.76

112.8866.33

109.0099.9664.4592.51

106.06

100106.4489.7899.77

109.13

105.76

100

100100100100100100100

100100100100100100100

100100100100

100

100

Institute of management Sciences, BZU. Page 47

Internship report on Bank Alfalah

Horizontal analysis BANK ALFALAH LIMITED

INCOME STATEMENT2009-2010

Particulars 2010 2009

Mark up/interest incomeMinus: Mark up/interest expenseNet interest incomeMinus: ProvisionsNet mark up income after provisionPlus: non markup interest incomeGross incomeMinus: operating expense

Profit before taxationMinus: income taxProfit after taxation

105.56103.34125.37104.63137.7290.85

117.51115.92

134.67335.58107.96

100100100100100100100100

100100100

Institute of management Sciences, BZU. Page 48

Internship report on Bank Alfalah

Institute of management Sciences, BZU. Page 49

Internship report on Bank Alfalah

PROFITABILITY RATIOS:

1. NET PROFIT MARGIN

PROFIT AFTER TAX / TOTAL REVENUE

2009 = [897035 /16089385] * 100

= 5.57%

2010 = [968452 / 18382969] * 100

= 5.26%

COMMENTSThe net profit margin of the bank shows an decreasing trend. It came down to 5.26 in 2010,even

despite the high profitability before taxes. It was because of the greater amount of tax paid

during the year 2010. Moreover, the denominator i.e. the total revenues have been increasing

continuously which signifies the expanding business operations but a slight difference from

previous year due to great tax expense.

2. RETURN ON EQUITY

NET INCOME / EQUITY RATIO

2009 = [897035 /19770260] * 100

= 4.53%

Institute of management Sciences, BZU. Page 50

Internship report on Bank Alfalah

2010 = [968452/ 19726556] * 100

= 4.90%

COMMENTSThis ratio i.e. return on equity shows the return the owners of the business enjoy after paying all

the financial expenses and other liabilities of the business.

The return on equity increased from 4.5% to 4.90%, which is a reasonable increase and has

resulted due to the growing profits of the banks. In 2010, pre-tax profit has increased almost by

a good amount of previous year’s profit. So, a consistent increase in profit shows a positive and a

very healthy and pleasing news for the owners.

RETURN ON INVESTMENT:

NET INCOME / TOTAL ASSETS

2009= [897035/38907055]*100

=0.24%

2010 = [968452 / 411483839] * 100

= 0.24%

Profit on investment follows the same trend as that of previous year although the assets have

been increased this year but a huge amount of expenses and liabilities this ratio doesn’t show a

considerable increase, either they should employ more assets to increase this ratio or they should

have a reasonable control on liabilities.

Institute of management Sciences, BZU. Page 51

Internship report on Bank Alfalah

NET INCOME / RISK ASSETS

2009 = [897035 / 214250634] * 100

= 0.41%

2010 = [968452 / 249639748] * 100

= 0.39%

ADMINISTRATIVE EXPENSES TO DEPOSITS

[ADMIN. EXPENSES / DEPOSITS]* 100

2009 = [12,578,080/ 354,015,311] * 100

= 3.55%

2010 = [10,923,507/324,759,752] * 100

= 3.36%

COMMENTSThis ratio is very helpful in determining the relationship between the deposits and the costs

associated with maintaining them. The benchmarked figure is 2% to 3% in the banking sector.

The administrative expenses should exceed the level of 3%, for deposits.

Institute of management Sciences, BZU. Page 52

Internship report on Bank Alfalah

The ratio signifies the management’s efficiency and shrewdness of maintaining deposits.

Even decreasing trend, even with the increase in deposits, signifies management’s commitment

and professional outlook.

LIQUIDITY RATIOS

1. FINANCING / DEPOSITS + BORROWED FUNDS

2009 = [188,042,438/ 358,715,435] * 100

= 57.77%

2010 = [207,152,546 / 345,413,673] * 100

= 54.44%

COMMENTSDecreasing trend in the ratio during this year indicates that the bank is utilizing its funds

improperly. So it is not a healthy sign.

Decrease in year 2010, due to the increase in advances. While on the other hand the

borrowed funds have been decreased as compared to last year, or bank should make emphasis on

increasing its deposits, or should lessen its advances.

DUE TO BANKS / TOTAL DEPOSITS

2009 = [20,653,921/324,759,752] * 100

= 18.79%

2010 = [13,700,124 /354,015,311] * 100

Institute of management Sciences, BZU. Page 53

Internship report on Bank Alfalah

= 22.65%

COMMENTSThis ratio signifies the financial mix of bank. In ideal situations, there should be decreasing trend or consistency in this ratio. In case of BAL, although there is significant increase in deposits but borrowing is decreasing

considerably. So to compensate this bank should either increase their deposits or to make a

proportion borrowing should also be increased.

4. DUE FROM BANKS / TOTAL ASSETS

2009 = [22,722,639 /389,070,055] * 100

= 5.84%

2010 = [16,179,255 /411,483,839] * 100

= 3.93%

COMMENTS:This ratio signifies the percentage of receivables in the total assets. In normal practices,

bank usually keeps some of its funds in other banks, as it is safe source of financing. However,

this percentage should not be too high. High percentage would mean that bank is not financing in

open market. But, again it depends upon the market conditions.

In case of BAL, this ratio is quite normal. A reasonable decrease in this ratio is being

observed which is very significant.

Institute of management Sciences, BZU. Page 54

Internship report on Bank Alfalah

DUE FROM BANKS / DUE TO BANKS

2009 = [22,722,639 / 20,653,921]

= 1.1:1

2010 = [16179255 / 13700124]

= 1.18:1

COMMENTSIn ideal situations, this ratio should be 1:1 or more. Whereas, in this case the ratio is

according to the standards. Receivables are greater than payables to banks, which is due to

decrease in bank borrowing. However, there is an increasing trend in this ratio, which shows

better management approach towards liquidity position.

Institute of management Sciences, BZU. Page 55

Internship report on Bank Alfalah

CAPATALIZATION RATIO:

1. CAP. FUNDS / TOTAL ASSETS

2009 = [22133420 /389070055] * 100

= 5.64%

2010 = [22305544 /411483389] * 100

= 5.42%

COMMENTSThe ratio signifies the bank’s contribution of equity in total assets. Strong equity base

indicates the low risk factor. In usual practice of banks, they emphasize more on deposits than

injecting new equity in the business.

In case of Bank Alfalah, the percentage of shareholder’s equity to total assets is almost

consistent. However, the increase or decrease in capital funds is due to surplus or deficit on

revaluation. In year 2010 the equity of bank has been decreased up to a negligible figure but

bank should increase to a reasonable extent.

2. CAP. FUNDS / RISK ASSETS

2009 = [22133420 / 188042438] * 100

= 11.77%

2010 = [22305544 / 207152546] * 100

= 10.76%

Institute of management Sciences, BZU. Page 56

Internship report on Bank Alfalah

3.CAP. FUNDS / TOTAL DEPOSITS

2009 = [22,133,420/324,759,759] * 100

= 6.8%

2010 = [22,305,544/354,015,311] * 100

= 6.3%

COMMENTSThese are very crucial ratio and have great importance especially for the creditors.

These show the long-term solvency of the organization.

In all the capitalization ratios, one thing is common during the two years, that with the

expansion in branch network, and increase in business operations in the form of advances and

deposits, bank’s capital base has been consistent.

It is because, that the bank is on the way of expanding its business and for this purpose

it is relying much on its deposits. But I think that the bank should also increase its level of

reserves to sustain the trust of creditors.

Institute of management Sciences, BZU. Page 57

Internship report on Bank Alfalah

COVERAGE RATIO

EBIT/INTEREST EXPENSE

2009= [12017858/24654180]

=0.48

2010= [14122586/23855448]

=0.59

This ratio tells how easily company can pay its outstanding debt or interest. 1f this ratio is

below 1, it is questionable it means that company is not generating sufficient revenues to satisfy

its expenses, in the case of BAL the ratio is below 1, but consistently increasing as they are

investing more in securities and subsidiaries they are not efficiently covering their interest

expenses.

Institute of management Sciences, BZU. Page 58

Internship report on Bank Alfalah

LEVERAGE RATIOS:

DEBT TO EQUITY RATIO

TOTAL DEBT/SHARE HOLDER’S EQUITY

2009= [389,178,295/19,726,556]

=19.72

2010= [366,936,635/19,770,260]

=18.56

COMMENTS:

This ratio tells that how much creditors are providing against shareholder’s equity, lower trend in

this ratio is considered reasonable, as this ratio is decreasing in current year, but this is a very

slight change, the lower this ratio higher the level of financing is provided by shareholders. But

what I conclude is that bank should its equity capital instead of increasing liabilities

DEBT TO ASSETS RATIO

TOTAL DEBT/TOTAL ASSETS

2009= [389178295/411483832]

=0.94

2010= [366936635/389070055]

= 0.94

Institute of management Sciences, BZU. Page 59

Internship report on Bank Alfalah

COMMENTS:

This ratio highlights the importance of debt financing to firm by showing the percentage of

firm’s assets that is supported by debt financing. 94% debt to equity ratio tells that 94 percent of

banks’s assets are financed with debt financing, while the remaining 6% comes from equity. The

ratio is same for both of the year, but bank should raise its fund in order to lessen this ratio.

MARETABILITY RATIO

PRICE PER EARNING P/E

MARKET PRICE OF SHARE/EARNING PER SHARE

2009=[10.00/0.71]

=13.88

2010= [10.00/.72]

=14.04

COMMENTS:

This ratio indicates the confidence that investors have in the firm’s future performance, higher

this ratio the greater the investor confidence. In the case of BAL there is significant increase in

this ratio current year, so it is s good trend

Institute of management Sciences, BZU. Page 60

Internship report on Bank Alfalah

RECOMMENDATIONS:

After doing internship of 6 weeks in Bank Alfalah Limited, I have analyzed some problem in the

Bank. Following are my recommendations:

Misdistribution of work:

In Bank Alfalah, there is misdistribution of work; some people are over burdened with

the work. So I suggest that there should be fair distribution of work in all the departments.

Participative management:

Participative management concept should be adopted, where ideas from the employees should

also be taken, not only for developing products but also on service, efficiency, employee morale

etc. in order to improve them.

Fax Machines and Photocopying Machine:

The number of Fax machines and photocopying machine in the bank are also less than

they are needed. For photocopying one has to go downstairs. So there should be more machines

and also their placement should be at the right place.

Training programs

Institute of management Sciences, BZU. Page 61

Internship report on Bank Alfalah

BAL should introduce more training programs for their employees. It will help less

educated and less experienced staff to grow and be a valuable part of the bank.

Institute of management Sciences, BZU. Page 62

Internship report on Bank Alfalah

CONCLUSION

Bank Alfalah Limited is the one the best bank in international banking sector. Its

growth rate is highest among all local banks. Bank Alfalah Limited has potential to become top

ranking bank in Pakistan banking industry. At present there is no such organization in the

world that is free from problem and challenges. Every concern has to strive and struggle a lot

to be more profitable and to get more competitive edge.

My basic purpose of this internship is to learn about the working of bank. During my

internship I got knowledge about general banking, foreign exchange and advances. Staff member

of Bank Alfalah Limited is cooperative with me and really help me to achieve my objective.

The management of BAL is taking strategic steps to enable the bank to emerge as a strong and

progressive institution. It is continuing to make efforts to refine its products and operations to

make them more compatible. New deposit schemes have been introduced and an action plan to

maintain revenue growth in future. As the business and economic conditions remain uncertain,

BAL continues to develop the new products like it has been doing in past.

Institute of management Sciences, BZU. Page 63

Internship report on Bank Alfalah

Bibliography

www.bankalfalah.com

www.bop.com.pk

www.sbp.org.pk

www.business-standard.com

www.sheshunoff.com

Staff of the Bank Alfalah Limited.

Annual report of Bank Alfalah Limited.

Institute of management Sciences, BZU. Page 64

Internship report on Bank Alfalah

Institute of management Sciences, BZU. Page 65

![[Internship Report] folder... · Web view[Internship Report] [Internship Report] 3 [Internship Report] Prince Mohammed Bin Fahd University College of Computer Engineering and Science](https://img.pdfslide.net/doc/110x75/5adbc5e37f8b9add658e5f6e/internship-report-folderweb-viewinternship-report-internship-report-3-internship.jpg)